spsurv: An R package for semi-parametric survival analysis

spsurv: An R package for semi-parametric survival analysis

Renato Valladares Panaro

Advisor: Vinícius Diniz Mayrink

Co-advisor: Fábio Nogueira Demarqui

Departamento de Estatística

Instituto de Ciências Exatas

Universidade Federal de Minas Gerais

Belo Horizonte, MG - Brasil

February 2020

Resumo

Avanços na computação e no desenvolvimento de software permitiram cálculos mais complexos e menos custosos no que diz respeito a pesquisas médicas (análise de sobrevivência), a estudos de engenharia (confiabilidade) e a observação de eventos sociais (análise de eventos históricos). Assim sendo, muitos esforços de modelagem semi-paramétrica para dados de tempo até o evento surgiram nos últimos anos. Neste contexto, este trabalho apresenta uma estrutura flexível baseada no polinômio de Bernstein para modelagem de dados de sobrevivência. Essa abordagem inovadora é aplicada na estimação de funções de base desconhecidas inerentes de famílias de modelos existentes na literatura, como modelos de riscos proporcionais, chances proporcionais e tempo de falha acelerado. Além da contribuição literária, este trabalho também contribui com rotinas automatizadas inéditas para a comunidade de usuários da linguagem R, com o suporte de algoritmos implementados no software Stan. Ao final do estudo, a implementação das rotinas propostas foi discutida e avaliada através de estudos de simulação. A criação de um pacote R surge como alternativa para agrupar todas essas importantes contribuições. Além disso, os modelos baseados no polinômio de Bernstein de riscos proporcionais, de chances proporcionais e de tempo de falha acelerado foram ajustados a dados reais de pacientes portadores de câncer, usando tanto o método de estimação por máxima verossimilhança quanto algoritmos Bayesianos.

Abstract

Software development innovations and advances in computing have enabled more complex and less costly computations in medical research (survival analysis), engineering studies (reliability analysis), and social sciences event analysis (historical analysis). As a result, many semi-parametric modeling efforts emerged when it comes to time-to-event data analysis. In this context, this work presents a flexible Bernstein polynomial (BP) based framework for survival data modeling. This innovative approach is applied to existing families of models such as proportional hazards (PH), proportional odds (PO), and accelerated failure time (AFT) models to estimate unknown baseline functions. Along with this contribution, this work also presents new automated routines in R, taking advantage of algorithms available in Stan. The proposed computation routines are tested and explored through simulation studies based on artificial datasets. The tools implemented to fit the proposed statistical models are combined and organized in an R package. Also, the BP based proportional hazards (BPPH), proportional odds (BPPO), and accelerated failure time (BPAFT) models are illustrated in real applications related to cancer trial data using maximum likelihood (ML) estimation and Markov chain Monte Carlo (MCMC) methods.

Keywords: Proportional hazards; proportional odds; accelerated failure time; Bernstein polynomial

Chapter 1 Introduction

Lifetime research is one of the earliest fields in statistics. According to Hacking (2006), one of its first applications dates back to the 1700s when John Graunt published the first set of analyses upon the London Bills of Mortality. After that, as from Graunt’s book review, tabulations also began in France and other western European countries later on. At the beginning of the eighteen century, increasing annuity incomes also demanded expertise in life expectancy calculations. So, De Moivre, Daniel Bernoulli, and other pioneers contributed to the discussion of available techniques to accurately evaluate life tables at that time, giving rise to the field of study called survival analysis (Rickert, 2017).

Nowadays, software development innovations and recent advances in computing have enabled tools to handle more sophisticated statistical techniques to time-to-event data. Indeed, R software libraries (R Core Team, 2019) containing specific routines such as survival (Terry M. Therneau and Patricia M. Grambsch, 2000), survminer (Kassambara and Kosinski, 2018), timereg (Scheike and Zhang, 2011) and flexsurv (Jackson, 2016) have become essential tools for practitioners, professionals and researchers. Likewise, the spsurv package was designed to contribute with a flexible set of semi-parametric survival regression modelings, including proportional hazards (PH), proportional odds (PO), and accelerated failure time (AFT) models for right-censored data. The proposed package provides extensions based on a fully likelihood-based approach for either Bayesian or maximum likelihood (ML) estimation procedures, along with smooth estimates for unknown baseline functions based on Bernstein polynomial (BP).

Over the past years, the BP have been widely related to regression modeling (Tenbusch, 1997; Chang et al., 2007) and probability density function estimation (Vitale, 1975; Petrone, 1999; Babu et al., 2002; Choudhuri et al., 2004). In contrast, few contributions relating to BP with survival analysis regression can be found in the literature. Some applications in this sense have emerged as alternatives to the partial likelihood estimation proposed by Cox (1972). Chang et al. (2005), for example, estimated the failure rate considering a Beta Process a priori to homogeneous populations. The polynomial degree was treated as a random quantity in this reference. Especially, Osman and Ghosh (2012) addressed the baseline hazard function using BP and provided, among other results, proof on the likelihood log-concavity property for the proposed modeling. This characteristic leads to less costly computational procedures to find Bayesian estimators and is also necessary to guarantee the uniqueness of the ML estimator. The authors also focused on the failure rate but allowed crossing survival curves. In this case, the developed model includes covariates (non-homogeneous population) and a fixed polynomial degree.

More recently, McLain and Ghosh (2013) proposed time transformation models assuming linearity between the survival times and the covariates. Chen et al. (2014) used a transformed BP, centered at standard parametric families, in the accelerated hazards model framework. This application assumes a random degree polynomial by applying a Dirichlet process. Zhou et al. (2017) used BP to approximate the cumulative baseline hazard function. Besides, Zhou and Hanson (2018) proposed modeling the baseline hazard function through a prior distribution called transformed Bernstein polynomial. In this proposal, the authors assume a parametric distribution as central (e.g., Weibull) and use the Bernstein polynomial structure (linked to the baseline survival function) to allow variations around the central choice. That allows greater flexibility in the format of the baseline hazard function. Wu et al. (2018) introduced a flexible Bayesian nonparametric procedure to estimate the odds under the case of interval censoring.

The spsurv interfaces with Stan for more flexibility in terms of user-defined modeling. Stan is an open-source platform that has a specific language and many built-in log-probability functions that can be used to define custom likelihood functions and prior specifications (Carpenter et al., 2017). The program has extensive supporting literature available online such as reference manuals, forums, articles, and books for users and developers. The Stan currently defaults to NUTS sampling, which consists of a Hamiltonian Monte Carlo (Duane et al., 1987) extension that explores the posterior distribution more efficiently (Hoffman and Gelman, 2014). In addition, access to Stan can be established through several modules integration: such as rstan (Stan Development Team, 2018), PyStan (integrated with Python), MatlabStan (integrated to MATLAB), Stan.jl (integrated with Julia) and StataStan (integrated to Stata).

The general goal of this work is to present the spsurv package along with technical details and practical aspects of its usage. The specific contributions of the present work are:

-

•

Explore the BP approach to semi-parametric modeling in survival analysis. Here, we consider three contexts: PH, PO, and AFT models.

-

•

Present a comprehensive simulation study to show that each model performs well under the Bayesian or Frequentist inference approach.

-

•

Build a R package called spsurv that shall be used to fit the semi-parametric models discussed in this dissertation.

This study is organized as follows: Chapter 2 presents the necessary background on survival analysis, which is essential to comprehend the theoretical basis of this work. Afterward, Chapter 3 consists of a summary of how to address BP in the context of approximation or estimation (survival analysis). The next chapter (Chapter 4) explores implementation issues and statistical inference concerns. Achievements from simulation studies were discussed in Chapter 5. Chapter 6 discusses two real data applications and the main results reached, along with comments on the interpretation of the distinct approaches and frameworks. Chapter 7 summarizes the whole content of this dissertation, highlights the first results, and shows the most significant proposals of future work. Finally, the main spsurv package routines are introduced in Appendix. Here we indicate, how to fit a model, discuss summary elements, and present specific graphs for the survival data analysis in R.

Chapter 2 Survival analysis fundamentals

Survival analysis is a field of study in statistical science dedicated to solving problems in which the time to an event of interest is of a reasonable importance (Cox, 1972). For this, a random variable describes the continuously distributed time to a particular event of interest, namely occurrence or failure time. The time-to-event observations are considered incomplete in a manner that each response is subject to censoring, where represents an individual (e.g.: patient or equipment).

An observation is classified as right-censored or left-censored when the event of interest did not occur within the survey period. Particularly, an observation is said to be right-censored if the failure time is greater than the censoring time , but it is unknown by how much. The right censoring assumption adopted for this work is properly denoted as

| (2.1) |

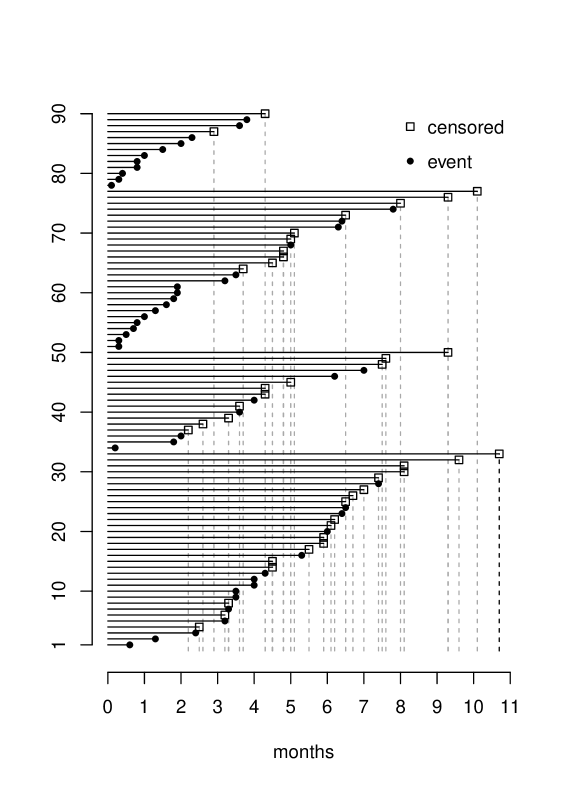

In contrast, if the failure time is lower than the censoring time, but it is uncertain by how much, the data is said to be left-censored. Not least, the data is classified as interval-censored when both right and left censoring are likely to happen. In this situation, the event occurs between two censoring times within the period of the survey. In other words, that is to say, that the failure time is lower than an upper censoring time and greater than a lower censoring time. To identify censoring and failure times, let be the failure binary indicator, assume that = 1 indicates that the observed time point is a failure time. Figure 2.1 shows a real right censoring mechanism example, this data is further explored in Chapter 5.

Some ordinary situations might have caused the right-censored records in monthly lifetimes reports of laryngeal cancer patients (see Figure 2.1). For instance, a right-censored time might have measured the time that a patient dropped the study, or it might have described the lifetime of a certain patient due to uncontrolled external causes of death. Remarkably, the total research time was reported for patient number 33 in this study because the patient has not experienced the event of interest (death) before the end of the survey.

Henceforth, consider the cumulative distribution function (c.d.f.) i.e. so that is the survival function. The survival function is of great interest in medical research since it describes the probability of a patient experiencing the event of interest beyond a specified time. According to Colosimo and Giolo (2006), similar survival functions may have

completely different failure rate functions. This occurs because the failure (or hazard) rate function is defined as:

Other important functions, such as the cumulative hazard function, , and the odds function, , play a key role in modeling lifetime data. These functions are related to the survival function and they can be obtained from it. For instance, some very useful established relationships are: , , and .

Klein and Moeschberger (1997) carefully detail the construction of the likelihood function for survival experiments. In short, consider a survey where failures and right censoring times (2.1) have been reported, so that:

| (2.2) | ||||

where represents the effects of each patient’s individual characteristics that might influence on their respective remaining lifetime (failure time), such as age, gender, or disease status. In general, the goal of survival analysis regression models is to draw inferences about the effect of those explanatory variables to the time-to-event response. Also,the present work relies on the assumption of a non-informative censoring mechanism, therefore the failure and censoring times are considered mutually independent in (2.2). As importantly, the probability distribution of the censoring times does not bring any information about the failure times distribution (Klein and Moeschberger, 1997). As a consequence, the likelihood function for non-informative right-censored data is:

| (2.3) | ||||

The likelihood representation in (2.3) is general in the sense that PH, PO and AFT survival models for non-informative right-censored data can be derived from it.

Generally, health studies are focused on finding disease prognosis. Therefore, it is required to include regression coefficients to investigate the impact of the explanatory variables on the time response. In line with this idea, the PH, PO and AFT classes of survival regression will be presented in this chapter for right-censored data; more details on basic aspects of survival analysis can be found in Klein and Moeschberger (1997), Ibrahim et al. (2001), (Collett, 2015), Colosimo and Giolo (2006), and Kalbfleisch and Prentice (2011).

2.1 Proportional hazards model

The PH model (Cox, 1972) incorporates regression-like arguments into the statistical framework by multiplying a non-negative function of the covariates to the hazard rates (Kalbfleisch and Prentice, 2011). In short, the cross product, between the column vector of features and the column vector of constant coefficients , exponentially increments (or decrements) the reference group hazard function. The referred group (or population) is determined upon common characteristics among patients. For example, the group of patients whose observed covariates are all equal to zero is referred to as the baseline (or reference) group. The baseline hazard function that describes the reference group is and the PH model formulation is then given by:

| (2.4) |

where ( patient). The multiplicative form in (2.4) is the most popular in the literature. In this case, there is no intercept due to the presence of . The intercept can be included using part of the functional structure adopted for the baseline hazard function. For example, in the parametric case, we can parameterize a regression that includes an intercept using the Weibull hazard function form. Otherwise, if the regression does not include an intercept, the baseline hazard, and its related functions, incorporate this constant term (Colosimo and Giolo, 2006).

In the proportional hazards context, the ratio between hazard rate functions of individuals belonging to distinct groups is constant over time. The and patients are compared through hazards ratio (HR):

| (2.5) |

where the vector of regression effects is being replaced by some estimate in order to obtain the estimated HR. As the short form (2.5) contains only the constant regression effects, the ratio between the two patients is proportional over time, leading to the proportional hazards classification. Furthermore, the survival function described before is now written in the presence of regression elements as follows:

| (2.6) |

where is the survival function for the reference group, i.e. . Cox (1972) did not consider any formulation for the survival times distribution. Conversely, the author treated the baseline survival as an unspecified component of the model. The Cox’s PH (CoxPH) model was classified as a semi-parametric model since the baseline time-dependent term do not rely on any functional form. Indeed, it does not assume a parameter based (or any) formulation. For this reason, it is not feasible to employ fully likelihood-based inference procedures to the CoxPH model. As a consequence, partial ML methods became very popular on the purpose of drawing inferences from the CoxPH model. Afterward, Breslow (1972) proposed a fully non-parametric step function to estimate the survival baseline functions which preserved its inherent properties and relationships with associated elements.

The likelihood function for inferences related to the PH model can be derived from (2.3). As mentioned, the general likelihood function for right-censored data is adapted to the specific models.

The likelihood function whose inferences obtained refer to the PH class models is:

| (2.7) | ||||

.

The PH model have been widely applied due to the fact that the HR (2.5) is straightforward to interpret (Colosimo and Giolo, 2006). Although PH models are very popular in the literature, other classes of frameworks such as the PO and AFT can be considered. As reported by De Iorio et al. (2009), the PH model is limited to situations in which the proportional HR assumption is not violated over time. For instance, the PO model is often of great interest for researchers, as it relies on the proportional odds ratio rather than the proportional hazards ratio assumption. Above all, the AFT does not rely on any assumption of proportionality. In this case, the median time ratio is a consequence from its logarithm relation to the predictors.

The next section describes the PO case, built to represent the chance on the occurrence of an event of interest at a given time. The afterward section represents the AFT case; this is one of the most comprehensive classes of survival models (Collett, 2015). At the end of this chapter, we discuss the relation between the studied frameworks.

2.2 Proportional odds model

The PO model (Bennett, 1983) is intended to situations in which survival curves tend to get closer to each other (but they do not cross) along time, for different groups of subject in the study. The PO model is built on the assumption of constant odds ratio (OR) between groups which consists of the odds of an event occurring in some group divided by the odds on event occurring in another group. The OR on the occurrence of an event of interest regarding the baseline group (OR0) is given by:

As the survival function describes the probability of an individual experiencing the event beyond a specific time, the OR of 1 indicates that the event is equally likely to occur in both groups at the specified time. An OR lower than 1 indicates that the event is less likely to occur in the reference group. Conversely, if the OR is higher than 1, the event is more likely to occur in the reference group. Alternatively, we write:

| (2.8) |

Note that, the covariates, together with their effects, assemble the regression argument , that was previously included through the survival function in . Correspondingly, the regression is also included in (2.8) as . The odds on occurring an event for the reference group is . Similar to the hazard function in the PH model (2.4), the odds on the occurrence at a time has a similar multiplicative configuration as the one for the baseline hazard. Therefore, two patients can be compared in the absence (decrease) or presence (increase) of certain characteristic through the odds ratio (OR). We write:

| (2.9) |

It should be noted that, the short form (2.9) contains only the fixed estimated effects over time, which means that the OR is proportional over time, leading to the so called proportional odds classification.

Few changes are made to the general likelihood expression (2.3) in order to obtain the likelihood form related to the PO model. The fully likelihood function that allows inference for the PO model is:

| (2.10) | ||||

with . It is noteworthy that, the PO model can be formulated under the parametric or semi-parametric frameworks. As an example, we can obtain a PO model with the parametric Log-logistic functional form in the baseline functions. The PO model can also be parameterized to have an intercept in the regression. According to Bennett (1983), the partial likelihood approach does not have a simple closed form in this case. As a solution to this issue, the author applies a full likelihood Newton-Raphson method involving the transformation of the failure times to the Log-logistic distribution. Later, Pettitt (1984) developed an alternative rank based distribution-free inference method to compute the estimates for the PO models.

The previous two sections were dedicated to present some critical notations and elements related to the PH and PO models. As stated before, the AFT model does not rely on any assumption over hazards or odds proportionality. Instead, the AFT model is interpreted in terms of the median times ratio, commonly referred to as the acceleration factor. The next section shows the main aspects of the AFT modeling. These three settings (PH, PO, and AFT) are the main statistical approaches to be investigated in this dissertation.

2.3 Accelerated failure time model

In the AFT model, the explanatory variables act multiplicatively on the time scale and thus affect the rate at which the survival curve decays along the time (Collett, 2015). The AFT modeling can be represented by the following log-linear relationship with the observed times:

| (2.11) |

where is the random variable that describes the time-to-event for the patient, and are, respectively, the location and scale parameters of the distribution for the random variable . According to Hosmer Jr et al. (2008), the AFT models are predominantly applied under a parametric perspective. In this case, a distribution function is assumed either for the random variable or . Indeed, the survival function might be obtained directly from or indirectly from . One can write:

| (2.12) | ||||

where represents the percentile of the distribution assigned to . For instance, the random variable might follow a standard Normal, Log-gamma or Logistic distribution. As a result, will have Log-normal, Gamma or Log-logistic distribution, respectively. In particular, consider that the AFT survival function can be rewritten in terms of the reference group survival as:

| (2.13) | ||||

For an AFT model, the hazard function can be obtained with (2.13) using the following relation:

| (2.14) | ||||

Typically, the joint effect of covariates accelerates or decelerates the failure time, leading to the AFT family. Additionally, the AFT likelihood function is obtained with (2.3) as well:

| (2.15) | ||||

The interpretation of the estimated AFT coefficients takes into account the logarithmic scale of the response. According to Hosmer Jr et al. (2008), two patients can be compared in the absence (decrease) or presence (increase) of a certain characteristic through the estimated time ratio (TR). This quantity is calculated with the median (or any percentile) of the survival time for a given group of patients divided by the median survival time for the another group. In order to obtain the TR for the median time point consider:

| (2.16) |

Accordingly,

| (2.17) |

Then, the TR is then given by:

| (2.18) |

This quantity is often referred to as the acceleration factor (Hosmer Jr et al., 2008). Klein and Moeschberger (1997) discuss about the Exponential, Weibull, Log Normal, Log-logistic and Gamma, among other distributions, to describe time-to-event data using the AFT framework. In fact, we can assume any distribution function for combined with any general class of survival model to assemble a parametric model. Some associations of that nature lead to parametric forms of known distributions, we will look at two cases: the Weibull PH and AFT; and the Log-logistic PO and AFT.

The next section describes the relationship between some parametric forms for the three general families presented previously in this chapter. The models being discussed will assume parametric forms for the baseline functions. The patterns found in the next section will be explored in the simulation study and real applications. In particular, the parametric AFT models described have supported the generation of simulated data (Chapter 5).

2.4 Relationship between the parametric AFT and other families

Although parametric models are not the focus of this work; it is essential to review some commonly used cases to study the advantages of the BP based models. In particular, we will focus on two of the most used probability distributions since they provide the three classes of models that are of interest to this dissertation. In this work, we will stick to the Weibull and the Log-logistic parametric formulations due to their specific relationship with the AFT class of models. The Weibull model is an option with both PH and AFT classes, while the Log-logistic formulation is considered for both PO and AFT. The artificial data sets investigated in Chapter 5 were obtained, assuming the parametric AFT versions for these two distributions. The main idea behind this strategy is to evaluate the BP based survival regression estimates obtained when fitting data sets originated from distinct data-generating models.

2.4.1 Weibull AFT and Weibull PH

The Weibull density function is often used to describe the lifetime of industrial products. Its popularity is since it can represent strictly increasing, strictly decreasing, or constant behaviors for the hazard function (Klein and Moeschberger, 1997). The Weibull distribution is parameterized in the present dissertation with the following configuration of density function:

where is the scale parameter and is the shape parameter. The survival and hazard functions for a Weibull distributed time-to-event random variable are respectively:

| (2.19) | ||||

According to Collett (2015), the Weibull distribution can be used to support a parametric AFT model, allowing to differ between groups. For this, we need to keep the AFT structure in (2.14) and adopt the Weibull hazard function (2.19) for the reference group. The Weibull AFT (WAFT) is defined as follows:

| (2.20) |

In (2.20), we can observe the Weibull hazard structure described in (2.19). As mentioned, the scale parameter differs between group and we can write , with scale and shape . On the other hand, if a Weibull distribution is assumed for under the PH framework (WPH) in (2.4), it then follows that . The hazard function in this case is rewritten as:

Technically, it is possible to compare both models in terms of the resulting scale parameter . One of the goals of the simulation studies is to compare the BPPH and the BPAFT when fitted to the same data set originated from the WAFT model. Consider that is the linear predictor for an individual under the WAFT framework and is the linear predictor for an individual under the WPH model. Explicitly, , that is, . Thus, the regression element of the WPH model is compatible with the regression of the WAFT model multiplied by the negative of the shape parameter.

In the case that a Weibull distribution is assumed in the PO model framework, or a Log-logistic distribution is assumed for the PH model, it is not feasible to find a parametric hazard function structure. The Weibull distribution model is the only parametric model that belongs to the AFT and the PH families at the same time. In the same way, the Log-logistic distribution model is the only parametric option belonging to the PO and AFT, simultaneously. The next topic describes how this relationship works within the parametric framework.

2.4.2 Log-logistic AFT and Log-logistic PO

The Log-logistic distribution can also provide a parametric model for analyzing right-censored survival data. Unlike the Weibull distribution, which is more popular, its hazard function is not always monotonic. In turn, the hazard function can be unimodal, monotonically decreasing and, also, it can have an increasing configuration at the beginning and a decreasing configuration for large time points. The Log-logistic distribution is parameterized in this dissertation as follows:

where is the scale and is the shape parameter.

Survival, hazard and odds functions are, respectively:

| (2.21) | ||||

The Log-logistic distribution can be used as the basis for an parametric AFT model, allowing to differ between groups or, generally, introducing covariates that affect as a linear function of the covariates (Collett, 2015).

Similar to the WAFT and WPH models, the Log-logistic AFT (LLAFT) and the Log-logistic PO (LLPO) formulations are assembled with the general survival framework (either AFT or PO) and the Log-logistic parametric form of the baseline functions (2.21). Assuming that are independent Log-logistic random variables in the AFT framework (2.11), we have:

| (2.22) |

As a result, we find the Log-logistic hazard structure described in (2.21). Thus, we write, with scale parameter and shape parameter . At the same time, the Log-logistic odds function (2.21) can be rewritten in terms of the PO framework (2.8) as:

In this case, one can show that, follows a Log-logistic distribution with scale parameter and shape parameter , i.e, . The previous statements regarding the distributions of the ’s in the LLAFT and LLPO settings justify the strategy for comparing these cases in terms of the scale parameter. We write the following equality: , i.e. , where is the linear predictor for an individual under the LLAFT framework and linear predictor for a subject under the LLPO model. Other distributions do not provide similarities with respect to the relationship between the parametric Weibull and Log-logistic survival models and their respective AFT cases.

Although parametric versions of the AFT model are often the first choice in many applications in the literature, the study developed in this dissertation is focused on the semi-parametric configuration of the survival classes in this chapter. That is to say that we will not impose a probability distribution to describe the time response. In this sense, the BP based approach proposed in Osman and Ghosh (2012) arises as a flexible and appealing semi-parametric alternative, allowing different shapes for the baseline function without need to pre-specify a distribution for the response variable. The approach explored in this dissertation has a non-parametric appeal concerning the baseline functions. In the sense that the parametric shape of the baseline functions is distribution-free. In other words, the parameters that determine the shape of the baseline functions are not related to the parameters of any probability distribution function. Despite the semi-parametric appeal of the BP based survival models, they indeed make use of fully parametric techniques.

The next chapter is dedicated to the BP presentation, along with facts, properties, and typical nuances resulting from its mathematical formulation. Lorentz (1953) has exhaustively exposed theoretical results and important facts about the BP in the context of mathematical analysis, such as proofs of theorems, generalizations, derivatives, asymptotic formulations, and approximation examples. In addition, Farouki (2012) discussed relevant applications to the BP as a celebration for the centennial anniversary of this topic. The discussion accounts for aspects related to symmetry, non-negativity, and differentiation properties. At the end of the next chapter, the BP is presented in the context of survival analysis.

Chapter 3 Bernstein polynomial

The BP were introduced by Bernstein (1912) for the approximation of any continuous function whose domain is restricted to the interval . According to Lorentz (1953), the Bernstein Polynomial of degree m for the function c(x) is given by:

| (3.1) |

where is called the BP basis polynomial (or just basis). Farouki and Rajan (1987) discuss an alternative formulation to accommodate functions restricted to ; such that . We write:

| (3.2) |

In the present work, we will refer to the highest order of the BP basis polynomials (individual terms) as degree and to the BP basis polynomial order simply as order. Lorentz (1953) properly discusses on how to demonstrate the Weierstrass approximation theorem. The theorem say that every restricted continuous function can be approximate by a polynomial function, as close as desired, in the real domain. Using a finite BP, having a sufficiently high degree, it can be shown that uniformly. Briefly, consider a sequence of polynomials and the existence of some polynomial of a high degree . In such a way that, for every and :

The approximation ability of BP has been widely explored for the approximation of real-valued functions regarding several contexts in literature. BP is a crucial topic in the present dissertation, since the semi-parametric survival analysis via BP is the main structure to support the routines implemented in the R package proposed here. In the next section, we highlight some useful BP properties and facts. At the end of this chapter, the BP is introduced in the context of survival regression.

3.1 BP basis properties

The focus of this section is on the BP basis polynomial that will serve as the main structure for the approximation of the target function by the linear combination of lower (or equal) order polynomials. Consider the probability of successes in trials of a binomially distributed random variable

with individual probability of success in each trial, that is . According to some authors (Gzyl and Palacios, 1997; Koralov and Sinai, 2007; Cichoń and Gołębiewski, 2012; Aldà and Rubinstein, 2017), the BP formulation in (3.1) can be interpreted as the expected value of the random variable , where is the target function in (3.1):

The BP basis polynomials should sum up to one, as well as the binomial probability mass function, therefore, we write:

| (3.3) |

Some properties of the BP basis are important to build the semi-parametric model described ahead in this dissertation. In particular, four key properties were described by Farouki (2012) as follows:

-

•

symmetry:

(3.4) -

•

recursion:

(3.5) -

•

non-negativity:

(3.6) -

•

derivatives:

(3.7)

The BP properties are also broadly discussed in many applications of computer aided geometric design methodologies (computational mathematics methods to describe geometric objects). More details on basic properties of the BP can be found in the references: Davis (1963), Farouki and Rajan (1987), Farouki and Rajan (1988) and Farouki (2008).

Figure 3.1 illustrates the BP basis symmetry (3.4), recursion (3.5), and non-negativity (3.6) properties, considering and polynomial degrees. Panel (a) shows the Bernstein polynomial basis of order , the left-hand side basis is and the right-hand side basis is , corresponding to the black (darkest color) and the yellow (lightest color), respectively. All the basis polynomials, including these two, follow the properties presented in (3.4), (3.5), (3.6) and (3.7). As for instance, due to the the symmetry property we have: . Also, the non-negative property can be observed at the image of the curves presented in the Panel (a). In turn, Panel (b) illustrates the fact that the same properties are maintained for higher order polynomial basis. As discussed previous in this chapter, higher degree polynomials are expected to provide better approximations to the target function. It is also noteworthy that, for , the yellow curve begins

rising from 0.4 while, when , it starts rising from 0.7, that illustrates that the basis order is lower than the basis order.

In particular, if the curves are evaluated at any fixed point in , the basis sum up to one (3.3), especially, .

The BP differentiation can be obtained from the derivative property (3.7) of the basis. This property provides the necessary results for the introduction of the BP in the survival analysis regression context, explored further in this dissertation. The last section of this chapter discusses how the BP differentiation expression can be used to estimate cumulative hazard, odds and related functions. The first partial derivative with respect to of the formulation in (3.1) provides:

| (3.8) | ||||

where . According to Farouki (2012), consider by definition , thus we have:

| (3.9) | ||||

where is the difference of first order of the function at (Lorentz, 1953). It is important to notice that the basis derivatives are lower order basis written in terms of the difference . The second difference, for example, is:

The BP derivative consists of a lower order basis (3.9) due to the recursion property (3.5). This property provides a recursive relationship for a sequential differentiation (Lorentz, 1953), given by:

In this section, we have included some properties about the BP polynomial basis that will be important in building the BP models for survival data. Primarily, the derivative properties are used in the last section of this chapter about BP in survival analysis. Besides, the BP was presented from the perspective of a Binomial distributed random variable, this alternative perspective can facilitate the interpretation of the BP and make the presentation of its properties more intuitive. The next section shows how to use BP to approximate real-valued continuous functions. For example, the BP approximation should capture any continuous function, including non-negative cases such as the hazard rate functions.

3.2 Finite BP approximation

In the present section, we will illustrate how the BP is used to approximate known real valued functions, we have chosen a Weibull hazard function as an example of real-valued target function. The Weibull distribution is a very popular choice when it comes to parametric models, as mentioned in Chapter 2. Assuming that the target function has a non-negative domain restricted to , the equation (3.2) becomes:

| (3.10) |

In order to obtain (3.10), we have assumed an upper bound limit for the hazard function in (2.19). Suppose that and , such that . Then, we have:

| (3.11) | ||||

Accordingly, the Bernstein polynomial basis in (3.10) are:

| (3.12) | ||||||

The finite BP approximation is obtained with the cross product between the BP basis in (3.12) and the values of the target function (3.11) evaluated at the equidistant points .

Figures 3.2 and 3.3 illustrate the behavior of every single product (individual term) of this finite BP (3.11), two configurations of the Weibull hazard function are explored. Note that, in this case, there is no symmetry. In Figure 3.2, for example, the scaled (multiplied) basis polynomials are more concentrated to the right-hand corner compared to Figure 3.1. The resulting approximation consists of the sum of every (polynomial) curve in solid-colored lines; the finite BP curve is represented in dash-dotted lines. As expected, when increases, from Panels (a) to (b) in Figures 3.2 and 3.3, the BP approximation gets closer to the actual target curve. The higher degree in BP, Panel (b), indeed provides a closer approximation to the target function. The target function must be known so that it can play the role of modifying each basis form presented in Figure 3.1.

Although the approximation of target hazard rate functions is often successful, the approach is not suitable for real data applications as the target function is unknown in practice. The researcher cannot know in advance the true distribution of the time until the occurrence of an event. Hence, the next section presents an alternative to estimate unknown cumulative hazard and odds functions for right-censored data, which uses the BP based survival regression modeling.

3.3 BP in survival analysis

The topic of this section is central to the proposal of the semi-parametric survival modeling developed in this dissertation. The methodology behind the elements that will be presented here was introduced in Osman and Ghosh (2012). The authors took advantage of a finite BP in order to estimate positively bounded functions in survival regression modeling, such as the cumulative hazard function . For this, consider (3.2) to approximate :

| (3.13) |

The first BP differentiation (3.9) with respect to the time is:

| (3.14) | ||||

It is important to emphasize that the polynomial basis were rewritten as , in which corresponds to the beta density function. Moreover, note that the quantities do not depend on the time. Thereby, these quantities should be estimated as we cannot know in advance the true cumulative hazard function value. Hereafter, these elements will be called BP parameters . Some parametric models have been criticized because of the hazard decay for large time values (Klein and Moeschberger, 1997). Using the BP it is possible to estimate either increasing, decreasing, convex, concave, and other shapes of functions, such that the estimates for dictates the shape that the functions related to the BP will assume, similar to what happened in Figures 3.2 and 3.3. The hazard and cumulative hazard functions in the BP formulation are:

| (3.15) |

where , and . Since this model does not impose any functional form on the hazard function, it is said to have a non-parametric appeal. Some properties of the key functions for survival analysis, mentioned in Section 2, are preserved when the BP structure is assumed. For example, the cumulative hazard function is monotonic non-decreasing as a consequence of the restriction .

As stated in Chapter 2, the inclusion of regression coefficients is required in order to achieve the statistical purpose of investigating the impact of covariates over the time response. Hence, the formulation (3.15) shall be included in the baseline hazard function of the PH likelihood function (2.7), as follows:

| (3.16) | ||||

where . Osman and Ghosh (2012) discuss proofs on the strictly concavity, the uniqueness of the maximum likelihood estimates and good differentiability properties that ease likelihood, gradient and Hessian matrix calculations.

The BP is also suitable to estimate the baseline odds on the event occurrence (Demarqui et al., 2019). This can be done due to the properties shared by the odds function and the cumulative hazard function. Similar to the cumulative hazard function, the odds function is a monotonic non decreasing function with and . The formulation (3.15) shall be included in the baseline odds function of the PO likelihood function (2.10), i.e., and , in order to define the next likelihood function:

| (3.17) |

in this case . The BP parameters are denoted by , to indicate the estimation of the odds instead of the cumulative hazard function. Finally, the likelihood function of the AFT model adapts the BP structure thought the hazard and cumulative hazard functions. The formulation (3.15) shall be included in the baseline odds function of the AFT likelihood (2.15). This provides:

| (3.18) | ||||

where . The likelihood in (3.16) refers to the Bernstein polynomial based proportional hazards (BPPH) model, the likelihood (3.17) refers to the Benstein polynomials based proportional odds (BPPO) model and the likelihood in (3.18) refers to the Bernstein polynomial accelerated failure time (BPAFT) model under the right censoring mechanism.

This chapter summarizes the usage of the BP in the finite approximation of positive continuous functions such as the hazard rate function. We emphasize that the target function must be known in advance to approximate it by the BP. Further, we also have comments on how to use BP under the statistical perspective of estimation. Osman and Ghosh (2012) proposed methods to estimate the hazard (target) function using the BP when this function is unknown. In this context, the next chapter presents some implementation details that were crucial to fit the BP based regression models.

Chapter 4 Inference procedures and technical issues

Throughout the package implementation, some workarounds had to be done to guarantee a stable version of the R package implemented to fit the BP models. This chapter provides some perspective of what had to be done internally (without user interference) to achieve satisfactory performance in the simulation study results (Chapter 5). According to Gjessing et al. (2010), the presence of an exponential structure combined with other complex formulations might lead to an unstable model, with numerical problems. Our primary purpose is to avoid the explosive behavior of the survival regression models, also reported in Aalen et al. (2008) and Kalbfleisch and Prentice (2011).

Aware of the numerical stability problems, the survival package (Terry M. Therneau and Patricia M. Grambsch, 2000), for example, includes routines that internally standardize the covariates before evaluating the likelihood, in order to avoid an overflow in the argument of the exponential function. According to the R help documentation, the functions to fit models in the survival package, such as survival::coxph, internally scale and center data; see the “details” section of ?coxph() in the R console. The adoption of this kind of feature brings some counterparts to the likelihood as a whole. Particularly, these counterparts are related to the regression coefficients and BP parameters scale. Consider the standardization of covariates as:

where and , such that and are the column vector of sample means and the column vector of sample standard deviations, respectively. For example, consider the inclusion of standardized covariates (explanatory variables) in the BPPH hazard function (2.7), as follows:

where the symbol denotes the Hadamard (element-wise) product and the standard linear predictor is denoted by . The parametric space of interest is rewritten in terms of the new coefficients defined under the mentioned standardization , so that:

Fully likelihood methods for ML estimation and Bayesian estimation were applied considering the transformed space. Thereafter, the quantities of interest could be recovered given the invariance property of the ML estimators or through the posterior mode (or any summary) of transformed chains, following the relations:

| (4.1) |

| (4.2) |

In this form, the BP survival regression estimates would be driven by the sample standard deviations towards close to zero values, and the BP estimates would be inflated or deflated depending on the sample means . It is expected that this technique brings more stability and accuracy to the proposed package. From the Bayesian perspective, the prior choice is made regarding the standardized coefficients. As mentioned, we shall expect little deviations from zero and a great variability for the BP parameters as they shall depend on the arguments to the exponential function.

From the Bayesian perspective, as a single effect can have a huge impact for the final result, one might assume, for example, the generic weakly informative and the weakly informative prior choices and for the regression coefficients, respectively. Also, generic or weakly informative Log-normal priors have been tested to express the lack of previous information about the BP parameters, the reader is reminded that, in this case, a Normal prior specification to the BP parameters in log-scale is equivalent to a Log-normal prior specification to the actual scale, that is: Thus, the prior choice for the BP parameters is analogue, that is, or . According to the default configuration of the spsurv, for each model fit, four chains of size 2000 are built for each quantity of interest, using the NUTS algorithm (Hoffman and Gelman, 2014) provided in Stan. The first 1000 iterations are discarded as a burn-in (warm-up) period. After the sampling procedure, model comparison criteria are calculated using the loo package (Vehtari et al., 2019).

Under the Frequentist perspective, the maximization algorithm is applied to the likelihood function to determine the ML estimates. The likelihood ratio (LR) test and Wald score tests are available for the BPPH, BPPO, or BPAFT models. The LR test statistic is not affected by the standardization as this statistic consists of twice the difference between two likelihood functions: . Conversely, the Wald test statistic is affected by the standardization because the multivariate z-statistic is based on the Fisher information: where the observed Fisher information matrix is intended to be a sample-based version equivalent to the negative of the estimated Hessian matrix (log-likelihood second derivative). Nevertheless, the observed information matrix obtained refers to the information of standard configuration discussed at the beginning of this chapter. Hence, the Delta method is required to recover the observed information of interest (Oehlert, 1992; Casella and Berger, 2002; Cooch, 2008). According to this point, we write:

| (4.3) |

| (4.4) |

where represents the function described in (4.2) and represents the gradient column vector of partial derivatives such that .

The Fisher information is also needed to build confidence intervals. In this case, it is necessary to compute the estimated variance-covariance matrix, which is equivalent to the inverse of the observed Fisher information matrix . In practice, some numerical problems may be experienced when dealing with the inversion of the observed information. The matrix can be singular due to numerical approximations. To circumvent this issue, we consider a block-wise strategy for inversion that is defined for the following partition:

| (4.5) |

Once the matrix is partitioned, it can be inverted block-wise as follows (Bernstein, 2009):

where refers to the regression block, and for the symmetric covariance blocks and for the BP parameters block. Here we have that, is and is a , so that both can be inverted. Also, must be invertible.

Significance tests and confidence intervals were not proposed for the BP parameters since these parameters do not reflect any covariate effect or interpretative quantities. In turn, they dictate the shape of survival curves analogously to the scale parameters in parametric models. Beyond the necessary adjustments regarding the application of the model with transformed coefficients discussed earlier in this chapter, Osman and Ghosh (2012) comment on the choice of the polynomial degree and states that this is closely related to the true hazard function shape. There is a bias-variance trade-off in which a small degree polynomial is likely to result in biased estimates, while a large degree polynomial might introduce excessive variation. The package structure will allow the users to choose the best polynomial degree for their applications. However, this choice must take into account the purpose of user-defined modeling. If a high-precise estimation of the baseline functions is not interesting to the study, the practitioner should choose low-degree polynomials. Otherwise, high-degree polynomials are preferable. The recommendation (Osman and Ghosh, 2012) is to the use of as the choice of polynomial degree that is set as the default in the spsurv package.

The upper bound restriction, in (3.13), is not considered a parameter in the spsurv package structure. According to Osman and Ghosh (2012), in the context of survival analysis: and in probability. Thus, the main function of the package internally sets . Although this is applied to the implementation, one should know that any estimator for would generate an improper survival function, that is, we would have:

| (4.6) | ||||

where we can not guarantee that . In special,

| (4.7) | ||||

As a solution to this inconsistency, a tail adjustment is necessary to satisfy ; see Osman and Ghosh (2012). Although there are some choices of corrections that provides a survival function that meets the requirement, these kind of corrections do not affect the estimates of the BP based survival models. The correction applied to the survival function formulation after the last observed time, will not change the estimates presented in this dissertation. Note that, the time region beyond does not contain any time response.

We close here the third chapter of this dissertation. The next chapter is dedicated to a comprehensive simulation study that compares the overall performance of the BPPH, BPPO, and BPAFT. The main aim of the next chapter is to assess whether the BP estimates behave well in distinct scenarios. After the analysis involving artificial data sets, the dissertation will be focused on applications of the BP models to real problems.

Chapter 5 Monte Carlo simulation study

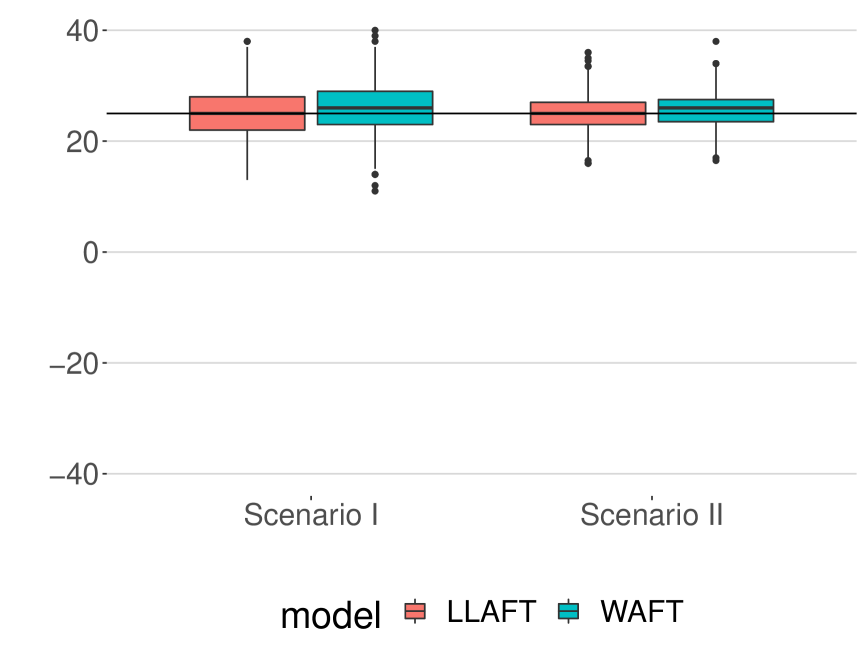

In this chapter, we present a Monte Carlo (MC) simulation study to evaluate the performance of the BP based models in terms of estimation. The analysis is divided in two scenarios: sample size (Scenario I) and sample size (Scenario II). For both cases, the same covariates were used to generate 1000 replications (data sets), from LLAFT and WAFT (parametric) models. Censoring times were produced based on the same distribution used to generate the failure times. Figure A.12 (Appendix F) shows how the censoring rate was distributed for each simulated data set generated.

Ideally, the simulated survival times can be generated from the relationship , where is a uniformly distributed random variable and is the failure time random variable. In fact, it is feasible to generate a random variable observation from its own survival function (if the survival is invertible). One can introduce an observed value from and, therefore, obtain . We can show that:

According to Ross (2012), this method is often called the Inverse Transform Sampling (ITS). In this case, denotes the survival function adopted for either from WAFT (2.20) or LLAFT (2.22). Table 5.1 shows the settings of each data generator model:

| Data set # | Model | Covariate | Covariate | Shape | Censoring scale | Average % censoring |

|---|---|---|---|---|---|---|

| 1 | LLAFT | |||||

| 2 | WAFT |

As stated earlier, the censoring mechanism is non-informative. Hence, both event and censoring times were generated independently through the ITS method. The censoring times, for each data set, were also generated from the Weibull (WAFT) and the Logistic (LLAFT) survival functions. In order to achieve approximately 25% average censoring (Table 5.1), the scale parameter for the censoring times, were set to be in (2.20) and in (2.22). It should be mentioned that, the distribution of failure times is individual (not indentically distributed), that is, the value of the scale parameter (or ) in the survival function differ between the artificial groups created (see Chapter 2). Summary statistics for these parameters were presented in Table 5.2:

| Model | Scale | Min. | 1st Qu. | Median | Mean | 3rd Qu. | Max. |

|---|---|---|---|---|---|---|---|

| LLAFT | 3541.2876 | 16202.3240 | 28818.4750 | 79166.4723 | 57127.7961 | 4510736.9826 | |

| WAFT | 25.2166 | 40.4366 | 47.4655 | 50.9704 | 56.1337 | 189.7279 |

Note that the Table 5.1 shows only the settings for the Scenario II. However, Scenario I can be obtained by simply using the first 100 elements of the 200 sized data sets. We also emphasize that, the MC simulation study were based on two distinct likelihood maximization methods and four distinct prior specifications for every replication in each of the two scenarios. A sensitivity analysis for the prior specifications of the BP parameters was applied to evaluate the impact of the initial uncertainty about these unknown quantities. Table 5.3 shows the four hyperparameter choices tested. In this context, independence between all parameters was assumed a priori.

| Prior # | Prior for | Prior for | ||||

|---|---|---|---|---|---|---|

| 1 | ||||||

| 2 | ||||||

| 3 | ||||||

| 4 |

Under the Bayesian framework, Prior 1 and Prior 2 specifications provide more information to the regression coefficients (Table 5.3) due to the belief in slight deviations from zero. As mentioned in Chapter 4, the covariates were standardized before fitting the models, which means that atypical values will have less impact in the regression estimates once they have been internally standardized. In this context, Priors 3 and 4, provided less information to the regression coefficients aiming to offer a contrasting choice.

The primary goal of this analysis is to investigate how the regression estimates are affected by distinct levels of uncertainty attributed to the BP parameters. The next section shows the results of this simulation study for Scenario I. Results for Scenario II are explained later in this dissertation. All the simulation study results are presented in Appendix B. The conclusions about the simulation studies are given in the last section of this chapter.

5.1 Scenario I: sample size

This section presents the results for the data sets with a sample size of . In the investigations conducted in this dissertation, we choose to explore five statistics in the evaluation of the estimation under the MC scheme: the average estimate (est.), the average estimated standard error (se.), the standard error of the estimates (sde.), the relative bias (rb.) and the coverage probability. For this, consider a generic parameter, and assume that is the ML (or the posterior) estimate. The analysis of the results from the MC replications takes into account the next elements:

-

•

the average estimate (est.):

(5.1) -

•

the average estimated standard error (se.):

(5.2) -

•

the standard error of the estimates (sde.):

(5.3)

where denotes the estimated standard error (or posterior standard

deviation) obtained for and denotes the true value. In order to account for the distance between the reported estimate and the true estimate, the relative bias is considered with the following formulation:

| (5.4) |

The uncertainty related to the replications is expressed based on interval estimates for the regression coefficients. Thus, another interesting element to be considered in the analysis is the coverage probability of the model. The coverage probability is the percentage of the MC replications that provide a 95% interval that captures the true value of the parameter. In the frequentist approach, we consider 95% confidence intervals. In the Bayesian framework, the investigation is based on 95% HPD (Highest Probability Density) credibility intervals.

The study presented here was developed with the following strategy. The BPPH and BPAFT models were fitted to the data sets that originated from the WAFT model. Meanwhile, the BPPO and BPAFT models were fitted to the data sets that originated from the LLAFT model. These settings are comparable based on the relationships discussed in section 2.4. For comparative purposes, we have also fitted the generator models (parametric AFT) using the routine provided by survreg::survival.

| ML | WAFT | LLAFT | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| 2 | 2.0090 | 0.2282 | 0.2724 | 0.4253 | 0.8967 | 2 | 2.0030 | 0.2223 | 0.2325 | 0.1438 | 0.9434 | ||

| -1 | -1.0080 | 0.3046 | 0.3729 | -0.7903 | 0.8947 | -1 | -1.0210 | 0.3065 | 0.3174 | -2.1136 | 0.9434 | ||

The results in Table 5.4 do not provide any indication that the procedure to generate data (ITS) contains errors. As expected, the relative bias is very close to zero (less than 3%), which suggests that the generator model recovers well the true value of the coefficients. Furthermore, the coverage rates of the confidence intervals are close to the nominal value of 95%, reflecting the good interval estimation provided by the model fit. In conclusion, Table 5.4 indicates that the generator model (either WAFT or LLAFT) can recover the true values of the coefficients. In this sense, we can consider that this table is a useful reference for the evaluation of the BP based survival regression model routines proposed here. The purpose of this section is to verify whether the BP based model’s statistics provided are similar to the statistics provided by the model that generated the data (Table 5.4).

| BFGS | BPPH | BPAFTa | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -4.4807 | 0.5814 | 0.7670 | -12.0172 | 0.8250 | 2 | 2.0398 | 0.1271 | 0.3209 | 1.9885 | 0.6497 | ||

| 2 | 2.2373 | 0.5170 | 1.0465 | 11.8664 | 0.9080 | -1 | -1.0169 | 540.4119 | 0.7781 | -1.6880 | 0.6562 | ||

| LBFGS | BPPH | BPAFTb | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -4.4774 | 0.6129 | 0.7478 | -11.9343 | 0.8480 | 2 | 2.0368 | 0.1287 | 0.3209 | 1.8376 | 0.6596 | ||

| 2 | 2.2617 | 0.5275 | 1.8072 | 13.0832 | 0.9130 | -1 | -1.0047 | 126.6637 | 0.5935 | -0.4669 | 0.6539 | ||

| Prior 1 | BPPH | BPAFTc | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -3.4030 | 0.4419 | 0.3167 | 14.9300 | 0.7450 | 2 | 2.0950 | 0.2026 | 0.2158 | 4.7580 | 0.9248 | ||

| 2 | 1.7060 | 0.4556 | 0.4021 | -14.6900 | 0.9200 | -1 | -1.0490 | 0.2569 | 0.3075 | -4.9360 | 0.9468 | ||

| Prior 2 | BPPH | BPAFT | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -3.9730 | 0.5486 | 0.4770 | 0.6630 | 0.9740 | 2 | 1.9890 | 0.5050 | 0.4935 | -0.5537 | 0.9660 | ||

| 2 | 1.9540 | 0.5050 | 0.4854 | -2.2920 | 0.9660 | -1 | -1.0250 | 0.2421 | 0.3042 | -2.4770 | 0.9250 | ||

| Prior 3 | BPPH | BPAFT | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -3.4800 | 0.4519 | 0.3335 | 13.0000 | 0.8250 | 2 | 2.1060 | 0.2058 | 0.2211 | 5.3111 | 0.9190 | ||

| 2 | 1.7440 | 0.4590 | 0.4124 | -12.8100 | 0.9320 | -1 | -1.0620 | 0.2640 | 0.4569 | 6.2430 | 0.9420 | ||

| Prior 4 | BPPH | BPAFT | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | ||

| -4 | -4.1230 | 0.5730 | 0.5326 | -3.0750 | 0.9670 | 2 | 2.0590 | 0.1957 | 0.2223 | 2.9660 | 0.9160 | ||

| 2 | 2.0630 | 0.5144 | 0.5251 | 3.1550 | 0.9620 | -1 | -1.0360 | 0.2484 | 0.4540 | -3.5970 | 0.9170 | ||

The Table 5.5 displays the mentioned statistics for the estimates of the BP based models applied to the WAFT data set replications in Scenario I. This table shows twelve possible configurations for fitting the 1000 MC data sets using the spsurv package. The first two refer to the Frequentist approaches either under the PH or AFT frameworks. The Broyden–Fletcher–Goldfarb–Shanno (BFGS) algorithm was first used to promote the likelihood maximization. Secondly, another option of optimization algorithm was tested to assess if there is any empirical evidence in preferring some of them; the Limited-memory BFGS (LBFGS) algorithm was used with that purpose, both algorithms are built-in Stan. Besides, the Bayesian model fit is also included assuming the prior specifications described in Table 5.3.

It is noteworthy that we chose not to explore the Newton method, which was also made available to the user in the spsurv package, to save computational time. In our experience, this method tends to be slow to handle the BP models. We also highlight that the mentioned optimization methods can often find a local maximum rather than the global one. The likelihood function was evaluated concerning four ML estimates that considered distinct random initial values for the optimizer to mitigate this kind of bias. Thus, the largest likelihood estimate obtained with these four possible fits were selected. Both BFGS and LBFGS are iterative methods for solving nonlinear optimization problems (Fletcher, 2000). The LBFGS is a BFGS extension with a limited-memory; the BFGS algorithm accumulates all the gradient values, including the first ones. On the other hand, the LBFGS drops old gradients in favor of the new ones. The LBFGS is useful to avoid the bias of the initial gradient; even so, the estimated Hessian will still be biased by initial values until enough gradients are accumulated close to the solution.

In short, according to Table 5.5, we can consider that the BP based models provided good results when applied to Bayesian inference, especially looking for the Prior 2 and 4 relative biases. Under the Frequentist approach, the BP based models did not produce results as good as the generator model fits (Table 5.4); in particular, the BPPH model fits provided relatively biased estimates. In comparison, we might also suggest that the Bayesian approach is less error-prone, i.e. we found here fewer problems regarding the computation of the estimates. For example, an amount of 178 non-converging estimates were found in the BPAFT case (for both BFGS and LBFGS). At the same time, only the first prior specification provided fewer than expected replications (). As a result, the number of valid MC replications decreased due to issues in computing the estimates (see the caption of Table 5.5). In the Bayesian case, the reason for detecting those missing values is related to the non-mixing chains that can occur due to the initial values that were randomly assigned by Stan internally.

Table A.3 (Appendix B) shows the MC simulation study for the estimates of the BP models applied to LLAFT data set. We found similar conclusions about interval estimates for the BPAFT model under the ML perspective applied to LLAFT data. Both average standard error and the coverage probability reflect the underestimated standard errors. Consequently, the BPAFT has presented narrower confidence intervals compared to the interval ranges from the generator model. Also, the optimization problems once more have caused a decrease in the number of valid MC replications. For the BPPO and BPAFT models, a total of 98 non-converging estimates and 17 non-finite Hessian matrices were found (see the caption of Table A.3). Regarding the Bayesian model fits sensitivity analysis, the same conclusion can be maintained: the prior specification that presented the best results was again Prior 2, which consists of attributing generic weakly informative priors to the regression coefficients and vague prior information to the BP parameters. Above all, we found that the Bayesian BP based survival regression models can provide accurate inferences (Prior 2) in using the three classes: PO, PH, and AFT.

In general, it is possible to state that the estimates provided by the LBFGS method are very similar when compared to the BFGS. Some model comparison criteria such as the LR statistic, the Akaike information criterion (Akalke, 1974), and the Bayesian information criterion (Schwarz et al., 1978), for example, could be applied in this case to support the comparison between those algorithm estimates. However, we chose the one that indicated the highest coverage rate to BP based models applied to Frequentist inference. For this reason, the ML results of the LBFGS algorithm will be used in the comparison between the estimates of the two inferential approaches. From the Bayesian perspective, the deviance information criterion (DIC) (Spiegelhalter et al., 2002), the Watanabe–Akaike information criterion (WAIC) (Watanabe, 2013) and the logarithm of the pseudo-marginal likelihood (LPML) (Geisser and Eddy, 1979) was calculated to assist the evaluation of the prior choice. The LPML and WAIC criteria were multiplied by -2, so that the three criteria have a similar interpretation to facilitate the understanding, that is, the lower is the value of the criterion, the better the model fits the data. It is expected that the prior choice that presented consistently little relative bias, and near 95% coverage rate will also outperform the other models concerning the above criteria. Accordingly, Figure 5.1 shows the relative difference between some reported prior choice criterion and the value of the same criterion regarding Prior 2, for the identical MC replication.

The relative difference is somehow similar to relative bias (5.5). Instead, it accounts for the distance from another criterion (or estimate) rather than the distance from the true values. The relative difference accounts for the distance between the reported criterion (or estimate) and the value of some reference criterion:

| (5.5) |

where is the Prior 2 (reference) criterion (or estimate) and is the referred prior criterion (Prior 1, Prior 3 or Prior 4). The relative difference is a ratio with the numerator being the difference between estimates and the denominator being the magnitude of the reference value. Negative and positive results indicate that the criterion is being evaluated above or below the reference estimate, respectively. The fraction is multiplied by 100, leading to a percentage representation of its magnitude. Some MC replicas provided non-finite values for the -2 WAIC and -2 LPML. Therefore the relative difference was only included if the three criteria were valid for both priors in the same MC replication comparison.

Figure 5.1 suggests that the model comparison criteria -2 LPML and -2 WAIC do not differ about the best model to be chosen. The results have indicated that Prior 2 fit is often preferable to other fits. Besides, we can state that the -2 WAIC and -2 LPML are suitable for comparing BP based survival regression models in Scenario I since most of them indicated the best fit concerning relative bias and coverage probability. Although Christensen et al. (2011) states that LPML is preferable in many cases. We have also found that the DIC criterion is more sensitive than the -2 LPML and -2 WAIC when it comes to BP based models comparison. The relative difference presented by this one was higher than expected. Also, we discovered that the DIC criterion in BPPO and BPPH do not reflect the findings of this simulation study Scenario because it often indicates Prior 4 as the preferable model. From our analysis: we conclude that Prior 2 is slightly better than Prior 4 (making sense to be chosen). But we have learnt that the prior choice is essential for the best fit.

Table 5.6 shows the results of the Bayesian (Prior 2) and the Frequentist (LBFGS) approaches. Remarkably, the BPAFT coverage probabilities under the ML approach do not approximate to the nominal level of 95%. Note that, the average standard error (se.) and the standard error of the estimates (sde.) under the ML perspective are not close. It is noteworthy that these statistics are tight in the Bayesian case. Therefore, we can suggest there exists a rough approximation error in the Delta Method applied. The average estimated standard error of the BPAFT applied to the WAFT data set in (Table 5.6), is, on average, underestimated, and exceedingly overestimated for the second coefficient. This conclusion is based on the comparison with the results from the generator model (Table 5.4). In turn, this overly estimated average standard error is justified by the presence of discrepant values in the standard error estimation. Indeed, it can be seen that the below-expected coverage probability reflects the fact that most estimated confidence intervals for BPAFT models were exceptionally narrow. Despite the unsuccessful confidence interval estimation, the relative bias is very low for the BPAFT estimates (see Table 5.4).

| LBFGS | BPPH | BPAFTa | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (WAFT) | true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | |

| -4 | -4.4774 | 0.6129 | 0.7478 | -11.9343 | 0.8480 | 2 | 2.0368 | 0.1287 | 0.3209 | 1.8376 | 0.6596 | ||

| 2 | 2.2617 | 0.5275 | 1.8072 | 13.0832 | 0.9130 | -1 | -1.0047 | 126.6637 | 0.5935 | -0.4669 | 0.6539 | ||

| Prior 2 | BPPH | BPAFT | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (WAFT) | true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | |

| -4 | -3.9730 | 0.5486 | 0.4770 | 0.6630 | 0.9740 | 2 | 1.9890 | 0.5050 | 0.4935 | -0.5537 | 0.9660 | ||

| 2 | 1.9540 | 0.5050 | 0.4854 | -2.2920 | 0.9660 | -1 | -1.0250 | 0.2421 | 0.3042 | -2.4770 | 0.9250 | ||

| LBFGS | BPPOb | BPAFTc | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (LLAFT) | true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | |

| -4 | -4.3523 | 0.6417 | 0.7813 | -8.8071 | 0.8548 | 2 | 2.0345 | 0.1586 | 0.3123 | 1.7269 | 0.6897 | ||

| 2 | 2.2170 | 0.6935 | 0.7646 | 10.8513 | 0.9330 | -1 | -1.0222 | 0.2150 | 0.4025 | -2.2193 | 0.6886 | ||

| Prior 2 | BPPO | BPAFTd | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (LLAFT) | true | est. | se. | sde. | rb. | cov. | true | est. | se. | sde. | rb. | cov. | |

| -4 | -4.0437 | 0.6195 | 0.5562 | -1.0925 | 0.9600 | 2 | 2.0441 | 0.2321 | 0.2538 | 2.2041 | 0.9189 | ||

| 2 | 2.0677 | 0.6770 | 0.6631 | 3.3839 | 0.9560 | -1 | -1.0426 | 0.3237 | 0.3453 | -4.2609 | 0.9319 | ||

Apart from the performance of the ML interval estimation, the BP based models provided good estimates regarding the prior choices that attributed higher uncertainty to the BP parameters, such as the Prior 2 and Prior 4 (Appendix Table 5.5). As mentioned in Chapter 4, this should be justified by the fact that the prior specification and the maximization account for the transformed BP coefficients, for instance in the PH class. This implies that the estimates in the standardized case are inflated or deflated according to the argument of the exponential function. For this reason, even a generic weakly informative prior can undermine the ability of the model to find the true value of the parameter. For instance, values near zero are considerably possible to the BP parameters and should often occur as the argument of the exponential function might be negative valued. In summary, when standardized covariates are passed to the BP based models, vague priors should be considered to express the uncertainty about the variability of the BP parameters. Compared to Prior 4, a more precise information about the regression coefficients in Prior 2 has lead, on average, to lower posterior standard deviations and lower relative bias.

Considering Tables 5.5 and A.3, the average relative bias that accounted for the most considerable difference between estimated and actual values was reported in the application of the BPPH model under the ML approach; the reported average absolute bias was around 12%. Simultaneously, the shortest distances captured by the relative bias were in the BPPH application under the Prior 2 approach, together with the BPAFT application under the ML approach, with approximate 2% of average relative bias. Except for the BPPH model under ML, all modeling options provided an average absolute bias near or less than 10%.

Also, the Figures 5.2 and 5.3 show the relative bias comparison between the models that provided, in most cases, the adequate results concerning the relative bias. From a Frequentist perspective, we can say that there is no difference in using the BFGS or the LBFGS. Therefore, we chose to stick with the second, as it consists of an extension of the BFGS. On the other hand, the applications under the Prior 2 model presented a lower bias. Thus, those results were chosen to represent Bayesian applications. The panels refer to the illustration of the pairwise estimates that were previously summarized separately (Tables 5.5 and A.3), an estimate was only displayed in these graphs if both estimation approaches were valid for the same MC data set. The Panel (a) shows the dispersion of the relative bias for the BP based Bayesian estimates in red, the BP based ML estimates in green, and the parametric ML estimates obtained with the generator model in blue (either WAFT or LLAFT). The relationship between the parametric models that are under comparison in these figures was previously described in Section 2.4. It is possible to compare the PH, or the PO, with the AFT, only by multiplying the negative value of the scale parameter to the regression coefficients estimates provided by the AFT model. In this case, the shape parameter chosen for the two generator models was 2 (see Table 5.1). The Panel (b) illustrates the dispersion of the ratio between the absolute relative bias of the ML estimates over the Bayesian estimates for the same MC replication.