Gini Index based Initial Coin Offering Mechanism

Abstract

As a fundraising method, Initial Coin Offering (ICO) has raised billions of dollars for thousands of startups in the past two years. Existing ICO mechanisms place more emphasis on the short-term benefits of maximal fundraising while ignoring the problem of unbalanced token allocation, which negatively impacts subsequent fundraising and has bad effects on introducing new investors and resources. We propose a new ICO mechanism which uses the concept of Gini index for the very first time as a mechanism design constraint to control allocation inequality. Our mechanism maintains an elegant and straightforward structure. It allows the agents to modify their bids as a price discovery process, while limiting the bids of whales. We analyze the agents’ equilibrium behaviors under our mechanism. Under natural technical assumptions, we show that most agents have simple dominant strategies and the equilibrium revenue approaches the optimal revenue asymptotically in the number of agents. We verify our mechanism using real ICO dataset we collected, and confirm that our mechanism performs well in terms of both allocation fairness and revenue.

Keywords Mechanism Design; Initial Coin Offering; Gini Index

1 Introduction

As a primary fundraising tool for startups, Initial Coin Offering (ICO) is very eye-catching in the capital market. According to [4], ICOs ended in 2017 and raised around billions (USD) in total. By 2018, the ICO fundraising market has grown significantly. The total fundraising for the year reached billions (USD), and the number of ended ICOs increased to .

Despite the popularity and the huge amounts of funds being raised, popular ICO mechanisms are surprisingly unsophisticated. Vitalik Buterin [1] analyzed some token sale models and claimed that an optimal token sale model has not been discovered yet. There are two commonly used ICO mechanisms. One is simply the fixed price mechanism. There are two variants of this mechanism: uncapped sales and capped sales. Uncapped sales does not limit the number of coins sold. The aim is to accept as much capital and as many investors into the project as possible. Capped sales sells a fixed number of coins, and cuts off additional investment once all coins are sold. The fixed price mechanism does not offer a price discovery process. Many cryptocurrencies released via ICOs have different degrees of appreciation after their tokens are listed on exchanges. The average ICO is under priced by [5], while some tokens are appreciated by more than [8]. Another commonly used mechanism is the Dutch auction, which offers a much better price discovery process. It starts the auction with a high price, which keeps decreasing until enough participants are willing to purchase all coins according to the market price. The Dutch auction also has its drawbacks. E.g., it requires the participants actively monitor the auction progress.

For both the fixed price mechanism with capped sales and the Dutch auction, whales (large investors) can end the auction early by putting in large investments, which takes away the investment opportunities from the smaller investors. Wealth inequality is a significant problem in the cryptocurrency community, which goes against the principle of decentralization, especially if the coin is based on proof-of-stake (that favors richer holders). It is also worth mentioning that the tokens sold in an ICO normally amount to no more than of the tokens. The unsold tokens are still in the hands of the release team. The hidden danger of sharp depreciation (dumping large amounts of coins) caused by whales is a vital threat for the development team.

Roubini [7] testified in a hearing of the US Senate Committee on Banking, Housing and Community Affairs: “wealth in crypto-land is more concentrated than in North Korea where the inequality Gini coefficient is (it is in the quite unequal US): the Gini coefficient for Bitcoin is an astonishing .” Many cryptocurrency buyers expressed dissatisfaction to the wealth gap on Internet forums, calling “whale-sale completely against the ethos of Ethereum and Cryptocurrency” [11]. We collected the data from a few ICOs. Based on our calculation, the Gini index of token allocation in most of the ICOs is higher than . For example, for Gnosis (with a Gini index of ), the top of the users invested . In sharp contrast, the bottom of the users invested only in total! The top two investors invested and , respectively.

As a means of balance, in this paper, we introduce a Gini index based ICO mechanism to achieve a more balanced token allocation by limiting whales. Since Corrado Gini proposed the concept of Gini index for the first time in 1912, Gini index has been widely used to measure wealth gap. Gini index was also studied recently in mechanism design [10]. The authors used Gini index to evaluate allocation fairness in simulations. In our paper, the Gini index is a mechanism design constraint. Our analysis is based on the specific mathematical structure of the Gini index.

The Gini index may not be meaningful in environments where false name bids [12] are possible, as a whale may simply divide her investment and participate via multiple accounts. Existing ICOs in practise do often involve the Know Your Customer (KYC) process and only the users in the whitelist can join the ICO. KYC is a process in which a business verifies its customers’ identities, as well as the risk of illegal intent. KYC processes are also being used to comply with anti-bribery and other regulations (e.g., it is illegal to sell cryptocurrencies to customers from countries/territories where cryptocurrencies are banned). The US Securities and Exchange Commission (SEC) has announced the intent to pursue ICOs without a proper KYC processes. Besides document verification, existing KYC processes use manual approaches like video conversation to verify customers’ identities.

We propose the Gini mechanism, which has a list of desirable properties:

-

•

The Gini mechanism is a simple prior-free mechanism with elegant description. It is a key advantage for practical applications. Data related to ICO events are extremely volatile. It is unrealistic to assume a known prior distribution. Therefore, computational approaches (e.g., deep learning based mechanism design [3, 9] and classic automated mechanism design [2]) are not possible.

-

•

The Gini mechanism offers a price discovery process. We believe any mechanism that asks for a valuation is not realistic for ICOs. Before an ICO starts, the agents have difficulty in the valuation of the coin. The value of a cryptocurrency depends heavily on its popularity. The Gini mechanism only asks for the agents’ budgets (i.e., how much do you plan to invest). Based on the budgets, the mechanism calculates a price. The Gini mechanism has the property that it produces higher prices if there are higher budgets and more agents. That is, the more popular the coin is, the higher the price gets. During the running of the mechanism, the agents have the ability to adjust their budgets. For example, if the price is too high for an agent, then she could pull out (reduce her budget to ). If the price gets too low, then the agent would max out her investment (honestly report her maximum budget). We show that a pure strategy -equilibrium exists. Under this equilibrium, agent is playing a pure strategy (offering a single budget) and this is at most away from her best response in terms of utility. The depend on the actual data. In our experiments, the are always tiny compared to the agents’ maximum budgets.

-

•

For most of the agents, the strategies are straight-forward. They either max out their budgets or completely pull out of the investment. Only a handful of agents have room for calculated equilibrium behaviors — they face the situations where investing too much results in a price that is too high, while investing too little results in little utility gain. A carefully chosen budget can create a nice balance between the price increment and her marginal utility gain.

-

•

The mechanism produces nearly optimal revenue in experiments. In terms of theoretical guarantee, asymptotically (when the number of agents goes to infinity), under natural technical assumptions, the mechanism’s revenue converges to the optimal revenue.

As a last but not least contribution of this paper, we plan to release our collected dataset, which can be used to analyze user behaviors in ICOs and for agent-based simulations of ICOs. For convenience, in our datasets, all monetary amounts are provided in both Ether and USD, based on real-time exchange rate at the time of the transactions. Our dataset consists of six popular ICOs, collected according to the following selection rules:

- Rule 1:

-

More than 10 millions (USD) raised.

- Rule 2:

-

Using the Dutch auction as the ICO model.

- Rule 3:

-

The number of transactions is more than 500.

2 Model Description

The unit size of digital currencies tend to be tiny. For example, satoshi is the name for the smallest unit of bitcoin, which equals one hundred millionth of a bitcoin. In our model, we treat coins as infinitely divisible, which allows us to normalize the number of coins to . That is, we are selling one divisible item (one coin) to agents. For presentation purposes, we say that agent receives coin () if she receives fraction of the coin. Agent ’s type is denoted as , where is her valuation for the coin111If the whole coin reserve is released via the ICO mechanism, then an agent’s valuation is essentially her view of the market cap. and is her budget. For now, we defer any discussion on the difference between an agent’s private true budget limit and her reported budget limit. We will discuss the agents’ strategies in Section 4.

Since we are selling currencies, we believe all agents should face the same exchange rate. In an ICO mechanism, the agents would pay monetary payments (e.g., USD or other cryptocurrencies like Ether) in exchange of a fraction of the coin. Let and be two agents, each receiving and coin, and each paying and . We should have . This exchange ratio can also be interpreted as the price of the coin. Essentially, we require that our mechanism offers the same price to all agents. If we charge from an agent, then this agent should receive coin.

For agent , having a budget of does not necessarily mean that the mechanism will charge her exactly . Let be agent ’s actual spending under the mechanism. The budget constraint is . Agent receives coin and her utility equals

The agents aim to maximize their utilities. Again, we defer any discussion on strategies to Section 4.

A mechanism outputs the price and an allocation . for all and . An allocation is feasible only if it honours the budget constraint: for all .

We also introduce a new mechanism design constraint to limit the degree of inequality in our allocations. The popular Gini index is used to measure allocation inequality. We set a constant Gini cap on the Gini index. That is, a feasible allocation’s Gini index should never exceed . The Gini cap is a mechanism parameter chosen by the mechanism designer, with . A higher Gini cap implies that we have a higher tolerance on allocation inequality.

The standard way to compute the Gini index is as follows. Let be the allocation. We sort the in ascending order to obtain the . So is the smallest value among the and is the largest value among the . The Gini index equals

However, there is one issue with the above definition. The whole point of considering the Gini index is to ensure allocation equality. Generally speaking, we want to avoid situations where some agents receive too little while some other agents receive too much. If an agent has a huge budget, to prevent her from receiving too much, the mechanism can simply set an investment cap. That is, any investment beyond the cap is not accepted. On the other hand, if an agent has a tiny budget, to prevent her from receiving too little, we have to reduce the price to accommodate her tiny budget, which may significantly hurt the mechanism performance — after all, an ICO mechanism’s goal is to raise money.

Let us consider an extreme example with and . Let us assume that agents have budgets and the remaining agents have very high budgets. In this case, there are no feasible allocations. All allocations’ Gini indices exceed . To show this, we note that , so the Gini coefficient becomes

Actually, for any constant , we can find type profiles that make it impossible to allocate (to meet the Gini cap). We do not wish to simply fail the ICO in these scenarios. Instead, we allow the mechanism to ignore agents who receive nothing from the Gini index calculation. For the above example, if we ignore all agents who receive nothing, then feasible allocation is possible. We focus on the remaining agents, who all have positive budgets. We could simply allocate every agent an equal share (), by setting the price low enough so that every agent can afford coin. Equal sharing has a Gini index of . Therefore, ignoring agents saves us from infeasible situations. There are two arguments for the flexibility of ignoring agents who receive nothing:

-

•

We are not considering all billion people when calculating the Gini index anyway. People who have not joined the ICO are not fundamentally different from agents who receive nothing in the ICO.

-

•

We are able to achieve much higher revenue under this assumption. We can construct example situations where one tiny-budget agent becomes the revenue bottleneck. By not allocating anything to this agent and not including her in the Gini index calculation, we sometimes can increase the revenue by infinite many times.

Formally speaking, for our specific model, we calculate the Gini index as follows:

Definition 1 (Flexible Gini Index).

We allow the mechanism to pick the number of winners from a set . includes all the allowed winner numbers.

The non-winners all receive nothing, and they are not included in the Gini index calculation.

Let be the allocation for the winners. We still have that and . We sort the in ascending order to obtain the . So is the smallest value among the and is the largest value among the . The Gini index for winners is defined as:

| (1) |

Here are a few example setups for :

-

•

: No agents can be ignored. We fall back to the standard definition.

-

•

: The mechanism can ignore of the agents.

-

•

: The mechanism picks at least a half of the agents as winners.

is also the mechanism’s parameter. is the minimum number of winners. We should not allow the mechanism to pick too few winners. Having only one winner leads to a very nice Gini index — it is always , but it is also meaningless.

The set of feasible allocations is determined by the allowed winner numbers , the Gini cap , the price , and finally the agents’ budgets. If we increase the price , then every agent’s allocation upper limit is reduced. Therefore, the set of feasible allocations either stays the same or shrinks. The total revenue of a mechanism is exactly the price (because we have only one coin for sale). Therefore, to maximize revenue, a natural idea is to push up the price to the point so that any further price increment makes feasible allocation impossible. We propose the Gini mechanism based on exactly this idea.

Informal description of the Gini mechanism: The Gini mechanism does not ask for the agents’ valuations at all. The mechanism produces a price based on the agents’ budgets alone. We start with an infinitesimally small price and raise the price until any further price increment results in no feasible allocations. At the final price, the feasible allocation is unique subject to tie-breaking.

3 Formal Mechanism Description

We start with a procedure that will be used as a building block of the Gini mechanism. The procedure answers the following question: given the agents’ budgets (the ), given the price and the number of winners , what is the allocation that minimizes the Gini index?

In the context of the above question, we do not have a Gini cap. Instead, we search for an allocation that minimizes the Gini index. An allocation is feasible if it satisfies the following:

-

•

and .

-

•

. is agent ’s spending and is the budget limit. If , then we say this agent is maxed out.

-

•

At least elements of the are s.

Without loss of generality, we assume . Let be the feasible allocation that minimizes the Gini index. We first notice that it is without loss of generality to assume . The reason is that if we have and , then swapping and results in a feasible allocation with the same Gini index. This also means that we can set to to s as we have only winners.

We then consider only the winners (agent to ). If agent is not maxed out (), then agent must receive the same allocation amount (i.e., ). For if it is not, we could increase by a small (still affordable by ) and decrease by the same (ensuring that we still have ). We end up with a feasible allocation with a strictly smaller Gini index.

Furthermore, among the winners, let be the agent that is not maxed out with the smallest index . Agent must have the same allocation amount as . This implies that is also not maxed out, which implies that agent should also have the same allocation. That is, the only allocation structure we need to consider is

In this allocation, we refer to as the allocation cap. is the number of capped agents.

By definition of , we have , so the above structure can be rewritten into

| (2) |

The total allocation must be , hence must satisfy the following equation:

| (3) |

The only constraint on is that it serves as a cap, so . The left side of Equation (3) is strictly increasing in . The only way Equation (3) does not have a solution is when has already reached but the left side is still less than .

| (4) |

If this happens, then we do not have any feasible allocations. For convenience, we define the minimum Gini index to be for this case. When Equation (3) has solutions, the solution is unique. By solving for , we can find the allocation that minimizes the Gini index, based on Expression (2). The optimal (Gini-index-minimizing) allocation is unique subject to a consistent tie-breaking rule. The allocation essentially does not allocate to the lowest agents (in terms of budgets). This is the only place where we need tie-breaking. We may simply break ties by favoring agent over agent if . The optimal allocation then sets an allocation cap . All agents below max out their budgets and all agents at least can only get .

Let us then consider the relationship between and the minimum Gini index, while fixing the agents’ budgets and the winner number . We define to be the minimum Gini index for price .

Proposition 1.

When , .

Proof.

When , we set and Equation (3) is satisfied and every winner receives the same allocation , which corresponds to a Gini index of . ∎

The Gini mechanism starts with an infinitesimally small price. Proposition 1 basically says that initially feasible allocations must exist if at least agents have positive budgets, regardless of the Gini cap.222Even if less than agents have positive budgets, we may still be able to find an infinitesimally small price that makes feasible allocation possible. If no feasible allocation exists even with infinitesimally small price, then our mechanism fails. In this case, the mechanism designer should consider raising the Gini cap. The Gini mechanism then increases the price until any further increment results in no feasible allocations. The next proposition guarantees that when the price is large enough, no feasible allocations exist.

Proposition 2.

When , .

Proof.

This is based on Inequality (4). ∎

Proposition 1 and 2 together are not enough. How can we determine when we have reached an optimal price so that any further increment results in no feasible allocations? Also, we need to prove that exists. For example, it could be that the price can increase in without causing infeasibility, but when the price reaches exactly , all of a sudden no feasible allocations exist. In this case, technically speaking does not exist. It cannot be . Of course, in practice, is fine. We will show that always exists. Situations like the above do not occur.

Proposition 3.

As we increase in , is continuously nondecreasing in .

Proof.

As we increase , every agent’s allocation upper limit () is decreased. So the set of allowed allocations either stays the same or shrinks. Therefore, the minimum Gini index is nondecreasing with the price.

Combining all propositions, we have the following theorem:

Theorem 1.

Fixing the agents’ budgets and the number of winners , we define the maximum price to be the maximum price where the minimum Gini index is at most the Gini cap . At price , there are feasible allocations. Any increment in results in no feasible allocations.

exists and the corresponding feasible allocation is unique subject to tie-breaking.

Proof.

Based on Proposition 2, if the minimum Gini index at is at most , then this is the maximum price. Any higher price results in a Gini index of . At this price, the only feasible allocation is that the lowest agents in terms of budgets do not receive anything and the highest agents all max out.

We then consider situations where the minimum Gini index at is strictly higher than . When , the minimum Gini index is , so . Let . Given that is continuously nondecreasing based on Proposition 3, contains either one point, or is a closed interval. In both cases, exists. At price , the only feasible allocations are the Gini-index-minimizing allocations, which are unique subject to tie-breaking. If an allocation is not Gini minimizing and is feasible, then the minimum Gini index must be strictly below , which means that the price can still be pushed up due to the continuity between the price and the minimum Gini index. ∎

The maximum price can be calculated via a simple binary search inside the interval . Next, we formally define the Gini mechanism.

Definition 2 (Gini mechanism).

and are mechanism parameters. Given the agents’ budgets, for every allowed winner number in , we find the maximum price where the minimum Gini index is at most the Gini cap . We then choose the price to be the overall maximum . If there are multiple values with the same overall maximum price, then we break ties by favoring more winning agents. We pick the unique feasible allocation corresponding to the price.

4 Equilibrium under the Gini Mechanism

In this section, we start the discussion on the agents’ strategies. The way we would implement the Gini mechanism in practise is as follows: We announce a time frame for the ICO. During the time frame, the agents can join/leave anytime, and can change their investment amounts (budgets) anytime. (Technically, joining and leaving are special cases of changing budgets.) The Gini mechanism maintains the current price and allocation throughout the time frame. We assume that the time frame is long enough so that at some point, after all interested agents have joined, an equilibrium on the budgets are to be reached.333In practise, most ICOs are conducted over the Ethereum network. Here, an equilibrium will always be reached due to the transaction fees. In this paper’s model, we do not consider transaction fees. The equilibrium price/allocation eventually become the final price/allocation.

Our discussion involves three closely related concepts:

-

•

We use to denote agent ’s true maximum budget. This is ’s private information.

-

•

We use to denote agent ’s reported budget. Agent can report arbitrary nonnegative budget, including reporting a value above .

-

•

We use to denote agent ’s spending. The spending is always at most the reported budget. That is, .

We use to denote the current budget profile. We can also call this the agents’ current strategies. We still assume that . For every winner number , we use to denote the maximum price for winners and budget profile . The Gini mechanism’s price for budget profile is the maximum over the for .

Now we introduce a few propositions, which will be used for analyzing agents’ strategies.

Proposition 4.

For any , is nondecreasing in every coordinate (every ). This also means that is nondecreasing in every coordinate, because the maximum of monotone functions are still monotone.

Proof.

When we increase agent ’s budget , feasible allocations remain feasible allocations. If previously we can push the price to a certain point, then we still can (and may be able to push the price up even more). ∎

Proposition 5.

For any , is continuous in every coordinate (every ). This also means that is continuous in every coordinate, because the maximum of continuous functions are still continuous.

Proof.

We focus on a specific . If we change to for every , then the maximum price also changes by times (to offset the change in budgets). Let be the maximum price. For an arbitrary , to change the price from to , we can increase every to . This also means that for a specific , if the increment in is at most , and we do not change the other coordinates (this means less increment in price because the price is monotone in every coordinate), then the price increment is at most . The same argument works for decrement. ∎

Proposition 6.

Agent faces a minimum investment amount and a maximum investment cap . Both are determined by the other agents’ budgets (i.e., ). Agent ’s spending is when her budget is below and her spending stays at when her budget grows beyond the cap. In between the minimum and the maximum investment amounts, the price strictly increases in ’s reported budget.

Proof.

We raise ’s budget from . At some point when her budget reaches , for the first time she becomes a winner under the Gini mechanism. Due to tie-breaking, it could be that ’s budget must be strictly above for her to become a winner. We ignore this technicality. Once becomes a winner. That means at the current price, is a winner in at least one feasible allocation. Let the set of feasible allocations where is a winner be . If is not capped in at least one allocation in , then by increasing ’s budget, the cap of this allocation decreases at the current price, which leads to strictly smaller Gini index. This then means the overall price should strictly increase as a result. If is capped in all feasible allocations in , then any increment in ’s budget has no effect anywhere, this means that has already reached her maximum investment cap. ∎

Proposition 7.

For any and , is nondecreasing in . This also means that is nondecreasing in , because the minimum of monotone functions are still monotone.

Proof.

If is small and is not a winner, then increasing has no effect on the price. If is large and is capped, then again, the increment in has no effect on the price. When price stays the same, is nondecreasing in . When is a winner and not capped, when increasing , the price gets strictly higher. If ’s allocation decreases, then all uncapped agents’ allocations decrease. If any agent is capped, then the cap increases. This results in strictly higher Gini index, which makes the allocation infeasible. If no agents is capped, then , which is also nondecreasing in . ∎

Proposition 8.

Assuming , for any ,

This also means that the partial derivative of against is bounded above by .

We focus on budget profiles without ties for convenience. In an actual equilibrium, if the budget profile contains ties, then we can simply perturb the budgets infinitesimally to remove ties. We have shown that the price function is continuous, so perturbing the budgets will only change the agents’ utilities infinitesimally.

Proof.

We focus on a specific winner number and a specific budget profile with .

Let . Let us analyze the derivative with respect to when . If is already capped under this budget profile, then the derivative is . So we only need to consider the situation where is not capped. We reduce to and change the price from to . We consider a new allocation where every other agent’s spending stays the same, but ’s spending is reduced by . This is still a feasible allocation but may not meet the Gini cap. We consider the Gini index of the new allocation. Let us consider the definition of the Gini index in (1). For the new allocation, the only change is a reduction in proportion of in both the numerator and the denominator. The numerator is multiplied by (the indices are from to for the winners in (1)). The denominator is multiplied by . Since , we have and

We want the first term of (1) to be at most to meet the Gini cap. So lowering ’s proportion only helps this goal. This means that the new allocation also meets the Gini cap. So the overall price should be at least . In conclusion, the derivative is at most when .

We then consider . If , then is not a winner and the derivative is . We only present the proof for . This is the winner with the lowest budget. This budget has the highest impact on the price. is not capped, for otherwise the Gini index equals . Therefore, we can adjust both up and down. ’s spending is the same as her budget.

We first consider the case where is not capped. We define a few terms (the are the actual spendings of the agents):

-

•

-

•

-

•

-

•

The first term of (1) is then . When the Gini cap is met, . (If the Gini cap is not met, then all agents spend all their budgets, in which case any change in budget corresponds to a derivative of at most .) We use to denote .

We change to . We consider a new allocation with the following spendings. Agent ’s spending is increased from to . Other agents from to keep their current spendings. The agents from to reduce their spendings by a factor of .

The first term of the Gini index of this new allocation is then . We set so that this term equals .

This implies that the new allocation is still feasible given the above . Since we assume agent is not capped, there is room for pushing down the spendings of agent to by multiplying the original spendings by . The price corresponding to the new allocation is the denominator of the first term of the Gini index, which is (under the Gini mechanism, the price is always equal to the total spending). The derivative of against equals

We simply the derivative:

To maximize the derivative, we minimize instead. is minimized when all are the same for . The ratio is minimized to

So is minimized to . The derivative is maximized to

The above increases with , but is at most , so the above is maximized to

The above expression increases with . When goes to infinity, we have the final upper bound .

When is capped, we consider changing to instead. All analysis is almost identical. After the change, , but if and future agents are capped, there is room for increasing the spendings. ∎

Given the above propositions, we demonstrate that for most agents, the strategies are fairly simple. We start with a sufficient condition for an agent to report budget.

Proposition 9.

If , then an agent’s best strategy is to report a budget of .

In experiments, generally we have that is very close to the . Our observation is that an agent’s impact on the overall price is very limited. This proposition essentially says that if an agent’s value is below (about) the current price, then she wants to leave (by setting the budget to ).

Proof.

The price is nondecreasing in the agents’ budgets. is the lowest price faces by unilateral budget change. If this price is still at least her valuation, then she does not want to invest. ∎

Now we provide a sufficient condition for an agent to report her true maximum budget. It is not as simple as, for example, if , then an agent would report her actual maximum. For reporting the maximum budget, an agent’s valuation must be slightly higher than the . This is to ensure that the utility gain for buying more is always greater than the utility loss caused by price increment for the existing purchase.

Proposition 10.

If , then agent ’s best strategy is to report her true maximum budget.

Here, , which represents the highest “effective” budget for agent . Any higher budget is essentially the same or violates the budget constraint. is ’s allocation when her budget is .

In experiments, generally we have that is very close to . is generally very small for most agents. For example, if there are agents in total, then we know for sure that at most agents can get allocations at least . That means for the remaining agents, we have . Let us consider , so . For an agent among these agents, if her valuation is at least (about) the current price, divided by , then she wants to report her true maximum budget.

Proof.

Due to Proposition 6, agent faces a minimum and a maximum investment amount. If her true maximum budget is below the minimum amount, then this agent is irrelevant. We only consider agents who can meet the minimum investment amounts. We use to denote ’s utility. Let us analyze the derivative of against when is identical to the spending . That is, we consider in between the minimum investment amount and .

| (5) |

| (6) |

We compare the Gini mechanism’s revenue against the first-best optimal revenue. The first-best optimal revenue is calculated as an optimization problem, assuming that we know all the agents’ private valuations and private budgets. Given a price , we filter out all agents who can afford , and then derive the Gini-index-minimizing allocation based on the true maximum budgets. If the Gini index is at most the Gini cap, then is an achievable price. We solve for the highest .

Theorem 2.

Under the following assumptions, the Gini mechanism’s equilibrium revenue approaches the first-best optimal revenue with probability , as the number of agents goes to infinity.

-

•

The agents’ private valuations are drawn i.i.d. from a distribution with a value upper bound . For any , . This basically assumes that the upper bound is a meaningful upper bound, in the sense that there is a positive probability to draw a value close to the upper bound.

-

•

The agents’ private budgets are drawn i.i.d. from a distribution with a positive expectation.

-

•

There is a constant minimum winner number. Above that, all winner numbers are allowed.

Proof.

We find a constant integer so that and is at least the minimum winner number. can always be found. There is a positive probability to draw an agent with valuation above and budget above . As the number of agents goes to infinity, the probability of drawing such agents equals , where is another constant integer. Among these agents, for at least of them, the allocation is at most . (For example, there are at most agents who allocation is at least .) If the equilibrium price is less than , then according to Expression (5), these agents would max out their budgets under the equilibrium. Each of these agents has a budget that is at least . So at the equilibrium price, only allocating to these agents alone results in an allocation with a Gini index of , which means that any equilibrium price strictly lower than is not possible. (If it is lower, then it should be raised due to the existence of an allocation with Gini index.) Given that and are arbitrary constants, we have that the equilibrium price can be made arbitrarily close to . is obviously an upper bound on the first-best optimal revenue. ∎

5 Experiments

In this section, we evaluate the Gini mechanism using real ICO data. The selection criteria for our dataset are mentioned in Section 1. Our dataset is compiled based on previous Dutch auction based ICOs. Each ICO dataset contains the agents’ budgets and their entering prices to the Dutch auction. In an ICO Dutch auction, even if an agent enters early, she still pays according to the ending price. So for agents with small budgets (who cannot buy all the coins and stop the auction), entering the auction when the price meets the valuation is a reasonable strategy. For this reason, we use the entering prices as the agents’ valuations. In our experiments, we also included a list of generated bids. The reason for this is that there are many observing agents whose data are missing from our datasets. An observing agent is someone who has low valuation. The auction ended before such an agent logs her bid. If the dataset contains agents, then we add in another generated agents. The generated agents’ budgets are sampled from real budgets, and the valuations are just the ending price times a random value from to (drawn according to the uniform distribution).

We numerically compute an approximate Nash equilibrium. We first calculate the first-best optimal price and use it to initialize the budget profile. An agent reports the true maximum budget if her valuation is at least the first-best optimal price, and reports otherwise. From this point on, we go through the agents one-by-one and have each agent update the budget to her best response. We stop when an equilibrium has been reached.

Our experiments involve thousands of agents, which seems very daunting when it comes to equilibrium computation. Fortunately, with the help of Proposition 9 and Proposition 10, we test these two sufficient conditions and find that most agents either report the maximum budget or .

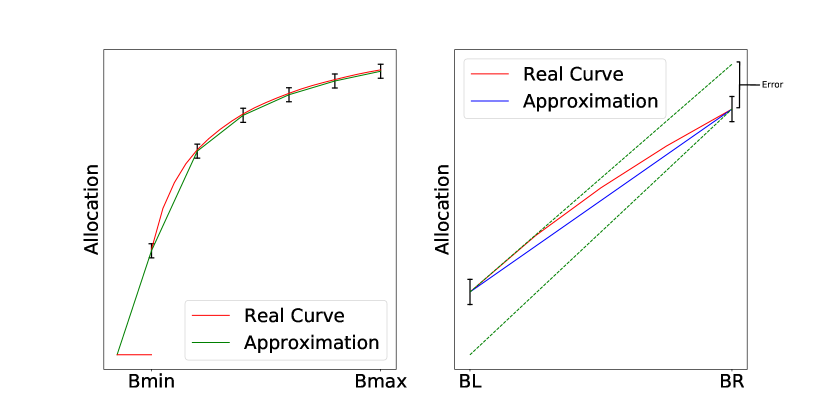

For a handful of agents who do prefer to report a budget that is somewhat in between s and their maximum budgets, we use numerical simulation to calculate their best responses. We focus on a specific agent . Figure 1 (Left) shows ’s real allocation curve. When ’s budget is below a minimum investment amount (denoted as in the figure), her allocation is . When ’s budget grows above a maximum amount (denoted as in the figure), her allocation stays the same. In between, her allocation curve is approximately concave: by investing more, pushes up the price, so the marginal gain gets smaller and smaller. The real allocation curve is unknown to us, so we resort to its approximation in our equilibrium calculation. We use piecewise straight lines to approximate the real allocation curve, by sampling a few allocation values and then connect them together. We call the sampled points the turning points in our piecewise linear curve. To ensure that we end up with a concave curve, we use a linear program to move the turning points slightly up or down. For example, let the be the y-coordinates of the turning points (). The linear program is constructed as follows (the are constants and the variables are the ):

| min | (7) | |||||

| s.t. | ||||||

It should be noted that in our approximation, we used a non-horizontal straight line in between and . This is fine because both before or after the approximation, the agents’ best strategies do not involve any budget strictly in between and .

With a concave allocation curve, the agent’s utility function is also concave. For example, when the budget is in between and , the utility curve is just the allocation curve times a constant (the agent’s valuation), then subtracts a linear term (the payment). According to [6], for a -person game with concave utility function, a pure strategy Nash equilibrium always exist. Our experiments show that after the approximation, a pure strategy Nash equilibrium (a deterministic budget profile) is very easy to find.

Our approximation introduces two sources of errors. First, we have the error from the linear program. Then, as shown in Figure 1 (Right), there is error due to using a straight line to approximate the real curve. Let and be the x-coordinates of two adjacent turning points. The price at is lower than the price at . For any budget value in between and , the allocation is in between and . The gap is at most , which is maximized when approaches the larger budget . We go through every adjacent pair of turning points to get the largest error. Given these two sources of errors, our computed Nash equilibrium is not an exact equilibrium. Suppose when we calculate the best response for agent , the maximum error in terms of ’s utility is , then we can only say this agent’s response is at most away from the best response (we could be underestimating the actual best response and overestimating the approximate best response).

The experiments are conducted using parameter and . Table 1 shows the decomposition of agents for different ICOs. The data format is “total number of agents = agents who report 0 based on Proposition 9 + agents who report the true maximum budget based on Proposition 10 + agents with nontrivial strategies.” As shown in the table, the number of agents with nontrivial strategies are only a handful. Table LABEL:tb:experiment1 compares the equilibrium revenue under the Gini mechanism (Gini Rev.) against the first-best optimal revenue (Opt. Rev.).444Gini Rev. is higher than Opt. Rev. for Metronome due to numerical error. The unit is Ether. For Polkadot, due to numerical error, one agent keeps changing her budget back and forth while the other agents do not change their budgets. The Gini revenue is only changed at the second digit after the decimal point due to this agent’s back and forth. Err. represents the maximum utility error. That is, under our equilibrium, an agent’s utility is at most this value away from the best response utility. The unit of error is Ether, so it can be quite significant in its absolute value. For Gnosis, Ether is worth about USD in November 2019. Err./Budget is the maximum ratio between the utility error and an agent’s true maximum budget. For Gnosis, this value is . Errors for the other ICOs are significantly better.

| Raiden | 8574=1663+6907+4 |

| Metronome | 2884=384+2496+4 |

| Polkadot | 5910=1522+4377+11 |

| GoNetwork | 5210=1351+3854+5 |

| Gnosis | 1518=304+1209+5 |

| Gini Rev. | Opt. Rev. | Err. | Err./Budget | |

|---|---|---|---|---|

| Raiden | 42177 | 42177 | 1.84e-3 | 2.63e-4 |

| Metronome | 8516 | 8515 | 6.85e-3 | 4.38e-4 |

| Polkadot | 104689 | 104735 | 9.75e-3 | 2.14e-4 |

| GoNetwork | 14352 | 14356 | 2.86e-3 | 2.60e-4 |

| Gnosis | 104117 | 104117 | 1.41e-1 | 1.45e-3 |

References

- [1] Vitalik Buterin. Analyzing token sale models. June 2017.

- [2] Vincent Conitzer and Tuomas Sandholm. Complexity of mechanism design. In Adnan Darwiche and Nir Friedman, editors, UAI ’02, Proceedings of the 18th Conference in Uncertainty in Artificial Intelligence, University of Alberta, Edmonton, Alberta, Canada, August 1-4, 2002, pages 103–110. Morgan Kaufmann, 2002.

- [3] Paul Duetting, Zhe Feng, Harikrishna Narasimhan, David Parkes, and Sai Srivatsa Ravindranath. Optimal auctions through deep learning. In Kamalika Chaudhuri and Ruslan Salakhutdinov, editors, Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 1706–1715, Long Beach, California, USA, 09–15 Jun 2019. PMLR.

- [4] Icobench. Ico market analysis 2018. 2018.

- [5] Paul P. Momtaz. Initial coin offerings. Available at SSRN: https://ssrn.com/abstract=3166709 or http://dx.doi.org/10.2139/ssrn.3166709, July 2018.

- [6] J. B. Rosen. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica, 33(3):520–534, 1965.

- [7] Nouriel Roubini. Testimony for the hearing of the us senate committee on banking, housing and community affairs on “exploring the cryptocurrency and blockchain ecosystem”. November 2018.

- [8] David Cerezo Sanchez. An optimal ICO mechanism. SSRN Electronic Journal, September 2017. Available at SSRN: https://ssrn.com/abstract=3040343 or http://dx.doi.org/10.2139/ssrn.3040343.

- [9] Weiran Shen, Pingzhong Tang, and Song Zuo. Automated mechanism design via neural networks. In Proceedings of the 18th International Conference on Autonomous Agents and MultiAgent Systems, AAMAS ’19, pages 215–223, Richland, SC, 2019. International Foundation for Autonomous Agents and Multiagent Systems.

- [10] Abhinav Sinha and Achilleas Anastasopoulos. Mechanism design for fair allocation. In 2015 53rd Annual Allerton Conference on Communication, Control, and Computing (Allerton), Monticello, IL, USA, sep 2015. IEEE.

- [11] Wit22. Bat ico whale-sale - completely against the ethos of ethereum and cryptocurrency. 2019.

- [12] Makoto Yokoo, Yuko Sakurai, and Shigeo Matsubara. The effect of false-name bids in combinatorial auctions: new fraud in internet auctions. Games and Economic Behavior, 46(1):174 – 188, 2004.