Bandit Learning with Delayed Impact of Actions

Abstract

We consider a stochastic multi-armed bandit (MAB) problem with delayed impact of actions. In our setting, actions taken in the past impact the arm rewards in the subsequent future. This delayed impact of actions is prevalent in the real world. For example, the capability to pay back a loan for people in a certain social group might depend on historically how frequently that group has been approved loan applications. If banks keep rejecting loan applications to people in a disadvantaged group, it could create a feedback loop and further damage the chance of getting loans for people in that group. In this paper, we formulate this delayed and long-term impact of actions within the context of multi-armed bandits. We generalize the bandit setting to encode the dependency of this “bias" due to the action history during learning. The goal is to maximize the collected utilities over time while taking into account the dynamics created by the delayed impacts of historical actions. We propose an algorithm that achieves a regret of and show a matching regret lower bound of , where is the number of arms and is the learning horizon. Our results complement the bandit literature by adding techniques to deal with actions with long-term impacts and have implications in designing fair algorithms.

1 Introduction

Algorithms have been increasingly involved in high-stakes decision making. Examples include approving/rejecting loan applications [23, 37], deciding on employment and compensation [5, 19], and recidivism and bail decisions [1]. Automating these high-stakes decisions has raised ethical concerns on whether it amplifies the discriminative bias against protected classes [52, 14]. There have also been growing efforts towards studying algorithmic approaches to mitigate these concerns. Most of the above efforts have focused on static settings: a utility-maximizing decision maker needs to ensure her actions satisfy some fairness criteria at the decision time, without considering the long-term impacts of actions. However, in practice, these decisions may often introduce long-term impacts to the rewards and well-beings for the human agents involved. For example,

-

A regional financial institute may decide on the fraction of loan applications from different social groups to approve. These decisions could affect the development of these groups: The capability of applicants from a group to pay back a loan might depend on the group’s socio-economic status, which is influenced by how frequently applications from this group have been approved [6, 18].

These observations raise the following concerns. If being insensitive with the long-term impact of actions, the decision maker risks treating a historically disadvantaged group unfairly. Making things even worse, these unfair and oblivious decisions might reinforce existing biases and make it harder to observe the true potential for a disadvantaged group. While being a relatively under-explored (but important) topic, several recent works have looked into this problem of delayed impact of actions in algorithm design. However, these studies have so far focused on understanding the impact in a one-step delay of actions [45, 36, 31], or a sequential decision making setting without uncertainty [47, 33, 51, 66, 46, 20, 67].

Our work departs from the above line of efforts by studying the long-term impact of actions in sequential decision making under uncertainty. We generalize the multi-armed bandit setting by introducing the impact functions that encode the dependency of the “bias” due to the action history of the learning to the arm rewards. Our goal is to learn to maximize the rewards obtained over time, in which the rewards’ evolution could depend on the past actions.

The history-dependency reward structure makes our problem substantially more challenging. In particular, we first show that applying standard bandit algorithms leads to linear regret, i.e., existing approaches will obtain low rewards with a biased learning process. To address this challenge, under relatively mild conditions for the dependency dynamics, we present an algorithm, based on a phased-learning template which smoothes out the historical bias during learning, that achieves a regret of . Moreover, we show a matching lower regret bound of that demonstrates that our algorithm is order-optimal. Finally, we conduct a series of simulations showing that our algorithms compare favorably to other state-of-the-art methods proposed in other application domains. From a policy maker’s point of view, our paper explores solutions to learn the optimal sequential intervention when the actions taken in the past impact the learning environment in an unknown and long-term manner. We believe our work nicely complements the existing literature that focuses more on the “understanding” of the dynamics [33, 45, 66, 67].

Related work.

Our work contributes to algorithmic fairness studied in sequential settings. Prior works either study fairness in sequential learning settings without considering long-term impact of actions [34, 49, 27, 7, 30, 54] or explore the delayed impacts of actions with focus on addressing the one-step delayed impacts or sequential learning with full information [33, 45, 6, 31, 51, 18, 20]. Our work differs from the above and studies delayed impacts of actions in sequential decision making under uncertainty. Our formulation bears similarity to reinforcement learning since our impact function encodes memory (and is in fact Markovian [53, 62]), although we focus on studying the exploration-exploitation tradeoff in bandit formulation. Our learning formulation builds on the rich bandit learning literature [42, 3] and is related to non-stationary bandits [60, 8, 9, 43, 38]. Our techniques share similar insights with Lipschitz bandits [39, 59] and combinatorial bandits [13] in that we also assume the Lipschitz reward structure and consider combinatorial action space. There are also recent works that have formulated delayed action impact in bandit learning [56, 38], but in all of these works, the setting and the formulation are different from the ones we consider in the present work. More discussions on related work can be found in Appendix A.

2 Problem Setting

We formulate the setting in which an institution sequentially determines how to allocate resource to different groups. For example, a regional financial institute may decide on overall frequency of loan applications to approve from different social groups. The police department may decide on the amount of patrol time allocated to different regions.

The institution is assumed to be a utility maximizer, aiming to maximize the expected reward associated with the allocation policy over time. If we assume the reward111The reward could be whether a crime has been stopped or whether the borrower pays the monthly payment on time. For applications that require longer time periods to assess the rewards, the duration of a time step, i.e., the frequency to update the policy, would also need to be adjusted accordingly. for allocating a unit of resource to a group is i.i.d. drawn from some unknown distribution, this problem can be reduced to a standard bandit problem, with each group representing an arm. The goal of the institution is then to learn a sequence of arm selections to maximize its cumulative rewards.

In this work, we extend the bandit setting and consider the delayed impact of actions. Below we formalize our setup which introduces impact functions to bandit framework.

Action space. There are base arms, indexed from to , with each base arm representing a group. At each discrete time , the institution chooses an action, called a meta arm, which specifies the probability to activate each base arm. Let be the -dimensional probability simplex. We denote the meta arm as . Each base arm is activated independently according to their in . The institution only observes the reward from the arms that are activated. Our feedback model deviates slightly from the classical bandit feedback and shares similarity to combinatorial bandits: instead of assuming always observing one arm’s reward each time, we observe the reward of one arm in expectation, i.e., we can potentially observe no arm’s reward or multiple arms’ rewards. This modeling choice is mainly needed to resolve a technicality issue and has been adopted in the literature [65, 13]. Most of our algorithms and results extend to the case where only one arm is activated according to .222The upper bound becomes , which is slightly worse than in . But the upper bound is still tight in . We provide discussions in Remark D.6

Remark 2.1.

We can also interpret the meta-arm as specifying the proportion of resources allocated to each base arm. The interpretation impacts the way the rewards are generated (i.e., instead of observing the rewards of the realized base arms, the institution observes the rewards of all base arms with non-zero allocations.) Our analysis utilizes the idea of importance weighting and could deal with both cases in the same framework. To simplify the presentation, we focus on the case of interpreting the meta-arm as probabilities, though our results apply to both interpretations.

Delayed impacts of actions. We consider the scenario in which the rewards of actions are unknown a priori and are influenced by the action history. Formally, let be the action history at time . We define the impact function to summarize the impact of the learner’s actions to the reward generated in each group, where is the function mapping the action history to its current impact on arms’ rewards. In the following discussion, we make implicit and use the vector to denote the impact to each group, where captures the impact of action history to arm .

Rewards and regret. The reward for selecting group at time depends on both and the historical impact . In particular, when the arm representing group is activated, the institution observes a reward (the instantaneous reward is bounded within ) drawn i.i.d. from a unknown distribution with mean and claims the sum of rewards from activated arms as total rewards. is unknown a priori but is Lipschitz continuous (with known Lipschitz constant ) with respect to its input, i.e., a small deviation of the institution’s actions has small impacts on the unit reward from each group. When action is taken at time , the institution obtains an expected reward

| (1) |

As for the impact function, we focus on the setting in which is a time-discounted average, with each component defined as

| (2) |

where is the time-discounting factor. 333Here we follow the tradition to define when . Intuitively, is a weighted average with more weights on recent actions. We would like to highlight that our results extend to a more general family of impact functions and do not require the exact knowledge of impact functions (see discussion in Section 5.2). We also note that when , our setting reduces to a special case where the impact function only depends on the current action (action dependent), instead of the entire history of actions (discounted by 0 right away). We study this special case of interest in Section 4.

Let be the algorithm the institution deploys. The goal of is to choose a sequence of actions that maximizes the total utility. The performance of is characterized by regret, defined as

| (3) |

where the expectation is taken on the randomness of algorithm and the utility realization.444In this paper, we adopt the standard regret definition and compare against the optimal fixed policy. Another possible regret definition is to compare against the optimal dynamic policy that could change based on the history. However, calculating the optimal dynamic policy in our setting is nontrivial as it requires to solve an MDP with continuous states.

2.1 Exemplary Application of Our Setup

We provide an illustrative example to instantiate our model. Consider a police department who needs to dispatch a number of police officers to different districts. Each district has a different crime distribution, and the goal (absent additional fairness constraints) might be to maximize the number of crimes caught [22]. 555 As discussed by Elzayn et al. [22], there might be other goals besides simply catching criminals, including preventing crime, fostering community relations, and promoting public safety. We use the same goal they adopted for the illustrative purpose. The effects of police patrol resource allocated to each district may aggregate over time and then impact the crime rate of that district. In other words, the crime rate in each district depends on how frequently the police officers have been dispatched historically in this district.

To simplify the discussion, we normalize the expected police resource to be one unit. Each district has a default average crime rate at the beginning of the learning process. This crime rate can (at most) be decreased to . All of these are unknown to the police department. The police department makes a resource allocation decision at each time step. We use to denote the crime rate in district at time , taking into account the impact of historical decisions. Assume is the amount of police resource dispatched to district at time ( for all ), the expected number of crimes caught at district at time would be . Note that here can be interpreted as the probability of allocating police resource (randomly sending the patrol team to each of the districts) or the fraction of allocated police resource.

Below we provide one natural example of the interaction between the impact function and the reward. At time step , let denote the historical decisions of the police department for district . Now given where is the current decision for district , assume that the crime rate at time in district is in the following form:

| (4) |

where is the impact function that summarizes how historical actions would impact the current crime rate. One possible example is as we defined in Equation (2). This impact function has two natural properties:

-

When (e.g., ), the police department keeps dispatching the police officers to district with probability , then district will reach its lowest crime rate.

-

When (e.g., ), the police department rarely dispatch police officers to district , The crime rate in district will reach its highest level.

In this example, treating each district as an arm and directly applying standard bandit algorithms might reach suboptimal solutions since the reward dynamic is not considered. In this paper, we develop algorithms that can take into account this history-dependent reward dynamic and achieve no-regret learning. Our results hold for a general class of impact functions (under mild conditions) and do not need to assume the exact knowledge of the impact function.

3 Overview of Main Results

We summarize our main results in this section. First, we present an important, though perhaps not surprising, negative result: if the institution is not aware of the delayed impact of actions, applying existing standard bandit algorithms in our setting leads to linear regrets. This negative result highlights the importance of designing new algorithms when delayed impact of actions are present. The formal statement and analysis are in Appendix C.

Lemma 3.1 (Informal).

If the institution is unaware of the delayed impact of actions, applying standard bandit algorithms (including UCB, Thompson Sampling) leads to linear regrets.

While the negative result might not be surprising, as it resembles similarity to the negative results on applying classic bandit algorithm to a non-stationary setting, it points out the need to design new algorithms for settings with delayed impact of actions. The key challenge introduced by our setting is in estimating the arm rewards: when pulling the same meta arm at different time steps, the institution does not guarantee to obtain rewards drawn from the targeted distribution according to the chosen meta arm, as the arm reward depends on the impact function . To address this challenge, we note that if the institution keeps pulling the same meta-arm repeatedly, the impact function (and thus the arm reward associated with the meta-arm) would converge to some value. This observation leads to our approaches. We first develop a bandit algorithm that works with impacts that converge “immediately" (or equivalently only depend on “immediate” actions, echoing the case with in Equation (2)). We then propose a phased-learning reduction template that reduces our general setting to the above one and achieves a sublinear regret.

Theorem 3.2 (Informal).

There is an algorithm that achieves an optimal regret bound for the bandit problem with the impact function defined in Equation (2). In addition, there is a matching lower bound of .

To provide an overview of our approaches, we start with action-dependent bandits (Section 4), where the impact at time depends only on the action at , i.e., , namely in Equation (2). This setting not only captures the one-step impact but also offers a backbone for the phase-learning template for the general history-dependent scenario. In this setting, when a meta-arm is selected, each base arms is activated with probability , and the institution observes the realized rewards for all activated base arms and receives the sum of them as total rewards. Since we know the probability for activating each base arm, we may apply importance weighting to simulate the case as if the learner is selecting probabilities and obtain signals at each time step. This interpretation transforms our problem structure to a setting similar to combinatorial bandits. Furthermore, since both are Lipschitz continuous, we adopt the idea from Lipschitz bandits to discretize the continuous space of each . With these ideas combined, we design a UCB-like algorithm that achieves a regret of .

With the solution of action-dependent bandits, we explore the general history-dependent bandits with impact functions following Equation (2) (Section 5). The main idea is to divide total time rounds into phases, and then selecting the same actions in each phase to smooth out impacts of historically made actions, which will then help reduce the problem to an action-dependent one. One challenge is to construct appropriate confidence bound and adjust the length of each phase to account for the historical action bias. With a careful combination with our results for action-dependent bandits, we present an algorithm which can also achieve a regret of the order . We further proceed to show that this bound is tight and provide numerical experiments.

4 Action-Dependent Bandits

In this section, we study action-dependent bandits, in which the impact function , corresponding to in Equation (2). Our algorithm starts with a discretization over the space . Formally, we uniformly discretize for each base arm into intervals of a fixed length , with carefully chosen such that is an positive integer.666Smarter discretization generally does not lead to better regret bounds [39]. Let be the space of discretized meta arms, i.e., for each , and for all . Let denote the optimal strategy in discretized space . After a meta arm is selected, each arm is independently activated with probability . From now, we use to denote the realization of corresponding reward. The learner observes activated arms, and observes the instantaneous reward of each activated arm . We use importance weighting [29] to construct the unbiased realized reward for each of the elements in :

| (5) |

Since the probability activating arm is , it is easy to see that . Given the importance-weighted rewards , we re-frame our problem as choosing a -dimensional probability measure (one value for each base arm). In particular, for each base arm , will take the value from , and we refer to as the discretized arm.

Remark 4.1.

The above importance-weighting technique enables us to “observe” samples of for all base arms when selecting . This technique helps to bridge the gap between the interpretation of whether is a probability distribution or an allocation over base arms. Our following techniques can be applied in either interpretation.

By doing so, our problem is now similar to combinatorial bandits, in which we are choosing discretized arms and observe the corresponding rewards. Below we describe our UCB-like algorithm based on the reward estimation of discretized arms. We define the set to record all the time steps such that the deployed meta arm contains the discretized arm . We can maintain the empirical estimates of the mean reward for each discretized arm and compute the UCB index for each meta arm :

| (6) |

where is the cardinality of set . With the UCB index in place, we are now ready to state our algorithm in Algorithm 1. The next theorem provides the regret bound of Algorithm 1.

Theorem 4.2.

Let . The regret of Algorithm 1 (with respect to the optimal arm in non-discretized ) is upper bounded as follows: .

Proof Sketch.

Similar to the proofs of the family of UCB-style algorithms for MAB, after an appropriate discretization, we can derive the regret as the sum of the badness (suboptimality of a meta arm) for all (discretized) suboptimal meta arm selection. However, this will cost us an exponential in the order of final regret bound: this is because we need to take the summation over all feasible suboptimal meta arms, which the number grows exponentially with . To tackle this challenge, we focus on the derivations of badness via tracking the minimum suboptimal selections in the space of realized actions (base arms), which enables us to reduce the exponential to a polynomial . On a high level, our proof proceeds in the following steps:

-

In Step , we obtain a high probability bound of the estimation error for the expected rewards of meta arms after discretization.

-

In Step , we bound the probability on deploying a suboptimal meta arm when selected sufficiently many number of times, where we quantify such sufficiency via , which is the minimum number of selection of a discretized arm contained in a suboptimal meta arm.

-

In Step and Wrapping-up step, we bound the expected value of and connect the regret for playing suboptimal meta arms with the regret incurred by including discretized arms which are not in optimal strategy (in discretized space).

Finally, the regret bound of Algorithm 1 can be achieved by optimizing the discretization parameter. ∎

Discussions

Our techniques have close connections to Lipschitz bandits [16, 50] and combinatorial bandits [13, 12]. Given the Lipschitz property of , we are able to utilize the idea of Lipschitz bandits to discretize the strategy space and achieve sublinear regret with respect to the optimal strategy in the non-discretized strategy space. Moreover, we achieve a significantly improved regret bound by utilizing the connection between our problem setting and combinatorial bandits. In combinatorial bandits, the learner selects actions out of action space at each time step, where in our setting. Directly applying state-of-the-art combinatorial bandit algorithms [13] in our setting would achieve an instance-independent regret bound of , while we achieve a lower regret of .777We compare our results with a tight regret bound achieved in Theorem 2 of [13]. The detailed derivations are deferred to Appendix D.2.1. The reason for our improvement is that, for each base arm, regardless of which probability it was chosen, we can update the reward of the base arm, which provides information for all meta arms that select this arm with a different probability. This reduces the exploration and helps achieving the improvement. In addition to the above improvement, we would like to highlight that another of our main contributions is to extend the action-dependent bandits to the problem of history-dependent bandits, as discussed in Section 5.

Another natural attempt to tackle our problem is to apply EXP3 [4], which achieves sublinear regret even when the arm reward is generated adversarially. However, note that the optimal policy in our setting could be a mixed strategy, while the “sublinear” regret of EXP3 is with respect to a fixed strategy. Therefore, when applying EXP3 over the set of base arms, it still implies a linear regret in our setting. The other option is to apply EXP3 over the set of meta arms. Since the number of meta arms is exponential in , it would incur a regret exponential in due to the size of meta arms.

5 History-Dependent Bandits

We now describe how to utilize our results for action-dependent bandits to solve the history-dependent bandit learning problem, with the impact function specified in Equation (2). The crux of our analysis is the observation that, in history-dependent bandits, if the learner keeps selecting the same strategy for a long enough period of time, the expected one-shot utility will be approaching the utility of selecting in the action-dependent bandits. More specifically, suppose after time , the current action impact for all arms is . Assume that the learner is interested in learning about the utility of selecting next. Since the rewards are influenced by , selecting at time does not necessarily give us the utility samples at . Instead, the learner can keep pulling this meta arm for a non-negligible consecutive rounds to ensure that approaches . Following this idea, we decompose the total number of time rounds into phases which each phase is associated with rounds. We denote as the phase index and as the selected meta-arm in the -th phase. To summarize the above phased-learning template:

-

In each phase , we start with an approaching stage: the first rounds of the phase. This stage is used to “move" with towards to .

-

In the second stage, namely, estimation stage, of each phase: the remaining rounds. This stage is used for collecting the realized rewards and estimating the true reward mean on action .

-

Finally, we leverage our tools in action-dependent bandits to decide what meta arm to select in each phase.

![[Uncaptioned image]](/html/2002.10316/assets/x1.png)

Note that even if we keep pulling the arm with the constant probability in the approaching stage, the action impact in the estimation stage is not exactly the same as meta arm we want to learn, i.e., for , due to the finite length of the stage. However, we can guarantee all for is close enough to by bounding its approximation error w.r.t . The above idea enables a more general reduction algorithm that is compatible with any bandit algorithm that solves the action-dependent case. Let be the ratio of number of rounds in estimation stage of each phase. We present this reduction in Algorithm 2 and a graphical illustration in Figure 1.

5.1 History-Dependent UCB

In this section, we show how to utilize the reduction template to achieve a regret bound for history-dependent bandits. We first introduce some notations. For each discretized arm , similar to action-dependent case, we define as the set of all time indexes till the end of phase in estimation stages such that arm is pulled with probability . We define the following empirical computed from our observations and the empirical utility : 888est in superscript stands for esttimation stage.

| (7) |

where is the total number of rounds pulling arm with probability in all estimation stages, and is defined similarly as in Equation (5). We use the smoothed-out frequency in the estimation stage as an approximation for the discounted frequency right after the approaching stage.

We compute our UCB for each meta arm at the end of each phase. We define and compute , the approximation error incurred after our attempt to smooth out the historical action impact. With these preparations, we present the phased history-dependent UCB algorithm (in companion with Algorithm 2) in Algorithm 3. The main result of this section is given as follows:

Theorem 5.1.

For a constant ratio , we match the optimal regret order for action-dependent bandits. When is smaller, the impact function “forgets" the impact of past-taken actions faster, therefore less rounds in approaching stage would be needed (see ’s dependence in ) and this leads to larger .

Remark 5.2.

The dependence of our regret on the phase length is encoded in . When implementing our algorithm (Section 7), we calculate via given the ratio . We also run simulations of our algorithm on different ratios , the results show that the performance of our algorithm are not sensitive w.r.t. specifying s - in practice, we do not require the exact knowledge of , instead we can afford to use a rough estimation of its upper bound to compute .

5.2 Extension to General Impact Functions

So far, we discuss settings when the impact function is specified as in Equation (2). However, the same technique we presented earlier can be applied for a more general family of impact functions. In particular, as long as the impact function converges after the learner keeps selecting the same action, our result holds. To be more precise, we only require to satisfy the condition when the learner keeps pulling arm with probability for round. The function can be an arbitrary monotone function as long as it is continuous and differentiable, for example: . In fact, the property of is only used when we estimate how close is to after the approaching stage with repeatedly selecting . For a different , we define new reward mean functions , and tune parameters and accordingly to bound the approximation error for (change the Lipschitz constant). This way we can follow the same algorithmic template to achieve a similar regret.

Moreover, we do not require exact knowledge of the impact function . We only require the impact functions to satisfy the above conditions for our algorithms/analysis to hold. With the same arguments, while we assume the reward function is fed with the same impact function , our formulation generalizes to different impact functions for , as long as these impact functions are able to stabilize given a consecutive adoption of the desired action.

6 Matching Lower Bounds

For both action- and history-dependent bandit learning problems, we have proposed algorithms that achieve a regret bound of . We now show the above bounds are order-optimal with respect to and , i.e., the lower bounds of our action- and history-dependent bandits are both , as summarized below.

Theorem 6.1.

Let and , there exist problem instances that for our action- and history-dependent bandits, respectively, the regret for any algorithm follows: .

For the lower bound proof of action-dependent bandits (included in Appendix F), we following the standard randomized problem instances construction used in combinatorial bandits and Lipschitz bandits and use information inequality to prove the lower bound. For history-dependent bandits, we show that for a general class of reward function which satisfies the proper property (see Definition G.1), solving history-dependent bandits is as least as hard as solving action-dependent bandits. Armed with the above derived lower bound of action-dependent bandits, we can then conclude the lower bound of history-dependent bandits.

7 Numeric Experiments

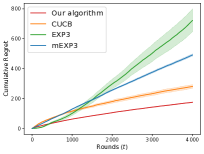

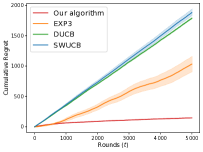

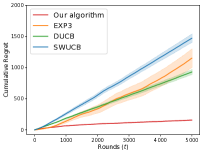

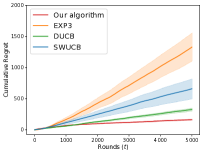

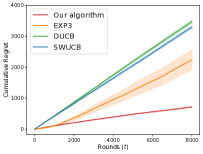

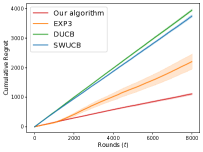

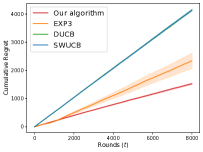

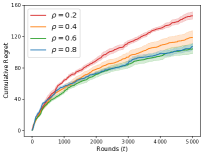

We conducted a series of simulations to understand the performance of our algorithms. The detailed setups and discussion are in Appendix I. We first compare our algorithm with some baselines under action-dependent bandits and other non-stationary baselines under history-dependent bandits with different (the parameter in time-discounted frequency). The results, as shown in Fig. 2, demonstrate that our proposed algorithm consistently outperforms the baseline methods. We also note that the performance of our algorithm is relatively robust w.r.t. difference choices of , i.e., the time-discounting factor for the impact. One explanation is that our algorithm utilizes repeated pulling to smooth out historical bias. Given the exponential-decaying nature of time discounting, the amount of pulling required for the impact to converge does not depend on too heavily. As shown in our theoretical regret upper bounds, gamma can be absorbed with other numeric constants, and when the time horizon increases, the effect of gamma on our algorithm’s performance is diminishing, which aligns with our empirical observation. We also examine our algorithm with larger number of base arms and different ratios . The results, as in Figure 3, show that our algorithm outperforms other baselines when goes large. Furthermore, in our regret bounds (see Theorem 5.1), the regret scales linearly w.r.t . Though the presented results absorb other numeric constants, it is expected to see that the slope of the regret curve is proportionally increasing along with increasing . The results also suggest that our algorithm is not sensitive to different , though one could see the regret is slightly lower when is increasing, which is expected from our regret bound.

8 Conclusion and Future Work

We explore a multi-armed bandit problem in which actions have delayed impacts to the arm rewards. We propose algorithms that achieve a regret of and provide a matching lower regret bound of . Our results complement the bandit literature by exploring the action history dependent biases in bandits. While our model have its limitations, it captures an important but relatively under-explored angle in algorithmic fairness, the long-term impact of actions in sequential learning settings. We hope our study will open more discussions along this direction.

Acknowledgments and Disclosure of Funding

We thank the anonymous reviewers for their valuable comments. This work is supported in part by the Office of Naval Research Grant N00014-20-1-2240 and the National Science Foundation (NSF) FAI program in collaboration with Amazon under grant IIS-1939677 and IIS-2040800.

References

- Angwin et al. [2016] Angwin, J., Larson, J., Mattu, S., and Kirchner, L. Machine bias. ProPublica, May, 23:2016, 2016.

- Audibert & Bubeck [2010] Audibert, J.-Y. and Bubeck, S. Regret bounds and minimax policies under partial monitoring. Journal of Machine Learning Research, 11:2785–2836, 2010.

- Auer et al. [2002a] Auer, P., Cesa-Bianchi, N., and Fischer, P. Finite-time analysis of the multiarmed bandit problem. Machine learning, 47(2-3):235–256, 2002a.

- Auer et al. [2002b] Auer, P., Cesa-Bianchi, N., Freund, Y., and Schapire, R. E. The nonstochastic multiarmed bandit problem. SIAM journal on computing, 32(1):48–77, 2002b.

- Bartik & Nelson [2016] Bartik, A. and Nelson, S. Credit reports as resumes: The incidence of pre-employment credit screening. 2016.

- Bartlett et al. [2018] Bartlett, R., Morse, A., Stanton, R., and Wallace, N. Consumer-lending discrimination in the era of fintech. Unpublished working paper. University of California, Berkeley, 2018.

- Bechavod et al. [2019] Bechavod, Y., Ligett, K., Roth, A., Waggoner, B., and Wu, S. Z. Equal opportunity in online classification with partial feedback. In Advances in Neural Information Processing Systems, pp. 8972–8982, 2019.

- Besbes et al. [2014] Besbes, O., Gur, Y., and Zeevi, A. Stochastic multi-armed-bandit problem with non-stationary rewards. In Advances in neural information processing systems, pp. 199–207, 2014.

- Besbes et al. [2015] Besbes, O., Gur, Y., and Zeevi, A. Non-stationary stochastic optimization. Operations research, 63(5):1227–1244, 2015.

- Cella & Cesa-Bianchi [2020] Cella, L. and Cesa-Bianchi, N. Stochastic bandits with delay-dependent payoffs. In International Conference on Artificial Intelligence and Statistics, pp. 1168–1177. PMLR, 2020.

- Cesa-Bianchi & Lugosi [2012] Cesa-Bianchi, N. and Lugosi, G. Combinatorial bandits. Journal of Computer and System Sciences, 78(5):1404–1422, 2012.

- Chen et al. [2016a] Chen, W., Hu, W., Li, F., Li, J., Liu, Y., and Lu, P. Combinatorial multi-armed bandit with general reward functions. In Advances in Neural Information Processing Systems, pp. 1659–1667, 2016a.

- Chen et al. [2016b] Chen, W., Wang, Y., Yuan, Y., and Wang, Q. Combinatorial multi-armed bandit and its extension to probabilistically triggered arms. The Journal of Machine Learning Research, 17(1):1746–1778, 2016b.

- Chouldechova [2017] Chouldechova, A. Fair prediction with disparate impact: A study of bias in recidivism prediction instruments. Big data, 5(2):153–163, 2017.

- Combes et al. [2015] Combes, R., Shahi, M. S. T. M., Proutiere, A., et al. Combinatorial bandits revisited. In Advances in Neural Information Processing Systems, pp. 2116–2124, 2015.

- Combes et al. [2020] Combes, R., Proutière, A., and Fauquette, A. Unimodal bandits with continuous arms: Order-optimal regret without smoothness. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 4(1):1–28, 2020.

- Cortes et al. [2017] Cortes, C., DeSalvo, G., Kuznetsov, V., Mohri, M., and Yang, S. Discrepancy-based algorithms for non-stationary rested bandits. arXiv preprint arXiv:1710.10657, 2017.

- Cowgill & Tucker [2019] Cowgill, B. and Tucker, C. E. Economics, fairness and algorithmic bias. preparation for: Journal of Economic Perspectives, 2019.

- Cowgill & Zitzewitz [2009] Cowgill, B. and Zitzewitz, E. Incentive effects of equity compensation: Employee level evidence from google. Dartmouth Department of Economics working paper, 2009.

- D’Amour et al. [2020] D’Amour, A., Srinivasan, H., Atwood, J., Baljekar, P., Sculley, D., and Halpern, Y. Fairness is not static: deeper understanding of long term fairness via simulation studies. In Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, pp. 525–534, 2020.

- Duran & Verloop [2018] Duran, S. and Verloop, I. M. Asymptotic optimal control of markov-modulated restless bandits. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 2(1):1–25, 2018.

- Elzayn et al. [2019] Elzayn, H., Jabbari, S., Jung, C., Kearns, M., Neel, S., Roth, A., and Schutzman, Z. Fair algorithms for learning in allocation problems. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pp. 170–179, 2019.

- Fuster et al. [2018] Fuster, A., Goldsmith-Pinkham, P., Ramadorai, T., and Walther, A. Predictably unequal? the effects of machine learning on credit markets. 2018.

- Gael et al. [2020] Gael, M. A., Vernade, C., Carpentier, A., and Valko, M. Stochastic bandits with arm-dependent delays. In International Conference on Machine Learning, pp. 3348–3356. PMLR, 2020.

- Garivier & Moulines [2011] Garivier, A. and Moulines, E. On upper-confidence bound policies for switching bandit problems. In International Conference on Algorithmic Learning Theory, pp. 174–188, 2011.

- Gelman et al. [2007] Gelman, A., Fagan, J., and Kiss, A. An analysis of the new york city police department’s “stop-and-frisk” policy in the context of claims of racial bias. Journal of the American statistical association, 102(479):813–823, 2007.

- Gillen et al. [2018] Gillen, S., Jung, C., Kearns, M., and Roth, A. Online learning with an unknown fairness metric. In Advances in Neural Information Processing Systems, pp. 2600–2609, 2018.

- Goel et al. [2016] Goel, S., Rao, J. M., Shroff, R., et al. Precinct or prejudice? understanding racial disparities in new york city’s stop-and-frisk policy. The Annals of Applied Statistics, 10(1):365–394, 2016.

- Gretton et al. [2009] Gretton, A., Smola, A., Huang, J., Schmittfull, M., Borgwardt, K., and Schölkopf, B. Covariate shift by kernel mean matching. Dataset shift in machine learning, 3(4):5, 2009.

- Gupta & Kamble [2019] Gupta, S. and Kamble, V. Individual fairness in hindsight. In Proceedings of the 2019 ACM Conference on Economics and Computation, pp. 805–806, 2019.

- Heidari et al. [2019] Heidari, H., Nanda, V., and Gummadi, K. P. On the long-term impact of algorithmic decision policies: Effort unfairness and feature segregation through social learning. arXiv preprint arXiv:1903.01209, 2019.

- Ho et al. [2016] Ho, C.-J., Slivkins, A., and Vaughan, J. W. Adaptive contract design for crowdsourcing markets: Bandit algorithms for repeated principal-agent problems. Journal of Artificial Intelligence Research, 55:317–359, 2016.

- Hu & Chen [2018] Hu, L. and Chen, Y. A short-term intervention for long-term fairness in the labor market. In Proceedings of the 2018 World Wide Web Conference, pp. 1389–1398, 2018.

- Joseph et al. [2016] Joseph, M., Kearns, M., Morgenstern, J. H., and Roth, A. Fairness in learning: Classic and contextual bandits. In Advances in Neural Information Processing Systems, pp. 325–333, 2016.

- Joulani et al. [2013] Joulani, P., Gyorgy, A., and Szepesvári, C. Online learning under delayed feedback. In International Conference on Machine Learning, pp. 1453–1461, 2013.

- Kannan et al. [2019] Kannan, S., Roth, A., and Ziani, J. Downstream effects of affirmative action. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pp. 240–248, 2019.

- Kleinberg et al. [2018] Kleinberg, J., Ludwig, J., Mullainathan, S., and Sunstein, C. R. Discrimination in the age of algorithms. Journal of Legal Analysis, 10, 2018.

- Kleinberg & Immorlica [2018] Kleinberg, R. and Immorlica, N. Recharging bandits. In 2018 IEEE 59th Annual Symposium on Foundations of Computer Science, pp. 309–319, 2018.

- Kleinberg et al. [2008] Kleinberg, R., Slivkins, A., and Upfal, E. Multi-armed bandits in metric spaces. In Proceedings of the fortieth annual ACM symposium on Theory of computing, pp. 681–690, 2008.

- Kocsis & Szepesvári [2006] Kocsis, L. and Szepesvári, C. Discounted ucb. In 2nd PASCAL Challenges Workshop, volume 2, 2006.

- Kolobov et al. [2020] Kolobov, A., Bubeck, S., and Zimmert, J. Online learning for active cache synchronization. In International Conference on Machine Learning, pp. 5371–5380. PMLR, 2020.

- Lai & Robbins [1985] Lai, T. L. and Robbins, H. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics, 6(1):4–22, 1985.

- Levine et al. [2017] Levine, N., Crammer, K., and Mannor, S. Rotting bandits. In Advances in neural information processing systems, pp. 3074–3083, 2017.

- Li et al. [2019] Li, F., Liu, J., and Ji, B. Combinatorial sleeping bandits with fairness constraints. IEEE Transactions on Network Science and Engineering, 2019.

- Liu et al. [2018] Liu, L. T., Dean, S., Rolf, E., Simchowitz, M., and Hardt, M. Delayed impact of fair machine learning. In International Conference on Machine Learning, pp. 3150–3158, 2018.

- Liu et al. [2020] Liu, L. T., Wilson, A., Haghtalab, N., Kalai, A. T., Borgs, C., and Chayes, J. The disparate equilibria of algorithmic decision making when individuals invest rationally. In Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, pp. 381–391, 2020.

- Liu [2017] Liu, Y. Fair optimal stopping policy for matching with mediator. In Uncertainty in Artificial Intelligence, 2017.

- Liu & Ho [2018] Liu, Y. and Ho, C.-J. Incentivizing high quality user contributions: New arm generation in bandit learning. In Thirty-Second AAAI Conference on Artificial Intelligence, 2018.

- Liu et al. [2017] Liu, Y., Radanovic, G., Dimitrakakis, C., Mandal, D., and Parkes, D. C. Calibrated fairness in bandits. Proceedings of the 4th Workshop on Fairness, Accountability, and Transparency in Machine Learning, 2017.

- Magureanu et al. [2014] Magureanu, S., Combes, R., and Proutiere, A. Lipschitz bandits: Regret lower bound and optimal algorithms. In Conference on Learning Theory, pp. 975–999, 2014.

- Mouzannar et al. [2019] Mouzannar, H., Ohannessian, M. I., and Srebro, N. From fair decision making to social equality. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pp. 359–368, 2019.

- Obermeyer et al. [2019] Obermeyer, Z., Powers, B., Vogeli, C., and Mullainathan, S. Dissecting racial bias in an algorithm used to manage the health of populations. Science, 366(6464):447–453, 2019.

- Ortner et al. [2012] Ortner, R., Ryabko, D., Auer, P., and Munos, R. Regret bounds for restless markov bandits. In International Conference on Algorithmic Learning Theory, pp. 214–228, 2012.

- Patil et al. [2020] Patil, V., Ghalme, G., Nair, V., and Narahari, Y. Achieving fairness in the stochastic multi-armed bandit problem. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pp. 5379–5386, 2020.

- Pike-Burke & Grünewälder [2019] Pike-Burke, C. and Grünewälder, S. Recovering bandits. arXiv preprint arXiv:1910.14354, 2019.

- Pike-Burke et al. [2018] Pike-Burke, C., Agrawal, S., Szepesvari, C., and Grunewalder, S. Bandits with delayed, aggregated anonymous feedback. In International Conference on Machine Learning, pp. 4105–4113, 2018.

- Schmit & Riquelme [2018] Schmit, S. and Riquelme, C. Human interaction with recommendation systems. In International Conference on Artificial Intelligence and Statistics, pp. 862–870, 2018.

- Seznec et al. [2019] Seznec, J., Locatelli, A., Carpentier, A., Lazaric, A., and Valko, M. Rotting bandits are no harder than stochastic ones. In The 22nd International Conference on Artificial Intelligence and Statistics, pp. 2564–2572, 2019.

- Slivkins [2014] Slivkins, A. Contextual bandits with similarity information. The Journal of Machine Learning Research, 15(1):2533–2568, 2014.

- Slivkins & Upfal [2008] Slivkins, A. and Upfal, E. Adapting to a changing environment: the brownian restless bandits. In Conference on Learning Theory, pp. 343–354, 2008.

- Tang & Ho [2019] Tang, W. and Ho, C.-J. Bandit learning with biased human feedback. In Eighteenth International Conference on Autonomous Agents and Multi-Agent Systems, 2019.

- Tekin & Liu [2010] Tekin, C. and Liu, M. Online algorithms for the multi-armed bandit problem with markovian rewards. In Proceedings of the 48th Annual Allerton Conference on Communication, Control, and Computing (Allerton), 2010.

- Verloop et al. [2016] Verloop, I. M. et al. Asymptotically optimal priority policies for indexable and nonindexable restless bandits. The Annals of Applied Probability, 26(4):1947–1995, 2016.

- Vernade et al. [2017] Vernade, C., Cappé, O., and Perchet, V. Stochastic bandit models for delayed conversions. arXiv preprint arXiv:1706.09186, 2017.

- Wang & Chen [2017] Wang, Q. and Chen, W. Improving regret bounds for combinatorial semi-bandits with probabilistically triggered arms and its applications. In Advances in Neural Information Processing Systems, pp. 1161–1171, 2017.

- Zhang et al. [2019] Zhang, X., Khaliligarekani, M., Tekin, C., et al. Group retention when using machine learning in sequential decision making: the interplay between user dynamics and fairness. In Advances in Neural Information Processing Systems, pp. 15243–15252, 2019.

- Zhang et al. [2020] Zhang, X., Tu, R., Liu, Y., Liu, M., Kjellström, H., Zhang, K., and Zhang, C. How do fair decisions fare in long-term qualification? 2020.

| Setup | Notations | Explanations | |

|---|---|---|---|

| basic setup | the number of (base) arms; time horizon | ||

| arm index; time round | |||

| probability simplex | |||

| discretization parameter | |||

| probability simplex after discretization with | |||

| meta arm/mixed strategy | |||

| optimal meta arm | |||

| optimal meta arm in | |||

| expected reward function of arm | |||

| arm ’s hyperparameter on tradeoff the expected reward and fairness | |||

| the probability on pulling arm , at time | |||

| the Lipschitz constant of | |||

| the Lipschitz constant of | |||

| the maximum | |||

| the realized reward at time | |||

| the importance weighted reward | |||

| the empirical reward mean of discretized arm | |||

| cumulative regret till time | |||

| the badness of meta arm | |||

| the meta arm deployed in time round | |||

| actions impact function | |||

| action dependent bandit | the number of times when pulling arm with prob till time | ||

| number of pulls of meta arm till time | |||

| the set of all meta arms which contain | |||

| total number of pulls of all meta arms in | |||

| for some | |||

| the empirical reward mean of meta arm | |||

| the expected reward of meta arm | |||

| history dependent bandit | time-discounted factor | ||

| the length of phase | |||

| the length of approaching stage | |||

| the ratio of estimation stages over each phase | |||

| the index of each phase | |||

| the set of all indexes which arm is pulled with prob | |||

| the time-discounted empirical frequency | |||

| the empirical reward mean of discretized arm in all estimation stages | |||

| the empirical reward mean of meta arm in all estimation stages | |||

| the number of rounds that arm is pulled with prob in the first phases | |||

Appendix A Related Work

Our learning framework is based on the rich bandit learning literature [3, 42]. However, instead of making the standard assumption of i.i.d. or adversarial rewards, we consider the setting in which the arm reward depends on the action history. The settings most similar to ours are non-stationary bandits, including restless bandits [60, 8, 25, 63, 21], in which the reward of each arm changes over time regardless of whether the arm is pulled, and rested bandits [43, 58, 17], in which the reward of arm evolves only when it is pulled. In contrast, our model encodes a generic dependency of actions taken in the past and our setting is sort of a mix between the above two. On one hand, the reward of each arm is restless, because even if we do not select a particular arm at step , the arm’s underlying state will continue to evolve (this is represented by our definition of ), which will change the expected reward to be seen in the future. On the other hand, the changing of rewards does depend on actions, so in this sense, it is related to rested bandit. Technically, due to the presence of historical bias, we allow the learner to learn the optimal strategy in a continuous space which is built on the probabilistic simplex over all arms. Meanwhile, our work distinguishes from prior works in that our proposed framework does not require the exact knowledge of dependency function except to the extent of a Lipschitz property and a convergence property.

Our formulation bears similarity to reinforcement learning since our impact function encodes memory (and is in fact Markovian [53, 62]), although we focus on studying the exploration-exploitation tradeoff in bandit formulation. Our techniques and approaches share similar insights with Lipschitz bandits [39, 59, 50, 16] and combinatorial bandits [11, 15, 13, 12] in that we also assume the Lipschitz reward structure and consider combinatorial action space. However, our setting is different since the arm reward explicitly depends on the learner’s action history. We have a detailed regret comparisons with the regret of directly applying techniques in combinatorial bandits to our setting in Section 4.

There are several works that formulate delayed feedback in online learning [35, 64, 56, 38, 55, 24, 10, 41]. We discuss the ones that are mostly related to ours. In particular, Pike-Burke et al. [56] considers the setting in which the observed reward is a sum of a number of previously generated rewards which happen to arrive in the given round. Joulani et al. [35] and Vernade et al. [64] focus on the setting where either feedback or reward is delayed. Our work differs from the above works in that, in our setting, the reward of the arm is influenced by the action history while the above works still consider stationary rewards (though the reward realization could be delayed). There have also been works that study the setting that explores different generative process of reward distribution of arms, e.g., the reward of the arm depends on strategic or biased human behavior [32, 48, 61]. The more closer works to ours include considering the arm of the reward is an increasing concave function of the time since it was last played Kleinberg & Immorlica [38], or decreases as it was played more time [43, 58]. Our work differs from the above in that we formalize an impact function that permits more general form of the reward evolvement as a function of the history of arm plays.

Our work also has implications in algorithmic fairness. one related line of works have studied fairness in the sequential learning setting, however they do not consider long-term impact of actions [34, 7, 49, 30, 27, 44]. For the explorations of delayed impacts of actions, the studies so far have focus on addressing the one-step delayed impacts or a multi-step sequential setting with full information [31, 33, 45, 51, 18, 6]. Our work differs from the above and studies delayed impacts of actions in sequential decision making under uncertainty.

Appendix B Lagrangian Formulation

While our setting follows standard bandit settings and aims to maximize the utility, it can be extended to incorporate fairness constraints as commonly seen in the discussion of algorithmic fairness. For example, consider the notion of group fairness, which aims to achieve approximate parity of certain measures across groups. Let be the fairness measure for group (which could reflect the socioeconomic status of the group). One common approach is to impose constraints to avoid the group disparity. Let be the tolerance parameter, the fairness constraints at can be written as: is unknown a priori and is dependent on the historical impact. Incorporating the fairness constraints would transform the goal of the institution as a constrained optimization problem:

We can then utilize the Lagrangian relaxation: impose the fairness requirement as soft constraints and obtain an unconstrained optimization problem with a different utility function. As long as we also observe (bandit) feedback on the fairness measures at every time step, the techniques developed in this work can be extended to include fairness constraints.

To simplify the presentation, we fix a time and drop the dependency on in the notations.

Definition B.1.

The Lagrangian where of our problem can be formulated as:

where . The notation is a pair of combination and is the index of each pair of this combination.

The problem then reduces to jointly maximize over and minimize over . Rearranging and with a slight abuse of notations, we have the following equivalent optimization problem:

| (8) |

where . Due to the uncertainty of reward function and fairness measure (recall that our fairness criteria is defined as the parity of socio-economic status cross different groups, which we can only observe the realization drawn from an unknown distribution), we treat the above optimization problem as a hyperparameter optimization: similar to choosing hyperparameters (the Lagrange multipliers: and ) based on a validation set in machine learning tasks. Therefore, given a fixed set of and , the problem in (8) can be reduced to the following:

| (9) |

Appendix C Negative Results

In this section, we show that an online algorithm which ignores its action’s impact would suffer linear regret. We consider two general bandit algorithms: TS (Thompson Sampling) and a mean-converging family of algorithms (which includes UCB-like algorithms). These are the two most popular and robust bandit algorithms that can be applied to a wide range of scenarios. We prove the negative results respectively. In particular, we construct problem instances that could result in linear regret if the deployed algorithm ignore the action’s impact.

Example 1.

Considering the following Bernoulli bandit instance with two arms, indexed by arm 1 and arm 2, i.e., . For any , define the expected reward of each arm as follows:

-

arm 1:

-

arm 2:

It is easy to see that is the optimal strategy for the above bandit instance.

We first prove the negative result of Thompson Sampling using the above example. The Thompson Sampling algorithm can be summarized as below.

Lemma C.1.

For the reward structure defined in Example 1, Thompson Sampling would suffer linear regret if it doesn’t consider the action’s impact it deploys at every time round, namely, it takes the sample mean as the true mean reward of each arm.

Before we proceed, we first prove the following strong law of large numbers in Beta distribution. We note that the below two lemmas are not new results and can be found in many statistical books. We provide proofs here for the sake of making the current work self-contained.

Lemma C.2.

Consider the Beta distribution Beta whose pdf is defined as , where is the beta function, then for any positive such that , when , the limit of can be characterized by Dirac delta function .

Proof.

By Stirling’s approximation, we can write the asymptotics of beta function as follows:

Thus, when , i.e., for large and , we can approximate the pdf in the following:

where . It’s easy to see that has a unique maximum at , by invoking Lemma C.3 will complete the proof. ∎

Lemma C.3.

Let be any bounded measurable non-negative function with a unique maximum at , and suppose is continuous at . For define where normalizes such that . Consider any continuous function defined on and , then we have and .

Proof.

For any , we have

For any , and due to the continuous property of on , which further implies that there exists a constant such that whenever . Thus, given , we have

It suffices to show that the second term in RHS of above inequality will converge to 0 as . Let denote the norm of when is restricted to . Note that for any nonnegative integrable functions , we have

Recall the definition of , thus, we have , which immediately showing that

which further implies that . Thus, there must exist such that ,

| (10) |

Since , we then have , this implies the second term of RHS of (C) converging to 0 as . ∎

We now ready to prove Lemma C.1.

Proof.

We prove this by contradiction. Let denote the expected regret incurred by TS up to time round , and denote the number of rounds when the algorithm deploys the (mixed) strategy . Furthermore, let denote the received of arm up to time round . Recall that in Thompson Sampling, we have . By the reward function defined in Example 1, it’s immediate to see that

Now suppose Thompson Sampling achieves sublinear regret, i.e., , which implies following

Thus, by the strong law of large numbers and invoking Lemma C.2, the sample and will converge as follows:

Then it’s almost surely that . This leads to following holds for sure

Thus, consider the regret incurred from the th round to th round, the regret will be

where the second equality follows that holds almost surely from to . This shows that , which contradicts that the algorithm achieves the sublinear regret. ∎

We now show that a general class of algorithms, which are based on mean-converging, will suffer linear regret if it ignores the action’s impact. This family of algorithms includes UCB algorithm in classic MAB problems.

Definition C.4 (Mean-converging Algorithm [57]).

Define as the set of time rounds such the arm is chosen. Let be the empirical mean of arm up to time . The mean-converging algorithm assigns for each arm if following holds true:

-

is the function of and time ;

-

if .

Lemma C.5.

For the reward structure defined in Example 1, the mean-converging Algorithm will suffer linear regret if it mistakenly take the sample mean as the true mean reward of each arm.

Proof.

We prove above lemma by contradiction. Let denote the number of plays with deploying the strategy by algorithm till time . Suppose a mean-converging Algorithm achieves sublinear regret, then it must have and . By the definition of mean-converging algorithm and recall the reward structure defined in Example 1, the score assigned to arm 1 by the algorithm must be converging to 1, and the score of assigned to arm 2 must be converging to 0.5. By the strong law of large numbers, it suffices to show that , which implies the algorithm would suffer linear regret after time rounds and thus completes the proof. ∎

Appendix D Missing Proofs for Action-Dependent Bandits

D.1 The naive method that directly utilize techniques from Lipschitz bandits

We first give a naive approach which directly applies Lipschitz bandit technique to our action-dependent setting. Recall that each meta arm specifies the probability for choosing each base arm . We uniformly discretize each into intervals of a fixed length , with carefully chosen such that is an positive integer. Let be the space of discretized meta arms, i.e., for each , and for all . We then run standard bandit algorithms on the finite set .

There is a natural trade-off on the choice of , which controls the complexity of arm space and the discretization error. show that, with appropriately chosen , this approach can achieve sublinear regret (with respect to the optimal arm in the non-discretized space ).

Lemma D.1.

Let . Running a bandit algorithm which achieves optimal regret on the strategy space attains the following regret (w.r.t. the optimal arm in non-discretized ): .

Proof.

As mentioned, we uniformly discretize the interval of each arm into interval of a fixed length . The strategy space will be reduced as , which we use this as an approximation for the full set . Then the original infinite action space will be reduces as finite , and we run an off-the-shelf MAB algorithm , such as UCB1 or Successive Elimination, that only considers these actions in . Adding more points to makes it a better approximation of , but also increases regret of on . Thus, should be chosen so as to optimize this tradeoff. Let denote the best strategy in discretized space . At each round, the algorithm can only hope to approach expected reward , and together with additionally suffering discretization error:

Then the expected regret of the entire algorithm is:

where is the total reward of the algorithm, and is the regret relative to . If attains optimal regret on any problem instance with time horizon and arms, then,

Thus, we need to choose to get the optimal trade-off between the size of and its discretization error. Recall that is Lipschitz-continuous with the constant of , thus, we could bound the by restricting to be nearest w.r.t . Let , then it’s easy to see that

Thus, the total regret can be bounded above from:

By choosing we obtain:

where . ∎

D.2 Missing Discussions and Proofs of Theorem 4.2

Step : Bounding the error of .

For any , define the empirical reward . The first step of our proof is to bound for each meta arm with high probability.999We use to denote the estimation error, as has been used as the discretization parameter. Using the Hoeffding’s inequality, we obtain

where . By choosing in the above inequality, for each meta arm at time , we have that , with the probability at least .

Step : Bounding the probability on deploying suboptimal meta arm.

With the above high probability bound we obtain in Step , we can construct an UCB index for each meta arm :

| (11) |

The above constructed UCB index gives the following guarantee:

Lemma D.2.

At any time round , for a suboptimal meta arm , if it satisfies , then with the probability at least . Thus, for any ,

where denotes the badness of meta arm .

Proof.

We prove this lemma by considering two “events” which occur with high probability: (1) the UCB index of each meta arm will concentrate on the true mean utility of ; (2) the empirical mean utility of each meta arm will also concentrate on the true mean utility of . We then show that the probability of either one of the events not holding is at most . By a union bound we prove above desired lemma.

| By Event 1 | ||||

| By Event 2 | ||||

where . The first inequality (By Event 1) comes from that and the probability of third inequality or fifth inequality not holding is at most . ∎

Intuitively, Lemma D.2 essentially shows that for a meta arm , if its is sufficiently sampled with respect to , that is, sampled at least times, we know that the probability that we hit this suboptimal meta arm is very small.

Step : Bounding the .

Ideally, we would like to bound the number of the selections on deploying the suboptimal meta arm, i.e., , in a logarithmic order of . However, if we proceed to bound this by separately considering each meta arm, the final regret bound will have an order with exponent in since the number of meta arms grows exponentially in . Instead, we turn to bound . Recall that by the definitions of and , the pulls of is upper bounded by its . This quantity will help us to reduce the exponential to the polynomial . This is formalized in the following lemma.

Lemma D.3.

For each suboptimal meta arm , we have that .

Proof.

To simplify notations, for each discretized arm , we define the notion of super set which contains all the meta arms that include this discretized arm. For suboptimal meta arm and its , we have

We add in the first equality to account for (step (D.2)) initial pull of every discretized arm by the algorithm (the initialization phase). In step (D.2), suppose for contradiction that the indicator takes value of at more than time steps, where . Let be the time step at which this indicator is for the -th time. Then the number of pulls of all meta arms in is at least times until time (including the initial pull), and for all , which implies . Thus, the indicator cannot be for any , contradicting the assumption that the indicator takes value of more than times. This bounds by . In step (D.2), we apply the lemma D.2 to bound the first conditional probability term and use the fact that the probabilities cannot exceed to bound the second probability term. ∎

We use this connection in the following step to reduce the computation of regret on pulling all suboptimal meta arms so that to calculate the regret via the summation over discretized arms.

Wrapping up: Proof of Theorem 4.2.

We are now ready to prove Theorem 4.2. We first define notations that are helpful for our analysis. To circumvent the summation over all feasible suboptimal arms , for each discretized arm , we define the notion of super set which contains all suboptimal meta arms that include this discretized arm. With a slight abuse of notations, we also sort all meta arms in as in ascending order of their expected rewards, where is the cardinality of the super set . For , we also define where , and specifically ; . Let denote the regret relative to the best strategy in the discretized space parameterized by . With these notations, we first establish the following instance-dependent regret.

Lemma D.4.

Following the UCB designed in (11), we have the following instance-dependent regret on the discretized arm space: , where .

Proof.

Note that by definition, we can compute the regret as follows:

| (12) |

Observe that, by Lemma D.3, for each discretized arm , there are two possible cases:

-

There exists a meta arm , and its . Then by linearity of expectation, we can bound the expectation of total number of pulls for all as follows

-

There exists no meta arm , and for each is . In this case, for each , there always exists another discretized arm that is included in such that but . Thus, for each , together with other meta arms which also include discretized arm as , we have that

The above observations imply that even though we can not find any meta arm in such that , we can always carry out similar analysis by finding another discretized arm but , such that . Thus, for each discretized arm , we can focus on the case where is able to attain the minimum for some . For analysis convenience, instead of looking at the counter of , i.e., , we will define a counter for each discretized arm and the value of at time is denoted by . The update of is as follows: For a round (here is the number of rounds needed for initialization), let be the meta arm selected in round by the algorithm. Let . We increment by one, i.e., . In other words, we find the discretized arm with the smallest counter in and increment its counter. If such is not unique, we pick an arbitrary discretized arm with the smallest counter. Note that the initialization gives . It is easy to see that for any , we have .

With the above change of counters, Lemma D.2 and Lemma D.3 then have the implication on selecting discretized arm given its counter . To see this, for each , we define sufficient selection of discretized arm with respect to as being selected times and ’s counter being incremented in these selected instances. Then Lemma D.2 tells us when is sufficiently selected with respect to , the probability that the meta arm is selected by the algorithm is very small. On the other hand, when ’s counter is incremented, but if is under-selected with respect to , we incur a regret of at most for some .

Define , the number of selection that is considered sufficient for a meta arm with reward away from the optimal strategy with respect to time horizon . With the above analysis, we define following two situations for the counter of each discretizad arm:

Clearly, we have . With these notations, we can write (12) as follows:

| (13) |

The proof of this lemma will complete after establishing following two claims:

| Claim 1: | (14) | |||

| Claim 2: | (15) |

We now first prove the Claim 1 as in (14), i.e., for any , we have following upper bound over counters of sufficiently selected discretized arms. To see this, by definition of , it reduces to show that for any ,

where the last step (D.2) is due to Lemma D.2, thus (14) follows from a simple series bound.

We now proceed to analyze the discretized arms that are not sufficiently included in the meta arm chosen by the algorithm and prove the Claim 2 as in (15). For any under-selected discretized arm , its counter will increase from to . To simplify the notation, we set . Suppose that at round , is incremented, and for some . Notice that we are only interested in the case that is under-selected. In particular, if this is indeed the case, for some . (Otherwise, is sufficiently selected based on the counter value .) Thus, we will suffer a regret of (step (D.2)). As a result, for counter , we will suffer a total regret for those playing suboptimal meta arms that include under-selected discretized arms at most in rounds that is incremented (step (D.2)). In what follows we establish the above analysis rigorously.

Now, we can compute the regret incurred by selecting the meta arm which includes under-selected discretized arms:

| (16) |

Equipped with the above set of results, the bound of regret (13) follows by combing the bounds in (14) and (15). ∎

To achieve instance-independent regret bound, we need to deal with the case when the meta-arm gap is too small, leading the regret to approach infinite. Nevertheless, one can still show that when , the regret contributed by this scenario scales at most at time horizon .

Lemma D.5.

Following the UCB designed in (11), we have: .

Proof.

Following the proof of Lemma D.4, we only need to consider the meta arms that are played when they are under-sampled. We particularly need to deal with the situation when is too small. We measure the threshold for based on , i.e., the counter of disretized arm at time horizon . Let be a set of possible counter values at time horizon . Our analysis will then be conditioned on the event that . By definition,

| (17) |

We define

,

i.e., .

To achieve instance-independent regret bound, we consider following two cases:

Case 1: , we thus have

| (18) |

Case 2: . Let . Observe that we have and the counter never go beyond , we thus have

| (19) |

Thus, combining (18) and (19), we have

where (D.2) is by Jesen’s inequality and . Put all pieces together, we have the instance-independent regret bound as stated in the lemma. Observe that the final inequality does not depend on the event , we thus can drop this conditional expectation. ∎

With the above lemma in hand, picking will give us desired result in Theorem 4.2. 101010Here the choice of absorbs Lipschitz constant of .

Remark D.6.

When only one arm is activated according to , the Hoeffding’s inequality is adapted as follows:

The below analysis carries over with accordingly changing to , and the condition of in Lemma D.2 is changed to to account for larger . As a result, the instance-independent regret bound in Lemma D.5 is changed to . Together with the discretization error, one can then optimize the choice of to get regret bound.

D.2.1 Regret Bound Comparison with [13]

In the work [13], the authors study the setting when pulling the meta arm, each base arm in (or possibly other base arm) this meta arm will be triggered and played as a result. Back to our setting, this is saying that when pulling a meta arm , each base arm will be triggered with its corresponding probability (discretized arm) . The authors in [13] discuss a general setting which allows complex reward structure where only requires two mild conditions. In particular, one of the condition they need for expected reward of playing a meta arm is the bounded smoothness (cf., Definition 1 in [13].). In the Theorem 2 of [13], the authors give results when the function used to characterize bounded smoothness is for some and . In more detail, they achieve a regret bound where is the minimum triggering probability across all base arms and is the largest badness of the suboptimal meta arm in discretized space. 111111For simplicity, the bound we present here omits a non-significant term. Adapt to our setting, by inspection, we have , , , and . Substituting these values to the above bound, ignoring constant factors and combining with the discretization error, we have

Picking will give us result.

Appendix E Proof of Theorem 5.1 for History-dependent Bandits

In this section, we provide the analysis of Theorem 5.1. The analysis follows a similar structure to the one used in the proof of the regret bound in Theorem 4.2. However, due to the existence of historical bias, we need to perform a careful computation when handling the high-probability bounds. Specifically, we need to prove that, after deploying consecutively for moderate long rounds (tuning ), the approximation error is small enough. The analysis is provided below.

Step 1: Bounding the small error of with high-probability.

Our first step is to ensure the empirical mean reward estimation we obtain from the information we collected in all the estimation stages will approximate well the true mean of meta arm we want to deploy.

To return a high-probability error bound, we first bound the approximation error incurred due to the dependency of history of arm selection (“historical bias"). This is summarized below.

Lemma E.1.

Keeping deploying in the approaching stage with rounds, and collect all reward feedback in the following estimation stage for the empirical estimation of rewards generated by , one can bound the approximation error as follows:

where denote the empirical mean of rewards if the instantaneous reward is truly sampled from mean reward function according to .

Proof.

The proof of this lemma is mainly built on analyzing the convergence of via pulling the base arms with the same probability consistently. For the ease of presentation, let us suppose and let be the total number of estimation rounds in the first phases. Thus, at the end of the approaching stage, we have

where . Recall that during the approaching stage, we consistently pull arm with the same probability . Thus, the approximation error of w.r.t. can be computed as:

Recall that . In the estimation stage, we approximate all the realized utility as the utility generated by the meta arm . However, note that we actually cannot compute the empirical value of , instead, we use of each phase as an approximation of , i.e., we approximate all as and use as the approximation of . Recall that for any , we have:

Thus, the approximation error on the empirical estimation can be computed as follows:

∎

With the approximation error at hand, we can then bound the error of with high probability:

Lemma E.2.

With probability at least , we have

where .

Step 2: Bounding the probability on deploying suboptimal meta arm.

Till now, with the help of the above high probability bound on the empirical reward estimation, the history-dependent reward bandit setting is largely reduced to an action-dependent one with a certain approximation error. Then, similar to our argument on upper bound of action-dependent bandits, we have the following specific Lemma for history-dependent bandits:

Lemma E.3.

At the end of each phase, for a suboptimal meta arm , if it satisfies , then with the probability at least , we have , i.e.,

Proof.

To prove the above lemma, we construct two high-probability events. Event 1 corresponds to that the UCB index of each meta arm concentrates on the true mean utility of ; Event 2 corresponds to that the empirical mean utility of each approximated meta arm concentrates on the true mean utility of . The probability of Event 1 or Event 2 not holding is at most . By the definition of the constructed UCB, we’ll have

| By Event 1 | ||||

| By Event 2 |

where the first inequality (E) is due to , and the probability of step (By Event 1) or (By Event 2) not holding is at most . ∎

The above lemma implies that we will stop deploying suboptimal meta arm and further prevent it from incurring regret as we gather more information about it such that .

Step 3: Bounding the .

The results we obtain in Step 2 implies following guarantee:

Lemma E.4.

For each suboptimal meta arm , we have following:

Proof.

For notation simplicity, suppose . For each suboptimal arm , and suppose there exists such that , then