Binary Scoring Rules that Incentivize Precision

All proper scoring rules incentivize an expert to predict accurately (report their true estimate), but not all proper scoring rules equally incentivize precision. Rather than treating the expert’s belief as exogenously given, we consider a model where a rational expert can endogenously refine their belief by repeatedly paying a fixed cost, and is incentivized to do so by a proper scoring rule.

Specifically, our expert aims to predict the probability that a biased coin flipped tomorrow will land heads, and can flip the coin any number of times today at a cost of per flip. Our first main result defines an incentivization index for proper scoring rules, and proves that this index measures the expected error of the expert’s estimate (where the number of flips today is chosen adaptively to maximize the predictor’s expected payoff). Our second main result finds the unique scoring rule which optimizes the incentivization index over all proper scoring rules.

We also consider extensions to minimizing the moment of error, and again provide an incentivization index and optimal proper scoring rule. In some cases, the resulting scoring rule is differentiable, but not infinitely differentiable. In these cases, we further prove that the optimum can be uniformly approximated by polynomial scoring rules.

Finally, we compare common scoring rules via our measure, and include simulations confirming the relevance of our measure even in domains outside where it provably applies.

1 Introduction

In the context of decision theory, a scoring rule rewards predictors for the accuracy of their predictions [Goo52, Bri50, Sav71]. In the context of a binary choice (e.g. “Will it rain tomorrow?”), a scoring rule can be thought of as a function , where if a predictor reports a probability of rain, then the predictor’s reward is if it rains and if it does not rain.111To be clear: if and a predictor predicts a probability of to it raining, then the predictor receives reward if it rains and if it does not rain. We consider settings in which there are two possible outcomes that are treated symmetrically (as this definition assumes), and henceforth refer to scoring rules in terms of this function . Traditionally, scoring rules are concerned with incentivizing accurate reports. For example, a scoring rule is called proper if a predictor is always incentivized to tell the truth, in the sense that reporting the predictor’s true belief strictly maximizes the predictor’s expected reward.

Of course, there is an extraordinary amount of flexibility in selecting a proper scoring rule. For example, if a continuously differentiable scoring rule satisfies and for all , then is proper. Any increasing function on can therefore be extended to a proper scoring rule on (see Corollary 2.6). Much prior work exists comparing proper scoring rules by various measures, e.g. [Win+96, GR07, DM14], but there is little which formally analyzes the extent to which proper scoring rules incentivize precision (see Section 1.2 for a discussion of prior work).

As a motivating example, consider the problem of guessing the probability that one of two competing advertisements will be clicked. With zero effort, a predictor could blindly guess that each is equally likely. But the predictor is not exogenously endowed with this belief, they can also endogenously exert costly effort to refine their prediction. For example, the predictor could sample which ad they would click themselves, or poll members of their household for additional samples. A more ambitious predictor could run a crowdsourcing experiment, paying users to see which link they would click. Any proper scoring rule will equally incentivize the predictor to accurately report their resulting belief, but not all scoring rules equally incentivize the costly gathering of information.

We propose a simple model to formally measure the extent to which a scoring rule incentivizes costly refinement of the predictor’s beliefs. Specifically, we consider a two-sided coin that comes up heads with probability , and is drawn uniformly from (we refer to as the bias of the coin). Tomorrow the coin will be flipped, and we ask the predictor to guess the probability that it lands heads. Today, the predictor can flip the coin (with bias ) any number of times, at cost per flip. While we choose this model for its mathematical simplicity, it captures examples like the previous paragraph surprisingly well: tomorrow, a user will be shown the two advertisements (clicking one). Today, the predictor can run a crowdsourcing experiment and pay any number of workers to choose between the two ads. This simple model also captures weather forecasting using ensemble methods surprisingly well, and we expand on this connection in Appendix A.

With this model in mind, consider the following two extreme predictions: on one hand, the predictor could never flip the coin, and always output a guess of . On the other, the predictor could flip the coin infinitely many times to learn exactly, and output a guess of . Note that both predictions are accurate: the predictor is truthfully reporting their belief, and that belief is correct given the observed flips. However, the latter prediction is more precise. All proper scoring rules incentivize the predictor to accurately report their true prediction in both cases, but different scoring rules incentivize the predictor to flip the coin a different number of times. More specifically, every scoring rule induces a different optimization problem for the predictor, thereby leading them to produce predictions of different quality. In this model, the key question we answer is the following: which scoring rules best incentivize the predictor to produce a precise prediction?

1.1 Our Results

Our first main result is the existence of an incentivization index. Specifically, if denotes the expected error that a rational predictor makes when incentivized by scoring rule with cost per flip, we give a closed-form index with the following remarkable property: for all respectful (see Definition 3.1) proper scoring rules and , the inequality implies the existence of a sufficiently small such that for all (Theorem 3.3). We formally introduce this index in Definition 3.2, but remark here that it is not a priori clear that such an index should exist at all, let alone that it should have a closed form.222Indeed, a priori it is possible that , but , and , but , and so on. The existence of an incentivization index rules out this possibility.

With an index in hand, we can now pose a well-defined optimization problem: which proper scoring rule minimizes the incentivization index? Our second main result nails down this scoring rule precisely; we call it (see Theorem 4.1).

We also extend our results to the moment for , where now denotes the expected power of the error that a rational predictor makes when incentivized by with cost per flip, and again derive an incentivization index and an optimal scoring rule .

Some optimal rules have a particularly nice closed form (for example, as , the optimal rule pointwise converges to a polynomial), but many do not. We also prove, using techniques similar to the Weierstrass approximation theorem [Wei85], that each of these rules can be approximated by polynomial scoring rules whose incentivization indices approach the optimum.

Finally, beyond characterizing the optimal rules, the incentivization indices themselves allow for comparison among popular scoring rules, such as logarithmic (), quadratic (), and spherical (). We plot the predictions made by our incentivization index (which provably binds only as ) for various values of , and also confirm via simulation that the index has bite for reasonable choices of .

1.2 Related Work

To the best of our knowledge, [Osb89] was the first to consider scoring rules as motivating the predictor to seek additional information about the distribution before reporting their belief. This direction is revisited in work of [Cle02], and has gained more attention recently [Tsa19, RS17, Har+20]. While these works (and ours) each study the same phenomenon, there is little technical overlap and the models are distinct: each explores a different aspect of this broad agenda. For example, [RS17] considers the predictor’s incentive to outperform competing predictors (but there is no costly effort — the predictors’ beliefs are still exogenous). [Har+20] (which is contemporaneous and independent of our work) is the most similar in motivation, but still has significant technical differences (beyond the two subsequent examples). On one hand, their model is more general than ours in that they consider multi-dimensional state spaces (rather than binary ones, in our model). On another hand, it is more restrictive in that they consider only two levels of effort (versus infinitely many, in our model).

Our work also fits into the broad category of principal-agent problems. For example, works such as [CDP15, LC16, Che+18, CZ19] consider a learning principal who incentivizes agents to make costly effort and produce an accurate data point. Again, the models are fairly distinct, as these works focus on more sophisticated learning problems (e.g. regression), whereas we perform a more comprehensive dive into the problem of simply eliciting the (incentivized-to-be-precise) belief.

In summary, there is a sparse, but growing, body of work addressing the study of incentivizing effort in forming predictions, rather than just accuracy in reporting them. The above-referenced works pose various models to tackle different aspects of this agenda. In comparison, our model is arguably the simplest, and we develop a deep understanding of optimal scoring rules in this setting.

1.3 Summary and Roadmap

Section 2 lays out our model, and contains some basic facts to help build intuition for reasoning about the incentivization properties of scoring rules. Our main results are detailed in Sections 3 through 6, along with intuition for our techniques.

-

•

Section 3 defines the incentivization index, and provides a sufficient condition (Definition 3.1) for the incentivization index to nail down the expected error of a rational predictor, up to . This is our first main result, which gives a framework to formally reason about scoring rules that incentivize precision.

-

•

Section 4 finds the unique proper scoring rule which optimizes the incentivization index. This is our second main result, which finds novel scoring rules, and also sets a benchmark with which to evaluate commonly-studied scoring rules.

- •

-

•

Section 6 proves that there exist polynomial scoring rules with incentivization indices arbitrarily close to the optimum.

-

•

All sections additionally consider the expected power of the error for any .

-

•

Section 7 concludes.

2 Model and Preliminaries

2.1 Scoring Rules and their Rewards

This paper considers predicting a binary outcome for tomorrow: heads or tails. The expert or predictor is asked to output a probability with which they believe the coin will land heads. Tomorrow, should the coin land heads, their reward is ; should it not, their reward is (note that the reward is symmetric: it is invariant under swapping the labels ‘heads’ and ‘tails’). Throughout this paper, we consider a scoring rule to be defined by this function . Observe that if the expert believes the true probability of heads to be , and chooses to guess , then the expected reward is .

Definition 2.1 (Expected Reward).

For scoring rule , denote by the expected reward of an expert who predicts when their true belief is .

Let also be the expected reward of an expert who reports their true belief . We may drop the superscript when the scoring rule is clear from context.

A scoring rule is (weakly) proper if it (weakly) incentivizes accurate reporting. In our notation:

Definition 2.2.

A scoring rule is proper (resp. weakly proper) if for all , the expected reward function is strictly (resp. weakly) maximal at on .

Note that the optimal scoring rules designed in this paper are all (strictly) proper. However, we will show them to be optimal even with respect to the larger class of weakly proper scoring rules.

2.2 Modeling the Expert’s Behavior

We model the expert as Bayesian. Specifically, the expert initially believes the coin bias is uniformly distributed in . Today, the expert may flip the coin any number of times in order to gauge its true bias, and pays per flip. After having flipped the coin times, and seen heads, the expert believes the true bias is (Fact C.2).333By this, we mean the expert believes the coin would land heads with probability , if it were flipped again. Once done flipping, the expert reports the coin bias. Tomorrow, the coin is flipped once, and the expert receives reward for the prediction based on the outcome via scoring rule (known to the expert in advance), as described in Section 2.1.

It remains to define when the expert should stop flipping. Below, an adaptive strategy simply refers to a (possibly randomized) stopping rule for the expert, i.e. a rule that, given any number of past flips and the scoring rule , tells the expert whether to stop or flip once again. The payoff of an adaptive strategy is simply the expert’s expected reward for following that strategy, minus the expected number of coin flips.

Definition 2.3.

A globally-adaptive expert uses the payoff-maximizing adaptive strategy.

Nailing down the expert’s optimal behavior as a function of is quite unwieldy. Thus, we derive our characterizations up to terms (as ). When is large, one may reasonably worry that these terms render our theoretical results irrelevant. In Appendix H we simulate the expert’s optimal behavior for large , and confirm that our results hold qualitatively in this regime.

Finally, we define a natural measure of precision for the expert’s prediction.

Definition 2.4.

The expected error associated with a scoring rule and cost is . The expectation is taken over , drawn uniformly from , and , the prediction of a globally-adaptive expert after flipping the coin ( is a random variable which depends on ).

We will also consider generalizations to other moments, and define .

2.3 Scoring Rule Preliminaries

Our proofs will make use of fairly heavy single-variable analysis, and therefore will require making some assumptions on : continuity, differentiability, but also more technical ones. We will clearly state them when necessary, and confirm that all scoring rules of interest satisfy them. For these preliminaries, we need only assume that is continuously differentiable so that everything which follows is well-defined. First, Lemma 2.5 provides an alternative characterization of proper (and weakly proper) scoring rules. The proof is in Appendix C.

Lemma 2.5.

A continuously differentiable scoring rule is weakly proper if and only if for all , and . It is (strictly) proper if and only if additionally almost everywhere444Almost everywhere on refers to the interval except a set of measure zero. in .

Corollary 2.6.

Let be strictly increasing almost everywhere (resp., nondecreasing everywhere) and continuously differentiable on . Then can be extended to a continuously differentiable proper (resp., weakly proper) scoring rule on by defining for .

2.4 First Steps towards Understanding Incentivization

In this section, we state a few basic facts about the expert’s expected reward, and how it changes with additional flips. We defer all proofs to Appendix C. Reading these proofs may help a reader gain technical intuition for the model. Our analysis will focus mostly on the reward function rather than , so the following fact will be useful:

Fact 2.7.

For a weakly proper scoring rule , we have and on .

Lemma 2.8 observes how this expected reward evolves with an additional flip.

Lemma 2.8.

If the expert has already flipped the coin times, seeing heads, then their expected increase in reward for exactly one additional flip is .

Lemma 2.8 suggests that the function should be convex: if it were not, that would leave open the possibility of the expert potentially losing expected reward as a result of performing more flips (meaning that the expert might get a smaller reward for a better estimate of the coin bias).

Lemma 2.9 ([McC56]).

Let be any proper (resp., weakly proper) scoring rule. Then is strictly convex (resp., weakly convex) almost everywhere on .

Corollary 2.10.

Let be a proper (resp., weakly proper) scoring rule. Then the expert’s increased expected reward from an additional flip is strictly positive (resp., weakly positive).

Because we are interested in incentivizing the expert to take costly actions, the scale of a proper scoring rule will also be relevant. For example, if is proper, then so is , and clearly does a better job of incentivizing the expert (Lemma 2.8). As such, we will want to first normalize any scoring rule under consideration to be on the same scale. A natural normalization is to consider two scoring rules to be on the same scale if expected payoff they provide to the expert is the same (where the expectation is taken over both the bias and the flips of the coin).

Definition 2.11.

We define to be the expected payoff to a globally-adaptive expert via scoring rule (when the bias is drawn uniformly from , and the expert may pay per flip).

Recall that the (expected) payoff of a perfect expert is , since a perfect expert has expected payoff if the coin has bias , and the coin’s bias is chosen uniformly from . For proper (but not necessarily weakly proper) scoring rules, we show that as the expected payoff of a globally-adaptive expert approaches the payoff of a perfect expert. (This is true no matter the coin’s bias, though we only need this result in expectation over the bias.) Intuitively, this is because the number of flips approaches as , so the expert is rewarded as if they are perfect.

Proposition 2.12.

Let be a proper scoring rule. Then . That is, .

Assuming that two scoring rules have addresses one potential scaling issue. But there is another issue as well: whenever is proper, the scoring rule is also proper, and again clearly does a better job incentivizing the expert (again directly by Lemma 2.8). As such, we will also normalize so that for all : the expert’s expected reward is always non-negative if they are perfect. We conclude this section with a formal statement of this normalization. Appendix C confirms the implications of the definition, and also contains a few lemmas stating equivalent conditions.

Definition 2.13.

A scoring rule is normalized if , and . This implies that , and that a perfectly calibrated expert gets non-negative expected reward. It also implies that an expert who flips zero coins gets zero expected reward.

3 An Incentivization Index

This section presents our first main contribution: an incentivization index which characterizes the expert’s expected error. The main result of this section, Theorem 3.3, requires scoring rules to be analytically nice in a specific way. We term such scoring rules respectful.

Definition 3.1.

A proper scoring rule with reward function is respectful if:

-

(1)

is strongly convex on . That is, on for some .

-

(2)

is Riemann integrable on any closed subinterval of .555Note this does not necessarily require be defined on the entire , just that it is defined almost everywhere.

-

(3)

, and s.th. for all : on .666Except in places where is undefined.

Recall that is strictly convex for any strictly proper scoring rule, so strong convexity is a minor condition. Likewise, the second condition is a minor “niceness” assumption. We elaborate on the third condition in detail in Appendix D, and confirm that frequently used proper scoring rules are indeed respectful. We briefly note here that intuitively, the third condition asserts that does not change too quickly (except possibly near zero and one) for small enough coin-flipping costs . The particular choice of is not special, and could be replaced with any constant .

Definition 3.2 (Incentivization Index).

We define the incentivization index of a scoring rule :

Theorem 3.3.

If is a respectful, continuously differentiable proper scoring rule, then:

More generally, if is the moment of the standard normal distribution, then:

Intuitively, the incentivization index captures the expert’s error as .777Proposition 3.9 in Section 3.4 gives intuition for why is proportional to . More formally, for any two respectful proper scoring rules , implies that there exists a sufficiently small such that for all . As previously referenced, Theorem 3.3 says nothing about how big or small this might be, although simulations in Appendix H confirm that it does not appear to be too small for typical scoring rules.

The rest of this section is organized as follows. Sections 3.1 through 3.6 outline our proof of Theorem 3.3. The key steps are given as precisely-stated technical lemmas with mathematical intuition alongside them, to illustrate where precision is needed for the proof to carry through. Complete proofs of these lemmas can be found in Appendix E. In Appendix D, we confirm that natural scoring rules are respectful (which is mostly a matter of validating the third condition in Definition 3.1).

3.1 Proof Outline of Theorem 3.3

We provide below an executive overview of our approach. The concrete steps are separated out as formally-stated technical lemmas in the following sections, with proofs deferred to Appendix E. Before beginning, we highlight the main challenge: to prove Theorem 3.3, we need to capture the precise asymptotics of the expert’s expected error. Upper bounds can be easily shown via concentration inequalities; however, traditional lower bounds via anti-concentration results would simply state that the expected error tends to as (which holds for every proper scoring rule, and doesn’t distinguish among them). So not only are we looking for two-sided bounds on the error, but we need to gauge the precise rate at which it approaches zero. Moreover, even obtaining the order of magnitude of the error as , which turns out to be , still does not suffice: we need to compute the exact coefficient of . This difficulty motivates the need for the technical lemmas stated in this section to be very precise. Our outline is as follows:

-

•

All of our analysis first considers a locally-adaptive expert, who flips the coin one additional time if and only if the expected increase in reward from that single flip exceeds .

-

•

Our first key step, Section 3.2, provides an asymptotic lower bound on the number of times an expert flips the coin, for all respectful .

-

•

Our second key step, Section 3.3, provides a coupling of the expert’s flips across all possible true biases . This helps prove uniform convergence bounds over all for the expert’s error: we can now define an unlikely “bad” event of overly-slow convergence without reference to .

-

•

Our third key step, Section 3.4, provides tight bounds on the number of flips by a locally-adaptive expert, up to factors. Note that the first three steps have not referenced an error measure at all, and only discuss the expert’s behavior.

- •

-

•

Finally our last step, Section 3.6, shows that the globally-adaptive expert behaves nearly-identically to the locally-adaptive expert, up to an additional factor of flips.

We now proceed to formally state the main steps along this outline, recalling that the first several steps consider a locally-adaptive expert, whose definition is restated formally below:

Definition 3.4 (Locally-Adaptive Expert).

The locally-adaptive expert flips one more time if and only if making a single additional coin flip (and then stopping) increases their expected payoff.

3.2 Step One: Lower Bounding Expert’s Number of Flips

We begin by tying the expert’s expected marginal reward from one additional flip to . Below, denotes the random variable which is the expert’s belief after flips. The important takeaway from Claim 3.5 is that for fixed , the expert’s expected belief as a function of changes (roughly) as — this takeaway will appear in later sections.

Claim 3.5.

Let be the expected increase in the expert’s reward (not counting the paid cost ) from the flip of the coin, given current belief . Then there exist such that:

Recalling that the locally-adaptive expert decides to flip the coin for the time if and only if , and assuming that is bounded away from zero (Condition 1 in Definition 3.1), we arrive at a simple lower bound on the number of coin flips.

Claim 3.6.

For all such that is bounded away from zero, there exists such that the expert is guaranteed to flip the coin at least times for all (no matter the true bias).

3.3 Step Two: Ruling Out Irregular Coin-Flipping Trajectories

The expert’s coin-flipping behavior depends on , which depends on the fraction of realized coin flips which are heads, which itself depend on the coin’s true bias . Note, of course, that as . If instead we had that exactly, we could leverage Claim 3.5 to better understand the number of flips as a function of . Unfortunately, will not equal exactly, and it is even possible to have far from , albeit with low probability.

The challenge, then, is then how to handle these low-probability events, and importantly how to do so uniformly over . To this end, we consider the following coupling of coin-flipping processes over all possible biases. Specifically, rather than first drawing bias and then flipping coins with bias , we use the following identically distributed procedure:

-

(1)

Generate an infinite sequence of uniformly random numbers in .

-

(2)

Choose uniformly at random from .

-

(3)

For each , coin comes up heads if and only if .

Under this sampling procedure, is the expert’s estimate after flipping coins, where is the number of heads in the first flips, if is the value chosen in step (2).

With this procedure, we can now define a single bad event uniformly over all . Intuitively, holds when, no matter what is chosen in step (2), the expert’s Bayesian estimate of never strays too far from after flips. More formally, the complement of is our single bad event:

The expression on the right-hand side of the inequality can be rewritten as , where the radical term gives the order of the expected difference between and . So intuitively, holds unless the actual difference between and far exceeds its expected value.

We have defined so that, on the one hand, our subsequent analysis becomes tractable when holds, and on the other hand, fails to hold with probability small enough that our asymptotic results are not affected. Below, Claim 3.7 gives the property we desire from , and Claim 3.8 shows that is unlikely. The key takeaway from Claim 3.7 is that when holds, the expert’s prediction is close to for all and and this closeness shrinks with .

Claim 3.7.

The exists a sufficiently large such that for all : if holds, then

Claim 3.8.

3.4 Step Three: Tightly Bounding Expert’s Number of Flips

We now nail down the precise asymptotics of the number of the expert’s flips as a function of the true bias . This becomes significantly more tractable after assuming holds. Below, the random variable denotes the number of flips that a locally-adaptive expert chooses to make.

Proposition 3.9.

Assume that holds for some , and let be as in Definition 3.1. There exists a constant and cost such that for all and all , we have

3.5 Step Four: Translating Number-of-Flips Bounds to Error Bounds

Having pinned down quite precisely, we will now obtain a tight bound on the error of the locally-adaptive expert’s reported prediction. By contrast, the previous three steps performed an analysis of the locally-adaptive expert’s coin-flipping behavior, which does not depend on the choice of error metric. Lemma 3.10 below is a formal statement of the main step of this process, which nails down the asymptotics of the error conditioned on . Below, denotes a random variable equal to the locally-adaptive expert’s error when the cost is and the true bias is (and the scoring rule is implicit).

Lemma 3.10.

Let and be the moment of a standard Gaussian. Let (so is implicitly a function of ). For all we have

where the term is a function of (but not ) that approaches zero as approaches zero.

Lemma 3.10 is the key, but far from only, step in translating Proposition 3.9 to tight bounds on the locally-adaptive expert’s error. Intuitively, it states that the value of the expert’s error will be, up to a factor, consistent with what one would expect from using a quantitative central limit theorem in conjunction with the bound on from Proposition 3.9.

3.6 Step Five: From Locally-Adaptive to Globally-Adaptive Behavior

Finally, we extend our previous analysis from locally-adaptive to globally-adaptive experts. In particular, for a scoring rule that gives finite expected reward to a perfect expert, we prove that the globally-adaptive expert does not flip significantly more than a locally-adaptive expert would, and therefore their achieved errors are equal up to a factor. Below, the random variable denotes the number of flips by the globally-adaptive expert.

Lemma 3.11.

Assume is respectful and normalizable (i.e. ). Let be as in Proposition 3.9. There exists a , such that for all : If holds and , then

Lemma 3.11 is the key step in this portion of the analysis. The remaining work is to bound the impact of negligible events (such as failing, or being extremely close to or ) on our analysis. This completes our outline of the proof of Theorem 3.3 (and we refer the reader back to Section 3.1 for a reminder of this outline).

4 Finding Optimal Scoring Rules

Now that we have shown that the incentivization index characterizes how well any respectful scoring rule incentivizes a globally-adaptive expert to minimize error, we have a well-defined optimization problem: which normalized proper scoring rule has the lowest incentivization index (and therefore minimizes the expert’s expected error)? Recall the following necessary and sufficient set of conditions for a continuously differentiable and normalized scoring rule to be weakly proper:888Including weakly proper scoring rules in our optimization domain makes the analysis simpler. The optimal scoring rules are in fact strictly proper.

-

•

(Lemma 2.5) For all , and .

- •

- •

So our goal is just to find the scoring rule which satisfies these constraints and minimizes the incentivization index:

The main result of this section is the following theorem:

Theorem 4.1.

The unique continuously differentiable normalized proper scoring rule which minimizes is:

While is certainly challenging to parse, importantly it is a closed form, and can thus be numerically evaluated (and, it is provably optimal). A complete proof of Theorem 4.1 appears in Appendix F. Appendix B contains several plots of these scoring rules, alongside traditional ones. Section 5 immediately below also gives further discussion of these rules.

5 Comparing Scoring Rules

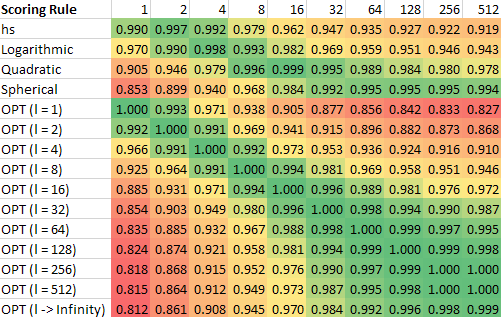

In this section we compare various scoring rules by their incentivization indices, for various values of . Of particular interest are the values (expected absolute error), (expected squared error), and the limit as (which penalizes bigger errors “infinitely more” than smaller ones, so this regime corresponds to minimizing the probability of being very far off).

5.1 Optimal Scoring Rules for Particular Values of

We begin by noting some values of for which the function takes a nice closed form. happens to not be one such value. For , the functions can be written in terms of elementary functions on the entire interval . For , the closed form on is a polynomial, although its extension via Corollary 2.6 to is not. For , the closed form on both and is a polynomial, although they are different. Interestingly, as , the closed form converges pointwise to a single polynomial. Specifically, for these values of :

For : On , we have

For : On , we have

and on , we have

Finally, as : on the entire interval , pointwise converges to

We refer to this last rule as . Intuitively, minimizing the expected value of error raised to a power that approaches infinity punishes any error infinitely more than an even slightly smaller error. Put otherwise, this metric judges a scoring rule by the maximum (over ) of the spread of the distribution of expert error. The scoring rule has a very special property, which is that the quantity , which appears in the incentivization index, is a constant regardless of . This means that, in the limit as , the distribution of the expert’s error is the same regardless of . It makes intuitive sense that making the spread of the distribution of expert error uniform over all also minimizes the maximum of these spreads, which explains why has this interesting property.

As some of these rules are not infinitely differentiable, a natural question to ask is: what infinitely differentiable normalized function minimizes ? While (as we have shown by virtue of being the unique minimizer) achieving an incentivization index equal to with an infinitely differentiable scoring rule is impossible, it turns out that it is possible to get arbitrarily close — and in fact it is possible to get arbitrarily close with polynomial scoring rules. The main idea of the proof is to use the Weierstrass approximation theorem to approximate with polynomials. See Section 6 for a full proof.

5.2 Comparison of Incentivization Indices of Scoring Rules

We compare commonly studied scoring rules such as quadratic, logarithmic, and spherical, and refer to their normalizations as , respectively. Additionally we include for comparison the normalization of the scoring rule, defined as . This scoring rule was prominently used in [BB20] to prove their minimax theorem for randomized algorithms.

Figure 1 states for various scoring rules (the lower the better).

| 0.260 | 0.0732 | 0.00644 | |

| 0.279 | 0.0802 | 0.00694 | |

| 0.296 | 0.0889 | 0.00819 | |

| 0.255 | 0.0723 | 0.00658 | |

| 0.253 | 0.0728 | 0.00719 | |

| 0.255 | 0.0718 | 0.00661 | |

| 0.261 | 0.0732 | 0.00639 | |

| 0.311 | 0.0968 | 0.00974 |

Figure 1 lets us compare the performance of various scoring rules by our metric for any particular value of . However, as one can see, decreases as increases. This makes sense, since measures the expected -th power of error. For this reason, if we wish to describe how a given scoring rule performs over a range of values of , we need to normalize these values. We do so by taking the -th root and dividing these values by the -th root of the optimal (smallest) index (and take the inverse so that larger numbers are better). This gives us the following measure of scoring rule precision, which makes sense across different values of :

Figure 2, which evaluates this expression for a selection of scoring rules and values of , reveals some interesting patterns. Of the hs, logarithmic, quadratic, and spherical scoring rules, the hs scoring rule is the best one for the smallest values of and is in fact near-optimal for . The logarithmic rule is the best one for somewhat larger values of and is in near-optimal for . For larger values of , the quadratic scoring rule is best, and is near-optimal for . For even larger values of , the spherical scoring rule is the best of the four. This pattern suggests that for any given proper scoring rule there is a trade-off between incentivizing precision at low and at high values of ; it would be interesting to explore this further.

Below is a continuous version of Figure 2. The chart shows how the numbers above vary as ranges from to .

![[Uncaptioned image]](/html/2002.10669/assets/Comparison_200.png)

And below is a zoomed-in version where ranges from to .

![[Uncaptioned image]](/html/2002.10669/assets/Comparison_10.png)

6 Almost-Optimal Incentivization Indices with Polynomial Respectful Scoring Rules

The main result of this section is the following theorem, stating that polynomial,999To be clear, when we say a scoring rule is polynomial, we mean simply that is a polynomial function. respectful proper scoring rules suffice to get arbitrarily close to the optimal incentivization index.

Theorem 6.1.

For and , there exists a respectful polynomial normalized proper scoring rule satisfying .

The proof of Theorem 6.1 uses ideas from the Weierstrass approximation theorem. However, the Weierstrass approximation theorem gives a particular measure of “distance” between two functions, which does not translate to these functions having similar incentivization indices. So one challenge of the proof is ensuring convergence of a sequence of polynomials to in a measure related to . A second challenge is to ensure that all polynomials in this sequence are themselves proper, respectful scoring rules. Like previous technical sections, we include a few concrete lemmas to give a sense of our proof outline.

For example, one step in our proof is to characterize all analytic proper scoring rules (that is, proper scoring rules that have a Taylor expansion which converges on their entire domain ). A necessary condition to be analytic is to be infinitely differentiable, which rules of the form are not, for any fixed . We therefore seek to approximate such scoring rules with polynomial scoring rules (which are analytic), which are also respectful and proper.

Theorem 6.2.

Let be analytic. Then is a proper scoring rule if and only if is nonconstant, everywhere, and

for some .

As an example to help parse Theorem 6.2, the quadratic scoring rule has , and for all other . Using Theorem 6.2, we can conclude the following about for any proper scoring rule :

Lemma 6.3.

Let be analytic. Then is a proper scoring rule if and only if is not uniformly zero, nonnegative everywhere, and can be written as

Lemma 6.3 provides clean conditions on what functions are safe to use in our sequence of approximations, and our proof follows by following a Weierstrass approximation-type argument while keeping track of these conditions. The rest of the details for the proof of Theorem 6.1 can be found in Appendix G.

7 Conclusion

We propose a simple model, where an expert can expend costly effort to refine their prediction, and study the effectiveness of different scoring rules in incentivizing the expert to form a precise belief. Our first main result (Theorem 3.3) identifies the existence of a closed-form incentivization index: scoring rules with a lower index incentivize the expert to be more accurate. Our second main result (Theorem 4.1) identifies the unique optimal scoring rule with respect to this index. Section 5 then uses the incentivization index to compare common scoring rules (including our newly-found optimal ones), and Section 6 shows that one can get arbitrarily close to the optimal incentivization index with polynomial scoring rules.

Our model is mathematically simple to describe, and yet it captures realistic settings surprisingly well (see Section 1 and Appendix A). As such, there are many interesting directions for future work. For example:

-

•

Our work considers a globally-adaptive expert, and establishes that they behave nearly identically to a locally-adaptive expert. What about a non-adaptive expert, who must decide a priori how many flips to make before seeing their results?

-

•

Our work considers a principal who wishes to minimize expected error. What if instead the principal wishes to optimize other objectives? In particular, are there objectives that are optimized by simpler rules (such as quadratic, logarithmic, etc.)?

-

•

Our work considers optimal scoring rules for the incentivization index, and shows that polynomial scoring rules approach the optimum. Do exceptionally simple scoring rules (such as quadratic, logarithmic, etc.) guarantee a good approximation to the optimal incentivization index for all ?

References

- [BB20] Shalev Ben-David and Eric Blais “A New Minimax Theorem for Randomized Algorithms” In CoRR abs/2002.10802, 2020 arXiv: https://arxiv.org/abs/2002.10802

- [Bri50] Glenn W. Brier “Verification of Forecasts Expressed in Terms of Probability” In Monthly Weather Review 78.1, 1950, pp. 1–3

- [CDP15] Yang Cai, Constantinos Daskalakis and Christos H. Papadimitriou “Optimum Statistical Estimation with Strategic Data Sources” In Proceedings of The 28th Conference on Learning Theory, COLT 2015, Paris, France, July 3-6, 2015, 2015, pp. 280–296 URL: http://proceedings.mlr.press/v40/Cai15.html

- [Che+18] Yiling Chen, Nicole Immorlica, Brendan Lucier, Vasilis Syrgkanis and Juba Ziani “Optimal Data Acquisition for Statistical Estimation” In Proceedings of the 2018 ACM Conference on Economics and Computation, Ithaca, NY, USA, June 18-22, 2018 ACM, 2018, pp. 27–44 DOI: 10.1145/3219166.3219195

- [Cle02] Robert T. Clemen “Incentive contracts and strictly proper scoring rules” In Test 11.1, 2002, pp. 167–189

- [CZ19] Yiling Chen and Shuran Zheng “Prior-free Data Acquisition for Accurate Statistical Estimation” In Proceedings of the 2019 ACM Conference on Economics and Computation, EC 2019, Phoenix, AZ, USA, June 24-28, 2019 ACM, 2019, pp. 659–677 DOI: 10.1145/3328526.3329564

- [DM14] Alexander Philip Dawid and Monica Musio “Theory and applications of proper scoring rules” In METRON 72.2, 2014, pp. 169–183

- [Est98] D. Estep “Practical Analysis in One Variable”, Undergraduate Texts in Mathematics New York: Springer, 1998

- [GBR07] Tilmann Gneiting, Fadoua Balabdaoui and Adrian E. Raftery “Probabilistic forecasts, calibration and sharpness” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 69, 2007, pp. 243–268

- [Goo52] I.. Good “Rational Decisions” In Journal of the Royal Statistical Society: Series B (Methodological) 14.1, 1952, pp. 107–114

- [GR05] Tilmann Gneiting and Adrian E Raftery “Atmospheric science. Weather forecasting with ensemble methods.” In Science (New York, N.Y.) 310.5746, 2005, pp. 248–9

- [GR07] Tilmann Gneiting and Adrian E Raftery “Strictly Proper Scoring Rules, Prediction, and Estimation” In Journal of the American Statistical Association 102.477 Taylor & Francis, 2007, pp. 359–378

- [Har+20] Jason D. Hartline, Yingkai Li, Liren Shan and Yifan Wu “Optimization of Scoring Rules” In CoRR abs/2007.02905, 2020 arXiv: https://arxiv.org/abs/2007.02905

- [LC16] Yang Liu and Yiling Chen “A Bandit Framework for Strategic Regression” In Advances in Neural Information Processing Systems 29: Annual Conference on Neural Information Processing Systems 2016, December 5-10, 2016, Barcelona, Spain, 2016, pp. 1813–1821 URL: http://papers.nips.cc/paper/6190-a-bandit-framework-for-strategic-regression

- [McC56] J McCarthy “Measures of the Value of Information” In Proceedings of the National Academy of Sciences of the United States of America 42.9, 1956, pp. 654–5

- [Osb89] Kent Osband “Optimal Forecasting Incentives” In Journal of Political Economy 97.5, 1989, pp. 1091–1112

- [RS17] Tim Roughgarden and Okke Schrijvers “Online Prediction with Selfish Experts” In Advances in Neural Information Processing Systems 30: Annual Conference on Neural Information Processing Systems 2017, 4-9 December 2017, Long Beach, CA, USA, 2017, pp. 1300–1310 URL: http://papers.nips.cc/paper/6729-online-prediction-with-selfish-experts

- [Sav71] Leonard J. Savage “Elicitation of Personal Probabilities and Expectations” In Journal of the American Statistical Association 66.336 [American Statistical Association, Taylor & Francis, Ltd.], 1971, pp. 783–801

- [Tsa19] Elias Tsakas “Robust Scoring Rules” In SSRN, 2019

- [Tsa88] Constantino Tsallis “Possible generalization of Boltzmann-Gibbs statistics” In Journal of Statistical Physics 52.1, 1988, pp. 479–487 DOI: 10.1007/BF01016429

- [Wei85] K. Weierstrass “Über die analytische Darstellbarkeit sogenannter willkürlicher Functionen einer reellen Veränderlichen” In Verl. d. Kgl. Akad. d. Wiss. Berlin 2, 1885, pp. 633–639

- [Win+96] R.. Winkler, Javier Muñoz, José L. Cervera, José M. Bernardo, Gail Blattenberger, Joseph B. Kadane, Dennis V. Lindley, Allan H. Murphy, Robert M. Oliver and David Ríos-Insua “Scoring rules and the evaluation of probabilities” In Test 5.1, 1996, pp. 1–60

Appendix A Relationship of Model to Ensemble Weather Forecasts

A major shift occurred in the field of weather forecasting around the turn of the 21st century. In the previous century, weather forecasting was viewed as inherently deterministic: a forecasting model would take as input some initial conditions and use differential equations to simulate future states of the atmosphere. A major complication of this approach, however, was that initial conditions are not perfectly known. While many weather stations observe conditions throughout the Earth, the chaotic nature of atmospheric phenomena meant that even small inaccuracies in initial conditions would produce substantial forecast inaccuracies even a few days into the future.

Starting in the early 1990s and continuing into the early 2000s, there was a paradigm shift away from deterministic forecasts and toward forecasts based on ensembles. An ensemble is a run of a forecast model based on a perturbed set of initial conditions. Instead of making simulating the atmosphere starting from one “best guess” set of initial conditions, ensemble-based forecasts would run some number — generally between 5 and 100 — ensembles, and use the results of these ensemble runs to generate a forecast [GR05].

The initial conditions used in ensemble models are typically chosen by “ensemble prediction systems,” which attempt to sample the conditions from a probability distribution based on real-world uncertainty. The forecasts generated by ensemble models can treated as a sample from the probability distribution over the future weather. For instance, if 60% of ensembles produce rain in New York seven days from now, a model might estimate the chance of rain in New York seven days from now at 60%, perhaps slightly adjusted based on a prior inferred from historical climate data [GBR07].

Each ensemble can be thought of as a coin flip whose cost is measured in time, energy, or computational resources. Each additional ensemble has a constant cost. The final forecast for a weather event is (roughly speaking) the fraction of ensembles that showed the event occurring. In this way, ensemble-based weather forecasting strongly parallels our coin flip based model of expert learning.

Appendix B Plots of Some Relevant Scoring Rules

Below is a plot of for .

![[Uncaptioned image]](/html/2002.10669/assets/Opt_g_Comparison.png)

As demonstrated by the plot, optimal scoring rules for larger values of are “flatter,” choosing to sacrifice rewarding precision near and , in favor of rewarding precision closer to . An expert rewarded by does not particularly care to distinguish between 98% and 99% probabilities, since the scoring rule is basically flat near the tails; this is not the case for . Conversely, because is steeper than near , an expert cares more about differentiating between a 50% and a 51% chance if rewarded with than with .

Another, perhaps more enlightening way to view these scoring rules is through the quantity . Up to a constant factor depending on the cost of a flip, this is the variance of the normal distribution that approximates the distribution of the expert’s response if the true bias of the coin is (for small ) — or, put otherwise, the expected squared error. Below is a plot of this quantity for a variety of the scoring rules we have discussed.

![[Uncaptioned image]](/html/2002.10669/assets/Opt_g_Variance_Comparison.png)

This reinforces our previous point: optimal rules for small value of result in very small errors near and , but relatively large errors in the middle. In Section 5.1, we discussed in brief why it makes sense that the value of is constant for the scoring rule . This chart reinforces the point: since our normalization constraints force a trade-off between minimizing expert error for different values of the coin’s bias , the scoring rule whose error is independent of will have the minimum possible value of the maximum error over all .

Finally, below is a plot like the previous one, but including the (normalized) logarithmic, quadratic, and spherical rules.

![[Uncaptioned image]](/html/2002.10669/assets/g_Variance_Comparison.png)

In Section 5.2, we noted that the logarithmic rule is near-optimal for , the quadratic rule for , and the spherical rule for even larger . This plot helps provide some intuition: the log scoring rule is similar in shape to and similarly for the quadratic scoring rule and , and for the spherical scoring rule and .

Appendix C Omitted Proofs from Section 2

C.1 Some Mathematical Preliminaries

We will use the following mathematical facts throughout our proofs, and include them here for reference.

Fact C.1.

.

Proof.

Consider computing the probability of the following event in two different ways: there are values drawn independently and uniformly at random from , . The event occurs if and only if the first elements are all smaller than the , which is smaller than all of the last elements.

One way to compute this probability is to first sample uniformly from , and then compute the probability that each of the first elements are all smaller, and each of the last are all larger. This probability is exactly .

Another way is to first draw the values, and then sample a random permutation to map them to . Then for any values, the event occurs if and only if the smallest element is mapped to , and then that the smallest values are mapped to . This happens with probability . ∎

Fact C.2.

Say that the expert has flipped the coin times, and of them were heads. Then the expert believes that the probability of heads is .

Proof.

This follows from an application of Bayes rule. The probability of seeing of heads, conditioned on the true bias being is . Therefore, the probability of seeing of heads (unconditioned) is (by Fact C.1). Therefore, the density that the true bias is , conditioned on seeing of heads is , and the probability of seeing heads on the next flip is:

∎

C.2 Omitted Proofs

Proof of Lemma 2.5.

We first prove that if is weakly proper then it satisfies the two stated constraints. Suppose that is weakly proper. It is clear that satisfies the first equation: for all , in order for to have a maximum at , its derivative must be at . So we first conclude that we must have for all . Next, observe that

| (1) |

Suppose for contradiction that for some , we have . Since is continuous, on some open interval containing . On that open interval, then, the sign of is the opposite of the sign of — that is, negative when and positive when . But then is strictly minimized, rather than maximized, at on this interval, contradicting that is weakly proper.

To prove the stronger claim when is proper, assume for contradiction that is not strictly positive almost everywhere. Then because is continuous, there is an interval of non-zero length in which on the entire interval. Let lie on the interior of this interval. Equation (1) then establishes that is in an interval around , meaning that is not the unique maximizer for , contradicting that is proper.

Conversely, suppose that satisfies the two stated constraints. We show that is weakly proper by showing a stronger statement: that for all , weakly increases on and weakly decreases on . By the first constraint, (1) holds. By the second constraint, for all , is either or has the sign of , i.e. positive if and negative if . This means that is weakly increasing on and weakly decreasing on , and so attains a weak global maximum at , as desired.

To prove the stronger claim when almost everywhere, we show that strictly increases almost everywhere on and strictly decreases almost everywhere on . Again, (1) holds, so by the second constraint we have that has the sign of almost everywhere, i.e. positive if and negative if . Thus, is strictly increasing almost everywhere on and strictly decreasing almost everywhere on , and so attains a strict global maximum at , as desired. ∎

Proof of Corollary 2.6.

As is strictly positive on , and is strictly (resp., weakly) positive almost everywhere on , we immediately conclude that is also strictly (resp., weakly) positive almost everywhere on . Therefore, is proper (resp., weakly proper) by Lemma 2.5. ∎

This extension will be relevant when we design optimal scoring rules, so we provide a quick example to help parse it.

Remark C.3.

Consider the function , which is strictly increasing on . Defining for results in (where is the necessary constant to make continuous at ). Clearly on (as promised by Corollary 2.6), so we have just constructed a proper scoring rule:

Proof of Fact 2.7.

Proof of Lemma 2.8.

This is a direct application of Fact C.2, which states that if the expert has flipped heads of coin, their guess at the coin’s bias is . Currently, the expert believes the probability of heads to be . So their expected reward if they stop flipping now is exactly . If they flip once more and stop, then with probability they will get a heads, updating their belief to , and yielding expected reward . With probability they will get a tails, updating their belief to and yielding expected reward . ∎

Proof of Proposition 2.12.

First, we wish to argue that as , no matter the true bias, the number of flips any expert will choose to make approaches . To see this, observe that after flips, the expert’s current belief will always be an integer multiple of . So if , then the expert will always flip the coin at least times as long as . Observe also that the minimum is taken over finitely many terms, all of which are strictly positive, so is strictly positive. Therefore, for all , there is a sufficiently small such that whenever the cost is at most , the expert flips at least times no matter the true bias. Note that while these calculations are done for an adaptive expert, they hold for a non-adaptive expert as well because the non-adaptive expert would want to flip at least coins no matter the outcomes.

Now, let’s consider the expected reward for an expert who makes exactly flips no matter what. For all , such an expert sees total heads with probability . And conditioned on seeing heads, the expert’s expert reward tomorrow is . Therefore, we can conclude:

Lemma C.4.

For all , the expected reward after coin flips is .

Now, we want to understand the limt of this sum as . Observe that for each , the sum is a Riemann sum for the function on (i.e. each lies inside the interval ). Therefore, the limit as is just the Riemann integral, and we get:

So now we can conclude that the non-adaptive expert gets expected payoff . As , the number of flips , and the expected payoff as approaches . For the adaptive experts, observe that by Lemmas 2.8 and 2.9 that as long as they flip the coin at least times with probability , their expected reward is at least as large as if they flipped it exactly times with probability . As their expected reward can certainly not exceed (as this is the reward of a perfect expert who knows exactly the bias), their expected reward must also approach as (and therefore as as well). ∎

Lemma C.5.

For a continuously differentiable (weakly) proper scoring rule , for all if and only if .

Proof of Lemma C.5.

Lemma C.6.

For any weakly proper scoring rule :

Proof of Lemma C.6.

We have

where the last step follows by separating into its own integral and substituting . Now we integrate by parts, letting and , so that and , to get

Expressing as , we obtain the first equality. To obtain the equality with the third expression, we use integration by parts again, letting and , so that and , to get that is equal to

∎

Corollary C.7.

A scoring rule is normalized if , and .

Appendix D Properties of Respectful Scoring Rules

We state several sufficient conditions for a scoring rule to be respectful, confirm that typical scoring rules are respectful, and provide a brief discussion.

Claim D.1.

If Conditions 1 and 2 of Definition 3.1 hold and is bounded on then is respectful.

This should be clear: take to be small enough such that times the lower bound on exceeds the upper bound on . Scoring rules such as the quadratic scoring rule and the spherical scoring rule satisfy the hypotheses of Claim D.1. One well-known generalization of the quadratic scoring rule is the Tsallis rule [Tsa88]. This rule, parametrized by , is defined to be the scoring rule for which . When , this yields the quadratic scoring rule.

For , it is evident that the Tsallis rule satisfies the hypotheses of Claim D.1. However, this is not so for (except for ). Perhaps more importantly, the logarithmic scoring rule does not satisfy Claim D.1 either. This motivates the following result (the proof appears at the end of this section).

Claim D.2.

Suppose that Conditions 1 and 2 of Definition 3.1 are satisfied. Suppose further that is bounded on any closed sub-interval of , and that there exist constants and such that . Then is respectful.

The logarithmic scoring rule satisfies the hypotheses of Claim D.2 ( and ). The Tsallis rule with (and ) also satisfies these hypotheses ( and ). The proof of Claim D.2 is more involved, and deferred to Appendix E.

We briefly discuss ways in which proper scoring rules can fail to be respectful. One way a scoring rule can be disrespectful is if grows extremely quickly near zero (e.g. ). Such functions, however, are outside the scope of this entire exercise because they are not normalizable. That is, such have , and provide infinite expected payment to the expert. So this “limitation” of respectfulness is more of a restatement of normalizability.

Another way a scoring rule could be disrespectful is if is not bounded away from zero. For example: or . If remains “very flat” near for a “large interval”, then is infinite anyway. This implies that we should expect the error to be a larger order of magnitude than , and for such functions to not incentivize precision well at all (although we do not explicitly prove this). This makes sense: if , then the expert gains by flipping the coin to refine their current belief (Lemma 2.8). It is also possible that is not bounded away from zero, but also not “very flat”. We conjecture that Theorem 3.3 does hold for such functions, but that our approach does not establish this. While it is possible to come up with such functions (e.g., the two above) which elude Theorem 3.3’s precise statement, this does not affect commonly-studied scoring rules, nor the scoring rules designed in this paper (sometimes leaning on Theorem 6.1).

Finally, as with any exercise in analysis, there are continuous functions that behave erratically near zero, such as . While it may or may not be the case that Theorem 3.3 extends to such functions, this does not seem particularly relevant.

Proof of Claim D.2.

Let be as in Claim D.2. If then the claim is uninteresting: is bounded on and so the statement is subsumed by Claim D.1. The interesting case is when .

We first consider the case when . Note that . To see this, suppose for contradiction that this limit is finite. We may write

by L’Hôpital’s rule, so , contradicting that .

Now, the fact that lets us apply L’Hôpital’s rule:

This means that

so in particular, there exists such that for all we have and so . On the other hand, is bounded on by assumption.

To finish, let as in Definition 3.1 equal . Assume is small enough that the following conditions are satisfied:

-

•

on .

-

•

.

Then the last condition of Definition 3.1 will be satisfied on ; it will also be satisfied on for any satisfying the second condition above, because on that interval we have

By symmetry of about (and antisymmetry of ) we have that the condition also holds on , as desired.

Now we consider the case that . As above, we have . Proceeding similarly, we have

This means that there exists such that for all we have and so . We finish as before.

Finally, consider the case that . Let be a lower bound on , as in the statement of Claim D.2. It suffices to show that for for small enough, we have on . Let be such that for all . On we have

if is small enough that . (As before, we also need to make sure that is small enough that the condition is satisfied on .) This concludes the proof. ∎

Appendix E Omitted Proofs from Section 3

Proof of Claim 3.5.

Say of the first flips were heads, so . The expert’s expected reward is . The expert reasons: with probability , the next coin will come up heads and my new estimate will be ; with probability it will be come up tails and my new estimate will be . Therefore, the expert’s expected increase in reward from flipping the -th coin is

Since is twice differentiable, we may use Taylor’s approximation theorem to write

for some . Similarly we have

for some . When we plug these expressions into the formula for above, the zeroth- and first-order terms cancel. We are left with

Note that , so , and similarly for . This completes the proof. ∎

Proof of Claim 3.6.

Suppose that for all . By Claim 3.5 we have

Now, we have that , and decreases as gets farther from . This means that

Therefore, if then , so for some (not to be confused with ), if is small enough. ∎

Proof of Claim 3.7.

Let be such that . We have

so

For fixed and for , this maximum divided by is maximized when (or ), in which case the ratio is . Therefore we have

for large enough. (Here we again use that , so is minimized at .) ∎

Proof of Claim 3.8.

We have

Now, let be the fraction of the first coin flips that were heads (so is an average of i.i.d. Bernoulli random variables that are with probability ). Note that is within of , and for large we have for all . This means that for large , by the triangle inequality we have that if then . Therefore, for large we have

We bound each of these probabilities. Recall the following version of the Chernoff bound: for , if is a sum of i.i.d. Bernoulli random variables with , then

We apply this to our random variables (so and ). Assume . Let . Then

If , a symmetry argument yields the same result. Therefore, for sufficiently large we have

The last step comes from observing that for positive and plugging in . Now, this summand is bounded by a constant, since converges, and so we have

as desired. ∎

Proof of Proposition 3.9.

We assume for convenience that (which is safe, as Definition 3.1 holds for all whenever it holds for ).

Fix . Let be as in Claim 3.6. As before, let be the predictor’s estimate for the bias of the coin after flips. Then for small enough that and , for , we have

This follows from Claim 3.7, noting that if and then .

Now, recall Claim 3.5:

for some . In the remainder of this proof, what we essentially argue is that on this interval is not too far from , because of our bound on as plus or minus a small quantity.

We ask: for a given (possibly negative) , how far from can be? Well, since is integrable, we have

Now, since is respectful we have that for small enough, if then

where is defined to be the number on the interval between and minimizing (i.e. farthest from ).

Define . Then . We use this fact to prove the following.

Claim E.1.

Proof.

We prove this for positive . The result follows for negative because if some is a counterexample for some negative , then where for serves as a counterexample for . (This is because for any , by the fundamental theorem of calculus.) Additionally, we may assume that , because if there is a counterexample function to the claim then where also serves as a counterexample.

We prove that

The left inequality suffices because for all , so in particular .

We begin with the right inequality. Suppose for contradiction that . Let be the set of points in where . Since contains , it is nonempty; let . Since is continuous, we have . Pick small enough that the set of points with is nonempty. Let , so . Note that

It follows that for some . (Otherwise the value of the integral would be at most the integral of from to , which is at most , since .) Therefore, because for all , we have that

so . But then we have that and , contradicting the definition of as the infimum of .

The proof of the left inequality above proceeds similarly, but is not exactly analogous. Suppose for contradiction that . Define to be the supremum of points in where (so ). Then is zero at and at , so

which means that for some we have that (otherwise the value of the integral would be at least ). Since for all , we have that

so . This is a contradiction, since on the one hand we have , but on the other hand was defined as the supremum of points where . This completes the proof. ∎

How large of an do we care about? The farthest that and can be from is , for small . (This is because we assumed for convenience that , which means that , so .) Therefore, by Claim E.1 we have

where is either , whichever is farther from . It is easy to check101010Without loss of generality assume , so . Then , so it suffices to show that . This is indeed the case, as for small , so . that for small enough we have that , and so we have

for small enough , where . (Here we use that for small positive .) It follows, then, by Claim 3.5, that

Note that since and , we may write

for small enough that the second-to-last step holds. (In the last step we use that .) A similar calculation shows that for small enough.111111An extra appears, but this term is dominated by for small . Also note that . Putting these approximations all together, we note that the approximation is the dominant one, which means that there is a constant such that

| (2) |

Therefore, since the expert stops flipping when , we have

This holds for any such that ; a sufficient condition is . ∎

A note on terminology: We will sometimes say that a function is uniformly over . This means that and are implicitly functions of as well, but that approaches zero uniformly in (i.e. for all there exists such that for all , we have for all (relevant) values of ). So for instance, the in the statement of Lemma 3.10 is uniform in .

To prove Lemma 3.10 we first prove the following general proposition.

Proposition E.2.

Let and be random variables taking values in for each real number and (some arbitrary set that depends on ). Let . If uniformly over , then uniformly over . Separately, if uniformly over , then uniformly over .

Proof.

The condition that is simply a convenient one to guarantee that all relevant expectations are finite. Now, for any , we have

| (3) |

where the inequality follows by a union bound.

We start with the first statement. Dividing Equation E by , we have

The limit of as approaches zero is by assumption, so for small enough we have that for all . In other words, for every there exists such that for all we have that . Since , we have that for all there exists such that for all and we have that . This proves the first statement.

As for the second statement, we divide Equation E by to obtain

so

The limit of as approaches zero is by assumption, so for small enough we have that for all . In other words, for every there exists such that for all we have that . Since , we have that for all there exists such that for all and we have that . This proves the second statement. ∎

We now prove Lemma 3.10.

Proof (of Lemma 3.10).

Fix any and .

Let be the expert’s error after flips, i.e. . Let be the distance from their guess after flips to their guess after flips. Then the expert’s error after flips lies between and by the triangle inequality. That is, we have

so

which means that

We will later prove the following claim:

Claim E.3.

We have

uniformly over . That is, for all there exists such that for all , the fraction above is less than for all .

Now, given this claim, observe that by the first statement of Proposition E.2 (with and ) we have

By the second statement of the claim (with and ) we have

Note that the premise of the second claim holds for these and , because and so certainly if then .

By the squeeze theorem, it follows that

Note that this limit holds uniformly over .

To complete the proof, we use the fact (proven in Claim E.4) that

We have

Therefore we have

as desired. ∎

We now prove Claim E.3 by approximately computing and . We begin with the former.

Claim E.4.

where the term is a function of (but not ) that approaches zero as approaches zero.

Proof.

We use the Berry-Esseen theorem, a result about the speed of convergence of a sum of i.i.d. random variables to a normal distribution.

Theorem E.5 (Berry-Esseen theorem).

Let be i.i.d. random variables with , , and . Let and let be the CDF of . Let be the standard normal distribution. Then for all we have

for some universal constant independent of and the distribution of the .

Define to be if the expert flips heads (which happens with probability ) and if the expert flips tails (which happens with probability ). Let . Then and . Plugging in these and into the Berry-Esseen theorem, we have

Now, we want to approximate . Note that is within of , the number of heads flipped divided by . This means that . For this reason, we focus on computing and subsequently correct for this small difference.

Observe that

Now, observe on the other hand that

where is a random variable drawn from a normal distribution with mean zero and variance . Now we ask: how different is this second quantity (the integral involving ) from the first one (the integral involving )?

The answer is, not that different. Indeed, as we derived, is within of for all . Furthermore, for any , if then and are both . (For this follows by concentration of normal distributions; the claim for follows from Claim 3.8, realizing the fact that there is nothing special about the in the exponent except that it is less than .) Similarly, if then both and are exponentially close to . Finally, for we have and . This means that is within

of . Now, since and , we have that . It is easy to check that setting any shows that

where the depends only on , not on . Note that uniformly over . This means that uniformly over .

Now, recall that , so

and thus

By the first statement of Proposition E.2 (with and ), we have that

uniformly over . By the second statement (with and ), we have that

uniformly over . (The premise of the second statement is satisfied because .) Therefore, the squeeze theorem tells us that

uniformly over . Therefore, we have where the term only depends on .

Finally, note that

Since and (where the does not depend on ), we have that is within of . Applying Proposition E.2 in the same way as earlier, we find that . We know that . This completes the proof. ∎

We can now prove Claim E.3.

Proof (of Claim E.3).

Let . Define as follows: and for , is either (if the -th flip is heads, i.e. with probability ) or (if the -th flip is tails, i.e. with probability . Note that is a martingale.

Now, observe that for any , we have

This is because is one more than the number of heads in the first flips and is one more than the number of heads in the first flips. Thus,

Therefore we have

Here, the last inequality follows from the fact that the arithmetic mean of and is less than or equal to the -power mean (since ).

Now, it is clear that , since by Proposition 3.9. We now show that . We make use of a tool called the Burkholder-Davis-Gundy inequality.

Definition E.6.

Let be a martingale. The quadratic variation of , denoted , is equal to

Note that is a random variable, not a number.

Theorem E.7 (Burkholder-Davis-Gundy inequality).

Let . There is a constant such that for every martingale with , we have

We wish to bound above. To do so, we bound above. Observe that is a sum of independent random variables that are each either (with probability ) or (with probability ). Thus, . Observe that

The last line comes from a Chernoff bound. In particular, we have that for . Setting gives us the expression above. Now, we can bound the integral as follows:

Note that is continuous, converges on , and approaches zero as . It follows that is bounded on ; in other words, our integral is (i.e. possibly depends on but is at most a constant for fixed ). Therefore, we have

Therefore we have

Therefore, we have that . By the same reasoning as in the proof of Claim E.4, it follows that . We previously showed that . This completes the proof. ∎

Theorem E.8.

If is a respectful, normalizable, continuously differentiable proper scoring rule, and is the expected error of a locally adaptive expert rewarded by when the coin has bias and the cost of a flip is , then

Proof (of Theorem E.8).

Let , i.e. a large enough function of that it is guaranteed that the expert flips the coin at least times. We have

We wish to compute the limit of this quantity as approaches zero. Note that

This is because is bounded between and and , which goes to zero faster than goes to infinity. Therefore we have

(We may ignore the term above because it approaches in the limit.) We may write this quantity as

Let us focus on the second summand. Let . We assume ; the other case is analogous.

We consider two sub-cases: and . First suppose that . Note that since holds, we have for all that

This in particular is true of , so

since and so .

Now suppose that . Recall the notation from the discussion preceding the definition of . For any , we have

so .

This means that

so we can ignore this summand. Therefore, we have

From Lemma 3.10, we have that

By the squeeze theorem, we conclude that.

∎

Below is our proof of Lemma 3.11, followed by a proof of Theorem 3.3. Our approach will be to compare the behavior of a locally adaptive expert to that of a globally adaptive one. We will assume that the experts observe the same stream of coin flips (each heads with probability unknown to the experts) but that they may decide to stop at different times. As before, we will let where is the number of the first flips to have come up heads; since the experts see the same coin flips, we do not need to distinguish between for the locally adaptive expert and for the globally adaptive expert. We will let and be the number of times the locally and globally adaptive experts flip the coin, respectively (so ). (We used the notation in place of in Proposition 3.9.) Let be as in the definition of respectful scoring rules, and in particular we will assume that as before (for any that witnesses that a scoring rule is respectful, any smaller also works).

The bulk of the proof of Theorem 3.3 has already been completed, if we think of Theorem E.8 as a step in the proof. The bulk of the remainder is proving the following lemma.

Proof of Lemma 3.11.

Suppose the globally adaptive expert flips the coin times. We show that they do not flip the coin another time.

By definition of , we have that

It is easy to check that because (by Claim 3.6) and (so ), the above relationship between and implies that . This allows us to use some results from our analysis of locally adaptive experts. In particular, by Equation 2 in the proof of Proposition 3.9, we have that

Conditional on (and by definition implies ), we also have

In particular this means that

for small enough. This means that if then . Furthermore, for any we will have .

However, this does not mean that the globally adaptive expert won’t flip the coin for the -th time, because they don’t know that is true. From the expert’s perspective, if they knew (or even ) to be true, they would stop flipping the coin; but perhaps they should keep flipping the coin because of the outside chance that is false.

This turns out not to be the case, because the probability that is false is so small. In particular, from the expert’s perspective, if being false, they cannot achieve reward better than the expectation of conditional on the coins they’ve flipped and on being false. We show that if the scoring rule is normalizable (i.e. is finite), then this quantity isn’t too large. In particular, we show the following:

Claim E.9.

Let be the random variable corresponding to the number of heads flipped in the first flips. Then for any , we have

Proof.

We have

Let us consider the expectation conditioned on . Consider the distribution of conditioned on , , and . Consider also the uniform distribution on .

We claim that stochastically dominates , i.e. for all . To see this, observe that the PDF of is an increasing function on . This is because on is a constant multiple of the distribution of conditioned on , , and ; but in this case the condition is redundant because if then holds. So is the distribution of conditioned on and . Clearly the PDF of increases on (because the expert starts with uniform priors and updates more strongly on against values of farther from , which is greater than for small enough).

Now, the expectation of if were drawn from instead of is equal to . On the other hand, the actual expectation of (i.e. with drawn from ) is necessarily smaller. This is because is convex and symmetric about , meaning that is decreasing on . Since stochastically dominates , we conclude that

The same inequality holds conditional instead on , which concludes the proof. ∎

From the expert’s perspective, this means that if they flip the coin for the -th time, then:

-

•