One model is not enough: heterogeneity in cryptocurrencies’ multifractal profiles

Abstract

This letter studies of the multifractal dynamics in 84 cryptocurrencies. It fills an important gap in the literature, by studying this market using two alternative multi-scaling methodologies. We find compelling evidence that cryptocurrencies have different degree of long range dependence, and –more importantly – follow different stochastic processes. Some of them follow models closer to monofractal fractional Gaussian noises, while others exhibit complex multifractal dynamics. Regarding the source of multifractality, our results are mixed. Time series shuffling produces a reduction in the level of multifractality, but not enough to offset it. We find an association of kurtosis with multifractality.

Keywords: cryptocurrencies; generalized Hurst exponent; multifractality; Efficient Market Hypothesis

JEL codes: C4; G01; G14

1 Introduction

Contemporary to the outbreak of the 2008 financial crisis, an anonymously posted paper attributed to Nakamoto, (2009), set the grounds for a new type of financial asset. This new synthetic product, aimed at bypassing the traditional banking system, became known as cryptocurrency. In spite of the fact that its properties as “currency” has been cast in doubt by Yermack, (2013), Dwyer, (2015), Selgin, (2015), and Schilling and Uhlig, (2019), it is undoubtedly a financial asset of great interest among investors. Shortly after its launching, Bitcoin became tantamount of cryptocurrency. This success led many entrepreneurs to develop their own crytpocurrencies. Elbahrawy et al., (2017) trace the evolutionary dynamics of this market, finding that until the beginning of 2017 the average birth rate of new cryptocurrencies was slightly larger than the average death rates, with an average net increment in the number of coins in the long run. As of March 2020, there are more than 5000 cryptocurrencies, which are traded on 20877 platforms, adding up a market capitalization of 142 USD billions (Coinmarket,, 0120). These figures highlight the economic relevance of this phenomenon.

Cryptocurrencies studies emerge as new and frutiful empirical area, where researchers look for insights of this novel product. Recent surveys (Yli-Huumo et al.,, 2016; Corbet et al.,, 2019; Merediz-Solà and Bariviera,, 2019) show aspects that has been covered until now: statistical properties of daily returns (Urquhart,, 2016; Bariviera et al.,, 2017); safe haven characteristics of Bitcoin (Bouri et al.,, 2017; Smales,, 2019); correlation of main cryptocurrencies with traditional assets (Corbet et al.,, 2018; Aslanidis et al.,, 2019); and portfolio optimization (Platanakis and Urquhart,, 2019).

Nevertheless, there are several gaps in the literature. Firstly, most empirical studies focus their attention on Bitcoin, or at most on the five biggest cryptocurrencies (Bitcoin, Ethereum, Bitcoin Cash, Ripple, Litecoin). Secondly, the scale dimension remains unstudied.

Hence, an alternative approach is necessary. This letter expands and complements previous literature on cryptocurrencies in three aspects: (i) it uses a multi-scaling approach that represents a new approach to this market; (ii) it works with a comprehensive set of cryptocurrencies, which reflects more accurately the behavior of the market; and (iii) it presents a criterion for selecting more appropriate stochastic models of cryptocurrencies dynamics.

2 Methods

2.1 Long range memory

The Efficient Market Hypothesis (EMH) represents the cornerstone of financial economics, upon which many areas (e.g. portfolio optimization, option pricing) are built. It is based on the idea price movements in a competitive market constitute a fair game. The pioneering work by Bachelier, (1900) proposes the the arithmetic Brownian motion as a suitable model to represent the price dynamics of French bonds. Several decades later, Samuelson, (1965) rediscovers Bachelier’s model, proposing a geometric Brownian motion model111The geometric Brownian motion had been independently proposed by Osborne, (1959, 1962) and sets the grounds for the EMH. The definition and classification of the EMH is owed to Fama, (1970). Briefly, the EMH requires that returns of financial assets follow a Markov process with respect to the respective underlying information set.

Contrary to this ideal model, several papers find long memory in traditional financial assets, using different methods (Barkoulas et al.,, 2000; Carbone et al.,, 2004; McCarthy et al.,, 2009; Cajueiro et al.,, 2009). An important research line in statistics and econometrics is directed at detecting long memory in financial time series. Different alternatives have been formulated (e.g.: fractional Brownian motion, fractional Lèvy flights) to account for long memory. However, they are all defined within a monofractal framework. Even Autoregressive Fractionally Integrated Moving Average (ARFIMA) processes, proposed by Granger and Joyeux, (1980) as a generalization of Box and Jenkins, (1994) models, assume a monofractal stationary process.

Regarding cryptocurrencies, there are also several studies on long range dependence. Bariviera, (2017) shows a declining trend in long range dependence in Bitcoin returns, but a persistent long range memory in daily volatility. Tiwari et al., (2018) observe that the Bitcoin market has a trend towards the informational efficiency, albeit it exhibits long range dependence during April-August, 2013 and August-November, 2016. Such results are aligned with those previously found by Urquhart, (2016). More recently, Phillip et al., (2019) show that faster transacted currencies show stronger oscillating long run autocorrelations. Kristoufek and Vosvrda, (2019) examine and produce an efficiency ranking of fourteen coins and tokens according to the well-established Efficiency Index developed by Kristoufek and Vosvrda, (2013). For the sake of brevity, we refer to Corbet et al., (2019) and Merediz-Solà and Bariviera, (2019) for further details on the empirical financial literature on cryptocurrencies.

In a recent contribution, Kukacka and Kristoufek, (2020) link the concepts of multifractality and complexity, and replicate the statistical dynamic properties of the time series by means of several agent-based models. In a broad sense, we can say that multifractality is a statistical feature of time series realated to its non-trivial scaling properties. For a comprehensive discussion on multifractality in financial markets see the recent review by Jiang et al., (2019)

2.2 Generalized Hurst exponent

Harold Edwin Hurst, a British engineer, developed in a series of papers (Hurst,, 1951; Hurst, 1956a, ; Hurst, 1956b, ; Hurst,, 1957) an empirical method to measure the long range dependence of river discharges. His method marked a landmark in hydrology studies, and was found to have applications in other scientific domains. The original method, R/S, was based on the rescaled range of the partial sums of deviations of a time series from its mean.

Mandelbrot and Van Ness, (1968) postulate a generalization Brownian motion and Gaussian noise models, allowing for long range dependence, linked to the system’s Hurst exponent. Mandelbrot and Wallis, (1968) find that these fractional models behave remarkably good in hydrology, and Mandelbrot, (1972) proposes its use in economics.

Depending on the type of signal under analysis, and the goal of the research, we can select among a wide range of methods to compute the Hurst exponent. An exhaustive discussion on this topic is in Serinaldi, (2010).

The Hurst exponent does not only measure long range dependence, but it is also closely related to the fractal dimension of a time series, as shown by Sánchez-Granero et al., (2012). In economics, it is common to assume that the process under study is a fractional Brownian motion (fBm) or a fractional Gaussian noise (fGn). They are monofractal processes, meaning that the Hurst exponent scales linearly. However, real world phenomena can exhibit more complex dynamics. For example, Tuberquia-David et al., (2016) show that network traffic pattern present multifractal characteristics, meaning that the Hurst exponent scales nonlinearly.

In this paper we use two approaches to detect multifractality. The first one is the generalized Hurst exponent (GHE) developed in Di Matteo et al., (2003), and the second one is a multifractal version of the detrended fluctuation analysis presented in Kantelhardt et al., (2002). It was recently recognized (Lux and Segnon,, 2018; Buonocore et al.,, 2020) that multifractality could be considered an stylized fact of financial time series complementing those originally proposed by Cont, (2001).

2.3 The GHE estimator

In contrast to other methods, this first method is specially suitable for describing the multi-scaling properties in financial time series. Di Matteo et al., (2003, 2005) show that it provides robust and unbiased estimators on long term memory.

Without loss of generality, let consider a financial time series (with ). We are interested in analyzing the order moments of the distributions of increments, according to the time resolution (). Di Matteo, (2007) reveals that th-order moments are much less sensitive to outliers, and are associated with different features of the multi-scaling complexity of the time series. It is defined as

| (1) |

where is the expectation operator. The generalized Hurst exponent results from the scaling behavior of from the following relation:

| (2) |

This approach enables to signalize two situations: (a) uniscaling or unifractal processes where is constant; and (b) multi-scaling or multifractal processes where depends on .

This procedure raised some concerns by Kukacka and Kristoufek, (2020), who argue that sometimes GHE yields inconsistent results.

2.4 Multifractal Detrended Fluctuation Analysis

To counterbalance the possible drawbacks of the GHE estimator, we also utilize an alternative approach to the degree of multifractality. We employ the Multifractal Detrended Fluctuation Analysis (MF-DFA). This method, developed by Kantelhardt et al., (2002) is generalization of the celebrated Detrended Fluctuation Analysis by Peng et al., (1994). This is method is divided into five steps. The first step determines the profile function:

| (3) |

The second step partitions into nonoverlapping segments of length . Then the third step computes the local trend for each segment using least square fitting, using linear, cuadratic or higher order polynomials. The fourth step computes the average over all segments, in order to obtain the th order fluctuation function:

| (4) |

Finally, the fifth step determine the scaling behavior drawing using the log-log plane

| (5) |

Kukacka and Kristoufek, (2020) proposes the use of the range of the generalized Hurst exponents () and the width of the multifractal spectrum () to measure the degree of multifractality in a time series.

2.5 The source of multifractality

It is not only important to detect the presence of multifractality in time series, but also to determine its source. According to Kantelhardt et al., (2002) two types of multifractality can be distinguished. The first type is related to the probability density function, and the second one is related to the varying long-range correlation structure in the time series.

In order to detect which kind of multifractality presents a time series, some tests on surrogated time series should be done. An straightforward strategy is to shuffle the original time series. This randomization will destroy non trivial correlations present in the original time series. Consequently, this procedure will allow to determine if the source of multifractality is the correlation structure. However, if the time series present multifractality due to the probability distribution, the measures of multifractality will not (significantly) change. Additionally, as highlihted by Kantelhardt et al., (2002) if both types of multifractality affect the time series, multifractality metrics will show a reduction in the shuffled series. A detailed discussion on the sources of multifractality in financial assets could be found in Barunik et al., (2012).

3 Data

Cryptocurrencies’ markets are not regulated by national authorities and market data lacks of proper independent standardization and verification. Consequently, a careful selection of the data sources is a key element in order to obtain reliable results.

Following Alexander and Dakos, (2020), we obtain our data from CryptoCompare, (0120), because other coin-ranking sites base their quotes on unreliable volume data.

We use daily price data of the eighty-four largest cryptocurrencies (coins and tokens), according to traded volume. The period under examination goes from 06/01/2018 to 05/03/2020, for a total of 790 observations. The selection criteria was based on the average daily volume traded over the period, and the availability of data for every day within the period under study.

A table with the list and descriptive statistics of daily logarithmic returns is included as a supplementary material to this letter.

4 Results

Most studies have been focusing on Bitcoin or, at most on a few cryptocurrencies. This fact generates an overrepresentation of the big players in the literature. The analysis of eighty-four cryptocurrencies allows depicting a more comprehensive landscape of this novel and rapidly evolving market.

Our empirical investigation is divided into two parts. The first one, computes the generalized Hurst exponent for and refines results by using a multi-scaling procedure with the computation of the curves of as a function of , following the procedure developed by Di Matteo and coworkers. The second one provides more robust results by computing the generalized Hurst exponent and the multifractal spectrum of the different cryptocurrencies using the MF-DFA framework.

The descriptive statistics of the logarithm of the average daily volume of the period, and the estimated Hurst exponents are displayed in Table 1.

| Gen. Hurst exponent | |||

| Log vol. | |||

| Obs. | 84 | 84 | 84 |

| Mean | 5.5210 | 0.5150 | 0.4471 |

| Median | 6.2597 | 0.5211 | 0.4812 |

| Min | 0.3564 | 0.2513 | |

| Max | 8.7063 | 0.7333 | 0.5692 |

| Std. Dev. | 1.8227 | 0.0622 | 0.0780 |

| Skewness | 0.0305 | ||

| Kurtosis | 3.3324 | 4.8306 | 2.5925 |

| Jarque-Bera | 12.0904 | 11.7414 | 11.8818 |

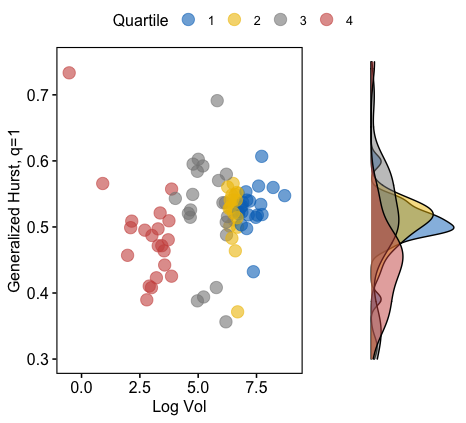

Results regarding the estimated Hurst exponents for uncover an uneven behavior of cryptocurrencies. describes the scaling behavior of the absolute values of the increments of a time series. We find that for most of the largest cryptocurrencies according to traded volume. Hence, behavior is congruent with a standard Brownian motion or with a somewhat persistent stochastic process. This is in line with previous findings (referred only to Bitcoin) by Urquhart, (2016), Bariviera, (2017), Phillip et al., (2019), and Aslan and Sensoy, (2019), among others.

From Figure 1 it can be seen that cryptocurrencies within the third and fourth volume quartiles behave differently. Their Hurst exponents spans between and . Coins in the third quartile tend to follow a persistent behavior (), whereas those in the fourth quartile are more likely to present an anti-persistent behavior (). In both cases, the time series are generally informational inefficient. A density plot is inserted on the right vertical axis of Figure 1 in order to show the distribution of the generalized Hurst exponent in the different quartiles.

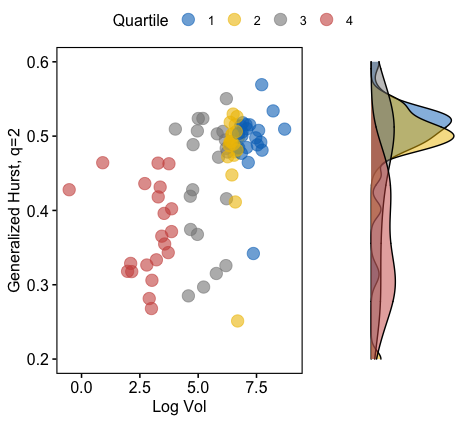

The Hurst exponents for is connected to the autocorrelation function and connected to the power spectrum (Flandrin,, 1989; Di Matteo et al.,, 2005). We observe, again, a noticeable behavior depending on cryptocurrency size. Cryptocurrencies in the first and second volume quantiles are roughly efficients, whereas the third and fourth quartiles exhibits an clear antipersistent behavior (see Figure 2).

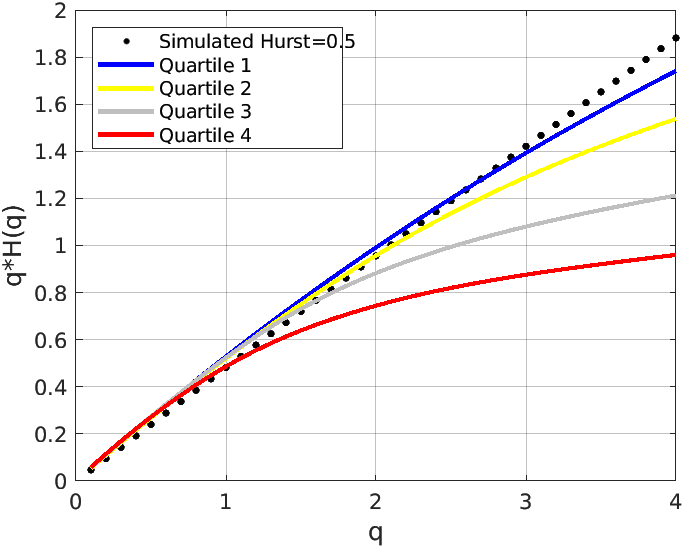

As mentioned in Section 1, we generalize the analysis of the Hurst exponent for different values of . Figure 3 displays the planar representation of . The results of the different coins are grouped into quartiles according to volume. As a benchmark model, we include also the results arising from a simulated time series of the same length and 222Simulation was performed using Matlab function wfbm. If the stochastic process under consideration is monofractal (i.e. the simulated time series), as a function of is a straight line, and its slope depends on the . However, the presence of nonlinearities in this function is a signature of multifractal processes. Thus, we provide compelling evidence against (fractional) Brownian, (fractional) Lèvy, and other additive, monofractal processes.

This analysis reinforces what was shown previously regarding the heterogeneous behavior of cryptocurrencies according to their volume size. Figure 3 clearly reveals that coins in the first quartile follow roughly unifractal processes, being a fractional brownian motion a suitable model for describing their behavior. On contrary, cryptoassets within the other cuartiles (specially those in the third and fourth) exhibit strong multifractality. In such cases, Brownian or Lèvy models (included their fractional varieties), are deemed inadequate for capturing their complex dynamics.

4.1 Source of multifractality: MF-DFA on original and shuffled time series

In the previous subsection we detected multifractality in all the time series. Its presence is particularly relevant in coins and tokens belonging to the third and fourth quartiles.

In order check for the robustness of our results, and following the advise of Kukacka and Kristoufek, (2020), we compute two multifractality measures () using MF-DFA method by Kantelhardt et al., (2002). We also conduct our empirical analysis on 1000 independent shuffled realizations of each time series, and construct the 95% confidence interval of the multifractal measures.

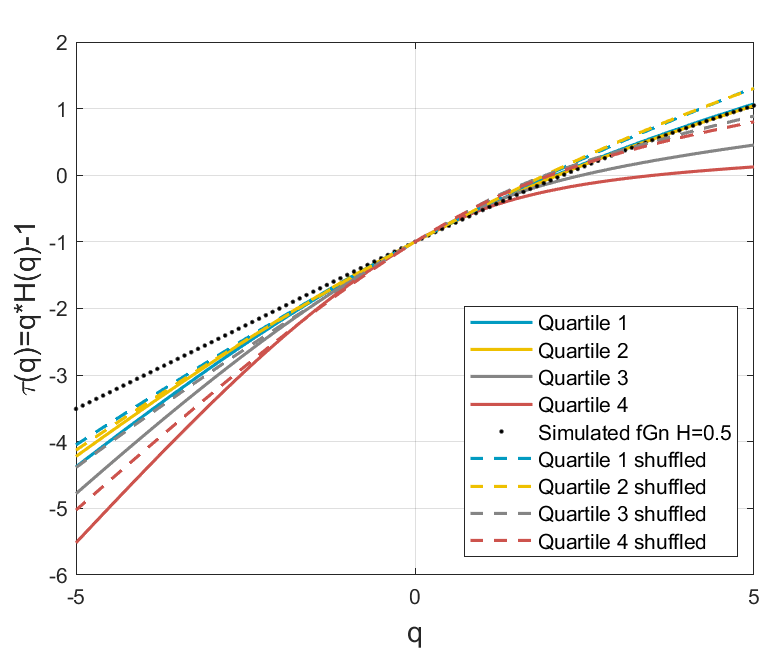

Figure 4 shows similar results to Figure 3, indicating that multifractality (albeit at different degrees) is present in all time series.

Table 2 presents the results of the two selected multifractality measures () using the original and shuffled realizations of the time series. Results are presented by quartiles. We observe that, even multifractality is reduced by the shuffling procedure, it does not vanish. This result indicates that the source of multifractality is (not only) a different long range correlation structure for small and large fluctuations.

We conduct also a detailed analysis of each coin and token of our sample, whose results can be found in the supplementary material to this paper. According to our results, is outside this confidence interval in 29 out of the 84 cryptocurrencies, representing 34% of our sample. This means that in almost two-thirds of the time series multifractality is due to the correlation structure, which is destroyed by the shuffling process. Rejection rates varies according cryptocurrency size. In the first and third quartiles 28% of the coins exhibit multifractality. In the second quartile, 24% show results compatible with multifractal dynamics. However, in the fourth quartile, multifractality affects 57% of the time series, meaning that an additional source of multifractality could be present. Similar results are found using as multifractality measure.

| MF-DFA | Multifractal spectrum | |||

|---|---|---|---|---|

| Original | Shuffled | Original | Shuffled | |

| Quartile 1 | 0.2658 | 0.2016 | 0.4640 | 0.3631 |

| Quartile 2 | 0.2628 | 0.2215 | 0.4145 | 0.3999 |

| Quartile 3 | 0.4636 | 0.3368 | 0.7344 | 0.5576 |

| Quartile 4 | 0.6825 | 0.4708 | 1.0162 | 0.7374 |

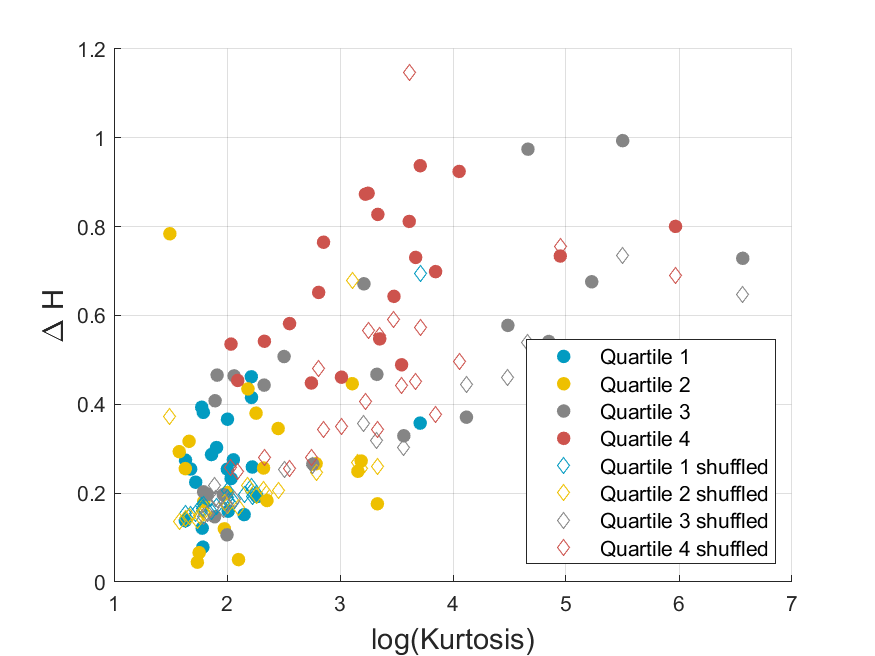

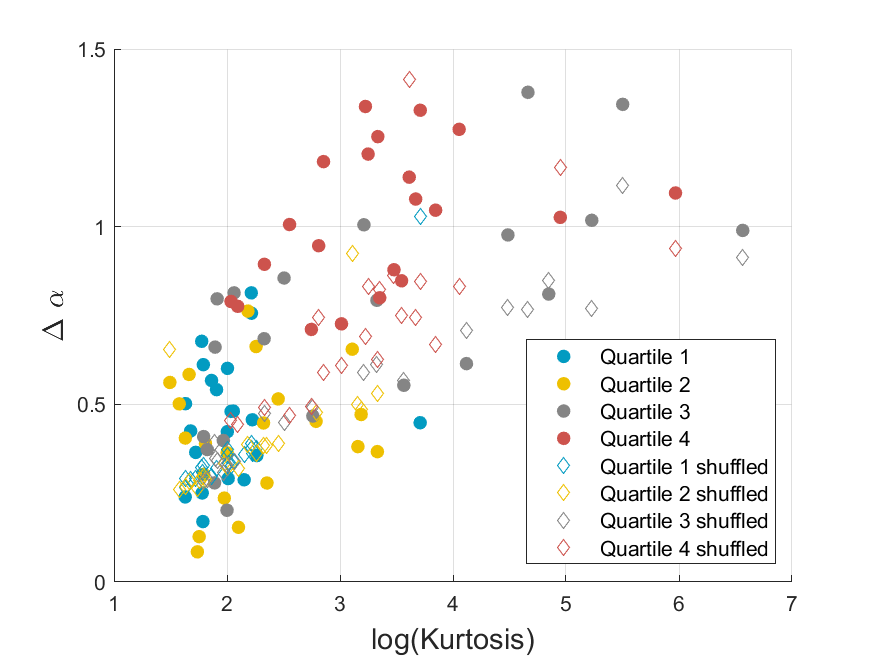

Subsequently, we explore the role of kurtosis in the multifractal profile of the time series. Kurtosis is a common descriptive statistic to signal the peakedness of the probability density function and the presence of fat tails. It was previously reported (Corbet et al.,, 2019; Aslanidis et al.,, 2019) that cryptocurrencies exhibit stronger fluctuations than traditional assets. This could be specially true for the smallest and most illiquid assets, which are prone to sudden jumps.

Figure 5 and 6 show an association between the measures of multifractality () and the estimated kurtosis of the time series. This association is (to a great extent) destroyed by the shuffling procedure in coins and tokens belonging to the first and second quartiles. Thus, kurtosis seems not to influence significantly in the level of multifractality of these coins. This result is consistent with our previous finding that only 28% (23%) of the cryptocurrencies in the first (second) quartile lie in the critical region of multifractality. However, extreme events (proxied by greater kurtosis) in the third and fourth quartiles seem to translate into stronger multifractality. As a caveat, we are not saying that these time series are less informational efficient, but that smaller coins and tokens present more frequent and larger jumps, which in turn induces more multifractality.

5 Conclusions

This letter sheds light on the multifractal behavior of the cryptocurrency market in a broad way.

We expand previous research computing the generalized Hurst exponent and the multifractal spectrum of eighty-four cryptocurrencies time series using two alternative methods.

According to our results, cryptocurrencies have a different long memory endowment, according to their size, proxied by traded volume. More importantly, we detected the presence of multiflactality in several time series. Largest cryptocurrencies (those in the first quartile of volume) seem to follow monofractal processes, consistent with a fractional Brownian motion. On contrary, other cryptocurrencies exhibit strong multifractality. This result poses some restrictions on the suitable stochastic models for such coins and tokens.

Regarding the source of multifractality, our results are mixed. According to our results, shuffling the time series produces a reduction in the level of multifractality, but does not offset all of it. This result is in agreement, regarding bitcoin, with Kukacka and Kristoufek, (2020). Consequently, there is another source of multifractality. We find an association of kurtosis with greater levels of multifractality. This association is stronger for the smallest coins and tokens of our sample.

Consequently, our results support the idea that cryptocurrencies differ not only among them in their long range dependence, but also in the stochastic processes that govern their dynamical behavior.

Our findings can be of interest for academics and practitioners alike. From the academic point of view, means that one model does not fit all. It is necessary to study on a case-by-case basis, in order to select the most appropriate model to describe return dynamics. From the practitioners point of view, means that there could be some arbitrage opportunities, depending on each cryptocurrency.

References

- Alexander and Dakos, (2020) Alexander, C. and Dakos, M. (2020). A critical investigation of cryptocurrency data and analysis. Quantitative Finance, 20(2):173–188.

- Aslan and Sensoy, (2019) Aslan, A. and Sensoy, A. (2019). Intraday efficiency-frequency nexus in the cryptocurrency markets. Finance Research Letters.

- Aslanidis et al., (2019) Aslanidis, N., Bariviera, A. F., and Martinez-Ibañez, O. (2019). An analysis of cryptocurrencies conditional cross correlations. Finance Research Letters, 31:130–137.

- Bachelier, (1900) Bachelier, L. (1900). Théorie de la spéculation. Annales scientifiques de l’École Normale Supérieure, Paris.

- Bariviera, (2017) Bariviera, A. F. (2017). The inefficiency of Bitcoin revisited: A dynamic approach. Economics Letters, 161:1–4.

- Bariviera et al., (2017) Bariviera, A. F., Basgall, M. J., Hasperué, W., and Naiouf, M. (2017). Some stylized facts of the Bitcoin market. Physica A: Statistical Mechanics and its Applications, 484:82–90.

- Barkoulas et al., (2000) Barkoulas, J. T., Baum, C. F., and Travlos, N. (2000). Long memory in the greek stock market. Applied Financial Economics, 10(2):177–184.

- Barunik et al., (2012) Barunik, J., Aste, T., Di Matteo, T., and Liu, R. (2012). Understanding the source of multifractality in financial markets. Physica A: Statistical Mechanics and its Applications, 391(17):4234–4251.

- Bouri et al., (2017) Bouri, E., Molnár, P., Azzi, G., Roubaud, D., and Hagfors, L. I. (2017). On the hedge and safe haven properties of bitcoin: Is it really more than a diversifier? Finance Research Letters, 20:192 – 198.

- Box and Jenkins, (1994) Box, G. E. P. and Jenkins, G. M. (1994). Time series analysis: forecasting and control. Holden-Day, San Francisco:.

- Buonocore et al., (2020) Buonocore, R. J., Brandi, G., Mantegna, R. N., and Di Matteo, T. (2020). On the interplay between multiscaling and stock dependence. Quantitative Finance, 20(1):133–145.

- Cajueiro et al., (2009) Cajueiro, D. O., Gogas, P., and Tabak, B. M. (2009). Does financial market liberalization increase the degree of market efficiency? The case of the Athens stock exchange. International Review of Financial Analysis, 18(1-2):50–57.

- Carbone et al., (2004) Carbone, A., Castelli, G., and Stanley, H. E. (2004). Time-dependent hurst exponent in financial time series. Physica A: Statistical Mechanics and its Applications, 344(1-2):267–271.

- Coinmarket, (0120) Coinmarket (20120). Crypto-Currency Market Capitalizations. https://coinmarketcap.com/currencies/. Accessed: 2020-03-16.

- Cont, (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223–236.

- Corbet et al., (2019) Corbet, S., Lucey, B., Urquhart, A., and Yarovaya, L. (2019). Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis, 62(June 2018):182–199.

- Corbet et al., (2018) Corbet, S., Meegan, A., Larkin, C., Lucey, B., and Yarovaya, L. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165:28 – 34.

- CryptoCompare, (0120) CryptoCompare (20120). Coins list. https://www.cryptocompare.com/coins/list/USD/1. Accessed: 2020-03-05.

- Di Matteo, (2007) Di Matteo, T. (2007). Multi-scaling in finance. Quantitative Finance, 7(1):21–36.

- Di Matteo et al., (2003) Di Matteo, T., Aste, T., and Dacorogna, M. M. (2003). Scaling behaviors in differently developed markets. Physica A: Statistical Mechanics and its Applications, 324(1-2):183–188.

- Di Matteo et al., (2005) Di Matteo, T., Aste, T., and Dacorogna, M. M. (2005). Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. Journal of Banking and Finance, 29(4):827–851.

- Dwyer, (2015) Dwyer, G. P. (2015). The economics of bitcoin and similar private digital currencies. Journal of Financial Stability, 17:81 – 91. Special Issue: Instead of the Fed: Past and Present Alternatives to the Federal Reserve System.

- Elbahrawy et al., (2017) Elbahrawy, A., Alessandretti, L., Kandler, A., Pastor-Satorras, R., and Baronchelli, A. (2017). Evolutionary dynamics of the cryptocurrency market. Royal Society Open Science, 4(11).

- Fama, (1970) Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2, Papers and Proceedings of the Twenty-Eighth Annual Meeting of the American Finance Association New York, N.Y. December, 28-30, 1969):pp. 383–417.

- Flandrin, (1989) Flandrin, P. (1989). On the spectrum of fractional brownian motions. IEEE Transactions on Information Theory, 35(1):197–199.

- Granger and Joyeux, (1980) Granger, C. W. J. and Joyeux, R. (1980). An introduction to long-memory time series and fractional differencing. Journal of Time Series Analysis, 1(1):15–29.

- Hurst, (1951) Hurst, H. E. (1951). Long-term storage capacity of reservoirs. Transactions of the American Society of Civil Engineers, 116:770–808.

- (28) Hurst, H. E. (1956a). Methods of using long-term storage in reservoirs. Proceedings of the Institute of Civil Engineers, 5(5):519–543.

- (29) Hurst, H. E. (1956b). The problem of long-term storage reservoirs. Hydrological Sciences Journal, 1(3):13–27.

- Hurst, (1957) Hurst, H. E. (1957). A suggested statistical model of some time series which occur in nature. Nature, 180(4584):494.

- Ihlen, (2012) Ihlen, E. A. F. (2012). Introduction to Multifractal Detrended Fluctuation Analysis in Matlab. Frontiers in Physiology, 3(June):1–18.

- Ihlen, (2020) Ihlen, E. A. F. (2020). Multifractal detrended fluctuation analyses. https://www.mathworks.com/matlabcentral/fileexchange/38262-multifractal-detrended-fluctuation-analyses. Retrieved May 17, 2020.

- Jiang et al., (2019) Jiang, Z. Q., Xie, W. J., Zhou, W. X., and Sornette, D. (2019). Multifractal analysis of financial markets: A review. Reports on Progress in Physics, 82(12):125901.

- Kantelhardt et al., (2002) Kantelhardt, J. W., Zschiegner, S. A., Koscielny-Bunde, E., Havlin, S., Bunde, A., and Stanley, H. (2002). Multifractal detrended fluctuation analysis of nonstationary time series. Physica A: Statistical Mechanics and its Applications, 316(1):87–114.

- Kristoufek and Vosvrda, (2013) Kristoufek, L. and Vosvrda, M. (2013). Measuring capital market efficiency: Global and local correlations structure. Physica A: Statistical Mechanics and its Applications, 392(1):184–193.

- Kristoufek and Vosvrda, (2019) Kristoufek, L. and Vosvrda, M. (2019). Cryptocurrencies market efficiency ranking: Not so straightforward. Physica A: Statistical Mechanics and its Applications, 531:120853.

- Kukacka and Kristoufek, (2020) Kukacka, J. and Kristoufek, L. (2020). Do ‘complex’ financial models really lead to complex dynamics? Agent-based models and multifractality. Journal of Economic Dynamics and Control, 113:103855.

- Lux and Segnon, (2018) Lux, T. and Segnon, M. (2018). Multifractal models in financetheir origin, properties, and applications. In Chen, S.-H., Kaboudan, M., and Du, Y.-R., editors, The Oxford Handbook of Computational Economics and Finance. Oxford University Press.

- Mandelbrot, (1972) Mandelbrot, B. B. (1972). Statistical methodology for nonperiodic cycles: From the covariance to rs analysis. In Annals of Economic and Social Measurement, Volume 1, number 3, NBER Chapters, pages 259–290. National Bureau of Economic Research.

- Mandelbrot and Van Ness, (1968) Mandelbrot, B. B. and Van Ness, J. W. (1968). Fractional Brownian Motions, Fractional Noises and Applications. SIAM Review, 10(4):422–437.

- Mandelbrot and Wallis, (1968) Mandelbrot, B. B. and Wallis, J. R. (1968). Noah, joseph, and operational hydrology. Water Resources Research, 4(5):909–918.

- McCarthy et al., (2009) McCarthy, J., Pantalone, C., and Li, H. C. (2009). Investigating long memory in yield spreads. Journal of Fixed Income, 19(1):73–81.

- Merediz-Solà and Bariviera, (2019) Merediz-Solà, I. and Bariviera, A. F. (2019). A bibliometric analysis of bitcoin scientific production. Research in International Business and Finance, 50:294–305.

- Nakamoto, (2009) Nakamoto, S. (2009). Bitcoin: A peer-to-peer electronic cash system. https://bitcoin.org/bitcoin.pdf/. Accessed: 2016-12-27.

- Osborne, (1959) Osborne, M. F. M. (1959). Brownian motion in the stock market. Operations Research, 7(2):145–173.

- Osborne, (1962) Osborne, M. F. M. (1962). Periodic structure in the brownian motion of stock prices. Operations Research, 10(3):345–379.

- Peng et al., (1994) Peng, C.-K., Buldyrev, S. V., Havlin, S., Simons, M., Stanley, H. E., and Goldberger, A. L. (1994). Mosaic organization of dna nucleotides. Physical Review E, 49(2):1685–1689.

- Phillip et al., (2019) Phillip, A., Chan, J., and Peiris, S. (2019). On long memory effects in the volatility measure of cryptocurrencies. Finance Research Letters, 28:95 – 100.

- Platanakis and Urquhart, (2019) Platanakis, E. and Urquhart, A. (2019). Portfolio management with cryptocurrencies: The role of estimation risk. Economics Letters, 177:76–80.

- Samuelson, (1965) Samuelson, P. A. (1965). Proof That Properly Anticipated Prices Fluctuate Randomly. Industrial Management Review, 6(2):41–49.

- Sánchez-Granero et al., (2012) Sánchez-Granero, M. J., Fernández-Martínez, M., and Trinidad-Segovia, J. E. (2012). Introducing fractal dimension algorithms to calculate the Hurst exponent of financial time series. The European Physical Journal B, 85(3):86.

- Schilling and Uhlig, (2019) Schilling, L. and Uhlig, H. (2019). Some simple bitcoin economics. Journal of Monetary Economics, 106:16 – 26.

- Selgin, (2015) Selgin, G. (2015). Synthetic commodity money. Journal of Financial Stability, 17:92 – 99. Special Issue: Instead of the Fed: Past and Present Alternatives to the Federal Reserve System.

- Serinaldi, (2010) Serinaldi, F. (2010). Use and misuse of some hurst parameter estimators applied to stationary and non-stationary financial time series. Physica A: Statistical Mechanics and its Applications, 389(14):2770–2781.

- Smales, (2019) Smales, L. (2019). Bitcoin as a safe haven: Is it even worth considering? Finance Research Letters, 30:385–393.

- Tiwari et al., (2018) Tiwari, A. K., Jana, R., Das, D., and Roubaud, D. (2018). Informational efficiency of bitcoin – an extension. Economics Letters, 163:106 – 109.

- Tuberquia-David et al., (2016) Tuberquia-David, M., Vela-Vargas, F., López-Chávez, H., and Hernández, C. (2016). A multifractal wavelet model for the generation of long-range dependency traffic traces with adjustable parameters. Expert Systems with Applications, 62:373 – 384.

- Urquhart, (2016) Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148:80–82.

- Yermack, (2013) Yermack, D. (2013). Is bitcoin a real currency? an economic appraisal. Working Paper 19747, National Bureau of Economic Research.

- Yli-Huumo et al., (2016) Yli-Huumo, J., Ko, D., Choi, S., Park, S., and Smolander, K. (2016). Where Is Current Research on Blockchain Technology?-A Systematic Review. PloS one, 11(10):e0163477.

Supplementary material

| Crypto | Obs. | Mean | Median | Min | Max | Std. Dev. | Skewness | Kurtosis | Jarque-Bera |

|---|---|---|---|---|---|---|---|---|---|

| ACHN | 789 | -0.6465 | -0.4455 | -31.2524 | 40.3689 | 7.3853 | 0.0643 | 6.7701 | 467.8120 |

| ACOIN | 789 | 0.0222 | -0.0924 | -642.0136 | 786.4650 | 36.6010 | 5.7431 | 391.1575 | 4957488.9982 |

| ADA | 789 | -0.3820 | 0.0000 | -29.1399 | 27.4731 | 5.8657 | -0.1756 | 6.1123 | 322.4990 |

| AION | 789 | -0.5223 | -0.4504 | -32.3820 | 30.2058 | 7.3928 | 0.0451 | 5.1096 | 146.5718 |

| ARG | 789 | 0.1121 | -0.0877 | -100.7488 | 141.5843 | 12.7185 | 1.7287 | 39.2419 | 43573.4217 |

| ARI | 789 | -0.3161 | -0.1309 | -43.0557 | 82.9262 | 9.6098 | 1.4270 | 17.3601 | 7046.9759 |

| ARN | 789 | -0.4634 | -0.3547 | -32.7932 | 53.0574 | 7.7215 | 0.3605 | 8.1794 | 899.0122 |

| BAT | 789 | -0.1312 | -0.0569 | -36.9243 | 28.1515 | 6.4885 | -0.2420 | 5.6834 | 244.4252 |

| BCD | 789 | -0.5210 | -0.5324 | -219.5634 | 225.5275 | 34.7946 | 0.1833 | 22.3872 | 12360.9851 |

| BCH | 789 | -0.2554 | -0.3140 | -30.6758 | 41.9398 | 6.5121 | 0.4938 | 9.1610 | 1279.9402 |

| BET | 789 | -0.2057 | -0.0969 | -151.7714 | 100.6797 | 15.5515 | -0.8957 | 28.5438 | 21555.9288 |

| BNB | 789 | -0.0119 | -0.0153 | -36.4052 | 23.4764 | 5.3866 | -0.4235 | 7.6622 | 738.1623 |

| BOST | 789 | -0.1515 | 0.0245 | -80.7112 | 94.6135 | 9.8526 | 0.9534 | 32.3838 | 28504.0433 |

| BTB | 789 | -0.4194 | -0.5946 | -112.7231 | 82.0514 | 13.8699 | -0.1622 | 12.8555 | 3196.6665 |

| BTC | 789 | -0.0808 | 0.0608 | -18.9167 | 16.7222 | 3.9346 | -0.2803 | 5.9933 | 304.8868 |

| BTCD | 789 | -0.3552 | -0.1088 | -130.8021 | 74.8189 | 8.4887 | -2.8383 | 88.7494 | 242788.1233 |

| BTM | 789 | -0.2498 | -0.1563 | -37.8147 | 69.1948 | 7.1966 | 0.8310 | 16.2541 | 5865.9775 |

| BTMK | 789 | -0.6063 | -0.0613 | -194.7520 | 183.8111 | 15.9052 | -1.3350 | 105.9850 | 348903.4458 |

| CACH | 789 | -0.3160 | -0.0743 | -78.0010 | 75.5404 | 7.8412 | -0.1794 | 28.0759 | 20676.0963 |

| CANN | 789 | -0.4099 | -0.3122 | -152.6686 | 163.8534 | 14.4065 | 1.2916 | 61.5005 | 112727.8183 |

| CAP | 789 | -0.2484 | 0.0626 | -426.2745 | 408.5881 | 52.2362 | 0.3860 | 37.0638 | 38165.8014 |

| CASH | 789 | -0.5327 | 0.0390 | -317.4608 | 127.6671 | 17.6535 | -6.9373 | 141.1032 | 633337.1767 |

| CBX | 789 | -0.5713 | -0.1947 | -173.0365 | 284.3819 | 20.9427 | 2.0769 | 57.6469 | 98741.4534 |

| CCN | 789 | -0.3522 | 0.0318 | -35.7165 | 32.9575 | 6.4058 | -0.4773 | 8.1235 | 892.9247 |

| CLAM | 789 | -0.3202 | -0.0927 | -91.0199 | 49.0385 | 7.7295 | -2.6068 | 35.3349 | 35265.8323 |

| CVC | 789 | -0.4552 | -0.0531 | -35.6778 | 32.2799 | 6.4506 | -0.3332 | 6.2040 | 352.0709 |

| DASH | 789 | -0.3241 | -0.2916 | -22.8908 | 39.8701 | 5.5138 | 0.5476 | 9.5572 | 1452.9624 |

| DGC | 789 | -0.3833 | 0.0000 | -37.6144 | 36.3121 | 8.4641 | -0.3107 | 7.6549 | 725.0299 |

| ELF | 789 | -0.3752 | -0.0621 | -29.6456 | 36.0310 | 7.2397 | 0.0800 | 5.9060 | 278.4677 |

| EMC2 | 789 | -0.3265 | -0.3665 | -51.1030 | 51.1508 | 10.2620 | 0.1591 | 10.2620 | 1737.0282 |

| ENJ | 789 | -0.1772 | -0.2164 | -42.9976 | 77.9986 | 8.2509 | 2.0260 | 23.5325 | 14399.3072 |

| ENRG | 789 | -0.4763 | -0.1491 | -70.7377 | 30.6517 | 6.1280 | -2.0585 | 27.8445 | 20849.3470 |

| EOS | 789 | -0.1214 | -0.0702 | -28.7411 | 35.0657 | 6.5429 | 0.3024 | 7.4113 | 651.7630 |

| ETC | 789 | -0.1801 | -0.0831 | -36.2296 | 30.7827 | 5.7578 | -0.2930 | 7.4205 | 653.7058 |

| ETH | 789 | -0.1878 | -0.1019 | -22.2767 | 17.9934 | 5.0447 | -0.3609 | 5.1191 | 164.7538 |

| GEO | 789 | -0.5341 | -0.3805 | -331.3922 | 339.6577 | 20.8935 | 1.9021 | 186.3900 | 1106124.2826 |

| GNT | 789 | -0.3697 | -0.1605 | -36.3795 | 52.2172 | 6.5724 | 0.2528 | 10.5234 | 1869.1748 |

| GTO | 789 | -0.5140 | -0.4676 | -43.2038 | 84.4657 | 9.1536 | 1.1219 | 15.7960 | 5548.3959 |

| ICX | 789 | -0.3776 | -0.1574 | -60.7342 | 40.8273 | 8.0278 | -0.2359 | 9.6235 | 1449.5530 |

| KCS | 789 | -0.2935 | -0.3150 | -28.3733 | 29.8662 | 6.3389 | 0.0947 | 6.6498 | 439.1097 |

| KNC | 789 | -0.2219 | 0.0000 | -55.2516 | 58.1159 | 11.8545 | -0.0603 | 7.2242 | 587.0904 |

| LIMX | 789 | -0.0764 | 0.0415 | -92.1752 | 109.5124 | 10.1987 | 0.9206 | 40.8651 | 47246.4305 |

| LRC | 789 | -0.4255 | -0.0827 | -30.5002 | 41.9089 | 7.2161 | 0.1971 | 7.1533 | 572.1954 |

| LSK | 789 | -0.3935 | -0.4529 | -27.3164 | 26.3976 | 6.0197 | 0.0797 | 5.9320 | 283.4470 |

| LTC | 789 | -0.1903 | -0.3236 | -23.2089 | 28.7415 | 5.2683 | 0.3302 | 6.4429 | 404.0318 |

| MANA | 789 | -0.1692 | 0.0743 | -61.6632 | 79.6635 | 7.6853 | 0.8800 | 24.2182 | 14902.5535 |

| MBL | 789 | 0.1879 | 0.0000 | -113.0223 | 318.6700 | 15.3015 | 10.9820 | 245.0695 | 1942257.4954 |

| MCO | 789 | -0.1420 | -0.1146 | -35.2500 | 46.1690 | 6.3769 | 0.1502 | 9.2438 | 1284.6039 |

| MIOTA | 789 | -0.3627 | -0.2534 | -30.8061 | 22.5011 | 5.7812 | -0.2587 | 5.3545 | 191.0468 |

| MONA | 789 | -0.1915 | -0.4290 | -39.4149 | 67.6841 | 7.6719 | 2.5334 | 24.8191 | 16494.8923 |

| MOON | 789 | -0.5358 | 0.0000 | -48.9576 | 24.0866 | 6.6536 | -1.5572 | 12.2443 | 3128.2807 |

| NANO | 789 | -0.4632 | -0.4115 | -41.6924 | 34.0628 | 7.4696 | -0.1879 | 7.4662 | 660.4142 |

| NEO | 789 | -0.2676 | -0.1794 | -29.1631 | 25.2006 | 6.1411 | -0.0023 | 5.6009 | 222.3978 |

| OMG | 789 | -0.3848 | -0.2395 | -26.3033 | 23.9605 | 6.0345 | -0.2443 | 5.1070 | 153.8039 |

| POLY | 789 | 0.6466 | -0.0927 | -74.0112 | 860.4205 | 31.4587 | 25.9158 | 709.0048 | 16474626.7901 |

| POWR | 789 | -0.3455 | 0.0000 | -35.9366 | 33.6455 | 6.5772 | 0.1750 | 7.2152 | 588.1475 |

| PRC | 789 | -0.3727 | -0.0394 | -126.7511 | 87.2883 | 11.9586 | -1.6035 | 34.6372 | 33243.0541 |

| QRK | 789 | -0.2496 | 0.0000 | -47.9456 | 62.0739 | 7.5338 | 0.1203 | 15.5921 | 5214.6090 |

| QTL | 789 | -0.2532 | -0.1325 | -30.3338 | 45.2547 | 6.6903 | 0.2904 | 10.2879 | 1757.1806 |

| QTUM | 789 | -0.4422 | -0.2782 | -37.5255 | 39.7683 | 6.4722 | 0.0967 | 7.8155 | 763.5804 |

| REP | 789 | -0.2296 | -0.0900 | -31.6676 | 51.2594 | 6.3314 | 0.8388 | 11.6203 | 2535.4303 |

| RIC | 789 | -0.4812 | 0.0375 | -149.0996 | 35.4242 | 8.5759 | -7.8577 | 127.3983 | 516857.8624 |

| SNT | 789 | -0.4410 | -0.2741 | -28.9278 | 28.1204 | 5.5881 | -0.2170 | 5.7765 | 259.6161 |

| SRN | 789 | -0.6145 | -0.4791 | -58.3293 | 48.7632 | 7.9451 | -0.2207 | 10.2111 | 1715.8862 |

| STEEM | 789 | -0.4478 | -0.4249 | -35.5088 | 37.8818 | 6.4200 | 0.1345 | 7.3960 | 637.6729 |

| STORM | 789 | -0.5849 | -0.6433 | -35.9387 | 99.2795 | 8.5338 | 1.8081 | 27.9611 | 20912.8677 |

| SWFTC | 789 | -0.4765 | -0.3775 | -37.0445 | 47.7890 | 7.8494 | 0.2390 | 8.8924 | 1148.9625 |

| SXC | 789 | -0.6798 | -0.2708 | -85.5243 | 120.6038 | 12.7925 | 0.5567 | 20.3478 | 9934.3193 |

| TRX | 789 | -0.2870 | -0.1965 | -34.7714 | 36.9231 | 6.5874 | -0.0859 | 6.7353 | 459.6622 |

| VET | 789 | -0.2584 | -0.0532 | -309.1562 | 233.9956 | 26.9495 | -1.1687 | 40.8282 | 47222.8119 |

| WAVES | 789 | -0.2865 | -0.2147 | -26.6230 | 38.3516 | 6.0615 | 0.3906 | 8.5999 | 1050.9990 |

| WTC | 789 | -0.4396 | -0.4270 | -29.5165 | 43.5201 | 7.3645 | 0.2089 | 6.1065 | 322.9881 |

| XBS | 789 | -0.2713 | 0.0348 | -89.3732 | 66.6890 | 9.5751 | -0.7232 | 25.7608 | 17099.8341 |

| XEM | 789 | -0.4316 | -0.1763 | -29.8042 | 24.0098 | 5.7501 | -0.0069 | 5.9686 | 289.7271 |

| XLM | 789 | -0.3096 | -0.2718 | -32.9406 | 26.8116 | 5.6059 | -0.0605 | 6.0157 | 299.4597 |

| XMR | 789 | -0.2213 | 0.0153 | -27.6457 | 18.5045 | 5.3125 | -0.3864 | 5.2822 | 190.8571 |

| XMY | 789 | -0.4934 | -0.3226 | -48.9548 | 28.0314 | 7.7976 | -0.4281 | 6.0080 | 321.5598 |

| XPY | 789 | -0.2489 | 0.0656 | -68.3288 | 66.1725 | 10.5757 | -0.2512 | 16.6274 | 6113.4152 |

| XRP | 789 | -0.3047 | -0.2841 | -36.7056 | 31.7479 | 5.3604 | 0.0917 | 9.1769 | 1255.4367 |

| XTZ | 789 | -0.0679 | 0.0000 | -99.9714 | 52.2926 | 7.9993 | -3.7663 | 51.7874 | 80114.7553 |

| XUC | 789 | -0.2481 | -0.2478 | -25.2063 | 29.2463 | 5.1009 | 0.3328 | 7.8677 | 793.5280 |

| YBC | 789 | -0.0960 | 0.0624 | -68.3073 | 35.7470 | 5.2919 | -2.2015 | 46.8009 | 63708.4791 |

| ZEC | 789 | -0.3217 | -0.3374 | -21.1347 | 22.3873 | 5.4391 | 0.0198 | 4.8426 | 111.6624 |

| ZET | 789 | -0.3848 | 0.0121 | -57.4514 | 87.3608 | 9.2349 | 1.0451 | 25.1554 | 16280.7154 |

Appendix A Multifractal measures for each cryptocurency.

| Original Series | Shuffled series | ||||

|---|---|---|---|---|---|

| Crypto | CL_0.025 | CL_0.975 | |||

| ACHN | 0.4658 | 0.1849 | 0.0388 | 0.3642 | * |

| ACOIN | 0.8007 | 0.6895 | 0.4157 | 0.8594 | |

| ADA | 0.1062 | 0.1768 | 0.0378 | 0.3464 | |

| AION | 0.2553 | 0.1425 | 0.0210 | 0.3049 | |

| ARG | 0.7308 | 0.4525 | 0.1765 | 0.6852 | * |

| ARI | 0.7649 | 0.3424 | 0.1076 | 0.5789 | * |

| ARN | 0.0504 | 0.1667 | 0.0300 | 0.3385 | |

| BAT | 0.0446 | 0.1383 | 0.0247 | 0.2924 | |

| BCD | 0.4464 | 0.6785 | 0.3549 | 0.9696 | |

| BCH | 0.4621 | 0.2140 | 0.0465 | 0.3992 | * |

| BET | 0.5473 | 0.5544 | 0.2586 | 0.8160 | |

| BNB | 0.2330 | 0.1736 | 0.0330 | 0.3531 | |

| BOST | 0.6431 | 0.5908 | 0.3168 | 0.8566 | |

| BTB | 0.5818 | 0.2566 | 0.0597 | 0.4622 | * |

| BTC | 0.3819 | 0.1745 | 0.0298 | 0.3541 | * |

| BTCD | 0.5777 | 0.4611 | 0.2045 | 0.7141 | |

| BTM | 0.2664 | 0.2459 | 0.0621 | 0.4397 | |

| BTMK | 0.9745 | 0.5391 | 0.3082 | 0.7784 | * |

| CACH | 0.8276 | 0.3431 | 0.1039 | 0.5606 | * |

| CANN | 0.3710 | 0.4457 | 0.2051 | 0.6757 | |

| CAP | 0.8118 | 1.1464 | 0.6598 | 1.6088 | |

| CASH | 0.7339 | 0.7552 | 0.3911 | 1.1027 | |

| CBX | 0.9244 | 0.4965 | 0.2320 | 0.7701 | * |

| CCN | 0.4538 | 0.2485 | 0.0685 | 0.4449 | * |

| CLAM | 0.3291 | 0.3024 | 0.0930 | 0.5187 | |

| CVC | 0.1970 | 0.1547 | 0.0274 | 0.3122 | |

| DASH | 0.3802 | 0.1949 | 0.0456 | 0.3704 | * |

| DGC | 0.5357 | 0.2575 | 0.0684 | 0.4600 | * |

| ELF | 0.3935 | 0.1716 | 0.0332 | 0.3380 | * |

| EMC2 | 0.4433 | 0.2802 | 0.0783 | 0.4855 | |

| ENJ | 0.2493 | 0.2697 | 0.0707 | 0.4831 | |

| ENRG | 0.4676 | 0.3194 | 0.0896 | 0.5550 | |

| EOS | 0.2540 | 0.2056 | 0.0391 | 0.3936 | |

| ETC | 0.3665 | 0.1908 | 0.0337 | 0.3803 | |

| eth | 0.2742 | 0.1540 | 0.0267 | 0.3256 | |

| GEO | 0.6759 | 0.5253 | 0.3002 | 0.7448 | |

| GNT | 0.1835 | 0.2002 | 0.0368 | 0.3869 | |

| GTO | 0.2653 | 0.2621 | 0.0670 | 0.4683 | |

| ICX | 0.1922 | 0.1997 | 0.0432 | 0.3854 | |

| KCS | 0.4080 | 0.1888 | 0.0355 | 0.3794 | * |

| KNC | 0.1469 | 0.2170 | 0.0462 | 0.4192 | |

| LIMX | 0.9372 | 0.5721 | 0.2860 | 0.8504 | * |

| LRC | 0.1967 | 0.1638 | 0.0275 | 0.3240 | |

| LSK | 0.1213 | 0.1599 | 0.0288 | 0.3236 | |

| LTC | 0.2869 | 0.1580 | 0.0276 | 0.3134 | |

| MANA | 0.2724 | 0.2546 | 0.0692 | 0.4578 | |

| MBL | 0.9937 | 0.7361 | 0.3659 | 1.1271 | |

| MCO | 0.2589 | 0.1918 | 0.0406 | 0.3822 | |

| MIOTA | 0.2544 | 0.1518 | 0.0279 | 0.3141 | |

| MONA | 0.6713 | 0.3557 | 0.1234 | 0.5675 | * |

| MOON | 0.5076 | 0.2525 | 0.0687 | 0.4437 | * |

| NANO | 0.1593 | 0.1813 | 0.0309 | 0.3749 | |

| NEO | 0.2247 | 0.1547 | 0.0253 | 0.3184 | |

| OMG | 0.1380 | 0.1405 | 0.0231 | 0.3044 | |

| POLY | 0.7288 | 0.6480 | 0.2831 | 1.4736 | |

| POWR | 0.1198 | 0.1791 | 0.0378 | 0.3583 | |

| PRC | 0.4891 | 0.4428 | 0.1793 | 0.7326 | |

| QRK | 0.4480 | 0.2797 | 0.0693 | 0.4889 | |

| QTL | 0.5420 | 0.2802 | 0.0758 | 0.4820 | * |

| QTUM | 0.2751 | 0.1811 | 0.0306 | 0.3520 | |

| REP | 0.3456 | 0.2050 | 0.0450 | 0.3998 | |

| RIC | 0.5415 | 0.5244 | 0.2293 | 0.8086 | |

| SNT | 0.0661 | 0.1507 | 0.0264 | 0.3115 | |

| SRN | 0.2566 | 0.2077 | 0.0473 | 0.3930 | |

| STEEM | 0.2016 | 0.1733 | 0.0315 | 0.3529 | |

| STORM | 0.1761 | 0.2611 | 0.0663 | 0.4711 | |

| SWFTC | 0.4346 | 0.2163 | 0.0389 | 0.4068 | * |

| SXC | 0.4611 | 0.3507 | 0.1018 | 0.5700 | |

| TRX | 0.3027 | 0.1699 | 0.0277 | 0.3390 | |

| VET | 0.3577 | 0.6949 | 0.3828 | 0.9865 | * |

| WAVES | 0.1517 | 0.1964 | 0.0355 | 0.3722 | |

| WTC | 0.1938 | 0.1532 | 0.0247 | 0.3034 | |

| XBS | 0.8752 | 0.5660 | 0.2886 | 0.8291 | * |

| XEM | 0.0785 | 0.1648 | 0.0274 | 0.3255 | |

| XLM | 0.1812 | 0.1561 | 0.0245 | 0.3283 | |

| XMR | 0.3167 | 0.1485 | 0.0296 | 0.3149 | * |

| XMY | 0.2030 | 0.1478 | 0.0248 | 0.3003 | |

| XPY | 0.6519 | 0.4796 | 0.2259 | 0.7469 | |

| XRP | 0.4156 | 0.2043 | 0.0424 | 0.3864 | * |

| XTZ | 0.7841 | 0.3719 | 0.1418 | 0.5943 | * |

| XUC | 0.4641 | 0.1861 | 0.0381 | 0.3596 | * |

| YBC | 0.6988 | 0.3765 | 0.1406 | 0.5887 | * |

| ZEC | 0.2934 | 0.1370 | 0.0255 | 0.3045 | |

| ZET | 0.8732 | 0.4054 | 0.1568 | 0.6558 | * |

| Original Series | Shuffled series | ||||

|---|---|---|---|---|---|

| Crypto | CL_0.025 | CL_0.975 | |||

| ACHN | 0.7969 | 0.3418 | 0.0887 | 0.6469 | * |

| ACOIN | 1.0948 | 0.9389 | 0.5907 | 1.1800 | |

| ADA | 0.2020 | 0.3297 | 0.0836 | 0.6304 | |

| AION | 0.4050 | 0.2689 | 0.0514 | 0.5503 | |

| ARG | 1.0777 | 0.7446 | 0.3507 | 1.1190 | |

| ARI | 1.1830 | 0.5892 | 0.2177 | 0.9763 | * |

| ARN | 0.1539 | 0.3182 | 0.0717 | 0.6219 | |

| BAT | 0.0849 | 0.2634 | 0.0587 | 0.5508 | |

| BCD | 0.6551 | 0.9240 | 0.4756 | 1.3677 | |

| BCH | 0.8137 | 0.3886 | 0.1130 | 0.7037 | * |

| BET | 0.7998 | 0.8237 | 0.4123 | 1.2120 | |

| BNB | 0.4802 | 0.3287 | 0.0746 | 0.6405 | |

| BOST | 0.8788 | 0.8638 | 0.4600 | 1.2608 | |

| BTB | 1.0060 | 0.4689 | 0.1436 | 0.8148 | * |

| BTC | 0.6117 | 0.3267 | 0.0747 | 0.6370 | |

| BTCD | 0.9766 | 0.7720 | 0.4001 | 1.1553 | |

| BTM | 0.4522 | 0.4782 | 0.1472 | 0.8102 | |

| BTMK | 1.3781 | 0.7681 | 0.4527 | 1.0919 | * |

| CACH | 1.2534 | 0.6259 | 0.2590 | 0.9828 | * |

| CANN | 0.6145 | 0.7092 | 0.3694 | 1.0539 | |

| CAP | 1.1393 | 1.4133 | 0.8233 | 2.0186 | |

| CASH | 1.0262 | 1.1660 | 0.6644 | 1.6672 | |

| CBX | 1.2739 | 0.8320 | 0.4582 | 1.2537 | * |

| CCN | 0.7758 | 0.4429 | 0.1445 | 0.7788 | |

| CLAM | 0.5537 | 0.5661 | 0.2399 | 0.9093 | |

| CVC | 0.3727 | 0.2894 | 0.0605 | 0.5474 | |

| DASH | 0.6627 | 0.3613 | 0.0979 | 0.6634 | |

| DGC | 0.7895 | 0.4555 | 0.1462 | 0.7890 | * |

| ELF | 0.6774 | 0.3210 | 0.0791 | 0.6197 | * |

| EMC2 | 0.6846 | 0.4744 | 0.1537 | 0.8179 | |

| ENJ | 0.3810 | 0.4993 | 0.1820 | 0.8634 | |

| ENRG | 0.7929 | 0.6132 | 0.2362 | 0.9990 | |

| EOS | 0.4229 | 0.3739 | 0.0929 | 0.6960 | |

| ETC | 0.6013 | 0.3572 | 0.0730 | 0.6905 | |

| ETH | 0.5019 | 0.2921 | 0.0638 | 0.5947 | |

| GEO | 1.0179 | 0.7685 | 0.4879 | 1.0676 | |

| GNT | 0.2786 | 0.3828 | 0.0913 | 0.7199 | |

| GTO | 0.4671 | 0.4907 | 0.1584 | 0.8531 | |

| ICX | 0.3558 | 0.3745 | 0.1008 | 0.6926 | |

| KCS | 0.6611 | 0.3469 | 0.0834 | 0.6633 | |

| KNC | 0.2789 | 0.3925 | 0.0962 | 0.7341 | |

| LIMX | 1.3277 | 0.8452 | 0.4525 | 1.2614 | * |

| LRC | 0.3982 | 0.3080 | 0.0679 | 0.5949 | |

| LSK | 0.2505 | 0.2973 | 0.0617 | 0.5697 | |

| LTC | 0.5672 | 0.2962 | 0.0647 | 0.5797 | |

| MANA | 0.4714 | 0.4863 | 0.1767 | 0.8241 | |

| MBL | 1.3442 | 1.1166 | 0.6022 | 1.6547 | |

| MCO | 0.4566 | 0.3610 | 0.0918 | 0.6705 | |

| MIOTA | 0.4251 | 0.2882 | 0.0623 | 0.5714 | |

| MONA | 1.0053 | 0.5892 | 0.2350 | 0.9335 | * |

| MOON | 0.8555 | 0.4494 | 0.1535 | 0.7891 | * |

| NANO | 0.2912 | 0.3331 | 0.0738 | 0.6733 | |

| NEO | 0.3648 | 0.2908 | 0.0660 | 0.6015 | |

| OMG | 0.2394 | 0.2669 | 0.0532 | 0.5616 | |

| POLY | 0.9894 | 0.9140 | 0.4314 | 1.9224 | |

| POWR | 0.2361 | 0.3325 | 0.0836 | 0.6410 | |

| PRC | 0.8478 | 0.7494 | 0.3607 | 1.1958 | |

| QRK | 0.7108 | 0.4926 | 0.1675 | 0.8468 | |

| QTL | 0.8941 | 0.4897 | 0.1663 | 0.8228 | * |

| QTUM | 0.4810 | 0.3377 | 0.0695 | 0.6345 | |

| REP | 0.5153 | 0.3887 | 0.1088 | 0.7424 | |

| RIC | 0.8104 | 0.8473 | 0.4180 | 1.2594 | |

| SNT | 0.1277 | 0.2849 | 0.0585 | 0.5751 | |

| SRN | 0.4476 | 0.3839 | 0.0950 | 0.7032 | |

| STEEM | 0.3634 | 0.3236 | 0.0693 | 0.6429 | |

| STORM | 0.3669 | 0.5313 | 0.1864 | 0.9052 | |

| SWFTC | 0.7625 | 0.3870 | 0.0985 | 0.7094 | * |

| SXC | 0.7265 | 0.6082 | 0.2143 | 0.9679 | |

| TRX | 0.5413 | 0.3188 | 0.0672 | 0.6215 | |

| VET | 0.4482 | 1.0281 | 0.5941 | 1.4569 | * |

| WAVES | 0.2877 | 0.3586 | 0.0910 | 0.6614 | |

| WTC | 0.3899 | 0.2898 | 0.0631 | 0.5498 | |

| XBS | 1.2043 | 0.8312 | 0.4218 | 1.2404 | |

| XEM | 0.1701 | 0.3095 | 0.0641 | 0.6034 | |

| XLM | 0.3031 | 0.2970 | 0.0615 | 0.5986 | |

| XMR | 0.5842 | 0.2818 | 0.0687 | 0.5818 | * |

| XMY | 0.4092 | 0.2835 | 0.0593 | 0.5654 | |

| XPY | 0.9464 | 0.7448 | 0.3610 | 1.1486 | |

| XRP | 0.7563 | 0.3766 | 0.0892 | 0.6966 | * |

| XTZ | 0.5616 | 0.6531 | 0.3249 | 1.0066 | |

| XUC | 0.8137 | 0.3398 | 0.0849 | 0.6322 | * |

| YBC | 1.0464 | 0.6688 | 0.3183 | 1.0112 | * |

| ZEC | 0.5013 | 0.2614 | 0.0540 | 0.5587 | |

| ZET | 1.3383 | 0.6914 | 0.3178 | 1.0888 | * |