Multivariate Goodness-of-Fit Tests Based on Wasserstein Distance

Abstract

Goodness-of-fit tests based on the empirical Wasserstein distance are proposed for simple and composite null hypotheses involving general multivariate distributions. For group families, the procedure is to be implemented after preliminary reduction of the data via invariance. This property allows for calculation of exact critical values and -values at finite sample sizes. Applications include testing for location–scale families and testing for families arising from affine transformations, such as elliptical distributions with given standard radial density and unspecified location vector and scatter matrix. A novel test for multivariate normality with unspecified mean vector and covariance matrix arises as a special case. For more general parametric families, we propose a parametric bootstrap procedure to calculate critical values. The lack of asymptotic distribution theory for the empirical Wasserstein distance means that the validity of the parametric bootstrap under the null hypothesis remains a conjecture. Nevertheless, we show that the test is consistent against fixed alternatives. To this end, we prove a uniform law of large numbers for the empirical distribution in Wasserstein distance, where the uniformity is over any class of underlying distributions satisfying a uniform integrability condition but no additional moment assumptions. The calculation of test statistics boils down to solving the well-studied semi-discrete optimal transport problem. Extensive numerical experiments demonstrate the practical feasibility and the excellent performance of the proposed tests for the Wasserstein distance of order and and for dimensions at least up to . The simulations also lend support to the conjecture of the asymptotic validity of the parametric bootstrap.

keywords:

and

1 Introduction

Wasserstein distances are metrics on spaces of probability measures with certain finite moments. They measure the distance between two such distributions by the minimal cost of moving probability mass in order to transform one distribution into the other. Wasserstein distances have a long history and continue to attract interest from diverse fields in statistics, machine learning, and computer science, in particular image analysis; see for instance the monographs and reviews by Santambrogio (2015), Peyré and Cuturi (2019), and Panaretos and Zemel (2019).

A natural application of any meaningful distance between distributions is to the goodness-of-fit (GoF) problem—namely, the problem of testing the null hypothesis that a sample comes from a population with fully specified distribution or with unspecified distribution within some postulated parametric model . GoF problems certainly are among the most fundamental and classical ones in statistical inference. Typically, GoF tests are based on some distance between the empirical distribution and the null distribution or an estimated distribution in the null model . The most popular ones are the Cramér–von Mises (Cramér, 1928; von Mises, 1928) and Kolmogorov–Smirnov (Kolmogorov, 1933; Smirnov, 1939) tests, involving distances between the cumulative distribution function of and the empirical one. Originally defined for univariate distributions only, they have been extended to the multivariate case, for instance in Khmaladze (2016), who proposes a test that has nearly all properties one could wish for, including asymptotic distribution-freeness, but whose implementation is computationally heavy and quickly gets intractable.

Many other distances have been considered in this context, though. Among them, distances between densities (after kernel smoothing) have attracted much interest, starting with Bickel and Rosenblatt (1973) in the univariate case. Bakshaev and Rudzkis (2015) recently proposed a multivariate extension; the choice of a bandwidth matrix, however, dramatically affects the outcome of the resulting testing procedure. Fan (1997) considers a distance between characteristic functions, which accommodates arbitrary dimensions; the idea is appealing but the estimation of the integrals involved in the distance seems tricky. McAssey (2013) proposes a heuristic test that relies on a comparison of the empirical Mahalanobis distance with a simulated one under the null. Still in a multivariate setting, Ebner, Henze and Yukich (2018) define a distance based on sums of powers of weighted volumes of th nearest neighbour spheres.

The use of the Wasserstein distance for GoF testing has been considered mostly for univariate distributions (Munk and Czado, 1998; del Barrio et al., 1999; del Barrio et al., 2000; del Barrio, Giné and Utzet, 2005). For the multivariate case, available methods are restricted to discrete distributions (Sommerfeld and Munk, 2018) and Gaussian ones (Rippl, Munk and Sturm, 2016). Indeed, serious difficulties, both computational and theoretical, hinder the development of Wasserstein GoF tests for general multivariate continuous distributions, particularly in the case of composite null hypotheses. Such hypotheses are generally more realistic than simple ones. Of particular practical importance is the case of location–scale and location–scatter families: tests of multivariate Gaussianity, tests of elliptical symmetry with given standard radial density, etc., belong to that type. Although the asymptotic null distribution of empirical processes with estimated parameters is well known (van der Vaart, 1998, Theorem 19.23), the actual exploitation of that theory in GoF testing remains problematic because of the difficulty of computing critical values.

The aim of this paper is to explore the potential of the Wasserstein distance for GoF tests of simple (consisting of one fully specified distribution) and composite (consisting of a parametric family of distributions) null hypotheses involving continuous multivariate distributions. The tests we are proposing are based on the Wasserstein distance between the empirical distribution of the data or estimated residuals on the one hand and a model-based estimate thereof on the other hand. We concentrate on the continuous case, i.e., the distributions under the null hypothesis are absolutely continuous with respect to the -dimensional Lebesgue measure. The test statistic involves the Wasserstein distance between a discrete empirical distribution and a continuous distribution specified by the null hypothesis. Calculating such a distance requires solving the semi-discrete transportation problem, an active area of research in computer science.

In case of a simple null hypothesis, the null distribution of the test statistic does not depend on unknown parameters. Exact critical values can be calculated with arbitrary precision via a Monte Carlo procedure, by simulating from the null distribution and computing empirical quantiles.

Exact critical values can also be computed for Wasserstein tests for the GoF of a group family, that is, a model that arises by applying a transformation group to some specified distribution (Lehmann and Casella, 1998, pp. 16–23). If the parameter estimate is equivariant, the data can be reduced in such a way that their distribution no longer depends on the unknown parameter. The Wasserstein distance between this parameter-free distribution and the empirical distribution of the reduced data then provides a test statistic whose null distribution does not depend on the unknown parameter either. Important special cases include elliptical distributions with known radial distribution and unknown location vector and scatter matrix. In particular, our approach yields a novel test for multivariate normality with unknown mean vector and covariance matrix.

For general parametric models, the test statistic measures the Wasserstein distance between the empirical distribution and the model-based one with estimated parameter. A reduction via invariance is no longer possible and we rely on the parametric bootstrap to calculate critical values. Still, some parameters, such as location-scale parameters, can be factored out, again by relying on transformation groups. The question whether the parametric bootstrap has the correct size under the null hypothesis remains open. A proof of that property would require asymptotic distribution theory for the empirical Wasserstein distance—a hard and long-standing open problem, which we briefly review in Section 1.2, the solution of which is beyond the scope of this paper. Monte Carlo experiments, however, support our conjecture that the parametric bootstrap has the correct size at least asymptotically.

In all cases, even in the general parametric case, we show that our Wasserstein GoF tests are consistent against fixed alternatives, that is, the null hypothesis under such alternatives is rejected with probability tending to one as the sample size tends to infinity. For the general parametric case, the proof relies on the uniform consistency in probability of the empirical distribution with respect to the Wasserstein distance, uniformly over families of distributions that satisfy a uniform integrability condition. To the best of our knowledge, this result is new.

We conduct an extensive simulation study to assess the finite-sample performance of the Wasserstein tests of order in comparison to other GoF tests. The set-up involves both simple and composite null hypotheses as well as a wide variety of alternatives. The experiments lend support to the conjecture that the parametric bootstrap is valid asymptotically. In comparison to other GoF tests available in the literature, the Wasserstein test demonstrates good power. This is especially true for the test of multivariate normality, where, out of the many available tests in the literature, we select the ones of Royston (1983), Henze and Zirkler (1990) and Rizzo and Székely (2016) as benchmarks.

In a recent strand of literature, measure transportation serves to link a multivariate probability measure to a standard reference distribution, yielding novel concepts of multivariate ranks, signs, and quantiles (Carlier et al., 2016; Chernozhukov et al., 2017; Hallin et al., 2020). Here we do not make this step, as the Wasserstein distances we are considering are between distributions defined on the sample space.

The outline of the paper is as follows. In the remainder of this introduction, we introduce the Wasserstein distance (Section 1.1), review the asymptotic theory of empirical Wasserstein distance (Section 1.2), and provide some information on the computational methods for the semi-discrete transportation problem underlying the implementation of the Wasserstein GoF tests (Section 1.3). In Section 2, we give a formal description of the GoF test procedure for simple null hypotheses. Section 3 addresses the composite null hypothesis that the unknown distribution belongs to some group family. Composite null hypotheses covering general parametric models are treated in Section 4. In Section 4.1 we mention a hybrid approach, where some components of the parameter vector are factored out by relying on a transformation group. In Section 5, finally, we report on the results of our numerical experiments. In Appendix A, the convergence of the empirical Wasserstein distance uniformly over certain classes of underlying distributions is stated and proved. Appendix B is related to the consistency of the parametric bootstrap. The other appendices contain further details on the simulation study.

1.1 Wasserstein distance

Let be the set of Borel probability measures on and let be the subset of such measures with a finite moment of order . For , let be the set of probability measures on with marginals and , i.e., such that and for Borel sets . The -Wasserstein distance between is

with the Euclidean norm. In terms of random variables and with laws and , respectively, the -Wasserstein distance is the smallest value of over all possible joint distributions of .

The -Wasserstein distance defines a metric on , which thereby becomes a complete separable metric space (Villani, 2009, Theorem 6.18 and the bibliographical notes). Convergence in the metric is equivalent to weak convergence plus convergence of moments of order ; see for instance Bickel and Freedman (1981, Lemmas 8.1 and 8.3) and Villani (2009, Theorem 6.9).

For univariate distributions and with distribution functions and , the -Wasserstein distance boils down to the -distance

| (1) |

between the respective quantile functions and . This representation considerably facilitates both the computation of the distance and the asymptotic theory of its empirical versions. Also, the optimal transport plan mapping to is immediate: if has no atoms, then , while monotonicity of implies the optimality of the coupling , see for instance Panaretos and Zemel (2019, Section 1.2.3).

1.2 Asymptotic theory: results and an open problem

To construct critical values for Wasserstein GoF tests of general parametric models, we will propose in Section 4 the use of the parametric bootstrap. In general, proving consistency of the parametric bootstrap requires having, under contiguous alternatives, non-degenerate limit distributions of the statistic of interest (Beran, 1997; Capanu, 2019). For Wasserstein distances involving empirical distributions, such results are still far beyond the horizon, as the following short survey will show.

Let be an i.i.d. (independent and identically distributed) sample from . The empirical distribution of the sample is , with the Dirac measure at . Assuming that has a finite moment of order , we are interested in the empirical Wasserstein distance .

According to Bickel and Freedman (1981, Lemma 8.4), the empirical distribution is strongly consistent in the Wasserstein distance: for an i.i.d. sequence with common distribution , we have almost surely as . Bounds and rates for the expectation of the empirical Wasserstein distance have been studied intensively; see Panaretos and Zemel (2019, Section 3.3) for a review. If is non-degenerate, then is at least of the order , and if is absolutely continuous, which is the case of interest here, the convergence rate cannot be faster than . Actually, the rate can be arbitrarily slow, even in the one-dimensional case (Bobkov and Ledoux, 2019, Theorem 3.3). Precise rates under additional moment assumptions are given, for instance, in Fournier and Guillin (2015). In Appendix A, we will show that the convergence in th mean takes place uniformly over families of probability measures satisfying a uniform integrability condition. For distributions on compact metric spaces, Weed and Bach (2019) provide sharp rates for in terms of what they coin the Wasserstein dimension of . For Lebesgue-absolutely continuous measures on , this dimension is just . Moreover, they exploit McDiarmid’s bounded difference inequality to derive a concentration inequality of around its expectation.

Asymptotic results on the distribution of the empirical Wasserstein distance in dimension are, however, surprisingly scarce. The question is whether there exist sequences and such that converges in distribution to a non-degenerate limit. Although this problem has already attracted a lot of attention, a general answer remains elusive.

The one-dimensional case is well-studied thanks to the link (1) to empirical quantile processes (del Barrio, Giné and Utzet, 2005; Bobkov and Ledoux, 2019). For discrete distributions, large-sample theory for the empirical Wasserstein distance is available too (Sommerfeld and Munk, 2018; Tameling, Sommerfeld and Munk, 2019). For multivariate Gaussian distributions, a central limit theorem for the empirical Wasserstein of order between the true distribution and the one with estimated parameters is given in Rippl, Munk and Sturm (2016). Although interesting and useful for GoF testing (see Section 5.1.1), this result does not cover the empirical distribution .

Ambrosio, Stra and Trevisan (2018) exploit the possibility to linearize the -Wasserstein distance in dimension in case the optimal transport plan is close to the identity. The technique requires balancing the errors due to the dual Sobolev norm approximation and a smoothing step. Mena and Niles-Weed (2019) derive a limit theorem for the empirical entropic optimal transport cost. We refer to the latter for an introduction to optimal transport with entropic regularization. Recent progress has been booked in Goldfeld and Kato (2020), who obtain a central limit theorem for the empirical -Wasserstein distance after smoothing the empirical and the true distributions with a Gaussian kernel.

Important advances on the limit distribution have been made by del Barrio and Loubes (2019) who obtained results under fixed alternatives. For general for some , they establish a central limit theorem for

The result is proved using the Efron–Stein inequality combined with stability of optimal transport plans. Unfortunately, if , the asymptotic variance is zero, meaning that the random fluctuations of around its mean are of order smaller than . The authors conclude that their proof technique is of little use for the case we are interested in. The crucial problem of the limiting distribution of the empirical Wasserstein distance thus remains an important and difficult open problem.

1.3 Computational issues

In the last decade, important numerical developments have taken place in the area of measure transportation. The problem to be faced here is the computation of the Wasserstein distance between a discrete and a continuous distribution, the so-called semi-discrete optimal transportation problem. Most algorithms to date rely on the dual formulation of the problem, assuming that the source continuous probability measure admits a density w.r.t. the Lebesgue measure on ; see, e.g., Santambrogio (2015, Section 6.4.2) for a didactic exposition. This formulation is the basis for the multi-scale algorithm for the squared Euclidean distance () developed in Mérigot (2011), with further improvements in Lévy (2015) and Kitagawa, Mérigot and Thibert (2017). It requires constructing a power diagram or Laguerre–Voronoi diagram, partitioning into convex polyhedra called power cells. With the Euclidean distance as cost function () the edges of the cells involved in the tessellation are no longer linear, making the computation more demanding (Hartmann and Schuhmacher, 2020). Genevay et al. (2016) show that a semi-discrete reformulation of the dual program can be tackled by the stochastic averaged gradient (SAG) method (Schmidt, Le Roux and Bach, 2017).

In our numerical experiments in Section 5, we assess the finite-sample performance of the test statistic based on the -Wasserstein distance for and for -variate distributions for . To the best of our knowledge, an implementation of the SAG method is not yet available in R (R Core Team, 2018). After preliminary tests and running time assessment, we made the following choices of algorithms and implementations:

- •

-

•

In all other cases ( or ), we relied on our own C implementation of the SAG method as employed in Genevay et al. (2016).

A first version of the package making our implementation available is to be found on https://github.com/gmordant/WassersteinGoF.

2 Wasserstein GoF tests for simple null hypotheses

Let be an independent random sample from some unknown distribution . For some given fixed , consider testing the simple null hypothesis

based on the observations . Note that , under the alternative, is not required to have finite moments of order .

Let denote the empirical distribution and consider the test statistic

| (2) |

the th power of the -Wasserstein distance between and the distribution specified by the null hypothesis. Having bounded support, trivially belongs to , so that is well defined.

Actual computation of amounts to solving the semi-discrete optimal transport problem. In the numerical experiments in Section 5, we show results for . The theory, however, is developed for general .

Let for denote the distribution function of the test statistic under . Here, stands for the distribution under of the observation , the -fold product measure of on . The -value of the test statistic is , while the critical value for a test of size is

| (3) |

The test we propose is then

| (4) |

The exact size of the GoF test in (4) is , with equality if and only if is continuous at . The type I error is thus bounded by the nominal size , and often equal to it. The null distribution of depends on , so that needs to be calculated for each separately.

Although -values and critical values usually cannot be calculated analytically, they can be approximated with any desired degree of precision via the following simple Monte Carlo algorithm. Draw a large number of independent random samples of size from , compute the test statistic for each such sample, and approximate by the empirical distribution function of the simulated test statistics. Critical values and -values then can be calculated from the approximated . By the Donsker theorem, any desired accuracy can be achieved by drawing sufficiently many samples.

Under the alternative hypothesis, the test rejects the null hypothesis with probability tending to one, i.e., is consistent against any fixed alternative .

Proposition 1 (Consistency).

For every , the test is consistent against any with :

Proof.

Fix . For any , the critical value tends to zero as . Indeed, by Bickel and Freedman (1981, Lemma 8.4), we have in -probability and thus for any . It follows that, for every and every , we have for all sufficiently large .

Let with . We consider two cases according as has finite moments of order or not.

First, suppose that . Still by Bickel and Freedman (1981, Lemma 8.4), we have in -probability as . The triangle inequality for the metric yields

in -probability. Hence in -probability as . But since and by assumption. It follows that , as required.

Second, suppose that . Let denote the Dirac measure at . Since is a metric, the triangle inequality implies

Now, is a constant and . As the expectation of under is infinite, the law of large numbers implies that in -probability as . The same then holds for and thus

3 Wasserstein GoF tests for group families

Let and let be a group of measurable transformations . That is, should be closed under composition ( implies ) and under inversion ( implies ). If the random variable has distribution , the random variable has distribution , where the subscripted symbol denotes the push-forward of a measure by a measurable function. Let be the group family generated by and . We assume further that the transformation is identifiable, that is, the map is one-to-one, so that implies that and have different distributions, with again . Note that for any element of we have , so that the choice of in is in some sense arbitrary.

Group families form one of the two principal classes of models covered in Lehmann and Casella (1998). Here are some prominent examples of transformation groups on and some models that they generate.

Example 1 (Location–scale families).

For , define by for . The model is the location-scale family generated by . We can also consider just the location family generated by the subgroup and the scale family generated by the subgroup . In dimension , we can generate in this way the normal and exponential families, for instance.

Example 2 (Affine transformations and elliptical distributions).

For and non-singular, define by for . If is the -variate standard normal distribution , then is the family of all -variate Gaussian distributions with positive definite covariance matrix. More generally, if is spherically symmetric around the origin, then is the family of elliptical distributions with a given characteristic generator and positive definite scatter matrix (Cambanis, Huang and Simons, 1981; Fang, Kotz and Ng, 1990). Besides the Gaussian family, another common example is the multivariate Student t distribution with a fixed number of degrees of freedom. For elliptical families, the matrix is not identifiable from the model but only the matrix is. Identifiability can be restored by restricting to the set of lower triangular matrices with positive elements on the diagonal.111For every symmetric positive definite matrix , there exists a unique lower triangular matrix with positive diagonal elements, called Cholesky triangle, producing the Cholesky decomposition (Golub and Van Loan, 1996, Theorem 4.2.5). Note that the case of elliptical distributions with possibly degenerate scatter matrices is not covered here, as the corresponding affine transformation is not invertible.

In the examples above, the transformation group is parametrized by a Euclidean parameter with for some dimension , so that . We will assume this to be the case in general and write . The model then takes the form . The mappings and are assumed to be one-to-one. The parametrization then is also one-to-one, i.e., the model parameter is identifiable. Models generated by infinite-dimensional transformation groups exist as well, but the theory here is intended for the finite-dimensional situation, as the conditions to come seem too restrictive otherwise.

Let for some . Assume that, for all , there exists such that

| (5) |

Then it is easy to verify that belongs to for every too and, therefore, . This condition on is fulfilled for the transformations in Examples 1 and 2.

Let be a group family as just described. Given an i.i.d. sample from some unspecified , we wish to test the hypothesis

| (6) |

The parameter of the transformation is an unknown nuisance. In contrast to Section 2, the null hypothesis is thus a composite one. An important special case is when is the -variate standard normal distribution and is the affine group in Example 2: the testing problem (6) then concerns the hypothesis of multivariate normality with unspecified positive definite covariance matrix.

Our testing strategy is to choose some estimator for and compute “residuals” of the form

| (7) |

yielding an empirical distribution . The test statistic we propose is

| (8) |

If the null distribution of does not depend on the unkown parameter , then we can compute critical values and -values for as if the true distribution is . As in Section 2, the null distribution of can then be computed up to any desired accuracy via Monte Carlo random sampling from , and this prior to having observed the sample.

For any , let denote the mapping characterized by , so that . The estimator is said to be equivariant (Lehmann and Casella, 1998, Definition 2.5) if for every and for every , we have

| (9) |

Equivariance is a natural symmetry requirement and is satisfied for many common estimators. For a location parameter, it is satisfied by the mean and the median, or in fact any weighted average of the order statistics. For a scale parameter, it is satisfied by the standard deviation and by the mean or median absolute deviation. For the affine group in Example 2 with restricted to be lower triangular and with positive diagonal elements, it is satisfied by the lower Cholesky triangle of the empirical covariance matrix. The proof of the latter is elementary and follows from the uniqueness of the Cholesky decomposition and the fact that the set of lower triangular matrices with positive diagonal elements forms a multiplicative group. Equivariance is also satisfied by maximum likelihood estimators provided the transformations are diffeormorphisms: by the change-of-variables formula, maximizes the likelihood given the sample if and only if maximizes the likelihood given the sample .

In the group model , if the estimator is equivariant, then for an i.i.d. sample from , the joint distribution of in (7) does not depend on and is the same as if were an i.i.d. sample from . As a consequence, the distribution of in (8) under any is the same as under . Let denote its cumulative distribution function. The -value of the observed test statistic is

while the critical value at level is

For the testing problem (6), we propose the test

| (10) |

The actual size of the test is , with equality if and only if is continuous in . Formally, the case of a single null hypothesis in Section 2 can be seen as a special case by letting and the trivial group containing only the identity mapping.

Since the null distribution does not depend on any unknown parameter, critical values and -values values can be computed with arbitrary precision by a Monte Carlo algorithm as we did in Section 2. The difference is now that we generate samples from . Note that the critical values can be computed prior to having seen the data.

To show that the test is consistent, we need an extra assumption on : for every there exists such that for all in some neighbourhood of , we have

| (11) |

The condition is fulfilled for the transformation groups and parametrizations in Examples 1 and 2. For the affine group in Example 2, the property (11) follows from continuity of matrix inversion with respect to the matrix norm induced by the Euclidean norm. We will also need weak consistency of the estimator: for every , we have as in -probability. To prove this for the affine group in Example 2, it is helpful to know that the map that sends a positive definite symmetric matrix to its Cholesky triangle is differentiable (Smith, 1995) and thus continuous.

Proposition 2 (Consistency against fixed alternatives).

The pseudo-parameter in Proposition 2(ii) depends on the estimator: for instance, in a location-scale model and if , if we estimate the location and scale parameters by the empirical mean and standard deviation, respectively, then denotes the vector of population means and standard deviations.

Proof.

(i) The sample is equal in distribution to for some , where is an i.i.d. sample from . Since we are interested in convergence in probability, we can then in fact suppose that for all and compute probabilities under .

The empirical distribution of is denoted by . By the triangle inequality for the Wasserstein distance,

| (12) |

Since has a finite moment of order , the second term on the right-hand side converges to zero in probability by Bickel and Freedman (1981, Lemma 8.4).

To bound the first term on the right-hand side of the previous equation, consider the coupling of and via the discrete uniform distribution on the pairs for . It follows that

where is the estimated parameter from . Let denote the parameter that corresponds to the identity transformation: for all . Then and, by assumption, as in probability. Let be small enough so that (11) holds for all with . Then, on the event that , we have

As , the weak consistency of and the law of large numbers imply that, in probability,

We conclude that both terms in the bound (12) for converge to zero in probability. Hence the same is true for .

(ii) By (i), it follows that for every . It is thus sufficient to show that, under the alternative hypothesis, there exists such that .

Let , that is, is the law of , where is the inverse transformation of and where has law . By assumption, , for otherwise . Also, , since and since each in satisfies (5).

Put for , an i.i.d. sample from . Let be its empirical distribution. The estimated residuals are . By the same argument as in (i), we have

as in probability. By the continuous mapping theorem, it follows that as in probability. But then as in probability, and the null hypothesis is rejected with probability tending to one. ∎

4 Wasserstein GoF tests for general parametric families

Extending the scope of Section 3, consider the problem of testing whether the unknown common distribution of a sample of observations belongs to some parametric family of distributions on . The parameter space is some metric space and the map is assumed to be one-to-one and continuous in a sense to be specified. Given an independent random sample from some unknown distribution , the goodness-of-fit problem consists of testing

| (13) |

Assume that every has a finite moment of order , that is, . Recall that denotes the empirical distribution of the sample. The test statistic we propose is

| (14) |

where is some consistent (under ) estimator sequence of the true parameter . The distribution of under in (13) being for some , let for denote the null distribution function of the test statistic. As -value and critical value, we would like to take

| (15) |

respectively, for some . This choice is infeasible, however, since the true parameter is unknown. Therefore, we propose to replace by the bootstrapped quantity , yielding the test

| (16) |

We reject as soon as exceeds the critical value at the estimated parameter. The substitution of by qualifies as a parametric bootstrap.

To compute the critical value in practice, we rely, as before, on a Monte Carlo approximation: resample from , compute the test statistic, and approximate by the empirical distribution function of the resampled test statistics. By the Dvoretzky–Kiefer–Wolfowitz inequality (Massart, 1990), the difference between and its Monte Carlo approximation can be controlled explicitly and uniformly in and in the unknown parameter, and this in terms of the Monte Carlo sample size only. To speed up the calculations in case of a low-dimensional parameter space, we pre-compute an approximation of the critical value function in this way for in a finite grid and then compute by interpolation and/or smoothing.

Under the null hypothesis and if the true parameter is , the size of the test is now the random quantity

In contrast to Sections 2 and 3, it is no longer guaranteed that this risk is bounded by . The question remains open whether under the null hypothesis the actual size of the test indeed converges to . To prove this conjecture would require non-degenerate limit distribution theory for , not only for fixed , but even for sequences converging to at certain rates which depend on the model under study (Beran, 1997; Capanu, 2019). As discussed in Section 1.2, such asymptotic distribution theory is still far beyond the horizon. Our numerical experiments in Section 5, however, support the conjecture that the parametric bootstrap produces a test with the right asymptotic size. For any , any , and a sufficiently regular parametric model and estimator sequence , we conjecture that converges to one as . In Appendix B, we provide a theoretical justification of the consistency of the parametric bootstrap in the univariate case, for which the asymptotic distribution theory of the empirical Wasserstein distance is well developed.

Nevertheless, against a fixed alternative, the consistency of the test (16) based on the parametric bootstrap can be established theoretically. The key is a law of large numbers for the empirical distribution in Wasserstein distance uniformly over classes of distributions that satisfy a uniform integrability condition, see Appendix A. For the parameter estimator , we assume weak consistency locally uniformly in : if denotes the metric on and if denotes the collection of compact subsets of , we will require that

| (17) |

As illustrated in Remark 1 below, this condition is satisfied, for instance, for moment estimators of a Euclidean parameter under a uniform integrability condition.

Proposition 3 (Consistency).

Let , for , be a model indexed by a metric space . Assume the following conditions:

-

(a)

the map is one-to-one and -continuous;

-

(b)

is weakly consistent locally uniformly in , i.e., (17) holds.

Then, the following properties hold:

-

(i)

in -probability locally uniformly in , i.e.,

-

(ii)

the critical values tend to zero uniformly in , i.e.,

-

(iii)

for every such that there exists with

we have .

Proof.

(i) By the triangle inequality, it follows that

| (18) |

for all . It is then sufficient to show that, for any compact , each of the -distances on the right-hand side of (18) converges to in -probability uniformly in .

First, since is compact and is -continuous, the set

is compact in equipped with the -distance. By Bickel and Freedman (1981, Lemma 8.3(b)) or Villani (2009, Definition 6.8(b) and Theorem 6.9) and a subsequence argument, it follows that is uniformly integrable with respect to , i.e.,

Corollary 1 then implies that in -probability as , uniformly in .

Second, as is compact and is -continuous, there exists, for every scalar , a scalar such that222This is a slight generalization of the well-known property that a continuous function on a compact set is uniformly continuous. As a proof, fix and consider for each a scalar such that for all with we have . Cover by open balls with centers and radii . By compactness, extract a finite cover with centers . Put . For every and with , there exists such that and then also . By the triangle inequality, .

It follows that

By condition (b), the latter probability converges to as uniformly in .

(ii) Fix , , and . By (i), there exists an integer such that

By definition of the critical values, also for all and .

(iii) Let and be as in the statement. Put . We have

In view of (ii), we have as , so that it is sufficient to show that there exists , depending on and , such that . Consider two cases, and , according as has a finite moment of order or not.

First, suppose that . We have for every while the map is continuous. As is compact, . On the event , the triangle inequality implies

We obtain that

As and , the latter probability converges to one by the assumption made on and the fact that in -probability as .

Second, suppose that . Since is continuous, is finite, with as in (iii) and the Dirac measure at . By an argument similar to the second part of the proof of Proposition 1, it follows that as . ∎

Remark 1 (Uniform consistency).

Under a mild moment condition, the uniform consistency condition (b) in Proposition 3 is satisfied for method of moment estimators—call them moment estimators—of a Euclidean parameter . In the method of moments, an estimator of is obtained by solving (with respect to ) the equations

for some given -tuple of functions such that : is a homeomorphism between and ; see, for instance, van der Vaart (1998, Chapter 4). The consistency of uniformly in for any compact then follows from the uniform consistency over of as an estimator of for such . By van der Vaart and Wellner (1996, Proposition A.5.1), a sufficient condition for the latter is that the functions are -uniformly integrable for , i.e.,

Since for , a further sufficient condition is that there exists such that for .

Remark 2 (Parameter estimate under the alternative).

Remark 3 (Non locally compact parameter spaces).

Proposition 3 allows for infinite-dimensional parameter spaces . An example would be the space of all copulas of given dimension equipped with a metric that metrizes weak convergence, a space that is still compact thanks in view of Prohorov’s theorem. If is not locally compact, however, then condition (iii) is too severe and the compact set should be replaced by its enlargement for some sufficiently small (van der Vaart and Wellner, 1996, Definition 1.3.7). The conditions on the model and on the estimator should then be modified accordingly. We are grateful to an anonymous Referee for pointing this out.

4.1 Parametric models with group subfamilies

Consider again the testing problem (13). Sometimes the unknown parameter can be decomposed as , where, for fixed , the subfamily is a group family as in Section 3, generated by a group of transformations independent of . Think for instance of the case where is a vector of shape parameters and a vector of location–scale parameters, with the group of Example 1.

Suppose further that a weakly consistent estimator exists with the following two properties:

-

(i)

is invariant under : writing , we have

(19) for all and all possible samples .

-

(ii)

is equivariant as in (9).

Then we propose a hybrid approach: compute the estimated residuals

| (20) |

and form the test statistic

| (21) |

with the parameter yielding the identity transformation . For , the distribution function of the test statistic depends on but not on . It can thus be computed as if , that is, . The proof of this invariance property relies on (i)–(ii) above.

The actual -value of under is

while the critical value for a test of size is now

Both are infeasible, however, since the null distribution of depends on the unknown . We therefore compute -values and critical values under . More precisely, we apply the parametric bootstrap. The test thus takes the form

| (22) |

In practice, the distribution and the associated critical values are computed by Monte Carlo approximation, as described in the paragraph following (16). If the dimension of is sufficiently low, we can pre-compute the critical values for on a finite grid and then reconstruct the critical value function by interpolation or smoothing. The reduction from to thus brings a clear computational benefit.

We conjecture that, asymptotically, the test has the correct size under the null hypothesis. The obstacle for the proof is the same as before: required is the asymptotic distribution of the empirical Wasserstein distance, which is a very hard, long-standing open problem. In Section 5.3, we provide numerical support for the conjecture by an application to a five-dimensional distribution with separate location-scale parameters for each margin (ten parameters in total) and a single copula parameter. By exploiting invariance, the computation of the critical value is facilitated as the copula parameter remains as single argument.

5 Finite-sample performance of GoF tests

This section is devoted to a numerical assessment of the finite-sample performance of the Wasserstein-based GoF tests introduced in the previous sections. We compare them, whenever possible, with other tests. The case of a simple null hypothesis (Section 2) is treated in Section 5.1. The performances of various tests for multivariate normality, which is a special case of the hypothesis of a group model in Section 3, are compared in Section 5.2.1, along with an illustration involving a Student t distribution with known degrees of freedom in Section 5.2.2. Section 5.3 considers, in line with Section 4.1, the more general composite null hypothesis of a parametric family indexed by marginal location and scale parameters along with a copula parameter. Numerical results support the conjecture of the (asymptotic) validity of the parametric bootstrap for calculating critical values. To the best of our knowledge, no GoF test is available in the literature for such cases except for the method described by Khmaladze (2016), the numerical implementation of which, however, remains unsettled.

Throughout, we consider the Wasserstein distances of order . The level of the tests is set to 5%, the sample size is , and the number of replicates considered in the estimation of power curves is . As mentioned in Section 1.3 we relied on the R package transport (Schuhmacher et al., 2019) in case and and on our own C implementation of the algorithm proposed by Genevay et al. (2016) in all other cases. See also Appendix D for some details on the calculation of the critical values.

5.1 Simple null hypotheses

The setting is as in Section 2: given an independent random sample from some unknown , we consider testing the simple null hypothesis , where is fully specified.

Two other goodness-of-fit tests will be used as benchmarks: the test by Rippl, Munk and Sturm (2016), which is based on the -Wasserstein distance and is specific for multivariate Gaussian distributions, and the adaptation of the Kolmogorov–Smirnov test by Khmaladze (2016), which is based on empirical process theory. Both tests are described in some detail in Appendix C.

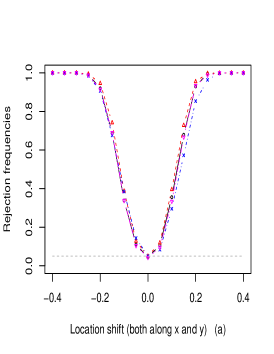

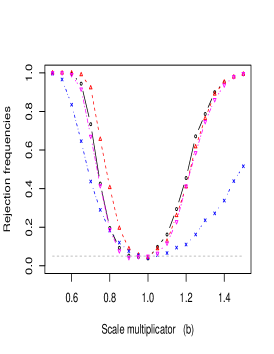

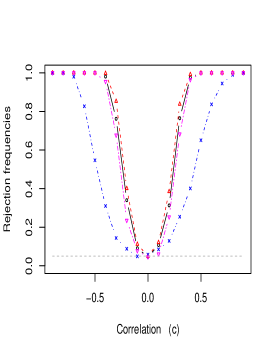

5.1.1 Bivariate Gaussian distribution

In Figure 1, we assess the performance of the GoF tests of where is a centered bivariate Gaussian with identity covariance matrix. The alternatives in panels (a)–(f) are as follows:

-

(a)

with location shift along the main diagonal (rejection frequencies plotted against );

-

(b)

(rejection frequencies plotted against );

-

(c)

with correlation (rejection frequencies plotted against );

-

(d)

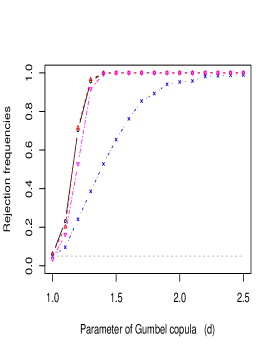

has standard normal margins but Gumbel copula with parameter (rejection frequencies plotted against );

-

(e)

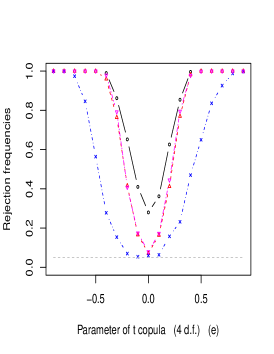

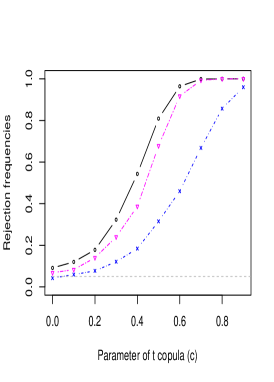

has standard Gaussian margins but a bivariate Student t copula with degrees of freedom and correlation parameter (rejection frequencies plotted against );333Note that is not Gaussian, even for .

-

(f)

is the “boomerang-shaped” Gaussian mixture described in Appendix E (rejection frequencies plotted against the mixing weight ).444The mixture is constructed so that the first and second moments of remain close to those of .

The Gumbel and Student t copula simulations in (d) and (e) were implemented from the R package copula (Hofert et al., 2018).

|

|

|

|

|

|

|

|

||

Inspection of Figure 1 indicates that the Khmaladze test, as a rule, is uniformly outperformed by the Rippl–Munk–Sturm and Wasserstein tests. The Rippl–Munk–Sturm test, of course, does relatively well under the Gaussian alternatives of panels (a)–(c) where, however, the Wasserstein test is almost as powerful (while its validity, contrary to that of the Rippl–Munk–Sturm test, extends largely beyond the Gaussian null hypothesis). Against the non-Gaussian alternatives in panels (d)–(f), the Wasserstein test has higher power than the Rippl–Munk–Sturm and Khmaladze tests, with the exception of the Gumbel copula alternative in panel (d), where the Rippl–Munk–Sturm and Wasserstein tests perform equally well. For the “boomerang mixture” of panel (f), the Rippl–Munk–Sturm test fails to capture the change in distribution. There is little difference between the Wasserstein tests with and , except for the -copula, where yields a more powerful test than .

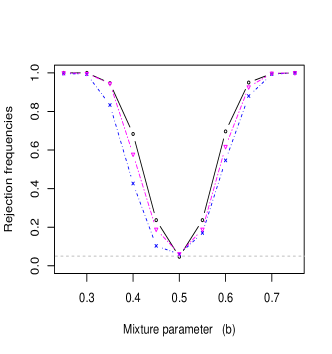

5.1.2 Mixture of bivariate Gaussian distributions

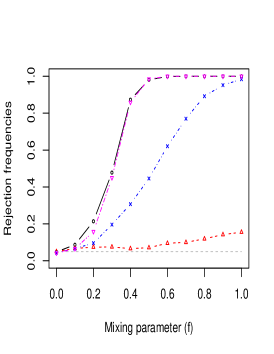

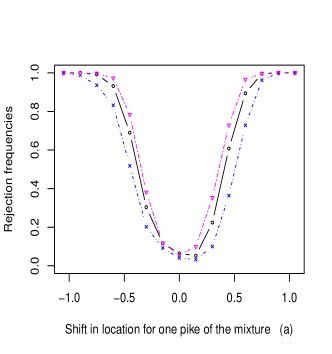

Figures 2 to 4 concern non-Gaussian null distributions , so that the Rippl–Munk–Sturm test no longer applies. In Figure 2, the null distribution is the Gaussian mixture The alternatives in both panels are as follows:

-

(a)

(rejection frequencies plotted against the location shift );

-

(b)

(rejection frequencies plotted against the mixing weight ).

Both Wasserstein tests have higher power than the Khmaladze (2016) test.

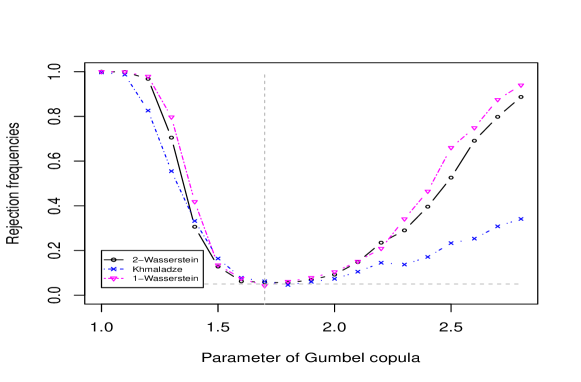

5.1.3 Gumbel copula and Gaussian marginals

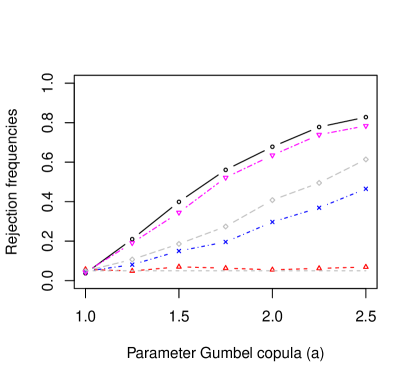

In Figure 3, has standard Gaussian margins and a Gumbel copula with parameter . The alternative is of the same form but with another value of the copula parameter . Again, the Wasserstein tests at have quite comparable performance and yield higher empirical powers in most cases.

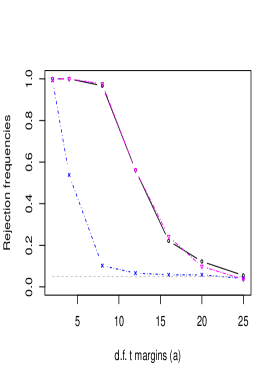

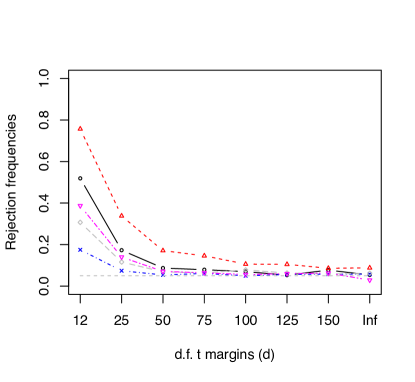

5.1.4 A five-dimensional Student distribution

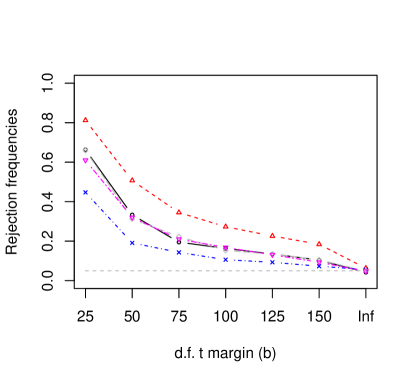

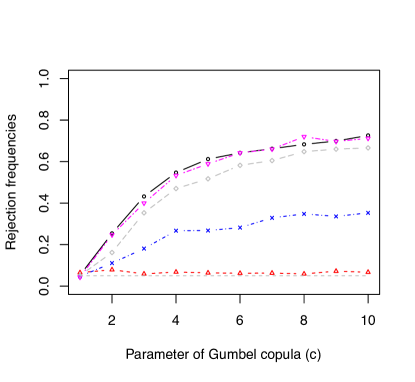

Let us turn now to a higher-dimensional case. In Figure 4, we test for the null hypothesis with a five-dimensional distribution with independence copula and Student margins. The following alternatives are considered:

-

(a)

A distribution with independence copula and Student margins. The rejection frequencies are plotted against .

-

(b)

A distribution with independence copula and margins equal to the Student distribution shifted by . The rejection frequencies are plotted against .

-

(c)

A distribution , where is the bivariate Student distribution with degrees of freedom and dependence parameter . Note that does not correspond to the null hypothesis. The rejection frequencies are plotted against .

The Khmaladze Kolmogorov–Smirnov test is most sensitive to the change in location (b), although the two Wasserstein tests perform quite well too. For the other two alternatives, the Wasserstein tests have much higher power than the Khmaladze test. For the Wasserstein test, there is little difference between and , except for case (c), in which the choice of yields higher power.

|

|

|

|

|

||

The alternatives (a)–(c) are explained in Section 5.1.4. In (c), no setting corresponds to the null hypothesis.

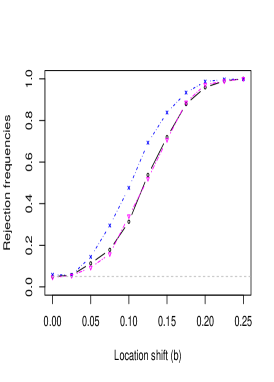

5.2 Elliptical families as group models

Elliptical distributions arise as group models for the group of affine transformations, see Example 2 in Section 3. Two notable examples are the multivariate normal family and the multivariate Student distribution with a fixed number of degrees of freedom. We assess the finite-sample performance of the Wasserstein test in (10) for with residuals computed by

with the sample mean vector and the lower Cholesky triangle of the empirical covariance matrix of .

5.2.1 Testing for multivariate normality

Testing for multivariate normality is a well-studied problem for which many tests have been put forward. As benchmarks, we will consider here the tests proposed in Royston (1983), Henze and Zirkler (1990), and Rizzo and Székely (2016). Royston’s test is a generalisation of the well-known Shapiro–Wilks test. It only tests whether the margins are Gaussian and ignores the dependence structure. The Henze–Zirkler test statistic is an integrated weighted squared distance between the characteristic function of the multivariate standard normal distribution and the empirical characteristic function of the empirically standardized data. Interestingly, Ramdas, García Trillos and Cuturi (2017) showed that the Wasserstein distance and the energy distance of Rizzo and Székely (2016) are connected, as the so-called entropy-penalized Wasserstein distance interpolates between them two. We borrowed the implementation of these tests from the R package MVN (Korkmaz, Goksuluk and Zararsiz, 2014). The test by Rippl, Munk and Sturm (2016) considered in Section 5.1 does not apply, since it only can handle fully specified Gaussian distributions, while here, the mean vector and covariance matrix are unknown.

In Figure 5, we consider dimensions [top row, panels (a) and (b)] and [bottom row, panels (c) and (d)]. Here are the alternative distributions :

-

(a)

A bivariate distribution with standard normal margins and a bivariate Gumbel copula with parameter . Rejection frequencies are plotted against .

-

(b)

A bivariate distribution with independent margins, one of which is standard normal while the other one is Student t with degrees of freedom. Rejection frequencies are plotted against .

-

(c)

A five-variate distribution given by , where is a bivariate distribution with Gumbel copula indexed by a parameter and with standard normal margins. Rejection frequencies are plotted against .

-

(d)

A five-variate distribution with independent margins, all of which are Student . Rejection frequencies are plotted against the common parameter .

|

|

|

|

|

|

|

The Wasserstein tests have the highest power against the copula alternatives in (a) and (c), while Royston’s test has no power at all, as expected. For the Student t alternatives in panels (b) and (d), Royston’s test comes out as most powerful, but the Wasserstein and energy tests (Rizzo and Székely, 2016) perform quite well too. It is also worth noticing that in panel (b), Royston’s test had a type I error of 6.3% and in panel (d) this rose to 8.8%.

5.2.2 Bivariate elliptical Student with unknown location and scatter

For fixed scalar , the -variate elliptical Student family with degrees of freedom and unknown location and scatter is generated by the affine transformation group in Example 2 applied to a spherical distribution whose radial density is that of the square root of a rescaled Fisher variable. In dimension , we consider the hypothesis that is of this form with .

Figure 6 provides a plot of rejection frequencies under bivariate skew-t alternatives (Azzalini, 2014) with marginal skewness parameters and . Simulations were based on the R package sn (Azzalini, 2020). In principle, the empirical process approach in Khmaladze (2016) leads to test statistics that are asymptotically distribution-free, but their numerical implementation involves a number of multiple integrals, the computation of which remains problematic.

5.3 General parametric families

Turning to more general parametric families , we investigate the finite-sample performance of the Wasserstein-based tests in Section 4. We consider models indexed by location, scale, and shape parameters. As in Section 4.1, the location-scale parameters are treated as stemming from the transformation group in Example 1 of Section 3, while for the shape parameters, we apply the parametric bootstrap. The test is thus the one we define in (22). We numerically investigate our conjecture that the test has the correct size asymptotically. In theory, the Khmaladze (2016) approach also applies, but its implementation is intricate and remains unsettled, especially when there are multiple parameters.

5.3.1 Gaussian margins and AMH copula

Let consist of the bivariate distributions with Gaussian marginals and an Ali–Mikhail–Haq (AMH) copula, yielding a five-dimensional parameter vector with AMH copula parameter , means and standard deviations . The means and standard deviations are estimated by their empirical counterparts, so that the residuals (20) are with

| (23) |

for and . Following Genest, Ghoudi and Rivest (1995), the copula parameter is estimated via a rank-based maximum pseudo-likelihood estimator. Obviously, the component-wise ranks of the data and those of the residuals in (23) coincide, so that , as required, depends on the data only through the residuals. The test statistic in (21) is the Wasserstein distance between the empirical distribution of the residuals and the bivariate distribution with standard Gaussian margins and AMH copula with the estimated parameter.

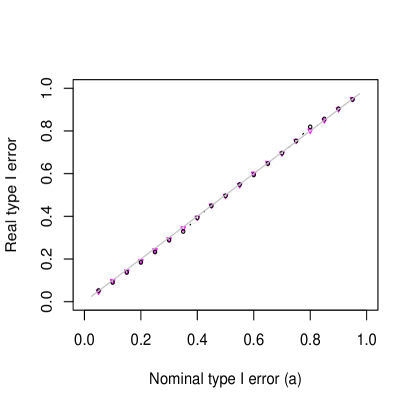

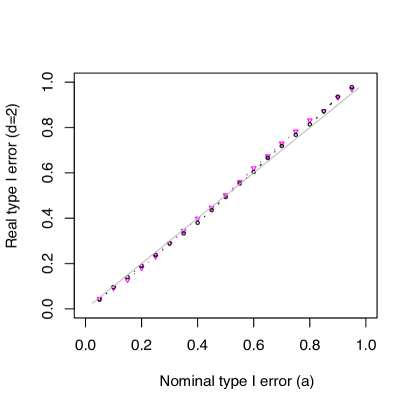

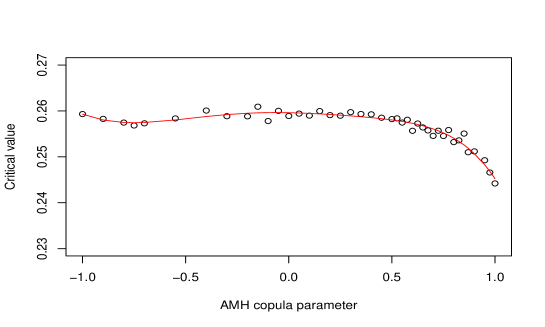

We first checked the validity of the parametric bootstrap procedure of Section 4. To do so, we simulated independent random samples of size from with . For each sample, we calculated the test statistic in (21) and checked whether or not it exceeds the bootstrapped critical value for equal to multiples of . The critical values were computed as described below (22). The points in Figure 7(a) show the empirical type I errors as a function of . The diagonal line fits the points well, supporting the conjecture that the parametric bootstrap is asymptotically valid.

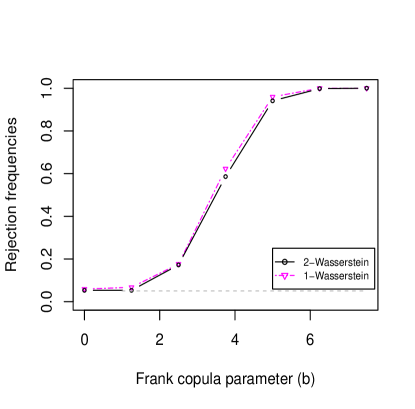

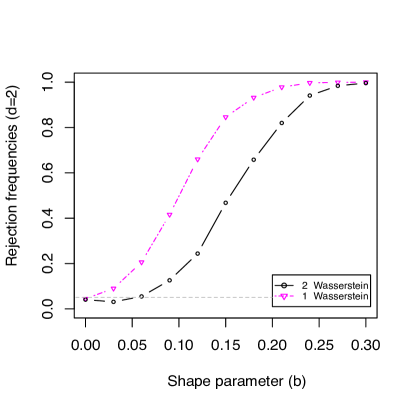

Figure 7(b) similarly displays the rejection frequencies of the Wasserstein test for under an alternative whose copula belongs to the Frank family. If the Frank copula parameter is equal to zero, the Frank copula reduces to the independence copula, which is a member of the AMH family too.

|

|

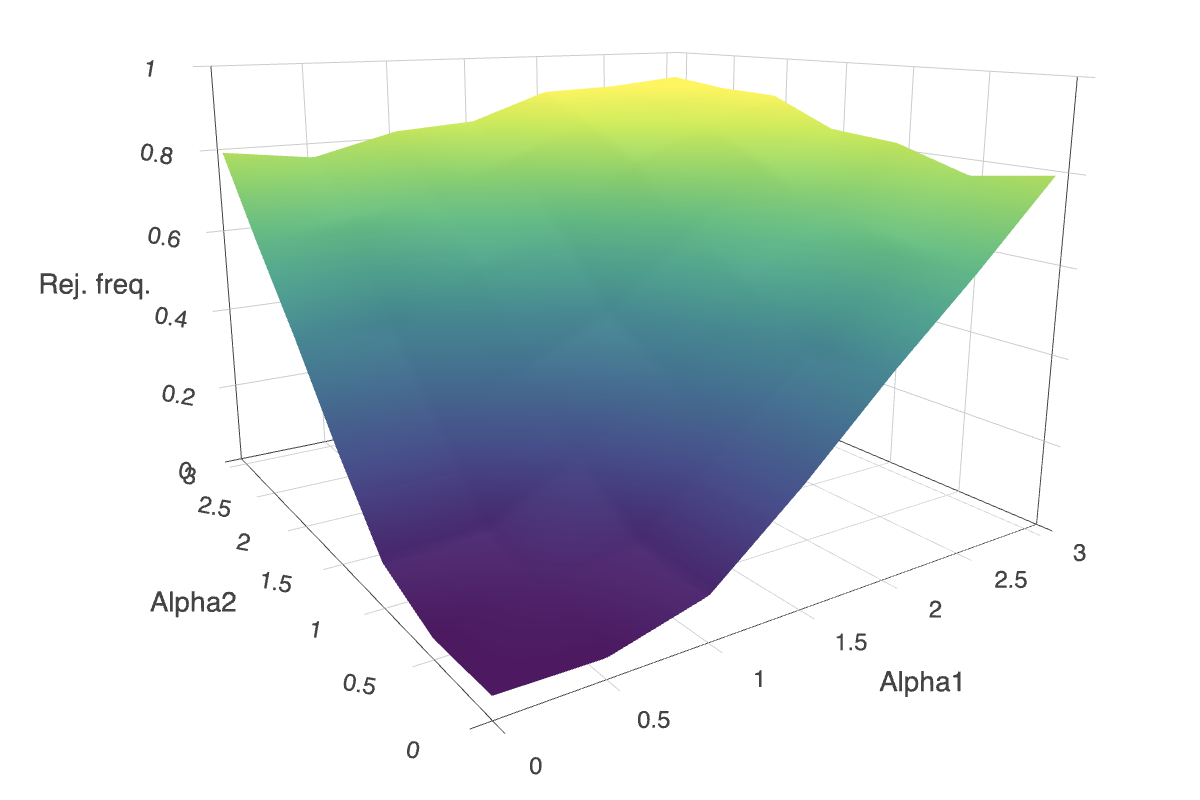

5.3.2 A multivariate Gumbel max-stable family

Next, let be the family of -variate distributions with Gumbel margins with unknown location and scale parameters for and a Gumbel copula with unknown shape parameter . Each is thus a -variate max-stable distribution, that is, a possible large-sample limit of the vector of affinely normalized component-wise maxima of an i.i.d. sample from a common distribution (Beirlant et al., 2004, Chapter 9).

There are parameters in total. We treat the location-scale parameters as indexing the transformation group in Example 1 of Section 3. The parameters are estimated in two stages:

-

1.

The location-scale parameters are estimated separately for each margin by maximum likelihood, producing and .

-

2.

The copula parameter is estimated by maximum likelihood on the basis of the estimated residuals with

This two-stage maximum pseudo-likelihood estimation procedure usually enjoys a high relative efficiency with respect to the full maximum likelihood estimator and is computationally much simpler (Joe, 2005). The location-scale estimators are equivariant under location-scale transformations. The residuals and the copula parameter estimator are thus invariant under such transformations.

We then proceed as in Section 4.1. The goodness-of-fit statistic in (21) measures the Wasserstein distance between the empirical distribution of the estimated residuals and the -variate max-stable distribution with standard Gumbel margins and Gumbel copula with the estimated parameter. The goodness-of-fit test is carried out as in (22).

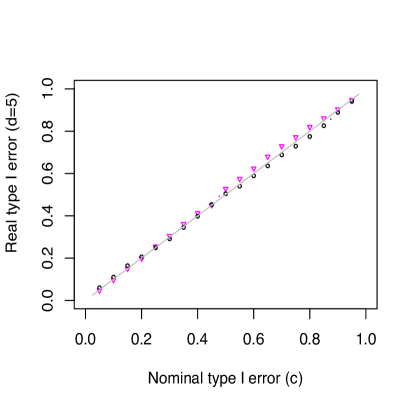

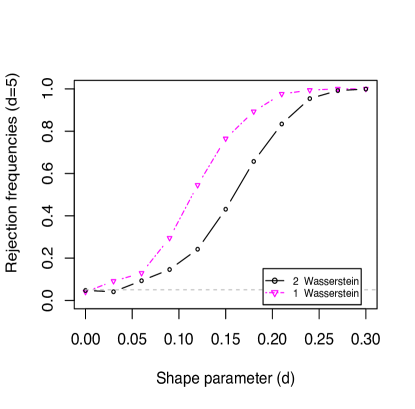

Figure 8 shows simulation results in dimensions and on top and bottom rows, respectively.

-

•

On the left, the evaluation of the bootstrap accuracy is carried out as in Figure 7(a). Samples are generated from a distribution in the model with Gumbel copula parameter . The results support the conjecture that the Wasserstein-based tests with critical values calculated by the parametric bootstrap have the correct size, at least asymptotically.

-

•

On the right, the power is calculated against alternative distributions whose margins are Generalized Extreme-Value (GEV) distributions with common shape parameter indicated on the horizontal axis. Note that corresponds to the null hypothesis. For , the distribution has finite moments up to order only. This explains perhaps why the power of the Wasserstein test for is less than for .

|

|

|

|

Acknowledgements

The authors gratefully acknowledge the remarks and comments made by the reviewers that greatly helped improve the paper. J. Segers gratefully acknowledges funding from FNRS-F.R.S. grant CDR J.0146.19.

References

- Ambrosio, Stra and Trevisan (2018) {barticle}[author] \bauthor\bsnmAmbrosio, \bfnmL.\binitsL., \bauthor\bsnmStra, \bfnmF.\binitsF. and \bauthor\bsnmTrevisan, \bfnmD.\binitsD. (\byear2018). \btitleA PDE approach to a 2-dimensional matching problem. \bjournalProbability Theory and Related Fields \bpages1–45. \endbibitem

- Azzalini (2014) {bbook}[author] \bauthor\bsnmAzzalini, \bfnmAdelchi\binitsA. (\byear2014). \btitleThe Skew-Normal and Related Families. \bseriesInstitute of Mathematical Statistics (IMS) Monographs \bvolume3. \bpublisherCambridge University Press, Cambridge \bnoteWith the collaboration of Antonella Capitanio. \bmrnumber3468021 \endbibitem

- Azzalini (2020) {bmanual}[author] \bauthor\bsnmAzzalini, \bfnmA.\binitsA. (\byear2020). \btitleThe R package sn: The Skew-Normal and Related Distributions such as the Skew-., \baddressUniversità di Padova, Italia. \endbibitem

- Bakshaev and Rudzkis (2015) {barticle}[author] \bauthor\bsnmBakshaev, \bfnmAleksej\binitsA. and \bauthor\bsnmRudzkis, \bfnmRimantas\binitsR. (\byear2015). \btitleMultivariate goodness-of-fit tests based on kernel density estimators. \bjournalNonlinear Analysis. Modelling and Control \bvolume20 \bpages585–602. \endbibitem

- Beirlant et al. (2004) {bbook}[author] \bauthor\bsnmBeirlant, \bfnmJ.\binitsJ., \bauthor\bsnmGoegebeur, \bfnmY.\binitsY., \bauthor\bsnmSegers, \bfnmJ.\binitsJ., \bauthor\bsnmTeugels, \bfnmJ. L.\binitsJ. L., \bauthor\bsnmDe Waal, \bfnmD.\binitsD. and \bauthor\bsnmFerro, \bfnmC.\binitsC. (\byear2004). \btitleStatistics of Extremes: Theory and Applications. \bpublisherWiley. \endbibitem

- Beran (1997) {barticle}[author] \bauthor\bsnmBeran, \bfnmRudolf\binitsR. (\byear1997). \btitleDiagnosing bootstrap success. \bjournalAnnals of the Institute of Statistical Mathematics \bvolume49 \bpages1–24. \endbibitem

- Bickel and Freedman (1981) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmFreedman, \bfnmDavid A.\binitsD. A. (\byear1981). \btitleSome asymptotic theory for the bootstrap. \bjournalThe Annals of Statistics \bvolume9 \bpages1196–1217. \endbibitem

- Bickel and Rosenblatt (1973) {barticle}[author] \bauthor\bsnmBickel, \bfnmP. J.\binitsP. J. and \bauthor\bsnmRosenblatt, \bfnmM.\binitsM. (\byear1973). \btitleOn some global measures of the deviations of density function estimates. \bjournalThe Annals of Statistics \bvolume1 \bpages1071–1095. \endbibitem

- Bobkov and Ledoux (2019) {barticle}[author] \bauthor\bsnmBobkov, \bfnmSergey\binitsS. and \bauthor\bsnmLedoux, \bfnmMichel\binitsM. (\byear2019). \btitleOne-dimensional empirical measures, order statistics, and Kantorovich transport distances. \bjournalMem. Amer. Math. Soc. \bvolume261 \bpagesv+126. \bdoi10.1090/memo/1259 \bmrnumber4028181 \endbibitem

- Cambanis, Huang and Simons (1981) {barticle}[author] \bauthor\bsnmCambanis, \bfnmStamatis\binitsS., \bauthor\bsnmHuang, \bfnmSteel\binitsS. and \bauthor\bsnmSimons, \bfnmGordon\binitsG. (\byear1981). \btitleOn the theory of elliptically contoured distributions. \bjournalJournal of Multivariate Analysis \bvolume11 \bpages368–385. \endbibitem

- Capanu (2019) {barticle}[author] \bauthor\bsnmCapanu, \bfnmMarinela\binitsM. (\byear2019). \btitleA unified approach to proving parametric bootstrap consistency for some goodness-of-fit tests. \bjournalStatistics \bvolume53 \bpages58–80. \endbibitem

- Carlier et al. (2016) {barticle}[author] \bauthor\bsnmCarlier, \bfnmGuillaume\binitsG., \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmGalichon, \bfnmAlfred\binitsA. \betalet al. (\byear2016). \btitleVector quantile regression: an optimal transport approach. \bjournalThe Annals of Statistics \bvolume44 \bpages1165–1192. \endbibitem

- Chernozhukov et al. (2017) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmGalichon, \bfnmAlfred\binitsA., \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmHenry, \bfnmMarc\binitsM. \betalet al. (\byear2017). \btitleMonge–Kantorovich depth, quantiles, ranks and signs. \bjournalThe Annals of Statistics \bvolume45 \bpages223–256. \endbibitem

- Cramér (1928) {barticle}[author] \bauthor\bsnmCramér, \bfnmA\binitsA. (\byear1928). \btitleOn the composition of elementary errors. \bjournalScandinavian Actuarial Journal \bvolume1 \bpages13-74. \endbibitem

- del Barrio, Giné and Utzet (2005) {barticle}[author] \bauthor\bsnmdel Barrio, \bfnmEustasio\binitsE., \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmUtzet, \bfnmFrederic\binitsF. (\byear2005). \btitleAsymptotics for functionals of the empirical quantile process, with applications to tests of fit based on weighted Wasserstein distances. \bjournalBernoulli \bvolume11 \bpages131–189. \endbibitem

- del Barrio and Loubes (2019) {barticle}[author] \bauthor\bsnmdel Barrio, \bfnmE.\binitsE. and \bauthor\bsnmLoubes, \bfnmJ. M.\binitsJ. M. (\byear2019). \btitleCentral limit theorems for empirical transportation cost in general dimension. \bjournalThe Annals of Probability \bvolume47 \bpages926–951. \endbibitem

- del Barrio et al. (1999) {barticle}[author] \bauthor\bparticledel \bsnmBarrio, \bfnmEustasio\binitsE., \bauthor\bsnmCuesta-Albertos, \bfnmJuan A.\binitsJ. A., \bauthor\bsnmMatrán, \bfnmCarlos\binitsC. and \bauthor\bsnmRodríguez-Rodríguez, \bfnmJesús M.\binitsJ. M. (\byear1999). \btitleTests of goodness of fit based on the -Wasserstein distance. \bjournalThe Annals of Statistics \bvolume27 \bpages1230–1239. \endbibitem

- del Barrio et al. (2000) {barticle}[author] \bauthor\bsnmdel Barrio, \bfnmE.\binitsE., \bauthor\bsnmCuesta-Albertos, \bfnmJ. A.\binitsJ. A., \bauthor\bsnmMatrán, \bfnmC.\binitsC., \bauthor\bsnmCsörgö, \bfnmS.\binitsS., \bauthor\bsnmCuadras, \bfnmC. M.\binitsC. M., \bauthor\bparticlede \bsnmWet, \bfnmT.\binitsT., \bauthor\bsnmGiné, \bfnmE.\binitsE., \bauthor\bsnmLockhart, \bfnmR.\binitsR., \bauthor\bsnmMunk, \bfnmA.\binitsA. and \bauthor\bsnmStute, \bfnmW.\binitsW. (\byear2000). \btitleContributions of empirical and quantile processes to the asymptotic theory of goodness-of-fit tests. \bjournalTest \bvolume9 \bpages1–96. \endbibitem

- Ebner, Henze and Yukich (2018) {barticle}[author] \bauthor\bsnmEbner, \bfnmBruno\binitsB., \bauthor\bsnmHenze, \bfnmNorbert\binitsN. and \bauthor\bsnmYukich, \bfnmJoseph E\binitsJ. E. (\byear2018). \btitleMultivariate goodness-of-fit on flat and curved spaces via nearest neighbor distances. \bjournalJournal of Multivariate Analysis \bvolume165 \bpages231–242. \endbibitem

- Fan (1997) {barticle}[author] \bauthor\bsnmFan, \bfnmYanqin\binitsY. (\byear1997). \btitleGoodness-of-fit tests for a multivariate distribution by the empirical characteristic function. \bjournalJournal of Multivariate Analysis \bvolume62 \bpages36–63. \endbibitem

- Fang, Kotz and Ng (1990) {bbook}[author] \bauthor\bsnmFang, \bfnmKai-Tai\binitsK.-T., \bauthor\bsnmKotz, \bfnmSamuel\binitsS. and \bauthor\bsnmNg, \bfnmKai-Wang\binitsK.-W. (\byear1990). \btitleSymmetric multivariate and related distributions. \bpublisherChapman & Hall, \baddressLondon. \endbibitem

- Fournier and Guillin (2015) {barticle}[author] \bauthor\bsnmFournier, \bfnmNicolas\binitsN. and \bauthor\bsnmGuillin, \bfnmArnaud\binitsA. (\byear2015). \btitleOn the rate of convergence in Wasserstein distance of the empirical measure. \bjournalProbability Theory and Related Fields \bvolume162 \bpages707–738. \endbibitem

- Genest, Ghoudi and Rivest (1995) {barticle}[author] \bauthor\bsnmGenest, \bfnmC.\binitsC., \bauthor\bsnmGhoudi, \bfnmK.\binitsK. and \bauthor\bsnmRivest, \bfnmL. P.\binitsL. P. (\byear1995). \btitleA semiparametric estimation procedure of dependence parameters in multivariate families of distributions. \bjournalBiometrika \bvolume82 \bpages543–552. \endbibitem

- Genevay et al. (2016) {binproceedings}[author] \bauthor\bsnmGenevay, \bfnmAude\binitsA., \bauthor\bsnmCuturi, \bfnmMarco\binitsM., \bauthor\bsnmPeyré, \bfnmGabriel\binitsG. and \bauthor\bsnmBach, \bfnmFrancis\binitsF. (\byear2016). \btitleStochastic optimization for large-scale optimal transport. In \bbooktitleAdvances in Neural Information Processing Systems \bpages3440–3448. \endbibitem

- Goldfeld and Kato (2020) {barticle}[author] \bauthor\bsnmGoldfeld, \bfnmZiv\binitsZ. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2020). \btitleLimit Distribution Theory for Smooth Wasserstein Distance with Applications to Generative Modeling. \bjournalarXiv preprint arXiv:2002.01012. \endbibitem

- Golub and Van Loan (1996) {bbook}[author] \bauthor\bsnmGolub, \bfnmGene H.\binitsG. H. and \bauthor\bsnmVan Loan, \bfnmCharles F.\binitsC. F. (\byear1996). \btitleMatrix Computations, \beditionthird ed. \bpublisherThe Johns Hopkins University Press, \baddressBaltimore and London. \endbibitem

- Hallin et al. (2020) {barticle}[author] \bauthor\bsnmHallin, \bfnmMarc\binitsM., \bauthor\bsnmdel Barrio, \bfnmEustasio\binitsE., \bauthor\bsnmCuesta Albertos, \bfnmJuan.\binitsJ. and \bauthor\bsnmMatrán, \bfnmCarlos\binitsC. (\byear2020). \btitleDistribution and quantile functions, ranks, and signs in dimension : a measure transportation approach. \bjournalThe Annals of Statistics \bpages(to appear). \endbibitem

- Hartmann and Schuhmacher (2020) {barticle}[author] \bauthor\bsnmHartmann, \bfnmValentin\binitsV. and \bauthor\bsnmSchuhmacher, \bfnmDominic\binitsD. (\byear2020). \btitleSemi-discrete optimal transport: a solution procedure for the unsquared Euclidean distance case. \bjournalMathematical Methods of Operations Research \bvolume92 \bpages133–163. \endbibitem

- Henze and Zirkler (1990) {barticle}[author] \bauthor\bsnmHenze, \bfnmN.\binitsN. and \bauthor\bsnmZirkler, \bfnmB.\binitsB. (\byear1990). \btitleA class of invariant consistent tests for multivariate normality. \bjournalCommunications in Statistics. Theory and Methods \bvolume19 \bpages3595–3617. \endbibitem

- Hofert et al. (2018) {bmanual}[author] \bauthor\bsnmHofert, \bfnmMarius\binitsM., \bauthor\bsnmKojadinovic, \bfnmIvan\binitsI., \bauthor\bsnmMaechler, \bfnmMartin\binitsM. and \bauthor\bsnmYan, \bfnmJun\binitsJ. (\byear2018). \btitlecopula: Multivariate Dependence with Copulas \bnoteR package version 0.999-19.1. \endbibitem

- Horowitz and Karandikar (1994) {barticle}[author] \bauthor\bsnmHorowitz, \bfnmJoseph\binitsJ. and \bauthor\bsnmKarandikar, \bfnmRajeeva L.\binitsR. L. (\byear1994). \btitleMean rates of convergence of empirical measures in the Wasserstein distance. \bjournalJournal of Computational and Applied Mathematics \bvolume55 \bpages261–273. \endbibitem

- Joe (2005) {barticle}[author] \bauthor\bsnmJoe, \bfnmHarry\binitsH. (\byear2005). \btitleAsymptotic efficiency of the two-stage estimation method for copula-based models. \bjournalJournal of Multivariate Analysis \bvolume94 \bpages401–419. \endbibitem

- Khmaladze (2016) {barticle}[author] \bauthor\bsnmKhmaladze, \bfnmE. V.\binitsE. V. (\byear2016). \btitleUnitary transformations, empirical processes and distribution free testing. \bjournalBernoulli \bvolume22 \bpages563–588. \endbibitem

- Kitagawa, Mérigot and Thibert (2017) {barticle}[author] \bauthor\bsnmKitagawa, \bfnmJ.\binitsJ., \bauthor\bsnmMérigot, \bfnmQ.\binitsQ. and \bauthor\bsnmThibert, \bfnmB.\binitsB. (\byear2017). \btitleConvergence of a Newton algorithm for semi-discrete optimal transport. \bjournalarXiv preprint arXiv:1603.05579v2. \endbibitem

- Kolmogorov (1933) {barticle}[author] \bauthor\bsnmKolmogorov, \bfnmAndrey\binitsA. (\byear1933). \btitleSulla determinazione empirica di una legge di distribuzione. \bjournalGiornale dell’Istituto Italiano degli Attuari \bvolume4 \bpages83-91. \endbibitem

- Korkmaz, Goksuluk and Zararsiz (2014) {barticle}[author] \bauthor\bsnmKorkmaz, \bfnmSelcuk\binitsS., \bauthor\bsnmGoksuluk, \bfnmDincer\binitsD. and \bauthor\bsnmZararsiz, \bfnmGokmen\binitsG. (\byear2014). \btitleMVN: An R Package for Assessing Multivariate Normality. \bjournalThe R Journal \bvolume6 \bpages151–162. \endbibitem

- Lehmann and Casella (1998) {bbook}[author] \bauthor\bsnmLehmann, \bfnmE. L.\binitsE. L. and \bauthor\bsnmCasella, \bfnmGeorge\binitsG. (\byear1998). \btitleTheory of Point Estimation, \bedition2nd ed. \bpublisherSpringer Science+Business Media, \baddressNew York. \endbibitem

- Lévy (2015) {barticle}[author] \bauthor\bsnmLévy, \bfnmB.\binitsB. (\byear2015). \btitleA numerical algorithm for L2 semi-discrete optimal transport in 3D. \bjournalESAIM: Mathematical Modelling and Numerical Analysis \bvolume49 \bpages1693–1715. \endbibitem

- Massart (1990) {barticle}[author] \bauthor\bsnmMassart, \bfnmP.\binitsP. (\byear1990). \btitleThe tight constant in the Dvoretsky–Kiefer–Wolfowitz inequality. \bjournalThe Annals of Probability \bvolume18 \bpages1269–1283. \endbibitem

- McAssey (2013) {barticle}[author] \bauthor\bsnmMcAssey, \bfnmMichael P\binitsM. P. (\byear2013). \btitleAn empirical goodness-of-fit test for multivariate distributions. \bjournalJournal of Applied Statistics \bvolume40 \bpages1120–1131. \endbibitem

- Mena and Niles-Weed (2019) {binproceedings}[author] \bauthor\bsnmMena, \bfnmGonzalo\binitsG. and \bauthor\bsnmNiles-Weed, \bfnmJonathan\binitsJ. (\byear2019). \btitleStatistical bounds for entropic optimal transport: sample complexity and the central limit theorem. In \bbooktitleAdvances in Neural Information Processing Systems \bpages4541–4551. \endbibitem

- Mérigot (2011) {binproceedings}[author] \bauthor\bsnmMérigot, \bfnmQ.\binitsQ. (\byear2011). \btitleA multiscale approach to optimal transport. In \bbooktitleComputer Graphics Forum \bvolume30 \bpages1583–1592. \bpublisherWiley Online Library. \endbibitem

- Munk and Czado (1998) {barticle}[author] \bauthor\bsnmMunk, \bfnmA.\binitsA. and \bauthor\bsnmCzado, \bfnmC.\binitsC. (\byear1998). \btitleNonparametric validation of similar distributions and assessment of goodness of fit. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume60 \bpages223–241. \endbibitem

- Panaretos and Zemel (2019) {barticle}[author] \bauthor\bsnmPanaretos, \bfnmVictor M\binitsV. M. and \bauthor\bsnmZemel, \bfnmYoav\binitsY. (\byear2019). \btitleStatistical aspects of Wasserstein distances. \bjournalAnnual Review of Statistics and Its Application \bvolume6 \bpages405–431. \endbibitem

- Peyré and Cuturi (2019) {barticle}[author] \bauthor\bsnmPeyré, \bfnmGabriel\binitsG. and \bauthor\bsnmCuturi, \bfnmMarco\binitsM. (\byear2019). \btitleComputational Optimal Transport. \bjournalFoundations and Trends in Machine Learning \bvolume11 \bpages355–607. \bdoi10.1561/2200000073 \endbibitem

- Ramdas, García Trillos and Cuturi (2017) {barticle}[author] \bauthor\bsnmRamdas, \bfnmAaditya\binitsA., \bauthor\bsnmGarcía Trillos, \bfnmNicolás\binitsN. and \bauthor\bsnmCuturi, \bfnmMarco\binitsM. (\byear2017). \btitleOn Wasserstein two-sample testing and related families of nonparametric tests. \bjournalEntropy \bvolume19 \bpagesPaper No. 47, 15. \endbibitem

- Rippl, Munk and Sturm (2016) {barticle}[author] \bauthor\bsnmRippl, \bfnmT.\binitsT., \bauthor\bsnmMunk, \bfnmA.\binitsA. and \bauthor\bsnmSturm, \bfnmA.\binitsA. (\byear2016). \btitleLimit laws of the empirical Wasserstein distance: Gaussian distributions. \bjournalJournal of Multivariate Analysis \bvolume151 \bpages90–109. \endbibitem

- Rizzo and Székely (2016) {barticle}[author] \bauthor\bsnmRizzo, \bfnmM. L.\binitsM. L. and \bauthor\bsnmSzékely, \bfnmG. J.\binitsG. J. (\byear2016). \btitleEnergy distance. \bjournalWiley Interdisciplinary Reviews: Computational Statistics \bvolume8 \bpages27–38. \endbibitem

- Royston (1983) {barticle}[author] \bauthor\bsnmRoyston, \bfnmJ. P.\binitsJ. P. (\byear1983). \btitleSome techniques for assessing multivariate normality based on the Shapiro–Wilk W. \bjournalJournal of the Royal Statistical Society: Series C (Applied Statistics) \bvolume32 \bpages121–133. \endbibitem

- Santambrogio (2015) {bbook}[author] \bauthor\bsnmSantambrogio, \bfnmFilippo\binitsF. (\byear2015). \btitleOptimal Transport for Applied Mathematicians. \bseriesProgress in Nonlinear Differential Equations and their Applications \bvolume87. \bpublisherBirkhäuser/Springer, Cham. \endbibitem

- Schmidt, Le Roux and Bach (2017) {barticle}[author] \bauthor\bsnmSchmidt, \bfnmM.\binitsM., \bauthor\bsnmLe Roux, \bfnmN.\binitsN. and \bauthor\bsnmBach, \bfnmF.\binitsF. (\byear2017). \btitleMinimizing finite sums with the stochastic average gradient. \bjournalMathematical Programming \bvolume162. \endbibitem

- Schuhmacher et al. (2019) {bmanual}[author] \bauthor\bsnmSchuhmacher, \bfnmDominic\binitsD., \bauthor\bsnmBähre, \bfnmBjörn\binitsB., \bauthor\bsnmGottschlich, \bfnmCarsten\binitsC., \bauthor\bsnmHartmann, \bfnmValentin\binitsV., \bauthor\bsnmHeinemann, \bfnmFlorian\binitsF. and \bauthor\bsnmSchmitzer, \bfnmBernhard\binitsB. (\byear2019). \btitletransport: Computation of Optimal Transport Plans and Wasserstein Distances \bnoteR package version 0.12-1. \endbibitem

- Smirnov (1939) {barticle}[author] \bauthor\bsnmSmirnov, \bfnmNikolai V\binitsN. V. (\byear1939). \btitleOn the estimation of the discrepancy between empirical curves of distribution for two independent samples. \bjournalBull. Math. Univ. Moscow \bvolume2 \bpages3-14. \endbibitem

- Smith (1995) {barticle}[author] \bauthor\bsnmSmith, \bfnmS. P.\binitsS. P. (\byear1995). \btitleDifferentiation of the Cholesky Algorithm. \bjournalJournal of Computational and Graphical Statistics \bvolume4 \bpages134–147. \endbibitem

- Sommerfeld and Munk (2018) {barticle}[author] \bauthor\bsnmSommerfeld, \bfnmM.\binitsM. and \bauthor\bsnmMunk, \bfnmA.\binitsA. (\byear2018). \btitleInference for empirical Wasserstein distances on finite spaces. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume80 \bpages219–238. \endbibitem

- Tameling, Sommerfeld and Munk (2019) {barticle}[author] \bauthor\bsnmTameling, \bfnmCarla\binitsC., \bauthor\bsnmSommerfeld, \bfnmMax\binitsM. and \bauthor\bsnmMunk, \bfnmAxel\binitsA. (\byear2019). \btitleEmpirical optimal transport on countable metric spaces: Distributional limits and statistical applications. \bjournalThe Annals of Applied Probability \bvolume29 \bpages2744–2781. \endbibitem

- R Core Team (2018) {bmanual}[author] \bauthor\bsnmR Core Team (\byear2018). \btitleR: A Language and Environment for Statistical Computing \bpublisherR Foundation for Statistical Computing, \baddressVienna, Austria. \endbibitem

- van der Vaart (1998) {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. (\byear1998). \btitleAsymptotic Statistics. \bpublisherCambridge University Press, \baddressCambridge. \endbibitem

- van der Vaart and Wellner (1996) {bbook}[author] \bauthor\bsnmvan der Vaart, \bfnmAad W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1996). \btitleWeak Convergence and Empirical Processes. With Applications to Statistics. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Villani (2009) {bbook}[author] \bauthor\bsnmVillani, \bfnmCédric\binitsC. (\byear2009). \btitleOptimal Transport: Old and New. \bpublisherSpringer-Verlag, Berlin. \endbibitem

- von Mises (1928) {bbook}[author] \bauthor\bsnmvon Mises, \bfnmR. E.\binitsR. E. (\byear1928). \btitleWahrscheinlichkeit, Statistik und Wahrheit. \bpublisherJulius Springer, \baddressBerlin. \endbibitem

- Weed and Bach (2019) {barticle}[author] \bauthor\bsnmWeed, \bfnmJonathan\binitsJ. and \bauthor\bsnmBach, \bfnmFrancis\binitsF. (\byear2019). \btitleSharp asymptotic and finite-sample rates of convergence of empirical measures in Wasserstein distance. \bjournalBernoulli \bvolume25 \bpages2620–2648. \endbibitem

Appendix A Uniform convergence of the empirical Wasserstein distance

We establish here the convergence to zero in probability, uniformly in the underlying distribution , of the empirical Wasserstein distance when has a compact -closure. The result is thus a law of large numbers for the empirical distribution in Wasserstein distance uniformly in the underlying distribution akin to Chung’s uniform law of large numbers (van der Vaart and Wellner, 1996, Proposition A.5.1).

Actually, Theorem 1 establishes the stronger result that the convergence to zero holds uniformly in the -th mean. The Markov inequality then implies (Corollary 1) the desired uniform convergence in probability. The notation is that of Section 1.2, with standing for expectation under an independent random sample from .

Theorem 1.

Let be such that

| (24) |

Then we have

The condition on is equivalent to assuming that the closure of in the metric space is compact. This follows from Prohorov’s theorem and the characterization of -convergence in Bickel and Freedman (1981, Lemma 8.3) or Villani (2009, Theorem 6.9).