Semi-closed form solutions for barrier and American options written on a time-dependent Ornstein Uhlenbeck process

-

In this paper we develop a semi-closed form solutions for the barrier (perhaps, time-dependent) and American options written on the underlying stock which follows a time-dependent OU process with a lognormal drift. This model is equivalent to the familiar Hull-White model in FI, or a time dependent OU model in FX. Semi-closed form means that given the time-dependent interest rate, continuous dividend and volatility functions, one need to solve numerically a linear (for the barrier option) or nonlinear (for the American option) Fredholm equation of the first kind. After that the option prices in all cases are presented as one-dimensional integrals of combination of the above solutions and Jacobi theta functions. We also demonstrate that computationally our method is more efficient than the backward finite difference method used for solving these problems, and can also be as efficient as the forward finite difference solver while providing better accuracy and stability.

Introduction

The Orstein-Uhlenbeck (OU) process with time-dependent coefficients is very popular among practitioners for modeling interest rates and credit. That is because it is relatively simple, allows negative interest rates (which recently has become a hot feature) , and could be calibrated to the given term-structure of interest rates and to the prices or implied volatilities of caps, floors or European swaptions since the mean-reversion level and volatility are functions of time. The most known among this class are Hull-White and Vasicek models, see (Brigo and Mercurio, 2006) and references therein.

The Hull-White model is a one-factor model for the stochastic short interest rate of the form

| (1) |

where is the time, is the constant speed of mean-reversion, is the mean-reversion level, is the volatility of the process, is the standard Brownian motion under the risk-neutral measure. This model can also be used for pricing Equity or FX derivatives if one assumes that the mean-reversion level vanishes, while the mean-reversion rate is replaced either by for Equities, or by for FX, where are the deterministic interest rate and continuous dividends, and are the deterministic domestic and foreign interest rates.

Without loss of generality in this paper we are concentrated on the Equity world. Since the process in Eq. (1) is Gaussian the model is tractable for pricing European plain vanilla options. However, for exotic options, e.g., highly liquid barrier options, or for American options these prices are not known yet in closed form. Therefore, various numerical methods are used to obtain them, that sometimes could be computationally expensive. In this paper we attack this problem by constructing a semi-closed form solutions for the prices of barrier and American options written on the process Eq. (1). The results obtained in the paper are new. Our approach to a certain degree is similar to that in (Mijatovic, 2010), who, however, used a different underlying process (the lognormal model with local spot-dependent volatility, and constant interest rates and dividends, but time-dependent barriers). Therefore, our model is more general in a sense that all parameters of the model are time-dependent, while adding time-dependent barriers can be naturally done within our approach. Also, as compared with (Mijatovic, 2010), we don’t use a probabilistic argument, rather a theory of partial differential equations (PDE). At the end we demonstrate that computationally our method is more efficient than the backward finite difference method used to solve these problems, and can also be as efficient as the forward finite difference solver while providing better accuracy and stability.

1 Problem for pricing barrier options

We start by specifying the dynamics of the underlying stock price to be

| (2) |

where now is the deterministic short interest rate, and is the stock price111It is easy to show that this model is equivalent to the Hull-White model.. Here we don’t specify the explicit form of but assume that they are known either as a continuous functions of time , or as a discrete set of values for some moments .

Further in this section we consider a contingent claim written on the underlying process in Eq. (2) which is the Up-and-Out barrier Call option. It is known that by the Feynman-Kac formula, (Klebaner, 2005) one can obtain a parabolic (linear) PDE which solution gives the Up-and-Out barrier Call option price conditional on , which reads

| (3) |

This equation should be solved subject to the terminal condition at the option maturity

| (4) |

and the boundary conditions

| (5) |

where is the upper barrier.

Our goal now is to build a series of transformations to transform Eq. (3) to the heat equation.

1.1 Transformation to the heat equation

To transform the PDE Eq. (3) to the heat equation we first make a change of the dependent and independent variables as follows:

| (6) |

where new functions has to be determined in such a way, that the equation for is the heat equation. This can be done by substituting Eq. (6) into Eq. (3) and providing some tedious algebra. The result reads

| (7) | ||||

The function solves the following ordinary differential equation (ODE)

| (8) | ||||

The Eq. (8) by substitution

| (9) |

can be further transformed to the Riccati equation

| (10) |

This equation cannot be solved analytically for arbitrary functions , but can be efficiently solved numerically. Also, in some cases it can be solved in closed form. For instance, if (which at the current market is a typical case), then can be reduced to . Then assuming in the first approximation on

| (11) |

we obtain the solution

| (12) |

where is an integration constant. Thus, Eq. (11) can be re-written as

where is the normal variance, and is the average normal variance. Thus, our solution in Eq. (12) is correct if and also , because then can always be chosen to obey the inequality .

With these explicit definitions Eq. (3) transforms to the form

| (13) |

The next step is to make a change of the time variable

| (14) |

so Eq. (13) finally takes the form of the heat equation

| (15) |

The Eq. (15) should be solved subject to the terminal condition

| (16) |

and the boundary conditions

| (17) |

These conditions directly follow from Eq. (4), Eq. (5), while is now a time-dependent upper barrier 222Therefore, we can also naturally solve the same problem with the time-dependent upper barrier as this just changes the definition of .. The function is the inverse map of Eq. (14). It can be computed for any by substituting it into Eq. (14), then finding the corresponding value of , and finally inverting.

1.2 Solution of the barrier pricing problem

The PDE in Eq. (15), Eq. (16), Eq. (17) is a parabolic equation which solution should be found at the domain with moving boundaries. These kind of problems are known in physics for a long time. Similar problems arise in the field of nuclear power engineering and safety of nuclear reactors; in studying combustion in solid-propellant rocket engines; in laser action on solids; in the theory of phase transitions (the Stefan problem and the Verigin problem (in hydromechanics)); in the processes of sublimation in freezing and melting; in the kinetic theory of crystal growth; etc., see (Kartashov, 1999) and references therein. Analytical solutions of these problems require non-traditional, and sometimes sophisticated methods. Those methods were actively elaborated on by the Russian mathematical school in the 20th century starting from A.V. Luikov, and then by B.Ya. Lyubov, E.M. Kartashov, and many others.

As applied to mathematical finance, one of these methods - the method of heat potentials - was actively utilized by A. Lipton and his co-authors who solved various problems of mathematical finance by using this approach, see (Lipton, 2002; Lipton and de Prado, 2020) and references therein. Another method that we use in this paper is the method of a generalized integral transform. Below we closely follow (Kartashov, 2001) when give an exposition of the method.

We start by introducing an integral transform of the form

| (18) |

where is a complex number with , and . Let us multiply both parts of Eq. (15) by and then integrate on from zero to :

Integrating by parts, we obtain

With allowance for the boundary conditions in Eq. (17) and the definition in Eq. (18) we obtain the following Cauchy problem

| (19) | ||||

The Eq. (19) can be solved explicitly, assuming that is known. The solution reads

| (20) |

As , and , the function at . Therefore, letting tend to , we obtain an equation which makes connection between the moving boundary and :

| (21) |

Using the definitions in Eq. (16) and Eq. (7), the integral in the RHS of Eq. (21) can be represented as

| (22) | ||||

Thus, Eq. (21) takes the form

| (23) |

where F(p) is known from Eq. (22).

The Eq. (23) is a linear Fredholm integral equation of the first kind, (Polyanin and Manzhirov, 2008). The solution can be found numerically on a grid by solving a system of linear equations. In other words, given functions we can compute first , then , and finally (or , thus determining the moving boundary . Next we can solve Eq. (23) for and substitute it into Eq. (20) to obtain the generalized transform of in the explicit form. Therefore, if this transform can be inverted back, we solved the problem of pricing Up-and-Out barrier Call options.

1.3 The inverse transform

In this Section the description of inversion is borrowed from (Kartashov, 2001). Since that book has never been translated into English, we provide a wider exposition of the method. Also, the book contains various typos that are fixed here.

As known from a general theory of the heat equation, the solution of the heat equation at the space domain can be expressed via Fourier series of the form, (Polyanin, 2002)

where are the eigenfunctions of the heat operator , and are its eigenvalues.

Therefore, by analogy we look for the inverse transform of , or for the solution of Eq. (20) in terms of , to be a generalized Fourier series of the form, (Kartashov, 2001)

| (24) |

where are some functions to be determined. Note, that this definition automatically respects the vanishing boundary conditions for . We assume that this series converges absolutely and uniformly for any .

Applying this generalized integral transform to both parts of Eq. (18) and integrating, we obtain

| (25) |

The LHS of this equation is regular everywhere except simple poles on the negative semi-axis, see Fig, 1.3

Let us sequentially integrate both sides of Eq. (25) on along contours . The contour consists of the vertical line , the half-round of radius (the contour crosses the axis in the middle point between and with the center in the origin), and two horizontal lines . It means that the circle doesn’t hit any pole of the LHS of Eq. (25). Then by the Cauchy’s residual theorem, (Mitrinovic and Keckic, 1984) the integral taken along the contour is equal to times the sum of residuals of the LHS of Eq. (25) that lie inside

As poles are simple, and the function under the integral in the LHS of Eq. (25) has the form , the residual of such a function is, (Mitrinovic and Keckic, 1984)

The above analysis is the basis for running a residual machinery to calculate all the coefficients .

1.3.1 Residual machinery

Let us denote via the following contour integral

Below we show that all coefficients can be expressed via these integrals.

1. Coefficient .

Integrating Eq. (25) along the contour gives

Observe, that

where the second result is due to the Cauchy integral theorem, (Mitrinovic and Keckic, 1984). Then

| (26) |

2. Coefficient .

3. Coefficient .

Proceeding in a similar manner, we obtain a general formula for the coefficients

| (27) |

where is the Kronecker symbol.

1.3.2 The final solution

To calculate the integrals in the RHS of Eq. (27), we rewrite them in the explicit form by using the solution for previously found in Eq. (20)

As is a periodic complex function with the period , the RHS of this equation is regular everywhere except simple poles , where vanishes. It is easy to checks that these poles are exactly . Therefore, we again can directly apply the Cauchy residual theorem. Computing residuals, after some algebra we obtain

| (28) |

Thus, from Eq. (24) and Eq. (28) we find the final solution

This can also be re-written as

| (29) | ||||

We proceed with the observation that the sums in Eq. (29) could be expressed via Jacobi theta functions of the third kind, (Mumford et al., 1983). By definition

| (30) |

Therefore,

| (31) | ||||

A well-behaved theta function must have parameter , (Mumford et al., 1983). This condition holds at any .

2 Pricing American options

We recall that an American option is an option that can be exercised at anytime during its life. American options allow option holders to exercise the option at any time prior to and including its maturity date, thus increasing the value of the option to the holder relative to European options, which can only be exercised at maturity. The majority of exchange-traded options are American. For a more detailed introduction, see (Detemple, 2006; Hull, 1997).

It is known that pricing American (or Bermudan) options requires solution of a linear complimentary problem. Various efficient numerical methods have been proposed for doing that. For instance, when the underlying stock price follows the time-dependent Black-Scholes model these (finite-difference) methods are discussed in (Itkin, 2017) (see also references therein).

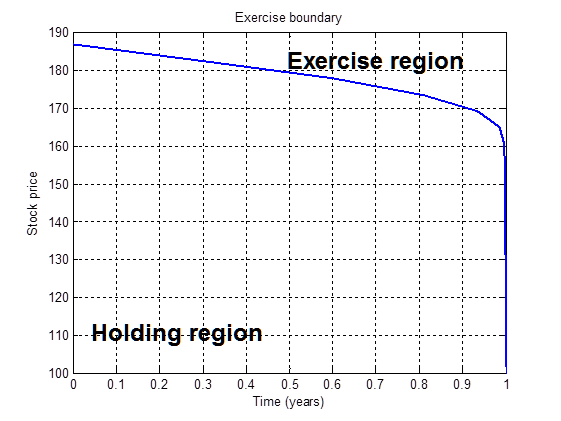

Another approach, elaborated e.g., in (Andersen et al., 2016) for the Black-Scholes model with constant coefficients, uses a notion of the exercise boundary . The boundary is defined in such a way, that, e.g., for the American Put option at it is always optimal to exercise the option, therefore . For the complimentary domain the earlier exercise is not optimal, and in this domain obeys the Black-Scholes equation. This domain is called the continuation (holding) region. The problem of pricing American options lies in the fact that is not known in advance. Instead, we only know the price of the American option at the boundary. For instance, for the American Put we have , and for the American Call - . A typical shape of the exercise boundary for the Call option obtained with the parameters is presented in Fig. 2. The method proposed in (Andersen et al., 2016) finds by numerically solving an integral (Volterra) equation for . The resulting scheme is straightforward to implement and converges at a speed several orders of magnitude faster than existing approaches.

In terms of this paper, the continuation region is a domain with the moving boundary where the option price solves the corresponding PDE. In case of our model in Eq. (2) this is the PDE in Eq. (3). Therefore, this problem is, by nature, similar to that for the barrier options considered in Section 1, but the difference is as follows.

-

•

For the barrier option pricing problem the moving boundary (the time-dependent barrier) is known, as this is stated in Eq. (17). But the Option Delta at the boundary is not, and should be found by solving the linear Fredholm equation Eq. (23). Also, the problem is solved subject to the vanishing condition at the barrier (the moving boundary) for the option value.

-

•

For the American option pricing problem the moving boundary is not known. However, the option Delta at the boundary is known (it follows from the conditions and expressed in variables and according to their definitions in Section 1). Also the boundary condition for the American Call and Put at the exercise boundary (the moving boundary) differs from that for the Up-and-Out barrier option, namely: it is for the Call, and for the Put

Because of the similarity of these two problems, it turns out that the American option problem can be solved for the continuation region together with the simultaneous finding of the exercise boundary, by using the same approach that we proposed for solving the barrier option pricing problem. However, due to the highlighted differences, some equations slightly change.

2.1 Solution of the American Call option pricing problem

Since the PDE we need to solve is the same as in Eq. (3), we do same transformations as in Section 1, and come up to the same heat equation as in Eq. (15). It should be solved subject to the terminal condition

and the boundary conditions

where . We underline once again that the function here is not known yet, while is known. These problems with the free boundaries are also well known in physics.

We proceed by using the same transformation in Eq. (18), and by analogy with Eq. (19) obtain the following Cauchy problem

This problem can be solved explicitly to yield, (Kartashov, 2001)

Accordingly, instead of Eq. (21) we obtain

This is a nonlinear Fredholm equation of the first kind, but now with respect to the function . It can also be solved numerically (iteratively).

The next step is to reduce our problem to that with homogeneous boundary conditions. This can be done by change of the dependent variable

The function solves the same heat equation with the same terminal condition, and with the homogeneous boundary conditions. Therefore, it can be solved by using the method of generalized integral transform described in Section 1.2. The solution reads

Again, using the definition of the Jacobi theta function in Eq. (30), this can be finally re-written as

3 Numerical example

To test performance and accuracy of our method in this Section we provide a numerical example where a particular time dependence of is chosen as

| (33) |

Here are constants. With this model Eq. (10) can be solved analytically to yield

| (34) |

Accordingly, from Eq. (9) we find

| (35) |

and from Eq. (7)

| (36) |

The algorithm described in Section 1 was implemented in python. We did it for two reasons. First, we found neither any standard implementation of the Jacobi theta functions in Matlab, nor any custom good one. Surprisingly, this is also not a part of numpy or scipy packages in python. However, they are available as a part of the python package mpmath which is a free (BSD licensed) Python library for real and complex floating-point arithmetic with arbitrary precision, see (Johansson, 2007). It has been developed by Fredrik Johansson since 2007, with help from many contributors.

Also, we didn’t find any standard implementation of solver for the Fredholm integral equation of the first kind in both python and Matlab. Therefore, we implemented a Tikhonov regularization method as this is described in (Fuhry, 2001). In particular, with the model used in this Section, the function reads

| (37) |

Finally to validate the results provided by our method, we implemented a FD solver for pricing Up-and-Out barrier options. This solver is based on the Crank–Nicolson scheme with a few Rannacher first steps, and uses a non-uniform grid, in more detail see, eg., (Itkin, 2017). We implemented two solvers: one for the backward PDE, and the other one - for the forward PDE. But logically, since in this paper we solved the backward PDE, it does make sense to compare our method with the backward solver. This implementation has been done in Matlab.

In our particular test we choose parameters of the model as they are presented in Table 1.

| 0.02 | 0.01 | 0.5 | 0.1 | 0.2 | 90 | 60 |

We recall, that here is the normal volatility. Therefore, we choose its typical value by multiplying the log-normal volatility by the barrier level.

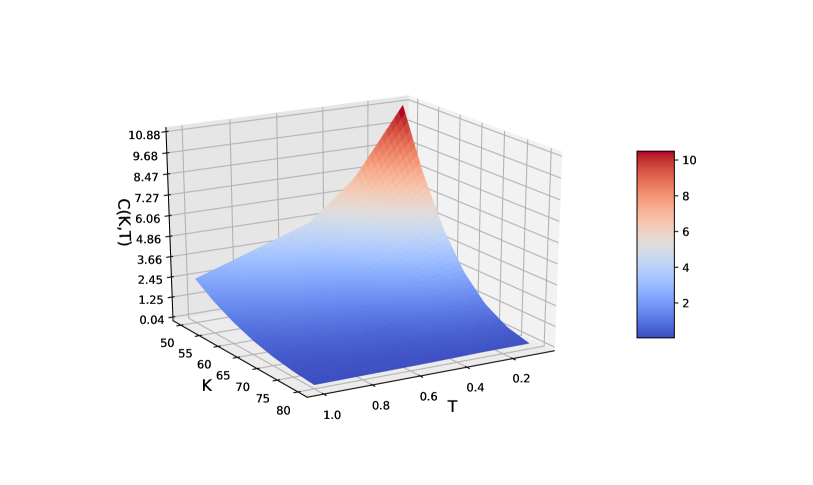

We run the test for a set of maturities and strikes . The Up-and-Out barrier Call option prices computed in such an experiment are presented in Fig. 3.

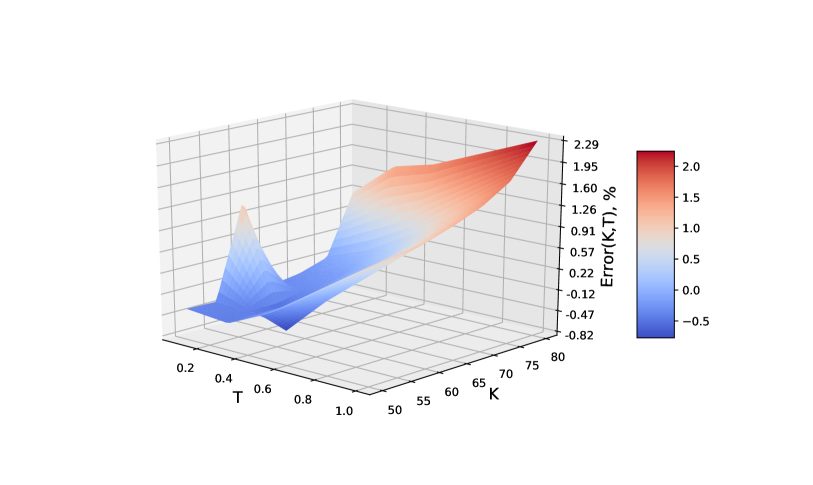

In Fig. 4 the relative errors between the Up-and-Out barrier Call option prices obtained by using our method and the FD solver are presented as a function of the option strike and maturity . Here to provide a comparable accuracy we run the FD solver with 101 nodes in space and the time step = 0.01.

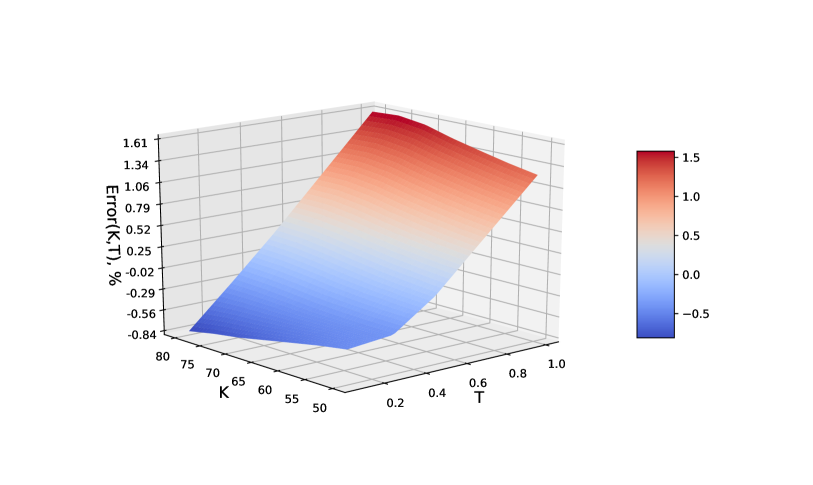

It can be seen that the quality of the FD solution is not sufficient. Therefore, we reran it by using 201 nodes in space and the time step = 0.001. The relative errors between our semi-analytic and the FD solutions in this case are presented in Fig. 5.

It can be seen that the agreement becomes better, so the relative error decreases. However, the cost for this improvement of the FD method is speed. In Table 2 we compare the elapsed time of both methods. The column "no " has the following meaning. Since the volatility and the interest rate change with time relatively slow, contribution of the second integral in Eq. (32) to the option price is negligible. Therefore, in this particular case we can find the option price by computing only the first integral in Eq. (32). Accordingly, we don’t need to solve the Fredholm equation Eq. (23) that almost halves the elapsed time.

| Test | semi-analytic | semi-analytic, no | FD-101, | FD-201, | FD-201, |

| Elapsed time, sec | 0.23 | 0.16 | 0.36 | 0.65 | 3.6 |

Finally, it is known that linear algebra in python (numpy) is almost 3 times slower than that in Matlab. Therefore, given the same accuracy, our method is about 30-40 times faster than the backward FD solver.

Of course, the forward FD solver is by an order of magnitude faster than the backward one if we need to simultaneously price multiple options of various strikes and maturities, but written on the same underlying. However, for barrier options this approach requires a very careful implementation, which often is not universal and with a lot of tricks involved.

4 Discussion

Our attention in Section 1 was drawn to the Up-and-Out barrier Call option . Obviously, using the barriers parity, (Hull, 1997), the price of the Down-and-Out barrier Call option can be found as , where is the price of the European vanilla Call option. It is known that the latter is given by the corresponding formula for the process with constant coefficients, where those efficient constant coefficients are defined as

Second, as shown in Section 1.2, the barriers also could be some arbitrary functions of time, as this changes just the definition of function . And our method provides the full coverage of this case with no changes.

Third, and perhaps the most important point is about computational efficiency of our method. In addition to what was presented in Section 3, let’s look at this problem from a theoretical pint of view. Suppose the barrier pricing problem is attacked by solving the forward PDE for a set of strikes and a set of maturities numerically by some FD method on a grid with nodes in the space domain , and nodes in the time domain . Then the complexity of this method is known to be . This should be compared with the complexity of our approach.

Let’s assume that the Riccati equation in Eq. (10) can be solved either analytically, or, at least, approximately, as this is discussed in Section 1.1. Then the first computational step consists in solving the linear Fredholm equation in Eq. (23). This can be done on a rarefied grid with nodes and complexity . The intermediate values in can be found (if necessary) by interpolation with the complexity . As the integral kernel doesn’t depend on strikes , this calculation can be done simultaneously for all strikes still preserving the complexity .

The final solution of the pricing problem is provided in the form of two integrals in Eq. (32). Therefore, if we need the option price at a single value of (same as when solving the forward PDE), but for all strikes and maturities, the complexity is , where is the number of points in the space, and is the complexity of computing the Jacobi theta function . Normally, for the typical values of in the FD method (about 50–100 or even more). Thus, the total complexity of our method is fully determined by the solution of the Fredholm equation. Therefore, our method is slower than the corresponding FD method if . For the American option this situation is worse since instead of solving a linear Fredholm equation we need to solve a nonlinear equation. This can be done iteratively, e.g., using iterations until the method converges to the given tolerance. Then the total complexity becomes . However, our experiments show that using just points in space could be sufficient, while further increase of doesn’t change the results.

Also, the accuracy of the method in can be increased if one uses high-order quadratures for computing the final integrals. For instance, one can use the Simpson instead of the trapezoid rule that doesn’t affect the complexity of our method. While increasing the accuracy for the FD method is not easy (i.e., it significantly increases the complexity of the method, e.g., see (Itkin, 2017)).

References

- Andersen et al. (2016) L. Andersen, M. Lake, and D. Offengenden. High-performance american option pricing. Journal of Computational Finance, 20(1):39–87, 2016.

- Brigo and Mercurio (2006) D. Brigo and F. Mercurio. Interest Rate Models – Theory and Practice with Smile, Inflation and Credit. Springer Verlag, 2nd edition, 2006.

- Detemple (2006) J. Detemple. American-Style Derivatives: Valuation and Computation. Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton, London, New York, 2006.

- Fuhry (2001) M. Fuhry. A new tikhonov regularization mathod. mathesis, Kent State University Honors College, May 2001.

- Hull (1997) John C. Hull. Options, Futures, and Other Derivatives. Prentice Hall, 3rd edition, 1997.

- Itkin (2017) A. Itkin. Pricing Derivatives Under Lévy Models. Modern Finite-Difference and Pseudo-Differential Operators Approach., volume 12 of Pseudo-Differential Operators. Birkhauser, 2017.

- Johansson (2007) F. Johansson. Mpmath library. URL http://mpmath.org/, 2007.

- Kartashov (1999) E. M. Kartashov. Analytical methods for solution of non-stationary heat conductance boundary problems in domains with moving boundaries. Izvestiya RAS, Energetika, (5):133–185, 1999.

- Kartashov (2001) E.M. Kartashov. Analytical Methods in the Theory of Heat Conduction in Solids. Vysshaya Shkola, Moscow, 2001.

- Klebaner (2005) F. Klebaner. Introduction to stochastic calculus with applications. Imperial College Press, London, UK., 2005.

- Lipton (2002) A. Lipton. The vol smile problem. Risk, pages 61–65, February 2002.

- Lipton and de Prado (2020) A. Lipton and M.L. de Prado. A closed-form solution for optimal mean-reverting trading strategies, 2020. available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3534445.

- Mijatovic (2010) A. Mijatovic. Local time and the pricing of time-dependent barrier options. Finance and Stochastics, 14(1):13–48, 2010.

- Mitrinovic and Keckic (1984) D.S. Mitrinovic and J.D. Keckic. The Cauchy method of residues: Theory and Applications. Mathematics and its Applications. Springer, Netherlands, 1984. ISBN 978-90-277-1623-1.

- Mumford et al. (1983) D. Mumford, C. Musiliand M. Nori, E. Previato, and M. Stillman. Tata Lectures on Theta. Progress in Mathematics. Birkhäuser Boston, 1983. ISBN 9780817631093.

- Ohyama (1995) Y. Ohyama. Differential relations of theta functions. Osaka Journal of Mathematics, 32(2):431–450, 1995.

- Polyanin (2002) A.D. Polyanin. Handbook of linear partial differential equations for engineers and scientists. Chapman & Hall/CRC, 2002.

- Polyanin and Manzhirov (2008) P. Polyanin and A.V. Manzhirov. Handbook of Integral Equations: Second Edition. Handbooks of mathematical equations. CRC Press, 2008. ISBN 9780203881057.