Mortality and Healthcare: a Stochastic Control Analysis under Epstein-Zin Preferences

Abstract

This paper studies optimal consumption, investment, and healthcare spending under Epstein-Zin preferences. Given consumption and healthcare spending plans, Epstein-Zin utilities are defined over an agent’s random lifetime, partially controllable by the agent as healthcare reduces mortality growth. To the best of our knowledge, this is the first time Epstein-Zin utilities are formulated on a controllable random horizon, via an infinite-horizon backward stochastic differential equation with superlinear growth. A new comparison result is established for the uniqueness of associated utility value processes. In a Black-Scholes market, the stochastic control problem is solved through the related Hamilton-Jacobi-Bellman (HJB) equation. The verification argument features a delicate containment of the growth of the controlled morality process, which is unique to our framework, relying on a combination of probabilistic arguments and analysis of the HJB equation. In contrast to prior work under time-separable utilities, Epstein-Zin preferences facilitate calibration. The model-generated mortality closely approximates actual mortality data in the US and UK; moreover, the efficacy of healthcare can be calibrated and compared between the two countries.

MSC (2010): 91G10, 93E20.

JEL: G11, I12

Keywords: Consumption-investment problem, Healthcare, Mortality, Gompertz’ law, Epstein-Zin utilities, Random horizons, Backward stochastic differential equations.

1 Introduction

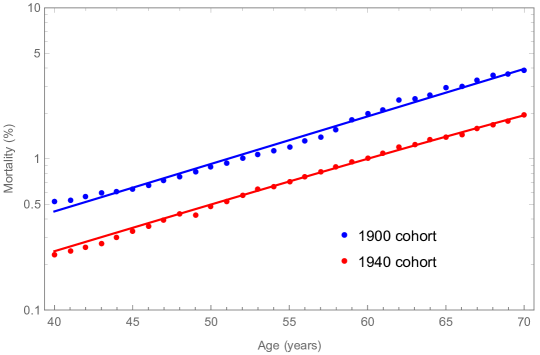

Mortality, the probability that someone alive today dies next year, exhibits an approximate exponential growth with age, as observed by Gompertz [13] in 1825. Despite the steady decline of mortality at all age groups across different generations, the exponential growth of mortality within each generation has remained remarkably stable, which is called the Gompertz law. Figure 1 displays this clearly: in the US, mortality of the cohort born in 1900 and that of the cohort born in 1940 grew exponentially at a similar rate; the latter is essentially shifted down from the former.

At the intuitive level, this “shift down” of mortality across generations can be ascribed to continuous improvement of healthcare and accumulation of wealth. Understanding precisely how this “shift down” materializes demands careful modeling in which wealth evolution, healthcare choices, and the resulting mortality are all endogenous. Standard models of consumption and investment do not seem to serve the purpose: the majority, e.g. [35], [25], [26], and [30], consider no more than exogenous mortality, leaving no room for healthcare.111As an exception, the literature on health capital, initiated by [14], considers endogenous healthcare. Despite its development towards more realistic models, e.g. [11], [10], [36], [18], [16], the Gompertz law remains largely absent.

Recently, Guasoni and Huang [15] directly modeled the effect of healthcare on mortality: healthcare reduces Gompertz’ natural growth rate of mortality, through an efficacy function that characterizes the effect of healthcare spending in a society. Healthcare, as a result, indirectly increases utility from consumption accumulated over a longer lifetime. Under the constant relative risk aversion (CRRA) utility function , , an optimal strategy of consumption, investment, and healthcare spending is derived in [15], where the constraint is justified by interpreting as an agent’s elasticity of intertemporal substitution (EIS). Specifically, to model mortality endogenously, we need to be cautious of potential preference for death over life. To avoid this, [15] assumes that an agent can leave a fraction , not necessarily all, of his wealth at death to beneficiaries, reflecting the effect of inheritance and estate taxes. It is shown in [15] that the optimization problem is ill-posed for . Indeed, with , or EIS less than one, the income effect of future loss of wealth at death is so substantial that the agent reduces current consumption to zero, leading to the ill-posedness; see below [15, Proposition 3.2] for details.

Despite the progress in [15], the artificial relation that EIS is the reciprocal of relative risk aversion, forced by CRRA utility functions, significantly restricts its applications. Although a preliminary calibration was carried out in [15, Section 5], it was not based on the full-fledged model in [15], but a simplified version without any risky asset. Indeed, once a risky asset is considered, it is unclear whether should be calibrated to relative risk aversion or EIS. More crucially, empirical studies largely reject relative risk aversion and EIS being reciprocals to each other: it is widely accepted that EIS is larger than one (see e.g. [3], [2], [6], and [5]), while numerous estimates of relative risk aversion are also larger than one (see e.g. [32], [3], and [17]).

In this paper, we investigate optimal consumption, investment, and healthcare spending under preferences of Epstein-Zin type, which disentangle relative risk aversion (denoted by ) and EIS (denoted by ). In particular, we impose throughout the paper

Assumption 1.

and .

This specification implies a preference for early resolution of uncertainty (as explained in [31]), and conforms to empirical estimations mentioned above.

Our Epstein-Zin utility process has several distinctive features. First, it is defined on a random horizon , the death time of an agent. Prior studies on Epstein-Zin utilities focus on a fixed-time horizon; see e.g. [8], [28], [23], [29], [22], and [34]. To the best our knowledge, random-horizon Epstein-Zin utilities are developed for the first time in Aurand and Huang [1], where the horizon is assumed to be a stopping time adapted to the market filtration. Our studies complement [1], by allowing for a stopping time (i.e. the death time) that need not depend on the financial market. Second, the random horizon is controllable: one slows the growth of mortality via healthcare spending, which in turn changes the distribution of . Note that a controllable random horizon was considered in a few prior studies, e.g. [21] and [9], but all under time-separable utilities. Third, to formulate our Epstein-Zin utilities, we need not only a given consumption stream (as in the literature), but also a specified healthcare spending process . Given the pair , the Epstein-Zin utility is defined as the right-continuous process that satisfies a random-horizon dynamics (i.e. (2.6) below), with a jump at time . Thanks to techniques of filtration expansion, we decompose as a function of and a process that solves an infinite-horizon backward stochastic differential equation (BSDE) under solely the market filtration; see Proposition 2.1. That is, the randomness from death and from the market can be dealt with separately. By deriving a comparison result for this infinite-horizon BSDE (Proposition 2.2), we are able to uniquely determine the Epstein-Zin utility for any -admissible strategy (Definition 2.3); see Theorem 2.1.

In a Black-Scholes financial market, we maximize the time-0 Epstein-Zin utility over permissible strategies of consumption, investment, and healthcare spending (Definition 4.2). First, we derive the associated Hamilton-Jacobi-Bellman (HJB) equation, from which a candidate optimal strategy is deduced. Taking advantage of a scaling property of the HJB equation, we reduce it to a nonlinear ordinary differential equation (ODE), for which a unique classical solution exists on strength of the Perron method construction in [15]. This, together with a general verification theorem (Theorem 3.1), yields the optimality of ; see Theorem 4.1.

Compared with classical Epstein-Zin utility maximization, the additional controlled mortality process in our case adds nontrivial complexity. In deriving the comparison result Proposition 2.2, standard Gronwall’s inequality cannot be applied due to the inclusion of . As shown in Appendix A.2, a transformation of processes, as well as the use of both forward and backward Gronwall’s inequalities, are required to circumvent this issue. On the other hand, in carrying out verification arguments, we need to contain the growth of to ensure that the Epstein-Zin utility is well-defined. This is done through a combination of probabilistic arguments and analysis of the aforementioned nonlinear ODE; see Appendix A.4 for details.

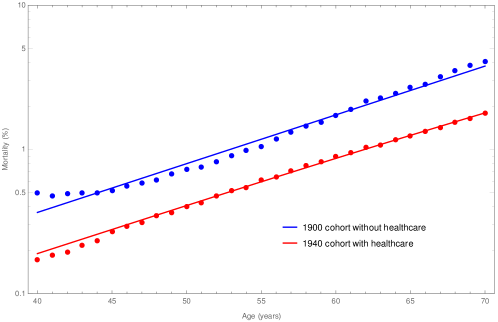

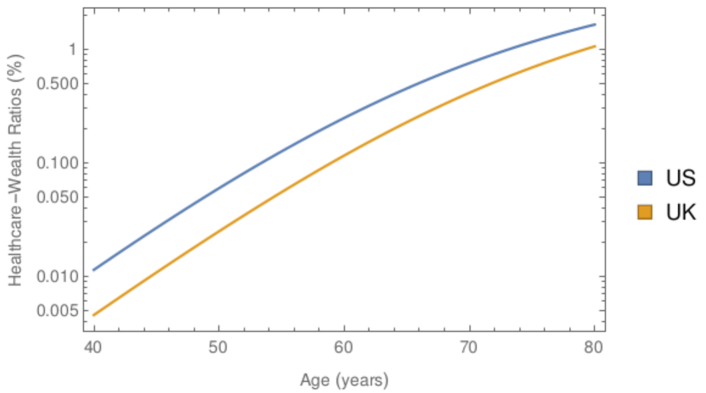

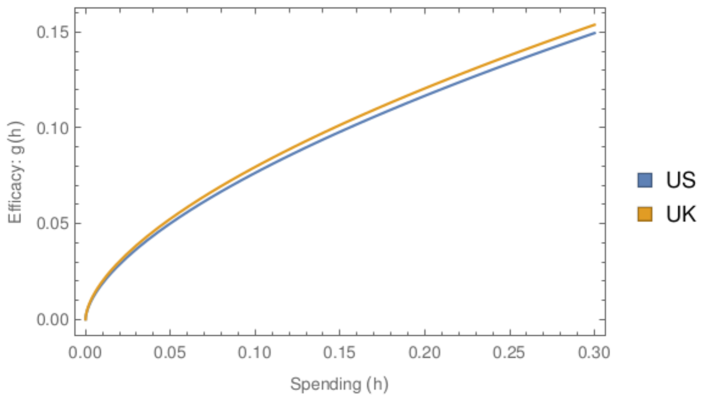

Our model is calibrated to mortality data in the US and UK. Under the simplifying assumption that the cohort born in 1900 had no healthcare and the cohort born in 1940 had full access to healthcare, we generate an endogenous mortality curve for the 1940 cohort. Figure 1 shows that the model-implied mortality (red line) closely reproduces actual data in the US (red dots). Our model performs well also for the UK data; see Figure 2. We also compute the optimal healthcare spending across different ages (Figure 3(a)) and calibrate the efficacy of healthcare in these two countries (Figure 3(b)).

The rest of the paper is organized as follows. Section 2 establishes Epstein-Zin utilities over one’s random lifetime, with healthcare spending incorporated. Section 3 introduces the problem of optimal consumption, investment, and healthcare spending under Epstein-Zin preferences, and derives the related HJB equation and a general verification theorem. Section 4 characterizes optimal consumption, investment, and healthcare spending in three different settings of aging and access to healthcare. Section 5 calibrates our model to mortality data in the US and UK. Most proofs are collected in Appendix A.

2 Epstein-Zin Preferences with Healthcare Spending

Let be a probability space equipped with a filtration that satisfies the usual conditions. Consider another probability space supporting a random variable that has an exponential law

| (2.1) |

We denote by the product probability space . The expectations taken under , , and will be denoted by , , and , respectively.

Consider an agent who obtains utility from consumption, partially determines his lifespan through healthcare spending, and has bequest motives to leave his wealth at death to beneficiaries. Specifically, we assume that the mortality rate process of the agent evolves as

| (2.2) |

where , a nonnegative -progressively measurable process, represents the proportion of wealth spent on healthcare at each time , while is the efficacy function that prescribes how much the natural growth rate of mortality is reduced by healthcare spending . For any , the random lifetime of the agent is formulated as

| (2.3) |

The information available to the agent is then defined as with

| (2.4) |

That is, at any time , the agent knows the information contained in and whether he is still alive (i.e. whether holds); he has no further information of , as the random variable is inaccessible to him. Finally, we assume that the agent can leave a fraction , not necessarily all, of his wealth at death to beneficiaries, reflecting the effect of inheritance and estate taxes.

Remark 2.1.

Now, let us define a non-standard Epstein-Zin utility process that incorporates healthcare spending. First, recall the Epstein-Zin aggregator given by

| (2.5) |

where and represent the agent’s relative risk aversion and EIS, respectively, as stated in Section 1. Given a consumption stream , assumed to be nonnegative -progressively measurable, and a healthcare spending process introduced below (2.2), we define the Epstein-Zin utility on the random horizon to be a -adapted semimartingale satisfying

| (2.6) |

where we use the notation . In (2.6), we assert that the loss of wealth at death results in a decreased bequest utility, by a factor of . This assertion will be made clear and justified in Section 4, where a financial model is in place; see Remark 4.4 particularly.

Before solving (2.6) for , we introduce a general definition of infinite-horizon BSDEs.

Definition 2.1.

Let be an -progressively measurable process satisfying for all . For any , we say is a solution to the infinite-horizon BSDE

| (2.7) |

if the following conditions hold: (i) is -progressively measurable, and (ii) for any there exists an -martingale such that (2.7) holds for .

Remark 2.2.

Without a terminal condition, (2.7) can have infinitely many solutions. Indeed, as long as admits proper monotonicity, there are solutions to (2.7) that satisfy “ for -measurable random variable ” or “ for ”; see [7] and [12]. We will address this non-uniqueness issue by enforcing appropriate “terminal behavior”; see Remark 2.6.

The next result shows that the -adapted in (2.6) can be expressed as a function of and an -adapted process that satisfies an infinite-horizon BSDE.

Proposition 2.1.

Let be nonnegative -progressively measurable. Then, is a -adapted semimartingale, with for all , that satisfies (2.6) if and only if

| (2.8) |

where is an -adapted semimartingale, with for all , that satisfies the infinite-horizon BSDE

| (2.9) |

with defined by

| (2.10) |

Proof.

See Section A.1. ∎

Remark 2.3.

Proposition 2.1 actually holds more generally beyond the specific driver in (2.5) and the boundary condition “” for encoded in (2.6). Specifically, in (2.6), if we allow for a general Borel driver and replace therein by for a general continuous function that grows at most linearly, the arguments in the proof of Proposition 2.1 (see Section A.1) still hold, leading to an upgraded version of Proposition 2.1 with in (2.8) and in (2.10) replaced by and , respectively.

In view of Proposition 2.1, to uniquely determine the Epstein-Zin utility process , we need to find a suitable class of stochastic processes among which there exists a unique solution to (2.9). To this end, we start with imposing appropriate integrability and transversality conditions.

Definition 2.2.

For any , define . Then, for any nonnegative -progressively measurable , we denote by the set of all -adapted semimartingales that satisfy the following integrability and transversality conditions:

| (2.11) |

Remark 2.4.

Condition (2.11) is similar to [24, (2.3)], but the controlled mortality in our case complicates the transversality condition: unlike [24, (2.3)], the exponential term no longer contains a constant rate, but a stochastic one involving . This adds nontrivial complexity to deriving a comparison result (Proposition 2.2) and the use of verification arguments (Theorem 4.1).

Remark 2.5.

We now introduce the appropriate collection of strategies we will focus on.

Definition 2.3.

Let be nonnegative -progressively measurable. For any , we say is -admissible if there exists satisfying (2.9) and

| (2.12) |

Remark 2.6.

Condition (2.12) is the key to a comparison result for (2.9), as shown in Proposition 2.2 below. In a sense, (2.11)-(2.12) is the enforced “terminal behavior”, under which a solution to (2.7) can be uniquely identified. Technically, (2.12) is similar to typical conditions imposed for infinite-horizon BSDEs, such as [7, (H1’)] and the one in [12, Theorem 5.1]: all of them require the solution to be bounded from above by a tractable process. Moreover, for classical Epstein-Zin utilities (without healthcare), a similar condition was imposed in [24, (2.5)]. In fact, Definition 2.3 is in line with [24, Definition 2.1], but adapted to include the controlled mortality .

A comparison result for BSDE (2.9) can now be established.

Proposition 2.2.

Proof.

See Section A.2. ∎

Theorem 2.1.

Remark 2.7.

Results in this section in fact hold true more generally, for certain specifications of that do not fulfill Assumption 1. For instance, for the cases “, ” and “”, Theorem 2.1 can be similarly established by suitably adjusting (2.11)-(2.12). This will allow the main result of this paper, Theorem 4.1 below, to be generalized to these cases.

3 Problem Formulation

Let be an -adapted standard Brownian motion. Consider a financial market with a riskfree rate and a risky asset given by

| (3.1) |

where and are given constants. Given initial wealth , at each time , an agent chooses a consumption rate , invests a fraction of his wealth on the risky asset, and spends another fraction on healthcare. The resulting dynamics of the wealth process is

| (3.2) |

Definition 3.1.

The agent aims at maximizing his lifetime Epstein-Zin utility by choosing in a suitable collection of strategies , i.e.

| (3.3) |

where the equality follows from (2.8). In this section, we only require to satisfy

| (3.4) |

Our focus is to establish a versatile verification theorem under merely (3.4). A more precise definition of , depending on specification of , , and , will be introduced in Definition 4.2.

3.1 A General Verification Theorem

Under the current Markovian setting (i.e. (3.1) and (3.2)), we take

| (3.5) |

i.e. the optimal value should be a function of the current wealth and mortality. The relation (A.10), derived from (2.6), suggests the following dynamic programming principle: With the shorthand notation and for , for any ,

| (3.6) |

By applying Itô’s formula to , assuming enough regularity of , we get

where the operator is defined by

| (3.7) |

for any . We can then rewrite (3.1) as

The HJB equation associated with is then

| (3.8) | ||||

Equivalently, this can be written in the more compact form

| (3.9) |

Theorem 3.1.

Proof.

(i) Fix . Consider an arbitrary . For any and , by applying Itô’s formula to , we get

where the operator is defined in (3.7). Thanks to (3.10), is a true martingale. Hence, the above equality shows that is a solution to BSDE (2.7), with . On the other hand, (3.4) implies that is -admissible, so that there exists a unique solution to (2.9) that satisfies (2.12) (Theorem 2.1). Since is a solution to (3.1), and equivalently to (3.9), we have

| (3.14) |

We then conclude from Proposition 2.2 that for all . In particular, . By the arbitrariness of , , as desired.

(ii) Fix . If , we can repeat the arguments in part (a), obtaining (3.14) with the inequality replaced by equality. This shows that is a solution to (2.9). Also, (3.4) implies that is -admissible, so that there is a unique solution to (2.9) satisfying (2.12) (Theorem 2.1). As also satisfies (2.12), we have for all ; particularly, . With in part (a), we conclude and is an optimal control. ∎

3.2 Reduction to an Ordinary Differential Equation

If we assume heuristically that , , is differentiable, and the inverse of is well-defined, then the optimizers stated in Theorem 3.1 (ii) can be uniquely determined as

| (3.15) |

Plugging these into (3.1) yields

| (3.16) |

Using the ansatz , the above equation reduces to

| (3.17) |

where

| (3.18) |

Moreover, the maximizers in (3.15) now become

| (3.19) |

These maximizers indeed characterize optimal consumption, investment, and healthcare spending, as will be shown in the next section.

4 The Main Results

Let us now formulate the set of permissible strategies in the optimization problem (3.3). First, take in Definition 2.2 to be

| (4.1) |

so that in Definition 2.2 becomes

| (4.2) |

Definition 4.1.

Let the set of strategies such that , satisfies (2.11) (with therein taken to be ) as well as for

Let be defined as , except that the second part of (2.11) is replaced by

| (4.3) |

Definition 4.2.

The set of permissible strategies , denoted by , is defined as follows.

-

(i)

For the case and (i.e. with neither aging nor healthcare), ;

-

(ii)

For the case (i.e. with aging),

Remark 4.1.

The rest of the section presents main results in three different settings of aging and access to healthcare, in order of complexity.

4.1 Neither Aging nor Healthcare

When the natural growth rate of mortality is zero () and healthcare is unavailable (), the mortality process is constant, i.e. . Consequently, in the HJB equation (3.1), all derivatives in should vanish; also, as is nondecreasing in by definition, the second supremum in (3.1) should be zero. Corresponding to this largely simplified HJB equation, (3.17) reduces to

which directly implies . The problem (3.5) can then be solved explicitly.

Proposition 4.1.

Proof.

See Section A.3. ∎

Proposition 4.1 shows that without aging and healthcare, optimal investment follows classical Merton’s proportion, while the optimal consumption rate is the constant , dictated by the fixed mortality . By (3.18), for the case , no longer depends on . Indeed, with no loss of wealth (and thus utility) at death, dying sooner or later does not make a difference to one who maximizes lifetime utility plus bequest utility.

As for and , we observe from (3.18) that a larger mortality rate induces a larger consumption rate due to EIS . This can be explained by the usual income and substitution effects in response to negative wealth shocks. A larger mortality rate makes the loss of wealth at death more pressing and imminent. This reduces the total income generated by saving up to the death time, leading to the income effect that reduces consumption in the current period. On the other hand, as saving is now less effective in generating future income, the opportunity cost of consumption in the current period decreases. This brings about the substitution effect that increases current consumption. As is known in the literature, when EIS , the substitution effect prevails, encouraging the agent to consume more.

4.2 Aging without Healthcare

When the natural growth of mortality is positive () but healthcare is unavailable (), mortality grows exponentially, i.e. . As and is nondecreasing in by definition, the second supremum in (3.1) vanishes. It follows that (3.17) reduces to

| (4.4) |

This type of differential equations can be solved explicitly.

Lemma 4.1.

Fix , and define the function by

| (4.5) |

If in (4.1), then is the unique solution to the ordinary differential equation

| (4.6) |

such that . Moreover, satisfies

| (4.7) |

Proof.

Similarly to (A.8) in [15], (4.6) admits the general solution

To ensure , we need , which identifies the corresponding solution as

A straightforward change of variable then gives the formula (4.5). Now, replacing the positive constants , , and in [15, Lemma A.1] by , , and in our setting, we immediately obtain the remaining assertions. ∎

Proposition 4.2.

Proof.

See Section A.5. ∎

Observe from (3.18) and (4.1) that

| (4.8) |

As and for all , the condition ensures for all . This, together with ((4.7) with ), shows that in Proposition 4.2 is essentially a well-posedness condition, ensuring that the optimal consumption rate is strictly positive for all . Moreover, with , (4.7) stipulates that aging enlarges consumption rate, but the increase does not exceed the growth of aging ; note that the increase in consumption results from the same substitution effect as discussed below Proposition 4.1.

4.3 Aging and Healthcare

For the general case where the natural growth of mortality is positive () and healthcare is available (), we need to deal with the equation (3.17) in its full complexity.

Assumption 2.

Let be twice differentiable with , and for , and satisfies the Inada condition

| (4.9) |

as well as

| (4.10) |

Condition (4.10) was first introduced in [15]. Its purpose will be made clear after the optimal healthcare spending strategy is introduced in Theorem 4.1; see Remark 4.3.

Lemma 4.2.

Proof.

By replacing positive constants , , and in [15, Appendix A.3] (particularly Theorems 3.1 and 3.2) by , , and in our setting, we get the desired results. ∎

Remark 4.2.

Theorem 4.1.

Proof.

See Section A.4. ∎

Theorem 4.1 identifies the marginal efficacy of optimal healthcare spending, , to be inversely proportional to , the elasticity of consumption with respect to mortality, where the constant of proportionality depends on EIS . Note that a larger EIS implies less healthcare spending, as is strictly decreasing. In a sense, healthcare spending is like saving: it crowds out current consumption, but potentially enlarges future consumption by extending one’s lifetime. Since a larger EIS means a stronger substitution effect (as discussed below Proposition 4.1), one substitutes more consumption for saving-like healthcare spending with a larger .

Remark 4.3.

Remark 4.4.

5 Calibration: A Preliminary View

In this section, we calibrate the model in Section 4.3 to actual mortality data. We take as given , , , , , , and . A safe rate approximates the long-term average real rate on Treasury bills in [4], and the time preference is also consistent with estimates therein; is estimated in [3]; follows the specification in [22] and [34]; and are taken from the long-term study [19]; is a rough estimate of inheritance and estate taxes in developed countries. These values ensure in (4.1). In addition, we take the efficacy function to be

| (5.1) |

The equation (3.17) then becomes

| (5.2) |

and the optimal healthcare spending process is now where is the unique solution to (5.2). The endogenous mortality is then

| (5.3) |

We calibrate , , , and to mortality data in the US and UK. For each country, the natural growth rate of mortality is estimated from mortality data for the cohort born in 1900, assuming no healthcare available. Given this estimated , healthcare parameters and in (5.1), as well as initial mortality , are calibrated by matching the endogenous mortality curve (5.3) with mortality data for the cohort born in 1940, through minimizing the mean squared error (MSE). Essentially, we work under the assumption that the 1900 cohort had no access to healthcare (whence its mortality grew exponentially with the Gompertz law) and the 1940 cohort had full access to healthcare. This is a crude simplification, but conforms to several realistic constraints; see [15, Section 5.2].

It is worth noting that solving (5.2) directly for is challenging. To the best of our knowledge, the mainstream solvers (e.g. in Mathematica and Matlab) crucially require that the first derivative in a first-order ODE be expressed as a function of and . Such an expression is not available to (5.2) because of the nonlinearity induced by . In an attempt to circumvent this, we follow [22, Algorithm 8.1] to approximate in a recursive manner. The algorithm, however, converges for some specifications of and diverges otherwise.222[22, Algorithm 8.1] converges desirably for a typical Epstein-Zin utility maximization problem without the consideration of healthcare. When healthcare is considered, the convergence breaks down due to the added efficacy function . This makes it inappropriate for the purpose of calibration, where we need to solve (5.2) for a wide range of and select the best specification that brings the model-implied mortality closest to data.

In view of this, we settle ourselves with a fairly simple approximate of , i.e.

| (5.4) |

which is the average of the upper and lower bounds of in (4.11). By Lemmas 4.1 and 4.2,

As has an explicit formula for any specification of , thanks to the formulas (3.18) and (4.5), it facilitates the calibration significantly. The results are listed in Table 1.

| Country | (%) | Model MSE | MSE | |||

| United States (US) | 7.24069 | 1.34995 | 0.19 | 0.61 | 0.0436896 | 0.128984 |

| United Kingdom (UK) | 7.79605 | 0.843827 | 0.19 | 0.60 | 0.0249924 | 0.12755 |

We stress that the calibration performed in this section, based on in (5.4), is only preliminary. A more sophisticated approximation of is certainly needed for an in-depth, full-fledged calibration. The purpose of our preliminary study is to demonstrate the potential of our model and possibly draw more attention to this problem for further developments.

5.1 Results

In Figure 1, the blue line is obtained by linearly regressing mortality data of the 1900 cohort (blue dots), while the red line is the model-implied mortality curve calibrated to mortality data of the 1940 cohort (red dots). Clearly, our model reproduces declines in mortality that are very close to ones observed historically. When compared with [15, Figure 5.2], Figure 1 provides a much better fit. This improvement can be attributed to the use of Epstein-Zin utilities (so that and can both take empirically relevant values), the inclusion of risky assets, and modifications of calibration methods. Figure 2 shows that our model also performs well for the UK data.

We also compare our model performance with linear regression. Indeed, without any idea of healthcare, one can model mortality data of the 1940 cohort by linear regression (as we did for the 1900 cohort). Our model outperforms linear regression: the sixth column of Table 1 reports MSEs under our model, significantly smaller than those under linear regression in the seventh column.

Figure 3(a) displays the model-implied optimal healthcare spending. In both countries, the proportion of wealth spent on healthcare is negligible at age 40, but increases to 0.5-1% at age 80. Figure 3(b) presents the calibrated efficacy function for the two countries. It particularly indicates that healthcare is more effective (in reducing mortality growth) in the UK than in the US. Along with Figure 3(a), we find that lower efficacy of healthcare is compensated by larger healthcare spending relative to wealth. That is, with enhanced efficacy, our model stipulates less healthcare spending, instead of more to exploit the reduced marginal cost to curtail mortality growth.

While Figure 3(b) hints at the potential of our model as a new analytic tool for healthcare efficacy, we stress that a more in-depth statistical and economic analysis is required here. First, one needs to find the confidence intervals for the estimated , so as to test the hypothesis that the parameter differences across countries are statistically significant. Second, the economic interpretation of demands further investigation. While a higher unambiguously raises efficacy, the effect of is subtle: The efficacy increases faster with a lower when is small, but with a larger when is large. A careful analysis of these issues is well-warranted but beyond the scope of this paper, and we will leave it for future research.

Appendix A Proofs

A.1 Proof of Proposition 2.1

First, we assume that is a -adapted semimartingale, with for all , that satisfies (2.6). Our goal is to show that must be of the form (2.8). In view of (2.3) and (2.1), for any , it holds for -a.e. that

| (A.1) |

Also, since is a -adapted semimartingale, it follows from (2.4) that there exists an -adapted semimartingale such that

| (A.2) |

Indeed, for any fixed , consider for all . As is -adapted, (2.4) implies is constant -a.s. on . By defining , with , for all , is an -adapted semimartingale satisfying (A.2). Also note that , as , for all . Now, observe that

| (A.3) |

where the second and last equalities follow from Fubini’s theorem for conditional expectations (see [27, Theorem 27.17]), the third equality is due to the tower property of conditional expectations and (A.2), the fourth equality results from and , and the fifth equality holds thanks to (A.1). Next, for -a.e. fixed , consider the cumulative distribution function of given the information , i.e.

Thanks to (A.1), for . This implies

| (A.4) |

which is the density function of given the information . It follows that

| (A.5) |

where the first line results from (by (A.2)), the second line follows from the tower property of conditional expectations, and the third line is due to the density formula (A.4). Since is right-continuous, it has at most countably many jumps on , so that we may use (instead of ) in the last term of (A.5). Finally,

| (A.6) |

where the first equality follows from the tower property of conditional expectations and (A.2), the second equality is due to , and the third equality is a consequence of (A.1). Now, combining (A.3), (A.5), and (A.6), we obtain from (2.6) and that

| (A.7) |

where we use the notation . This, together with (A.2), particularly implies

| (A.8) |

where

For any , since there exists such that (in view of (2.3) and (2.1)), we conclude from (A.8) that . We can then simplify (A.7) as

| (A.9) |

where satisfies

| (A.10) |

Now, note that the above equation directly implies

where

is an -martingale on , thanks to (A.10). Applying generalized Itô’s formula for semimartingales (see [20, Theorem I.4.57]) to gives Since by definition (by (2.2)), is again an -martingale. Hence, is a solution to BSDE (2.9). This, together with (A.9), yields the desired result.

Next, we prove the converse, i.e. a process given by (2.8) has the three properties: (i) it is a -adapted semimartingale; (ii) for all ; (iii) it satisfies (2.6). By the construction in (2.8), properties (i) and (ii) follow directly from being an -adapted semimartingale with for all . Now, by applying generalized Itô’s formula for semimartingales (see [20, Theorem I.4.57]) to , we see that satisfies (A.10). This, together with the same arguments in (A.3), (A.5), and (A.6), shows that in (2.8) satisfies (2.6).

A.2 Derivation of Proposition 2.2

Lemma A.1.

Proof.

As in the proof of [24, Lemma B.1], (A.11) holds by the mean value theorem provided that for all . To this end, note that

Thanks to Assumption 1, a direct calculation shows , i.e. is increasing in . This, together with satisfying (2.12), implies that for all , , where . By direct calculation,

where the second equality follows from the definition of and . ∎

To prove Proposition 2.2, we intend to follow the idea in the proof of [24, Theorem 2.2]. The involvement of the controlled mortality in (2.11), as well as the possibility that therein can be negative (Remark 2.5), result in additional technicalities. The proof below combines arguments in [24, Theorem 2.2] and [12, Theorem 2.1], adapted to weaker regularity of processes.

Proof of Proposition 2.2.

Recall the function in (A.12). Fix , define

| (A.13) |

and consider the stopping time . Applying generalized Itô’s formula (see [20, Theorem I.4.57]) to , , yields

where , are some -martingales on . As by the definition of in (2.2), is a true martingale for . Hence,

Observe that

where the first inequality follows from , and the second is due to Lemma A.1, which is applicable here as for . Thanks to the above inequality,

| (A.14) |

where the second line follows from and (A.13). Multiplying both sides by yields

where the second inequality follows from the right continuity of and . Indeed, the right continuity implies , so that . Set , and write the previous inequality as Taking expectations on both sides and using Fubini’s theorem give

| (A.15) |

where is well-defined as and , thanks to (Definition 2.2), for . Now, if , by writing , we apply standard Gronwall’s inequality to get , or equivalently

| (A.16) |

If , applying backward Gronwall’s inequality (see [33, Proposition 2]) to (A.15) also gives (A.16). By (A.16), (A.13), and (A.12), we obtain

| (A.17) |

Since is arbitrary, the transversality condition in for and immediately implies

| (A.18) |

That is, . This entails , and thus . Since is arbitrary, we conclude that for all . ∎

A.3 Proof of Proposition 4.1

For any fixed such that , define for . In order to apply Theorem 3.1, we need to verify all its conditions. It can be checked directly that , as a one-variable function, solves (3.1) in a trivial way, with all derivatives in being zero. For any , since satisfies (2.11) (with in place of ), so does , i.e. . By the definitions of and , and (3.10) is satisfied. As , and by definition. It follows that and are unique maximizers of the supremums in (3.11), respectively. The supremum in (3.12) is zero, as and . Hence, trivially maximizes (3.12). The only condition that remains to be checked is “ in (3.13) belongs to and satisfies (2.12)”.

Observe that a unique solution to (3.2) exists as a geometric Brownian motion

| (A.19) |

This implies that

| (A.20) |

which is again a geometric Brownian motion that satisfies the dynamics

Consequently,

| (A.21) |

where

Remarkably, by the definitions of and in (3.18) and (4.2), a direct calculation shows that , where the inequality follows from . It follows from (A.21) that

| (A.22) |

On the other hand, we can rewrite (A.20) as

| (A.23) |

where is a geometric Brownian motion with the dynamics , . As is a martingale, we can apply the Burkhölder-Davis-Gundy inequality to get

| (A.24) |

for some constant . By Jensen’s inequality and Fubini’s theorem,

We then conclude from the above two inequalities that

| (A.25) |

By (A.22) and (A.25), satisfies (2.11) (with in place of ), and so does the process , i.e. . By applying Itô’s formula to and noting

| (A.26) |

a consequence of (A.25) and , we argue as in the proof of Theorem 3.1 that is a solution to (2.9). Moreover,

By (4.8), this shows that satisfies (2.12) with . Hence, is -admissible, so that we can conclude . Theorem 3.1 is then applicable, asserting that and optimizes (3.5).

A.4 Proof of Theorem 4.1

Define for . To apply Theorem 3.1, we need to verify all its conditions. It can be checked, as in (3.15)-(3.17), that solves (3.1). By the definitions of and , and (3.10) is satisfied for any . As , , and satisfies Assumption 2, , , and in (3.19) are unique maximizers of the supermums in (3.11) and (3.12). It remain to show (i) for any , ; (ii) , defined using , , and as in (3.13), belongs to and satisfies (2.12).

(i) Take any , and set for . We will prove .

- •

-

•

First, we claim that the process is bounded from above; more specifically,

(A.29) Observe that

(A.30) where the second equality follows as solves (4.6) with . For each , consider

We deduce from (A.30) that local maximizers of must belong to , i.e.

(A.31) Also, by and (4.7),

(A.32) This particularly implies that

(A.33) Now, there are three distinct possibilities: 1) There exists such that for all . Then, and (A.32) implies for all . It then follows from (A.31) and (A.28) that

(A.34) where the last inequality follows from (A.33). Moreover,

i.e. (A.29) holds. 2) There exists such that for all . By (A.30), is strictly decreasing for . Thus, . By the estimate in (A.34), (A.29) holds. 3) Neither 1) nor 2) above holds. This entails . Hence, , so that (A.29) holds by the estimate in (A.34). Now, since (by (4.11)), , and ,

where the equality follows from (A.28) and (A.27), and the last inequality is due to (A.29). Recalling that , we conclude from (4.3) and the above inequality that

On the other hand, since ,

where the finiteness is a direct consequence of .

- •

(ii) Now, we show that and satisfies (2.12). Observe that a unique solution to (2.2) exists. As by definition only depends on , , and the current mortality rate, is a deterministic process. Thanks to (4.13), is strictly increasing. Also, a unique solution to (3.2) exists, which admits the formula

| (A.35) |

-

•

Case (ii)-1: . As is strictly increasing, , where the second inequality follows from (4.11) and (4.7). With this and , we deduce from (A.35) that (A.20) holds with “” therein replaced by “”. As entails (see (4.8)), the same arguments in Proposition 4.1 can be applied to to show that satisfies (2.11). With this, we can argue as in Case (i)-1 to show that belongs to

-

•

Case (ii)-2: and . As solves (3.17) and maximizes the supremum in (3.17),

where the inequality follows from (4.13). This gives , so that

(A.36) where the last inequality follows from (see (4.11)). For any , consider defined as in (A.27). Observe that can be written as

where is the upper incomplete gamma function . Similarly to the argument in [15, (A.6)-(A.7)], by using the fact ,

(A.37) where the inequality follows from the definition of and . This, together with being a strictly increasing deterministic process, implies the existence of such that

(A.38) Consider the constant In view of (A.35), (A.36), and (see (4.8)),

where is the driftless geometric Brownian motion defined below (A.23), and the second inequality follows from (A.38). It follows that

where the equality follows from a direct calculation using the definition of in (4.2), and the convergence is due to . Namely, satisfies (4.3). On the other hand, by (A.36) and , we obtain from (A.35) that

where is again the driftless geometric Brownian motion defined below (A.23). By the Burkhölder-Davis-Gundy inequality, we obtain the estimate in (A.24) with therein replaced by . This then implies , by the inequality preceding (A.25). Finally, under and (4.3), the same argument as in Case (i)-2 shows that belongs to

- •

Finally, by applying Itô’s formula to and using (A.26), a consequence of (A.25) and , we argue as in the proof of Theorem 3.1 that is a solution to (2.9). Also,

| (A.39) |

where the inequality follows from (by (4.11) and (4.7)) and the fact that if and if . By (4.8), this shows that satisfies (2.12) with . Hence, is -admissible, and we can now conclude . By Theorem 3.1, and optimizes (3.5).

A.5 Proof of Proposition 4.2

Define for . To apply Theorem 3.1, we need to verify all its conditions. It can be checked directly that solves (3.1), as is a solution to (4.4) (Lemma 4.1). By the definitions of and , and (3.10) is satisfied for any . Following part (i) of the proof of Theorem 4.1, we get for any ; the proof is much simpler here, as in the current setting. As , , and are unique maximizers of the supremums in (3.11), respectively. The supremum in (3.12) is zero, as and . Hence, trivially maximizes (3.12). It remains to show that , defined using , , and as in (3.13), belongs to and satisfies (2.12).

Observe that as , and a unique solution to (3.2) exists, which satisfies the dynamics (A.19) with replaced by . This implies

| (A.40) |

- •

-

•

Case 2: and . For any , consider the constant defined in (A.27). Similarly to (A.37), using the fact that yields

(A.41) where the inequality follows from the definition of and . This implies that there exists some such that

(A.42) Consider Now, by and (A.40) ,

where is the driftless geometric Brownian motion defined below (A.23), and the inequality follows from (A.42). It follows that

where the second line follows from a direct calculation using the definition of in (4.2), and the convergence is due to . On the other hand, similarly to (A.23), we rewrite (A.40) as

where is again the driftless geometric Brownian motion defined below (A.23). By Burkhölder-Davis-Gundy’s inequality, we obtain the estimate in (A.24) with therein replaced by . This implies , by the inequality preceding (A.25). Under and (4.3), the same argument as in Case (i)-2 of the proof of Theorem 4.1 shows that belongs to

- •

Finally, by applying Itô’s formula to and using (A.26), a consequence of (A.25) and , we argue as in the proof of Theorem 3.1 that is a solution to (2.9). Also, the same calculation as in (A.39), with therein replaced by , can be carried out, thanks to by (4.7). This shows that satisfies (2.12) with . Hence, is -admissible, and we can conclude . By Theorem 3.1, and optimizes (3.5).

References

- [1] J. Aurand and Y.-J. Huang, Epstein-Zin utility maximization on random horizons, (2019). Preprint, available at https://arxiv.org/abs/1903.08782.

- [2] R. Bansal, Long-run risks and financial markets, Review - Federal Reserve Bank of St.Louis, 89 (2007), pp. 283–299.

- [3] R. Bansal and A. Yaron, Risks for the long run: A potential resolution of asset pricing puzzles, The Journal of Finance, 59 (2004), pp. 1481–1509.

- [4] J. Beeler and J. Y. Campbell, The long-run risks model and aggregate asset prices: An empirical assessment, Critical Finance Review, 1 (2012), pp. 141–182.

- [5] L. Benzoni, P. Collin-Dufresne, and R. S. Goldstein, Explaining asset pricing puzzles associated with the 1987 market crash, Journal of Financial Economics, 101 (2011), pp. 552–573.

- [6] H. S. Bhamra, L.-A. Kuehn, and I. A. Strebulaev, The levered equity risk premium and credit spreads: A unified framework, The Review of Financial Studies, 23 (2010), pp. 645–703.

- [7] P. Briand, B. Delyon, Y. Hu, E. Pardoux, and L. Stoica, Lp solutions of backward stochastic differential equations, Stochastic Processes and their Applications, 108 (2003), pp. 109 – 129.

- [8] D. Duffie and P.-L. Lions, PDE solutions of stochastic differential utility, J. Math. Econom., 21 (1992), pp. 577–606.

- [9] P. H. Dybvig and H. Liu, Lifetime consumption and investment: retirement and constrained borrowing, J. Econom. Theory, 145 (2010), pp. 885–907.

- [10] I. Ehrlich, Uncertain lifetime, life protection, and the value of life saving, Journal of health economics, 19 (2000), pp. 341–367.

- [11] I. Ehrlich and H. Chuma, A model of the demand for longevity and the value of life extension, Journal of Political economy, 98 (1990), pp. 761–782.

- [12] S. Fan, Bounded solutions, solutions and solutions for one dimensional BSDEs under general assumptions, Stochastic Process. Appl., 126 (2016), pp. 1511–1552.

- [13] B. Gompertz, On the nature of the function expressive of the law of human mortality and on a new mode of determining the value of life contingencies, Philosophical Transactions of the Royal Society of London, 115 (1825), pp. 513–583.

- [14] M. Grossman, On the concept of health capital and the demand for health, Journal of Political economy, 80 (1972), pp. 223–255.

- [15] P. Guasoni and Y.-J. Huang, Consumption, investment and healthcare with aging, Finance and Stochastics, 23 (2019), pp. 313–358.

- [16] R. E. Hall and C. I. Jones, The value of life and the rise in health spending, The Quarterly Journal of Economics, 122 (2007), pp. 39–72.

- [17] L. P. Hansen, J. Heaton, J. Lee, and N. Roussanov, Intertemporal substitution and risk aversion, in Handbook of Econometrics, J. J. Heckman and E. E. Leamer, eds., vol. 6A, Elsevier, 1 ed., 2007, ch. 61, pp. 3967–4056.

- [18] J. Hugonnier, F. Pelgrin, and P. St-Amour, Health and (other) asset holdings, The Review of Economic Studies, 80 (2013), pp. 663–710.

- [19] F. Imperial, Modelling Stock Prices and Stock Market Behaviour using the Irrational Fractional Brownian Motion: An Application to the S&P500 in Eight Different Periods, PhD thesis, June 2018.

- [20] J. Jacod and A. N. Shiryaev, Limit theorems for stochastic processes, vol. 288 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences], Springer-Verlag, Berlin, second ed., 2003.

- [21] I. Karatzas and H. Wang, Utility maximization with discretionary stopping, SIAM J. Control Optim., 39 (2000), pp. 306–329.

- [22] H. Kraft, T. Seiferling, and F. T. Seifried, Optimal consumption and investment with Epstein-Zin recursive utility, Finance Stoch., 21 (2017), pp. 187–226.

- [23] H. Kraft, F. T. Seifried, and M. Steffensen, Consumption-portfolio optimization with recursive utility in incomplete markets, Finance Stoch., 17 (2013), pp. 161–196.

- [24] Y. Melnyk, J. Muhle-Karbe, and F. T. Seifried, Lifetime investment and consumption with recursive preferences and small transaction costs, Mathematical Finance, forthcoming, (2017). Available at http://dx.doi.org/10.2139/ssrn.2970469.

- [25] S. F. Richard, Optimal consumption, portfolio and life insurance rules for an uncertain lived individual in a continuous time model, Journal of Financial Economics, 2 (1975), pp. 187–203.

- [26] S. Rosen, The value of changes in life expectancy, Journal of Risk and uncertainty, 1 (1988), pp. 285–304.

- [27] R. L. Schilling, Measures, integrals and martingales, Cambridge University Press, Cambridge, second ed., 2017.

- [28] M. Schroder and C. Skiadas, Optimal consumption and portfolio selection with stochastic differential utility, J. Econom. Theory, 89 (1999), pp. 68–126.

- [29] T. Seiferling and F. T. Seifried, Epstein-zin stochastic differential utility: Existence, uniqueness, concavity, and utility gradients, (2016). Preprint. Available at https://dx.doi.org/10.2139/ssrn.2625800.

- [30] D. S. Shepard and R. J. Zeckhauser, Survival versus consumption, Management Science, 30 (1984), pp. 423–439.

- [31] C. Skiadas, Recursive utility and preferences for information, Economic Theory, 12 (1998), pp. 293–312.

- [32] A. Vissing-Jørgensen and O. Attanasio, Stock-market participation, intertemporal substitution, and risk-aversion, American Economic Review, 93 (2003), pp. 383–391.

- [33] X. Wang and S. Fan, A class of stochastic gronwall’s inequality and its application, Journal of Inequalities and Applications, (2018).

- [34] H. Xing, Consumption-investment optimization with Epstein-Zin utility in incomplete markets, Finance Stoch., 21 (2017), pp. 227–262.

- [35] M. E. Yaari, Uncertain lifetime, life insurance, and the theory of the consumer, The Review of Economic Studies, 32 (1965), pp. 137–150.

- [36] M. Yogo, Portfolio choice in retirement: Health risk and the demand for annuities, housing, and risky assets, Journal of Monetary Economics, 80 (2016), pp. 17–34.