A Scalar-Parameterized Mechanism For Two-Sided Markets

Abstract

We consider a market in which both suppliers and consumers compete for a product via scalar-parameterized supply offers and demand bids. Scalar-parameterized offers/bids are appealing due to their modeling simplicity and desirable mathematical properties with the most prominent being bounded efficiency loss and price markup under strategic interactions. Our model incorporates production capacity constraints and minimum inelastic demand requirements. Under perfect competition, the market mechanism yields allocations that maximize social welfare. When market participants are price-anticipating, we show that there exists a unique Nash equilibrium, and provide an efficient way to compute the resulting market allocation. Moreover, we explicitly characterize the bounds on the welfare loss and prices observed at the Nash equilibrium.

1 Introduction

The distinction between consumers and producers in marketplaces is increasingly fading. In the retail electricity sector, increased consumer participation—either as generation suppliers or price-responsive demanders—is driving the emergence of a digital platform marketplace where end-use customers can engage in transcations coordinated via a central entity or market manager as proposed in Tabors et al. (2016). Similar digital marketplaces have emerged in the areas of ride-sharing (Uber, Lyft), lodging (Airbnb), online retail and trading auctions (Amazon, Ebay) etc. A common feature of these multi-sided marketplaces is a collection of agents who can take up the mantle of being suppliers or consumers while the market clears through a centralized mechanism, often operated by a market manager. Motivated by these transformations, in this paper we study a two-sided market with a finite number of suppliers that compete to supply a product to price-responsive consumers. Our focus is on uniform price markets that clear through a centralized mechanism that sets a single per-unit price on the product for all participants. Every consumer (supplier) expresses her willingness to buy (offer) via a demand bid (supply offer) that fully characterizes her demand (supply) quantity at a given market price. We investigate the following market design question: What is the right mechanism that allows market actors sufficient flexibility to declare their willingness to offer/buy such that it yields efficient allocations, i.e., an allocation that maximizes social welfare?

The seminal work by Klemperer and Meyer (1989) demonstrated that in the absence of uncertainty there exist an enormous multiplicity of equilibria in supply functions. Hence, there is a need to resort to stylized offer/bid functions that appropriately restrict the family of supply offers and demand bids which the market actors are allowed to utilize. The well-known Bertrand and Cournot competition models are examples of simple (degenerate) supply offer strategies in markets with uniform prices. However, the Bertrand model typically assumes that each participant is willing to supply the entire demand, which may not be satisfied in a number of cases. Variations of the Bertrand model with capacity constraints have been proposed, however, in such settings pure Nash equilibria may not exist as shown in Shubik (1959). The Cournot model has a number of appealing properties when studying oligopolies in markets with relatively high demand elasticity. However, when demand elasticity is low Cournot competition may exhibit arbitrarily high welfare loss (see Day et al. (2002)). Furthermore, pure quantity or price competition cannot adequately represent markets with more complicated offer structures. An example of such markets are day-ahead wholesale electricity markets that operate either as pools or power exchanges. In these markets, power producers submit offers to supply varying quantities at succesively higher prices and the demand side specifies the quantity willing to purchase at succesively lower prices. Linear supply functions is another candidate family of functions to model strategic interactions among suppliers. However, the work of Baldick et al. (2004) illustrates that it is not straightforward to incorporate capacity constraints into linear supply offers. Moreover, arbitrary high efficiency loss at the Nash equilibrium is possible, particularly when suppliers have highly heterogeneous cost functions (see Li et al. (2015)).

In this work, we restrict our attention on a specific family of supply offers and demand bids, referred to as scalar-parameterized supply functions, studied by Johari and Tsitsiklis (2003) and Johari and Tsitsiklis (2011) in markets with inelastic supply and demand respectively. The specific family of offer/bid functions allows market actors to have one-dimensional action spaces, when faced with a single market price. Such market mechanisms are simple to implement and are considered to be fair among market participants. Moreover, the work of Johari et al. (2004) and Johari and Tsitsiklis (2011) showed that such supply offers possess a number of attractive properties including bounded Price of Anarchy and price markups at the Nash equilibrium. The family of supply functions considered here is a capacitated version of those introduced by Johari and Tsitsiklis (2011) that have been studied by Xu et al. (2016) and Lin and Bitar (2017) under perfectly inelastic demand. Such supply functions prohibit situations where firms can offer in the market beyond their means.

In this paper, we aim to study the most general setting: a two-sided market where both supply and demand compete through supply offers and demand bids, which we present in Section 2. In sections 3 and 4, we characterize the market outcome in situations when all market actors are (i) pure price-takers and (ii) price-anticipating. We show that under perfect competition our market mechanism yields allocations that maximize social welfare. When both sides of the market are price-anticipating, the misrepresentation of private information has the potential to induce market allocations that are suboptimal to the efficient outcome. However, our analysis in Section 5 indicates that both the welfare loss and the price markup at the Nash equilibrium are bounded. Numerical experiments in Section 6 illustrate the main insights of the analysis. Section 7 concludes the paper. All proofs are provided in the Appendix.

Notation: Let denote the set of real numbers and the set of non-negative real numbers. Denote the transpose of a vector by . Let be the vector including all but the element of . Finally, denote by the vector of all ones with appropriate size.

2 The Market Model

We consider a market with a finite number of consumers and firms competing for a product. Denote the set of consumers by and the set of suppliers by . Let denote consumer ’s quantity demanded, which must be greater than a minimum inelastic demand level denoted by . Let denote the quantity supplied by firm that must lie below each supplier’s maximum capacity limit denoted by . Each consumer receives utility for consuming amount and each firm incurs costs for producing quantity . We make the following assumption on the utility and cost functions.

Assumption 1. For each , is concave, strictly increasing and continuously differentiable for with . For each , is convex, strictly increasing and continuously differentiable with for . Over the domain , .

The aggregate welfare maximization problem is given by

| (1a) | ||||

| subject to | (1b) | |||

| (1c) | ||||

| (1d) | ||||

Henceforth, we will refer to every allocation that solves (1) as efficient. In effect, such allocations can be viewed as those determined by a central entity or market manager that has perfect knowledge on the market and all participants. However, and are generally not available to the market manager.

Hence, is there a mechanism that allows market actors to express their preferences in a way that it yields efficient market allocations? We consider the following market mechanism for supply and demand allocations. Let consumer provide to the market manager a parameter . Given price , the consumer is willing to buy , where

| (2) |

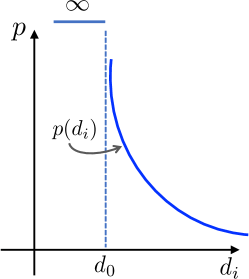

The expression in (2) represents the quantity the consumer is willing to buy, given the inelastic component , the market price , and the parameter . The inelastic demand represents the minimum quantity the consumer must be supplied while represents the price-responsive portion of her demand. Note that the demand bid is decreasing in price, i.e., it is downward sloping. For ease of exposition we consider equal minimum demand among consumers in the market. The case with distinct is straightforward to generalize. Note that this assumption does not make the consumers homogeneous as each consumer is described by a different utility function.

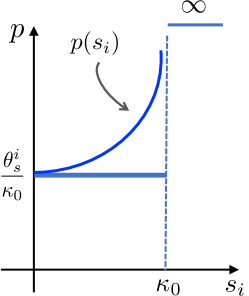

Let firm submit to the market manager a parameter . Given price , the firm is willing to supply , where

| (3) |

The supply offer (3) represents the quantity the firm is willing to supply as a function of price. The supply offer is further parameterized in the capacity , which represents the supplier’s maximum production capacity. For ease of exposition we consider equal capacities among firms in the market. We refer to Figure 1 for illustrations of how and vary with price. Observe that as the demand approaches , the consumer’s willingness to buy approaches infinity. Similarly, as the supply quantity approaches the firm’s maximum capacity the requested market price grows large.

Let and represent the collection of demand bid and supply offer parameters, respectively. The market manager chooses price to clear the market such that supply equals demand, i.e.,

| (4) |

Such choice is only possible when in which case the market price is given by

| (5) |

Throughout the paper, we assume and thus the market price is well-defined. In the case where , i.e., every market participant submits a zero parameter, we adopt the following conventions

For markets with a perfectly inelastic demand , the residual supply index () is often adopted as a suitable indicator of market power. Precisely, the of firm measures the capability of the aggregate market capacity—excluding that of —to meet demand . In the model considered here, the inelastic portion of demand is . Mathematically, if

is strictly less than one, then firm is said to be pivotal. See Newbery (2008) and Swinand et al. (2010) for further details. As we show in Section 4, the presence of pivotal suppliers is critical in the analysis of the market outcome under strategic interactions.

3 Perfect Competition

In this section, we study the market outcome assuming all market participants are pure price-takers. We aim to establish the existence and characterization of the competitive market equilibrium taking into account the profit-maximizing nature of market actors. Given market price each consumer maximizes the payoff

| (6) |

Similarly, each supplier maximizes

| (7) |

We now proceed with our first result which shows that when consumers bid in (2) and firms offer in (3) the market supports an efficient competitive equilibrium.

Theorem 1

Suppose Assumption 1 is satisfied. Then, there exists a competitive market equilibrium satisfying:

| (8) |

| (9) |

| (10) |

Moreover, the supply vector defined by and the demand vector defined by is an efficient allocation.

According to Theorem 1, under perfect competition, suppliers and demanders maximize their payoffs and the resulting market allocation is efficient. This implies that given price , the firms have no incentive to deviate from supplying and consumers have no incentive to deviate from buying . Thus the competitive market allocation is efficient and the market clearing price is the shadow value of the constraint . In other words, at the marginal social benefit of additional output equals the marginal social cost. The preceding argument establishes the first fundamental theorem of welfare economics: if the price and the allocation constitute a competitive equilibrium, then this allocation is efficient.111In economics the notion of efficiency is, typically, equivalent to that of Pareto optimality. In other words, a Pareto optimal market allocation means that there is no other allocation that can make any market actor better off without making another actor worse off..

4 Strategic Suppliers and Demanders

In contrast to the price-taking model, we now consider a model where the market participants are price-anticipating. Price-anticipating suppliers and consumers realize that the market price is a function of their actions and adjust their payoff accordingly. The payoff for the price-anticipating consumer is

| (11) |

Note that the payoff of each consumer now depends on the actions of all other market participants, that are collectively incorporated in the market price. Similarly, for each firm the payoff function depends on her action and the actions of all other market participants. Therefore, the payoff of firm is given by

| (12) |

We define the game with denoting the set of players with strategy spaces and payoffs given by (11) and (12). Our goal is to study the existence (and uniqueness) of the Nash equilibria of and provide an efficient way to compute the equilibrium. A bid/offer profile constitutes a Nash equilibrium if

We begin with the following result that illustrates how certain market parameters influence the existence of a Nash equilibrium of .

Lemma 1

does not admit a Nash equilibrium if a pivotal supplier exists in the market.

In effect, Lemma 1 implies that when firms cannot supply the entire inelastic demand in the market, then there exists a pivotal supplier that faces a non-zero inflexible demand that has infinite willigness to pay. This makes the suppliers’ payoff grow unbounded with respect their action . Hence, a Nash equilibrium cannot exist in this case. As a consequence of Lemma 1, there cannot exist a Nash equilibrium with since, by definition, the single supplier is pivotal. In view of the above Lemma, we impose the following assumption.

Assumption 2. for each firm

Equipped with the previous observations, we present our main result that explicitly characterizes the unique Nash equilibrium of .

Theorem 2

Suppose Assumptions 1-2 hold. admits unique Nash equilibrium in . Moreover, the supply profile

and the demand profile

are given by the unique solution of the following convex program

| (13a) | ||||

| subject to | (13b) | |||

| (13c) | ||||

| (13d) | ||||

where

| (14) |

| (15) |

Computing Nash equilibria is, in general, hard as shown by Daskalakis et al. (2009). Theorem 2 establishes the computation of the market allocation at the Nash equilibrium—and the Nash equilibrium itself—through the solution of a convex program in instead of solving M+N problems in the actions , which can be cumbersome depending on the structure of the utility and cost functions. The crux of Theorem 2 is the construction of an appropriate convex program that yields the market allocation at the Nash equilibrium—a technique closely related to the use of potential functions in characterizing Nash equilibria (Monderer and Shapley (1996)). However, the functions (14) and (15) are not potentials for , since they depend on the allocations and not on the players’ decisions. Hence, we cannot use these functions to conclude anything about convergence of best response dynamics to the Nash equilibrium. However, in the following section, we exploit the structure of and to find bounds on the efficiency loss and the markup of prices observed at the Nash equilibrium.

5 Efficiency Loss And Price Markups

The structure of the modified utility and cost functions allows us to make a number of interesting observations about the behavior of strategic market actors. First, note that since are assumed convex and increasing, it follows that Similarly, since are concave and increasing, for each consumer we have . In effect, strategic suppliers misrepresent their costs functions through , which are greater than the true cost at every . On the other hand, strategic consumers misrepresent their utilities through , which are smaller than the true utility at every . Moreover, since the maximum value of occurs at . However, in our next result, we show that the social welfare at the Nash is bounded below and can be relatively close to the optimal value provided some minimum available production capacity. In order to compute bounds on price markups at the Nash equilibrium we utilize the Lerner index ( see Lerner (1934)), which we define as

| (16) |

The Lerner index measures a firm’s market power and it varies from zero to one, with higher values indicating greater market power. The following result summarizes the efficiency loss at the Nash equilibrium and the price markups.

Theorem 3

Suppose Assumptions 1-2 hold. Let be the socially optimal allocation from (1) and be the market allocation at the Nash equilibrium of . It follows that

| (17) |

where and . Moreover, when we have

| (18) |

Finally, the Lerner index at the Nash equilibrium satisfies

| (19) |

In effect, Theorem 3 provides a lower bound on the social welfare at the Nash equilibrium and an upper bound on the market price with respect to the true marginal cost of suppliers. Notice that is in the worst case 3/4 of the aggregate utility less of the aggregate costs at the efficient allocation. We do not claim this bound is tight; there may exist an even tighter bound on the social welfare the computation of which we relegate to future work. Higher values of yield values of the social welfare at the Nash equilibrium closer to . The worst-case values for arise when , although it never reaches it. Intuitively, when the aggregate production capacity of supply is relatively close to the total inelastic demand, then firms’ market power increases over consumers, gradually inducing pivotalness as . Specifically, for the efficiency loss can be arbitrarily high, similar to that derived by Xu et al. (2016) for a market with capacity-constrained suppliers. When the worst-case aggregate cost coefficient in (17) is equal to two and we recover the worst-case bound of Johari and Tsitsiklis (2011) derived for uncapacitated supply function competition. Moreover, (18) shows that provided some minimum available production capacity, the social welfare at the Nash equilibrium is no lower than 3/4 of the aggregate utility less 4/3 of the aggregate cost at the efficient allocation, which is not much lower than . From (19) note that the Lerner index is strictly less than one due to the non-pivotal supplier assumption. As grows large, goes to zero, indicating less market power on the supply side. As approaches , the index grows large implying high market power since there is little available capacity to supply anything more than the total inelastic demand.

6 Illustrative Examples

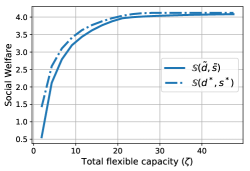

In this section we provide numerical experiments to illustrate the behavior of the social welfare under perfect competition and strategic interactions with respect to specific problem parameters. As shown in Section 5, the key parameter that affects social welfare is the total flexible capacity in the market .

Consider a market with and . Let each consumer have utility

Note that the above utility function is strictly concave and increasing and attains a minimum value for every . Moreover, every supplier incurs costs given by

The modified utility for each at which the Nash equilibrium can be computed via (13) is

Similarly, for each the modified cost is given by

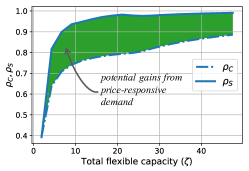

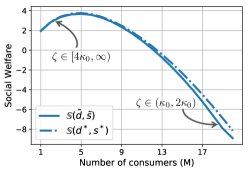

Figures 2a and 2b illustrate how social welfare under perfect competition and at the Nash equilibrium varies with respect to .222For the experiments we assumed that the vector of utility coefficients is and of the cost coefficients is . More specifically, we start with a value of —just slightly higher than and to avoid pivotal suppliers—and increase it gradually. Observe that the higher the value of the closer is to . On the other hand, the smaller is, the higher the efficiency loss at the Nash equilibrium. To gain additional insights, define the following ratio

For the special case in which the market has perfectly inelastic, non-strategic demand, we utilize the wost-case market performance metric , which is adjusted from Xu et al. (2016) and is given by

| (20) |

Figure 2b demonstrates that the worst-case value of occurs when where the ratio . Immediately after , the ratio jumps to and stays above after .

Note that lies everywhere above except when where =. This implies that although consumers are strategic, the market efficiency loss is lower-bounded by the worst-case performance of a market with perfectly inelastic demand. It remains to be shown whether this outcome holds more broadly, for any choice of cost and utility functions. Finally, increasing the number of consumers, while keeping the production capacity constant, widens the disparity between and as shown in Figure 2c. This illustrates the effect of increasing the inelastic portion of demand and as such inducing higher market power on the existing set of firms, which is also captured by the Lerner index in (19).

7 Conclusion

We studied a market with suppliers and consumers that compete in supply offers and demand bids for a product. Our analysis showed that with a specific family of scalar-parameterized offers/bids, the market supports an efficient competitive equilibrium. Under strategic interactions, we showed there exists a unique Nash equilibrium and propose an efficient way of computing the induced market allocation. Moreover, the welfare loss and the price markups at the Nash equilibrium are bounded. Understanding how uncertainty on the supply capacity and minimum demand affects the market outcome is an interesting direction for future research. Furthermore, a study of the market competition and efficiency loss when only one side (demand or supply) is strategic would complete the analysis of the deterministic model. The market mechanism presented here has multiple interesting applications. For example, owing to their simplicity, scalar-parameterized offers/bids can be effectively utilized to model competition among retail electricity customers that are becoming both consumers and producers, due to the proliferation of distributed energy resources.

References

- Baldick et al. [2004] R. Baldick, R. Grant, and E. Kahn. Theory and application of linear supply function equilibrium in electricity markets. Journal of Regulatory Economics, 25(2):143–167, Mar 2004.

- Daskalakis et al. [2009] C. Daskalakis, P. Goldberg, and C. Papadimitriou. The complexity of computing a nash equilibrium. SIAM Journal on Computing, 39(1):195–259, 2009.

- Day et al. [2002] C. J. Day, B. F. Hobbs, and Jong-Shi Pang. Oligopolistic competition in power networks: a conjectured supply function approach. IEEE Transactions on Power Systems, 17(3):597–607, Aug 2002.

- Johari and Tsitsiklis [2003] R. Johari and J. N. Tsitsiklis. Network resource allocation and a congestion game: the single link case. In 42nd IEEE International Conference on Decision and Control (IEEE Cat. No.03CH37475), volume 3, pages 2112–2117 Vol.3, Dec 2003.

- Johari and Tsitsiklis [2011] R. Johari and J. N. Tsitsiklis. Parameterized supply function bidding: Equilibrium and efficiency. Operations Research, 59(5):1079–1089, 2011.

- Johari et al. [2004] R. Johari, S. Mannor, and J. N. Tsitsiklis. Efficiency loss in a resource allocation game: A single link in elastic supply. In 2004 43rd IEEE Conference on Decision and Control (CDC) (IEEE Cat. No.04CH37601), volume 5, pages 4679–4683 Vol.5, Dec 2004.

- Klemperer and Meyer [1989] P. D. Klemperer and M. A. Meyer. Econometrica, (6), 1989.

- Lerner [1934] A. P. Lerner. The concept of monopoly and the measurement of monopoly power. The Review of Economic Studies, 1(3):157–175, 1934.

- Li et al. [2015] N. Li, L. Chen, and M. A. Dahleh. Demand response using linear supply function bidding. IEEE Transactions on Smart Grid, 6(4):1827–1838, July 2015.

- Lin and Bitar [2017] W. Lin and E. Bitar. A structural characterization of market power in power markets. CoRR, abs/1709.09302, 2017. URL http://arxiv.org/abs/1709.09302.

- Monderer and Shapley [1996] D. Monderer and L. S. Shapley. Potential games. Games and Economic Behavior, 14(1):124 – 143, 1996.

- Newbery [2008] D. Newbery. Predicting market power in wholesale electricity markets. Cambridge working papers in economics, Faculty of Economics, University of Cambridge, Aug 2008. URL https://ideas.repec.org/p/cam/camdae/0837.html.

- Shubik [1959] M. Shubik. Strategy and market structure. 1959.

- Swinand et al. [2010] G. Swinand, D. Scully, S. Ffoulkes, and B. Kessler. Modeling EU electricity market competition using the residual supply index. The Electricity Journal, 23(9):41 – 50, 2010.

- Tabors et al. [2016] R. Tabors, G. Parker, P. Centolella, and M. Caramanis. White Paper on Developing Competitive Electricity Markets and Pricing Structures. White paper, Tabors Caramanis Rudkevich (TCR), April 2016.

- Xu et al. [2016] Y. Xu, N. Li, and S. H. Low. Demand response with capacity constrained supply function bidding. IEEE Transactions on Power Systems, 31(2):1377–1394, March 2016.

Appendix A Proof of Theorem 1.

The crux of our derivations relies on Lagrangian duality to establish that the equilibrium conditions of (8)-(9) together with (10) are equivalent to the optimality conditions of (1). We begin with the consumer’s problem. The payoff in (6) is concave in each player’s action . Hence, the Karush-Kuhn-Tucker (KKT) optimality conditions are both necessary and sufficient. An optimal strategy must satisfy

| (21a) | |||

| (21b) |

Each supplier’s payoff is concave in the action . Moreover, an optimal strategy must lie in the closed interval . If not, then it is easy to show that for . Therefore, such strategies cannot occur at the equilibrium since they yield negative payoff. As such, an optimal strategy must satisfy

| (22a) | |||

| (22b) |

We now turn to problem (1) solved by the market manager. Associate Lagrange multiplier with the equality constraint (1b). The objective function is continuous and concave over a compact convex set. Therefore, there exists at least one optimal solution and that satisfy

| (23a) | |||

| (23b) |

Similarly, the supply vector must satisfy

| (24a) | |||

| (24b) |

Primal feasibility requires

| (25) |

Note that since and are strictly increasing and there exists at least one . If the pair satisfies (24b) and we let then satisfy (22b) and . In effect (24b) become equivalent to (22b). Similarly, if the pair satisifes (23b) and we let then satisfy (21b) and . In this case, (23b) become equivalent to (21b). Finally, the market clearing condition in (25) yields . Hence, is a competitive equilibrium. Now suppose that satisfy (21b),(22b) and (5). Let for and for . Then, it is easy to verify that the vector satisfies (23b) and (24b). Therefore, is an efficient allocation.

Appendix B Proof of Lemma 1.

Let firm be a pivotal supplier. Then it must hold

| (26) |

i.e., the total production capacity less that of ’s is less than the total inelastic demand in the market. In this case, the first derivative of the supplier’s payoff becomes

| (27) |

Therefore, the payoff is strictly increasing in the action and grows unbounded. A Nash equilibrium does not exist.

Appendix C Proof of Theorem 2.

We break the proof into five steps. First, we show that any Nash equilibrium has at least two positive components and we derive the necessary and sufficient conditions for such equilibrium. Next we establish the existence and uniqueness of the market allocation at the Nash equilibrium and derive the optimality conditions for (13). We show that under the demand bid (2) and the supply offer (3) the equilibrium conditions of all players become equivalent to the optimality conditions of (13). Finally, we establish uniqueness of the Nash equilibrium.

Step 1. Any Nash Equilibrium Has at Least Two Positive Components.

First, it is straightforward to see that cannot occur at the Nash equilibrium since and therefore the market does not clear. Next, we consider two cases. First, assume that . Fix firm and let . Note that, in this case, is not possible by the non-pivotal supplier assumption. A Nash equilibrium cannot exist with all consumers bidding zero and all but one supplier offering a strictly positive . Second, assume . Fix consumer and let . Then, implies . Hence, consumer faces a total available residual supply equal to . In this case, the payoff of consumer is given by

| (28) |

which is strictly increasing as becomes small and attains its maximum when . Thus for any there exists an infinitesimally smaller and positive that yields higher payoff. Moreover, by definition . A Nash equilibrium does not exist in this case. Hence, at the Nash equilibrium, the vector has at least two positive components.

Step 2. Necessary and Sufficient Nash Equilibrium Conditions. Having shown that any Nash equilibrium must have at least two positive components, we only focus in the region where . Note that, for each consumer (firm), her payoff is strictly concave in the action (). Hence, the KKT optimality conditions are both necessary and sufficient. Moreover, we must have

in order for . We have the following equilibrium conditions.

A demand profile is a Nash profile if and only if

| (29a) | |||

| (29b) |

A supply profile is a Nash equilibrium if and only if

| (30a) | |||

| (30b) |

The equilibrium conditions (29b) and (30b) are derived from the KKT conditions of each player’s payoff maximization problem, where the payoff of each consumer and supplier is given by expressions (11) and (12) respectively.

Step 3. Existence and Uniqueness of the Nash Market Allocation. Equipped with the above relations we now proceed to the market manager’s problem. Note that is strictly concave and is strictly convex. Hence, the objective function is continuous and strictly concave over a compact set. Specifically, the Hessian matrix of has diagonal elements

| (31) |

and for . Hence, is negative definite and there exists a unique optimal solution to (13).

Step 4. Necessary and Sufficient Conditions for the Market Allocation. Let be the unique optimal solution to (13). There exists a Lagrange mutliplier such that

| (32a) | |||

| (32b) | |||

| (32c) | |||

| (32d) | |||

| (32e) |

Note that since there is at least one and and are strictly increasing, then . Consider the action vectors for and for . Note that and for every consumer and every firm respectively. Suppose now that and for and let for . This implies that . Then from (32a) we have . However, we have for each . Therefore, (32b) cannot hold for every . Thus, the vector cannot have all components zero except one . Similarly, cannot have all components zero except one for some firm . This is obvious by the non-pivotal supplier assumption since it holds for every supplier . Hence, at least two components of are positive. Moreover, since if and only if , if and only if , then it is not hard to see that (32e) become equivalent to (29b)-(30b). Hence, the action vector is a Nash equilibrium. This also establishes existence of the Nash equilibrium.

We now reverse the argument. Let be a Nash equilibrium profile. That is, it satisfies (29b)-(30b). Therefore, it has at least two positive components and . Define the demand allocation for and the supply allocation for . It follows that satisfy (32e) with .

Step 5. Uniqueness of the Nash Equilibrium. We have shown that all Nash equilibria yield a unique market allocation. Uniqueness of the Nash equilibrium follows from the fact that the transformation from to is one-to-one.

Appendix D Proof of Theorem 3.

Step 1. Bounding the Price Markups To derive the upper bound on the Lerner index we note that at the Nash equilibrium there exists at least one firm such that or . Therefore,

| (33) |

Utilizing (33) and substituting in the expression of yields the bound in (19).

Step 2. Bounding the Social Welfare. Let and . In this step we aim to bound the social welfare at the Nash equilibrium, i.e., . Specifically,

| (34a) | ||||

| (34b) | ||||

| (34c) | ||||

| (34d) | ||||

| (34e) | ||||

| (34f) | ||||

| (34g) | ||||

Inequality (34a) follows from the optimality conditions of (13) while (34c) from the definitions of and . Inequality (34d) follows from concavity of and convexity of . Step (34e) follows from the fact that for every and for every . Inequality (34f) follows from concavity of and that

The last inequality follows from minimizing the expression , which is minimized for , where . Finally, note that is a decreasing function of . Hence, when the highest value of is 4/3.