Old Problems, Classical Methods, New Solutions

Abstract

We use a powerful extension of the classical method of heat potentials, recently developed by the present author and his collaborators, to solve several significant problems of financial mathematics. We consider the following problems in detail: (A) calibrating the default boundary in the structural default framework to a constant default intensity; (B) calculating default probability for a representative bank in the mean-field framework; (C) finding the hitting time probability density of an Ornstein-Uhlenbeck process. Several other problems, including pricing American put options and finding optimal mean-reverting trading strategies, are mentioned in passing. Besides, two nonfinancial applications - the supercooled Stefan problem and the integrate-and-fire neuroscience problem - are briefly discussed as well.

1 Introduction

The method of heat potentials (MHP) is a highly robust and versatile approach frequently exploited in mathematical physics; see, e.g., [50, 48, 24, 51] among others. It is essential in numerous vital fields, such as thermal engineering, nuclear engineering, and material science.

However, it is not particularly popular in mathematical finance, even though the first meaningful use case was described by the present author almost twenty years ago. The specific application was to pricing barrier options with curvilinear barriers, see [31], Section 12.2.3.

In this document, we demonstrate how a powerful extension of the classical MHP, recently developed by the present author and his collaborators, can be used to solve seemingly unrelated problems of applied mathematics in general and financial mathematics in particular, see [35, 36, 37, 38, 39].

Specifically, we use the extended method of heat potentials (EMHP) for (A) calibrating the default boundary for a structural default model with constant default intensity; (B) finding a semi-analytical solution of the mean-field problem for a system of interacting banks; (C) developing a semi-analytical description for the hitting time density for an Ornstein-Uhlenbeck process. Besides, we demonstrate the efficacy of the EMHP by considering two nonfinancial applications: (A) the supercooled Stefan problem; (B) the integrate-and-fire model in neuroscience.

We note in passing that, in addition to the problems discussed in this document, the EMHP has been successfully used for pricing American put options and for finding optimal strategies for mean-reverting spread trading, see [36, 37].

We emphasize that in most cases, the EMHP beats all other known approaches to the problem in question, and in some instances, for example, for the boundary calibration problem, it is the only one that can be used effectively.

2 Mathematical preliminaries

In this section, we describe the classical MHP and its beneficial extensions proposed by the author and his collaborators.

2.1 The method of heat potentials

Consider a standard heat equation in a one-sided domain with a moving boundary :

| (1) |

Without loss of generality, we can assume that ; the case of a nonzero initial condition can be solved by splitting:

where is the standard heat kernel,

Thus, we can restrict ourselves to the case of zero initial condition:

where

The MHP allows one to represent in the form

| (2) |

where solves the Volterra equation of the second kind:

| (3) |

and

Similarly, the solution to the problem

has the form

where

Finally, the solution to the two-sided problem

has the form

where

2.2 Extensions

While Eqs (2), (3) provide an elegant solution to problem (1), in many instances we are interested in the behavior of this solution on the boundary itself. For instance, in numerous problems of mathematical finance, some of which are described below, what we need to know is the function

which represent the outflow of probability from the computational domain. This function can be calculated in two ways.

On the other hand, a useful formula derived by the present author and his collaborators, see [35, 36, 37, 39], gives an alternative expression for :

| (5) |

where

On the surface, Eqs (4), (5) look very different. However, a useful Lemma proven in [39], allows one to connect the two.

Lemma Let be a differentiable function, such that . Then

Alternatively,

We emphasize that Eq. (5) is easier to use than Eq. (4) in most situations because it does not involve differentiation. However, if the cumulative outflow is of interest, the latter equation can be more efficient, since it can be rewritten as follows:

We can calculate and by the same token. It is important to understand that both Eqs (5) and (4) can be used in the one-sided case, however, in the case when two boundaries are present, we can only use Eq. (5) because this equation allows calculating and individually while Eq. (4) calculates the difference .

2.3 Generalizations

If the MHP were applicable only to standard Wiener process, it would be advantageous, if somewhat narrow in scope. Fortunately, it can be applied to a general diffusion satisfying the so-called Cherkasov’s condition, which guarantees that it can be transformed into the standard Wiener process. Such diffusions are studied in [9], [46], and [5]. The applications of Cherkasov’s condition in financial mathematics are discussed in [31], Section 4.2, and [34], Chapter 9.

Consider a diffusion governed by

We wish to calculate boundary-related quantities, such as the distribution of the hitting time of a given time-dependent barrier :

To this end, we introduce

where the lower limit of integration is chosen as convenient. Define

and assume that Cherkasov’s condition is satisfied, so that

Then we can transform into the standard Wiener process via the following mapping

where

In particular, the initial condition becomes

The corresponding transition probability density transforms as follows

Moreover, the boundary transforms to

Since the MHP is specifically designed for dealing with curvilinear boundaries, we get a solvable problem. A powerful application of the above approach is demonstrated in Section 5, where the hitting time probability distribution for an Ornstein-Uhlenbeck process is studied.

2.4 Numerics

There are numerous well-known approaches to solving Volterra equations; see, [30], among many others. We choose the most straightforward approach and show how to solve the following archetypal Volterra equation with weak singularity numerically:

where is a non-singular kernel. We write

| (6) |

We wish to map this equation to a grid . To this end, we introduce the following notation:

Then, the right hand side of Eq. (6) can be approximated by the trapezoidal rule as

| (7) |

where

so that

| (8) |

Thus, can be found by induction starting with .

Eq. (8) is the blueprint for all the subsequent numerical calculations.

3 The structural default model

3.1 Preliminaries

The original, and straightforward, structural default model was introduced by Merton, [41], who assumed that default could happen only at debt maturity. His model was extended by Black and Cox, [4], who considered the default, which can happen at any time by introducing flat default boundary representing debt covenants. Numerous authors expanded their model including [19, 18, 3], who considered curvilinear boundary whose shape can be calibrated to the market default probability. One of the major unsolved issues with the above model was articulated by Hyer et al., [19], who pointed out that, unless the shape of the default boundary is very carefully chosen, the probability of short-term default is too low. This issue was addressed by several authors, including [13, 17, 32], who proposed to introduce jump and or uncertainty to increase this probability. We show below that it is possible to calibrate the default boundary in such a way that constant default intensity can be matched. We emphasize that the direct problem - calculating the default probability given the boundary - is linear (albeit relatively involved), while the inverse problem - finding the boundary given the default probability - is nonlinear (and hence even more involved). Additional details are given in [37].

3.2 Formulation

We wish to find the boundary for a structural default model corresponding to a constant default intensity . We denote the corresponding default probability by

The introduce time , such that default is impossible for . Thus the default boundary starts at . The idea is to calculate the corresponding boundary , provided it exists, and then let .

It is clear that at time , the transition probability is

where is the heat kernel:

At time , the first possibility of default occurs. For the transition probability satisfies the following Fokker–Planck problem

The default probability density is given by

Alternatively,

3.3 Governing system of integral equations

We split as follows

where

| (9) |

and is the Heaviside function. Solving Eq. (9) as a convolution of heat kernel with the initial condition, we get

where , see [37]. Thus

Accordingly, in view the discussion in Section 2.2, we need to solve the following system of integral equations:

| (10) |

Alternatively, we can rewrite Eqs (10) in integrated form

| (11) |

where is the bivariate normal distribution.

We postpone the discussion of the corresponding numerics until the next Section, where a more general case is considered.

3.4 The choice of

Recall that the default probability has the form

The barrier has to start at , , and there should be no barrier before that. We wish to find such that

Thus,

and

Now,

where

so that

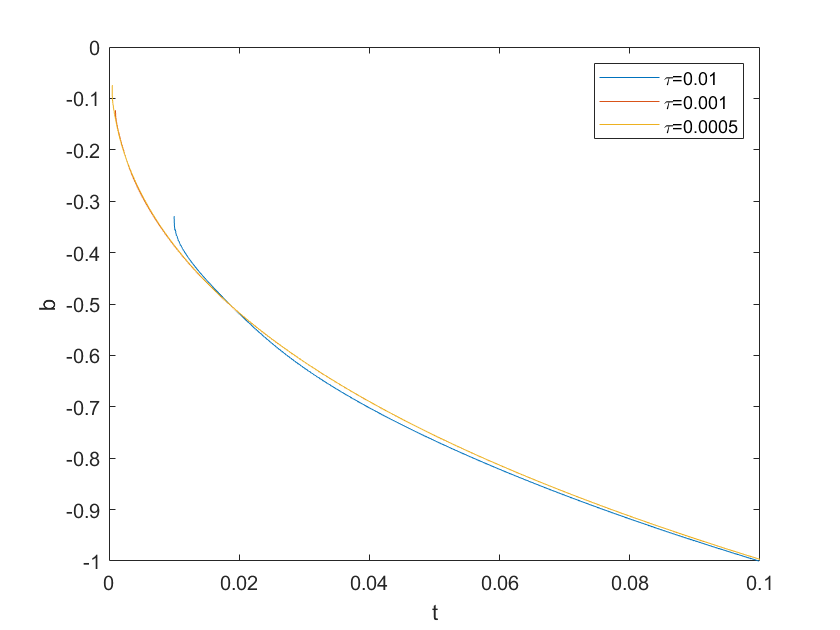

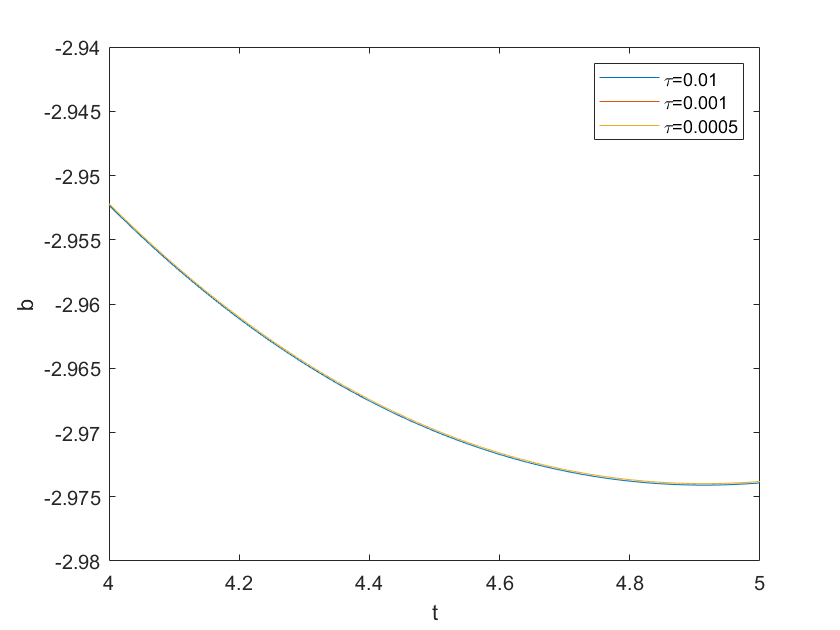

3.5 Default boundaries

3.6 Main conjecture

Conjecture For a given time interval , there exists a parameter interval , such that for any , the default boundary can be calibrated to the default intensity . We can construct the corresponding boundary as follows:

4 Mean-field banking system

4.1 Preliminaries

No bank is an island - they operate as a group. Tangible links between banks manifest themselves via interbank loans; intangible links are manifold - overall sentiment, ease of doing business, and others. Hence, to build a meaningful structural default model for a bank, one needs to take into account this bank’s interactions with all the banks whom it lends to or borrows from. Eisenberg and Noe developed a Merton-like model of the bank default (default can happen only at maturity) in the seminal paper [12]. The present author extended the Eisenberg-Noe model to the Black-Cox setting (default can happen at any time before maturity provided that debt covenants are violated); see [33]. Lipton’s work was subsequently generalized in [21, 22]. Recently, several authors considered the interconnected banking system in the mean-field framework and studied a representative bank, see [16, 20, 25, 42, 43] among many others. In this section, we also use the mean-field approach. Additional details are given in [39].

4.2 Interconnected banking system

We follow [33] and assume that the dynamics of bank ’s total external assets is governed by

where are independent standard Brownian motions for , and the liabilities, both external and mutual , are constant.

Bank is assumed to default when its assets fall below a certain threshold determined by its liabilities, namely at time , where is a default boundary which we now work out. At time ,

where is the recovery rate of bank . If bank defaults at time , the default boundary of bank jumps by

The distance to default has the following dynamics:

or, approximately,

where

In the limit for , all have the same dynamics:

where characterizes the strength of interbank interactions. Thus, we are dealing with a mean-field problem - the behavior of a representative bank depends on the behavior of all other banks, and all of them have the same dynamics. Hence, the problem in question is nonlinear.

| (12) |

The change of variables yields the familiar initial-boundary-value problem (IBVP):

As before, we split in two parts

where is the standard heat kernel, while is the solution of the following problem:

4.3 Governing system of integral equations

Using our standard approach, we obtain the following system of nonlinear Volterra integral equations

| (13) |

where

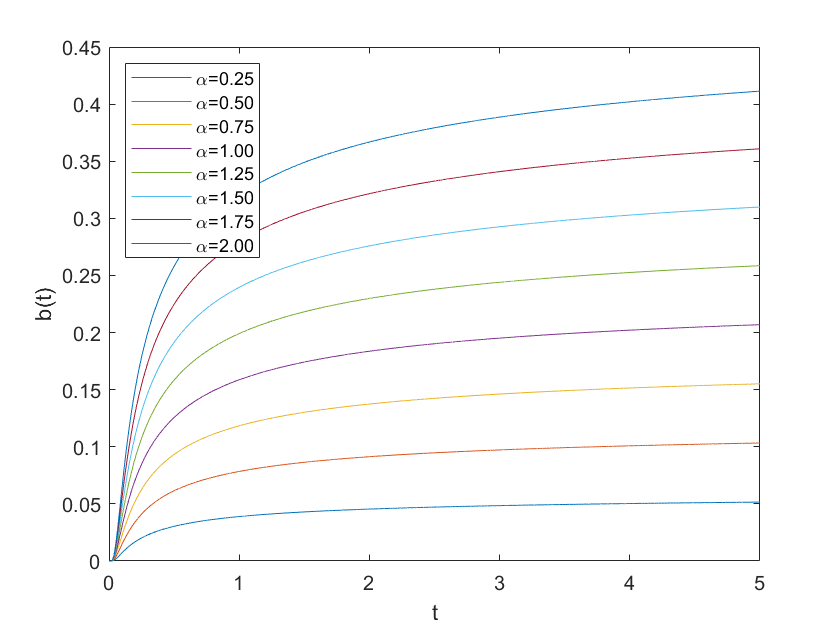

4.4 Numerical solution

In the spirit of Eq. (7), we get the following approximation for Eqs (13) for :

Here and below we use the following notation

For we have:

For we have:

where the nonlinear equation for has to be solved by the Newton-Raphson method.

For we have

Assuming that are known, we can express in terms of :

and obtain a nonlinear equation for :

which again is solved by the Newton-Raphson method.

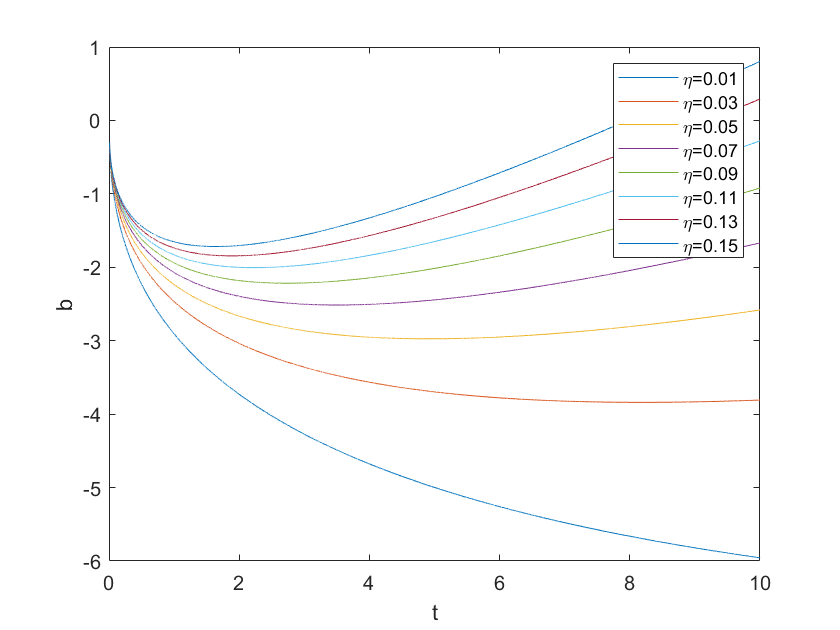

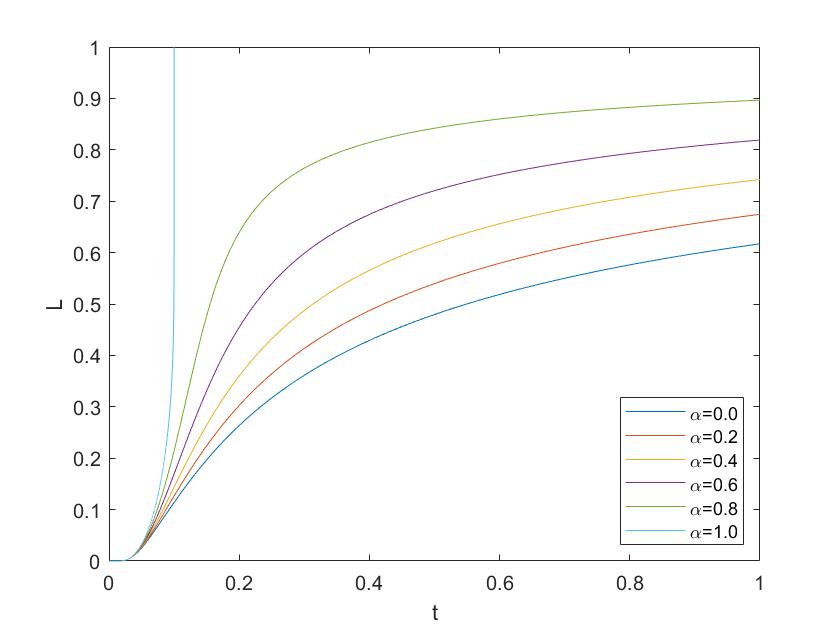

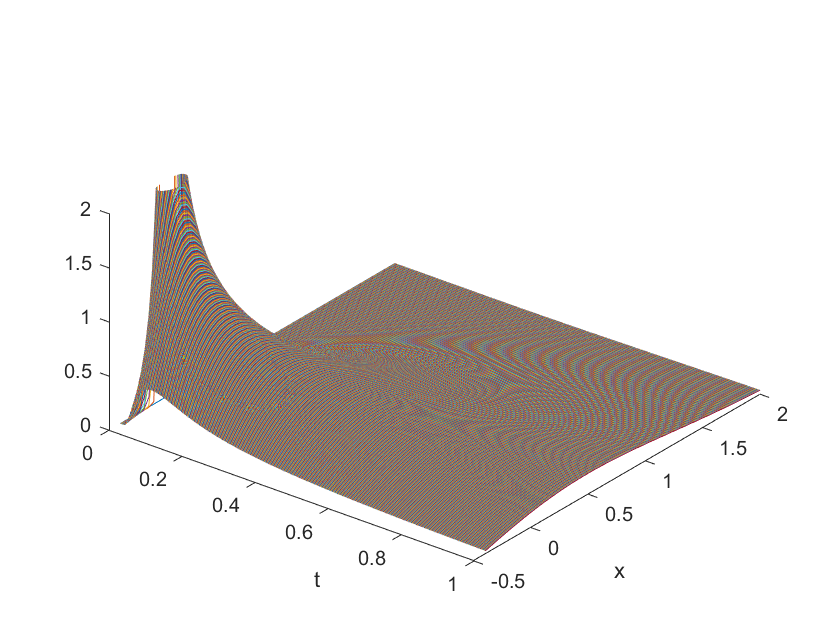

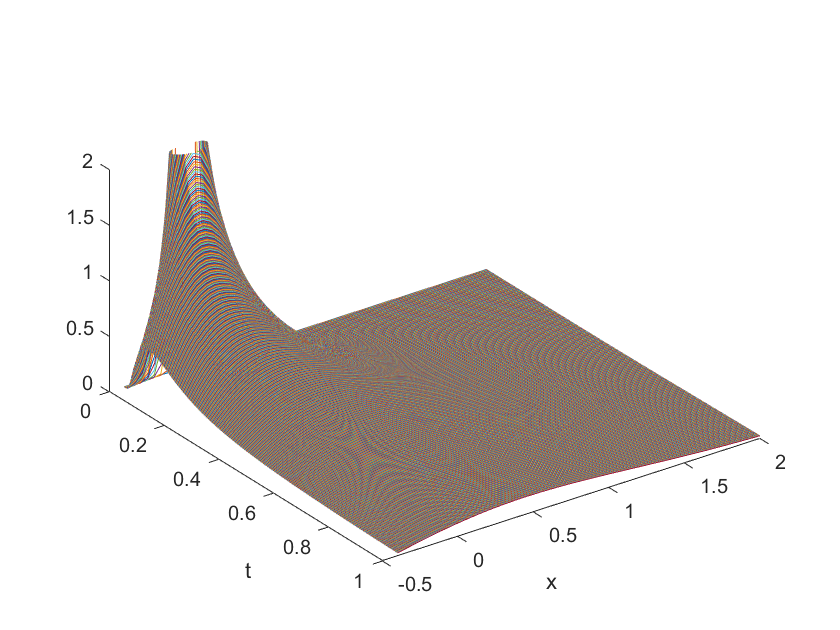

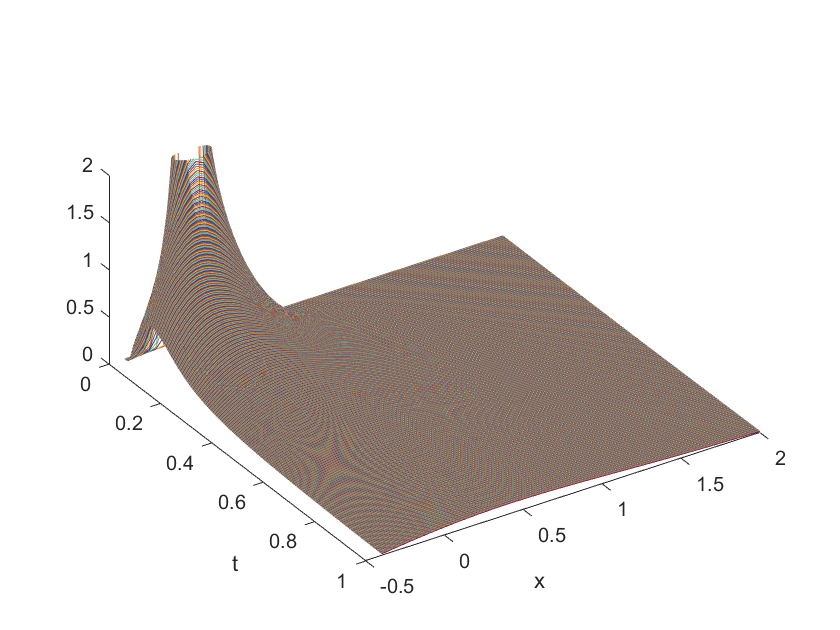

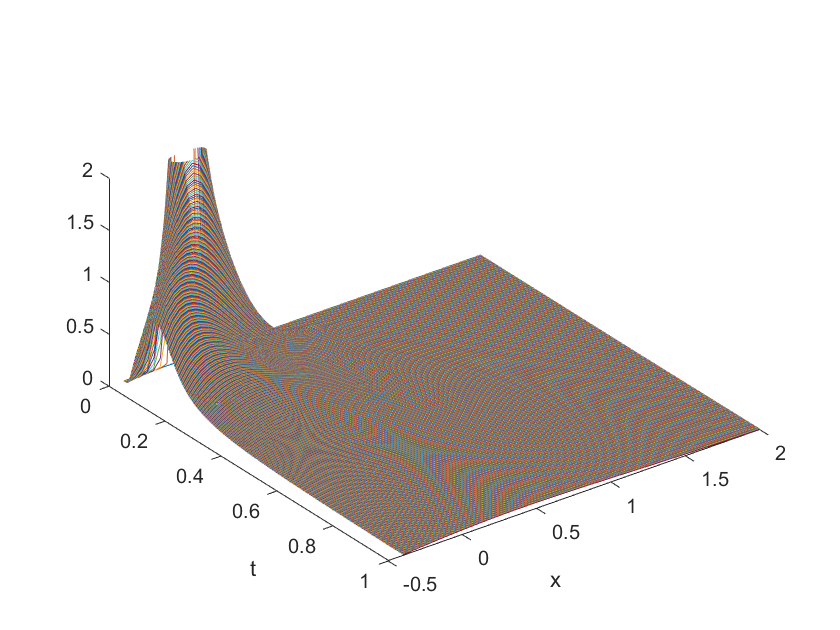

In Figure 4 we show cumulative loss probability for several representative values of .

| Figure 4 near here. |

A striking feature of this figure is the ”phase transition” occurring at , when default after a finite time becomes inevitable. By contrast, for , the default probability reaches unity only asymptotically when .

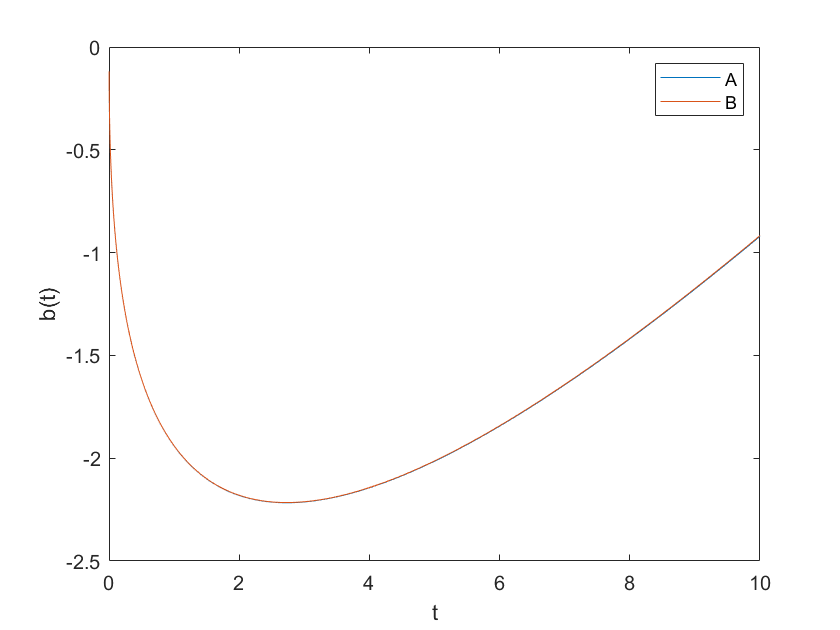

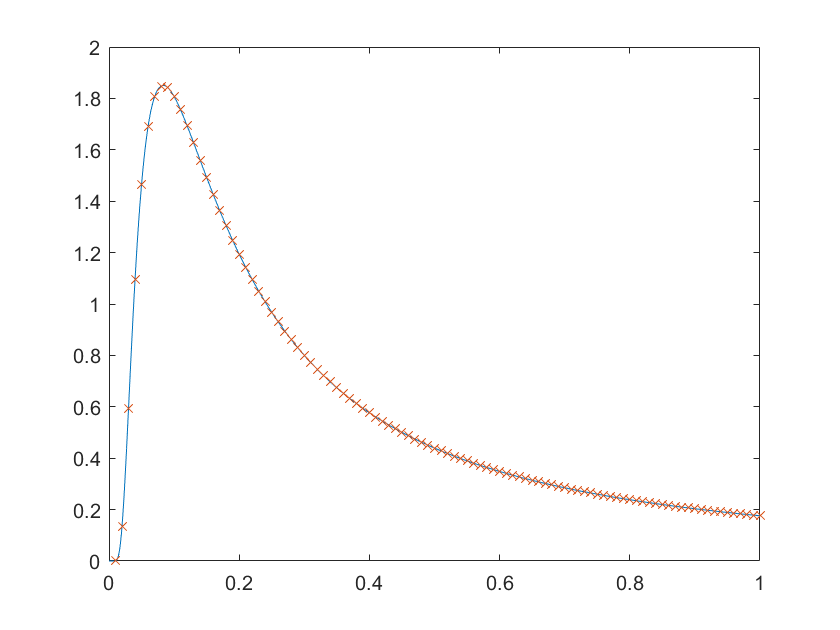

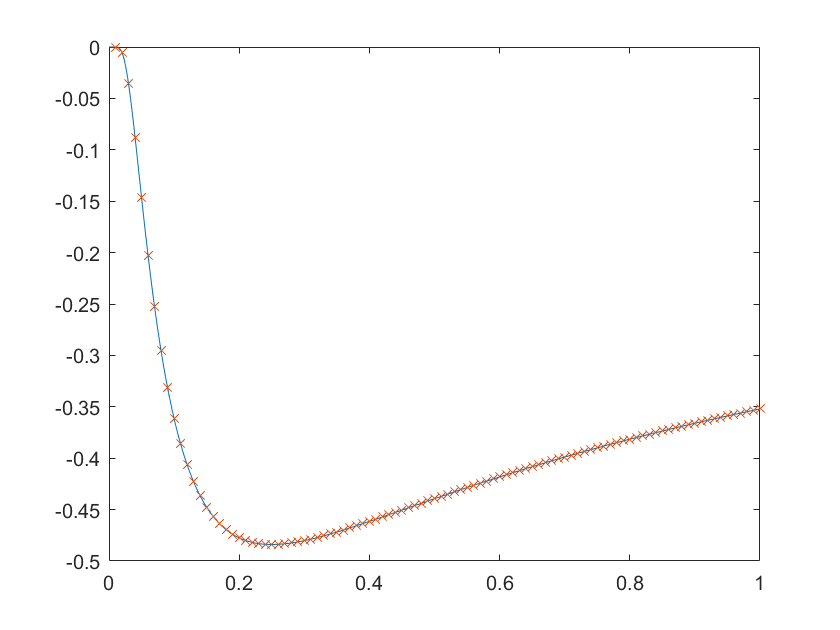

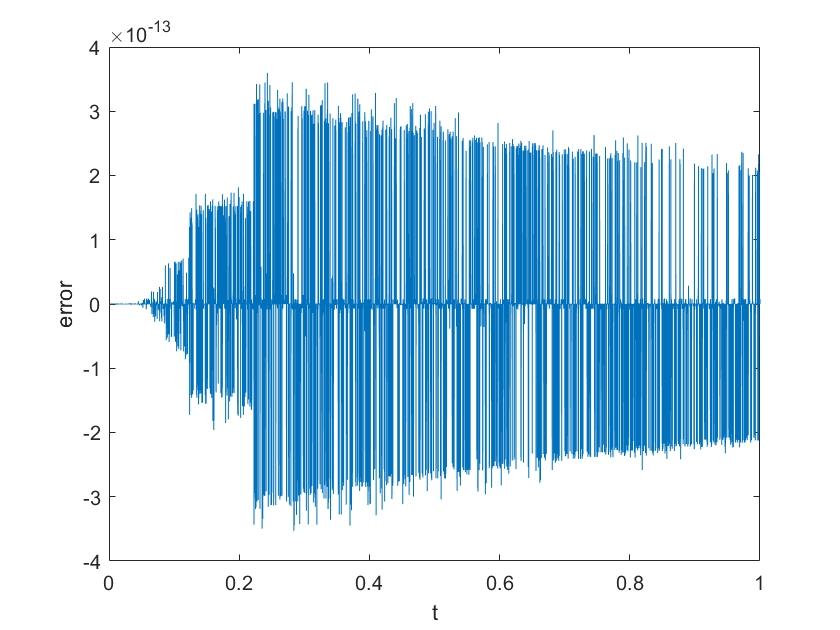

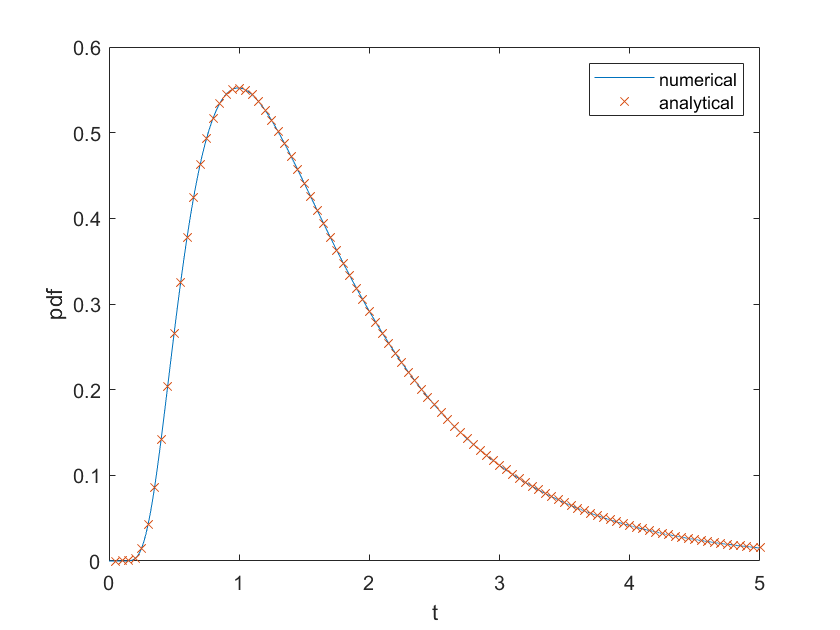

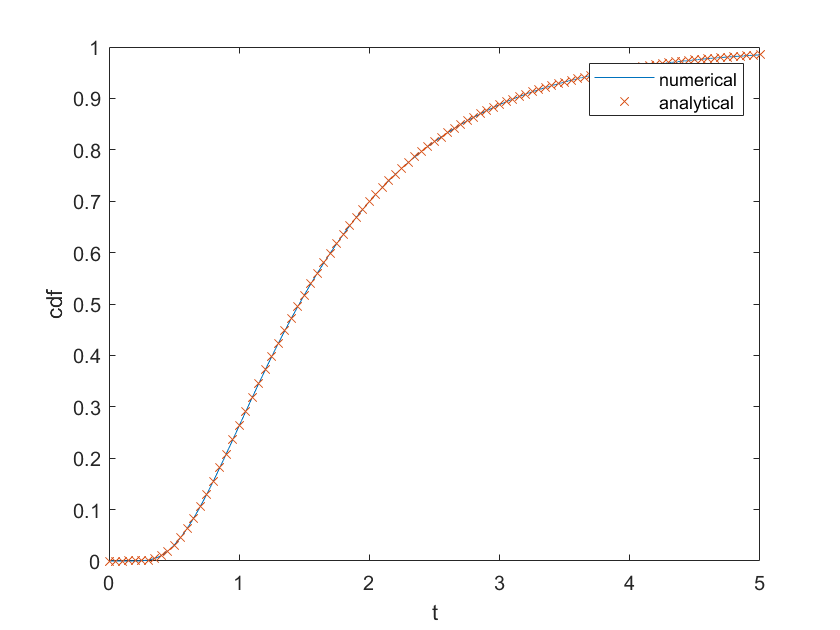

We notice that for , , can be calculated analytically. For benchmarking purposes, we compare numerical and analytical results in Figure 5, (a), (b). As usual, the efficiency of the Newton-Raphson method, which is illustrated in Figure 5 (c) is nothing short of miraculous.

| Figure 5 near here. |

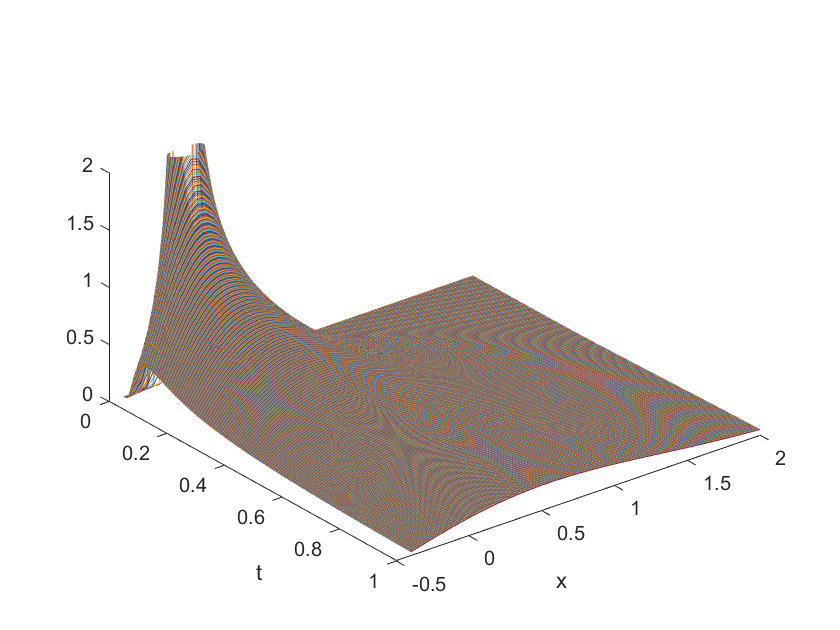

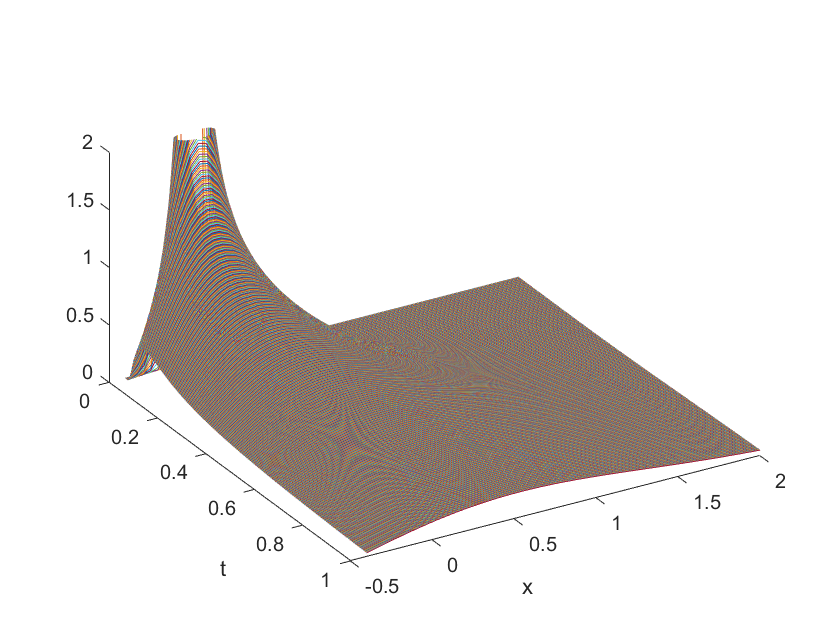

In Figure 6 we represent shifted probability density surfaces for representative values of used in Figure 4.

| Figure 5 near here. |

The shift is made in order to make the connection with Section 3 more transparent; after this shift all the processes start at and the boundaries are given by .

5 Hitting time probability distribution for an Ornstein-Uhlenbeck process

5.1 Preliminaries

In a seminal paper, Fortet developed an original approach to calculating probability distribution of the hitting time for a diffusion process, [14]. Fortet’s equation can be viewed as a variant of the Einstein-Smoluchowski equation, [11, 49]. A general overview can be found in [6, 7].

Numerous attempts to find an analytical result for the Ornstein-Uhlenbeck (OU) process have been made since 1998 when Leblanc and Scaillet first derived an analytical formula, which contained a mistake, [26]. Two years later, Leblanc et al. published a correction on the paper, [27]; unfortunately, the correction was erroneous as well, as was shown by [15].

In this section, we use the EMHP to calculate the distribution of the hitting time for an OU process. Our approach is semi-analytical and can handle both constant and time-dependent parameters. It is worth noting that the latter case cannot be solved using the Laplace transform method. Additional information can be found in [36].

5.2 Main equations

To calculate the density of the hitting time probability distribution, we need to solve the following forward problem

| (14) |

This distribution is given by

5.3 Particular case,

Before solving the general problem via the EMHP, let us consider a particular case of . Green’s function for the OU process in question has the form

where

Since , the method of images works, so that

This result is useful for benchmarking purposes.

5.4 General case

To be concrete, consider the case . We wish to transform the IBVP (14) into the standard IBVP for a heat equation with a moving boundary. To this end, we introduce new independent and dependent variables as follows:

| (15) |

and get the IBVP of the form

Here

5.5 The governing system of integral equations

The corresponding system of Volterra integral equations has the form

| (16) |

where

This system is linear, so that is expressed in terms of directly and there is no need to use the Newton-Raphson method.

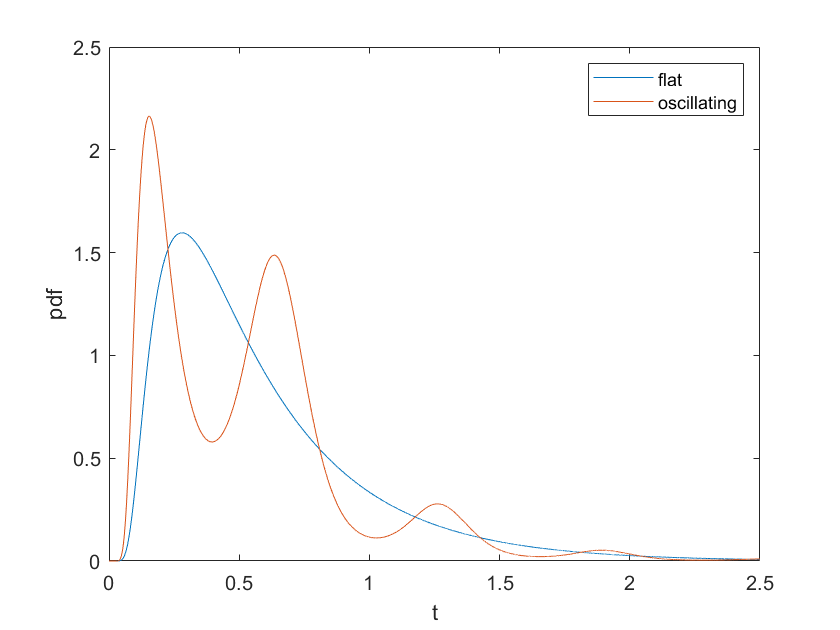

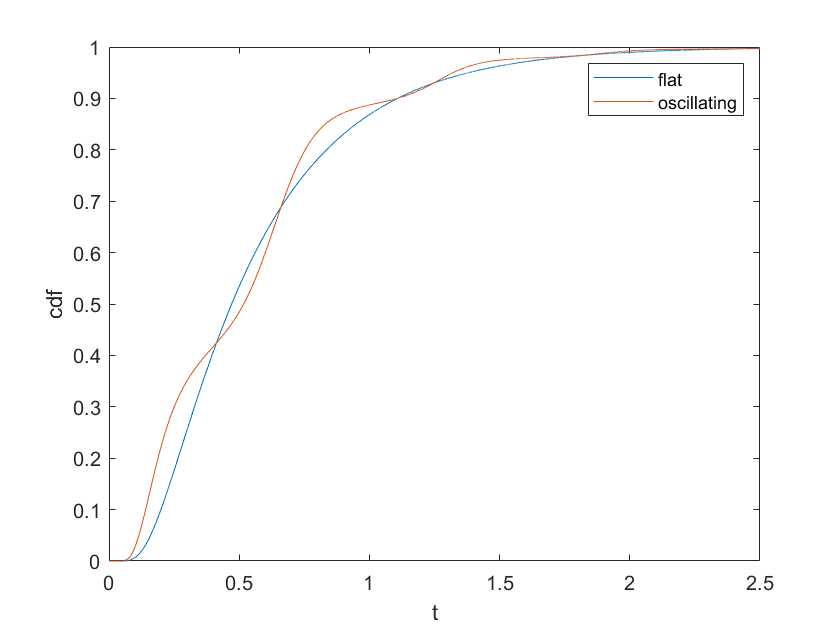

5.6 Flat boundary

Assuming that the boundary is flat, we can simplify Eqs (16) somewhat. We notice that

introduce

and write the first equation (16) in the form

| (17) |

Provided that is known, we can represent is the form

It is worth noting that the analytical solution is available in two cases: (A) when the solution can be found by using the method of images; (B) when the boundary transforms into the linear boundary , which can be treated by the method of images as well.

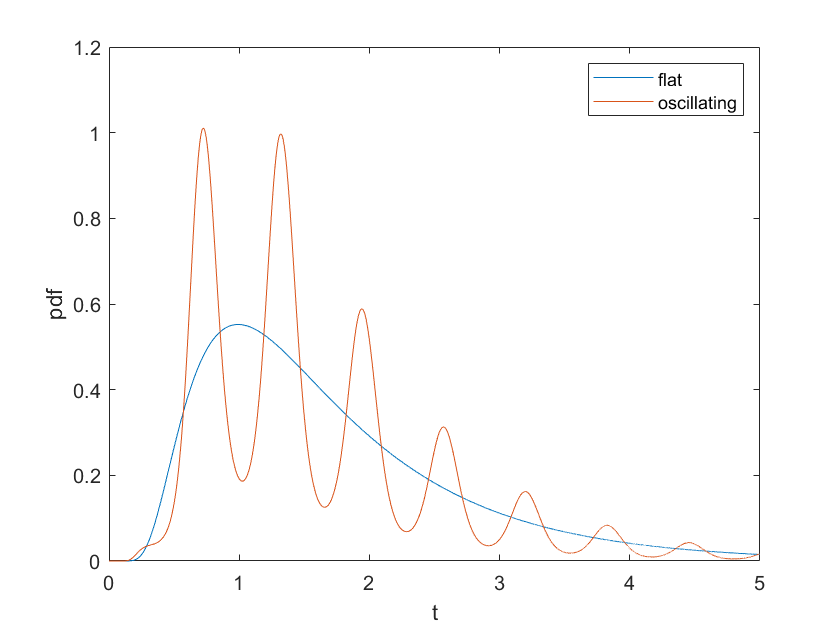

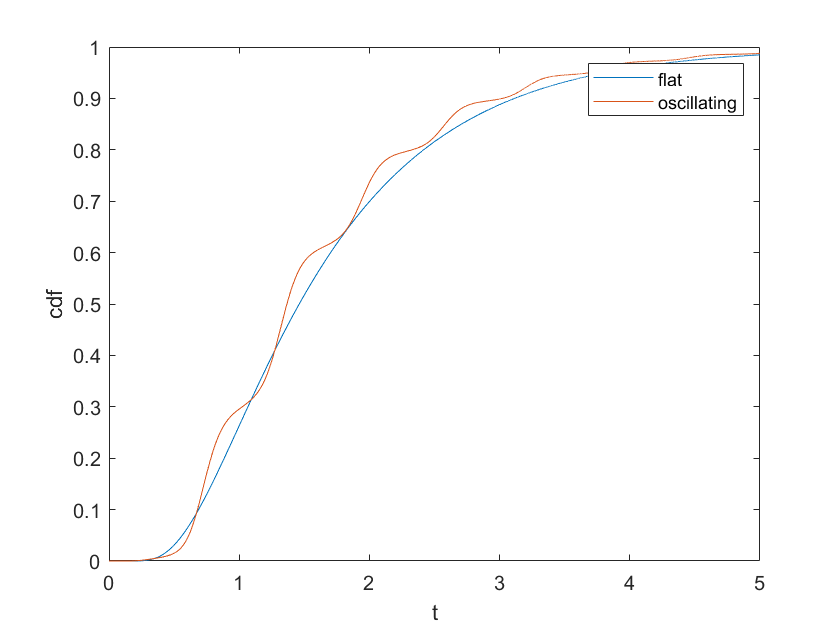

We show the probability density function (pdf) and the cumulative density function (cdf) for the hitting time in Figure 7. It is interesting to note that the undulation of the boundary causes considerable variations in the pdfs, which are naturally less pronounced for the corresponding cdfs.

| Figure 7 near here. |

5.7 Abel integral equation

Consider Eq. (17), which we got for the standard OU process. For small values of , this equation can be approximated by an Abel integral equation of the second kind.

This equation can be solved analytically using direct - inverse Laplace transforms. The direct Laplace transform yields

Then, can be expressed as

Taking the inverse Laplace transform, we get the final expression for

Alternatively, one can represent an analytical solution of an Abel equation

in the form

where

see [45].

Abel equations naturally arise in many financial mathematics situations, mainly, when fractional differentiation is involved, see, e.g., [2].

6 The supercooled Stefan problem

The Stefan problem is of great theoretical and practical interest, see, e.g., [23, 48, 10] and references therein. The classical Stefan problem studies the evolving boundary between the two phases of the same medium, such as ice and water. Thus, this problem boils down to solving the heat equation with a free boundary, which is determined by a matching condition. The main equations for the supercooled Stefan problem, are very similar to the mean-field banking equations:

where is the negative temperature profile, and is the liquid-solid boundary. The location of the boundary is determined by the matching condition

As usual, we represent as , where solves the following IBVP

By using Eq. (4) we get the following system of coupled Volterra equations:

| (18) |

where

System of integral equations (18) is very similar to system (11) and can be solved by the same token.

In this section, we deal with one of the rare instances when financial mathematics results can be successfully used in the broader applied mathematics context rather than the other way around.

7 The integrate-and-fire neuron excitation model

7.1 Governing equations

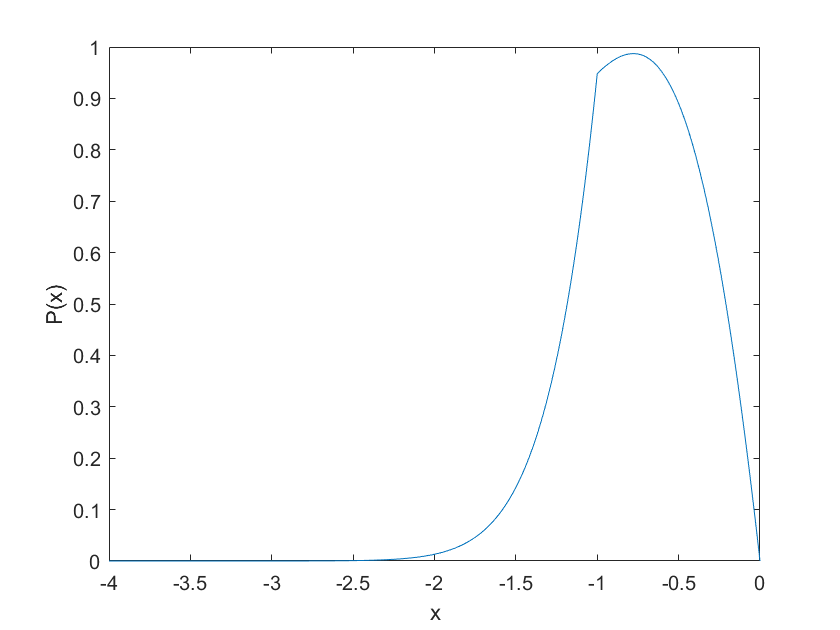

7.2 The stationary problem

Because the integrate-and-fire equations are probability-preserving, there exists a stationary solution, which solves the time-independent Fokker–Planck problem:

We represent in the form

where is the Heaviside function, and notice that

| (20) |

where are unknown constants, which have to be determined as part of the solution. In view of the boundary conditions, it is clear that

Moreover, since is continuous at the second matching condition (20) is satisfied automatically.

The method of separation of variables yields

while the method of variation of constants yields

where is Dawson’s integral,

Thus,

and

At the same time, in the stationary case, the probability density has to integrate to unity:

which is a nonlinear equation for , because both and are known functions of . Once this equation is solved numerically, the entire profile is determined. It is worth noting that the integral can be computed analytically:

while the second integral can be split into two parts, the first of which can be computed analytically, and the second one has to be computed numerically:

Thus, the corresponding nonlinear equation for can be written as

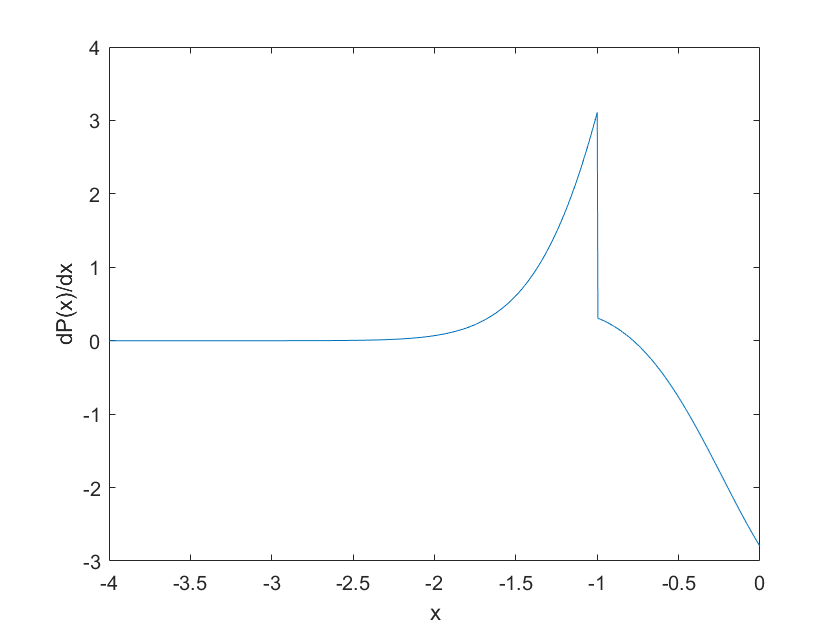

We show the stationary profile and its derivative in Figure 9. As expected, jump down at .

| Figure 9 near here. |

7.3 The nonstationary problem

First, we use the following transformation of variables:

and get the following IBVP:

Thus, by choosing in such a way that

or, explicitly,

we get the IBVP for the standard Ornstein-Uhlenbeck process:

As usual, we split as follows:

where the first term solves the governing equation and satisfies the initial, but not the boundary conditions, while solves the following IBVP:

where

We apply the familiar change of variables (15) and get the following IBVP for :

| (21) |

where

Denoting by , we can split the IBVP (21) into two IBVPs:

and a matching condition:

We can now use results from Section 2 to reduce these equations to a very efficient (but highly nonlinear) system of Volterra integral equations. Due to the lack of space, an analysis of the corresponding system will be presented elsewhere.

8 Conclusions

In this document, we describe an analytical framework for solving several relevant and exciting problems of financial engineering. We show that the EMHP is a powerful tool for reducing partial differential equations to integral equations of Volterra type. Due to their unique nature, these equations are relatively easy to solve. In some cases, we can solve these equations analytically by judiciously using the Laplace transform. In other cases, we can solve them numerically by constricting highly accurate numerical quadratures. We demonstrate that the EMHP has numerous applications in mathematical finance and far beyond its confines.

Acknowledgement 1

Valuable discussions with our Investimizer colleagues Dr. Marsha Lipton, and Dr. Marcos Lopez de Prado are gratefully acknowledged.

Acknowledgement 2

The contents of this document were presented at a conference at the Hebrew University of Jerusalem in December 2018. Exemplary efforts of the organizers, Dr. David Gershon and Prof. Mathieu Rosenbaum, are much appreciated.

Acknowledgement 3

Some of the ideas described in this document were developed jointly with Dr. Vadim Kaushansky and Prof. Christoph Reisinger.

References

- [1] Alili, L., Patie, P. and Pedersen, J.L. (2005). Representations of the first hitting time density of an Ornstein–Uhlenbeck process. Stoch. Models, 21(4), 967–980.

- [2] Andersen, L. and Lipton, A. (2013). Asymptotics for exponential L´evy processes and their volatility smile: survey and new results. International Journal of Theoretical and Applied Finance, 16 (1) 1350001 (98 pages).

- [3] Avellaneda, M. and Zhu, J. (2001). Distance to default. Risk, 14(12), 125–129.

- [4] Black, F. and and Cox, J.C. (1976). Valuing corporate securities: Some effects of bond indenture provisions, J. Finance 31(2), 351–367.

- [5] Bluman, G.W. (1980). On the transformation of diffusion processes into the Wiener process. SIAM. J. Appl. Math., 39(2), 238–247.

- [6] Borodin, A.N. and Salminen, P. (2012). Handbook of Brownian Motion: Facts and Formulae, (Birkhäuser, Basel).

- [7] Breiman, L. (1967). First exit times from a square root boundary. In Fifth Berkeley Symposium, Vol. 2, pp. 9–16 (Berkeley).

- [8] Carrillo, J., Gonz´alez, M., Gualdani, M. and Schonbek, M. (2013). Classical solutions for a nonlinear Fokker-Planck equation arising in computational neuroscience, Comm. Partial Differential Equations 38(3), 385–409.

- [9] Cherkasov, I.D. (1957). On the transformation of the diffusion process to a Wiener process. Theor. Probab. Appl., 2(3), 373–377.

- [10] Delarue, F., Nadtochiy, S. and Shkolnikov, M. (2017). Global solutions to the supercooled Stefan problem with blow-ups: regularity and uniqueness. arXiv preprint.

- [11] Einstein, A. (1905). Über die von der molekularkinetischen theorie der wärme geforderte bewegung von in ruhenden flüssigkeiten suspendierten teilchen. Ann. Phys., 322(8), 549–560.

- [12] Eisenberg, L. and Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2), 236–249.

- [13] Finkelstein V and Lardy, J. P. (2001) Assessing default probabilities from equity markets: simple closed-form solution. Presented at the ICBI Global Derivatives Conference, Juan les Pins.

- [14] Fortet, R. (1943) Les fonctions altatoires du type de markoff associees a certaines equations linlaires aux dfrivees partielles du type parabolique. J. Math. Pures Appl., 22, 177–243.

- [15] Göing-Jaeschke, A. and Yor, M. (2003). A clarification note about hitting times densities for Ornstein–Uhlenbeck processes. Finance Stoch., 7(3), 413–415.

- [16] Hambly, B., Ledger, S., and Sojmark, A. (2018). A McKean–Vlasov equation with positive feedback and blow-ups. arXiv preprint.

- [17] Hilberink. B., and Rogers, L. (2002) Optimal capital structure and endogenous default Finance and Stochastics 6, 237–263.

- [18] Hull, J., and White, A. (2001). Valuing credit default swaps, II. Journal of Derivatives 8(3), 12–22.

- [19] Hyer, T., Lipton, A., Pugachevsky, D., and Qui, S. (1998). A hidden-variable model for risky bonds. Bankers Trust working paper.

- [20] Ichiba, T., Ludkovski, M., and Sarantsev, A. (2018). Dynamic contagion in a banking system with births and defaults. arXiv preprint.

- [21] Itkin, A. and Lipton, A. (2015). Efficient solution of structural default models with correlated jumps and mutual obligations. International Journal of Computer Mathematics, 92(12), 2380–2405.

- [22] Itkin, A. and Lipton, A. (2017). Structural default model with mutual obligations. Review of Derivatives Research, 20,15–46.

- [23] Kamenomostskaja, S. L. (1961). On Stefan’s problem, Mat. Sb. (N.S.) 53 (95), 489–514.

- [24] Kartashov, E. (2001). Analytical Methods in the Theory of Heat Conduction of Solids. Vysshaya Shkola, Moscow 706.

- [25] Kaushansky, V. and Reisinger, C. (2018). Simulation of particle systems interacting through hitting times. arXiv preprint.

- [26] Leblanc, B. and Scaillet, O. (1998). Path dependent options on yields in the affine term structure model. Finance Stoch., 2(4), 349–367.

- [27] Leblanc, B., Renault, O. and Scaillet, O. (2000) A correction note on the first passage time of an Ornstein-Uhlenbeck process to a boundary. Finance Stoch., 4(1), 109–111.

- [28] Lewis, T. J. and Rinzel, J. (2003). Dynamics of spiking neurons connected by both inhibitory and electrical coupling, J. Comput. Neurosci. 14(3), 283–309.

- [29] Linetsky, V. (2004) Computing hitting time densities for CIR and OU diffusions: Applications to mean-reverting models. J. Comput. Finance, 7, 1–22.

- [30] Linz, P. (1985) Analytical and Numerical Methods for Volterra Equations (SIAM, Philadelphia, PA).

- [31] Lipton, A. (2001). Mathematical Methods for Foreign Exchange: A Financial Engineer’s Approach. World Scientific, Singapore.

- [32] Lipton, A. (2002). Assets with Jumps. Risk 15 (9), 149–153.

- [33] Lipton, A. (2016). Modern monetary circuit theory, stability of interconnected banking network, and balance sheet optimization for individual banks. International Journal of Theoretical and Applied Finance, 19(6).

- [34] Lipton, A. (2018) Financial Engineering: Selected Works of Alexander Lipton. World Scientific, Singapore.

- [35] Lipton, A. and Kaushansky, V. (2018). On the first hitting time density of an Ornstein-Uhlenbeck process. arXiv preprint.

- [36] Lipton, A. and Kaushansky, V. (2020). On the first hitting time density for a reducible diffusion process. Quantitative Finance. DOI: 10.1080/14697688.2020.1713394

- [37] Lipton, A. and Kaushansky, V. (2020). Physics and Derivatives: On Three Important Problems in Mathematical Finance. The Journal of Derivatives.

- [38] Lipton, A. and Lopez De Prado, M. (2020). A closed-form solution for optimal mean-reverting trading strategies. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3534445.

- [39] Lipton, A., Kaushansky, V. and Reisinger, C. (2019).Semi-analytical solution of a McKean–Vlasov equation with feedback through hitting a boundary. European Journal of Applied Mathematics. doi:10.1017/S0956792519000342.

- [40] Lopez De Prado, M. (2018). Advances in financial machine learning. John Wiley Sons, Hoboken, NJ.

- [41] Merton, R. (1974). On the pricing of corporate debt: the risk structure of interest rates. Journal of Finance 29, 449–470.

- [42] Nadtochiy, S. and Shkolnikov, M. (2017). Particle systems with singular interaction through hitting times: application in systemic risk modeling. arXiv preprint.

- [43] Nadtochiy, S. and Shkolnikov, M. (2018). Mean field systems on networks, with singular interaction through hitting times. arXiv preprint.

- [44] Ostojic, S., Brunel, N. and Hakim, V. (2009). Synchronization properties of networks of electrically coupled neurons in the presence of noise and heterogeneities, J. Comput. Neurosci. 26, no. 3, 369–392.

- [45] Polyanin, A.D. and Manzhirov, A.V. (1998). Handbook of Integral Equations, CRC Press, Boca Raton, FL.

- [46] Ricciardi, L.M. (1976). On the transformation of diffusion processes into the Wiener process. J. Math. Anal. Appl., 54(1), 185–199.

- [47] Ricciardi, L.M. and Sato, S. (1988). First-passage-time density and moments of the Ornstein–Uhlenbeck process. J. Appl. Probab., 25(1), 43–57.

- [48] Rubinstein, L. (1971). The Stefan Problem. Vol. 27 of Translations of Mathematical Monographs. American Mathematical Society, Providence, RI.

- [49] Von Smoluchowski, M. (1906). Zur kinetischen theorie der brownschen molekularbewegung und der suspensionen. Ann. Phys., 326(14), 756–780.

- [50] Tikhonov, A. N., and Samarskii, A. A.. (1963). Equations of Mathematical Physics. Dover Publications, New York. English translation.

- [51] Watson, N. A. (2012). Introduction to Heat Potential Theory. Number 182 in Mathematical Surveys and Monographs. American Mathematical Society, Providence, RI.