Informed trading, limit order book and implementation shortfall: equilibrium and asymptotics

Abstract.

We propose a static equilibrium model for limit order book where profit-maximizing investors receive an information signal regarding the liquidation value of the asset and execute via a competitive dealer with random initial inventory. While the dealer’s initial position plays a role similar to noise traders in Kyle [16], he trades against a competitive limit order book populated by liquidity suppliers as in Glosten [12]. We show that an equilibrium exists for bounded signal distributions, obtain closed form solutions for Bernoulli-type signals and propose a straightforward iterative algorithm to compute the equilibrium order book for the general case. We obtain the exact analytic asymptotics for the market impact of large trades and show that the functional form depends on the tail distribution of the private signal of the insiders. In particular, the impact follows a power law if the signal has fat tails while the law is logarithmic in case of lighter tails. Moreover, the tail distribution of the trade volume in equilibrium obeys a power law in our model. We find that the liquidity suppliers charge a minimum bid-ask spread that is independent of the amount of ‘noise’ trading but increasing in the degree of informational advantage of insiders in equilibrium. The model also predicts that the order book flattens as the amount of noise trading increases converging to a model with proportional transactions costs. In case of a monopolistic insider we show that the last slice traded against the limit order book is priced at the liquidation value of the asset. However, competition among the insiders leads to aggressive trading causing the aggregate profit to vanish in the limiting case . The numerical results also show that the spread increases with the number of insiders keeping the other parameters fixed. Finally, an equilibrium may not exist if the liquidation value is unbounded. We conjecture that existence of equilibrium requires a sufficient amount of competition among insiders if the signal distribution exhibit fat tails.

1. Introduction

Kyle [16] studies in a simple but remarkably powerful framework a single risk neutral informed trader and a number of non-strategic uninformed liquidity traders submitting orders to a market maker, who aggregates all the orders and clear the market at a single price. Consequently, Kyle’s batch trading model does not produce a bid-ask spread. However, his model allows for an explicit characterisation of equilibrium parameters - including the optimal strategy of the informed trader as well as the equilibrium pricing rule. This in turn allows us to analyse how the private information is disseminated to the market and gets incorporated into the prices over time. In particular, Kyle’s lambda yields an explicit measurement of market’s liquidity and price impact of trades.

While the role of the market makers and the price setting mechanism of Kyle’s batch trading model were in line with the practices of specialists and floor traders of the main exchanges in the the 80s, the role of the designated market makers has diminished in recent years. Nowadays most of the equity and derivative exchanges have moved to the electronic limit order book format. What distinguishes limit order markets from markets with a uniform market-clearing price as in Kyle [16] is that each limit order is executed at its respective limit price leading to discriminatory pricing.

The case of liquidity suppliers moving first and submitting limit orders to be later hit by potentially informed market order was first studied by Rock [23] and Glosten [12]. In equilibrium even infinitesimal trades have significant impact, which results in a positive bid-ask spread unlike the uniform price auction models. Following the approach initiated by Rock and Glosten, Seppi [24] studies the liquidity provision by a specialist competing against a competitive limit order book. His model also allows a discussion on market design issues such as the effect of ‘tick size.’ Based on the model assumptions of [24] Parlour and Seppi [18] build a model of competition between exchanges. In another static model Foucault and Menkveld [10] consider an equilibrium among limit order traders and a broker than can be one of two types and use this model to study the effects of market fragmentation in the context of rivalry between Euronext and the London Stock Exchange in the Dutch stock market.

While useful for policy purposes, the above static models have also some undesirable features. Probably the most unrealistic feature of these models is that, quoting Parlour and Seppi [19], “investors either have an inelastic motive to trade, and are willing to pay for immediate execution via market orders, or they are entirely disinterested liquidity providers with no reason to trade other than to be compensated for supplying liquidity via limit orders.” In particular, unlike the Kyle’s model, their focus is more concentrated on the supply side of the liquidity and the investors’ trading strategies are not completely endogenous. As a result, the shape of the limit order book, which in general can only be obtained numerically, that arises in these models does not truly capture the impact of trades by a rational investor with price elastic motives.

In this paper we present a static microstructure model for the limit order book, where the adverse selection occurs due to the existence of informed traders (henceforth called insiders). Following Kyle [16], the insiders know the liquidation value of the asset in advance and place a market order to maximise their expected profit. They submit their order to a competitive dealer who already has a position that is independent from the liquidation value. The dealer trades the aggregate amount against a competitive limit order book populated by liquidity suppliers that arrived to the market before the dealer and the insiders.

Our assumption that the limit order book is competitive requires a justification in view of the results of Biais et al. [5] and Back and Baruch [3]. First of all, the competitive offer curve should be viewed as a limiting book when the number of limit order traders increases to infinity. However, as shown in an example in [3] the competitive book is not always obtained as a limit of Nash equilibiria among finitely many liquidity providers if the level of adverse selection faced by the limit order traders is not high enough. In our model there is always sufficient adverse selection since we assume that the dealer’s own demand for the asset is normally distributed.

Even though we model the interactions in a single period model, our framework also has the flavour of a continuous-time Kyle model considered by Back [2]. Indeed, in case of a monopolistic insider, we show that conditional on the last infinitesimal slice of the aggregate order traded by the dealer against the order book is priced at on average, reminiscing the convergence of the equilibrium price to the liquidation value by the end of the trading horizon in the continuous-time Kyle model. Thus, all private information gets incorporated into the order book once the last slice has traded. This is in contrast with the corresponding Kyle model in one period111In the corresponding one-period Kyle model, where is normally distributed with mean , the average price for the aggregate order conditional on equals ., which is not surprising given the uniform pricing in the Kyle model.

The above ‘convergence’ result motivates the analysis of the case of multiple insiders. In the same vein as Holden and Subrahmanyam [14] we also model and solve the imperfect competition among insiders who observe the liquidation value perfectly. As in [14] this competition leads to more aggressive trading. We find that (conditional on ) the average price for the last slice traded by the dealer exceeds if the insiders are buying in equilibrium, which can be attributed to more aggressive buying due to the competition. An analogous observation holds when the optimal strategy in equilibrium is to sell. We obtain an explicit formula for the aggregate profit of the insiders that shows that the aggregate profit converges to as .

We characterise the equilibrium strategy of insiders and the corresponding equilibrium order book as a solution of an integral equation, which is equivalently given by the fixed point of an integral operator. Although this equation admits an analytic solution only in very restrictive settings, its numerical implementation is straightforward. We establish the existence of equilibrium when the fundamental value is bounded and obtain numerical solutions for a number of unbounded distributions commonly found in the literature and used in practice.

Despite the fact that the exact form of the order book can only be solved numerically, we are nevertheless able to obtain the exact analytic asymptotics when the order size is large. Moreover, due to the scaling property of the normal distribution, these asymptotics still provide a good approximation for small orders if the variance of the dealer’s demand is sufficiently small. The error in such an approximation appears to be still low even in the case of higher variance as confirmed visually by our numerical studies.

Due to the discriminatory pricing in the order book, our model produces a non-zero bid-ask spread in equilibrium. We find that the bid-ask spread imposed by the limit order traders is the same regardless of the variance of the initial inventory of the dealer. The shape of the order book, however, is not invariant to the changes in this variance; on the contrary, the order book flattens as it increases. That is, the limit order traders do not need to extract significantly higher rents for larger trades if the information content of the order is very small. In the limit the equilibrium converges to one where the transaction cost is proportional to the trade size. Moreover, similar to the model considered by Foucault [9], our model also predicts that a larger price volatility leads to a bigger bid-ask spread - a phenomenon that is empirically documented by Ranaldo [22]. Indeed, we show that the spread gets wider as the variance of the private signal of the insiders increases, which corresponds to the case of a higher informational advantage.

That we can compute the price impact of large trades has profound implications for practitioners. Portfolio managers endeavour to find mispriced assets in order to beat their benchmarks. When they decide to change their holdings to take advantage of a mispricing, they create orders in an order management system; the trading desk routes these orders to broker-dealers for execution. When they do so, on average, the price to buy is greater than at the time of the decision, and vice-versa, the selling price is lower, because the trade’s effect on supply and demand causes market impact. The implementation shortfall is thereby the value lost by not being able to execute at the decision price [20]. Understanding how this implementation shortfall scales with trade size is essential to optimize the investment management process. A market impact model is needed in order to maximize net trading profits. It is also important to optimize position sizes, limit liquidity risk and estimate a portfolio’s capacity.

Empirical data provides some clues as to the shape and scale of market impact. In particular, it has been known for some time that impact is a concave function of trade size (see Torre [26]). But biases in the data, a low signal-to-noise ratio and other issues prevent practitioners from determining the functional form of market impact precisely, particularly for large trades where data is sparse. Models used by practitioners include square root and logarithm (e.g. Torre [26], Potters and Bouchaud [21], Almgren et al. [1], Bershova and Rakhlin [4], and Zarinelli et al. [29]). When calibrated to data, these models yield similar results for small to moderate trade sizes, but they yield very different predictions for the impact of for very large trades. This is unfortunate given that the largest trades typically dominate the aggregate implementation shortfall for most portfolios. The absence of a consensus on the shape of market impact for very large trades motivates the search for a theoretical framework that would capture the essential features of trading and yet be sufficiently parsimonious to be testable.

We show that the market impact follows a power law or a logarithmic law depending on the distribution of the liquidation value. The price impact, and equivalently the implementation shortfall, has a power law if the liquidation value has fat tails while lighter tails lead to a logarithmic behaviour.

Our framework also allows us to compute the tails of the probability distribution associated with aggregate volume. For a large class of distributions that can be used to model the liquidation value we show that the tail probability distribution for the trade volume obeys a power law. The power-law behavior of order sizes has been documented previously in various contexts: Gopikrishnan et al. [13] showed that the market volume in a time interval has a power-law tail with exponent 1.7; Lillo et al. consider off-book trades [17] and find an exponent ranging from 1.59 to 1.74. Vaglica et al. reconstructed metaorders in Spanish stock exchange using data with brokerage codes and found that the metaorder transaction size is distributed has a power law tail with exponent 1.7 [28]. And in a study performed directly on institutional trade data from Alliance Bernstein, Bershova and Rakhlin found a tail exponent 1.56 for metaorder sizes [4].

Our proof of the existence of equilibrium assumes that the liquidation value of the asset is bounded. However, our numerical experiments suggests that equilibrium exists for a large class of unbounded signals. Moreover, the asymptotics of these solutions agree with the analytical forms that our theory predicts. However, unlike the bounded case, an equilibrium may not exist for all unbounded distributions. Given the premise of numerical results and our formal calculations we conjecture that existence of equilibrium requires a sufficient amount of competition among insiders if the signal distribution exhibit fat tails. For instance, when the private signal is given by a Student’s t-distribution our numerical iterations diverge in case of a monopolistic insider.

We also consider an alternative model where instead of sending the order to a dealer with an existing inventory, the informed investors send the order to an institutional trading desk that also receives orders from noise traders. The aggregate is liquidated against a limit order book; however, in the case of the institutional trading desk the insiders and noise traders all receive allocations at the same average price. While we were not able to find an existence proof for this model, numerical solutions are similar to those of the dealer inventory model.

Structure of the paper is as follows: We present the dealer inventory model in the next section. In Section 3, we show the existence of an equilibrium and characterize some of its properties. Section 4 considers the asymptotic behaviour of market impact. Numerical solutions are provided in Section 5 for the dealer inventory model. Section 6 explores the trading desk model numerically and compares results with the dealer inventory model.

2. The market structure and equilibrium

Our model is built upon Glosten [12] and the trading takes place in one-period: There are three class of investors that are all risk-neutral: 1) competitive liquidity suppliers who post limit orders, 2) a competitive dealer who clears the market, and 3) insider(s), who know(s) the liquidation value of the asset. All random variables in this section are assumed to be define on a complete probability space and is the expectation operator associated to .

Liquidity suppliers move first and place limit orders that give rise to an order book. That is, if the limit order book is defined by some function , the market order moving up (or down) the book faces a cost of as soon as hitting the limit order at level . The dealer already has number of shares of the asset, which is assumed to be independent of . The dealer’s initial inventory in the asset is unknown by other market participants. The insider chooses a trade size to maximise her expected profit conditional on her private information.

Let us first consider the case . We assume that the cost of a market order of units by the insider is

| (2.1) |

The above cost can be justified as a result of Bertrand competition among dealers whose initial mean-zero inventories are normally distributed with identical variance . Indeed, first observe that when the insider trades units via the dealer, the dealer’s inventory changes from to . If the cost to the insider is given by (2.1), the total profit of the dealer after trading via the liquidity suppliers is given by

which is the cost of liquidating his initial inventory directly via the limit order book. Therefore, no dealer will be willing to charge less than (2.1). The insider knows the distribution of but do not know the inventories of individual dealers. Dealers first announce that they will price according to 2.1 plus a premium (the dealer’s profit). Insider then chooses a dealer based on this information, before knowing . Bertrand competition will then drive the dealer’s premium to zero. That is, an individual dealer knows that if he charges higher than what is proposed by (2.1), he will be undercut by another dealer. Thus, a Bertrand competition will lead to (2.1) for the cost of the trades of the insider.

Remark 1.

Note that the quote given by the competitive dealer that leads to (2.1) does not violate the limit order protection rule that is mandated by the SEC in the US. To see this suppose the insider wants to buy many units. She is charged on average for this transaction. If is bigger than the best ask, i.e. , the price priority implies that the limit sell orders at price and less must be filled first. Thus, the dealer will first buy many shares at a cost of and the remaining shares in his inventory at . This makes his cumulative cost and final profit coinciding with above calculations.

Thus, in view of (2.1) the expected profit of the insider from a market order of size is given by

where is the expectation operator for the insider with the private information . Since is assumed nondecreasing, the first order condition characterises the unique achieving the maximum expected profit via , where

| (2.2) |

and is the probability density function of a mean-zero Gaussian random variable with variance . Note that since is non-decreasing and not constant, is strictly increasing and one-to-one. Thus, .

We shall also consider the case of multiple insiders trading via the same competitive dealer and knowing the value of . Assuming that the dealer charges each insider an amount proportional to their order size, the expected profit of an individual insider placing an order of size is given by

where denotes the aggregate demand of the other insiders. The number of insiders will be denoted by .

The first order condition associated with the above optimisation problem of an individual insider is again given by

As every insider has symmetric information and is risk-neutral, the equilibrium demand for each insider must be the same and satisfy

Denoting the total informed demand by , the above can be rewritten as , where

| (2.3) |

and is interpreted by continuity to be

Moreover, it follows from the monotonicity of that defined via (2.3) is strictly increasing. Also note that (2.3) reduces to (2.2) when . Thus, we shall always refer to (2.3) when discussing the optimal strategies of the insiders regardless of the value of .

In what follows the total informed demand will be denoted by and we assume following Glosten [12] that limit prices are given by ‘tail expectations.’ That is, denoting the total demand by ,

| (2.4) |

The value is not relevant for the subsequent computations and can be freely chosen to be any value between the best ask and the best bid .

The definition (2.4) entails that liquidity suppliers earn zero aggregate profit on average. Indeed, the expected profit is given by

where the last equality is due to the definition of the conditional expectation.

Definition 2.1.

The strict monotonicity of leads to the following result that in particular yields an explicit formula for the aggregate profit of the insiders.

Proposition 2.1.

Let be an equilibrium and defined by (2.3). Then, the following hold:

-

(1)

For any we have

(2.5) -

(2)

when and, for , (resp. ) if (resp. ). More precisely,

(2.6) -

(3)

The aggregate expected liquidation profit of the insiders conditional on is given by

(2.7)

The expression (2.6) reveals an interesting feature of our model akin to Kyle’s model in continuous time. Observe that can be viewed as the last slice that is traded with the limit order traders. Thus, when there is a monopolistic insider, (2.6) shows that the final slice is priced at the actual value of similar to the convergence of the equilibrium price to the liquidation value of the asset in the continuous time version of the Kyle model studied in Back [2] for general payoffs. As expected, this ‘convergence’ disappears when the liquidation value of the asses is observed by more than one insider. Such a competition leads to a more aggressive trading as in Holden and Subrahmanyam [14] and results in higher (resp. lower) market valuation if the optimal strategy is to buy (resp. sell).

In practice an important trading benchmark for traders is the implementation shortfall. Perold [20] defines it as the difference between a ‘paper trading’ benchmark and the actual trading costs. Assuming that the benchmark is given by the ex-ante valuation , the associated shortfall in our context can be defined as follows:

Definition 2.2.

Let be a function that defines the limit order book in a Glosten equilibrium. Then, the implementation shortfall associated with trading units is given by

Observe that is simply the expected average cost of trading units. As the following result shows, it is smaller than the marginal cost , which is given by the first order condition (2.3).

Proposition 2.2.

Let be a function that defines the limit order book in a Glosten equilibrium and be given by the first order condition (2.3). Then,

In particular, for and for .

3. Characterisation of Glosten equilibrium

Suppose that is an equilibrium. Writing instead of to ease the exposition and using the definition of when , we get

Similarly, for .

Next introduce the right-continuous functions and via

Note that for all . Moreover, and .

Now let us compute for :

On the other hand, at most for countably many . Thus, for almost all and we have for all

| (3.8) |

Similarly, for

| (3.9) |

In order to obtain an equation for it will be convenient to define, for any continuous , the mappings

Let us also set

| (3.10) |

Now, combining (2.3), (3.8) and (3.9) yields an equation for :

| (3.11) |

If one can change the order of integration in above222We shall see later that this is justified when is bounded from below, then (3.11) can be rewritten as

| (3.12) |

with

| (3.13) |

The preceding calculations show that the existence of a solution for the above integral equation is a necessary condition for equilibrium. We in fact have the converse, too.

Theorem 3.1.

In view of the above theorem finding an equilibrium boils down to finding a solution of (3.11). Moreover, equilibrium will be uniquely defined if there exists a unique solution of (3.11). As usual, solutions of (3.11) will be identified as fixed-points of a mapping. Before analysing in depth this fixed-point problem, we shal observe few properties of equilibrium. The following scaling property of is inherited from the analogous property of the Gaussian distribution.

Proof.

Similar manipulations yield

which establishes the claim. ∎

A straightforward corollary to the above is the following.

Corollary 3.1.

Consider the solutions of (3.11) for any .

In particular, inherits the same scaling property of . A simple but striking consequence of this property concerns the equilibrium bid-ask spread.

Definition 3.1.

Let be a function with right and left limits defining an order book. The bid-ask spread of the associated order book is given by .

Corollary 3.2.

Suppose that uniqueness holds for the solutions of (3.11). Then, does not depend on . Moreover, for fixed , is decreasing in for and increasing in for .

Thus, the liquidity suppliers charge a bid-ask spread that does not vanish even if the amount of ‘noise’ trading is excessively large. Moreover, the dependency of the limit price on is not monotone. In particular, approaches to the supremum (resp. infimum) of the set of possible values of for (resp. ) when . We shall see these phenomena occurring explicitly in Examples 3.1 and 3.2. Furthermore, if we consider the limiting behaviour in the other direction as , we observe that the order book gets flatten and converges to the one that yields transaction costs that are proportional to the order size.

A similar scaling property will hold when the signal distribution possesses a form of self-similarity, which can be proved by similar methods.

Corollary 3.3.

A typical example of a self-similar random variable is mean-zero Normal random variable. In this case , where is the parameter corresponding to standard deviation. Similarly, , when corresponds to an exponential random variable with mean (hence, standard deviation) . The above corollary therefore shows that the bid ask spread gets bigger as the variance of the information signal gets higher, indicating that the liquidity suppliers charge a bigger bid-ask spread when the informational asymmetry gets bigger.

Another consequence of the uniqueness of solutions of (3.11) is that the aggregate expected profit of the insiders vanishes as .

Proposition 3.2.

Definition 3.2.

is said to be symmetric if and have the same distribution. That is, for all .

Proposition 3.3.

Proof.

Observe that . Thus, utilising the fact that and differ from their left limits at most at countably many points and is symmetric around zero, we obtain

where . Moreover,

Thus, is also a solution of (3.11), which establishes the first assertion. The second assertion follows from a change of variable in (3.11) as above and using the assumed symmetry of . ∎

Example 3.1.

Suppose that . Then, the unique symmetric solution of (3.11) is defined by

In this case it is easily seen that in equilibrium (resp. ) if (resp. ). Moreover, .

Although the insiders’ optimal market order is to buy or sell an infinite amount, their profit remains finite. Indeed, when , the aggregate expected profit is given by

where and the second line is due to the fact that . Note that the total profit is independent of .

Example 3.2.

Consider the case . Then, similar considerations as above should yield and . Moreover, symmetry considerations must lead to , which suggests that the insider does not trade when . Indeed, the unique solution of (3.11) is given by

Differently from Example 3.1, the order book will not be flat since the insider does not trade when . One can obtain via (3.9) and (3.8). Alternatively, for

where the first equality follows from the fact that is infinite when or , and the third follows from the independence of and . Similarly, for ,

In particular, the bid-ask spread is given by , independent of the noise volume and of .

3.1. Existence of Glosten equilibrium

We shall denote the interior of the support of the random variable by , where , and define on the support of

| (3.16) |

so that and .

We impose the following condition on the function to ensure that the integral equation (3.11) is well-defined and changing the order of integration in (3.12) is justified.

Assumption 3.1.

Observe that the above is automatically satisfied if is bounded from below in view of (A.38). Moreover, if is a continuous function satisfying (3.11) and is symmetric, it satisfies the above assumption in view of Proposition 3.3 and the finiteness of .

One of the useful consequences of the above assumption is the strict monotonicity of solutions of (3.11).

Lemma 3.1.

Theorem 3.2.

Suppose . Then, there exists a Glosten equilibrium.

Under the hypotheses of Theorem 3.2 it is clear that for . However, in view of the bounds given by (A.37) and (A.38) it is possible to obtain sharper bounds on any solution of (3.11).

Theorem 3.3.

Suppose and let be as in (3.16). Then the following statements are valid.

-

(1)

There exists a maximal nondecreasing solution333 is a maximal nondecreasing solution if for all , where is any other nondecreasing solution. to

(3.17) Moreover, this maximal solution is not constant and any solution of (3.11) is bounded from above by this maximal solution.

-

(2)

There exists a minimal nondecreasing solution444 is a minimal nondecreasing solution if for all , where is any other nondecreasing solution. to

Moreover, this minimal solution is not constant and any solution of (3.11) is bounded from below by this minimal solution.

We shall see in the next section that behaves like (resp. ) as (resp. ).

4. Market impact asymptotics

In this section we are interested in the market impact associated with large orders. More precisely, we will be computing the asymptotics of the marginal cost of trades, which is given by the function . As we shall see later, the asymptotic form of will coincide (up to a scaling factor) with that of implementation shortfall . We will also be able to compute the tail asymptotics of the distribution of the total demand in equilibrium.

Definition 4.1.

A function is said to be regularly varying of index at if

Analogously, a function is said to be regularly varying of index at if is regularly varying of index at .

We shall first start with the asymptotics of solutions of (3.17) and (2) which will later allow us to compute the asymptotics of interest.

Theorem 4.1.

Suppose that , , and has a continuous derivative. Then, the following statements are valid:

Remark 2.

Observe that when is finite,

Similarly, if is finite.

The above shows that (resp. ) is slowly varying at (resp. ) if (resp. ). We can obtain a better estimate of how slow its variation is under a further assumption on .

Theorem 4.2.

Assume that , , has a continuous derivative and and are as in Theorem 4.1. Then, the following statements are valid:

Corollary 4.1.

Assume that , , has a continuous derivative and and are as in Theorem 4.1. Then, the following statements are valid:

Remark 3.

Note that if , we have

implying and in Part 1) of Corollary 4.1. An analogous consideration applies to the second part.

The results above now allow us to compute the asymptotics of solutions of (3.11).

Theorem 4.3.

Assume that , , has a continuous derivative and and are as in Theorem 4.1. Let be any solution of (3.11). Then, the following statements are valid:

-

(1)

is regularly varying of index at , where is given by (4.19).

Moreover, if and there exist an integer and a real constant such that

the following asymptotics hold:

(4.23) -

(2)

is regularly varying of index at , where is given by (4.20).

Moreover, if , and there exist an integer and a real constant such that

then

(4.24)

Remark 4.

Upon integrating by parts we arrive at

Now suppose that for some differentiable such that

for some and . A straightforward application of L’Hospital rule shows that

which in turn implies

For instance, if

for some , , and , we deduce that

We also have the exact analogue of Corollary 4.1 that can be proven by exactly the same arguments.

Corollary 4.2.

Assume that , , has a continuous derivative and and are as in Theorem 4.1. Let be any solution of (3.11). Then, the following statements are valid:

-

(1)

Suppose that there exist an integer and a real constant such that

Then, is regularly varying at of index

-

(2)

Suppose that there exist an integer and a real constant such that

Then, is regularly varying at of index

Remark 5.

Although Corollary 4.2 appears rather technical, it uncovers the distribution of the total volume traded in equilibrium. Indeed, for

Thus, under the hypothesis of Corollary 4.2, the tail distribution of equilibrium is regularly varying at infinity. That is,

where is a slowly varying function and

Moreover, since the aggregate order is given by and and are independent, we have for

which can easily be shown to be regularly varying at infinity with the same index. Thus,

| (4.25) |

for some regularly varying . In particular, if has light tails, i.e. , is regularly varying of index .

Analogous computations yield for the sell side

| (4.26) |

where

We have seen in Proposition 2.2 that the implementation shortfall is smaller than . In view of Theorem 4.3 we have a more precise relationship for large .

Corollary 4.3.

Corllary 4.3 shows that for large implementation shortfall and the marginal cost of trading are almost indistinguishable. This is even more pronounced when (resp. ) is slowly varying, i.e. (resp. ). Observe that can be estimated from market data using the open limit order book governed by , while the computation of depends also on the estimate of .

Remark 6.

We have focused in this section the asymptotics of and . However, one also naturally wonders the asymptotic shape of the limit order book. Using our framework it is easy to show that and behave similarly for large values. Indeed, recalling the measure defined in (B.50), we formally obtain

using the mean value theorem and the continuity of the derivative of together with the fact that the is regularly varying with index since the measure converges to the point mass at as . In particular, the order book is also regularly varying with the same index .

5. Numerical studies

This section is devoted to description of results obtained in previous version via a naive numerical search for a fixed point: Starting with an , we compute until the distance between successive iterations become negligibly small, where corresponds to the right side of (3.11). Although the proofs of the statements concerning the existence of equilibrium and its asymptotics relied on a boundedness assumption, we shall also presents the solutions of the fixed point problems associated with equilibria with unbounded signals.

Since can be absorbed into the units for measuring equity in view of (3.1), we will set in all numerical tests with no loss of generality in this section.

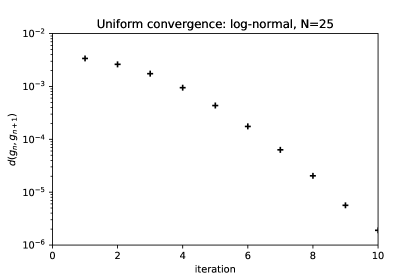

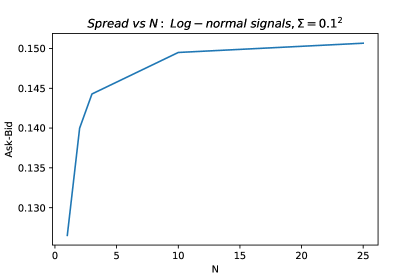

The iteration converges exponentially for all cases considered below. We illustrate the convergence in Figure 1 by showing the uniform distance between successive iterations for log-normal signals with .

In practice, the signals distribution is at least partly known to practitioners since it can be inferred from the options montage and the event calendar. For example, an insider may have advance knowledge of the result of clinical trials of a new treatment from a biopharmaceutical company, or the insider may have been tipped about a number to be released in a scheduled earnings call. The signals distributions in these two examples are quite different. In the case of clinical trial results, the signal is drawn from a bounded distribution since the outcome is bounded by total success and total failure. On the other hand, earnings surprises can be arbitrarily large. Earnings calls can be priced in a naive jump-diffusion model by assuming the surprise is drawn from a log-normal distribution; the jump variance is estimated by comparing the at-the-money implied volatility(ATMIV) for the two nearest options expirations, as proposed by Dubinsky and Johannes [7].

The shape of market impact as a function of trade size is important to practitioners to address capacity and position sizing. Various functional forms have been explored in the literature (see, e.g., [4], [11], [21] and [26]), including and . Rejecting either of these forms empirically is challenging due to three practical difficulties: (1) the spread and market impact terms are collinear for small orders, (2) signal-to-noise ratios are weak for executions that take a small percentage of market volume, and (3) for very large trades, order sizes are often increased if liquidity is available, or reduced if liquidity is hard to find, leading to bias in the data. In absence of clear empirical evidence, theoretical predictions for the shape of market impact provide valuable insight into how trading costs scale with trade size. One testable conclusion from this paper is that market impact should be different ahead of an event with an unusual distribution of signals, if market makers believe that an informed trader may have advance knowledge of the signal.

We consider first the case of bounded signals that was the focus of the previous section.

5.1. Bounded signals

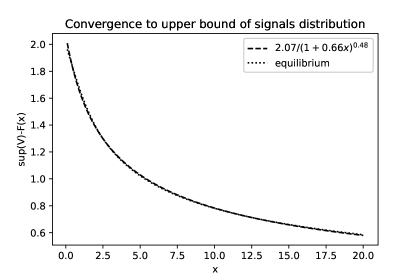

5.1.1. Truncated Gaussian distribution

If signals are drawn from the truncated Gaussian distribution with density for , the numerical solution for equilibrium converges to the upper bound as in accordance with the predictions of Theorem 4.3. We show and the theoretical prediction for its asymptotic behavior in Figure 2.

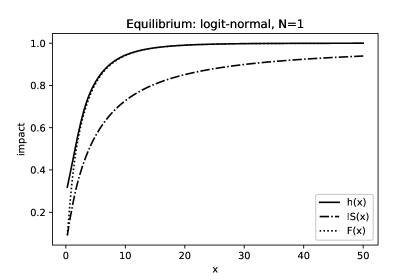

5.1.2. Logit-normal distribution

If price is a probablility-weighted average over two possible outcomes , where the probability is a sigmoidal function of a Gaussian generator potential as , the signals distribution is the logit-normal distribution with density . This distribution has support in .

We show the equlibrium solution for , the order book and the implementation shortfall for logit-normal signals, in Figure 3.

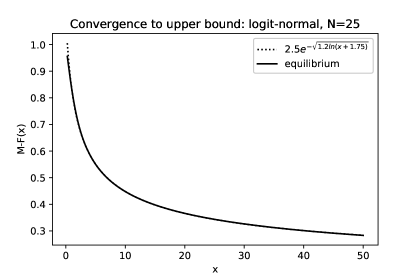

Note that the logit normal distribution does not satisfy the hypothesis of Theorem 4.3. Thus, our theory cannot predict the asymptotics of for this distribution. However, the following formal arguments yield the asymptotics that seem to be verified by the numerical experiments. Observe that for , 2.3 becomes

| (5.29) |

It follows that . Moreover, for large values of , we roughly have . Let us consider the large limit and drop the term. Using the approximation and expanding to first order in we find that asymptotically

whihc yields

The numerical solution shown in Figure 4 for is consistent with this asymptotic form.

5.2. Unbounded signals

In what follows, we place emphasis on unbounded signals; that is, when the support of is unbounded. Although we do not have a theoretical justification for the existence of a solution for (3.11) in the case of unbounded signals, we were able to arrive at numerical solutions via the above numerical search.

The asymptotic behavior of for large signals will depend on the tail behaviour of the distribution of . Assuming the interchange of limits and integrals in the proof of Theorem 4.3, we can show that

where in case of . Solution of the above equation immediately yields that, for , is regularly varying at of order , where

| (5.30) |

Observe that when , in contrast to the bounded case, where . Since must be non-negative, this places the restriction on :

| (5.31) |

Thus, we conjecture that (5.31) is a necessary condition for the existence of equilibrium when . Observe that for a fat tailed unbounded distribution, . Thus, a sufficient competition among insiders is necessary for the equilibrium to exist. Such a condition is always satisfied in the bounded case since for .

As in the bounded case will be slowly varying at infinity when . In this case, if we assume

| (5.32) |

for some and , formal calculations yield

| (5.33) |

Tables 1 and 2 summarise the predicted asymptotics for a class of distributions commonly used in the literature and practice.

| Distribution | Density | |

|---|---|---|

| Beta prime | ||

| Fréchet | ||

| Lomax | ||

| Pareto | ||

| Student |

In above probability densities are given up to a scaling factor and implicit constraints are enforced to ensure they are well defined with finite mean. Moreover, in all of the above.

| Distribution | Density | Asymptotics |

|---|---|---|

| Exponential | ||

| Gaussian | ||

| Inverse Gaussian | ||

| Normal Inverse Gaussian | ||

| Weibull |

In above probability densities are given up to a scaling factor and implicit constraints are enforced to ensure they are well defined with finite mean. Moreover, for the Normal Inverse Gaussian distributiuon.

5.2.1. Gaussian signals

We assume that the mean of equals . The numerical solution is shown in Figure 5 together with the asymptotic behavior.

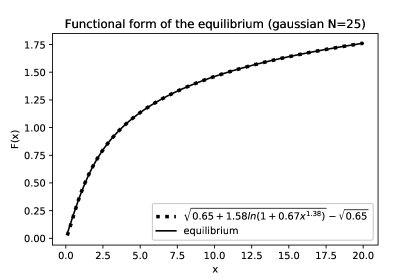

5.2.2. Log-normal signals

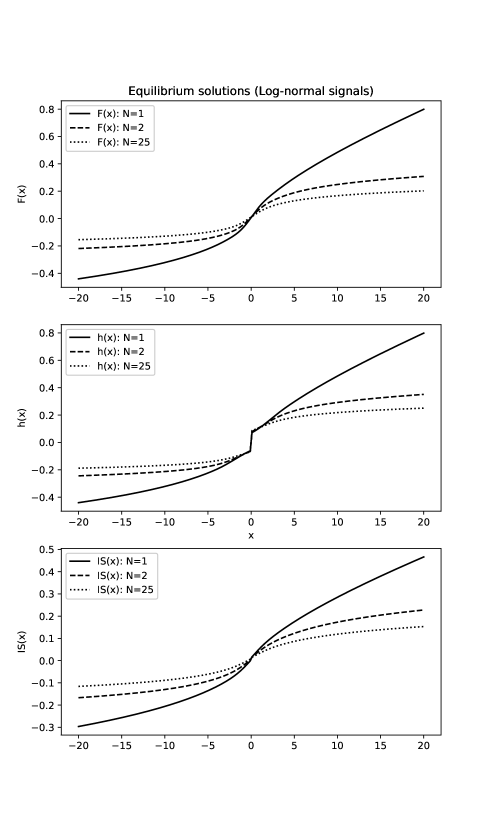

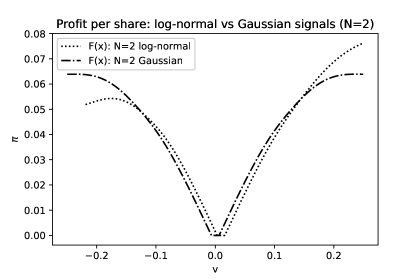

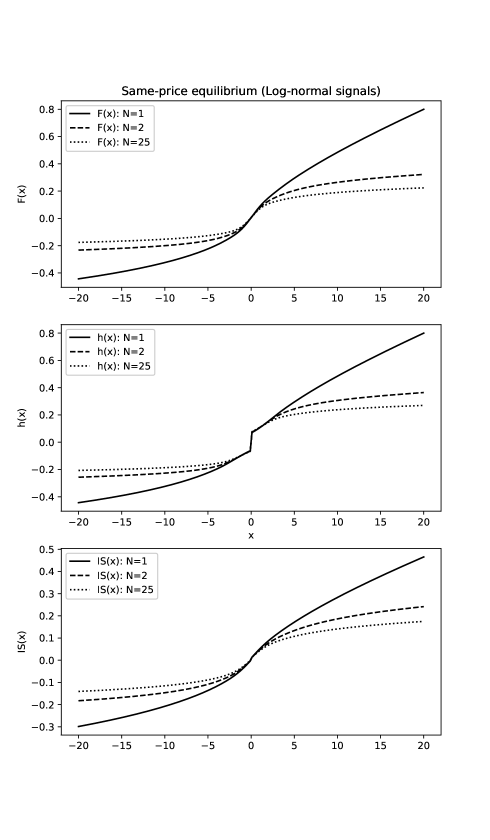

For a log-normal distribution, the mean is an arbitrary scale factor which we set to and, thus, the density is . We choose a large signal variance in our numerical experiments below, illustrative of an earnings announcement for a high-volatility name. Moreover, we translate the distribution by so that the mean is . The equilibrium solutions for and are shown for various values of in Figure 6.

Observe that the equilibrium is not symmetric around its mean: a market maker who is short the stock runs the risk of unbounded losses, whereas for a long position the maximum loss is always bounded since price cannot fall below zero.

The log-normal distribution does not satisfy the conditions of Theorem 4.3. Thus, we do not have a theoretical prediction for the asymptotic market impact. However, we find numerically that the implementation shortfall fits . Asymptotically, both the shortfall and are consistent with . We note that the large-size behavior is more concave than both the square root commonly used by practitioners and also the model that has been suggested in some empirical studies, e.g. [4].

The asymmetry between positive and negative signals is clearly visible in the figure as we chose a rather large signal with a standard deviation of .

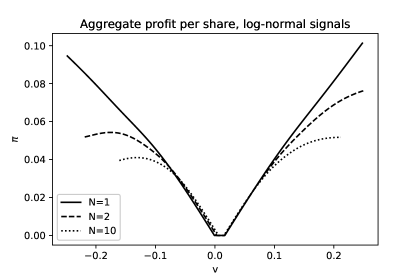

The aggregate profit is a decreasing function of the number of informed investors and we show the profit as a function of trade size below for various values of in Figure 8. Moreover, Figure 9 shows how the spread depends on the number of informed investors.

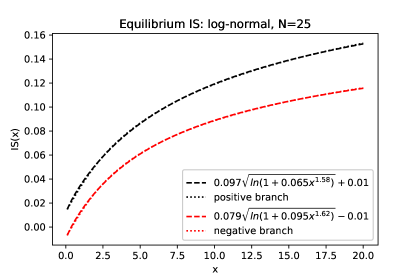

The greater positive tail mass for the log-normal signals implies that large positive signals yield a greater profit than for Gaussian signals with the same , and vice-versa, negative signals yield a smaller profit in the log-normal case (Figure 10).

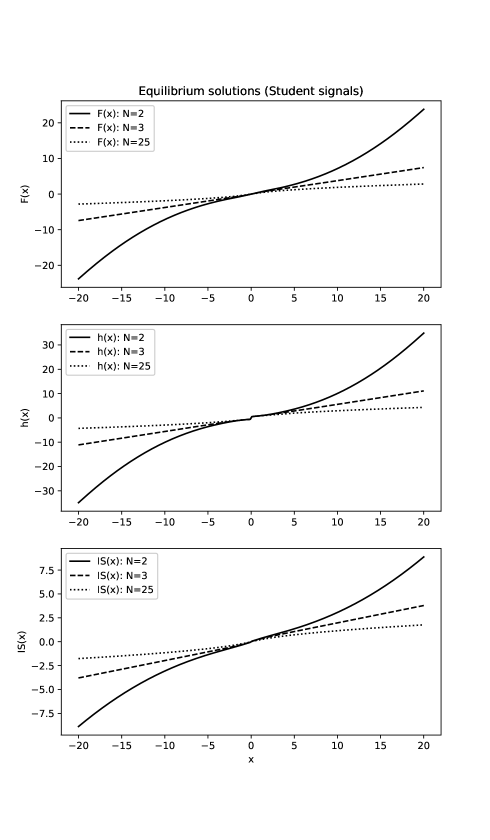

5.2.3. Student signals

We explore the effect of fat tails in the signal distribution next. We consider the case where signals drawn from a Student t-distribution with , . This is reminiscent of some empirical studies such as Plerou [27]. However, we note that we are assuming a Student distribution of arithmetic returns. The power-law tail of geometric returns in Plerou’s study implies an infinite expected price.

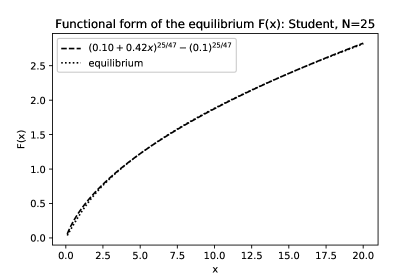

In view of Table 1 the expected asymptotics is . Moreover, our conjecture predicts no equilibrium when . Indeed, no numerical solution for can be found when . The equilibrium asymptotically parabolic for (theoretical ), linear for (theoretical ) and concave for . The numerical solutions are shown in Figure 11. For , the asymptotic exponent is according to our theory. The numerical solution is compared to this prediction in Figure 12.

The case of power-law tailed signal distributions was considered previously by Farmer et al. in the case of perfect competition between insiders [8]. One can view their model as the limiting case of the one considered herein as in case of a Pareto-tailed distribution with exponent .

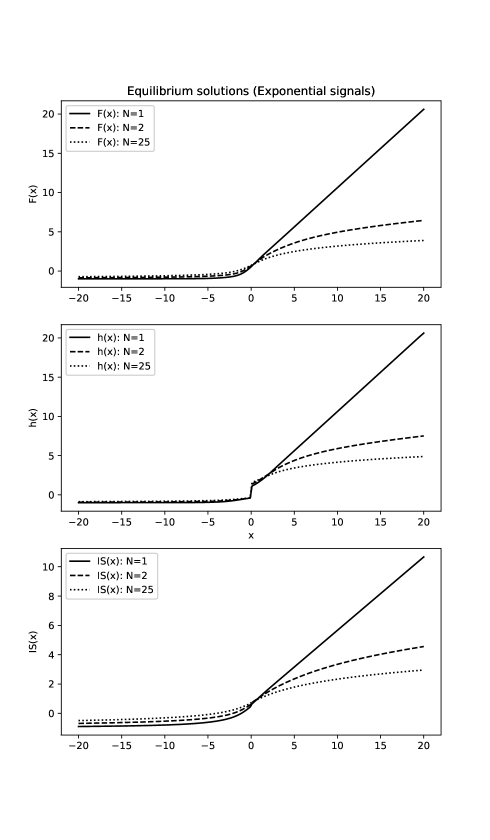

5.2.4. Exponential signals

We are not aware of any situation that gives rise to an exponential distribution for an asset’s price666A possible exception is Kou and Wang [15] who consider an asymmetric double exponential distribution for jumps in the asset price. However, the case is of interest to illustrate the effect of extreme asymmetry. For exponential signals, the probability density function is given by for . We take and translate the distribution by so that the mean equals for the numerical solutions. The numerics indicate that the equilibrium is asymptotically linear for the case of monopolistic insider and concave in case of competitive investors, as shown in Figure 13.

6. Same-price liquidation

Up to now, we assumed that the dealer had an initial position and liquidated his total position after trading with the insider via the limit order book and argued that a Bertrand competition leads to a price to the insider given by (2.1). An alternative framework also of interest to practitioners is one where portfolio managers and noise traders submit their orders to an aggregator (institutional trading desk), which merges the orders into a block (“metaorder”, in the literature), liquidates for some average price, and allocates shares with the same average price to noise traders and insiders. We refer to this framework as same-price liquidation. The expected profit of the insiders in this case is

| (6.34) |

In this case the corresponding first order condition for the maximisation problem is given by , where

where and is given by the tail expectation as above.

The problem with this first order condition is that it is not clear whether it yields a maximum as defined above is not necessarily increasing, i.e. we may not have a concave function to maximise in contrast to the problem studied in previous section.

However, if one assumes that is increasing and obtains the corresponding integral equation, one can still get a fixed point. Moreover, our numerical solutions always suggest an increasing solution yielding a ‘numerical’ proof of the existence of equilibrium.

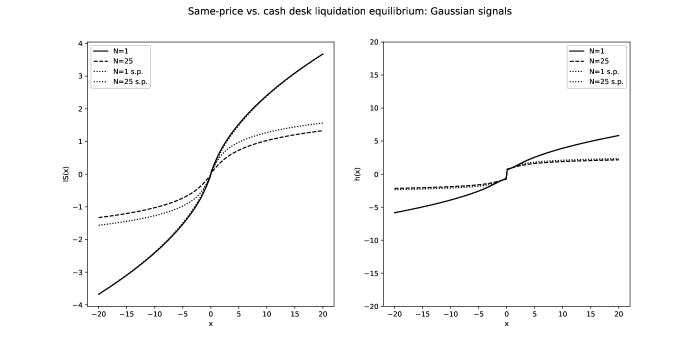

The solutions are similar in form and share the same asymptotic behaviour for both bounded and unbounded signal distributions. We show as an example the case of log-normal signals in Figure 14.

Figure 15 compares the same-price liquidation model to the dealer inventory model in the case of Gaussian signals. The dotted lines represent the same-price liquidation equilibria. Market impact is somewhat greater with same-price liquidation than for the dealer inventory model, for . For the insider case, the two are essentially identical.

7. Conclusion

In this article, we explored how private information is transferred into the market price through a limit order book. Since empirical data on very large trades is sparse and often biased, it is important to develop a theoretical understanding of the process in order to discriminate between various proposals for the shape of the impact function.

We proposed an asymmetric information based equilibrium model where informed investors draw a signal and send their orders to a dealer with an initial position who executes at the net cost to liquidate the aggregate amount against a limit order book. Unlike the earlier static equilibrium models developed for limit order markets, the informed traders’ positions are determined endogenously in equilibrium. We showed that solutions exist in the case of bounded signals and discussed properties of the equilibrium including the asymptotic behavior of the implementation shortfall for large trades.

Our results provide the micro-foundations for a large number of empirical findings including those on price impact and volume. We found that market impact is asymptotically a power of trade size if the signal has fat tails, whereas the impact becomes of the form for some for lighter tails.

Our numerical experiments show that our results remain valid for unbounded signals with analogous impact asymptotics. Moreover, for fat-tailed signal distributions, an equilibrium only exists if there is a sufficient amount of competition. In the particular case of Student distribution, if the tail exponent is , there is no equilibrium in the case of a monopolistic insider, and the shape of market impact tends to a square root in the limit where the number of informed investors is large, . Although we do not have an analytic proof, the bid-ask spread seems to be an increasing and bounded function of the number of informed investors.

A relevant and arguably more realistic extension of our framework while still remaining in a static setting is to consider the scenario in which the insiders receive different but possibly correlated signals regarding the liquidation value. On the other hand, due to our assumption that the insiders’ orders arrive simultaneously to the dealer, the optimisation problem of each insider requires the solution of a nonlinear filtering problem even in the case of Gaussian signals. Our present technology is not yet able to deal with such complications and, therefore, we postpone the discussion of this extension to subsequent research.

In reality limit order markets are dynamic and thus the order books change over time reflecting the changes in market parameters. The analytic characterisation of the equilibrium in the current framework in terms of the fixed point of an integral operator makes us optimistic regarding an extension of the current framework to a dynamic setting in continuous time. However, continuous trading brings extra flexibilities to portfolio choice - including the option to place a market or limit order at each trade - resulting in a more complicated model. This extension, though extremely interesting, will thus be left for future research.

References

- [1] R. Almgren, C. Thum, E. Hauptmann, and H. Li, Direct estimation of equity market impact, Risk, (2005).

- [2] K. Back, Insider trading in continuous time, The Review of Financial Studies, 5 (1992), pp. 387–409.

- [3] K. Back and S. Baruch, Strategic liquidity provision in limit order markets, Econometrica, 81 (2013), pp. 363–392.

- [4] N. Bershova and D. Rakhlin, The non-linear market impact of large trades: evidence from buy-side order flow, Quantitative Finance, 13 (2013), pp. 1759–1778.

- [5] B. Biais, D. Martimort, and J.-C. Rochet, Competing mechanisms in a common value environment, Econometrica, 68 (2000), pp. 799–837.

- [6] N. H. Bingham, C. M. Goldie, and J. L. Teugels, Regular variation, vol. 27, Cambridge university press, 1989.

- [7] A. Dubinsky and M. Johannes, Fundamental uncertainty, earning announcements and equity options, Columbia University Working paper, (2006).

- [8] J. D. Farmer, A. Gerig, F. Lillo, and H. Waelbroeck, How efficiency shapes market impact, Quantitative Finance, 13 (2013), pp. 1743–1758.

- [9] T. Foucault, Order flow composition and trading costs in a dynamic limit order market, Journal of Financial markets, 2 (1999), pp. 99–134.

- [10] T. Foucault and A. J. Menkveld, Competition for order flow and smart order routing systems, The Journal of Finance, 63 (2008), pp. 119–158.

- [11] X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, Institutional investors and stock market volatility, The Quarterly Journal of Economics, 121 (2006), pp. 461–504.

- [12] L. R. Glosten, Is the electronic open limit order book inevitable?, The Journal of Finance, 49 (1994), pp. 1127–1161.

- [13] P. Gopikrishnan, V. Plerou, X. Gabaix, and H. E. Stanley, Statistical properties of share volume traded in financial markets, Physical review e, 62 (2000), p. R4493.

- [14] C. W. Holden and A. Subrahmanyam, Long-lived private information and imperfect competition, The Journal of Finance, 47 (1992), pp. 247–270.

- [15] S. G. Kou and H. Wang, Option pricing under a double exponential jump diffusion model, Management science, 50 (2004), pp. 1178–1192.

- [16] A. S. Kyle, Continuous auctions and insider trading, Econometrica, 53 (1985), pp. 1315–1335.

- [17] F. Lillo, M. Szabolcs, and J. D. Farmer, Theory for long memory in supply and demand, Physical review e, 71 (2005), p. 066122.

- [18] C. A. Parlour and D. J. Seppi, Liquidity-based competition for order flow, The Review of Financial Studies, 16 (2003), pp. 301–343.

- [19] , Limit order markets: A survey, Handbook of financial intermediation and banking, 5 (2008), pp. 63–95.

- [20] A. F. Perold, The implementation shortfall: Paper versus reality, Journal of Portfolio Management, 14 (1988), p. 4.

- [21] M. Potters and J.-P. Bouchaud, More statistical properties of order books and price impact, Physica A: Statistical Mechanics and its Applications, 324 (2003), pp. 133–140.

- [22] A. Ranaldo, Order aggressiveness in limit order book markets, Journal of Financial Markets, 7 (2004), pp. 53–74.

- [23] K. Rock, The specialist’s order book and price anomalies, tech. rep., Harvard University, 1989.

- [24] D. J. Seppi, Liquidity provision with limit orders and a strategic specialist, The Review of Financial Studies, 10 (1997), pp. 103–150.

- [25] A. Tarski, A lattice-theoretical fixpoint theorem and its applications., Pacific journal of Mathematics, 5 (1955), pp. 285–309.

- [26] N. Torre, BARRA Market impact model handbook, Berkeley, 1997.

- [27] P. V., P. Gopikrishnan, L. A. Nunez Amaral, and E. H. Stanley, Scaling of the distribution of price fluctuations of individual companies, Phys. Rev. E, 60 (1999), p. 6519.

- [28] G. Vaglica, F. Lillo, E. Moro, and R. N. Mantegna, Scaling laws of strategic behavior and size heterogeneity in agent dynamics, Physical review e, 77 (2008), p. 036110.

- [29] E. Zarinelli, M. Treccani, J. D. Farmer, and F. Lillo, Beyond the square root: evidence for logarithmic dependence of market impact on size and participation rate, Market Microstructure and Liquidity, 1 (2015).

Appendix A Auxiliary results

Lemma A.1.

and are non-decreasing on the support of .

Proof.

Suppose . Note that is non-decreasing if

Indeed, the left side of the above equals

which is non-negative since on the set .

The second assertion is proved analogously. ∎

Lemma A.2.

Let be a continuous function and (resp. ) be the unique solution of

| (A.35) |

Then, the following hold:

-

(1)

There exits a solution on a filtered probability space to the following SDE:

(A.36) where is either or and is a Brownian motion with .

-

(2)

and , where (resp. ) corresponds to the solution of (A.36) if (resp ) and stands for the expectation under .

-

(3)

.

-

(4)

Suppose further that is non-decreasing. Then, are non-decreasing, too. Consequently, is non-decreasing. Moreover,

(A.37) (A.38)

Proof.

We shall prove the claims for only, the corresponding proof for being analogous.

-

(1)

Note that

Then, if is a Brownian motion on a filtered probability space with , is a bounded martingale with , where . Thus, we can define a new measure on by

By means of Girsanov’s theorem, under , solves (A.36).

-

(2)

Observe that

-

(3)

The claim is equivalent to

Using and , the above is valid if and only if

which holds since for any we have in view of Lemma A.1 and is not constant.

-

(4)

Now, suppose is non-decreasing, which in turn implies since is non-increasing. Therefore, as is Lipschitz on for any , the standard comparison results for SDEs applied to (A.36) in conjunction with Lemma A.1 imply

since we can construct all these solutions indexed by their starting point on the same probability space due to the local Lipschitz property of . This shows the desired monotonicity .

Similarly, the same comparison principle yields that the solution of (A.36) is bounded from above by in case of since . Combined with the monotonicity property of , we deduce .

∎

Appendix B Proofs

Proof of Proposition 2.1.

Proof of Proposition 2.2.

Note that for all . We shall show the result for , the remaining case is similar and easier.

Using the first representation in (2.5), we obtain

which yields the first assertion once divided by .

The remaining claims follow from (resp. ) for (resp. ) and for all since is strictly increasing. ∎

Proof of Proposition 3.2.

First observe that is bounded since is a bounded random variable by assumption. Thus the dominated convergence theorem in conjunction with the continuity of , and thus that of and , show that both of and solve (3.14). As (3.14) can have at most one solution, exists.

Also note that is strictly increasing and continuous by Lemma 3.1. Thus, Thus,

Since each takes values in , , and the measure on converges weakly to the point mass at , we have

This completes the proof. ∎

Proof of Lemma 3.1.

We give the proof for the solutions of (3.11), the analogous property of the solutions of (3.14) can be proven similarly.

Monotone convergence theorem in conjunction with Assumption 3.1 implies

Moreover, . To see this, first note that

Next, the measure

converges to the point mass at . Indeed, for any , we have

which converges to as .

Thus, using the representation of via (3.12), we deduce

Note that changing the order of integration is justified thanks to Assumption 3.1. On the other hand, for any since whenever . This in turn implies . Similarly, . Thus, is strictly increasing in view of (3.12) since and, therefore, is not constant. ∎

Proof of Theorem 3.2.

The proof will be based on an application of Schauder’s fixed point theorem to a suitable mapping defined on the space of non-decreasing continuous functions, i.e. the candidate functions for the solution of (3.11). Note that since takes values in , so does . This justifies the representation (3.12) for . Since in equilibrium must also be taking values in , we must expect to take values in , too. Thus, we can concentrate on functions on that takes values in . Moreover, will possess a derivative that is bounded by

To see this first observe that

Therefore,

We shall show the existence of a fixed point in the normed space , i.e. the space of Borel measurable functions that are square integrable with respect to , where

Note that is equivalent to the Lebesgue measure on . Next define

and let

It is easy to see that is a convex subset of .

Next define the operator on via

where and and are as defined in (3.10) and (3.13), respectively. Note that for each

is a probability measure on .

-

Step 1

( maps into itself): It is easy to verify that is continuous and takes values in in view of Lemma A.2 and that

Moreover, is differentiable with a derivative bounded by by using the above computations that led to the estimate . Thus, .

-

Step 2

( is compact): Let . Then there exists such that -a.e. we have for each . Then by Arzela-Ascoli Theorem there exists a subsequence that converges uniformly on compacts to a continuous function . Without loss of generality let us assume that converges to . Note that necessarily for all , i.e . Finally, as s are uniformly bounded and is a probability measure, the dominated convergence theorem yields in .

-

Step 3

( is continuous): Suppose in as . In view of the definition of we may assume without loss of generality that that s are continuous since changing on a Lebesgue null set does not alter the value of . By another application of Arzela-Ascoli theorem there exists a subsequence that converges pointwise to some continuous function, which we may identify with due to the uniqueness of -limits up to a null set. Thus, we may assume is continuous, too.

Moreover, the same argument shows that every subsequence of has a further subsequence that converges to pointwise since continuous functions that agree on Lebesgue null sets should agree at every point. Thus, pointwise as .

Next, since is uniformly bounded, the dominated convergence theorem yields

On the other hand, Lemma A.2 and Girsanov theorem imply for

where is the expectation operator for under which is a standard Brownian motion, and is the function in Lemma A.2 defined by the terminal condition . Since and are continuous except on a Lebesgue null set, the dominated convergence theorem yields

Similarly,

Thus, we have shown for . Analogous arguments yields the convergence for , which in turn establishes the pointwise convergence of to ; i.e.

This yields the claim by an application of the dominated convergence theorem since s are uniformly bounded.

Therefore, admits a fixed point in by Schauder’s fixed point theorem. That is, there exists a such that . Hence, there exists a solution to (3.11). The claim now follows from Theorem 3.1. ∎

Proof of Theorem 3.3.

-

(1)

Let be the space of nondecreasing functions on that take values in and define an operator on via

First observe that if since is non-decreasing. Thus, setting and for , we observe that is an increasing sequence of nondecreasing continuous functions taking values in . Thus, the limit, exists, is nondecreasing, and continuous by Dini’s theorem. It also follows from the dominated convergence theorem and that has only countably many discontinuities that is a solution of (3.17).

Now let denote the set of all solutions of (3.17) in and define

Clearly, takes values in . Due to the aforementioned monotonicity for all . Consequently, . Setting and for , we again obtain an increasing sequence which converges to some element of . Moreover, , which in turn implies by the construction of .

Note that if is constant, it has to equal since . However, under this assumption, the right side of (3.17) equals

as . Thus, cannot be constant.

-

(2)

Since , the proof follows the similar lines as above and, hence, omitted

∎

Proof of Theorem 4.1.

We shall give a proof of the first statement as the second one can be proven along similar lines. We can assume without loss of generality that since, otherwise, we can replace by and redefine and accordingly.

By means of a straightforward change of variable we obtain for

Observe that the measure converges to the Dirac measure at point as .

-

Step 1:

For

for some by the Mean Value Theorem, where stands for the derivative of , since . Thus,

(B.41) as .

-

Step 2:

Let . Then, in view of the first step, Fatou’s lemma yields

Thus, if for some , it must be for almost all . However, for all since is decreasing. Thus, for all . In particular, is bounded away from on for any .

-

Step 3:

It follows from Step 2 and Corollary 2.0.5 in [6] that

for some constants and . Moreover, since for we have

and for large enough , we deduce that the mapping is bounded when belongs to bounded intervals in .

-

Step 4:

Moreover,

which in turn implies

(B.42) Since is bounded when belongs to bounded intervals in by Step 3, we obtain, for any ,

(B.43) where in view of (B.41) provided that the limit exists.

Furthermore, in view of (B.42) we also have

(B.44) -

Step 5:

Applying the arguments of Step 4 to the second and the third integrals in (B) now shows that for

(B.45) In particular, exists. Using the initial condition that , direct manipulations show that

∎

Proof of Theorem 4.2.

We shall again only give the proof the first statement and assume without loss of generality that .

For any define

Straightforward manipulations similar to the ones employed in the proof of Theorem 4.1 leads to

for some independent of , where the first inequality follows from that and for and the second is due to the boundedness of .

Moreover, for

due to the monotonicity of . Thus, utilising the boundedness of once more, we arrive at

| (B.46) |

for some that is independent of .

-

Step 1:

Let be as above and consider the operator defined by

Clearly is increasing, i.e. if .

-

Step 2:

For and ,

(B.47) Thus, if for some and , we have

where the last inequality is due to the hypothesis that .

In particular, given for some , whenever .

-

Step 3:

Define

and observe that the restriction of to belongs to for all .

In view of Step 2 we have that for large enough . Thus, it admits a fixed point in for large enough by Tarski’s theorem (Theorem 1 in [25]). In fact, it admits a unique fixed point. Indeed, if and are two fixed points of in ,

Thus,

for some . Since , the above implies . Applying the same argument to , we deduce .

-

Step 4:

In view of Step 3 we have that for all for large enough . Thus, Theorem 3.1.5 in [6] yields is bounded in bounded subintervals of uniformly in .

-

Step 5:

In view of Step 4 and using arguments similar to the ones used in Steps 4 and 5 of the proof of Theorem 4.1, we arrive at

where for . The unique solution of the above equation with is given by

-

Step 6:

Consider

Observe that

which converges to as since is slowly varying at . Thus,

where is a slowly varying function at . That is,

Since (cf. Proposition 1.3.6 (i) and (iii) in [6]), we have

∎

Proof of Corollary 4.1.

Again we only prove the first statement. The hypothesis implies is regularly varying with index at . Thus, is regularly varying of index at , which in particular implies

| (B.48) |

in view of Theorem 1.5.11(ii) in [6].

Moreover, direct manipulations yield

which in turn implies

Therefore,

where the second equality follows from (B.48).

Proof of Theorem 4.3.

We shall give a proof of the first statement as the second one can be proven along similar lines.

By means of a change of variable employed in earlier proofs we obtain for

where

| (B.50) |

We shall first demonstrate that for the measure converges to the Dirac measure at point as . Indeed, let be the maximal solution of (3.17) and observe that for any and

where the last inequality is due to the fact that by Theorem 3.3.

Moreover, since is regularly varying at with some index by Corollary 4.1, we have for some for all by Proposition 1.3.6(v) in [6]. Therefore,

| (B.51) |

the right side of which converges to as . Similary, we can show

-

Step 1:

Let . It follows from the same argument in Step 2 of the proof of Theorem 4.1 that is bounded away from on for any . This in turn implies the mapping is bounded when belongs to bounded intervals in as in Step 3 of the same proof.

- Step 2:

-

Step 3:

If , the proof of Theorem 4.2 can be applied verbatim once we show that is bounded in uniformly in , where

Since is eventually larger than and for , we have for large enough

where the last inequality follows from Part (4) of Lemma A.2 since is increasing in for positive . Thus, can be shown to be bounded by the same function that bounds introduces in the proof of Theorem 4.2. Repeating the remaining arguments therein yields the claim.

∎

Proof of Corollary 4.3.

It follows from Theorem 3.1 that must solve (3.11). In particular is regularly varying at of order .

In view of Proposition 2.2 we have

Observe that by Proposition 1.3.6 (v) in [6]. Thus, . This justifies the application of the L’Hospital rule to arrive at

where the third equality follows from Exercise 1.11.13 applied to .

Asymptotic relationship near is proved the same way. ∎