The Sample Complexity of Meta Sparse Regression

Abstract

This paper addresses the meta-learning problem in sparse linear regression with infinite tasks. We assume that the learner can access several similar tasks. The goal of the learner is to transfer knowledge from the prior tasks to a similar but novel task. For parameters, size of the support set , and samples per task, we show that tasks are sufficient in order to recover the common support of all tasks. With the recovered support, we can greatly reduce the sample complexity for estimating the parameter of the novel task, i.e., with respect to and . We also prove that our rates are minimax optimal. A key difference between meta-learning and the classical multi-task learning, is that meta-learning focuses only on the recovery of the parameters of the novel task, while multi-task learning estimates the parameter of all tasks, which requires to grow with . Instead, our efficient meta-learning estimator allows for to be constant with respect to (i.e., few-shot learning).

1 Introduction

Current machine learning algorithms have shown great flexibility and representational power. On the downside, in order to obtain good generalization, a large amount of data is required for training. Unfortunately, in some scenarios, the cost of data collection is high. Thus, an inevitable question is how to train a model in the presence of few training samples. This is also called Few-Shot Learning Wang et al., (2019). Indeed, there might not be much information about an underlying task when only few examples are available. A way to tackle this difficulty is Meta-Learning Vanschoren, (2018): we gather many similar tasks instead of several examples in one task, and use the data from different tasks to train a model that can generalize well in the similar tasks. This hopefully also guarantees a good performance of the model for a novel task, even when only few examples are available for the new task. In this sense, the model can rapidly adapt to the novel task with prior knowledge extracted from other similar tasks.

As a meta-learning example, for the particular model class of neural networks, researchers have developed algorithms such as Matching Networks Vinyals et al., (2016), Prototypical Networks Snell et al., (2017), long-short term memory-based meta-learning Ravi and Larochelle, (2017), Model-Agnostic Meta-Learning (MAML) Finn et al., (2017), among others. These algorithms are experimental works that have been proved to be successful in some cases. Unfortunately, there is a lack of theoretical understanding of the generalization of meta-learning, in general, for any model class. Some of the algorithms can perform very well in tasks related to some specific applications, but it is still unclear why those methods can learn across different tasks with only few examples given for each task. For example, in few shot learning, the case of 5-way 1-shot classification requires the model to learn to classify images from 5 classes with only one example shown for each class. In this case, the model should be able to identify useful features (among a very large learned feature set) in the 5 examples instead of building the features from scratch.

There has been some efforts on building the theoretical foundation of meta-learning. For MAML, Finn et al., (2019) showed that the regret bound in the online learning regime is , and Fallah et al., (2019) showed that MAML can converge and find an -first order stationary point with iterations. A natural question is how we can have a theoretical understanding of the meta-learning problem for any algorithm, i.e., the lower bound of the sample complexity of the problem. The upper and lower bounds of sample complexity is commonly analyzed in simple but well-defined statistical learning problems. Since we are learning a novel task with few samples, meta-learning falls in the same regime than sparse regression with large number of covariates and a small sample size , which is usually solved by regularized (sparse) linear regression such as LASSO, albeit for a single task. Even for a sample efficient method like LASSO, we still need the sample size to be of order to achieve correct support recovery, where is the number of non-zero coefficients among the coefficients. The rate has been proved to be optimal Wainwright, (2009). If we consider meta-learning, we may be able to bring prior information from similar tasks to reduce the sample complexity of LASSO. In this respect, researchers have considered the multi-task problem, which assumes similarity among different tasks, e.g., tasks share a common support. Then, one learns for all tasks at once. While it seems that considering many similar tasks together can bring information to each single task, the noise or error is also introduced. In the results from previous papers, e.g., Jalali et al., (2010); Obozinski et al., (2011); Negahban and Wainwright, (2011), in order to achieve good performance on all tasks, one needs the number of samples to scale with the number of tasks . (See Table 1.) More specifically, one requires or for each task, which is not useful in the regime where with respect to . Results from other papers, e.g., Lounici et al., (2011); Ollier and Viallon, (2017), only apply to deterministic (non-random) covariates.

| Model | Regularization | Rate of for support recovery |

|---|---|---|

| Ours | (only to recover the common support) | |

| Negahban and Wainwright, (2011) | ||

| Obozinski et al., (2011) | ||

| Jalali et al., (2010) |

Our contribution in this paper is as follows. First, we proposed a meta-sparse regression problem and a corresponding generative model that are amenable to solid statistical analysis and also capture the essence of meta-learning. Second, we prove the upper and lower bounds of the sample complexity of this problem, and show that they match in the sense that and . Here is the number of coefficients in one task, is the number of non-zero coefficients among the coefficients, and is the sample size of each task. In short, we assume that we have access to possibly an infinite number of tasks from a distribution of tasks, and for each task we only have limited number of samples. Our goal is to first recover the common support of all tasks and then use it for learning a novel task. The take-away message of our paper is that simply by merging all the data from different tasks and solving a regularized (sparse) regression problem (LASSO), we can achieve the best sample complexity rate for identifying the common support and learning the novel task. The merge-and-solve method seems to be intuitive while its validity is not trivial. To the best of our knowledge, our results are the first to give upper and lower bounds of the sample complexity of meta-learning problems.

2 Method

Here, we present the meta sparse regression problem as well as our regularized regression method.

2.1 Problem setting

We consider the following meta sparse regression model. The dataset containing samples from multiple tasks is generated as follows:

| (1) |

where, indicates the -th task, is a constant across all tasks, and is the individual parameter for each task. Note that the tasks are the related tasks we collect for helping solve the novel task . Each task contains training samples. The sample size of task is denoted by , which is equal to in the setting above, but generally it could also be larger than .

We assume tasks are related in a way that are independently drawn from one distribution , which is a sub-Gaussian distribution with mean 0 and variance proxy for each entry. Furthermore, we do not assume entries to be mutually independent. Sub-Gaussianity is a very mild assumption, since the class of sub-Gaussian random variables includes for instance Gaussian random variables, any bounded random variable (e.g., Bernoulli, multinomial, uniform), any random variable with strictly log-concave density, and any finite mixture of sub-Gaussian variables. We denote the support set of each task as . Here we consider the case that and , . This assumption is possible as the sub-Gaussian distribution of on the -th entry can be a mixture of some other sub-Gaussian distributions and a Dirac distribution that can cancel out the -th entry in .

We assume that are i.i.d and follow a sub-Gaussian distribution with mean 0 and variance proxy . Sample covariates are independent with each other for any . Each sample is a sub-Gaussian vector with variance proxy no greater than . The samples from different tasks can have different distributions, and we only assume that if we put all samples from all tasks together, their second moment matrix satisfies the mutual incoherence condition, i.e., where denotes the submatrix of with rows in and columns in . A random vector in is sub-Gaussian if for any , the inner product is a sub-Gaussian random variable. The variance proxy of is defined as the maximum of the variance proxy of inner product, i.e., . This concept is proportional to the Orlicz norm of (introduced in Section 4.3), which is also used in Vershynin, (2012).

Remark 2.1 (Difference between meta sparse regression and multitask learning).

Our setting and analysis focuses on the case that the sample size of each task is fixed and small, and the number of tasks goes to infinity, while the number of tasks in multitask learning is usually fixed, or grows with the sample size of each task. The mutual incoherence condition and are also common and mild assumptions in the multitask learning literature Jalali et al., (2010); Negahban and Wainwright, (2011); Obozinski et al., (2011). Our problem focuses on recovering only and while multitask learning focuses on recovering for all tasks which is much more difficult if the sample size of each task is fixed.

2.2 Our method

In meta sparse regression, our goal is to use the prior tasks and their corresponding data to recover the common support of all tasks. We then estimate the parameters for the novel task. For the setting we explained above, this is equivalent to recover .

First, we determine the common support over the prior tasks by the support of formally introduced below, i.e., , where

| (2) |

Note that we have tasks in total, and samples for each task.

Second, we use the support as a constraint for recovering the parameters of the novel task . That is

| (3) |

We point out that our method makes a proper application of regularized (sparse) regression, and in that sense is somewhat intuitive. In what follows, we show that this method correctly recovers the common support and the parameter of the novel task. At the same time, our method is minimax optimal, i.e., it achieves the optimal sample complexity rate.

3 Main results

First, we state our result for the recovery of the common support among the prior tasks.

Theorem 3.1.

Let be the solution of the optimization problem (2). If and

with probability greater than , we have that

-

1.

the support of is contained within (i.e., );

-

2.

,

where are constants.

Remark 3.2 (Theorem 3.1).

The scale terms in and in are typically encountered in the analysis of the single-task sparse regression or LASSO Wainwright, (2009). The two additional terms in are due to the difference in the coefficients among tasks, and our simulations show that is sufficient in the settings we consider. In our technical analysis, the additional terms come from the concentration inequality of a random variable with finite Orlicz norm we used, which is the main novelty in our proof: bounding the product of three random variables.

Next, we state our result for the recovery of the parameters of the novel task. The proof can be found in appendix Section D.

Theorem 3.3.

The theorems above provide an upper bound of the sample complexity, which can be achieved by our method. The lower bound of the sample complexity is an information-theoretic result, and it relies on the construction of a restricted class of parameter vectors. We consider a special case of the setting we previously presented: all non-zero entries in are 1, and all non-zero entries in are also 1. We use to denote the set of all possible parameters . Therefore the number of possible outcomes of the parameters .

If the parameter is chosen uniformly at random from , for any algorithm estimating this parameter by , the answer is wrong (i.e., ) with probability greater than if . Here we use to denote the sample size of task . This fact is proved in the following theorem. The detailed proof is included in appendix Section E.

Theorem 3.4.

Let . Furthermore, assume that is chosen uniformly at random from . We have:

where are constants.

In the following section, we prove that the mutual information between the true parameter and the data is bounded by . In order to prove Theorem 3.3, we use Fano’s inequality and the construction of a restricted class of parameter vectors. The use of Fano’s inequality and restricted ensembles is customary for information-theoretic lower bounds Wang et al., (2010); Santhanam and Wainwright, (2012); Tandon et al., (2014).

4 Sketch of the proof of Theorem 3.1

We use the primal-dual witness framework Wainwright, (2009) to prove our results. First we construct the primal-dual candidate; then we show that the construction succeeds with high probability. Here we outline the steps in the proof. (See the supplementary materials for detailed proofs.)

We first introduce some useful notations:

is the matrix of collocated (covariates of all samples in the -th task). Similarly, and . is the matrix of collocated (covariates of all samples in all tasks). Similarly, . is the sub-matrix of containing only the rows corresponding to the support of , i.e., with . Similarly, , , and . is the sub-matrix of containing only the rows and columns corresponding to the support of .

4.1 Primal-dual witness

Step 1: Prove that the objective function has positive definite Hessian when restricted to the support, i.e.,

Step 2: Set up a restricted problem:

| (4) |

Step 3: Choose the corresponding dual variable to fulfill the complementary slackness condition:

, if , otherwise

Step 4: Solve to let fulfill the stationarity condition:

| (5) | ||||

| (6) |

Step 5: Verify that the strict dual feasibility condition is fulfilled for :

In order to prove support recovery, we only need to show that step 1 and step 5 hold. The proof of step 1 being satisfied with high probability under the condition is in appendix Section A. Next we show that step 5 also holds with high probability.

4.2 Strict dual feasibility condition

We first rewrite (5) as follows:

Then we solve for . and plug it in (6). We have

where is an orthogonal projection matrix, is the sample covariance matrix, and is the dual variable chosen at step 3.

One can bound the norm of by the techniques used in Wainwright, (2009): if and , we have

where is a constant. Proof of this result is shown in appendix Section B.

Note that the remaining two terms containing are new to the meta-learning problem and need to be handled with novel proof techniques.

We first rewrite with respect to each of its entries (denoted by ) as follows: , we have

| (7) |

We know that are sub-Gaussian random variables. It is well-known that the product of two sub-Gaussian is sub-exponential (whether they are independent or not). To characterize the product of three sub-Gaussians and the sum of the i.i.d. products, we need to use Orlicz norms and a corresponding concentration inequality.

4.3 Orlicz norm

Here we introduce the concept of exponential Orlicz norm. For any random variable and , we define the (quasi-) norm as

We define . This concept is a generalization of sub-Gaussianity and sub-exponentiality since the random variable family with finite exponential Orlicz norm corresponds to the -sub-exponential tail decay family which is defined by

where are constants. More specifically, if , we set so that fulfills the -sub-exponential tail decay property above. We have two special cases of Orlicz norms: corresponds to the family of sub-Gaussian distributions (with , i.e., proportional to the variance proxy) and corresponds to the family of sub-exponential distributions.

A good property of the Orlicz norm is that the product or the sum of many random variables with finite Orlicz norm has finite Orlicz norm as well (possibly with a different .) We state this property in the two lemmas below.

Lemma 4.1.

[Lemma A.1, A.3 in Götze et al., (2019)] Let be random variables such that for some and let . Then

By the lemma above, we know that the sum (with respect to ) of the products in (7) is a -sub-exponential tail decay random variable. The details are shown in the next subsection. This result does not require any independence condition, thus we will use this fact for bounding both and .

4.4 -sub-exponential tail decay random variable

For , we have

4.5 Concentration inequality for

We know that for different and , the random variables are independent with and . Now we use a concentration inequality to bound .

Lemma 4.2 (Theorem 1.4 in Götze et al., (2019)).

Let be a set of independent random variables satisfying for some . There exists a constant such that for any , we have

where

We let , and

Then we have

Therefore, can be bounded by with probability

where are constants.

4.6 Bound on

By definition,

where we define

| (8) |

Since the independence between random variables is not necessary in Lemma 4.1, we use the same technique for bounding to bound . More specifically, under the same condition to bound , we have

| (9) |

Now we can transform into the first part in by replacing with . We know that . Therefore we can bound using the same technique for bounding in appendix Section B: if , we have

where are constants.

4.7 Bound on and the estimation error

Since we have bounded each part of , we have with high probability, therefore the first part of Theorem 3.1 about support recovery () is proved through primal-dual witness by finishing step 1 and step 5. The proof for the second part of Theorem 3.1 about the estimation error uses similar techniques. Details can be found in the appendix Section C.

5 Discussions

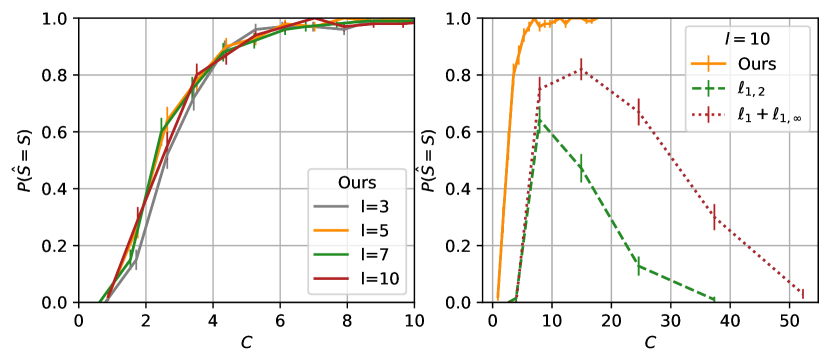

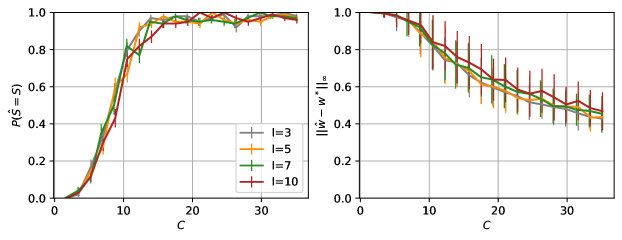

Our problem setting and method are amenable to solid statistical analysis. By focusing on sparse regression, our analysis shows clearly the difference between meta-learning and multi-task learning. In meta-learning, we only need to recover and , thus the number of samples needed for each task (including the novel task) is . When , meta-learning can recover with high probability (shown in the left panel of Figure 1 where ), therefore for the novel task, it only needs . For multi-task learning, one needs to recover for all , which requires the sample size at least (see Table 1.) When , the sample size of multi-task learning goes to infinity which is supported by the right panel of Figure 1: when grows and is fixed at , the probability of exact support recovery of decreases to . (For details about Figure 1 and additional experiments, see appendix Section F.)

While meta sparse regression might apparently look similar to the classical sparse random effect model Bondell et al., (2010), a key difference is that in the random effect model, the experimenter is interested on the distribution of the estimator instead of support recovery. To the best of our knowledge, our results are the first to give upper and lower bounds of the sample complexity of meta-learning problems.

Although our paper shows that a proper application of regularized (sparse) regression achieves the minimax optimal rate, it is still unclear whether there is a method that can improve the constants in our results. To have further theoretical understanding of meta-learning, one could consider other algorithms, such as nonparametric regression or neural networks. We believe that our results are a solid starting point for the sound statistical analysis of meta-learning.

References

- Bergstra et al., (2013) Bergstra, J., Yamins, D., and Cox, D. (2013). Making a science of model search: Hyperparameter optimization in hundreds of dimensions for vision architectures. In Dasgupta, S. and McAllester, D., editors, Proceedings of the 30th International Conference on Machine Learning, volume 28 of Proceedings of Machine Learning Research, pages 115–123, Atlanta, Georgia, USA. PMLR.

- Bondell et al., (2010) Bondell, H. D., Krishna, A., and Ghosh, S. K. (2010). Joint variable selection for fixed and random effects in linear mixed-effects models. Biometrics, 66(4):1069–1077.

- Fallah et al., (2019) Fallah, A., Mokhtari, A., and Ozdaglar, A. (2019). On the convergence theory of gradient-based model-agnostic meta-learning algorithms. arXiv preprint arXiv:1908.10400.

- Fano, (1952) Fano, R. (1952). Class notes for course 6.574: Transmission of information. MIT, 4:3.

- Finn et al., (2017) Finn, C., Abbeel, P., and Levine, S. (2017). Model-agnostic meta-learning for fast adaptation of deep networks. In Proceedings of the 34th International Conference on Machine Learning-Volume 70, pages 1126–1135. JMLR. org.

- Finn et al., (2019) Finn, C., Rajeswaran, A., Kakade, S., and Levine, S. (2019). Online meta-learning. In Chaudhuri, K. and Salakhutdinov, R., editors, Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 1920–1930, Long Beach, California, USA. PMLR.

- Götze et al., (2019) Götze, F., Sambale, H., and Sinulis, A. (2019). Concentration inequalities for polynomials in -sub-exponential random variables. arXiv preprint arXiv:1903.05964.

- Jalali et al., (2010) Jalali, A., Sanghavi, S., Ruan, C., and Ravikumar, P. K. (2010). A dirty model for multi-task learning. In Advances in Neural Information Processing Systems, pages 964–972.

- Kouno et al., (2013) Kouno, T., de Hoon, M., Mar, J. C., Tomaru, Y., Kawano, M., Carninci, P., Suzuki, H., Hayashizaki, Y., and Shin, J. W. (2013). Temporal dynamics and transcriptional control using single-cell gene expression analysis. Genome biology, 14(10):R118.

- Lounici et al., (2011) Lounici, K., Pontil, M., Van De Geer, S., Tsybakov, A. B., et al. (2011). Oracle inequalities and optimal inference under group sparsity. The Annals of Statistics, 39(4):2164–2204.

- Negahban and Wainwright, (2011) Negahban, S. N. and Wainwright, M. J. (2011). Simultaneous support recovery in high dimensions: Benefits and perils of block -regularization. IEEE Transactions on Information Theory, 57(6):3841–3863.

- Obozinski et al., (2011) Obozinski, G., Wainwright, M. J., Jordan, M. I., et al. (2011). Support union recovery in high-dimensional multivariate regression. The Annals of Statistics, 39(1):1–47.

- Ollier and Viallon, (2017) Ollier, E. and Viallon, V. (2017). Regression modelling on stratified data with the lasso. Biometrika, 104(1):83–96.

- Ravi and Larochelle, (2017) Ravi, S. and Larochelle, H. (2017). Optimization as a model for few-shot learning. In International Conference on Learning Representations.

- Santhanam and Wainwright, (2012) Santhanam, N. P. and Wainwright, M. J. (2012). Information-theoretic limits of selecting binary graphical models in high dimensions. IEEE Transactions on Information Theory, 58(7):4117–4134.

- Scarlett, (2019) Scarlett, J. (2019). An introductory guide to fano’s inequality with applications in statistical estimation. Information-Theoretic Methods in Data Science.

- Snell et al., (2017) Snell, J., Swersky, K., and Zemel, R. (2017). Prototypical networks for few-shot learning. In Advances in Neural Information Processing Systems, pages 4077–4087.

- Tandon et al., (2014) Tandon, R., Shanmugam, K., Ravikumar, P. K., and Dimakis, A. G. (2014). On the information theoretic limits of learning ising models. In Advances in Neural Information Processing Systems, pages 2303–2311.

- Vanschoren, (2018) Vanschoren, J. (2018). Meta-learning: A survey. arXiv preprint arXiv:1810.03548.

- Vershynin, (2012) Vershynin, R. (2012). Introduction to the non-asymptotic analysis of random matrices, page 210–268. Cambridge University Press.

- Vershynin, (2018) Vershynin, R. (2018). High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press.

- Vinyals et al., (2016) Vinyals, O., Blundell, C., Lillicrap, T., Wierstra, D., et al. (2016). Matching networks for one shot learning. In Advances in Neural Information Processing Systems, pages 3630–3638.

- Wainwright, (2009) Wainwright, M. J. (2009). Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (lasso). IEEE Transactions on Information Theory, 55(5):2183–2202.

- Wang et al., (2010) Wang, W., Wainwright, M. J., and Ramchandran, K. (2010). Information-theoretic bounds on model selection for gaussian markov random fields. In 2010 IEEE International Symposium on Information Theory, pages 1373–1377. IEEE.

- Wang et al., (2019) Wang, Y., Yao, Q., Kwok, J. T., and Ni, L. M. (2019). Generalizing from a few examples: A survey on few-shot learning. ACM Computing Surveys (CSUR).

- Yu, (1997) Yu, B. (1997). Assouad, Fano, and Le Cam. Springer-Verlag.

Appendix A Proof of step 1 in the primal-dual witness

We know that

| (10) |

We first show a useful theorem on bounding the difference between the sample covariance matrix and the population covariance matrix.

Lemma A.1 (Theorem 4.6.1 in Vershynin, (2018)).

Let be an matrix whose rows are independent, mean zero, sub-gaussian isotropic random vectors in . Then for any , we have

with probability .

To prove (10), we need to bound away from 0. We find independent isotropic random vectors such that (by the proof of Theorem 4.7.1 in Vershynin, (2018), is the submatrix of restricted on in both row and column, and are also sub-Gaussian with ) and define , . Then we use a similar technique as Lemma 4.1.5 in Vershynin, (2018):

where we set .

If , we will have and also .

If , we let , . If , we let , . Under both cases, we have .

Therefore, if we have tasks, (10) holds with probability greater than , where is a constant.

Appendix B Bound of in Section 4.2

Recall that

In order to bound , we consider each entry of the vector. That is, for , we need to bound

Since each entry in is sub-Gaussian, we know is also sub-Gaussian. We define by decomposition:

where is an independent sub-Gaussian random variable for all . We assume its variance proxy is which is proportional to .

We can rewrite based on :

By the mutual incoherence condition, we have . Therefore we only need to bound since the variance proxy for is (and we can bound by the concentration inequality of sub-Gaussian random variables).

For the first part , by the techniques in appendix Section A, we have

with probability , where is a constant.

For the second part, we have

By the concentration inequality of which is a sub-exponential random variable, we have that the last inequality holds with probability where are constants.

Now we define and the event . We have

Therefore, if and , we have that holds with probability greater than .

Appendix C Bound of estimation error

The second part in Theorem 3.1 is about the estimation error. We first write the estimation error in the following form:

By the technique in appendix Section A, we know

holds with probability greater than , where is a constant.

For , we have

which can be bounded by the concentration inequality of sub-exponential random variables. Here we let . By Lemma 4.1, we know . We then use Theorem 1.4 in Götze et al., (2019) again:

We let , and , then

holds with probability greater than , where is a constant.

For , we use the definition in (8) and we set in the bound (9). We know that

holds with probability greater than .

Therefore, we can bound the estimation error: with probability greater than , we have

Appendix D Proof of Theorem 3.3

We use the primal dual witness framework as in the proof of Theorem 3.1. Since for this novel -th task, is not considered, the choice of and can be more flexible. We set and .

For step 1, similar to the step 1 in Theorem 3.1, with probability greater than , we have

For step 5, we only have one part which is in the proof of step 5 in Theorem 3.1. We can use the technique in appendix Section B. With probability greater than , we have

For the estimation error bound, we can use the technique in appendix Section C. We only need to consider the two parts which does not contain . With probability greater than , we have

Appendix E Proof of Theorem 3.4

We first introduce Fano’s inequality Fano, (1952); Yu, (1997) (the version below can also be found directly in Scarlett, (2019)).

Lemma E.1.

(Fano’s inequality) With input dataset , for any estimator with possible outcomes, i.e., , if is generated from a model with true parameter chosen uniformly at random from the same possible outcomes , we have:

Now we show that , where are constants, and represents the parameter we want to recover. Here is all the data in the tasks, is the data in the first tasks, and is the data of task . The mutual information is bounded by the following steps.

Given the common coefficient , the data for each task is independent from each other. Therefore we have

| (11) |

First, we consider the first part (11). We use to denote . Let . Note that

Furthermore

This is because conditioning on , the data for each task is independent and therefore

If we set , , we have

Therefore

We know is a function of only when , and . Therefore, we have

Therefore

For any task , conditioning on , we know all samples in are i.i.d. If we set to be the -th sample in the task , and , we have

Therefore,

Then we consider the second part (11). For the task , conditioning on , since we know all samples in are i.i.d., we have

Combining the results above, we have

Finally, from Fano’s inequality, we know

Appendix F Additional experiments

In this section, we first present simulations to show that Theorem 3.1 holds in the sense that for different choices of and , one only needs to recover the true common support with high probability. We then perform a real-world experiment with a gene expression dataset from Kouno et al., (2013) which was used in the experimental validation of Ollier and Viallon, (2017). Our meta-learning method has lower mean square error (MSE) of the prediction on a new task than multi-task methods.

F.1 Simulations

For all the experiments in this section, we let , and perform repetitions for each setting. We compute the empirical probability of successful support recovery as the number of times we obtain exact support recovery among the repetitions, divided by . We compute the standard deviation as , that is, by using the formula of the standard deviation of the Binomial distribution. For the estimation error , we calculate the mean and standard deviation by using the empirical results of the repetitions.

F.1.1 Gaussian distribution setting

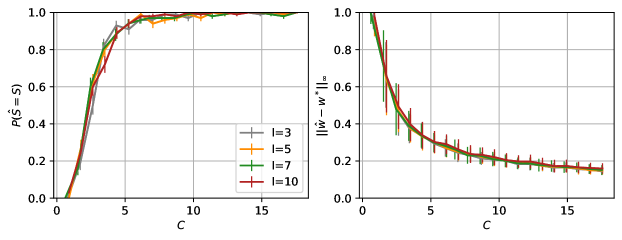

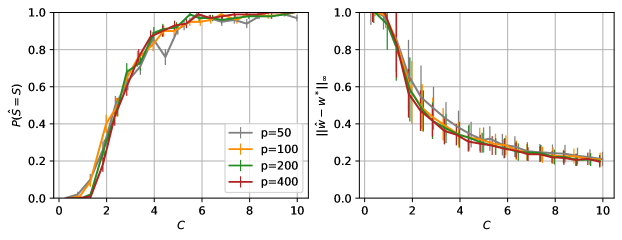

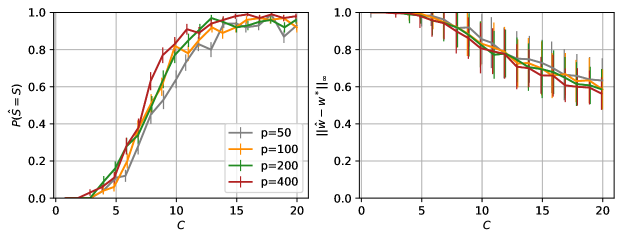

We first consider the setting of different sample size . We choose and use for all the pairs of . We denote the set by . For all , we set , , , which are mutually independent. We set , and having five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . The results are shown in Figure 2. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

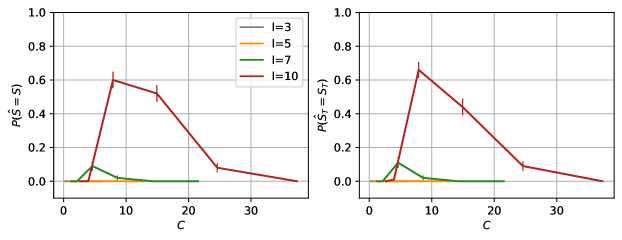

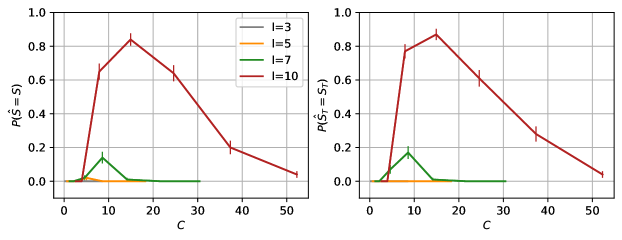

Next we show that the problem described above cannot be solved by multi-task methods. We use two multi-task methods with regularization terms being Obozinski et al., (2011) and Jalali et al., (2010) respectively. The results are shown in Figure 3 and 4, where we take . We show both and since the multi-task learning methods are not designed for recovering only the union of the supports of all tasks. As we claimed in Table 1, the multi-task methods require that grows with in order to retain the probability of support recovery. Therefore we see when is fixed at , the probability of support recovery first increases then decreases to as increases. For the method of Obozinski et al., (2011), we use as the parameter for the norm; for the method of Jalali et al., (2010), we use as the parameter of the norm and as the parameter of the norm. We also tried different choices of and the trends of the results are similar.

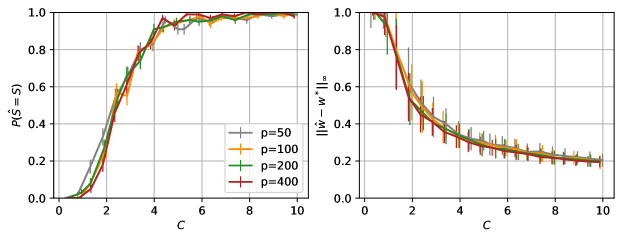

Then, for our method we consider the setting of different number of parameters . We choose and use for all the pairs of . For all , we set , , , which are mutually independent. We set , and having five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . The results are shown in Figure 5. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

F.1.2 Uniform distribution setting

In this paper we only assume that the distributions are sub-Gaussian which includes the uniform distribution. Therefore in this section, we replace the Gaussian distribution setting in the appendix Section F.1.1 with a uniform distribution setting.

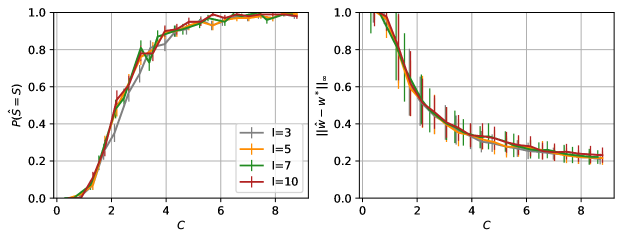

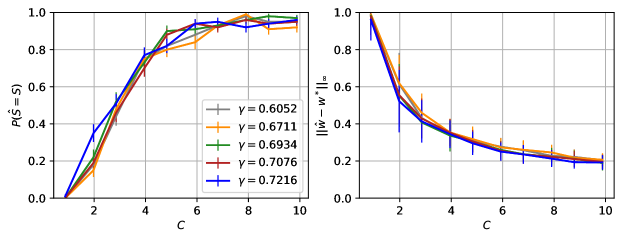

For all , we set , , , which are mutually independent. We consider the setting of different sample size . We choose and use for all the pairs of . We set , and having five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . The results are shown in Figure 6. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

Then we consider the setting of different number of parameters . We choose and use for all the pairs of . For all , we set , , , which are mutually independent. We set , and having five entries equal to 1, and the rest of the entries being 0. The results are shown in Figure 7. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

F.1.3 Mixture of sub-Gaussian distribution setting

In Section 2.1, we state that we can consider the setting under the sub-Gaussian distribution assumption. Therefore in this section, we replace the Gaussian distribution setting of in the appendix Section F.1.1 with a mixture of sub-Gaussian distribution setting. More specifically, we consider a mixture of a Dirac distribution and a Gaussian distribution.

For all , we set , , , which are mutually independent. We consider the setting of different sample size . We choose and use for all the pairs of . We set , and having five entries equal to 2, and the rest of the entries being 0. The support of is same as the support of denoted by while the support of could be a subset of , i.e., . More specifically, the distribution of means that for the -th parameter in the -th task, i.e., , there is a 50% probability that , and a 50% probability that .

The results are shown in Figure 8. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

Then we consider the setting of different number of parameters . We choose and use for all the pairs of . The distribution setting is same as in Figure 8. We set , and . The results are shown in Figure 9. The number of tasks is rescaled to defined by . For different choices of , the curves overlap with each other perfectly (for both and ).

F.1.4 Gaussian distribution setting with entries in being correlated

In this section, we consider three different correlation settings in for our method:

-

1.

are i.i.d. from where is not a diagonal matrix;

-

2.

are i.i.d. from , and , i.e., for each task, the covariance matrix of is different and sampled from a matrix distribution ;

-

3.

are i.i.d. from , and , i.e., for each task, the covariance matrix of depends on the task specific coefficient .

First, we consider the setting of a nondiagonal which leads to in the mutual incoherence condition, where . For the simulations we present in the previous sections, the entries in are independent, therefore the covariance matrix of is diagonal and the corresponding . Here we consider the case that the entries in are not independent. We choose and use for all the pairs of . We set with five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . For all , we set , , , which are mutually independent. The covariance matrix where is a sum of a randomly generated orthonormal matrix and a matrix with each entry i.i.d. from , i.e., . After we generate , we calculate the corresponding . We generate different with different . The results are shown in Figure 10. The number of tasks is rescaled to defined by .

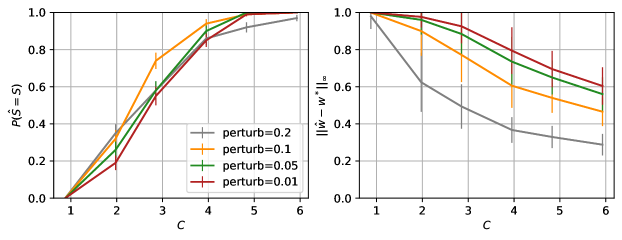

Then, we consider the setting of different for each task, i.e., . We choose and use for all the pairs of . We set with five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . For all , we set , , , which are mutually independent. For each task, the covariance matrix where is a sum of a randomly generated orthonormal matrix and a perturbation matrix with each entry i.i.d. from , i.e., . We choose the perturbation range from . The results are shown in Figure 11. The number of tasks is rescaled to defined by .

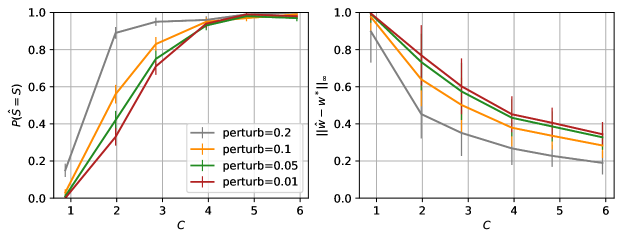

Finally, we consider the setting that for each task, the distribution of depends on the task specific coefficient . We choose and use for all the pairs of . We set with five entries equal to 1, and the rest of the entries being 0. The support of is same as the support of . For all , we set , , which are mutually independent. For each task, , and the covariance matrix where is a sum of a randomly generated orthonormal matrix and a perturbation matrix , i.e., . We choose the perturbation range from . The results are shown in Figure 12. The number of tasks is rescaled to defined by .

F.2 Real-world experiments with a gene expression dataset

The single-cell gene expression dataset from Kouno et al., (2013) contains expression levels of transcription factors measured at distinct time-points. This dataset contains single cells for each time-point and was used in the experimental validation of Ollier and Viallon, (2017). The original objective is to determine the associations among the transcription factors and how they vary over time. We formulate this as a meta-learning problem by setting the first of the time-points as the tasks (for training) and the -th time-point as the novel task (for testing), i.e., . Similar to the analysis in Ollier and Viallon, (2017), we pick one particular transcription factor, EGR2, as the response variable , and the other factors as the covariates in , i.e., . The true value of the support size is unknown. We choose to model this problem as few-shot learning.

We first randomly permute the single cells (i.e., samples) while keeping their relative order in all of the time points (i.e., tasks). Then we find a good choice of hyperparameters: in our method, for the norm of the method in Obozinski et al., (2011); and for the and norms, respectively of the method in Jalali et al., (2010). We use the tree-structured Parzen estimator approach (TPE) optimizing the criterion of expected improvement (EI) in the Python package hyperopt Bergstra et al., (2013).

The search space is for all these hyperparameters. For one choice of the hyperparameters, we choose samples in each of the tasks as training samples, and choose the rest samples as validation samples. The TPE-EI algorithm evaluates choices of hyperparameters to minimize the mean square error of the prediction on the validation samples.

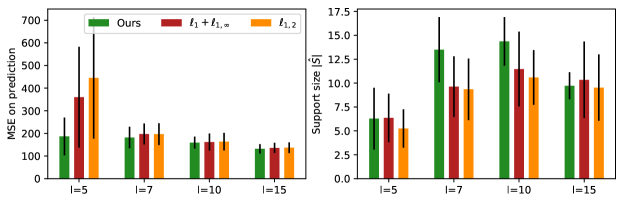

After we determine the hyperparameters from all the three methods (ours, , and ), we choose samples in each of the tasks to train models by these methods to estimate (for multi-task methods, .) The mean and standard deviation of the size of the estimated support are shown in the right panel of Figure 13.

When the estimated common supports are obtained, we can use LASSO constrained on the common support to solve for the new task, i.e., the -th time point. We determine the choice of hyperparameters using hyperopt in the same way shown above. Then we use LASSO with being set to those hyperparameters to estimate the support of the new task. Since the weight estimation of by LASSO is not very accurate when the sample size is small, we use linear regression to estimate again with the support recovered by LASSO. The performance is measured by the mean square error (MSE) of prediction on the rest samples. For one estimated common support, we take random choices of the training samples in the new task and calculate the mean of the the prediction error. The mean and standard deviation of MSE are shown in the left panel of Figure 13.

All the mean and standard deviation results (shown as error bars) in Figure 13 are obtained from repetitions of the experiment setting above. From Figure 13 we can see that our method has lower MSE when is small. Since is not large and does not grow, the multi-task methods also perform well when is large enough. We also show that the size of the estimated common support by our methods is not significantly larger than the ones by the other two multi-task methods, which suggests that our method produces a more accurate estimation of the common support set.