Optimizing effective numbers of tests by vine copula modeling

Abstract

In the multiple testing context, we utilize vine copulae for optimizing the effective number of tests. It is well known that for the calibration of multiple tests (for control of the family-wise error rate) the dependencies between the marginal tests are of utmost importance. It has been shown in previous work, that positive dependencies between the marginal tests can be exploited in order to derive a relaxed Šidák-type multiplicity correction. This correction can conveniently be expressed by calculating the corresponding ”effective number of tests” for a given (global) significance level. This methodology can also be applied to blocks of test statistics so that the effective number of tests can be calculated by the sum of the effective numbers of tests for each block. In the present work, we demonstrate how the power of the multiple test can be optimized by taking blocks with high inner-block dependencies. The determination of those blocks will be performed by means of an estimated vine copula model. An algorithm is presented which uses the information of the estimated vine copula to make a data-driven choice of appropriate blocks in terms of (estimated) dependencies. Numerical experiments demonstrate the usefulness of the proposed approach.

keywords:

Dißmann Algorithm , family-wise error rate , global significance level , Kendall’s , local significance levels , multiple testingMSC:

[2010] 62J15 , 62H20 , 62E17[table]font=scriptsize,style=plaintop

1 Introduction

Dependence modeling by means of copula functions has recently received a lot of attention in multiple testing, see Dickhaus and Gierl (2013), Bodnar and Dickhaus (2014), Schmidt et al. (2014), Schmidt et al. (2015), Stange et al. (2015), Cerqueti and Lupi (2018), Neumann et al. (2019), and Sections 2.2.4 and 4.4 of Dickhaus (2014). For example, Dickhaus and Gierl (2013) have explicitly shown that the copula approach leads to the most general construction method for multivariate single-step multiple tests under known univariate marginal null distributions of test statistics or -values, respectively.

In the present work, we contribute to copula-based multiple testing by demonstrating how vine copula models (cf. Czado (2019) and references therein) can be used to optimize effective numbers of tests in the sense of Dickhaus and Stange (2013) for control of the family-wise error rate (FWER). Assuming that the dependency structure among the test statistics is a nuisance parameter (of potentially infinite dimension), we propose to fit a regular vine copula model to the observed data. Under certain structural assumptions, this entails an approximation of the joint null distribution of the vector of test statistics, which can then be used to calibrate a multivariate multiple test for FWER control. By means of computer simulations, we will demonstrate that this strategy clearly improves existing approaches. In particular, choosing blocks of highly dependent test statistics by means of the estimated vine copula can lead to a substantial increase in statistical power when compared with a naively chosen block structure.

The rest of the material is structured as follows. In Section 2, we introduce our basic statistical model, the concept of effective numbers of tests, and the vine copula modeling technique. Section 3 contains our proposed methodology for combining these concepts. Some remarks on the implementation are provided in Section 4. Section 5 presents numerical examples, and we conclude with a discussion in Section 6.

2 Notation and preliminaries

2.1 Multiple testing

Throughout the work, we will assume the following statistical model.

Model 1.

Let denote a sample size, and assume that we can observe stochastically independent and identically distributed (i.i.d.) random vectors , where takes values in for and . Altogether, this entails an observable random matrix

taking its values in the sample space . Assume that we have uncertainty about the distribution of . We express this by writing , where is a parameter vector, such at each refers to the marginal distribution of , . Moreover, denotes the copula of . For the distribution of the entire sample represented by , we write . Assume that we would like to test (simultaneously) null hypotheses , where each refers to , . We may hence interpret each as a subset of . The corresponding alternative hypothesis will be denoted by . For testing versus , we assume that a real-valued test statistic is at hand, where , . The vector of all test statistics will be denoted by . The multiple test based on will be denoted by , where the event means that we reject in favor of , . For the calibration of , we aim at controlling the FWER, which is given by

where denotes the index set of true null hypotheses under . For a given constant , we say that controls the FWER at level under and , if holds true.

Model 1 is a standard multiple testing model in the context of studies with endpoints, which are all measured for the same observational units; see, among many others, Dickhaus and Stange (2013), Stange et al. (2015), and Neumann et al. (2019). Under Model 1, we make the following general assumptions.

- (GA1)

-

For all , the test statistic tends to larger values under the alternative . We thus reject in favor of for large values of .

- (GA2)

-

The copula is a nuisance parameter in the sense that it does not depend on .

- (GA3)

-

There exists a parameter value in the global null hypothesis which maximizes the FWER of the multiple test which is under consideration. Such a parameter value is often called a ”least favorable (parameter) configuration”, LFC for short.

- (GA4)

-

For all , the marginal distribution of under is known, and it only depends on the -th component .

Theorem 1 (Effective numbers of tests, Theorem 3.1 in Dickhaus and Stange (2013)).

Under our general assumptions (GA1) - (GA4), let be such, that fulfills the MSMi property in the sense of Definition 2.2 of Dickhaus and Stange (2013) for some under . Define critical values such that for a fixed local significance level in each marginal. Define also for :

-

(i)

In case of , set . Otherwise, let

Moreover, for every , define

Then it holds

(1) for an ”effective number of tests” of order , given by

-

(ii)

Optimized bounds and :

If, for every permutation , the MSMi property is preserved if is replaced by , it is possible to optimize and, consequently, in that the maximum strength of positive dependence between and the preceding , , is used. For , this leads to an optimized versionAn optimized effective number of tests of order is given by .

Remark 1.

-

(a)

The MSMi property is a positive dependency property. In plain terms, it means that a particular test statistic tends to small values, given the information that test statistics with have realized small values.

-

(b)

The bound on the right-hand side of (1) is of Šidák-type, where is replaced by .

-

(c)

It holds that . If , this has the interpretation that we ”effectively” only have to correct for tests, due to certain similarities between them.

-

(d)

In practice, we have to find the value of such that the right-hand side of (1) equals the pre-defined global significance level . This can be achieved by starting with a reasonable upper bound for , and iteratively evaluating (1) and decreasing until the aforementioned equality holds (approximately).

2.2 Vine copulae

Here, we collect some essential definitions and properties of (regular) vines and vine copulae. For more details, see Chapter 5 in Czado (2019) and the references therein.

Definition 1 (Vine).

Let . The set is called a vine of elements, where denotes the set of edges of , if

-

(i)

is a connected tree with nodes and edges , and

-

(ii)

is a tree with nodes , for .

If it holds, in addition, that

-

(iii)

for all and , where denotes the symmetric difference,

then is called a regular vine (R-vine). As usual in graph theory, we call the number of edges which are connected to a particular node the degree of that node.

Definition 2 (Complete union, conditioning set, conditioned set).

Let be a given vine of elements, and let be a given edge. The set is called the complete union of . In words, denotes the set of nodes in the first tree which can be ”reached” from . Letting , we call the conditioning set of . Finally, the conditioned set of is defined by

where for .

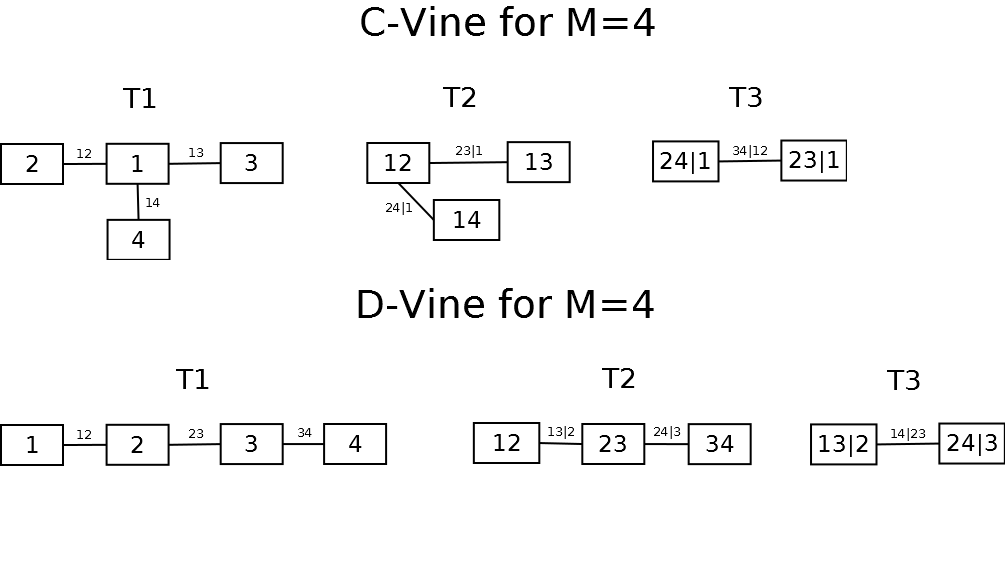

Example 1.

Let . Figure 1 graphically displays two R-vine structures of four elements.

-

(a)

The upper panel in Figure 1 displays a C-vine structure for . A C-vine is a regular vine fulfilling that every tree has a node with degree , for .

-

(b)

The lower panel in Figure 1 displays a D-vine structure for . A D-vine is a regular vine fulfilling that all nodes in have a degree of at most .

Each edge in Figure 1 is labeled such, that the elements of the corresponding conditioning set are provided after the ””, and the elements of the corresponding conditioned set are provided before the ””. This kind of notation will be used throughout the remainder.

Definition 3 ((Regular) Vine distribution).

Let be a given vine of elements. The vine distribution induced by is given by the so-called ”pair copula construction”, meaning that a bivariate copula is attached to each edge . Formally, a triple is called a regular vine distribution, if is a vector of continuous and invertible cumulative distribution functions (cdfs) on , is a regular vine in dimension , and is a set of bivariate copula functions.

We say that the -valued random vector possesses the regular vine distribution , if is the marginal cdf of for all , and if is the (conditional) bivariate copula of given for each edge .

The tuple will be referred to as a regular vine copula throughout the remainder.

Theorem 2 (Corollary 1 in Bedford and Cooke (2001)).

Let be a regular vine of elements. Assume that the (conditional) copula possesses a copula density for each edge with conditioning set and conditioned elements and . Furthermore, assume that the cdf admits a Lebesgue density for each . Then, there exists a unique probability distribution on which has the Lebesgue density

| (2) |

Hence, under the aforementioned assumptions there exists an -valued random vector possessing the regular vine distribution , and is the conditional cdf of given , where and .

3 Proposed methodology

The following lemma, the proof of which is deferred to A, connects the concept of effective numbers of tests with copula theory.

Lemma 1.

Let and . For all , denote by the univariate marginal cdf of under , and assume that is continuous and strictly increasing on its support. Furthermore, let , , for a fixed local significance level . To avoid pathologies, assume that . Then we have, that

| (3) |

As mentioned in part (ii) of Theorem 1, it is advantageous for an optimization (in terms of statistical power) of the effective number of tests to find a structure / pattern in the degree of dependency among the test statistics . This means, that we aim at subdividing the total index set into blocks, such that the inner-block dependencies between test statistics are strong, while test statistics belonging to different blocks exhibit weak dependencies or are even stochastically independent. As argued in Section 5 of Stange et al. (2016), in some applications like, for instance, genetic association analyses, an appropriate block structure or at least appropriate block lengths can be deduced from expert knowledge about the experiment. An effective number of tests of appropriate order can then be calculated for every block separately. Letting denote the effective number of tests of order in block , where is the total number of blocks, we can take the number

| (4) |

as a (conservative) approximation of the optimized total effective number of tests of order . In this, the term ”conservative” means, that under MSMi the sum in (4) is guaranteed to be not smaller than ; see Section 5 in Stange et al. (2016) for further details.

Our proposed methodology is to apply vine copula modeling for (i) finding the appropriate block structure, and (ii) estimating the copulae appearing in (3). The underlying pair copula construction can be exploited in a greedy-style algorithmic manner to determine an appropriate block structure. This property makes the vine approach particularly well-suited in our context. In the remainder of this section, we explain the two steps indicated above in more detail.

For automated model selection and pair copula estimation, we employ Algorithm 3.1 of Dißmann et al. (2013), referred to as ”The Dißmann Algorithm” in Section 8.3 of Czado (2019). This algorithm delivers an estimate of the vine structure underlying the data, as well as an estimate of the family of pair copulae underlying the construction in (2). Furthermore, for regularization purposes, we choose a truncation level and finally work with the approximation

| (5) |

where the ’s refer to the estimated vine structure . A formal, information criterion-based method for choosing has been proposed by Nagler et al. (2019). However, from our experience, the choice often works well in practice.

Remark 2.

- (i)

-

(ii)

Comparing (5) with (2) and noticing that the density of the independence (or: product) copula is identically equal to one on the unit cube, it becomes clear that in (5) only the first (estimated) trees of are explicitly taken into account. In the remaining trees, all pair copulae are set to the independence copula. This strategy is justified, because the Dißmann Algorithm is designed to capture the most pronounced dependencies in the first trees.

-

(iii)

The estimated (joint) density refers to the distribution of . For calibrating the multiple test , though, we need the null distribution of the vector of test statistics. However, since is a given function of the (i.i.d.) data vectors , the dependency structure among the components of already determines the dependency structure among . Even if the mapping is complicated, we can approximate the joint distribution of the random vector under with arbitrary precision by means of a Monte Carlo simulation, once the dependency structure among the components of has been estimated.

Based on the estimated quantities and , we propose the following algorithm for finding appropriate blocks for the operationalization of (4). In Algorithm 1, we assume that the blocks (or groups) are all of (approximately) equal size.

Algorithm 1 (Greedy algorithm for determining a grouping of the test statistics).

-

The estimated quantities and , and the targeted group size.

-

Grouping of the test statistics, which correspond to the nodes in the first tree in .

-

1)

Find the pair of coordinates with largest estimated Kendall’s coefficient (according to ), and assign the two corresponding nodes to Group 1.

-

2)

Find all nodes, which share an edge (according to ) with a node in Group 1, but are themselves not in Group 1 (yet). We call these nodes the neighbors.

-

3)

Choose the neighbor with the strongest dependency with Group 1, and assign this neighbor to Group 1. This means, that we find

(6) where denotes the neighboring node of from Group 1, and denotes the set of nodes from Group 1 which are neighbors of . In (6), denotes the estimated (unconditional) Kendall’s coefficient of and , and denotes the estimated conditional Kendall’s coefficient of and given .

-

4)

Repeat 3), until Group 1 has reached the targeted group size.

-

5)

For Group 2 until Group (last group), carry out steps 1) to 4) analogously by considering only those nodes, which have not been assigned to any group yet. If no neighbors are found, go to the next group.

-

6)

If there are still nodes left which have not been assigned to any group yet, assign them randomly to those groups which have not yet reached the targeted group size.

Remark 3.

-

(i)

The neighboring node appearing in (6) is uniquely determined, because the tree contains no cycle.

-

(ii)

When constructing Group 1, it is guaranteed that a neighbor can be found.

-

(iii)

In the case that is fixed in advance, the targeted group size is .

-

(iv)

For Algorithm 1, only the first two trees in , together with their corresponding pair copulae from , are needed.

-

(v)

For any given copula on , the corresponding Kendall’s coefficient is given by

with .

4 Details on the implementation

Summarizing the proposed methodology presented in Sections 2 and 3, we obtain the following data analysis workflow.

Scheme 1.

Given are the realized data matrix , the null hypotheses , the mappings (test statistics) , their univariate marginal cdfs under , the FWER level , the order for the effective numbers of tests, and the number of blocks.

-

1)

In order to have (approximately) marginally uniformly distributed data as input for the Dißmann Algorithm, we transform the data points with their empirical marginal cdfs, meaning that we set

-

2)

We apply the Dißmann Algorithm to obtained in Step 1), and receive the estimated quantities and . The Dißmann Algorithm also computes and outputs all estimated (conditional and unconditional) Kendall’s coefficients pertaining to ; cf. Part (v) of Remark 3.

- 3)

-

4)

We carry out a Monte Carlo simulation for approximating the joint distribution of under the global null hypothesis . In this simulation, we combine the univariate marginal cdfs under with the estimated vine copula from Step 2).

- 5)

-

6)

We reject the global null hypothesis , iff there exists an with . Furthermore, we reject all individual null hypotheses with , .

In the remainder of this section, we briefly describe how we have implemented this workflow in the statistical computing environment R (https://www.r-project.org/).

4.1 Implementation of the Dißmann Algorithm

The Dißmann Algorithm is included in the R package VineCopula (https://cran.r-project.org/web/packages/VineCopula/); see the function RVineStructureSelect in that package. As one argument, the transformed data are required. As another argument, copula families are required, from which the bivariate copulae appearing in are chosen. For our numerical experiments described in Section 5, we have taken the following families.

-

0)

Independence copula (product copula),

-

1)

Gaussian copula family,

-

3)

Clayton copula family,

-

4)

Gumbel copula family,

-

5)

Frank copula family,

-

6)

Joe copula family,

together with their rotated versions. The numbering in the above list corresponds to that in the R package VineCopula. The package also offers further families, but we have worked only with the aforementioned ones. Finally, the function RVineStructureSelect requires the specification of the truncation level . In our experiments, we have set ; cf. Part (iv) of Remark 3.

4.2 Implementation of the other steps in Scheme 1

A custom implementation of Algorithm 1 is available from the authors upon request. Notice, that all required quantities for Algorithm 1 (namely, , , as well as the estimated (conditional and unconditional) Kendall’s coefficients pertaining to ) are delivered by the Dißmann Algorithm. Hence, it essentially remains to code the neighbor search and the evaluation of (6).

For the simulation in Step 4) of Scheme 1, we have used the function RVineSim from the

R package VineCopula. This function generates pseudo-random vectors from the estimated vine copula. Combining this with the principle of quantile transformation yields pseudo-random vectors which behave like realizations of under .

Many further resources for working with vine copulae can be found at http://www.vine-copula.org/.

5 Numerical experiments

5.1 Multivariate Gaussian model

In our first numerical example, we let . We assume that follows the -variate normal distribution with mean vector and covariance matrix . In our simulations, we set for and for . The covariance matrix is given by

The marginal test problems of interest are assumed to be versus for . The vector is given by , where , for . We let . Making use of Propositions 4.1 and 4.2 in Dickhaus (2014), it can be shown that fulfills the MSM2 property under , and that this property is preserved under coordinate permutations.

Analyzing the structure of , we see that there are three blocks of highly correlated coordinates, namely , , and . The goals of our computer simulations are to assess (i) how reliably our proposed methodology can identify these blocks, and (ii) how much gain in statistical power can be achieved by exploiting the dependency structure. We performed simulation runs for sample sizes . The number of groups has been set to , with a targeted group size of five per group.

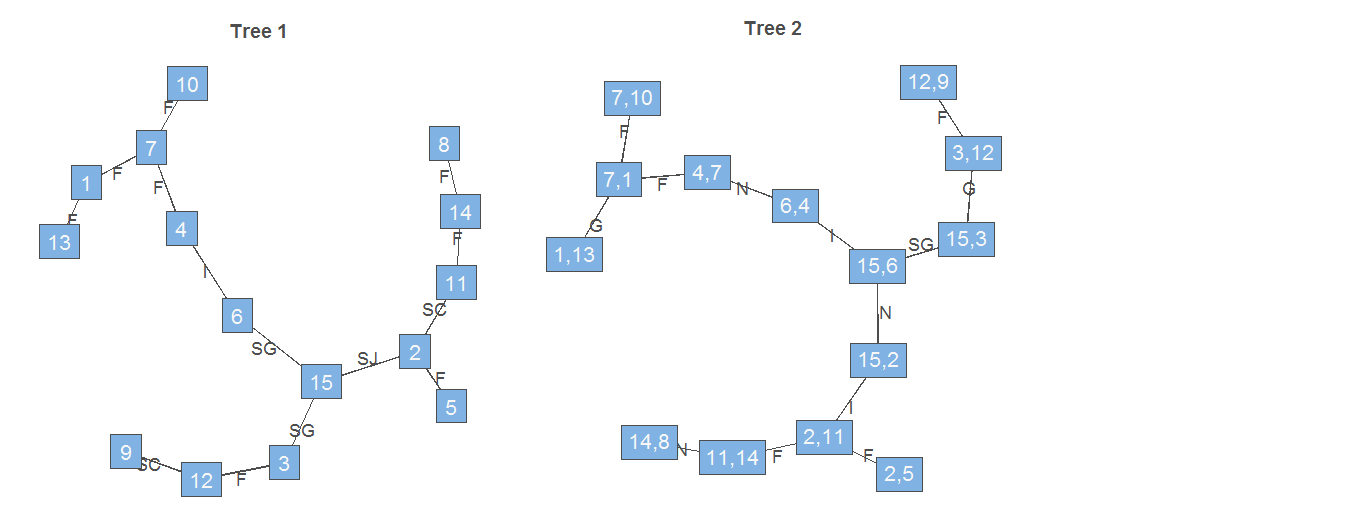

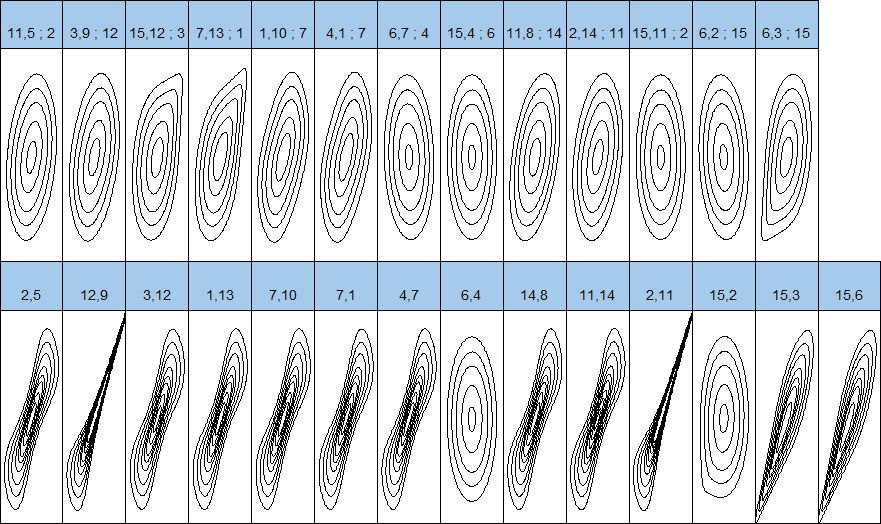

For one particular simulation run with , Figure 2 displays the two estimated trees in . Furthermore, Figure 3 displays the contour lines of the estimated pair copulas in .

Tables 1 - 3 display our (averaged) simulation results. Since all test statistics have the same null distribution, we have chosen . The rows labeled ”fixed groups” refer to the fixed group structure , , and .

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 15 | 15 | 15 |

| fixed groups | 11.84 | 11.79 | 11.72 |

| chosen groups | 8.63 | 8.75 | 8.8 |

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 2.928 | 2.928 | 2.928 |

| fixed groups | 2.857 | 2.856 | 2.854 |

| chosen groups | 2.755 | 2.759 | 2.761 |

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 9 | 22.625 | 37.875 |

| fixed groups | 9.75 | 24.75 | 40.6875 |

| chosen groups | 11.4375 | 27.125 | 44.25 |

The results in Tables 1 - 3 clearly demonstrate the advantage of choosing the blocks in a data-driven manner. Our proposed methodology leads to a decrease in the effective numbers of tests and in turn to an increase in statistical power, when compared with the setup with fixed groups.

Finally, we have also simulated under , in order to assess how well the FWER level is kept when applying our proposed methodology. As displayed in Table 4, we have found no indication for a violation of the FWER level.

| Sample size | 100 | 200 | 300 |

| Šidák correction | 1.25 | 2.75 | 2.5 |

| fixed groups | 3.25 | 3 | 3.25 |

| chosen groups | 4 | 3.75 | 4 |

5.2 Vine copula model

In our second numerical example, we let , and we assume that the Lebesgue density of on is given by

| (7) |

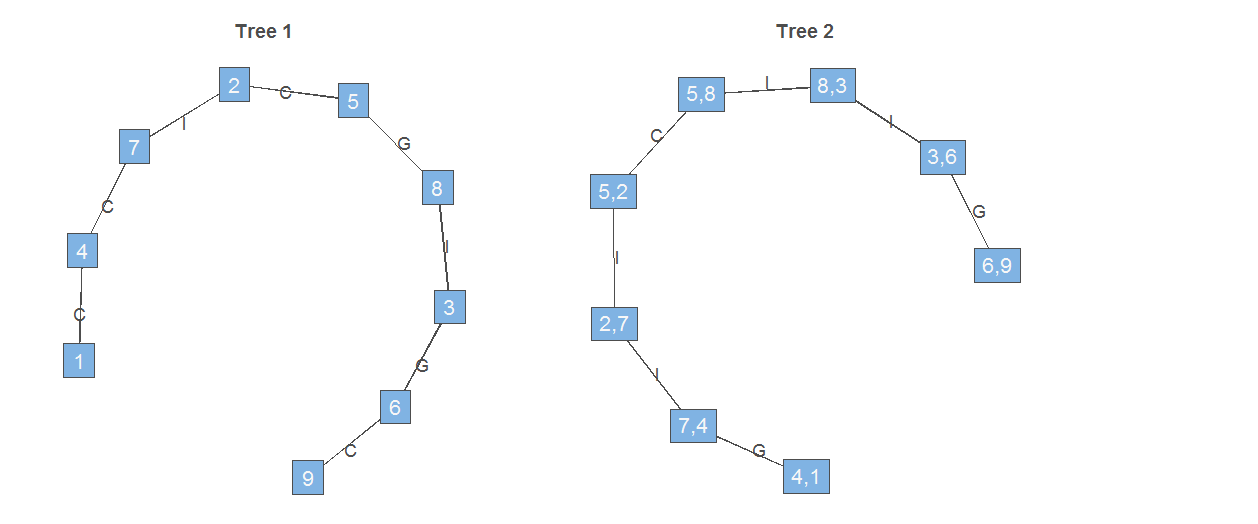

cf. (2). The marginal densities are Lebesgue densities of univariate normal distributions with unit variance. The expected values of these normal distributions are set to zero in the first five coordinates and the remaining ones are set to . The vine utilized in (7) is a D-Vine with truncation level , and its structure is displayed in Figure 4.

In Table 5, we list the copula families utilized in , together with the values of the associated copula parameters.

| Tree | Nodes | Copula family | Copula parameter |

| 1 | 1,4 | Clayton | 11 |

| 4,7 | Clayton | 12 | |

| 2,5 | Clayton | 12 | |

| 5,8 | Gumbel | 8 | |

| 3,6 | Gumbel | 7 | |

| 6,9 | Clayton | 8 | |

| 2 | 1,7—4 | Gumbel | 2 |

| 2,8—5 | Clayton | 11 | |

| 3,9—6 | Gumbel | 2 |

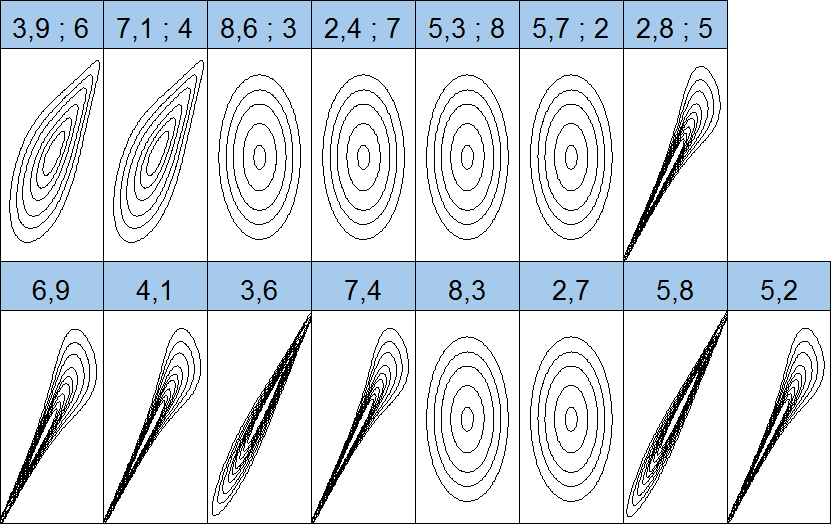

To all nodes which do not appear in Table 5, the independence copula has been assigned. Hence, we have the three independent blocks , , and of three coordinates each in the data-generating process for the distribution of . For a further illustration, Figure 5 displays the corresponding contour plots.

We assume, that is given as the marginal expected value in coordinate , and that the test problem of interest is given by versus for . The test statistics are given by , where for . Hence, . Under , each marginally possesses the standard normal distribution on (leading to choosing the same critical value for each ), while has a shifted normal distribution under the alternative . In terms of the marginal tests, the only difference to the setup in Section 5.1 is, that we now carry out one-sided -tests instead on two-sided ones. Furthermore, the dependency structure of is now much more involved, such that a simple check of the validity of the MSM2 property is not straightforward here. However, notice that the copula families appearing in Table 5 are only capable of expressing positive dependencies, indicating that MSM2 is likely to be fulfilled in this simulation. In particular, the covariance matrix of has only non-negative entries.

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 9 | 9 | 9 |

| fixed groups | 7.68 | 7.78 | 7.78 |

| chosen groups | 4.95 | 4.91 | 4.88 |

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 2.531 | 2.531 | 2.531 |

| fixed groups | 2.478 | 2.482 | 2.482 |

| chosen groups | 2.318 | 2.315 | 2.313 |

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 15.625 | 32.625 | 52.3125 |

| fixed groups | 16.75 | 34.25 | 54.8125 |

| chosen groups | 21.875 | 40.375 | 60.8125 |

| Sample size | 100 | 200 | 300 |

|---|---|---|---|

| Šidák correction | 3.5 | 1.25 | 2.25 |

| fixed groups | 3.5 | 1.25 | 3.25 |

| chosen groups | 4.75 | 2.75 | 4.25 |

6 Conclusion

We have proposed a vine copula-based construction method for multivariate multiple tests. The main advantage of the vine copula estimation approach is, that the tree structure in straightforwardly allows for choosing appropriate blocks for a block-wise evaluation of the effective numbers of tests. In the computer simulations presented in Section 5, the dependency structure was explicitly given. Notice, however, that the workflow from Scheme 1 is data-driven in the sense, that the pair copulae are chosen from a large pool of copula families on the basis of the sample only, without relying on any prior information about the type of dependencies among the test statistics. This is particularly useful in cases with a moderate or high dimensionality , when it is typically infeasible to model (pair) copulae of the data explicitly. Due to the combinatorial explosion involved in the vine model selection, we consider (cf. Section 5.1) or (cf. Section 5.2) already as quite high dimensionalities in our context.

There are several possible extensions of the present work. First, it may be of interest to compare our approach with further data-driven techniques, in particular with multivariate resampling techniques as proposed, for instance, by Westfall and Young (1993). We have not included such a comparison here, because our main point was to demonstrate how much can be gained by choosing the blocks in a sophisticated manner instead of a naive choice. Second, one may consider nonparametric copula estimators in . Finally, from the theoretical perspective it may of interest to analyze conditions for the validity of the MSM2 property for certain relevant families of pair copulae. In the case of Archimedean copula families, an important contribution in this direction has been made by Müller and Scarsini (2005). The authors analyze conditions for the validity of the MTP2 property for such families. It is well-known that MTP2 distributions are also MSM2 distributions; see Glaz and Johnson (1984).

Acknowledgments

We thank Claudia Czado for fruitful discussions and André Neumann for helpful comments.

Appendix A Proof of Lemma 1

Straightforward calculation yields, that

| (8) |

because is assumed strictly increasing. Define . By the principle of probability integral transform, this random variable is uniformly distributed on under . Hence, we get that

by definition of . Applying the analogous calculation to the denominator of (8) yields the assertion.

References

- Bedford and Cooke (2001) Bedford, T., Cooke, R. M., 2001. Probability density decomposition for conditionally dependent random variables modeled by vines. Ann. Math. Artif. Intell. 32 (1-4), 245–268.

-

Bodnar and Dickhaus (2014)

Bodnar, T., Dickhaus, T., 2014. False discovery rate control under Archimedean

copula. Electronic Journal of Statistics 8 (2), 2207–2241.

URL https://doi.org/10.1214/14-EJS950 -

Cerqueti and Lupi (2018)

Cerqueti, R., Lupi, C., 2018. Copulas, uncertainty, and false discovery rate

control. International Journal of Approximate Reasoning 100, 105–114.

URL https://doi.org/10.1016/j.ijar.2018.06.002 - Czado (2019) Czado, C., 2019. Analyzing dependent data with vine copulas. A practical guide with R. Vol. 222 of Lecture Notes in Statistics. Cham: Springer.

- Dickhaus (2014) Dickhaus, T., 2014. Simultaneous statistical inference. With applications in the life sciences. Berlin Heidelberg: Springer.

- Dickhaus and Gierl (2013) Dickhaus, T., Gierl, J., 2013. Simultaneous test procedures in terms of p-value copulae. In: Proceedings on the 2nd Annual International Conference on Computational Mathematics, Computational Geometry & Statistics (CMCGS 2013). Global Science and Technology Forum (GSTF), pp. 75–80.

- Dickhaus and Stange (2013) Dickhaus, T., Stange, J., 2013. Multiple point hypothesis test problems and effective numbers of tests for control of the family-wise error rate. Calcutta Statistical Association Bulletin 65 (1-4), 123–144.

- Dißmann et al. (2013) Dißmann, J., Brechmann, E. C., Czado, C., Kurowicka, D., 2013. Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis 59, 52–69.

- Glaz and Johnson (1984) Glaz, J., Johnson, B. M., 1984. Probability inequalities for multivariate distributions with dependence structures. Journal of the American Statistical Association 79 (386), 436–440.

- Müller and Scarsini (2005) Müller, A., Scarsini, M., 2005. Archimedean copulae and positive dependence. Journal of Multivariate Analysis 93 (2), 434–445.

-

Nagler et al. (2019)

Nagler, T., Bumann, C., Czado, C., 2019. Model selection in sparse

high-dimensional vine copula models with an application to portfolio risk.

Journal of Multivariate Analysis 172, 180 – 192.

URL http://www.sciencedirect.com/science/article/pii/S0047259X18300630 - Neumann et al. (2019) Neumann, A., Bodnar, T., Pfeifer, D., Dickhaus, T., 2019. Multivariate multiple test procedures based on nonparametric copula estimation. Biom. J. 61 (1), 40–61.

- Schmidt et al. (2015) Schmidt, R., Faldum, A., Gerß, J., 2015. Adaptive designs with arbitrary dependence structure based on Fisher’s combination test. Statistical Methods & Applications 24 (3), 427–447.

- Schmidt et al. (2014) Schmidt, R., Faldum, A., Witt, O., Gerß, J., 2014. Adaptive designs with arbitrary dependence structure. Biometrical Journal 56 (1), 86–106.

-

Stange et al. (2015)

Stange, J., Bodnar, T., Dickhaus, T., 2015. Uncertainty quantification for the

family-wise error rate in multivariate copula models. AStA Adv. Stat. Anal.

99 (3), 281–310.

URL http://dx.doi.org/10.1007/s10182-014-0241-5 -

Stange et al. (2016)

Stange, J., Loginova, N., Dickhaus, T., 2016. Computing and approximating

multivariate chi-square probabilities. Journal of Statistical Computation and

Simulation 86 (6), 1233–1247.

URL https://doi.org/10.1080/00949655.2015.1058798 - Westfall and Young (1993) Westfall, P. H., Young, S. S., 1993. Resampling-based multiple testing: examples and methods for p-value adjustment. Wiley Series in Probability and Mathematical Statistics. Applied Probability and Statistics. Wiley, New York.