Aggregated hold out for sparse linear regression with a robust loss function

Abstract

Sparse linear regression methods generally have a free hyperparameter which controls the amount of sparsity, and is subject to a bias-variance tradeoff. This article considers the use of Aggregated hold-out to aggregate over values of this hyperparameter, in the context of linear regression with the Huber loss function. Aggregated hold-out (Agghoo) is a procedure which averages estimators selected by hold-out (cross-validation with a single split). In the theoretical part of the article, it is proved that Agghoo satisfies a non-asymptotic oracle inequality when it is applied to sparse estimators which are parametrized by their zero-norm. In particular, this includes a variant of the Lasso introduced by Zou, Hastié and Tibshirani [49]. Simulations are used to compare Agghoo with cross-validation. They show that Agghoo performs better than CV when the intrinsic dimension is high and when there are confounders correlated with the predictive covariates.

1 Introduction

From the statistical learning point of view, linear regression is a risk-minimization problem wherein the aim is to minimize the average prediction error on a new, independent data-point , as measured by a loss function . When , this yields classical least-squares regression; however, Lipschitz-continuous loss functions have better robustness properties and are therefore preferred in the presence of heavy-tailed noise, since they require fewer moment assumptions on [8, 20]. Similarly to the norm in the least-squares case, measures of performance for estimators can be derived from robust loss functions by substracting the risk of the (distribution-dependent) optimal predictor, yielding the so-called excess risk.

In the high-dimensional setting, where with potentially , full linear regression cannot be achieved in general: the minimax excess risk is bounded below by a positive function of (proposition 2.2). Stronger assumptions on the regression coefficient are needed in order to estimate it consistently.

A popular approach is to suppose that only a small number of covariates are relevant to the prediction of , so that may be sought among the sparse vectors with less than non-zero components. Estimators which target such problems include the Lasso [36], least-angle regression [11] (a similar, but not identical method [16, Section 3.4.4]), and stepwise regression [16, Section 3.3.2]. In the robust setting, variants of the Lasso with robust loss functions have been investigated by a number of authors [22, 34, 6, 44].

Such methods generally introduce a free hyperparameter which regulates the ”sparsity” of the estimator; sometimes this is directly the number of non-zero components, as in stepwise procedures, sometimes not, as in the case of the Lasso, which uses a regularization parameter . In any case, the user is left with the problem of calibrating this hyperparameter.

Several goals are conceivable for a hyperparameter selection method, such as support recovery - finding the ”predictive” covariates - or estimation of a ”true” underlying regression coefficient with respect to some norm on . From a prediction perspective, hyperparameters should be chosen so as to minimize the risk, and a good method should approach this minimum. As a consequence, the proposed data-driven choice of hyperparameter should allow the estimator to attain all known convergence rates without any a priori knowledge, effectively adapting to the difficulty of the problem.

For the Lasso and some variants, such as the fused Lasso, Zou, Wang, Tibshirani and coauthors have proposed [49] and investigated [43, 38] a method based on Mallow’s and estimation of the ”degrees of freedom of the Lasso”. However, consistency of this method has only been proven [43] in an asymptotic setting where the dimension is fixed while grows, hence not the setting considered here. Moreover, the method depends on specific properties of the Lasso, and may not be readily applicable to other sparse regression procedures.

A much more widely applicable procedure is to choose the hyperparameter by cross-validation. For the Lasso, this approach has been recommended by Tibshirani [37], van de Geer and Lederer [39] and Greenshtein [13], among many others. More generally, cross-validation is the default method for calibrating hyperparameters in practice. For exemple, R implementations of the elastic net [12] (package glmnet), LARS [11] (package lars) and the huberized lasso [48] (package hqreg) all incorporate a cross-validation subroutine to automatically choose the hyperparameter.

Theoretically, cross-validation has been shown to perform well in a variety of settings [1]. For cross-validation with one split, also known as the hold-out, and for a bagged variant of v-fold cross-validation [23], some general oracle inequalities are available in least squares regression [26, Corollary 8.8] [46] [23]. However, they rely on uniform boundedness assumptions on the estimators which may not hold in high-dimensional linear regression. For the more popular V-fold procedure, results are only available in specific settings. Of particular interest here is the article [32] which proves oracle inequalities for linear model selection in least squares regression, since linear model selection is very similar to sparse regression (the main difference being that in sparse regression, the ”models” are not fixed a priori but depend on the data). This suggests that similar results could hold for sparse regression.

However, in the case of the Lasso at least, no such general theoretical guarantees exist, to the best of our knowledge. Some oracle inequalities [23, 30] and also fast rates [17, Theorem 1] have been obtained, but only under strong distributional assumptions: [23] assumes that has a log-concave distribution, [30] that is a gaussian vector, and [17, Theorem 1] assumes that there is a true model and that the variance-covariance matrix is diagonal dominant. Recently, Chetverikov et al. [7] have obtained fast rates (up to log-terms) for a certain class of conditional distributions (of given ) which are smooth transformations of Gaussian distributions. In contrast, there are also theorems [5] [17, Theorem 2] which make much weaker distributional assumptions but only prove convergence of the (in-sample) error at the ”slow” rate or slower. Though this rate is basically minimax [33] for the model

| (1) |

a hyperparameter selection method should adapt also to the favorable cases where the Lasso converges faster ([21, Theorem 14]); these results do not show that CV has this property.

Thus, the theoretical justification for the use of standard CV, which selects a single hyperparameter by minimizing the CV risk estimator, is somewhat lacking. In fact, two of the articles mentioned above introduce variants of CV which modify the final hyperparameter selection step; a bagged CV in [23] and the aggregation of two hold-out predictors in [5]. In practice too, there is reason to consider alternatives to hyperparameter selection in sparse regression: sparse estimators are unstable, and selecting only one estimator can result in arbitrarily ignoring certain variables among a correlated group with similar predictive power [47]. For the Lasso, these difficulties have motivated researchers to introduce several aggregation schemes, such as the Bolasso [3], stability selection [27], the lasso-zero [9] and the random lasso [45], which are shown to have some better properties than the standard Lasso.

Since aggregating the Lasso seems to be advantageous, it seems logical to consider aggregation rather than selection to handle the free hyperparameters. In this article, we consider the application to sparse regression of the aggregated hold-out procedure. Aggregated hold-out (agghoo) is a general aggregation method which mixes cross-validation with bagging. It is an alternative to cross-validation, with a comparable level of generality. In a previous article with Sylvain Arlot and Matthieu Lerasle [25], we formally defined and studied Agghoo, and showed empirically that it can improve on cross-validation when calibrating the level of regularization for kernel regression. Though we came up with the name and the general mathematical definition, Agghoo has already appeared in the applied litterature in combination with sparse regression procedures [18], among others [42], under the name ”CV + averaging” in this case.

In the present article, the aim is to study the application of Agghoo to sparse regression with a robust loss function. Theoretically, assuming an norm inequality to hold on the set of sparse linear predictors, it is proven that Agghoo satisfies an asymptotically optimal oracle inequality. This result applies also to cross-validation with one split (the so-called hold-out), yielding a new oracle inequality which allows norms of the sparse linear predictors to grow polynomially with the sample size. Empirically, Agghoo is compared to cross-validation in a number of simulations, which investigate the impact of correlations in the design matrix and sparsity of the ground truth on the performance of aggregated hold-out and cross-validation. Agghoo appears to perform better than cross-validation when the number of non-zero coefficients to be estimated is not much smaller than the sample size. The presence of confounders correlated to the predictive variables also favours Agghoo relative to cross-validation.

2 Setting and Definitions

The problem of non-parametric regression is to infer a predictor from a dataset of pairs, where and . The pairs will be assumed to be i.i.d, with joint distribution . The prediction error made at a point is measured using a non-negative function of the residual . The global performance of a predictor is assessed on a new, independent data point drawn from the same distribution using the risk . The optimal predictors are characterized by a.s. The risk of any optimal predictor is (in general) a non-zero quantity which characterizes the intrinsic amount of “noise” in unaccounted for by the knowledge of . A predictor can be compared with this benchmark by using the excess risk . Taking yields the usual least-squares regression, where and . However, the least-squares approach is known to suffer from a lack of robustness [20, Chapter 7]. For this reason, in the field of robust statistics, a number of alternative loss functions are used. One popular choice was introduced by Huber [19].

Definition 2.1

Let . Huber’s loss function is .

When , converges to the least-squares loss. When , converges to the absolute value loss of median regression. Thus, the parameter allows a trade-off between robustness and approximation of the least squares loss.

The rest of the article will focus on sparse linear regression with the loss function . Thus, notations , and are to be understood with respect to .

2.1 Sparse linear regression

With finite data, it is impossible to solve the optimization problem over the set of all predictors . Some modeling assumptions must be made to make the problem tractable. A popular approach is to build a finite set of features and consider predictors that are linear in these features: . This is equivalent to replacing with and regressing on . For theoretical purposes, it is thus equivalent to assume that for some and predictors are linear: .

As the aim is to reduce the risk , a logical way to choose is by empirical risk minimization:

Empirical risk minimization works well when but will lead to overfitting in large dimensions [41]. Indeed, if is too large, no estimator can succeed at minimizing the risk over , as the following proposition shows.

Proposition 2.2

Let and be a positive definite matrix of dimension . For any , let denote the distribution such that iff almost surely, , where , and are independent. Then for any ,

where denotes the infimum over all estimators and denotes the linear functional .

Proposition 2.2 is proved in appendix A. With respect to , the lower bound of proposition 2.2 scales as when and as when , as could be expected from the definition of the Huber loss (Definition 2.1). With respect to and , it scales as when . Moreover, there is a positive lower bound on the minimax risk when is of order . Thus, for such large values of , consistent risk minimization cannot be achieved uniformly over the whole of .

Sparse regression attempts instead to locate a “good” subset of variables in order to optimize risk for a given model dimension. The Lasso [37] is now a standard method of achieving sparsity. The specific version of the Lasso which we consider here is given by the following definition.

Definition 2.3

Let and let be a dataset such that and for all and some . Let be the Huber loss defined in Definition 2.1. For any , let

| (2) |

Now let

2.2 Hyperparameter tuning

The zero-norm of a vector is the integer . Many sparse estimators, such as best subset or forward stepwise [16, Section 3.3], are directly parametrized by their desired zero-norm, which must be chosen by the practitioner. It controls the “complexity” of the estimator, and hence the bias-variance tradeoff. In the case of the standard Lasso (Definition 2.3 with ), Zou, Hastie and Tibshirani [49] showed that is an unbiased estimator of the “degrees of freedom” of the estimator . As a consequence, [49] suggests reparametrizing the lasso by its zero-norm. Applying their definition to the present setting yields the following.

Definition 2.4

The (optional) constraint has some potential practical and theoretical benefits. From the practical viewpoint, it allows to reduce the computational complexity by excluding lasso solutions with excessively large norm, which may be expected to perform poorly anyway. From a theoretical viewpoint, it helps control the norms of the predictor , thus avoiding inconsistency issues encountered by the empirical risk minimizer for some pathological designs [31] .

More generally, consider any sequence of learning rules which output linear predictors . To prove the main theoretical result of this article (Theorem 3.2), we make the following assumptions on the collection .

Hypothesis 2.1

For any , let denote a dataset of size . Assume that

-

1.

Almost surely, for all , .

-

2.

For all , ,

where

Moreover, condition 1 is naturally satisfied by such sparse regression methods as forward stepwise and best subset [16, Section 3.3]. Condition 3 states that the intercept is chosen by empirical risk minimization, with a specific tie-breaking rule in case the minimum is not unique.

2.3 Aggregated hold out applied to the zero-norm parameter

The tuning of the zero-norm is important to ensure good prediction performance by optimizing the bias-variance tradeoff. Depending on the application, practicioners may want more or less sparsity, depending on their requirements in terms of computational load or interpretability. For this reason, we consider the problem of selecting the zero-norm among the set , for some which may depend on the sample size. This article investigates the use of Agghoo in this context, as an alternative to cross-validation. Agghoo is a general hyperparameter aggregation method which was defined in [25], in a general statistical learning context. Let us briefly recall its definition in the present setting. For a more detailed introductory discussion of this procedure, we refer the reader to [25]. To simplify notations, fix a collection of linear regression estimators. First, we need to define hold-out selection of the zero-norm parameter.

Definition 2.5

Let be a dataset. For any , denote . Let then

Using the hyperparameter together with the dataset to train a linear regressor yields the hold-out predictor

Aggregation of hold-out predictors is performed in the following manner.

Definition 2.6

Let be a collection of subsets of , where . Let:

Agghoo outputs the linear predictor:

Thus, Agghoo also yields a linear predictor, which means that it can be efficiently evaluated on new data. If the have similar support, will also be sparse: this will happen if the hold-out reliably identifies a true model. On the other hand, if the supports have little overlap, the Agghoo coefficient will lose sparsity, but it can be expected to be more stable and to perform better.

The linear predictors aggregated by Agghoo are only trained on part of the data. This subsampling (typically) decreases the performance of each individual estimator, but combined with aggregation, it may stabilize an unstable procedure and improve its performance, similarly to bagging.

An alternative would be to retrain each regressor on the whole data-set , yielding the following procedure, which we call ”Aggregated cross-validation” (Agcv).

Definition 2.7

Let be a collection of subsets of , where . Let:

The output of Agcv is the linear predictor:

Agghoo is easier to study theoretically than Agcv due to the conditional independence: . For this reason, the theoretical section will focus on Agghoo, while in the simulation study, both Agghoo and Agcv will be considered.

In comparison to Agghoo and Agcv, consider the following definition of a general cross-validation method.

Definition 2.8

Let be a collection of subsets of , where . Let

Let then

CV outputs the linear predictor

This makes clear the difference between cross-validation and Agghoo (or Agcv): cross-validation averages the hold-out risk estimates (and selects a single linear predictor) whereas Agghoo and Agcv aggregate the selected predictors . If the parameter is used instead of the in Definition 2.6, this yields the bagged CV method of Lecué and Mitchell [23]. This method applies bagging to individual estimators , whereas Agghoo also bags the estimator selection step. When there is a single, clearly established optimal model of small dimension, the advantages of a more accurate model selection step (as in CV and its bagged version) may outweigh the gains due to aggregation. In contrast, when there are many different sparse linear predictors with close to optimal performance, model selection will be unstable and aggregation should provide benefits relative to selection of a single parameter .

2.4 Computational complexity

There are two types of computational costs to take into account when considering a (sparse) linear predictor such as : the cost of calculating the parameters at training time and the cost of making a prediction on new data, i.e computing for some . In this section, Agghoo, Agcv and cross-validation are compared with respect to these two types of complexity.

Let be some finite collection of sparse linear regression estimators. Let denote the expected maximal number of non-zero coefficients. In particular, under point 1 of hypothesis 2.1, . Let and , where is given by hypothesis (Reg-) below (equation 4).

Computational complexity at training time

Agghoo, Agcv and cross-validation must all compute the hold-out risk estimator for each subset in and each . Let denote the number of operations needed for this.

For a given subset , the estimators must be computed for all , which may be more or less expensive depending on the method. In the case of the Lasso, the whole path can be computed efficiently using the LARS-Lasso algorithm [11].

Then, the empirical risk of all estimators must be calculated on the test set. On average, this takes at least operations to compute the risk of the least sparse ( scalar products involving an average of non-zero coefficients) and at most operations in general. In particular, .

In a next step, Agghoo and agcv compute the minima of vectors of length , whereas cross-validation averages these vectors and calculates the argmin of the average. Both operations have complexity of order .

It is in their final step that the three methods differ slightly. Agghoo uses the which have been computed in a previous step, whereas Agcv and cross-validation must compute the and , respectively. The complexity of this depends on the method, but can be expected to be small compared to , as there is only one estimator to fit instead of .

Finally, Agghoo and Agcv must aggregate vectors drawn from the and , with respective complexity and , provided that a suitably ”sparse” representation is used for the . Assuming , this is negligible compared to .

All in all, Agghoo, Agcv and cross-validation have a similar complexity at training time, of order , with most likely being the dominant term.

Evaluation on new data

Given new data , the complexity of evaluating is proportional to . If the sparse estimators perform as intended and consistently identify similar subsets of predictive variables, then Agghoo and Agcv sould not lose much sparsity compared to CV, as the and should all have similar supports.

At worst, if the supports of the are disjoint, may be as much as times greater than . In contrast, should heuristically be of the same order as – as both and optimize the same bias-variance tradeoff with respect to the ”complexity parameter” . However, this situation is one in which the hold-out is very unstable, so Agghoo can be expected to yield significant improvements in exchange for the increased computational cost. The same argument applies to agcv.

3 Theoretical results

Let and denote an i.i.d dataset with common distribution . Let be a collection of linear regressors which satisfies assumption 2.1. Let be a collection of subsets of . In this section, we give bounds for the risk of the Agghoo estimator (Definition 2.6) built from the collection .

3.1 Hypotheses

To state and prove our theoretical results, a number of hypotheses are required. First, the collection of subsets - chosen by the practitioner - should satisfy the following two conditions.

(Reg)

There exists an integer such that and

| (4) |

Let also denote the size of the validation sets.

Independence of from ensures that for , is also iid with distribution . The assumption that contains sets of equal size ensures that the pairs are equidistributed for . Most of the data partitioning procedures used for cross-validation satisfy hypothesis (Reg- ), including leave--out, -fold cross-validation (with ) and Monte-Carlo cross-validation [1].

To state an upper bound for , we also need to quantify the amount of noise in the distribution of given , in a way appropriate to the Huber loss . That is the purpose of the following assumption.

(Lcs)

Let . Let denote an optimal predictor, i.e a measurable function such that for almost all . Assume that there exists and a positive real number such that

| (5) |

where denotes the parameter of the Huber loss.

Equation (5) is specific to the Huber loss: it requires the conditional distribution of the residual to put sufficient mass in a region where the Huber function is quadratic. For example, assume that where is independent from and has a continuous, positive density in a neighbourhood of . If the Huber parameter is proportional to or larger than , then a constant value of can be chosen, independently of . On the other hand, if , the optimal value of satisfies .

Finally, some hypotheses are needed to deal with pathological design distributions which can in general lead to inconsistency of empirical risk minimization [31]. To illustrate the problem as it applies to the hold-out, consider a distribution such that for some vector subspace , as in [31]. Assume to simplify that . Let denote the orthogonal projection on . With small, but positive probability, for all . On this event, it is clearly impossible to estimate . Likewise, the hold-out cannot correctly assess the impact of the orthogonal components of the estimators on the risk, since only depends on , whereas out of sample predictions may depend on (since ). This means that the hold-out-selected predictors may be arbitrarily far from optimal in general.

To avoid this issue, two sets of assumptions have been made in the litterature. First, there are boundedness assumptions: for example, if the predictors and the variable are uniformly bounded, this clearly limits the impact of low-probability events such as on the risk. Such hypotheses have been used to prove general oracle inequalities for the hold-out [14, Chapter 8] [26, Corollary 8.8] and cross-validation [40]. Alternatively, pathological designs can be excluded from consideration by assuming an norm inequality or ”small ball” type condition [28, 29]: this has been used to study empirical risk minimization over linear models [31, 2].

In this article, a combination of both approaches is used. First, we assume a weak uniform upper bound on norms of the predictors (hypothesis (Uub)). The bound is allowed to grow with at an arbitrary polynomial rate.

(Uub)

Let be iid with distribution , where is given by hypothesis (Reg- ). Let be independent from . There exist real numbers such that

-

1.

-

2.

For the Lasso, if in Definition 2.3, then hypothesis (Uub) holds if in addition . This is the case if the components of have variance and is polynomial in , or if the components of are sub-exponential with constant and is polynomial in .

Hypothesis (Uub) is much weaker than boundedness assumptions usually made in the litterature, where typically the norm is used instead of the norm, and the bound is a constant rather than a polynomial function of . Point of Hypothesis (Uub) is natural in the sense that an estimator which violates it cannot perform well anyway: assuming that , by definition of , for any ,

| (6) |

Thus, if grows faster than , then so do the expected risk and expected excess risk of . Point of Hypothesis (Uub) can be seen as an ”empirical version” of point 1, wherein the independent variable is replaced by the elements of . The lack of independence between and makes this condition less straightforward than . However, by the Cauchy-Schwarz inequality, it is always the case that . Thus, it is enough to suppose that and are bounded by for some .

Together with the weak uniform bound (Uub), we assume that for sparse linear predictors with , the norm is equivalent to the stronger ”Orlicz norm” defined below.

Definition 3.1

Let be a real random variable. Let . The norm of is defined by the formula

with the convention . We say that if .

Plainly, if and only if is sub-exponential; it can be shown that is indeed a norm.

The constant relating and is allowed to depend on in the following way.

(Ni)

Let and . For any , let

| (7) |

There exists a constant such that

| (8) |

The interpretation of this hypothesis is not obvious. Note first that is a non-decreasing function of , and in particular,

Unlike , is invariant under linear transformations of : in other words, it only depends on the linear space spanned by the columns of . In particular, does not depend on the covariance matrix of , provided that it is non-degenerate. The inequality can be interpreted as an effective, scale invariant version of sub-exponentiality: it states that the tail of is sub-exponential with a scale parameter which isn’t too large compared to its standard deviation. In sections 3.3 , 3.4 and 3.5, we shall give examples where simple bounds can be proved for or .

3.2 Main Theorem

When Agghoo is used on a collection of linear regression estimators satisfying Hypothesis (2.1), such as the Lasso parametrized by the number of non-zero coefficients, as in Definition 2.4, the following theorem applies.

Theorem 3.2

Let and be random variables with joint distribution such that hypothesis (Lcs) holds. Let be a dataset of size . Let , where is given by assumption (Reg- ). Let denote the Huber loss parameter from Definition 2.1.

Let be an integer such that and be a collection of linear regression estimators which satisfies hypothesis (2.1). Assume that hypotheses (Ni) and (Uub) hold.

There exist numerical constants such that, for any such that ,

| (9) |

Theorem 3.2 is proved in appendix B. Theorem 3.2 compares the excess risk of Agghoo to that of the best linear predictor in the collection , trained on a subset of the data of size . Taking in Theorem 3.2 yields an oracle inequality for the hold-out, which is also cross-validation with one split. It is, to the best of our knowledge, the first theoretical guarantee on hyperparameter aggregation (or selection) for the huberized Lasso. That appears in the oracle instead of is a limitation, but it is logical, since estimators aggregated by Agghoo are only trained on samples of size . Typically, the excess risk increases at most by a constant factor when a dataset of size is replaced by a subset of size , and this constant tends to as . This allows to take of order (), while losing only a constant factor in the oracle term.

In addition to the oracle, , the right hand side of equation (9) contains two remainder terms. Since , the second of these terms is always negligible with respect to the first as for fixed . Assuming that are both of order , the first remainder term is with respect to . In comparison, the minimax risk for prediction in the model is greater than a constant times by proposition 2.2. Thus, if more than independent components of are required for prediction of , the remainder term can be expected to be negligible compared to the oracle as a function of .

As a function of a scale parameter in a model , where is distributed symmetrically around , the remainder term scales as , where depends only on and on the fixed distribution of . When is lower bounded and if is sufficiently regular, then (see the discussion of hypothesis (Lcs)). In that case, the rate is the same as in the minimax lower bounds of Proposition 3.2, and can therefore be considered correct. When , is suboptimal for Gaussian distributions , where the correct scaling is (by Proposition 2.2 and a simple comparison with least squares). However, Theorem 3.2 makes no moment assumptions whatsoever on the residual - thus, it is logical that the parameter , which controls the robustness of the Huber loss, should appear in the bound.

In equation (9), there is a tradeoff between the oracle and the remainder terms, governed by the tuning parameter . must be larger than a positive constant depending on and ; as a result, Theorem 3.2 only yields a nontrivial result when . Note that hypothesis (Ni), which defines , allows to decrease with as fast as , in case is a constant - as when is gaussian (see section 3.3 below). Assuming only that and that the remainder term is negligible compared to the oracle, equation (9) proves that by taking slowly enough - an ”optimal” oracle inequality.

3.3 Gaussian design

In the case where is a Gaussian vector, follows a centered normal distribution. As a result, - defined in equation (7) - is a fixed numerical constant, equal to , where . It follows that for any fixed , hypothesis (Ni) holds as soon as is large enough.

Moreover, for Gaussian design, it is possible to show that the Lasso estimators of Definition 2.4 satisfy hypothesis (Uub) for any (including ), as long as has some moments and isn’t too large. More precisely, hypothesis (Uub) holds with independent from . This leads to the following corollary.

Corollary 3.3

Assume that is a Gaussian vector, that for some , and that hypothesis (Lcs) holds. Let and let be the Agghoo estimator built from the collection . Assume that and

| (10) |

There exist numerical constants such that for all and all ,

Corollary 3.3 allows to take at any rate slower than , so that the asymptotic constant in front of the oracle is . The constraint (10) imposed on by Corollary 3.3 is mild, since there are strong practical and theoretical reasons to take much smaller than anyway: this enforces sparsity – minimizing computational complexity and improving interpretability – and allows better control of the minimax risk (Proposition 2.2). Equation (10) serves only to prove that satisfies hypothesis (Uub), hence it could be replaced by a polynomial bound on and on , as explained in the discussion of hypothesis (Uub).

3.4 Nonparametric bases

Given real random variables , a linear model may be a poor approximation to the actual regression function . A popular technique to obtain a more flexible model is to replace the one-dimensional variable with a vector , where spans a space of functions known for its good approximation properties, such as trigonometric polynomials, wavelets or splines ([16, Chapter 5]). is practically always allowed to tend to as grows to make sure that the approximation error of by functions in converges to . In this section, we discuss conditions under which Theorem 3.2 applies to such models.

It turns out that most of the classical function spaces satisfy an equation of the form

where is some constant independent of [4, Section 3.1]. By replacing , defined on , by defined on , we can see that the correct scaling with respect to is . Thus, if the distribution of dominates the uniform measure on , in the sense that for some and any measurable , , then

In particular, if contains the constant functions - which is the case with splines, wavelets and trigonometric polynomials - then equation (7) holds with of order . Thus, equation (30) of hypothesis (Ni) holds under the assumption that for some constant . Assuming that and are both of order (for example, a fold split with fixed ), this assumption is mild: as a consequence of [14, Theorem 11.3] and approximation-theoretic properties of the spaces [10], taking , for example, is sufficient to attain minimax convergence rates [35] [14, Theorem 3.2] over standard classes of smooth functions.

Note that even though , this does not in general imply that : for example, in the case of regular histograms on , so and when , . The property does, however, hold in the case of the Fourier basis: as a result, may be arbitrarily large, and only bounds on (the maximal zero-norm of the estimators) are required. We examine this case in detail in the following section.

3.5 The Fourier basis

Suppose that real variables are given, and that we wish to find the best predictor of among periodic functions of . Let denote the minimizer of the risk among all measurable periodic functions on . For all , let and . Let , where and . One can easily show that , where minimizes among measurable functions on . By taking large and using sparse methods, it is possible to approximate functions which have only a small number of non-zero Fourier coefficients, but potentially at high frequencies, as is commonly the case in practice [15].

Let be a collection of sparse linear regression estimators satisfying hypothesis 2.1 and let denote the predictor . Given this initial collection of linear predictors, Definition 3.4 below constructs a second collection which also satisfies hypothesis (Uub) under an appropriate distributional assumption (Corollary 3.6, equation (14)).

Definition 3.4

Let be defined by

| (11) |

where

For any , let .

By construction, also satisfies hypothesis 2.1. Replacing by may improve performance and cannot significantly degrade it, as proposition 3.5 below makes clear.

Proposition 3.5

Assume that for some and let . If

| (12) |

for some numerical constant ,

| (13) |

Theorem 3.2 can be applied to the collection , which yields the following Corollary.

Corollary 3.6

Assume that has a density such that

| (14) |

Assume that there exists such that almost surely,

There exists a constant such that, if

| (15) |

for some , then

| (16) |

If the periodicity of represents (say) a yearly cycle, then Equation (14) states that each ”time of year” is sampled with a positive density, i.e that the density of is lower bounded by a positive constant on . This ensures that equation (7) holds with of order , so that hypothesis (8) reduces to . In particular, if is constant and is of order , then is allowed to grow with at rate . This is a reasonable restriction, as by Proposition 2.2, one cannot expect to estimate more than coefficients with reasonable accuracy (a convergence rate being too slow for most practical purposes).

Corollary then deduces an oracle inequality with leading constant (arbitrarily close to ) and remainder term of order , which is typically negligible in the non-parametric setting of this corollary. For this reason, corollary 3.6 can be said to be optimal, at least up to constants.

3.6 Effect of V

The upper bound given by Theorem 3.2 only depends on through and . The purpose of this section is to show that for a given value of , increasing always decreases the risk. This is proved in the case of monte carlo subset generation defined below.

Definition 3.7

For and , let be generated independently of the data by drawing elements independently and uniformly in the set

For fixed , the excess risk of Agghoo is a non-increasing function of .

Proposition 3.8

Let be two non-zero integers. Let . Then:

Proof Let . Let . Then

It follows by convexity of that

For any , and is independent of , therefore . This yields the result.

It can be seen from the proof that the proposition also holds for Agcv. Thus, increasing can only improve the performance of these methods. The same argument does not apply to CV, because CV takes an argmin after averaging, and the argmin operation is neither linear nor convex. Indeed, no comparable theoretical guarantee has been proven for CV, to the best of our knowledge, even though increasing the number of CV splits (for given ) generally improves performance in practice.

Proposition 3.8 does not quantify the gain due to aggregation. This gain depends on the properties of the convex functional , in particular on its modulus of strong convexity in a neighbourhood of the target (assuming that at least some estimators in the collection are close to ). Moreover, as for any loss function, the gain due to aggregation depends on the diversity of the collection : the more the hold-out estimators vary with respect to , the greater the effect of aggregation.

More precisely, under hypothesis (Lcs), we can prove the following improvement to Proposition 3.8.

Proposition 3.9

Let be independent from . Assume that satisfies hypothesis (Lcs). For any , let denote the event . Then for any ,

| (17) |

When is small enough, the event occurs with high probability. As a consequence, if , then

| (18) |

where denotes the largest median of a random variable .

Proposition 3.9 is proved in appendix C.3. It quantifies the gain due to aggregation in terms of the parameter of the Huber loss, the constant given by hypothesis (Lcs) and the distance between two hold-out estimators that are close enough to . Taking recovers the least-squares case, where and there are no constraints on . Only two indices appear in the right-hand side of equation (17): that is a consequence of the exchangeability of the collection for Monte-Carlo subset generation. The same result also applies to fold Agghoo, since it also yields an exchangeable collection. For arbitrary , all distinct pairs of indices would have to be considered.

Going beyond proposition 3.9 requires giving nontrivial lower bounds on , which is no easy task, given the complex dependencies involved. Results in this direction have only recently been obtained in the setting of least-squares density estimation [24, Chapters 5-6].

A few general heuristics apply: first, if there is one learning rule in the collection which is much better than the others, the hold-out can be expected to select it most of the time: in that case, Agghoo reduces to bagging, and potential gains depend on the stability of . In contrast, if there are many rules which are close to optimal, while being distant from each other, then the gains of aggregation can be expected to be large, even if the individual rules are stable.

4 Simulation study

This section focuses on hyperparameter selection for the Lasso with huber loss, either using a fixed grid or using the reparametrization from Definition 2.4. The methods considered for this task are Aggregated hold-out given by Definition 2.6, Aggregated cross-validation given by Definition 2.7 and standard cross-validation given by Definition 2.8. In all cases, the subsamples are generated independently from the data and uniformly among subsets of a given size , as in Definition 3.7. Thus, all three methods share the same two hyperparameters: , the fraction of data used for training the Lasso, and , the number of subsets used by the method.

For the huberized Lasso with a fixed grid, the hqreg_raw function from the R package hqreg [48] is used with a fixed grid designed to emulate the default choice: a geometrically decreasing sequence of length , with maximum value and minimum value . The fixed value of is obtained by averaging the (data-dependent) default value chosen by hqreg_raw over independent datasets. To compute the reparametrization given by Definition 2.4, we implemented the LARS-based algorithm described by Rosset and Zhu [34], which allows to compute the whole regularization path.

I.i.d training samples of size are generated according to a distribution , where and , with independent from . To illustrate the robustness of the estimators, Cauchy noise is used: . The performance of Agghoo and cross-validation may depend on the presence of correlations between the covariates and the sparsity of the ground truth . To investigate these effects, three parametric families of distribution are considered for , in sections 4.1, 4.2 and 4.3.

The risk of each method is evaluated on an independent training set of size , and results are averaged over repetitions of the simulation. More precisely, training sets of size are generated, along with test sets , each of size . For each simulation and any learning rule among the six obtained by combining Agghoo, monte carlo CV and AGCV with either a fixed grid or the zero-norm parametrization, the average excess risk

is computed on the test set for all values of and .

4.1 Experimental setup 1

is generated using the formula , where are independent standard Gaussian random variables, and is a parameter regulating the strength of the correlations. The regression coefficient has a support of size drawn at random from , and is defined by , where is a uniform random permutation, if and if , with calibrated so that . The noise parameter is , while the Huber loss parameter is set to – a suboptimal choice in this setting, but convenient for computing the huberized Lasso regularization path.

Choice of parameter

For all methods, in most cases the optimal value of is or , similarly to what was observed in the rkhs case [25], where was recommended. Table 1 displays the quantity

where Sd denotes the (empirical) standard deviation and the optimal choice of , Thus, values of bigger than a few units suggest that is suboptimal to a statistically significant degree. When , is displayed in black on table 1. When , is displayed in blue on table 1. Exceptions where are highlighted in red, with the value .

| r = 150 | r = 60 | r = 24 | ||||||

|---|---|---|---|---|---|---|---|---|

| method | V | 15 | 1 | 15 | 1 | 15 | 1 | |

| 1 | grid agghoo | 1 | 2.2 | 2.7 | 3.0 | 2.7 | 0.5 | 5.6 |

| 2 | grid agghoo | 2 | 2.5 | 2.1 | 3.1 | 1.4 | 1.0 | 7.9 |

| 3 | grid agghoo | 5 | 2.5 | 6.8 | 3.5 | 0.6 | 0.6 | 11.9 |

| 4 | grid agghoo | 10 | 0.7 | 7.2 | 3.7 | 1.1 | 4.5 | 16.7 |

| 5 | grid cv | 1 | 1.0 | 3.9 | 1.6 | 0.1 | 1.2 | 1.5 |

| 6 | grid cv | 2 | 0.8 | 5.0 | 2.6 | 0.5 | 1.4 | 1.1 |

| 7 | grid cv | 5 | 1.4 | 2.8 | 1.5 | 0.8 | 0.5 | 3.7 |

| 8 | grid cv | 10 | 2.0 | 2.6 | 2.9 | 1.1 | 1.6 | 5.9 |

| 9 | grid agcv | 1 | 1.0 | 3.9 | 1.6 | 0.1 | 1.2 | 1.5 |

| 10 | grid agcv | 2 | 0.3 | 2.0 | 1.4 | 1.9 | 0.3 | 0.8 |

| 11 | grid agcv | 5 | 0.3 | 2.2 | 0.5 | 0.7 | 0.5 | 1.1 |

| 12 | grid agcv | 10 | 0.5 | 0.4 | 0.0 | 0.3 | 0.8 | 1.0 |

| 13 | norm agghoo | 1 | 1.3 | 4.1 | 2.0 | 0.3 | 0.5 | 5.6 |

| 14 | norm agghoo | 2 | 3.0 | 1.4 | 3.2 | 1.3 | 1.9 | 9.2 |

| 15 | norm agghoo | 5 | 4.0 | 6.7 | 5.1 | 3.3 | 4.0 | 13.7 |

| 16 | norm agghoo | 10 | 4.6 | 7.3 | 7.0 | 3.7 | 5.2 | 18.5 |

| 17 | norm cv | 1 | 4.3 | 9.4 | 4.3 | 1.1 | 2.0 | 3.9 |

| 18 | norm cv | 2 | 1.9 | 7.2 | 1.8 | 4.4 | 4.8 | 2.7 |

| 19 | norm cv | 5 | 2.7 | 5.3 | 2.4 | 3.3 | 1.5 | 0.7 |

| 20 | norm cv | 10 | 6.1 | 4.6 | 5.4 | 3.5 | 0.6 | 0.1 |

| 21 | norm agcv | 1 | 4.3 | 9.4 | 4.3 | 1.1 | 2.0 | 3.9 |

| 22 | norm agcv | 2 | 1.9 | 5.8 | 2.4 | 4.5 | 5.9 | 3.5 |

| 23 | norm agcv | 5 | 2.1 | 1.9 | 1.0 | 4.0 | 5.7 | 3.7 |

| 24 | norm agcv | 10 | 4.5 | 1.0 | 3.3 | 3.6 | 7.3 | 3.9 |

Most of the exceptions occur on the column , , while most of the others are of low statistical significance, with values less than on the fourth column ( and ). Thus, table 1 confirms the claim that for all methods, in most cases. For grid agghoo, norm agghoo, grid agcv and , for all simulations. Comparing now and , grid agghoo and norm agghoo with show a clear pattern: is better or as good as in all cases except where is significantly better. For other methods, results are not so clear and the difference in risk between the two values of is often insignificant.

Choice of

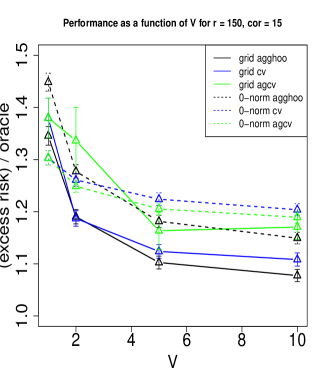

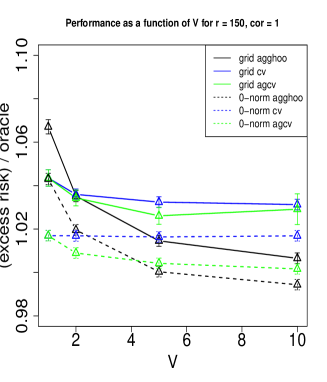

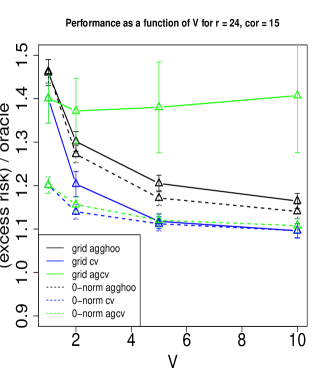

For all methods considered, performance is expected to improve when is increased, but by how much? If the performance increase is too slight, it may not be worth the additional computational cost. In figure , the mean excess risk for the optimal value of is displayed as a function of , with error bars corresponding to one standard deviation. The scale used for the vertical axis in each graph is the average excess risk of the oracle with respect to the fixed grid over the parameter. Quantifying performance as a percentage of the oracle risk, when , Agghoo improves by roughly from to , by roughly from to and by a few percent more from to . CV with the standard grid behaves similarly in these two simulations, while CV with the zero-norm parametrization shows much less improvement when is increased. Thus, taking is advantageous, but there are clearly diminishing returns to choosing much larger than this. For CV with the zero-norm parametrization, seems sufficient in these simulations .

Comparison between methods

From figure 1, it appears that grid agcv is a very poor choice, being worse than both grid agghoo and grid cv for all values of when , and being the worst of all the methods for when , as well as highly unstable, as the size of the error bars clearly shows.

Interestingly, norm agcv behaves much better, being the second best method when , and very close to the best when and .

Generally speaking, of the two types of parametrization of the Lasso, the zero-norm parametrization appears to perform better than the standard grid when correlations are small (), while the performance is significantly worse when and .

Comparing now Agghoo and CV, Agghoo appears to be better than CV when in situations where is larger (). This seems to hold for both the standard parametrization (grid agghoo) and the zero-norm one (norm agghoo). The relation is reversed for small , with CV performing better than Agghoo for all values of when .

Further studies

The previous simulations suggest that Agghoo performs better than CV in the case of high intrinsic dimension. This behaviour is logical, since the cross-validated Lasso will ignore some predictive variables when there are too many of them, and randomized aggregation may help recover more of the support. However, the effect of correlations is unclear. Experimental setup 1 mixes different types of correlations: correlations between predictive variables, correlations between predictive and non-predictive variables, and correlations among non-predictive variables. It is possible that one type of correlation favours Agghoo while another favours CV.

To gain a more accurate idea of when Agghoo is advantageous over CV, two more settings are studied, considering separately correlations among predictive variables, and between predictive and non-predictive variables. Since previous simulations showed that and were the optimal parameters, only those parameters will be considered in the following.

Since the choice of lasso parametrization did not seem to affect the relative performance of Agghoo and CV, we only consider the standard parametrization, as it is more popular and also easier to use in our simulations. Agcv is not considered either, since it was discovered to be unreliable in previous simulations.

4.2 Experimental setup 2: correlations between predictive and noise variables

Let be the number of predictive variables and let each predictive covariate have ”noise” covariates which are correlated with it at level . Assume that , where is the total number of variables. Let , and be independent standard gaussian variables. For any and any , let and for , let . For the regression coefficient, choose , where . Let then be distributed conditionnally on as . The loss function used here is with .

Results

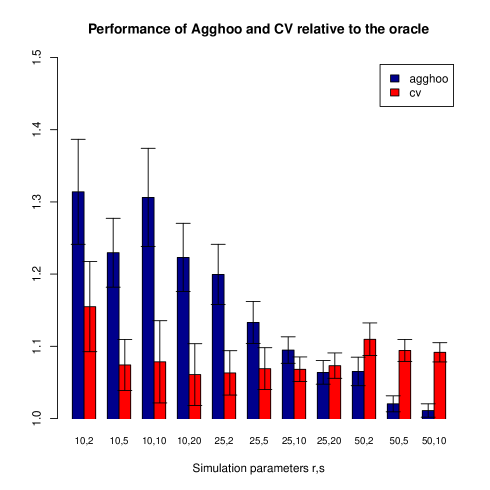

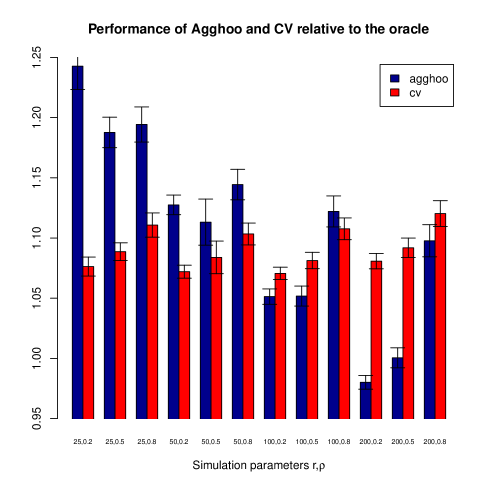

Figure 2 shows a bar plot of the average excess risk of CV and Agghoo as a fraction of the average risk of the oracle. 90 % error bars were estimated using a normal approximation. Parameters used for Agghoo and CV were and ( yields similar result).

Overall, Agghoo’s risk relative to the oracle significantly decreases as the zero-norm of increases from to , as was observed in section 4.1 . For and separately, the risk relative to the oracle significantly decreases as increases from to . For , this trend is unclear due to the random errors.

In contrast, CV’s performance relative to the oracle shows no statistically significant trend either as a function of or as a function of .

As a result of these trends, Agghoo performs significantly worse than CV for and significantly better when , especially when . When , CV performs significantly better than Agghoo for and and they perform similarly when and .

4.3 Experimental setup 3: correlations between predictive variables

We consider now predictive covariates which are correlated between them, and independent from the unpredictive covariates. As above, let denote the number of predictive variables and be the level of correlations. Let , and be standard Gaussian random variables. The random variable is then defined by for and for . As in section 4.2, the regression coefficient is a constant vector of the form , where this time .

is distributed conditionnally on as and the loss function used is the Huber loss .

Results

Figure 3 shows a barplot generated in the same way as in section 4.2. Parameters used for Agghoo and CV were and , which is optimal in this case for both Agghoo and CV.

As in previous simulations, Agghoo’s performance relative to the oracle improves significantly when the intrinsic dimension grows from to , for a given value of . The decrease in relative risk is faster for small values of . As a result, Agghoo performs best, relative to the oracle, when for , whereas best performance seems to occur at for smaller values of , up to random errors.

For cross-validation, the relative risk seems more or less unaffected by the dimension , but shows an increasing trend as a function of for all values of .

As a result, Agghoo performs better than CV for and for and . For and , Agghoo even performs significantly better than the oracle! This is possible, since the Agghoo regression coefficient does not itself belong to the Lasso regularization path.

5 Conclusion

Aggregated hold-out (Agghoo) satisfies an oracle inequality (Theorem 3.2) in sparse linear regression with the Huber loss. This oracle inequality is asymptotically optimal in the non-parametric case where the intrinsic dimension tends to with the sample size , provided that an norm inequality holds on the set of sparse linear predictors. The condition holds for gaussian vectors and for classical approximation spaces in non-parametric regression. In the case of the trigonometric basis, this approach yields an oracle inequality in which the total dimension does not appear.

When Monte-Carlo subsampling is used (Definition 3.7), Agghoo has two parameters, and . Theoretically, it is shown that Agghoo’s performance always improves when grows for a fixed . Simulations show a large improvement from to in some cases, but diminishing returns for . With respect to , simulations show that or is optimal or near optimal in most cases. In particular, a default choice of , seems reasonable.

Compared to cross-validation with the same number of splits , simulations show that Agghoo performs better when the intrinsic dimension is large enough ( in section 4.1, in section 4.2 and in 4.3) for observations and covariates. Correlations between predictive and non-predictive covariates, which increase the number of covariates correlated with the response , clearly favour Agghoo relative to CV and the oracle, whereas the effect of correlations between predictive covariates is ambiguous.

Acknowledgements

While finishing the writing of this article, the author (Guillaume Maillard) has received funding from the European Union’s Horizon 2020 research and innovation program under grant agreement No 811017.

Appendix A Proof of Proposition 2.2

The proof follows the same lines as the proof of [31, Theorem 1], with some differences due to the non-quadratic risk.

Since is allowed to depend on , which is positive definite by assumption, we can always replace the by . Thus, it can be assumed without loss of generality that . Using the notation of Proposition 2.2

where are assumed to be independent from the sample . Since are independent, centered normal variables, is centered normal, with variance .

It follows that

Let also , so that .

Consider the prior on . Then a classical computation [31] shows that the posterior is gaussian and centered at the ridge estimator

where is the empirical covariance matrix. Fix a sample and let be independent from . Notice that

Set now . Since , knowing , is centered normal and independent from , which is also centered normal. It follows that , since is an odd function. This shows that is a Bayes estimator with respect to the prior and the loss function .

Thus, for any estimator ,

, so by convexity of , must be convex. Hence, by Jensen’s inequality,

Under , , so

Since , is almost surely non-degenerate. It follows that

Let . By Fatou’s lemma,

Since the are iid normal and independent from the , conditionnally on , is centered normal, with covariance matrix

It follows by lemma A.1 that

By convexity of the function on the positive definite matrices (lemma A.2),

Since is non-decreasing and convex,

By definition, , where , so

This proves the proposition.

Lemma A.1

Let be a gaussian vector, where is positive definite. Then

Proof Let . Then

Thus, the lemma is equivalent to

Let . Let , where is diagonal and is orthogonal. Let be the diagonal coefficients of (that is to say, the eigenvalues of ). Then

As is orthogonal, , so

The coefficients are positive (since is positive definite) and sum to (since by construction). It follows by Jensen’s inequality that

This proves the lemma.

Lemma A.2

The function is convex over the convex cone of positive definite matries.

Proof Let be a positive definite matrix. Let be a small, symmetric perturbation. Then

Therefore,

For any positive real , . It follows that

| (19) |

For any two matrices , let . It is easy to see that this defines a scalar product. Thus, by the Cauchy-Schwarz inequality,

Thus,

By equation (19), this proves that the Hessian of at is non-negative definite.

Appendix B Proof of Theorem 3.2

The idea of the proof is to apply [25, Theorem 17] using suitable functions .

In this proof, we shall adopt the following notational conventions. The notation will be reserved for probabilities and expectations which involve the sample (or ). For a (possibly random) function , will denote the expectation taken with respect to only (ignoring the potential randomness in the construction of ). The notation will be used for any other expectation. Moreover, for any measurable function , we denote

For a random function , let

with a similar definition for .

Fix a dataset , and for any , let . More precisely, to apply [25, Theorem 17], one must show inequalities of the form : for all ,

| (20) |

where are non-decreasing functions. Since is Lipschitz, it is enough to control and by functions of and .

B.1 A few lemmas

Lemma B.1

Let be a non-negative random variable such that

where . Let be an increasing, differentiable function. Then for all ,

Proof

Lemma B.2

Let be a random variable. Then for all ,

In particular, if for some , then .

Proof Let , , , then by Hölder’s inequality,

Now by definition, , , and

Assume now that . Then

It follows that

which yields the result.

Lemma B.3

Let be a random variable. Then for all ,

Lemma B.4

Let be a random variable such that , where . Then for all integers ,

Proof Since , the statement is true for . Consider now . Let be a real number to be determined later. Then

By definition of and a Chernoff bound, the variable satisfies for all , therefore by lemma B.1,

An easy induction argument shows that

It follows that

Let . Then for all ,

As a result, for all ,

We now prove that for all , . For all ,

therefore

It follows that for all , . In particular, , therefore

Lemma B.5

There exists a constant such that, for any sub-exponential random variable and any ,

B.2 Controlling the norm

First, let us bound the supremum norm by the norm.

Claim B.5.1

For any , recall that . Then:

Proof Let be independent from and observe that for any ,

where (using the notations of hypothesis 2.1). Note that . Hence, by the triangle inequality,

By hypothesis 2.1, . Thus, if , . The definition of (equation (7)) implies that

A uniform bound on the Orlicz norm is also required.

Definition B.6

Let

can be bounded as follows.

Claim B.6.1

Assume that hypotheses (Reg- ), (Uub) hold and that for some , . Then

Proof Let . Defining and changing variables in hypothesis 2.1 from to , we can rewrite as

where

Therefore, differentiating with respect to ,

Assume by contradiction that

| (21) |

Let be such that (21) holds. Then by monotony of , for all in ,

It follows that

| (22) |

By integration, this implies that for all ,

| (23) | ||||

| (24) |

If , then for small enough , (24) contradicts the minimality of . On the other hand, if , then averaging (21) over yields

Then for , (23) contradicts the minimality of . Thus, (21) leads to a contradiction. Let be such that . Then

Exchanging and yields

Let be independent from . For any ,

As is independent from , conditionnally on , by hypothesis 2,

Hence, by lemma B.5,

Thus, by the hypotheses of claim B.6.1,

The result follows since for all , .

B.3 Proving hypotheses

The following lemmas will be useful.

Lemma B.7

For any ,

Proof

Claim B.7.1

Let . Let ; is a risk minimizer. Under hypothesis (Lcs), almost surely, for any ,

As a result, for any ,

Proof Recall that

Then and . By differentiating under the expectation, almost surely, for any such that ,

This proves the first equation. Since is a global minimum, it follows that, for any ,

Because is convex, for any such that ,

Similarly, for ,

.

This proves the lemma.

We now relate the norm to the excess risk in the following Proposition.

Proposition B.8

Let be random variables. Let be the Huber loss with parameter . Assume that satisfies hypothesis (Lcs). Let be measurable functions. If for some , , then

where .

In particular, there exists a constant such that, whenever for some ,

| (25) |

where . One can take .

Proof Let satisfy the hypotheses of proposition B.8. Let where

Let

Notice that in the notation of claim B.7.1, and in particular, . Define the event . By claim B.7.1,

| (26) |

Let . By lemma B.2,

By definition, on , , therefore by lemma B.7.1,

It follows that

| (27) |

From equations (26) and (27), it follows that

Therefore, either or

In either case,

Finally, by lemma B.7,

| (28) |

where . This proves the first equation. Let now . By lemma B.3,

since decreases on , as shown in the proof of lemma B.5. Let Then for all ,

It follows from equation (28) that

where .

We are now ready to obtain functions such that holds. In the following, fix and write for short. Because the Huber loss is Lipschitz,

Therefore, for all ,

Let . By claim B.5.1, , hence by lemma B.4, since ,

Using the notation of Proposition B.8, let

| (29) |

By Proposition B.8,

which proves . Now by Definition B.6 and lemma B.3,

which proves .

B.4 Conclusion of the proof

We have proved that and hold, where is defined in Proposition B.8. It remains to apply [25, Theorem 17] and to express the remainder term as a simple function of and . We recall here the definition of the operator used in the statement of that theorem.

Definition B.9

For any function and any , let

The following lemma will facilitate the computation of .

Lemma B.10

Let and . Then if and only if and then .

Proof

To find , notice that given the definition of ,

the condition is obviously necessary for the infimum to be finite.

Assume now that . For any , then as well as (since we assumed ), therefore .

Thus by definition, (in particular, is finite).

Furthermore, by definition

of , ,

that is .

The following claim can now be proved.

Claim B.10.1

Assume that hypotheses (Reg- ) and (Lcs) hold. If and are such that

| (30) |

then applying Agghoo to the collection yields the following oracle inequality.

Proof Theorem [25, Theorem 17] applies with , and it remains to bound the remainder terms . Now assume that equation (30) holds.

Bound on

Bound on

Bound on

is non-increasing, therefore, is the unique nonnegative solution to the equation

It follows that

| (33) |

Since by assumption, and

By equation (33),

| (34) |

Bound on

is the unique nonnegative solution to the equation

which yields

Moreover,

Therefore, since by assumption ,

| (35) |

Conclusion

Summing up equations (31), (32), (34) and (35), [25, Theorem 17] implies that assuming equation (30) holds for , for all ,

| (36) |

By hypothesis (30) and since by hypothesis (Reg- ),

hence claim B.6.1 applies with . Thus,

It follows that

This proves Claim B.10.1.

Theorem 3.2 can now be derived from claim B.10.1. Let be such that for some numerical constant , to be determined later. Then , so by hypothesis (Ni),

Letting , we can rewrite the above equation as

Since for any , , and by definition,

Let now , so that equation (30) holds. By claim B.10.1,

Since , and , which proves Theorem 3.2.

Appendix C Applications of Theorem 3.2

C.1 Gaussian vectors

Proof For any , is a centered gaussian random variable. By homogeneity of norms, the quotient does not depend on the scale parameter ; it is therefore a numerical constant; moreover one can check that for , . Thus, we can choose so that

| (37) |

It remains to prove point 2 of hypothesis 2.1 for some constant . Let . Let be such that . By the inequality , for any ,

It follows by definition of that

| (38) |

On the other hand, letting ,

| (39) |

For all , let . Clearly, is a semi-norm. Let be the covariance matrix of . For all , let denote the vector space . Let

Let finally . Since by construction,

it follows from equations (38), (39) and the definition of that

| (40) |

By Hölder’s inequality, for any ,

If , then by lemma C.1 below,

| (41) |

for some numerical constant . For any , the vector has components . For any ,let and . By the Cauchy-Schwarz inequality, equation (40) and since ,

Let , , . Let

| (42) |

Then, by two applications of Hölder’s inequality,

By definition, ,

Therefore, if , then by lemma C.1 below, for some constant ,

| (43) |

Let us now bound , where we recall that is given by equation (42). Since for any , , is a standard normal vector of size , by the gaussian concentration inequality, there exists some constant such that

Since by assumption and and since ,

From equation (43), we can conclude that for some constant ,

Together with (41), this proves point 2. of hypothesis 2.1. with and .

By equation (37), hypothesis (Ni) holds with . Let , so that implies . Then, by Theorem 3.2 and since (by equation (10)), we obtain Corollary 3.3 with .

Lemma C.1

There exists a constant such that for any subset such that and for all ,

Moreover, if in addition , then for all ,

As a result, for any ,

Proof By restricting to a subspace, we can always assume that is a norm. Let be the unit sphere in norm . Let . By changing coordinates, it is easy to see that the metric entropy of in norm is the same as that of the euclidean sphere in the euclidean norm. Therefore, for any , there exists a finite set , of cardinality less than and such that for any , there exists such that . Therefore,

| (44) |

By definition,

As is a standard normal vector, . Hence, by the union bound and the Gaussian concentration inequality,

| (45) |

On the other hand, for any , is standard normal, therefore

| (46) |

By the union bound, it follows from equations (44), (45) and (46) that

Let now . Then

Moreover, there exists a constant such that

Because , . Using the inequality , it follows by the same argument that . Since ,

It follows that

Finally, since ,

which yields the first inequality for some constant . The second inequality then follows from the union bound:

By assumption, , which yields the second equation. As a result, for any

C.2 Fourier series

C.2.1 Proof of Corollary 3.6

Let and . Since , for any , by the Cauchy Schwarz inequality,

Therefore,

On the other hand, for all , , where the variable has density on , which by assumption is greater than . Therefore, by orthonormality of the trigonometric basis,

Thus, for any and ,

which proves that . Take in equation (15), so that, since and ,

C.2.2 Proof of proposition 3.5

Let and . By lemma B.7.1,

| (47) |

Let be the support of , and denote the component of the vector . By the Cauchy-Schwarz inequality and orthogonality of the trigonometric basis,

Since , it follows that

therefore by equation (15), on the event ,

On the event , , therefore by equation (47),

Let . Thus, on the event that ,

On the other hand, if , by definition, so

Let . By Hölder’s inequality,

Hence, by lemma C.2 with , there exists a constant such that

| (48) |

Moreover, by lemma C.3 below, for all ,

Thus, equation (13) follows from equation (48) and the additional assumption that .

Lemma C.2

Let be positive real numbers and let . Then

Proof The function is continuous, tends to at and , so reaches a global minimum on . As is differentiable,

Thus, for all ,

Lemma C.3

Let be an integer and be iid random variables such that, for some and , . Let

Then for all ,

Proof Remark first that for any ,

For any , let , and . Thus,

so that

Let be such that and let be such that . By monotony of , for all , and for all , . Since by definition of ,

it follows that .

Let . By the union bound and Markov’s inequality, for all ,

Symetrically,

so that one can take and with probability greater than . It follows that, for any ,

| (49) |

For any , , where

This yields the result under the condition that .

C.3 Proof of proposition 3.9

For any , denote by for simplicity. For any , let

Let also

By Jensen’s inequality,

| (50) |

Let now . By claim B.7.1, for any ,

Averaging over yields

Combining this bound with equation (50) yields

Taking expectations yields equation (17) by exchangeability of the . Assume now that . By claim B.7.1,

It follows that . Since the have the same distribution, also. Thus, by definition of the median,

References

- [1] Sylvain Arlot and Alain Celisse. A survey of cross-validation procedures for model selection. Statistics Surveys, 4:40–79, 2010.

- [2] Jean-Yves Audibert and Olivier Catoni. Robust linear least squares regression. Ann. Statist., 39(5):2766–2794, 10 2011.

- [3] Francis Bach. Bolasso: Model consistent lasso estimation through the bootstrap. Proceedings of the 25th international conference on Machine learning, 33-40, 05 2008.

- [4] Lucien Birgé and Pascal Massart. Minimum contrast estimators on sieves: exponential bounds and rates of convergence. Bernoulli, 4(3):329–375, 09 1998.

- [5] Sourav Chatterjee and Jafar Jafarov. Prediction error of cross-validated Lasso. arXiv e-prints, page arXiv:1502.06291, feb 2015.

- [6] X. Chen, Z. J. Wang, and M. J. McKeown. Asymptotic analysis of robust lassos in the presence of noise with large variance. IEEE Transactions on Information Theory, 56(10):5131–5149, Oct 2010.

- [7] Denis Chetverikov, Zhipeng Liao, and Victor Chernozhukov. On cross-validated Lasso in high dimensions. The Annals of Statistics, 49(3):1300 – 1317, 2021.

- [8] Geoffrey Chinot, Guillaume Lecué, and Matthieu Lerasle. Robust statistical learning with lipschitz and convex loss functions. Probability Theory and Related Fields, 176(3):897–940, Apr 2020.

- [9] Pascaline Descloux and Sylvain Sardy. Model selection with lasso-zero: adding straw to the haystack to better find needles. arXiv e-prints, page arXiv:1805.05133, May 2018.

- [10] R.A. DeVore and G.G. Lorentz. Constructive Approximation. Grundlehren der mathematischen Wissenschaften. Springer Berlin Heidelberg, 1993.

- [11] Bradley Efron, Trevor Hastie, Iain Johnstone, and Robert Tibshirani. Least angle regression. Ann. Statist., 32(2):407–499, 04 2004.

- [12] Jerome Friedman, Trevor Hastie, and Rob Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of statistical software, 33(1):1–22, 2010. 20808728[pmid].

- [13] Eitan Greenshtein and Ya’Acov Ritov. Persistence in high-dimensional linear predictor selection and the virtue of overparametrization. Bernoulli, 10(6):971–988, 12 2004.

- [14] László Györfi, Michael Kohler, Adam Krzyżak, and Harro Walk. A Distribution-Free Theory of Nonparametric Regression. Springer New York, 2002.

- [15] Haitham Hassanieh. The Sparse Fourier Transform: Theory and Practice. Association for Computing Machinery and Morgan & Claypool, 2018.

- [16] Trevor Hastie, Robert Tibshirani, and Jerome Friedman. The Elements of Statistical Learning. Springer New York, 2009.

- [17] Darren Homrighausen and Daniel McDonald. Risk consistency of cross-validation with lasso-type procedures. Statistica Sinica, 27, 08 2013.

- [18] Andres Hoyos-Idrobo, Yannick Schwartz, Gael Varoquaux, and Bertrand Thirion. Improving sparse recovery on structured images with bagged clustering. In 2015 International Workshop on Pattern Recognition in NeuroImaging. IEEE, jun 2015.

- [19] Peter J. Huber. Robust estimation of a location parameter. Ann. Math. Statist., 35(1):73–101, 03 1964.

- [20] Peter J. Huber and Elvezio M. Ronchetti. Robust Statistics. John Wiley & Sons, Inc., jan 2009.

- [21] Vladimir Koltchinskii, Alexandre Tsybakov, and Karim Lounici. Nuclear norm penalization and optimal rates for noisy low rank matrix completion. Annals of Statistics - ANN STATIST, 39, 11 2010.

- [22] Sophie Lambert-Lacroix and Laurent Zwald. Robust regression through the huber’s criterion and adaptive lasso penalty. Electron. J. Statist., 5:1015–1053, 2011.

- [23] Guillaume Lecué and Charles Mitchell. Oracle inequalities for cross-validation type procedures. Electron. J. Statist., 6:1803–1837, 2012.

- [24] Guillaume Maillard. Hold-out and Aggregated hold-out. PhD thesis, 2020. Thèse de doctorat dirigée par Arlot, Sylvain et Lerasle, Matthieu Mathématiques appliquées université Paris-Saclay 2020.

- [25] Guillaume Maillard, Sylvain Arlot, and Matthieu Lerasle. Aggregated hold-out. Journal of Machine Learning Research, 22(20):1–55, 2021.

- [26] Pascal Massart. Concentration Inequalities and Model Selection, volume 1896 of Lecture Notes in Mathematics. Springer, Berlin, 2007. Lectures from the 33rd Summer School on Probability Theory held in Saint-Flour, July 6–23, 2003, With a foreword by Jean Picard.

- [27] Nicolai Meinshausen and Peter Bühlmann. Stability selection. Journal of the Royal Statistical Society Series B, 72:417–473, 09 2010.

- [28] Shahar Mendelson. Learning without concentration. J. ACM, 62:21:1–21:25, 2014.

- [29] Shahar Mendelson. Learning without concentration for general loss functions. Probability Theory and Related Fields, 171(1):459–502, Jun 2018.

- [30] Léo Miolane and Andrea Montanari. The distribution of the Lasso: Uniform control over sparse balls and adaptive parameter tuning. arXiv e-prints, page arXiv:1811.01212, Nov 2018.

- [31] Jaouad Mourtada. Exact minimax risk for linear least squares, and the lower tail of sample covariance matrices. arXiv preprint arXiv:1912.10754, 2019.

- [32] Fabien Navarro and Adrien Saumard. Slope heuristics and V-Fold model selection in heteroscedastic regression using strongly localized bases. ESAIM: Probability and Statistics, 21, 2017.

- [33] Philippe Rigollet and Alexandre Tsybakov. Exponential screening and optimal rates of sparse estimation. Ann. Statist., 39(2):731–771, 04 2011.

- [34] Saharon Rosset and Ji Zhu. Piecewise linear regularized solution paths. The Annals of Statistics, 35(3):1012–1030, 2007.

- [35] Charles J. Stone. Optimal global rates of convergence for nonparametric regression. Ann. Statist., 10(4):1040–1053, 12 1982.

- [36] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B. Methodological, 58(1):267–288, 1996.

- [37] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), 58(1):267–288, 1996.

- [38] Ryan J. Tibshirani and Jonathan Taylor. Degrees of freedom in lasso problems. Ann. Statist., 40(2):1198–1232, 04 2012.

- [39] Sara van de Geer and Johannes Lederer. The Lasso, correlated design, and improved oracle inequalities. arXiv e-prints, page arXiv:1107.0189, jul 2011.

- [40] Mark J. van der Laan, Sandrine Dudoit, and Aad W. van der Vaart. The cross-validated adaptive epsilon-net estimator. Statist. Decisions, 24(3):373–395, 2006.

- [41] V. N. Vapnik. An overview of statistical learning theory. Transactions on Neural Networks, 10(5):988–999, sep 1999.

- [42] Gaël Varoquaux, Pradeep Reddy Raamana, Denis A. Engemann, Andrés Hoyos-Idrobo, Yannick Schwartz, and Bertrand Thirion. Assessing and tuning brain decoders: Cross-validation, caveats, and guidelines. NeuroImage, 145:166–179, jan 2017.

- [43] Hansheng Wang and Chenlei Leng. Unified lasso estimation by least squares approximation. Journal of the American Statistical Association, 102(479):1039–1048, 2007.

- [44] Hansheng Wang, Guodong Li, and Guohua Jiang. Robust regression shrinkage and consistent variable selection through the lad-lasso. Journal of Business and Economic Statistics, 25(3):347–355, 2007.

- [45] Sijian Wang, Bin Nan, Saharon Rosset, and Ji Zhu. Random lasso. Ann. Appl. Stat., 5(1):468–485, 03 2011.

- [46] Marten Wegkamp. Model selection in nonparametric regression. Ann. Statist., 31(1):252–273, 02 2003.

- [47] Huan Xu, Constantine Caramanis, and Shie Mannor. Sparse algorithms are not stable: A no-free-lunch theorem. IEEE transactions on pattern analysis and machine intelligence, 34, 08 2011.

- [48] Congrui Yi and Jian Huang. Semismooth newton coordinate descent algorithm for elastic-net penalized huber loss regression and quantile regression. Journal of Computational and Graphical Statistics, 26(3):547–557, 2017.

- [49] Hui Zou, Trevor Hastie, and Robert Tibshirani. On the ”degrees of freedom” of the lasso. Annals of Statistics, 35(5):2173–2192, 2007.