Cournot-Nash equilibrium and optimal transport in a dynamic setting

Abstract

We consider a large population dynamic game in discrete time. The peculiarity of the game is that players are characterized by time-evolving types, and so reasonably their actions should not anticipate the future values of their types. When interactions between players are of mean-field kind, we relate Nash equilibria for such games to an asymptotic notion of dynamic Cournot-Nash equilibria. Inspired by the works of Blanchet and Carlier [15] for the static situation, we interpret dynamic Cournot-Nash equilibria in the light of causal optimal transport theory. Further specializing to games of potential type, we establish existence, uniqueness and characterization of equilibria. Moreover we develop, for the first time, a numerical scheme for causal optimal transport, which is then leveraged in order to compute dynamic Cournot-Nash equilibria. This is illustrated in a detailed case study of a congestion game.

1 Introduction

We consider a discrete-time dynamic game played by agents and study its behaviour as goes to infinity. Agents take actions in time in order to minimize a cost function that depends on the whole population of players in a mean-field fashion. Agents may have different characteristics or preferences, which define their own “type” and may change (progressively) in time. The types play a crucial role in the choice of an agent’s dynamic actions, since the latter can only rely on the partial knowledge of types to date. Let us illustrate this with an example.

Example 1.1.

Agents represent different delivery services. Each of these must visit a number of sites in a given order (for instance, supermarkets or costumers). The decision of each agent is whether to take the quick or the slow road in between sites. The mean-field character of the situation arises because of congestion on the roads, which is caused by the population of agents. At each site an agent collects a parcel, to be delivered to the next site. Parcels may be tagged as “express” or “normal”, and there is a penalty for the slow delivery of an express parcel. The type of the agent is the sequence of parcel tags. In the dynamic game we consider, an agent may solely base her actions (ie. taking quick or slow road) on the observed sequence of parcel tags, but is uninformed about the tags of future parcels. By contrast, in a static game, the full sequence of parcel tags is available from the start of the game. In Section 5.1 we illustrate how this leads to a different behaviour of the agents when we compare the dynamic and static games.

We study Nash equilibria for such dynamic games by considering an asymptotic formulation of the problem (namely where we think of a continuum of infinitely small players), whose solutions we refer to as dynamic Cournot-Nash equilibria. The relevance of this problem for the finite population game is justified by limiting results that we prove under suitable assumptions; see Propositions 2.5 and 2.8.

The first main contribution of the present paper is an equivalent reformulation of the asymptotic problem in terms of optimal transport. In doing so we are strongly inspired by the work of Blanchet and Carlier [15] for static games. Crucially, in our dynamic setting actions take place in time and cannot anticipate the evolution of agents’ types. This imposes a constraint in the optimal transport setting, which is known in the literature under the name of causality, c.f. [9].

Our second main contribution is to establish existence, and a characterization, of dynamic Cournot-Nash equilibria for the prominent subclass of potential games. This for example allows us to include congestion effects in the cost function. Games of this type are particularly tractable since, as it is well-known, they can be recast as variational problems. Specifically, the search for dynamic Cournot-Nash equilibria boils down to solving optimization problems over causal couplings.

Finally, we provide an algorithm to compute optimal causal couplings, which is the first numerical method for causal optimal transport and therefore a result of its own interest. In the present context, this allows us to compute dynamic Cournot-Nash equilibria, as well as cooperative equilibria and the Price of Anarchy in the asymptotic formulation. Thanks to our convergence results, this leads to the computation of approximate equilibria for the -player game. Given its generality, we expect the algorithm to be used in other applications of causal optimal transport, e.g. in implementing the discretization scheme proposed in [1] or in the machine learning context currently under development in [3].

For illustration, we implement the aforementioned algorithm in a toy model, akin to Example 1.1. This model is used to further highlight the difference between the notions of dynamic and static Cournot-Nash equilibria.

1.1 Related literature

From the mathematical perspective, our formulation is closely related to mean field games (MFG) in a discrete-time setting (see e.g. [29]). For this parallel, the different types of agents considered in our setup correspond to different subpopulations of players in the MFG (see Remark 3.8 below for more details). The theory of mean field games aims at studying dynamic games as the number of agents tends to infinity. It was established independently in the mathematical community by Lasry and Lions [36, 37], and in the engineering community by Huang, Malhamé and Caines [32, 31], and has since seen a burst in activity, as e.g. documented in the recent monograph by Carmona and Delarue [19]. See also Cardialaguet’s [17], based on P.L. Lions’ lectures at Collége de France, for seminal results on mean field games. The key assumption is that players are symmetric and rational, and the idea is to approximate large -player systems by studying the behaviour as .

Various efforts have been made to rigorously prove that, when the number of players tends to infinity, the original -player system indeed converges to the MFG limit. In the original paper [37], the authors proved such a result for the stationary case, while convergence is established for dynamical MFG in other specific cases by e.g. [10] for the linear quadratic case and [26, 21] for finite state MFG, among others. Several papers were devoted to deal with more general cases based on different notions of convergence, see e.g. [18, 34, 40, 22]. Given that MFG assumes the players to be competitive, the Nash equilibria may not result in optimal social cost. This leads to the discussion of (in)efficiency of the equilibria and originates the concept of Price of Anarchy (PoA). [30] studied the inefficiency of Nash equilibria for the linear quadratic case, and [20] defined and analyzed the PoA for MFG systems. See also [11] for a thorough analysis of the price of anarchy in a continuous-time terminal ranking game with non-local mean field effect, and a connection to the so-called Schrödinger problem.

The articles which are the closest to ours are the works by Blanchet and Carlier [13, 15] where, building on the seminal contribution of Mas-Colell [39], a connection between static Cournot-Nash equilibria and optimal transport is developed. From a probabilistic perspective, large static anonymous games have been recently studied by Lacker and Ramanan in [35], with an emphasis on large deviations and the asymptotic behaviour of the Price of Anarchy. We also refer to this paper for a thorough review on the (vast) game theoretic literature. The crucial difference between the above papers and the present one is the dynamic nature of the game we consider here. It is also worth mentioning that [12] also considers a variational formulation to study competitive games with mean field effect. Similar to our paper, the cost is separable and of potential type, and this leads to a formulation in terms of an optimal transport cost plus an energy functional. A possible extension is provided in [14] where also the non-potential and non-separable cases are considered: It could be of interest to develop in the future a corresponding picture in the dynamic setting.

To deal with our dynamic setting, we use tools from causal optimal transport (COT) rather than classical optimal transport. In a nutshell, COT is a relative of the optimal transport problem where an extra constraint, which takes into account the arrow of time (filtrations), is added. This in turn is crucial to ensure, in our application, the adaptedness of players’ actions to their types in a dynamic framework. The theory of COT, used to reformulate our asymptotic equilibrium problem, has been developed in the works [38, 9]. This theory has been successfully employed in various applications, e.g. in mathematical finance and stochastic analysis [2, 1], in operations research [42, 43, 44], and in machine learning [3]. The novel numerical method developed in the present article can therefore be used to approach a variety of problems, including for example the value of information in dynamic control problems [2], stability of superhedging and utility maximization [8], and McKean-Vlasov optimization problems [1].

A series of numerical methods have been proposed for MFG to help gaining a better understanding of equilibrium, see e.g. [5, 6, 7, 12, 28]. On the other hand, numerics for a symmetrized version of causal optimal transport, the so-called bicausal transport, have been developed by Pflug and Pichler in [42, 43, 44], who refer to it as nested distance. The method used in those papers, that relies on a dynamic programming principle, seems to be ill-suited for the causal transport problem (cf. [46]). To the best of our knowledge, the present paper provides the first numerical method for causal optimal transport. For this, we leverage on the regularization approach developed by Cuturi [23] in the classical optimal transport framework; see also [41].

2 The N-player game and its associated Cournot-Nash limit

Let and be two Polish spaces equipped with their respective sigma-algebras, and a fixed time horizon. We consider a population of players indexed by .

At every time , player is characterized by its own type, which is an element of , and is denoted by . We write

for the vector collecting the types of the population of players at time , and similarly

for the vector collecting the type-path of player . Accordingly, is the space of all possible type paths. We denote by a typical element of , which we may represent as either

as context will reveal. Finally, in situations where the number of players is varying, we will write , , , and , to stress the dependence on . Otherwise we will drop the dependence on for most of the objects yet to be introduced.

From the beginning of the game, type distributions are known for all players, and we denote them by . We so define the associated product measure

On the other hand, at time the collection of players’ time- types is publicly known: We thus set

We now describe the actions that the players are to decide. At every time , each agent needs to choose an action from . This choice may only depend on the available information at time , and is therefore defined through an -measurable function

We define , , and , with the same conventions as before. We henceforth call pure strategy an element

We consider a cost function

| (2.1) |

This captures the fact that each player faces a cost which depends on its own type (eg. ) and action (eg. ), and on the distribution of actions of all other players (anonymous game). For simplicity, we assume throughout that is measurable and lower-bounded, so all integrals that we will considered are well-defined.

From the beginning of the game, the types distributions , are known, thus each player needs to average over all possible evolutions of types. Therefore, for every pure strategy , the cost faced by player is

where we use to denote .

Definition 2.1 (Pure Nash equilibrium).

Strategy is a pure Nash equilibrium for the -player game if111The r.h.s. corresponds to replacing the action by for player , leaving all other players unmodified.

| (2.2) |

for all and all -adapted -valued processes .

As pure equilibria rarely exist, a typical approach is to consider randomized strategies: the choice of action at time depends on types only up to time (“non-anticipativity”), but there may be also other factors influencing the game (eg. independent randomization), thus -adaptedness may fail: A measurable function is called mixed strategy if, for all and all bounded Borel functions , the map

is -measurable.222In plain language: A mixed strategy assigns an ‘action distribution’ to each type-path . The -dependence of such an ‘action distribution’ is assumed to be -adapted. Note that this is equivalent to the conditional independence given , for all , under the measure

| (2.3) |

The cost faced by player when following a mixed strategy is then given by

| (2.4) |

In what follows we write rather than , if context is clear.

Definition 2.2 (Mixed Nash equilibrium).

A mixed strategy is called a mixed Nash equilibrium for the -player game if

for all and all mixed strategies satisfying:

| (2.5) | ||||

We note that Condition (2.5) can be rephrased as: If and are associated to and as in (2.3), then the joint distribution of is the same under either or .

Finding or characterizing equilibria for the -player game is an extremely hard task, even when existence can be proved. Hence rather than directly studying (mixed) Nash equilibria, we will formulate an alternative equilibrium problem for a “representative player”. Proposition 2.5 below shows that this provides a way to approximate equilibria for large (but finite) systems of players. The following definition translates the non-anticipativity of mixed-strategies to the asymptotic framework where essentially we deal with a continuum of identical players.

Notation: For a probability measure , with -marginal (resp. -marginal) of we mean the distribution of the projection of onto (resp. ). We also denote by the conditional law of the coordinate given the coordinates under .

Definition 2.3.

A probability measure is called causal if

| (2.6) |

If has -marginal and -marginal , it is called a causal (Kantorovich) transport from into . Furthermore, is called pure (or a Monge transport) if, for all , -a.s. for some measurable function .

The expression in (2.6) means that, at every time , given (“history of up to time ”), the conditional distribution of under is independent of for all (“future of ”). In other words, the amount of mass transported by into a subset of depends on the source space only up to time . In probabilistic language, a pure causal plan is the joint law of a pair of processes where is adapted to the information of , and in a sense that can be made precise, general causal plans are combinations (mixtures) of pure plans.

Definition 2.4 (Cournot-Nash equilibrium).

Given , a causal transport is called dynamic Cournot-Nash equilibrium for a type- population if, denoting by the -marginal of , it holds

| (2.7) |

where minimization is done over causal transports with -marginal .

Note that finding dynamic Cournot-Nash equilibria amounts to solving a fixed point problem: for any measure , we first need to solve the minimization problem in (2.7) and then check whether the solution has -marginal .

We henceforth fix a compatible metric on , with which we define the sum-metric on . For , we introduce the -Wasserstein distance on the set of measures which integrate for some (and then all) :

We now proceed to present two results, Propositions 2.5 and 2.8, which together justify the interpretation of dynamic Cournot-Nash equilibria as an asymptotic version of dynamic Nash equilibria in finite games (Definition 2.2). For static games this was already explored by Blanchet and Carlier [13], while in the continuous-time case this runs very close to the work of Lacker [34] for mean field games.

Proposition 2.5.

Assume that for some and we have

Let be a dynamic Cournot-Nash equilibrium for a type- population and such that its -marginal belongs to . For each , consider the -agent problem with types . Then, for every , there is such that, for all , the strategy

is an -player mixed -Nash equilibrium, in the sense that

| (2.8) |

for all and all -player mixed strategies such that (2.5) holds.

A first result on the approximations of Nash equilibria via solutions of mean field games was proven by P.L. Lions during his lectures at Collège de France, see [17].

Remark 2.6.

The assumption , in the above proposition can be replaced by the weaker assumption that the sequence , is -chaotic: for all and all continuous and bounded,

We decided to present the result in the simpler case stated in the proposition in order to avoid technicalities and keep the proof shorter.

Remark 2.7.

Note that, in the -Nash equilibrium proposed in Proposition 2.5, each player plays a strategy which is -adapted. That is, even with full information on the type-path evolution of the entire population at hand, there is an approximate Nash equilibrium where players determine their strategies according only to their own type path, and that can be constructed based on a Cournot-Nash equilibrium. In MFG terms, such “myopic” strategies are called distributed. Note that also forms an approximate Nash equilibrium for any partial-information version of the game, as long as player can at least observe the evolution of its own type.

Proof of Proposition 2.5.

Fix and let be a mixed strategy satisfying (2.5) w.r.t. . To ease the notation, we set for all , and write for , and for the law of an iid sequence of -distributed random variables. Clearly

Note that the measure , defined as the -marginal of the measure , has -marginal and satisfies (2.6). It follows that is equal to

By definition of Cournot-Nash, the last term is non-positive, and from this we derive

| (2.9) |

where . Note that, by the assumption of Lipschitz continuity of , we have , hence the r.h.s. of (2.9) is dominated by

| (2.10) |

where the equality follows from the fact that satisfies (2.5) w.r.t. . On the other hand, for iid , LLN implies the following two convergences as for any fixed :

-a.s., and weakly converges to . These convergences in turn imply

Since for each , also in , and so the r.h.s. of

is uniformly integrable, and thus also the l.h.s. is. This yields

Therefore, for every , there is such that, for all and all ,

and the result follows from (2.10). ∎

We now want to prove some kind of converse of Proposition 2.5, that is, to find dynamic Cournot-Nash equilibria as limit of dynamic (-)Nash equilibria in -player games, when the size of the population tends to infinity. This is notoriously the difficult implication, and indeed, in order to get such a result, we require a strong assumption.

Proposition 2.8.

Let be a dynamic Nash equilibrium for the -player problem with types , and set . Assume that the cost function is continuous on and bounded. For , define the (random) measures on :

Assume that, for , the sequence

| (2.11) |

converges to in the sense that

for all bounded, measurable in the first argument and continuous in the last two ones. Assume further that where . Then is a Cournot-Nash equilibrium for a type- population, where .

Remark 2.9.

1. An analogue version of this proposition still holds true if, instead of Nash equilibria, the are taken to be -Nash equilibria in the sense of (2.8).

2. Let be a Cournot-Nash equilibrium with -marginal , and be the corresponding -Nash equilibria for the -player games constructed in Proposition 2.5. Then the sequence in (2.11) converges to in the desired sense.

3. The strong assumption in this proposition is the degeneracy condition .

Without it, one would need to interpret the limit as a weak Cournot-Nash equilibrium, in the same spirit as [34]. Here we do not develop this weaker formulation.

Proof.

We first show that the cost associated to is smaller than the cost associated to any causal measure of pure type with -marginal . Fix such a measure , with corresponding functions as in Definition 2.3, and set . Since is Nash, for all we have

where . By summing up over and dividing by , we get

| (2.12) |

Now, by convergence of the in (2.11), for the l.h.s. in (2.12) converges to

whereas the r.h.s. converges to

Therefore

| (2.13) |

for every pure causal measures with -marginal .

To justify that is a Cournot-Nash equilibrium for a type- population, it remains to extend (2.13) to not necessarily pure. From the “chattering lemma” (see, e.g., [25, Theorem 2.2], [27, Theorem 4], [34, Lemma 6.5]), for any causal measure with -marginal , there are pure causal measures with the same -marginal and such that weakly. The proof then follows from (2.13), being continuous in and bounded from above. ∎

3 Optimal transport perspective

In this section we study existence, uniqueness, and characterization of dynamic Cournot-Nash equilibria by means of optimal transport techniques.

We start by recalling the general formulation of the classical optimal transport problem: given two Polish measure spaces and , and a cost function , the optimal transport problem is defined as

where is the set of all transports of into . If and are endowed with filtrations, say and , we can also define the causal optimal transport (COT) problem

| (3.1) |

where denotes the subset of measures in which are causal w.r.t. , that is, such that and , the map is -measurable. Roughly speaking, the amount of mass transported by a causal plan to a subset of the target space belonging to depends on the source space only up to time . Thus, a causal plan transports mass in a non-anticipative way.

From now on we will consider transports between the spaces and , endowed with the respective canonical filtrations. In this way the above definition of causality corresponds to the one we gave in Definition 2.3 above. In this setting we will simply denote by the set of causal transports of into . Looking at (2.7), it is clear that finding dynamic Cournot-Nash equilibria amounts to solving a generalized version of a causal transport problem in which the second marginal is not fixed (while the first marginal is the population type). In particular, a dynamic Cournot-Nash equilibrium with marginals and will also solve the COT problem in the sense of (3.1), between the measures and and with cost function .

Remark 3.1.

Finding Cournot-Nash equilibria for a type- population amounts to solving the following fixed point problem:

-

1.

, for some ;

-

2.

has second marginal ,

where we used the notation .

3.1 Potential Games

In this section we consider a separable cost, that is,

| (3.2) |

This means that we are considering the case where agents face an idiosyncratic part of the cost, only depending on their own type and action, and a mean-field component depending on other agents’ strategies; see the discussion after (2.1).

Example 3.2.

Classical examples for the mean-field interaction term consist in penalizing (resp. encouraging) similar actions among players. For example (cf. [15]):

-

•

repulsive effect (congestion): , where , is a reference measure w.r.t. which congestion is measured, and is increasing. This translates the fact that frequently played strategies are costly, and leads to dispersion in the strategy distribution w.r.t. .

-

•

attractive effect: is a convex subset of an Euclidean space and we have , where is a symmetric convex function which is minimal on the diagonal and increases with the distance from the diagonal. This leads to concentration of strategies.

In this section we will consider a special class of games, so-called potential games, where the mean-field functional is the first variation of another function , called energy function.

Assumption 3.3.

For example, the repulsive and attractive functionals introduced above are the first variation of the following functions, respectively:

| (3.4) |

where .333A further example of energy function is given by , where is a concave, compact subset of a topological space, and a measurable function strictly concave in the first argument. In this case , where is the unique optimizer for .

Under Assumption 3.3, it is natural to consider the following variational problem

| (3.5) |

where COT is the causal optimal transport of into w.r.t. the cost function :

| (3.6) |

We say that a pair solves the variational problem (3.5) if solves the optimization in (3.6), and its -marginal solves the one in (3.5). The following theorem states the equivalence between Cournot-Nash equilibria and first order optimality of problem (3.5).

Theorem 3.4.

Let be convex. Then the following are equivalent:

-

(i)

is a dynamic Cournot-Nash equilibrium;

-

(ii)

the pair made of and its -marginal solves the variational problem (3.5).

Convexity is for example satisfied by in (3.4) since is increasing in the second argument. Note however that the request of convexity can be weakened in Theorem 3.4; see Remark 3.5.

Proof.

(ii)(i): let solve (3.5), then, for any , . In particular, for any and ,

by convexity of . This implies

Therefore, for every ,

Since was arbitrary in , is a Cournot-Nash equilibrium by Remark 3.1.

(i)(ii): let be a Cournot-Nash equilibrium, and be its -marginal.

From 1. in Remark 3.1,

that is, solves COT; see also the discussion above Remark 3.1. We are then left to prove that solves the optimization in (3.5). By running backward the argument used in the first part of the proof, and using convexity of , we have that

which concludes the proof.

∎

Remark 3.5.

1. Convexity of has been used only for the implication “”. In fact, we proved that convex implies that is LL-monotone, and that this in turn ensures the implication “”. The notion of LL-monotonicity, introduced by Lasry and Lions, can be written as

| (3.7) |

2. Note that we do not have any restriction on the Polish space , thus, already for , Theorem 3.4 above generalizes Theorem 1 and Proposition 1 in [15], and our arguments provides an easier proof that does not use Kantorovich duality and potentials. The same is true for the existence and uniqueness results in [15]; see Corollaries 3.6 and 3.7 below.

3. Variational problems with similar structure to (3.5) appeared already in the work [1] by the first two authors and Carmona, concerning a discretization scheme for (extended) mean-field control problems. Accordingly we may expect that the algorithms in Section 4 below may be of relevance in that context too.

Corollary 3.6 (Uniqueness).

If is strictly convex, then all Cournot-Nash equilibria have the same second marginal, that is, the distribution of the optimal strategies is unique.

Proof.

Strict convexity is for example satisfied by in (3.4) when is strictly increasing in the second variable.

Corollary 3.7 (Existence).

Assume bounded from below and lower-semi-continuous, and consider the mean-field functionals in Example 3.2. Cournot-Nash equilibria exist under either:

1. and satisfy the growth condition: there is a coercive444Ie. . differentiable function such that , for some , and all .

2. , and continuous, and for some and .

Proof.

Since is bounded from below and lower-semi-continuous, then COT admits an optimal solution for any pair of marginals; this is a simple consequence of Lemma 6.1. By the same lemma we derive that the function is lower semicontinuous (and of course lower bounded). Indeed, if weakly, then is weakly compact and so is also weakly compact by Lemma 6.1. If attains , then (up to passing to a subsequence) for some , and thus . We are then left to prove that the respective growth conditions ensure existence of solutions to the minimization in (3.5), so that we can conclude by Theorem 3.4.

For Point 1, we first derive . For any optimizing sequence for (3.5), we may assume that . By de la Vallée-Poussin theorem, the set of densities is uniformly integrable and hence weakly relatively compact in . If is any accumulation point in this set, then we have weakly. Since is convex and continuous, is lower semicontinuous. This shows, by the first paragraph, that is an optimizer of (3.5).

On the other hand, for Point 2, we first observe that for each , for some constants . As a result, if is a minimizing sequence then for some large enough constant . By Markov’s inequality we obtain tightness of , and we may conclude as for Point 1 after proving that is weakly lower semicontinuous. To prove the latter, assume that weakly. By Skorokhod representation, on some probability space there are random variables such that a.s. and for each . Possibly extending the probability space, we build an independent family of random variables with the same properties. We conclude by Fatou’s lemma:

∎

Remark 3.8.

In order to make a parallel between the current framework and the typical setting in mean field games, note that here there are no state dynamics, and that the cost is set as the average over possible evolution of types rather than an expectation or average “over noise”. Remarkably, the different type paths of agents could correspond to different subpopulations of players in the game, and each agent faces a cost that depends on their own type/population. Therefore our setting accommodates (possibly infinite) multiple populations. However, unlike what is generally done in the literature on multi-population mean field games (see e.g. [4]), we do aggregate all actions of the game into a single (empirical) measure rather than letting each subpopulation contribute in a separate way. Separating the actions of players according to the population they belong to would involve a different mathematical analysis. For example, in the limiting problem, the dependence on the distribution of actions of all players (what we denote by ) would be replaced by the disintegration of w.r.t. its first marginal , yielding a cost . Moreover, a separable cost in this case would take a form of the kind . Of course things would simplify by considering finitely many types of agents, that is a finite numbers of subpopulations, which corresponds to having an atomic measure . We do not pursue this analysis here.

3.2 Social planner and Price of Anarchy

From a social planner perspective, optimal strategies in an -player game are those that minimize the total cost, which corresponds to minimizing the average cost (this latter form is the suitable one in order to study this problem asymptotically). In this way we find the so called cooperative equilibria. The corresponding optimization problem for is the following:

where denotes the second marginal of ; to be compared with the asymptotic formulation of the Nash (competitive) equilibria in Definition 2.4 or Remark 3.1. In the separable case (3.2), this can be written as

| (3.8) |

to be compared with the variational problem (3.5) obtained in the competitive case.

With the same arguments used in Corollary 3.7, we can prove existence of solutions for the asymptotic formulation of the cooperative problem.

Corollary 3.9.

The Price of Anarchy is then defined as the ratio between the worst-case Nash equilibrium total cost and the socially optimal total cost. Asymptotically,

| (3.9) |

where is the total cost associated to the strategy distribution , and is the set of optimizers in the minimization problem in (3.5). In Section 4, we will develop numerics to compute the Price of Anarchy, and we will illustrate its behaviour with some example.

4 Numerical methods

In Section 4.1 we present a numerical scheme for the causal optimal transport problem. The algorithm uses duality to transform the problem, and then applies the Sinkhorn method to solve an essential part of it. Relying on it, we also develop a numerical method for Cournot-Nash equilibria, in Section 4.2. The Python code implementing these algorithms is freely available and can be found in https://github.com/JunchaoJia-LSE/CNGonCOT. Numerical experiments show that the proposed methods are efficient and stable.

4.1 A numerical method for causal optimal transport

We borrow the setting of Section 3.1. Thus COT denotes the causal optimal transport problem of into w.r.t. the cost function , namely

We first recall a known result (see [9, Proposition 2.4] or [2, Lemma 5.4]). As a matter of terminology, whenever is a stochastic process defined on , we shall say that “ is -adapted” if for each the r.v. is a function of , and define “ is -adapted” in an analogue fashion. We use the notation for the space of continuous bounded functions on the space . Finally, we say that a process is continuous if each r.v. is a continuous function.

Proposition 4.1.

For , the following are equivalent:

-

1.

is causal (ie. );

-

2.

For every bounded -adapted continuous process , and each bounded -adapted -martingale , we have:

(4.1) -

3.

For each , , and , the following vanishes

(4.2)

Definition 4.2.

We denote by the linear space spanned by the stochastic integrals appearing in Equation (4.1), namely

Similarly, we introduce the set equal to the linear span of the functions

as we vary .

Proposition 4.1 leads to existence and duality for COT. Notice that, unlike in [9, 2], we shall make no assumption on whatsoever. Hence the next result needs a proof, which we provide in the appendix.

Theorem 4.3.

Assume that is lower semicontinuous and bounded from below. Then COT is attained and duality holds:

Of all the above duality identities, we now solely exploit

| (4.3) |

The driving idea is that can be efficiently approximated using Sinkhorn iterations. It is convenient to define

| (4.4) |

From now on, we specialize to a discrete setting. To be consistent with the notation above, however, we keep the notation of integral w.r.t. .

Assumption 4.4.

The sets and are finite, say and .

For , we use the notation , where and denote the elements in and , respectively. The entropy of is then defined as

Note that the entropy is uniformly bounded:

| (4.5) |

We now add an entropic penalization to the transport problem and consider, for , the problem

| (4.6) |

The penalization term makes the function inside the brackets strictly convex in , which ensures existence of a unique optimizer in the weakly compact set . The entropic regularization technique has been widely used to approximate classical optimal transport problems and easily obtain numerical solutions; see [16] for an application to Cournot-Nash equilibria.

Theorem 4.5.

We have

and the convergence is monotonically increasing.

Proof.

Note that, due to Assumption 4.4, the space is generated by a finite basis, say for some (see Appendix 6.2 for details). Then, by setting , and for small enough, Theorem 4.5 suggests the following approximation of the causal transport problem:

| (4.9) |

Recalling the comment after (4.6), for any fixed the minimization problem in (4.9) admits a unique optimizer, say . This problem can be numerically solved in an efficient way by implementing the powerful Sinkhorn algorithm as described by Cuturi [23]. On the other hand, to handle the maximization problem in (4.9), note that Danskin’s theorem [24] implies the following result, which we employ in Algorithm 1 to perform gradient descent.

Lemma 4.7.

is differentiable w.r.t , with

| (4.10) |

is the standard Sinkhorn algorithm to compute (see [23]); is a chosen gradient descent step; the stop criterion consists in the improvement of the optimal value being less than a fixed threshold.

Algorithm 1 shows the most vanilla version of a gradient descent method that we can use. Given that we have an explicit expression for the gradient, cf. (4.10), we can also leverage any other first order optimization algorithm to perform Steps 4 to 7 in the algorithm, that is, to minimize the function in the variable. Indeed, in practice we implemented such an optimization procedure using the SLSQP method in Python’s Scipy optimization package, feeding the method with the explicit calculated gradients. Numerical experiments demonstrate that this outperforms, in terms of efficiency, both the vanilla gradient descent method and alternative zero order methods.

4.2 A numerical method for dynamic Cournot-Nash equilibria

In this section we provide an algorithm to compute dynamic Cournot-Nash equilibria in the potential game setting of Section 3.1. Thanks to Theorem 3.4, when the energy function is convex, this boils down to solving the variational problem (3.5). That is, we have an additional optimization step (in ) w.r.t. the previous section. Here again, we use Theorem 4.5 to approximate causal transport problems with regularized problems given in (4.6). For small enough we obtain a reasonable approximation.

Lemma 4.8.

| (4.11) |

Proof.

As in (4.7), but adding in each of its terms and then minimizing in . ∎

As a matter of fact, in order to deal with the optimization in in (3.5), it is convenient to use the dual formulation of the penalized transport problems (see [41, Proposition 4.4]):

where

and the exponential is understood component-wise. (To lighten the notation, we do not stress dependence on , since this is the type distribution which is fixed.)

From now on we think of small being fixed, and set

| (4.12) |

Proposition 4.9.

The function is differentiable, with

| (4.13) |

where is any optimizer in (4.12). Without loss of generality we may assume that .

Proof.

Note that, for fixed, the supremum of in the variables is uniquely attained at some . On the other hand, there is a unique function such that are optimal if and only if . Then, from Danskin’s theorem [24] and the definition of , we have

Now, if and are optimizers, then , and so . This establishes (4.13). The final conclusion follows after a possible translation of by a constant. ∎

Remark 4.10.

Note that is a result of the Sinkhorn algorithm, and this facilitates the optimization w.r.t. . Thanks to the explicit expression of the gradient, we can search the optimal efficiently. This enables us to compute, in a reasonable amount of time, numerous different cases in the example of next subsection.

All this leads to Algorithm 2, in which we perform gradient decent at the level of . To wit, Step therein uses (4.13) to perform the descent step. (To be precise, Step 5 in fact computes first and then outputs normalized so as to be a probability vector.) On the other hand, Step applies Algorithm 1. The stop criterion consists again in the improvement of the optimal value being less than a fixed threshold.

5 Examples

5.1 A case study in a toy model

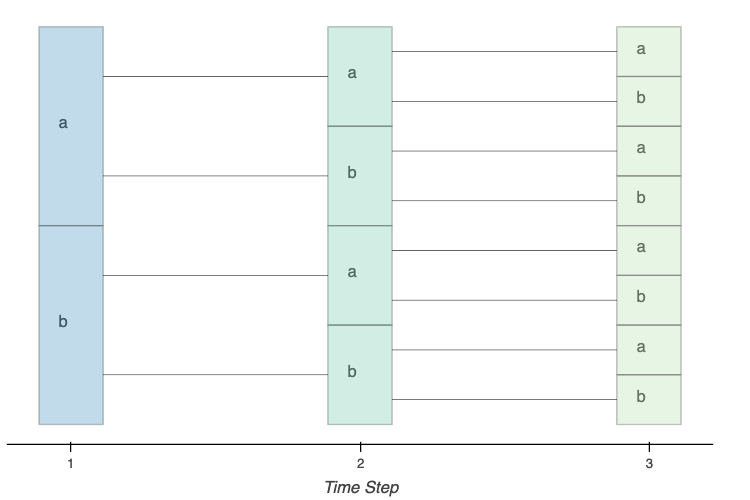

In this section, we apply the numerical scheme developed in the previous section in a simple two-stage game (), cf. Example 1.1. We consider a number of messengers (agents) delivering parcels from to and then from to , where are names of three sites (Fig. 1).

The structure of the example, though very simple, can be adapted to many other situations. For instance, we can imagine that are different stages of economic development. And the agents are different companies. For each company, at each stage, the market demand for its product may be either Extensive (E) or Normal (N), and the company can choose either to Quickly (Q) expand its producing capacity or to Slowly (S) do so. Naturally, different choices will result in different benefits/costs, e.g. if the demand is Extensive, then Quickly expanding will be better than Slowly expanding. The choice at current stage will also influence the benefits of next stage, since more capacity at this stage will also persist to next stage, which will be beneficial if the demand at that time is Extensive. Also, in this setting, there is a mean field congestion cost: if too many companies choose to quickly expand at a certain stage, then resource will be scarce, and the cost will be higher (e.g. higher employee wages). Other than the specific form of cost function, this application is essentially equivalent to the messenger example proposed above. By solving this problem, we can understand different capacity expansion behaviors for different companies and also how much would be saved if the companies were regulated.

5.1.1 Path space of types

At the starting site , each agent gets a parcel of two possible types:

-

E.

Express type, which is better to be delivered as quickly as possible, otherwise a penalty will be imposed.

-

N.

Normal type, which can be delivered either quickly or slowly, and no penalty will be imposed based on that.

After delivering the parcel to , each agent gets another parcel to be delivered from to . The parcel can again be of the two types described above. Therefore, the type space is , and the path space of types is . In accordance with the notation introduced in Section 2, we denote by the random process of types on the path space, that has fixed (and known) distribution .

5.1.2 Path space of actions and cost function

For delivering parcels between each pair of sites, the agents have two kinds of roads between which to choose: Quick road (Q) and Slow road (S). Therefore, the action space is , and the path space of actions is . Taking a Slow road is penalized when delivering a parcel of Express type. Specifically, if a messenger’s parcel is of Express type and she takes the Slow road, there will be a penalty of . Taking the Slow road in the first stage also affects the delivery time of the parcel to be delivered in the second stage. This results in a cost of when taking S in the first stage while having a parcel E in the second stage. In addition, there is a mean-field cost that takes into account congestion, and equals the percentage of agents taking the same road.

The distribution of the action process has support on the four points , , and we denote the respective probabilities by . The cost just described fits into the separable cost framework (3.2), where the type-action part is described by the matrix:

| Q,Q | Q,S | S,Q | S,S | |

|---|---|---|---|---|

| E,E | 0 | 0.5 | 0.5 | 1 |

| E,N | 0 | 0 | 0.5 | 0.5 |

| N,E | 0 | 0.5 | 0.25 | 0.75 |

| N,N | 0 | 0 | 0 | 0 |

and the mean-field part of the cost is given by:

Note that the functional defined above is the first variation of the energy functional given by

| (5.1) |

To see this, fix any measure and let . The probabilities , are defined coherently with previous notation. Then we have

5.1.3 Static versus dynamic equilibria

We define the type distribution via a parameter . At the first step we have , while the transition probabilities for the second step are

In the two tables below we report agents’ configurations at equilibria (optimal ’s) in the two cases:

-

A.

agents know the full type path from the beginning (i.e. static equilibria, as studied in [15]);

-

B.

agents know the type distribution from the beginning, but the actual paths are only revealed progressively in time (i.e. dynamic equilibria studied in the present paper).

We consider several values of , to illustrate the effect of having full versus non-anticipative information. Mathematically, this means that the tables in B are calculated by solving problem (3.5), namely

whereas those in A are computed by replacing COT with OT, namely

A. Static Cournot-Nash equilibria for different values of .

B. Dynamic Cournot-Nash equilibria for different values of .

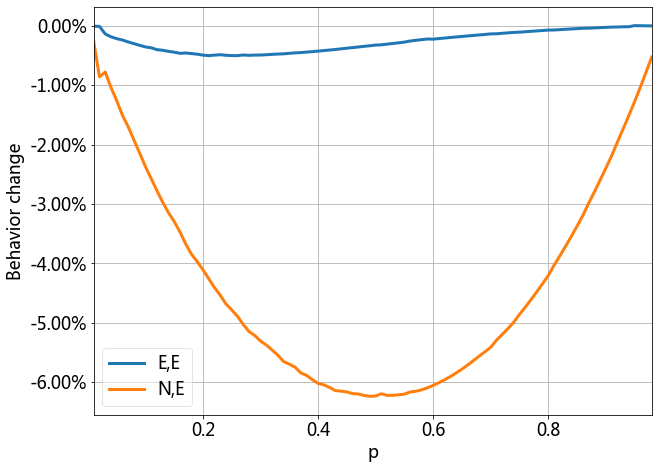

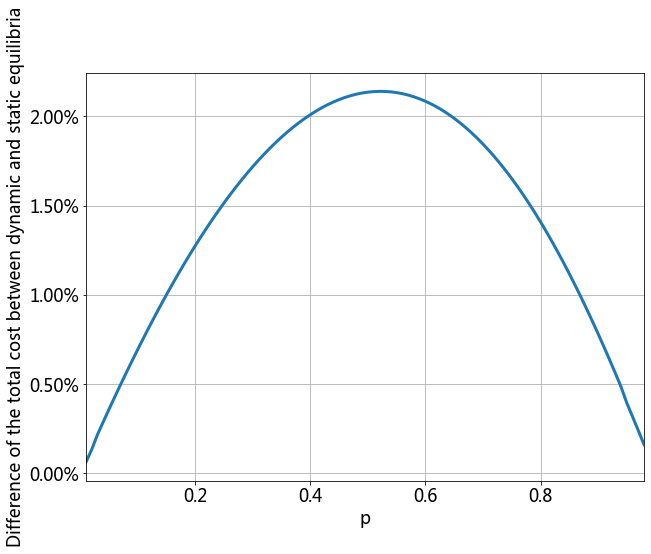

As expected, knowing future types affects agents’ choice in previous times as well. To wit, an agent that at the first stage already knows that she will get a parcel E at the next stage (rows 1 and 3, table A) will have more incentive to take the Q road in the first stage, as compared to the case where she only knows the current type (table B). To see this phenomenon more clearly, in Figure 2-l.h.s. we illustrate the different behaviour of agents of type (E,E) and (N,E) in the static and dynamic case, as function of the parameter . Obviously in the two extreme situations , the knowledge of the distribution already reveals the full type path from the outset of the game, and thus static and dynamic equilibria coincide. The farther we are from these trivial situations, the more difference of information there is between static and dynamic case, hence the bigger the difference in the behaviour of agents at equilibrium. An analogous effect is seen in Figure 2-r.h.s., where we report the (relative) difference between total cost in the static and dynamic equilibria.

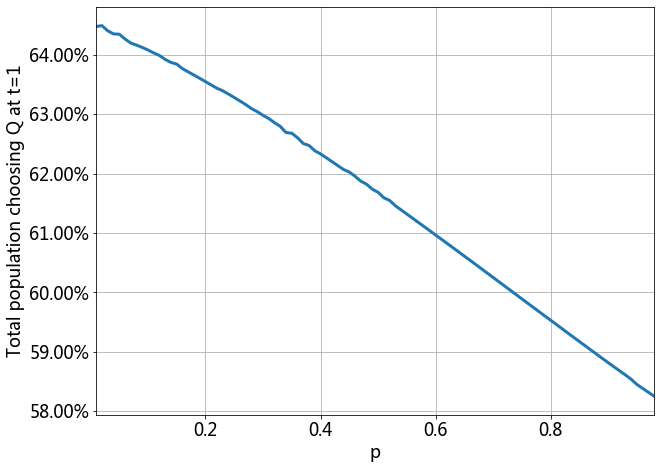

Figure 3 reports the probability of taking the Q road at stage 1 in the dynamic Cournot-Nash equilibria. Note that corresponds to the case where all agents switch parcel type from stage 1 to stage 2, while corresponds to the case of all agents getting in stage 2 the same parcel type they get in stage 1. Clearly, in the first case all agents have some incentive to take the Q road at stage 1, either because they have a parcel E at that stage, or because they will have it at the next stage, since in either case taking the S road would involve a penalty. On the other hand, in the second case, only half of the agents, the (E,E) type, have such an incentive. This observation gives the right intuition about the behaviour of agents at equilibrium, as we see from the monotonicity illustrated in Figure 3.

5.1.4 Price of Anarchy

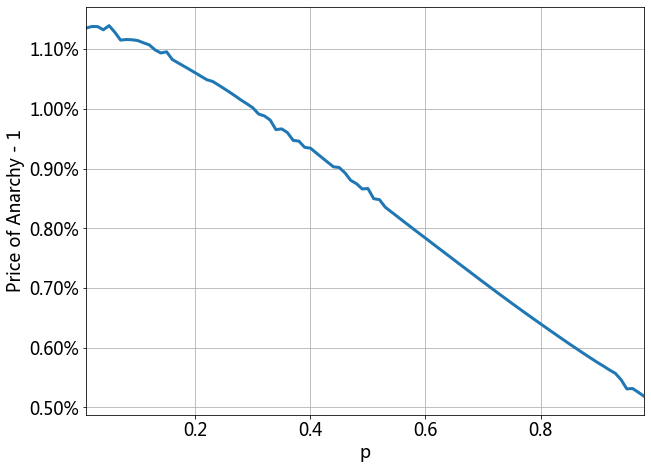

Let the type distribution be as in Section 5.1.3. Note that, since the functional in (5.1) is strictly convex, by Corollary 3.6 the distribution of the optimal actions is unique, and so is the total cost associated to competitive equilibria. The latter equals , and is the numerator of the PoA in (3.9). In Figure 4 we plot the Price of Anarchy against . We notice that the smaller is, that is, the higher the probability of switching parcel type between stage 1 and 2, the higher the PoA, thus, the higher the difference between competitive and cooperative equilibria. The rationale here is that congestion at the first stage increases when becomes smaller, since in that case there is a stronger incentive to take the Quick road.

5.2 On closed-form solutions: The Knothe-Rosenblatt case

We will now consider a class of cost functions in discrete time for which we can characterize the optimal transport problem inside (3.5), and thus mixed-strategy equilibria too, thanks to Theorem 3.4. We denote by the cumulative distribution of (with projection onto the first coordinate), and by the cumulative distribution of the -marginal of given the first ones, whenever is a measure in multiple dimensions. The increasing -dimensional Knothe-Rosenblatt rearrangement555 The reader might know it by the name quantile transform or Knothe-Rosenblatt coupling. of and is defined as the law of the random vector where

| (5.2) | ||||

for independent and uniformly distributed random variables on . Additionally, if -a.s. all the conditional distributions of are atomless (e.g. if has a density), then this rearrangement is induced by the (Monge) map

where and

In the proposition below we use the notation and .

Proposition 5.1.

Assume that one of the following conditions is satisfied:

-

(a)

has independent marginals, and is such that, for all , satisfies the Spence-Mirrlees condition ;

-

(b)

has independent increments, and , with convex.

Then Cournot-Nash equilibria (if they exist) are determined by the second marginal, and precisely given by the Knothe-Rosenblatt rearrangement. Moreover, if has a density, all Cournot-Nash equilibria are in fact pure (and given by the Knothe-Rosenblatt map).

Proof.

Under condition (a) or (b), Theorem 2.7 and Corollary 2.8 in [BBLZ] imply that, for any , the causal transport problem COT admits a unique solution which is given by the Knothe-Rosenblatt rearrangement, and that if has a density, then the unique solution to COT is given by the Knothe-Rosenblatt map. Theorem 3.4 above concludes. ∎

6 Appendix

6.1 Auxiliary results and profs

Lemma 6.1.

Let be a weakly compact set of measures, and be given. Then the set is weakly compact.

Proof.

Call and the Polish topologies of and , respectively. Consider

for (some) regular conditional distributions of . We can view the collection of these measurable mappings as a measurable function from into a Polish space. By [33, Theorem 13.11], there is a stronger Polish topology on , which we call , whose Borel sets are the same as for , and such that the above mapping is continuous when the domain space is given the topology. Let us denote by the topology on generated by convergence w.r.t. -continuous bounded functions, and the topology generated by convergence w.r.t. -continuous bounded functions. By [9, Proposition 2.4] we know that causality can be tested by integration against functions of the form

for each , bounded -continuous and bounded -continuous. Notice that the function in brackets is then by definition also -continuous, so the overall expression is -continuous. It follows that is -closed. On the other hand, is also -tight, since as a Borel measure is still tight w.r.t. the stronger topology induced by -continuous bounded functions. Thus is -compact and in particular also -compact. ∎

Proof of Theorem 4.3.

The existence follows from Lemma 6.1, since is weakly compact, and the functional is lower semicontinuous. For the duality, me may first stregthen the topology on , just as we did in the proof of Lemma 6.1, so guaranteeing that the conditional distributions are continuous. Doing so shows that each is continuous after strengthening the topology. Similarly, the proof of [9, Proposition 2.4] reveals that the martingales are determined by the conditional distributions , and so each can be assumed continuous after strengthening the topology. Crucially, since remains a Borel measure after this strengthening of topology, the set is still compact after we accordingly strengthen the weak topology on . This proves that

by Proposition 4.1 and a familiar application of Sion’s minimax theorem. The remaining identities are obtained by applying Kantorovich duality (cf. [45]) to and . ∎

Lemma 6.2.

If is lower bounded and lower semicontinuous, then

Proof.

Very similar to the proof of Theorem 4.3, where Sion’s minimax theorem is invoked. We only have to check that is convex and lower semicontinuous. Letting , which is a convex continuous function on , this immediately implies that is convex and continuous. ∎

6.2 Basis for

We first get a better understanding of -adapted and -adapted processes, as introduced at the beginning of Section 4, in the finite setting of Assumption 4.4, where and . Consider the case where we have three-steps, , and two possible actions, say . Then the path space of actions can be represented with the tree in Figure 5.

We call ‘node’ every box of the tree, and ‘leaf’ any node at the terminal time . Now, any -adapted process can be represented with a tree with same structure, while having any possible values in the nodes. Clearly, a basis for such processes can be given by assigning the value 1 to any of the nodes of the tree and 0 to all other nodes. This means that -adapted processes can be identified with elements in . In general, for any number of steps and any number of actions , -adapted processes are identified with vectors in , with .

Analogously, we can represent the path space of types with a tree, which defines the structure of all -adapted processes. Now, to build the set , we are only interested in -adapted processes that are -martingales. For these processes, knowing the values at terminal time is enough, since values at previous times are then determined by backward recursion thanks to the martingale property. A basis for such processes can therefore be given by assigning 1 to any of the leaves of the tree representing , and 0 to all other leaves. -adapted -martingales can therefore be identified with vectors in .

Finally, is generated by the finite basis of elements of the form , where is a basis for the -adapted processes and is a basis for the -adapted -martingales. We denote such a basis for by , where .

References

- [1] Beatrice Acciaio, Julio Backhoff-Veraguas, and René Carmona. Extended mean field control problems: stochastic maximum principle and transport perspective. SIAM Journal on Control and Optimization,, 57(6):3666–3693, 2019.

- [2] Beatrice Acciaio, Julio Backhoff-Veraguas, and Anastasiia Zalashko. Causal optimal transport and its links to enlargement of filtrations and continuous-time stochastic optimization. Stochastic Processes and their Applications, 130(5):2918–2953, 2020.

- [3] Beatrice Acciaio, Michael Munn, Li K. Wenliang, and Tianlin Xu. Cot-gan: Generating sequential data via causal optimal transport. NeurIPS, 2020.

- [4] Yves Achdou, Martino Bardi, and Marco Cirant. Mean field games models of segregation. Mathematical Models and Methods in Applied Sciences, 27(01):75–113, 2017.

- [5] Yves Achdou and Italo Capuzzo-Dolcetta. Mean field games: numerical methods. SIAM Journal on Numerical Analysis, 48(3):1136–1162, 2010.

- [6] Yves Achdou and Mathieu Laurière. Mean field games and applications: Numerical aspects. arXiv preprint arXiv:2003.04444, 2020.

- [7] Noha Almulla, Rita Ferreira, and Diogo Gomes. Two numerical approaches to stationary mean-field games. Dynamic Games and Applications, 7(4):657–682, 2017.

- [8] Julio Backhoff-Veraguas, Daniel Bartl, Beiglböck Mathias, and Eder Manu. Adapted Wasserstein distances and stability in mathematical finance. Finance and Stochastics, 24(3):601–632, 2020.

- [9] Julio Backhoff-Veraguas, Mathias Beiglbock, Yiqing Lin, and Anastasiia Zalashko. Causal transport in discrete time and applications. SIAM Journal on Optimization, 27(4):2528–2562, 2017.

- [10] Martino Bardi. Explicit solutions of some linear-quadratic mean field games. Networks & Heterogeneous Media, 7(2):243, 2012.

- [11] Erhan Bayraktar and Yuchong Zhang. Terminal ranking games. arXiv preprint arXiv:1906.09628, 2019.

- [12] Jean-David Benamou, Guillaume Carlier, and Filippo Santambrogio. Variational mean field games. In Active Particles, Volume 1, pages 141–171. Springer, 2017.

- [13] Adrien Blanchet and Guillaume Carlier. From Nash to Cournot-Nash equilibria via the Monge-Kantorovich problem. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 372(2028):20130398, 2014.

- [14] Adrien Blanchet and Guillaume Carlier. Remarks on existence and uniqueness of Cournot-Nash equilibria in the non-potential case. Mathematics and Financial Economics, 8(4):417–433, 2014.

- [15] Adrien Blanchet and Guillaume Carlier. Optimal transport and Cournot-Nash equilibria. Mathematics of Operations Research, 41(1):125–145, 2016.

- [16] Adrien Blanchet, Guillaume Carlier, and Luca Nenna. Computation of Cournot-Nash equilibria by entropic regularization. Vietnam Journal of Mathematics, 46(1):15–31, 2018.

- [17] Pierre Cardaliaguet. Notes on mean field games (from P.-L. Lions’ lectures at Collège de France). 2010.

- [18] Pierre Cardaliaguet, François Delarue, Jean-Michel Lasry, and Pierre-Louis Lions. The master equation and the convergence problem in mean field games. arXiv preprint arXiv:1509.02505, 2015.

- [19] René Carmona and François Delarue. Probabilistic Theory of Mean Field Games with Applications I-II. Springer, 2018.

- [20] René Carmona, Christy V Graves, and Zongjun Tan. Price of anarchy for mean field games. ESAIM: Proceedings and Surveys, 65:349–383, 2019.

- [21] Alekos Cecchin and Markus Fischer. Probabilistic approach to finite state mean field games. Applied Mathematics & Optimization, 81(2):253–300, 2020.

- [22] Alekos Cecchin, Paolo Dai Pra, Markus Fischer, and Guglielmo Pelino. On the convergence problem in mean field games: a two state model without uniqueness. SIAM Journal on Control and Optimization, 57(4):2443–2466, 2019.

- [23] Marco Cuturi. Sinkhorn distances: Lightspeed computation of optimal transport. In Advances in neural information processing systems, pages 2292–2300, 2013.

- [24] John M Danskin. The theory of max-min, with applications. SIAM Journal on Applied Mathematics, 14(4):641–664, 1966.

- [25] Nicole El Karoui, Du Huu Nguyen, and Monique Jeanblanc-Picqué. Existence of an optimal Markovian filter for the control under partial observations. SIAM journal on control and optimization, 26(5):1025–1061, 1988.

- [26] Rita Ferreira and Diogo A Gomes. On the convergence of finite state mean-field games through -convergence. Journal of Mathematical Analysis and Applications, 418(1):211–230, 2014.

- [27] Wendell Fleming and Makiko Nisio. On stochastic relaxed control for partially observed diffusions. Nagoya Mathematical Journal, 93:71–108, 1984.

- [28] Diogo Gomes, Roberto M Velho, and Marie-Therese Wolfram. Socio-economic applications of finite state mean field games. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 372(2028):20130405, 2014.

- [29] Diogo A Gomes, Joana Mohr, and Rafael Rigao Souza. Discrete time, finite state space mean field games. Journal de mathématiques pures et appliquées, 93(3):308–328, 2010.

- [30] P Jameson Graber. Linear quadratic mean field type control and mean field games with common noise, with application to production of an exhaustible resource. Applied Mathematics & Optimization, 74(3):459–486, 2016.

- [31] Minyi Huang, Peter E Caines, and Roland P Malhamé. Large-population cost-coupled lqg problems with nonuniform agents: individual-mass behavior and decentralized -Nash equilibria. IEEE transactions on automatic control, 52(9):1560–1571, 2007.

- [32] Minyi Huang, Roland P Malhamé, and Peter E Caines. Large population stochastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence principle. Communications in Information & Systems, 6(3):221–252, 2006.

- [33] Alexander Kechris. Classical descriptive set theory, volume 156 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1995.

- [34] Daniel Lacker. A general characterization of the mean field limit for stochastic differential games. Probability Theory and Related Fields, 165(3-4):581–648, 2016.

- [35] Daniel Lacker and Kavita Ramanan. Rare Nash equilibria and the price of anarchy in large static games. Mathematics of Operations Research, 44(2):400–422, 2019.

- [36] Jean-Michel Lasry and Pierre-Louis Lions. Jeux à champ moyen. i–le cas stationnaire. Comptes Rendus Mathématique, 343(9):619–625, 2006.

- [37] Jean-Michel Lasry and Pierre-Louis Lions. Mean field games. Japanese journal of mathematics, 2(1):229–260, 2007.

- [38] Rémi Lassalle. Causal transport plans and their Monge-Kantorovich problems. Stochastic Analysis and Applications, 36(3):452–484, 2018.

- [39] Andreu Mas-Colell. On a theorem of Schmeidler. Journal of Mathematical Economics, 13(3):201–206, 1984.

- [40] Marcel Nutz, Jaime San Martin, Xiaowei Tan, et al. Convergence to the mean field game limit: a case study. The Annals of Applied Probability, 30(1):259–286, 2020.

- [41] Gabriel Peyré and Marco Cuturi. Computational Optimal Transport: With Applications to Data Science. Now Foundations and Trends, 2019.

- [42] Georg Pflug. Version-independence and nested distributions in multistage stochastic optimization. SIAM Journal on Optimization, 20(3):1406–1420, 2009.

- [43] Georg Pflug and Alois Pichler. A distance for multistage stochastic optimization models. SIAM Journal on Optimization, 22(1):1–23, 2012.

- [44] Georg Pflug and Alois Pichler. Multistage stochastic optimization. Springer Series in Operations Research and Financial Engineering. Springer, Cham, 2014.

- [45] Cedric Villani. Topics in optimal transportation. Number 58. American Mathematical Soc., 2003.

- [46] Anastasiia Zalashko. Causal optimal transport: theory and applications. PhD thesis, University of Vienna, 2017.