Error bounds in estimating the out-of-sample prediction error using leave-one-out cross validation in high-dimensions

Kamiar Rahnama RadWenda ZhouArian MalekiBaruch CollegeCity University of New YorkColumbia UniversityColumbia University

Abstract

We study the problem of out-of-sample risk estimation in the high dimensional regime where both the sample size and number of features are large, and can be less than one. Extensive empirical evidence confirms the accuracy of leave-one-out cross validation (LO) for out-of-sample risk estimation. Yet, a unifying theoretical evaluation of the accuracy of LO in high-dimensional problems has remained an open problem. This paper aims to fill this gap for penalized regression in the generalized linear family. With minor assumptions about the data generating process, and without any sparsity assumptions on the regression coefficients, our theoretical analysis obtains finite sample upper bounds on the expected squared error of LO in estimating the out-of-sample error. Our bounds show that the error goes to zero as , even when the dimension of the feature vectors is comparable with or greater than the sample size . One technical advantage of the theory is that it can be used to clarify and connect some results from the recent literature on scalable approximate LO.

Keywords: High-dimensional statistics, Regularized estimation, Out-of-sample risk estimation, Cross validation, Generalized linear models, Model selection.

1 Introduction

Balancing the sensible level of model complexity against model fitness is a fundamental challenge faced by any learning algorithm. A model that is too simple can fail to capture the essential pattern in the data, and a model that is too complex is oversensitive to the idiosyncrasies of the particular data, resulting in highly variable patterns that are mere mirages in the noise. The learning algorithm’s ability to perform well on new, previously unseen data is typically used to set the model complexity. This performance is known as the out-of-sample error.

To be concrete, let be our dataset where and denote the features and response, respectively. The goal is to obtain an estimate of the response for a newly observed feature vector. We assume observations are independent and identically distributed draws from some joint unknown distribution . We model this distribution as , and estimate using the optimization problem

(1)

where is called the loss function, and is called the regularizer. Both the regularizer and the regularization parameter have significant effects on the performance of the estimate by controlling the complexity of the model. Hence, for picking a good regularizer, , or tuning the parameter one would like to estimate the out-of-sample prediction error, defined as

(2)

where is a new, previously unseen sample from the unknown distribution independent of , and is a function that measures the closeness of to . A standard choice for is .

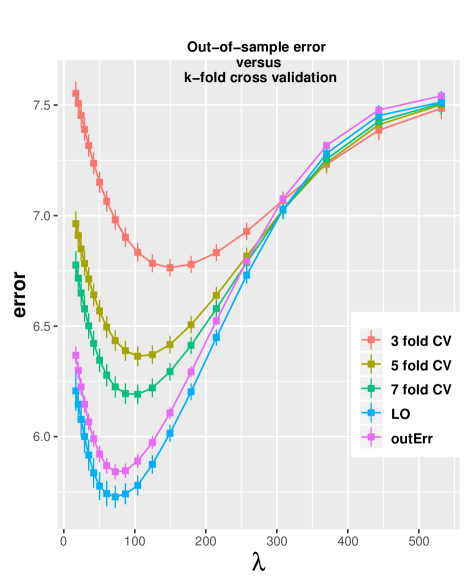

Figure 1: Comparison of -fold cross validation (for ) and leave-one-out cross validation with the true (oracle-based) out-of-sample error for the elastic-net problem where and . The upward bias of -fold CV clearly decreases as number of folds increase. and . The number of nonzero elements of the true is set to and their values is set to . Dimensions are and . Extra-sample test data is where . The true (oracle-based) out-of-sample prediction error is . All depicted quantities are averages based on 100 random independent samples, and error bars depict one standard error.

The problem of risk estimation has been extensively studied in the past fifty years and popular estimates, such as -fold cross validation [Stone, 1974] are used extensively in practical systems. However, the emergence of high-dimensional estimation problems in which the number of features is comparable or even larger than the number of observations , deemed many standard techniques in-accurate. For instance, Figure 1 compares the estimates obtained from -fold cross validation for different values of . As is clear in this figure, given the importance of each observation in high-dimensional settings, standard techniques, such as -fold suffer from a large bias.

One of the existing estimates of that seems to be accurate in high-dimensional settings is the leave-one-out cross validation (LO), which is defined through the following formula:

In this paper, we study the expected squared error of LO in estimating the out-of-sample error, in the high-dimensional setting, where both and are large, and can be less than one. We focus on regularized regression in the generalized linear family, and we make no sparsity assumption on the vector of regression coefficients. In short, we obtain an almost sharp upper bound on the error . These bounds not only show that as , but they also capture the rate of this convergence. This finally establishes what has been observed in empirical studies; obtains accurate out-of-sample risk estimates even in high-dimensional problems.

An important advantage of our theoretical results is that they can be used to clarify and connect some results from the recent literature on computationally efficient approximation to LO. For instance, [Rahnama Rad and Maleki, 2019] showed that in the same high dimensional regime, as , where stands for a computationally efficient approximation of LO we formally refer to in Section 1.2. A major consequence of our theory is that it shows that is a consistent estimator of . We make these statements more concrete in the next sections.

1.1 Notation

We first review the notations that will be used in the rest of the paper. Let stand for the th row of . and stand for and , excluding the th entry and the th row , respectively, and let be defined likewise.

Additionally, let stand for the regularized estimate in (1) when and are excluded.

Moreover, define

Likewise, define . The notation denotes polynomial of with a finite degree. Let and stand for the largest and smallest eigenvalues of , respectively. We state when the set of values is stochastically bounded.

1.2 Computational complexity of LO and its approximation

where is the active set of and is the matrix restricted to columns indexed by . With minor assumptions about the data generating process and without any sparsity assumption on the vector of regression coefficients, [Rahnama Rad and Maleki, 2019] (Theorem 3 and Corollary 1) proved that for various regularizers and regression methods in the high dimensional setting where is constant while .

Our finite sample bounds in the next section show that with similar (easy to check) regularity conditions, for various regularizers and regression methods, estimate go to zero as but is a fixed number. As a byproduct of this result, we show that in this high dimensional regime as . We will more formally state these claims in Section 3.

2 Main results

2.1 Our assumptions

Our goal is to evaluate the accuracy of LO in estimating the out-of-sample prediction error in the high-dimensional regime.

Our results are valid for finite values of and .

Later, in order to make asymptotic conclusions, we suppose that is constant while .

We now state our assumptions for theorem 1.

For simplicity of exposition, we start by stating a strong version of our assumptions, which often requires uniform bounds.

Weaker analogues are discussed in 2.3.

As the assumptions may appear somewhat opaque and technical, we will discuss them in the context of usual assumptions and concrete examples of standard generalized linear models.

Assumption 1.

The vectors are independent zero mean vectors with covariance such that for a nonnegative constant .

Assumption 1 characterizes the different distributions obtained for each and .

The rows are scaled in a way that ensures and , assuming that (for ) is , e.g. .

For instance, under the linear model , this scaling ensures that the signal-to-noise ratio in each observation remains fixed as grow (when the noise variance is a non-zero constant).

Unless we make explicit assumptions about the sparsity of , without the scaling, the Hessian of the optimization problem (1) is dominated by the data, making the regularizer, and in turn , irrelevant.

In this paper, we make no sparsity assumption on the vector of regression coefficients.

For similar finite signal-to-noise ratio scalings in the high-dimensional asymptotic analysis see [El Karoui, 2017, El Karoui et al., 2013, Bean et al., 2013, Donoho and Montanari, 2016, Donoho et al., 2011, Bayati and Montanari, 2012, Nevo and Ritov, 2016, Su et al., 2017, Dobriban and Wager, 2018, Rahnama Rad and Maleki, 2019, Xu et al., 2019].

Under this scaling, the optimal value of will be [Mousavi et al., 2018].

Assumption 2.

We assume the functions and are twice differentiable in . We also assume that and are convex in and , respectively. Let be a sample from the unknown distribution independent of . We assume there exists constants and , such that, for all , uniformly:

where , and .

Assumption 2 characterizes the smoothness of the GLM problem (and its associated leave-one-out versions).

As we will show below there are many examples, such as logistic and robust regression, in which we can find and .

However, in some other popular examples, such as linear or Poisson regression, is a random quantity and we cannot find an absolute constant to dominate it everywhere.

As will be discussed later in Section 2.3, we can weaken Assumption 2 at the expense of a slightly stronger moment condition on the feature vector .

Example 1. In the generalized linear model family, for the negative logistic regression log-likelihood , where , for it is easy to show that for any and , leading to .

Example 2. Our next example is about a smooth approximation of the Huber loss used in robust estimation, known as the pseudo-Huber loss:

(6)

where is a fixed number. If we use this loss for the linear regression problem, and set . It is easy to show that for any and , leading to .

Our next example is concerned with another popular loss function in linear regression, namely the absolute deviation. However, since we would like our loss functions to be differentiable, we use the following smooth approximation of the absolute deviation loss, , introduced in [Schmidt et al., 2007]:

where is fixed.111 Note that .

Example 3. For , we have . In fact, it is straightforward to show that for any and .

Assumption 3.

For define the two matrices

(7)

We assume that there exists a fixed number , such that

Assumption 3 characterizes the curvature of the GLM problem (and its associated leave-one-out versions).

In some examples, such as the ones that have ridge or smoothed elastic-net as the regularizer, it is straightforward to confirm this assumption.

For instance, for the ridge regularization, , we have .

In Section 2.3, we explain how this assumption can be relaxed (at the expense of requiring more stringent moment conditions on ) to cover more examples.

Having stated our assumptions, we now move on to stating our main result before proposing a number of examples to demonstrate how this result can be applied in common GLM cases.

2.2 Main theorem

Based on these assumptions we can now evaluate the accuracy of LO in estimating . The following theorem proves that the expected square error of in estimating is small even in high-dimensional asymptotic settings.

The only term that is not explicitly computed in terms of the constants in our assumptions is .

Hence, to obtain an explicit quantitative bound for a specific GLM problem requires computing this quantity.

We present two examples below.

Corollary 1.

(Ridge regularized logistic regression) Consider the negative logistic regression log-likelihood , and the regularizer , where . Furtherassume that is iid , where . If , then there exists a constant such that

where

(8)

The proof of this corollary can be found in Section D of the supplementary material.

Corollary 2.

(Pseudo-Huber loss with strongly convex regularizer)

We consider again the pseudo-Huber loss defined in (6) with parameter . As this loss is typically used in regression settings, we consider a linear regression model ,

where denotes i.i.d. zero-mean noise, and with . We additionally assume that the regularizer is strongly convex with parameter ,222Note that this is a fairly benign assumption in practice: it is common to introduce a slight ridge penalty which automatically

satisfies this assumption. , and .

Under these conditions, there exists a fixed number

(depending on , , , , and ) such that

The proof of this corollary can be found in Section E of the supplementary material.

To summarize, the examples presented in Corollary 1 and 2 satisfy the assumption needed for Theorem 1.

2.3 Extensions

As we discussed in Section 2.1, we can weaken the assumptions without a major change in our proofs or the main conclusions of our result. In this section, we aim to present one such weaker set of assumptions that enables our analyses to cover several other popular examples, such as the Poisson and linear regression.

Assumption 1′.

We assume that are i.i.d. zero mean vectors with covariance such that for a non-negative constant . Furthermore, there exists a fixed number , such that .

Note that this assumption is more stringent than Assumption 1. However, in essence the only extra requirement of this assumption is a bound on the fourth moments. Hence, it holds for a wide range of random features including sub-Gaussian and sub-exponential features. Thanks to this slightly stronger moment assumption we can weaken the other assumptions.

Assumption 2′.

We assume the functions and are twice differentiable in . Moreover, assume and are convex in and , respectively. Let be a sample from the unknown distribution independent of . We assume that there exist constants and , such that for all , uniformly

where , and .

Compared to Assumption 2 that requires to be bounded everywhere, this assumption requires the moment of to be bounded. This simple modification enables our theoretical results to be applied to a much broader set of regression techniques, including Poisson, linear, and negative binomial regression. These three examples will be studied later in this section.

Assumption 3′.

Let and be as defined in Assumption 3.

We assume that there exists a fixed number , such that

Again, compared to Assumption 3, this assumption only bounds the moments of the minimum eigenvalue of the matrix. The following example shows an example in which it is impossible to find a positive lower bound for the minimum eigenvalue, but still the moments of the inverse of the minimum eigenvalue are bounded.

Example 1.

Suppose that and that the loss function is strongly convex with parameter , and the regularizer is convex. Finally, suppose that , with . Then, there exists a fixed number that satisfies Assumption 3′ for large enough values of and .

The proof can be found in Section F of the supplementary material.

As we discussed before one can prove the accuracy of under Assumptions 1′, 2′, and 3′. The following theorem formalizes this claim.

where the outer expectation is taken with respect to the data and:

and .

The proof can be found in Section G of the supplementary material. As we described before, this theorem can cover several generalized linear models, that could not be covered by Theorem 1. We mention three important examples below.

Corollary 3.

(Square loss with elastic-net penalty)

Consider the data generating mechanism , where , , and . Suppose that we use the smoothed elastic-net optimization

where for , , and is a smooth approximation of the -norm. Then, there exists a fixed number, , such that

Since the proof of this claim is long, we defer it to Section H of the supplementary material.

Corollary 4.

[Poisson regression with soft-rectifying link]

Consider the data-generating mechanism ,

where denotes the soft-rectifying link, , and . Finally, assume that denotes the smoothed elastic-net regularizer introduced in Corollary 3. Under these assumptions, there exists a fixed number, , such that:

The proof can be found in Section I of the supplementary file.

Remark 1.

We have assumed here that is multivariate Gaussian. As might be clear to the reader from the proof, this normality assumption on may be relaxed to an moment assumption at the cost of a slightly more complicated proof.

Corollary 5(Negative-Binomial Regression).

We consider the problem of negative binomial regression with fixed shape parameter and exponential link.

Here, the negative log-likelihood is given by:

where denotes a constant which only depends on and .

Assume the data generating process is such that , and that . Finally, similar to Corollary, 3 we use the smoothed elastic-net as the regularizer.

Under these assumptions, there exists a fixed number, , such that

The proof can be found in Section J of the supplementary material.

3 Connection of and

We mentioned in Section 1.2 that different approximations of have been proposed in the literature to reduce the computational complexity of . Among such approximations, the formula introduced in (1.2), is analyzed in [Rahnama Rad and Maleki, 2019] under a similar asymptotic framework as the one discussed in our paper:

Theorem 3.

[Rahnama Rad and Maleki, 2019]

Suppose that is constant while . Under the assumption , for the regression problems discussed in Corollaries 1, 2, 3, and 4 we have

Note that the ultimate goal of is to use it as an estimate of . Hence, while Theorem 3 confirms the accuracy of ALO in approximating it does not explain whether the estimates obtained by or can be trusted in high-dimensional settings. However, we can combine this result with Theorems 1 and 2 to prove the accuracy of in estimating . Toward this goal we first prove the following claim.

Theorem 4.

Suppose that is constant while . Under the assumption , for the regression problems discussed in Corollaries 1, 2, 3, and 4 we have

Proof.

For a fixed number

(9)

The first inequality in the above equations is due to Markov inequality, and the second inequality is a result of Theorems 1 and 2. As we discussed in Corollaries 1, 2, 3, and 4 either or are finite numbers. Hence, as increases, the final probability can be reduced to the desired level.

∎

Before we proceed to establish the accuracy of we have to clarify Theorem 4. Note that even under the idealized (but incorrect) assumption that the individual estimates are independent and s are the same as , the central limit theorem indicates that 333The notation means that we have both and . Hence, we should not expect the error of to be . Therefore, the above theorem seems to offer the sharpest result that is possible for . Note that the sharpness is with regard to the rate of convergence and not the constants.

Combining the results of Theorem 2 and Theorem 4 we can finally quantify the accuracy of in estimating .

Corollary 6.

Suppose that is constant while . Under the assumption , for the regression problems discussed in Corollaries 1, 2, 3, and 4 we have

The proof of this corollary is straightforward, and is hence skipped.

Note that this corollary finally establishes the fact that obtains accurate estimates of . While we have established this result for only four popular examples in this paper, Theorems 1, 2 and Theorem 3 of [Rahnama Rad and Maleki, 2019] can be applied to a much broader class of regression problems. Hence, a similar result is expected for such scenarios as well. Finally, we should emphasize that by comparing Theorems 4 and 6 one may notice that the accuracy of might be worse than by a logarithmic factor. At this stage, it is not clear whether this difference is an artifact of the proof of [Rahnama Rad and Maleki, 2019] or it is a real extra error that has been introduced by the approximation of .

4 Numerical Experiments

In this section, we present two numerical experiments to show that the bound given in Theorem 1 and 2 is sharp but not tight. Specifically, we generate synthetic data, and compare and for elastic-net linear regression and ridge logistic regression. In all the examples in this section, the rows of are . Here we let and . The codes for the Figure 1 and Table 1,2 are available at https://github.com/RahnamaRad/LO.

Square loss with elastic-net penalty.

We set , and . The true unknown parameter vector is sparse with non-zero elements independently drawn from a zero mean unit variance Laplace distribution, leading to (regardless of the values of and ). To generate data, we sample . Here the out-of-sample error is:

As we increase and , we keep the ratio constant. We numerically calculate MSE as a function of (and ) based on 100 synthetic data samples, for each , and . We fitted a line to model and obtained a slope of -1.03 (SE) and intercept of -0.46 (SE) with an Adjusted R-squared of 0.95. The slope of -1.03 () shows that the bound is sharp because it confirms the scaling of our theory. Table 1 shows the numerical MSE as a function of and .

MSE (SE)

40

400

0.0156 (0.0021)

80

800

0.0064 (0.0008)

120

1200

0.0039 (0.0006)

160

1600

0.0038 (0.0006)

200

2000

0.0028 (0.0004)

Table 1: Square loss with elastic-net penalty: MSE (and standard errors).

Logistic regression with ridge penalty.

We set (the negative logistic log-likelihood) and . To generate data, we sample . Here the out-of-sample error

where and .

As we increase and , we keep the ratio constant. We numerically calculate MSE as a function of (and ) based on 100 synthetic data samples, for each , and . We fitted a line to model and obtained a slope of -1.00 (SE) and intercept of 0.34 (SE) with an Adjusted R-squared of 0.99. The slope of -1.00 shows that the bound is sharp because it confirms the scaling of our theory. Table 2 compares the numerical MSE and the theoretical bound from Theorem 1 and Corollary 1. The theoretical upper bound was computed using 8 in Corollary 1 where in this example, we have , , and , leading to . The significant difference between the bound and the MSE shows that the bound is not tight.

MSE (SE)

Bound

100

100

0.0136 (0.0019)

63.12

300

300

0.0037 (0.0005)

21.04

500

500

0.0026 (0.0005)

12.62

700

700

0.0017 (0.0002)

9.02

900

900

0.0015 (0.0002)

7.01

1100

1100

0.0012 (0.0002)

5.74

Table 2: Logistic regression with ridge penalty: MSE (and standard errors) and the upper bound based on 8 in Corollary 1 of Theorem 1.

5 Conclusion

Leave-one-out estimators (and their approximate versions) have seen renewed interest recently in the context of big data and high-dimensional problems.

We show that, in general, leave-one-out risk estimators have desirable statistical behaviours in the high-dimensional setting.

Although the leave-out-risk estimator itself is generally computationally intractable, this result also implies consistency for a (growing) number of approximate leave-one-out estimators, and demonstrate that such estimators offer a potentially good direction for building risk estimators for high-dimensional problems.

Acknowledgement

K.R. was supported by the NSF DMS grant 1810888, and Eugene M. Lang Junior Faculty Research Fellowship. A.M. was supported by the NSF DMS grant 1810888.

References

[Allen, 1974]

Allen, D. (1974).

The relationship between variable selection and data augmentation and

a method for prediction.

Technometrics, 16:125–127.

[Bayati and Montanari, 2012]

Bayati, M. and Montanari, A. (2012).

The lasso risk for gaussian matrices.

IEEE Transactions on Information Theory, 58(4):1997–2017.

[Bean et al., 2013]

Bean, D., Bickel, P. J., El Karoui, N., and Yu, B. (2013).

Optimal m-estimation in high-dimensional regression.

Proceedings of the National Academy of Sciences,

110(36):14563–14568.

[Beirami et al., 2017]

Beirami, A., Razaviyayn, M., Shahrampour, S., and Tarokh, V. (2017).

On optimal generalizability in parametric learning.

NIPS, pages 3455–3465.

[Burman, 1990]

Burman, P. (1990).

Estimation of generalized additive models.

Journal of Multivariate Analysis, 32:230–255.

[Cawley and Talbot, 2008]

Cawley, G. and Talbot, N. (2008).

Efficient approximate leave-one-out cross-validation for kernel

logistic regression.

Machine Learning, 71:243–264.

[Cessie and Houwelingen, 1992]

Cessie, S. and Houwelingen, J. (1992).

Ridge estimators in logistic regression.

Applied Statistics, 41(1):191–201.

[Craven and Wahba, 1979]

Craven, P. and Wahba, G. (1979).

Estimating the correct degree of smoothing by the method of

generalized cross-validation.

Numerische Mathematik, 31:377–403.

[Dobriban and Wager, 2018]

Dobriban, E. and Wager, S. (2018).

High-dimensional asymptotics of prediction: Ridge regression and

classification.

Ann. Stat., 46(1):247–279.

[Donoho et al., 2011]

Donoho, D., Maleki, A., and Montanari, A. (2011).

Noise sensitivity phase transition.

IEEE Trans. Inform. Theory, 57(10).

[Donoho and Montanari, 2016]

Donoho, D. and Montanari, A. (2016).

High dimensional robust m-estimation: Asymptotic variance via

approximate message passing.

Probab Theory Relat Fields, 166(3-4):935–969.

[El Karoui, 2017]

El Karoui, N. (2017).

On the impact of predictor geometry on the performance on

high-dimensional ridge-regularized generalized robust regression estimators.

Probability Theory Related Fields, 170(1-2):95–175.

[El Karoui et al., 2013]

El Karoui, N., Bean, D., Bickel, P., Lim, C., and Yu, B. (2013).

On robust regression with high-dimensional predictors.

PNAS, 110(36):14557–14562.

[Giordano et al., 2019]

Giordano, R., Stephenson, W., Liu, R., Jordan, M., and Broderick, T. (2019).

A swiss army infinitesimal jackknife.

JMLR, 89(1139-1147).

[Golub et al., 1979]

Golub, G., Heath, M., and Wahba, G. (1979).

Generalized cross-validation as a method for choosing a good ridge

parameter.

Technometrics, 21(2):215–223.

[Meijer and Goeman, 2013]

Meijer, R. and Goeman, J. (2013).

Efficient approximate k-fold and leave-one-out cross-validation for

ridge regression.

Biometrical Journal, 55(2):141–155.

[Mousavi et al., 2018]

Mousavi, A., Maleki, A., and Baraniuk, R. (2018).

Consistent parameter estimation for lasso and approximate message

passing.

The Annals of Statistics, 46(1):119–148.

[Nevo and Ritov, 2016]

Nevo, D. and Ritov, Y. (2016).

On Bayesian robust regression with diverging number of predictors.

Electron. J. Statist., 10(2):3045–3062.

[Obuchi and Kabashima, 2016]

Obuchi, T. and Kabashima, Y. (2016).

Cross validation in lasso and its acceleration.

J. Stat. Mech. Theor. Exp., 53(304):1–36.

[Obuchi and Kabashima, 2018]

Obuchi, T. and Kabashima, Y. (2018).

Accelerating Cross-Validation in Multinomial Logistic

Regression with ell1-Regularization.

Journal of Machine Learning Research, 19:1–30.

[Opper and Winther, 2000]

Opper, M. and Winther, O. (2000).

Gaussian processes and SVM: Mean field results and leave-one-out.

In Smola, A., Bartlett, P., Scholkopf, B., and Schuurmans, D.,

editors, Advances Large Margin Classifiers, pages 43–56. MIT Press,

Cambridge, MA.

[O’Sullivan et al., 1986]

O’Sullivan, F., Yandell, B., and Raynor, W. (1986).

Automatic smoothing of regression functions in generalized linear

models.

JASA, 81(393):96–103.

[Rahnama Rad and Maleki, 2019]

Rahnama Rad, K. and Maleki, A. (2019).

A scalable estimate of the extra-sample prediction error via

approximate leave-one-out.

arXiv:1801.10243v3.

[Schmidt et al., 2007]

Schmidt, M., Fung, G., and Rosales, R. (2007).

Fast optimization methods for l1 regularization: A comparative study

and two new approaches.

In ECML, pages 286–297. Springer.

[Stephenson and Broderick, 2019]

Stephenson, W. and Broderick, T. (2019).

Sparse Approximate Cross-Validation for High-Dimensional

GLMs.

arXiv preprint arXiv:1905.13657.

[Stone, 1974]

Stone, M. (1974).

Cross-validatory choice and assesment of statistical predictions.

J R Stat Soc Series B, 36(2):111–147.

[Su et al., 2017]

Su, W., Bogdan, M., and Candes, E. (2017).

False discoveries occur early on the Lasso path.

Ann. Stat., 45(5):2133–2150.

[Takahashi and Kabashima, 2018]

Takahashi, T. and Kabashima, Y. (2018).

A statistical mechanics approach to de-biasing and uncertainty

estimation in lasso for random measurements.

Journal of Statistical Mechanics: Theory and Experiment,

7(073405).

[Vehtari et al., 2016]

Vehtari, A., Mononen, T., Tolvanen, V., Sivula, T., and Winther, O. (2016).

Bayesian leave-one-out cross-validation approximations for

Gaussian latent variable models.

Journal of Machine Learning Research, 17(1):3581–3618.

[Wang et al., 2018]

Wang, S., Zhou, W., Maleki, A., Lu, H., and Mirrokni, V. (2018).

Approximate Leave-One-Out for High-Dimensional

Non-Differentiable Learning Problems.

International Conference on Machine Learning.

[Xu et al., 2019]

Xu, J., Maleki, A., Rahnama Rad, K., and Hsu, D. (2019).

Consistent risk estimation in high-dimensional linear regression.

arXiv:1902.01753.

Supplementary Material

Appendix A Notation

Let and .

Appendix B Background material on Gaussian random variables, vectors and matrices

In this section, we review a few important results regarding the functions of Gaussian matrices and Gaussian vectors that are used in our examples. The first result is about the moments of the inverse of the minimum eigenvalue of a Wishart matrix.

Lemma 1.

(Lemma 19 of [Xu et al., 2019])

Let , and suppose that while for . Then,

for a fixed , we have

(10)

Our next two lemmas are concerned with the moments of a Gaussian and random variables:

Lemma 2.

Let . Then, we have

(11)

where the notation denotes the double factorial. Furthermore, when is even the above inequality is in fact an equality.

The proof of this claim is straightforward and can be found in many standard statistics text books.

Lemma 3.

Let , i.e., it has a distribution with degrees of freedom. Then, for any integer we have

We would like to use Theorem 1 to prove this corollary. Toward this goal, we first have to prove that Assumptions 1, 2, and 3 hold, and that is bounded. Given the fact that is , Assumption 1 holds. As we discussed in Example 1, Assumption 2 holds as well with . Finally, given that the regularizer is ridge Assumption 3 holds too. Hence, the only remaining step is to check the boundedness of . In the rest of the proof we aim to prove that

(14)

Note that

where to obtain the last inequality we have used . Furthermore, since , we have

(15)

Comparing with the zero estimator yields, . Since for any , we get . Therefore, we can say that for ridge regularized logistic regression

To summarize, using the bound above and Theorem 1 (with ) , for ridge regularized logistic regression, we conclude that

(16)

where the last equation is due to (shown in Example 1) and .

We would like to use Theorem 1 to prove this corollary. Toward this goal we have to confirm Assumptions 1, 2, and 3 and prove the boundedness of . Assumption 1 is already assumed in the corollary. Assumption 2 is also confirmed in Example 2 so that . Since the regularizer is assumed to be strongly convex, Assumption 3 is also automatically satisfied with . Hence, the only remaining step is to obtain an upper bound for . In the rest of the proof we prove that

We have

Furthermore, we have that . Additionally, note that using the strong convexity of the regularizer, and by comparing the value of at and , we have that .444We have used the fact that .

Therefore,

We may bound this quantity explicitly in terms of the covariance of :

Hence,

To summarize, using the bound above and Theorem 1 (with ), we conclude that

where the last equation is due to (shown in Example 2) and .

It is straightforward to check that, for any , we have:

This implies that:

Define the vectors . Hence, .

Furthermore, define the matrix as the matrix that has as its rows.

It is straightforward to check that:

The fact that the quantity is lower bounded by a constant for large values of when is proved in [Xu et al., 2019]. See Lemma 1 in the supplementary material.

The proof of this result is very similar to the proof of Theorem 1. Hence, instead of rewriting the proof, we only emphasize on the differences between the proofs of Theorems 1 and 2. The strategy of the proof is exactly the same. We break the error between and into and and try to bound the second moments of these quantities.

The following lemma obtains an upper bound for the second moment of .

As is clear, we would like to use Theorem 2 to prove our claim. Toward this goal, we have to prove that Assumptions 1′, 2′, and 3′ hold. Furthermore, we have to obtain an upper bound for the constant , which in turn requires us to bound .

Given that is Gaussian, Assumption 1′ is automatically satisfied. Furthermore, since the regularizer is elastic-net, it is straightforward to prove Assumption 3′. To see this, first note that, for all , we have almost surely:

where . Hence, it is straightforward to see that

Hence, the only remaining steps are to prove Assumption 2′ and bound the term . Given that , we have

Hence,

Hence, if we prove Assumption 2′, we have also proved that

In the rest of this section, we focus on the proof of Assumption 2′. Note that . Under these assumptions, we prove that there exists a fixed number such that , and .

Consider the following definitions:

(17)

Furthermore, define . Our optimization problem can be written as

Since , where , the optimality conditions yield

Hence,

It is then straightforward to prove that

(18)

Our goal is to show that all the “finite” moments of the elements of , including the moment required in our example, are . From (18) we have

(19)

Hence, we bound each of the above three terms separately in the following lemmas:

Define . According to the matrix inversion lemma we have

(21)

Note that conditioned on the distribution of is a zero mean Gaussian random variable with variance . Hence, (21) and the moments of a Gaussian random variable (see Lemma 2) lead to

(22)

Hence, by the law of iterated expectation, we obtain

Since the minimum eigenvalue of the Hessian of is , therefore the minimum eigenvalue of (for all ) is greater than , leading to

This together with yields

Define . According to the matrix inversion lemma we have

(28)

Furthermore, we have

(29)

Note that for two random variables and we have

Hence,

(30)

First note that, since the maximum eigenvalue of is we have

(31)

Hence,

(32)

Furthermore, we have

1.

According to Lemma 3, , where the last inequality is according to the assumption .

2.

Note that . Furthermore, . Hence, using the the moments of Gaussian (see Lemma 2), we have

(33)

3.

Given , the distribution of is . Furthermore, , where the last inequality is due to (26). Hence, we have

(34)

Since , and , we have

(35)

where for the last inequality we assumed that .

Finally, we compute an upper bound on . Since is independent of and , we conclude that given and , is a Gaussian random variable with mean zero and variance

where , and the second inequality is due to (27). Hence,

The goal of this section is to use Theorem 2 to prove corollary 4. Hence, we have to confirm that Assumptions 1′, 2′, and 3′ hold, and that is bounded. Similar to what we did at the beginning of Section H, it is straightforward to check the validity of Assumptions 1′ and 3′. Hence, we only focus on proving Assumption 2′ and finding an upper bound for .

Regarding Assumption 2′, we first prove that under the assumptions of this corollary, there exists a fixed number , such that

and .

Since , we have

where . We have that, for all , and

, from which we deduce that:

(36)

In particular, we have that:

To obtain equality (a) we have used the moment generating function of the Poisson distribution with .

To obtain inequality (b) we have used the moment generating function of a Gaussian distribution and the fact that . Given that the upper bound we derived in (36) for the derivative of the loss function does not depend on the second input argument of the loss, that is , the proof that Poisson loss satisfies the other conditions of Assumption 2′ for will be exactly similar and hence is skipped.

In particular, we have verified the conditions of Assumption 2′ for any convex regularizer.

Now we turn our attention to bounding . First note that

(37)

Furthermore, from the mean value theorem we have:

Hence, we have:

(38)

To complete the proof we have to show that both and are bounded. First note that, using and, for any , , yields

(39)

Hence,

(40)

The following facts will help us bound these terms:

On the other hand, it is straightforward to check that for any we have

(42)

By combining these equations we obtain:

(43)

Note that is a Gaussian random variable with mean zero and variance . Hence, is bounded by a constant.

Note that in order to show that this term is bounded from above by a constant, we only need to show that terms of the form:

are bounded for and . As previously, we note that is a Gaussian random variable with variance , and hence is bounded. Hence, the only remaining step is to prove the boundedness of , where is at most 2. Note that conditioned on the random variable is Gaussian with the variance that is bounded by .

Hence, using Lemma 2 we have

The definition of (and comparing it with ) yields

The -strong convexity of the smoothed elastic-net regularizer , and the fact that , leads to

Since , we only prove that is bounded.

Toward this goal we have:

(45)

Hence, we have to prove that and are bounded.

First note we proved in (43) that:

(46)

Note that is a Gaussian random variable with variance , and hence is bounded. On the other hand,

(47)

It is straightforward to prove that . Hence,

(48)

where to obtain the last inequality we used the mean value theorem

where , and the facts that and . Using (48) we obtain:

Similar to the proofs of Corollaries 4, 3, we would like to use Theorem 2 to prove our claim. Toward this goal, We have to prove that Assumptions 1′, 2′, and 3′ hold. Furthermore, we have to obtain an upper bound for the constant , which in turn requires us to bound . Again, the proofs of Assumptions 1′ and 3′ are exactly the same as we presented in the last two sections. Hence, we only focus on Assumption 2′ and . We would like to prove that the conditions of Assumption 2′ are satisfied with .

It we compute the derivative of the log-likelihood, we will obtain

(50)

We thus deduce that:

As the bound (50) is free of , the same argument above applies to the other requirements in Assumption 2′.

Now we turn our attention to the calculation of . Note that

Note that by removing the constant from the log-likelihood we obtain

(51)

The rest of the proof is very similar to the proof that we presented for Corollary 4. Hence, we skip it.