Risk-Aware Submodular Optimization for Multi-Robot Coordination

Abstract

We study the problem of incorporating risk while making combinatorial decisions under uncertainty. We formulate a discrete submodular maximization problem for selecting a set using Conditional-Value-at-Risk (CVaR), a risk metric commonly used in financial analysis. While CVaR has recently been used in optimization of linear cost functions in robotics, we take the first step towards extending this to discrete submodular optimization and provide several positive results. Specifically, we propose the Sequential Greedy Algorithm that provides an approximation guarantee on finding the maxima of the CVaR cost function under a matroidal constraint. The approximation guarantee shows that the solution produced by our algorithm is within a constant factor of the optimal and an additive term that depends on the optimal. Our analysis uses the curvature of the submodular set function, and proves that the algorithm runs in polynomial time. This formulates a number of combinatorial optimization problems that appear in robotics. We use two such problems, vehicle assignment under uncertainty for mobility-on-demand and sensor selection with failures for environmental monitoring, as case studies to demonstrate the efficacy of our formulation. We also study the problem of adaptive risk-aware submodular maximization. We design a heuristic solution that triggers the replanning only when certain conditions are satisfied, to eliminate unnecessary planning. In particular, for the online mobility-on-demand study, we propose an adaptive triggering assignment algorithm that triggers a new assignment only when it can potentially reduce the waiting time at demand locations. We verify the performance of the Sequential Greedy Algorithm and the adaptive triggering assignment algorithm through simulations.

Index Terms:

risk-aware decision making, conditional value at risk, submodular maximization, sequential greedy algorithm.I Introduction

Combinatorial optimization problems find a variety of applications in robotics. Typical examples include:

-

Task allocation: How to allocate tasks to robots to maximize the overall utility gained by the robots [3]?

-

Combinatorial auction: How to choose a combination of items for each player to maximize the total rewards [4]?

Algorithms for solving such problems find use in sensor placement for environment monitoring [1, 2], robot-target assignment and tracking [5, 6, 7, 8, 9, 10], and informative path planning [11, 12]. The underlying optimization problem in most cases can be written as:

| (1) |

where denotes a ground set from which a subset of elements must be chosen. Typically, is a monotone submodular utility function [13, 14]. Submodularity is the property of diminishing returns. Many information theoretic measures, such as mutual information [2], and geometric measures such as the visible area [15], are known to be submodular. denotes a matroidal constraint [13, 14]. Matroids are a powerful combinatorial tool that can represent constraints on the solution set, e.g., cardinality constraints (“place no more than sensors”) and connectivity constraints (“the communication graph of the robots must be connected”) [16]. The objective of this problem is to find a set satisfying a matroidal constraint and maximizing the utility . The general form of this problem is NP-complete. However, a greedy algorithm yields a constant factor approximation guarantee [13, 14].

In practice, sensors can fail or get compromised [17] or robots may not know the exact positions of the targets [18]. Hence, the utility is not necessarily deterministic but can have uncertainty. Our main contribution is to extend the traditional formulation given in Equation 1 to also account for the uncertainty in the actual cost function. We model the uncertainty by assuming that the utility function is of the form where is the decision variable and represents a random variable which is independent of . We focus on the case where is monotone submodular in and integrable in .

The traditional way of stochastic optimization is to use the expected utility as the objective function:

| (2) |

Since the sum of the monotone submodular functions is monotone submodular, is still monotone submodular in . Thus, the greedy algorithm still retains its constant-factor performance guarantee [13, 14]. Examples of this approach include influence maximization [19], moving target detection and tracking [18], and robot assignment with travel-time uncertainty [20].

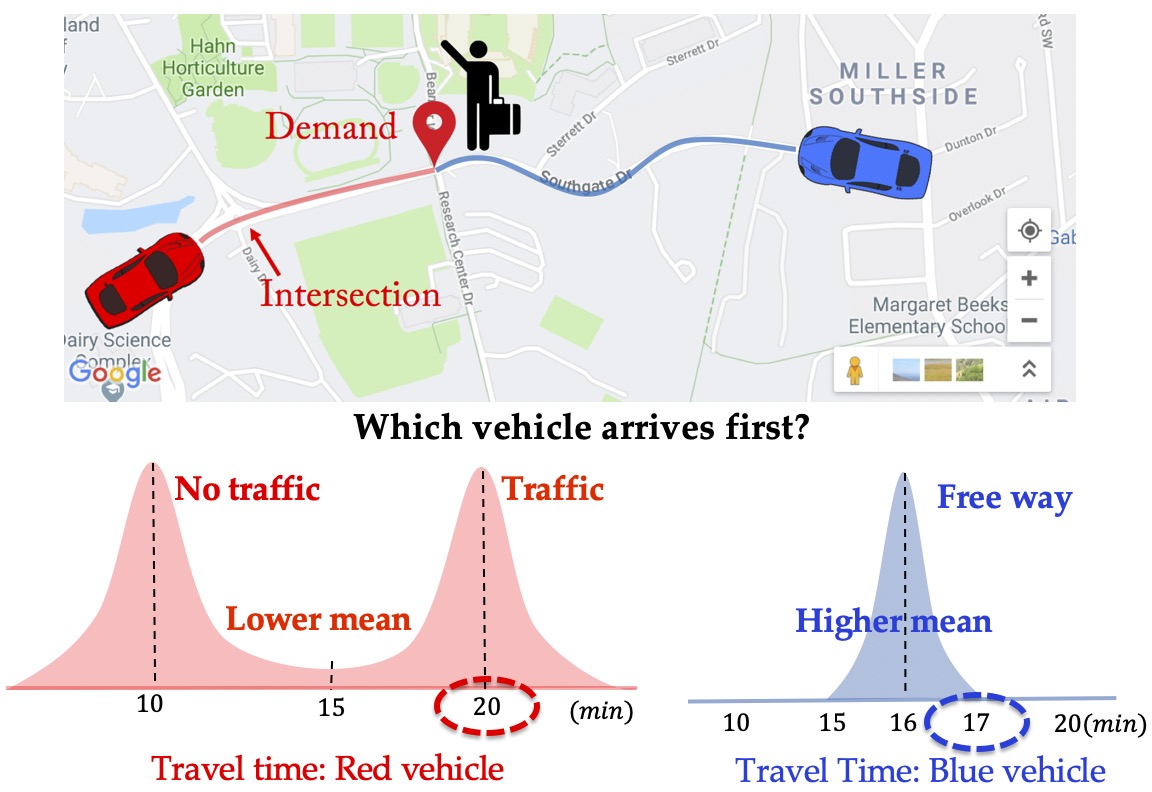

While optimizing the expected utility has its uses, it also has its pitfalls too. Consider the example of mobility-on-demand where two vehicles, the red vehicle and the blue vehicle, are available to pick up the passengers at a demand location (Fig. 1). The red vehicle is closer to the demand location, but it needs to cross an intersection where it may need to stop and wait. The blue vehicle is further from the demand location but there is no intersection along the path. The travel time for the red vehicle follows a bimodal distribution (with and without traffic stop) whereas that for the blue vehicle follows a unimodal distribution with a higher mean but lower uncertainty. Clearly, if the passenger uses the expected travel time as the objective, they would choose the red vehicle. However, they will risk waiting a much longer time, i.e., about half of the times. A more risk-aware passenger would choose the blue vehicle which has higher expected waiting time but a lesser risk of waiting longer.

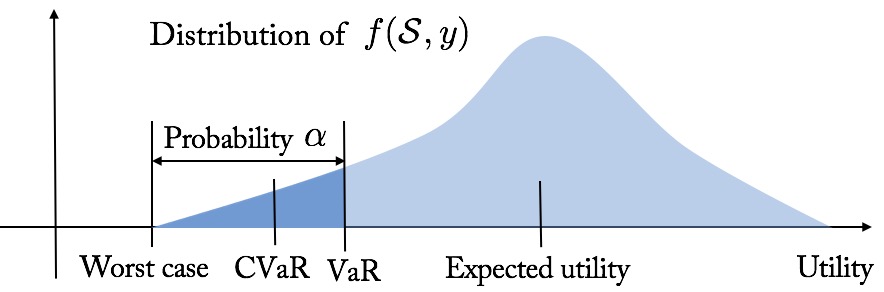

Thus, in these scenarios, it is natural to go beyond expectation and focus on a risk-aware measure. One popular coherent risk measure is Conditional-Value-at-Risk (CVaR) [21, 22]. CVaR is parameterized by a risk level . Informally, maximizing CVaR is equivalent to maximizing the expected utility in the worst -tail scenarios.111We formally review CVaR and other related concepts in Section II-C.

Related work. Several works have focused on optimizing CVaR. In their seminal work [22], Rockafellar and Uryasev presented an algorithm for CVaR minimization for reducing the risk in financial portfolio optimization with a large number of instruments. Note that, in portfolio optimization, we select a distribution over available decision variables, instead of selecting a single one. Later, they showed the advantage of optimizing CVaR for general loss distributions in finance [23].

Another popular risk measure in finance is the Value-at-Risk (VaR) [24], which is generally used for formulating the chance-constrained optimization problems. Yang and Chakraborty studied a chance-constrained combinatorial optimization problem that takes into account the risk in multi-robot assignment [25]. They later extended this to knapsack problems [26]. They solved the problem by transforming it to a risk-aware problem with mean-variance measure [27].

Compared to VaR, Rockafellar and Uryasev stated that CVaR has more desirable mathematical characteristics such as subadditivity, convexity, and coherence, and is easier to optimize when it is calculated from scenarios [22]. Also, Majumdar and Pavone argued that CVaR has better properties for quantifying risk than VaR or mean-variance based on six proposed axioms in the context of robotics [28].

When the utility is a discrete submodular set function, i.e., , Maehara presented a negative result for maximizing CVaR [29]— there is no polynomial time multiplicative approximation algorithm for this problem under some reasonable assumptions in computational complexity. To avoid this difficulty, Ohsaka and Yoshida in [30] used the same idea from portfolio optimization and proposed a method of selecting a distribution over available sets rather than selecting a single set, and gave a provable guarantee. Following this line, Wilder considered a CVaR maximization of a continuous submodular function instead of the submodular set functions [31]. They gave a –approximation algorithm for continuous submodular functions and also evaluated the algorithm for discrete submodular functions using portfolio optimization [30].

Contributions. In this paper, we first focus on the problem of selecting a single set, similar to [29], to optimize CVaR of a stochastic submodular set function. We propose an approximation algorithm with provable theoretical guarantees. Then we study the problem of adaptive risk-aware submodular maximization. We design a triggering replanning strategy that solves the CVaR optimization problem only at specific time steps to avoid unnecessary planning costs.

Our contributions are as follows:

-

We prove that the solution found by SGA is within a constant factor of the optimal performance along with an additive term which depends on the optimal value and a sampling error. We also prove that SGA runs in polynomial time (Theorem 1) and the performance improves as the running time increases.

-

We formulate an adaptive risk-aware submodular maximization problem for the online version (Problem 2). We devise an event-triggered replanning strategy that replans by SGA only when certain conditions are reached. Particularly, we design the Adaptive Triggering Assignment (ATA) for the online mobility-on-demand application (Algorithm 2) which triggers reassignment only at some specific time steps to avoid unnecessary assignments.

Organization of rest of the paper. We give the necessary background knowledge for the rest of the paper in Section II. We formulate the CVaR submodular maximization problem with two case studies in Section III. We present SGA along with the analysis of its computational complexity and approximation ratio in Section IV. We present an adaptive risk-aware submodular maximization problem and design a triggering replanning strategy in Section V. We illustrate the performance of SGA to the two case studies and evaluate the performance of ATA with street networks in Section VI. We conclude the paper in Section VII.

A preliminary version of this paper was first presented in [32] without the analysis of the approximation error induced by sampling method (see Section IV), the formulation of the adaptive risk-aware submodular maximization problem and a triggering replanning strategy (see Section V), and the numerical evaluations of ATA on street networks (see Section VI-C).

II Background and Preliminaries

We start by defining the conventions used in the paper.

Calligraphic font denotes a set (e.g., ). Given a set , denotes its power set. denotes the cardinality of . Given a set , denotes the set of elements in that are not in . denotes the probability of an event and denotes the expectation of a random variable. where denotes the set of integers.

Next, we give the background on set functions, the greedy algorithm, and risk measures.

II-A Background on set functions: Monotonicity, Submodularity, Matroid, and Curvature

We begin by reviewing useful properties of a set function defined for a finite ground set and matroid constraints.

Monotonicity [13]: A set function is monotone (non-decreasing) if and only if for any sets , we have .

Normalized Function [14]: A set function is called normalized if and only if .

Submodularity [13, Proposition 2.1]: A set function is submodular if and only if for any sets , and any element and , we have: . Therefore the marginal gain is non-increasing.

Matroid [33, Section 39.1]: Denote a non-empty collection of subsets of as . The pair is called a matroid if and only if the following conditions are satisfied:

-

for any set it must hold that , and for any set it must hold that .

-

for any sets and , it must hold that there exists an element such that .

We will use two specific forms of matroids that are reviewed next.

Uniform Matroid: A uniform matroid is a matroid such that for a positive integer , . Thus, the uniform matroid only constrains the cardinality of the feasible sets in .

Partition Matroid: A partition matroid is a matroid such that for a positive integer , disjoint sets and positive integers , and for all }.

Curvature [34]: Consider a matroid for , and a non-decreasing submodular set function such that (without loss of generality) for any element , . The curvature measures how far is from submodularity or linearity. Define curvature of over the matroid as:

| (3) |

Note that the definition of curvature (Eq. 3) implies that . Specifically, if , it means for all the feasible sets , . In this case, is a modular function. In contrast, if , then there exist a feasible and an element such that . In this case, the element is redundant for the contribution of the value of given the set .

II-B Greedy Approximation Algorithm

In order to maximize a set function , the greedy algorithm selects each element of based on the maximum marginal gain at each round, that is,

where .

We consider maximizing a normalized monotone submodular set function . For any matroid, the greedy algorithm gives a approximation [14]. In particular, the greedy algorithm can give a –approximation of the optimal solution under the uniform matroid [13]. If we know the curvature of the set function , we have a approximation for any matroid constraint [34, Theorem 2.3]. That is,

where is the set selected by the greedy algorithm, is the uniform matroid and is the function value with optimal solution. Note that, if , which means is modular, then the greedy algorithm reaches the optimal. If , then we have the –approximation.

II-C Risk measures

Let be a utility function with decision set and the random variable . For each , the utility is also a random variable with a distribution induced by that of . First, we define the Value-at-Risk at risk level .

Value at Risk:

| (4) |

Thus, denotes the left endpoint of the -quantile(s) of the random variable . The Conditional-Value-at-Risk is the expectation of this set of -worst cases of , defined as:

Conditional Value at Risk:

| (5) |

Figure 2 shows an illustration of and . is more popular than since it has better properties [22], such as coherence [35].

When optimizing , we usually resort to an auxiliary function:

where . We know that optimizing over is equivalent to optimizing the auxiliary function over and [22]. The following lemmas give useful properties of the auxiliary function .

Lemma 1.

If is normalized, monotone increasing and submodular in set for any realization of , the auxiliary function is monotone increasing and submodular, but not necessarily normalized in set for any given .

We provide the proofs for all the lemmas and the theorem in the appendix.

Lemma 2.

The auxiliary function is concave in for any given set .

Lemma 3.

For any given set , the gradient of the auxiliary function with respect to fulfills: .

III Problem Formulation and Case Studies

We first formulate the CVaR submodular maximization problem and then present two applications that we use as case studies.

III-A Problem Formulation

We consider the problem of maximizing over a decision set under a matroid constraint . We know that maximizing over is equivalent to maximizing the auxiliary function over and [22]. Thus, we propose the maximization problem as:

Problem 1 (CVaR Submodular Maximization).

| (6) | ||||

Problem 1 gives a risk-aware version of maximizing submodular set functions.

III-B Case Studies

The risk-aware submodular maximization (Problem 1) has many applications in robotics. In the following, we describe two specific applications which we will use in the simulations.

III-B1 Resilient Mobility-on-Demand

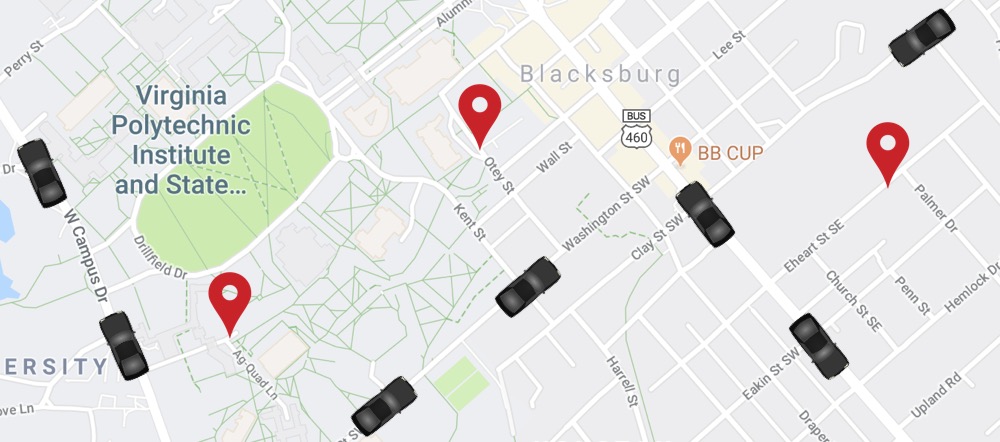

Consider a mobility-on-demand problem where we assign vehicles to demand locations under arrival-time uncertainty. An example is shown in Figure 3 where seven self-driving vehicles must be assigned to three demand locations to pick up passengers. We follow the same constraint setting in [20]— each vehicle can be assigned to at most one demand but multiple vehicles can be assigned to the same demand. Only the vehicle that arrives first is chosen for picking up the passengers. Note that the advantage of the redundant assignment to each demand is that it counters the effect of uncertainty and reduces the waiting time at demand locations [20]. This may be too conservative for consumer mobility-on-demand services but can be crucial for urgent and time-critical tasks such as delivering medical supplies [36].

Assume the arrival time for the vehicle to arrive at a demand location is a random variable. Its randomness can depend on the mean-arrival time. For example, it is possible to have a shorter path that passes through many intersections, which leads to uncertainty on arrival time. While a longer road (possibly a highway) has a lower arrival time uncertainty. Note that for each demand location, there is a set of vehicles assigned to it. The vehicle selected at the demand location is the one that arrives first. Then, this problem becomes a minimization one since we would like to minimize the arrival time at all demand locations. We convert it into a maximization one by taking the reciprocal of the arrival time. Specifically, we use the arrival utility which is the reciprocal of arrival time. Instead of selecting the vehicle at the demand location with minimum arrival time, we select the vehicle with maximum arrival utility. The arrival utility is also a random variable, and its randomness depends on mean-arrival utility. Denote the arrival utility for vehicle arriving at demand location as . Denote the subset of robots assigned to demand location as . Then, the arrival utility for a demand location is computed as . Further, we denote the assignment utility as the sum of arrival utilities at all locations, that is,

| (7) |

with and . indicates the selected set satisfies a partition matroid constraint, , which represents that each vehicle can be assigned to at most one demand. The assignment utility is monotone submodular in due to the “max” function. is normalized since . Here, we regard uncertainty as a risk. Our risk-aware assignment problem is a trade-off between assignment utility and uncertainty. Our goal is to maximize the total utilities at the demand locations while considering the risk from uncertainty.

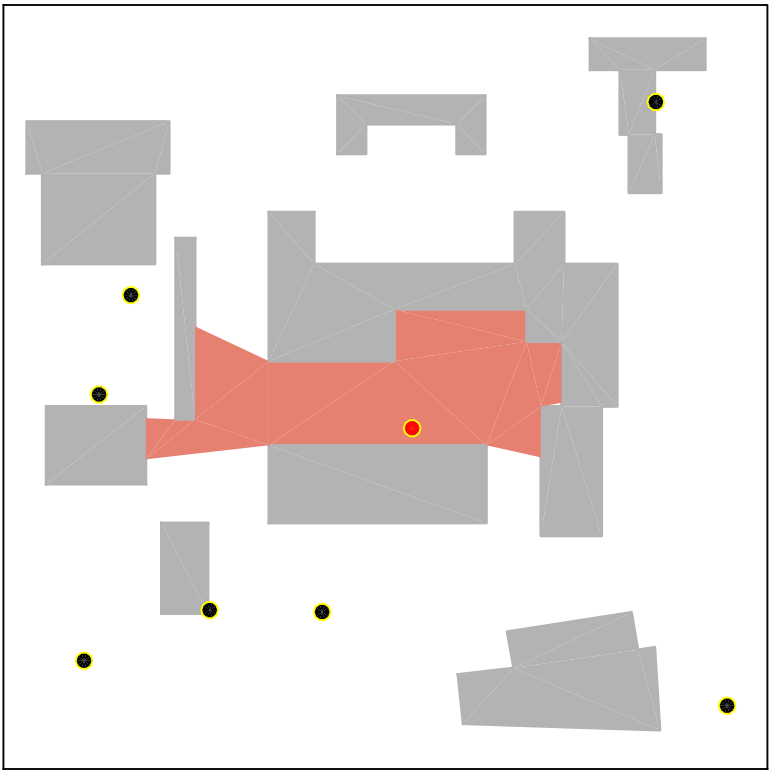

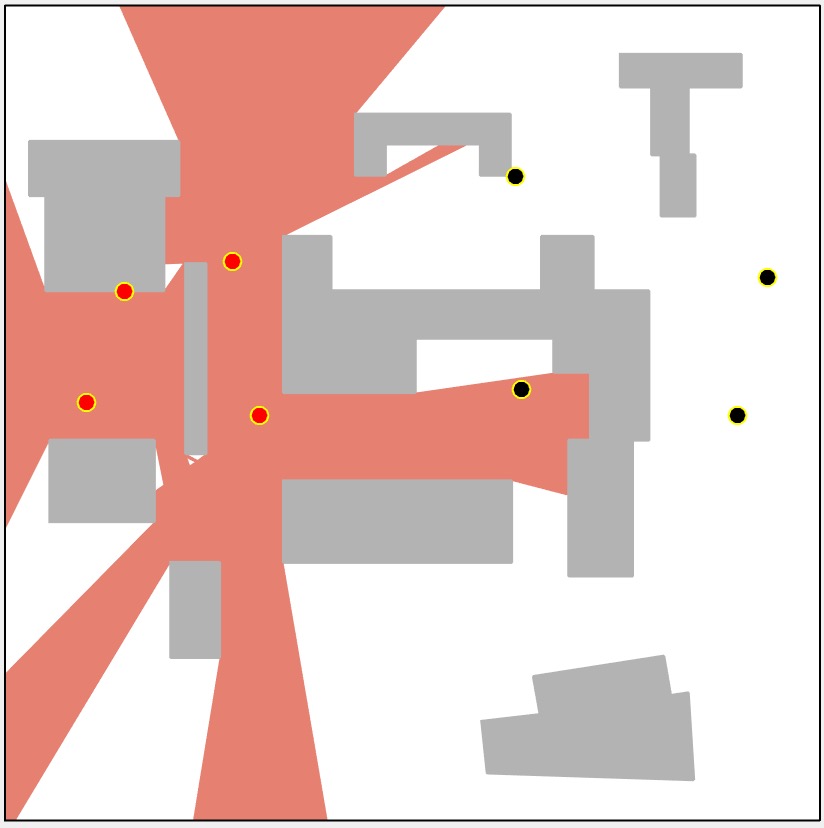

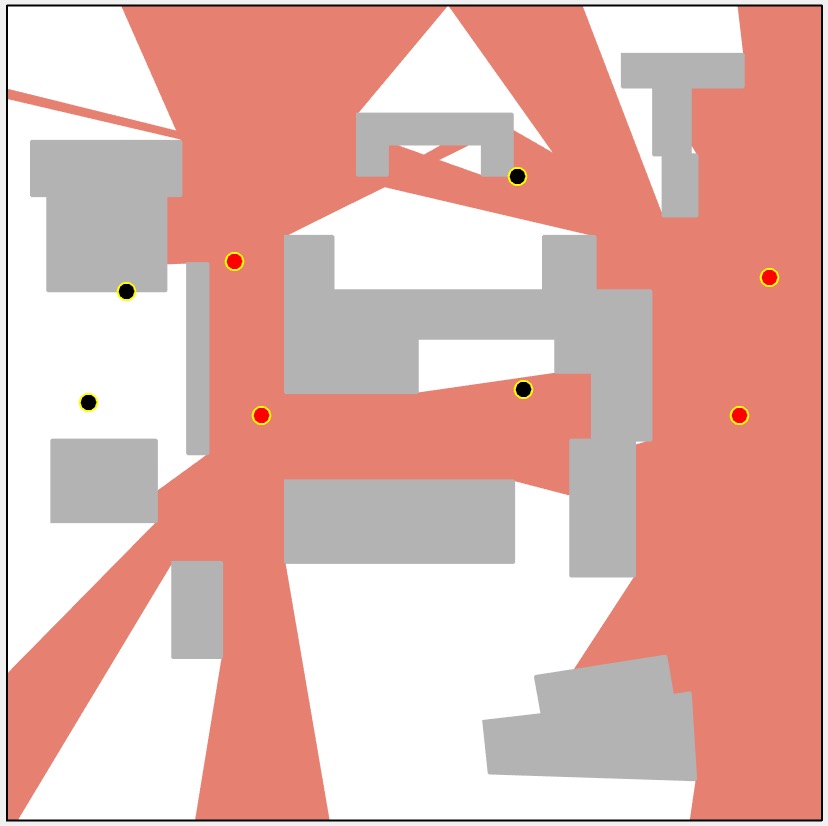

III-B2 Robust Environment Monitoring

Consider an environment monitoring problem where we monitor part of a campus with a group of ground sensors (Fig. 4). Given a set of candidate positions , we would like to choose a subset of positions , to place visibility-based sensors to maximally cover the environment. The visibility regions of the ground sensors are obstructed by the buildings in the environment (Fig. 4-(b)). Consider a scenario where the probability of failure of a sensor depends on the area it can cover. That is, a sensor covering a larger area has a larger risk of failure associated with it. This may be due to the fact that the same number of pixels are used to cover a larger area and therefore, each pixel covers proportionally a smaller footprint. As a result, the sensor risks missing out on detecting small objects.

Denote the probability of success and the visibility region for each sensor as and , respectively. Thus, the polygon each sensor monitors is also a random variable. Denote this random polygon as and denote the selection utility as the joint coverage area of a set of sensors, , that is,

| (8) |

The selection utility is monotone submodular in due to the overlapping area. is normalized since . Here, we regard the sensor failure as a risk. Our robust environment monitoring problem is a trade-off between area coverage and sensor failure. Our goal is to maximize the joint-area covered while considering the risk from sensor failure.

IV Algorithm and Analysis

We present the Sequential Greedy Algorithm (SGA) for solving Problem 1 by leveraging the useful properties of the auxiliary function . The pseudo-code is given in Algorithm 1. SGA mainly consists of searching for the appropriate value of by solving a subproblem for a fixed under a matroid constraint. Even for a fixed , the subproblem of optimizing the auxiliary function is NP-complete. Nevertheless, we can employ the greedy algorithm for the subproblem, and sequentially apply it for searching over all . We explain each stage in detail next.

IV-A Sequential Greedy Algorithm

These are four stages in SGA:

Initialization (Alg. 1, line 1)

Algorithm 1 defines a storage set and initializes it to be the empty set. Note that, for each specific , we can use the greedy algorithm to obtain a near-optimal solution based on the monotonicity and submodularity of the auxiliary function . stores all the pairs when searching all the possible values of .

Searching for (for loop in Alg. 1, lines 2–10)

We use a user-defined separation (Alg. 1, line 3) to sequentially search for all possible values of within . We use as an searching upper bound on . That is because, when is greater than the maximal value of , the auxiliary function , which is non-increasing in given the risk level . Thus, in order to maximize , we do not need to search for the cases when is larger than the maximum value of . Therefore we set the value of as the maximum value of . Even though is a random variable, its maximum value can be set by the user based on the specific problems at hand. For example, in the environment monitoring scenario (Section III-B), can be computed as the total area of the environment because this is the largest area that robots can jointly cover. In the mobility-on-demand scenario (Section III-B), can be the highest total utilities for reaching all demand locations (e.g., when there is no traffic congestion and vehicles travel with maximum legal speeds). We show how to find for these specific cases in Section VI.

Greedy algorithm (Alg. 1, lines 4–8)

Find the best pair (Alg. 1, line 11)

Based on the collection of pairs (Alg. 1, line 9), we pick the pair that maximizes as the final solution . We denote this value of by . Notably, .

Designing an Oracle: Note that an oracle is used to calculate the value of . We can use a sampling-based method, as an oracle, to approximate . Specifically, we sample realizations from the distribution of and approximate as . According to [30, Lemmas 4.1-4.5], if the number of samples is , the CVaR approximation error is less than with the probability at least . We provide a brief proof for the number of samples in the appendix.

Observability of : SGA uses an oracle to sample from for the approximation of . Notably, is partially known and its realizations (samples) can be taken from some historical data. For example, in the vehicle assignment problem (Section III-B), the samples of vehicles’ travel times can be drawn from some historical traffic data set. Even though the travel time is not exactly known beforehand, when the vehicle traverses a street (or path), its travel time can be observed and updated, as shown in the online version of the mobility-on-demand (Section V).

-

Ground set and matroid

-

User-defined risk level

-

Range of the parameter and discretization stage

-

An oracle that approximates as

-

Selected set and corresponding parameter

IV-B Performance Analysis of SGA

Let and be the set and the scalar chosen by SGA, and let the and be the set and the scalar chosen by the optimal solution. Our analysis uses the curvature, of function that is submodular in set . Then, we get our our main result.

Theorem 1.

Algorithm 1 yields a bounded approximation for Problem 1. Specifically,

| (9) |

with probability at least , when the number of samples, . The computational time is where and are the searching upper bound on and searching separation parameter, is the cardinality of the ground set .

SGA gives approximation of the optimal with three additional approximation errors. One approximation error comes from the searching separation . We can make this error arbitrarily small by setting to be close to zero with the cost of increasing the number of search operations . The second one is the sampling error from the oracle. Evidently, can be reduced by increasing the number of samples . The third one comes from the additive term,

| (10) |

which depends on the curvature and the risk level . When the risk level is very small, this error is very large which means SGA may not give a good performance guarantee of the optimal. However, if the function is close to modular in (), this error is close to zero. Notably, when and , SGA gives a near-optimal solution, i.e., .

Next, we briefly describe the proof of Theorem 1. We start with the proof of approximation ratio, then go to the analysis of the computational time. We need to prove on some structural lemmas beforehand. Let be the optimal set for a specific that maximizes and be the maximum value of . We sequentially search for with a searching separation . We first describe the relationship between the maximum founded by searching with a searching separation and .

Lemma 4.

| (11) |

Next, we describe the relationship between with set selected by our greedy approach and for each .

Lemma 5.

| (12) |

where is the curvature of the function in with a matroid constraint .

V Adaptive Risk-Aware Submodular Maximization

In this section, we study an adaptive version of the risk-aware submdoular maximization described in Problem 1. This is motivated by the real-time (or online) applications where either the external environment or the internal robot state is dynamic and changing. For example, the stochastic travel times of the vehicles are changing due to real-time traffic conditions in the mobility-on-demand and the sensors can fail at some point for environment monitoring. In these dynamic scenarios, if the planning is only scheduled at the initial time step and kept fixed (i.e., one-step planning), the robots (e.g., vehicles or sensors) may not be able to fully utilize the real-time information for achieving a better team performance.

Instead, the robots may need to replan to adapt to real-time situations. For instance, in the mobility-on-demand scenario, as the vehicles move they can use real-time traffic conditions to update the assignment for achieving shorter arrival time (i.e., higher utility) at demand locations as the actual travel time information is revealed.

One intuitive online strategy is to replan at all time steps. Clearly, the all-step planning can achieve a better performance than the one-step planning, since it fully utilizes the real-time information at all time steps. However, planning at all time steps can be costly (e.g., in terms of the computing resources or energy). Crucially, planning at all time steps may not be necessary.

Thus, instead of either one-step planning or all-step planning, we seek replanning strategies that can make risk-aware decisions with as fewer replanning efforts. Formally, our bicriteria optimization problem is stated as follows.

Problem 2 (Adaptive Risk-Aware Submodular Maximization).

Given a risk level , find a risk-aware sequential replanning strategy that decides when to replan and how to replan to

| (13) | ||||

where denotes the timespan of the planning process; denotes a replanning time step and denotes the replanning strategy (e.g., replacement or reassignment) at step ; denotes a sequence of replanning strategies corresponding to a sequence of replanning time steps during ; denotes the utility obtained by executing the sequence of replanning strategies ; denotes the number of times for replanning, and indicates there must exist an initial planning to start the process at time step .

In Problem 2, we aim to simultaneously maximize the process utility and minimize the number of replanning times . We seek a sequential replanning strategy that is nondominated or Pareto optimal for Problem 2. Here, the Pareto optimality depicts a situation where no solution other than could improve the process utility or reduce the number of replanning times without reducing the former or raising the latter, or there is no scope for either improving the process utility or reducing the number of replanning times.

Particularly, the process utility function captures the performance of the sequence of the replanning strategies during . For example, in the mobility-on-demand, it can be the total arrival utilities of all demand locations when these demand locations are reached by vehicles. Similarly, for environmental monitoring, it can be the joint area covered at the end of the execution horizon. The process utility is deterministic since it measures the performance when the process is done (i.e., at the final step ). Essentially the optimal process utility would be for a clairvoyant strategy that will know exactly how the scenario will unfold a priori. However, to compute the replanning strategy at some intermediate step , the robots need to optimize a stochastic utility , as the robots can only use the information (e.g., stochastic travel time or sensor working status) revealed so far and thus have uncertain knowledge of the future.

The optimal solution to Problem 2 can be found if we assume the robots know all the future information exactly, e.g., what the travel times will be or which sensors will fail. However, this is not the realistic scenario where the robots have no knowledge of what will exactly happen in the future. Thus, finding the optimal replanning strategy for Problem 2 is extremely difficult or even impossible. Notably, even with all-step planning, there is no guarantee on obtaining the optimal value of the process utility. That is because, using the information unveiled so far, the planning is myopic and could mislead the planning in the future steps. Also, minimizing the number of replanning times simultaneously makes Problem 2 even more challenging.

Instead, we relax the hardness of Problem 2 by fixing the strategy to decide how to replan at every replanning step and build on it to present a heuristic solution that is two-fold. Specifically, we leverage SGA (Algorithm 1) to compute . That is because, at each replanning step , we aim to design a risk-aware strategy to optimize the stochastic utility with representing the uncertainty of the environment in the future steps (i.e., from the current step to the end step ). That is,

which is exactly an instance of Problem 1 and SGA gives a bounded approximation (Theorem 1).

Then the question left is to decide when to replan to minimize . To this end, we exploit an event-driven mechanism where the planning is updated or recomputed only when certain conditions are met. For environmental monitoring, there is an obvious solution that the (well-working) sensors update the replacement by SGA only when some sensor fails. In this way, they can maintain a good monitoring performance without replacing themselves at all time steps. Such a strategy is not obvious for the mobility-on-demand case. Therefore, we explicitly describe the online version of the mobility-on-demand and design a triggering reassignment strategy to determine when to replan.

Online Mobility-on-Demand and Triggering Vehicle Reassignment

We study an online version of the resilient mobility-on-demand described in Section III-B. Similarly, we assign vehicles to serve demand locations. The assignment process starts at time step when vehicles start traveling toward their assigned demand locations by the initial vehicle-demand assignment. The process ends at time step when all the demand locations are reached by the vehicles. We denote the stochastic arrival time for each vehicle to each demand location at step as with the mean and variance . Then the corresponding arrival utility at step is computed as . The arrival time and arrival utility can be updated based on the real-time vehicles’ positions and traffic conditions (e.g., real-time waiting times at intersections). Similarly, for each demand location, we assign a set of vehicles to it and only the vehicle that arrives first at the demand location is chosen. The objective is to develop a replanning strategy that maximizes the total arrival utilities (or equivalently, minimizes the total arrival times) of all demand locations when all these demand locations are reached by vehicles while having the minimum number of times for replanning, as captured by Problem 2.

Toward this end, we design an adaptive triggering assignment strategy (ATA) in Algorithm 2. Specifically, for deciding how to reassign at each reassignment step , we use SGA to update the vehicle-demand assignment by using the vehicles’ real-time arrival utilities . This is based on the fact that, at each intermediate step , the problem turns out to be maximizing the CVaR of the stochastic utility function,

with and denoting the vehicle-demand assignment and the set of vehicles assigned to demand location at step . We know optimizing the CVaR of is an instance of Problem 1 and SGA yields a solution with a bounded approximation (Theorem 1). Before that, we need to decide when to reassign (i.e., the reassignment step ) which is tackled by ATA (Alg. 2) where an event-driven mechanism is adopted to update the assignment only when certain conditions are met.

A general version of ATA is described in Algorithm 2. Please find a specific implementation of ATA for the mobility-on-demand in street networks in the appendix (Alg. 3).222For clarity, we drop the time indices of notations for online mobility-on-demand in Alg. 3 and the corresponding simulations in Section VI-C. ATA mainly contains two assignment steps—initial assignment (Alg. 2, line 1) and triggering assignment (Alg. 2, line 7). Once the initial assignment (Alg. 2, line 1) is done, each vehicle travels toward its (firstly) assigned demand location (Alg. 2, line 3) and updates its arrival time and corresponding arrival utility at each time step (Alg. 2, line 4).

The reassignment is triggered by checking the arrival times of vehicles assigned to each demand location (Alg. 2, line 5). Specifically, among the set of vehicles assigned to demand location , if the arrival time of one vehicle is less than that of one other vehicle on average and has smaller uncertainty (Alg. 2, line 6), a new assignment is triggered (Alg. 2, line 7). Because, in this case, there is no need to continue assigning vehicle to demand location . Instead, it would be helpful to trigger a new assignment to assign vehicle to other demand locations. Here, is the triggering ratio. It regulates the triggering frequency, e.g., a larger triggers more assignments. ATA terminates when all demand locations are reached by vehicles (Alg. 2, line 2).

It is intuitive that ATA can (probably) achieve a shorter arrival time than one-step assignment since the real-time information (e.g., vehicles’ positions and traffic conditions) can be utilized for updating assignments. One simple example could be that if a demand location is reached by some vehicle, the other vehicles assigned to it and yet have not arrived should be reassigned to other demand locations. However, scheduling reassignment at every step, as in all-step reassignment, may not be necessary or even detrimental in some cases. That is because, the reassignment based on the information revealed so far (before the final step) is myopic and could be misleading for the future assignments. Clearly, all-step reassignment with the most number of reassignments increases the chance of misleading. In the next section, we illustrate the comparisons of these three assignment algorithms and the effect of the triggering ratio .

VI Simulations

We perform numerical simulations to verify the performance of SGA in risk-aware mobility-on-demand and robust environment monitoring, and the performance of adaptive triggering assignment (ATA) in online risk-aware mobility-on-demand. Our code is available online.333https://github.com/raaslab/risk˙averse˙submodular˙selection

VI-A Resilient Mobility-on-Demand under Arrival Time Uncertainty

We consider assigning supply vehicles to demand locations in a 2D environment. The positions of the demand locations and the supply vehicles are randomly generated within a square environment of 10-unit side length. Denote the Euclidean distance between demand location and vehicle position as . Based on the distribution discussion of the arrival utility distribution in Section III-B, we assume each arrival utility has a uniform distribution with its mean proportional to the reciprocal of the distance between demand and vehicle . Furthermore, the uncertainty is higher if the mean utility is higher. Note that, the algorithm can handle other, more complex, distributions for arrival times. We use a uniform distribution for ease of exposition. Specifically, denote the mean of as and set . We model the arrival utility distribution to be a uniform distribution as follows:

where .

From the assignment utility function (Eq. 7), for any realization of , say ,

where indicates one realization of . If all vehicle-demand pairs are independent from each other, models a multi-independent uniform distribution. We sample times from underlying multi-independent uniform distribution of and approximate the auxiliary function as

We set the upper bound of the parameter as , to make sure . We set the searching separation for as .

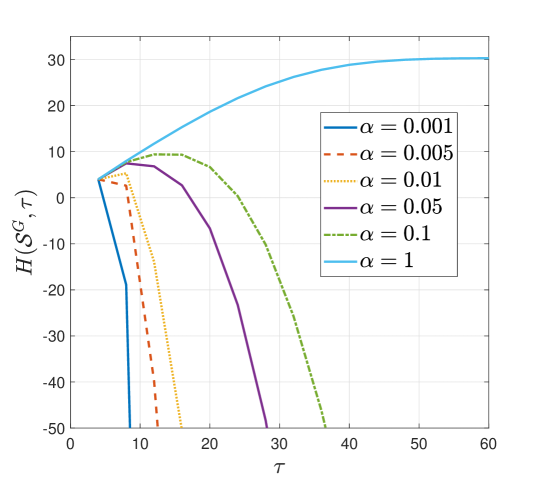

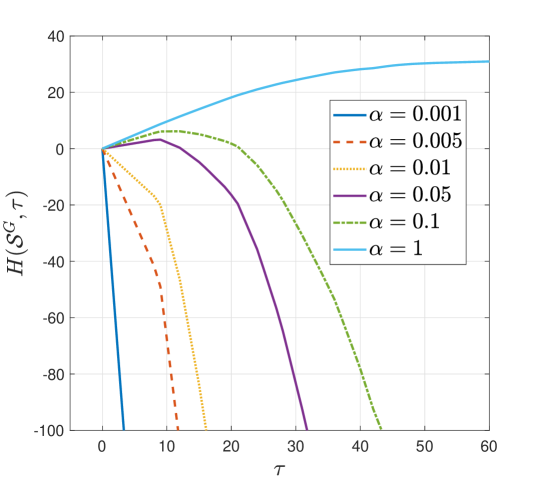

After receiving the pair from SGA, we plot the value of and with respect to different risk levels in Figure 5. Figure 5-(a) shows that increases when increases. This suggests that SGA correctly maximizes . Figure 5-(b) shows that is concave or piecewise concave, which is consistent with the property of .

We plot the distribution of assignment utility,

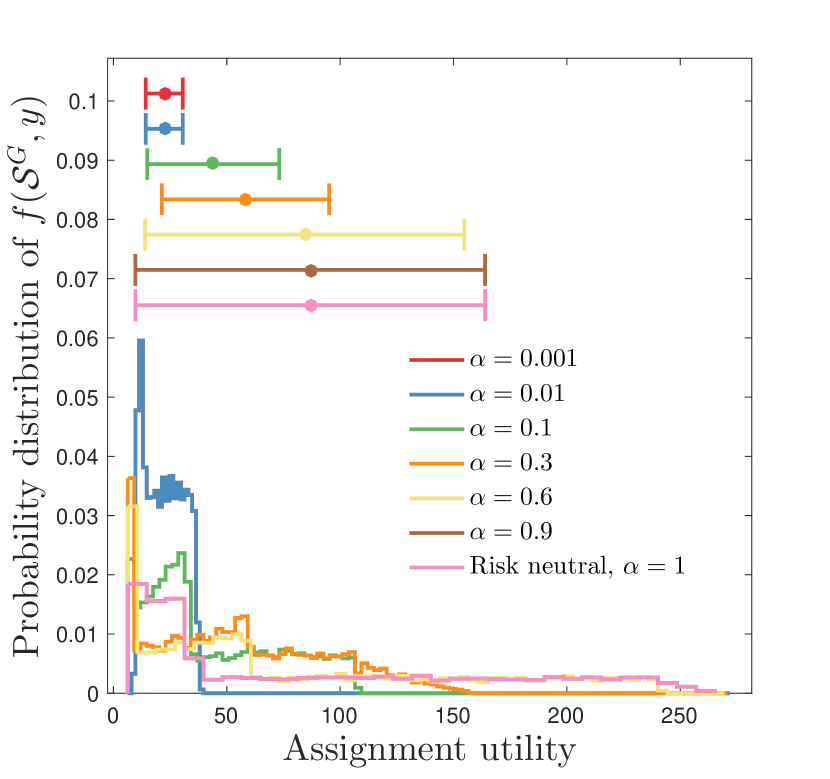

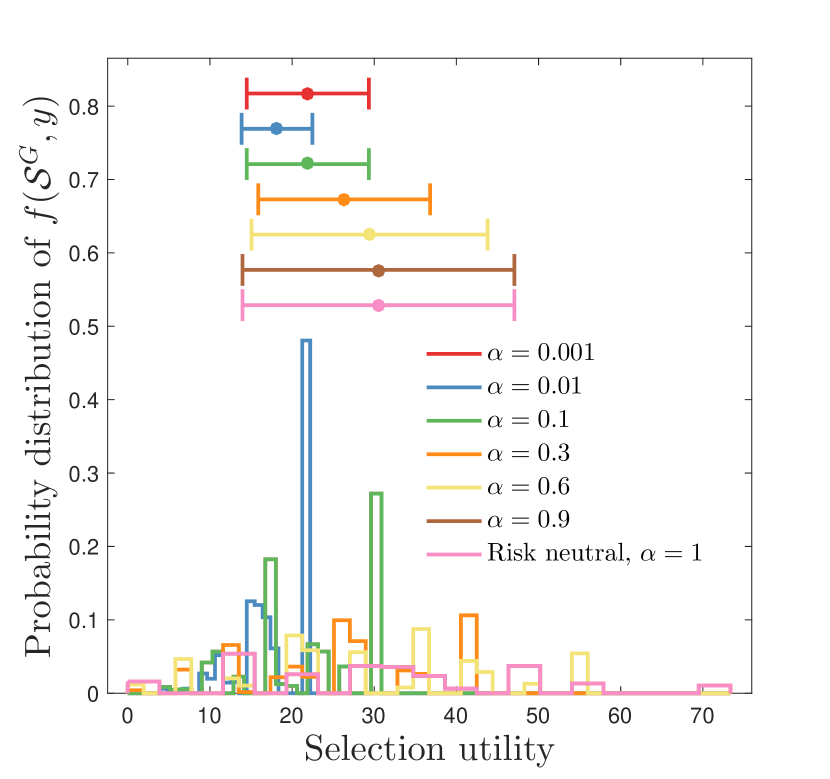

in Figure 8 by sampling times from the underlying distribution of . is a set of vehicles assigned to demand location by SGA. . When the risk level is small, vehicle-demand pairs with low utilities (equivalently, low uncertainties) are selected. This is because a small risk level indicates the assignment is conservative and only willing to take a little risk. Thus, lower utility with lower uncertainty is assigned to avoid the risk induced by the uncertainty. In contrast, when is large, the assignment is allowed to take more risk to gain more assignment utility. Vehicle-demand pairs with high utilities (equivalently, high uncertainties) are selected in such a case.

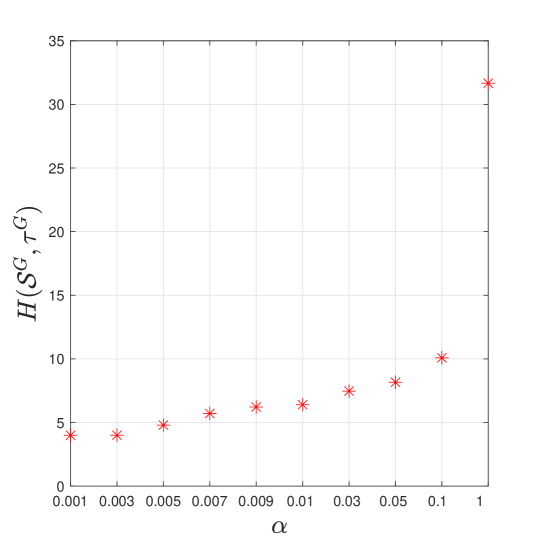

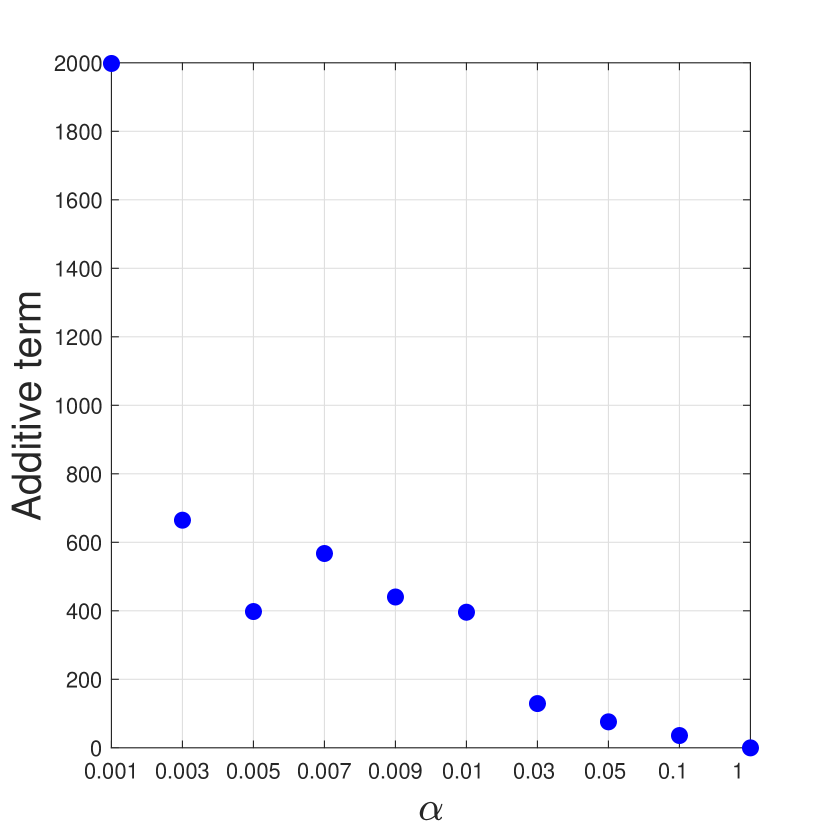

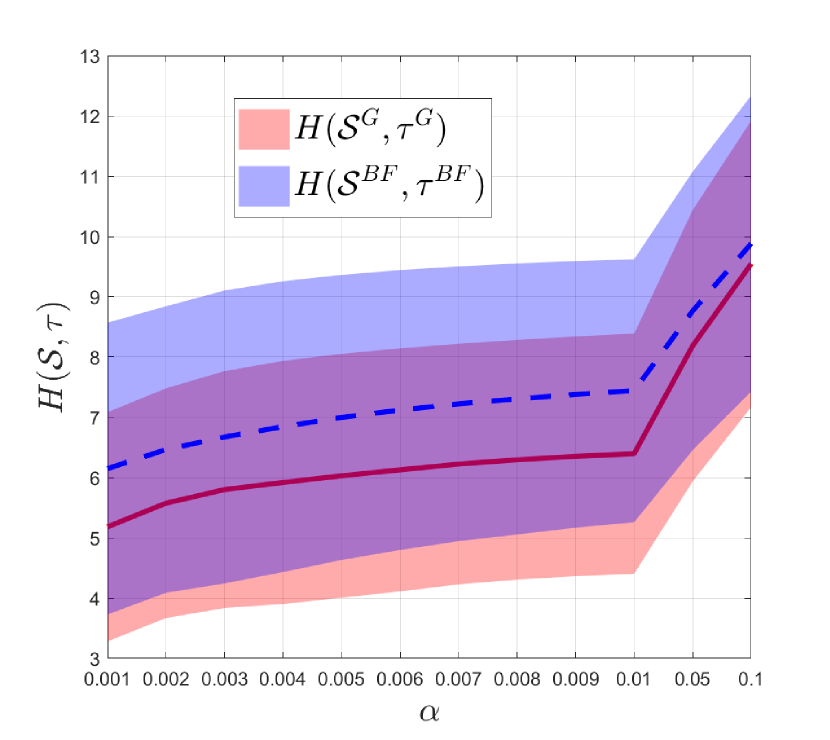

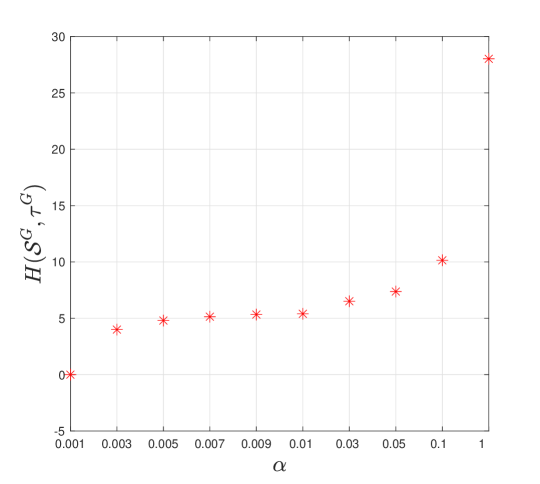

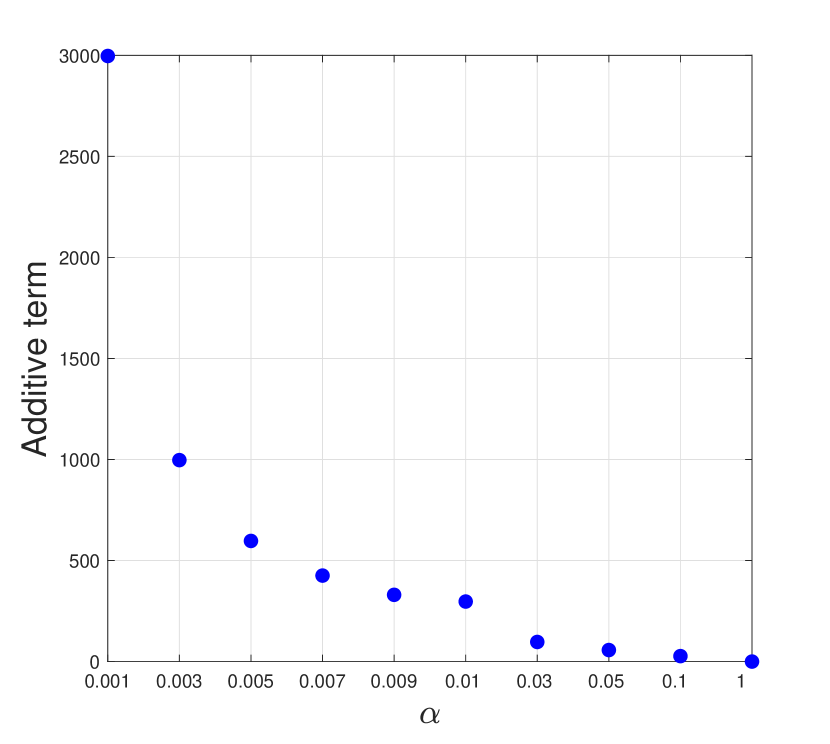

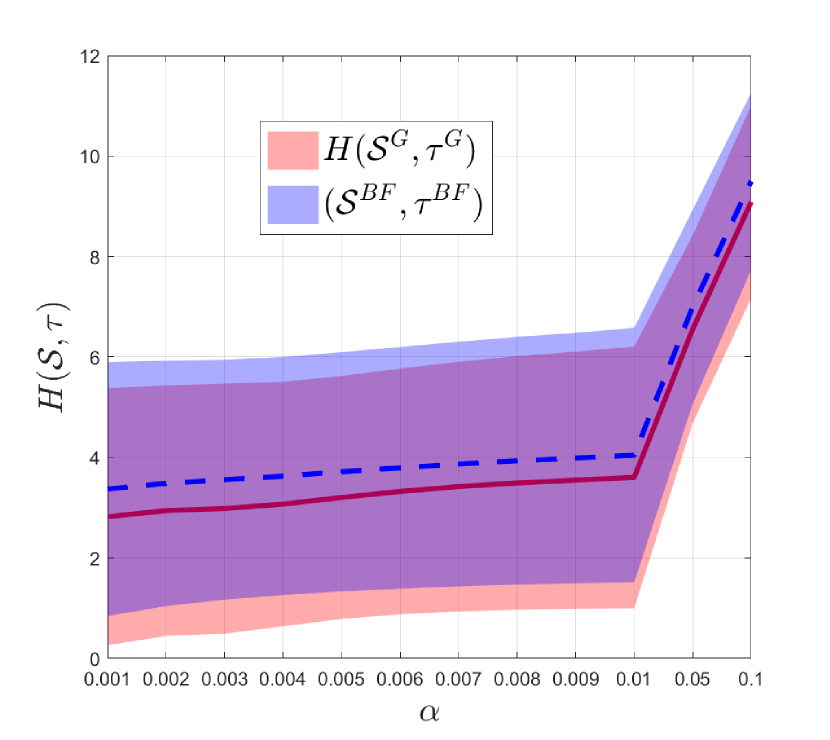

Figure 8 depicts the additive approximation error (Eq. 10) of SGA with respect to the risk level . It shows that when is close to zero, SGA has a large approximation error and the error vanishes quickly when increases (especially when ). Since SGA may not give a good solution with a large additive approximation error, it is worth evaluating how well SGA does when the risk level is very small.

To this end, for , we compare SGA with a sequential brute-force algorithm that uses the brute-force search as a subroutine instead of the greedy algorithm (lines 5-8) in Algorithm 1, as shown in Figure 8. That is, for each specific , we use the brute-force search to enumerate all possible sets to find the optimal set that maximizes . For example, in this mobility-on-demand case with 6 vehicles assigned to 4 demand locations, the total number of feasible assignments can be computed as the total number of ways to partition 6 vehicles into 4 disjoint sets (i.e., 65, see [37]) multiplying by the total number of permutations of 4 demand locations (i.e., 24), that is . Over all these 1560 possible assignments, we select out the assignment set that maximizes at each . Then we choose the best pair that gives the maximum value of , denoted as , over all pairs (collected when searching for all possible values of ). By referring to the proof of the approximation ratio of SGA (proof of Theorem 1 in the appendix), it is easy to verify that the sequential brute-force algorithm gives the following guarantee for maximizing ,

| (14) |

with probability at least , when the number of samples, . Different from SGA, the sequential brute-force algorithm does not have the additive approximation error.

We compare the performance of SGA and the sequential brute-force algorithm using the same positions of 6 vehicles and 4 demand locations randomly generated in 30 trials. Figure 8 shows that SGA works comparatively with the sequential brute-force algorithm for maximizing on average when is close to zero. This suggests SGA can still perform relatively well when it has a large additive approximation error due to very small risk levels.

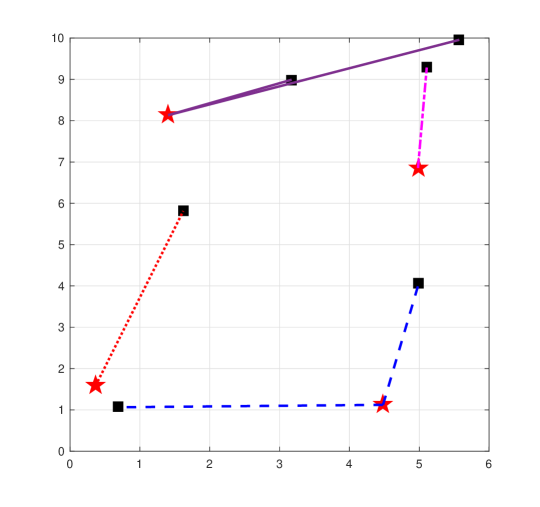

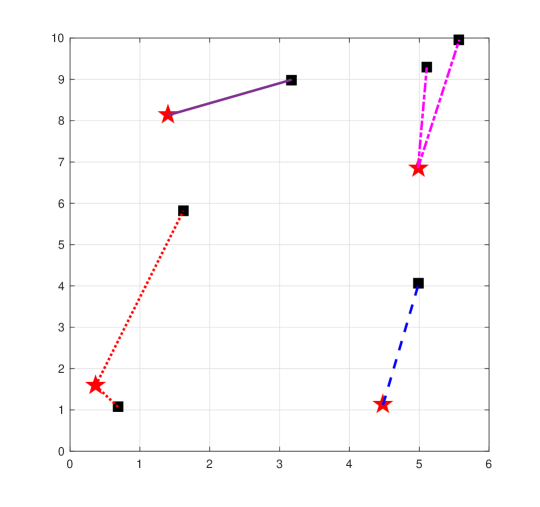

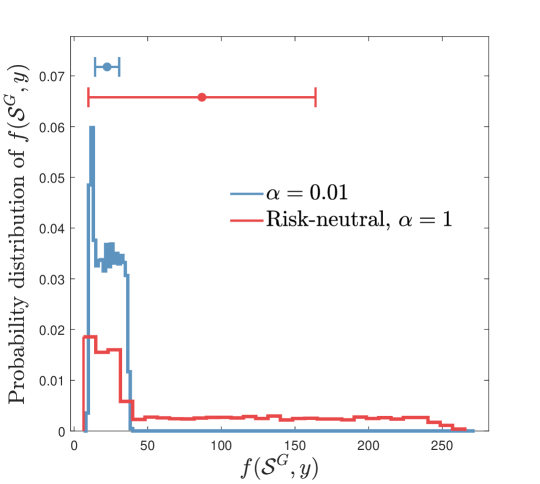

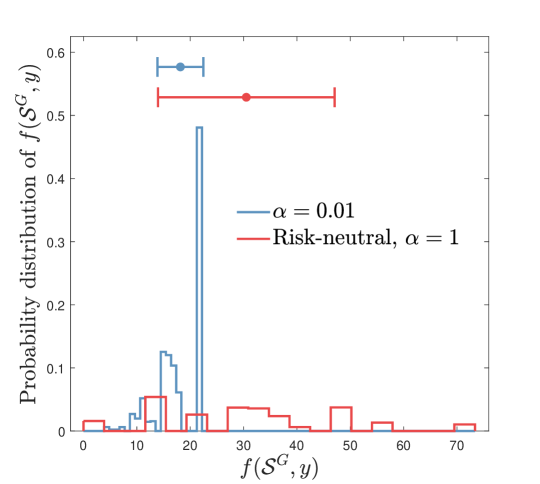

We also compare SGA (using CVaR measure) with the greedy algorithm (using the expectation, i.e., risk-neutral measure [20]) in Figure 9. Note that risk-neutral measure is a special case of measure when . We give an illustrative example of the assignment by SGA for two extreme risk levels, and . When is small (), the assignment is conservative and thus farther vehicles (with lower utility and lower uncertainty) are assigned to each demand (Fig. 9-(a)). In contrast, when , nearby vehicles (with higher utility and higher uncertainty) are selected for the demands (Fig. 9-(b)). Even though the mean value of the assignment utility distribution is larger at than at , it is exposed to the risk of receiving lower utility since the mean-std bar at has smaller left endpoint than the mean-std bar at (Fig. 9-(c)).

VI-B Robust Environment Monitoring

We consider selecting locations from candidate locations to place sensors in the environment (Fig. 4). Denote the area of the free space as . The positions of candidate locations are randomly generated within the free space . We calculate the visibility region for each sensor by using the VisiLibity library [38]. Based on the sensor model discussed in Section III-B, we set the probability of success for each sensor as

and model the working of each sensor as a Bernoulli distribution with probability of success and probability of failure. Thus the random polygon monitored by each sensor , follows the distribution

| (15) |

From the selection utility function (Eq. 8), for any realization of , say ,

where indicates one realization of by sampling . If all sensors are independent of each other, we can model the working of a set of sensors as a multi-independent Bernoulli distribution. We sample times from the underlying multi-independent Bernoulli distribution of and approximate the auxiliary function as

We set the upper bound for the parameter as the area of all the free space and set the searching separation for as .

We use SGA to find the pair with respect to several risk levels . We plot the value of for several risk levels in Figure 10-(a). A larger risk level gives a larger , which means the pair found by SGA correctly maximizes with respect to the risk level . Moreover, we plot functions for several risk levels in Figure 10-(b). Note that is computed by SGA at each . For each , shows the concavity or piecewise concavity of function .

Based on the calculated by SGA, we sample times from the underlying distribution of and plot the distribution of the selection utility,

in Figure 13. Note that, when the risk level is small, the sensors with smaller visibility region and a higher probability of success should be selected. Lower risk level suggests a conservative selection. Sensors with a higher probability of success are selected to avoid the risk induced by the sensor failure. In contrast, when is large, the selection would like to take more risk to gain more monitoring utility. The sensors with a larger visibility region and a lower probability of success should be selected. Figure 13 demonstrates this behavior except when . This is because when is very small, the approximation error (Eq. 10) is very large as shown in Figure 13, and thus SGA may not give a good solution.

Therefore, it is necessary to see how well SGA performs for small risk levels. Similar to the mobility-on-demand case, we compare SGA with a sequential brute-force algorithm that uses the brute-force search as a subroutine to enumerate all possible feasible placements for finding the optimal sensor placement for each specific . For instance, in this environment monitoring scenario with selecting 4 placement locations from 8 candidate locations, there will be placements in total. From these 70 possible placements, we choose the placement that maximizes at each . Then we pick out the best pair that has the maximum value of , denoted by , from all pairs (collected when searching for all possible values of ). Note that the sequential brute-force algorithm has no additive error for maximizing (Eq. 14).

With the same set of 8 candidate locations randomly generated in 30 trials, we compare SGA with the sequential brute-force algorithm for small risk levels in Figure 13. The result shows that on average SGA works comparatively with the sequential brute-force algorithm (especially when ) for maximizing . This implies SGA can still work relatively well on average when the risk level is close to zero.

We also compare SGA by using CVaR measure with the greedy algorithm by using the expectation, i.e., risk-neutral measure (mentioned in [2, Section 6.1]) in Figure 14. In fact, the risk-neutral measure is equivalent to the case of when . We give an illustrative example of the sensor selection by SGA for two extreme risk levels, and . When risk level is small (), the selection is conservative and thus the sensors with small visibility region are selected (Fig. 14-(a)). In contrast, when , the risk is neutral and the selection is more adventurous, and thus sensors with large visibility region are selected (Fig. 14-(b)). The mean-std bars of the selection utility distributions in Figure 14-(c) show that the selection utility at the expectation () has larger mean value than the selection at . However, the selection at has the risk of gaining lower utility since the left endpoint of mean-std bar at is smaller than the left endpoint of mean-std bar at .

VI-C Online Resilient Mobility-on-Demand

In this section, we show the effectiveness of ATA (Algs. 2, 3) by using the online mobility-on-demand with street networks. A detailed description of the settings is provided in the appendix. We compare the performance of ATA with the other three assignment strategies, offline, one-step, and all-step assignments, in terms of the arrival time, the number of assignments, and the running time. The offline assignment is a clairvoyant strategy that knows the vehicles’ arrival times (i.e., knows how the stochastic scenario will play out) exactly and uses the standard greedy algorithm [14] to compute the assignment.444In the simulation, this is done by first storing the realistic arrival times of the vehicles at the final step and then using the greedy algorithm [14] to compute an offline assignment. Thus, it can be set as a baseline. The difference of the three online assignment strategies, ATA, one-step assignment, and all-step assignment comes from how often the assignment is scheduled— In the one-step assignment, the assignment is calculated at the initial time step and is fixed thereafter; In the all-step assignment, the assignment is computed at each time step; In ATA, the assignment is triggered only at specific time steps. In both one-step and all-step assignments, all vehicles apply the “per-step online travel” rule (Alg. 3, lines 16-25) to go towards the assigned demand locations, as in the case of ATA. Particularly, in these three online assignment strategies, we compute the arrival time as the summation of all per-step time intervals ( in Eq. 20) from time of the first step to the final step when all demand locations are reached.

We consider assigning supply vehicles to demand locations on a street network, , created using OSMnx [39]. OSMnx is a python package that allows for easily constructing, projecting, visualizing, and analyzing complex street networks [39]. We give an example showing a network of drivable public streets created by OSMnx in Blacksburg, VA, USA in Figure 15. OSMnx also allows for finding a shortest path between two nodes (intersections) of the networks by Dijkstra’s algorithm if there exists one (Fig. 15). Thus, we use OSMnx to compute a shortest path from each vehicle’s initial position to each demand location, if there exists one. We can also extract the intersection degree and edge length of the street network directly by using OSMnx.

We model the waiting time at intersection following a truncated normal distribution,

| (16) |

where denotes the maximum waiting time at the intersection . We set the variance of the waiting time to be proportional to the degree of the intersection, i.e., with . A larger degree means more incoming and outgoing edges, and thus the traffic at this intersection is more likely to be congested, which increases the probability of higher waiting time. Notably, the truncated Gaussian distribution is just one possible way to capture the randomness of the waiting time. In practice, instead of assuming a particular distribution, one would use historic traffic data to model the distribution at each intersection and along every edge. Our algorithm works for any model that can be sampled.

We set and model the maximum waiting time as . The model assumes that a larger degree of an intersection implies a larger maximum waiting time there. We model the real-time waiting time at an intersection for each vehicle as a sample from the truncated normal distribution (Eq. 16). In practice, the real-time waiting time can be acquired when the vehicle reaches the intersection.

We set and use the speed limits of the street network in Blacksburg from Google Maps to compute the edge travel time (see Eq. 17). If a demand location is not reachable from a vehicle’s position, we set the path travel time (Eq. 18) from the vehicle to the demand as infinity. We set the risk level in SGA (Alg. 1).

VI-C1 Qualitative Results

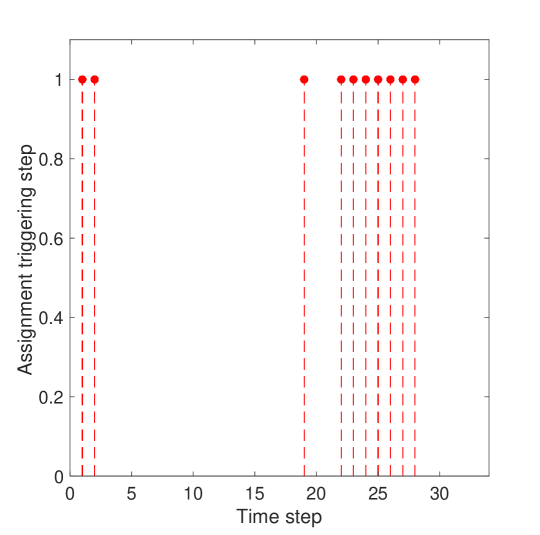

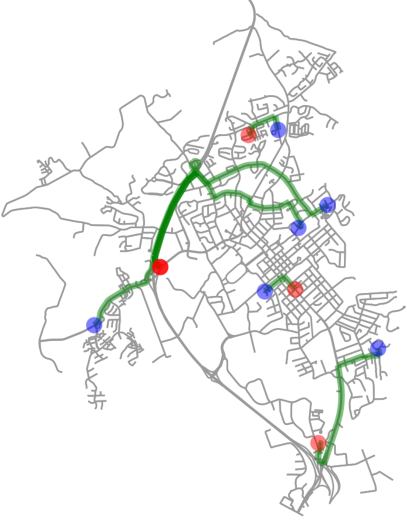

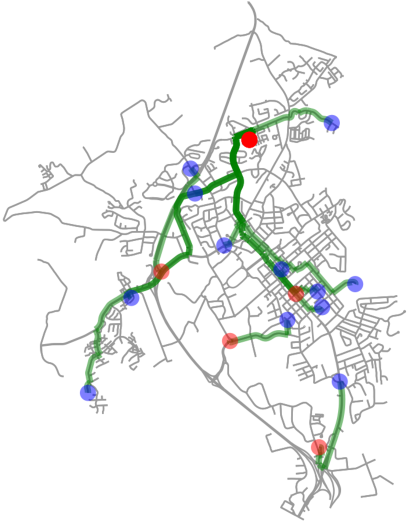

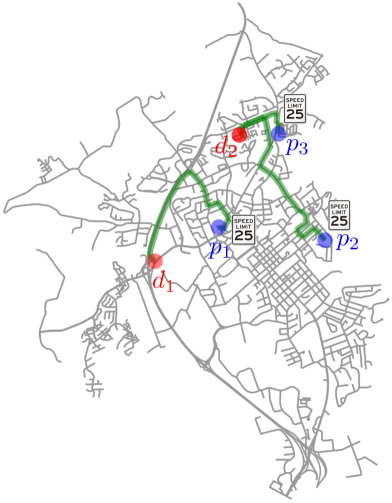

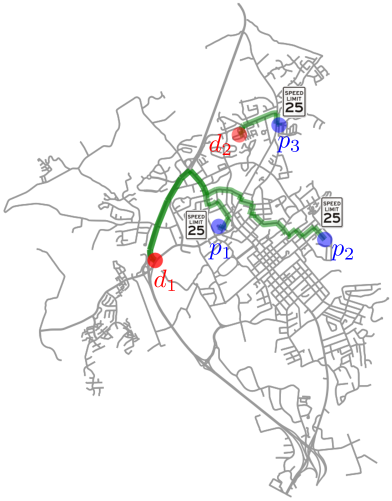

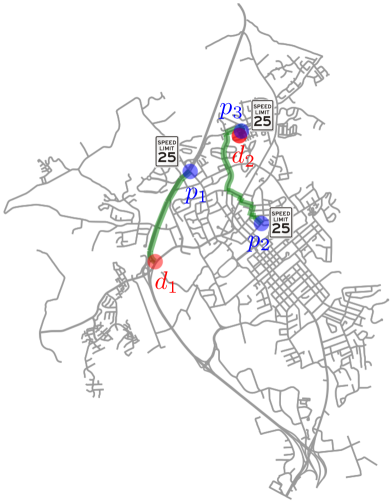

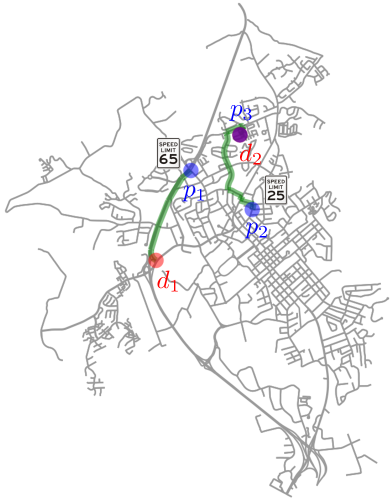

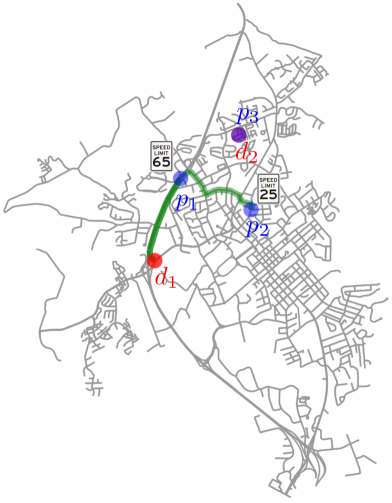

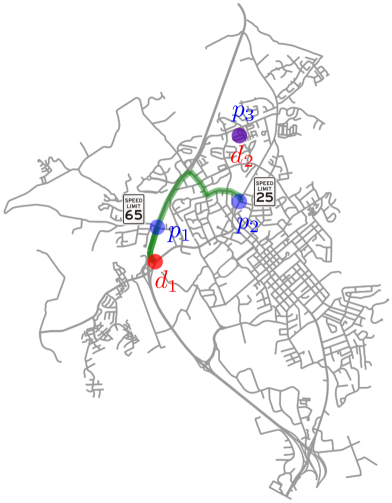

We first show one trial of ATA in action in Figure 18 where we assign vehicles to demand locations with triggering ratio . Since we model the real-time waiting time at each intersection as a random sample from its distribution, ATA can end up with different results in different trials, even with the same vehicles’ initial positions and demand locations.

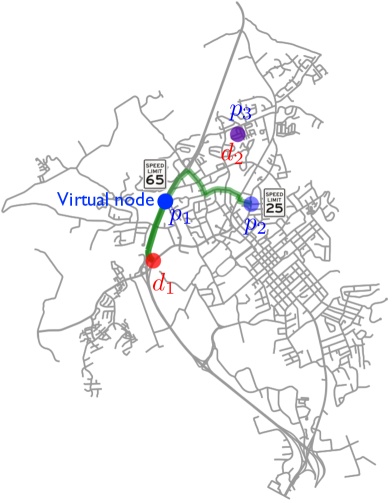

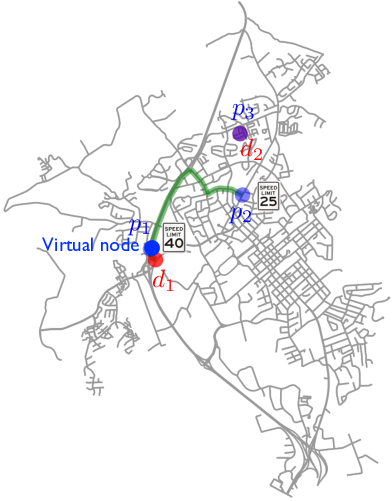

In Figure 18, ATA starts at time step 1 (Fig. 18-(a)) and ends at time step 34 (Fig. 18-(l)) when the two demand locations, and , are reached. Within these 34 time steps, the assignment is only triggered at 10 time steps (steps 1, 2, 19, 22, 23, 24, 25, 26, 27, 28) as shown in Figure 16. At these 10 steps, the triggering conditions with (Eqs. 21 and 22) are satisfied. For example, at step 1 (Fig. 18-(a)), the path length from to is less than half of that from to (Eq. 21) and the path degree from to is less than that from to (Eq. 22). In this case, there is no need to continue assigning vehicle 2 to since it is likely that vehicle 3 will reach earlier than vehicle 2. Therefore, triggering the reassignment to assign vehicle 2 to could be helpful in reducing the arrival time at (step 2, Fig. 18-(b)). Similar assignment flip happens from step 22 (Fig. 18-(e)) to step 23 (Fig. 18-(f)) where vehicle 2 is switched to be assigned to . However, the assignment does not flip at all triggering time steps. For example, even though the assignment is triggered at step 19 (Fig. 16), the assignment remains the same at step 20 (Fig. 18-(c) & (d)). One possible reason could be that assigning vehicle to is still more helpful, since vehicle is already very close to (Fig. 18-(c) & (d)). ATA also guarantees that once a demand is reached, e.g., in step 28, is reached by vehicle 3 (Fig. 18-(g)), no vehicle will be assigned to it later (Fig. 18-(h), (i), (j), (k), (l)). Particularly, in this 3-vehicle 2-demand system, there is not even reassignment triggered afterwards (Fig. 16). In Figure 18-(i) & (k), we create virtual nodes (darker blue dots) to denote the intermediate positions of the vehicle on the highway.

VI-C2 Quantitative Results

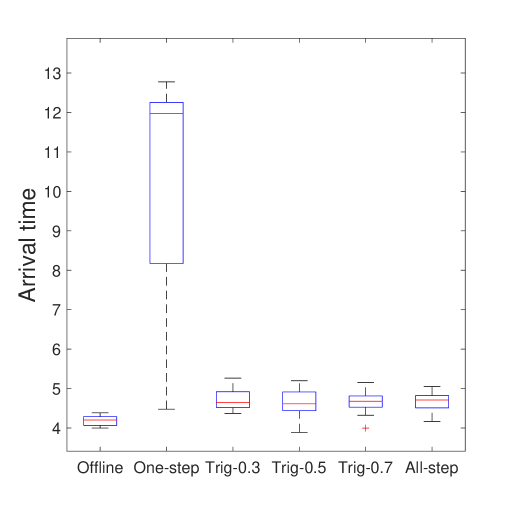

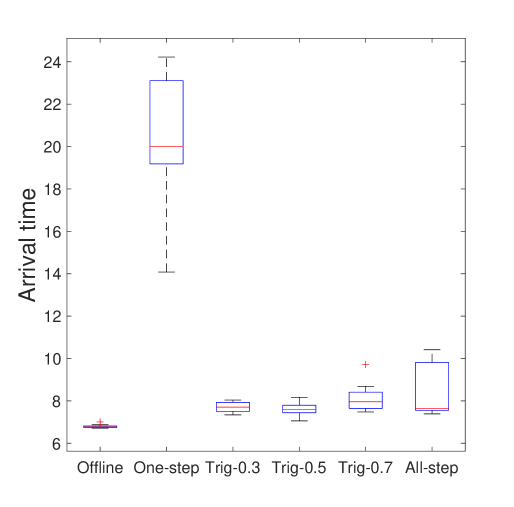

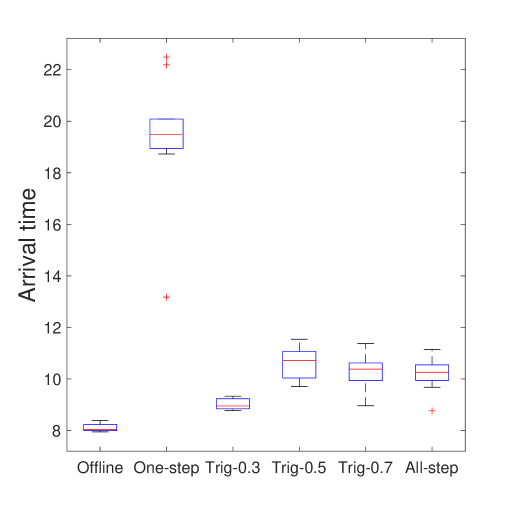

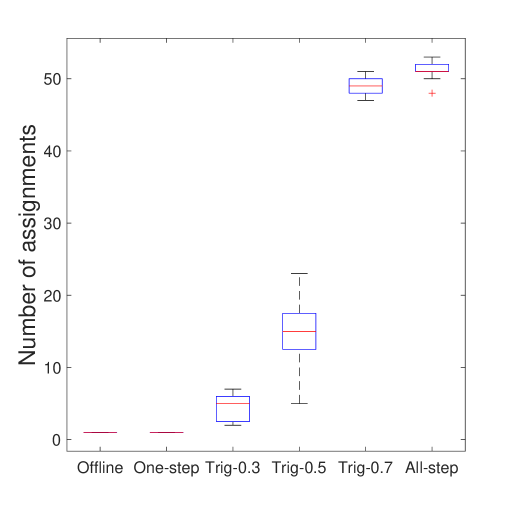

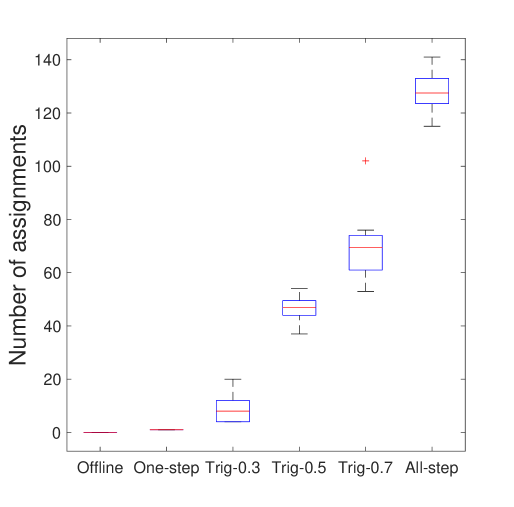

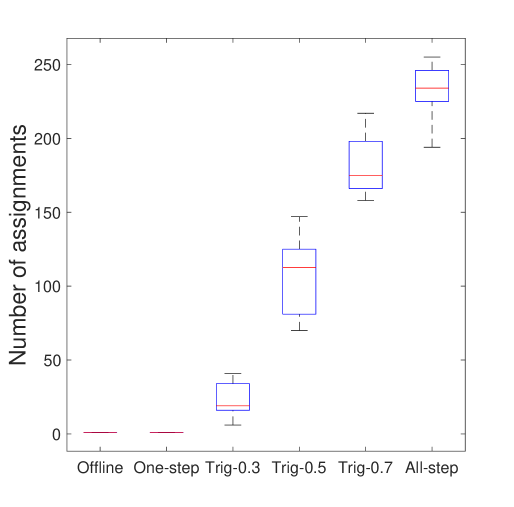

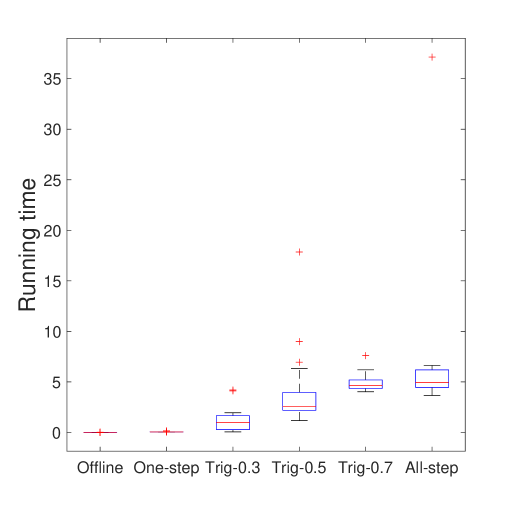

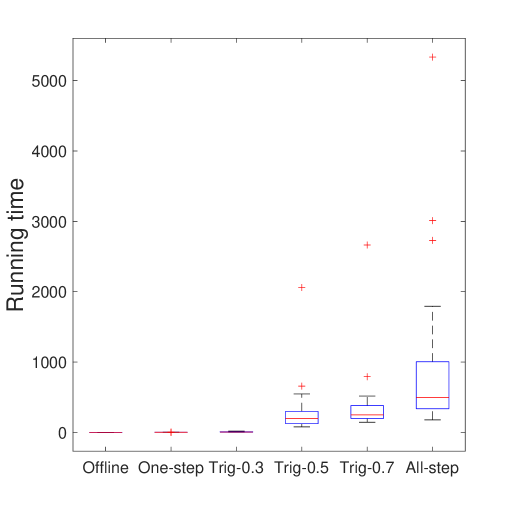

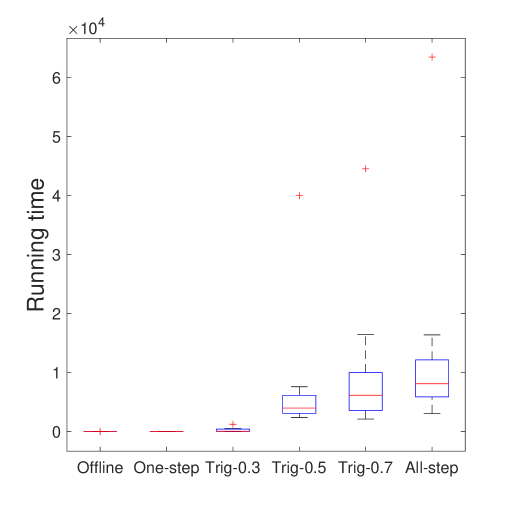

We then compare the arrival time, number of assignments, and running time of these three assignment strategies in Figure 19. We execute all three assignment strategies in 10 trials with the same initial vehicles’ positions and demand locations. In particular, we consider three scales of vehicle-demand system, e.g., (Fig. 18), (Fig. 17-(a)) and (Fig. 17-(b)). For each scale of the vehicle-demand system, we evaluate three different triggering ratios, , in each trial.

Figure 19-(a), (b) & (c) show that the offline assignment performs the best in terms of the arrival time, which is intuitive given that it knows the arrival times exactly, while the other three online assignments have the uncertain knowledge of the arrival times only. We observe that ATA with some suitable triggering ratios (e.g., in Fig. 19-(a), in Fig. 19-(b), and in Fig. 19-(c)) performs close to the offline strategy, which shows the effectiveness of ATA. Also, note that ATA and the all-step assignment reach all demand locations earlier than the one-step assignment. This is expected since in ATA and all-step assignment, the vehicles are reassigned to reduce arrival time using the real-time information, while one-step assignment only assigns the vehicles at the initial time step. For the same reason, one-step assignment has less running time and fewer assignments, as shown in Figure 19-(d) to (i).

Figures 19-(d) to (i) show that ATA schedules fewer assignments and use less running time than that of the all-step assignment. In particular, Figures 19-(d), (e), & (f) show that ATA with avoids at least half of the assignments compared to all-step assignment. Even with fewer assignments, ATA performs comparably with or in some cases even better than all-step assignment in terms of the arrival time as shown in Figure 19-(a), (b) & (c). Particularly, with respect to the average of arrival time, ATA with triggering ratio , , and performs better than all-step assignment in 3-vehicle 2-demand (Fig. 19-(a)), 6-vehicle 4-demand (Fig. 19-(b)), and 12-vehicle 5-demand (Fig. 19-(c)) systems, respectively. This result echoes the analysis at the end of Section V that more assignments may not always help because the assignment using the traffic conditions revealed so far is nearsighted.

We also observe from Figure 19-(d) to (i) that a larger triggering ratio leads to more assignments and more running time of ATA. This is because, with a larger triggering ratio, the assignment will be triggered more frequently as shown in Algorithm 2, line 6. Particularly, for three triggering ratios , ATA with schedules fewer assignments (Fig. 19-(d), (e) & (f)) and spends less running time (Fig. 19-(g), (h) & (i)), while achieving a comparable (Fig. 19-(a) & (b)) or even better (Fig. 19-(c)) performance than that of ATA with . This again verifies the fact that more assignments during the online mobility-on-demand process may be unhelpful and even misleading.

VII Conclusion and Discussion

We studied a risk-aware discrete submodular maximization problem. We provided the first positive results for discrete CVaR submodular maximization for selecting a set under matroidal constraints. In particular, we proposed the Sequential Greedy Algorithm and analyzed its approximation ratio and the running time. We also studied the problem of the adaptive risk-aware submodular problem for the online version of the mobility-on-demand and environmental monitoring cases. We presented a triggering replanning strategy for this problem. In particular, for online mobility-on-demand, we designed an adaptive triggering assignment strategy (Algorithm 2) to reduce unnecessary computation. We demonstrated the two practical use-cases of the CVaR submodular maximization problem and verified the effectiveness of adaptive triggering assignment approach (Algorithm 2).

Notably, our Sequential Greedy Algorithm works for any matroid constraint. In particular, the multiplicative approximation ratio can be improved to if we know that the constraint is a uniform matroid [34, Theorem 5.4].

The additive term in our analysis depends on . This term can be large when the risk level is very small. Even though, in practice, SGA works relatively well on average with small risk levels (Figs. 8 & 13), our ongoing work is to remove this dependence on , perhaps by designing another algorithm specifically for low risk levels. We note that if we use an optimal algorithm instead of the greedy algorithm as a subroutine, then the additive term disappears from the approximation guarantee (e.g., the sequential brute-force algorithm). The algorithm also requires knowing . We showed how to find (or an upper bound for it) for the two case studies considered in this paper. Devising a general strategy for finding is part of our ongoing work.

Note that, in the adaptive triggering assignment (ATA), increasing the triggering ratio results in more assignments but may not always improve the performance (i.e., achieving a shorter arrival time) as shown in Figure 19. Thus, our second future research direction is to design a generic approach for deciding the best triggering ratio .

Our third line of ongoing work focuses on applying the risk-aware strategy to multi-vehicle routing, patrolling, and informative path planning in dangerous environments [40] and mobility on demand with real-world data sets (2014 NYC Taxicab Factbook).555http://www.nyc.gov/html/tlc/downloads/pdf/2014˙taxicab˙fact˙book.pdf

In the mobility-on-demand application, we define the objective function as the sum of arrival utilities at all demand locations (Eq. 7). The “sum” metric captures total assignment utility and is commonly used in vehicle assignment problems (see [20, 41]). However, in the mobility-on-demand scenario, one typically expects all demand locations to be reached by vehicles within the least time. Hence, a more desirable objective would be to maximize the minimum arrival utility (or equivalently, to minimize the maximum arrival time) to each demand location [42]. However, the minimum arrival utility (or maximum arrival time) is not submodular (or supermodular) in the decision set , so that Algorithm 1 may not be directly utilized or have a bounded approximation guarantee to optimize it. Therefore, our fourth future research avenue is to revisit the mobility-on-demand application with the objective of maximizing minimum arrival utility (or minimizing maximum arrival time) and, building on Algorithm 1, design corresponding risk-aware algorithms with hard guarantees.

As a final comment, we discuss the reason for choosing CVaR over other risk-aware measures such as mean-variance [27] and VaR [25]. In general, this is a design choice and CVaR may not be the best choice in some cases. Generally speaking, for the utility with Gaussian distribution, it is more convenient to use the mean-variance measure given that it has a closed-form expression [43] and is equivalent to CVaR with appropriate risk parameters selected. However, since it needs to know the mean and variance of the distribution, it does not work for arbitrary distributions (without a closed-form expression). VaR measures how much a low utility we might get with a given probability. If the distribution of the utility is smooth (or stable), VaR is sufficient for measuring the risks. However, the more fluctuant the utility, the greater the chance that VaR will not quantify the risks well, as it only cares about a single cutoff point. CVaR is a more suitable measure for this scenario by considering all the bad tailed cases. CVaR is also more desirable for the cases where the bad low probability (tailed) events have large value or impact and can cause huge losses since it is more conservative than VaR (Fig. 2). Further, CVaR has nicer properties than mean-variance and VaR for capturing risks in robotics [28] and is easier for optimization when it is computed by drawing samples [22].

Appendix A Appendix

We start by describing the settings for the online mobility-on-demand with street networks. We then introduce the corresponding OTA in Algorithm 3 based on these settings. After that, we provide proofs for the lemmas and the theorem in this paper.

A-A Online Mobility-on-Demand with Street Networks

We consider the vehicles travel on a street network with the intersections as nodes and the drive-way connecting two adjacent intersections, and , as edges . Notably, the street network is a directed graph because of the driving direction on the street. We use to denote the degree of a node, which is the number of the incoming and outgoing edges of the node.

For an edge , we denote its the length by . Denote a path from node to node as a series of orderly connected edges on the graph with the following form . We compute the length and the degree of path by the summation of the lengths of all edges and the summation of the degrees of all nodes on the path, respectively. Denote the set of all nodes on path as .

Due to the unpredictable traffic condition at the intersection (node), we assume that the waiting time at an unseen intersection is a random variable, denoted as . We assume the variance of the waiting time, is proportional to the degree of the intersection. Because, for an intersection, a larger degree means more incoming and outgoing edges, and thus the traffic condition at this intersection can have larger uncertainty. However, when vehicle arrives at an intersection, it can acquire the real-time traffic condition and the waiting time at the intersection.

We compute the time to traverse an edge by

| (17) |

where denotes the limited speed on edge and . Here, we do not consider the uncertain traffic condition when the vehicle is travelling on the edges. Thus, as shown in Equation 17, the edge travel time can be obtained beforehand.

Then, the time to traverse a path combines the waiting time at all the intersections and the time to travel through all the edges on the path. That is,

| (18) |

Notably, the path travel time is a random variable with its randomness induced by the waiting time. Similarly, we compute the path travel time by using a sampling method—taking an equal number of samples of the waiting time at each intersection and then using Equation 18 with appropriate dimension manipulation. Clearly, the arrival utility to from through traveling along path can be computed as

| (19) |

We denote the time that each vehicle needs to arrive at the next intersection as . Then the per-step time interval is computed as

| (20) |

Notably, the per-step time interval depends on the from all the vehicles and can be changing at each time step. Also, when computing at each step, some vehicles may wait at the intersections whereas the others may be travelling on the edges.

For simplicity, we assume the vehicles’ initial positions and the demand locations are some nodes (intersections) of graph . 666Indeed, if the positions of some vehicles are not at the intersections, we can easily create corresponding virtual intersections for them and add the virtual intersections on the graph.

A-B Online Triggering Assignment on Street networks

In this section, we explicitly introduce our online triggering assignment strategy on street networks in Algorithm 3.

-

Graph with intersections and edges

-

demand locations with corresponding intersections, , . vehicles’ initial positions with corresponding intersections, ,

Initial assignment (Alg. 3, lines 1-3). We first find a shortest path from each vehicle’s initial position to each demand location by using Dijkstra’s algorithm (Alg. 3, line 1). Then, we use Equations 18, 19 to compute the arrival utility of these shortest paths (Alg. 3, line 2). Finally, we select a risk level and use SGA (Alg. 1) to get an initial vehicle-to-demand assignment with (Alg. 3, line 3).

After the initial assignment, each vehicle knows its assigned demand location with the corresponding shortest path, (computed in Alg. 3, line 1). Then each vehicle travels on its shortest path towards its assigned demand location. Notably, the demand location and the corresponding (shortest) path assigned to each vehicle can be changing because of the online reassignment later on.

Our terminated condition is to guarantee that all demand locations are reached (Alg. 3, line 5), which needs an underlying assumption that the number of vehicles is larger than the number of demand locations, i.e., .

Per-step time interval update (Alg. 3, lines 4, 6-15). To update the per-step time interval at each time step, each vehicle stores the previous intersection it was in, , which is initialized by an empty set (Alg. 3, line 4).

-

If vehicle arrives at a new intersection (Alg. 3, line 7), it updates its previous intersection by the current new intersection (Alg. 3, line 8) and acquires the real-time waiting time at the new intersection (Alg. 3, line 9). Also, it computes the time to spend for arriving at the next intersection as (Alg. 3, line 10).

Per-step online travel (Alg. 3, lines 16-25). Based on the current per-step time interval , each vehicle can decide its motion at the current time step.

-

if vehicle ’s waiting time at the current intersection is less than per-step time (Alg. 3, line 21), it will leave the current intersection or it is already travelling on the current edge , i.e., . In both cases, even though vehicle cannot reach the next intersection (since ), it will traverse some distance on the current edge (Alg. 3, line 23), which is computed by leveraging on Equation 17 as,

Triggering reassignment (Alg. 3, lines 26-31). We trigger the reassignment when some condition happens. Recall that, for each demand location , it has a set of vehicles assigned to it. Thus, in total, there are shortest paths to demand . We check for all demand locations (Alg. 3, line 26) and trigger the reassignment as long as there exists a demand location with,

| (21) | |||

| (22) |

where denotes the triggering ratio (Alg. 3, line 27). Because, in this case, there exists a path that has a shorter travel length and smaller travel time uncertainty (remember we use the degree to capture the waiting time uncertainty), than that of the other path . Thus, there is no need to continue assigning the vehicle with path to the demand . We therefore trigger the reassignment and hopefully assign this vehicle to other demand location to reduce the total travel time (Alg. 3, lines 28-30). Notably, the triggering ratio regulates the frequency of reassignment, i.e., a larger triggers more reassignments.

A-C Proofs

Proof of Lemma 1:

Proof.

Since is monotone increasing and submodular in , is monotone decreasing and supermodular in , and its expectation is also monotone decreasing and supermodular in . Then is monotone increasing and submodular in .

Proof of Lemma 2:

Proof.

Since is convex in , its expectation is also convex in . Then is concave in and is concave in . ∎

Proof of Lemma 3:

Proof.

By using the result in [22, Lemma 1 and Proof of Theorem 1], we know that is concave and continuously differentiable with derivative given by

where is the cumulative distribution function of . Thus, , which proves the lemma. ∎

Proof of the number of samples :

Proof.

We reach the statement by using the proof by Ohsaka and Yoshida [30, Lemmas 4.1-4.5]. We have via taking (the upper bound of the search separation ), in their Lemma 4.4. Then, in their Lemma 4.5, to make

| (23) |

we need to set

| (24) |

By Dvoretzky-Kiefer-Wolfowitz inequality, Inequality 24 fulfills with probability at least . Thus, by setting , we have . ∎

Proof of Lemma 11:

Proof.

Denote with . From Lemmas 2 and 3, we know is concave in and . The properties of concavity and bound on the gradient give

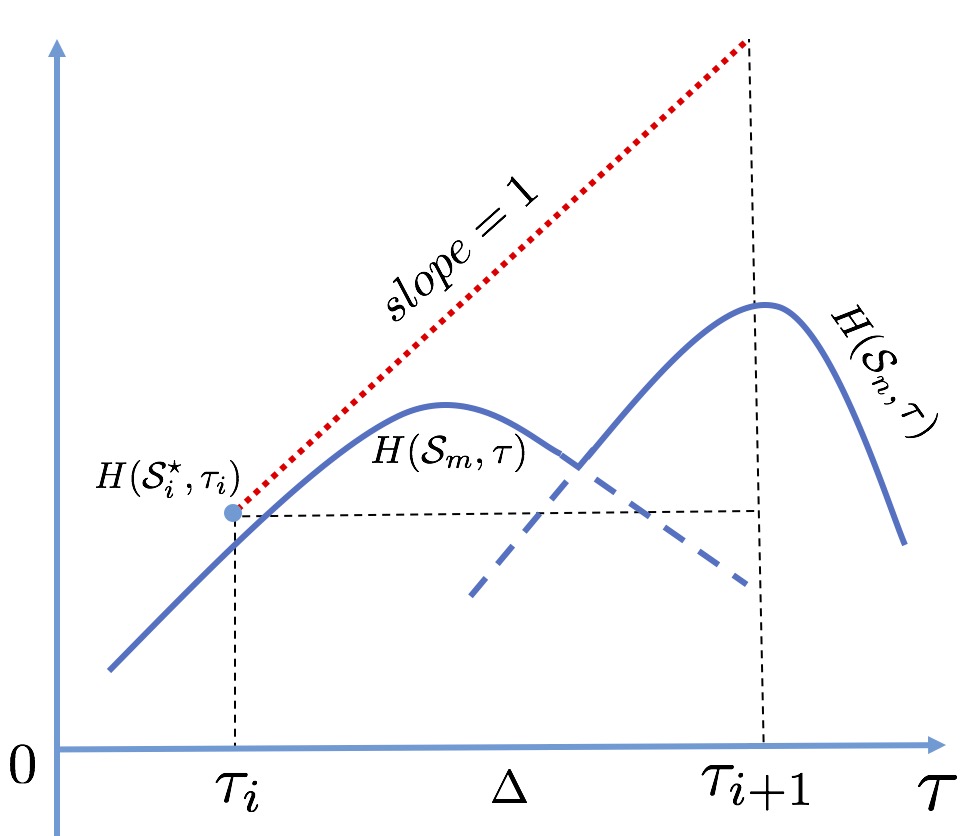

We illustrate this claim by using Figure 20-(a). Since is the optimal set at for maximizing , the value of with any other set at is at most . That is, . Since is a concave function of for any specific , can be a single concave function, i.e., or or a piecewise concave function by a combination of several concave functions, i.e., a combination of and during (Figure 20-(a)). In either case, is below the line starting at with during (the red dotted line in Fig. 20-(a)). Since and has a bounded gradient . Thus, .

Then we have . Note that is the maximum value of at each interval . The maximum value of , is equal to one of . Thus, we reach the claim in Lemma 11. ∎

Proof of Lemma 5:

Proof.

We use a the previous result [34, Theorem 2.3 ] for the proof of this claim. We know that for any given , is a non-normalized monotone submdoular function in (Lemma 1). For maximizing normalized monotone submodular set functions, the greedy approach can give a approximation of the optimal performance with any matroid constraint [34, Theorem 2.3]. After normalizing by , we have

| (25) |

with any matroid constraint. Given and , we transform Equation 25 into,

| (26) |

Thus, we prove the Lemma 5. ∎

Proof of Theorem 1:

Approximation bound. From Equation 12 in Lemma 5, we have is bounded by

| (27) |

Denote this upper bound as

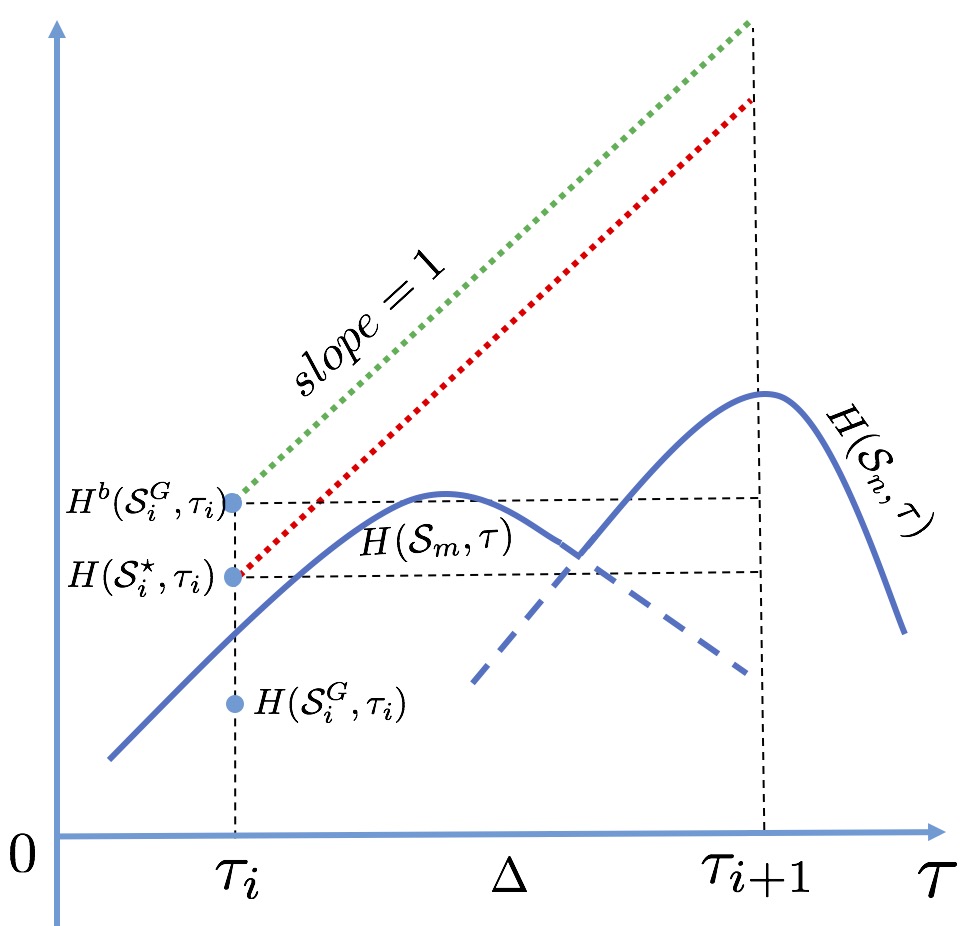

We know is below the line starting at with during (the red dotted line in Fig. 20-(a)/(b)) (Lemma 11). must be also below the line starting at with during (the green dotted line in Fig. 20-(b)). Similar to the proof in Lemma 11, we have and

| (28) |

SGA selects the pair as the pair with . Then by Inequalities 27 and 28, we have

| (29) |

By rearranging the terms, we get

| (30) |

Note that we use an oracle to approximate with error by the sampling method (Eq. 23). By considering the sampling error , we reach the statement of the approximation bound in Theorem 1.

Computational time. Next, we give the proof of the computational time of SGA in Theorem 1. We verify the computational time of SGA by following the stages of the pseudo code in Algorithm 1. First, from Algorithm 1, lines 2 to 10, we use a “for” loop for searching which takes evaluations. Second, within the “for” loop, we use the greedy algorithm to solve the subproblem (Alg. 1, lines 4–8). In order to select a subset with size from a ground set with size , the greedy algorithm takes rounds (Alg. 1, line 5), and calculates the marginal gain of the remaining elements in at each round (Alg. 1, line 6). Thus, the greedy algorithm takes evaluations. Third, by calculating the marginal gain for each element, the oracle samples times for computing . Thus, overall, the “for” loop containing the greedy algorithm with the oracle sampling takes evaluations. Last, finding the best pair from storage set (Alg. 1, line 11) takes time. Therefore, the computational complexity for SGA is,

given .

References

- [1] J. O’Rourke, Art gallery theorems and algorithms. Oxford University Press Oxford, 1987, vol. 57.

- [2] A. Krause, A. Singh, and C. Guestrin, “Near-optimal sensor placements in gaussian processes: Theory, efficient algorithms and empirical studies,” Journal of Machine Learning Research, vol. 9, no. Feb, pp. 235–284, 2008.

- [3] B. P. Gerkey and M. J. Matarić, “A formal analysis and taxonomy of task allocation in multi-robot systems,” The International Journal of Robotics Research, vol. 23, no. 9, pp. 939–954, 2004.

- [4] J. Vondrák, “Optimal approximation for the submodular welfare problem in the value oracle model,” in Proceedings of the fortieth annual ACM symposium on Theory of computing. ACM, 2008, pp. 67–74.

- [5] J. R. Spletzer and C. J. Taylor, “Dynamic sensor planning and control for optimally tracking targets,” The International Journal of Robotics Research, vol. 22, no. 1, pp. 7–20, 2003.

- [6] O. Tekdas and V. Isler, “Sensor placement for triangulation-based localization,” IEEE transactions on Automation Science and Engineering, vol. 7, no. 3, pp. 681–685, 2010.

- [7] P. Tokekar, V. Isler, and A. Franchi, “Multi-target visual tracking with aerial robots,” in Intelligent Robots and Systems (IROS 2014), 2014 IEEE/RSJ International Conference on. IEEE, 2014, pp. 3067–3072.

- [8] L. Zhou, V. Tzoumas, G. J. Pappas, and P. Tokekar, “Resilient active target tracking with multiple robots,” IEEE Robotics and Automation Letters, vol. 4, no. 1, pp. 129–136, 2018.

- [9] L. Zhou and P. Tokekar, “Sensor assignment algorithms to improve observability while tracking targets,” IEEE Transactions on Robotics, vol. 35, no. 5, pp. 1206–1219, 2019.

- [10] L. Zhou, V. Tzoumas, G. J. Pappas, and P. Tokekar, “Distributed attack-robust submodular maximization for multi-robot planning,” in 2020 IEEE International Conference on Robotics and Automation (ICRA). IEEE, 2020, pp. 2479–2485.

- [11] A. Singh, A. Krause, C. Guestrin, and W. J. Kaiser, “Efficient informative sensing using multiple robots,” Journal of Artificial Intelligence Research, vol. 34, pp. 707–755, 2009.

- [12] G. Shi, L. Zhou, and P. Tokekar, “Robust multiple-path orienteering problem: Securing against adversarial attacks,” in 2020 Robotics: Science and Systems (RSS), 2020, to appear.

- [13] G. L. Nemhauser, L. A. Wolsey, and M. L. Fisher, “An analysis of approximations for maximizing submodular set functions–i,” Mathematical programming, vol. 14, no. 1, pp. 265–294, 1978.

- [14] M. L. Fisher, G. L. Nemhauser, and L. A. Wolsey, “An analysis of approximations for maximizing submodular set functions—ii,” in Polyhedral combinatorics. Springer, 1978, pp. 73–87.

- [15] H. Ding and D. Castanón, “Multi-agent discrete search with limited visibility,” in Decision and Control (CDC), 2017 IEEE 56th Annual Conference on. IEEE, 2017, pp. 108–113.

- [16] R. K. Williams, A. Gasparri, and G. Ulivi, “Decentralized matroid optimization for topology constraints in multi-robot allocation problems,” in Robotics and Automation (ICRA), 2017 IEEE International Conference on. IEEE, 2017, pp. 293–300.

- [17] A. D. Wood and J. A. Stankovic, “Denial of service in sensor networks,” computer, vol. 35, no. 10, pp. 54–62, 2002.

- [18] P. Dames, P. Tokekar, and V. Kumar, “Detecting, localizing, and tracking an unknown number of moving targets using a team of mobile robots,” The International Journal of Robotics Research, vol. 36, no. 13-14, pp. 1540–1553, 2017.

- [19] D. Kempe, J. Kleinberg, and É. Tardos, “Maximizing the spread of influence through a social network,” in Proceedings of the ninth ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 2003, pp. 137–146.

- [20] A. Prorok, “Redundant robot assignment on graphs with uncertain edge costs,” in Distributed autonomous robotic systems. Springer, 2019, pp. 313–327.

- [21] G. C. Pflug, “Some remarks on the value-at-risk and the conditional value-at-risk,” in Probabilistic constrained optimization. Springer, 2000, pp. 272–281.

- [22] R. T. Rockafellar and S. Uryasev, “Optimization of conditional value-at-risk,” Journal of risk, vol. 2, pp. 21–42, 2000.

- [23] ——, “Conditional value-at-risk for general loss distributions,” Journal of banking & finance, vol. 26, no. 7, pp. 1443–1471, 2002.

- [24] J. Morgan et al., Riskmetrics technical document. New York RiskMetrics, 1996.

- [25] F. Yang and N. Chakraborty, “Algorithm for optimal chance constrained linear assignment,” in Robotics and Automation (ICRA), 2017 IEEE International Conference on. IEEE, 2017, pp. 801–808.

- [26] ——, “Algorithm for optimal chance constrained knapsack problem with applications to multi-robot teaming,” in 2018 IEEE International Conference on Robotics and Automation (ICRA). IEEE, 2018, pp. 1043–1049.

- [27] H. Markowitz, “Portfolio selection,” The journal of finance, vol. 7, no. 1, pp. 77–91, 1952.

- [28] A. Majumdar and M. Pavone, “How should a robot assess risk? towards an axiomatic theory of risk in robotics,” in Robotics Research. Springer, 2020, pp. 75–84.

- [29] T. Maehara, “Risk averse submodular utility maximization,” Operations Research Letters, vol. 43, no. 5, pp. 526–529, 2015.

- [30] N. Ohsaka and Y. Yoshida, “Portfolio optimization for influence spread,” in Proceedings of the 26th International Conference on World Wide Web. International World Wide Web Conferences Steering Committee, 2017, pp. 977–985.

- [31] B. Wilder, “Risk-sensitive submodular optimization,” in Proceedings of the 32nd AAAI Conference on Artificial Intelligence, 2018.

- [32] L. Zhou and P. Tokekar, “An approximation algorithm for risk-averse submodular optimization,” in International Workshop on the Algorithmic Foundations of Robotics. Springer, 2018, pp. 144–159.

- [33] A. Schrijver, Combinatorial optimization: polyhedra and efficiency. Springer Science & Business Media, 2003, vol. 24.

- [34] M. Conforti and G. Cornuéjols, “Submodular set functions, matroids and the greedy algorithm: tight worst-case bounds and some generalizations of the rado-edmonds theorem,” Discrete applied mathematics, vol. 7, no. 3, pp. 251–274, 1984.

- [35] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath, “Coherent measures of risk,” Mathematical finance, vol. 9, no. 3, pp. 203–228, 1999.

- [36] E. Ackerman and E. Strickland, “Medical delivery drones take flight in east africa,” IEEE Spectrum, vol. 55, no. 1, pp. 34–35, 2018.

- [37] GeeksforGeeks, “Count number of ways to partition a set into k subsets,” https://www.geeksforgeeks.org/count-number-of-ways-to-partition-a-set-into-k-subsets/, September 2020, (Accessed on 12/02/2020).

- [38] K. J. Obermeyer and Contributors, “VisiLibity: A c++ library for visibility computations in planar polygonal environments,” http://www.VisiLibity.org, 2008, r-1.

- [39] G. Boeing, “Osmnx: New methods for acquiring, constructing, analyzing, and visualizing complex street networks,” Computers, Environment and Urban Systems, vol. 65, pp. 126–139, 2017.

- [40] S. Jorgensen, R. H. Chen, M. B. Milam, and M. Pavone, “The team surviving orienteers problem: routing teams of robots in uncertain environments with survival constraints,” Autonomous Robots, vol. 42, no. 4, pp. 927–952, 2018.

- [41] A. Prorok, “Robust assignment using redundant robots on transport networks with uncertain travel time,” IEEE Transactions on Automation Science and Engineering, vol. 17, no. 4, pp. 2025–2037, 2020.

- [42] M. Malencia, V. Kumar, G. Pappas, and A. Prorok, “Fair robust assignment using redundancy,” IEEE Robotics and Automation Letters, vol. 6, no. 2, pp. 4217–4224, 2021.