[table]capposition=top

An Evaluation of Change Point Detection Algorithms

2 The Alan Turing Institute, London, UK

)

Abstract

Change point detection is an important part of time series analysis,

as the presence of a change point indicates an abrupt and significant

change in the data generating process. While many algorithms for

change point detection have been proposed, comparatively little

attention has been paid to evaluating their performance on real-world

time series. Algorithms are typically evaluated on simulated data and

a small number of commonly-used series with unreliable ground truth.

Clearly this does not provide sufficient insight into the comparative

performance of these algorithms. Therefore, instead of developing yet

another change point detection method, we consider it vastly more

important to properly evaluate existing algorithms on real-world data.

To achieve this, we present a data set specifically designed for the

evaluation of change point detection algorithms that consists of

37 time series from various application domains.

Each series was annotated by five human annotators to provide ground

truth on the presence and location of change points. We analyze the

consistency of the human annotators, and describe evaluation metrics

that can be used to measure algorithm performance in the presence of

multiple ground truth annotations. Next, we present a benchmark study

where 14 algorithms are evaluated on each of the time series

in the data set.

Our aim is that this data set will serve as a proving ground in the

development of novel change point detection algorithms.

Keywords: change point detection, time series analysis, benchmark evaluation

1 Introduction

Moments of abrupt change in the behavior of a time series are often cause for alarm as they may signal a significant alteration to the data generating process. Detecting such change points is therefore of high importance for data analysts and engineers. The literature on change point detection (CPD) is concerned with accurately detecting these events in time series data, as well as with modeling time series in which such events occur. Applications of CPD are found in finance (Lavielle and Teyssiere, 2007), business (Taylor and Letham, 2018), quality control (Page, 1954), and network traffic analysis (Kurt et al., 2018), among many other domains.

There is a large body of work on both the theoretical and practical aspects of change point detection. However, less attention has been paid to the evaluation of CPD algorithms on real-world time series. Existing work often follows a predictable strategy when presenting a novel detection algorithm: the method is first evaluated on a set of simulated time series with known change points where both the model fit and detection accuracy are evaluated. An obvious downside of such experiments is that the dynamics of the simulated data are often particular to the paper, and any model that corresponds to these dynamics has an unfair advantage. Subsequently the proposed method is typically evaluated on only a small number of real-world time series. These series are often reused (e.g., the univariate well-log data of Ó Ruanaidh and Fitzgerald, 1996), may have been preprocessed (e.g., by removing outliers or seasonality), and may not have unambiguous ground truth available. When evaluating a proposed method on real-world data, post-hoc analysis is frequently applied to argue why the locations detected by the algorithm correspond to known events. Clearly, this is not a fair or accurate approach to evaluating novel change point detection algorithms.

Rather than proposing yet another detection method and evaluating it in the manner just described, we argue that it is vastly more important to create a realistic benchmark data set for CPD algorithms. Such a data set will allow researchers to evaluate their novel algorithms in a systematic and realistic way against existing alternatives. Furthermore, since change point detection is generally an unsupervised learning problem, an evaluation on real-world data is the most reliable approach to properly compare detection accuracy. A benchmark data set can also uncover important failure modes of existing methods that may not occur in simulated data, and suggest avenues for future research based on a quantitative analysis of algorithm performance.

Change point detection can be viewed as partitioning an input time series into a number of segments. It is thus highly similar to the problem of image segmentation, where an image is partitioned into distinct segments based on different textures or objects. Historically, image segmentation suffered from the same problem as change point detection does today, due to the absence of a large, high-quality data set with objective ground truth (as compared to, for instance, image classification). It was not until the Berkeley Segmentation Data Set (BSDS; Martin et al., 2001) that quantitative comparison of segmentation algorithms became feasible. We believe that it is essential to develop a similar data set for change point detection, to enable both the research community as well as data analysts to quantitatively compare CPD algorithms.

To achieve this goal, we present the first data set specifically designed to evaluate change point detection algorithms that consists of time series from diverse application domains. We developed an annotation tool and collected annotations from data scientists for 37 real-world time series. Using this data set, we perform a large-scale quantitative evaluation of existing algorithms. We analyze the results of this comparison to uncover failure cases of present methods and discuss various potential improvements. To summarize, our main contributions are as follows.

-

1.

We describe the design and collection of a data set for change point detection algorithms and analyze the data set for annotation quality and consistency. The data set is made freely available to accelerate research on change point detection.111See https://github.com/alan-turing-institute/TCPD.

-

2.

We present metrics for the evaluation of change point detection algorithms that take multiple annotations per data set into account.

-

3.

We evaluate a significant number of existing change point detection algorithms on this data set and provide the first benchmark study on a large number of real-world data sets using two distinct experimental setups.222All code needed to reproduce our results is made available through an online repository:

https://github.com/alan-turing-institute/TCPDBench.

The remainder of this paper is structured as follows. In Section 2 we give a high-level overview and categorization of existing work on CPD. Section 3 presents a framework for evaluating change point methods when ground truth from multiple human annotators is available. The annotation tool and data set collection process are described in Section 4, along with an analysis of data quality and annotator consistency. The design of the benchmark study and an analysis of the results is presented in Section 5. Section 6 concludes.

2 Related Work

Methods for CPD can be roughly categorized as follows: (1) online vs. offline, (2) univariate vs. multivariate, and (3) model-based vs. nonparametric. We can further differentiate between Bayesian and frequentist approaches among the model-based methods, and between divergence estimation and heuristics in the nonparametric methods. Due to the large amount of work on CPD we only provide a high-level overview of some of the most relevant methods here, which also introduces many of the methods that we subsequently consider in our evaluation study. For a more expansive review of change point detection algorithms, see e.g., Aminikhanghahi and Cook (2017) or Truong et al. (2020). Note that we focus here on the unsupervised change point detection problem, without access to external data that can be used to tune hyperparameters (Hocking et al., 2013a; Truong et al., 2017).

Let denote the observations for time steps , where the domain is -dimensional and typically assumed to be a subset of . A segment of the series from will be written as . The ordered set of change points is denoted by , with for notational convenience. In offline change point detection we further use to denote the length of the series and define . Note that we assume that a change point marks the first observation of a new segment.

Early work on CPD originates from the quality control literature. Page (1954) introduced the CUSUM method that detects where the corrected cumulative sum of observations exceeds a threshold value. Theoretical analysis of this method was subsequently provided by Lorden (1971). Hinkley (1970) generalized this approach to testing for differences in the maximum likelihood, i.e., testing whether and differ significantly, for model parameters , , and . Alternatives from the literature on structural breaks include the use of a Chow test (Chow, 1960) or multiple linear regression (Bai and Perron, 2003).

In offline multiple change point detection the optimization problem is given by

| (1) |

with a cost function for a segment (e.g., the negative maximum log-likelihood), a hyperparameter, and a penalty on the number of change points. An early method by Scott and Knott (1974) introduced binary segmentation as an approximate CPD algorithm that greedily splits the series into disjoint segments based on the above cost function. This greedy method thus obtains a solution in time. An efficient dynamic programming approach to compute an exact solution for the multiple change point problem was presented in Auger and Lawrence (1989), with time complexity for a given upper bound on the number of change points.

Improvements to these early algorithms were made by requiring the cost function to be additive, i.e., . Using this assumption, Jackson et al. (2005) present a dynamic programming algorithm with complexity. Killick et al. (2012) subsequently extended this method with a pruning step on potential change point locations, which reduces the time complexity to be approximately linear under certain conditions on the data generating process and the distribution of change points. A different pruning approach was proposed by Rigaill (2015) using further assumptions on the cost function, which was extended by Maidstone et al. (2017) and made robust against outliers by Fearnhead and Rigaill (2019). Recent work in offline CPD also includes the Wild Binary Segmentation method (Fryzlewicz, 2014) that extends binary segmentation by applying the CUSUM statistic to randomly drawn subsets of the time series. Furthermore, the Prophet method for Bayesian time series forecasting (Taylor and Letham, 2018) supports fitting time series with change points, even though it is not a dedicated CPD method. These offline detection methods are generally restricted to univariate time series.

Bayesian online change point detection was simultaneously proposed by Fearnhead and Liu (2007) and Adams and MacKay (2007). These models learn a probability distribution over the “run length”, which is the time since the most recent change point. This gives rise to a recursive message-passing algorithm for the joint distribution of the observations and the run lengths. The formulation of Adams and MacKay (2007) has been extended in several works to include online hyperparameter optimization (Turner et al., 2009) and Gaussian Process segment models (Garnett et al., 2009; Saatçi et al., 2010). Recent work by Knoblauch and Damoulas (2018) has added support for model selection and spatio-temporal models, as well as robust detection using -divergences (Knoblauch et al., 2018).

Nonparametric methods for CPD are typically based on explicit hypothesis testing, where a change point is declared when a test statistic exceeds a certain threshold. This includes kernel change point analysis (Harchaoui et al., 2009), the use of an empirical divergence measure (Matteson and James, 2014), as well as the use of histograms to construct a test statistic (Boracchi et al., 2018). Both the Bayesian online change point detection methods and the nonparametric methods support multidimensional data.

Finally, we observe that in the field of genomics a number of data sets exist that can be used to evaluate change point detection methods (e.g., Hocking et al., 2013a, b, 2014). While this is an important application domain for CPD algorithms, we are interested in evaluating the performance of change point algorithms on general real-world time series from diverse domains. Moreover, the data sets proposed in Hocking et al. (2013b, 2014) make use of labeled regions that are annotated as containing a change point or not, instead of labels of the exact change point locations. While in this work exact labels are preferred over labeled regions, the latter can certainly simplify the annotation task for longer time series. We allow a small margin of error in the evaluation metrics to take any potential uncertainty of the annotators into account.

3 Evaluation Metrics

In this section we review common metrics for evaluating CPD algorithms and provide those that can be used to compare algorithms against multiple ground truth annotations. These metrics will also be used to quantify the consistency of the annotations of the time series, which is why they are presented here. Our discussion bears many similarities to that provided by Martin et al. (2004) and Arbelaez et al. (2010) for the BSDS, due to the parallels between change point detection and image segmentation.

Existing metrics for change point detection can be roughly divided between clustering metrics and classification metrics. These categories represent distinct views of the change point detection problem, and we discuss them in turn. The locations of change points provided by annotator are denoted by the ordered set with for and for . Then implies a partition, , of the interval into disjoint sets , where is the segment from to for . Recall that we use and for notational convenience.

Evaluating change point algorithms using clustering metrics corresponds to the view that change point detection inherently aims to divide the time series into distinct regions with a constant data generating process. Clustering metrics such as the variation of information (VI; Arabie and Boorman, 1973), adjusted Rand index (ARI; Hubert and Arabie, 1985), Hausdorff distance (Hausdorff, 1927), and segmentation covering metric (Everingham et al., 2010; Arbelaez et al., 2010) can be readily applied. We disregard the Hausdorff metric because it is a maximum discrepancy metric and can therefore obscure the true performance of methods that report many false positives. Following the discussion in Arbelaez et al. (2010) regarding the difficulty of using VI for multiple ground truth partitions and the small dynamic range of the Rand index, we choose to use the covering metric as the clustering metric in the experiments.

For two sets the Jaccard index, also known as Intersection over Union, is given by

| (2) |

Following Arbelaez et al. (2010), we define the covering metric of a partition by a partition as

| (3) |

For a collection of ground truth partitions provided by the human annotators and a partition given by an algorithm, we compute the average of for all annotators as a single measure of performance.

An alternative view of evaluating CPD algorithms considers change point detection as a classification problem between the “change point” and “non-change point” classes (Killick et al., 2012; Aminikhanghahi and Cook, 2017). Because the number of change points is generally a small proportion of the number of observations in the series, common classification metrics such as the accuracy score will be highly skewed. It is more useful to express the effectiveness of an algorithm in terms of precision (the ratio of correctly detected change points over the number of detected change points) and recall (the ratio of correctly detected change points over the number of true change points). The -measure provides a single quantity that incorporates both precision, , and recall, , through

| (4) |

with corresponding to the well-known F1-score (Van Rijsbergen, 1979).

When evaluating CPD algorithms using classification metrics it is common to define a margin of error around the true change point location to allow for minor discrepancies (e.g., Killick et al., 2012; Truong et al., 2020). However with this margin of error we must be careful to avoid double counting, so that for multiple detections within the margin around a true change point only one is recorded as a true positive (Killick et al., 2012). To handle the multiple sets of ground truth change points provided by the annotator, we follow the precision-recall framework from the BSDS proposed in Martin et al. (2004). Let denote the set of change point locations provided by a detection algorithm and let be the combined set of all human annotations. For a set of ground truth locations we define the set of true positives of to be those for which such that , while ensuring that only one can be used for a single . The latter requirement is needed to avoid the double counting mentioned previously, and is the allowed margin of error. The precision and recall are then defined as

| (5) | ||||

| (6) |

With this definition of precision, we consider as false positives only those detections that correspond to no human annotation. Further, by defining the recall as the average of the recall for each individual annotator we encourage algorithms to explain all human annotations without favoring any annotator in particular.333This definition of recall is the macro-average of the recall for each annotator, as opposed to the micro-average, . When using situations can arise where it is favorable for the detector to agree with the annotator with the most annotations, which is not a desirable property. Note that precision and recall are undefined if the annotators or the algorithm declare that a series has no change points. To avoid this, we include as a trivial change point in and . Since change points are interpreted as the start of a new segment this choice does not affect the meaning of the detection results.

Using both the segmentation covering metric and the F1-score in the benchmark study allows us to explore both the clustering and classification view of change point detection. In the experiments we use a margin of error of .

4 Change Point Data Set

This section describes the tool used in collecting the change point annotations, as well as the data sources, the experimental protocol, and an analysis of the obtained annotations.

4.1 Annotation Tool

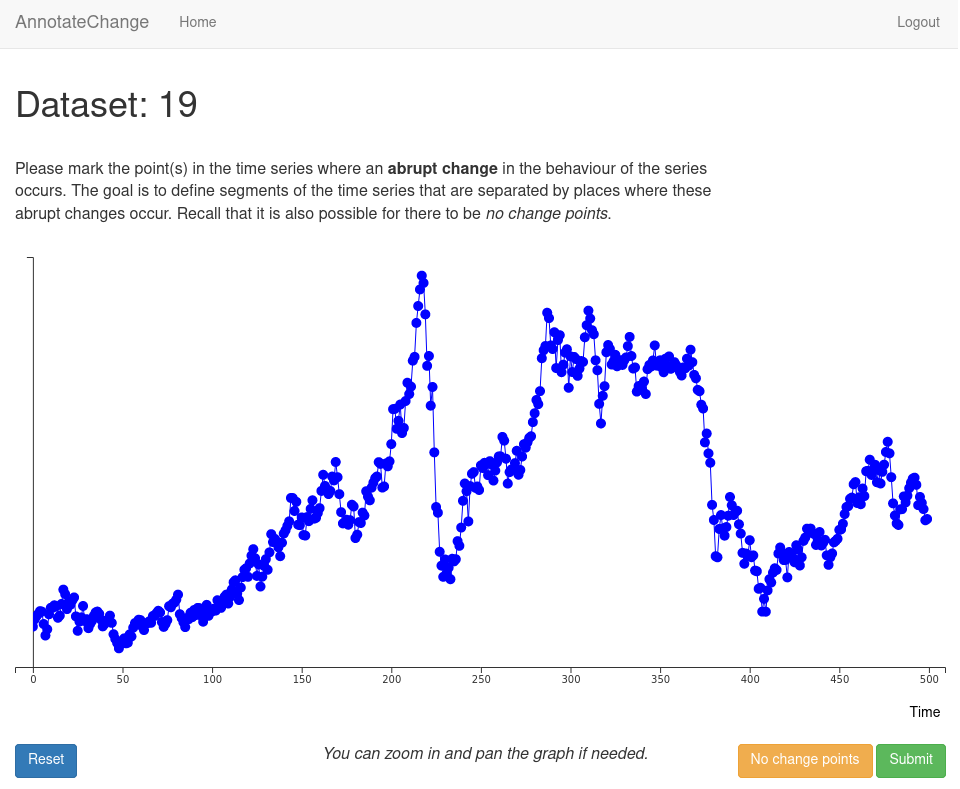

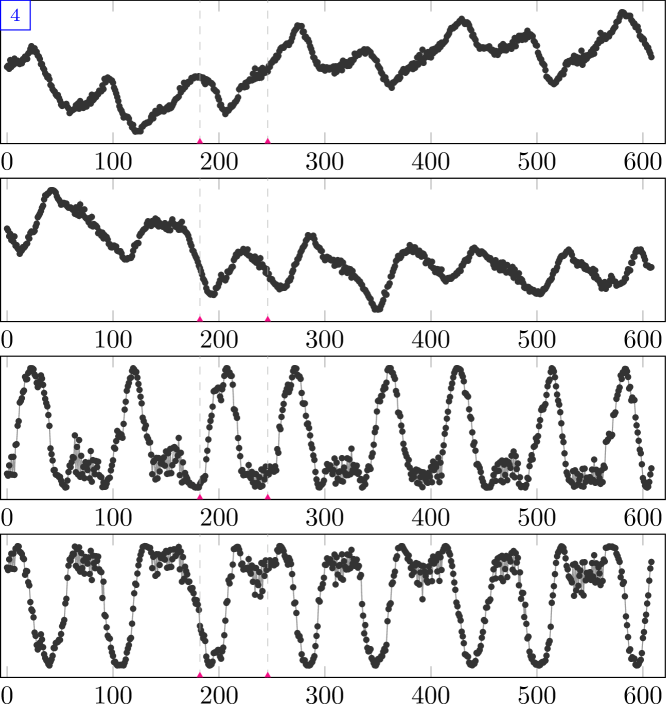

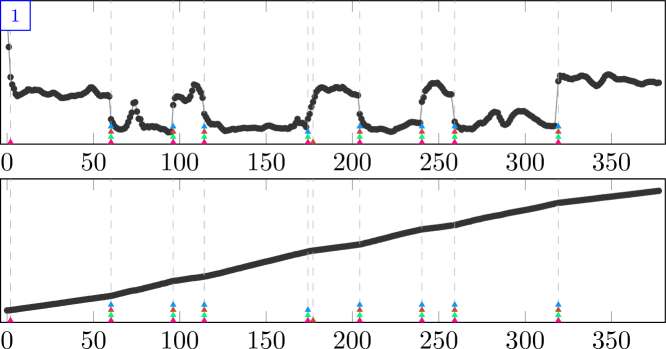

To facilitate the collection of the annotated data set, we created a web application that enables annotators to mark change points on a plot of a time series (see Figure 1).444The web application is made available as open-source software, see: https://github.com/alan-turing-institute/AnnotateChange. Annotators can select multiple change points in the data or can signal that they believe the time series contains no change points. The application allows the annotators to zoom in and pan to particular sections of the time series for closer inspection. Before annotators are provided with any real-world time series, they are required to go through a set of introductory pages that describe the application and show various types of change points (including changes in mean, variance, trend, and seasonality). These introductory pages also illustrate the difference between a change point and an outlier. During this introduction the annotator is presented with several synthetic time series with known change points and provided with feedback on the accuracy of their annotations. If the annotator’s average F1-score is too low on these introductory data sets, they are kindly asked to repeat the introduction. This ensures that all annotators have a certain baseline level of familiarity with annotating change points.

To avoid that annotators use their knowledge of historical events or are affected by other biases, no dates are shown on the time axis and no values are present on the vertical axis. The names of the series are also not shown to the annotators. Furthermore, the annotation page always displays the following task description to the annotators:

Please mark the point(s) in the time series where an abrupt change in the behavior of the series occurs. The goal is to define segments of the time series that are separated by places where these abrupt changes occur. Recall that it is also possible for there to be no change points.

This description is purposefully left somewhat vague to avoid biasing the annotators in a specific direction, and is inspired by the rubric in the BSDS (Martin et al., 2001).

4.2 Data Sources

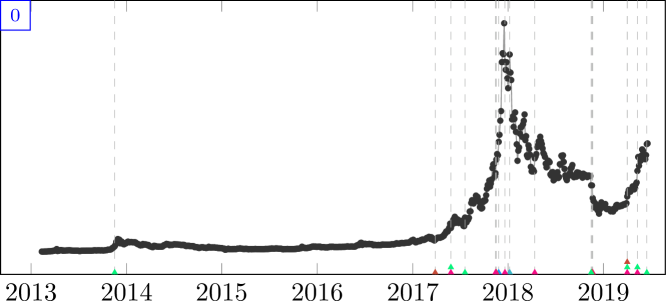

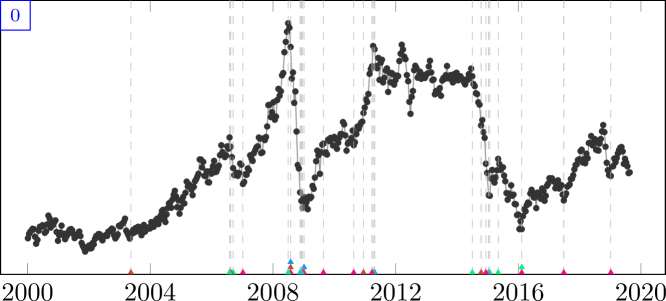

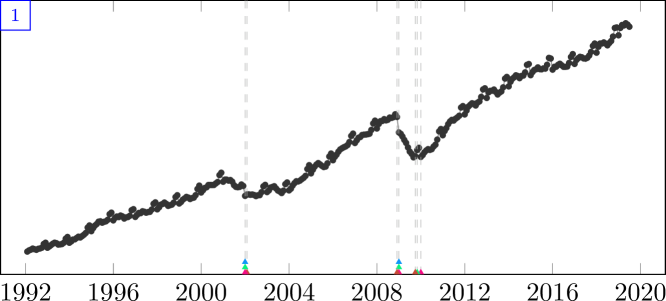

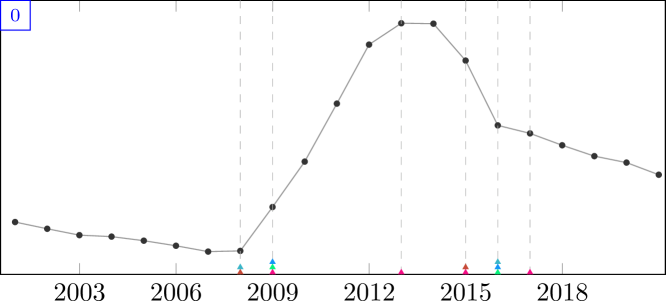

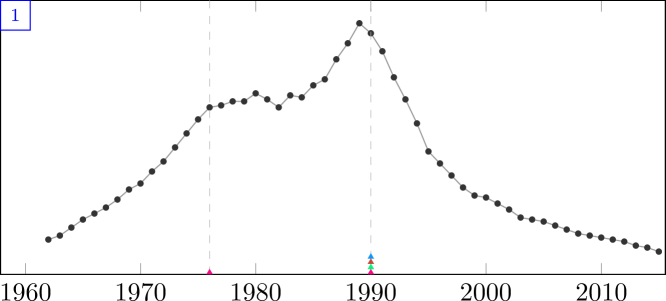

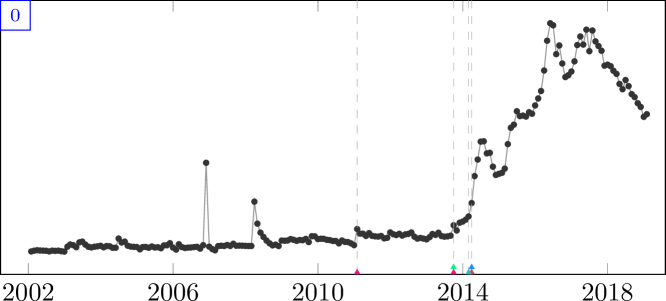

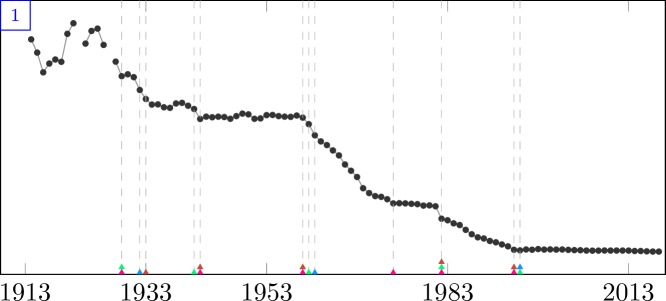

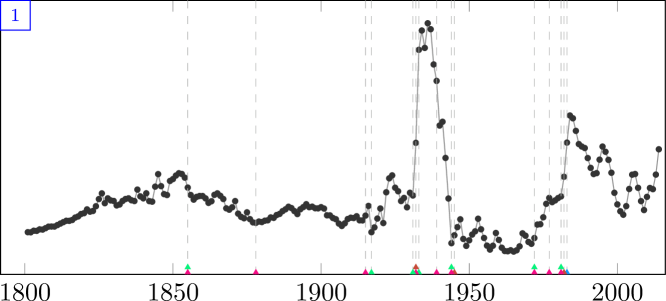

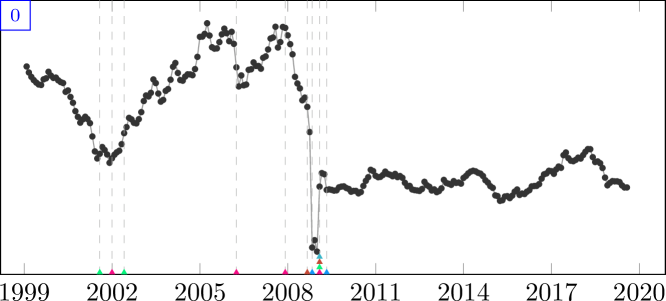

Time series were collected from various online sources including the WorldBank, EuroStat, U.S. Census Bureau, GapMinder, and Wikipedia. A number of time series show potential change point behavior around the financial crisis of 2007–2008, such as the price for Brent crude oil (Figure 1), U.S. business inventories, and U.S. construction spending, as well as the GDP series for various countries. Other time series are centered around introduced legislation, such as the mandatory wearing of seat belts in the U.K., the Montreal Protocol regulating CFC emissions, or the regulation of automated phone calls in the U.S. Various data sets are also collected from existing work on change point detection and structural breaks, such as the well-log data set (Ó Ruanaidh and Fitzgerald, 1996), a Nile river data set (Durbin and Koopman, 2012), and a sequence from the bee-waggle data set (Oh et al., 2008). The main criterion for including a time series was whether it displayed interesting behavior that might include an abrupt change. Several time series were included that may not in fact contain a change point but are nevertheless considered interesting for evaluating CPD algorithms due to features such as seasonality or outliers.

A total of 37 real time series were collected for the change

point data set. This includes 33 univariate and 4 multivariate series (with

either 2 or 4 dimensions). One of the univariate time series

(uk_coal_employ, Figure 37 in

Appendix D) has two missing observations, and nine other

series show seasonal patterns. Unbeknownst to the annotators we added

5 simulated “quality control” series with known change points

in the data set, which allows us to evaluate the quality of the annotators

in situ (see below). Four of these series have a change point with a

shift in the mean and the fifth has no change points. Of the quality control

series with a change point two have a change in noise distribution, one

contains an outlier, and another has multiple periodic components. The change

point data set thus consists of 42 time series in total. The

average length of the time series in the data set is

327.7, with a minimum of 15 and

a maximum of 991. Additional descriptive statistics are

provided in Table 4 in Appendix C.1 and

visualizations of all series are provided in Appendix D. Note

that because we ask the annotators to mark all points in the series

that they believe to be change points, we have chosen time series for which

this task is feasible.

4.3 Annotation Collection

Annotations were collected in several sessions by inviting data scientists and

machine learning researchers to annotate the series. We deliberately chose not

to ask individuals who have extensive background knowledge on the various

domains of the time series, as this could affect the objectivity of their

annotations. For example, asking someone who is familiar with oil prices to

annotate the brent_spot series might allow them to use outside

knowledge that is not available from the behavior of the series alone. The

annotation tool randomly assigned time series to annotators whenever they

requested a new series to annotate, with a bias towards series that already

had annotations. The same series was never assigned to an annotator more than

once. In total, eight annotators provided annotations for the

42 time series, with five annotators assigned

to each time series. On average the annotators marked

7.4 unique change points per series, with a

standard deviation of 7.0, a minimum of

0 and a maximum of

26. The provided annotations for each series are

shown in Appendix D.

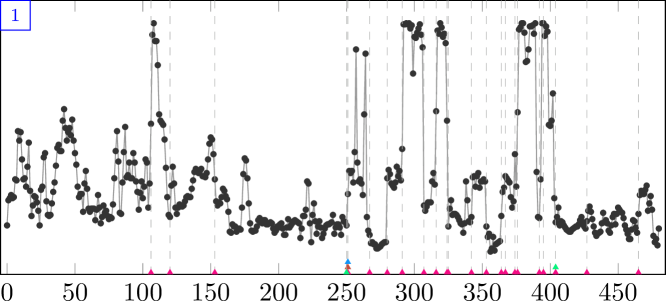

Although all annotators successfully completed the introduction before annotating any real time series, some nonetheless commented on the difficulty of deciding whether a series had a change point or not. In some cases this was due to a significant change spanning multiple time steps, which led to ambiguity about whether the transition period should be marked as a separate segment or not (see e.g., Figure 1). Another source of ambiguity were periodic time series with abrupt changes (e.g., bank, Figure 6), which could be regarded as a stationary switching distribution without abrupt changes or a series with frequent change points. In these cases annotators were advised to use their intuition and experience as data scientists to evaluate whether they considered a potential change to be an abrupt change. Note that uncertainty in the exact position of an annotation is partially alleviated by the margin of error included in the evaluation metrics (in particular the F1-score, see Section 3).

4.4 Consistency

As mentioned above we included five “quality control” series to evaluate the

accuracy and consistency of the human annotators in practice, which are shown

in Appendix D.2. On two of the four series with known

change points (Figure 42 and

Figure 44) all annotators identified the true change

point within three time steps of the correct location. On another time series,

quality_control_2, four of the five annotators identified the change

point within two time steps, with a fifth annotator believing there to be no

change points (Figure 43). The most difficult series to

annotate was the one with periodic features (quality_control_4,

Figure 45). Here, two of the annotators voted there to

be no change points while the three other annotators identified the change

correctly within three time steps, with one also incorrectly marking several

other points as change points. The series without change points,

quality_control_5, was correctly identified as such by all annotators.

This suggests that human annotators can identify the presence and location of

change points with high accuracy on most kinds of time series, with seasonal

effects posing the biggest challenge.

To quantitatively assess the consistency of the annotators we evaluate each

individual annotator against the four others on every time series, using the

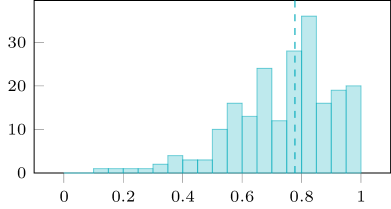

metrics presented previously. Figure 2 shows the histograms

of these one-vs-rest (OvR) scores for both metrics. The figures show that on

average there is a high degree of agreement between annotators, with the

median annotator score approximately 0.8 for the covering metric and 0.9 for

the F1-score (for both metrics a score of 1.0 indicates perfect agreement). It

can also be seen that the values are generally higher on the F1-score, which

is due to the margin of error in this metric and the fact that the F1-score

uses the union of annotated change points in the definition of the precision.

In Appendix B we additionally present a simulation

study to explore the extent to which the observed annotator agreement can be

expected by chance. We find that for both metrics and for the majority of time

series the observed average OvR annotator agreement is significantly higher

than can be expected by chance. The few cases with low agreement are often due

to one or two annotators disagreeing with the others. An example of this is

the lga_passengers series, where there is a high level of agreement

between four of the annotators about the number and approximate location of

the change points, but one annotator believes there are no change points (see

Figure 24).

5 Benchmark Study

This section presents a benchmark study of existing change point algorithms on the data set of human-annotated time series. We describe the methods included in the study, the setup of the experiments, and the results of the evaluation. The code and data used in this benchmark study are available through an online repository.555See: https://github.com/alan-turing-institute/TCPDBench.

| Name | Method | Reference |

|---|---|---|

| amoc | At Most One Change | Hinkley (1970) |

| binseg | Binary Segmentation | Scott and Knott (1974) |

| bocpd | Bayesian Online Change Point Detection | Adams and MacKay (2007) |

| bocpdms | bocpd with Model Selection | Knoblauch and Damoulas (2018) |

| cpnp | Nonparametric Change Point Detection | Haynes et al. (2017) |

| ecp | Energy Change Point | Matteson and James (2014) |

| kcpa | Kernel Change-Point Analysis | Harchaoui et al. (2009) |

| pelt | Pruned Exact Linear Time | Killick et al. (2012) |

| prophet | Prophet | Taylor and Letham (2018) |

| rbocpdms | Robust bocpdms | Knoblauch et al. (2018) |

| rfpop | Robust Functional Pruning Optimal Partitioning | Fearnhead and Rigaill (2019) |

| segneigh | Segment Neighborhoods | Auger and Lawrence (1989) |

| wbs | Wild Binary Segmentation | Fryzlewicz (2014) |

| zero | No Change Points |

5.1 Experimental Setup

The aim of the study is to obtain an understanding of the performance of existing change point methods on real-world data. With that in mind we evaluate a large selection of methods that are either frequently used or that have been recently developed. Table 1 lists the methods included in the study. To avoid issues with implementations we use existing software packages for all methods, which are almost always made available by the authors themselves. We also include the baseline zero method, which always returns that a series contains no change points.

Many of the methods have (hyper)parameters that affect the predicted change point locations. To obtain a realistic understanding of how accurate the methods are in practice, we create two separate evaluations: one showing the performance using the default settings of the method as defined by the package documentation, and one reporting the maximum score over a grid search of parameter configurations. We refer to these settings as the “Default” and “Oracle” experiments, respectively. The Default experiment aims to replicate the common practical setting of a data analyst trying to detect potential change points in a time series without any prior knowledge of reasonable parameter choices. The Oracle experiment aims to identify the highest possible performance of each algorithm by running a full grid search over its hyperparameters. It should be emphasized that while the Oracle experiment is important from a theoretical point of view, it is not necessarily a realistic measure of practical algorithm performance. Due to the unsupervised nature of the change point detection problem we can not in general expect those who use these methods to be able to tune the parameters such that the results match the unknown ground truth. For a detailed overview of how each method was applied, see Appendix A.

Since not all methods support multidimensional time series or series with missing values, we separate the analysis further into univariate and multivariate time series. While it is possible to use the univariate methods on multidimensional time series by, for instance, combining the detected change points of each dimension, we chose not to do this as it could skew the reported performance with results on series that the methods are not explicitly designed to handle. Furthermore, because the programming language differs between implementations we do not report on the computation time of the methods. All series are standardized to zero mean and unit variance to avoid issues with numerical precision arising for some methods on some of the time series. The quality control time series were not included in the benchmark study, but performance on these series is reported in Appendix C.1.

The Bayesian online change point detection algorithms that follow the framework of Adams and MacKay (2007) compute a full probability distribution over the location of the change points and therefore do not return a single segmentation of the series. To allow for comparisons to the other methods we use the maximum a posteriori (MAP) segmentation of the series (see, e.g., Fearnhead and Liu, 2007). The MAP segmentation results in a single set of detected change points that can be compared to those provided by offline methods.

5.2 Results

| Default | Oracle | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Univariate | Multivariate | Univariate | Multivariate | ||||||||

| Cover | F1 | Cover | F1 | Cover | F1 | Cover | F1 | ||||

| amoc | 0.668 | 0.653 | 0.717 | 0.773 | |||||||

| binseg | 0.672 | 0.698 | 0.774 | 0.873 | |||||||

| bocpd | 0.594 | 0.662 | 0.455 | 0.610 | 0.783 | 0.886 | 0.801 | 0.941 | |||

| bocpdms | 0.590 | 0.495 | 0.512 | 0.426 | 0.753 | 0.659 | 0.689 | 0.654 | |||

| cpnp | 0.488 | 0.586 | 0.759 | 0.845 | |||||||

| ecp | 0.470 | 0.560 | 0.402 | 0.545 | 0.693 | 0.773 | 0.590 | 0.725 | |||

| kcpa | 0.069 | 0.124 | 0.047 | 0.071 | 0.608 | 0.686 | 0.649 | 0.774 | |||

| pelt | 0.652 | 0.674 | 0.772 | 0.864 | |||||||

| prophet | 0.522 | 0.472 | 0.554 | 0.502 | |||||||

| rbocpdms | 0.561 | 0.397 | 0.485 | 0.352 | 0.717 | 0.677 | 0.649 | 0.559 | |||

| rfpop | 0.341 | 0.476 | 0.784 | 0.870 | |||||||

| segneigh | 0.642 | 0.635 | 0.777 | 0.875 | |||||||

| wbs | 0.264 | 0.365 | 0.366 | 0.482 | |||||||

| zero | 0.566 | 0.645 | 0.464 | 0.577 | 0.566 | 0.645 | 0.464 | 0.577 | |||

We first analyze the average scores for each of the methods in the two experiments, before presenting an in-depth analysis of statistically significant differences. Table 2 shows the average scores on each of the considered metrics for both experiments (complete results are available in Appendix C).666For the Default experiment the rbocpdms method failed on two of the univariate time series (bitcoin and scanline_126007) and therefore received a score of zero on these series. Results on uk_coal_employ are excluded from the results for both experiments because the majority of methods do not handle time series with missing values. We see that for the Default experiment the binseg method of Scott and Knott (1974) achieves the highest average performance on the univariate time series, closely followed by amoc (on the covering metric) and pelt (on the F1 score). For this experiment the bocpdms method (Knoblauch and Damoulas, 2018) does best for the multivariate series when using the covering metric, but bocpd (Adams and MacKay, 2007) does best on the F1-score. In the Oracle experiment — where hyperparameters of the methods are varied to achieve better performance — we see that bocpd does best for both the univariate and multivariate time series on the F1 score, but rfpop does slightly better on the univariate experiments when using the covering metric.

We note that the zero method outperforms many of the other methods, especially in the Default experiment. This is in part due to the relatively small number of change points per series, but also suggests that many methods return a large number of false positives. Furthermore, we see that for prophet and wbs the hyperparameter tuning has a relatively small effect on performance. This is unsurprising however, since these methods also have a small number of hyperparameters that can be varied. For instance, for prophet only the maximum number of change points can be tuned, and the results show that this is insufficient to achieve competitive performance. By contrast, parameter tuning has a significant effect on the performance of kcpa and rfpop, making the latter competitive with the best performing methods. We reiterate however, that the Oracle experiment is not indicative of real-world performance, since a data scientist would have no automatic way of identifying the most accurate segmentation of the series among those found by a grid search (which in the case of rfpop total over 2400 configurations, see Appendix A).

While the average scores allow for general statements on the performance of the different methods, they are not suitable for evaluating the significance of performance differences because they represent measurements on distinct data sets (Demšar, 2006). Instead, an analysis of ranks can be used to show statistically significant differences. This involves assigning a numeric rank to method on data set with the best performing method receiving rank 1, the second best rank 2, etc. In the case of ties fractional ranks are assigned (i.e., if two methods achieve the highest score on a data set they are both assigned rank 1.5 and the third-best method is assigned rank 3). As discussed in detail in Demšar (2006), the Friedman test is a non-parametric test to evaluate the null hypothesis that all methods perform equally well. Furthermore, pairwise tests can be performed to assess whether two methods perform significantly differently, while correcting for the family-wise error rate.

Let denote the average rank of method over all data sets. Under the null hypothesis of equal performance between the methods the Friedman test statistic, given by

| (7) |

follows a distribution with degrees of freedom (Friedman, 1937, 1940). When running this test for the experiments on univariate data sets we reject the null hypothesis for both metrics on both experiments ( in all cases, resulting in -values of zero). We can subsequently perform post-hoc tests to uncover statistically significant differences between methods. While Demšar (2006) recommends the Nemenyi test (Nemenyi, 1963) as a post-hoc test for individual differences, later work by Benavoli et al. (2016) argued that the Wilcoxon signed-rank test is to be preferred (Wilcoxon, 1945). Thus, for each pair of methods we compute the Wilcoxon signed-rank test with the null hypothesis of no significant differences in the performance of two methods. To correct for multiple testing we subsequently apply Holm’s procedure to control the family-wise error rate (Holm, 1979).

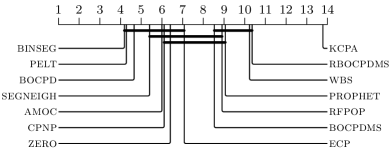

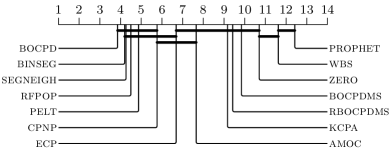

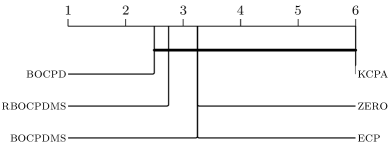

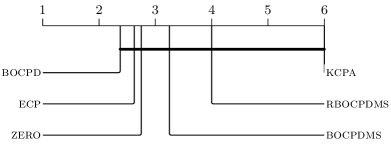

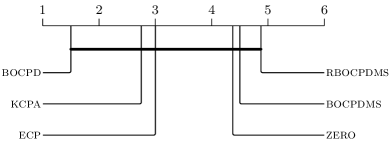

To summarize the results of the statistical tests we use the critical-difference (CD) diagrams proposed by Demšar (2006), see Figure 3. These figures show the average ranks of the methods, with methods that are not significantly different from each other connected by horizontal lines. For example, in Figure 3a the wbs and rfpop methods perform statistically significantly different from all other methods, but not from each other. The CD-diagram for the Oracle experiment also shows that when hyperparameters can be varied the bocpd method achieves the highest average rank. Moreover, depending on the metric considered it also statistically significantly outperforms a number of alternative methods (8 methods for the F1 score). It is noteworthy that even though bocpd assumes a simple Gaussian model with constant mean for each segment, it outperforms methods that allow for more complex time series behavior such as trend and seasonality (prophet), or autoregressive structures (bocpdms). From the critical difference diagrams we can also see that for both experiments and metrics, the kcpa, prophet, and wbs methods perform statistically significantly worse than the best performing methods. We also see that in our experiments no method performs significantly better than the zero method on the Default experiment, while this does not hold for the Oracle experiment.

By analyzing the performance of the methods on each individual time series in

the data set we can gain some understanding of which time series are “easy”,

in the sense that many methods achieve high scores on the evaluation metrics

(see Appendix C). For the Default

experiment, it is particularly noticeable that 9 of the 14 methods achieve an

F1 score of 1.0 on the nile time series. One possible explanation for

this could be that this series exhibits a single change point (according to

most annotators, see Figure 26), which also appears to be a clear

shift in the mean of the series. We can also look at which time series

appeared to be “difficult”, in the sense that the methods failed to do well

on it. Here, one noticeable case is the businv series where annotators

generally agree on three change point locations, yet even in the Oracle

experiment the maximum obtained F1 score is only 0.650.

Finally, we observe that the choice of evaluation metric affects the ranking of the algorithms (see Figure 3). Because the annotations are combined in a single set of ground truth change points when computing the precision, it is easier to achieve a high F1-score than it is to obtain a high score on the covering metric. Indeed, a high score on the covering metric indicates a high degree of agreement with each individual annotator, whereas a high value on the F1-score indicates a strong agreement with the combined set of annotations. Nevertheless, the best performing method is the same regardless of the metric, which reflects a degree of stability in the relative performance of the methods.

6 Discussion

We have introduced the first dedicated data set of human-annotated real-world time series from diverse application domains that is specifically designed for the evaluation and development of change point detection algorithms. Moreover, we have presented a framework for evaluating change point detection algorithms against ground truth provided by multiple human annotators, with two change point metrics that take distinct but complementary approaches to evaluating detection performance. With this data set we have conducted a thorough evaluation of a large selection of existing change point algorithms in an effort to discover those that perform best in practice. This benchmark study has shown that the binary segmentation algorithm of Scott and Knott (1974) performs best on univariate time series when using the default algorithm parameters from Killick and Eckley (2014), but its performance is not statistically significantly different from several other change point detection methods. When hyperparameter tuning is performed, the bocpd method of Adams and MacKay (2007) outperforms all other methods on both univariate and multivariate time series. However, the differences between it and some other algorithms (binseg, segneigh, and rfpop, among others) have been shown to not be statistically significantly different.

Both the introduced data set and the benchmark study can be extended and improved in the future, and our open-source code repository linked previously is set up to facilitate this. However, the present paper has already provided novel insights in the practical performance of change point detection algorithms and indicated potential topics for further research on algorithm development. For instance, future work could focus on incorporating automated hyperparameter tuning methods to bridge the gap between the Default and Oracle performance of the methods (perhaps taking inspiration from the work of Turner et al., 2009 for bocpd). It would also be relevant to understand why binseg performs as well or better than some of the more advanced methods, especially in the absence of hyperparameter tuning. Importantly, the presented change point data set and benchmark study motivate these research directions based on a quantitative analysis of algorithm performance, which was not previously possible.

Because of the unsupervised nature of the change point detection problem, it is difficult to compare algorithms in settings other than through simulation studies. But since the goal is ultimately to apply these algorithms to real-world time series, we should strive to ensure that they work well in practice. The change point data set presented here was inspired by the Berkeley Segmentation Data Set introduced in Martin et al. (2001) as well as the PASCAL VOC challenge (Everingham et al., 2010). In the past, these data sets have been crucial in accelerating the state of the art in image segmentation and object recognition, respectively. Our hope is that the data set and the benchmark study presented in this work can do the same for change point detection.

Acknowledgments

The authors would like to thank James Geddes as well as the other annotators who preferred to remain anonymous. We are also grateful to Siamak Zamani Dadaneh for helpful comments on an earlier version of this manuscript, as well as for suggesting the zero baseline method. Finally, we would like to thank the anonymous reviewers for their comments, which have helped improve the paper. This work was supported in part by The Alan Turing Institute under EPSRC grant EP/N510129/1.

Changelog

Below is a list of changes to the arXiv version of this paper.

-

•

v3

-

–

Expanded the grid search for some of the methods in the Oracle experiment

-

–

Changed from rank plots to critical-difference diagrams

-

–

Updated the results section taking into account the above changes

-

–

Expanded analysis of annotator agreement

-

–

Various minor corrections and clarifications

-

–

-

•

v2

-

–

Added the zero method to the comparison.

-

–

Added summary statistics in the text regarding the length of the time series and the number of annotated change points.

-

–

Added rank plots for multivariate time series to the appendix.

-

–

Corrected an error in the computation of the F1 score and updated the results and the online code repository. This correction had no major effect on our conclusions.

- –

-

–

Updated acknowledgements.

-

–

-

•

v1

-

–

Initial version.

-

–

Appendix A Simulation Details

This section presents additional details of the implementations and configurations used for each of the algorithms. Where possible, we used packages made available by the authors of the various methods. During the grid search those hyperparameter configurations that led to computational errors (e.g., numerical overflow) were skipped. While we describe our experimental setup in detail below, we also recommend the reader to check our online repository to reproduce our setup exactly.777See: https://github.com/alan-turing-institute/TCPDBench.

-

•

amoc, binseg, pelt, and segneigh were implemented using the R

changepointpackage, v2.2.2 (Killick and Eckley, 2014).-

–

As default parameters we used the

cpt.meanfunction, following Fryzlewicz (2014), with the Modified Bayes Information Criterion (MBIC) penalty, the Normal test statistic, and minimum segment length of 1. For binseg and segneigh we additionally used the default value of for the maximum number of change points/segments. -

–

During the grid search, we varied the parameters as follows:

- Function:

-

cpt.mean,cpt.var, andcpt.meanvar. - Penalty:

-

None, SIC, BIC, MBIC, AIC, Hannan-Quinn, Asymptotic (using p-value 0.05), and Manual (with a grid of 101 values for the regularization parameter, evenly spaced on a log scale between and ).

- Test Statistic:

-

Normal, CUSUM, CSS, Gamma, Exponential, and Poisson (where appropriate for the specified function).

- Max. CP:

-

5 (default) or (max). Only for binseg or segneigh.

Combinations of parameters that were invalid for the method were ignored.

-

–

-

•

cpnp was implemented with the R

changepoint.nppackage (v0.0.2). The penalty was varied in the same way as for pelt (see above) with the addition that in the grid search the number of quantiles was varied on the grid . -

•

rfpop was called using the

robsegpackage available on GitHub.888https://github.com/guillemr/robust-fpop, version 2019-07-02. As default setting the biweight loss function was used. During the grid search the parameters were varied as follows:- Loss:

-

L1,L2,Outlier,Huber - Penalty value:

-

lambdawas varied on a grid of 101 values evenly spaced on a log scale between and (as above for the methods in thechangepointpackage). - Threshold:

-

the

lthresholdparameter was varied on a grid of 11 values evenly spaced on a log scale between and .

We observe that because in addition to the loss function this method has two parameters that need to be evaluated on a grid, it has the largest number of hyperparameter configurations of any method in the Oracle experiment ( in total).

-

•

ecp and kcpa were accessed through the R

ecppackage (v3.1.1) available on CRAN (James and Matteson, 2013). For ecp the parameter settings were:-

–

As default parameters we used the

e.divisivefunction with , minimum segment size of 30, 199 runs for the permutation test and a significance level of 0.05. -

–

The grid search consisted of:

- Algorithm:

-

e.divisiveore.agglo - Significance level:

-

0.05 or 0.01.

- Minimum segment size:

-

2 (minimal) or 30 (default)

-

:

For the

e.aggloalgorithm only the parameter has an effect.

The kcpa method takes two parameters: a cost and a maximum number of change points. In the default experiment the cost parameter was set to 1 and we allowed the maximum number of change points possible. In the grid search the cost parameter was varied in the same way as above for the methods in the

changepointpackage, on a grid of 101 values evenly spaced on a log scale between and , and the maximum number of change points was varied between the maximum possible and , which corresponds to the methods in thechangepointpackage. -

–

-

•

wbs was evaluated using the R package of the same name available on CRAN (v1.4).

-

–

As defaults we used the SSIC penalty, the integrated version, and the default of 50 for the maximum number of change points.

-

–

During the grid search we used:

- Penalty:

-

SSIC, BIC, MBIC

- Integrated:

-

true, false

- Max CP:

-

50 (default) or (max)

-

–

-

•

bocpd was called using the R package

ocp(v0.1.1), available on CRAN (Pagotto, 2019). For the experiments we used the Gaussian distribution with the negative inverse gamma prior. The prior mean was set to , since the data is standardized. No truncation of the run lengths was applied.-

–

For the default experiment the intensity () was set to 100, the prior variables were set to , , and .

-

–

For the grid search, we varied the parameters as follows:

- Intensity:

-

- :

-

- :

-

- :

-

-

–

-

•

bocpdms and rbocpdms were run with the code available on GitHub.999https://github.com/alan-turing-institute/bocpdms/ at Git commit hash f2dbdb5, and https://github.com/alan-turing-institute/rbocpdms/ at Git commit hash 643414b, respectively. The settings for bocpdms were the same as that for bocpd above, with the exception that during the grid search run length pruning was applied by keeping the best 100 run lengths. This was done for speed considerations. No run length pruning was needed for bocpdms with the default configuration, but this was applied for rbocpdms. For rbocpdms we used the same settings, but supplied additional configurations for the and parameters. As default values and during the grid search we used . For both methods we applied a timeout of 30 minutes during the grid search and we used a timeout of 4 hours for rbocpdms in the default experiment.

-

•

prophet was run in R using the

prophetpackage (v0.4). As Prophet requires the input time vector to be a vector of dates or datetimes, we supplied this where available and considered the series that did not have date information to be a daily series. By supplying the dates of the observations Prophet automatically chooses whether to include various seasonality terms. For both experiments we allowed detecting of change points on the entire input range and used a threshold of for selecting the change points (in line with the change point plot function in the Prophet package). During the grid search we only varied the maximum number of change points between the default (25) and the theoretical maximum ().

Appendix B Simulated Annotator Agreement

In this section we present the results of a simulation study that aims to quantify the extent to which the annotator agreement described in Section 4.4 can be expected by chance.

For every time series in the data set we simulate a set of change point annotations for each of the annotators. Next, for each annotator we compute the one-vs-rest (OvR) annotator agreement compared to the simulated other annotators, as described in the main text. These values are then averaged into a single value that represents the simulated average OvR annotator agreement. By repeating this process a large number of times we obtain a distribution over the average OvR annotator agreement for a particular time series. Naturally, we can also compute the average OvR annotator agreement for the human annotators. We can then compute the -value for the hypothesis that the average OvR annotator agreement for the human annotators is larger than what is expected by chance. Formally, if is a random variable reflecting the distribution of the simulated average OvR annotator agreement and is the observed human OvR annotator agreement, then we are interested in the probability .

Recall from the main text that is the number of change points identified by annotator , and is the index of change point . We simulate the annotations as follows for each simulated annotator ,

| (8) | ||||

| (9) |

where is a hyperparameter for the simulation discussed below. Note that the domain for the change points is chosen such that no change points can be declared at the first and last time index.101010For very short time series (e.g., centralia) the value of may exceed the length of the series if the rate of the Poisson distribution, , is set too high. If that occurs in the simulation is capped at the maximum possible value of . For each time series in the data set we simulate 100,000 sets of annotations and compute the average OvR annotator agreement. The -value for each series is then approximated as the proportion of realizations of that are larger or equal to . The rate of the Poisson distribution, , affects the number of change points for each simulated annotator. A priori, there is no information on how this rate should be chosen such that the simulation is as close as possible to the real-world case. Thus, we propose to set to the number of change points declared per human annotator averaged over all time series in the data set ().

| Dataset | Covering | F1 |

|---|---|---|

apple |

0.014 | 0.001 |

bank |

0.000 | 0.000 |

bee_waggle_6 |

0.001 | 0.000 |

bitcoin |

0.008 | 0.049 |

brent_spot |

0.149 | 0.018 |

businv |

0.011 | 0.000 |

centralia |

0.172 | 0.744 |

children_per_woman |

0.000 | 0.000 |

co2_canada |

0.013 | 0.000 |

construction |

0.016 | 0.008 |

debt_ireland |

0.000 | 0.001 |

gdp_argentina |

0.042 | 0.001 |

gdp_croatia |

0.006 | 0.013 |

gdp_iran |

0.015 | 0.006 |

gdp_japan |

0.009 | 0.000 |

global_co2 |

0.051 | 0.000 |

homeruns |

0.606 | 0.043 |

iceland_tourism |

0.000 | 0.000 |

jfk_passengers |

0.004 | 0.003 |

lga_passengers |

0.275 | 0.003 |

measles |

0.000 | 0.000 |

nile |

0.002 | 0.000 |

occupancy |

0.416 | 0.001 |

ozone |

0.009 | 0.001 |

quality_control_1 |

0.000 | 0.000 |

quality_control_2 |

0.001 | 0.000 |

quality_control_3 |

0.000 | 0.000 |

quality_control_4 |

0.145 | 0.001 |

quality_control_5 |

0.000 | 0.000 |

rail_lines |

0.002 | 0.001 |

ratner_stock |

0.000 | 0.012 |

robocalls |

0.019 | 0.018 |

run_log |

0.052 | 0.001 |

scanline_126007 |

0.735 | 0.014 |

scanline_42049 |

0.002 | 0.000 |

seatbelts |

0.005 | 0.000 |

shanghai_license |

0.000 | 0.000 |

uk_coal_employ |

0.389 | 0.002 |

unemployment_nl |

0.718 | 0.005 |

us_population |

0.011 | 0.000 |

usd_isk |

0.001 | 0.003 |

well_log |

0.005 | 0.001 |

Using the above simulation setup we obtain the -values listed in

Table 3. We observe that conditional on the assumptions made

in the simulation, for most time series in the data set the observed average

OvR annotator agreement for the human annotators is significantly larger than

what can be expected by chance. For the F1-score we find a -value larger

than only for the centralia time series. This is unsurprising

for two reasons: this series consists of only 15 observations, and there is

disagreement amongst the annotators on the existence of change points in the

series. For the covering metric there are few additional series where the

-value obtained from the simulation is larger than . This can be

explained by the fact that this metric rewards high agreement with each

individual annotator, and in these series there is some amount of

disagreement among the annotators.

Appendix C Additional Tables and Figures

Below we present additional tables and figures to support the material in the main text. In some tables the results on the quality control time series are included for completeness, but these are not used in the benchmark study.

C.1 Tables

| Frequency | Length () | Dim. () | Min CP | Max CP | Avg CP | |

|---|---|---|---|---|---|---|

1. apple |

Daily† | 622 | 2 | 1 | 8 | 2.4 |

2. bank |

Daily | 581 | 1 | 0 | 0 | 0.0 |

3. bee_waggle_6 |

Unit | 609 | 4 | 0 | 2 | 0.4 |

4. bitcoin |

Daily† | 774 | 1 | 1 | 7 | 4.0 |

5. brent_spot |

Fortnightly | 500 | 1 | 2 | 11 | 6.0 |

6. businv |

Monthly | 330 | 1 | 0 | 3 | 2.2 |

7. centralia |

Decenially | 15 | 1 | 0 | 3 | 1.2 |

8. children_per_woman |

Yearly | 301 | 1 | 1 | 4 | 2.2 |

9. co2_canada |

Yearly | 215 | 1 | 2 | 7 | 4.4 |

10. construction |

Monthly | 319 | 1 | 0 | 2 | 1.2 |

11. debt_ireland |

Yearly | 21 | 1 | 2 | 4 | 2.4 |

12. gdp_argentina |

Yearly | 59 | 1 | 0 | 3 | 1.2 |

13. gdp_croatia |

Yearly | 24 | 1 | 0 | 1 | 0.6 |

14. gdp_iran |

Yearly | 58 | 1 | 0 | 3 | 1.6 |

15. gdp_japan |

Yearly | 58 | 1 | 0 | 1 | 0.4 |

16. global_co2 |

Quadrennial | 104 | 1 | 0 | 2 | 0.8 |

17. homeruns |

Yearly | 118 | 1 | 0 | 7 | 2.2 |

18. iceland_tourism |

Monthly | 199 | 1 | 0 | 1 | 0.2 |

19. jfk_passengers |

Monthly | 468 | 1 | 0 | 2 | 1.0 |

20. lga_passengers |

Monthly | 468 | 1 | 0 | 7 | 3.4 |

21. measles |

Weekly | 991 | 1 | 0 | 1 | 0.2 |

22. nile |

Yearly | 100 | 1 | 0 | 1 | 0.6 |

23. occupancy |

Every 16 min. | 509 | 4 | 2 | 12 | 6.2 |

24. ozone |

Yearly | 54 | 1 | 0 | 2 | 1.0 |

25. quality_control_1 |

Unit | 313 | 1 | 1 | 1 | 1.0 |

26. quality_control_2 |

Unit | 283 | 1 | 0 | 1 | 0.8 |

27. quality_control_3 |

Unit | 366 | 1 | 1 | 1 | 1.0 |

28. quality_control_4 |

Unit | 500 | 1 | 0 | 4 | 1.2 |

29. quality_control_5 |

Unit | 325 | 1 | 0 | 0 | 0.0 |

30. rail_lines |

Yearly | 37 | 1 | 1 | 2 | 1.8 |

31. ratner_stock |

Daily† | 600 | 1 | 1 | 2 | 1.6 |

32. robocalls |

Monthly | 52 | 1 | 0 | 2 | 1.6 |

33. run_log |

Every 5 sec. | 376 | 2 | 0 | 9 | 6.6 |

34. scanline_126007 |

Unit | 481 | 1 | 0 | 22 | 5.2 |

35. scanline_42049 |

Unit | 481 | 1 | 2 | 10 | 6.6 |

36. seatbelts |

Monthly | 192 | 1 | 0 | 3 | 1.8 |

37. shanghai_license |

Monthly | 205 | 1 | 1 | 2 | 1.2 |

38. uk_coal_employ |

Yearly | 105 | 1 | 0 | 6 | 3.8 |

39. unemployment_nl |

Yearly | 214 | 1 | 0 | 9 | 4.0 |

40. us_population |

Monthly | 816 | 1 | 0 | 1 | 0.4 |

41. usd_isk |

Monthly | 247 | 1 | 1 | 4 | 2.4 |

42. well_log |

Unit | 675 | 1 | 2 | 17 | 9.6 |

| Dataset | amoc | binseg | bocpd | bocpdms | cpnp | ecp | kcpa | pelt | prophet | rbocpdms | rfpop | segneigh | wbs | zero |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

bank |

0.967 | 0.509 | 0.048 | 0.188 | 0.053 | 0.127 | 0.036 | 0.509 | 0.361 | 0.644 | 0.036 | 0.509 | 0.048 | 1.000 |

bitcoin |

0.764 | 0.754 | 0.717 | 0.748 | 0.364 | 0.209 | 0.046 | 0.758 | 0.723 | F | 0.168 | 0.758 | 0.304 | 0.516 |

brent_spot |

0.423 | 0.627 | 0.586 | 0.265 | 0.411 | 0.387 | 0.022 | 0.627 | 0.527 | 0.504 | 0.225 | 0.630 | 0.242 | 0.266 |

businv |

0.574 | 0.562 | 0.463 | 0.459 | 0.402 | 0.311 | 0.013 | 0.603 | 0.478 | 0.529 | 0.123 | 0.494 | 0.108 | 0.461 |

centralia |

0.675 | 0.564 | 0.612 | 0.650 | 0.564 | 0.675 | 0.440 | 0.564 | 0.675 | 0.624 | 0.528 | 0.564 | 0.253 | 0.675 |

children_per_woman |

0.798 | 0.798 | 0.758 | 0.427 | 0.486 | 0.397 | 0.048 | 0.798 | 0.521 | 0.762 | 0.154 | 0.771 | 0.186 | 0.429 |

co2_canada |

0.527 | 0.608 | 0.716 | 0.276 | 0.514 | 0.639 | 0.263 | 0.611 | 0.540 | 0.432 | 0.497 | 0.612 | 0.480 | 0.278 |

construction |

0.525 | 0.466 | 0.395 | 0.571 | 0.334 | 0.352 | 0.016 | 0.423 | 0.502 | 0.584 | 0.092 | 0.423 | 0.198 | 0.575 |

debt_ireland |

0.321 | 0.635 | 0.584 | 0.312 | 0.635 | 0.321 | 0.210 | 0.635 | 0.321 | 0.306 | 0.489 | 0.635 | 0.248 | 0.321 |

gdp_argentina |

0.667 | 0.667 | 0.630 | 0.711 | 0.451 | 0.737 | 0.061 | 0.667 | 0.534 | 0.711 | 0.332 | 0.631 | 0.068 | 0.737 |

gdp_croatia |

0.605 | 0.605 | 0.642 | 0.655 | 0.642 | 0.708 | 0.108 | 0.605 | 0.708 | 0.655 | 0.353 | 0.605 | 0.108 | 0.708 |

gdp_iran |

0.484 | 0.477 | 0.520 | 0.580 | 0.448 | 0.583 | 0.062 | 0.477 | 0.583 | 0.580 | 0.248 | 0.503 | 0.066 | 0.583 |

gdp_japan |

0.654 | 0.654 | 0.578 | 0.645 | 0.522 | 0.802 | 0.041 | 0.654 | 0.802 | 0.777 | 0.269 | 0.654 | 0.048 | 0.802 |

global_co2 |

0.743 | 0.748 | 0.640 | 0.731 | 0.313 | 0.535 | 0.173 | 0.638 | 0.284 | 0.745 | 0.368 | 0.634 | 0.187 | 0.758 |

homeruns |

0.683 | 0.683 | 0.526 | 0.677 | 0.516 | 0.611 | 0.047 | 0.683 | 0.574 | 0.559 | 0.354 | 0.590 | 0.312 | 0.511 |

iceland_tourism |

0.764 | 0.764 | 0.595 | 0.616 | 0.383 | 0.382 | 0.017 | 0.764 | 0.453 | 0.869 | 0.293 | 0.650 | 0.512 | 0.946 |

jfk_passengers |

0.839 | 0.839 | 0.541 | 0.831 | 0.561 | 0.438 | 0.008 | 0.839 | 0.373 | 0.668 | 0.264 | 0.791 | 0.409 | 0.630 |

lga_passengers |

0.427 | 0.458 | 0.496 | 0.444 | 0.473 | 0.386 | 0.013 | 0.474 | 0.434 | 0.382 | 0.412 | 0.543 | 0.477 | 0.383 |

measles |

0.951 | 0.951 | 0.081 | 0.255 | 0.098 | 0.060 | 0.005 | 0.213 | 0.603 | 0.296 | 0.046 | 0.367 | 0.081 | 0.951 |

nile |

0.880 | 0.880 | 0.888 | 0.870 | 0.880 | 0.857 | 0.032 | 0.880 | 0.758 | 0.753 | 0.880 | 0.880 | 0.880 | 0.758 |

ozone |

0.701 | 0.600 | 0.602 | 0.560 | 0.441 | 0.574 | 0.070 | 0.635 | 0.574 | 0.614 | 0.309 | 0.627 | 0.070 | 0.574 |

rail_lines |

0.786 | 0.786 | 0.767 | 0.416 | 0.738 | 0.428 | 0.103 | 0.786 | 0.534 | 0.416 | 0.439 | 0.786 | 0.103 | 0.428 |

ratner_stock |

0.873 | 0.913 | 0.796 | 0.866 | 0.380 | 0.185 | 0.021 | 0.908 | 0.444 | 0.864 | 0.162 | 0.914 | 0.176 | 0.450 |

robocalls |

0.641 | 0.641 | 0.808 | 0.622 | 0.677 | 0.601 | 0.069 | 0.641 | 0.601 | 0.607 | 0.447 | 0.760 | 0.069 | 0.601 |

scanline_126007 |

0.519 | 0.464 | 0.346 | 0.506 | 0.433 | 0.327 | 0.025 | 0.444 | 0.503 | F | 0.316 | 0.567 | 0.263 | 0.503 |

scanline_42049 |

0.424 | 0.631 | 0.892 | 0.832 | 0.529 | 0.490 | 0.121 | 0.745 | 0.441 | 0.418 | 0.257 | 0.730 | 0.432 | 0.211 |

seatbelts |

0.683 | 0.797 | 0.757 | 0.526 | 0.750 | 0.615 | 0.020 | 0.797 | 0.628 | 0.526 | 0.484 | 0.765 | 0.727 | 0.528 |

shanghai_license |

0.920 | 0.920 | 0.856 | 0.616 | 0.474 | 0.518 | 0.020 | 0.920 | 0.768 | 0.730 | 0.381 | 0.826 | 0.209 | 0.547 |

uk_coal_employ |

M | M | M | 0.429 | M | 0.356 | 0.356 | M | 0.481 | M | M | M | M | 0.356 |

unemployment_nl |

0.507 | 0.669 | 0.495 | 0.570 | 0.503 | 0.470 | 0.039 | 0.648 | 0.507 | 0.539 | 0.243 | 0.648 | 0.222 | 0.507 |

us_population |

0.736 | 0.391 | 0.219 | 0.801 | 0.391 | 0.089 | 0.003 | 0.506 | 0.096 | 0.632 | 0.803 | 0.307 | 0.043 | 0.803 |

usd_isk |

0.853 | 0.735 | 0.672 | 0.866 | 0.480 | 0.616 | 0.023 | 0.730 | 0.436 | 0.578 | 0.163 | 0.730 | 0.194 | 0.436 |

well_log |

0.453 | 0.695 | 0.776 | 0.787 | 0.772 | 0.601 | 0.020 | 0.679 | 0.411 | 0.661 | 0.787 | 0.647 | 0.719 | 0.225 |

quality_control_1 |

0.992 | 0.992 | 0.887 | 0.990 | 0.683 | 0.620 | 0.010 | 0.992 | 0.693 | 0.986 | 0.655 | 0.992 | 0.687 | 0.503 |

quality_control_2 |

0.922 | 0.922 | 0.927 | 0.921 | 0.922 | 0.927 | 0.010 | 0.922 | 0.723 | 0.922 | 0.922 | 0.922 | 0.922 | 0.638 |

quality_control_3 |

0.996 | 0.996 | 0.997 | 0.977 | 0.831 | 0.997 | 0.008 | 0.996 | 0.500 | 0.990 | 0.658 | 0.996 | 0.996 | 0.500 |

quality_control_4 |

0.563 | 0.518 | 0.511 | 0.670 | 0.481 | 0.257 | 0.009 | 0.538 | 0.508 | 0.733 | 0.059 | 0.538 | 0.080 | 0.673 |

quality_control_5 |

1.000 | 1.000 | 1.000 | 0.994 | 1.000 | 1.000 | 0.006 | 1.000 | 1.000 | 0.994 | 1.000 | 1.000 | 1.000 | 1.000 |

apple |

0.365 | 0.359 | 0.305 | 0.007 | 0.694 | 0.425 | ||||||||

bee_waggle_6 |

0.089 | 0.860 | 0.116 | 0.004 | 0.226 | 0.891 | ||||||||

occupancy |

0.549 | 0.443 | 0.530 | 0.050 | 0.437 | 0.236 | ||||||||

run_log |

0.815 | 0.387 | 0.657 | 0.128 | 0.584 | 0.304 |

| Dataset | amoc | binseg | bocpd | bocpdms | cpnp | ecp | kcpa | pelt | prophet | rbocpdms | rfpop | segneigh | wbs | zero |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

bank |

0.667 | 0.400 | 0.047 | 0.118 | 0.044 | 0.154 | 0.008 | 0.400 | 0.154 | 0.286 | 0.015 | 0.333 | 0.039 | 1.000 |

bitcoin |

0.367 | 0.426 | 0.692 | 0.269 | 0.463 | 0.338 | 0.092 | 0.672 | 0.446 | F | 0.284 | 0.672 | 0.464 | 0.450 |

brent_spot |

0.272 | 0.483 | 0.521 | 0.239 | 0.607 | 0.478 | 0.104 | 0.465 | 0.249 | 0.321 | 0.490 | 0.431 | 0.516 | 0.315 |

businv |

0.455 | 0.370 | 0.270 | 0.370 | 0.304 | 0.301 | 0.047 | 0.370 | 0.275 | 0.238 | 0.245 | 0.312 | 0.230 | 0.588 |

centralia |

0.763 | 0.909 | 0.909 | 0.846 | 0.909 | 0.763 | 0.714 | 0.909 | 0.763 | 0.846 | 1.000 | 0.909 | 0.556 | 0.763 |

children_per_woman |

0.618 | 0.618 | 0.637 | 0.337 | 0.326 | 0.349 | 0.068 | 0.618 | 0.310 | 0.432 | 0.246 | 0.337 | 0.271 | 0.507 |

co2_canada |

0.544 | 0.691 | 0.619 | 0.265 | 0.578 | 0.817 | 0.169 | 0.661 | 0.482 | 0.381 | 0.569 | 0.661 | 0.520 | 0.361 |

construction |

0.516 | 0.709 | 0.634 | 0.410 | 0.602 | 0.574 | 0.038 | 0.709 | 0.324 | 0.291 | 0.185 | 0.709 | 0.316 | 0.696 |

debt_ireland |

0.469 | 0.760 | 0.760 | 0.611 | 0.760 | 0.469 | 0.519 | 0.760 | 0.469 | 0.530 | 0.824 | 0.760 | 0.538 | 0.469 |

gdp_argentina |

0.889 | 0.889 | 0.947 | 0.583 | 0.818 | 0.824 | 0.131 | 0.889 | 0.615 | 0.452 | 0.571 | 0.947 | 0.148 | 0.824 |

gdp_croatia |

0.583 | 0.583 | 1.000 | 0.583 | 1.000 | 0.824 | 0.160 | 0.583 | 0.824 | 0.452 | 0.400 | 0.583 | 0.167 | 0.824 |

gdp_iran |

0.492 | 0.492 | 0.622 | 0.492 | 0.330 | 0.652 | 0.219 | 0.492 | 0.652 | 0.395 | 0.609 | 0.395 | 0.246 | 0.652 |

gdp_japan |

0.615 | 0.615 | 0.800 | 0.471 | 0.667 | 0.889 | 0.068 | 0.615 | 0.889 | 0.471 | 0.190 | 0.615 | 0.077 | 0.889 |

global_co2 |

0.929 | 0.929 | 0.754 | 0.458 | 0.421 | 0.754 | 0.167 | 0.754 | 0.463 | 0.458 | 0.293 | 0.754 | 0.179 | 0.846 |

homeruns |

0.812 | 0.812 | 0.729 | 0.552 | 0.604 | 0.675 | 0.133 | 0.812 | 0.723 | 0.508 | 0.661 | 0.397 | 0.593 | 0.659 |

iceland_tourism |

0.643 | 0.643 | 0.486 | 0.391 | 0.391 | 0.391 | 0.021 | 0.643 | 0.220 | 0.667 | 0.200 | 0.486 | 0.200 | 0.947 |

jfk_passengers |

0.776 | 0.776 | 0.437 | 0.559 | 0.574 | 0.437 | 0.026 | 0.776 | 0.354 | 0.296 | 0.344 | 0.650 | 0.437 | 0.723 |

lga_passengers |

0.422 | 0.438 | 0.630 | 0.297 | 0.606 | 0.392 | 0.054 | 0.438 | 0.366 | 0.348 | 0.498 | 0.395 | 0.524 | 0.535 |

measles |

0.947 | 0.947 | 0.069 | 0.124 | 0.118 | 0.069 | 0.004 | 0.124 | 0.391 | 0.117 | 0.030 | 0.327 | 0.039 | 0.947 |

nile |

1.000 | 1.000 | 1.000 | 0.800 | 1.000 | 1.000 | 0.040 | 1.000 | 0.824 | 0.452 | 1.000 | 1.000 | 1.000 | 0.824 |

ozone |

0.531 | 0.650 | 0.650 | 0.531 | 0.750 | 0.723 | 0.109 | 1.000 | 0.723 | 0.559 | 0.375 | 1.000 | 0.113 | 0.723 |

rail_lines |

0.846 | 0.846 | 0.846 | 0.349 | 0.966 | 0.537 | 0.200 | 0.846 | 0.423 | 0.349 | 0.571 | 0.846 | 0.205 | 0.537 |

ratner_stock |

0.776 | 0.824 | 0.783 | 0.500 | 0.306 | 0.282 | 0.034 | 0.650 | 0.280 | 0.559 | 0.203 | 0.824 | 0.250 | 0.571 |

robocalls |

0.800 | 0.800 | 0.966 | 0.696 | 0.832 | 0.636 | 0.179 | 0.800 | 0.636 | 0.593 | 0.714 | 0.966 | 0.182 | 0.636 |

scanline_126007 |

0.710 | 0.739 | 0.820 | 0.718 | 0.889 | 0.732 | 0.101 | 0.759 | 0.644 | F | 0.649 | 0.732 | 0.616 | 0.644 |

scanline_42049 |

0.485 | 0.713 | 0.962 | 0.844 | 0.705 | 0.580 | 0.164 | 0.804 | 0.269 | 0.390 | 0.460 | 0.748 | 0.571 | 0.276 |

seatbelts |

0.474 | 0.683 | 0.583 | 0.383 | 0.509 | 0.321 | 0.051 | 0.683 | 0.452 | 0.383 | 0.494 | 0.583 | 0.583 | 0.621 |

shanghai_license |

0.868 | 0.868 | 0.713 | 0.491 | 0.437 | 0.698 | 0.048 | 0.868 | 0.532 | 0.326 | 0.357 | 0.713 | 0.208 | 0.636 |

uk_coal_employ |

M | M | M | 0.495 | M | 0.513 | 0.513 | M | 0.639 | M | M | M | M | 0.513 |

unemployment_nl |

0.566 | 0.876 | 0.683 | 0.592 | 0.683 | 0.620 | 0.145 | 0.773 | 0.566 | 0.495 | 0.549 | 0.773 | 0.571 | 0.566 |

us_population |

1.000 | 0.667 | 0.216 | 0.471 | 0.216 | 0.174 | 0.007 | 0.471 | 0.159 | 0.320 | 0.889 | 0.320 | 0.077 | 0.889 |

usd_isk |

0.785 | 0.657 | 0.609 | 0.678 | 0.504 | 0.661 | 0.079 | 0.657 | 0.489 | 0.282 | 0.390 | 0.657 | 0.513 | 0.489 |

well_log |

0.279 | 0.534 | 0.796 | 0.797 | 0.822 | 0.818 | 0.069 | 0.555 | 0.149 | 0.517 | 0.923 | 0.485 | 0.724 | 0.237 |

quality_control_1 |

1.000 | 1.000 | 0.800 | 0.667 | 0.667 | 0.667 | 0.025 | 1.000 | 0.500 | 0.667 | 0.667 | 1.000 | 0.571 | 0.667 |

quality_control_2 |

1.000 | 1.000 | 1.000 | 0.667 | 1.000 | 1.000 | 0.028 | 1.000 | 0.545 | 0.667 | 1.000 | 1.000 | 1.000 | 0.750 |

quality_control_3 |

1.000 | 1.000 | 1.000 | 0.667 | 0.571 | 1.000 | 0.022 | 1.000 | 0.667 | 0.667 | 0.286 | 1.000 | 1.000 | 0.667 |

quality_control_4 |

0.810 | 0.873 | 0.658 | 0.438 | 0.608 | 0.393 | 0.028 | 0.726 | 0.335 | 0.360 | 0.233 | 0.726 | 0.246 | 0.780 |

quality_control_5 |

1.000 | 1.000 | 1.000 | 0.500 | 1.000 | 1.000 | 0.006 | 1.000 | 1.000 | 0.500 | 1.000 | 1.000 | 1.000 | 1.000 |

apple |

0.513 | 0.382 | 0.513 | 0.029 | 0.239 | 0.594 | ||||||||

bee_waggle_6 |

0.121 | 0.388 | 0.124 | 0.010 | 0.179 | 0.929 | ||||||||

occupancy |

0.807 | 0.461 | 0.750 | 0.107 | 0.329 | 0.341 | ||||||||

run_log |

1.000 | 0.475 | 0.792 | 0.139 | 0.660 | 0.446 |

| Dataset | amoc | binseg | bocpd | bocpdms | cpnp | ecp | kcpa | pelt | prophet | rbocpdms | rfpop | segneigh | wbs | zero |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

bank |

1.000 | 1.000 | 1.000 | 0.997 | 1.000 | 0.238 | 0.509 | 1.000 | 1.000 | 0.997 | 1.000 | 1.000 | 0.053 | 1.000 |

bitcoin |

0.771 | 0.771 | 0.822 | 0.778 | 0.757 | 0.772 | 0.778 | 0.796 | 0.723 | 0.743 | 0.802 | 0.796 | 0.409 | 0.516 |

brent_spot |

0.503 | 0.650 | 0.667 | 0.484 | 0.642 | 0.653 | 0.571 | 0.659 | 0.527 | 0.709 | 0.669 | 0.659 | 0.310 | 0.266 |

businv |

0.574 | 0.580 | 0.693 | 0.459 | 0.676 | 0.690 | 0.405 | 0.705 | 0.539 | 0.689 | 0.603 | 0.705 | 0.154 | 0.461 |

centralia |

0.675 | 0.675 | 0.753 | 0.650 | 0.675 | 0.753 | 0.753 | 0.675 | 0.675 | 0.624 | 0.675 | 0.675 | 0.253 | 0.675 |

children_per_woman |

0.804 | 0.804 | 0.834 | 0.925 | 0.817 | 0.718 | 0.613 | 0.804 | 0.521 | 0.839 | 0.798 | 0.804 | 0.284 | 0.429 |

co2_canada |

0.527 | 0.776 | 0.773 | 0.584 | 0.667 | 0.751 | 0.739 | 0.760 | 0.605 | 0.654 | 0.768 | 0.760 | 0.552 | 0.278 |

construction |

0.629 | 0.626 | 0.631 | 0.571 | 0.575 | 0.524 | 0.395 | 0.575 | 0.561 | 0.744 | 0.732 | 0.626 | 0.300 | 0.575 |

debt_ireland |

0.635 | 0.859 | 0.814 | 0.803 | 0.777 | 0.798 | 0.747 | 0.779 | 0.321 | 0.689 | 0.859 | 0.859 | 0.248 | 0.321 |

gdp_argentina |

0.737 | 0.737 | 0.737 | 0.711 | 0.737 | 0.737 | 0.367 | 0.737 | 0.592 | 0.711 | 0.737 | 0.737 | 0.326 | 0.737 |

gdp_croatia |

0.708 | 0.708 | 0.708 | 0.675 | 0.708 | 0.708 | 0.623 | 0.708 | 0.708 | 0.708 | 0.783 | 0.708 | 0.108 | 0.708 |

gdp_iran |

0.583 | 0.583 | 0.583 | 0.719 | 0.583 | 0.583 | 0.505 | 0.583 | 0.583 | 0.753 | 0.626 | 0.583 | 0.295 | 0.583 |

gdp_japan |

0.802 | 0.802 | 0.802 | 0.777 | 0.802 | 0.802 | 0.525 | 0.802 | 0.802 | 0.802 | 0.802 | 0.802 | 0.283 | 0.802 |

global_co2 |

0.758 | 0.758 | 0.758 | 0.745 | 0.758 | 0.665 | 0.602 | 0.758 | 0.284 | 0.745 | 0.758 | 0.758 | 0.338 | 0.758 |

homeruns |

0.694 | 0.694 | 0.694 | 0.681 | 0.646 | 0.694 | 0.501 | 0.694 | 0.575 | 0.688 | 0.687 | 0.694 | 0.407 | 0.511 |

iceland_tourism |

0.946 | 0.946 | 0.946 | 0.936 | 0.946 | 0.842 | 0.655 | 0.946 | 0.498 | 0.936 | 0.946 | 0.946 | 0.512 | 0.946 |

jfk_passengers |

0.844 | 0.845 | 0.842 | 0.855 | 0.845 | 0.807 | 0.563 | 0.839 | 0.373 | 0.627 | 0.859 | 0.845 | 0.514 | 0.630 |

lga_passengers |

0.434 | 0.541 | 0.563 | 0.512 | 0.534 | 0.653 | 0.536 | 0.547 | 0.446 | 0.470 | 0.547 | 0.547 | 0.501 | 0.383 |

measles |

0.951 | 0.951 | 0.951 | 0.950 | 0.951 | 0.105 | 0.400 | 0.951 | 0.603 | 0.096 | 0.951 | 0.951 | 0.084 | 0.951 |

nile |

0.888 | 0.880 | 0.888 | 0.876 | 0.880 | 0.888 | 0.888 | 0.880 | 0.758 | 0.876 | 0.888 | 0.880 | 0.880 | 0.758 |

ozone |

0.721 | 0.701 | 0.741 | 0.798 | 0.648 | 0.676 | 0.451 | 0.701 | 0.574 | 0.798 | 0.783 | 0.701 | 0.309 | 0.574 |

rail_lines |

0.786 | 0.786 | 0.789 | 0.767 | 0.803 | 0.768 | 0.773 | 0.786 | 0.534 | 0.789 | 0.786 | 0.786 | 0.103 | 0.428 |

ratner_stock |

0.874 | 0.915 | 0.908 | 0.872 | 0.892 | 0.874 | 0.771 | 0.914 | 0.444 | 0.863 | 0.914 | 0.914 | 0.182 | 0.450 |

robocalls |

0.666 | 0.788 | 0.808 | 0.741 | 0.806 | 0.808 | 0.808 | 0.760 | 0.601 | 0.672 | 0.789 | 0.760 | 0.559 | 0.601 |

scanline_126007 |

0.634 | 0.633 | 0.631 | 0.688 | 0.561 | 0.390 | 0.494 | 0.633 | 0.503 | 0.581 | 0.578 | 0.633 | 0.329 | 0.503 |

scanline_42049 |

0.425 | 0.868 | 0.892 | 0.887 | 0.787 | 0.862 | 0.860 | 0.862 | 0.441 | 0.667 | 0.866 | 0.870 | 0.690 | 0.211 |

seatbelts |

0.683 | 0.797 | 0.800 | 0.630 | 0.825 | 0.800 | 0.800 | 0.797 | 0.635 | 0.658 | 0.797 | 0.797 | 0.727 | 0.528 |

shanghai_license |

0.930 | 0.930 | 0.929 | 0.911 | 0.929 | 0.920 | 0.497 | 0.930 | 0.804 | 0.912 | 0.924 | 0.930 | 0.351 | 0.547 |

uk_coal_employ |

M | M | M | 0.504 | M | 0.356 | 0.356 | M | 0.481 | M | M | M | M | 0.356 |

unemployment_nl |

0.627 | 0.669 | 0.673 | 0.656 | 0.652 | 0.501 | 0.476 | 0.650 | 0.507 | 0.634 | 0.650 | 0.650 | 0.447 | 0.507 |

us_population |

0.803 | 0.803 | 0.737 | 0.802 | 0.734 | 0.508 | 0.272 | 0.803 | 0.135 | 0.713 | 0.803 | 0.803 | 0.050 | 0.803 |

usd_isk |

0.865 | 0.865 | 0.875 | 0.869 | 0.853 | 0.858 | 0.714 | 0.865 | 0.436 | 0.818 | 0.865 | 0.865 | 0.401 | 0.436 |

well_log |

0.463 | 0.830 | 0.803 | 0.797 | 0.825 | 0.846 | 0.864 | 0.814 | 0.411 | 0.753 | 0.846 | 0.814 | 0.768 | 0.225 |

quality_control_1 |

0.996 | 0.992 | 0.996 | 0.990 | 0.992 | 0.989 | 0.620 | 0.992 | 0.693 | 0.990 | 0.992 | 0.992 | 0.687 | 0.503 |

quality_control_2 |

0.927 | 0.927 | 0.927 | 0.922 | 0.922 | 0.927 | 0.927 | 0.922 | 0.723 | 0.922 | 0.922 | 0.927 | 0.922 | 0.638 |

quality_control_3 |

0.997 | 0.996 | 0.997 | 0.991 | 0.996 | 0.997 | 0.997 | 0.996 | 0.500 | 0.991 | 0.996 | 0.996 | 0.996 | 0.500 |

quality_control_4 |

0.742 | 0.673 | 0.673 | 0.670 | 0.673 | 0.540 | 0.535 | 0.673 | 0.673 | 0.670 | 0.673 | 0.673 | 0.506 | 0.673 |

quality_control_5 |

1.000 | 1.000 | 1.000 | 0.994 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.994 | 1.000 | 1.000 | 1.000 | 1.000 |

apple |

0.846 | 0.783 | 0.758 | 0.462 | 0.699 | 0.425 | ||||||||

bee_waggle_6 |

0.891 | 0.887 | 0.116 | 0.730 | 0.737 | 0.891 | ||||||||

occupancy |

0.645 | 0.524 | 0.666 | 0.581 | 0.544 | 0.236 | ||||||||

run_log |

0.824 | 0.563 | 0.819 | 0.824 | 0.616 | 0.304 |

| Dataset | amoc | binseg | bocpd | bocpdms | cpnp | ecp | kcpa | pelt | prophet | rbocpdms | rfpop | segneigh | wbs | zero |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

bank |

1.000 | 1.000 | 1.000 | 0.500 | 1.000 | 0.200 | 0.333 | 1.000 | 1.000 | 0.500 | 1.000 | 1.000 | 0.043 | 1.000 |