Pricing with Variance Gamma Information

Abstract

In the information-based pricing framework of Brody, Hughston & Macrina, the market filtration is generated by an information process defined in such a way that at some fixed time an -measurable random variable is “revealed”. A cash flow is taken to depend on the market factor , and one considers the valuation of a financial asset that delivers at . The value of the asset at any time is the discounted conditional expectation of with respect to , where the expectation is under the risk neutral measure and the interest rate is constant. Then , and for . In the general situation one has a countable number of cash flows, and each cash flow can depend on a vector of market factors, each associated with an information process. In the present work we introduce a new process, which we call the normalized variance-gamma bridge. We show that the normalized variance-gamma bridge and the associated gamma bridge are jointly Markovian. From these processes, together with the specification of a market factor , we construct a so-called variance-gamma information process. The filtration is then taken to be generated by the information process together with the gamma bridge. We show that the resulting extended information process has the Markov property and hence can be used to develop pricing models for a variety of different financial assets, several examples of which are discussed in detail.

Key words: Information-based asset pricing, Lévy processes, gamma processes,

variance gamma processes, Brownian bridges, gamma bridges,

nonlinear filtering.

I Introduction

The theory of information-based asset pricing put forward by Brody, Hughston & Macrina Macrina2006 ; BHM2007 ; BHM2008 ; BHM2008dam is concerned with the determination of the price processes of financial assets from first principles. In particular, the market filtration is constructed explicitly, rather than simply assumed, as it is in traditional approaches. The simplest version of the model is as follows. We fix a probability space . An asset delivers a single random cash flow at some specified time , where time denotes the present. The cash flow is a function of a random variable , which we can think of as a “market factor” that is in some sense revealed at time . In the general situation there will be many factors and many cash flows, but for the present we assume that there is a single factor such that the sole cash flow at time is given by for some Borel function . For simplicity we assume that interest rates are constant and that is the risk neutral measure. We require that should be integrable. Under these assumptions, the value of the asset at time is

| (1) |

where denotes expectation under and is the short rate. Since the single “dividend” is paid at time , the value of the asset at any time is of the form

| (2) |

where is the market filtration. The task now is to model the filtration, and this will be done explicitly.

In traditional financial modelling, the filtration is usually taken to be fixed in advance. For example, in the widely-applied Brownian-motion-driven model for financial markets, the filtration is generated by an -dimensional Brownian motion. A detailed account of the Brownian framework can be found, for example, in Karatzas & Shreve Karatzas Shreve . In the information-based approach, however, we do not assume the filtration to be given a priori. Instead, the filtration is constructed in a way that specifically takes into account the structures of the information flows associated with the cash flows of the various assets under consideration.

In the case of a single asset generating a single cash flow, the idea is that the filtration should contain partial or “noisy” information about the market factor , and hence the impending cash flow, in such a way that is -measurable. This can be achieved by allowing to be generated by a so-called information process with the property that for each such that the random variable is -measurable. Then by constructing specific examples of cádlàg processes having this property, we are able to formulate a variety of specific models. The resulting models are finely tuned to the structures of the assets that they represent, and therefore offer scope for a useful approach to financial risk management. In previous work on information-based asset pricing, where precise definitions can be found that expand upon the ideas summarized above, such models have been constructed using Brownian bridge information processes Macrina2006 ; BHM2007 ; BHM2008 ; Rutkowski Yu ; BDF2009 ; BHM2010 ; BHM2011 ; FHM2012 ; HM2012 ; Menguturk 2013 , gamma bridge information processes BHM2008dam , Lévy random bridge information processes hoyle2010 ; HHM2012 ; HHM2015 ; Menguturk 2018 ; HMM2020 , and Markov bridge information processes MS2019 . In what follows we present a new model for the market filtration, based on the variance-gamma process. The idea is to create a two-parameter family of information processes associated with the random market factor . One of the parameters is the information flow-rate . The other is an intrinsic parameter associated with the variance gamma process. In the limit as tends to infinity, the variance-gamma information process reduces to the type of Brownian bridge information process considered by Brody, Hughston & Macrina Macrina2006 ; BHM2007 ; BHM2008 .

The plan of the paper is as follows. In Section II we recall properties of the gamma process, introducing the so-called scale parameter and shape parameter . A standard gamma subordinator is defined to be a gamma process with . The mean at time of a standard gamma subordinator is . In Theorem 1 we prove that an increase in the shape parameter results in a transfer of weight from the Lévy measure of any interval in the space of jump size to the Lévy measure of any interval such that and . Thus, roughly speaking, an increase in results in an increase in the rate at which small jumps occur relative to the rate at which large jumps occur. This result concerning the interpretation of the shape parameter for a standard gamma subordinator is new as far as we are aware.

In Section III we recall properties of the variance-gamma process and the gamma bridge, and in Definition 1 we introduce a new type of process, which we call a normalized variance-gamma bridge. This process plays an important role in the material that follows. In Lemmas 1 and 2 we work out various properties of the normalized variance-gamma bridge. Then in Theorem 2 we show that the normalized variance-gamma bridge and the associated gamma bridge are jointly Markov, a property that turns out to be crucial in our pricing theory. In Section IV, at Definition 2, we introduce the so-called variance-gamma information process. The information process carries noisy information about the value of a market factor that will be revealed to the market at time , where the noise is represented by the normalized variance-gamma bridge. In equation (58) we present a formula that relates the values of the information process at different times, and by use of that we establish in Theorem 3 that the information process and the associated gamma bridge are jointly Markov.

In Section V, we consider a market where the filtration is generated by a variance gamma information process along with the associated gamma bridge. In Lemma 66 we work out a version of the Bayes formula in the form that we need for asset pricing in the present context. Then in Theorem 4 we present a general formula for the price process of a financial asset that at time pays a single dividend given by a function of the market factor. In particular, the a priori distribution of the market factor can be quite arbitrary, specified by a measure on , and the only requirement being that should be integrable. In Section VI we present a number of examples, based on various choices of the payoff function and the distribution for the market factor, the results being summarized in Propositions 1, 2, 3, and 4. We conclude with comments on calibration, derivatives, and how one determines the trajectory of the information process from market prices.

II Gamma Subordinators

We begin with some remarks about the gamma process. Let us as usual write for the non-negative real numbers. Let and be strictly positive constants. A continuous random variable on a probability space will be said to have a gamma distribution with scale parameter and shape parameter if

| (3) |

where

| (4) |

denotes the standard gamma function for , and we recall the relation . A calculation shows that , and . There exists a two-parameter family of gamma processes of the form on . By a gamma process with scale and shape we mean a Lévy process such that for each the random variable is gamma distributed with

| (5) |

If we write and for the so-called Pochhammer symbol, we find that . It follows that and , where and , or equivalently , and .

The Lévy exponent for such a process is given for by

| (6) |

and for the corresponding Lévy measure we have

| (7) |

One can then check that the Lévy-Khinchine relation

| (8) |

holds for an appropriate choice of (kyprianou2014fluctuations, , Lemma 1.7).

By a standard gamma subordinator we mean a gamma process for which . This implies that and . The standard gamma subordinators thus constitute a one-parameter family of processes labelled by . An interpretation of the parameter is given by the following:

Theorem 1.

Let be a standard gamma subordinator with parameter . Let be the Lévy measure of the interval for . Then for any interval such that and the ratio

| (9) |

is strictly greater than one and strictly increasing as a function of .

Proof.

By the definition of a standard gamma subordinator we have

| (10) |

Let and note that the integrand in the right hand side of (10) is a decreasing function of the variable of integration. This allows one to conclude that

| (11) |

from which it follows that and hence . To show that is strictly increasing as a function of we observe that

| (12) |

where the so-called exponential integral function is defined for by

| (13) |

See reference AS1970 , Section 5.1.1, for properties of the exponential integral. Next, we compute the derivative of , which gives

| (14) |

where

| (15) |

We note that

| (16) |

which shows that the sign of the derivative in (14) is strictly positive if and only if

| (17) |

But clearly

| (18) |

for , which after a change of integration variables and use of (15) implies

| (19) |

which is equivalent to (17), and that completes the proof. ∎

We see therefore that the effect of an increase in the value of is to transfer weight from the Lévy measure of any jump-size interval to any possibly-overlapping smaller-jump-size interval of the same length. The Lévy measure of such an interval is the rate of arrival of jumps for which the jump size lies in that interval.

III Normalized Variance-Gamma Bridge

Let us fix a standard Brownian motion on and an independent standard gamma subordinator with parameter . By a standard variance-gamma process with parameter we mean a time-changed Brownian motion of the form

| (20) |

It is straightforward to check that is itself a Lévy process, with Lévy exponent

| (21) |

Properties of the variance-gamma process, and financial models based on it, have been investigated extensively in Madan 1990 ; Madan Milne 1991 ; Madan Carr Chang 1998 ; Carr Geman Madan Yor 2002 and many other works.

The other object we require going forward is the gamma bridge BHM2008dam ; Emery Yor 2004 ; Yor 2007 . Let be a standard gamma subordinator with parameter . For fixed the process defined by

| (22) |

for and for will be called a standard gamma bridge, with parameter , over the interval . One can check that for the random variable has a beta distribution (BHM2008dam, , pp. 6-9). In particular, one finds that its density is given by

| (23) |

where

| (24) |

It follows then by use of the integral formula

| (25) |

that for all we have

| (26) |

and hence

| (27) |

Accordingly, one has

| (28) |

and therefore

| (29) |

One observes, in particular, that the expectation of does not depend on , whereas the variance of decreases as increases.

Definition 1.

For fixed , the process defined by

| (30) |

for and for will be called a normalized variance gamma bridge.

We proceed to work out various properties of this process. We observe that is conditionally Gaussian, from which it follows that and . Therefore and ; and thus by use of (28) we have

| (31) |

Now, recall Yor 2007 ; Emery Yor 2004 that the gamma process and the associated gamma bridge have the following fundamental independence property. Define

| (32) |

Then, for every it holds that and are independent. In particular and are independent for and . It also holds that and are independent for and . Furthermore, we have:

Lemma 1.

If and then and are independent.

Proof.

We recall that if a random variable is normally distributed with mean and variance then

| (33) |

where is defined by

| (34) |

Since is conditionally Gaussian, by use of the tower property we find that

| (35) |

where the last line follows from the independence of and . ∎

By a straightforward extension of the argument we deduce that if and then and are independent. Further, we have:

Lemma 2.

If and then and are independent.

Proof. We recall that the Brownian bridge defined by

| (36) |

for and for is Gaussian with , , and for . Using the tower property we find that

| (37) |

where in the final step we use (30) along with properties of the Brownian bridge.

A straightforward calculation shows that if and then

| (38) |

With this result at hand we obtain the following:

Theorem 2.

The processes and are jointly Markov.

Proof.

To establish the Markov property it suffices to show that for any bounded measurable function , any , and any , we have

| (39) |

We present the proof for . Thus we need to show that

| (40) |

As a consequence of (38) we have

| (41) |

Therefore, it suffices to show that

| (42) |

Let us write

| (43) |

for the joint density of . Then for the conditional density of and given we have

| (44) |

Thus,

| (45) |

Similarly,

| (46) |

where for the conditional density of and given we have

| (47) |

Note that the conditional probability densities that we introduce in formulae such as those above are “regular” conditional densities (williams1991, , p. 91). We shall show that

| (48) |

Writing

| (49) |

for the joint distribution function, we see that

| (50) |

where the last step follows as a consequence of Lemma 2. Thus we have

| (51) |

where the next to last step follows by virtue of the fact that and are independent for and . Similarly,

| (52) |

and hence

| (53) |

Thus we deduce that

| (54) | |||

| (55) |

and

| (56) |

and the theorem follows. ∎

IV Variance Gamma Information

Fix and let be a normalized variance gamma bridge, as defined by (30). Let be the associated gamma bridge defined by (22). Let be a random variable and assume that , and are independent. We are led to the following:

Definition 2.

By a variance-gamma information process carrying the market factor we mean a process that takes the form

| (57) |

for and for , where is a positive constant.

The market filtration is assumed to be the standard augmented filtration generated jointly by and . A calculation shows that if and then

| (58) |

We are thus led to the following result required for the valuation of assets.

Theorem 3.

The processes and are jointly Markov.

V Information Based Pricing

Now we are in a position to consider the valuation of a financial asset in the setting just discussed. One recalls that is understood to be the risk-neutral measure and that the interest rate is constant. The payoff of the asset at time is taken to be an integrable random variable of the form for some Borel function , where is the information revealed at . The filtration is generated jointly by the variance-gamma information process and the associated gamma bridge . The value of the asset at time is then given by the general expression (2), which on account of Theorem 3 reduces in the present context to

| (63) |

and our goal is to work out this expectation explicitly.

Let us write for the a priori distribution function of . Thus and we have

| (64) |

Occasionally, it will be typographically convenient to write in place of , and similarly for other distribution functions. To proceed, we require the following:

Lemma 3.

Let be a random variable with distribution and let be a continuous random variable with distribution and density . Then for all for which we have

| (65) |

where denotes the conditional distribution , and where

| (66) |

Proof.

For any two random variables and it holds that

| (67) |

Here we have used the fact that for each there exists a Borel measurable function such that . Then for we define

| (68) |

Hence

| (69) |

By symmetry, we have

| (70) |

from which it follows that we have the relation

| (71) |

Moving ahead, let us consider the measure on defined for each by setting

| (72) |

for any . Then is absolutely continuous with respect to . Indeed, suppose that for some . Now, . But if , then , and hence , and therefore . Thus vanishes for any for which vanishes. It follows by the Radon-Nikodym theorem that for each there exists a density such that

| (73) |

Note that is determined uniquely apart from its values on -null sets. Inserting (73) into (71) we obtain

| (74) |

and thus by Fubini’s theorem we have

| (75) |

It follows then that is determined uniquely apart from its values on -null sets, and we have

| (76) |

This relation holds quite generally and is symmetrical between and . Indeed, we have not so far assumed that is a continuous random variable. If is, in fact, a continuous random variable, then its distribution function is absolutely continuous and admits a density . In that case, (76) can be written in the form

| (77) |

from which it follows that for each value of the conditional distribution function is absolutely continuous and admits a density such that

| (79) |

and that concludes the proof. ∎

Armed with Lemma 66, we are in a position to work out the conditional expectation that leads to the asset price, and we obtain the following:

Theorem 4.

The variance-gamma information-based price of a financial asset with payoff at time is given for by

| (80) |

Proof.

To calculate the conditional expectation of , we observe that

| (81) |

by the tower property, where the inner expectation takes the form

| (82) |

Here by Lemma 66 the conditional distribution function is

| (83) |

Therefore, the inner expectation in equation (81) is given by

| (84) |

But the right hand side of (84) depends only on and . It follows immediately that

| (85) |

which translates into equation (80), and that concludes the proof. ∎

VI Examples

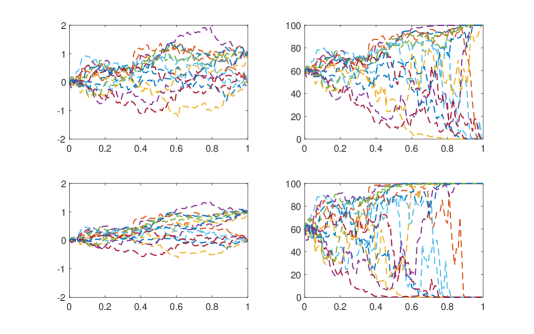

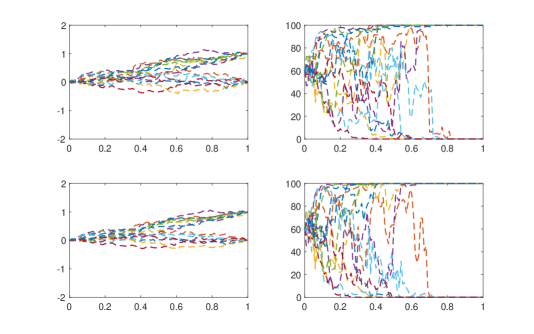

Going forward, we present some examples of variance-gamma information pricing for specific choices of (a) the payoff function and (b) the distribution of the market factor . In the figures, we display sample paths for the information processes and the corresponding prices. These paths are generated as follows. First, we simulate outcomes for the market factor . Second, we simulate paths for the gamma process over the interval and an independent Brownian motion . Third, we evaluate the variance gamma process over the interval by subordinating the Brownian motion with the gamma process, and we evaluate the resulting gamma bridge . Fourth, we use these ingredients to construct sample paths of the information processes, where these processes are given as in Definition 2. Finally, we evaluate the pricing formula in equation (80) for each of the simulated paths and for each time step.

Example 1. We begin with the simplest case, that of a unit-principal credit-risky bond without recovery. We set , with and , where . Thus, we have

| (86) |

where

| (87) |

and denotes the Dirac measure concentrated at the point , and we are led to the following:

Proposition 1.

The variance-gamma information-based price of a unit-principal credit-risky discount bond with no recovery is given by

| (88) |

Now let denote the outcome of chance. By use of equation (57) one can check rather directly that if = 1, then , whereas if = 0, then . More explicitly, we find that

| (89) |

whereas

| (90) |

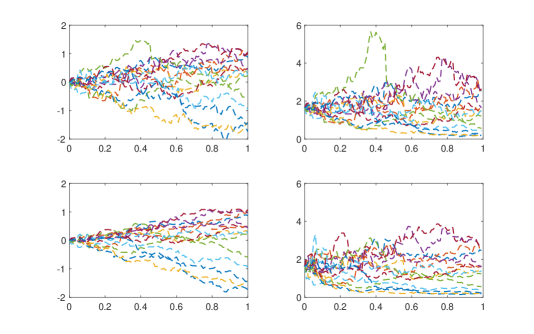

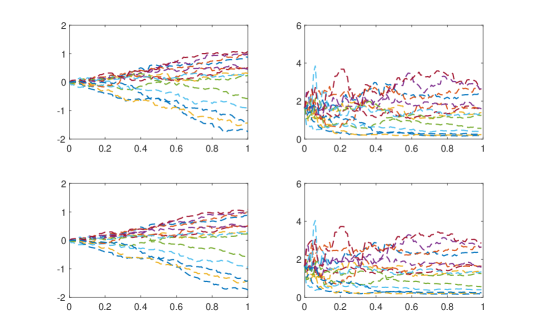

and the claimed limiting behaviour of the asset price follows by inspection. In Figures 1 and 2 we plot sample paths for the information processes and price processes of credit risky bonds for various values of the information flow-rate parameter. One observes that for the information processes diverge, thus distinguishing those bonds that default from those that do not, only towards the end of the relevant time frame; whereas for higher values of the divergence occurs progressively earlier, and one sees a corresponding effect in the price processes. Thus, when the information flow rate is higher, the final outcome of the bond payment is anticipated earlier, and with greater certainty. Similar conclusions hold for the interpretation of Figures 3 and 4.

Example 2. As a somewhat more sophisticated version of the previous example, we consider the case of a defaultable bond with random recovery. We shall work out the case where and the market factor takes the value with probability and is uniformly distributed over the interval with probability , where . Thus, for the probability measure of we have

| (91) |

and for the distribution function we obtain

| (92) |

The bond price at time is then obtained by working out the expression

| (93) |

and it should be evident that one can obtain a closed-form solution. To work this out in detail, it will be convenient to have an expression for the incomplete first moment of a normally-distributed random variable with mean and variance . Thus we set

| (94) |

and for convenience we set

| (95) |

Then we have

| (98) |

Finally, we obtain the following:

Proposition 2.

The variance-gamma information-based price of a defaultable discount bond with a uniformly-distributed fraction of the principal paid on recovery is given by

| (99) |

where

| (100) |

Example 3. Next we consider the case when the payoff of an asset at time is log-normally distributed. This will hold if and . It will be convenient to look at the slightly more general payoff obtained by setting with . If we recall the identity

| (101) |

which holds for and , a calculation gives

| (102) |

where

| (103) |

For , the price is thus given in accordance with Theorem 4 by

| (104) |

Then clearly we have

| (105) |

and a calculation leads to the following:

Proposition 3.

The variance-gamma information-based price of a financial asset with a log-normally distributed payoff such that is given for by

| (106) |

More generally, one can consider the case of a so-called power-payoff derivative for which

| (107) |

where is the payoff of the asset priced above in Proposition 3. See Bouzianis Hughston 2019 for aspects of the theory of power-payoff derivatives. In the present case if we write

| (108) |

for the value of the power-payoff derivative at time , we find that

| (109) |

where

| (110) |

Example 4. Next we consider the case where the payoff is exponentially distributed. We let , so , and take . A calculation shows that

| (111) |

where we set

| (112) |

and

| (113) |

As a consequence we obtain:

Proposition 4.

The variance-gamma information-based price of a financial asset with an exponentially distributed payoff is given by

| (114) |

where and are defined as in Example 2.

VII Conclusion

In the examples considered in the previous section, we have looked at the situation where there is a single market factor , which is revealed at time , and where the single cash flow occurring at depends on the outcome for . The value of a security with that cash flow is determined by the information available at time . Given the Markov property of the extended information process it follows that there exists a function of three variables such that , and we have worked out this expression explicitly for a number of different cases, given in Examples 1-4. The general valuation formula is presented in Theorem 4.

It should be evident that once we have specified the functional dependence of the resulting asset prices on the extended information process, then we can back out values of the information process and the gamma bridge from the price data. So in that sense the process is “visible” in the market, and can be inferred directly, at any time, from a suitable collection of prices. This means, in particular, that given the prices of a certain minimal collection of assets in the market, we can then work out the values of other assets in the market, such as derivatives. In the special case we have just been discussing, there is only a single market factor; but one can see at once that the ideas involved readily extend to the situation where there are multiple market factors and multiple cash flows, as one expects for general securities analysis, following the principles laid out in references BHM2007 ; BHM2008 , where the merits and limitations of modelling in an information-based framework are discussed in some detail.

The potential advantages of working with the variance-gamma information process, rather than the highly tractable but more limited Brownian information process should be evident – these include the additional parametric freedom in the model, with more flexibility in the distributions of returns, but equally important, the scope for jumps. It comes as a pleasant surprise that the resulting formulae are to a large extent analytically explicit, but this is on account of the remarkable properties of the normalized variance-gamma bridge process that we have exploited in our constructions. Keep in mind that in the limit as the parameter goes to infinity our model reduces to that of the Brownian bridge information-based model considered in BHM2007 ; BHM2008 , which in turn contains the standard geometric Brownian motion model (and hence the Black-Scholes option pricing model) as a special case. In the case of a single market factor , the distribution of the random variable can be inferred by observing the current prices of derivatives for which the payoff is of the form

| (115) |

for . The information flow-rate parameter and the shape parameter can then be inferred from option prices. When multiple factors are involved, similar calibration methodologies are applicable.

Acknowledgements.

The authors wish to thank G. Bouzianis and J. M. Pedraza-Ramírez for useful discussions. LSB acknowledges support from (a) Oriel College, Oxford, (b) the Mathematical Institute, Oxford, (c) Consejo Nacional de Ciencia y Tenconología (CONACyT), Ciudad de México, and (d) LMAX Exchange, London. We are grateful to the anonymous referees for a number of helpful comments and suggestions.References

-

(1)

Abramowitz, M. & Stegun, I. A., eds. (1972) Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. United State Department of Commerce, National Bureau of Standards, Applied Mathematics Series 55.

- (2) Bouzianis, G. & Hughston, L. P. (2019) Determination of the Lévy Exponent in Asset Pricing Models. International Journal of Theoretical and Applied Finance 22 (1), 1950008.

- (3) Brody, D. C., Hughston, L. P. & Macrina, A. (2007) Beyond Hazard Rates: a New Framework for Credit-Risk Modelling. In Advances in Mathematical Finance (M. C. Fu, R. A. Jarrow, J.-Y. J. Yen & R. J. Elliot, eds.) Basel: Birkhäuser.

- (4) Brody, D. C., Hughston, L. P. & Macrina, A. (2008a) Information-Based Asset Pricing. International Journal of Theoretical and Applied Finance 11 (1), 107-142b.

- (5) Brody, D. C., Hughston, L. P. & Macrina, A. (2008b) Dam Rain and Cumulative Gain. Proceeding of the Royal Society A 464, 1801-1822.

- (6) Brody, D. C., Davis, M. H. A., Friedman, R. L. & Hughston, L. P. (2009) Informed Traders. Proceedings of the Royal Society A 465, 1103-1122.

- (7) Brody, D. C., Hughston, L. P. & Macrina, A. (2010) Credit Risk, Market Sentiment and Randomly-Timed Default. In Stochastic Analysis in 2010 (D. Crisan, ed.) Berlin: Springer-Verlag.

- (8) Brody, D. C., Hughston, L. P. & Macrina, A. (2011) Modelling Information Flows in Financial Markets. In Advanced Mathematical Methods for Finance (G. Di Nunno & B. Øksendal, eds.) Berlin: Springer-Verlag.

- (9) Carr, P., Geman, H., Madan, D. B. & Yor, M. (2002) The Fine Structure of Asset Returns: an Empirical Investigation. Journal of Business 75 (2), 305-332.

- (10) Émery, M. & Yor, M. (2004) A Parallel between Brownian Bridges and Gamma Bridges. Publications of the Research Institute for Mathematical Sciences, Kyoto University 40, 669-688.

- (11) Filipović, D., Hughston, L. P. & Macrina, A. (2012) Conditional Density Models for Asset Pricing. International Journal of Theoretical and Applied Finance 15 (1), 1250002.

- (12) Hoyle, E. (2010) Information-Based Models for Finance and Insurance. PhD Thesis, Imperial College London.

- (13) Hoyle, E., Hughston, L. P. & Macrina, A. (2011) Lévy Random Bridges and the Modelling of Financial Information. Stochastic Processes and their Applications 121, 856-884.

- (14) Hoyle, E., Hughston, L. P. & Macrina, A. (2015) Stable-1/2 Bridges and Insurance. In Advances in Mathematics of Finance (A. Palczewski & L. Stettner, eds.) Banach Center Publications 104, 95-120. Warsaw: Polish Academy of Sciences.

- (15) Hoyle, E., Macrina, A. & Mengütürk, L. A. (2020) Modulated Information Flows in Financial Markets. International Journal of Theoretical and Applied Finance 23 (4), 2050026.

- (16) Hughston, L. P. & Macrina, A. (2012) Pricing Fxed-Income Securities in an Information-Based Famework. Applied Mathematical Finance 19 (4), 361-379.

- (17) Karatzas, I. & Shreve, S. E. (1998) Methods of Mathematical Finance. New York: Springer-Verlag.

- (18) Kyprianou, A. E. (2014) Fluctuations of Lévy Processes with Applications, second edition. Berlin: Springer-Verlag.

- (19) Macrina, A. (2006) An Information-based Framework for Asset Pricing: X-factor Theory and its Applications. PhD Thesis, King’s College London.

- (20) Macrina, A. & Sekine, J. (2019) Stochastic Modelling with Randomized Markov Bridges. Stochastics 19, 1-27.

- (21) Madan, D. & Seneta, E. (1990) The Variance Gamma (VG) Model for Share Market Returns. Journal of Business 63, 511-524.

- (22) Madan, D. & Milne, F. (1991) Option Pricing with VG Martingale Components. Mathematical Finance 1 (4), 39-55.

- (23) Madan, D., Carr, P. & Chang, E. C. (1998) The Variance Gamma Process and Option Pricing. European Finance Review 2, 79-105.

- (24) Mengütürk, L. A. (2013) Information-Based Jumps, Asymmetry and Dependence in Financial Modelling. PhD Thesis, Imperial College London.

- (25) Mengütürk, L. A. (2018) Gaussian Random Bridges and a Geometric Model for Information Equilibrium. Physica A 494, 465-483.

- (26) Rutkowski, R. & Yu, N. (2007) An Extension of the Brody-Hughston-Macrina Approach to Modeling of Defaultable Bonds. International Journal of Theoretical and Applied Finance 10 (3), 557-589b.

- (27) Williams, D. (1991) Probability with Martingales. Cambridge University Press.

- (28) Yor, M. (2007) Some Remarkable Properties of Gamma Processes. In Advances in Mathematical Finance (M. C. Fu, R. A. Jarrow, J.-Y. J. Yen & R. J. Elliot, eds.) Basel: Birkhäuser.

- (2) Bouzianis, G. & Hughston, L. P. (2019) Determination of the Lévy Exponent in Asset Pricing Models. International Journal of Theoretical and Applied Finance 22 (1), 1950008.