Asymptotic delay times of sequential tests based on -statistics for early and late change points

Abstract

Sequential change point tests aim at giving an alarm as soon as possible after a structural break occurs while controlling the asymptotic false alarm error. For such tests it is of particular importance to understand how quickly a break is detected. While this is often assessed by simulations only, in this paper, we derive the asymptotic distribution of the delay time for sequential change point procedures based on U-statistics. This includes the difference-of-means (DOM) sequential test, that has been discussed previously, but also a new robust Wilcoxon sequential change point test. Similar to asymptotic relative efficiency in an a-posteriori setting, the results allow us to compare the detection delay of the two procedures. It is shown that the Wilcoxon sequential procedure has a smaller detection delay for heavier tailed distributions which is also confirmed by simulations. While the previous literature only derives results for early change points, we obtain the asymptotic distribution of the delay time for both early as well as late change points. Finally, we evaluate how well the asymptotic distribution approximates the actual stopping times for finite samples via a simulation study.

Keywords: Stopping time; robust monitoring; Wilcoxon test; run length; CUSUM procedure

1 Introduction

Monitoring time series for structural breaks have a long tradition in time series going back to [25, 26]. In the seminal paper of [7] sequential change point tests are introduced that allow to control the asymptotic false alarm rate (type-I-error) while guaranteeing that the procedure will asymptotically stop with probability one if a change occurs by assuming the existence of a stationary historic data set. This approach has then been adopted for a variety of settings and a variety of monitoring statistics. For example, [2, 17, 19] derive procedures in linear models, [14] for changes in the error distribution of autoregressive time series, [12] for renewal processes while [5] consider changes in GARCH models. [22] derive a unified theory based on estimating functions, that has been extended to different monitoring schemes by [23]. Bootstrap methods designed for the particular needs of sequential procedures have also been proposed by [15, 18, 20]. In this paper, we will revisit the sequential test based on -statistics that has been proposed in [21], which includes a difference-of-means (DOM) as well as Wilcoxon sequential test. A similar setting for a-posteriori change point tests have been considered by [8] for independent data, which has been extended to time series by [9].

Starting with [1], who consider a mean change model, several papers derived the limit distribution of the corresponding stopping times. For example [3, 10] consider a modified test statistic for changes in the mean, [4, 6] consider changes in a linear regression models, while [13] consider changes in renewal processes. All of those papers only obtain results for early (sublinear) change points, where the time of change relative to the length of the historic data set vanishes asymptotically. In contrast, we will derive the corresponding results not only for such early change points but also for late (linear and even superlinear) relative to the length of the historic data set, which has been an open problem even for the mean change problem and the standard DOM statistic until now.

As in the setting of [7] we assume the existence of a stationary historic data set . Then, we monitor new incoming data by testing for a structural break after each new observation based on a monitoring statistic . The procedure stops and detects a change as soon as The weight function is chosen such that converges in distribution to some non-degenerate limit distribution (as the length of the historic data set grows to infinity) if no change occurs. If the threshold is chosen as the corresponding -quantile, the procedure has an asymptotic false alarm rate of (while still having asymptotic power one under alternatives).

To illustrate, consider the mean change model

| (1.1) |

where is a stationary time series with mean . The change in the mean is given by and is allowed to depend on .

For this situation the classical difference-of-means (DOM) monitoring statistic is given by

| (1.2) |

The corresponding sequential procedure has already been investigated by several authors including [2, 7, 17, 19]. Clearly, this is a sequential version of a two-sample statistic that similarly to the two-sample -test is not robust. Given the good properties of a Wilcoxon/Mann-Whitney two-sample test it is promising to consider the Wilcoxon monitoring statistic

| (1.3) |

which was recently proposed by [21]. Both statistics are sequential -statistics of the following type:

| (1.4) |

where the kernel is a measurable function and with is an independent copy of . In this framework, the DOM-kernel is given by such that . The Wilcoxon-kernel is given by , such that .

The stopping time of the corresponding sequential procedure is given by

| (1.5) |

where . The monitoring procedure stops as soon as the monitoring statistic exceeds in absolute value a critical curve given by . If is chosen as the -quantile of the limit distribution as given in Theorem 1, the asymptotic false alarm rate is given by . The above weight function is often chosen in the literature because the corresponding limit distribution as given in Theorem 1 has a nice well-known structure (noting that the supremum is only taken over despite the infinite observation horizon). [21] consider a much larger class of weight functions including in particular weight functions of the type

| (1.6) |

that also have this nice property. However, it is well known that a choice of only results in a quicker detection for early changes (see also Remark 4 below). Because the main focus of this paper lies on the analysis of the detection delay for late changes, where the critical curve for larger values of lies above the critical curve for (see e.g. Figure 6.1 in [27]), the results are derived for only. Nevertheless, for early changes the corresponding results for all have been considered in Section 5.1 in [27] and are summarized in Theorem 7 below.

This paper is organized as follows: In Section 2 we derive the asymptotic delay times for -statistics, where we first discuss the threshold selection in Section 2.1. In Section 2.2 we obtain conditional results given the historic data, before we discuss corresponding consequences for the unconditional results in Section 2.3. It turns out that for late changes, the influence of the historic data set to the asymptotic expected stopping time is no longer negligible. We explain how to obtain the standardizing sequences for the asymptotic results in Section 2.4 giving a sketch of the main proof ideas along the way. In Section 2.5 we give some simulations indicating that the asymptotic result gives indeed a good approximation of the small sample behavior. In Section 3 we compare the DOM with the Wilcoxon procedure both based on theoretic considerations and by simulations. After some conclusions in Section 4 we finally provide the proofs in Section 5.

2 Asymptotic delay times

We consider the following model, which generalizes the above mean change model as given by (1.1),

| (2.1) |

where and are suitable stationary time series with unknown distribution, not necessarily centered fulfilling certain assumptions specified below. The distribution of the time series after the change and thus the change itself is allowed to depend on . The change point fulfills with some unknown and unknown .

The parameter effectively determines whether a change occurs early or late (compared to the length of the historic data set) and will influence the asymptotic distribution of the stopping time.

Definition 1.

Changes with are classified as early or sublinear (in m) whereas changes with are classified as late change. In the latter case we further distinguish between linear changes () and superlinear changes ().

In the previous literature, only the stopping times for early, i.e. sublinear, changes were obtained, while even for the DOM monitoring statistic the asymptotic distribution for late (i.e. linear and superlinear) changes has not been derived to the best of our knowledge.

Furthermore, define the (unknown) magnitude of the change by

| (2.2) |

where is independent of and . We allow for fixed as well as local changes whose magnitude does decrease to 0, while at the same time being large enough to be asymptotically detectable with probability tending to one (see Remark 1):

Assumption 1.

-

(i)

.

-

(ii)

.

For the DOM monitoring procedure with we obtain by

| (2.3) |

such that in the mean change model (1.1) it holds . For the Wilcoxon monitoring procedure with we obtain

| (2.4) |

such that in the mean change model (1.1) it holds for

and a similar expression for .

2.1 Threshold selection

In this section, we discuss the selection of the threshold . Theorem 1 states the limit distribution of the monitoring statistic in the situation of no change (i.e. ) which allows to determine the threshold in such a way that the asymptotic false alarm rate is controlled by a previously chosen . Proposition 1 shows under which conditions the probability of a false alarm before a change occurs vanishes asymptotically. Most importantly, it shows that for late changes this can only be achieved if the threshold increases to infinity. This is in contrast to early changes as previously discussed in the literature.

In order to state the assumptions we need to introduce a version of Hoeffding’s decomposition (see [16]) which is widely used in the context of -statistics. However, in contrast to the classical two-sample situations, the monitoring sample contains both random variables following the distribution of and those following as soon as . Therefore, additional terms appear taking this into account. Define

| (2.5) |

The terms and correspond to the usual Hoeffding’s decomposition where both samples share the same distribution, while the terms and correpond to the ones where the second sample follows the distribution of . Then, the following decomposition holds for :

| (2.6) |

Here, the signal part is given by as defined in (2.2), the first two summands are the historic parts involving

the third and fourth summand are the monitoring part with

while the last summand is a remainder term

For an analogous decomposition holds, where has to be replaced by making the terms involving and and disappear (see also (2.1) in [21]), i.e.

| (2.7) |

For the DOM kernel with we obtain by (2.3)

where in the mean change model (1.1) it holds .

For the Wilcoxon kernel with and a continuous with distribution function it holds with (2.4)

where in the mean change model (1.1) it holds .

Assumption 2.

Let be a stationary time series that fulfills the following assumptions for a given kernel function with the notation as in (2.5):

-

(i)

with . -

(ii)

It holds for

The second assumption follows for example from a functional central limit theorem as in the next theorem. For a discussion of these assumptions for independent as well as dependent observations, we refer to Section 2.3 in [21].

The proof of the following theorem can be found in [21] (Theorem 1 and Corollary 2), where the additional Hájek-Rényi-type inequality in that paper (as in (2.21) below) is only required for weight functions as in (1.6) with but not for as here.

Theorem 1.

Let Assumption 2 (i) be fulfilled in addition to the following functional central limit theorem (for any )

where is a non-degenerate centered bivariate Wiener process with . Additionally, let the following Hájek-Rényi-type inequality hold: For any sequence it holds uniformly in

Then, if no change occurs (i.e. ), it holds as

where is a standard Wiener processes.

If the assumption is not fulfilled, the limit distribution is more complicated (see Theorem 1 in [21]). However, both the DOM and the Wilcoxon-kernel fulfill this assumption.

Remark 1.

The theorem shows that the monitoring procedure has asymptotic size if the threshold is chosen as the -quantile of the limit distribution in Theorem 1. Furthermore, Theorem 3 and the respective proof in [21] imply that changes are detected asymptotically with probability one as under Assumption 1 (ii); for more details we refer to [21].

Under the following assumptions the probability of a false alarm before the change occurs converges to zero. This is necessary in order to have stopping times that are asymptotically not contaminated by false alarms.

Assumption 3.

Let the following assumptions on the threshold hold:

| (2.8) | ||||

| (2.9) |

where and and are defined by . For late changes let .

For a bounded sequence of critical values assertion (2.9) cannot be fulfilled for late changes if fulfills a central limit theorem (an assumption that is required to derive the limit distribution in the no-change situation). On the other hand, for assertion (2.9) is automatically fulfilled as soon as , which holds for any sequence fulfilling (2.8) (including using asymptotic quantiles as critical values) for early changes, and for any sequence for late changes.

2.2 Asymptotic distribution of the delay times

In this section we consider the following delay time

| (2.11) |

which in contrast to the stopping time as in (1.5) explicitely excludes early rejections due to false alarms. By choosing a threshold satisfying Assumption 3, early rejections are prevented asymptotically with probability one such that the delay time is asymptotically equivalent to the stopping time .

Effectively, there are two essential differences when considering late changes as opposed to early changes:

-

•

As stated in Proposition 1 for late changes the threshold needs to diverge in order to asymptotically guarantee that no false alarm prior to the change has occurred. For early changes fixed thresholds (such as quantiles of the limit distribution in the no change situation) can and have been used.

-

•

For early changes, the influence of the historic data set on the stopping time is asymptotically negligible. This is no longer the case for late changes. Heuristically, this can be seen from decomposition (2.1) where , , and , , are of the same order, so that the factors effectively determine the dominating terms. For early changes only observations are necessary to reliably detect a change point (see Lemma 1 b)), hence the factors in front of and are of smaller order than the ones in front of and , making these terms asymptotically negligible (for a mathematically rigorous proof of this statement we refer to Lemma 5.6 in [27]). On the other hand, for late changes, this is no longer true, in fact for linear changes with all four terms are of the same order while for late changes the terms involving the historic data set even dominate.

A consequence of the second observation is that for late change points the asymptotic stopping time can no longer be expected to be independent of the historic data set or more precisely of and . In order to deal with this, we will first derive results conditional on and that will then also lead to unconditional results as well. For this reason we assume that the monitoring data set is independent of the historic data set so that and do not depend on the conditioning variables and .

Assumption 4.

Let the monitoring data set be independent of and .

This assumption is only required to get (for any index set and )

| (2.12) |

which clearly follows from the independence assumption. As soon as this equality holds at least asymptotically, the independence assumption can be dropped. We conjecture that this is possible if a suitable dependence structure allowing for example for big-block-small-block arguments is being used. However, for clarity of presentation of the results for monitoring -statistics, we will leave this for future work.

Assumption 5.

-

(a)

Let and be stationary time series that fulfill the following assumptions for a given kernel function :

-

(i)

with . -

(ii)

For all the following Hajek-Renyi-type inequality holds

-

(i)

-

(b)

For very early changes with (which is a certain subclass of early sublinear changes), we require additionally to (a) the following functional central limit theorem

for , where is a non-degenerate centered bivariate Wiener process with and .

-

(c)

For later changes with , we require additionally to (a)

-

(i)

as , where is as in (b).

-

(ii)

as .

-

(i)

The variance of the limit distribution of the delay time for early changes depends on the interplay between the magnitude of the change in combination how early the change occurs. More precisely with and the notation of Assumption 5, consider

| (2.13) |

By Assumption 1 (ii) for late changes always the last case that applies. The assumptions on the threshold are clearly fulfilled for any constant threshold for early changes as well as for any sequence of thresholds converging to infinity in case of late changes.

The following assumptions imply Assumption 3.

Assumption 6.

Let , , as well as

The below theorem shows that properly standardized delay times will be asymptotically normal with the above variance . This shows that for sublinear changes with a combination of a small (particularly early) and/or small magnitude the asymptotic variance of the delay time is determined by distributional properties of the observations after the change occurred. On the other hand for late (linear and superlinear) changes or even sublinear changes but with a larger magnitude of the change, the asymptotic variance is determined by distributional properties of the observations before the change occurs. The second case is the transition between those two situations.

Theorem 2.

Let Assumptions 1 – 3 be satisfied. Consider the standardizing sequences

| (2.14) | ||||

where is the sign of , and

| (2.15) |

Then, it holds

where is the distribution function of the standard Gaussian distribution and is as in (2.13).

In particular the theorem shows that the sequence represents the asymptotic expected delay while represents the asymptotic variability.

Assumption 7.

Let

| (2.16) |

If a law of iterated logarithm for holds we can quantify for the latter condition (that also implies (2.9)) precisely.

Remark 2.

Often fulfills a law of iterated logarithm, i.e.

| (2.17) |

for some . In case of the DOM kernel this comes down to the usual law of iterated logarithm for , while for the Wilcoxon kernel it comes down to a law of iterated logarithm for . In this case (2.16) is fulfilled for early changes (i.e. with ) if a constant threshold (for example obtained as a quantile from the limit distribution in Theorem 1) is applied.

On the other hand, for late changes () assertion (2.16) is not satisfied for a constant threshold but is fulfilled as soon as

| (2.18) |

i.e. in particular, if grows faster to infinity than . In case of linear changes with , this condition can be weakened further, where the left hand side only needs to be larger than .

Similarly, by the law of iterated logarithm the other assertions can also be quantified.

Corollary 3.

This is of particular interest for the DOM kernel, where the remainder terms are equal to zero such that and coincide.

Theorem and corollary follow relatively easily from the below result for the conditional probability given and . This may also be of independent interest as the historic data is known when the monitoring starts (but and will typically depend on unknown distributional properties of the observations).

As in Corollary 3 we only get the result for . Because the remainder term depends on the historic data set as well, its neglibility conditionally on and cannot be established based on Assumptions 2 (i) and 5 (a) (i) alone. On the other hand to prove the neglibility conditionally on and , these assumptions are sufficient (see the proof of Theorem 2).

To obtain the below result, we need the sequences and to fulfill (2.19). By Assumption 7 the corresponding sequences of random variables and fulfill (2.19) almost surely. Despite the fact that conditional probabilities are only defined almost surely, this does not mean that we can drop (2.19) and still obtain the same limit distribution. This is because the ’almost surely’ for the conditional probability refers to a one-set for each fixed , whereas ’almost surely’ as in Assumption 7 refers to a one-set with respect to a limit result (which is not uniform in ).

Theorem 4.

The main ideas to obtain the standarizing sequence and as well as of the proof of the above theorem can be found in Section 2.4.

2.3 Consequences for unconditional results

We obtain the following unconditional results as an immediate corollary of Theorem 2 by an application of Lebesgue’s dominated convergence theorem

Corollary 5.

Under the assumptions of Theorem 2 it holds with the same notation

The normalizing sequences in this theorem clearly still depend on the historic data via and . However, the following theorem shows that the influence on the asymptotic variance is negligible, while for the asymptotic delay time the influence of the historic data is only negligible for early changes. For late but linear changes the dependence on is negligible, which is still true for superlinear changes if is not too large (i.e. the change not too late) in combination with the magnitude of the change being sufficiently large. While only depends on distributional properties of the random variables before the change, also depends on distributional properties after the change.

Theorem 6.

Under the assumptions of Theorem 2 it holds with the same notation:

-

a)

For any it holds

-

b)

Let

which holds for all sublinear and linear changes but also some superlinear (not too late with sufficiently large magnitude) changes. Then, it holds that

-

c)

For early (sublinear) changes with it holds

Remark 3.

For early changes, the factor in is negligible (see Section 5.4 for a proof). In the previous literature the asymptotic delay time was thus reported as in corresponding results. However, even for early changes, where this term is negligible (in contrast to late changes), the term can be seen as a bias correction leading to considerably better approximations in small samples as can be seen in Figure 3 below. This is due to the fact, that this term is always strictly greater than such that the asymptotic distribution without the bias correction systematically underestimates the delay time in small samples.

For early changes, the assertion of Theorem 6 c) has also been established in Theorem 5.3 in [27] for different weight functions with under a slightly different set of assumptions.

Theorem 7.

Let the change fulfill Assumption 1 with constant. Additionally let the time series before the change fulfill the assumptions of Theorem 1, where Assumption 2(i) needs to be strengthend to fulfill for all in addition to

| (2.21) |

for all . Additionally, let Assumption 5(a) hold with the same stronger assumption on as above, Assumption 5 (b) and .

Remark 4.

The previous result can be used to establish that for sublinear changes a close to leads to an asymptotically smaller delay time and is thus preferable for early changes (see Section 5.4 for a proof). However, this comes at the cost of a higher probability of a false alarm at the very beginning of the monitoring period (see e.g. Figure 1 in [21]).

A corresponding analysis for late changes by means of the asymptotic delay times is left for future work. However, given that the procedure stops as soon as the critical curve (as defined by ) is exceeded by the monitoring statistic one can easily compare the critical curves instead. It turns out that – for constant critical values chosen as -quantiles of the limit distribution in the no-change scenario as in Remark 1 – critical curves corresponding to smaller are above those with larger first, but drop beneath them relatively quickly showing that larger values of are better for early changes while smaller ones are better for late changes. In fact, the simulations in [23] show that this happens relatively soon, leading to best results for the choice . Indeed the quotient of two weight functions as in (1.6) with is given by

where . Consequently, this quotient is first smaller than one, but will eventually be larger than one. In fact, looking more closely, one can easily achieve that this happens for the first time, when for some suitable . In particular, this guarantees, that achieves best results in the superlinear case, which is one of the reasons we restrict the main discussion in this paper to this case.

2.4 Asymptotic expectation and variance of the delay times and main proof ideas

In this section we shed some light at the derivation of the standardizing sequences , representing the asymptotic expected delay, as well as , representing its asymptotic variability, which is a crucial step in the proof of Theorem 4 and thus ultimately of Theorem 2.

With the notation of Theorem 4 the aim it is to derive normalizing sequences and such that the limit distribution of can be established. Denote with , as in Theorem 4.

Denoting

| (2.22) |

the main idea following [1] is the duality between the standardized delay time and the monitoring statistic:

| (2.23) |

For other weight functions it can be necessary to choose a more complicated that fulfills (2.4). For the weight function in (1.6) with , for example,

has been used in the proof of Theorem 7 (see (5.8) in [27]) as well as by [1] and [10]. For the two definitions coincide.

To get the desired result, in view of (2.4), it is sufficient to find sequences and such that

| (2.24) |

and

| (2.25) |

as then it holds

To this end one first looks for sequences and such that (2.25) holds. They will naturally depend on and thus on and , such that the final task is to find and fulfilling (2.24).

So, first, let us have a closer look at (2.25): Clearly, captures the expectation and the variance of .

In the situation of this paper, the supremum in (2.25) is dominated by (for a rigorous statement see Lemma 2 below) such that and can be constructed with respect to . The mean correction has to capture the signal part as well as the historic parts of as in (2.1) (the latter at least for late changes as discussed at the beginning of Section 2.2), where one has to take into account whether the historic parts strengthen or counteract the change.

These considerations and (2.2) lead to the choice

| (2.26) |

Then, the limit distribution is determined by the monitoring part which for fulfills a central limit theorem with summands and thus requires a scaling of . In combination with the weight function this leads to the choice

| (2.27) |

Proposition 2 shows that the above choices of and indeed fulfill (2.25). By (2.22), (2.26) and (2.27) we get

Choosing as in (2.14)

| (2.28) |

the terms on the last line cancel, such that by (2.19)

By Assumption 1(ii) and (2.19) it holds

| (2.29) |

As it follows for large enough

| (2.30) |

Hence, choosing as in (2.15)

| (2.31) |

guarantees

| (2.32) |

such that

This shows that (2.24) is fulfilled for these choices of normalizing sequences. By these considerations and Proposition 2 below the proof of Theorem 4 is complete.

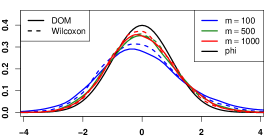

2.5 Simulations

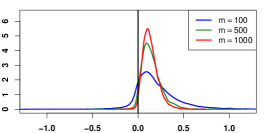

In Sections 2.2 and 2.3, we have shown that the stopping time converges to a Gaussian distribution if standardized appropriately. We will now evaluate the fit obtained from that asymptotic approximations in small samples numerically.

To this end we simulate mean changes as in (1.1) with . We use historic data sets of length and a monitoring horizon of . For early changes we use a constant threshold fulfilling both Assumptions 6 and 7, where is the -quantile of with (corresponding to a -level test as in Remark 1), where is based on simulations of a Wiener process on a grid of points. For late changes we choose such that equality in (2.18) holds as . This choice fulfills Assumption 6 and almost fulfills Assumption 7, see Remark 2.

For better comparability for different kernels as well as different distributions of the underlying time series, we additionally divide the standardized stopping time by such that the limit distribution is standard normal in all situations.

We simulate i.i.d. Gaussian and distributed time series as well as AR(1) time series with parameter Gaussian and innovations. In the latter case, and are replaced by estimators of the long-run covariance which is estimated with a Bartlett kernel based on the historic data set. and are given by (2.3) and (2.4), where the latter is determined numerically. For time series with -distributed errors the latter is estimated by means of Monte-Carlo simulations (based on independent time series of length each), so is for the Wilcoxon statistic. All curves below are based on repetitions.

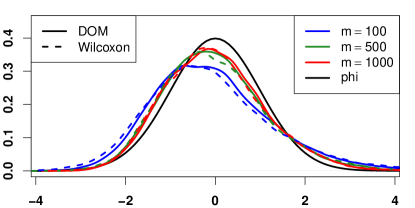

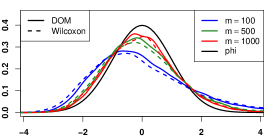

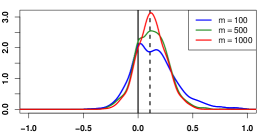

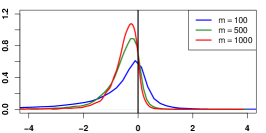

Figure 1 shows estimated densities of the standardized stopping times for different lengths of the historic data sets for independent standard normally distributed observations along with the standard normal density. The standardization is done as in Corollary 5 including a division by . In all cases the fit is reasonably good and becomes better with increasing length of the historic data set.

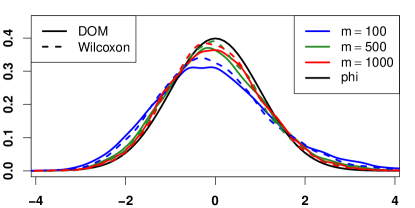

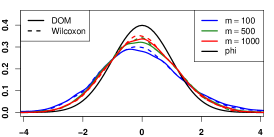

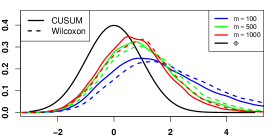

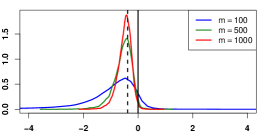

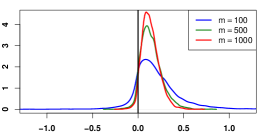

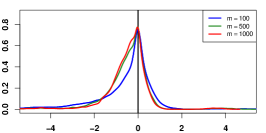

The simulation results for distributed errors look very similar. For time series errors this is also true, but with a somewhat slower convergence i.e. somewhat longer historic data sets are required to get similar results. This is not surprising given that the effective sample size is smaller for positively correlated time series errors and at the same time the long-variance has been estimated for each time series while the true variance has been used for i.i.d. data. To illustrate these points, Figure 2 shows the corresponding results for (where results for different values of look very similar).

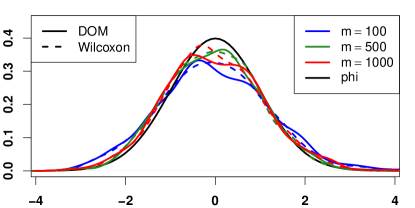

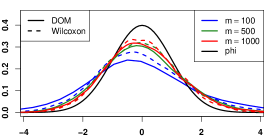

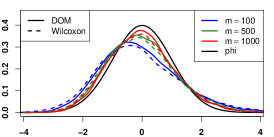

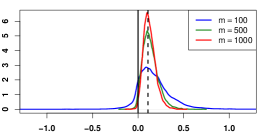

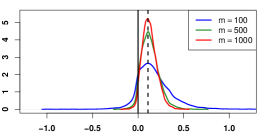

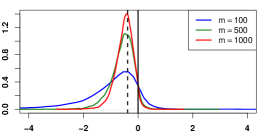

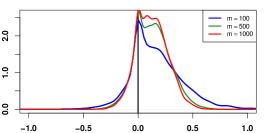

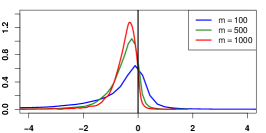

Simulation results for all cases if is replaced by as in Theorem 6 a) as well as for sublinear and linear changes if is replaced by as in Theorem 6 b) look very similar. For sublinear changes by Theorem 6 c) the asymptotic distribution is independent of both and such that and can be used. To illustrate this point Figure 3 (a) and (b) give the corresponding simulation results for for i.i.d. normal errors. Clearly, the fit with the additional knowledge of and is somewhat better than the one without that additional information, but the difference is not very large. As indicated by Remark 3 the factor in is asymptotically negligible in this case and has not been included in the previous literature. However, as seen in Figure 3 (c) even for a historic sample length of a large bias remains without this factor.

3 DOM versus Wilcoxon sequential change point procedures

In this section, we use the asymptotic results from the previous section to compare the detection delay of the DOM and the Wilcoxon sequential change point procedures. We then confirm these results by means of simulations.

3.1 Theoretical comparison

| N(0,1) | Laplace(0,1) | t(3) | |

|---|---|---|---|

| 0.109 | -0.126 | -0.379 |

In this section we compare the delay as in (2.20) for the two methods. For early changes this corresponds to the expected delay as given in Theorem 6 c), while for late changes we have replaced the random quantities and in by their expected values.

Consider critical values as in the previous section with being equal to the asymptotic -quantile of for early changes and to for late changes.

Some direct calculations show that

| (3.1) |

Clearly, the difference in signal-to-noise ratio as given in Table 1 determines which procedure detects changes quicker and quantifies by how much (relative to how late the change is and how long the historic data set is). This shows that – as expected – the Wilcoxon detects changes faster for more heavy-tailed distributions such as e.g. the and Laplace distribution, while the DOM is preferable for Gaussian data. Futhermore, the factor indicates that the difference is bigger for later changes which is not asymptotically negligible for late changes. Finally, a more detailed calculation shows that the term is in fact always strictly larger than 1 such that a bias in the same direction as indicated by the difference in signal-to-noise ratio occurs and the true difference can be expected to be somewhat larger than indicated by the above expression.

3.2 Comparison based on simulations

In this section, we show simulations indicating the difference in stopping time for the two procedures. In order to have comparable results for different lengths of the historic data set, we standardize both as well as the actually difference of the observed delay time by see (3.1).

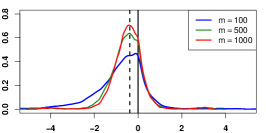

Exemplary estimated densities of the observed difference for i.i.d. data can be found in Figure 4. Positive values indicate that the DOM procedure was faster while negative values indicate that the Wilcoxon procedure was faster, where for better readability there is a vertical solid line at 0. The dashed line indicates the theoretic value as given in Table 1.

For the standard normal distribution, the estimated densities are well concentrated around the theoretical value showing that the DOM procedure detects changes more quickly than the Wilcoxon procedure. Opposite behavior can be observed for the heavy-tailed distribution as predicted by the negative value in Table 1. In all cases the predicted bias in the direction towards the theoretical quantile can be seen. Keeping in mind that the actual delay times in all plots have been divided by , it is clear that the advantage of one procedure over the other is strongly increasing the later the change occurs. Taking a closer look at the values on the -axis indicates that potential gain from using the Wilcoxon kernel in case of a distribution is much larger than the loss in the normal case as predicted by Table 1.

For time series errors as above (i.e. an AR(1) time series with parameter and Gaussian as well as innovations) the general tendency remains true, where the signal-to-noise ratio is no longer given by the above table. Figure 5 shows the corresponding results.

4 Conclusions

In this paper we have derived the limit distribution of the stopping time of a sequential change point procedure based on -statistics. While, previously, only results for changes that occur early in the monitoring period were obtained, we also derive such results for late changes. In the case of late changes there are two fundamental differences to the early change situation:

First, there is a positive probability of a false alarm before the change has actually occured if constant critical values are used, while this probability is asymptotically negligible for early change points. Such constant critical values are used for sequential testing as they allow to control the asymptotic false alarm rate at a fixed level. Consequently, it is not surprising that for later changes there is also a positive probability of such an alarm before the change point occurs. Early changes on the other hand occur by definition asymptotically at the very beginning of the monitoring period such that there has been no time for a false alarm yet.

Secondly, for late changes the stopping time depends on the historic sample, while this dependence is asymptotically negligible for early changes. By conditioning on the relevant quantities of the historic data set we first derive asymptotic results for the stopping time in all situations. From these we obtain unconditional results as well, where for late changes the expected delay time depends on the historic data set while this is not true for early changes. As a contrast the asymptotic variability of the delay time does not depend on the historic data for early or late changes.

As a side product we obtain a better approximation for early changes as compared to previous results by including an additional factor that is necessary for late changes but asymptotically negligible for early changes. Nevertheless, taking it into account results in a much better small sample approximation for early changes as shown in simulations, effectively removing the strong bias that has been reported in previous simulations.

Furthermore, we have derived the stopping times not only for the standard DOM monitoring procedure but also for a more robust Wilcoxon procedure. Based on these results we theoretically compare the stopping times of both methods revealing that the Wilcoxon procedure is significantly quicker for heavy-tailed distributions while only being somewhat slower for the normal distribution, which has also been confirmed in simulations.

In future work, the same methodology can also be applied to compare stopping times for different weight functions and different types of monitoring schemes such as Page-CUSUM (see e.g. [10]), modified MOSUM (see e.g. [23]) or the monitoring scheme of [11]. So far such a comparison was only possible for early changes and has only been done for different weight functions as well as the Page- versus classical CUSUM monitoring scheme.

5 Proofs

5.1 Proofs of Section 2.1

Proof of Theorem 1.

5.2 Proof of Theorem 4

As discussed in Section 2.4 the proof of Theorem 4 is complete as soon as we have proven Proposition 2, which is achieved in this section.

Some of the findings and direct consequences of the derivation of the expected asymptotic delay time and its variability of Section 2.4 are summarized in the following lemma:

Lemma 1.

Proof.

By (2.22) and (2.32), it holds

| (5.1) |

such that by (2.29) it holds

from which (a) follows. By (2.29) it holds

showing the first assertion in b). By (5.1) and (2.30) it follows

Assertion c) is a direct consequence of b).

Finally, by (2.22), (2.28) and (2.31) it holds

| (5.2) |

where in the last line for linear changes was used and for early changes that in this case by (2.29).

Assertion d) follows from this and c) because . The latter converges to infinity for superlinear changes as in that case . It also converges to infinity for sublinear (early) changes as in that case by (5.1) and (2.29). For linear changes it is bounded (from above and below), but so that the assertion also follows.

Lemma 2.

Under the assumptions of Theorem 4 it holds for any , fixed, as

Proof.

Proposition 2.

Proof.

By Assumption 5 (b) resp. (c) it holds for uniformly in

where the positivity holds for large enough by (2.19) and Lemma 1 d) and e). Consequently, uniformly in , it holds for large enough uniformly in

On the one hand, setting and noting that , as well as this implies by Lemma 1 (a) and (b)

On the other hand, by Lemma 1 b) and c) uniformly in for large enough

In the last equation we used the fact, that the last supremum is taken in for large enough, because by Lemma 1 b) and (e) in combination with (2.19) the following representation holds

where the last term is increasing in for large enough.

Putting the above together shows that

As soon as , the factor in front of the last term converges to zero by Lemma 1 a), while by Assumption 5 (c) the stochastic part is bounded in probability, such that the full term is . If that is not the case, then by Assumption 5 (b)

where by the almost sure continuity of a Wiener process, the last term converges to 0 for . Because all the other -terms were uniformly in , this gives the result by Lemma 2, Assumption 5 (b) or (c) in addition to Lemma 1 a).∎

5.3 Proof of Theorem 2

We are now ready to prove Theorem 2.

Proof of Theorem 2.

By Lemma 1 (c) and Assumption 2(i) it holds

With Assumption 5 (a)(i), Lemma 1 (c) and Theorem 3 in [24] we get

showing that for any it holds for

Hence

Because (2.19) is also fulfilled in a -stochastic sense for and by Assumption 6, the assertion follows by an application of the subsequence principle and Theorem 4. ∎

5.4 Proofs of Section 2.3

Proof of Theorem 6.

The arguments leading to (2.29) show that

| (5.3) |

The same assertion holds for as well as , where in the latter case can be replaced by . Additionally, the assertions of Lemma 1 also hold with replaced by where appropriate. Consequently,

| (5.4) |

and assertion a) follows with Corollary 5. Furthermore,

| (5.5) |

By definition it holds

where the last line follows from (5.4), (5.5) and by as in Lemma 1 a).

For late changes it also holds as in Lemma 1 a), for early changes that as can be seen e.g. by (5.3). Consequently,

Finally, by some calculations this yields

proving b). Similarly,

such that

where the last term converges to zero for sublinear changes only as in Lemma 1 a), completing the proof of c). ∎

Proof of Remark 3.

Proof of Remark 4.

If , then by (5.15) in [27] it holds

Then either an analogous assertion holds for with such that

or by (5.15) in [27] it holds , such that

such that for large enough.

Consider now the case, where . Then an analogous assertion also holds with (noting that in the sublinear case eventually, so that the expression is increasing in ), such that by (5.15) in [27] we get that is bounded. Furthermore, by definition

such that

by Lemma 5.4 (i) in [27], completing the proof in this case. ∎

Acknowledgements

This work has been supported by the Research Training Group "Mathematical Complexity Reduction" (314838170, GRK 2297 MathCoRe) and by the Collaborative Research Center "Statistical modeling of nonlinear dynamic processes" (SFB 823, Teilprojekt C1) of the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation).

References

- [1] A. Aue and L. Horváth. Delay time in sequential detection of change. Statistics & Probability Letters, 67(3):221–231, 2004.

- [2] A. Aue, L. Horváth, M. Hušková, and P. Kokoszka. Change-point monitoring in linear models. The Econometrics Journal, 9(3):373–403, 2006.

- [3] A. Aue, L. Horváth, P. Kokoszka, and J. Steinebach. Monitoring shifts in mean: Asymptotic normality of stopping times. Test, 17(3):515–530, 2008.

- [4] A. Aue, L. Horváth, and M. Reimherr. Delay times of sequential procedures for multiple time series regression models. Journal of Econometrics, 149(2):174–190, 2009.

- [5] I. Berkes, E. Gombay, L. Horváth, and P. Kokoszka. Sequential change-point detection in garch (p, q) models. Econometric theory, 20(6):1140–1167, 2004.

- [6] A. Černíková, M. Hušková, Z. Prášková, and J. Steinebach. Delay time in monitoring jump changes in linear models. Statistics, 47(1):1–25, 2013.

- [7] C.-S. Chu, M. Stinchcombe, and H. White. Monitoring structural change. Econometrica, 64:1045–1065, 1996.

- [8] M. Csörgő and L. Horváth. Invariance principles for changepoint problems. Journal of Multivariate Analysis, 27:151–168, 1988.

- [9] H. Dehling, R. Fried, and M. Wendler. Change-point detection under dependence based on two-sample u-statistics. Dawson, Kulik, Ould Haye, Szyszkowicz, Zhao (Eds.) Asymptotic Laws and Methods in Stochastics - A Volume in Honour of Miklos Csörgő, Springer, New York, 2015.

- [10] S. Fremdt. Asymptotic distribution of the delay time in page’s sequential procedure. Journal of Statistical Planning and Inference, 145:74–91, 2014.

- [11] J. Gösmann, T. Kley, and H. Dette. A new approach for open-end sequential change point monitoring. arXiv preprint arXiv:1906.03225, 2019.

- [12] A. Gut and J. Steinebach. Truncated sequential change-point detection based on renewal counting processes. Scandinavian journal of statistics, 29(4):693–719, 2002.

- [13] A. Gut and J. Steinebach. Truncated sequential change-point detection based on renewal counting processes ii. Journal of statistical planning and inference, 139(6):1921–1936, 2009.

- [14] Z. Hlávka, M. Hušková, C. Kirch, and S. G. Meintanis. Monitoring changes in the error distribution of autoregressive models based on fourier methods. Test, 21(4):605–634, 2012.

- [15] Z. Hlávka, M. Hušková, C. Kirch, and S. G. Meintanis. Bootstrap procedures for online monitoring of changes in autoregressive models. Communications in Statistics-Simulation and Computation, 45(7):2471–2490, 2016.

- [16] W. Hoeffding. A class of statistics with asymptotically normal distribution. The Annals of Mathematical Statistics, 19:293–325, 1948.

- [17] L. Horváth, M. Hušková, P. Kokoszka, and J. Steinebach. Monitoring changes in linear models. Journal of Statistical Planning and Inference, 126:225–251, 2004.

- [18] M. Hušková and C. Kirch. Bootstrapping confidence intervals for the change-point of time series. Journal of Time Series Analysis, 29(6):947–972, 2008.

- [19] M. Hušková and A. Koubková. Monitoring jump changes in linear models. Journal of Statistical Research, 39(2):51–70, 2005.

- [20] C. Kirch. Bootstrapping sequential change-point tests. Sequential Analysis, 27(3):330–349, 2008.

- [21] C. Kirch and C. Stoehr. Sequential change point tests based on U-statistics. arXiv preprint arXiv:1912.08580, 2019.

- [22] C. Kirch and J. Tadjuidje Kamgaing. On the use of estimating functions in monitoring time series for change points. Journal of Statistical Planning and Inference, 161:25–49, 2015.

- [23] C. Kirch and S. Weber. Modified sequential change point procedures based on estimating functions. Electronic Journal of Statistics, 12(1):1579–1613, 2018.

- [24] F. Móricz. Moment inequalities and the strong laws of large numbers. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 35:299–314, 1976.

- [25] E. Page. Continuous inspection schemes. Biometrika, 41:100–115, 1954.

- [26] E. Page. Control charts with warning lines. Biometrika, 42:243–257, 1955.

- [27] C. Stoehr. Sequential change point procedures based on U-statistics and the detection of covariance changes in functional data. dissertation, Otto-von-Guericke University Magdeburg, 2019.