Eigen Value Analysis in Lower Bounding Uncertainty of Kalman Filter Estimates

Abstract

In this paper we are concerned with the error-covariance lower-bounding problem in Kalman filtering: a sensor releases a set of measurements to the data fusion/estimation center, which has a perfect knowledge of the dynamic model, to allow it to estimate the states, while preventing it to estimate the states beyond a given accuracy. We propose a measurement noise manipulation scheme to ensure lower-bound on the estimation accuracy of states. Our proposed method ensures lower-bound on the steady state estimation error of Kalman filter, using mathematical tools from eigen value analysis.

keywords:

Non-linear systems, estimation, monitoring, lower-bound, optimization, privacy, eigen value analysis1 Introduction

In various applications such as air traffic in Kirubarajan and Bar-Shalom (2003), ground traffic in Work et al. (2008), power grid in Ghahremani and Kamwa (2011), and health monitoring in Yi et al. (2013), state estimation plays in important role. Kalman filtering covers a wide variety of such applications. A Kalman filter used in any of these scenarios provides information about the accuracy of the state estimates. For an air traffic system this might be the accuracy of the GPS location, whereas for the smart grid this might be the power consumption pattern for a house-hold. These estimates rely on the measurement data shared by the user itself and might be publicly available. Publicly available measurement data can be utilized with a knowledge about the dynamics to accurately estimate states of a particular individual entity such as a house-hold power consumption pattern or states of a covert satellite.

The primary concern in each of these cases is to ensure that the measurement data can not be used by someone with exact knowledge of the dynamics to estimate the states beyond certain accuracy. The optimal strategy to ensure this is, not sharing any measurement data at all. This strategy is impractical because a user who wants privacy might be a part of the bigger network whose operation relies on data sharing. For a smart grid reliable data sharing of the house-hold consumption ensure optimal power distributions, whereas in case of satellites this ensures reduced risk of collision between two active satellites which have undergone orbit changing maneuvers.

Ruling out the possibility of not sharing any data, the problem essentially convert to the following: how can we transform the measurement data that will ensure state estimation error, using a Kalman filter, of some or all of the states to be always above a certain accuracy level ?

Contributions of the paper: On a formulation level, if the system dynamics for states is: and the measurement equation for measurements is: whose Kalman filtering based covariance update equation is:

where and denotes the prior and posterior covariance matrix, the question that we are interested in answering is: manipulate matrix such that a certain lower-bound is satisfied. Regulating is akin to adding synthetic measurement noise, deciding noise intensity for active sensors such as lidar or laser, and scheduling or selecting sensing regimes. Sensor selection techniques are covered in Singh et al. (2017),Zhang et al. (2017),and Tzoumas et al. (2016) among others.

Similar question is dealt most recently in Song et al. (2018). The authors investigate the existence of a linear transformation of the measurement space, compressing the measurement information, thus inflating the estimation error covariance. Apart from using a linear transform, we can also regulate the covariance of the steady state error estimates by adding noise to the measurements. This is the major difference between our work and the existing ones, is that we are interested in calculating the measurement noise covariance that satisfies the of lower-bound on the estimation error covariance.

Notations: Let and (+) represent the sets of natural number and real (positive real) numbers respectively. The state space of system is a closed set in , where is the dimension of the states. Transpose of a square matrix is denoted as . A positive definite (semi-definite) matrix is denoted by () and () if (), for some matrix . The set of all positive definite (semi-definite) matrices of size is denoted by (). Let denotes eigen value of the matrix , when we arrange them as . Similarly, singular values of , are arranged in non-increasing order: . Let diag() denotes a diagonal matrix, with as its diagonal elements. We assume that is continuous and is a Lebesgue measure and p() is the probability density function (pdf). The expected value of the random variable with respect to p() is represented as .

Layout of the paper: The remainder of the paper is organized as follows. In Section 2, we present the system model along with its corresponding measurement model. In Section 3, we present Kalman filtering, leading to the problem statement in Section 4. In Section 5, we introduce preliminary results that lead us to the algorithm to solve the sensor covariances in section 6. In Section 7, the proposed framework is applied to a system. The paper finally concludes with Section 8.

2 System dynamics and measurement model

We focus on the class of discrete-time linear time invariant stochastic systems. Let represent the true states of a system at the time instant, where for all . The dynamics is modeled as:

| (1) |

where is the state transition matrix and matrix . The process noise variable , is the dimensional zero-mean Gaussian additive noise with .

The discrete dynamics in (1) is observed by a linear measurement model. Let denote the measurement taken at the time instant as:

| (2) |

where is corrupted by a dimensional additive observation noise . The sensor noise at each time instant is a zero mean Gaussian random variable with . The matrix is known as the observation or the measurement matrix.

The initial state of (1) is modeled by a Gaussian random variable with mean and covariance . The random variable denotes the system state at the time instant. The process noise , observation noise and initial state variable are all assumed to be independent, unless otherwise specified. These assumptions are strongly motivated by analytic tractability. The restriction to zero-mean noise sources is not a loss of generality. When the noise sources are no longer zero mean, the , and matrices are modified and extra states are introduced as shown in Anderson and Moore (1979).

3 Kalman filtering

The discrete time system in (1) and (2) induces a Kalman filter, as the optimal state estimator, with dynamics:

| (Kalman Gain) | ||||

| (Mean Propagation) | ||||

| (Covariance Propagation) | ||||

| (Mean Update) | ||||

| (Covariance Update) | ||||

| (Initial State Mean) | ||||

| (Initial State Covariance) |

where the variables , denotes the prior and posterior mean estimate of the random variable , and is the Kalman gain, at time . The positive semi-definite matrices are the prior and posterior covariance matrix at time instant respectively. Matrix inverse of the observation noise covariance is defined as the precision matrix .

4 Problem statement

The problem that we address is as follows: we assume that the system matrices () and noise parameter of (1) and (2) are all known. The matrix which is the sensor noise covariance, is the design variable. For a prescribed lower bound on the steady state prior covariance of the state error estimate using Kalman filter, we need to design or the precision matrix , that satisfies a prescribed lower-bound on the steady state error covariance.

The final result is presented as a theorem. The proof of this theorem depends upon another theorems that we first prove in the succeeding section as preliminary results.

5 Preliminaries

5.1 Preliminary results:

Middleton and Goodwin (1990) introduced the Unified Algebraic Riccati Equation :

| (3) |

where and represent constant matrices, is in , the matrix is the positive definite solution to (3), and represents sampling period.

We introduce an extra parameter in UARE and call it UARE-R. This UARE-R:

| (4) |

is often encountered in Optimal Control and Estimation problems such as in Bryson (2018) and Anderson and Moore (1979).

Remarks 1: (a) Using , replacing by , and by , we recover the Continuous Time Algebraic Riccati Equation (CARE), solution to which gives us the steady state covariance for a Kalman-Bucy filter. (b) Using , replacing by , and by we recover the Discrete Algebraic Riccati Equation (DARE) associated with steady state covariance of the Kalman Filter, where denotes the steady-state error covariance matrix.

5.2 Eigen value based analysis

In the following two theorems we examine the characterization of the bounds on the matrix of the UARE-R, as a function of .

As our final result we provide the theorem that connects the eigen values of to lower bounds on . This opens up a way to generate the feasible set for choosing matrix.

Theorem 1

Let be the positive solution of the UARE-R in equation (4), then

| (5) |

where the matrix is defined as,

| (6) |

and the positive constant is defined as,

| (7) |

where is defined as,

| (8) |

We have,

| (9) |

Re-writing UARE-R as:

| (10) |

and using (9),

| (11) |

Using Matrix Inversion lemma we get,

| (12) |

Following Lee (2003) we have,

| (13) | ||||

| (14) |

Using (13) and (14) in (12), we have:

| (15) |

Lemma 1 in Lee (2003) (Amir-Moez 1956) states,

for any symmetric matrices, and .

Using and we have,

| (16) |

Using equation (16) in equation (15) after applying eigen value operator on equation (15), we get,

Using and then rearranging we get,

| (17) |

which is of quadratic form. Hence finally,

where,

| (18) |

We have,

| (19) |

Using equation (19) in equation (15) we get,

| (20) |

Using the lower bound in (12) we get,

| (21) |

6 Choosing to Lower-bound

We discussed how we retrieve DARE:

for solving the steady-state covariance matrix for Kalman filter, applying suitable substitution to the UARE-R. Conventionally, designing is related to upper bounding the performance of a filter with some additional constraints. Topics like differential privacy as in Dwork et al. (2014) and bounded information exchange such as in robotics as in Butler et al. (2015) has lead to the requirement of switching between different matrices to keep the performance within bounds (upper or lower), rather than just upper bounding it. In this work, we utilize Theorem 1 to propose a technique to design the measurement noise covariance matrix or the precision matrix such that the is lower bounded. We will see in the succeeding sections that the feasible set of is represented as a set of linear matrix inequality (LMI).

In deriving the following result, we first construct the feasible set of that satisfies prescribed lower bound on the matrix . A particular choice of matrix results from an optimization problem over the set of feasible for a given cost function. We use to represent a generic cost function.

Remarks 2: If is a diagonal matrix, the cost function is essentially over the space of vector , that constitutes the diagonal elements of .

6.1 Calculate : Lower bound for steady state Kalman filtering

Using , replacing by and by in UARE-R, we recover the Discrete Algebraic Riccati Equation (DARE) associated with steady state covariance update equation of a linear system using Kalman Filter.

We assume complete detectability of [] and stabilizability of [] (Anderson and Moore (1979), pg.82) for (1) and (2). This ensure that the steady state prior covariance matrix exists and is unique (for a fixed ) for the corresponding DARE.

Theorem 2

For a given scalar cost function c() and an lower bound on the spectrum of , the solution , whose spectrum is

where , that satisfies a given lower bound on the steady state prior covariance matrix of Kalman filter, is given by the following optimization problem.

Such that,

where,

We first take a look at Theorem 1, the lower bound theorem. The variable is defined as,

We notice that is a function of . We assume that , i.e. upper bounded. We define:

It can be proved that . Hence we have,

| (22) |

Using Theorem 1 we have,

Now suppose we want to lower bound by . That is ensured if we have,

If we assume that the matrix is invertible we have,

Since , is invertible, we have,

| (23) |

For and given lower bound on , which is , we can calculate the feasible solutions to the diagonal matrix. Using , replacing by and by we get:

Where

6.2 Choosing feasible lower bound of for Kalman filter

The desired covariance bounds on should be chosen carefully. When system matrices and noise parameter is already chosen or are known, there exists an upper bound and lower bound on the for any choice of the matrix under certain conditions. Choosing any positive definite matrices, as the desired , outside this bounds, will result in an infeasible solution for the matrix. Hence it is important to choose the desired performance bound accordingly. The prescribed should lie between and satisfying the following:

The matrices is calculated using in the DARE. When , the DARE is solved using generalized Shur method as in Sima and Benner (2015) on an extended matrix pencil. The covariance satisfies the following:

The matrix is calculated by using in the DARE. An unique exists if is stable.

In the succeeding section we apply our sensor selection algorithm for a prescribed lower-bound on the steady state error covariance matrix.

7 Numerical Expriment

The system considered here is a dimensional discrete time linear Gaussian system. The matrices are chosen to be identity. The matrix is . The and matrices are chosen such that [] pair is detectable and [] pair is stabilizable. We choose to be a diagonal matrix. Hence, the spectrum of , i.e. are its diagonal elements. We choose Theorem 2 and show results for minimizing norm on (), for a prescribed lower bound on , where and . The matrix in this example is chosen to be . The matrices and are first calculated. The eigen values of

while the eigenvalues of all are equal to 1.

We then select the prescribed lower bound to be . This convex combination ensures a smooth transition from to when goes from to . We calculate and . We select the upper bound to be 0.03.

The eigen values of :

We solve the optimization problems using CVX in Matlab. The minimum norm cost is 18336.433 . On a 2GHz Intel Core i5 machine, the problem takes 1.20 seconds.

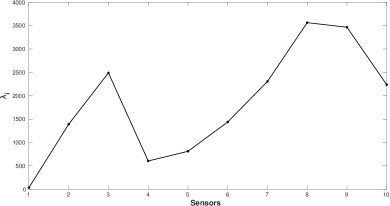

The vector of sensors for norm shown in fig(1) are:

The noise covariance that we calculated is the minimum noise that needs to be in the measurements to ensure that the steady state error covariance matrix is greater than the prescribed lower bound . This is verified by calculating the eigen values of the matrix, which turns out to be all positive. Matrix is the DARE solution for the optimal . We notice that there is a large gap between the lower bound and the final steady state value of . This is due to the fact that we used eigen value approximations in deriving the result. An ad-hoc method to reduce this gap is to iteratively reduce the magnitude of the till the eigenvalues of remain all positive. We found out that we can reduce the by a factor of and still ensure .

The calculated can be assumed to be comprised of actual measurement noise due to the system and synthetic noise . Since in most practical cases is known, our algorithm effectively calculates the minimum synthetic noise that needs to be added to the actual measurement to ensure privacy with respect to state estimation.

8 Conclusion

In this paper we formulate an algorithm to calculate the measurement noise covariance which ensures that the steady state error covariance of the state estimates are lower-bounded by a prescribed bound. We introduce a modified Unified Algebraic Riccati Equation (R-UARE) and exploit eigen value analysis to construct a feasible set of measurement noise covariance. This feasible set is convex and is represented as an LMI. We choose a convex cost function over this convex feasible set of measurement noise covariance, and calculate an optimal noise covariance for system design, which is studied numerically in an example.

References

- Anderson and Moore (1979) Anderson, B.D. and Moore, J.B. (1979). Optimal filtering. Englewood Cliffs, 21, 22–95.

- Bryson (2018) Bryson, A.E. (2018). Applied optimal control: optimization, estimation and control. Routledge.

- Butler et al. (2015) Butler, D.J., Huang, J., Roesner, F., and Cakmak, M. (2015). The privacy-utility tradeoff for remotely teleoperated robots. In Proceedings of the Tenth Annual ACM/IEEE International Conference on Human-Robot Interaction, 27–34. ACM.

- Dwork et al. (2014) Dwork, C., Roth, A., et al. (2014). The algorithmic foundations of differential privacy. Foundations and Trends® in Theoretical Computer Science, 9(3–4), 211–407.

- Ghahremani and Kamwa (2011) Ghahremani, E. and Kamwa, I. (2011). Dynamic state estimation in power system by applying the extended kalman filter with unknown inputs to phasor measurements. IEEE Transactions on Power Systems, 26(4), 2556–2566.

- Kirubarajan and Bar-Shalom (2003) Kirubarajan, T. and Bar-Shalom, Y. (2003). Kalman filter versus imm estimator: when do we need the latter? IEEE Transactions on Aerospace and Electronic Systems, 39(4), 1452–1457. 10.1109/TAES.2003.1261143.

- Lee (2003) Lee, C.H. (2003). Matrix bounds of the solutions of the continuous and discrete riccati equations–a unified approach. International Journal of Control, 76(6), 635–642.

- Middleton and Goodwin (1990) Middleton, R.H. and Goodwin, G.C. (1990). Digital Control and Estimation: A Unified Approach (Prentice Hall Information and System Sciences Series). Prentice Hall Englewood Cliffs, NJ.

- Sima and Benner (2015) Sima, V. and Benner, P. (2015). Solving linear matrix equations with slicot. European Control Conference, ECC 2003.

- Singh et al. (2017) Singh, P., Chen, M., Carlone, L., Karaman, S., Frazzoli, E., and Hsu, D. (2017). Supermodular mean squared error minimization for sensor scheduling in optimal kalman filtering. In 2017 American Control Conference (ACC), 5787–5794. IEEE.

- Song et al. (2018) Song, Y., Wang, C.X., and Tay, W.P. (2018). Privacy-aware kalman filtering. In 2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE. 10.1109/icassp.2018.8462600.

- Tzoumas et al. (2016) Tzoumas, V., Jadbabaie, A., and Pappas, G.J. (2016). Near-optimal sensor scheduling for batch state estimation: Complexity, algorithms, and limits. In 2016 IEEE 55th Conference on Decision and Control (CDC), 2695–2702. IEEE.

- Work et al. (2008) Work, D.B., Tossavainen, O.P., Blandin, S., Bayen, A.M., Iwuchukwu, T., and Tracton, K. (2008). An ensemble kalman filtering approach to highway traffic estimation using gps enabled mobile devices. In 2008 47th IEEE Conference on Decision and Control, 5062–5068. IEEE.

- Yi et al. (2013) Yi, T.H., Li, H.N., and Gu, M. (2013). Wavelet based multi-step filtering method for bridge health monitoring using gps and accelerometer. Smart Structures and Systems, 11(4), 331–348.

- Zhang et al. (2017) Zhang, H., Ayoub, R., and Sundaram, S. (2017). Sensor selection for kalman filtering of linear dynamical systems: Complexity, limitations and greedy algorithms. Automatica, 78, 202–210.