Exact asymptotics of component-wise extrema of two-dimensional Brownian motion

Abstract: We derive the exact asymptotics of

where is a correlated two-dimensional Brownian motion with correlation and . It appears that the play between and leads to several types of asymptotics. Although the exponent in the asymptotics as a function of is continuous, one can observe different types of prefactor functions depending on the range of , which constitute a phase-type transition phenomena.

Key Words: Two-dimensional Brownian motion; exact asymptotics; component-wise extrema; quadratic programming problem; generalised Pickands-Piterbarg constants.

AMS Classification: Primary 60G15; secondary 60G70

1. Introduction

Distributional properties of component-wise extrema of stochastic processes attract growing interest in recent literature. On one side, it is a natural object of interest in the extreme value theory of random fields. On the other side, strong motivation to investigate component-wise extrema stems for example from multivariate stochastic models applied to modern multidimensional risk theory, financial mathematics or advanced communication networks, to name some of the applied-probability areas.

We consider a standard correlated Brownian motion with constant correlation , and let be its two parameter extension, where

The aim of this paper is to find exact asymptotics of

| (1) |

where with , .

Due to its importance in, e.g., quantitative finance or ruin theory, the component-wise maxima

have been studied extensively; see, e.g., [13, 10, 17, 23, 22]. In particular, some formulas for the joint distribution of are known. Unfortunately, they are in the form of infinite-sums of integrals of some special functions, which makes them of limited use in drawing out asymptotic properties of as .

Interestingly, in [13] it was worked out a formula for joint survival function of , where is an independent exponential random variable with parameter . Vector as well as have bivariate exponential distribution (BVE) in the sense of the terminology of Kou and Zhong [13], that is: (i) it has exponential marginals and (ii) it is absolute continuous with respect to two-dimensional Lebesgue measure. The later property for follows from Theorem 7.1 in [2] combined with the fact that , see also related Lemma 4.4 in [6]. We remark that requirement (ii) implies that does not belong to the classical examples of Marshall-Olkin-type BVE; see [16]. Since there are no results in the literature on qualitative properties of our BVE distribution, as a by-product of the results of this contribution, we analyze the dependence structure of and in an asymptotical sense of Resnick [21]; see Remarks 2.2 (b) and Remarks 2.4 (b) for more details. We refer also to a related work of Rogers and Shepp [22] who considered correlation structure of for two Brownian motions without drift.

A need to consider the joint survival function for appeared also in Lieshout and Mandjes [14] who considered two parallel queues sharing the same Brownian input (which is the case of ) and also a Brownian tandem queue. We refer to [15] for further discussions on Gaussian-related queueing models and to [3, 5] for the analysis of a related simultaneous ruin problem for the correlated Brownian motion model.

It is worth noting that in recent papers [25, 11], the component-wise maxima in discrete models defined by

with independent and identically distributed Gaussian random vectors, were discussed.

The first step in understanding the asymptotics of (1) is to find its logarithmic asymptotics. This was done recently in [7], in an insurance context, where was interpreted as the probability of component-wise ruin. More precisely, by an application of Theorem 1 in [8]

| (2) |

where

| (3) |

and is the inverse matrix of with and . The main contribution of [7] includes the detailed analysis of the two-layer minimisation problem involved in , which results in an explicit logarithmic asymptotics of ; see also Proposition 3.1 below.

In order to get the exact asymptotics of as , we employ a modification of the double-sum technique, accommodated to the analysis of multivariate extremes investigated in this contribution; see Theorems 2.1 and 2.3, which constitute the main results of this paper. It appears that the play between and leads to several types of asymptotics. Although in [7] it was noticed, that the exponent in the asymptotics as a function of , called therein an adjustment coefficient, is continuous, one can observe different types of prefactor functions depending on the range of . This phase-type phenomena has no intuitive explanations.

In the rest of the paper we assume that and without loss of generality suppose that . Note that for ,

and, for ,

| (4) |

To work out the case , one can use a result from [24], to show that

| (5) |

where is the indicator function.

The rest of this paper is organised as follows. In Section 2, we present the exact asymptotics of , given in Theorems 2.1, 2.3. Section 3 recalls the explicit expressions for and derived in [7]. The main lines of proofs are displayed in Section 4 and Section 5, respectively, followed by the Appendix consisting of technical calculations.

We conclude this section by showing some notation and conventions used in this work. All vectors here are -dimensional column vectors written in bold letters. For instance , with ⊤ the transpose sign. Operations with vectors are meant component-wise, so for any . For any set , any and any denote

Next, let us briefly mention the following standard notation for two given positive functions and . We write or simply , if (). Further, write if , and write if

2. Main results

In this section we present the exact asymptotics of , for which we need some additional notation. First, define

| (6) |

These are key points, based on which we consider different scenarios of . Next, let

| (9) |

with

| (10) |

Moreover, denote, for any fixed ,

| (11) |

and define

where the finiteness can be proved by following a standard argument in proving the finiteness of Pickands and Piterbarg type constants; see, e.g., [18] (or Lemma 4.2 in [3]). Interestingly, a new Pickands-Piterbarg constant

appears in the scenario ; the existence, finiteness and positiveness of this constant are proved in Theorem 2.1 below.

We split the statement of the main results on the exact asymptotics into two scenarios: and respectively.

Theorem 2.1.

Suppose that . We have, as

where

Remarks 2.2.

(a). It turns out that the special scenario is of different nature than the scenarios analyzed in Theorem 2.1. Note that in this case we have in Lemma A.1, which implies that around its optimizing point function defined in Section 3 takes different form than for other scenarios. This makes its analysis go out of the approach that works for the other scenarios. In Section 4.4, following the same lines of reasoning as given in the proof of case in Theorem 2.1, we find the following bounds for the case of

| (14) |

(b). It follows from Theorem 2.1 and (5) that for any

According to the terminology from [21], this means that is asymptotically independent of . Similarly, one can see that is also asymptotically independent of (note that the notion of asymptotically independence is not symmetric). Furthermore, for , we have that is asymptotically independent of , but is asymptotically dependent of (equivalent to) .

Next we give the result for the case where . In this case, we have and

Theorem 2.3.

Suppose that . We have, as

where

Remarks 2.4.

(a). Note that comparing scenario of Theorem 2.3 with of Theorem 2.1, there is an additional 2 appearing in the asymptotics. The reason for this is that there are two equally important minimizers of in the case of .

(b). For any , we have that and are mutually asymptotically independent.

3. Analysis of the two-layer minimization problem

In this section, for completeness and for reference we recall some notation and the result on the two-layer minimization problem (3) derived in [7]. Recall that with

We define for the following functions:

Since appears in the above formula, we shall consider a partition of the quadrant , namely

| (17) |

For convenience we denote and . Hereafter, all sets are defined on , so will be omitted.

Note that can be represented in the following two different forms:

| (20) | |||||

| (23) |

Denote further

| (24) |

The following result gives a full analysis of the two-layer minimization problem (3), which is crucial for our derivation of the exact asymptotics of . We refer to [7] for its detailed proof.

Proposition 3.1.

-

(i).

Suppose that .

For we havewhere, is the unique minimizer of .

For we havewhere are the only two minimizers of .

-

(ii).

Suppose that . We have

where is the unique minimizer of .

- (iii).

-

(iv).

Suppose that . We have

where is the unique minimizer of .

-

(v).

Suppose that . We have , and

where the minimum of is attained at , with , and is the unique minimizer of .

-

(vi).

Suppose that . We have

where the minimum of is attained when .

4. Proof of Theorem 2.1

The proof of Theorem 2.1 will be presented in the order of cases (i) , (ii) , (iii) , (iv) in the following subsections.

Note that by self-similarity

| (25) |

and recall the notation for the optimizer points as introduced in Proposition 3.1.

4.1. (i) Scenario .

4.1.1. Splitting on subregions

We first split the region into the following two parts:

where is some small constant which can be identified later on. It follows from (25) that

| (26) | |||

Furthermore, we have, for all large ,

| (27) |

where

with

Next, we further split the rectangle into smaller rectangles. To this end, we denote, for any fixed

where , (we denote by the smallest integer that is larger than ). Define

and

We have from the generalized Bonferroni’s inequality (see Lemma A.2 in Appendix Proof of Lemma A.1)

| (28) |

where

4.1.2. Upper bounds and estimates

In what follows, we shall derive upper bounds for in Lemma 4.1, the exact asymptotics of in Lemma 4.2 and asymptotic behaviour for in Lemma 4.3. The proofs of the lemmas are displayed in Appendix Proof of Lemma A.1. Recall that we assume .

Lemma 4.1.

For any chosen small we have, for all large ,

hold for some constants not depending on .

Below we discuss the asymptotics of . Define

Lemma 4.2.

We have, as ,

The last lemma is concerned with the asymptotic behaviour of .

Lemma 4.3.

It holds that

4.1.3. Asymptotics of

4.2. (ii) Scenario

4.2.1. Splitting on subregions

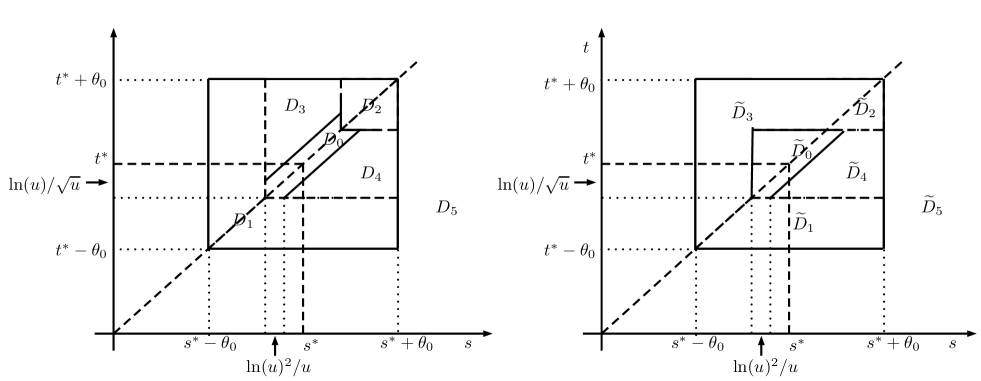

We split the region into five pieces as shown in Figure 1 (left). Namely, with some small and large, let

Clearly, we have the following bounds

| (30) |

where

Next, we consider a further partition of . Recall given in (11). Denote, for any and

where , . Define further

and

Thus, it follows from the Bonferroni’s inequality that

| (32) |

where

4.2.2. Upper bounds and estimates

In what follows, we shall derive upper bounds for in Lemma 4.4, the exact asymptotics of in Lemma 4.5 and asymptotic behaviour for in Lemma 4.7. The proofs of the lemmas are displayed in Appendix Proof of Lemma A.1.

Lemma 4.4.

For any chosen small we have, for all large ,

hold for some constants not depending on .

Lemma 4.5.

For any we have, as ,

Below, we show, for any fixed , the sub-additivity property of as a function of .

Lemma 4.6.

Let be fixed, we have for any

and further,

The last lemma gives some asymptotic results for .

Lemma 4.7.

For any ,

and

where are three constants which do not dependent on , and does not dependent on .

4.2.3. Asymptotics of

4.3. (iii) Scenario

Since the idea of the proof of this case is similar to that of scenarios (i) and (ii), we present only main steps. We split the region into five pieces as shown in Figure 1 (right). Namely, with some small and large, let

Clearly, we have the following bounds

| (33) |

where

Similar arguments as used in scenarios (i), (ii) give that

| (34) |

and

| (35) |

and the asymptotically negligibility of . Note that in proving the bound for , in addition to (45) as in the proof of Lemma 4.1, we also need the fact that (for )

Consequently, the claim follows by formulas (33)-(35) and the asymptotically negligibility of . This completes the proof of scenario in Theorem 2.1.

4.4. (iv) Scenario

5. Proof of Theorem 2.3

For , we have that . The case follows from (4). Thus the interesting scenarios include (i) and (ii) . The claim for (ii) follows directly from (iii) in Theorem 2.1, with . Next, we shall focus on the proof for (i) . The proof goes with the same arguments as in the proof of scenario (i) in Theorem 2.1, but now there are two minimizers of the function namely, , with

We first split the region into three parts. Namely, with some small , let

As in the proof of scenario (i) of Theorem 2.1, the main contribution of the asymptotics comes from . Note further that

By symmetric property of the model we know that . Next, we show in Lemma 5.1 that is asymptotically negligible compared with . The proof of it is displayed in Appendix Proof of Lemma A.1.

Lemma 5.1.

For any chosen small we have for all large

holds for some constant which do not depend on .

The rest of the proof is the same as those in the proof of scenario (i) in Theorem 2.1, and thus omitted. This completes the proof.

Appendix A Proofs of Lemmas 4.1-5.1

In this section we give proofs of Lemmas 4.1-5.1 that are the building blocks of the proofs of Theorems 2.1 and 2.3.

We begin with the analysis of the local behaviour of function at its minimizer in scenarios (i)–(iv) of Proposition 3.1, respectivelly.

Lemma A.1.

Assume that . We have

-

(i).

If , then as ,

where, with

-

(ii).

If , then

-

–

(ii.1), as , with (i.e., ),

where

-

–

(ii.2), as , with (i.e., ),

where

-

–

(ii.3), as , with (i.e., ),

where

-

–

-

(iii).

If (in this case ), then

-

–

(iii.1), as , with ,

-

–

(iii.2), as , with ,

-

–

(iii.3), as , with ,

-

–

The proof of Lemma A.1 is tedious but only involves basic calculations using Taylor expansion, and thus it is omitted.

Next we present below a generalized version of the Bonferroni’s inequality. The proof can be found in, e.g., [9].

Lemma A.2.

Let be a probability space and and be events in with . Then

A.1. Proof of Lemma 4.1

Let be a fixed large constant (will be determined later). It is easily seen that

Next we consider upper bounds for each term on the right-hand side. According to Lemma 5 of [7], for any fixed , there exists a unique index set

such that

| (37) |

and

| (38) |

Thus,

| (39) | |||

where

| (40) |

Note that

| (41) |

In order to apply the Borell-TIS inequality, we first show that

holds for any on the boundary .

In fact, if the above does not hold for some boundary point , then for any there exist a sequence and some measurable set such that , and

for all large enough . Then we have

| (42) |

On the other hand, by Lemma 6 of [7] we have for all , and thus by (41) and (23) we have . This is a contradiction with (42). Therefore, is almost surely bounded. Consequently, by the Borell-TIS inequality (see, e.g., [1]) we have, for any fixed small constant

holds for all such that

Moreover, since is the standard Brownian motion,

showing that the random process has almost surely bounded sample paths on . Again by the Borell-TIS inequality

holds for all . Since for all large enough it holds that the claim for is established.

Below we consider . Since , we have from Proposition 3.1 that for any chosen small

and further (cf. (40))

with

Thus, similarly to (A.1) we conclude that

| (43) |

Since are all smooth functions and

one can check that, for all

Therefore, an application of the Piterbarg’s inequality in [4][Lemma 5.1] (see also [18][Theorem 8.1] or [20][Theorem 3]) yields that

| (44) |

where is some constant which does not depend on and

Moreover, we have from (i) of Lemma A.1 that for all

| (45) | |||||

holds with some small , where for all (see also the proof of (b).(i) in Lemma 9 of [7] for )

Thus

Inserting the above to (44) completes the proof.

A.2. Proof of Lemma 4.2

We first analyze the summand . We set

| (46) |

It follows that

| (49) | |||||

| (52) |

Since for all large the covariance matrix of is given by

Thus, the density function of is given by

By conditioning on the value of we rewrite (49) as

Using change of variables we further obtain

where

Now, we analyse . Due to the fact that , we have for all , and large enough

Thus, by the properties of Brownian motion

Next we have

where the exponent can be rewritten as

Define

Thus, it follows that

Further, we obtain from (i) of Lemma A.1 that, for all large enough ,

holds uniformly for

Consequently, by Lemma A.3 below we obtain

which gives the result for . The claim for follows with the same arguments.

Lemma A.3.

For any

holds uniformly for

We omit the tedious proof of Lemma A.3 since its idea is standard, i.e., it is based on finding a uniform integrable bound for the integrand and then using the dominated convergence theorem.

A.3. Proof of Lemma 4.3

Let us begin with . It follows that

In order to deal with we note that

where

Then we have

Using the same arguments as in the proof of Lemma 4.2 we obtain

which gives that

Next we consider which is more involved. We have (recall (46) for )

| (58) | |||||

| (61) |

with

For notational simplicity, we shall denote

Again by conditioning on the event

we have

where

and

where

Similarly as in the proof of Lemma 4.2, we obtain

where

Next, some elementary calculations give that

Further, note that

holds for some and

holds uniformly for (hereafter when we write we mean )).

Consequently

| (63) |

holds uniformly for as , where (by (b).(i) of Lemma 9 of [7] or Lemma A.1.(i) with )

Next, we consider the uniform, in , limit of the following:

For the conditional mean we can derive that

which further gives that

For the conditional variance of the increments we have

Therefore, similarly as in Lemma A.3 we can show that as

Consequently, the dominated convergence theorem gives

| (64) | |||

holds uniformly for , as .

Next we derive a useful upper bound for , :

| (65) |

In order to prove (65), by taking we arrive at

| (68) | |||||

| (69) |

Define, for any integers ,

with

Using the same arguments as in the derivation of (68) one can show that

| (71) |

Comparing (68) and (71) we derive

The finiteness of can be proved by using the Borell-TIS inequality. This justifies bound (65).

A.4. Proof of Lemma 4.4

The claim for follows from the same arguments as that for of Lemma 4.1. Next, as in the proof of Lemma 4.1, using the Piterbarg’s inequality we can show that

where is some constant which does not depend on and thus the claim for follows since

where the last inequality follows by (ii.3) of Lemma A.1. Finally, the claim for can be proved similarly, by using Piterbarg’s inequality and (ii.1)-(ii.2) of Lemma A.1.

A.5. Proof of Lemma 4.5

We first analyse the summand . Let

Then

Define , whose density function is given by

with the covariance matrix given by

By conditioning on the value of and using change of variables , we further obtain

Consequently, similar arguments as in the proof of Lemma 4.2 yield

This completes the proof.

A.6. Proof of Lemma 4.6

A.7. Proof of Lemma 4.7

We begin with the analysis of . We first look at . Denote

It is derived that

Next, we look at . We define

Consider the conditional process

We have that is a normally distributed random vector, with mean

and covariance matrix given by (suppose )

Thus, for the mean

as , where the convergence is uniform for . Similarly, we can derive that, for any

as , uniformly for . Consequently, we have, as

Similar arguments as those in the proof of Lemma 4.2 gives that

where (recall notation in (9))

It follows further from (ii.2) of Lemma A.1 that there exists some such that, for all small,

thus, for sufficiently large

holds for all , where . This implies that, for large

Based on the above discussions we obtain

Similar bounds can be found for , and thus the first claim follows.

Next we consider . For any we have

where, with ,

with

Next we have that is a normally distributed random vector, with mean

and covariance matrix given by (suppose )

Similarly as before, one can get

as where

with an independent copy of . Particularly, letting we can show, similarly as in (65), that

Therefore, as

Finally, we consider . Note that

where

Consequently, the claim for follows directly by using Lemma 4.5.

A.8. Proof of Lemma 5.1

Similarly as in (A.1) we obtain

where, we used the fact that , and

Further note that

We obtain

Thus, for sufficiently small ,

where we use continuity of the functions involved. Again, using the Borell-TIS inequality we obtain

holds for all large such that

Thus, the claim follows.

Supplemental materials

This section includes technical proofs of Lemma A.1 and Lemma A.3.

Proof of Lemma A.1

(i). Recall that for any the global minimizer is given by

In a small neighbourhood of this point, we have

Next we calculate the first few partial derivatives. We have

Since

one can obtain that

Further calculations show that

| (86) | |||

Consequently, the claim in (i) is established.

(ii). For , the global minimizer is given by

Three different types of expansion are available for , according to

(ii.1) . Consider the two representations of given in (12) and (13). Using the representation (12) we can show that

On the other hand, using representation in (13) we can show that i.e.,

In fact, for we have that

and for we have by (d).(i) of Lemma 7 in [7] (note ) that the above still holds. Furthermore, we have by (b).(ii) of Lemma 9 in [7] that, for all

Moreover, by using representation (13) one can show that

Then, for (where ), we have by Taylor expansion

as required.

(ii.2) . Similarly as in (ii.1), we have

where follows similarly as the positiveness of , by using Lemma 7 in [7]. Moreover, one can show that

Consequently, by Taylor expansion the claim of (ii.2) is established.

(ii.3) . The claim follows by considering the univariate function defined in (14).

(iii). Note that in this case and . The claims follows by combining the above discussions in (i)-(ii). This completes the proof.

Proof of Lemma A.3

The proof consists of two steps. In Step I, we derive the limit, as of the integrand for any fixed . In Step II, we look for uniform integrable upper bound of , by which we show that the limit can pass into the integral. For simplicity, in the following when we write , we mean

Step I. Recall

where

It follows that is normally distributed with mean value and covariance matrix given, respectively, by

Therefore, denoting for any

| (88) |

we can show that its mean is given by

| (89) | |||||

and its variance is given by

| (90) | |||||

Similarly, we can derive that, for any

| (91) |

By (89) and (91) we have, for any ,

| (92) | |||

as , where the convergence is uniform with respect to . Thus, by Lemma 4.2 in [26] we conclude that the finite dimensional distributions of converge to the finite dimensional distributions of as uniformly with respect to . Further, note that from (91) we have

holds, for all , when is large. This guarantees the uniform tightness of (see, e.g., Proposition 9.7 in [19]), and thus we conclude that the stochastic processes converge weakly to as uniformly with respect to . Therefore, we have from the continuous mapping theorem that for any

as , uniformly with respect to . Further, it follows that

holds uniformly with respect to . Thus,

holds uniformly with respect to .

Step II. In order to pass the limit into the integral, it is sufficient to find an integrable upper bound such that

holds for all large , uniformly with respect to . The four quadrants will be considered separately.

(i). . In this case, an upper bound for is chosen to be 1, and for some small

Thus, we choose

(ii). . In this case,

and for some small

Thus, for any we choose (with denoting the indicator function)

(iii). . In this case, for some small

and

Next we derive an upper bound for . It follows from (89) and (92) that

holds for all large and uniformly in , with some small constant and . Then

We consider the following two subsets of :

with some small constant.

Below, we derive upper bounds on , respectively. Note, from (91), for all large and all ,

for any . Hence, by the Sudakov-Fernique inequality (see, e.g., [1])

Moreover, it follows from (90) that, for sufficiently large and all ,

Thus, we have from the Borell-TIS inequality (Theorem 2.1.1 in [1]) that, on for all large and

Therefore, on we can choose

On the other hand, we have, for some ,

holds for all large . Thus, on we can choose

(iv). . In this case, for some small

and

By similar arguments as (iii), we can choose

This competes the proof.

Acknowledgement: TR & KD were partially supported by NCN Grant No 2018/31/B/ST1/00370 (2019-2022).

References

- [1] R.J. Adler and J.E. Taylor. Random fields and geometry. Springer Monographs in Mathematics. Springer, New York, 2007.

- [2] J. Azaïs and M. Wschebor. Level sets and extrema of random processes and fields. John Wiley & Sons, 2009.

- [3] K. Dȩbicki, E. Hashorva, L. Ji, and T. Rolski. Extremal behavior of hitting a cone by correlated Brownian motion with drift. Stochastic Processes and their Applications, 128(12):4171–4206, 2018.

- [4] K. Dȩbicki, E. Hashorva, and P. Liu. Ruin probabilities and passage times of -reflected Gaussian process with stationary increments. ESAIM: Probability and Statistics, 21:495–535, 2017.

- [5] K. Dȩbicki, E. Hashorva, and Z. Michna. Simultaneous Ruin Probability for Two-Dimensional Brownian Risk Model. Accepted for publication in J. Appl. Probab., 2019.

- [6] K. Dȩbicki, E. Hashorva, and L. Wang. Extremes of vector-valued Gaussian processes. arXiv e-prints: arXiv:1911.06350, 2019.

- [7] K. Dȩbicki, L. Ji, and T. Rolski. Logarithmic asymptotics for probability of component-wise ruin in two-dimensional Brownian model. Risks, 7(83), 2019.

-

[8]

K. D

bicki, K. M. Kosiński, M. Mandjes, and T. Rolski. Extremes of multidimensional Gaussian processes. Stochastic Process. Appl., 120(12):2289–2301, 2010.‘ e - [9] E. Hashorva and L. Ji. Extremes and first passage times of correlated fractional Brownian motions. Stochastic Models, 30(3):272–299, 2014.

- [10] H. He, W. P. Keirstead, and J. Rebholz. Double lookbacks. Mathematical Finance, 8(3):201–228, 1998.

- [11] H. Honnappa, P. Jaiswal, and R. Pasupathy. Large deviations of gaussian extremes on convex sets. Manuscript. https://web.ics.purdue.edu/ pasupath/PAPERS/ldextremes.pdf, 2020.

- [12] L. Ji. On the cumulative Parisian ruin of multi-dimensional Brownian motion models. Preprint, https://arxiv.org/pdf/1811.10110.pdf, 2019.

- [13] S. Kou and H. Zhong. First-passage times of two-dimensional Brownian motion. Adv. Appl. Prob., 48:1045–1060, 2016.

- [14] P. Lieshout and M. Mandjes. Tandem Brownian queues. Math. Methods Oper. Res., 66:275–298, 2007.

- [15] M. Mandjes. Large Deviations for Gaussian Queues: Modelling Communication Networks. Wiley, Chichester, 2007.

- [16] A. W. Marshall and I. Olkin. A multivariate exponential distribution. J.Amer. Statist. Assoc., 62:30–44, 1967.

- [17] A. Metzler. On the first passage problem for correlated Brownian motion. Statistics and Probability Letters, 80:277–284, 2010.

- [18] V. I. Piterbarg. Asymptotic methods in the theory of Gaussian processes and fields, volume 148 of Translations of Mathematical Monographs. American Mathematical Society, Providence, RI, 1996.

- [19] V. I. Piterbarg. Twenty lectures about Gaussian processes. Atlantic Financial Press, London, New York, 2015.

- [20] Vladimir I. Piterbarg. High extrema of Gaussian chaos processes. Extremes, 19(2):253–272, 2016.

- [21] S. Resnick. Extreme Values, Regular Variation and Point Processes. Springer-Verlag, 1987.

- [22] L. C. G. Rogers and L. Shepp. The correlation of the maxima of correlated Brownian motions. J. Appl. Prob., 43(2):880–883, 2006.

- [23] J. Shao and X. Wang. Estimates of the exit probability for two correlated Brownian motions. Adv. Appl. Prob., 2013(45):37–50.

- [24] M. Teunen and M. Goovaerts. Double boundary crossing result for the Browian motion. Scandinavian Actuarial Journal, 1994(2):139–150.

- [25] R. van der Hofstad and H. Honnappa. Large deviations of bivariate Gaussian extrema. Queueing Systems, 93:333–349, 2019.

- [26] Y. Zhou and Y. Xiao. Tail asymptotics for the extremes of bivariate Gaussian random fields. Bernoulli, 2017(23):1566–1598.