Complete Subset Averaging for Quantile Regressions ††thanks: The authors would like to thank the Editor, Peter Phillips, the Co-Editor, Arthur Lewbel, and three anonymous referees for helpful comments and suggestions, which have led to substantial improvements. They also thank Xun Lu and Liangjun Su for helpful discussion and sharing their codes. Shin is grateful for partial support by the Social Sciences and Humanities Research Council of Canada (SSHRC-435-2018-0275). This work was made possible by the facilities of WestGrid (www.westgrid.ca) and Compute Canada (www.computecanada.ca).

Abstract

We propose a novel conditional quantile prediction method based on complete subset averaging (CSA) for quantile regressions. All models under consideration are potentially misspecified and the dimension of regressors goes to infinity as the sample size increases. Since we average over the complete subsets, the number of models is much larger than the usual model averaging method which adopts sophisticated weighting schemes. We propose to use an equal weight but select the proper size of the complete subset based on the leave-one-out cross-validation method. Building upon the theory of Lu and Su (2015), we investigate the large sample properties of CSA and show the asymptotic optimality in the sense of Li (1987). We check the finite sample performance via Monte Carlo simulations and empirical applications.

Keywords: complete subset averaging, quantile regression, prediction, equal-weight, model averaging.

JEL classification: C21, C52, C53

1 Introduction

Quantile regression (QR) has emerged as an essential tool since Koenker and Bassett (1978) (see, e.g. Koenker (2005)). QR estimates the response of conditional quantiles of outcome variables with respect to changes in the covariates. The entire response distribution of outcome variables in economic models provides a broader insight than the classical mean regression. Moreover, in many economic applications, tail quantiles have highly valuable information. See, for example, wage distribution in labor economic applications (Buchinsky, 1998) and stock return quantiles (Value-at-Risk) in financial market analysis (Duffie and Pan, 1997). Recently, policymakers have begun to pay attention to the left tail quantiles of GDP growth (Growth-at-Risk) as a measure of downside risks associated with tight financial conditions (Adrian, Boyarchenko, and Giannone, 2019). There has also been an increasing interest in climate change, in particular, more frequent and intense extreme weather conditions. A tail quantile is the main object of interest in this analysis (Bhatia, Vecchi, Knutson, Murakami, Kossin, Dixon, and Whitlock, 2019). Estimation, inference, and prediction of the conditional quantiles are thus important but require a careful econometric analysis due to their nonlinear structure and nonstandard limit theory.

In this paper, we propose a novel prediction method based on complete subset averaging (CSA) for quantile regressions. Following Lu and Su (2015), we work on the framework such that all models under consideration are potentially misspecified and that the dimension of regressors goes to infinity as the sample size increases. The CSA method that we propose works as follows. First, pick the numbers of regressors out of all regressors available in the data. Then, there exist complete subsets of size . Second, estimate all the quantile regression models and save all the conditional quantile predictors from each model. Finally, the conditional quantile predictor is constructed as the average of all the quantile predictors estimated in Step 2. Since we average over the complete subsets, the number of models is much larger than the usual model averaging methods selecting the weight of each model. We propose to use an equal weight but select the optimal size of the complete subset based on the leave-one-out cross-validation method.

The CSA approach has a couple of advantages over the existing model averaging method which adopts sophisticated weighting schemes. First, it may produce better forecasts in practice because there is no sampling variance from the weight estimation. This result is already reported both in the forecasting and machine learning literature in the mean regression setup (see, e.g. Breiman (1996), Clemen (1989), Stock and Watson (2004), Smith and Wallis (2009), and Elliott, Gargano, and Timmermann (2013)). Second, it does not ask a researcher to choose the initial set of models and the order of each model. In practice, the model averaging methods with different weights usually construct the set of models in an encompassing way and the forecasting performance could depend on the researcher’s discretion. Third, CSA averages over a larger number of submodels and one could expect an additional noise reduction from it. However, CSA is possibly more demanding in computation, and we will discuss this issue in detail later.

The contribution of this paper is twofold. First, building upon the theory of Lu and Su (2015), we show that the complete subset quantile regression (CSQR) estimator converges the pseudo-true value and satisfies asymptotic normality under mild regularity conditions. The uniform convergence property of CSQR is also provided. Based on these pointwise and uniform limit theories, we prove the asymptotic optimality of in the sense of Li (1987). Second, we implement the CSA method and show that it performs quite well both in simulations and real data sets. Especially, we show that the performance is still satisfactory when we use a fixed number of subsets randomly drawn from the complete subsets when the time budget does not allow estimating the quantile regressions of the whole subsets. We also provide regularity conditions on the choice of the fixed number of subsets. Finally, we provide a theory that compares the performance of equal weighting and optimal weighting in quantile regression. This result justifies our intuition such that optimal weighting forecasts poorly when the number of models increases and extends the existing result in mean regression.

Finally, we summarize related literature. Lu and Su (2015) and Elliott, Gargano, and Timmermann (2013) are closely related to this paper. The former proposes the jackknife model averaging (JMA) method for the quantile prediction problem and derives the nonstandard asymptotic properties of the estimator. Our approach is different from theirs in that we use complete subsets for models to be averaged and that we choose a scalar from the cross-validation method instead of a weighting vector . The latter proposes the CSA method in the mean prediction problem and shows by simulation studies that the CSA predictor outperforms alternative methods like bagging, ridge, lasso, and Bayesian model averaging. However, they do not show any optimality result of the estimator. Hansen (2007) and Hansen and Racine (2012) show the optimality of model averaging based on the Mallows criterion and that of the jackknife model averaging, respectively. Ando and Li (2014) propose a model averaging method in a high-dimensional setting and show the optimality result. Komunjer (2013) provides a great review on the quantile prediction problem of time-series data. Meinshausen (2006) proposes a quantile prediction method based on random forest. Lee (2016) studies the inference problem of the predictive quantile regression when the regressors are persistent. In the empirical finance literature, Meligkotsidou, Panopoulou, Vrontos, and Vrontos (2019, 2021) apply complete subset quantile regression to forecast realized volatility and the risk premium.

The rest of the paper is organized as follows. Section 2 introduces the model and the CSQR estimator. Section 3 presents the asymptotic properties of the CSQR estimator and the asymptotic optimality. The Monte Carlo simulation results are reported in Section 4. Section 5 investigates two empirical applications and illustrates the advantage of the proposed method. Section 6 concludes. All the proofs are deferred to the appendix.

We use the following notation. For a matrix , represents its Frobenius norm . Let and denote the smallest and largest eigenvalues of . We use the notation to denote ; and to denote .

2 Model and Estimator

In this section, we lay out the model under study and propose the complete subset averaging (CSA) quantile predictor. We also discuss the choice of the subset size based on the cross-validation method.

2.1 CSA Quantile Predictor

Consider a random sample for , where the dimension of can be countably infinite. Following Lu and Su (2015), we assume that is generated from the following linear quantile regression model: for ,

| (1) |

where , , , and is the -th conditional quantile function of given . Note that we drop from each expression for notational simplicity and that satisfies the quantile restriction . Equivalently, we can also express as is often done in the quantile regression literature.

We consider a sequence of covariates available, which approximate the above quantile regression model:

where is the approximation error and is the total number of available regressors that may increase as the sample size increases. Thus, we presume that all models are misspecified in a finite sample as in Hansen (2007).111Using quantile crossings, Phillips (2015) also shows that quantile regresssion is always at the risk of model misspecification unless the parameters are local to constant over .

Given regressors, we consider a model composed of regressors, where . There are different ways to select regressors out of . Therefore, a subset of size is composed of different elements and a model is defined as a single element of them. We use index for each model. For example, consider that we have regressors and construct a subset of size . Then, we have different ways to choose a model as follows: and . Each model is indexed by . For succinct notation, we drop all subscripts from , , and and denote them as , , and unless there is any confusion.

We now consider a quantile regression model with regressors in a complete subset. Let model with a size be given. For observation , let be a -dimensional vector of regressors corresponding to model , i.e. in the above example. We can construct a linear quantile regression model with regressors :

| (2) |

where is again the approximation error when we use only regressors. The model in (2) is estimated by the standard method in linear quantile regression:

| (3) | ||||

| (4) |

where is a parameter space and is the check function. Note that the estimator is defined for each subset size and for each model with regressors. As noted above, we can think of different models and corresponding estimators that have regressors.

We have a few remarks here. First, we use the subscript to denote a generic model with regressors. However, the index set itself is defined in terms of , which implies that is also determined by . Recall the original notation above. Therefore, model has the same number of regressors and we cannot choose and in an arbitrary way. Second, we allow that the subset size goes to infinity as increases. In other words, there exists a sequence of subset sizes that diverges. This setting is natural as the upper bound goes to infinity as increases. Note that the number of regressors in each model ( in their notation) is also allowed to diverge in Lu and Su (2015). Both approaches allow more complex models to be averaged as grows, which is measured by and , respectively. However, Lu and Su (2015) require controlling the growth rates of and , separately. The proposed method constructs submodels based on the complete subsets, and is tightly related to and . As a result, the regularity condition on the complexity of the models is expressed only in terms of (see Assumption 3 in Section 3).

We finalize this subsection by defining the complete subset averaging (CSA) quantile predictor. Let the size of the complete subset be given. For each model, we estimate the parameter by (3) and construct the linear index . The CSA quantile predictor of given is defined as a simple average of those indices over different models:

The CSA quantile predictor is different from the JMA quantile predictor of Lu and Su (2015) in two respects. First, we do not select the set of models to be averaged since we average over the complete subsets of size . Second, CSA does not estimate the weights over different models. The idea of averaging over the complete subsets was first introduced by Elliott, Gargano, and Timmermann (2013) in the conditional mean prediction setup. Heuristically speaking, since the weights can be seen as additional parameters to be estimated in the model, the equal weight could perform better in a finite sample when the number of models (i.e. the dimension of a weight vector) is large.

2.2 Choice of Subset Size

We propose to choose the subset size using the leave-one-out cross-validation method. We will show in the next section that the subset size chosen by this method is optimal in the sense that it is asymptotically equivalent to the infeasible optimal choice.

For , we define a cross-validation objective function as follows:

| (5) | ||||

| (6) |

where is the jackknife estimator for , which is estimated by (3) without using the -th observation , and is a corresponding jackknife CSA quantile predictor for the -th outcome variable . The prediction error is measured by the check function . Then, we can choose the complete subset size that minimizes the cross-validation objective function as follows:

| (7) |

After choosing the complete subset size, the CSA quantile predictor is finally defined as

| (8) |

where the plugged-in is chosen by (7).

We finalize this subsection by adding some remarks on computation. First, we propose to use a fixed number of random draws of models when is too large to implement the method. Since , it can be quite large when the model has large potential regressors. The simulation studies in Section 4 reveal that the CSA quantile predictor still performs well with a feasible size of submodels randomly drawn from the complete subsets. We also provide regularity conditions that assure the asymptotic equivalence between using and in Section 3. Second, the proposed jackknife method can be immediately extended to the -fold cross-validation method, where is the partition size of the sample. Algorithm 1 below summarizes the leave-one-out cross-validation method for choosing .

| (9) |

3 Asymptotic Theory

In this section, we investigate the asymptotic properties of the complete subset quantile regression (CSQR) estimator. We first provide the pointwise and uniform convergence results of and , respectively. Then, we show the optimality of CSA in the sense of Li (1987), which implies that is asymptotically equivalent to the infeasible optimal choice of the subset size.

In addition to the model described in Section 2, we define some notation for later use. Let be a conditional probability density function for generic random variables and . Since all models are potentially misspecified in the model averaging literature, we define the pseudo-true parameter value for any given :

Let . For any such that and , we define

and

We need the following regularity conditions.

Assumption 1.

-

(i)

is i.i.d. generated by (1)

-

(ii)

a.s.

-

(iii)

and for some

Assumption 2.

-

(i)

is bounded above by and continuous over its support a.s.

-

(ii)

There exist constants and such that

-

(iii)

There exist constants and such that

-

(iv)

Assumption 3.

Let , , , and .

-

(i)

and

-

(ii)

and .

Conditions (i)–(ii) in Assumption 1 are the standard i.i.d. and the quantile restrictions. Assumption 1(iii) requires some finite moment restrictions to achieve the probability bounds of various sample mean objects in the proof. Assumption 2 allows conditional heteroskedasticity. Note that the eigenvalues of and are bounded and bounded away from zero for a given . However, these bounds can converge to zero or diverge to infinity as increases. The speed of convergence is restricted by Assumption 2 (iv). These bounded eigenvalue restrictions are commonly imposed in the literature that studies the increasing dimension of parameters (see, e.g. Portnoy (1984, 1985)). Assumptions 1–2 are standard and similar to those in Lu and Su (2015). See the additional remarks therein. Assumption 3 imposes some regularity conditions on the number of potential regressors and the sequence of the uniform bounds . Different from the regularity condition of JMA in Lu and Su (2015), we need not restrict the growth rate of potential models directly since is determined by . However, increases very quickly at a factorial rate of and we need a stronger restriction on . As noted in Assumption 3(ii), can increase at most the logarithmic rate of . In the case of JMA, the number of regressors can increase at the polynomial rate if we set in their notation. This is a trade-off in proving the uniform convergence results over a larger index set than that of JMA. We discuss this point in detail below in Theorem 2. The second part of Assumption 3(ii) holds if c̱ is bounded away from zero or converges to zero at the slower rate than when increases at the rate of .

First, we prove the convergence rate and the asymptotic normality of when the dimension of parameter increases.

Theorem 1.

Suppose that Assumptions 1, 2, and 3(i) hold. Let denote an matrix such that exists and is positive definite, where is a fixed integer. Then,

-

(i)

-

(ii)

.

This theorem provides an asymptotic theory for the quantile regression estimator when the model is misspecified and the number of parameters diverges to infinity as similarly seen in Lu and Su (2015). The convergence rate in (i) is a standard result when diverges as increases. To show the asymptotic normality with a diverging number of parameters, we also consider an arbitrary linear combination of represented by . The difference between two estimators, CSA and JMA, originates from the fact that CSA chooses the total number of the regressors first and the number of complete subset models follows automatically for each , whereas JSA selects the set of models (in their notation) in advance. Then, the size of regressors in case of JSA is determined by the sequence of models chosen by a researcher. Although there are slight differences in the definition of and and their bounds from those in Lu and Su (2015), the proof of Theorem 1 is identical to theirs, so is omitted.

We next turn our attention to the uniform convergence results of and . In addition to its own interest, the uniform convergence rates in the next theorem are required to prove to the asymptotic optimality of .

Theorem 2.

Suppose that Assumptions 1, 2, and 3(ii) hold. Then,

-

(i)

-

(ii)

.

Since CSA is defined on the index sets of and , the uniform convergence rates are defined over those sets, and . In case of , we need additional uniformity over . As a result, the regularity conditions that control the growth rates of and are different from those of JMA in Assumption 3 (ii). As discussed before, since the number of complete subsets increases at the factorial rate of , we need a restriction on slightly stronger than that of JMA. We follow the proof strategy in Lu and Su (2015) which extends the results of Rice (1984) by using the inequality in Shibata (1981, 1982). To handle the different growth rates, we provide new technical lemmas. The proof of Theorem 2 as well as these lemmas are provided in the appendix. Finally, the uniform convergence rates are expressed in terms of the sample size and the total number of regressors that goes to infinity as increases.

We next prove the prediction equivalence when we replace with . Let be a subset of such that elements are randomly drawn. Define to be the CSA quantile predictor using only models:

Let . We show the validity of in the following theorem:

Theorem 3.

Suppose that Assumptions 1–3 hold. Let and as . Furthermore, we assume that

Then, we have

The rate requirement for is mild and would work given . The uniform boundedness assumption on is weak and holds easily in most applications. We have some remarks on the uniform convergence assumption of the model average with the pseudo-true parameter . Let . Note that is discrete and the functional class size over is small. Thus, it depends on the dependent structure of to hold the uniform law of large numbers. For example, consider the following maximal inequality: for ,

where the second line holds from the Markov inequality. Since , a sufficient condition for the uniform convergence is . If is covariance stationary over for all , then the sufficient condition becomes the absolute summability condition . See, e.g. Fazekas and Klesov (2001) for more general conditions on the partial sums in a different dependent structure.

We now prove the asymptotic optimality of in the sense of Li (1987). Following Lu and Su (2015), we use the final prediction error (FPE, or the out-of-sample quantile prediction error) as a criterion to evaluate the prediction performance:

where is a sample. The next theorem shows that is asymptotically equivalent to the infeasible best subset size choice that is defined as a minimizer of .

Theorem 4.

Suppose that Assumptions 1–3. Then,

where

A similar optimality concept has been adopted in the context of the weighted average estimator (e.g. Hansen (2007), Hansen and Racine (2012), and Lu and Su (2015)) and in the context of the IV estimator (e.g. Donald and Newey (2001), Kuersteiner and Okui (2010), and Lee and Shin (2018)). Different from JMA, CSA considers the complete subsets given and does not require the pre-selection of models to be considered nor the order of models. Thus, the optimality result is also independent of the initial model selection/ordering issue once the total number of regressors is given. The index set of CSA is discrete while that of JMA or the jackknife model averaging in Hansen and Racine (2012) is compact. All require the finite moment condition similar to Assumption (A.1) in Li (1987) which is assured by Assumption 1 (iii) above. The idea of complete subset averaging has been adopted in the forecasting literature (e.g. Elliott, Gargano, and Timmermann (2013, 2015), Rapach, Strauss, and Zhou (2010)). This is the first formal result to show the optimality of the subset size selection.

Finally, we compare the performance of the nonstochastic equal weight with that of the optimal weight. In the mean prediction context, it has been observed that a simple arithmetic mean, i.e. the equal weight, outperforms the estimated optimal weight. This empirical phenomenon is known as the ‘forecast combination puzzle’ and some formal explanations under the mean squared error are provided by Smith and Wallis (2009), Elliott (2011), and Claeskens, Magnus, Vasnev, and Wang (2016), to name a few. Heuristically speaking, it happens when the estimation error of the optimal weight is large enough to dominate the efficiency loss caused by the equal weight. We extend this result to the class of smooth expected loss functions. This is crucial in our analysis since the check function does not give a closed-form solution, which is different from the mean squared error used in the existing literature.

We consider the following simplified framework to focus on the main idea. Let be be predictors for based on different models. For example, we can think of for any given . Let be an -dimensional weight vector combining the predictors. We consider only positive weights with , where is an -dimensional unit vector. Let and be the prediction error of and be a vector of these prediction errors. We define the prediction error of the combined predictor as . Then, we can define an optimal weight as

where is the standard -simplex and is an expected loss function. For example, the mean squared error in Elliott (2011) can be written in terms of the quadratic loss function: , where . The quantile prediction error adopted in this paper can be written in terms of the check function: . Let be an equal-weight vector and be an estimator for with . To illustrate our main point, we further impose that and .

Theorem 5.

Suppose that is twice differentiable on and that uniformly in . Let .

-

(i)

-

(ii)

E.

We have some remarks. First, it shows that the equal weight may work better than the estimated optimal weight when we average many models, i.e. when is large. Compared to the optimal prediction error , the efficiency loss by is bounded by , which converges to for large enough . On the contrary, the upper bound of the mean efficiency loss by diverges as increases. We admit that these upper bounds only reflect the worst case scenario. However, it confirms the intuition formally that the equal weight can outperform the estimated optimal weight under the class of smooth expected loss functions. Second, the prediction error of under a quadratic loss function converges to the optimal prediction error as increases. The same result is also proved in Proposition 1 in Elliott (2011). Different from his result, it does not require decomposing the prediction error into the common component and the idiosyncratic component. This result is summarized in Corollary 6 below. Third, to achieve the optimality, the estimation errors of the weight , , should vanish fast enough. Let . A sufficient condition for the optimality is . For example, if is a parametric rate, , then should be bounded by . When , for example, this condition is satisfied. However, if increases too fast, then will diverge and may work worse than .222We thank an anonymous referee and Co-editor for pointing out this intuition. Also, note that it is one sufficient condition. It is still possible that there exists a different set of conditions that guarantee the optimality. Fourth, , where are eigenvalues of since is symmetric. Thus, the uniform bound exists if is absolutely summable, . Fifth, if we restrict our attention to the expected check function adopted in this paper, is twice differentiable if the conditional density is smooth for all . From Theorem 1 in Angrist, Chernozhukov, and Fernández-Val (2006), we have

| (10) |

where is the conditional quantile function of given and . Thus, the smoothness of is implied by the twice differentiability of . Finally, equation (10) shows that CSA would not work well if we include many irrelevant models. Similar to the quantile regression specification error in Angrist et al. (2006), we call the quantile prediction specification error. If there are many irrelevant models, the optimal weight would be sparse, i.e. many elements of would be zeros. In such a case, CSA with results in a larger quantile prediction specification error given and . For example, if there is only one relevant regressor and all other coefficients equal zero besides one, the complete subsets will be composed of many irrelevant models. As we will see in the simulations studies in the next section, CSA does not perform well under this situation. Therefore, a pre-screening process is desirable to achieve a satisfactory result of CSA.

Corollary 6.

Suppose that we have a quadratic loss function, and that uniformly in , where . Then, we have

4 Monte Carlo Simulations

In this section, we investigate the finite sample performance of the proposed estimator in simple Monte Carlo experiments. We consider two categories of the simulation designs: (i) all candidate models are misspecified, and (ii) candidate models include the true model.

First, we adopt the following data generating process (DGP):

| (11) |

where and follows a multivariate normal distribution, with if and 1 if . Therefore, the regressors are possibly dependent on each other, which is a more general feature of the design than the existing literature, see, e.g., Hansen (2007) and Lu and Su (2015). The term follows independent of . The sample is i.i.d. over . The population is controlled by . We consider two sample sizes, . The number of potential regressors is set to , which is 15 and 20, respectively. Note that all candidate models are misspecified since there remain many missing regressors in the sample. We consider various DGPs by combining different , , and . We consider 38 different DGPs in total and estimate 74 different quantile models.

We compare the performance of the proposed Complete Subset Averaging estimator (CSA) with the Jackknife Model Averaging estimator (JMA) in Lu and Su (2015), the -penalized quantile regression (L1QR) in Belloni and Chernozhukov (2011), the bootstrap aggregating methods (BAG) in Breiman (1996) and -penalized quantile regression. L1QR and L2QR are also called the lasso and the ridge regression in the mean regression setup. The set of models used for JMA is constructed in an encompassing way, e.g. . For CSA, we set the maximum submodels to . Thus, we draw 100 models randomly from the complete subsets of size if is bigger than 100. Furthermore, we reduce some computational burden by applying 10-fold cross-validation when . The tuning parameter of L1QR is chosen by Equation (2.7) in Belloni and Chernozhukov (2011). The bootstrap size of BAG is set to be 1000. The tuning parameter of L2QR is chosen by 10-fold cross-validation over the set which is constructed after some pre-simulation studies.

To compare the performance, we first compute for each replication as follows. After estimating the model with in-sample observations, we generate additional 100 out-of-sample observations. Then, is calculated by

where is a predicted value by each method. Then, we construct the following three comparison measures:

where each subscript denotes generic notation for a forecasting method. Note that the loss to CSA ratio provides more direct binary comparison of each method to CSA. We set the total number of replications .

|

|

|

|

| CSA | JMA | L1QR | BAG | L2QR | CSA | JMA | L1QR | BAG | L2QR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Average FPE | |||||||||||

| 0.1 | 0.419 | 0.438 | 0.420 | 0.426 | 0.427 | 0.405 | 0.415 | 0.415 | 0.418 | 0.408 | |

| (0.043) | (0.047) | (0.037) | (0.035) | (0.048) | (0.033) | (0.035) | (0.033) | (0.033) | (0.033) | ||

| 0.2 | 0.420 | 0.439 | 0.421 | 0.429 | 0.435 | 0.404 | 0.415 | 0.415 | 0.419 | 0.409 | |

| (0.042) | (0.046) | (0.036) | (0.035) | (0.051) | (0.032) | (0.034) | (0.033) | (0.033) | (0.033) | ||

| 0.3 | 0.420 | 0.440 | 0.421 | 0.430 | 0.439 | 0.403 | 0.415 | 0.414 | 0.418 | 0.409 | |

| (0.041) | (0.045) | (0.036) | (0.035) | (0.053) | (0.032) | (0.033) | (0.033) | (0.032) | (0.032) | ||

| 0.4 | 0.421 | 0.442 | 0.424 | 0.430 | 0.437 | 0.403 | 0.416 | 0.414 | 0.418 | 0.408 | |

| (0.042) | (0.047) | (0.035) | (0.035) | (0.049) | (0.032) | (0.034) | (0.033) | (0.032) | (0.031) | ||

| 0.5 | 0.422 | 0.445 | 0.425 | 0.432 | 0.441 | 0.405 | 0.418 | 0.416 | 0.419 | 0.409 | |

| (0.042) | (0.046) | (0.035) | (0.035) | (0.053) | (0.032) | (0.034) | (0.033) | (0.032) | (0.032) | ||

| 0.6 | 0.423 | 0.447 | 0.427 | 0.436 | 0.443 | 0.407 | 0.421 | 0.418 | 0.420 | 0.411 | |

| (0.041) | (0.045) | (0.035) | (0.036) | (0.055) | (0.032) | (0.034) | (0.033) | (0.032) | (0.033) | ||

| 0.7 | 0.423 | 0.451 | 0.429 | 0.440 | 0.443 | 0.407 | 0.422 | 0.419 | 0.421 | 0.410 | |

| (0.043) | (0.046) | (0.036) | (0.036) | (0.052) | (0.031) | (0.033) | (0.033) | (0.032) | (0.032) | ||

| 0.8 | 0.424 | 0.455 | 0.434 | 0.455 | 0.447 | 0.407 | 0.425 | 0.421 | 0.427 | 0.413 | |

| (0.042) | (0.046) | (0.036) | (0.038) | (0.051) | (0.031) | (0.033) | (0.033) | (0.032) | (0.032) | ||

| 0.9 | 0.430 | 0.470 | 0.449 | 0.495 | 0.459 | 0.413 | 0.432 | 0.428 | 0.442 | 0.418 | |

| (0.043) | (0.048) | (0.038) | (0.049) | (0.055) | (0.033) | (0.035) | (0.034) | (0.035) | (0.033) | ||

| Winning Ratio | |||||||||||

| 0.1 | 27.8% | 8.6% | 14.9% | 19.5% | 29.2% | 34.2% | 10.1% | 6.8% | 11.3% | 37.6% | |

| 0.2 | 29.6% | 7.7% | 17.2% | 19.7% | 25.8% | 35.9% | 10.1% | 7.7% | 11.8% | 34.5% | |

| 0.3 | 33.6% | 6.9% | 16.2% | 20.9% | 22.4% | 39.4% | 8.9% | 7.9% | 10.9% | 32.9% | |

| 0.4 | 34.3% | 6.4% | 14.4% | 21.0% | 23.9% | 38.5% | 7.4% | 7.7% | 12.5% | 33.9% | |

| 0.5 | 35.8% | 5.9% | 16.3% | 18.0% | 24.0% | 38.4% | 8.8% | 7.2% | 13.4% | 32.2% | |

| 0.6 | 36.6% | 7.1% | 15.6% | 17.7% | 23.0% | 40.1% | 7.4% | 7.5% | 13.0% | 32.0% | |

| 0.7 | 38.8% | 4.4% | 15.5% | 16.0% | 25.3% | 40.4% | 6.3% | 7.1% | 12.3% | 33.9% | |

| 0.8 | 47.2% | 4.4% | 12.7% | 11.1% | 24.6% | 43.2% | 6.7% | 6.2% | 10.0% | 33.9% | |

| 0.9 | 54.1% | 4.2% | 9.9% | 3.6% | 28.2% | 43.0% | 5.3% | 6.1% | 6.7% | 38.9% | |

| Loss to CSA | |||||||||||

| 0.1 | NA | 77.3% | 59.6% | 57.0% | 55.6% | NA | 77.8% | 81.8% | 65.4% | 52.5% | |

| 0.2 | NA | 77.8% | 59.4% | 58.4% | 59.8% | NA | 79.1% | 82.6% | 64.2% | 55.2% | |

| 0.3 | NA | 79.8% | 62.2% | 61.1% | 61.5% | NA | 80.4% | 82.8% | 66.3% | 57.3% | |

| 0.4 | NA | 79.3% | 65.1% | 60.0% | 62.3% | NA | 82.8% | 83.2% | 65.2% | 54.2% | |

| 0.5 | NA | 80.7% | 65.6% | 61.6% | 62.1% | NA | 81.9% | 81.8% | 65.5% | 55.5% | |

| 0.6 | NA | 82.4% | 67.2% | 64.3% | 64.7% | NA | 82.7% | 82.4% | 66.1% | 57.1% | |

| 0.7 | NA | 84.7% | 69.8% | 64.5% | 62.3% | NA | 85.8% | 82.9% | 65.2% | 54.8% | |

| 0.8 | NA | 86.4% | 75.5% | 73.2% | 65.4% | NA | 85.6% | 85.4% | 69.5% | 56.5% | |

| 0.9 | NA | 89.2% | 82.6% | 86.0% | 68.0% | NA | 87.2% | 84.6% | 74.5% | 54.3% | |

-

•

Notes: The standard error of the average FPE is denoted inside the parentheses.

| CSA | JMA | L1QR | BAG | L2QR | CSA | JMA | L1QR | BAG | L2QR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Average FPE | |||||||||||

| 0.1 | 0.191 | 0.204 | 0.215 | 0.194 | 0.225 | 0.182 | 0.188 | 0.195 | 0.188 | 0.198 | |

| (0.028) | (0.036) | (0.040) | (0.023) | (0.046) | (0.019) | (0.021) | (0.025) | (0.020) | (0.026) | ||

| 0.2 | 0.191 | 0.205 | 0.215 | 0.196 | 0.226 | 0.181 | 0.188 | 0.194 | 0.188 | 0.198 | |

| (0.027) | (0.035) | (0.039) | (0.024) | (0.050) | (0.019) | (0.021) | (0.024) | (0.021) | (0.027) | ||

| 0.3 | 0.191 | 0.207 | 0.217 | 0.198 | 0.229 | 0.181 | 0.189 | 0.195 | 0.187 | 0.196 | |

| (0.029) | (0.036) | (0.040) | (0.025) | (0.049) | (0.019) | (0.021) | (0.025) | (0.020) | (0.025) | ||

| 0.4 | 0.192 | 0.209 | 0.218 | 0.196 | 0.224 | 0.181 | 0.189 | 0.194 | 0.188 | 0.197 | |

| (0.028) | (0.037) | (0.039) | (0.023) | (0.047) | (0.019) | (0.021) | (0.024) | (0.021) | (0.027) | ||

| 0.5 | 0.192 | 0.211 | 0.219 | 0.197 | 0.225 | 0.182 | 0.189 | 0.194 | 0.188 | 0.196 | |

| (0.029) | (0.036) | (0.040) | (0.023) | (0.046) | (0.019) | (0.021) | (0.025) | (0.020) | (0.026) | ||

| 0.6 | 0.193 | 0.212 | 0.220 | 0.199 | 0.225 | 0.182 | 0.191 | 0.196 | 0.190 | 0.197 | |

| (0.029) | (0.037) | (0.042) | (0.024) | (0.047) | (0.018) | (0.021) | (0.024) | (0.020) | (0.026) | ||

| 0.7 | 0.194 | 0.214 | 0.220 | 0.201 | 0.224 | 0.182 | 0.192 | 0.196 | 0.190 | 0.195 | |

| (0.032) | (0.038) | (0.040) | (0.025) | (0.046) | (0.018) | (0.021) | (0.024) | (0.021) | (0.025) | ||

| 0.8 | 0.194 | 0.216 | 0.225 | 0.208 | 0.223 | 0.183 | 0.193 | 0.197 | 0.193 | 0.195 | |

| (0.028) | (0.035) | (0.041) | (0.027) | (0.046) | (0.018) | (0.022) | (0.025) | (0.020) | (0.024) | ||

| 0.9 | 0.196 | 0.223 | 0.235 | 0.233 | 0.224 | 0.184 | 0.197 | 0.200 | 0.200 | 0.194 | |

| (0.027) | (0.035) | (0.041) | (0.032) | (0.046) | (0.018) | (0.022) | (0.025) | (0.021) | (0.023) | ||

| Winning Ratio | |||||||||||

| 0.1 | 38.8% | 10.0% | 8.0% | 34.2% | 9.0% | 38.4% | 12.8% | 8.3% | 26.7% | 13.8% | |

| 0.2 | 41.2% | 12.5% | 8.5% | 31.2% | 6.6% | 37.0% | 12.8% | 8.8% | 28.0% | 13.4% | |

| 0.3 | 43.0% | 9.5% | 8.1% | 32.5% | 6.9% | 37.5% | 11.1% | 8.8% | 27.4% | 15.2% | |

| 0.4 | 42.0% | 7.9% | 7.8% | 32.3% | 10.0% | 41.2% | 11.2% | 8.2% | 26.0% | 13.4% | |

| 0.5 | 43.7% | 7.7% | 8.9% | 31.5% | 8.2% | 38.6% | 10.7% | 9.2% | 26.7% | 14.8% | |

| 0.6 | 45.1% | 7.8% | 7.9% | 27.7% | 11.5% | 40.5% | 11.3% | 8.7% | 23.9% | 15.6% | |

| 0.7 | 44.9% | 6.8% | 9.4% | 27.6% | 11.3% | 41.6% | 11.0% | 6.7% | 22.6% | 18.1% | |

| 0.8 | 47.1% | 8.5% | 8.7% | 18.7% | 17.0% | 42.4% | 9.2% | 8.4% | 19.4% | 20.6% | |

| 0.9 | 57.1% | 5.4% | 7.3% | 7.1% | 23.1% | 44.9% | 8.4% | 8.9% | 11.2% | 26.6% | |

| Loss to CSA | |||||||||||

| 0.1 | NA | 74.4% | 82.9% | 55.8% | 75.9% | NA | 73.8% | 84.4% | 61.2% | 70.0% | |

| 0.2 | NA | 75.5% | 83.2% | 59.4% | 79.0% | NA | 73.1% | 83.3% | 60.4% | 70.8% | |

| 0.3 | NA | 79.7% | 84.0% | 59.8% | 80.3% | NA | 76.3% | 83.8% | 58.7% | 69.9% | |

| 0.4 | NA | 80.8% | 84.2% | 57.2% | 76.3% | NA | 76.2% | 83.9% | 62.5% | 69.7% | |

| 0.5 | NA | 82.6% | 84.6% | 58.9% | 77.4% | NA | 75.0% | 82.6% | 60.7% | 68.8% | |

| 0.6 | NA | 81.8% | 84.6% | 60.7% | 74.6% | NA | 78.9% | 83.5% | 63.5% | 70.2% | |

| 0.7 | NA | 83.3% | 83.6% | 62.4% | 75.8% | NA | 80.5% | 86.9% | 62.4% | 66.9% | |

| 0.8 | NA | 83.1% | 84.8% | 67.9% | 74.5% | NA | 81.5% | 83.9% | 65.8% | 66.8% | |

| 0.9 | NA | 88.3% | 88.5% | 83.7% | 72.0% | NA | 84.1% | 85.0% | 76.3% | 64.8% | |

|

|

|

|

| CSA | JMA | L1QR | BAG | L2QR | CSA | JMA | L1QR | BAG | L2QR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Average FPE | |||||||||||

| 0.1 | 0.192 | 0.211 | 0.219 | 0.197 | 0.225 | 0.182 | 0.189 | 0.194 | 0.188 | 0.196 | |

| (0.029) | (0.036) | (0.040) | (0.023) | (0.046) | (0.019) | (0.021) | (0.025) | (0.020) | (0.026) | ||

| 0.2 | 0.300 | 0.320 | 0.315 | 0.307 | 0.331 | 0.287 | 0.298 | 0.299 | 0.296 | 0.296 | |

| (0.038) | (0.044) | (0.039) | (0.029) | (0.053) | (0.024) | (0.027) | (0.028) | (0.026) | (0.030) | ||

| 0.3 | 0.371 | 0.392 | 0.379 | 0.378 | 0.393 | 0.353 | 0.364 | 0.365 | 0.366 | 0.361 | |

| (0.038) | (0.043) | (0.037) | (0.033) | (0.051) | (0.029) | (0.032) | (0.031) | (0.030) | (0.032) | ||

| 0.4 | 0.409 | 0.432 | 0.413 | 0.419 | 0.428 | 0.394 | 0.406 | 0.405 | 0.405 | 0.397 | |

| (0.040) | (0.044) | (0.036) | (0.035) | (0.053) | (0.031) | (0.034) | (0.033) | (0.032) | (0.032) | ||

| 0.5 | 0.422 | 0.445 | 0.425 | 0.432 | 0.441 | 0.405 | 0.418 | 0.416 | 0.419 | 0.409 | |

| (0.042) | (0.046) | (0.035) | (0.035) | (0.053) | (0.032) | (0.034) | (0.033) | (0.032) | (0.032) | ||

| 0.6 | 0.410 | 0.432 | 0.414 | 0.419 | 0.433 | 0.393 | 0.405 | 0.404 | 0.406 | 0.400 | |

| (0.042) | (0.045) | (0.037) | (0.035) | (0.053) | (0.032) | (0.033) | (0.033) | (0.031) | (0.032) | ||

| 0.7 | 0.369 | 0.391 | 0.375 | 0.378 | 0.401 | 0.354 | 0.367 | 0.366 | 0.366 | 0.365 | |

| (0.041) | (0.045) | (0.036) | (0.033) | (0.053) | (0.029) | (0.031) | (0.031) | (0.029) | (0.031) | ||

| 0.8 | 0.300 | 0.320 | 0.310 | 0.307 | 0.334 | 0.286 | 0.297 | 0.298 | 0.296 | 0.300 | |

| (0.036) | (0.043) | (0.035) | (0.030) | (0.052) | (0.025) | (0.027) | (0.027) | (0.026) | (0.029) | ||

| 0.9 | 0.191 | 0.209 | 0.212 | 0.197 | 0.231 | 0.181 | 0.190 | 0.195 | 0.188 | 0.199 | |

| (0.029) | (0.034) | (0.036) | (0.024) | (0.047) | (0.019) | (0.022) | (0.025) | (0.020) | (0.027) | ||

| Winning Ratio | |||||||||||

| 0.1 | 43.7% | 7.7% | 8.9% | 31.5% | 8.2% | 38.6% | 10.7% | 9.2% | 26.7% | 14.8% | |

| 0.2 | 41.9% | 7.1% | 11.9% | 25.0% | 14.1% | 38.5% | 10.2% | 7.8% | 18.7% | 24.8% | |

| 0.3 | 37.0% | 6.0% | 13.9% | 23.3% | 19.8% | 37.0% | 10.3% | 8.7% | 15.2% | 28.8% | |

| 0.4 | 34.0% | 5.0% | 15.7% | 22.0% | 23.3% | 35.9% | 7.8% | 8.3% | 12.3% | 35.7% | |

| 0.5 | 35.7% | 5.9% | 16.3% | 18.1% | 24.0% | 38.3% | 8.8% | 7.2% | 13.5% | 32.2% | |

| 0.6 | 36.5% | 6.6% | 15.2% | 23.9% | 17.8% | 38.3% | 8.4% | 8.0% | 15.6% | 29.7% | |

| 0.7 | 38.1% | 8.1% | 14.7% | 25.9% | 13.2% | 42.3% | 8.5% | 7.3% | 18.5% | 23.4% | |

| 0.8 | 41.0% | 7.2% | 11.6% | 28.1% | 12.1% | 40.5% | 9.7% | 8.0% | 23.2% | 18.6% | |

| 0.9 | 43.3% | 8.6% | 9.6% | 30.7% | 7.8% | 41.5% | 11.6% | 7.6% | 26.5% | 12.8% | |

| Loss to CSA | |||||||||||

| 0.1 | NA | 82.6% | 84.6% | 58.9% | 77.4% | NA | 75.0% | 82.6% | 60.7% | 68.8% | |

| 0.2 | NA | 82.1% | 78.0% | 63.3% | 71.6% | NA | 78.3% | 83.2% | 62.5% | 61.6% | |

| 0.3 | NA | 81.6% | 70.8% | 59.4% | 64.0% | NA | 79.9% | 83.9% | 63.2% | 58.4% | |

| 0.4 | NA | 81.4% | 65.7% | 58.2% | 59.4% | NA | 81.9% | 80.0% | 62.9% | 53.0% | |

| 0.5 | NA | 80.7% | 65.6% | 61.1% | 62.1% | NA | 81.9% | 81.8% | 65.6% | 55.3% | |

| 0.6 | NA | 80.1% | 67.9% | 59.8% | 66.9% | NA | 80.2% | 80.5% | 63.1% | 56.9% | |

| 0.7 | NA | 78.9% | 71.4% | 60.9% | 71.1% | NA | 82.5% | 84.1% | 64.4% | 62.3% | |

| 0.8 | NA | 82.6% | 74.3% | 60.1% | 72.5% | NA | 81.5% | 82.1% | 63.4% | 65.3% | |

| 0.9 | NA | 80.1% | 81.6% | 61.2% | 81.0% | NA | 77.1% | 85.2% | 62.2% | 73.1% | |

| CSA | JMA | L1QR | BAG | L2QR | CSA | JMA | L1QR | BAG | L2QR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Average FPE | |||||||||||

| 0.0 | 0.493 | 0.488 | 0.503 | 0.516 | 0.530 | 0.449 | 0.447 | 0.455 | 0.484 | 0.458 | |

| (0.047) | (0.050) | (0.052) | (0.042) | (0.065) | (0.037) | (0.036) | (0.037) | (0.038) | (0.038) | ||

| 0.1 | 0.484 | 0.506 | 0.507 | 0.498 | 0.528 | 0.446 | 0.459 | 0.461 | 0.470 | 0.456 | |

| (0.046) | (0.049) | (0.049) | (0.040) | (0.060) | (0.036) | (0.038) | (0.037) | (0.037) | (0.038) | ||

| 0.2 | 0.461 | 0.490 | 0.487 | 0.474 | 0.500 | 0.429 | 0.445 | 0.447 | 0.446 | 0.442 | |

| (0.045) | (0.049) | (0.045) | (0.039) | (0.053) | (0.034) | (0.036) | (0.037) | (0.035) | (0.036) | ||

| 0.3 | 0.448 | 0.479 | 0.473 | 0.459 | 0.487 | 0.420 | 0.438 | 0.440 | 0.434 | 0.432 | |

| (0.044) | (0.049) | (0.042) | (0.037) | (0.054) | (0.034) | (0.035) | (0.036) | (0.032) | (0.035) | ||

| 0.4 | 0.440 | 0.471 | 0.464 | 0.449 | 0.474 | 0.418 | 0.434 | 0.437 | 0.427 | 0.429 | |

| (0.042) | (0.046) | (0.042) | (0.036) | (0.052) | (0.032) | (0.034) | (0.034) | (0.032) | (0.034) | ||

| 0.5 | 0.433 | 0.464 | 0.457 | 0.440 | 0.464 | 0.405 | 0.418 | 0.416 | 0.424 | 0.426 | |

| (0.043) | (0.047) | (0.042) | (0.035) | (0.053) | (0.032) | (0.034) | (0.033) | (0.033) | (0.035) | ||

| 0.6 | 0.428 | 0.458 | 0.450 | 0.435 | 0.457 | 0.411 | 0.428 | 0.430 | 0.420 | 0.420 | |

| (0.042) | (0.047) | (0.041) | (0.033) | (0.053) | (0.032) | (0.034) | (0.034) | (0.032) | (0.034) | ||

| 0.7 | 0.426 | 0.454 | 0.442 | 0.433 | 0.453 | 0.409 | 0.425 | 0.427 | 0.418 | 0.418 | |

| (0.041) | (0.046) | (0.038) | (0.034) | (0.053) | (0.033) | (0.033) | (0.034) | (0.032) | (0.033) | ||

| 0.8 | 0.423 | 0.449 | 0.435 | 0.430 | 0.443 | 0.408 | 0.423 | 0.424 | 0.420 | 0.414 | |

| (0.040) | (0.046) | (0.038) | (0.034) | (0.052) | (0.031) | (0.034) | (0.033) | (0.033) | (0.034) | ||

| 0.9 | 0.422 | 0.445 | 0.425 | 0.432 | 0.441 | 0.405 | 0.418 | 0.416 | 0.419 | 0.409 | |

| (0.042) | (0.046) | (0.035) | (0.035) | (0.053) | (0.032) | (0.034) | (0.033) | (0.032) | (0.032) | ||

| Winning Ratio | |||||||||||

| 0.0 | 20.2% | 33.9% | 14.3% | 15.6% | 16.0% | 23.0% | 31.1% | 8.7% | 6.7% | 30.5% | |

| 0.1 | 38.4% | 11.9% | 10.5% | 26.6% | 12.6% | 40.0% | 11.5% | 6.4% | 11.6% | 30.5% | |

| 0.2 | 44.3% | 7.7% | 7.9% | 28.4% | 11.7% | 43.4% | 9.1% | 6.9% | 16.2% | 24.4% | |

| 0.3 | 45.4% | 6.4% | 6.5% | 29.4% | 12.3% | 44.5% | 7.1% | 5.4% | 19.1% | 23.9% | |

| 0.4 | 46.0% | 6.6% | 6.2% | 28.6% | 12.6% | 43.4% | 8.1% | 5.4% | 21.2% | 21.9% | |

| 0.5 | 42.5% | 5.3% | 7.1% | 31.7% | 13.4% | 46.6% | 10.2% | 8.6% | 18.3% | 16.3% | |

| 0.6 | 44.4% | 4.8% | 6.3% | 27.1% | 17.4% | 43.7% | 5.8% | 4.2% | 21.4% | 24.9% | |

| 0.7 | 41.1% | 6.8% | 7.7% | 27.0% | 17.4% | 44.5% | 5.7% | 3.3% | 20.1% | 26.4% | |

| 0.8 | 38.7% | 6.7% | 10.3% | 22.3% | 22.0% | 38.7% | 7.9% | 4.3% | 17.5% | 31.6% | |

| 0.9 | 35.8% | 5.9% | 16.3% | 18.0% | 24.0% | 38.5% | 8.7% | 7.2% | 13.5% | 32.1% | |

| Loss to CSA | |||||||||||

| 0.0 | NA | 40.4% | 63.0% | 63.9% | 68.3% | NA | 44.0% | 67.7% | 73.5% | 58.0% | |

| 0.1 | NA | 73.7% | 77.0% | 61.5% | 73.7% | NA | 76.6% | 82.7% | 70.1% | 59.0% | |

| 0.2 | NA | 79.1% | 81.0% | 61.3% | 73.9% | NA | 81.4% | 86.5% | 65.7% | 62.9% | |

| 0.3 | NA | 83.8% | 82.9% | 58.8% | 73.2% | NA | 84.9% | 88.7% | 63.3% | 61.7% | |

| 0.4 | NA | 83.9% | 82.6% | 59.5% | 72.1% | NA | 82.6% | 87.9% | 61.4% | 61.7% | |

| 0.5 | NA | 87.1% | 82.5% | 55.8% | 70.2% | NA | 81.9% | 81.8% | 67.3% | 70.2% | |

| 0.6 | NA | 85.7% | 82.7% | 58.4% | 68.6% | NA | 85.3% | 88.6% | 59.3% | 59.1% | |

| 0.7 | NA | 84.3% | 79.1% | 57.4% | 67.7% | NA | 85.2% | 88.8% | 58.8% | 58.9% | |

| 0.8 | NA | 81.3% | 74.5% | 59.3% | 63.1% | NA | 83.3% | 87.8% | 61.7% | 53.9% | |

| 0.9 | NA | 80.7% | 65.6% | 61.6% | 62.1% | NA | 81.9% | 81.8% | 65.6% | 55.4% | |

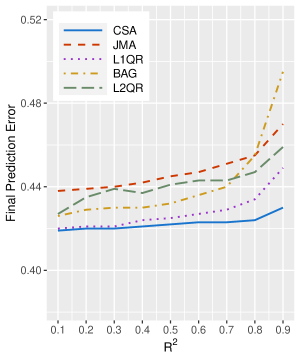

Figures 1–3 and Tables 1–4 summarize the simulation results over all designs. Overall, the performance of CSA compared to the alternative is quite satisfactory. We first direct our attention to Figure 1 and Tables 1–2. In these simulation designs, we vary over while setting . We consider two quantiles, and , respectively. From the four graphs in Figure 1, we confirm that CSA outperforms the alternative uniformly over ’s in terms of FPE in both quantiles. The prediction performance of CSA is better when the sample size is small, , and the gap decreases as the sample size increases to . At , L1QR performs the second when but L2QR does the second when . Thus, the performance order next to CSA is not stable. AT , BAG performs the second overall but it is deteriorated when is very high, e.g. . We also note that the performance of CSA is relatively stable over while that of the alternative increases steeply for larger when . The same results are confirmed in Tables 1–2. CSA shows the highest winning ratios over all designs except and , where that of L2QR is slightly higher. When we conduct the binary comparison (loss to CSA), all methods lose more than 50% to CSA over all designs and more than 80% in some designs. Therefore, we conclude that both the winning ratio and the loss to CSA are more favorable to CSA in this set of simulation designs.

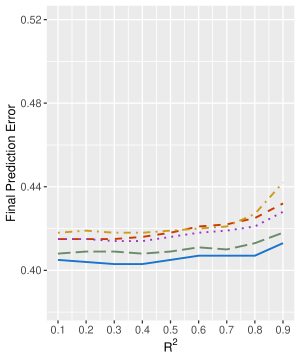

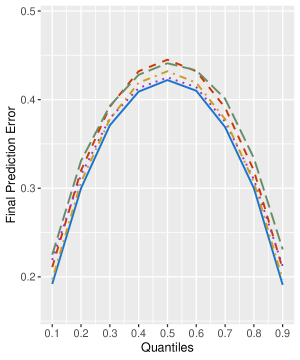

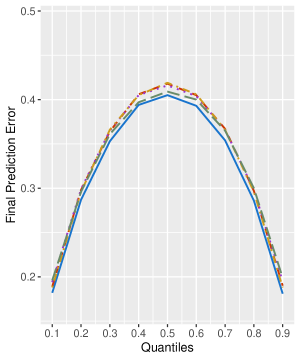

In the next simulation, we study the performance over a wider range of quantiles. We vary the quantile while setting and . The results are summarized in Figure 2 and Table 3. In Figure 2, CSA outperforms the alternative uniformly over all quantiles in both sample sizes followed by BAG and L2QR. Again, the gap decreases as the sample size increases. It is also interesting that all estimators predict better at the tail distributions and they show the largest prediction errors at the median. The winning ratio and the loss to CSA in Table 3 are also satisfactory.

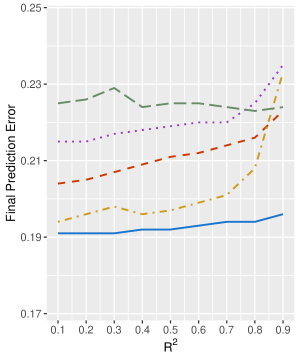

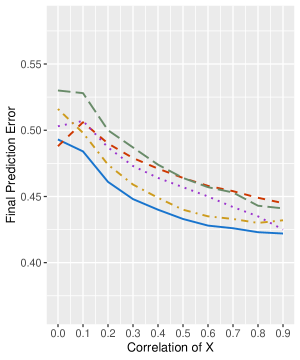

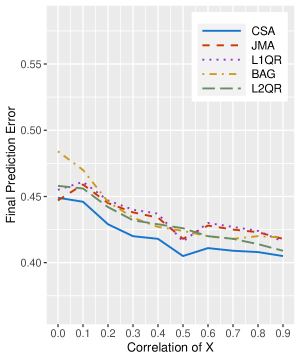

Third, we check the performance over different levels of dependency among the predictors. We vary while setting and . Since are generated from the multivariate normal distribution, they are independent when . Figure 3 reveals an interesting point. CSA performs better than the alternative when there exists any correlation between the predictors, i.e. . Recall that most simulation studies in the literature consider independent predictors. As we can see from the empirical applications in the next section, however, the predictors are usually correlated with each other. Therefore, it is promising that CSA performs better when there is any correlation among predictors. Elliott, Gargano, and Timmermann (2013) also report in the conditional mean prediction settings that the CSA approach performs better when predictors are correlated with each other. In Table 4, both the winning ratio and the loss to CSA statistics improve dramatically when is away from zero, where JMA performs the best.

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.415 | 0.424 | 0.419 | 0.430 | 0.419 | |

| (0.033) | (0.036) | (0.034) | (0.036) | (0.035) | |

| 0.420 | 0.443 | 0.424 | 0.426 | 0.427 | |

| (0.039) | (0.044) | (0.034) | (0.035) | (0.047) | |

| Winning Ratio | |||||

| 28.5% | 11.1% | 13.2% | 12.5% | 34.7% | |

| 32.7% | 5.4% | 11.1% | 21.7% | 29.1% | |

| Loss to CSA | |||||

| NA | 73.6% | 66.2% | 62.7% | 53.7% | |

| NA | 81.8% | 70.1% | 56.7% | 54.4% | |

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.406 | 0.412 | 0.411 | 0.422 | 0.406 | |

| (0.032) | (0.033) | (0.032) | (0.034) | (0.031) | |

| 0.407 | 0.419 | 0.419 | 0.417 | 0.408 | |

| (0.032) | (0.034) | (0.033) | (0.032) | (0.032) | |

| Winning Ratio | |||||

| 30.6% | 10.8% | 8.6% | 8.7% | 41.3% | |

| 35.2% | 9.2% | 6.5% | 13.0% | 36.1% | |

| Loss to CSA | |||||

| NA | 71.6% | 72.7% | 65.0% | 49.0% | |

| NA | 77.9% | 82.9% | 61.6% | 50.9% | |

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.414 | 0.426 | 0.419 | 0.429 | 0.415 | |

| (0.033) | (0.036) | (0.034) | (0.035) | (0.034) | |

| 0.418 | 0.443 | 0.422 | 0.429 | 0.429 | |

| (0.040) | (0.046) | (0.036) | (0.034) | (0.049) | |

| Winning Ratio | |||||

| 30.3% | 7.0% | 12.6% | 12.4% | 37.7% | |

| 33.1% | 4.7% | 14.5% | 16.9% | 30.8% | |

| Loss to CSA | |||||

| NA | 80.6% | 68.0% | 61.6% | 50.6% | |

| NA | 85.0% | 65.8% | 60.2% | 56.0% | |

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.406 | 0.414 | 0.411 | 0.422 | 0.406 | |

| (0.031) | (0.032) | (0.032) | (0.032) | (0.032) | |

| 0.406 | 0.419 | 0.416 | 0.420 | 0.410 | |

| (0.033) | (0.034) | (0.034) | (0.033) | (0.032) | |

| Winning Ratio | |||||

| 31.2% | 6.2% | 11.4% | 8.4% | 42.8% | |

| 40.3% | 6.6% | 8.8% | 11.9% | 32.4% | |

| Loss to CSA | |||||

| NA | 78.3% | 73.7% | 67.4% | 47.8% | |

| NA | 82.2% | 81.8% | 65.3% | 56.3% | |

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.422 | 0.422 | 0.420 | 0.430 | 0.421 | |

| (0.034) | (0.036) | (0.035) | (0.036) | (0.035) | |

| 0.437 | 0.442 | 0.431 | 0.430 | 0.439 | |

| (0.042) | (0.046) | (0.038) | (0.035) | (0.049) | |

| Winning Ratio | |||||

| 13.5% | 20.9% | 20.3% | 12.7% | 32.6% | |

| 14.7% | 16.9% | 18.3% | 25.6% | 24.5% | |

| Loss to CSA | |||||

| NA | 47.2% | 41.9% | 57.2% | 50.4% | |

| NA | 52.3% | 44.9% | 45.5% | 48.8% | |

| CSA | JMA | L1QR | BAG | L2QR | |

| Average FPE | |||||

| 0.414 | 0.410 | 0.411 | 0.423 | 0.411 | |

| (0.032) | (0.032) | (0.032) | (0.032) | (0.031) | |

| 0.418 | 0.416 | 0.419 | 0.422 | 0.415 | |

| (0.033) | (0.034) | (0.034) | (0.031) | (0.032) | |

| Winning Ratio | |||||

| 13.3% | 22.8% | 15.5% | 12.3% | 36.1% | |

| 13.9% | 24.9% | 12.6% | 17.4% | 31.2% | |

| Loss to CSA | |||||

| NA | 38.2% | 39.5% | 58.0% | 45.2% | |

| NA | 41.0% | 51.0% | 52.3% | 45.9% | |

We next consider the second category of simulation designs, where the candidate models include the true DGP. The new simulations are based on the following model:

where we observe all predictors in the sample. We consider when and when . Similar to the previous simulations, the population is controlled by . We set , , and . Instead of varying , , and , we consider three signal structures in this simulation:

| Decreasing signal : | |||

| Constant signal : | |||

| Sparse signal : |

Therefore, we consider 12 new DGPs in total.

Tables 5-7 summarize the simulation results. First of all, we take a look at the loss to CSA ratio in the second column (JMA) in these tables. Note that the loss ratio increases as increases over all different designs, which is expected by the theoretical results in Theorem 5. Second, CSA performs worse in the sparse signal models compared to the other two designs. As discussed under equation (10), this is expected from the theory in Section 3 since the sparse design generates many subsets with totally irrelevant predictors. Third, it is interesting that JMA does not particularly outperform in this setup, where the candidate models include the true one. Also, note that L1QR does not particularly outperform in the sparse signal model. In fact, L2QR performs well over all three signal designs. Given that L2QR is understudied in the literature, this would be an interesting topic for future research.

In sum, we confirm that CSA shows satisfactory finite sample properties via Monte Carlo simulation studies. Related to the forecast combination puzzle, we observe a similar phenomenon in quantile forecasting and confirm some theoretical predictions developed in Section 3.

5 Empirical Illustration

In this section, we investigate the performance of the proposed method with real data sets. Specifically, we revisit two empirical applications in Lu and Su (2015): (i) quantile forecast of excess stock returns; and (ii) quantile forecast of wages. Following the simulation studies in Section 4, we compare the performance of the complete subset averaging (CSA) method to the Jackknife Model Averaging (JMA), the -penalized quantile regression (L1QR), the bootstrap aggregating method (BAG), and the -penalized quantile regression (L2QR).

| CSA | JMA | L1QR | BAG | L2QR | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.05 | 48 | -0.071 (2) | -0.117 (4) | -0.088 (3) | 0.031 (1) | -4.331 (5) | 7.4 | 8 | ||

| 60 | -0.063 (3) | -0.125 (4) | -0.038 (2) | 0.009 (1) | -4.395 (5) | 8.1 | 8 | |||

| 72 | -0.001 (2) | -0.023 (4) | -0.005 (3) | 0.020 (1) | -3.955 (5) | 8.2 | 9 | |||

| 96 | 0.055 (1) | -0.020 (4) | -0.012 (3) | 0.027 (2) | -4.010 (5) | 8.1 | 9 | |||

| 120 | 0.104 (1) | 0.053 (2) | 0.028 (4) | 0.033 (3) | -3.655 (5) | 8.7 | 9 | |||

| 144 | 0.082 (1) | 0.045 (2) | 0.012 (4) | 0.019 (3) | -3.735 (5) | 9.1 | 9 | |||

| 180 | 0.039 (1) | 0.033 (2) | 0.023 (3) | -0.011 (4) | -2.311 (5) | 9.6 | 10 | |||

| 0.5 | 48 | 0.103 (1) | 0.076 (2) | -0.040 (4) | -0.016 (3) | -2.341 (5) | 9.8 | 10 | ||

| 60 | 0.089 (1) | 0.079 (2) | -0.036 (4) | -0.013 (3) | -2.078 (5) | 9.9 | 10 | |||

| 72 | 0.057 (2) | 0.067 (1) | -0.003 (3) | -0.009 (4) | -1.953 (5) | 10.0 | 10 | |||

| 96 | 0.049 (2) | 0.053 (1) | -0.013 (3) | -0.014 (4) | -2.206 (5) | 10.3 | 11 | |||

| 120 | 0.003 (2) | 0.013 (1) | 0.003 (3) | -0.011 (4) | -1.882 (5) | 10.5 | 11 | |||

| 144 | -0.012 (3) | -0.002 (1) | -0.006 (2) | -0.022 (4) | -1.648 (5) | 10.6 | 11 | |||

| 180 | 0.032 (2) | 0.034 (1) | 0.018 (3) | -0.012 (4) | -1.031 (5) | 10.5 | 11 |

-

•

Notes: The number in the parentheses denotes the performance ranking among the five different methods.

5.1 Stock Return

The same data set is composed of monthly observations of the US stock market from January 1950 to December 2005 (). The dependent variable is the excess stock return. We use the following twelve regressors: default yield spread, treasury bill rate, net equity expansion, term spread, dividend price ratio, earnings price ratio, long term yield, book-to-market ratio, inflation, return on equity, lagged dependent variable, and smoothed earnings price ratio. See Lu and Su (2015) and Campbell and Thompson (2007) for the details of the data set. Note that JMA needs to select the order of important regressors, but we do not need such a selection for CSA, BAG, L2QR. L1QR would select important regressors automatically by the -penalty.

We forecast the one-period-ahead excess stock returns at 0.5 and 0.05 quantiles using various fixed in-sample sizes, . The forecast performance is measured by the out-of-sample defined as

where the one-period-ahead -quantile prediction at time using the data from the past periods, and is the unconditional -quantile for the same periods. The out-of-sample measures the relative performance of a forecast method compared to the unconditional historical quantile. The higher values of imply better forecasting performance.

Table 8 summarizes the forecasting results. In addition to , we report the ranking of each forecasting method, the mean of , and the median of . The upper panel of Table 8 reports the results when . The of CSA is better than that of JMA uniformly over different sample sizes (). The gap between two ’s is substantial except . BAG performs well when is small. The performance of L2QR is not satisfactory over all in-sample sizes. We next turn our attention to the lower panel when . Again, CSA performs the best or second best except when . CSA performs better when is small while JMA does better when is larger. Overall, the gap between ’s is small when . As we have observed from the simulation studies, the performance of the two estimators becomes similar as the sample size increases in both panels. It is also noticeable that the selected of CSA increases as the sample size increases and that CSA selects relatively large across all and . Different from , BAG performs poorly when . L2QR also shows poor performance.

In sum, the performance of CSA is satisfactory in this forecasting exercise. It is quite stable over different in-sample sizes () and different quantiles in terms of the performance ranking. Among the alternative, BAG and JMA perform well in certain quantiles (0.05 and 05, respectively), but they do poorly when we apply them in different quantiles.

5.2 Wage

| CSA | JMA | L1QR | BAG | L2QR | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.05 | 50 | 0.066 (2) | -0.034 (3) | -0.035 (4) | 0.104 (1) | -0.139 (5) | 3.9 | 4 | ||

| 100 | 0.122 (2) | 0.073 (4) | 0.078 (3) | 0.133 (1) | 0.020 (5) | 5.5 | 6 | |||

| 150 | 0.138 (2) | 0.112 (4) | 0.113 (3) | 0.144 (1) | 0.076 (5) | 6.1 | 6 | |||

| 200 | 0.158 (1) | 0.125 (4) | 0.132 (3) | 0.154 (2) | 0.111 (5) | 6.6 | 7 | |||

| 0.5 | 50 | 0.252 (1) | 0.233 (3) | 0.198 (5) | 0.248 (2) | 0.212 (4) | 6.5 | 6 | ||

| 100 | 0.287 (1) | 0.276 (3) | 0.233 (5) | 0.285 (2) | 0.260 (4) | 7.7 | 8 | |||

| 150 | 0.302 (1) | 0.293 (3) | 0.253 (5) | 0.301 (2) | 0.290 (4) | 8.2 | 8 | |||

| 200 | 0.307 (2) | 0.302 (3) | 0.267 (5) | 0.312 (1) | 0.302 (4) | 8.4 | 9 |

-

•

Notes: The number in the parentheses denotes the performance ranking among the five different methods.

In this subsection we conduct the quantile forecast exercises using the Current Population Survey (CPS) data in 1975. The same data set is also used by Lu and Su (2015) and Hansen and Racine (2012) for quantile and mean forecast exercises, respectively. The sample size is and we use the logarithm of the average hourly wage as the dependent variable. We use the following ten regressors: professional occupation, years of education, years with current employer, female, service occupation, married, trade, SMSA, services, and clerk occupation.

We split the sample into the estimation sample randomly drawn observations and the evaluation sample of observations. The estimation sample size varies and and the random splitting is repeated 200 times for each . The out-of-sample is defined as

where is the -th conditional quantile predictor and is the unconditional -quantile estimate from the estimation sample. Again, measures the prediction performance relative to the unconditional quantile estimate.

Table 9 summarizes the exercise results.333s of JMA are different from the numbers reported in Table 5 in Lu and Su (2015) because they implemented the level of wage as a dependent variable which is supposed to be . We use in this empirical illustration. We confirm that CSA shows good and stable quantile prediction performance. In this application, BAG shows quite a similar performance to CSA. Similar to the stock return application, CSA performs better than BAG when and BAG does when . The prediction results of JMA, L1QR, and L2QR are worse than CSA and BAG. The performance gaps are larger when the sample size () is small and they narrow as increases. As predicted by the theory and also confirmed in the stock return application, the selected increases as increases.

6 Conclusion

In this paper, we propose a novel conditional quantile prediction method based on complete subset averaging of quantile regressions. We show the asymptotic properties of the estimator when the dimension of regressors diverges to infinity as the sample size increases. The size of the complete subset is chosen by the leave-one-out cross-validation method. We prove that the subset size chosen by this method is optimal in the sense that it is asymptotically equivalent to the infeasible optimal size minimizing the final prediction error. The prediction performance in the simulation studies and empirical applications is satisfactory.

We conclude with two potential extensions of the proposed method. First, we can think of a different approach in choosing the complete subset size. Recently, Hirano and Wright (ming) propose a Laplace cross-validation method, where the tuning parameter of interest is chosen by the pseudo-Bayesian posterior mean, and show that it works better than the standard cross-validation method when the risk function is asymmetric. It would be interesting to check how it performs in the CSA quantile prediction. Second, it will be useful if one can extend the results into the time-series data possibly including persistent regressors (e.g. Fan and Lee (2019)). We leave them for future research.

Appendix

In this appendix, we provide all necessary lemmas and technical proofs of the main text.

Lemma 1.

Let . Suppose that . Then, we can show the following rate conditions:

-

(i)

-

(ii)

-

(iii)

.

Proof of Lemma 1.

(i) Recall the dependency of on and . By construction, . Then, the result follows from .

(ii) Note that

(iii) Note that

It is enough to show that . Let . Then,

Therefore, and the desired result is established.

Lemma 2.

Suppose that (i) with , (ii) . Then,

Proof of Lemma 2.

The triangle inequality implies that

We first investigate :

We next turn our attention to . Let . Note that for some generic constant . Let . We have

Boole’s and Bernstein inequalities imply that

The convergence result follows from by Lemma 1 (i), by Lemma 1 (ii), and by Lemma 1 (iii).

Finally, we show that

Proof of Theorem 2

The proof is similar to Lu and Su (2015) except the last part that shows the convergence of the maximal inequality bound. Let for some large constant . Let . We also define

The same arguments in Lu and Su (2015) imply that, for any ,

The claim in (i) is established by showing that the following maximal inequality converges to zero:

We first derive the upper bound of it:

where . We apply similar arguments in the proof of Theorem 3.2 of Lu and Su (2015) to show that

where . Let and . Then, the above inequality for and the corrected version of Lemma 2.1 of Shibata (1981, 1982) imply that

For the last equality, note first that by Assumption 3(ii). The leading term becomes

where is a generic constant. The second line holds by the definition of , the third line holds by the fact that , the fifth line holds by Assumption 3(ii), and the last convergence result holds by 3(ii) and by taking some large .

Therefore, we establish the result in (i). Analogously, we can prove the result in (ii).

Proof of Theorem 3

Using the definition of and and the triangular inequality, we have

We first investigate :

The first inequality holds from the triangular inequality and the second one from the Cauchy-Schwartz inequality. The final inequality holds from the uniform convergence and boundedness assumptions, and Theorem 2 (ii) above. Similarly, we can show .

Proof of Theorem 4

It suffices to show that, with ,

| (12) |

We first expand the numerator by applying Knight’s identity repeatedly.

It is straightforward to derive all terms except . We need the following two results to get . Let be an expectation with respect to a random variable .

| (13) | ||||

| (14) | ||||

The identity (13) follows from the fact that does not depend on the -th observation. The second result (14) comes from

The second equality holds by the independence of the sample and the generic random variable .

We are now ready to prove (12). We first show that the denominator of (12) is uniformly bounded above zero and show the uniform convergence of .

Claim 1: . This results shows that the denominator of the LHS in (12) is bounded above zero. Let .

Claim 2: .

We first show that . Let and . Note that

We next show that and , respectively.

The last convergence result follows from the order conditions in Assumption 3.

We next turn our attention to :

The convergence results follow from Theorem 2, Lemma 2, and Assumption 3.

Claim 3: .

where

| and | |||

Since , we have

Thus, follows from the same arguments used for above.

We next investigate . We have

Claim 4: .

where

| and | |||

The proof of is similar to that of in Claim 2 and is omitted. Note that

The proof of is similar to that of in Claim 3 and is also omitted. It remains to show that . Note that

by the triangle inequality, , the Jensen’s inequality, for any real symmetric matrix .

Claim 5: .

by the triangle inequality, , and the similar arguments in the proof of .

Claim 6: . Since does not depend on , this result follows from the weak law of large numbers.

Proof of Theorem 5

(i) There exists between and such that

where is a Lagrange multiplier from the constraint optimization problem:

| (15) |

Note that the second equality above comes from the first order condition for and that the third equality holds by the normalization, for any weight . We investigate the upper bound of the quadratic term:

Since is an symmetric matrix, we can factorize it as , where is a diagonal matrix composed of the eigenvalues and is composed of the corresponding orthonormal eigenvectors . Note that

where denotes -norm. Therefore, we have

which establishes the desired result.

(ii) Using the similar arguments above, we have

where , , , and are all random objects in the second equality. The third inequality holds almost surely by the definition of . We establish the desired result by noting that .

Proof of Corollary 6

References

- Adrian et al. (2019) Adrian, T., N. Boyarchenko, and D. Giannone (2019). Vulnerable growth. American Economic Review 109(4), 1263–89.

- Ando and Li (2014) Ando, T. and K.-C. Li (2014). A model-averaging approach for high-dimensional regression. Journal of the American Statistical Association 109(505), 254–265.

- Angrist et al. (2006) Angrist, J., V. Chernozhukov, and I. Fernández-Val (2006). Quantile regression under misspecification, with an application to the US wage structure. Econometrica 74(2), 539–563.

- Belloni and Chernozhukov (2011) Belloni, A. and V. Chernozhukov (2011). -penalized quantile regression in high-dimensional sparse models. The Annals of Statistics 39(1), 82–130.

- Bhatia et al. (2019) Bhatia, K. T., G. A. Vecchi, T. R. Knutson, H. Murakami, J. Kossin, K. W. Dixon, and C. E. Whitlock (2019). Recent increases in tropical cyclone intensification rates. Nature communications 10(1), 1–9.

- Breiman (1996) Breiman, L. (1996). Bagging predictors. Machine Learning 24(2), 123–140.

- Buchinsky (1998) Buchinsky, M. (1998). The dynamics of changes in the female wage distribution in the USA: a quantile regression approach. Journal of Applied Econometrics 13(1), 1–30.

- Campbell and Thompson (2007) Campbell, J. Y. and S. B. Thompson (2007). Predicting excess stock returns out of sample: Can anything beat the historical average? The Review of Financial Studies 21(4), 1509–1531.

- Claeskens et al. (2016) Claeskens, G., J. R. Magnus, A. L. Vasnev, and W. Wang (2016). The forecast combination puzzle: A simple theoretical explanation. International Journal of Forecasting 32(3), 754–762.

- Clemen (1989) Clemen, R. T. (1989). Combining forecasts: A review and annotated bibliography. International Journal of Forecasting 5(4), 559–583.

- Donald and Newey (2001) Donald, S. G. and W. K. Newey (2001). Choosing the number of instruments. Econometrica 69(5), 1161–1191.

- Duffie and Pan (1997) Duffie, D. and J. Pan (1997). An overview of value at risk. Journal of Derivatives 4(3), 7–49.

- Elliott (2011) Elliott, G. (2011). Averaging and the optimal combination of forecasts. Manuscript, Department of Economics, UCSD.

- Elliott et al. (2013) Elliott, G., A. Gargano, and A. Timmermann (2013). Complete subset regressions. Journal of Econometrics 177(2), 357–373.

- Elliott et al. (2015) Elliott, G., A. Gargano, and A. Timmermann (2015). Complete subset regressions with large-dimensional sets of predictors. Journal of Economic Dynamics and Control 54, 86–110.

- Fan and Lee (2019) Fan, R. and J. H. Lee (2019). Predictive quantile regressions under persistence and conditional heteroskedasticity. Journal of Econometrics 213(1), 261–280.

- Fazekas and Klesov (2001) Fazekas, I. and O. Klesov (2001). A general approach to the strong law of large numbers. Theory of Probability & Its Applications 45(3), 436–449.

- Hansen (2007) Hansen, B. E. (2007). Least squares model averaging. Econometrica 75(4), 1175–1189.

- Hansen and Racine (2012) Hansen, B. E. and J. S. Racine (2012). Jackknife model averaging. Journal of Econometrics 167(1), 38–46.

- Hirano and Wright (ming) Hirano, K. and J. H. Wright (forthcoming). Analyzing cross-validation for forecasting with structural instability. Journal of Econometrics.

- Koenker (2005) Koenker, R. (2005). Quantile Regression. Econometric Society Monographs. Cambridge University Press.

- Koenker and Bassett (1978) Koenker, R. and G. Bassett (1978). Regression quantiles. Econometrica 46(1), 33–50.

- Komunjer (2013) Komunjer, I. (2013). Quantile prediction. In Handbook of Economic Forecasting, Volume 2, pp. 961–994. Elsevier.

- Kuersteiner and Okui (2010) Kuersteiner, G. and R. Okui (2010). Constructing optimal instruments by first-stage prediction averaging. Econometrica 78(2), 697–718.

- Lee (2016) Lee, J. H. (2016). Predictive quantile regression with persistent covariates: IVX-QR approach. Journal of Econometrics 192(1), 105–118.

- Lee and Shin (2018) Lee, S. and Y. Shin (2018). Complete subset averaging with many instruments. arXiv preprint arXiv:1811.08083.

- Li (1987) Li, K.-C. (1987). Asymptotic optimality for , , cross-validation and generalized cross-validation: discrete index set. The Annals of Statistics, 958–975.

- Lu and Su (2015) Lu, X. and L. Su (2015). Jackknife model averaging for quantile regressions. Journal of Econometrics 188(1), 40–58.

- Meinshausen (2006) Meinshausen, N. (2006). Quantile regression forests. Journal of Machine Learning Research 7(Jun), 983–999.

- Meligkotsidou et al. (2019) Meligkotsidou, L., E. Panopoulou, I. D. Vrontos, and S. D. Vrontos (2019). Quantile forecast combinations in realised volatility prediction. Journal of the Operational Research Society 70(10), 1720–1733.

- Meligkotsidou et al. (2021) Meligkotsidou, L., E. Panopoulou, I. D. Vrontos, and S. D. Vrontos (2021). Out-of-sample equity premium prediction: A complete subset quantile regression approach. The European Journal of Finance 27(1-2), 110–135.

- Phillips (2015) Phillips, P. C. (2015). Halbert White Jr. memorial JFEC lecture: Pitfalls and possibilities in predictive regression. Journal of Financial Econometrics 13(3), 521–555.

- Portnoy (1984) Portnoy, S. (1984). Asymptotic behavior of -estimators of regression parameters when is large. i. consistency. The Annals of Statistics 12(4), 1298–1309.

- Portnoy (1985) Portnoy, S. (1985). Asymptotic behavior of m estimators of p regression parameters when p2/n is large; ii. normal approximation. The Annals of Statistics, 1403–1417.

- Rapach et al. (2010) Rapach, D. E., J. K. Strauss, and G. Zhou (2010). Out-of-sample equity premium prediction: Combination forecasts and links to the real economy. The Review of Financial Studies 23(2), 821–862.

- Rice (1984) Rice, J. (1984, 12). Bandwidth choice for nonparametric regression. The Annals of Statistics 12(4), 1215–1230.

- Shibata (1981) Shibata, R. (1981). An optimal selection of regression variables. Biometrika 68(1), 45–54.

- Shibata (1982) Shibata, R. (1982). Amendments and corrections: An optimal selection of regression variables. Biometrika 69(2), 492–492.

- Smith and Wallis (2009) Smith, J. and K. F. Wallis (2009). A simple explanation of the forecast combination puzzle. Oxford Bulletin of Economics and Statistics 71(3), 331–355.

- Stock and Watson (2004) Stock, J. H. and M. W. Watson (2004). Combination forecasts of output growth in a seven-country data set. Journal of Forecasting 23(6), 405–430.