Bayesian Causal Inference with Bipartite Record Linkage

Abstract

In many scenarios, the observational data needed for causal inferences are spread over two data files. In particular, we consider scenarios where one file includes covariates and the treatment measured on one set of individuals, and a second file includes responses measured on another, partially overlapping set of individuals. In the absence of error free direct identifiers like social security numbers, straightforward merging of separate files is not feasible, so that records must be linked using error-prone variables such as names, birth dates, and demographic characteristics. Typical practice in such situations generally follows a two-stage procedure: first link the two files using a probabilistic linkage technique, then make causal inferences with the linked dataset. This does not propagate uncertainty due to imperfect linkages to the causal inference, nor does it leverage relationships among the study variables to improve the quality of the linkages. We propose a hierarchical model for simultaneous Bayesian inference on probabilistic linkage and causal effects that addresses these deficiencies. Using simulation studies and theoretical arguments, we show the hierarchical model can improve the accuracy of estimated treatment effects, as well as the record linkages, compared to the two-stage modeling option. We illustrate the hierarchical model using a causal study of the effects of debit card possession on household spending.

Keywords: Treatment; Matching; Observational; Fusion; Propensity

1 Introduction

Often, researchers seek to make causal inferences from variables spread over two datasets. For example, a social scientist seeks to link records from a survey and an administrative database to assess the effect of some policy on economic outcomes. Similarly, a health researcher seeks to link patients’ electronic health records and Medicare claims data to assess the effect of some medical intervention. As a final example, a researcher seeks to link records from a study done in the past to records in a current database to make inferences about long-term effects of a treatment, without having to incur the substantial costs of collecting new primary data.

When perfectly measured, unique identifiers like social security numbers or Medicare patient IDs are available in the two files, it is reasonably straightforward to link individuals across the files (based on these identifiers). However, often direct identifiers are missing from one or more files, or may not be made available due to privacy restrictions. In such situations, data files have to be linked based on indirect identifiers, such as individuals’ names, birth dates, addresses, and demographic information. These are inherently imperfect, e.g., they could be recorded differently on the files. This introduces uncertainty in linkages that should be propagated to the causal inferences.

Historically, record linkage and causal inference have been carried out as a two-stage process. The researcher first links records using a probabilistic record linkage model based on indirect identifiers, not taking into account available information on the outcome, covariate or treatment status. Subsequently, the researcher uses the set of linked records in a causal inference procedure. This two-stage approach suffers from two drawbacks. First, it does not propagate uncertainty from imperfect linkages. Second, it does not take advantage of relationships among the study variables that could enhance the accuracy of the linkages.

In this article, we propose a Bayesian hierarchical modeling framework for simultaneous causal inference and record linkage in observational studies. In particular, we consider scenarios where one file includes the treatment indicator and causally relevant covariates measured on a set of individuals, and the other file includes outcomes measured on a partially overlapping set of individuals. We follow the Bayesian paradigm for causal inference and posit models for the missing potential outcomes, conditional on the linking status and known covariates. We couple these outcome models with a probabilistic model for the unknown linkage statuses, i.e., which record pairs are links and which are not. For the outcome models, we consider both parametric and semi-parametric forms, with the latter based on a regression of the outcome on a flexible function of the propensity scores (Rosenbaum and Rubin, 1983). For the record linkage model, we use the Bayesian version of the Fellegi and Sunter (1969) model proposed by Sadinle (2017). As part of the model estimation, we generate plausible values of the missing potential outcomes, which we then use to estimate posterior distributions of causal effects.

Our work adds to a body of literature that uses Bayesian methods for simultaneous record linkage and statistical inference, including regression modeling (Gutman et al., 2013; Dalzell and Reiter, 2018) and population size estimation (Domingo-Ferrer, 2011; Tancredi and Liseo, 2011; Sadinle et al., 2018; Tancredi et al., 2018). It also adds to the literature on non-Bayesian methods for simultaneous record linkage and estimation (e.g., Scheuren and Winkler, 1991; Lahiri and Larsen, 2005; Chipperfield et al., 2011; Solomon and O’Brien, 2019). None of these Bayesian and and non-Bayesian works consider causal inference as the analysis goal. Wortman and Reiter (2018) introduced the concept of allowing the causal model to inform the linkage model. Their (non-Bayesian) approach uses point estimates of average causal effects to determine the thresholds at which record pairs links are declared links in a Fellegi and Sunter (1969) algorithm. It does not use the causal estimates to determine the record pairs to consider as possible links in the first place, which our Bayesian approach does. Further, their approach does not provide uncertainty quantification.

The remainder of the article proceeds as follows. In Section 2 we discuss the background, notations and the formulation of the Bayesian hierarchical model. We also present theoretical results arguing for improved inference on record linkage from a joint model compared to a two-stage model. In Section 3 we describe posterior computation for the model. In Section 4, we provide results from simulation studies used to assess the effectiveness of the hierarchical model, both for causal inference and for linkage quality. In Section 5 we apply a hierarchical model to data from an Italian household survey to link records between different files and assess the effect of debit card possession on household spending. Finally, in Section 6 we conclude with an eye towards future work.

2 Model and Prior Formulation

We define a few key concepts and assumptions related to causal inference in Section 2.1, and describe probabilistic record linkage in Section 2.2. We propose the Bayesian hierarchical modeling approach in Section 2.3.

2.1 Background and Notation for Bayesian Causal Inference

We assume a binary treatment, , with and indicating treatment and control assignment to individual , respectively. Let be the covariate vector and be the (continuous) outcome for individual . Each individual is assumed to have two potential outcomes (Rubin, 1974), one under each value of the treatment. We denote and as the potential outcomes for individual when or , respectively. The treatment effect for the th individual is given by . Other treatment effects can be defined as well, such as , although here we consider effects in the form of .

In reality, for each individual , we can observe only one of and ; that is, we can observe . Bayesian approaches to causal inference essentially treat the unobserved potential outcomes as missing data (Rubin, 2005; Hill, 2011; Ding et al., 2018). One can impute the missing values repeatedly by sampling from posterior predictive distributions, and use the resulting draws of each to make statements about causal effects. For example, one can compute the posterior distribution of the average of the causal effects for the individuals in the study, .

Following convention, we make the following assumptions to facilitate causal inferences.

-

1.

Stable unit treatment value assumption (SUTVA): The SUTVA contains two sub-assumptions, no interference between units (i.e., the treatment applied to one unit does not affect the outcome for another unit) and no different versions of any treatment (Rubin, 1974).

-

2.

Strong ignorability: Strong ignorability stipulates that for all , which means that there is no unobserved confounding, and that .

We also make use of propensity scores (Rosenbaum and Rubin, 1983). For any individual , let the propensity score i.e., the probability of being assigned to treatment given the covariate . Rosenbaum and Rubin (1983) show that the treatment assignment is independent of given under strong ignorability. Typically, propensity scores are estimated using binary regressions of the treatment on causally-relevant covariates. Analysts can use the resulting estimate in a variety of ways, for example, to create subsets of matched treated and control records (Stuart, 2010).

2.2 Background and Notation for Probabilistic Record Linkage

We consider the scenario where we seek to link two files, File A and File B, comprising and records, respectively. Without loss of generality, we assume that . We suppose each individual or entity is recorded at most once within each file, i.e., each file contains no duplicates. Under this setting, the goal of record linkage is to identify which records in File A and File B refer to the same subject. This setting is known as bipartite record linkage (Sadinle, 2017).

A corollary to the no-duplicates assumption comes in the form of a maximum one-to-one restriction in the linkage, i.e., a record in one file can be linked with a maximum of one record in the other file. Most commonly, the one-to-one linkage is enforced as a post-processing step after identifying a set of potentially many-to-one links. (e.g., Fellegi and Sunter, 1969; Jaro, 1989; Winkler, 1993; Belin and Rubin, 1995; Larsen and Rubin, 2001; Herzog et al., 2007). Alternatively, one can embed the bipartite matching constraint into a Bayesian model (Fortini et al., 2002; Tancredi and Liseo, 2011; Larsen, 2010; Gutman et al., 2013; Sadinle, 2017; Dalzell and Reiter, 2018), as we do here.

Following Sadinle (2017), we introduce for the records in File B to encode a particular linking status between the two files. Specifically, let

In the context of bipartite matching, one enforces whenever .

Suppose the two files include variables in common that can be used to link records across the files. We call these the linking variables or fields. For each pair of records in File AFile B, we define a -dimensional vector , where is a score reflecting the similarity in field for the record pair. In this article, for nominal variables (e.g., age, birth year, sex), we set when the values of field for records and are equal, and set otherwise. For string fields (e.g., names) we take into account partial agreement using the normalized Levenshtein Similarity metric (Winkler, 1990). This metric ranges between (no agreement) and (full agreement). We obtain it using the “levenshteinSim” function in the RecordLinkage package in R. We convert the distances into a binary by setting when the distance metric exceeds a predetermined threshold (e.g., 0.95), and otherwise. One can convert the metric into a multinomial variable for more refined comparisons (Sadinle et al., 2018; Wortman and Reiter, 2018).

Following Fellegi and Sunter (1969) and related literature, we assume that is a random realization from a mixture of two distributions, one for true links and the other for nonlinks. We have

| (1) |

where and comprise probabilities of agreement for each field specific to each mixture component. Again following typical practice, for computational convenience we assume conditional independence across fields, so that

| (2) |

As a prior distribution on the set of , such that for any , we follow a construct used in the bipartite record linkage literature, including Fortini et al. (2002), Larsen (2010) and Sadinle (2017). Specifically, let , where represents the proportion of matches expected a priori as a fraction of the smaller file. Here and throughout, when its argument is true, and otherwise. We assume is distributed according to a Beta() a priori. Marginalizing over , the total number of links between File A and File B, given by , is distributed according to a Beta-binomial () distribution. Conditioning on the number of records in File B with a link, all possible bipartite pairings are taken as equally likely. The final form of the prior distribution of , marginalizing over , is given by

| (3) |

The choice of the hyper-parameters and provides prior information on the number of overlapping records between the two files. We discuss the specific choices of and in Section 3. Finally, the parameters and follow i.i.d. distributions for all

2.3 Hierarchical Model for Bayesian Causal Inference and Record Linkage

To develop a joint model for Bayesian causal inference and record linkage, we specify the distribution of the outcome in File A depending on whether or not it is linked to any covariate and treatment in File B. For linked records, we specify the conditional distribution of using a regression of our choice. For records without a link, we specify a model for the marginal distribution of . We couple these with the model for record linkage in (1) – (3).

More specifically, the contribution to the likelihood function from the th record in File A is when , and is when , for any . Here, and represent parameters in the regression and in the marginal model for outcomes, respectively. Let and be the vector of outcomes in File A and vector of treatment statuses in File B, respectively, and be an dimensional matrix of covariates obtained from File B. The joint likelihood is given by

| (4) |

To illustrate the potential benefit of joint modeling over two-stage modeling, we examine the likelihood ratio that any pair of records is linked versus not linked. Under the joint model, the likelihood ratio of (i.e., record is linked to record ) and is given by

| (5) |

Notably, (5) depends on a contribution to the likelihood from the outcome model. In contrast, the likelihood ratio for linking records in the traditional two-stage model only involves the likelihood from the assumed probabilistic record linkage model. For this model, we have

| (6) |

Theorem 2.1 offers insight into the behavior of and .

Theorem 2.1

Assuming is bounded away from and in its support, we have

(a)

(b) .

-

Proof

The likelihood ratio under the joint model, , can be expressed as

(7)

The likelihood ratio under the two-stage model, , is given by (6), which we abbreviate as . Thus, , and Therefore, we have

as a consequence of this expression being a Kullback-Leibler divergence. And, we have

where the last inequality follows from the fact that the expression is times the Kullback-Leibler divergence between the two densities and .

Theorem 2.1 indicates that the likelihood ratio for the joint model is more extreme than the likelihood ratio for the two stage model, which facilitates more accurate identification of a link or no link between records and .

2.3.1 Outcome Models

Naturally, one should specify and to describe the distribution of outcomes as faithfully as possible. In this article, we specify models for and assume ; setting a more complicated distributional form for or extending to a categorical is relatively straightforward. For , we use a general mean-zero additive error form,

| (8) |

The specification for could be a simple linear form, although often in observational studies it is advantageous to use more flexible modeling (Hill, 2011).

We use a computationally favorable yet flexible specification for . In particular, we assume

| (9) |

where is the estimated propensity score. In the simulations of Section 4, we use , where is the logit link function and is the maximum likelihood estimate of obtained by fitting a logistic regression of on for all .

To afford model flexibility, we propose a semi-parametric choice for and using penalized splines (Ruppert et al., 2003). Let be a set of fixed knot points in . The functions and are represented using spline basis functions,

| (10) |

So, the parameters are This modeling framework is motivated by the penalized spline regression approaches in the Bayesian survey sampling literature (Zheng and Little, 2003, 2005), with survey weights replaced by propensity scores.

We suggest placing a large number of knots to estimate the semi-parametric functions accurately. However, even a moderately large choice of may result in model over-fitting. We therefore regularize the spline coefficients and . using Bayesian Lasso shrinkage priors. Following Park and Casella (2008), a scale-mixture representation of the Bayesian Lasso shrinkage prior is given by

| (11) |

We assign and priors. We also assign and priors. The prior specification is completed by setting prior distributions on as and a priori. We discuss the choice of hyper-parameters further in Section 3.

For comparisons, we also consider a parametric outcome regression. In this model, we set and , so that . We assign and a multivariate normal prior distribution. We let , and let follow an IG() prior.

3 Posterior Computation

Incorporating the prior information, the full posterior for the model with the semi-parametric outcome regression is proportional to

| (12) |

Similarly, the full posterior for the model with the parametric outcome regression is proportional to

| (13) |

Summaries of these posterior distributions cannot be computed in closed form. Thus, posterior computation proceeds through Markov chain Monte Carlo (MCMC) algorithms. In each iteration, we update the outcome regression parameters using the current set of model-determined links. We also re-estimate propensity scores based only on those records in File B that have been linked to File A in that iteration. We re-estimate propensity scores since these records correspond to the linked dataset on which causal inference is performed. The full posterior conditionals can be found in the supplementary material.

For either model, we let the MCMC chain run until apparent convergence ( iterations in our simulations) and discard an appropriate burn-in (the first iterations in our simulations). Let be the post burn-in MCMC iterates of , where . For each , we empirically estimate using the proportion of post burn-in samples where takes the value , i.e., , for . The most likely link for record in File B is the record satisfying . We denote this record as . When , we declare it most likely that record does not have a link in File A. The posterior distributions of each characterize the uncertainties associated with the links.

For posterior inferences on causal effects, we define the average treatment effect for the linked cases, which we abbreviate as ATEL.

| (14) |

where , and denotes the cardinality of . In expectation, the ATEL equals the usual average treatment effect for the records in File A when the linked records do not differ systematically from the full sample of File A; that is, linkages are independent of the potential outcomes. As we do not know for certain which record pairs are true links, we estimate the posterior distribution of the ATEL by computing (14) in each iteration of the MCMC sampler.

To draw posterior inferences on the ATEL, define as the counterfactual outcome for the th record in File A, where . At the -th post burn-in iteration, we impute the counterfactual outcomes for all linked individuals, i.e., all , from their posterior predictive distributions,

| (15) |

In (15), we sample using a treatment indicator that is opposite what is observed for its linked record, i.e., we set . We obtain the -th post burn-in iterate for the ATEL using (14) with over all .

4 Simulation Studies

We carry out simulation studies to assess the performance of the Bayesian hierarchical model, which for brevity we refer to as the joint model. We consider simulation scenarios in which we vary (a) the proportion of records in common between the two files and (b) the data generation model for the outcomes. Within these, we consider simulation scenarios with the correctly specified and a mis-specified outcome regression model. Finally, we present results from a simulation with missing outcome values.

4.1 Simulated Data Generation

We work with the RLdata10000 data from the R package, RecordLinkage (Sariyar and Borg, 2010). These data comprise an artificial population of records with first names, last names, birth years and birth dates. Among these, there are individuals whose values of these variables have been duplicated and then randomly perturbed, introducing errors into these potential linking variables.

The RLdata10000 data do not include covariates, treatments, or outcomes. Thus, we generate values of these for each of the unique individuals in the RLdata10000 file. For each individual , we generate covariates, and , sampled i.i.d. from standard normal distributions. We generate each individual’s binary treatment assignment from a Bernoulli distribution with probability given by

| (16) |

where . We generate each individual’s outcome from

| (17) |

where the superscript indicates the true data generating mechanism. We examine results for two choices of . The first uses linear functions in the propensity score: and . We call this Scheme L. The second uses nonlinear functions in the propensity score: and . We call this Scheme N.

We construct File A and File B by putting subsets of these records into two files. For any record, File A includes the outcome information, while File B includes the covariate and treatment information; both files include the imperfect linking variables. For ease of simulation, we set the sizes of File A and File B to be .

In any simulation, we randomly sample a subset of the individuals with duplicates. We put these records in File A and their duplicates in File B. The number of these overlapping individuals is denoted by , which is varied to be 100, 500, or 900. For the remaining records in File A, we randomly choose records from the individuals without duplicates, discarding their treatments and covariates and keeping their outcomes and the linking variables. To ensure that the non-overlapping records of File A and File B correspond to different individuals, we set aside these records from the records. To add the remaining records to File B, we randomly choose records from the remaining records, discarding their outcomes and keeping the treatments, covariates, and linking variables.

For comparisons, we consider the performance of two alternatives. In the two-stage model, we first link records using the posterior mode of each after fitting the bipartite Bayesian record linkage method as described in Section 2.2, without using the covariates, treatments, or outcomes. We then perform causal inference on the records linked in the initial step, i.e., the exercise is sequential as opposed to joint. Comparisons with this model reveal if the sharing of information between the record linkage and outcome models offers any inferential advantages. We also consider using the known links, that is, we make causal inferences with the true links. Although this approach is not feasible in practice, as one does not know the true links in genuine scenarios, we consider it a benchmark for the best we can do in these simulation scenarios.

For both the joint and two-stage models, we compare performance accuracy both in terms of record linkage and causal inference. For the former, we examine the positive predictive value (PPV) and the negative predictive value (NPV), defined as follows. Let be the posterior mode of . The PPV is the proportion of links that are actual matches and the NPV is the proportion of non-links that are actual non-matches. Let and . Let be the indicator function corresponding to set , ; . The PPV and NPV are defined as and , respectively. A perfect record linkage procedure would result in PPV=NPV=1.

To assess the quality of causal inference for all three methods, we use the mean squared error (MSE) of the post burn-in causal effects, i.e., MSE where is the value of the ATEL computed using all true links and is the th post burn-in estimate of ATEL. We also examine the posterior distributions and 95% credible intervals of the ATEL.

4.2 Results

We begin with results with no missing outcomes and with correct outcome model specifications. That is, we specify parametric or semi-parametric outcome regressions that match the choices of and in the data generation models in Section 4.1. We estimate the joint model and the two-stage model using four linking variables: first name, last name, birth date and birth year.

Table 1 summarizes the PPV and NPV for the joint model and two-stage model, averaged over replications—enough to generate sufficiently small Monte Carlo errors—when using the correct outcome model specifications. For both data generation schemes, both the PPV and NPV of the joint model decrease as the percentage of overlap between File A and File B decreases. The two-stage model follows a similar pattern. Comparing the two models, we see that the joint model tends to have a higher PPV than the two-stage model. The improved performance of the joint model becomes increasingly apparent as the amount of overlap decreases. The joint model also tends to have a higher NPV than the two-stage model, although the differences are negligible in the scenario with 10% overlap under Scheme N.

| True | Percentage | PPV | NPV | PPV | NPV |

| Model | of Overlap | (Joint) | (Joint) | (Two-Stage) | (Two-Stage) |

| 90 | |||||

| Scheme L | 50 | ||||

| 10 | |||||

| 90 | |||||

| Scheme N | 50 | ||||

| 10 |

| True | Percentage | Joint | Two-Stage | Known Link |

| Model | of Overlap | Model | Model | Model |

| 90 | ||||

| Scheme L | 50 | |||

| 10 | ||||

| 90 | ||||

| Scheme N | 50 | |||

| 10 |

The improvements in the linkages when using the joint model has benefits for the estimation of the causal effect. As evident in Table 2, the joint model performs significantly better on MSE than the two-stage model. The performance gap becomes more substantial as the percentage of overlap decreases, especially under Scheme L. Notably, the results from the joint model are similar to those from the gold-standard Known Link model in the 50% and 90% overlap scenarios.

We next examine performance when the outcome model does not exactly match the data generating model. In particular, we fit an outcome regression that is linear in the propensity score even though the outcomes are generated using Scheme N; and, we fit an outcome regression that uses the penalized splines even though the outcomes are generated using Scheme L. Here, we only consider the scenario with 90% overlap, which gives both methods the best chance to perform well. As evident in Table 3, not surprisingly performances of both models deteriorate substantially compared to the results in Table 1 and Table 2. We are imputing potential outcomes from mis-specified models, after all. When fitting the semi-parametric model to data generated under Scheme L, we observe higher PPV and NPV, as well as a lower MSE, for the joint model compared to the two-stage model. This is also the case when fitting the parametric model to data generated under Scheme N; however, in this scenario the differences are practically modest. Taken together, these results suggest that, even with model mis-specification, it may be advantageous to use the joint model over the two-stage model.

| True | Fitted | PPV | NPV | MSE | |||

| Model | Model | Joint | Two-Stage | Joint | Two-Stage | Joint | Two-Stage |

| Scheme L | Splines | ||||||

| Scheme N | Linear | ||||||

Finally, we examine the performance of the joint model and two-stage model in the presence of missing outcomes in File A. We blank either or of the values of in File A using a missing completely at random mechanism. We examine the cases of correct model specifications with overlap of records between File A and File B. To handle the missing values in the joint model, we sample the missing observations from their posterior predictive distributions in each MCMC iteration. For the two-stage model, based on the posterior mode of , we impute the missing values from their posterior predictive distributions after fitting the outcome model on the linked dataset.

| True | Missing | PPV | NPV | MSE | |||

| Model | % | Joint | Two-Stage | Joint | Two-Stage | Joint | Two-Stage |

| Scheme L | 5% | ||||||

| Scheme L | 10% | ||||||

| Scheme N | 5% | ||||||

| Scheme N | 10% | ||||||

Table 4 summarizes results over 20 independent simulation runs. The performance of joint model worsens as the percentage of missing data increases, although not by much in these scenarios. A similar trend is observed for the two-stage model. We continue to see advantages of the joint model over the two-stage model.

In the supplementary material, we describe results from additional simulation scenarios. In particular, we find that the relative performances of the joint model and two-stage model remain qualitatively unchanged when using correlated (rather than independent) covariates. We also lower the signal to noise ratio by increasing the regression variance. Not surprisingly, the performance gap between the joint model and the two-stage model closes as the variance increases.

5 Causal Study of Debit Cards

The past few decades have seen a steadily increasing global trend in the use of non cash payment instruments like credit, debit and prepaid cards. Thaler (1985) and Thaler (1999) argue that the form of payment instruments can have a significant impact on consumer decisions via mental accounting, a set of cognitive operations used by individuals and households to keep track of financial activities. Indeed, there is evidence that consumers who have cards would spend more than ones who do not (Cole, 1998). A comprehensive causal study carried out by Mercatanti et al. (2014) in this regard focuses on the effect of debit cards on spending. Mercatanti et al. (2014) argue that debit cards, unlike credit cards, do not allow consumers to incorporate additional long-term sources of funds in their spending decisions, thus eliminating any confounding intertemporal reallocations of wealth from the psychological effects on spending (Soman, 2001), and hence are more appropriate to look at for this kind of a causal study.

With this background in mind, we use an observational study of the causal effect of possession of debit cards on household consumption to illustrate the Bayesian hierarchical model for causal inference and record linkage, as we now describe.

5.1 Data Description and Background

We use data from the Italy Survey on Household Income and Wealth (SHIW). The SHIW is a nationally representative survey, run by the Bank of Italy once in every 2 years since 1965, with the only exception being that the 1997 survey was delayed to 1998. The purpose of this survey is to collect information on several aspects of Italian households’ economic and financial behavior. Since the data contain information related to household characteristics, spending and payment instruments, the SHIW can provide a useful opportunity to evaluate the causal effect of debit card possession on spending in Italian households.

We link two files comprising data collected during the years 1995 and 1998. A number of the same households participated in both years. In particular, our target population is the set of households having at least one current bank account but no debit cards before 1995. The treatment if the household (all members combined) possesses one and only one debit card at 1998, and if the household does not possess any debit cards at 1998. Households with more than one debit card are excluded from our sample. Here, it may be mentioned that ideally, an analysis with units being individuals that possess debit cards should be carried out, because debit cards are typically issued to individuals. But the SHIW survey only has this information at the household level. Our strategy to limit the sample of treated units to households possessing only one debit card ensures that a possible effect on household spending will be due to a certain individual possessing this card. Though we do not have exact information on the ownership of the card, we make the (reasonable) assumption that the head of the household has possession of the sole debit card.

The outcome on which we evaluate the treatment effect is the monthly average spending of the household on all consumer goods, measured in the latter survey (1998). For data quality control, we delete observations which have either negative values of the outcome (monthly spending) or unusually high ratios (greater than 5 and going up to 900) of monthly spending to monthly income. Upon implementing such data quality control measures, the data file corresponding to 1995 contains 589 observations with information on the treatment (debit card possession) and covariates, while the data file corresponding to 1998 (3919 observations) contains information on the outcome (monthly average household spending).

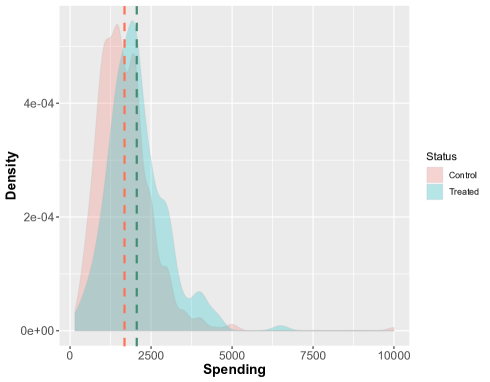

Both files contain a common set of imperfect linking variables, including the geographical area of residence of the household, the number of inhabitants in the town of the household, and the gender, birth year, marital status, region of birth and highest educational qualification of the head of the household. Fortunately, we also have a unique ID that we can use to perfectly link households across years. We use this ID variable to assess how well our model has linked observations in the two files, based on the other imperfect linking variables noted above. Using the unique matching ID, we observe that the file contains 191 observations in the treatment group (who possess a debit card) and the other 398 observations in the control group. An initial check on the spending distribution for the treatment and control groups (see Figure 1) hints at a positive effect of acquiring a debit card on household spending.

The covariates (possible confounders) we consider in this study are all measured in the initial survey (1995), and consist of the monthly average spending of the household on consumer goods in the initial survey year (lagged outcome), the net wealth of the household, the household net disposable income, the monthly average cash inventory held by the household, the average interest rate and the number of banks in the municipality where the household is located. The choice of these confounders appears to satisfy the strong ignorability condition, as we discuss in the online supplement. The lagged outcome is generally indicated in the economic literature as a fundamental confounder (Angrist and Pischke, 2009; Frölich and Sperlich, 2019). The cash inventory held by the household was introduced in the specific context by Mercatanti et al. (2014). The net wealth and the net disposable income are important indicators of the household economic condition. The last two covariates have been suggested by Attanasio et al. (2002), who have shown in non-causal contexts that the interest rate and the number of banks in the municipality where the household lives had a significant contribution to the probability of acquiring a debit card in Italy. Moreover, the number of banks is a good indicator of the size of the municipality.

5.2 Results

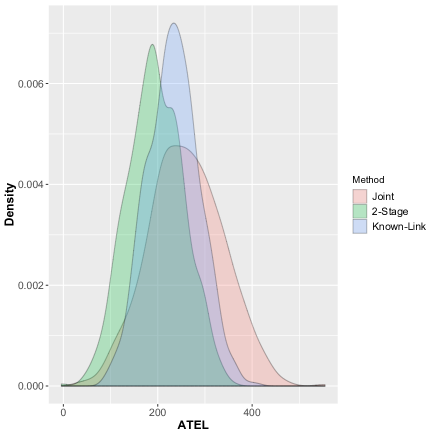

We implement the joint model with the semi-parametric outcome regression specification discussed in Section 2.3.1. We also include the two-stage model and the results using the known-links for comparisons. We use the same prior hyperparameter values as in the simulation studies; moderate perturbation of them leads to practically indistinguishable results. We let the MCMC chain run for 2000 iterations and discard the first 1500 as burn-in, and draw inferences on both the ATEL and record linkage based on the post burn-in iterates.

| Fitted Model | PPV | NPV | ATEL | ||

| 2.5% | 50% | 97.5% | |||

| Known-Link | – | – | 127.49 | 233.14 | 334.67 |

| Joint | 0.876 | 0.979 | 108.46 | 258.57 | 412.44 |

| Two-Stage | 0.847 | 0.881 | 84.08 | 193.28 | 306.16 |

Table 5 presents the PPV and NPV values, along with the posterior median and 95% credible intervals of the estimated ATEL (in thousand Italian Liras) for all models. Consistent with the simulation results, the joint model offers a noticeably better PPV and NPV than the two-stage model. Using the results from the known-links as a benchmark, we find that the posterior inferences for the joint model seem more plausible than those from the two-stage model. First, the posterior medians for the joint model and the known link model are more similar to one another than are the the posterior medians for the known-link model and two-stage model. Second, the 95% credible interval for the joint model is wider than the interval for the known-links model, which is sensible in that it reflects additional uncertainty from imperfect linkages. On the other hand, the 95% credible interval from the two-stage model actually is practically the same length as the interval for the known-links model, effectively portraying no propagation of uncertainty from imprecise linkages.

Figure 1 displays the posterior distributions of the ATEL. The results suggest that, on average, the effect of possession of a single debit card for a household leads to more monthly consumption than households that do not possess any debit card during the study period. Our analysis largely eliminates any potential confounding effect of intertemporal reallocation of wealth, since debit cards do not allow for long-term fund sources (Soman and Cheema, 2002). Hence, the significant estimated effects of debit card possession on spending may be attributed to psychological reasons (increased perceived amount of money) (Soman, 2001) and easier accessibility to financial resources (Morewedge et al., 2007). The estimated ATEL is higher than the ATT (the Average Treatment effect on the Treated) ( 200 thousand Italian Liras), in Mercatanti et al. (2014). This result is interpretable in the light of some recent economic models for the use of debit cards (e.g., see Kim and Lee, 2010 and references therein), which imply that the poor adopt debit cards later than the rest of the population. This is confirmed by Mercatanti et al. (2014) who show that households with debit cards generally have higher levels of income, wealth and education of the members in comparison with households without debit cards. Therefore, our estimated ATEL values indicate larger psychological effects on spending for people in disadvantageous social and economic conditions.

6 Discussion and Future Work

The Bayesian approach to causal inference and record linkage offers interesting future directions. For example, many data applications have predictors and treatment status residing in different files. This requires significant modifications of the approach presented here, as one needs a model for the covariates as well as the outcomes. Another important future direction is to extend this approach to other flexible outcome models.

We conclude with a connection to the philosophy of causal inference. Performing causal inference and record linkage simultaneously allows the values of the outcome variables to influence which records are used in the causal estimator. This is in conflict with the often followed advice that the design of the observational study should proceed separately from the analysis (Imbens and Rubin, 2015). As suggested by Wortman and Reiter (2018), if one seeks the potential gains in accuracy from using the relationships among the variables, this is the price to pay for working with imperfect linkages.

References

- Angrist and Pischke (2009) Angrist, J. D. and Pischke, J. (2009). Instrumental variables in action: sometimes you get what you need. mostly harmless econometrics: an empiricist’s companion.

- Attanasio et al. (2002) Attanasio, O. P., Guiso, L., and Jappelli, T. (2002). The demand for money, financial innovation, and the welfare cost of inflation: An analysis with household data. Journal of Political Economy, 110(2), 317–351.

- Belin and Rubin (1995) Belin, T. R. and Rubin, D. B. (1995). A method for calibrating false-match rates in record linkage. Journal of the American Statistical Association, 90(430), 694–707.

- Chipperfield et al. (2011) Chipperfield, J. O., Bishop, G., Campbell, P. D., et al. (2011). Maximum likelihood estimation for contingency tables and logistic regression with incorrectly linked data.

- Cole (1998) Cole, C. (1998). Identifying interventions to reduce credit card misuse through consumer behavior research. In Proceedings of the Marketing and Public Policy Conference, pages 11–13. Washington, DC: Georgetown University Press.

- Dalzell and Reiter (2018) Dalzell, N. M. and Reiter, J. P. (2018). Regression modeling and file matching using possibly erroneous matching variables. Journal of Computational and Graphical Statistics, 27(4), 728–738.

- Ding et al. (2018) Ding, P., Li, F., et al. (2018). Causal inference: A missing data perspective. Statistical Science, 33(2), 214–237.

- Domingo-Ferrer (2011) Domingo-Ferrer, J. (2011). Privacy in statistical databases. Springer.

- Fellegi and Sunter (1969) Fellegi, I. P. and Sunter, A. B. (1969). A theory for record linkage. Journal of the American Statistical Association, 64(328), 1183–1210.

- Fortini et al. (2002) Fortini, M., Nuccitelli, A., Liseo, B., and Scanu, M. (2002). Modelling issues in record linkage: a bayesian perspective. In Proceedings of the American Statistical Association, Survey Research Methods Section, pages 1008–1013.

- Frölich and Sperlich (2019) Frölich, M. and Sperlich, S. (2019). Impact evaluation. Cambridge University Press.

- Gutman et al. (2013) Gutman, R., Afendulis, C. C., and Zaslavsky, A. M. (2013). A bayesian procedure for file linking to analyze end-of-life medical costs. Journal of the American Statistical Association, 108(501), 34–47.

- Herzog et al. (2007) Herzog, T. N., Scheuren, F. J., and Winkler, W. E. (2007). Data quality and record linkage techniques. Springer Science & Business Media.

- Hill (2011) Hill, J. L. (2011). Bayesian nonparametric modeling for causal inference. Journal of Computational and Graphical Statistics, 20(1), 217–240.

- Imbens and Rubin (2015) Imbens, G. W. and Rubin, D. B. (2015). Causal inference in statistics, social, and biomedical sciences. Cambridge University Press.

- Jaro (1989) Jaro, M. A. (1989). Advances in record-linkage methodology as applied to matching the 1985 census of tampa, florida. Journal of the American Statistical Association, 84(406), 414–420.

- Kim and Lee (2010) Kim, Y. and Lee, M. (2010). A model of debit card as a means of payment. J. Econ. Dyn. Control, 34, 1359–1368.

- Lahiri and Larsen (2005) Lahiri, P. and Larsen, M. D. (2005). Regression analysis with linked data. Journal of the American statistical association, 100(469), 222–230.

- Larsen (2010) Larsen, M. D. (2010). Record linkage modeling in federal statistical databases. In FCSM Research Conference.

- Larsen and Rubin (2001) Larsen, M. D. and Rubin, D. B. (2001). Iterative automated record linkage using mixture models. Journal of the American Statistical Association, 96(453), 32–41.

- Mercatanti et al. (2014) Mercatanti, A., Li, F., et al. (2014). Do debit cards increase household spending? evidence from a semiparametric causal analysis of a survey. The Annals of Applied Statistics, 8(4), 2485–2508.

- Morewedge et al. (2007) Morewedge, C. K., Holtzman, L., and Epley, N. (2007). Unfixed resources: Perceived costs, consumption, and the accessible account effect. Journal of Consumer Research, 34(4), 459–467.

- Park and Casella (2008) Park, T. and Casella, G. (2008). The Bayesian lasso. Journal of the American Statistical Association, 103(482), 681–686.

- Rosenbaum and Rubin (1983) Rosenbaum, P. R. and Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55.

- Rubin (1974) Rubin, D. B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5), 688.

- Rubin (2005) Rubin, D. B. (2005). Bayesian inference for causal effects. Handbook of statistics, 25, 1–16.

- Ruppert et al. (2003) Ruppert, D., Wand, M. P., and Carroll, R. J. (2003). Semiparametric regression. Number 12. Cambridge university press.

- Sadinle (2017) Sadinle, M. (2017). Bayesian estimation of bipartite matchings for record linkage. Journal of the American Statistical Association, 112(518), 600–612.

- Sadinle et al. (2018) Sadinle, M. et al. (2018). Bayesian propagation of record linkage uncertainty into population size estimation of human rights violations. The Annals of Applied Statistics, 12(2), 1013–1038.

- Sariyar and Borg (2010) Sariyar, M. and Borg, A. (2010). The recordlinkage package: Detecting errors in data. The R Journal, 2(2), 61–67.

- Scheuren and Winkler (1991) Scheuren, F. and Winkler, W. E. (1991). Regression analysis of data files that are computer matched.

- Solomon and O’Brien (2019) Solomon, N. C. and O’Brien, S. M. (2019). A framework for decision threshold selection in record linkage.

- Soman (2001) Soman, D. (2001). Effects of payment mechanism on spending behavior: The role of rehearsal and immediacy of payments. Journal of Consumer Research, 27(4), 460–474.

- Soman and Cheema (2002) Soman, D. and Cheema, A. (2002). The effect of credit on spending decisions: The role of the credit limit and credibility. Marketing Science, 21(1), 32–53.

- Stuart (2010) Stuart, E. A. (2010). Matching methods for causal inference: A review and a look forward. Statistical science: a review journal of the Institute of Mathematical Statistics, 25(1), 1.

- Tancredi and Liseo (2011) Tancredi, A. and Liseo, B. (2011). A hierarchical bayesian approach to record linkage and population size problems. The Annals of Applied Statistics, 5(2B), 1553–1585.

- Tancredi et al. (2018) Tancredi, A., Steorts, R., Liseo, B., et al. (2018). A unified framework for de-duplication and population size estimation. Bayesian Analysis.

- Thaler (1985) Thaler, R. (1985). Mental accounting and consumer choice. Marketing science, 4(3), 199–214.

- Thaler (1999) Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral decision making, 12(3), 183–206.

- Winkler (1990) Winkler, W. E. (1990). String comparator metrics and enhanced decision rules in the fellegi-sunter model of record linkage.

- Winkler (1993) Winkler, W. E. (1993). Improved decision rules in the Fellegi-Sunter model of record linkage. Citeseer.

- Wortman and Reiter (2018) Wortman, J. H. and Reiter, J. P. (2018). Simultaneous record linkage and causal inference with propensity score subclassification. Statistics in Medicine, 37(24), 3533–3546.

- Zheng and Little (2005) Zheng, H. and Little, J. (2005). Inference for the population total from probability-proportional-to-size samples based on predictions from a penalized spline nonparametric model. Journal of Official Statistics, 21(1), 1.

- Zheng and Little (2003) Zheng, H. and Little, R. J. (2003). Penalized spline model-based estimation of the finite populations total from probability-proportional-to-size samples. Journal of Official Statistics, 19(2), 99.