Adaptive exponential power distribution

with moving estimator

for nonstationary time series

Abstract

While standard estimation assumes that all datapoints are from probability distribution of the same fixed parameters , we will focus on maximum likelihood (ML) adaptive estimation for nonstationary time series: separately estimating parameters for each time based on the earlier values using (exponential) moving ML estimator for and some . Computational cost of such moving estimator is generally much higher as we need to optimize log-likelihood multiple times, however, in many cases it can be made inexpensive thanks to dependencies. We focus on such example: exponential power distribution (EPD) family, which covers wide range of tail behavior like Gaussian () or Laplace () distribution. It is also convenient for such adaptive estimation of scale parameter as its standard ML estimation is being average . By just replacing average with exponential moving average: we can inexpensively make it adaptive. It is tested on daily log-return series for DJIA companies, leading to essentially better log-likelihoods than standard (static) estimation, with optimal tails types varying between companies. Presented general alternative estimation philosophy provides tools which might be useful for building better models for analysis of nonstationary time-series.

Keywords: nonstationary time series, exponential power distribution, adaptive models

I Introduction

In standard parametric estimation we choose some density family and assume that all datapoints are from this distribution using the same parameters . For maximum likelihood (ML) estimation we find maximizing having equal contribution of all datapoints . This estimation is perfect for i.i.d. sequence from stationary time series. For distinction, in analogy to static-adaptive separation of models in data compression [1], let us refer to it as static estimation.

For nonstationary time series these parameters might evolve in time, like estimated density in the bottom of Fig. 1. To estimate such parameter evolution, we focus here on adaptive estimation using moving estimator [2], which for time finds maximizing moving likelihood based only on the previously seen datapoints, for example using exponentially weakening weights:

| (1) |

where defines rate of weakening of contribution of the old points in such exponential moving average. For it becomes ML estimation based on all previous points. In practice usually , generally might differ between parameters (e.g. here for , for ).

While standard static estimation is performed once - finding a compromise for all datapoints, discussed adaptive estimation is generally much more computationally expensive - needs to be performed separately for each . However, in some situations it can be optimized at least for some parameters, by making it an evolving estimation exploiting previously found state. For example when standard ML estimation is given by average over some function of datapoints, we can transform it to adaptive estimation by just replacing this average with exponential moving average.

Specifically, we will focus on exponential power distribution (EPD) [3] family: , which covers wide range of tail behaviors like Gaussian () or Laplace () distribution. It is also convenient for such adaptive estimation of scale parameter as in standard ML estimation: is average of . We can transform it to adaptive estimation by just replacing average with exponential moving average: .

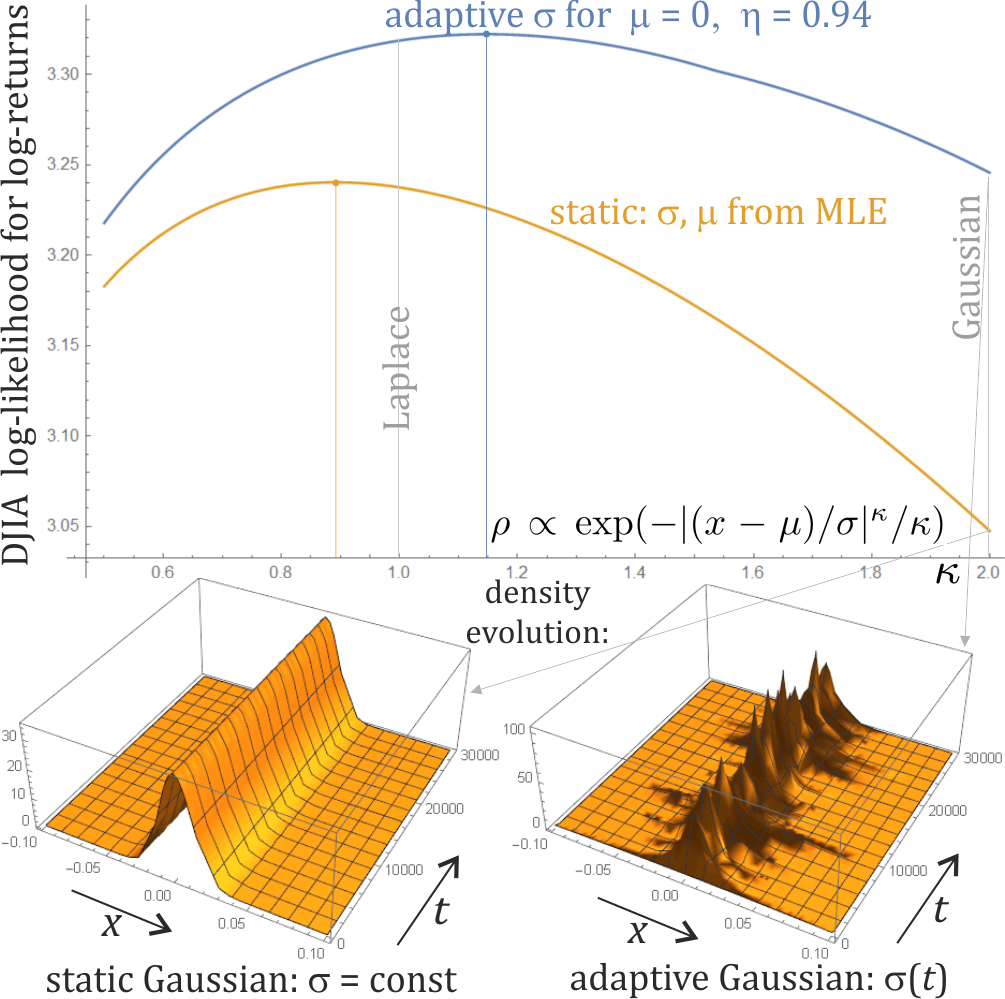

On example of 100 years Dow Jones Industrial Average (DJIA) daily log-returns and 10 years for 29 its recent companies, we have tested that such adaptive estimation of leads to essentially better log-likelihoods than standard static estimation as we can see in Fig. 1, 2. Surprisingly, the parameter defining tail behavior, usually just chosen as by assuming Gaussian distribution, turns out less universal - various companies have different optimal , much closer to heavier tail of Laplace distribution.

The discussed general philosophy of adaptive estimation directly focuses on non-stationarity of time series - trying to model evolution of parameters. Its applications like adaptive EPD can be used as a building block for the proper methods like ARIMA-GARCH family. Surprisingly, such adaptive EPD estimation (just ) for this data already turns out comparable with much more sophisticated standard methods like GARCH(1,1) [4], represented as red lines in Fig. 2. These more sophisticated models assume some arbitrary evolution of parameters, while moving estimator does not do it (is agnostic) - just shifts the estimator to get local parameters.

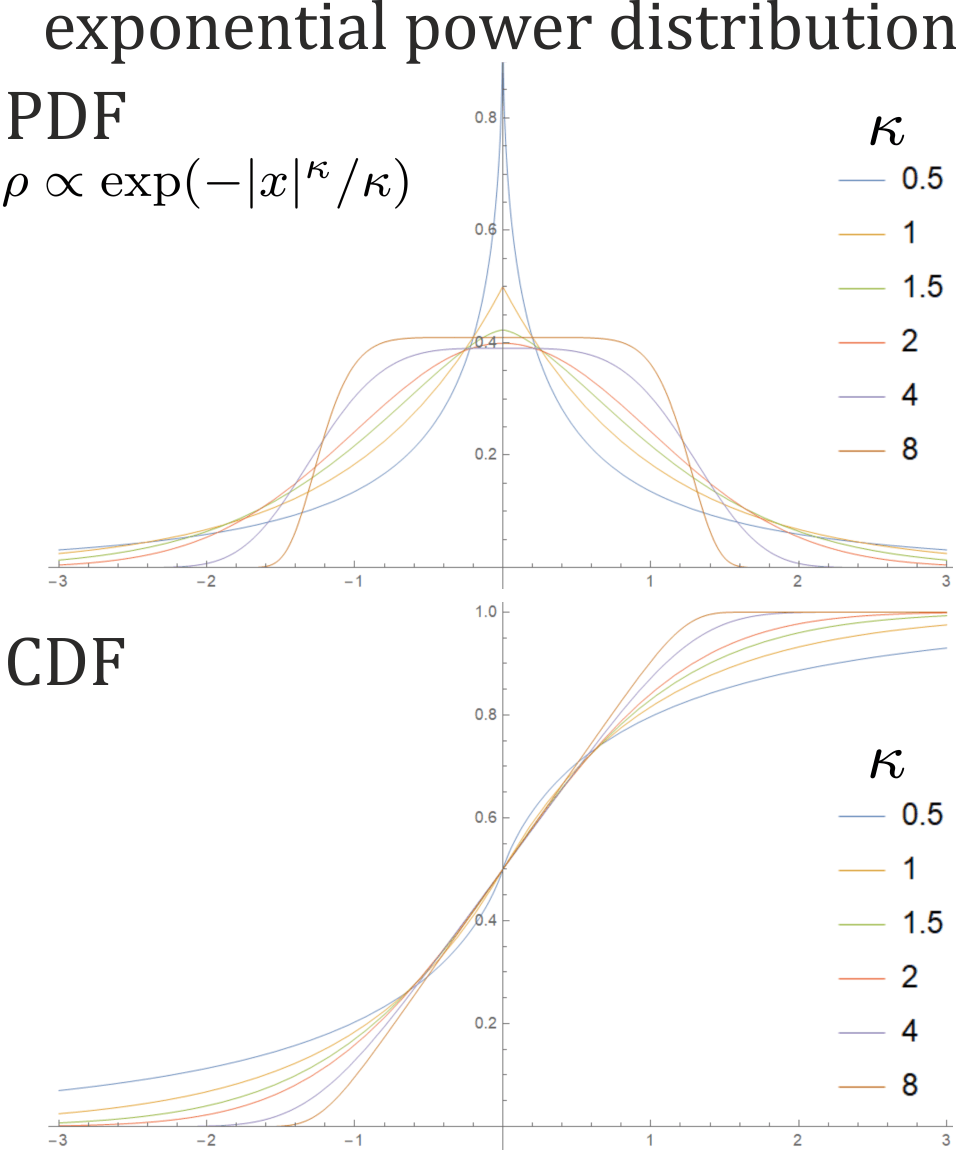

II Exponential power distribution (EPD)

For shape parameter, scale parameter and location, probability distribution function (PDF, ) and cumulative distribution function (CDF, ) of EPD are correspondingly:

| (2) |

where is Euler gamma function, is regularized incomplete gamma function. These PDF and CDF are visualized in Fig. 3.

II-A Static parameter estimation

Let us start with standard static ML estimation: assuming i.i.d sequence. For generality let use weights of points, assuming to imagine them as contribution of each point. In standard static estimation we assume equal contributions.

Such general weighted log-likelihood is:

| (3) |

From necessary condition we get maximum likelihood estimator for scale parameter (assuming fixed ):

| (4) |

There is no general analytic formula for the remaining parameters, but they can be estimated numerically. Estimation of the location can be expressed as:

| (5) |

for Gaussian distribution it is just mean of values . For Laplace distribution it is their median. Some practical approximation, e.g. as initial value of more sophisticated estimation, might be just using mean for all .

To approximately estimate the shape parameter , we can for example use the method of moments, especially that variance of EPD has simple form:

| (6) |

which is strongly decreasing with , e.g. for Laplace distribution, for Gaussian distribution.

II-B Adaptive estimation of scale parameter

Let us define moving log-likelihood for time using only its previous points, exponentially weakening weights of the old points to try to estimate parameters describing local behavior:

| (7) |

to get (exponential moving) weights summing to 1.

Now fixing , and optimizing , from (4) we get

| (8) |

which is exponential moving average (EMA), can be evolved iteratively:

| (9) |

initial has to be chosen arbitrarily.

We have transformed static estimator given by average, into adaptive estimator by just replacing average with exponential moving average. Observe that it can be analogously done for any estimator of form.

II-C Generalization, interpretation and choice of rate

To generalize the above, assume that estimation of parameter is analogously given by average ():

| (10) |

For the above parameter of EPD with fixed, we would have , .

Generally we analogously have adaptation for

| (11) |

Denoting , we can write it as:

| (12) |

allowing to imagine evolution of as random walk with step from random variable, which can evolve in time here. Generally is proportional to speed of this random walk.

This interpretation could be used to optimize the choice of , separately for each parameter, also its potential evolution. For example by calculating (e.g. exponential moving averaged) square root of variance of sequence, and evaluate square root of variance of random variable - dividing them we get estimation of parameter.

We can also try to adapt parameter based on data to optimize some final evaluation like:

for log-likelihood, or e.g. minus squared error for MSE.

E.g. using 12 recurrence, we can condition its time term with the current rate, :

| (13) |

what allows e.g. for gradient optimization of for the next step, like for some tiny use update.

We leave its details for future work as improvement by optimization from the fixed was practically negligible for the analyzed daily log-return data. Fig. 2 presents such difference by green plot for , and blue for individually optimized .

II-D Approximated adaptive estimation of ,

While in practice the most important seems adaptation of scale parameter , there might be also worth to consider adaptation of the remaining parameters. Their estimation rather does not have analytical formulas already in static case, hence for adaptive case we should look for practical approximations, preferably also based on EMA for inexpensive updating.

Location is mean of such parametric distribution, just using mean of datapoints as its estimator is optimal for Gaussian distribution case , and can be easily transformed to adaptive estimation. Hence a natural approximated estimation is analogous:

| (14) |

for e.g. and some chosen rate , not necessarily equal (for this data , ).

Adaptive estimation of seems more difficult. Some example of approximation is using method of moments e.g. with (6) formula, especially that we can naturally get adaptive estimation of moments with EMA. For example as here using additional analogous EMA for estimated recent mean :

Another general approach are gradient methods, adapting chosen parameter(s) e.g. to increase log-likelihood contribution. For example for some tiny :

III DJIA log-returns tests

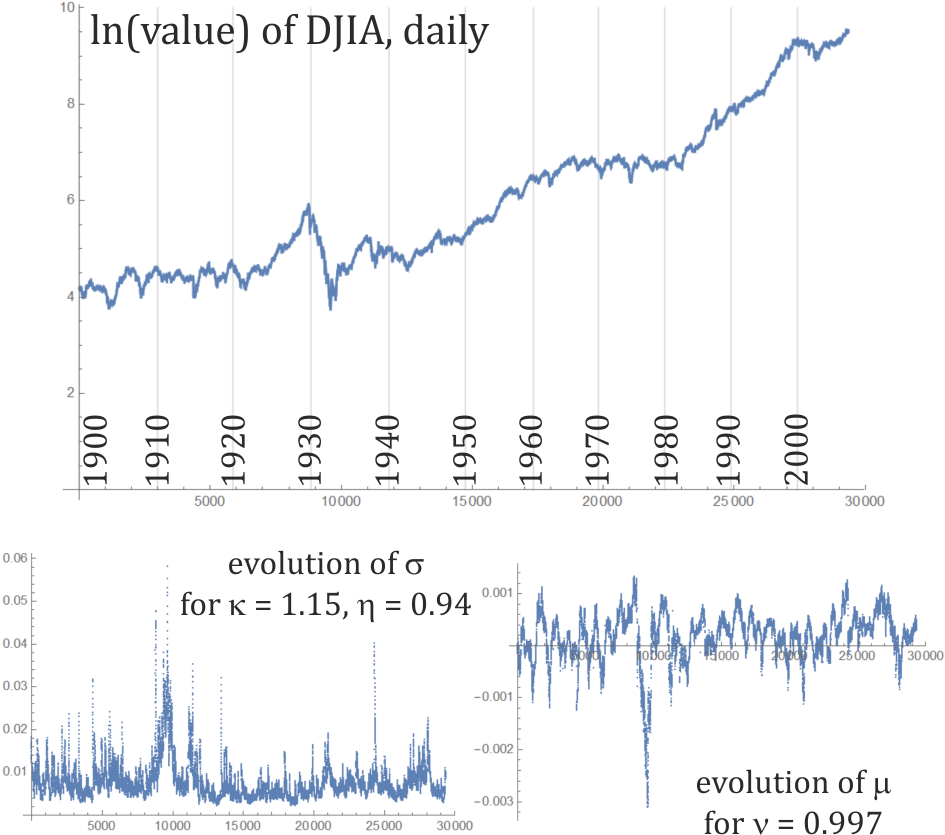

We will now look at evaluation of these methodologies from perspective of years daily Dow Jones index111Source of DJIA time series: http://www.idvbook.com/teaching-aid/data-sets/the-dow-jones-industrial-average-data-set/, values , working on log-returns sequence for for , summarized in Fig. 1.

As evaluation there is used mean log-likelihood: , where in static setting has constant parameters chosen by MLE, in adaptive these parameters evolve in time: are estimated based on previous values.

In adaptive settings there was arbitrarily chosen initial , , and from numerical search: , . Here are the obtained parameters and mean log-likelihoods for various settings:

-

•

static Gaussian () distribution has MLE mean , , giving ,

-

•

static Laplace () distribution has MLE median , , giving ,

-

•

static EPD has MLE , , , giving ,

-

•

Gaussian with and adaptive gives ,

-

•

Laplace with and adaptive gives ,

-

•

EPD optimal with and adaptive gives ,

-

•

Gaussian with adaptive and gives ,

-

•

Laplace with adaptive and gives ,

-

•

EPD with adaptive and gives .

We can see that standard assumption of static Gaussian can be essentially improved both by going to closer to Laplace distribution, and by switching to adaptive estimation of scale parameter . Additional adaptive estimation of location provides some tiny further improvement here. The final used evolution of and is presented in Fig. 4.

There were also trials for adapting , but were not able to provide a noticeable improvement here.

Figure 2 additionally contains such evaluation of log-returns for 29 out of 30 companies used for this index in September 2018. Daily prices for the last 10 years were downloaded from NASDAQ webpage (www.nasdaq.com) for all but DowDuPont (DWDP) - there were used daily close values for 2008-08-14 to 2018-08-14 period ( values) for the remaining 29 companies: 3M (MMM), American Express (AXP), Apple (AAPL), Boeing (BA), Caterpillar (CAT), Chevron (CVX), Cisco Systems (CSCO), Coca-Cola (KO), ExxonMobil (XOM), Goldman Sachs (GS), The Home Depot (HD), IBM (IBM), Intel (INTC), Johnson&Johnson (JNJ), JPMorgan Chase (JPM), McDonald’s (MCD), Merck&Company (MRK), Microsoft (MSFT), Nike (NKE), Pfizer (PFE), Procter&Gampble (PG), Travelers (TRV), UnitedHealth Group (UNH), United Technologies (UTX), Verizon (VZ), Visa (V), Walmart (WMT), Walgreens Boots Alliance (WBA) and Walt Disney (DIS).

III-A Further improvements with Hierarchical Correlation Reconstruction

The estimated parametric distributions of variables in separate times often leave statistical dependencies which can be further exploited.

For this purpose, we can use the best found model, here EPD with adaptive and for DJIA sequence, and use it for normalization of variables to nearly uniform distributions by going through cumulative distribution functions (CDF) of estimated parametric distributions: transform to sequence.

We can then take e.g. neighboring values of sequence, which should be from approximately uniform distribution on . In Hierarchical Correlation Reconstruction [6] we estimate distortion from this uniform distribution as a polynomial of modelled static or adaptive coefficients.

Obtained mean log-likelihood improvement for single variables was for static model (in 10-fold cross-validation), for adaptive (MSE moving estimator) - using polynomial model to improve the original EPD model. Polynomial model can improve behavior of body of the distribution, but has not much influence on the tails - EPD should mainly focus on proper tail behavior.

For modelling joint distribution of two neighboring variables : using the previous value to predict conditional distribution, the log-likelihood improvement was for static model, for adaptive. Analogously for three neighboring variables the improvement was for static model, for adaptive.

IV Adaptive asymmetric EPD

While EPD is a symmetric distribution, real data might have asymmetric e.g. tail behavior. To include it in parametric model, we can just glue two (2) formulas into asymmetric EPD (AEPD [5]) by using different shape parameter and/or scale parameter for the left and right part - generally:

| (15) |

for normalization as in (2) and is probability of the left part (), for standard symmetric.

For this parametrization is not necessarily continuous. It often can be ignored, e.g. when using CDF to normalize variable as in III-A. If it is an issue, we could smoothen transition e.g. by multiplying the left part by some sigmoid function of , the right one by one minus this functions, but it would require many arbitrary choices.

Alternatively, we can ensure continuity by satisfying

for example by choosing

| (16) |

There are many ways for AEPD adaptive estimation, some remarks:

-

•

Directly use e.g. moving estimator, but it would have high computational cost.

-

•

As previously, not optimal but a natural choice for estimator is .

-

•

While being only an approximation, it is tempting to treat and as being correspondingly from left or right separate distribution, updating e.g. scale parameter for exactly one of them:

-

•

As corresponds to probability of , we could update it e.g. as for some , where when is true, otherwise. However, it might be safer to use (16) continuity condition instead.

-

•

We can always use evolution of parameters based on gradients to improve log-likelihood, what should be considered separately for each parameter, using separate (tiny) learning rates and update e.g.

This is first order method, there might be also considered second order - trying to locally model the evaluation criterion as parabola or paraboloid of parameters and remain in its extremum, briefly discussed in [2].

To summarize, while we could always use moving estimator at high computational cost, choosing a more practical approximation has often large a freedom, also its optimization might be data dependent.

However, such e.g. AEPD model can/should be complemented with further models, like using its CDF to normalize variables to nearly uniform marginal distributions, then e.g. model joint distribution in a window as a polynomial (static or adaptive) as in III-A. Such polynomial model can extract and exploit complex behavior of body of the distribution, but not of the tail. Hence on e.g. AEPD normalization level we should mainly focus on getting proper tail behavior, maybe even using general non-continuous (15) form, as continuity is not required for normalization, and this non-continuity can be further smoothed with polynomials.

V Conclusions and further work

While applied time series analysis often uses static Gaussian distribution, there was shown that simple inexpensive generalization: to adaptive distribution, and to more general exponential power distribution, can essentially improve standard evaluation: log-likelihood.

This article is focused only on the basic general approaches, in practice it can be further improved by combining with complementing methods, for example mentioned in Section III-A additional high parameter modelling of joint distribution for variables normalized with CDF of distributions discussed here.

While discussed adaptive estimation of scale parameter is MLE-optimal, the remaining parameters rather require some approximations - worth further exploration of better approaches.

Another open question is finding better ways for choosing rate of exponential moving average, also varying in time to include changing rate of forgetting e.g. due to varying time differences.

In contrast e.g. to Levy/stable distributions, the discussed EPD does not cover heavy tails (1/polynomial density) - it is worth to search for practical adaptive estimation also for other types of parametric distributions.

This appendix contains Wolfram Mathematica source for used evaluation of adaptive exponential power distribution (vectorized for performance). The Prepend inserts initial values in the beginning, then [[1;;-2]] removes the last value, so the used density parameter is modeled based only on history:

(* xt: sequence of values, kap: fixed kappa *) (* eta, nu: EMA coefficients *) (* mu1, sigma1: initial mu, sigma *) cons = kap^(-1/kap)/2 /Gamma[1 + 1/kap]; mu = ExponentialMovingAverage[ Prepend[xt, mu1], nu][[1 ;; -2]]; sigma = ExponentialMovingAverage[ Prepend[Abs[xt - mu]^kap, sigma1^kap] , eta][[1 ;; -2]]^(1/kap); rho=cons*Exp[-((Abs[xt-mu]/sigma)^kap)/kap]/sigma; Mean[Log[rho]] (* mean log-likelihood *)

References

- [1] R. N. Williams, Adaptive data compression. Springer Science & Business Media, 2012, vol. 110.

- [2] J. Duda, “Parametric context adaptive laplace distribution for multimedia compression,” arXiv preprint arXiv:1906.03238, 2019.

- [3] D. Zhu and V. Zinde-Walsh, “Properties and estimation of asymmetric exponential power distribution,” Journal of econometrics, vol. 148, no. 1, pp. 86–99, 2009.

- [4] T. Bollerslev, “Generalized autoregressive conditional heteroskedasticity,” Journal of econometrics, vol. 31, no. 3, pp. 307–327, 1986.

- [5] D. Zhu and V. Zinde-Walsh, “Properties and estimation of asymmetric exponential power distribution,” Journal of econometrics, vol. 148, no. 1, pp. 86–99, 2009.

- [6] J. Duda, “Exploiting statistical dependencies of time series with hierarchical correlation reconstruction,” arXiv preprint arXiv:1807.04119, 2018.