Golrezaei et al.

Dynamic Incentive-Aware Learning: Robust Pricing in Contextual Auctions

Dynamic Incentive-aware Learning: Robust Pricing in Contextual Auctions

Negin Golrezaei \AFFSloan School of Management, Massachusetts Institute of Technology, Cambridge, MA, \EMAILgolrezae@mit.edu \AUTHORAdel Javanmard \AFFData Sciences and Operations Department, University of Southern California, Los Angeles, CA, \EMAILajavanma@usc.edu \AUTHORVahab Mirrokni111The names of the authors are in alphabetical order. Moreover, part of this work is done when Negin Golrezaei was a postdoctoral researcher at Google Research, New York. \AFFGoogle Research, New York, NY, \EMAILmirrokni@google.com

Motivated by pricing in ad exchange markets, we consider the problem of robust learning of reserve prices against strategic buyers in repeated contextual second-price auctions. Buyers’ valuations for an item depend on the context that describes the item. However, the seller is not aware of the relationship between the context and buyers’ valuations, i.e., buyers’ preferences. The seller’s goal is to design a learning policy to set reserve prices via observing the past sales data, and her objective is to minimize her regret for revenue, where the regret is computed against a clairvoyant policy that knows buyers’ heterogeneous preferences. Given the seller’s goal, utility-maximizing buyers have the incentive to bid untruthfully in order to manipulate the seller’s learning policy. We propose learning policies that are robust to such strategic behavior. These policies use the outcomes of the auctions, rather than the submitted bids, to estimate the preferences while controlling the long-term effect of the outcome of each auction on the future reserve prices. When the market noise distribution is known to the seller, we propose a policy called Contextual Robust Pricing (CORP) that achieves a T-period regret of , where is the dimension of the contextual information. When the market noise distribution is unknown to the seller, we propose two policies whose regrets are sublinear in . \KEYWORDSpricing, robust learning, strategic buyers repeated second-price auctions, online advertising

1 Introduction

In many online marketplaces, both sides of the market have access to rich dynamic contextual information about the products that are being sold over time. On the buying side, such information can influence the willingness-to-pay of the buyers for the products, potentially in a heterogeneous way. On the selling side, the information can help the seller differentiate the products and set contextual and possibly personalized prices. To do so, the seller needs to learn the impact of this information on buyers’ willingness-to-pay. Such contextual learning can be challenging for the seller when there are repeated interactions between the buying and the selling sides. With repeated interactions, the utility-maximizing buyers may have the incentive to act strategically and trick the learning policy of the seller into lowering their prices. Motivated by this, our key research question is as follows: How can the seller dynamically optimize (personalized) prices in a robust manner, taking into account the strategic behavior of the buyers?

One of the online marketplaces that faces this problem is the online advertising market. In this market, a prevalent approach to sell ads is via running real-time second-price auctions in which advertisers can use an abundance of detailed contextual information before deciding what to bid. In this practice, advertisers can target Internet users based on their (heterogeneous) preferences and targeting criteria. Targeting can create a thin and uncompetitive market in which few advertisers show interest in each auction. In such a thin market, it is crucial for the ad exchanges to effectively optimize the reserve prices in order to boost their revenue. However, learning the optimal reserve prices is rather difficult due to frequent interactions between advertisers and ad exchanges.

Inspired by this environment, we study a model in which a seller runs repeated (lazy) second-price auctions with reserve over time. In the lazy auction, an item is being sold to the buyer with the highest submitted bid as long his bid exceeds his reserve.222Another version of the second price auction is called “eager”. In this version, the buyers whose bids are less than their reserve price are first removed from the auction. Then, the item is allocated to one of the remaining buyers who has the highest submitted bid. The valuation (willingness-to-pay) of each buyer for the item in period , which is his private information, depends on an observable -dimensional contextual information in that period and his preference vector. We focus on an important special case of this contextual-based valuation model in which the buyer’s value is a linear function of his preference vector and contextual information, plus some random noise term, where the noise models the impact of contexts that are not measured/observed by the seller.333Appendix 8 discusses how our results can be extended to some of the nonlinear valuation models. The preference vector, which is unknown to the seller and fixed throughout the time horizon, varies across buyers. Thus, the preference vectors capture heterogeneity in buyers’ valuation.444In Appendix 8, we discuss pricing under the settings where the preference vectors change over time and as a result, the obtained data is perishable.

The seller’s goal is to design a policy that dynamically learns/optimizes personalized reserve prices. The buyers are fully aware of the learning policy used by the seller and act strategically in order to maximize their (time-discounted) cumulative utility. Dealing with such a strategic population of buyers, the seller aims at extracting as much revenue as the clairvoyant policy that is cognizant of the preference vectors a priori. These vectors determine the relationship between the valuation of the buyers and contextual information. Put differently, the seller would like to minimize her regret where the regret is defined as the difference between the seller’s revenue and that under the clairvoyant policy. Note that the clairvoyant policy provides a strong benchmark because the policy posts the optimal personalized reserve prices based on the observed contexts.

As stated earlier, the main hurdles in designing a low-regret learning policy in this setting are the frequent interactions between the seller and the buyers. Due to such interactions, the strategic buyers might have the incentive to bid untruthfully. This way, they may sacrifice their short-term utility in order to deceive the seller, to post them lower future reserve prices. Thus, while a single shot second-price auction is a truthful mechanism, repeated second-price auctions in which the seller aims at dynamically learning optimal reserve prices of strategic and utility-maximizing buyers may not be truthful. The untruthful bidding behavior of the buyers makes it hard for the seller to learn the optimal reserve prices, and this, in turn, can lead to her revenue loss. This highlights the necessity to design a robust learning policy that reduces buyers’ incentive to follow untruthful strategy. Beside this hurdle, the availability of the dynamic contextual information requires the seller to change the reserve prices dynamically over time, based on the contextual information. To do so, the seller needs to learn how buyers react to such information and based on the reactions, posts (dynamic) personalized reserve prices. The need to have a personalized reserve price is caused by heterogeneity in buyers’ preferences.

We consider setting where the seller (firm) is more patient than the buyer. We formalize it by considering time-discounted utility for the buyers. This is motivated by various applications. For example, in online advertisement markets, the advertisers (buyers) who retarget Internet users prefer showing their ads to the users who visited their website sooner rather than later.

In this paper, we propose three learning policies. The first policy, which we call Contextual Robust Pricing (CORP), is tailored to a setting where the distribution of the noise term in buyers’ valuation is known to the seller. We will refer to this noise as market or valuation noise. By studying this setting, we can characterize the seller’s revenue loss due to her lack of knowledge about the buyers’ (heterogeneous) response to contextual information. The second policy, that we call CORP-II, is a variant of the first policy. This policy lends itself to a setting where the unknown market noise distribution is fixed throughout the time horizon and belongs to a location–scale family.555A location–scale family is a family of probability distributions parametrized by a location parameter and a non-negative scale parameter. Then, if a probability distribution function of a random variable belongs to this family, the probability distribution function of random variable also belongs to this family. The location-scale families are quite broad and contain Normal, Elliptical, Cauchy, Uniform, Logistic, Laplace, and Extreme value distributions, as examples. The third policy, which is called Stable CORP (SCORP), is designed to the setting where the market noise distribution varies over time and as a result, the seller does not have the intention of learning the market noise distribution. She instead would like to design a learning policy that is robust to the uncertainty in the noise distribution.

In the remaining part of the introduction, we briefly discuss the salient characteristics of each policy separately and defer the formal description to Sections 4 and 5.

-

•

CORP Policy: When the market noise distribution is known to the seller, under a log-concavity assumption on the noise distribution, our CORP policy gets the cumulative T-period regret of order , where the regret is computed against the clairvoyant policy that knows the preference vectors as well as the market noise distribution. Here, is the number of buyers, is the buyers’ discount factor, and is the extra regret due to the strategic behavior of the buyers. The policy works in an episodic manner where the length of episodes doubles each time. Some of the periods in each episode are randomly assigned to exploration, and the rest of the periods are dedicated to exploitation. At the beginning of each episode, CORP updates its estimates of the preference vectors by running a maximum Likelihood estimator using only the auction outcomes from the previous episode and then adheres to those estimates throughout the episode. During the exploitation periods, CORP sets the reserves based on its estimates of the preference vectors and its knowledge of the noise distribution. As time progresses, the policy becomes more confident about its estimates and consequently uses those estimate over a longer episode.

We now highlight two important aspects of CORP. As explained earlier, the CORP policy has an episodic structure and updates its estimate of preference vectors only at the beginning of each episode. Such design makes the policy robust by restricting the future effect of the submitted bids. Specifically, bids in an episode are not used in choosing the reserve prices until the beginning of the next episode. Therefore, there is always a delay until a buyer observes the effect of a bid on reserves. Then, considering the fact that buyers are impatient and discount the future, they are more incentivized to bid truthfully.

There is another important aspect of the policy that ensures its robustness: its estimation method. Rather than using the submitted bids to estimate the preference vectors, the policy simply uses the outcome of the auctions. Because of this feature of the policy, bidding untruthfully does not always result in lower reserve prices; instead, it can impact the future reserve prices of a buyer when it leads to changing the outcome of an auction, i.e., when a buyer loses an auction due to underbidding or a buyer wins an auction due to overbidding. As it becomes more clear later, the CORP-II and SCORP policies are also designed in a way to enjoy the aforementioned robustness properties.

-

•

CORP-II Policy: We design this policy for the setting where market noise distribution, which is fixed throughout time horizon, is unknown and belongs to a location–scale family. This policy obtains a regret in the order of against a clairvoyant policy that knows the preference vectors and market noise distribution. Similar to the CORP policy, CORP-II estimates the preference vectors and parameters of the market noise distribution using a maximum Likelihood estimator. It also enjoys an episodic structure. However, due to uncertainty in the market noise distribution, the length of the episodes grows at a slower rate, compared with that in CORP.

-

•

SCORP Policy: Our SCORP policy is designed for a setting where the time-varying market noise distribution is unknown to the seller and belongs to an ambiguity set. Then, under the log-concavity assumption on the noise distribution, our policy that knows the ambiguity set, obtains the T-period regret of order . Here, the regret is computed against a benchmark called robust; see Definition 5.1. The robust benchmark bears some resemblance to the benchmark used in the regret analysis of CORP; it knows the true preference vectors and the ambiguity set and based on this knowledge chooses the reserve prices that work well against the worst distribution in the ambiguity set. In contrast to the benchmark used in CORP-II, the benchmark here does not intend to learn the noise distribution, as the distribution of the noise can be time-varying. It instead posts “robust” reserve prices.

The increase in the regret, compared to CORP-II, is due to the fact that the noise distribution is time-varying and as a result, the seller cannot hope to learn it. Because of this, the policy spends more time on exploration compared to CORP-II, which leads to its higher regret. SCORP uses the same episodic structure as CORP-II but dedicates the beginning portion of each episode to pure exploration. Concretely, in episode , with length , pure exploration phase consists of periods. Spending more time on exploration is not the sole difference between CORP-II and SCORP. Given that the noise distribution is time-varying, SCORP uses a least-square estimator to update the estimates of preference vectors, while CORP-II employs the maximum Likelihood estimator, taking advantage of the fact the market noise distribution is fixed and belongs to a location–scale family.

The rest of the paper is organized in the following manner. In Section 2, we review the literature related to our work. Section 3 formally defines our model. We present the CORP in Section 4 and present CORP-II and SCORP policies in Section 5. Finally, we conclude in Section 6.

This paper has an electronic companion. Appendix 7 reviews lower bounds on regret in different pricing settings. In Appendix 8, we provide a discussion on (i) extending our policies to a setting with some non-linear valuation models, and (ii) learning how to price when data is perishable. Appendices 9, 10, and 11 provide the proof of the regret bound of CORP, CORP-II, and SCORP, respectively.

2 Related Work

In this section, we briefly discuss the literature related to our work.

Dynamic Pricing with Learning: Our work is related to the growing body of research on dynamic pricing with learning; see (den Boer 2015) for a survey. (Rothschild 1974, Araman and Caldentey 2009, Farias and Van Roy 2010, Harrison et al. 2012, Cesa-Bianchi et al. 2015, Ferreira et al. 2016, Cheung et al. 2017) studied dynamic pricing with demand uncertainty in the non-contextual and Bayesian settings. In contrast, (Broder and Rusmevichientong 2012, den Boer and Zwart 2013, Besbes and Zeevi 2009) studied this type of problems in the frequentist settings. In these settings, the parameters of the model, which are unknown (but fixed), are estimated using the maximum Likelihood (ML) method or other estimation techniques. We note that there are two important aspects that distinguish our work from this line of literature: the presence of the contextual information and strategic behavior of the buyers. In the following, we elaborate on these aspects by reviewing the related work.

Contextual Dynamic Pricing with Learning in Non-strategic Environment: Recently, several works considered the problem of dynamic pricing in a non-strategic setting when the unknown demand function depends on the customers’ characteristics (aka contextual information). In such settings, customers are not strategic in a sense that they do not consider the impact of their current actions on the future prices they will see. Chen et al. (2015) studied this problem when the demand function follows the logit model and proposed an ML-based learning algorithm. Leme and Schneider (2018), Cohen et al. (2016), and Lobel et al. (2016) proposed a learning algorithm based on the binary search method when the demand function is linear and deterministic. In their models, buyers have homogenous preference vectors and are non-strategic. Hence, the problem reduces to a single buyer setting, where the buyer acts myopically, i.e., the buyer does not consider the impact of the current actions on the future prices. In our setting, however, the seller interacts with a heterogeneous set of buyers in repeated second-price auctions, rather than the posted-price mechanism. Thus, the seller should estimate a preference vector per buyer and use these estimates to set personalized contextual-based reserve prices. There is also a new line of literature that studied dynamic pricing with demand learning when the contextual information is high dimensional (but sparse); see Javanmard and Nazerzadeh (2019), Ban and Keskin (2017). Similar problems have been investigated in Bastani and Bayati (2015), Javanmard (2017).

As mentioned earlier, in our setting, the seller repeatedly interacts with a small number of strategic and heterogeneous buyers. We note that Edelman and Ostrovsky (2007) presented empirical evidence that showed buyers in online advertising markets act strategically. There is also a large body of literature that studied dynamic pricing in a setting where buyers are strategic and the demand function is known a priori; see, for example, Borgs et al. (2014), Besbes and Lobel (2015), Golrezaei et al. (2017b).666Very recently, Chen and Keskin (2018) study dynamic pricing with unknown demand. Here, customers have unit-demand, arrive over time, and time their purchase strategically. This literature highlights the importance of considering the strategic behavior of buyers in updating prices over time.

Pricing with Strategic Buyers and Demand Learning: Amin et al. (2013), Medina and Mohri (2014), and Kanoria and Nazerzadeh (2017) examined the problem of dynamic pricing with strategic buyers in a non-contextual environment.777Learning with strategic players has been studied very recently in different settings including spread betting markets (Birge et al. 2018) and multi-armed bandit settings (Braverman et al. 2017). In Amin et al. (2013) and Medina and Mohri (2014), the seller repeatedly interacts with a single strategic buyer via a posted-price mechanism. Similar to our setting, the seller is more patient than the buyer in a sense that the buyer discounts his future utility. Amin et al. (2013) showed that no learning algorithm can obtain a sub-linear regret when the buyer is as patient as the seller. In addition, via designing learning policies, they demonstrated that the seller can get a sub-linear regret bound when the buyer is less patient.

Kanoria and Nazerzadeh (2017) studied dynamic pricing when a group of strategic buyers competes with each other in repeated non-contextual second-price auctions. A main difference with our setting is that in their model, buyers are as patient as the firm and hence there is no time-discount factor for buyers’ utilities. They designed a near-optimal elegant pricing policy in which the reserve price of each buyer is computed using the submitted bids of other buyers. Specifically, for any , their policy can be designed to achieve of the expected revenue obtained under the static Myerson optimal auction for the valuation distribution. Note that this corresponds to a linear regret bound in our terms. Indeed in the setting that buyers do not discount their future utilities and buyers are utility-maximizer, it is impossible to get a sub-linear regret (Amin et al. 2013). Further, in (Kanoria and Nazerzadeh 2017) it is assumed that products to be sold are ex-ante identical, and that buyers are homogenous and their valuations are all drawn from a single distribution, which is unknown to the seller.

With respect to the homogeneity assumption, we point out that there exists empirical evidence that buyers are indeed heterogeneous (Guimaraes and Sheedy 2011, Johnson and Myatt 2003, Golrezaei et al. 2017a). It is not surprising that the heterogeneity in the markets makes the design of selling mechanisms more difficult. In addition, such difficulties get more severe when the seller needs to design dynamic selling mechanisms for a group of strategic buyers that compete with each other repeatedly.

Recently, Mahdian et al. (2017) studied a similar problem in a static non-contextual setting where the seller has access to (strategic) data points and using these data points, she would like to design a mechanism that can incentivize the buyers to be truthful in the first place. They show that when the market power of each buyer is negligible, designing such a mechanism is feasible. To achieve this result, they apply the technique of differential privacy (McSherry and Talwar 2007).

Closer to the spirit of this paper, Amin et al. (2014) studies the problem of pricing inventory in a repeated posted-price auction. The authors propose a pricing algorithm whose regret is in the order of in a contextual setting, against a strategic buyer. 888Dependency on is hidden in the big- notation. We point out that our regret result improves upon Amin et al. (2014) in the following directions:

-

-

We allow for market noise in our model, whereas Amin et al. (2014) considers noiseless setting which posits that buyer’s valuation is given as a linear function of features. Due to this difference, their algorithm and regret bound obtained for noiseless setting in Amin et al. (2014) cannot be applied to our noisy setting and vice versa. Nonetheless, by adding the noise component, we make the model richer. When the noise distribution is known, our CORP policy obtains a T-period regret of . In addition, when the noise distribution is unknown, our SCORP policy, which is doubly robust against strategic buyers and the uncertainty in the noise distribution, obtains a T-period regret of .

-

-

We consider a market of strategic buyers who participate in a second-price auction at each round, while Amin et al. (2014), motivated by targeting in online advertising, considers a single buyer case. Note that in case of a single buyer, there is no notion of bid, as the buyer only needs to decide if he is willing to purchase the item at the posted price. By contrast, in a market of buyers, each submitted bid of a buyer can potentially affect the utility of that buyer (instant and long-term utility), other buyers’ utilities and the seller’s revenue. We note that Section 5 in Amin et al. (2014) considers an extension to the multiple buyers case but assumes that the highest valuation in each period can be written as for a fixed parameter vector , and product feature (context) , which we find to be a strong assumption.

Behavior-based Pricing: Our work is also related to the literature on behavior-based pricing where the seller uses the past behavior of the buyers to update the prices (Hart and Tirole 1988, Schmidt 1993, Fudenberg and Villas-Boas 2006, Acquisti and Varian 2005, Esteves et al. 2009, Bikhchandani and McCardle 2012). In this literature, it is mostly assumed that the buyer’s valuation, which is drawn from a publicly known distribution, is fixed throughout the time horizon. Thus, the seller does not need to learn the valuation distribution; instead, the seller aims at learning the realized valuation of the buyer. Note that considering a static valuation for a buyer in the online advertising market is not reasonable, as in this market, buyer’s valuation can depend on the rich contextual information, which varies over time. We also note that in the behavior-based pricing literature, the seller and buyer usually get engaged in repeated games, where each of the player responds to other player’s strategy to form a perfect Bayesian Nash equilibrium.

3 Model

Before we describe the model, we adopt some notation that will be used throughout the paper. For an integer , we write . In addition, for a vector , we denote its coordinates by , for , and indicate its norm by . For two vectors , represents their inner product. Finally, denotes the indicator function: when event happens, and is zero otherwise.

We consider a firm who runs repeated second-price auctions with personalized reserve over a finite time horizon with length . In each period , the firm would like to sell an item to one of buyers. The item in period is represented by an observable feature (context) vector denoted by . We assume that the features are drawn independently from a fixed distribution , with a bounded support . Note that the length of the time horizon and distribution are unknown to the firm. For the sake of normalization and without loss of generality, we assume that , and hence take . We let be the second moment matrix of distribution , and assume that is a positive definite matrix, where is unknown to the firm.

For buyers’ valuations, we consider a feature-based model that captures heterogeneity among the buyers. In the following, we discuss the specifics of the valuation model. Valuation of buyer for an item in period depends on the feature vector and period and is denoted by . We assume that is a linear function of a preference vector and the feature vector . (We relax this assumption in Appendix 8.) That is,

| (1) |

Whenever it is clear from the context, we may remove the dependency of valuation on the feature vector and denote it by . Here, represents the buyer ’s preference vector, and for the sake of normalization, we assume that , , where is a constant. The terms ’s, , , which are independent of the feature vector , are idiosyncratic shocks and are referred to as noise. The noise terms are drawn independently and identically from a mean zero distribution with continuous density , where is a constant.999The noise aims at capturing features that are not observed/measured by the firm. We assume that the firm knows the distribution of the noise . We relax this assumption later in Section 5. Note that the valuation of buyer , , is not known to the firm, as the preference vector and realization of the noise are not observable to her. In addition, by our normalization, , with .

We make the following assumption on distribution of the noise .

[Log-concavity] and are log-concave in .

Assumption 3, which is prevalent in the economics literature (Bagnoli and Bergstrom 2005), holds by several common probability distributions including uniform, and (truncated) Laplace, exponential, and logistic distributions. A few remarks are in order regarding Assumption 1. If distribution is log-concave and its density is symmetric, i.e., , then is also log-concave. Moreover, if density is log-concave, the cumulative distribution function and the reliability function are also log-concave (Bagnoli and Bergstrom 2005). This implies that Assumption 3 is satisfied when the density is log-concave. We also point out that if a density has a monotone hazard rate (MHR), i.e., is increasing in , then is log-concave. This point, in turn, shows that all MHR and symmetric densities satisfy Assumption 3.

We next describe the repeated second-price auctions and discuss the firm’s problem. The goal of the firm is to maximize the cumulative expected revenue in repeated second-price auctions. The firm tries to achieve this by choosing reserves in a dynamic and personalized manner.

3.1 Second-price Auctions with Dynamic Personalized Reserves

Before defining a second-price auction, we need to establish some notation. For buyer and period , we let be the payment from buyer in period . Further, let be the allocation variable: if the item in period is allocated to buyer and is zero otherwise. We also let be the bid submitted by buyer and be the reserve price posted by the firm for buyer in period . We define and as the vectors of bids and reserves in period , respectively. Moreover, we denote by the history set observed by the firm up to period . This set includes buyers’ bids and reserve prices for all :

| (2) |

Below, we explain the details of the second-price auction with reserve. In period ,

-

•

The firm observes the feature vector . In addition, each buyer learns his valuation , defined in Equation (1).

-

•

For each buyer, the firm computes reserve price , as a function of history set and the feature vector .

-

•

Each buyer submits a bid of .

-

•

Let . If , then the item is allocated to buyer , and we have . In case of a tie, the item is allocated uniformly at random to one of the buyers among those with the highest bid. For all buyers who do not get the item, we have .

-

•

For each buyer , if he gets the item , then he pays . Otherwise, .

To lighten the notation, we henceforth use the following shorthands. For each period , we let and respectively denote the highest and second highest bids. Likewise, we define and as the highest and second highest valuations in period . We also let be the reserve price of the buyer with the highest bid. Therefore, , , and the firm receives a payment of if the item gets allocated and zero otherwise. We assume that for all periods , for some constant . In words, buyers submit bounded bids.

This version of the second-price auctions is called Lazy auctions (Paes Leme et al. 2016). Here, the item is allocated to a buyer with the highest submitted bid, as long as the buyer clears his reserve. In other words, the item will not be allocated to any buyer when the buyer with the highest submitted bid does not clear his reserve price. As stated in the introduction, there is another version of second-price auctions called Eager auctions. In Eager auctions, all the buyers that do not clear their reserve prices are eliminated first, and then the item is allocated to one of the remaining buyers that has the highest submitted bid. Paes Leme et al. (2016) showed that these two versions do not dominate each other in terms of their yield revenue. Thus, here we focus on the Lazy auctions, as reserve prices in these auctions can be optimized effectively; see Proposition 3.1. We further note that Kanoria and Nazerzadeh (2017) argued that even when buyers are homogeneous, designing a learning algorithm for eager second-price auctions that can incentivize the buyers to bid truthfully is very challenging.

The firm’s decision in any period is to find optimal reserve price , , and her objective is to maximize her (cumulative) expected revenue. Note that revenue of the firm is the total payment she collects from the buyers over the length of the time horizon. Let

| (3) |

be the expected revenue of the firm in period , where the expectation is w.r.t. to the noise distribution , feature distribution , and any randomness in the bidding strategy of buyers and learning policy used by the firm. Then, the total revenue of the firm is given by .

Maximizing the firm’s revenue is equivalent to minimizing her regret where the regret is defined as the difference between the firms’ revenue and the maximum expected revenue that the firm could earn if she knew the preference vectors . In the next section, we will formally define the firm’s regret.

3.2 Benchmark and Firm’s Regret

As stated earlier, the firm’s objective is to minimize her regret, which is the maximum expected revenue loss relative to a benchmark policy that knows the preference vectors in hindsight. When the preference vectors and noise distribution are known, to set the optimal reserves , the benchmark policy does not need any knowledge from the history set . Thus, with the knowledge of the preference vectors, all buyers are incentivized to bid truthfully against the benchmark policy. This is the case because single-shot second-price auctions are strategy proof (Myerson 1981).

We next characterize the benchmark policy. Let be the reserve of buyer in period posted by the benchmark policy and following our convention, we denote by the reserve price of the buyer with the highest bid.

Proposition 3.1 (Benchmark)

If the firm knows the preference vectors and (fixed) noise distribution , then the optimal reserve price of buyer for a feature vector is given by

| (4) |

and hence . In addition, in any period , the benchmark expected revenue is given by

| (5) |

where expectation is w.r.t. to the noise distribution and the feature distribution .

We refer to Appendix 12 for the proof of Proposition 3.1. We remark that the benchmark revenue is measured against truthful buyers, while the firm’s revenue under our policy is measured against strategic buyers who may not necessarily follow the truthful strategy.

Observe that the optimal reserve price of buyer in period , denoted by , solves the following optimization problem

This shows that the optimal reserve price of buyer does not depend on the number of buyers participating in the auction or their preference vectors. In other words, in (lazy) second-price auctions, when the preference vectors are known to the firm and the noise distribution is log-concave, the problem of optimizing reserve prices can be decoupled.101010This is not the case for the eager second-price auctions. Because of this, the benchmark, defined in Proposition 3.1, has a simple structure: For any feature vector , the optimal reserve price of buyer , , only depends on and feature , and is independent of , .

In fact, the benchmark policy offers the best mapping from the features to reserve prices, where this mapping does not change with time. This is due to the fact the noise distribution and the feature distribution remain unaltered across time and is the expected revenue of the firm in period , with the expectation taken w.r.t. the context vector and valuation noise.

Note that in non-contextual settings, the regret is measured against a policy that posts a single fixed optimal vector of reserve prices. In our contextual setting, by contrast, we would like to compare our learning policy with the best mapping from the feature (context) vectors to the vector of reserve prices. In addition, the benchmark’s optimal mapping depends on the buyer’s preference vector ; that is, the benchmark offers personalized reserve prices. Competing with such a strong benchmark that takes into account the impact of contexts as well as the heterogeneity among buyers is one of the challenges faced by the firm.

Having defined the benchmark, we are now ready to formally define the regret of a firm’s policy . Recall that the firm’s decision is to optimize reserve prices. To set the reserve prices optimally, the firm needs to learn the preference vectors . To do so, the firm faces the trade-off between exploration and exploitation. Such a trade-off is not the only hurdle that the firm is facing: the buyers can act strategically and interfere with the learning process of the firm by bidding untruthfully. Let us stress that the buyers’ behavior not only affects the outcome of the current auction but also can impact the future outcomes. The reason is that the firm can use the history set in posting reserves. Therefore, in general, each buyer’s bid may have a perpetual effect on the firm’s revenue. In Section 3.3, we further elaborate on the buyers’ bidding behavior. Thus, the firm’s goal is to deploy a robust learning policy that limits the long-run effect of each bid and tries to incentivize the buyers to be truthful.

Consider a policy that posts a vector of reserve prices , as a function of history set observed by the firm. Suppose that the buyers submit bids of , , where may not be equal to the vector of valuations . The submitted bid of buyer , , can depend on the learning policy used by the firm, context , his valuation , and history , where

Recalling our notation, we write to denote the reserve price, set by policy , of the buyer with the highest bid in period . Then, the expected revenue of the firm under policy in period reads as

| (6) |

where expectation is w.r.t. to the noise distribution , feature distribution , and any randomness in bidding strategy of the buyers.

Then, the worst-case cumulative regret of policy is defined by

| (7) |

Note that the regret of the policy is not a function of the feature distribution and the feature vectors . That is, we compute the regret of the policy against the worst feature distribution and preference vectors .

In the next section, we discuss buyers’ bidding behavior.

3.3 Utility-maximizing Buyers

We assume that each buyer is risk neutral and aims at maximizing his (time-discounted) cumulative expected utility. The utility of buyer in period with valuation is given by

where is a discount factor. The discount factor highlights the fact that the firm is more patient than the buyers. For instance, in online advertising markets, advertisers are willing to show their ads to the users who just visited their websites.111111Such a practice is known as retargeting (Amin et al. 2014, Golrezaei et al. 2017a). As another example, in cloud computing markets, the consumers would like to access enough capacity whenever they need it (Borgs et al. 2014). Note that through the allocation variables , utility , depends on the submitted bids of all the buyers, , and their reserve price used by the firm.

In any period , each buyer would like to maximize his time-discounted cumulative utility that he will earn in any period , which is defined as

We note that Amin et al. (2013) showed that it is impossible to get a sub-linear regret when buyers are utility-maximizer and do not discount their future utilities. We further remark that the firm does not need to know as our policies are oblivious to . However, as we show later, our regret bounds depend on .

All buyers fully know the learning policy that the firm is using to set the reserves.121212This assumption is inspired by the literature on the behavior-based pricing where it is shown that the firm can earn more revenue by committing to a pricing strategy (Hart and Tirole 1988, Salant 1989). See also Aviv and Pazgal (2008), Aviv et al. (2015) for a similar insight. More precisely, if the policy involves randomization, the buyers know in advance the policy and not the realization of the policy. Armed with this knowledge, buyers can potentially increase their future utility they earn via bidding untruthfully. Particularly, a buyer can underbid (shade) his bid by submitting bid , or he can overbid by submitting bid . Both shading and overbidding can potentially impact the firms’ estimate of preference vectors of the buyers and this, in turn, can hurt the firms’ revenue. However, shading can lead to a utility loss in the current period, as by shading, the buyer may lose an auction that he would have won by bidding truthfully. Similarly, overbidding can result in a utility loss in the current period, as by overbidding the buyer might end up paying more than his valuation.

We next present our robust policy, named CORP, for learning preference vectors through interaction with utility-maximizing buyers in repeated second-price auctions with reserve.

4 CORP: A Contextual Robust Pricing Policy

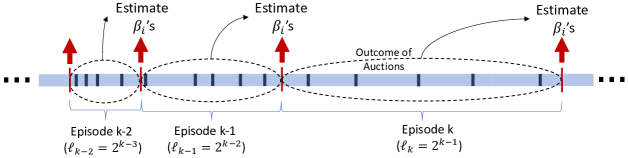

In this section, we present our learning policy. The description of the policy is provided in Table 1. For reader’s convenience, we also provide a schematic representation of CORP in Figure 1. The policy works in an episodic manner. It tries to learn the preference vectors by using Maximum Likelihood Estimation (MLE) and meanwhile sets the reserve prices based on its current estimates of the preference vectors. Episodes are indexed by , where the length of each episode, denoted by , is given by . Thus, episode starts in period and ends in period . Note that the length of episodes increases exponentially with . Throughout, we use notation to refer to periods in episode , i.e., .

At the beginning of each episode , we estimate the preference vectors of the buyers using the outcome of the auctions (’s) in the previous episode, i.e., episode , and we do not change our estimates during episode . Let be the estimated preference vector of buyer at the beginning of episode . Then, solves the following optimization problem:

| (8) |

where

| (9) |

is the negative of the log-likelihood function. Here, refers to the maximum bids of buyers other than buyer , in period ; that is, . Then, buyer wins the auction in period if and only if . Throughout the manuscript, to avoid ties, we make a simplifying assumption that the submitted bids are distinct. Similarly, we define . Note that is the probability of event , which is the probability that buyer does not win the item at time , upon bidding truthfully.131313Since the noise density is zero outside the interval , we have , for and for . In addition, . In computing the negative log-likelihood function, we adopt the convention of . The log-likelihood function is computed after running the auctions in all the periods of episode . Therefore, the firm has access to the required knowledge to compute the log-likelihood function . Specifically, by the time the firm computes , she has access to the submitted bids of the buyers in periods as well as the reserve prices used in these periods.

Now, one may wonder why CORP does not use a simple mean square error estimator for which the estimate of preference vector at the beginning of episode is given by . This quadratic estimator, unlike the maximum Likelihood estimator used in CORP, uses the submitted bids of buyers directly and as a result, it is rather vulnerable to the strategic behavior of the buyers. This is so because the mean square error estimators are sensitive to outliers and this undesirable property would be an advantage to strategic buyers to manipulate the seller’s pricing policy. In light of this observation, to estimate the preference vector of any buyer , CORP applies a maximum Likelihood estimator that only uses the outcome of the auctions , that we refer to as “censored bids”, and submitted bids of other buyers expect buyer ; see the definition of the log-likelihood function in Equation (9). This makes the estimation procedure of the policy robust to untruthful bidding behavior of the buyers, as untruthful bidding may not necessarily lead to a different outcome. In addition, due to this feature of the learning policy, the buyers are incentivized to bid truthfully unless they are interested in changing the outcome of the auction at the expense of losing their current utility. Later when we outline the proof of the regret bound of CORP, we further elaborate on this.

After estimating the preference vectors at the beginning of each episode , the policy proceeds to use its estimation to set reserve prices. In particular, the reserve price in period , , solves

| (10) |

Note that by Proposition 3.1, if , then where is the optimal reserve price of buyer in period .

We now discuss some of the important features of our policy.

-

•

In each episode , every period is assigned to exploitation with probability , and is assigned to exploration with probability . In the exploration periods, the firm chooses one of the buyers at random and allocates the item to him if his submitted bid is above a reserve price where is the uniform distribution in the range . In exploitation periods, the firm exploits her current estimate of the preference vectors to set the reserve prices where the estimates are obtained by applying the MLE method to the outcomes of auctions in episode .

As stated earlier, in the exploration periods, we randomly choose prices. However, the firm does not crucially use this randomness to identify the best reserve prices. Recall that to set the reserve prices, the firm uses all the data points in the previous episode, not only the data points in the exploration periods. The main purpose of setting reserve prices randomly in the exploration periods is to motivate the buyers to be truthful. Note that the buyer does not know if in a given period , the prices are set randomly. Thus, if he underbids in such a period, with a positive probability, he loses the opportunity to obtain a positive utility. Considering this and the fact that the buyers discount the future utilities, the randomized reserve prices incentivize the buyers to bid truthfully.

-

•

Another important factors that makes the CORP policy robust is its episodic structure and impatience of buyers. In the CORP policy, submitted bids in episode are not used in setting reserve prices until the beginning of the episode . Therefore, there is always a delay until buyers observe the effect of a bid on their reserves. Then, since buyers are impatient and maximize their discounted cumulative utility, they have less incentive to bid untruthfully. This is a salient property of the CORP policy that bounds the perpetual effect of each bid and, as we will see in the analysis, leads to robustness of the learning policy to the strategic behavior of buyers.

4.1 Regret Bound of the CORP Policy

We now state our main result on the regret of the CORP policy.

Theorem 4.1 (Regret Bound: Known Noise Distribution)

The regret bound of CORP presented in Theorem 4.1 consists of two terms and . The first term of the regret bound is due to the estimation error in preference vectors; that is, this term exists even if buyers were not strategic. The second term is due to the strategic behavior of the buyers. Observe that the second term decreases as buyers get less patient; i.e., gets smaller.

The proof of Theorem 4.1 is proved in Appendix 9. To bound the regret of our policy, we note that untruthful bidding has two undesirable effects for the firm. First of all, both overbidding and shading increase the estimation errors of the preference vectors and thus, consequently, introduce errors in the reserve prices set by the firm. Second of all, bidding untruthfully can lower the second highest submitted bid as well as the reserve price of the winner, and this reduces the firm’s revenue. By this observation, we divide the policy’s regret into two parts, where each part captures the negative consequences of one of the aforementioned effects.

To bound the regret associated with the first effect, in Proposition 9.1, we determine to which extent buyers’ “lies” impact the estimation errors of the preference vectors and the reserve prices. We say a buyer lies when his untruthful bid changes the outcome of the auction, , for this buyer relative to the truthful bidding. That is, we say buyer lies in period if holds. Our notion of lies is inspired by our maximum Likelihood estimator used in CORP. To estimate the preference vector of any buyer , the maximum Likelihood estimator, defined in (9), only uses the outcome of the auctions and submitted bids of other buyers expect buyer . Thus, untruthful bidding can change our estimate of preference vector of buyer and consequently his reserve price only when he “lies”.

Having established the impact of lies, we then show that the number of times that a buyer lies in each episode is logarithmic in the length of the episode; see Proposition 9.2. This bound is derived using the property of our estimation method. As stated earlier, to influence the estimation of the preference vectors and reserve prices, buyers need to change the outcome of the auctions where such a change is costly for them as it can lead to utility loss. We then make use of the fact that buyers are utility-maximizer and discount the future to bound the number of lies. Precisely, to get this bound, we compare the long-term excess utility obtained from a lie with the instant utility loss that it causes. In particular, we derive a lower bound on the utility loss of the buyers in episode by focusing on the random exploration periods. Note that buyers are not aware whether a period is an exploration period. Thus, with a positive probability, any untruthful bid leads to a utility loss. We further derive an upper bound on the (future) utility gain of the untruthful bidding in episode . Our upper bound is the total discounted utility that any buyer can hope to achieve in the next episodes. Thus, the bound includes potential future utility gains that a buyer can enjoy by manipulating other buyers’ strategy and their reserve prices. Then, by arguing that for any utility-maximizer buyer, the upper bound on the utility gain should be greater than or equal to the lower bound on the utility loss, we bound the number of lies of the buyer. By characterizing the impact of lies in Proposition 9.1 and bounding the number of lies in Proposition 9.2, we are able to bound the regret associated with the first effect, namely the gap between the posted reserves and the optimal ones.

To bound the regret associated with the second effect, we quantify the impact of bidding untruthfully on the second highest bids and reserve of the winner; see Lemma 9.3. When buyers bid untruthfully, the second highest bid may decrease. Further, the winner of the auction can change and this, in turn, can lower the reserve price of the winner. Any of these events will hurt the firm’s revenue. To quantify this impact, we upper bound the amount of underbidding and overbidding from each buyer using the fact that the buyer is utility-maximizer; see Proposition 9.2. To do so, we employ a similar argument that we used to bound the number of lies.

After characterizing the regret due to both effects, we bound the total regret during each episode, and show that the total regret is logarithmic in the length of the episode. The proof is completed by noting that there are episodes up to time , as the length of episodes doubles each time.

5 Knowledge of Market Noise Distribution

In the CORP policy, we assumed that the market noise distribution is known to the seller or can be estimated sufficiently well from side data. However, we do not always have this commodity in practice. Ideally, we prefer a pricing policy that uses such knowledge minimally, if at all. To relax this assumption, we consider setting where the market noise distribution is not fully known, but is believed to belong to a known ensemble of distributions:

-

•

Unknown (Fixed) Distribution from a Known Location-scale Ensemble: Suppose that the unknown market noise distribution belongs to a known location-scale family of log-concave distributions. To recall, a log-scale family of distribution is a one that for a variable belonging to this family, the distribution function of random variable also belongs to this family. Some examples include Normal, Uniform, Exponential, Logistic, and Extreme value distribution, to name a few. We propose a policy that achieves a regret of . (In Appendix 7, we further show that even when buyers are not strategic, no other policy can have a regret better than .) To design CORP-II, we adopt the MLE estimator in CORP to also estimate the parameters of the noise distribution as well as the preference vectors, and in this sense, we follow the path pursued in (Javanmard and Nazerzadeh 2019) for the case of the single, non-strategic buyer. We refer to Section 5.1 for the details.

-

•

Unknown (Time-varying) Distribution from a Given Ambiguity Set: This is a more general setting where the noise distribution is unknown and time-varying, but belongs to a given ambiguity set of the log-concave distribution. In Section 5.2, we propose the so-called SCORP policy whose regret is of order .

5.1 Unknown Distribution from a Known Location-Scale Ensemble

Consider a location-scale class of distributions :

| (12) |

where is a known log-concave distribution with mean zero and variance one. We assume that the noise distribution is , with unknown parameters , , where and respectively corresponds to the mean and the variance of the noise distribution. Without loss of generality, we can assume that ; otherwise, the mean of the noise term can be absorbed in the features as an intercept term. As an example, the set can be class of uniform distribution with the support of where is unknown and . As another example, the set can be a class of (truncated) normal distributions with unknown standard deviation from an interval.

We let and in the model (1), we multiply both sides with . This leads to

| (13) |

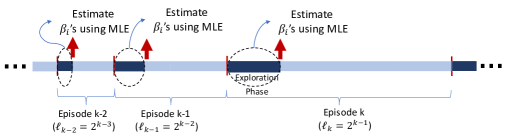

where , and . Notably, distribution of is . The valuation model (13) is similar to our previous model where the market noises were drawn from a known distribution . For this setting, we propose a pricing policy, named CORP-II which is very similar to the CORP policy: It has an episodic structure, where the length of episodes grows exponentially, namely episode is of length . The first periods of episode are the pure exploration periods. In each of these period, a buyer is chosen in a round robin fashion (call him ) and offer him the item at price of . For other buyers, we set their reserves to . In the remaining periods of the episode, we set the reserve prices based on the current estimates of the preference vectors and the scale parameter . Specifically, we let be the set of pure exploration periods in episode (so ) and form the negative log-likelihood function to estimate both and using the outcomes of auctions in :

| (14) |

The function is indeed the negative log-likelihood for allocation variables for , conditional on the feature vectors , and the events , , assuming that buyer is truthful. The term comes from the fact that the buyer is chosen in a round robin fashion and so for a fixed , there are fraction of the periods in contributing to the log-likelihood function .

Let solves the following optimization problem:

| (15) |

with .

In the exploitation phase, the reserve of each buyer is set to

| (16) |

The formal description of CORP-II policy is given in Table 2. We also provide a schematic representation of CORP-II in Figure 2. CORP-II has a very similar structure to CORP. The main difference is that unlike CORP, we have some forced (pure) exploration periods at the beginning of each episode at which we experiment with random prices to learn both the preference vectors and the parameters of the noise distribution. The force exploration periods are required because in the current setting the market noise distribution is not fully known; see lower bound on regret in Appendix 7. By comparison, in CORP, the market noise distribution is fully known to the seller and we have much fewer of exploration periods (recall that in CORP, in each period of episode , we do exploration with probability and so in expectation, we have only one exploration period in each episode).

Note that by the decoupling property (as stated in Proposition 3.1), the benchmark policy can focus on each buyer separately. This leads to the following optimal reserve, which optimizes the revenue obtained from buyer :

Our next theorem characterizes the regret bound of CORP-II policy against a benchmark that knows the buyers’ preference vectors and the true market noise distribution.

Theorem 5.1 (Regret Bound: Unknown Noise Distribution from a Location-Scale Ensemble)

Consider the valuation model (1) where the market noise ’s are generated from a distribution belonging to , defined in (12). Suppose that in the definition of satisfies Assumption 3. Then, the T-regret worst-case regret of CORP-II policy is at most

where the regret is computed against the clairvoyant that knows the buyers’ preference vectors and the noise distribution.

5.2 Unknown Distribution from a Given Ambiguity Set

The CORP policy presented in this paper is assumed to know the market noise distribution . This knowledge is used in forming the log-likelihood estimator to learn preference vectors ’s and also in setting the reserves for buyers as in (10). Furthermore, we relaxed this assumption in the previous section by assuming that is unknown and fixed and belongs to a location–scale family, and for this setting, we presented CORP-II policy. Nevertheless, in practice, it may very well be the case that distribution is unknown and time-varying and as a result, it cannot be well approximated. To address this problem, we propose a variant of the CORP policy, called Stable Contextual Robust Pricing (SCORP), which is robust against the lack of knowledge of . Specifically, we consider an ambiguity set of possible probability distributions for the market noise and propose a policy that works well for every probability distribution in the ambiguity set.

We make the following assumption on the ambiguity set . This assumption is analogous to Assumption 3.

[Log-concavity of the Ambiguity Set ] All functions are log-concave.

To be fair, in this case, we compare the regret of our policy against a benchmark policy, called robust, that knows the true preference vectors and the ambiguity set that includes , but is oblivious to distribution itself. The robust benchmark is defined as follows:

Definition 5.1 (Robust Benchmark)

In the robust benchmark, the reserve price of buyer for a feature vector is given by

| (19) |

and thus in this case.

The robust benchmark is motivated by our previous benchmark presented in Proposition 3.1. In our previous benchmark, we show that given a distribution and context , the revenue-maximizing reserve price for buyer solves . In the robust benchmark, the posted reserve prices have a similar form. However, the reserve prices which solves the optimization problem (19), are chosen in a robust way so that the benchmark performs well despite the uncertainty in the market noise distribution. We will discuss the complexity of optimization problem (19) in Section 5.2.1.

We note from the robust benchmark, as well as our learning policy, that we will present shortly do not aim at learning the distribution of market noise, as this distribution can vary across periods. For instance, in online advertising, the distribution of the noise can depend on many different factors including the time of the day and demographic information of the Internet users. Thus, instead of trying to learn the market noise distribution, we would like to use reserve prices that are robust to the uncertainty in the noise distribution.

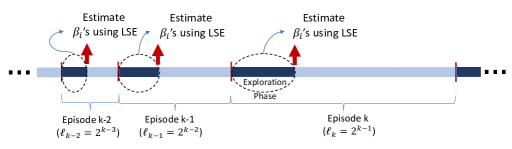

We are now ready to present our SCORP policy. This policy is a modified version of the CORP-II policy. For reader’s convenience, we also provide a schematic representation of SCORP in Figure 3. Similar to the CORP-II policy, SCORP has an episodic theme, with the length of episodes growing exponentially. As before, we denote the set of periods in episode by , i.e., , with . Each episode starts with a pure exploration phase of length . As before, we use notation to refer to periods in the pure exploration phase of episode , i.e., . During each period in , we choose one of the buyers uniformly at random and offer him the item at price of . For other buyers, we set their reserve prices to . Observe that in SCORP, because distribution is time-varying, we dedicate more periods to pure exploration than CORP-II. In the remaining periods of the episode (i.e., ), we offer the reserve prices based on the current estimates of the preference vectors which are obtained by applying the least-square estimator to the outcomes of auctions in the pure exploration phase, ; see Equations (20) and (22). This is the exploitation phase as we set reserves based on our best guess of the preference vectors.

We note that the SCORP policy follows a similar structure to the LEAP policy proposed in Amin et al. (2014). Assuming that the time horizon is known, the LEAP policy designates the first periods to pure exploration and the remaining periods to exploitation. Using the doubling trick, the LEAP policy is extended to the setting with an unknown time horizon, which then admits a similar structure to SCORP. In comparison between SCORP and LEAP, it is worth highlighting a few points: 1) SCORP generalizes LEAP to the case of multi-buyers. 2) LEAP considers a setting with noiseless valuations while SCORP allows for noise component in the valuation function. As a consequence, the pricing functions differ in the two policies. SCORP uses (22), which involves a min-max optimization over the ambiguity set while in LEAP, the prices in the exploitation periods are set as , for an appropriate choice of . 3) More on the technical part, SCORP updates its estimate on the preference vectors only at the end of each exploration phase while LEAP update its estimate at each period by taking a gradient step on the prediction loss.

The formal description of SCORP is given in Table 3.

Having presented our policy, we now highlight few important remarks about the estimation process of the policy. (i) Since the noise distribution is unknown and time-varying, SCORP employs the least-square estimator (LSE) rather than the maximum Likelihood method, used in CORP and CORP-II; compare Equations (9) and (14) with (21). To apply the least-square estimator, similar to the CORP and CORP-II policies, SCORP uses the outcome of the auctions, not the submitted bids. In particular, SCORP minimizes the loss function where the loss function is designed in a way to provide an unbiased estimator of the preference vectors under the truthful bidding strategy. To see why note that to estimate the preference vectors, we only use the outcome of the auctions, , in the exploration periods where in exploration periods, the prices are chosen uniformly at random in . Then, when buyers are truthful, the expectation of w.r.t. the randomness in prices and the noise in the valuations is . This implies that under the truthful bidding strategy, the expectation of for any exploration period is zero. Put differently, even under truthful bidding, the expectation of for exploitation periods is not zero and as a result, we only use the data in the exploration periods to estimate the preference vectors, and this, in turn, enforces the SCORP policy to dedicated periods to exploration. This makes SCORP robust to the strategic behavior of the buyers. (ii) Due to uncertainty in the noise distribution, for estimation, SCORP only utilizes the auction outcomes in the exploration phase where it does price experimentation. This is in contrast to CORP policy where all the auction outcomes in the previous episode are used to estimate the preference vectors. It is worth noting that in our analysis of the regret, we give up on the revenue collected during pure exploration phases and only use the outcomes of auctions in these phases to bound the estimation error of the preference vectors. (iii) So far, we argued SCORP is designed in a way to ensure robustness against strategic buyers. Importantly, we also note that the choice of reserve prices in the exploitation phase of SCORP makes this policy robust against the uncertainty in the noise distribution. Thus, SCORP is indeed doubly robust.

Our next result upper bounds the regret of the SCORP policy.

Theorem 0 (Regret Bound: Unknown Noise Distribution from an Ambiguity Set )

Suppose that Assumption 5.2 holds, and that the market noise distribution is unknown and belongs to uncertainty set . Then, the T-period worst-case regret of the SCORP policy is at most

where the regret is computed against the robust benchmark.

Observe that due to the strategic behavior of the buyers, the firm suffers from an extra regret of , where this regret shrinks as decreases. We note that while the regret of the CORP-II policy is in the order of , the regret of SCORP is . The higher regret of SCORP is mostly due to the fact that distribution is time-varying, and because of this, SCORP cannot make use of the exploratory effect of the noise. Considering this, the SCORP policy dedicates more periods to exploration This implies that the SCORP policy learns preference vectors at a slower rate than CORP-II policy. The slower learning rate is the main reason behind the higher regret of SCORP.

Remark 5.2

SCORP policy provides a very general machinery to design low-regret doubly robust learning policies, against different benchmarks.141414The firm may care about other objectives apart from her revenue. For instance, the firm might be interested in maximizing a convex combination of the welfare and revenue, or due to contracts and deals, she might be willing to prioritize some of the buyers by offering them lower reserve prices. To make it clear, assume that firm uses a benchmark that posts reserve price of for buyer , under context vector . Here, , where . Then, as long as is Lipschitz in its first argument, we can design a low-regret doubly robust learning policies against this benchmark by only changing the exploitation phase of the SCORP policy. Particularly, in a period in the exploitation phase of episode , we set ; see Equation (22) for comparison.

5.2.1 Complexity of SCORP

In SCORP, in each exploitation period, the optimization problem (22) needs to be solved to set reserve prices. Here, we discuss several cases where this optimization problem is rather easy to solve. We start by presenting an example in which the ambiguity set consists of uniform distributions. For this example, we provide a simple closed form solution for problem (22). We then discuss the uniform distributions are not exceptions in the sense that for many classes of distributions, the optimization problem of SCORP is indeed easy to solve.

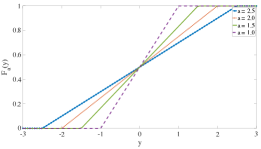

Example 5.3 (Uniform Distributions)

Assume that the ambiguity set includes all the uniform distributions with support of form where . The following theorem presents the optimal solution of problem (22) for the described . Before stating the theorem, let us stress again that in the setting of SCORP, the distribution can change over time. So, for this example it means that at step , the market noises are drawn from a uniform distribution , with support , where , is unknown and time varying.

Theorem 0

Suppose that includes all the uniform distributions with the support of where . Then, for any , we have

The proof of the theorem is deferred to the appendix. \Halmos

In Example 5.3, we observe that under uniform distributions, the robust optimization problem in (22) has a simple and easy-to-compute solution. This stems from the fact that the uniform distributions enjoy a single-crossing property; see Figure 4. To make it clear, let be the distribution of the uniform distribution in the range of where . Then, (i) for any , , (ii) for any and , , and (iii) for any and , . That is, for any , and cross each other once at . Having this single-crossing property, the inner optimization problem in (22) is easy to solve and as a result, problem (22) has a closed form solution. We highlight that uniform distributions are not the only distributions that enjoy such a property. Consider normal distributions with mean zero and variance , denoted by . Then, for any , and cross each other once at . In general, the location-scale families (with fixed location parameter) considered in Section 5.1, namely , satisfy the single-crossing property if is strictly increasing.

6 Conclusion

Motivated by online marketplaces with highly differentiated products, we formulated a dynamic pricing problem in the contextual setting. In this problem, a firm runs repeated second-price auctions with reserve and the item to be sold in each period is described by a context (feature) vector. In our model, contextual information of an item influences buyers’ valuations of that item in a heterogeneous way, via buyers’ preference vectors. Due to the repeated interaction of buyers with the firm, buyers have the incentive to game the firm’s policy by bidding untruthfully. We proposed three pricing policies to set the reserve prices of buyers. These policies aim at learning the preference vectors of buyers in a robust way against the strategic behavior of buyers and meanwhile maximize the firm’s collected revenue.

The main insight behind the robustness property of our approach is that by an episodic design, we limit the long-term effect of each bid on the firm’s estimates of the preference vectors. Further, instead of using the bids (data) we use only the outcomes of auctions (censored data) in estimating preference vectors. Interestingly, we show that using this censored data does not hamper the learning rate while bringing in robustness property. As the granularity of real-time data increases at an unprecedented rate, we believe the ideas of this work can serve as a starting point for other complex dynamic contextual learning and decision making problems.

Acknowledgement

N.G. was supported in part by the Junior Faculty Research Assistance Program at MIT and a Google Faculty Research Award. A.J. was supported in part by an Outlier Research in Business (iORB) grant from the USC Marshall School of Business, a Google Faculty Research Award and the NSF CAREER Award DMS-1844481. A.J. would also like to acknowledge the financial support of the Office of the Provost at the University of Southern California through the Zumberge Fund Individual Grant Program.

Authors’ Biographies

Negin Golrezaei. Negin Golrezaei is an Assistant Professor of Operations Management at the MIT Sloan School of Management. Her current research interests are in the area of machine learning, statistical learning theory, mechanism design, and optimization algorithms with applications to revenue management, pricing, and online markets. Before joining MIT, Negin spent a year as a postdoctoral fellow at Google Research in New York where she worked with the Market Algorithm team to develop, design, and test new mechanisms and algorithms for online marketplaces. She is the recipient of several awards including the 2018 Google Faculty Research Award; 2017 George B. Dantzig Dissertation Award; the INFORMS Revenue Management and Pricing Section Dissertation Prize; University of Southern California (USC) Ph.D. Achievement Award (2017), and USC Provost’s Ph.D. Fellowship (2011). Negin received her BSc (2007) and MSc (2009) degrees in electrical engineering from the Sharif University of Technology, Iran, and a Ph.D. (2017) in operations research from USC.

Adel Javanmard. Adel Javanmard is an Assistant Professor in the department of Data Sciences and Operations, Marshall School of Business at the University of Southern California. He also holds a courtesy appointment in the Computer Science Department within the USC Viterbi School of Engineering. Prior to joining USC in 2015, he obtained his Ph.D. in Electrical Engineering from Stanford University, followed by a postdoc at UC Berkeley and Stanford, supported by a fellowship from the NSF Center for Science of Information. Before that, he received BSc degrees in Electrical Engineering and Pure Math from Sharif University of Technology in 2009. His research interests are broadly in the area of high-dimensional statistical inference, machine learning and optimization. Adel is the recipient of several awards and fellowships, including the NSF CAREER award (2019), the Outlier Research in Business Award (2018), Dr. Douglas Basil Award for Junior Business Faculty (2018), the Zumberge Faculty Research and Innovation Fund (2017), Google Faculty Research Award (2016), the Thomas Cover dissertation award from the IEEE Society (2015), the CSoI Postdoctoral Fellowship (2015), the Caroline and Fabian Pease Stanford Graduate Fellowship (2010-2012).

Vahab Mirrokni. Vahab Mirrokni is a distinguished scientist, heading the New York and Zurich algorithms research groups at Google Research. The group consists of three main sub-teams: market algorithms, large-scale graph mining, and large-scale optimization. He received his Ph.D. from MIT in 2005 and his B.Sc. from the Sharif University of Technology in 2001. He joined Google Research in 2008, after spending a couple of years at Microsoft Research, MIT and Amazon.com. He is the co-winner of paper awards at KDD’15, ACM EC’08, and SODA’05. His research areas include algorithms, distributed and stochastic optimization, and computational economics. Recently he has been working on various algorithmic problems in machine learning, online optimization and dynamic mechanism design, and distributed algorithms for large-scale graph mining.

References

- (1)

- Acquisti and Varian (2005) Alessandro Acquisti and Hal R Varian. 2005. Conditioning prices on purchase history. Marketing Science 24, 3 (2005), 367–381.

- Amin et al. (2013) Kareem Amin, Afshin Rostamizadeh, and Umar Syed. 2013. Learning prices for repeated auctions with strategic buyers. In Advances in Neural Information Processing Systems. 1169–1177.

- Amin et al. (2014) Kareem Amin, Afshin Rostamizadeh, and Umar Syed. 2014. Repeated contextual auctions with strategic buyers. In Advances in Neural Information Processing Systems. 622–630.

- Araman and Caldentey (2009) Victor F Araman and René Caldentey. 2009. Dynamic pricing for nonperishable products with demand learning. Operations research 57, 5 (2009), 1169–1188.

- Aviv and Pazgal (2008) Yossi Aviv and Amit Pazgal. 2008. Optimal pricing of seasonal products in the presence of forward-looking consumers. Manufacturing & Service Operations Management 10, 3 (2008), 339–359.

- Aviv et al. (2015) Yossi Aviv, Mingcheng Mike Wei, and Fuqiang Zhang. 2015. Responsive pricing of fashion products: The effects of demand learning and strategic consumer behavior. Technical Report. Working Paper, Washington University.

- Bagnoli and Bergstrom (2005) Mark Bagnoli and Ted Bergstrom. 2005. Log-concave probability and its applications. Economic theory 26, 2 (2005), 445–469.

- Ban and Keskin (2017) Gah-Yi Ban and N Bora Keskin. 2017. Personalized dynamic pricing with machine learning. (2017).

- Bastani and Bayati (2015) Hamsa Bastani and Mohsen Bayati. 2015. Online decision-making with high-dimensional covariates. (2015).

- Besbes and Lobel (2015) Omar Besbes and Ilan Lobel. 2015. Intertemporal price discrimination: Structure and computation of optimal policies. Management Science 61, 1 (2015), 92–110.

- Besbes and Zeevi (2009) Omar Besbes and Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57, 6 (2009), 1407–1420.

- Bikhchandani and McCardle (2012) Sushil Bikhchandani and Kevin McCardle. 2012. Behavior-based price discrimination by a patient seller. The BE Journal of Theoretical Economics 12, 1 (2012).

- Birge et al. (2018) John R Birge, Yifan Feng, N Bora Keskin, and Adam Schultz. 2018. Dynamic Learning and Market Making in Spread Betting Markets With Informed Bettors. Available at SSRN 3283392 (2018).

- Borgs et al. (2014) Christian Borgs, Ozan Candogan, Jennifer Chayes, Ilan Lobel, and Hamid Nazerzadeh. 2014. Optimal multiperiod pricing with service guarantees. Management Science 60, 7 (2014), 1792–1811.

- Braverman et al. (2017) Mark Braverman, Jieming Mao, Jon Schneider, and S Matthew Weinberg. 2017. Multi-armed bandit problems with strategic arms. arXiv preprint arXiv:1706.09060 (2017).

- Broder and Rusmevichientong (2012) Josef Broder and Paat Rusmevichientong. 2012. Dynamic pricing under a general parametric choice model. Operations Research 60, 4 (2012), 965–980.

- Cesa-Bianchi et al. (2015) Nicolo Cesa-Bianchi, Claudio Gentile, and Yishay Mansour. 2015. Regret minimization for reserve prices in second-price auctions. IEEE Transactions on Information Theory 61, 1 (2015), 549–564.

- Chen and Keskin (2018) Hongfan Chen and N Bora Keskin. 2018. Markdown Policies for Demand Learning and Strategic Customer Behavior. Available at SSRN 3299819 (2018).

- Chen et al. (2015) Xi Chen, Zachary Owen, Clark Pixton, and David Simchi-Levi. 2015. A statistical learning approach to personalization in revenue management. (2015).

- Cheung et al. (2017) Wang Chi Cheung, David Simchi-Levi, and He Wang. 2017. Dynamic pricing and demand learning with limited price experimentation. Operations Research 65, 6 (2017), 1722–1731.

- Cohen et al. (2016) Maxime Cohen, Ilan Lobel, and Renato Paes Leme. 2016. Feature-based dynamic pricing. (2016).

- den Boer (2015) Arnoud V den Boer. 2015. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20, 1 (2015), 1–18.

- den Boer and Zwart (2013) Arnoud V den Boer and Bert Zwart. 2013. Simultaneously learning and optimizing using controlled variance pricing. Management science 60, 3 (2013), 770–783.

- Edelman and Ostrovsky (2007) Benjamin Edelman and Michael Ostrovsky. 2007. Strategic bidder behavior in sponsored search auctions. Decision support systems 43, 1 (2007), 192–198.

- Esteves et al. (2009) Rosa Branca Esteves and others. 2009. A survey on the economics of behaviour-based price discrimination. Technical Report. NIPE-Universidade do Minho.

- Farias and Van Roy (2010) Vivek F Farias and Benjamin Van Roy. 2010. Dynamic pricing with a prior on market response. Operations Research 58, 1 (2010), 16–29.

- Ferreira et al. (2016) Kris Johnson Ferreira, David Simchi-Levi, and He Wang. 2016. Online network revenue management using Thompson sampling. (2016).

- Fudenberg and Villas-Boas (2006) Drew Fudenberg and J Miguel Villas-Boas. 2006. Behavior-based price discrimination and customer recognition. Handbook on economics and information systems 1 (2006), 377–436.

- Gill et al. (1995) Richard D Gill, Boris Y Levit, and others. 1995. Applications of the van Trees inequality: a Bayesian Cramér-Rao bound. Bernoulli 1, 1-2 (1995), 59–79.

- Goldenshluger and Zeevi (2013) Alexander Goldenshluger and Assaf Zeevi. 2013. A linear response bandit problem. Stochastic Systems 3, 1 (2013), 230–261.

- Golrezaei et al. (2017a) Negin Golrezaei, Max Lin, Vahab Mirrokni, and Hamid Nazerzadeh. 2017a. Boosted Second-price Auctions for Heterogeneous Bidders. (2017).