Time-varying neural network for stock return prediction \author Steven Y. K. Wong\thanksSteven Wong and Richard Xu are with School of Electrical and Data Engineering, University of Technology Sydney, Australia. Corresponding email: steven.ykwong87@gmail.com., Jennifer S. K. Chan\thanksJennifer Chan and Lamiae Azizi are with School of Mathematics and Statistics, University of Sydney, Australia., Lamiae Azizi\footnotemark[2], \\ Richard Y. D. Xu\footnotemark[1] \date

Abstract

We consider the problem of neural network training in a time-varying context. Machine learning algorithms have excelled in problems that do not change over time. However, problems encountered in financial markets are often time-varying. We propose the online early stopping algorithm and show that a neural network trained using this algorithm can track a function changing with unknown dynamics. We compare the proposed algorithm to current approaches on predicting monthly U.S. stock returns and show its superiority. We also show that prominent factors (such as the size and momentum effects) and industry indicators, exhibit time varying predictive power on stock returns. We find that during market distress, industry indicators experience an increase in importance at the expense of firm level features. This indicates that industries play a role in explaining stock returns during periods of heightened risk.

Keywords— return prediction, deep learning, online learning, time-varying

1 Introduction

The motivating application of this work is in predicting cross-sectional stock returns in a portfolio context. At every interval, an investor forecasts expected return of assets and performs security selection. A closely related problem is asset pricing — a fundamental problem in financial theory111It is useful to remind readers that this paper is concerned with improving tools for stock return prediction, enabling practitioners to better select securities. Asset pricing, in an academic context, is more concerned with explaining the drivers of returns.. Asset pricing has been well studied. A survey by Harvey et al., (2016) documented over 300 cross-sectional factors published in journals. However, literature has also documented evidence of time-variability of the true asset pricing model (also known as concept drift in machine learning, Gama et al., , 2014). Pesaran and Timmermann, (1995) performed linear regressions with permutations of regressors on U.S. stocks and compared both statistical and financial measures for model selection. Both predictability and regression coefficients of the selected model changed over time. Bossaerts and Hillion, (1999) reported similar findings in international stocks. So why do relationships change over time? Changes in macroeconomic environment is one possibility. Other explanations offered by McLean and Pontiff, (2016) relate to statistical bias (also called data mining bias in machine learning) and effects of arbitrage by investors (which the authors referred to as publication-informed trading). Thus, it is unsatisfactory for a practitioner to learn a static model as out-of-sample performance can vary.

Recently, deep learning222Deep learning is a subfield of machine learing. An overview is provided in Section 2.2. has made significant advances across a wide range of applications, such as achieving human-like accuracy in image recognition tasks (Schroff et al., , 2015) and translating texts (Sutskever et al., , 2014). By contrast, machine learning in financial markets is still in its infancy. Weigand, (2019) provided a recent survey of machine learning applied to empirical finance and noted that machine learning algorithms show promise in addressing shortcomings of conventional models (such as the inability to model non-linearity or handle large number of covariates). Recent works have applied neural networks to the problem of cross-sectional stock return prediction (see, Messmer, , 2017; Abe and Nakayama, , 2018; Gu et al., , 2020). Gu et al., (2020) have modelled potential time-variability driven by macroeconomic conditions by interacting firm level features with macroeconomic indicators. However, they do not consider all possible avenues of time-variability of asset pricing models, such as effects of trading as highlighted by McLean and Pontiff, (2016). For instance, Lev and Srivastava, (2019) noted that the prominent value factor (Rosenberg et al., , 1985; Fama and French, , 1992) has been unprofitable for almost 30 years — a period that included multiple business cycles. In fact, the authors noted that returns to the value factor have been negative since 2007, suggesting a change in the underlying relationship.

To address this, we propose the online early stopping algorithm (henceforth, OES), for training neural networks that can adapt to a time-varying function. Our problem is characterized by information release over time and iterative decision making. Optimization in this context are called online as decisions are made with the knowledge of past information but not the future. In conventional neural network training, one of the hyperparameters is the number of optimization iterations . In OES, we propose to treat as a learnable parameter that varies over time (), as , and is recursively estimated over time. We provide with a new meaning — a regularization parameter that controls the amount of update neural network weights receive as new observations are revealed. Thus, if consecutive cross-sectional observations are very different then we would expect to be small and the neural network is prevented from overfitting to any one period. Conversely, a slowly changing function will have a high degree of continuity and we would expect the network to fit more tightly to each new observation. Using this training algorithm, a neural network can adapt to changes in the data generation process over time. For practitioners, we show that a neural network trained with OES can be a powerful prediction model and a useful tool for understanding the time-varying drivers of returns.

Neural network training is an optimization problem. We draw on concepts in online optimization to provide a performance bound that is related to the variability of each period. We do not assume any time-varying dynamics of the underlying function, a typical approach in online optimization. The benefit of this approach is that it can track any source of variability in the underlying function, including macroeconomic, arbitrage-induced, market condition-induced or other unknown sources. For instance, Lev and Srivastava, (2019) suggested that the negative return to the value factor was related to diminishing relevance of book equity as an accounting measure. Such drivers would not have been captured by the macroeconomic approach in Gu et al., (2020). Nonetheless, we acknowledge that a limitation of our approach is the inability to explain the source of variability.

We provide two evaluations of OES: 1) a simulation study based a data set simulated from a non-linear function evolving under a random-walk; 2) an empirical study of U.S. stock returns. The empirical study is based on Gu et al., (2020), who compared several machine learning algorithms for predicting monthly returns of all U.S. stocks. Majority of the data set were made available to the public and are used in this work. We note that the setup in Gu et al., (2020) is suboptimal for our portfolio selection problem for three reasons. Firstly, (raw) monthly stock returns contain characteristics that complicate the forecasting problem, such as outliers, heavy tails and volatility clustering (Cont, , 2001). These characteristics are likely to impede a predictor’s ability to learn. Secondly, the data set in Gu et al., (2020) contains stocks with very low market capitalization, are illiquid, and are unlikely to be accessible by institutional investors. Thirdly, at the individual stock level, forecasting stocks’ excess returns over risk free rate also encompasses forecasting market excess returns. As practitioners are typically concerned with relative performance between stocks333In the simplest form, a long-only investor will hold a portfolio of the top ranked stocks and a long-short investor will buy top ranked stocks and sell short bottom ranked stocks. Thus, relative performance is relevant to practitioners., the market return component adds unnecessary noise to the problem of relative performance forecasting. Thus, in addition to comparison with Gu et al., (2020), we also present results based on a more likely use case by practitioners, by excluding stocks with very low capitalization and forecasting cross-sectionally standardized excess returns. We show that forecasting performance significantly improved based on this re-formulation. We propose to measure performance using information coefficient (henceforth, IC), a widely applied performance measure in investment management (Ambachtsheer, , 1974; Grinold and Kahn, , 1999; Fabozzi et al., , 2011). OES achieves IC of on the U.S. equities data set, compared to under an expanding window approach in Gu et al., (2020).

A summary of our contributions in this paper are as follows:

-

•

We propose the OES algorithm which allows a neural network to track a time-varying function. OES can be applied to an existing network architecture and requires significantly less time to train than the expanding window approach in Gu et al., (2020). In our tests, OES took 1/7 the time to train and predict as the expanding window approach of DNN. This has a practical implication as practitioners wishing to employ deep learning models have limited time between market close and next day’s open to generate features and train new models, which is made worse if an ensemble is required.

-

•

We show that firm features exhibit time-varying importance and that the model changes over time. We find that some prominent features, such as market capitalization (the size effect) display declining importance over time and is consistent with the findings of McLean and Pontiff, (2016). This highlights the importance to have a time-varying model.

-

•

We find that firm features, in aggregate, experience a fall in importance in predicting cross-sectional returns during market distress (e.g. Dot-com bubble in 2000-01). Importance of sector dummy variables (e.g. technology and oil stocks) rose over the same period, suggesting importance of sectors is also time-varying. Our analysis indicates that sectors have an important role in predicting stock returns during market distress. We expect this to be especially true if market stress impacts on certain sectors more than others, such as travel and leisure stocks during a pandemic.

-

•

Using a subuniverse that is more accessible to institutional investors (by excluding microcap stocks), we show that OES exhibits superior predictive performance. We find that mean correlation between predictions of OES and DNN is only and monthly correlation is lowest immediately after a shock (e.g. recession). We attribute this to OES adapting to the recovery which manifests as lower drawdown post Global Financial Crisis.

-

•

We find that an ensemble formed by averaging the standardized predictions of the two models exhibits the highest IC, decile spread and Sharpe ratio. Thus, practitioners may choose to deploy both models in a complementary manner.

In the rest of this paper, we denote the algorithm of Gu et al., (2020) as DNN (Deep Neural Network) and our proposed Online Early Stopping as OES. This paper is organized as follows. Section 2 defines our cross-disciplinary problem, and provides overviews of neural networks and online optimization. Section 3 outlines our main contribution of this paper — the proposed OES algorithm which introduces time-variations to the neural network. Simulation results are presented in Section 4, which demonstrates the effectiveness of OES in tracking a time-varying function. An empirical study on U.S. stock returns is outlined in Section 5. Finally, Section 6 discusses the empirical finance problem and concludes the paper with some remarks.

2 Preliminaries

2.1 Definitions

Similar to a classical online learning setup, a player iteratively makes portfolio selection decisions at each time period. We call this iterative process per interval training. There are stocks in the market, each with features, forming input matrix at time . The -th row in is feature vector of stock . To simplify notations, we define return of stock as return over the next period, i.e., , where is price at time and is dividend at if a dividend is paid, and zero otherwise. Player predicts stock returns by choosing , which parameterizes prediction function . Market reveals and, for regression purposes, investor incurs squared loss,

where is the -th element of vector . The true function drifts over time and is approximated by with time-varying . Investor’s objective is to minimize loss incurred by choosing the best at time using observed history up to . Both the function form and time-varying dynamics of are not known. Hence a neural network is used to model the cross-sectional relationship at each and the time-variability is formulated as a network weights tracking problem. The loss function verifies the same assumptions adopted in Aydore et al., (2019), which are:

-

•

is bounded: ,

-

•

is L-Lipschitz: ,

-

•

is -smooth: .

We denote the gradient of at as and stochastic gradient as , or where the context is obvious, and respectively.

As performance measure, Gu et al., (2020) used pooled without mean adjustment in the denominator,

where is the pooled out-of-sample data set covering January 1987 to December 2016 in the empirical study. There are several shortcomings with this performance measure. The number of stocks in the U.S. equities data set starts from 1,060 in March 1957, peaks at over 9,100 in 1997, and falls to 5,708 at the end of 2016. A pooled performance metric will place more weight on periods with a higher number of stocks. An investor making iterative portfolio allocation decisions would be concerned with accuracy on average over time. Moreover, asset returns are known to exhibit non-Gaussian characteristics (Cont, , 2001). Summary statistics of monthly U.S. stock returns are provided in Table 2 (in Section 5), which clearly confirms the existence of considerable skewness and time-varying variance. Therefore, we provide three additional metrics. The first metric is the information coefficient (IC), defined as the cross-sectional Pearson’s correlation444Rank IC, which uses Spearman’s rank correlation instead of Pearson’s, is also used in practice. between stock returns and predictions. The time series of correlations is then averaged to give the final score. IC was first proposed by Ambachtsheer, (1974) and is widely applied in investment management for measuring predictive power of a forecaster or an investment strategy (Grinold and Kahn, , 1999; Fabozzi et al., , 2011). The second metric is the annualized Sharpe ratio, calculated as,

where is the difference between average realized monthly returns of decile 10 and decile 1 at , sorted on predicted returns. The third metric is the average monthly , where denominator is adjusted by the cross-sectional mean, as a conventional complement to .

2.2 Feedforward neural networks

An overview of neural networks is provided in this section. Interested readers are referred to Goodfellow et al., (2016) for a comprehensive review.

Neural networks are a broad class of high capacity models which were inspired by the biological brain and can theoretically learn any function (known as the Universal Approximation Theorem, see Hornik et al., , 1989; Cybenko, , 1989; Goodfellow et al., , 2016). A common form, the feedforward network, also known as multilayer perceptrons (MLP), is a subset of neural networks which forms a finite acyclic graph (Goodfellow et al., , 2016). There are no loop connections and values are fed forward, from the input layer to hidden layers, and to the output layer. The word ‘deep’ is prefixed to the name (e.g. deep feedforward network or deep neural network) to signify a network with many hidden layers, as illustrated in Figure 1. A feedforward network is also called a fully connected network if every node has every node in the preceding layer connected to it.

The output of each layer acts as input to the next layer and loss is ‘backpropagated’ by taking the partial derivative of loss with respect to weights at each layer. Each layer consists of activation function (e.g. rectified linear unit, defined as ), weights , bias , and output . The -th layer of the network is denoted as . For brevity, we drop the layer designation, and denote the entire network as and weight vector set , where is the number of layers. The network is trained with stochastic gradient descent (or variants) at time (but dropping the subscript for simplicity as the context is clear),

where is the weight vector at optimization iteration (also called epochs) and is step size.

At time , denotes the number of optimization iterations that are used to train the network and is found by monitoring loss on a validation set. This procedure is called early stopping (Morgan and Bourlard, , 1990; Reed, , 1993; Prechelt, , 1998; Mahsereci et al., , 2017). Training is stopped when the validation loss decreases by less than a predefined amount, called tolerance. Early stopping can be seen as a regularization technique which limits the optimizer to search in the parameter space near the starting parameters (Sjöberg and Ljung, , 1995; Goodfellow et al., , 2016). In particular, given optimization steps , the product can be interpreted as the effective capacity which bounds reachable parameter space from , thus behaving like regularization (Goodfellow et al., , 2016).

For time series problems where chronological ordering is important, popular approaches include expanding window (each new time slice is added to the panel data set) and rolling window (the oldest time slice is removed as a new time slice is added, Rossi and Inoue, , 2012). Instead of randomly splitting training and test sets, the out-of-sample procedure555As described in Bergmeir et al., (2018). can be used where the end of the series is withheld for evaluation. This is unsatisfactory in the context of stock return prediction for two reasons. First, each time period is drawn from a different data distribution (hereon denoted as for data set drawn at time , or for all periods in the out-of-sample data set). A pooled regression with window size effectively assumes data at is drawn from the average of the past observations. Secondly, if data is scarce in terms of time periods, estimates for optimal optimization steps can have large stochastic error. For instance, monthly data with a window size of 12 months and 3:1 training-validation split. is estimated using only 3 months of data. To the best of our knowledge, there is no procedure for adapting early stopping in an online context with time-varying dynamics.

2.3 Online optimization

Optimizing network weights to track a function evolving under unknown dynamics is an online optimization problem. A discussion on relevant concepts in online optimization is provided. Interested readers are encouraged to read Shalev-Shwartz, (2012) for an introduction. In online optimization literature, iterate is often denoted as and loss function as . We have used as iterate to be consistent with our parameter of interest and as loss function to avoid conflict with our use of as activation function.

Online optimization and its related topics have been well researched. Applications of online optimization in finance first came in the form of the Universal Portfolios by Cover, (1991). However, most of the early works in online optimization are on the convex case and assume each draw of loss function is from the same distribution (in other words, is stationary). These assumptions are not consistent with our problem. Recently, Hazan et al., (2017) extended online convex optimization to the non-convex and stationary case. This was further extended by Aydore et al., (2019) to the non-convex and non-stationary666Non-stationarity in online optimization literature refers to time-variability of loss function . case, with the proposed Dynamic Exponentially Time-Smoothed Stochastic Gradient Descent (DTS-SGD) algorithm. Non-convex optimization is NP-Hard777In computer science, NP-Hard refers a class of problems where no known polynomial run-time algorithm exists.. Therefore, existing non-convex optimization algorithms focus on finding local minima (Hazan et al., , 2017). For this reason, one difference between online convex optimization and online non-convex optimization is that the former focuses on minimizing sum of losses relative to a benchmark (for instance, the minimizer over all time intervals is one of the most basic benchmarks), and the latter focuses on minimizing sum of gradients (e.g. ). This optimization objective is called regret. Readers familiar with time-series analysis might be taken aback by the lack of parameters in a typical online optimization algorithm. This is due to the game theoretic approach of online optimization and the focus on worst case performance guarantees, as opposed to the average case performance in statistical learning. Regret bounds are typically functions of properties of the loss function (e.g. convexity and smoothness) and are dependent on environmental assumptions.

At each interval , DTS-SGD updates network weights using a time-weighted sum of past observed gradients. Time weighting is controlled by a forget factor . In analyzing DTS-SGD, we note two potential weaknesses. Firstly, neural networks are notoriously difficult to train. Geometry of the loss function is plagued by an abundance of local minima and saddle points (see Chapter 8.2 of Goodfellow et al., , 2016). Momentum and learning rate decay strategies (for instance, Sutskever et al., , 2013; Kingma and Ba, , 2015) have been introduced which require multiple passes over training data, adjusting learning rate each time to better traverse the loss surface. DTS-SGD is a single weight update at each time period which may have difficulties in traversing highly non-convex loss surfaces. Secondly, during our simulation tests, we observed that loss can increase after a weight update. One possibility is that a past gradient is taking the weights further away from the current local minima. This is particularly problematic for our problem as stock returns are very noisy.

3 Online early stopping

3.1 Tracking a restricted optimum

We start by providing an informal discussion of the algorithm. Neural networks are universal approximators. That is, it can approximate any function up to an arbitrary accuracy. Thus, given a network structure and a time-varying function, network weights trained with data from a single time interval (i.e., a cross-sectional slice of time) neatly summarizes the function at that interval and the Euclidean distance between consecutive sets of weights can be interpreted as the amount of variations in the latent function expressed in weight space. Simply using to predict on will lead to an overfitted result. To illustrate, suppose , and alternates in a sequence of . Then, it is clear that using to predict on will lead to a worse outcome than using . In this scenario, the optimal strategy is to never update weights (or scale updates by zero). Generally, the optimal policy is to regularize updates such that the network is not overfitted to any single period.

In the rest of this section, we present our main theoretical results. Formally, our goal is to track the unobserved minimizer of , a proxy for the true asset pricing model, as closely as possible. In regret analysis, it is desirable to have regret that scales sub-linearly to , which leads to asymptotic convergence to the optimal solution. Hazan et al., (2017) demonstrated that in the non-convex case, a sequence of adversarially chosen loss functions can force any algorithm to suffer regret that scales with as 888In computer science, notation refers to the lower bound complexity.. Locally smoothed gradients (over a rolling window of loss functions) were used to improve smoothed regret, with a larger advocated by Hazan et al., (2017). Aydore et al., (2019) extended this to use rolling weighted average of past gradients which gives recent gradients a higher weight to track a dynamic function. Inevitably, smoothing will track a time-varying minimizer with a tracking error that is proportionate to and the forget factor.

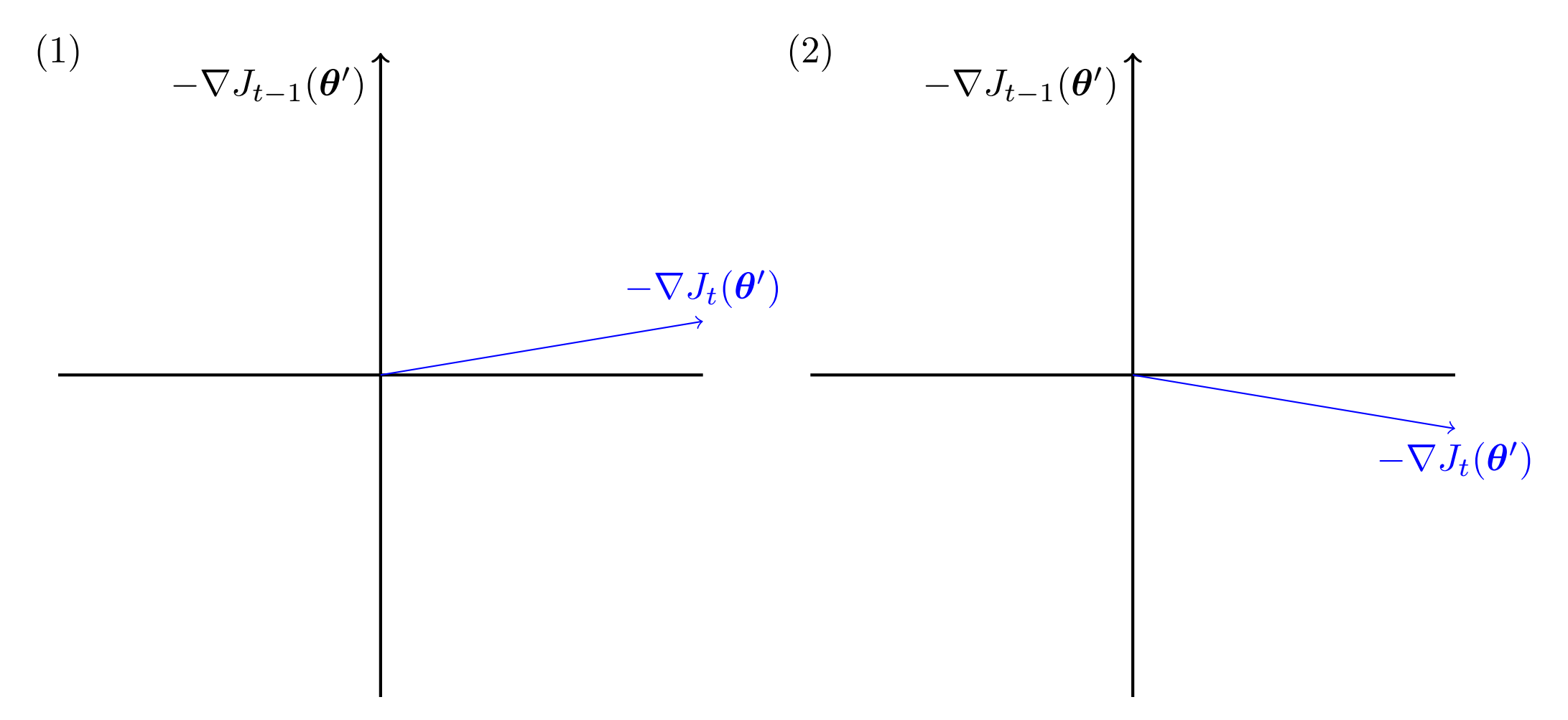

To address this, we propose a restricted optimum (denoted by at time ) as the tracking target of our algorithm. At time , the online player selects based on observed . As the network is trained using gradient descent, we propose to restrict the admissible weight set to the path formed from and extending along the gradient vector (in other words, the path traversed by gradient descent). The point along this path with the minimum is the restricted optimum. We argue that the trade-off between restricting the admissible weight space and solving the simplified problem is justified as other points in the weight space are not attainable via gradient descent and is thus unnecessary to consider all possible weight sets in . Without assuming any time-varying dynamics, updating weights using an average of past gradients (similar to Hazan et al., , 2017) will induce a tracking error to the time-varying function. To illustrate the restricted optimum concept, let be our starting point of optimization, and . The possible scenarios during training are (also illustrated in Figure 2):

-

1.

If , then moving along will also improve until is perpendicular to or has reached a local minima of .

-

2.

If , then following will not improve and training should terminate.

This observation motivates our online early stopping algorithm. In this section, we will use to denote restricted optimal weights at and to denote the online player’s choice of weights. Suppose evolves under the dynamics of,

where is sampled from an unknown distribution. can be interpreted as a regularizer which provides the optimal prediction weights on if we are restricted to travelling along the direction of . In this context, is the minimum gradient suffered by the player. Next, let be the optimal number of optimization steps at time and be the estimated number of optimization steps. At iteration , we solve optimal optimization steps ,

| (1) |

We start from as solving requires which we are yet to observe. This leads to optimal weights (the restricted optimum) trained on for prediction on ,

| (2) |

and can be approximated by,

which implies . To predict , we choose and train prediction weights on by substituting in (the rounded up estimate of optimization steps),

| (3) |

As is a constant chosen by hyperparameter search, can be interpreted as a proxy to the regularizer . Using our -smooth assumption (in Section 2.1) and substituting in definitions of and (in Equation 3), we obtain,

| (4) |

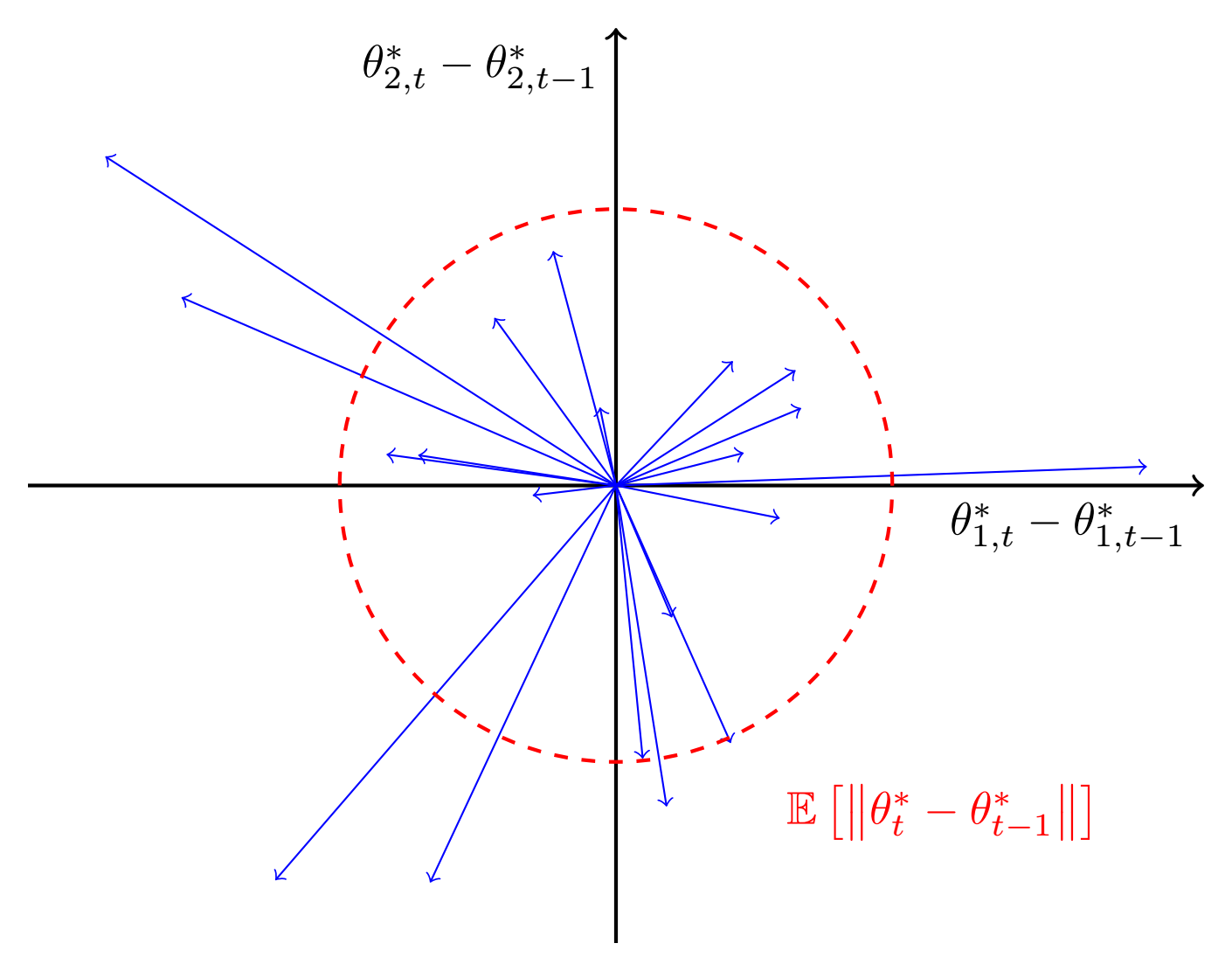

where we start from as our algorithm requires at least 2 cross-sectional observations. The elegance of Equation 4 is that it conforms with the conventional notion of regret, with cumulative gradient deficit against an optimal outcome in place of cumulative loss. As is the unbiased estimator of , Equation 4 indicates that the cumulative deficit is asymptotically bounded by the variance of . This concept is illustrated in Figure 3. If is constant, then will converge to and the optimal weights are achieved. Conversely, if has high variance, then the player will suffer a larger cumulative gradient deficit.

3.2 Online early stopping algorithm

Our strategy is to modify the early stopping algorithm to recursively estimate . An outline is provided below as an introduction to the pseudocode in Algorithm 1:

on line 4 is outlined in Algorithm 2. In our implementation of the algorithm, we have used stochastic gradient instead of the full gradient . Algorithm 2 contains the schematics of an early stopping algorithm with one modification adapted from Algorithm 7.1 and Algorithm 7.2 in Goodfellow et al., (2016). Validation is performed before the first training step to allow for the case where (i.e., we start from the optimal weights).

4 Simulation study

4.1 Simulation data

For the simulation study, we create the following synthetic data set:

-

•

months, each month consists of stocks.

-

•

Each stock has features, forming input matrix of and output vector .

-

•

Let be the value of feature of stock at time . Each feature value is randomly set to .

-

•

Each feature is associated with a latent factor , where and . follows a Wiener process and drifts over time.

-

•

Each output value is , where . Thus, is non-linear with respect to and the relationship changes over time.

We have used the same network setup and hyperparameter ranges as the empirical study on U.S. equities (outlined in Table 3) but with a batch size of 50. DNN has the same setup but is re-fitted at every 10-th time intervals. The data set is split into three 60 interval blocks. Hyperparameters for OES are chosen using a grid search, a procedure called hyperparameter tuning. For each hyperparameter combination, the network is trained on the first 60 intervals and validated on the next 60 intervals. Hyperparameters with the minimum MSE in the validation set is used in the remaining 60 intervals as out-of-sample data. Performance metrics are calculated using the out-of-sample set. DTS-SGD follows the same training scheme as OES, with additional hyperparameters: window period and forget factor .

4.2 Simulation results

Our synthetic data requires the network to adapt to time-varying dynamics. Table 1 records results of the simulation. DNN struggles to learn the time-varying relationships, with mean of and mean rank correlation of . This is expected as the expanding window approach used in DNN assumes the relationships at is best approximated by the average relationships in the observed past. OES significantly outperforms the other two methods in this simple simulation, achieving mean of and mean rank correlation of . This demonstrates OES’s ability to track a non-linear, time-varying function reasonably closely. There is a preference for higher regularization and learning rate. In Aydore et al., (2019), the authors reported issues of exploding gradient with the static time-smoothed stochastic gradient descent in Hazan et al., (2017) and that DTS-SGD provided greater stability. In our simulation test, we observed gradient instability with DTS-SGD as well. During training, loss can increase after a weight update. We hypothesize that a past gradient is taking network weights away from the direction of the current local minima and could be an issue with this general class of optimizers. Lastly, we find that mean tends to be slightly lower than (which is reasonable with a smaller denominator of a negative term).

| % | DNN | OES | DTS-SGD |

|---|---|---|---|

| Metrics | |||

| Pooled | -7.12 | 50.22 | 0.13 |

| Mean | -7.77 | 49.64 | -0.33 |

| IC | -4.21 | 71.24 | 6.29 |

| Hyperparameters | |||

| Mean penalty | 0.01 | 0.09 | 0.04 |

| Mean | 0.55 | 1.00 | 0.10 |

| Mean (periods) | 14 | ||

| Mean | 83.00 |

5 Predicting U.S. stock returns

5.1 Model and U.S. equities data

The U.S. equities data set in Gu et al., (2020) consists of all stocks listed in NYSE, AMEX, and NASDAQ from March 1957 to December 2016. Average number of stocks exceeds 5,200. Excess returns over risk-free rate are calculated as forward one month stock returns over Treasury-bill rates. As noted in Section 2.1, stock returns exhibit non-Gaussian characteristics. Table 2 presents descriptive statistics of excess returns. Monthly excess returns are positively skewed and contains possible outliers which may influence the regression. We follow Gu et al., (2020) in using MSE but note that MSE is not robust against outliers. As noted in Section 1, we also provide an alternative setup which excludes microcap stocks. The alternative setup and empirical results are presented in Section 5.4.

| % | 1957-1966 | 1967-1976 | 1977-1986 | 1987-1996 | 1997-2006 | 2007-2016 |

|---|---|---|---|---|---|---|

| Mean | 0.95 | 0.25 | 0.95 | 0.64 | 0.90 | 0.50 |

| Std Dev | 9.98 | 14.89 | 15.84 | 18.44 | 19.93 | 16.26 |

| Skew | 212.44 | 184.21 | 365.98 | 1059.88 | 502.41 | 783.70 |

| Min | -76.38 | -91.88 | -90.14 | -99.13 | -98.30 | -99.90 |

| 1% | -20.27 | -31.41 | -33.82 | -40.39 | -44.61 | -38.96 |

| 10% | -9.26 | -14.99 | -14.38 | -15.61 | -17.08 | -14.25 |

| 25% | -4.42 | -7.78 | -6.54 | -6.64 | -6.91 | -5.76 |

| 50% | -0.10 | -0.65 | -0.52 | -0.41 | 0.00 | 0.24 |

| 75% | 5.14 | 6.21 | 6.67 | 6.18 | 6.67 | 5.84 |

| 90% | 11.62 | 16.23 | 16.43 | 16.11 | 17.57 | 14.06 |

| 99% | 33.04 | 49.60 | 51.99 | 56.92 | 65.43 | 48.08 |

| Max | 255.29 | 432.89 | 1019.47 | 2399.66 | 1266.36 | 1598.45 |

Feature set includes 94 firm level features, 74 industry dummy variables (based on first two digits of Standard Industrial Classification code, henceforth SIC) and interaction terms with 8 macroeconomic indicators. The firm features and macroeconomic indicators used in Gu et al., (2020) are based on Green et al., (2017) and Welch and Goyal, (2008), respectively. Firm level features include share price based measures, valuation metrics and accounting ratios. The purpose of interacting firm level features with macroeconomic indicators is to capture any time-varying dynamics that are related to (common across all stocks) macroeconomic indicators. For instance, suppose valuation metrics have a stronger relationship with stock returns during periods of high inflation. Then, this information will be encoded in the interaction term. The aggregated data set therefore contains features. Each feature has been appropriately lagged to avoid look-forward bias, and is cross-sectionally ranked and scaled to . Table A.6 in the Internet Appendix of Gu et al., (2020) contains the full list of firm features.

A subset of the data is available on Dacheng Xiu’s website999Dacheng Xiu’s website https://dachxiu.chicagobooth.edu/ which contains 94 firm level characteristics and 74 industry classification. Our main result uses firm level features but results with the full 920 features are also provided as a comparison. At this point, it is useful to remind readers that our goal is to track a time-varying function when the time-varying dynamics are unknown. In other words, we assume that time-varying dynamics between stock returns and features are not well understood or are unobservable. As such, the subset of data without interaction terms is sufficient for our problem. If macroeconomic indicators do encode time-varying dynamics, our network will track changing macroeconomic conditions automatically.

Data is divided into 18 years of training (from 1957 to 1974), 12 years of validation (1975-1986), and 30 years of out-of-sample tests (1987-2016). We use monthly total returns of individual stocks from CRSP. Where stock price is unavailable at the end of month, we use the last available price during the month. Table 3 records test configurations as outlined in Gu et al., (2020) and in our replication. A total of six hyperparameter combinations ( penalty and in Table 3) are tested. We use the same training scheme as Gu et al., (2020) to train DNN. Once hyperparameters are tuned, the same network is used to make predictions in the out-of-sample set for 12 months. Training and validation sets are rolled forward by 12 months at the end of every December and the model is re-fitted. An ensemble of 10 networks is used, where each prediction is the average prediction of 10 networks.

| Parameter | Gu et al., (2020) | This paper |

|---|---|---|

| Preprocessing | Rank [-1, 1]; Fill median | Rank [-1, 1]; Fill median/0 |

| Hidden layers | 32-16-8 | 32-16-8 |

| Activation | H: ReLU / O: Linear | H: ReLU / O: Linear |

| Batch size | 10,000 | DNN 10,000 / OES 1,000 |

| Batch normalization | Yes | Yes |

| penalty | ||

| Early stopping | Patience 5 | Patience 5 / Tolerance 0.001 |

| Learning rate | ||

| Optimizer | ADAM | ADAM |

| Loss function | MSE | MSE |

| Ensemble | Average over 10 | Average over 10 |

To train OES, we keep the first 18 years (to 1974) as training data and next 12 years (to 1986) as validation data. For each permutation of hyperparameter set, we have trained an online learner up to 1986. Hyperparameter tuning is only performed once on this period, as opposed to every year in Gu et al., (2020). As the algorithm does not depend on a separate set of data for validation, we simply take the hyperparameter set with the lowest monthly average MSE over 1975-1986 as the best configuration to use for rest of the data set. Batch size of 1,000 for OES was chosen arbitrarily.

5.2 Predicting U.S. stock returns

In this section, we present our U.S. stock return prediction results. DTS-SGD did not complete training with a reasonable range of hyperparameters due to exploding gradient and is omitted from this section. As an overarching comment, for both DNN and OES on U.S. stock returns are very low, and are consistent with the findings of Gu et al., (2020). First, results with and without interaction terms are presented in Table 4, keeping in mind that our method should be compared against DNN without interaction terms. Without interaction terms, OES and DNN achieve IC of and , respectively. The relatively high correlation of OES (compared to DNN) indicates that it is better at differentiating relative performance between stocks. This is particularly important in our use case as practitioners build portfolios based on expected relative performance of stocks. For instance, a long-short investor will buy top ranked stocks and short sell bottom ranked stocks and earn the difference in relative return between the two baskets of stocks. Mean are and for OES and DNN, respectively. Note that the denominator of mean is adjusted by the cross-sectional mean of excess returns. Therefore, negative means of both OES and DNN indicate that neither method is able to accurately predict the magnitude of cross-sectional returns. Finally, OES scores on and DNN scores . The low values of both methods underscore the difficulty in return forecasting. DNN achieves higher Sharpe ratio than OES, at 1.63 and 0.83, respectively. As we will point out in Section 5.4, the high Sharpe ratio of DNN is driven by microcap stocks. Despite the very low , both methods are able to generate economically meaningful returns. This underscores our argument that is not the best measure of performance and verifies practitioners’ choice of correlation as the preferred measure. We observed similar performance with interaction terms, suggesting that the 8 macroeconomic time series have little interaction effect with the 94 features. In the subsequent results in this section, we only report statistics without interaction terms.

| With Interactions | W/O Interactions | |||||

|---|---|---|---|---|---|---|

| % | As reported | DNN | OES | DNN | OES | |

| Metrics | ||||||

| Pooled | 0.4 | 0.13 | -1.93 | 0.22 | -2.48 | |

| Mean | -9.89 | -11.93 | -9.68 | -12.17 | ||

| IC | 3.51 | 4.22 | 3.82 | 4.53 | ||

| P10-1 | 3.27 | 1.83 | 2.10 | 2.39 | 2.41 | |

| Sharpe ratio | 2.36 | 0.94 | 0.72 | 1.63 | 0.83 | |

| Hyperparameters | ||||||

| Mean penalty | 0.0012 | 0.0154 | 0.0024 | 0.0028 | ||

| Mean | 0.77 | 0.10 | 0.67 | 0.10 | ||

| As reported | DNN | OES | ||||||

|---|---|---|---|---|---|---|---|---|

| % | Predicted | Realized | Predicted | Realized | Predicted | Realized | ||

| P1 | -0.31 | -0.92 | -0.59 | -0.47 | -3.53 | -0.50 | ||

| P2 | 0.22 | 0.16 | 0.09 | 0.15 | -1.96 | 0.03 | ||

| P3 | 0.45 | 0.44 | 0.37 | 0.54 | -1.07 | 0.27 | ||

| P4 | 0.60 | 0.66 | 0.55 | 0.64 | -0.34 | 0.48 | ||

| P5 | 0.73 | 0.77 | 0.70 | 0.73 | 0.30 | 0.67 | ||

| P6 | 0.85 | 0.81 | 0.84 | 0.78 | 0.88 | 0.85 | ||

| P7 | 0.97 | 0.86 | 0.99 | 0.85 | 1.46 | 1.04 | ||

| P8 | 1.12 | 0.93 | 1.17 | 0.96 | 2.10 | 1.18 | ||

| P9 | 1.38 | 1.18 | 1.43 | 1.26 | 2.89 | 1.42 | ||

| P10 | 2.28 | 2.35 | 2.33 | 1.92 | 4.25 | 1.91 | ||

| P10-1 | 2.58 | 3.27 | 2.92 | 2.39 | 7.78 | 2.41 | ||

So why do IC and diverge? The answer lies in Table 5 and Figure 4. In here, we form decile portfolios based on predicted returns over the next month and track their respective realized returns. OES predicted values span a wider range than DNN. This has contributed to a lower , even though OES is able to better differentiate relative performance between stocks. DNN used a pooled data set which will average out time-varying effects. As a result, the average gradient will likely smaller in magnitude. This is evident from the lower mean penalty and higher learning rate chosen by validation. By contrast, OES trains on each time period individually and the norm of the gradient presented to the network at each period is likely to be larger. This led to a lower learning rate chosen by validation. Hence, variance of OES predicted values is higher and potentially requires higher or different forms of regularization.

In Table 5 and Figure 4, we observe that the prediction performance of DNN is concentrated on the extremities, namely P1 and P10, with realized mean returns of and respectively. Stocks between P3 and P7 are not well differentiated. By contrast, OES is better at ranking stocks across the entire spectrum. Realized mean returns of OES are more evenly spread across the deciles, resulting in higher correlation than DNN. P10-1 realized portfolio returns are similar across DNN and OES at and , respectively. However, the difference in mean return spread increases when calculated on a quintile basis (mean return of top of stocks minus bottom ), to and for DNN and OES, respectively. This reflects better predictiveness in the middle of the spectrum of OES. An investor holding a well diversified portfolio is more likely to utilize predictions closer to the center of the distribution and experience relative returns that are reminiscent of the quintile spreads (and even tertile spreads) rather decile spreads.

5.3 Time-varying feature importance

So far, our tests are predicated on time-varying relationships between features and stock returns. How do features’ importance change over time? To examine this, at every time period we train the OES model and make a baseline prediction. For each feature , all values of are set to zero and a new prediction is made. A new is calculated between the new prediction and the baseline prediction, denoted as . Importance of feature at time is calculated as . Our measure tracks features that the network is using. This is different to the procedure in Gu et al., (2020) where is calculated against actual stock returns, rather than a baseline prediction.

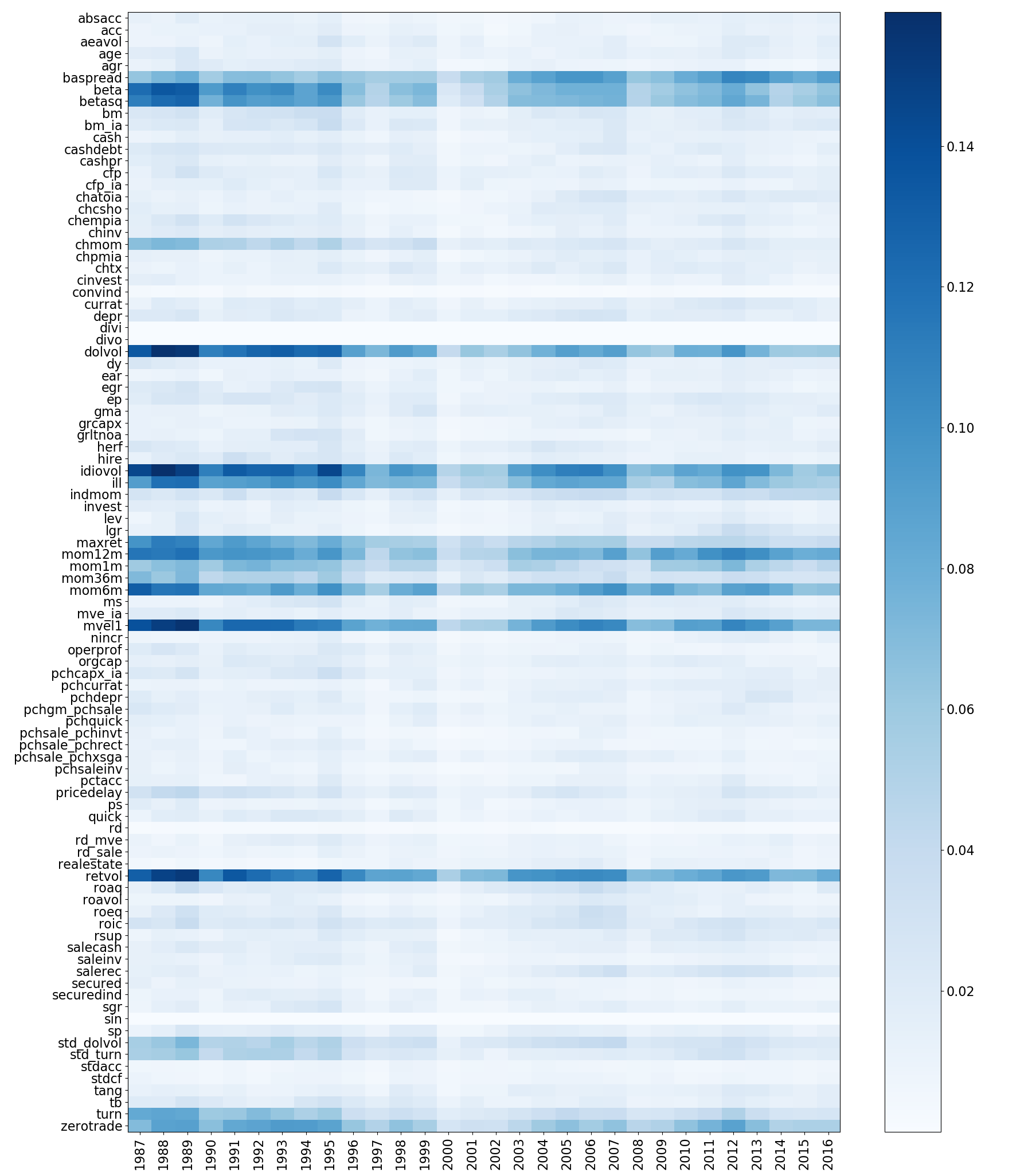

To illustrate the inadequacy of a non-time-varying model, we first track feature importance over January 1987 to December 1991. The top 10 features with the highest feature importance are (in order of decreasing importance): idiovol (CAPM residual volatility), mvel1 (log market capitalization), dolvol (monthly traded value), retvol (return volatility), beta (CAPM beta), mom12m (12-month minus 1-month price momentum), betasq (CAPM beta squared), mom6m (6-month minus 1-month month price momentum), ill (illiquidity), and maxret (30-day max daily return). Rolling 12-month averages were calculated to provide a more discernible trend, with the top 5 shown in Figure 5. Feature importance exhibits strong time-variability. Rolling 12-month average feature importance fell from 14-16% at the start of the out-of-sample period to a trough of 2-6% before rebounding. This indicates that the network would have changed considerably over time. Rapid falls in feature importance can be seen in Figure 5, over 1990-91, 2000-01 and 2008-09. These periods correspond to the U.S. recession in early 1990s, the Dot-com bubble and the Global Financial Crisis, respectively. Thus, market distress may explain rapid changes in feature importance.

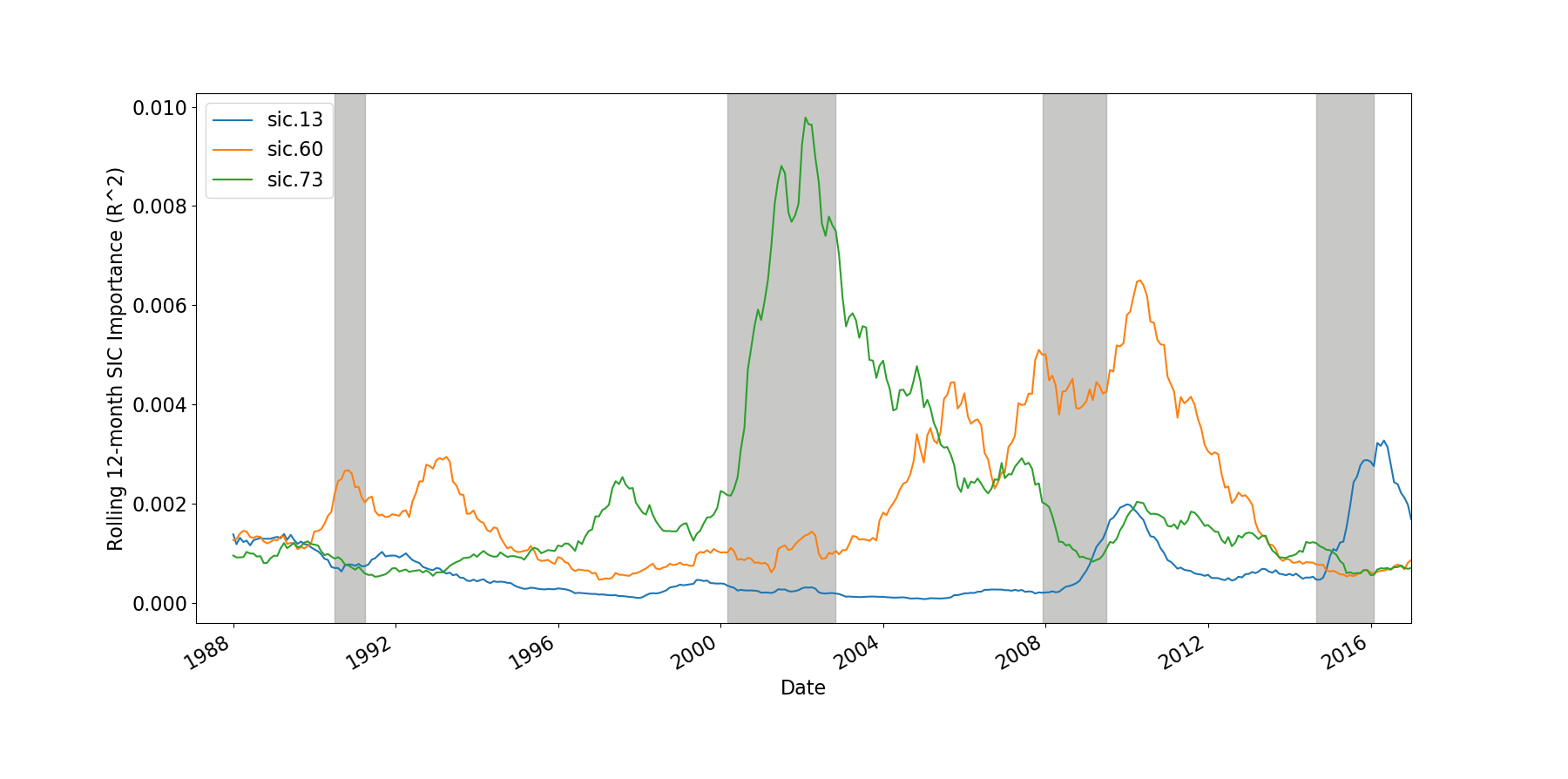

Next, we examine changes in importance for all features on a yearly basis. Figure 6 displays considerable year-to-year variations in feature importance. As there are just a few clusters of features with relatively higher feature importance, the network’s predictions can be attributed to a small set of features. This is likely due to the use of regularization which encourages sparsity. There is an overall trend towards lower importance over time, consistent with publication-informed trading hypothesis of McLean and Pontiff, (2016). For instance, the importance of the market capitalization (mvel1) has decreased over time, as documented in (Horowitz et al., , 2000). There are periods of visibly lower importance for all features, over 2000-02 and 2008-09, and to a lesser extent 1990 and 1997 (Asian financial crisis). If all features have lower importance during market distress, then what explains stock returns during these periods? To answer this question, we turn to importance of sectors, using SIC 13 (Oil and Gas), 60 (Depository Institutions) and 73 (Business Services) as proxies for oil companies, banks and technology companies, respectively. Figure 7 records the rolling 12-month average to baseline prediction of banks, oil and technology companies. The peak of importance of SIC 73 overlaps with the Dot-com bubble and peak of SIC 60 occurs just after the Global Financial Crisis (which started as a sub-prime mortgage crisis). Importance of SIC 13 peaked in 2016, coinciding with the 2014-16 oil glut which saw oil prices fell from over US$100 per barrel to below US$30 per barrel. This is an example of how an exogenous event that is confined to a specific industry impacts on predictability of stock returns. Thus, a plausible explanation for the observed results is that firm features explain less of cross-sectional returns during market shocks, which becomes increasingly explained by industry groups. This is particularly true if the market shock is industry related. For instance, technology companies during the Dot-com bubble, oil companies during an oil crisis and lodging companies during a pandemic. This underscores the importance to have a dynamic model that adapts to changes in the true model.

5.4 Investable simulation

As noted in Section 1, the data set in Gu et al., (2020) contains many stocks that are small and illiquid. The U.S. Securities and Exchange Commission, (2013) defines “microcap” stocks as companies with market capitalization below US$250–300 million and “nanocap” stocks as companies with market capitalization below US$50 million. At the end of 2016, there are over to 1,300 stocks with market capitalization below US$50 million and over 1,800 stocks with market capitalization between US$50 million and US$300 million. Together, microcap and nanocap stocks constitute close to half of the data set as at 2016. Thus, we also provide results excluding these difficult to trade stocks. At the end of every June, we calculate breakpoint based on the 5-th percentile of NYSE listed stocks and exclude stocks with market capitalization below this value. Once rebalanced, the same set of stocks are carried forward until the next rebalance (unless the stock ceases to exist). This cutoff is chosen to approximately include the larger half of U.S.-listed stocks, with the average number of stocks exceeding 2,600. We label this data set as the investable set. To mitigate the impact of outliers, we also winsorize excess returns at and for each month (separately). Winsorized returns are then standardized by subtracting the cross-sectional mean and dividing by cross-sectional standard deviation. Standardization is a common procedure in machine learning and can assists in network training (LeCun et al., , 2012). Predicting a dependent variable with zero mean also removes the need to predict market returns which is embedded in stocks’ excess returns (over risk free rate). This transformation allows the neural network to more easily learn the relationships between relative returns and firm characteristics.

| % | DNN | OES | Ensemble |

|---|---|---|---|

| Metrics | |||

| Pooled | 0.35 | -1.37 | |

| Mean | 0.35 | -1.37 | |

| IC | 5.74 | 6.05 | 6.29 |

| P10-1 | 1.69 | 2.41 | 2.60 |

| Sharpe ratio | 0.69 | 0.82 | 0.96 |

| Hyperparameters | |||

| Mean penalty | 0.0211 | 0.0046 | |

| Mean | 0.87 | 0.10 |

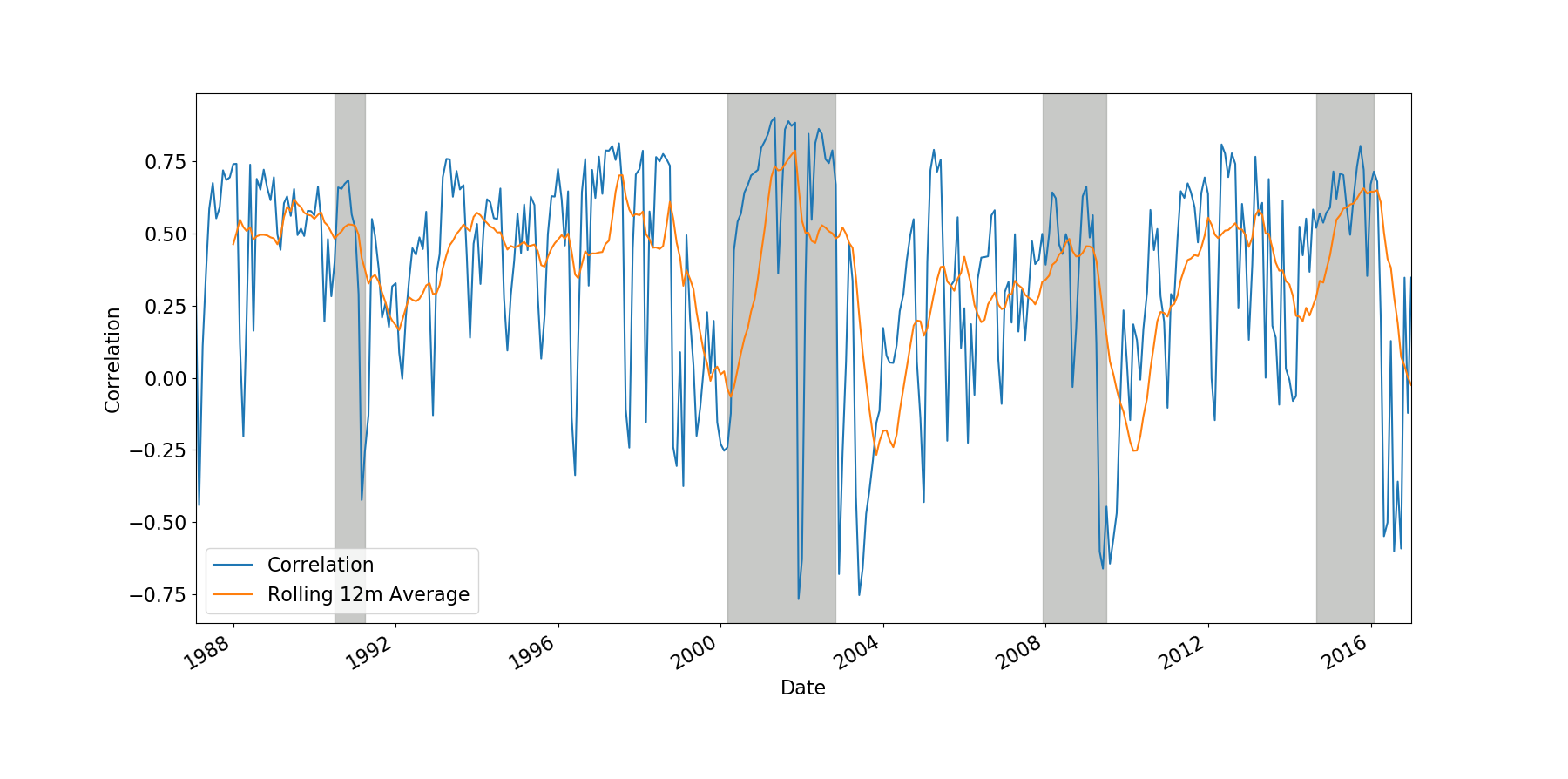

Results based on this investable set are presented in Table 6. Both and IC improved once microcaps are excluded, with OES scoring on IC and DNN on . However, DNN experienced a significant drop in mean decile spread (to per month) and Sharpe ratio (0.69), suggesting that microcaps are significant contributors to the results using the full data set. By contrast, mean decile spread and Sharpe ratio remain stable for OES, at and 0.82, respectively. This indicates that predictive performance of OES was not driven by microcap stocks. We believe this is a meaningful result for practitioners as this subset represents a relatively accessible segment of the market for institutional investors. An ensemble based on the average of cross-sectionally standardized predictions of the two models achieved the best IC, decile spread and Sharpe ratio relative to OES and DNN. Mean monthly correlation between OES and DNN is only . Thus, an ensemble based on the two methods can effectively reduce variance of the predictions. Monthly correlations between the two models are presented in Figure 8. We observe that correlation tends to be lowest immediately after a recession or crisis. We hypothesise that OES is quicker to react to an economic recovery.

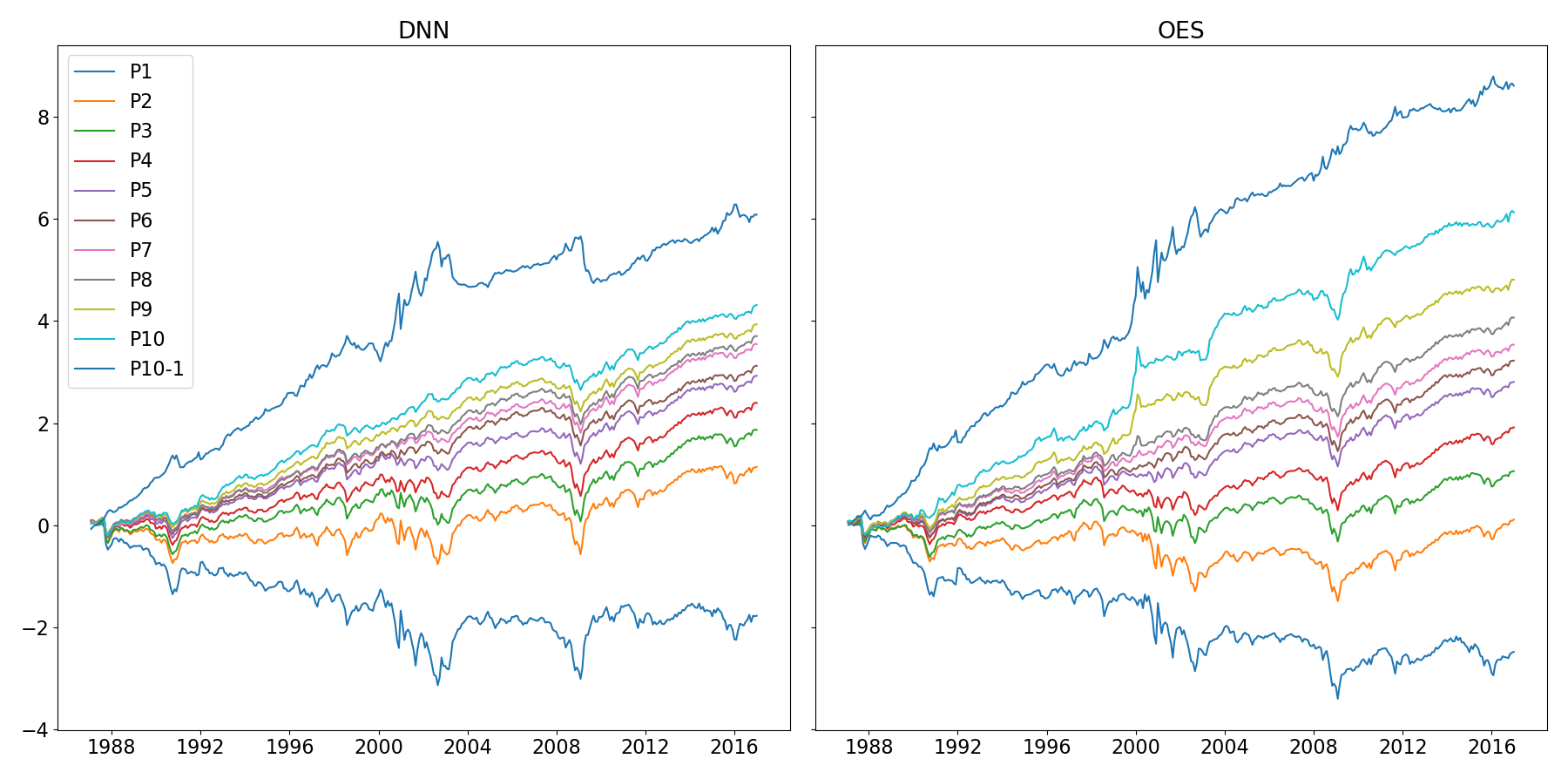

Turning to cumulative decile returns presented in Figure 9, we observe significant drawdowns for DNN during recovery phases of the Dot-com bubble and Global Financial Crisis. P1 of DNN bounced back sharply during these episodes, causing sharp drops in decile spreads and are consistent with momentum crashes (Daniel and Moskowitz, , 2016). By contrast, decile spreads of OES appear to react to the recovery more quickly. Consistent with prior findings, the spreads between decile 3 to 7 are also better under OES than DNN in the investable set. Given these favorable characteristics, practitioners are likely to find OES a useful tool to add to the armory of prediction models.

6 Conclusions

Stock return prediction is an arduous task. The true model is noisy, complex and time-varying. Mainstream deep learning research has focused on problems that do not vary over time and, arguably, time-varying applications have seen less advancements. In this work, we propose an online early stopping algorithm that is easy to implement and can be applied to an existing network setup. We show that a network trained with OES can track a time-varying function and achieve superior performance to DTS-SGD, a recently proposed online non-convex optimization technique. Our method is also significantly faster, as only two periods of training data are required at each iteration, compared to the pooled method used in Gu et al., (2020) which re-trains the network on the entire data set annually. In our tests, the pooled method took to iterate through the entire data set (an ensemble of ten networks therefore takes )101010Tests performed on AMD Ryzen™ 7 3700X, Python 3.7.3, Tensorflow 1.12.0 and Keras 2.2.4. Hyperparameter grid search was performed concurrently.. By contrast, our method took for a single pass over the entire data set (an ensemble of ten networks took ).

Gu et al., (2020) suggested that a small data set and low signal-to-noise ratio were reasons for the lack of improvement with a deeper network. To this end, we show that only a handful of features contribute to predictive performance. This may be due to correlation between features and the use of regularization which encourages sparsity. We also find evidence of time-varying feature importance. In particular, features such as log market capitalization (the size effect) and 12-month minus 1-month momentum have seen a gradual decrease to their importance towards the end of our test period, consistent with the publication-informed trading hypothesis of McLean and Pontiff, (2016). We find that sectors can also exhibit time-varying importance (for instance, technology stocks during the Dot-com bubble). These results have strong implications for practitioners forecasting stock returns using well known asset pricing anomalies. Excluding microcaps, we find that OES offers superior predictive performance in a subuniverse that is accessible to institutional investors. We find that correlation between OES and DNN is at its lowest after a recession or crisis. We argue that this is driven by faster reactions of OES in tracking the recovery. An ensemble based on the average prediction of the two models achieves the best IC and Sharpe ratio, suggesting that the two methods may be complementary.

From an academic perspective, recent advances in deep learning such as dropout and residual connections (He et al., , 2016) may allow deeper networks to be trained, which enables more expressive asset pricing models. Given the higher variance of predictions produced by OES, future work should explore alternative methods of regularization including dropouts, penalty or a mixture of regularization techniques. Lastly, we believe time-varying neural network is a relatively less explored domain of machine learning that has applications in both prediction and analysis of asset returns.

References

- Abe and Nakayama, (2018) Abe, M. and Nakayama, H. (2018). Deep learning for forecasting stock returns in the cross-section. In arXiv.

- Ambachtsheer, (1974) Ambachtsheer, K. (1974). Profit potential in an almost efficient market. Journal of Portfolio Management, 1(1):84.

- Aydore et al., (2019) Aydore, S., Zhu, T., and Foster, D. P. (2019). Dynamic local regret for non-convex online forecasting. In Wallach, H., Larochelle, H., Beygelzimer, A., d’Alché Buc, F., Fox, E., and Garnett, R., editors, Advances in Neural Information Processing Systems 32, pages 7980–7989. Curran Associates, Inc.

- Bergmeir et al., (2018) Bergmeir, C., Hyndman, R., and Koo, B. (2018). A note on the validity of cross-validation for evaluating autoregressive time series prediction. Computational Statistics & Data Analysis, 120:70–83.

- Bossaerts and Hillion, (1999) Bossaerts, P. and Hillion, P. (1999). Implementing statistical criteria to select return forecasting models: What do we learn? The Review of Financial Studies, 12(2):405–428.

- Cont, (2001) Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1:223–236.

- Cover, (1991) Cover, T. M. (1991). Universal portfolios. Mathematical Finance, 1(1):1–29.

- Cybenko, (1989) Cybenko, G. (1989). Approximation by superpositions of a sigmoidal function. Mathematics of Control, Signals and Systems, 2(4):303–314.

- Daniel and Moskowitz, (2016) Daniel, K. and Moskowitz, T. J. (2016). Momentum crashes. Journal of Financial Economics, 122(2):221–247.

- Fabozzi et al., (2011) Fabozzi, F. J., Grant, J. L., and Vardharaj, R. (2011). Common Stock Portfolio Management Strategies, volume 1, chapter 9, pages 229–270. John Wiley & Sons, Ltd.

- Fama and French, (1992) Fama, E. F. and French, K. R. (1992). The cross-section of expected stock returns. Journal of Finance, 47(2):427–465.

- Gama et al., (2014) Gama, J. a., Žliobaitė, I., Bifet, A., Pechenizkiy, M., and Bouchachia, A. (2014). A survey on concept drift adaptation. ACM Computing Surveys, 46(4):44:1–44:37.

- Goodfellow et al., (2016) Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep Learning. MIT Press. http://www.deeplearningbook.org.

- Green et al., (2017) Green, J., Hand, J. R. M., and Zhang, X. F. (2017). The characteristics that provide independent information about average U.S. monthly stock returns. The Review of Financial Studies, 30(12):4389–4436.

- Grinold and Kahn, (1999) Grinold, R. and Kahn, R. (1999). Active Portfolio Management: A Quantitative Approach for Producing Superior Returns and Controlling Risk. McGraw-Hill Education.

- Gu et al., (2020) Gu, S., Kelly, B., and Xiu, D. (2020). Empirical asset pricing via machine learning. The Review of Financial Studies, 33(5):2223–2273.

- Harvey et al., (2016) Harvey, C. R., Liu, Y., and Zhu, H. (2016). … and the cross-section of expected returns. The Review of Financial Studies, 29(1):5–68.

- Hazan et al., (2017) Hazan, E., Singh, K., and Zhang, C. (2017). Efficient regret minimization in non-convex games. In Precup, D. and Teh, Y. W., editors, Proceedings of the 34th International Conference on Machine Learning, ICML 2017, volume 70 of ICML, pages 1433–1441, Sydney, Australia. PMLR.

- He et al., (2016) He, K., Zhang, X., Ren, S., and Sun, J. (2016). Deep residual learning for image recognition. In Agapito, L., Berg, T., Kosecka, J., and Zelnik-Manor, L., editors, Proceedings of the 2016 IEEE Conference on Computer Vision and Pattern Recognition (CVPR), CVPR, pages 770–778, Las Vegas, NV, USA. IEEE.

- Hornik et al., (1989) Hornik, K., Stinchcombe, M., and White, H. (1989). Multilayer feedforward networks are universal approximators. Neural Networks, 2(5):359––366.

- Horowitz et al., (2000) Horowitz, J. L., Loughran, T., and Savin, N. (2000). The disappearing size effect. Research in Economics, 54(1):83–100.

- Kingma and Ba, (2015) Kingma, D. P. and Ba, J. (2015). Adam: A method for stochastic optimization. In Bengio, Y. and LeCun, Y., editors, Proceedings of the 3rd International Conference on Learning Representations, ICLR 2015, ICLR, San Diego, CA, USA.

- LeCun et al., (2012) LeCun, Y. A., Bottou, L., Orr, G. B., and Müller, K.-R. (2012). Efficient BackProp, pages 9–48. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Lev and Srivastava, (2019) Lev, B. and Srivastava, A. (2019). Explaining the recent failure of value investing. In SSRN.

- Mahsereci et al., (2017) Mahsereci, M., Balles, L., Lassner, C., and Hennig, P. (2017). Early stopping without a validation set. CoRR, abs/1703.09580.

- McLean and Pontiff, (2016) McLean, R. D. and Pontiff, J. (2016). Does academic research destroy stock return predictability? The Journal of Finance, 71(1):5–32.

- Messmer, (2017) Messmer, M. (2017). Deep learning and the cross-section of expected returns. In SSRN.

- Morgan and Bourlard, (1990) Morgan, N. and Bourlard, H. A. (1990). Generalization and parameter estimation in feedforward nets: Some experiments. In Touretzky, D. S., editor, Advances in Neural Information Processing Systems 2, pages 630–637. Morgan-Kaufmann.

- Pesaran and Timmermann, (1995) Pesaran, M. H. and Timmermann, A. (1995). Predictability of stock returns: Robustness and economic significance. Journal of Finance, 50:1201–1228.

- Prechelt, (1998) Prechelt, L. (1998). Early stopping - but when? In Neural Networks: Tricks of the Trade, This Book is an Outgrowth of a 1996 NIPS Workshop, pages 55–69, London, UK, UK. Springer-Verlag.

- Reed, (1993) Reed, R. D. (1993). Pruning algorithms-a survey. Transactions on Neural Networks, 4(5):740–747.

- Rosenberg et al., (1985) Rosenberg, B., Reid, K., and Lanstein, R. (1985). Persuasive evidence of market inefficiency. Journal of Portfolio Management, 11(3):9–16. Name - New York Stock Exchange; Copyright - Copyright Euromoney Institutional Investor PLC Spring 1985; Last updated - 2015-05-25.

- Rossi and Inoue, (2012) Rossi, B. and Inoue, A. (2012). Out-of-sample forecast tests robust to the choice of window size. Journal of Business & Economic Statistics, 30(3):432–453.

- Schroff et al., (2015) Schroff, F., Kalenichenko, D., and Philbin, J. (2015). Facenet: A unified embedding for face recognition and clustering. In Grauman, K., Learned-Miller, E., Torralba, A., and Zisserman, A., editors, Proceedings of the 2015 IEEE Conference on Computer Vision and Pattern Recognition (CVPR), CVPR, pages 815–823, Boston, MA, USA. IEEE.

- Shalev-Shwartz, (2012) Shalev-Shwartz, S. (2012). Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194.

- Sjöberg and Ljung, (1995) Sjöberg, J. and Ljung, L. (1995). Overtraining, regularization and searching for a minimum, with application to neural networks. International Journal of Control, 62(6):1391–1407.

- Sutskever et al., (2013) Sutskever, I., Martens, J., Dahl, G., and Hinton, G. (2013). On the importance of initialization and momentum in deep learning. In Dasgupta, S. and McAllester, D., editors, Proceedings of the 30th International Conference on Machine Learning, ICML 2013, volume 28 of ICML, pages 1139–1147, Atlanta, Georgia, USA. PMLR.

- Sutskever et al., (2014) Sutskever, I., Vinyals, O., and Le, Q. V. (2014). Sequence to sequence learning with neural networks. In Ghahramani, Z., Welling, M., Cortes, C., Lawrence, N. D., and Weinberger, K. Q., editors, Advances in Neural Information Processing Systems 27, pages 3104–3112. Curran Associates, Inc.

- U.S. Securities and Exchange Commission, (2013) U.S. Securities and Exchange Commission (2013). Microcap stock: A guide for investors. https://www.sec.gov/reportspubs/investor-publications/investorpubsmicrocapstockhtm.html. Accessed: 2021-01-03.

- Weigand, (2019) Weigand, A. (2019). Machine learning in empirical asset pricing. Financial Markets and Portfolio Management, 33:93–104.

- Welch and Goyal, (2008) Welch, I. and Goyal, A. (2008). A comprehensive look at the empirical performance of equity premium prediction. The Review of Financial Studies, 21(4):1455–1508.