Solving Non-Markovian Stochastic Control Problems driven by Wiener Functionals

Abstract.

In this article, we present a general methodology for stochastic control problems driven by the Brownian motion filtration including non-Markovian and non-semimartingale state processes controlled by mutually singular measures. The main result of this paper is the development of a numerical scheme for computing near-optimal controls associated with controlled Wiener functionals via a finite-dimensional approximation procedure. The theory does not require functional differentiability assumptions on the value process and ellipticity conditions on the diffusion components. Explicit rates of convergence are provided under rather weak conditions for distinct types of non-Markovian and non-semimartingale states. The analysis is carried out on suitable finite dimensional spaces and it is based on the weak differential structure introduced by [40, 41] jointly with measurable selection arguments. The theory is applied to stochastic control problems based on path-dependent SDEs and rough stochastic volatility models, where both drift and possibly degenerated diffusion components are controlled. Optimal control of drifts for nonlinear path-dependent SDEs driven by fractional Brownian motion with exponent is also discussed. Finally, we present a simple numerical example to illustrate the method.

Key words and phrases:

Stochastic Optimal Control, Stochastic Analysis1991 Mathematics Subject Classification:

Primary: 93E20; Secondary: 60H301. Introduction

Let be the set of continuous functions from to , let be a Borel functional, let be a fixed filtration and let be a family of admissible -adapted controls defined over . The goal of this paper is to develop a numerical scheme to solve a generic stochastic optimal control problem of the form

| (1.1) |

where is a given family of -adapted controlled continuous processes. A common approach to such generic control problem (see e.g [14, 20]) is to consider for each control , the value process given by

| (1.2) |

Two fundamental questions in stochastic control theory rely on sound characterizations of value processes and the development of concrete methods to produce either exact optimal controls (when exists)

or near-optimal controls (see e.g [57]) which realize

| (1.3) |

for an arbitrary error bound . Exact optimal controls may fail to exist due to e.g lack of convexity, moreover they are very sensitive to perturbations and numerical rounding. In this context, the standard approach is to consider near-optimal controls which exist under minimal hypotheses and are sufficient in most applications.

Two major tools for studying stochastic controlled systems are Pontryagin’s maximum principle and Bellman’s dynamic programming. While these two methods are known to be very efficient for establishing some key properties (e.g existence of optimal controls, smoothness of the value functional, sufficiency of subclasses of controls, etc), the problem of solving explicitly or numerically a given stochastic control problem remains a critical issue in the field of control theory. Indeed, except for a very few specific cases, the determination of an optimal control (either exact or near) is a highly nontrivial problem to tackle. The present article presents a systematic method to compute and characterize realizing (1.3) for a given stochastic control problem (1.2) driven by a generic controlled process.

In the Markovian case, a classical approach in solving stochastic control problems is given by the dynamic programming principle based on Hamilton-Jacobi-Bellman (HJB) equations. One popular approach is to employ verification arguments to check if a given solution of the HJB equation coincides with the value function at hand, and obtain as a byproduct the optimal control. Discretization methods also play an important role towards the resolution of the control problem. In this direction, several techniques based on Markov chain discretization schemes [37], Krylov’s regularization and shaking coefficient techniques (see e.g [35, 36]) and Barles-Souganidis-type monotone schemes [2] have been successfully implemented. We also refer the more recent probabilistic techniques on fully non-linear PDEs given by Fahim, Touzi and Warin [21] and the randomization approach of Kharroubi, Langrené and Pham [32, 33, 34].

Beyond the Markovian context, the value process (1.2) cannot be reduced to a deterministic PDE and the control problem (1.1) is much more delicate. Nutz [45] employs techniques from quasi-sure analysis to characterize one version of the value process as the solution of a second order backward stochastic differential equation (2BSDE) (see [53]) under a non-degeneracy condition on the diffusion component of a controlled non-Markovian stochastic differential equation driven by Brownian motion (henceforth abbreviated by CNM-SDE-BM). Nutz and Van Handel [44] derive a dynamic programming principle in the context of model uncertainty and nonlinear expectations. Inspired by the work [32], under the weak formulation of the control problem, Fuhrman and Pham [23] show a value process can be reformulated under a family of dominated measures on an enlarged filtered probability space where the CNM-SDE-BM might be degenerated. It is worth to mention that under a nondegeneracy condition on diffusion components of CNM-SDEs-BM, (1.2) can also be viewed as a fully nonlinear path-dependent PDE in the sense of [19] via its relation with 2BSDEs (see section 4.3 in [19]). In this direction, Possamaï, Tan and Zhou [48] derived a dynamic programming principle for a stochastic control problem w.r.t a class of nonlinear kernels. They obtained a well-posedness result for general 2BSDEs and established a link with path-dependent PDEs in possibly degenerated cases. We also drive attention to Qiu [50] who characterizes (1.2) driven by a CNM-SDE-BM as a solution of a suitable HJB-type equation and uniqueness is established under a non-degeneracy condition on the diffusion components. Under strong a priori functional differentiability conditions (in the sense of [18, 12]) imposed on (1.2), one can apply functional Itô’s formula to arrive at verification-type theorems. In this direction, we refer to e.g. Cont [13] and Saporito [52].

Discrete-type schemes for the optimal value (1.1) driven by CNM-SDEs-BM were studied in the context of G-expectations by Dolinsky [16] and also by Zhang and Zhuo [55], Ren and Tan [51] and Tan [54]. In [55, 51], the authors provide monotone schemes in the spirit of Barles-Souganidis for fully nonlinear path-dependent PDEs in the sense of [19] and hence one may apply their results for the study of (1.1). Under elipticity conditions, by employing weak convergence methods in the spirit of Kushner and Depuis, [54] provides a discretization method for the optimal value (1.1). Convergence rates are available only under strong regularity conditions on the value process (1.2) (see [55]) or in the state independent case [16, 54].

1.1. Main setup and contributions

The main contribution of this paper is the development of a new numerical scheme for computing near optimal controls of stochastic systems adapted to the Brownian motion filtration and parameterized by possibly mutually singular measures. In particular, we present a discrete-type approximation for a large class of nonlinear expectations driven by possibly non-Markovian and / or non-semimartingale controlled states. More importantly, our approximation is equipped with a suitable dynamic programming equation which allows us to compute near optimal controls much beyond the class of linear-quadratic optimal control problems. For instance, nonlinear controlled path-dependent degenerated SDEs driven by a possibly non-smooth Gaussian transformation of the Brownian motion is a typical application of our methodology. Under a rather weak -type regularity condition imposed on controlled states, this article develops a concrete methodology to solve numerically a given stochastic control problem of the form (1.1). None differentiability condition on the value process (1.2) is required. Moreover, the scheme is implementable using e.g regression Monte-Carlo techniques

The methodology is based on a weak version of functional Itô calculus developed by Leão, Ohashi and Simas [41] and inspired by Leão and Ohashi [40]. A given Brownian motion structure is discretized which gives rise to differential operators acting on piecewise constant processes adapted to a jumping filtration in the sense of [31] and generated by what we call a discrete-type skeleton (see Definition 3.1). For a given controlled state process , we construct a controlled imbedded discrete structure (see Definition 3.2 in Section 3) for the value process (1.2). This is a non-linear version of the imbedded discrete structures introduced by [41] and it can be interpreted as a discrete version of (1.2).

By using measurable selection arguments, we aggregate the controlled imbedded discrete structure into a single finite sequence of upper semianalytic value functions . Here, is the -fold cartesian product of , where is the action space, is suitable finite-dimensional space which accommodates the dynamics of the structure and is a suitable number of steps to recover (1.1) over the entire period as the discretization level goes to infinity. This procedure allows us to derive a dynamic programming equation over steps which is the building block to solve stochastic control problems much beyond the classical Markovian states, traditionally treated by Markov chain approximations and PDE methods. The dynamic programming principle presented in Section 5.1 allows us to select near optimal controls for (1.3) solely based on the discrete skeleton . We refer the reader to Section 7 for a simple numerical example which illustrates how one can make use of our methodology in a simple stochastic control problem.

The connection between the dynamic programming principle based on and the original control problem (1.1) is made via a strong robustness property found in a wide class of Wiener functionals as described by [41] in the linear expectation case. In this work, we take one step ahead towards the fully non-linear case. A first elementary consequence of our discretization scheme (see Proposition 4.2) is the fact that an arbitrary nonlinear expectation (see e.g [47]) driven by a strongly controlled Wiener functional associated with a controlled imbedded discrete structure (see Definition 3.3 in Section 3) is represented by

over a suitable set of stepwise constant -adapted processes. The concept of strongly controlled Wiener functional covers a wide class of stochastic systems which cannot be reduced to Markovian states without adding infinitely many degrees of freedom (see Sections 1.2 and 6).

The main results of this article, Theorems 5.1 and 5.2, state that for the class of strongly controlled Wiener functionals, we construct a dynamic programming algorithm for the discrete time analog of the nonlinear expectation (1.1) and for the corresponding (near) optimal control based on the skeleton . Furthermore, for a given error bound , the rate of convergence of our numerical scheme is proportional to

| (1.4) |

and

| (1.5) |

as . The rate in (1.4) and (1.5) depends on the degree of continuity of w.r.t a structure (see (3.10)) combined with large deviation principles related to a family of hitting times . The rate in (1.4) and (1.5) depends on an equiconvergence property (Theorem 11.1) for Brownian martingales w.r.t the structure and it is independent of the controlled state.

In contrast to previous works, we remark that our approach does not rely on a given representation of the value process (1.2) in terms of path-dependent PDE or 2BSDE. We develop a fully pathwise structure which allows us to make use the classical theory of analytic sets to construct near-optimal controls appearing in (1.4) by means of a list of analytically measurable functions which can be calculated from (5.9) or (5.12) for a given error bound . By composing those functions with the skeleton , we are able to compute near optimal controls realizing (1.4). More importantly, the whole dynamics on can be simulated by means of the first time Brownian motion hits and Bernoulli random variables. The regularity conditions of the theory boils down to a mild -type continuity hypothesis on the controlled state (see Assumption (B1)) combined with a Hölder modulus of continuity on the payoff functional (see Assumption (A1)).

In contrast to the framework of one fixed probability measure in [41], in the present context it is essential to aggregrate a given structure into a single deterministic finite sequence of maps due to a possible appearance of mutually singular measures induced by as varies over the set of controls . Moreover, we mention it is possible to prove a differential-type representation result for (1.2) by extending the framework of [41] to controlling probabilities via measurable selection arguments combined with Theorem 11.1. Since it is not our purpose to focus on the representation of (1.2), we leave this construction to a future work.

1.2. Examples

As a test of the relevance of the theory, we show that our methodology can be applied to controlled Wiener functionals of the form

where the non-anticipative functionals admit Lipschitz regularity w.r.t. control variables which in turn implies -Lipschitz regularity of w.r.t control processes (Assumption (B1)). We investigate three typical examples illustrating distinct types of path-dependency which fit into the theory developed in this paper:

| (1.6) |

| (1.7) |

and

| (1.8) |

where is a fractional Brownian motion (henceforth abbreviated by FBM) with exponent . In case of (1.6), the driving state is a CNM-SDE-BM and the lack of Markov property is due to non-anticipative functionals and which may depend on the whole path of . In this case, the controlled state satisfies a pseudo-Markov property in the sense of [11]. Case (1.7) illustrates a fully non-Markovian case: the controlled state is driven by a path-dependent nonlinear drift and by a very singular transformation of the Brownian motion into a non-Markovian and non-semimartingale noise. In particular, there is no probability measure on the path space such that the controlled state in (1.7) is a semimartingale. Case (1.8) has been devoted to a considerable attention in recent years in the context of rough stochastic volatility models when . In this direction, see e.g [1] and other references therein.

The methodology applied to (1.6) extends previous numerical schemes [54] by allowing to be degenerated, be unbounded and the convergence rate of the scheme envelops the state dependent case. In particular, the convergence rate is obtained without smoothness conditions on the value process (see e.g [51, 55]). We also highlight that the convergence rate given in Theorem 6.1 is faster than Th 2.8 in [54] because in this case we are able to take and . In other words, the rate associated to the non-Markovian fully nonlinear case is comparable to the Markovian semilinear case (when there is no control on the volatility part) previously treated by BSDE methods in the works [6, 56].

As far as the case (1.7) is concerned, an explicit solution of a generic linear-quadratic optimal control problem driven by Gaussian processes has been obtained by Duncan and Pasik-Duncan [17]. Infinite-dimensional lifts (and their approximations) of linear quadratic control problems driven by non-Markovian stochastic Volterra-type equations have been studied by Jaber, Miller and Pham [29, 30]. Despite many characterization of value functions, existence theorems for optimal controls (see e.g [5, 26, 9, 28, 39, 15]) and some numerical methods applied to the linear-quadratic case ([17, 29, 30]), to our best knowledge, this paper is the first to present a numerical scheme for nonlinear stochastic control problems driven by FBM.

Recently, Bayer, Friz, Gassiat, Martin and Stemper [1] presents discrete-type approximations in the sense of Hairer’s theory of regularity structures for rough stochastic volatility models and their European call options prices, i.e., classical linear expectation case. In the present paper, we treat the nonlinear case. At this point, it is important to stress our approximation does not need any type of renormalization procedure because our structure is imbedded into the Brownian motion world which allows us to get rid off divergent Stratonovich’s correction terms. See Section 6.3 and [46] for details.

Organization of Paper. The remainder of this article is organized as follows. Section 2 presents some notations and summarizes the standing assumptions of this article. Section 3 presents the basic discretization of the Brownian structure. Section 4 presents the discrete version of the value process. Section 5 presents the main results of this paper and a discussion of the dynamic programming algorithm associated with the discrete analog of the nonlinear expectation. Section 6 presents the controlled states (1.6), (1.7) and (1.8) as strongly controlled Wiener functionals. Section 7 presents a simple numerical example which illustrates the method. The Appendix sections 8 and 9 are devoted to the proofs of some technical results. Section 10 presents the proofs related to the measurable selection theorem and dynamic programming. Section 11 presents the proof of Theorems 5.1 and 5.2.

2. Controlled stochastic processes

Throughout this article, we are going to fix a filtered probability space equipped with a -dimensional Brownian motion where is the usual -augmentation of the filtration generated by under a fixed probability measure . For a pair of finite -stopping times , we denote

and The action space is the compact

for a given fixed . In order to set up the basic structure of our control problem, we first need to define the class of admissible control processes: for each pair of a.s finite -stopping times such that , we denote 111Whenever necessary, we can always extend a given by setting on the complement of a stochastic set .

| (2.1) |

For such family of processes, we observe they satisfy the following properties:

-

•

Restriction: for a.s.

-

•

Concatenation: If and for , then , where

(2.2) -

•

Finite Mixing: For every and , we have

Let be the Banach space of all -adapted finite-dimensional processes such that

for , where is an Euclidean norm and is a fixed terminal time. Let us denote

We also define as the space of all -adapted càdlàg processes such that

for .

Definition 2.1.

A continuous controlled Wiener functional is a map for some , such that for each and , depends on the control only on and has continuous paths for each .

In the sequel, we denote and we equip this linear space with the uniform convergence on . We now present the two standing assumptions of this article.

Assumption (A1): The payoff satisfies the following regularity assumption: There exists and a constant such that

for every .

Assumption (B1): There exists a constant such that

| (2.3) |

for every .

Remark 2.1.

Path-dependent controlled SDEs with Lipschitz coefficients are typical examples of controlled Wiener functionals satisfying Assumption (B1). See Remark 6.1

Remark 2.2.

Even though we are only interested in controlled Wiener functionals with continuous paths, we are forced to assume the payoff functional is defined on the space of càdlàg paths due to a discretization procedure. However, this is not a strong assumption since most of the functionals of interest admits extensions from to preserving Assumption (A1).

From now on, we are going to fix a controlled Wiener functional . For a given functional , we denote

| (2.4) |

and

| (2.5) |

where a.s. We stress the process has to be viewed backwards for each control . Throughout this paper, in order to keep notation simple, we omit the dependence of the value process in (2.5) on the controlled Wiener functional and the payoff , so we write meaning as a map .

Since we are not assuming that is the trivial -algebra, we cannot say that is deterministic. However, the finite-mixing property on the class of admissible controls implies that has the lattice property (see e.g Def 1.1.2 [38]) for every and . In this case, it is known

Remark 2.3.

One can easily check that under Assumptions (A1-B1), for any , depends only on the control restricted to the interval . Moreover, is a continuous controlled Wiener functional in the sense of Definition 2.1 and is an -supermartingale, in the sense that is an -supermartingale for each .

Definition 2.2.

We say that is an -optimal control if

| (2.6) |

In case, , we say that realizing (2.6) is an exact optimal control.

3. Discrete-type skeleton for the Brownian motion and controlled imbedded discrete structures

In this section, we introduce what we call a controlled imbedded discrete structure which is a natural extension of the approximation models presented in Leão, Ohashi and Simas [41]. Our philosophy is to view a controlled Wiener functional as a family of simplified models one has to build in order to extract the relevant information for the obtention of a concrete description of value processes and the construction of their associated (near or exact) optimal controls.

3.1. The underlying discrete skeleton

The discretization procedure will be based on a class of pure jump processes driven by suitable waiting times which describe the local behavior of the Brownian motion. We briefly recall the basic properties of this skeleton. For more details, we refer the reader to the work [41]. We start by constructing a sequence of hitting times which will be the basis for our discretization scheme. For a given sequence such that as , we set and

| (3.1) |

and corresponds to the maximum norm on . This implies

| (3.2) |

where

Then, we define by

for integers .

The multi-dimensional filtration generated by is naturally characterized as follows. Let be the filtration generated by . We observe

where for each . Let be the completion of and let be the -algebra generated by all -null sets in . We denote , where is the usual -augmentation (based on ) satisfying the usual conditions.

Definition 3.1.

The structure is called a discrete-type skeleton for the Brownian motion.

By the strong Markov property, we observe that

-

(1)

The jumps are independent and identically distributed (iid).

-

(2)

The waiting times are iid random variables in .

-

(3)

The families and are independent.

Moreover, it is immediate that is a square-integrable -martingale for each .

Remark 3.1.

The skeleton given in Definition 3.1 slightly differs from Def 2.1 in [41] and [42] if . Indeed, the choice of the hitting times differs from [41]. In the present work, we adopt (3.1) rather than

for . This allows us to reduce the complexity of the discretization scheme and, in contrast to Th 2.1 in [4], the transition probabilities are homogeneous in time (see Proposition 9.1). Since is a -dimensional stepwise constant martingale process satisfying properties (1), (2) and (3) above, then the basic underlying differential structure presented in [41] is still preserved. This article does not focus on representation results for controlled Wiener functionals. Hence the limiting differential structure will not be investigated and we leave this construction to a future work.

Let us start to introduce a subclass . For , let be the set of -predictable processes of the form

| (3.3) |

where for each , is an -valued -measurable random variable. To keep notation simple, we use the shorthand notations

| (3.4) |

where is the set of all controls of the form

| (3.5) |

where is an -valued -measurable random variable for every for an integer .

We also use a shorthand notation for as follows: with a slight abuse of notation, for and with , we write

| (3.6) |

This notation is consistent because only depends on the list of variables whenever and are controls of the form (3.3) for .

Let us now introduce the analogous concept of controlled Wiener functional but based on the filtration . For this purpose, we need to introduce some further notations. Let us define

| (3.7) |

where is the smallest integer greater or equal to and

| (3.8) |

where is an iid sequence of random variables with distribution for a real-valued standard Brownian motion . From Lemma 8.2, for each , we know that

as , for each and .

Remark 3.2.

The number should be interpretted as the number of necessary steps to compute a given nonlinear expectation (driven by a controlled Wiener functional) via a discrete-type dynamic programming equation. One can easily check that (see e.g [7]) , where is the density of in (3.8). By Th 5 in [24], we get a lower bound

Therefore, for given and , the number of periods grows no faster than the dimension of the driving Brownian motion.

Let be the set of all stepwise constant -optional processes of the form

where is -measurable for every and .

Let us now present two concepts which will play a key role in this work.

Definition 3.2.

A controlled imbedded discrete structure consists of the following objects: a discrete-type skeleton and a map from to such that

| (3.9) |

for each integer .

Definition 3.3.

A strongly controlled Wiener functional is a pair , where is a controlled Wiener functional and is a controlled imbedded discrete structure such that is uniformly integrable for each and

| (3.10) |

for .

The concepts of controlled imbedded discrete structures and strongly controlled Wiener functionals are nonlinear versions of the structures analyzed in [41]. The typical example we have in mind of a strongly controlled Wiener functional is a controlled state which drives a stochastic control problem.

4. The controlled imbedded discrete structure for the value process

In this section, we are going to describe the canonical controlled imbedded discrete structure associated with an arbitrary value process

where the payoff satisfies Assumption A1 and is an arbitrary controlled Wiener functional satisfying Assumption B1. Throughout this section, we are going to fix a controlled imbedded discrete structure

| (4.1) |

and we set

| (4.2) |

for . We assume is uniformly integrable for each . We then define

| (4.3) |

with boundary conditions

This naturally defines the map with jumps for . One should notice that only depends on so it is natural to write

Similar to the value process , we can write a dynamic programming principle for where the Brownian filtration is replaced by the discrete-time filtration .

Lemma 4.1.

Let . For each and in , there exists such that

for every . Therefore, for each

for and .

Proof.

For , let . Choose and apply the finite mixing property to exchange the esssup into the conditional expectation (see e.g Prop 1.1.4 in [38]) to conclude the proof. ∎

Proposition 4.1.

For each , the discrete-time value process satisfies

| (4.4) |

On the other hand, if a class of processes satisfies the dynamic programming equation (4.4) for every , then coincides with for every and for every .

Proof.

Fix . By using Lemma 4.1 and the identity

a.s for each , the proof is straightforward, so we omit the details. ∎

4.1. Convergence of optimal values

Throughout this section, we assume that is a strongly controlled Wiener functional. In this section, we aim to prove the controlled imbedded discrete structure given by (4.3) yields a solution of the control problem (1.1) for large enough. In the sequel, we present a density result which will play a key role in this article: we want to approximate any control by means of controls in the sets .

Lemma 4.2.

The subset is dense in w.r.t the -strong topology.

Proof.

We just need to apply Lemma 3.3 in [40] and routine density arguments based on simple processes. ∎

A simple combination of Lemma 4.2, Assumptions A1 and B1 yields the following nice characterization.

Lemma 4.3.

Under Assumptions A1 and B1, we have

We are now able to state two simple consequences.

Proposition 4.2.

Let be the value process associated with a payoff and a strongly controlled Wiener functional satisfying Assumption A1 and B1, respectively. Let be the value process (4.3) associated with . Then,

| (4.5) |

Proof.

Remark 4.1.

By Assumptions A1-B1,

| (4.7) |

for any dense subset of w.r.t -topology.

A simple but important consequence of Proposition 4.2 is the next result which states that optimal controls (either exacts or near) computed for the approximating problem

| (4.8) |

are near optimal controls for the control problem .

Proposition 4.3.

Assume the pair satisfies Assumptions A1-B1 and is a strongly controlled Wiener functional. For a given , let be a near optimal control associated with the control problem (4.8) written on . Then, is a near optimal control for the Brownian motion driving stochastic control problem, i.e., for a given

| (4.9) |

for every sufficiently large.

Proof.

Let us fix and a positive integer . By definition of , we have

| (4.10) |

Proposition 4.2 yields

| (4.11) |

for every sufficiently large. By using assumptions (3.10) and Assumption (A1), we also know there exists a positive constant such that

In the next section, we provide a discrete-type dynamic programming equation associated with (4.8) and the corresponding optimal control.

5. The Dynamic Programming Algorithm and Main Results

In this section, we present the main results of this paper: we describe the dynamic programming for the discrete time analog (4.8) of the nonlinear expectation (4.7) and for the corresponding optimal control based on the skeleton .

For a given choice of discrete-type skeleton , we will construct controlled functionals written on this structure. Before we proceed, it is important to point out that there exists a pathwise description of the dynamics generated by . Let us define

and

The -fold Cartesian product of is denoted by and a generic element of will be denoted by

| (5.1) |

where for . Let us define , where

for . Let us define

| (5.2) |

One should notice that

where is the Borel -algebra generated by .

The whole dynamics will take place in the history space . We denote and as the -fold Cartesian product of and , respectively. The elements of will be denoted by

| (5.3) |

where , and .

For a given admissible control , we define as follows

| (5.4) |

for . We identify as a constant (in the action space ) which does not necessarily depend on the control . By definition, we obtain that is an -measurable, for every and .

By applying properties (1), (2) and (3), the law of the system will evolve according to the following probability measure defined by

for , where is the probability measure defined by

5.1. Dynamic Programming

The dynamic programming associated with will be fully based on Proposition 4.1 but it involves delicate measurability issues. The first step is to aggregate the map into a single list of upper semi-analytic functions . We do this by using classical theory of analytic sets. The technical proofs of all unexplained statements are given in the Appendix 10.

At first, we observe that for a given control and a given , we can easily construct a Borel function such that and

| (5.6) |

for a.a and for every . In the sequel, in order to keep notation simple, we set .

We set and

where for .

The function

| (5.7) |

is called the optimal state-action value function and is the value functional. One can show (see Propositions 10.1 and 10.2),

for each control . Moreover, for every , there exists a measurable function such that

for every , where . In particular, if , for , then for every and , the control defined by

| (5.8) |

realizes

for every . The above construction suggests the following definition.

Definition 5.1.

A pair is admissible w.r.t the control problem (4.8) if for every and .

From dynamic programming principle (see Proposition 10.3), for any admissible pair w.r.t the control problem (4.8), the control

| (5.9) |

constructed via (5.8) (with ) realizes

Remark 5.1.

If the map is upper semicontinuous for , then we can apply the Borel measurable selection theorem (see, Prop 7.33 in [3]) to conclude that the function is also upper semicontinuous for each . Moreover, there exists a Borel measurable function such that

for every , where . If then, for a given , the list of controls defined by

| (5.10) |

realizes

for every . In particular, if is continuous, then given by

| (5.11) |

is a measurable function, where the maximum in the above right-hand side is taken w.r.t the lexicographical order. See e.g page 4 in [16]. Under these conditions, the control

5.2. Main Results: Convergence of the numerical scheme

For integers , let () be the set of all -predictable processes of the form

| (5.13) |

where for each , is an -valued -measurable random variable. Of course, for each , for every . We denote similar to (3.5) but the jumps of the controls are -measurable for .

We are now in position to state the main results of this article.

Theorem 5.1.

Let be the value process associated with a payoff satisfying Assumption A1 with -Hölder regularity and a strongly controlled Wiener functional satisfying Assumption B1. Let be the value process (4.3) associated with a controlled imbedded discrete structure . Then,

| (5.14) |

for each control . Moreover, if

| (5.15) |

then, for a given , we have

| (5.16) |

For a given error bound , we can provide the rate of convergence of the payoff associated with the optimal controls calculated via (5.14) (see (5.9), (5.12)).

Theorem 5.2.

Assume the pair satisfies Assumptions (A1-B1) and is a strongly controlled Wiener functional associated with a controlled imbedded discrete structure satisfying (5.15). Assume the pair is admissible in the sense of Definition 5.1. For a given error bound and , let be an -optimal control associated with the control problem (4.8) driven by and which can be calculated via (5.14). Then, is a near optimal control for the stochastic control problem (2.6). More precisely, if is the order of convergence given in (5.15), then for and , we have

| (5.17) |

Remark 5.2.

Condition (5.15) is stronger than (3.10) given in Definition 3.3. It is reminiscent from the equiconvergence property of Brownian martingales w.r.t (see Theorem 11.1) which is the key argument in the proofs of Theorems 5.1 and 5.2. However, we will see that (5.15) is naturally satisfied in many important classes of examples as described in Section 6.

Remark 5.3.

In order to implement the scheme designed in this section, one has to face iterative computation of the regression functions (see (5.7)) which appears in (5.14). Error estimates associated with approximations of conditional expectations can be investigated in terms of the Vapnik-Chervonenkis dimension of suitable approximation sets of functions. We leave this investigation to a future project. See [4] for the optimal stopping time case.

6. Controlled imbedded discrete structures for non-Markovian states

We now start to investigate how the abstract results obtained in previous sections can be applied to the examples mentioned in the Introduction. The goal here is to construct controlled imbedded discrete structures associated with controlled states of the form (1.6), (1.7) and (1.8) in such way that is a strongly controlled Wiener functional.

6.1. Path-dependent controlled SDEs

In the sequel, we make use of the following notation

| (6.1) |

This notation is naturally extended to processes. We say that is a non-anticipative functional if it is a Borel mapping and

The underlying state process is the following -dimensional controlled SDE

| (6.2) |

with a given initial condition . We define and we endow this set with the metric

Then, is a complete metric space equipped with the Borel -algebra. The coefficients of the SDE will satisfy the following regularity conditions:

Assumption (C1): The non-anticipative mappings and are Lipschitz continuous, i.e., there exists a pair of constants such that

for every and and . One can easily check by routine arguments that the SDE (6.2) admits a strong solution and

where , is a constant depending on , and the compact set .

Remark 6.1.

Due to Assumption C1, one can apply Jensen and Burkholder-Davis-Gundy’s inequalities to arrive at the following estimate: there exists a constant such that

for and . Then, by applying Grönwall’s inequality, we observe the controlled SDE (6.2) satisfies Assumption B1.

• Construction of the controlled imbedded discrete structure for (6.2). In the sequel, in order to alleviate notation, we are going to write controlled processes as

rather than and , respectively, as in previous sections. In this section, we will establish a slightly stronger property than (3.10), namely we construct jointly with a sequence such that

| (6.3) |

for and . The sequence will be precisely computed as a function of .

Let us fix a control . At first, we construct an Euler-Maruyama-type scheme based on the random partition as follows. Let us define is the constant function over . Let us define as follows

for and , where . The controlled structure is naturally defined by

| (6.5) |

for and . The pathwise version of (6.5) realizing (5.6) is straightforward to guess so we left the details to the reader.

• Checking that with is a strongly controlled Wiener functional. Let us now check that satisfies (6.3). For a given control , we set

for . In the sequel, it is convenient to introduce the following notation: for each , we set

| (6.6) |

We define

| (6.7) |

for The differential in (6.7) is interpreted in the Lebesgue-Stieljtes sense. One should notice that

for every . For a given , the idea is to analyse

In the remainder of this section, is a constant which may differ from line to line. The following result is very simple but very useful to our argument.

Lemma 6.1.

For every , and , we have

where is the Itô integral and is the Lebesgue Stieltjes integral.

Lemma 6.2.

Proof.

From Assumption C1, there exists a constant such that

| (6.8) |

for every and , where only depends on , and the compact set . The proof consists on routine arguments based on Burkholder-Davis-Gundy and Jensen inequalities jointly with Grönwall’s inequality on the function . We left the details to the reader. ∎

Lemma 6.3.

For every , there exists a constant which only depends on , such that

for every and .

Proof.

Let us fix and . Lemma 6.1 allows us to write

Lemma 6.4.

For every and , there exists a constant which only depends on and such that

for every and .

Proof.

Corollary 6.1.

For given , and , there exists a constant which depends on these parameters such that

| (6.9) |

for every and .

Proof.

for every and . Since and there exists a constant such that for every , we conclude (6.9). ∎

Theorem 6.1.

Assume satisfies Assumption A1 for and the coefficients of the controlled SDE (6.2) satisfy Assumption C1. Then, for every , there exists a constant which depends on such that

Proof.

In the sequel, is the Cramer-Legendre transform of , for an iid sequence of random variables as described in (3.8). Fix . Triangle inequality yields

| (6.11) |

By Corollary 6.1, we only need to estimate . For this purpose, we set and we observe

| (6.12) |

Let us fix . To shorten notation, we set . By using Jensen’s inequality, we notice that (see (6.8))

on , where does not depend on controls. This estimate yields

| (6.13) |

for every , where the constant in (6.13) does not depend on . Let us now treat the stochastic integral. For each and , let us denote

We observe for every and . For a given , we split

We observe

for . By the additivity of the stochastic integral, we have

| (6.14) |

By applying Burkholder-Davis-Gundy and Hölder inequalities to (6.14) and using (6.8) and Lemma 6.2, we get

for any and control . Here, the constant does not depend on controls, and . By applying Lemma 8.2, we get

| (6.15) | |||||

for every and . In order to estimate , we denote

for . We notice

for every . By applying Th 1 in [22] jointly with (6.8) and Lemma 6.2, there exists a constant which does not depend on controls such that

for every and . Then,

| (6.16) |

In (6.15) and (6.16), can be chosen arbitrarily and independently from . Summing up (6.9), (6.11), (6.13), (6.15) and (6.16), we conclude the following: for every and , there exists a constant which depends on and such that

| (6.17) |

for every and and which can be chosen arbitrarily and independently from . Now, let us define

where . Let be the density of . From Lemma 3 in [7], we know that as for every , where . Hence, there exists such that . Now, by the very definition

| (6.18) |

for every and . In addition, since for every , we have

| (6.20) | |||||

for every and . By using the representation , we also have the following: if and is a positive number, we have

Then, for every positive sequence as , we have

6.2. Path-dependent controlled SDEs driven by FBM

In this section, we investigate controlled Wiener functionals of the form

| (6.24) |

where , is a constant, is a non-anticipative functional satisfying Assumption (C1) and . For simplicity of presentation, the payoff functional will be Lipschitz and we set the state dimension equals to one. The path-dependence feature is much more sophisticated than previous example because the lack of Markov property comes from distorting the driving Brownian motion by a singular kernel and also from a non-anticipative drift which depends on the whole solution path.

Under Assumption C1, by a standard fixed point argument, one can show there exists a unique strong solution for (6.24) for each . Moreover, the following simple remark holds true.

Remark 6.2.

The controlled SDE (6.24) satisfies Assumption B1 due to modulus of continuity of given by Assumption C1.

Clearly, the first step is to construct an imbedded discrete structure for . If , then there is a pathwise representation

To get a piecewise constant process, we set

The case is much more delicate. In the philosophy of [41], it is important to work with a pathwise representation of FBM which will be denoted by for . Let be the space of Hölder continuous real-valued functions on and starting at zero equipped with the usual norm. Let us define

for . By Lemma 2.1 and Theorem 2.1 in [46], the map

is a bounded linear operator for which realizes

In the sequel, we recall (see (6.6)) and we define

| (6.25) |

where we set . The discrete structure for FBM with is given by

We observe

The controlled structure associated with (6.24) is given as follows: let us fix a control with jumps given by . Let us define

where . Then, we set given by

| (6.26) |

The pathwise version of (6.26) realizing (5.6) is straightforward to guess so we left the details to the reader.

Theorem 6.2.

Assume satisfy Assumption A1 with , satisfies Assumption C1 and let . If and , there exists a constant which depends on such that

| (6.27) |

for every . Moreover, for a given error bound and , let be an -optimal control associated with the control problem (4.8) driven by and which can be calculated via (5.9) or (5.12). Then,

| (6.28) |

Fix . For and a pair such that , , there exists a constant which depends on such that

| (6.29) |

for . Moreover, for a given error bound and , let be an -optimal control associated with the control problem (4.8) driven by and which can be calculated via (5.9) or (5.12). Then,

| (6.30) |

Proof.

We fix , , and . In the sequel, is a constant which may differ from line to line. By applying Theorem 3.1 [46] and repeating exactly the same steps (with the obvious modification by replacing by ) as in the proofs of Lemmas 6.2, 6.3 and 6.4, we can find a constant (depending on , such that

| (6.31) | |||||

In order to estimate , we observe

| (6.32) |

where

| (6.33) | |||||

One can easily check for every where is a constant which depends on and . Moreover, we shall invoke Lemma 8.2 (see (8.3)) to arrive at

| (6.34) |

for every . Now, from Garsia-Rodemich-Rumsey’s inequality (see e.g Lemma 7.4 in [43]), for all there exists a nonnegative random variable with for all such that

for all . Therefore,

6.3. Controlled rough stochastic volatility

Let us now investigate the third type of non-Markovian controlled state:

| (6.38) |

where (for simplicity), and satisfy the following assumption:

Assumption (D1): is bounded and there exists a constant such that

for every , , where .

The noise in (6.38) is a FBM with exponent . We assume is a functional of the Brownian motion

where for . By Lemma 1.1 and Theorem 1.1 in [46], we can write

For further details about rough stochastic volatility models, see e.g. [1]. By Itô’s formula,

| (6.39) |

where is the Doléans-Dade exponential. It is well-known (see e.g Prop A1 [10])

Representation (6.39), Th 1 in [25] and the boundedness assumption on allow us to state for every . Moreover, a similar computation as explained in Remark 6.1 gives Assumption (B1) for the controlled state (6.38). An imbedded discrete structure for the volatility process will be described by

| (6.40) |

for , where, for each , we define

| (6.41) |

and

Clearly, there exists a constant which only depends on such that

Then, Lemma 8.1 and Theorem 3.1 [46] applied to (LABEL:pathwiseZ_k) allow us to state the following result.

Corollary 6.2.

Fix and . For any pair satisfying , there exists a constant which depends on such that

for .

Let us fix a control . Starting from , we define

for . We then define similar to (6.5). This provides a controlled imbedded discrete structure . A pathwise representation of realizing (5.6) is clear by looking at the previous examples and identities (6.40), (6.41) and (LABEL:Seuler). We left the details of this representation to the reader.

Let us define

for and . We set

for . We define

| (6.44) |

for . The differential in (6.44) is interpreted in the Lebesgue-Stieljtes sense. One should notice that

| (6.45) |

for every . The idea is to analyse

By using Assumption (D1), one can follow the same arguments as described in Lemmas 6.1, 6.2, 6.3, 6.4 and Corollary 6.1 to arrive at the following estimates:

| (6.46) |

for and satisfying the compatibility condition described in Corollary 6.2. Moreover,

| (6.47) |

for a constant which depends on and . Summing up the estimates (6.46), (6.47) and applying Gröwnall’s inequality, we get

for every . Following the same argument as described in the proof of Theorem 6.1, we arrive at the following result.

7. Pseudocode and a numerical example

In this section, we explain how the methodology can be implemented in a concrete simple example. At first, we present a pseudo-code for a given stochastic control problem. For simplicity of exposition, we set the dimension of the Brownian motion equals to and we assume is continuous.

| (7.1) |

Let us now present a simple example to illustrate the theory developed in this article. We choose the example of hedging in a two-dimensional Black-Scholes model. For a given , we define

Let us consider

where, for simplicity, we assume and the riskless rate equals zero. The problem is

| (7.2) |

where

the controls represent the absolute percentages of the securities which an investor holds at time and . It is well-known there exists a unique choice of such that

where by Margrabe’s formula, we have

where

and is the cumulative distribution function of the standard Gaussian variable. We recall is the price of the option and is the so-called delta hedging which can be computed by means of the classical PDE Black-Scholes as a function of . We set , and . The discretization is given by

and , where follows (LABEL:Xeuler) (without the presence of controls) with the coefficients for , where is the delta Dirac function concentrated at . To shorten notation, we write Moreover, we use the shorthand notation for a conditional expectation w.r.t . At first, for a given , we apply the algorithm described above to get a Monte Carlo optimal control approximation . In this particular case, we can analytically solve (7.1) and the optimal control is given by: and for , we have

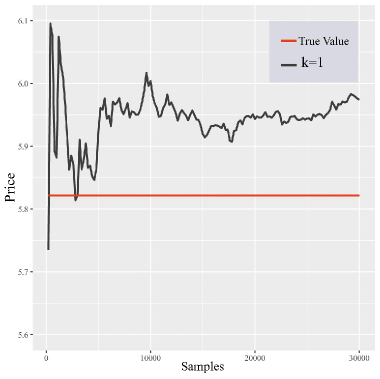

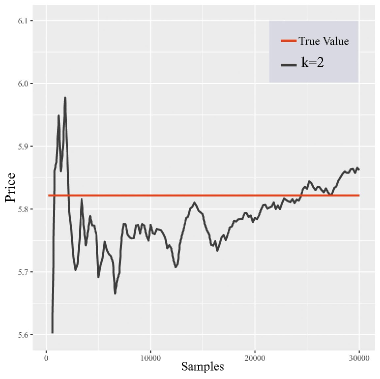

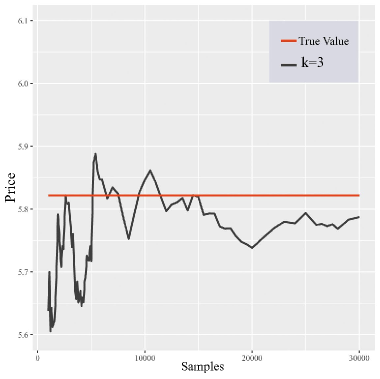

The estimated value is computed according to

In other words, . Table 1 presents a comparison between the true call option price and the associated Monte Carlo price . Figure 1 presents the Monte Carlo experiments for with and . The number of Monte Carlo iterations in the experiment is .

| k | Result | Mean Square Error | True Value | Difference | % Error |

|---|---|---|---|---|---|

| 1 | 5.9740 | 0.01689567 | 5.821608 | 0.152458 | 0.0261% |

| 2 | 5.8622 | 0.01158859 | 5.821608 | 0.04059157 | 0.0069% |

| 3 | 5.7871 | 0.00821813 | 5.821608 | 0.03441365 | 0.0059% |

8. Appendix A. Random mesh and large deviations

Lemma 8.1.

For every and , there exists a constant which depends on and such that

for every .

Proof.

We start by noticing (see (3.2)) that a.s where for an iid sequence of random variables with distribution equals to for a sequence of independent real-valued Brownian motions . We observe there exists such that

Let be the Cramer-Legendre transform of for the random variables described in (3.8).

Lemma 8.2.

For each and , we have

| (8.2) |

and

| (8.3) |

for every . Moreover, there exists a constant which depends on , and such that

| (8.4) |

for every .

9. Appendix B. Probability Kernel

In this section, we provide a closed form expression for the probability kernel (5.5) given by

In the sequel, is the density function (see e.g [7]) of for a standard Brownian motion . Formula for is a simple consequence of the strong Markov property of the Brownian motion. For simplicity, we present the formula for . The argument for is similar. In the sequel, we consider generic Borel sets of the form and for arbitrary open sets and . Clearly, this class of sets generates the Borel sigma algebra of . The proof of the following formula is lengthy but straightforward, so we omit the details.

Proposition 9.1.

Assume the underlying Brownian motion is -dimensional with . For each , and , we have

10. Appendix C. Construction of optimal controls: Measurable selection and -controls

In this section, we provide the proofs of the technical details associated with our dynamic programming algorithm described in Section 5.1. In the sequel, it will be important to deal with universally measurable sets. For readers who are not familiar with this class of sets, we refer to e.g [3]. If is a Borel space, let be the space of all probability measures defined on the Borel -algebra generated by . We denote

where is the -completion of w.r.t .

In the sequel, it will be useful to work with the set of all controls of the form (3.3) but is an -valued -measurable random variable for every for .

Lemma 10.1.

Let be a universally measurable function, where is a Borel space. Then, the composition is -mensurable, for every and .

Proof.

We need to show that given , the inverse image . Since is a universally measurable set, it is sufficient to check that for every universally measurable set in . Let be a probability measure on given by

For a given universally measurable set in , we can select (see e.g Lemma 7.26 in [3]) be such that

The set , so there exists such that . Then, and hence, . This concludes the proof.

∎

Let us now present a selection measurable theorem which will allow us to aggregate the map into a single list of upper semi-analytic functions . To keep notation simple, in the sequel we set . We fix a structure of the form (4.1) equipped with a Borel function realizing (5.6) with a given initial condition . For such structure, we write as the associated value process given by (4.3).

We start with the map defined by

By construction, is a Borel function.

Lemma 10.2.

Assume that for . Then,

| (10.1) |

Proof.

At first, we observe

| (10.2) |

for every . Elementary computation yields

for every control . Now, we recall for a given , there exists which fulfills the following: for each , there exists a set of full probability such that for . Let us denote . Then, in and hence

Identities (10.2) and (LABEL:iqual_2) allow us to conclude the proof. ∎

Lemma 10.3.

The map

is a Borel function from to .

Proof.

We just need to imitate the proof of Prop. 7.29 in ([3]). ∎

Lemma 10.4.

Let be the function defined by

for . Then, is upper semianalytic and for every , there exists an analytically measurable function which realizes

| (10.4) |

for every .

Proof.

The fact that is upper semianalytic follows from Prop 7.47 in [3] and Lemma 10.3 which say the map given by

is a Borel function (hence upper semianalytic). Moreover, by construction, is a Borel set. Let

Prop 7.50 in [3] yields the existence of an analytically measurable function such that

for every . ∎

Lemma 10.5.

If , then for every and , there exists a control such that

| (10.5) |

Proof.

For every , it follows from Equation (10.1) that equals (a.s) to

As a consequence, we obtain that

| (10.6) |

for every . By composing with in (10.4), we obtain that is an -measurable function (see, Lemma 10.1). Then, the definition of and Equation (10.6) yield that

| (10.7) |

For , let be the analytically measurable function which realizes (10.4). We take as the composition of an analytically measurable function with an -measurable one. In this case, by Lemma 10.1, we know that is an -measurable function. This shows that is an admissible control. It follows from (10.4) that

As is arbitrary, we conclude that

Moreover, as a consequence of Equation (LABEL:Ineq_3), we obtain that

∎

We are now able to iterate the argument as follows. From a backward argument, we can define the sequence of functions

| (10.10) |

for and .

Remark 10.1.

One can easily check that if , then

for .

Lemma 10.6.

For each , the map

is upper semianalytic from to .

Proof.

The same argument used in the proof of Lemma 10.3 applies here. We omit the details. ∎

Proposition 10.1.

The function is upper semianalytic for each . Moreover, for every , there exists an analytically measurable function such that

| (10.11) |

for every , where .

We are now able to define the value function at step as follows

Therefore, if then for , there exists which realizes

Proposition 10.2.

For each and a control , we have

| (10.12) |

Let be the functions given in Proposition 10.1. Observe that can be computed from (10.10) and (10.11). If , for , then for every , there exists a control defined by

| (10.13) |

which realizes

| (10.14) |

for every .

Proof.

We are now able to construct an -optimal control in this discrete level.

Proposition 10.3.

Let be an admissible pair w.r.t the control problem (4.8). Then, constructed via (10.13) is -optimal, where . In other words, for every and , the control realizes

| (10.15) |

Proof.

Fix and let , where we recall . The candidate for an -optimal control is

| (10.16) |

and

| (10.18) |

where (10.14) implies is less than or equals to

11. Appendix D. Proof of Theorems 5.1 and 5.2

In this section, we provide the proof of Theorems 5.1 and 5.2. The argument is divided into two parts. At first, we will prove it is possible to enlarge the set to without affecting . Secondly, we will establish an equiconvergence result for the family of Brownian martingales parameterized by . Finally, we invoke the property of the strongly controlled Wiener functionals as demonstrated in Section 6 for a variety of examples.

Since a.s for each , it is known (see e.g. Corollary 3.22 in [27]) that , where is the optional -algebra on and

where . To keep notation simple, we choose a version of defined everywhere and with a slight abuse of notation we write it as . Based on this fact, for each -valued and -measurable variable , there exists a list of Borel functions which realizes

| (11.1) |

for . In the sequel, in order to keep notation simple, we set . For a given and a list of Borel functions realizing (11.1), we then define the map given by

for and . Let us define

where is the identity map. For each represented by Borel functions realizing (11.1) and , we can represent

where is a pathwise representation for a structure .

Let be the disintegration of w.r.t and let be the disintegration of w.r.t for . In the sequel, is the projection of onto the last components. The proof of the following result is elementary, so we omit the details.

Lemma 11.1.

Let and let be a control associated with Borel functions realizing (11.1) for and . If , then

If and , then we can represent

where and are versions of and , respectively.

The following result shows the set of controls and are equivalent in a suitable sense.

Lemma 11.2.

For and , we have

| (11.2) | |||||

Proof.

Following the same argument employed in the proof of Lemma 10.2, we have

We now want to check equals to the expression (11.2). For a given control , let be a list of Borel functions such that

Let us define

where . Let be a control associated with Borel functions realizing (11.1) for . Moreover, we define the map given by

for and . We define and

with initial condition .

By Lemma 11.1,

where the esssup is computed over the set of all Borel functions for . Now, we define by

| (11.3) | |||||

By construction,

11.1. Equiconvergence of martingales

Let be the set of all stepwise constant processes of the form

| (11.5) |

where is a finite family of -stopping times and is an -valued -random element for . It is well-known (see e.g [49] Th 10 pp. 57) that the set of simple -predictable processes is a dense subset of w.r.t -topology.

| (11.6) |

Moreover, from Lemma 11.2, we know that

Now, for each with representation (11.5), we define

for , where is a finite -stopping time such that a.s for . Then, is an -adapted càdlàg process which jumps only at the hitting times . Let be the space of càdlàg functions from to equipped with the Skorohod metric

where is the set of all strictly increasing continuous bijections from onto and Id is the identity function.

Lemma 11.3.

for every .

Proof.

In the sequel, without any loss of generality, we set . Take with . Then, and for some . Moreover,

Let us consider

Then, is a pair of non-decreasing functions in . Then, there exist Lebesgue-Stieltjes measures which realize

Moreover,

| (11.8) |

where denotes the total variation norm of a signed measure. Let us consider , where and is the Dirac measure concentrated at zero. Clearly

where and (11.8) yields

| (11.9) |

Let us consider

By Fubini’s theorem, we can write

Now, we observe

| (11.10) | |||||

for every . The equality in the right-hand side of (11.10) holds true because is strictly increasing which allows us to state

for every . Hence, (LABEL:irate1), (11.9), (LABEL:irate5) yield

| (11.12) | |||||

Of course, and hence (11.12) yields

Since is arbitrary, we conclude the proof.

∎

For a given of the form (11.5), let .

Lemma 11.4.

for every .

Proof.

Let . Let for .

Let us define

Then, clearly a.s. We observe

and

This shows that .

∎

Theorem 11.1.

For a given , there exists a constant which depends only on and such that

| (11.13) |

for every . Moreover, for every .

Proof.

for every . There exists a constant depending on such that

for every . Hence, there exists a constant which depends on and such that

for every . This shows (11.13). In order to check the second assertion, we observe if we denote

for , then

whenever . This shows that is actually equal to over . Hence, for every and . ∎

Proof of Theorems 5.1 and 5.2: Firstly, formula (5.14) is a consequence of Propositions 4.1 and 10.2 and Remark 10.1. In one hand, Assumption A1 and Lemma 11.2 yield

| (11.14) |

for every . On the other hand, for a given , Assumption A1-B1, Theorem 11.1 and Hölder’s inequality yield

for every , where is a constant which depends on and the constant appearing in Assumption B1, i.e., (2.3). Then,

for every and . Hence,

for . This concludes the proof of Theorem 5.1. The proof of Theorem 5.2 is a simple consequence of Theorem 5.1 combined with Assumptions (A1-B1) and the definition of .

Acknowledgements The second author would like to thank UMA-ENSTA-ParisTech for the very kind hospitality during the first stage of this project. He also acknowledges the financial support from ENSTA ParisTech, AMSUD-MATH project grant 88887.197425/2018-00 and CNPq Bolsa de Produtividade de Pesquisa grant 303443/2018-9. Francys A. de Souza acknowledges the support of São Paulo Research Foundation (FAPESP) grant 2017/23003-6. The authors would like to thank M. Fragoso and P. Ruffino for stimulating discussions.

References

- [1] Bayer, C., Friz, P. K., Gassiat, P., Martin, J. and Stemper,B. (2019). A regularity structure for rough volatility. Math. Finance, 1-51.

- [2] Barles, G. and Souganidis, P.E. (1991). Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal. 4, 271-283.

- [3] Bertsekas, D.P. and Shreve, S. Stochastic optimal control: The discrete-time case. Athena Scientific Belmomt Massachusett, 1996.

- [4] Bezerra, S.C., Ohashi, A. and Russo, F. and Souza, F. A. (2020). Discrete-type approximations for non-Markovian optimal stopping problems: Part II. Methodol. Comput. Appl. Probab, 22, 1221-1255.

- [5] Biagini F., Hu, Y., Oksendal B., and Sulem, A. (2002). A stochastic maximum principle for processes driven by fractional Brownian motion. Stochastic Process Appl, 100, 1-2, 233-253.

- [6] Bouchard, B. and Touzi, N. (2004). Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Process. Appl. 111, 175-206.

- [7] Burq, Z. A. and Jones, O. D. (2008). Simulation of brownian motion at first-passage times. Math. Comput. Simul. 77, 1, 64-71.

- [8] Borodin, A. N. and Salminen, P., Handbook of Brownian Motion: Facts and Formulae. Birkhauser, 2002.

- [9] Buckdahn, R, and Shuai, J. (2014). Peng’s maximum principle for a stochastic control problem driven by a fractional and a standard Brownian motion. Science China Mathematics, 57, 10, 2025-2042.

- [10] Cheridito, P., Kawaguchi, H. and Maejima, M. (2003). Fractional Ornstein-Uhlenbeck processes. Electron. J. Probab, 8, 3, 14 p.

- [11] Claisse, J., Talay, D. and Tan, X. A Pseudo-Markov Property for Controlled Diffusion Processes. SIAM J. Control Optim, 54, 2, 1017-1029.

- [12] Cont, R. and Fournie, D. (2013). Functional Ito calculus and stochastic integral representation of martingales, Ann. of Probab, 41, 1, 109-133.

- [13] Cont, R. Functional Itô calculus and functional Kolmogorov equations, in: V Bally et al: Stochastic integration by parts and Functional Ito calculus (Lectures Notes of the Barcelona Summer School on Stochastic Analysis, Centro de Recerca de Matematica, July 2012), Springer: 2016.

- [14] Davis, M. Martingale methods in stochastic control, in Stochastic Control and Stochastic Differential Systems, Lecture Notes in Control and Information Sciences 16 Springer-Verlag, Berlin 1979.

- [15] Diehl, J., Friz, P. K. and Gassiat, P. (2017). Stochastic control with rough paths. Appl. Math. Optim, 75, 285–315.

- [16] Dolinsky, Y. (2012). Numerical schemes for G-expectations. Electron. J. Probab, 17, 1–15.

- [17] Duncan, T.E. and Pasik-Duncan, B. (2013). Linear-quadratic fractional Gaussian control. SIAM J. Control Optim, 51, 6, 4504-4519.

- [18] Dupire, B. Functional Itô calculus. Portfolio Research Paper 2009-04. Bloomberg.

- [19] Ekren, I., Touzi, N. and Zhang, J. (2016). Viscosity Solutions of Fully Nonlinear Parabolic Path Dependent PDEs: Part I. Ann. Probab. , 44, 2, 1212-1253.

- [20] El Karoui, N. (1979). Les Aspects Probabilistes du Contrôle Stochastique , in Ecole d’Eté de Probabilités de Saint-Flour IX, Lecture Notes in Math. 876.

- [21] Fahim, A., Touzi, N. and Warin, X. (2011). A probabilistic numerical method for fully nonlinear parabolic PDEs. Ann. Appl. Probab, 21, 4, 1322-1364.

- [22] Fischer, M. and Nappo, G. (2009). On the Moments of the Modulus of Continuity of Itô Processes. Stoch. Analysis Appl, 28, 1, 103-122.

- [23] Fuhrman, M. and Pham, H. (2015). Randomized and backward SDE representation for optimal control of non-Markovian SDEs. Ann. Appl. Probab, 25, 4, 2134-2167.

- [24] Gordon, Y., Litvak, A.E., Schütt, C. and Werner, E. (2006). On the Minimum of Several Random Variables. P. Am. Math. Soc, 134, 12, 3665-3675.

- [25] Grigelionis, B. and Mackevicius. V. (2003). The finiteness of moments of a stochastic exponential. Stat. Probab. Letters, 64, 243-248.

- [26] Han, Y., Hu, Y. and Song, J. (2013). Maximum principle for general controlled systems driven by fractional Brownian motions. Appl Math Optim, 7, 279-322.

- [27] He, S-w., Wang, J-g., and Yan, J-a. Semimartingale Theory and Stochastic Calculus, CRC Press, 1992.

- [28] Hu, Y. and Zhou, X. (2005). Stochastic control for linear systems driven by fractional noises. SIAM J Control Optim, 43, 2245-2277.

- [29] Jaber, E. A., Miller, E. and Pham, H. (2019). Integral operator Riccati equations arising in stochastic Volterra control problems. arXiv:1911.01903.

- [30] Jaber, E. A., Miller, E. and Pham, H. (2019). Linear–Quadratic control for a class of stochastic Volterra equations: solvability and approximation. arXiv: 1911.01900.

- [31] Jacod, J., and Skohorod. A.V. (1994). Jumping filtrations and martingales with finite variation. Lecture Notes in Math. 1583, 21-35. Springer.

- [32] Kharroubi, I. and Pham, H. (2014). Feynman-Kac representation for Hamilton-Jacobi- Bellman IPDE. Ann. Probab, 43, 4, 1823-1865.

- [33] Kharroubi, I. Langrenè, N. and Pham, H. (2014). A numerical algorithm for fully nonlinear HJB equations: An approach by control randomization. Monte Carlo Methods and Applications, 20, 2.

- [34] Kharroubi, I. Langrenè, N. and Pham, H. (2015). Discrete time approximation of fully nonlinear HJB equations via BSDEs with nonpositive jumps. Ann. Appl. Probab., 25, 4, 2301-2338.

- [35] Krylov, N. V. (1999). Approximating value functions for controlled degenerate diffusion processes by using piecewise constant policies. Electron. J. Probab. 4, 1-19.

- [36] Krylov, N.V. (2000). On the rate of convergence of finite-difference approximations for Bellmans equations with variable coefficients. Probab. Theory Relat. Fields, 117, 1, 1-116.

- [37] Kushner, H.J and Dupuis, P. Numerical Methods for Stochastic Control Problems in Continuous Time, 2nd edn., Applications of Mathematics, Vol. 24, Springer-Verlag, 2001.

- [38] Lamberton, D. Optimal stopping and American options, Daiwa Lecture Ser., Kyoto, 2008.

- [39] Mazliak, L. and Nourdin, I. (2008). Optimal control for rough differential equations. Stoch. Dyn. 08, 23.

- [40] Leão, D. and Ohashi, A. (2013). Weak approximations for Wiener functionals. Ann. Appl. Probab, 23, 4, 1660-1691.

- [41] Leão,D. Ohashi, A. and Simas, A. B. (2018). A weak version of path-dependent functional Itô calculus. Ann. Probab, 46, 6, 3399-3441.

- [42] Leão, D., Ohashi, A. and Russo, F. (2019). Discrete-type approximations for non-Markovian optimal stopping problems: Part I. J. Appl. Probab. 56, 4, 981-1005.

- [43] Nualart, D and Rascanu, A. (2002). Differential equations driven by fractional Brownian motion, Collect. Math. 53, 1, 55-81.

- [44] Nutz, M. and van Handel, R. (2013). Constructing Sublinear Expectations on Path Space. Stochastic Process. Appl, 123, 8, 3100-3121.

- [45] Nutz, M. (2012). A Quasi-Sure Approach to the Control of Non-Markovian Stochastic Differential Equations Electron. J. Probab, 17, 23, 1-23.

- [46] Ohashi, A and Souza, F.A. uniform random walk-type approximation for fracional Brownian motion with Hurst exponent . arXiv:2007.15472. 2020.

- [47] Peng, S. G-expectation, G-Brownian motion and related stochastic calculus of Itô type. In Stochastic analysis and applications. Springer, Berlin, Heidelberg, 2007, 541-567.

- [48] Possamaï, D., Tan, X. and Zhou, C. (2018). Stochastic control for a class of nonlinear kernels and applications. Ann. Probab, 46, 1, 551-603

- [49] Protter, P. Stochastic Integration and Differential Equations : A New Approach. 1990. Third edition.

- [50] Qiu, J. (2018). Viscosity Solutions of Stochastic Hamilton–Jacobi–Bellman Equations. SIAM J. Control Optim, 56, 5, 3708-3730.

- [51] Ren, Z and Tan, X. (2017). On the convergence of monotone schemes for path-dependent PDEs. Stochastic Process. Appl, 127, 6, 1738-1762.

- [52] Saporito, Y. (2019) Stochastic Control and Differential Games with Path-Dependent Influence of Controls on Dynamics and Running Cost. SIAM J. Control Optim, 57, 2, 1312-1327.

- [53] Soner, M., Touzi, N. and Zhang, J. (2012). The wellposedness of second order backward SDEs. Probab. Theory Relat. Fields, 153, 149-190.

- [54] Tan, X. (2014). Discrete-time probabilistic approximation of path-dependent stochastic control problems. Ann. Appl. Probab, 24, 5, 1803-1834.

- [55] Zhang, J and Zhuo, J. (2014). Monotone schemes for fully nonlinear parabolic path dependent PDEs, Journal of Financial Engineering, 1.

- [56] Zhang, J. (2004). A numerical scheme for BSDEs. Ann. Appl. Probab, 14, 459-488.

- [57] Zhou, X.Y. (1998). Stochastic near-optimal controls: Necessary and sufficient conditions for near optimality. SIAM. J. Control. Optim, 36, 3, 929-947.