Stochastic Gauss-Newton Algorithms for Nonconvex Compositional Optimization

Abstract

We develop two new stochastic Gauss-Newton algorithms for solving a class of non-convex stochastic compositional optimization problems frequently arising in practice. We consider both the expectation and finite-sum settings under standard assumptions, and use both classical stochastic and SARAH estimators for approximating function values and Jacobians. In the expectation case, we establish iteration-complexity to achieve a stationary point in expectation and estimate the total number of stochastic oracle calls for both function value and its Jacobian, where is a desired accuracy. In the finite sum case, we also estimate iteration-complexity and the total oracle calls with high probability. To our best knowledge, this is the first time such global stochastic oracle complexity is established for stochastic Gauss-Newton methods. Finally, we illustrate our theoretical results via two numerical examples on both synthetic and real datasets.

1 Introduction

We consider the following nonconvex stochastic compositional nonconvex optimization problem:

| (1) |

where is a stochastic function defined on a probability space , is a proper, closed, and convex, but not necessarily smooth function, and is the expectation of w.r.t. to .

As a special case, if is finite, i.e. and for and , then by introducting , can be written into a finite-sum , and (1) reduces to

| (2) |

This expression can also be viewed as a stochastic average approximation of in (1). Note that the setting (1) is completely different from in Davis & Grimmer (2019); Davis & Drusvyatskiy (2019); Duchi & Ruan (2018).

Problem (1) or its special form (2) covers various applications in different domains (both deterministic and stochastic) such as penalized problems for constrained optimization, parameter estimation, nonlinear least-squares, system identification, statistical learning, dynamic programming, and minimax problems (Drusvyatskiy & Paquette, 2019; Duchi & Ruan, 2018; Lewis & Wright, 2016; Nesterov, 2007; Tran-Dinh & Diehl, 2011; Wang et al., 2017a). Note that both (1) and (2) cover the composite form

| (3) |

for a given convex function if we introduce and to reformulate it into (1) or (2). This formulation, on the other hand, is an extension of (1). We will also show how to handle (3) in Subsection 4.3.

Our goal in this paper is to develop novel stochastic methods to solve (1) and (2) based on the following assumptions:

Assumption 1.1.

Assumption 1.2.

There exist such that the variance of and is uniformly bounded, i.e., and , respectively. In the finite sum case (2), we again impose stronger conditions and for all and for all .

Assumptions 1.1 and 1.2 are standard and cover a wide class of models in practice as opposed to existing works. The stronger assumptions imposed on (2) allow us to develop adaptive subsampling schemes later.

Related work. Problem (1) or (2) has been widely studied in the literature under both deterministic (including the finite-sum (2) and ) and stochastic settings, see, e.g., (Drusvyatskiy & Paquette, 2019; Duchi & Ruan, 2018; Lewis & Wright, 2016; Nesterov, 2007; Tran-Dinh & Diehl, 2011; Wang et al., 2017a). If and , then (1) reduces to the standard stochastic optimization model studied in, e.g. Ghadimi & Lan (2016); Pham et al. (2020). In the deterministic setting, the common method to solve (1) is the Gauss-Newton (GN) scheme, which is also known as the prox-linear method. This method has been studied in several papers, including Drusvyatskiy & Paquette (2019); Duchi & Ruan (2018); Lewis & Wright (2016); Nesterov (2007); Tran-Dinh & Diehl (2011). In such settings, GN only requires Assumption 1.1 to have global convergence guarantees (Drusvyatskiy & Paquette, 2019; Nesterov, 2007).

In the stochastic setting of the form (1), Wang et al. (2017a, b) proposed stochastic compositional gradient descent methods to solve more general forms than (1), but they required a set of stronger assumptions than Assumptions 1.1 and 1.2, including the smoothness of . These methods eventually belong to a gradient-based class. Other works in this direction include Lian et al. (2017); Yu & Huang (2017); Yang et al. (2019); Liu et al. (2017); Xu & Xu (2019), which also rely on a similar approach. Together with algorithms, convergence guarantees and stochastic oracle complexity bounds have also been estimated. For instance, Wang et al. (2017a) estimates oracle complexity for solving (1), while it is improved to in Wang et al. (2017b). Recent works such as Zhang & Xiao (2019a) further improve the complexity to . However, these methods are completely different from GN and require much stronger assumptions, including the smoothness of and .

One main challenge to design algorithms for solving (1) is the bias of stochastic estimators. Some researchers have tried to remedy this issue by proposing more sophisticated sampling schemes, see, e.g., Blanchet et al. (2017). Other works relies on biased estimators but using variance reduction techniques, e.g., Zhang & Xiao (2019a).

Challenges. The stochastic formulation (1) creates several challenges for developing numerical methods. First, it is often nonconvex. Many papers consider special cases when is convex. This only holds if is convex and is linear, or is convex and monotone and is convex or concave. Clearly, such a setting is almost unrealistic or very limited. One can assume weak convexity of and add a regularizer to make the resulting problem convex but this completely changes the model. Second, is often non-smooth such as norm, penalty, or gauge functions. This prevents the use of gradient-based methods. Third, even when both and are smooth, to guarantee Lipschitz continuity of , it requires simultaneously , , , and to be Lipschitz continuous. This condition is very restrictive and often requires additional bounded constraints or bounded domain assumption. Otherwise, it fails to hold even for bilinear functions. Finally, in stochastic settings, it is very challenging to form unbiased estimate for gradients or subgradients of , making classical stochastic-based method inapplicable.

Our approach and contribution. Our main motivation is to overcome the above challenges by following a different approach.111When this paper was under review, Zhang & Xiao (2020) was brought to our attention, which presents similar methods. We extend the GN method from the deterministic setting (Lewis & Wright, 2016; Nesterov, 2007) to the stochastic setting (1). Our methods can be viewed as inexact variants of GN using stochastic estimators for both function values and its Jacobian . This approach allows us to cover a wide class of (1), while only requires standard assumptions as Assumptions 1.1 and 1.2. Our contribution can be summarized as follows:

-

(a)

We develop an inexact GN framework to solve (1) and (2) using inexact estimations of and its Jacobian . This framework is independent of approximation schemes for generating approximate estimators. We characterize approximate stationary points of (1) and (2) via prox-linear gradient mappings. Then, we prove global convergence guarantee of our method to a stationary point under appropriate inexact computation.

-

(b)

We analyze stochastic oracle complexity of our GN algorithm when mini-batch stochastic estimators are used. We separate our analysis into two cases. The first variant is to solve (1), where we obtain convergence guarantee in expectation. The second variant is to solve (2), where we use adaptive mini-batches and obtain convergence guarantee with high probability.

-

(c)

We also provide oracle complexity of this algorithm when mini-batch SARAH estimators in Nguyen et al. (2017, 2019) are used for both (1) and (2). Under an additional mild assumption, this estimator significantly improves the oracle complexity by an order of compared to the mini-batch stochastic one.

We believe that our methods are the first ones to achieve global convergence rates and stochastic oracle complexity for solving (1) and (2) under standard assumptions. It is completely different from existing works such as Wang et al. (2017a, b); Lian et al. (2017); Yu & Huang (2017); Yang et al. (2019); Zhang & Xiao (2019a), where we only use Assumptions 1.1 and 1.2, while not imposing any special structure on and , including smoothness. When using SARAH estimators, we impose the Lipschitz continuity of to achieve better oracle complexity. This additional assumption is still much weaker than the ones used in existing works. However, without this assumption, our GN scheme with SARAH estimators still converges (see Remark 4.1).

Content. Section 2 recalls some mathematical tools. Section 3 develops an inexact GN framework. Sections 4 analyzes convergence and complexity of the two stochastic GN variants using different stochastic estimators. Numerical examples are given in Section 5. All the proofs and discussion are deferred to Supplementary Document (Supp. Doc.).

2 Background and Mathematical Tools

We first characterize the optimality condition of (1). Next, we recall the prox-linear mapping of the compositional function and its properties.

Basic notation. We work with Euclidean spaces and . Given a convex set , denotes the Euclidean distance from to . For a convex function , we denote its subdifferential, its gradient, and its Fenchel conjugate. For a smooth function , denotes its Jacobian. For vectors, we use Euclidean norms, while for matrices, we use spectral norms, i.e., . stands for number rounding.

2.1 Exact and Approximate Stationary Points

The optimality condition of (1) can be written as

| (5) |

Any satisfying (5) is called a stationary point of (1) or (2).

Since is convex, let be its Fenchel conjugate and . Then, (5) can be rewritten as

| (6) |

Now, if we define

| (7) |

then the optimality condition (5) of (1) or (2) becomes

| (8) |

Note that once a stationary point is available, we can compute as any element of .

In practice, we can only find an approximate stationary point and its dual such that approximates of (1) or (2) up to a given accuracy as follows:

Definition 2.1.

Given , we call an -stationary point of (1) if there exists such that

| (9) |

where is defined by (7). This condition can be characterized in expectation, where is taken over all the randomness generated by the problem and the corresponding stochastic algorithm, or with high probability . Such guarantees will be specified in the sequel.

2.2 Prox-Linear Operator and Its Properties

(a) Prox-linear operator. Since we assume that the Jacobian of is Lipschitz continuous with a Lipschitz constant , and is -Lipschitz continuous as in Assumption 1.1, we have (see Supp. Doc. A):

| (10) |

for all . Given , let and be a deterministic or stochastic approximation of and its Jacobian , respectively. We consider the following approximate prox-linear model:

| (11) |

where is a given constant. As usual, if and , then

| (12) |

is the exact prox-linear operator of . In this context, we also call an approximate prox-linear operator of .

(b) Prox-gradient mapping. We also define the prox-gradient mapping and its approximation, respectively as

| (13) |

Clearly if , then and is a stationary point of (1). In our context, we can only compute as an approximation of .

(c) Characterizing approximate stationary points. The following lemma bounds the optimality error defined by (7) via the approximate prox-gradient mapping .

Lemma 2.1.

3 Inexact Gauss-Newton Framework

In this section, we develop a conceptual inexact Gauss-Newton (iGN) framework for solving (1) and (2).

3.1 Descent Property and Approximate Conditions

Lemma 3.1 provides a key bound regarding (2.2), which will be used for convergence analysis of our algorithms.

Since we approximate both and its Jacobian in our prox-linear model (2.2), we assume that this approximation satisfies one of the following two conditions:

-

•

Condition 1: Given a tolerance and , at each iterate , it holds that

(16) where .

-

•

Condition 2: Given , , and , let and such that . For , we assume that

(17) while, for any iterate (), we assume that

(18)

The condition (16) assumes that both and should respectively well approximate and up to a given accuracy . Here, the function value must have higher accuracy than its Jacobian . The condition (18) is adaptive, which depends on the norm of the iterates and . This condition is less conservative than (16).

3.2 The Inexact Gauss-Newton Algorithm

We first present a conceptual stochastic Gauss-Newton method as described in Algorithm 1.

Algorithm 1 remains conceptual since we have not specified how to form and .

3.3 Convergence Analysis

Let us first state the convergence of Algorithm 1 under Conditon 1 or Condition 2 in the following theorem.

Theorem 3.1.

Remark 3.1.

The guarantee implies that . That is there exists subsequence of such that as and .

4 Stochastic Gauss-Newton Methods

4.1 SGN with Mini-Batch Stochastic Estimators

As a natural instance of Algorithm 1, we propose to approximate and in Algorithm 1 by mini-batch stochastic estimators as:

| (21) |

where the mini-batches and are not necessarily independent, , and . Using (21) we prove our first result in expectation on stochastic oracle complexity of Algorithm 1 for solving (1).

In practice, we may not need to explicitly form , but its matrix-vector product for some vector , when evaluating the prox-linear operator . This requires , which can be evaluated efficiently by using, e.g., automatic differentiation techniques.

Theorem 4.1.

Suppose that Assumptions 1.1 and 1.2 hold for (1). Let and defined by (21) be mini-batch stochastic estimators of and , respectively. Let be generated by Algorithm 1 called SGN to solve (1). Assume that and in (21) are chosen as

| (22) |

for some constant and . Furthermore, let be chosen uniformly at random in as the output of Algorithm 1 after iterations. Then

| (23) |

where .

Moreover, the number of function evaluations and the number of Jacobian evaluations to achieve do not exceed

| (24) |

Note that if we replace and in (22) by and , respectively, then the result of Theorem 4.1 still holds for (2) since it is a special case of (1).

Now, we derive the convergence result of Algorithm 1 for solving (2) using adaptive mini-batches. However, our convergence guarantee is obtained with high probability.

Theorem 4.2.

Suppose that Assumptions 1.1 and 1.2 hold for (2). Let and defined by (21) be mini-batch stochastic estimators to approximate and , respectively. Let be generated by Algorithm 1 for solving (2). Assume that and in (21) are chosen such that and for , with

| (25) |

for , and , , and given in Condition 2. Then, with probability at least , the bound (20) in Theorem 3.1 still holds.

Moreover, the total number of stochastic function evaluations and the total number of stochastic Jacobian evaluations to guarantee do not exceed

| (26) |

To the best of our knowledge, the oracle complexity bounds stated in Theorems 4.1 and 4.2 are the first results for the stochastic Gauss-Newton methods described in Algorithm 1 under Assumptions 1.1 and 1.2. Whereas there exist several methods for solving (1), these algorithms are either not in the form of GN schemes as ours or rely on a different set of assumptions. For instance, Duchi & Ruan (2018); Duchi et al. (2011) considers a different model and uses stochastic subgradient methods, while Zhang & Xiao (2019a, b) directly applies a variance reduction gradient descent method and requires a stronger set of assumptions.

4.2 SGN with SARAH Estimators

Algorithm 1 with mini-batch stochastic estimators (21) has high oracle complexity bounds when is sufficiently small, especially for function evaluations . We attempt to reduce this complexity by exploiting a biased estimator called SARAH in Nguyen et al. (2017) in this subsection.

More concretely, we approximate and by using the following SARAH estimators, respectively:

| (27) |

where the snapshots and are given, and and are two mini-batches of size and .

Using both the standard stochastic estimators (21) and these SARAH estimators (27), we modify Algorithm 1 to obtain the following double-loop variant as in Algorithm 2.

In Algorithm 2, every outer iteration , we take a snapshot using (21). Then, we run Algorithm 2 up to iterations in the inner loop but using SARAH estimators (27). Unlike (21), we are unable to exploit matrix-vector products for in (27) due to its dependence on .

Let us first prove convergence and oracle complexity estimates in expectation of Algorithm 2 for solving (1). However, we require an additional assumption for this case:

Assumption 4.1.

is -average Lipschitz continuous, i.e. for all .

Though Assumption 4.1 is relatively strong, it has been used in several models, including neural network training under a bounded weight assumption.

Given a tolerance and , we first choose , , and two constants and such that

| (28) |

Next, we choose the mini-batch sizes of , , , and , respectively as follows:

| (29) |

Then, the following theorem states the convergence and oracle complexity bounds of Algorithm 2.

Theorem 4.3.

Suppose that Assumptions 1.1 and 1.2, and 4.1 are satisfied for (1). Let be generated by Algorithm 2 to solve (1). Let and be chosen by (28), and the mini-batches , , , and be set as in (29). Assume that the output of Algorithm 2 is chosen uniformly at random in . Then:

The following bound holds

| (30) |

The total number of iterations to obtain is at most

Moreover, the total stochastic oracle calls and for evaluating stochastic estimators of and its Jacobian , respectively do not exceed:

| (31) |

Finally, we show that computed by our methods is indeed an approximate stationary point of (1) or (2).

Corollary 4.1.

Proof.

4.3 Extension to The Regularization Setting (3)

It is straight forward to extend our methods to handle a regularizer as in (3). If is nonsmooth and convex, then we can modify (2.2) as follows:

| (32) |

Then, we obtain variants of Algorithms 1 and 2 for solving (3), where our theoretical guarantees in this paper remain preserved. This subproblem can efficiently be solved by primal-dual methods as presented in Supp. Doc. E. If is -smooth, then we can replace in (2.2) by its quadratic surrogate .

5 Numerical Experiments

We conduct two numerical experiments to evaluate the performance of Algorithm 1 (SGN) and Algorithm 2 (SGN2). Further details of our experiments are in Supp. Doc. F.

5.1 Stochastic Nonlinear Equations

We consider a nonlinear equation: as the expectation of a stochastic function . This equation can be viewed as a natural extension of nonlinear equations from a deterministic setting to a stochastic setting, including stochastic dynamical systems and PDEs. It can also present as the first-order optimality condition of a stochastic optimization problem . Moreover, it can be considered as a special case of stochastic variational inequality in the literature, see, e.g., Rockafellar & Wets (2017).

Instead of directly solving , we can formulate it into the following minimization problem:

| (33) |

where such that is the expectation of , i.e., for , and is a given norm (e.g., -norm or -norm).

Assume that we take average approximation of to obtain a finite sum for sufficiently large . In the following experiments, we choose , and for , we choose as

where is the -th row of an input matrix , and , are two input vectors, and . These functions were used in binary classification involving nonconvex losses, e.g., Zhao et al. (2010). Since they are nonnegative, if we use the -norm, then (33) can be viewed as a model average of different losses in binary classification (see Supp. Doc. F).

We implement both Algorithms 1 (SGN) and 2 (SGN2) to solve (33). We also compare them with the baseline using the full samples instead of calculating and as in (21) and (27). We call it the deterministic GN scheme (GN).

Experiment setup. We test three algorithms on four standard datasets: w8a, ijcnn1, covtype, and url_combined from LIBSVM222Available online at https://www.csie.ntu.edu.tw/cjlin/libsvm/. Further information about these dataset is described in Supp. Doc. F.

To find appropriate batch sizes for and , we perform a grid search over different combinations of mini-batch sizes to select the best ones. More information about this process can be found in Supp. Doc. F.

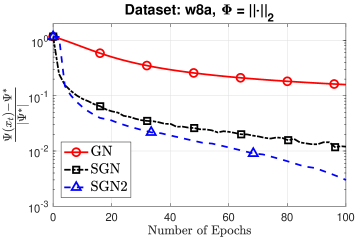

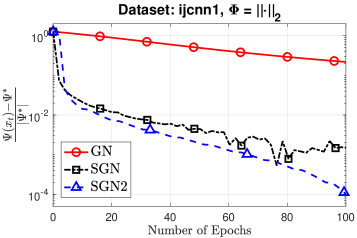

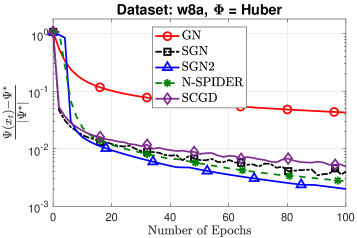

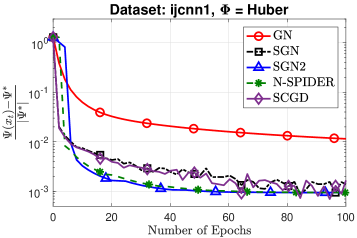

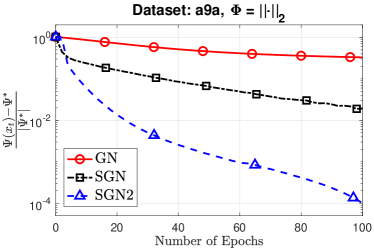

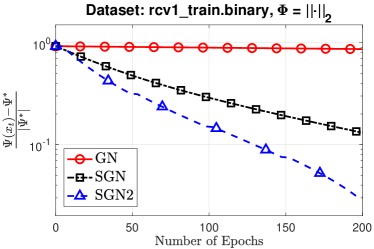

We evaluate these algorithms on instances of (33) using . We use and for all datasets. The performance of three algorithms is shown in Figure 1 for the w8a and ijcnn1 datasets. This figure depicts the relative objective residuals over the number of epochs, where is the lowest objective value obtained when running three algorithms until the relative residuals falls below . In both cases, SGN2 works best while SGN is still much better than the baseline GN in terms of sample efficiency.

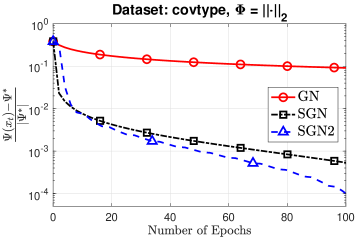

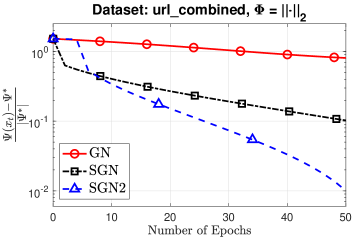

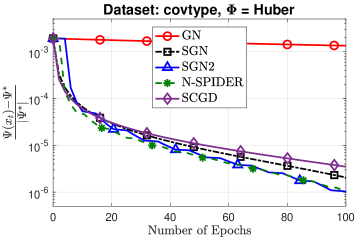

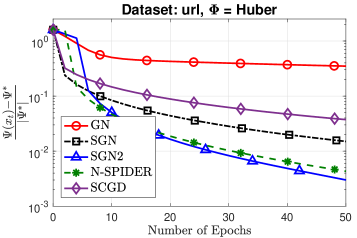

For covtype and url_combined datasets, we obverse similar behavior as shown in Figure 2, where SGN2 is more efficient than SGN, and both SGN schemes outperform GN. This experiment shows that both SGN algorithms are indeed much more sample efficient than the baseline GN algorithm.

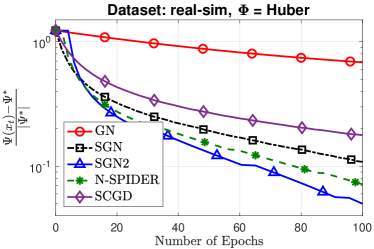

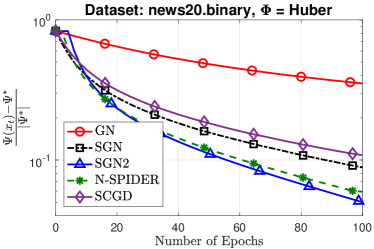

In order to compare with existing algorithms, we use a smooth objective function in (33) with a Huber loss, and otherwise, and . We implement the nested SPIDER method in Zhang & Xiao (2019a, Algorithm 3), denoted as N-SPIDER, and the stochastic compositional gradient descent in Wang et al. (2017a, Algorithm 1), denoted as SCGD.

We run 5 algorithms: GN, SGN, SGN2, N-SPIDER, and SCGD on 4 datasets as in the previous test. We choose and for all datasets. We tune the learning rate for both N-SPIDER and SCGD and finally obtain for both algorithms. We also set for N-SPIDER, see Zhang & Xiao (2019a, Algorithm 3). In addition, we conduct similar grid search as before to choose the suitable parameters for these algorithms. The chosen parameters are presented in Supp. Doc. F. The results on these datasets are depicted in Figure 3 and Figure 4.

From both figures, SGN2 seems to perform best in all datasets. N-SPIDER is better than SGN and comparable with SGN in ijcnn1 and covtye. SGN is comparable with SCGD in ijcnn1 dataset while having better performance in the remaining ones. GN still perform poorly in these cases since it use full samples to compute and .

5.2 Optimization Involving Expectation Constraints

We consider the following optimization problem:

| (34) |

where is a convex function, possibly nonsmooth, and is a smooth stochastic function. This problem has various applications such as optimization with conditional value at risk (CVaR) constraints and metric learning (Lan & Zhou, 2016) among others. Let us consider an exact penalty formulation of (34) as

| (35) |

where with and is a given penalty parameter. Clearly, (35) coincides with (3), an extension of (1).

We evaluate algorithms on the asset allocation problem (Rockafellar & Uryasev, 2000) as an instance of (34):

| (36) |

To apply our methods, we need to smooth by for a sufficiently small value . If we introduce , for , and , then we can reformulate the smoothed approximation of (36) into (3), where is the indicator of . Note that is Lipschitz continuous with the Lipschitz constant . In our experiments, we choose to be , , and . We were experimenting different and , and eventually set and .

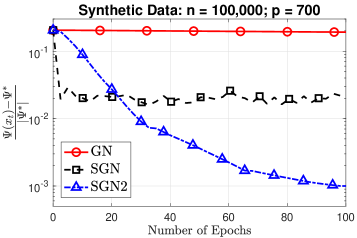

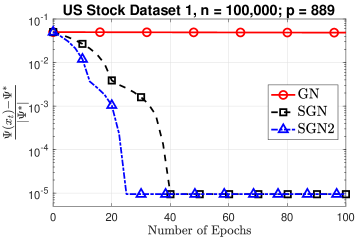

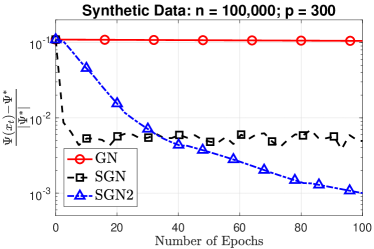

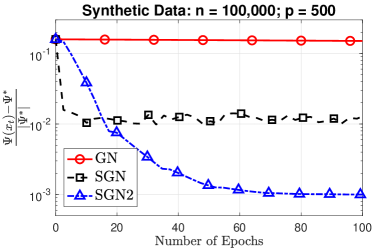

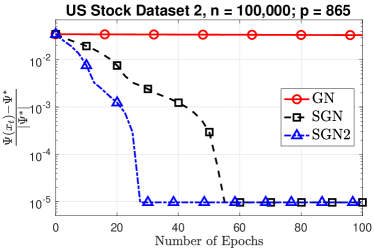

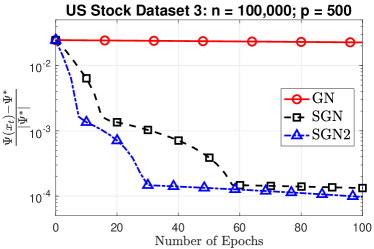

We test three algorithms: GN, SGN, and SGN2 on both synthetic and real datasets. We follow the procedures from Lan et al. (2012) to generate synthetic data with and . We also obtain real datasets of US stock prices for , , and types of stocks described, e.g., in Sun & Tran-Dinh (2019) then bootstrap them to obtain different datasets of sizes . The details and additional results are given in Supp. Doc. F.

The performance of three algorithms on these datasets is depicted in Figure 5. SGN is still much better than GN in both experiments while SGN2 is the best among three. With the large amount of samples per iteration, GN performs poorly in these experiments.

Numerical results have confirmed the advantages of SGN and SGN2 which well align with our theoretical analysis.

Acknowledgements

The work of Q. Tran-Dinh has partially been supported by the National Science Foundation (NSF), award No. DMS-1619884 and the Office of Naval Research (ONR), grant No. N00014-20-1-2088 (2020–2023). The authors are thankful to Deyi Liu for providing some parts of Python codes used in the experiment section.

References

- Bauschke & Combettes (2017) Bauschke, H. H. and Combettes, P. Convex analysis and monotone operators theory in Hilbert spaces. Springer-Verlag, 2nd edition, 2017.

- Beck & Teboulle (2009) Beck, A. and Teboulle, M. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM J. Imaging Sciences, 2(1):183–202, 2009.

- Blanchet et al. (2017) Blanchet, J., Goldfarb, D., Iyengar, G., Li, F., and Zhou, C. Unbiased simulation for optimizing stochastic function compositions. arXiv preprint arXiv:1711.07564, 2017.

- Chambolle & Pock (2011) Chambolle, A. and Pock, T. A first-order primal-dual algorithm for convex problems with applications to imaging. J. Math. Imaging Vis., 40(1):120–145, 2011.

- Davis & Drusvyatskiy (2019) Davis, D. and Drusvyatskiy, D. Stochastic model-based minimization of weakly convex functions. SIAM Journal Optim., 29(1):207–239, 2019.

- Davis & Grimmer (2019) Davis, D. and Grimmer, B. Proximally guided stochastic subgradient method for nonsmooth, nonconvex problems. SIAM J. Optim., 29(3):1908–1930, 2019.

- Drusvyatskiy & Paquette (2019) Drusvyatskiy, D. and Paquette, C. Efficiency of minimizing compositions of convex functions and smooth maps. Math. Program., 178(1-2):503–558, 2019.

- Duchi & Ruan (2018) Duchi, J. and Ruan, F. Stochastic methods for composite and weakly convex optimization problems. SIAM J. Optim., 28(4):3229–3259, 2018.

- Duchi et al. (2011) Duchi, J., Hazan, E., and Singer, Y. Adaptive subgradient methods for online learning and stochastic optimization. Journal of Machine Learning Research, 12:2121–2159, 2011.

- Esser (2010) Esser, J. E. Primal-dual algorithm for convex models and applications to image restoration, registration and nonlocal inpainting. PhD Thesis, University of California, Los Angeles, Los Angeles, USA, 2010.

- Ghadimi & Lan (2016) Ghadimi, S. and Lan, G. Accelerated gradient methods for nonconvex nonlinear and stochastic programming. Math. Program., 156(1-2):59–99, 2016.

- Goldstein et al. (2013) Goldstein, T., Esser, E., and Baraniuk, R. Adaptive primal-dual hybrid gradient methods for saddle point problems. Tech. Report., pp. 1–26, 2013. http://arxiv.org/pdf/1305.0546v1.pdf.

- Lan & Zhou (2016) Lan, G. and Zhou, Z. Algorithms for stochastic optimization with functional or expectation constraints. Comput. Optim. Appl., 76: 461–498, 2020.

- Lan et al. (2012) Lan, G., Nemirovski, A., and Shapiro, A. Validation analysis of mirror descent stochastic approximation method. Math. Program., 134(2):425–458, 2012.

- Lewis & Wright (2016) Lewis, A. S. and Wright, S. J. A proximal method for composite minimization. Math. Program., 158(1-2):501–546, 2016.

- Lian et al. (2017) Lian, X., Wang, M., and Liu, J. Finite-sum composition optimization via variance reduced gradient descent. In Artificial Intelligence and Statistics, pp. 1159–1167, 2017.

- Liu et al. (2017) Liu, L., Liu, J., and Tao, D. Variance reduced methods for non-convex composition optimization. arXiv preprint arXiv:1711.04416, 2017.

- Lohr (2009) Lohr, S. L. Sampling: Design and Analysis. Nelson Education, 2009.

- Nesterov (2004) Nesterov, Y. Introductory lectures on convex optimization: A basic course, volume 87 of Applied Optimization. Kluwer Academic Publishers, 2004.

- Nesterov (2007) Nesterov, Y. Modified Gauss-Newton scheme with worst case guarantees for global performance. Optim. Method Softw., 22(3):469–483, 2007.

- Nguyen et al. (2017) Nguyen, L. M., Liu, J., Scheinberg, K., and Takáč, M. SARAH: A novel method for machine learning problems using stochastic recursive gradient. ICML, 2017.

- Nguyen et al. (2019) Nguyen, L. M., van Dijk, M., Phan, D. T., Nguyen, P. H., Weng, T.-W., and Kalagnanam, J. R. Optimal finite-sum smooth non-convex optimization with SARAH. arXiv preprint arXiv:1901.07648, 2019.

- Pham et al. (2020) Pham, H. N., Nguyen, M. L., Phan, T. D., and Tran-Dinh, Q. ProxSARAH: An efficient algorithmic framework for stochastic composite nonconvex optimization. J. Mach. Learn. Res., 21:1–48, 2020.

- Rockafellar & Wets (2017) Rockafellar, R. T. and Wets, R. J. B. Stochastic variational inequalities: single-stage to multistage. Math. Program., 165(1):331–360, 2017.

- Rockafellar & Uryasev (2000) Rockafellar, T. R. and Uryasev, S. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000.

- Sun & Tran-Dinh (2019) Sun, T. and Tran-Dinh, Q. Generalized Self-Concordant Functions: A Recipe for Newton-Type Methods. Math. Program., 178:145–213, 2019.

- Tran-Dinh (2019) Tran-Dinh, Q. Proximal Alternating Penalty Algorithms for Constrained Convex Optimization. Comput. Optim. Appl., 72(1):1–43, 2019.

- Tran-Dinh & Diehl (2011) Tran-Dinh, Q. and Diehl, M. Proximal methods for minimizing the sum of a convex function and a composite function. Tech. Report, KU Leuven, OPTEC and ESAT/SCD, Belgium, May 2011.

- Tran-Dinh et al. (2018) Tran-Dinh, Q., Fercoq, O., and Cevher, V. A smooth primal-dual optimization framework for nonsmooth composite convex minimization. SIAM J. Optim., 28(1):96–134, 2018.

- Tropp (2012) Tropp, J. A. User-friendly tail bounds for sums of random matrices. Foundations of computational mathematics, 12(4):389–434, 2012.

- Wang et al. (2017a) Wang, M., Fang, E., and Liu, L. Stochastic compositional gradient descent: algorithms for minimizing compositions of expected-value functions. Math. Program., 161(1-2):419–449, 2017a.

- Wang et al. (2017b) Wang, M., Liu, J., and Fang, E. X. Accelerating stochastic composition optimization. The Journal of Machine Learning Research, 18(1):3721–3743, 2017b.

- Xu & Xu (2019) Xu, Y. and Xu, Y. Katyusha acceleration for convex finite-sum compositional optimization. arXiv preprint arXiv:1910.11217, 2019.

- Yang et al. (2019) Yang, S., Wang, M., and Fang, E. X. Multilevel stochastic gradient methods for nested composition optimization. SIAM J. Optim., 29(1):616–659, 2019.

- Yu & Huang (2017) Yu, Y. and Huang, L. Fast stochastic variance reduced admm for stochastic composition optimization. In Proceedings of the 26th International Joint Conference on Artificial Intelligence, pp. 3364–3370. AAAI Press, 2017.

- Zhang & Xiao (2019a) Zhang, J. and Xiao, L. Multi-level composite stochastic optimization via nested variance reduction. arXiv preprint arXiv:1908.11468, 2019a.

- Zhang & Xiao (2019b) Zhang, J. and Xiao, L. A stochastic composite gradient method with incremental variance reduction. Advances in Neural Information Processing Systems, 28:9078––9088, 2019b.

- Zhang & Xiao (2020) Zhang, J. and Xiao, L. Stochastic variance-reduced prox-linear algorithms for nonconvex composite optimization. arXiv preprint arXiv:2004.04357, 2020.

- Zhao et al. (2010) Zhao, L., Mammadov, M., and Yearwood, J. From convex to nonconvex: a loss function analysis for binary classification. In IEEE International Conference on Data Mining Workshops (ICDMW), pp. 1281–1288. IEEE, 2010.

Supplementary Document

Stochastic Gauss-Newton Algorithms for Nonconvex Compositional Optimization

Appendix A The Proof of Technical Results in Section 2: Mathematical Tools

This section provides the full proof of technical results in Section 2. Let us first recall the bound (10). The proof of this bound can be found, e.g., in Nesterov (2007). However, for completeness, we prove it here.

The proof of (10).

Since is -Lipschitz continuous with a Lipschitz constant , we have for any . On the other hand, since is -Lipschitz continuous, we have for any . Hence, we have

which proves (10). ∎

A.1 The Proof of Lemma 2.1: Approximate Optimality Condition

Lemma. 2.1. Suppose that Assumption 1.1 holds. Let be computed by (2.2) and be defined by (13). Then, of (1) or (2) defined by (7) with is bounded by

| (2.1) |

Proof.

Appendix B The Proof of Technical Results in Section 3: Convergence of Inexact GN Framework

This appendix provides the full proof of technical results in Section 3 on convergence of the inexact Gauss-Newton framework, Algorithm 1.

B.1 The Proof of Lemma 3.1: Descent Property

Lemma. 3.1. Let Assumption 1.1 hold, be computed by (2.2), and be the prox-gradient mapping of . Then, for any , we have

| (38) |

For any , we also have

| (15) |

Proof.

The optimality condition (37) can be written as

By convexity of , using the above relations, we have

which implies (38).

Now, combining (10) and (38), we can show that

Substituting into this estimate, we obtain

| (39) |

Using the Cauchy-Schwarz inequality, we have

Next, applying Young’s inequality to the right hand side of this inequality, for any , we obtain

| (40) |

Finally, plugging (40) into (39), we have

for any , which exactly implies (15). ∎

B.2 The Proof of Theorem 3.1: Convergence Rate of Algorithm 1

Theorem. 3.1. Assume that Assumptions 1.1 and 1.2 are satisfied. Let be generated by Algorithm 1 to solve either (1) or (2). Then, the following statements hold:

Consequently, with , the total number of iterations to achieve is at most

where for the case and for the case .

Proof.

Using the second inequality of (15) with and , we have

| (41) |

(a) If (16) holds for some , then using (16) into (41), we have

where . Since , the last estimate leads to

By induction, , and , we can show that

| (42) |

which leads to (19).

(b) If (17) and (18) are used, then from (41) and (18), we have

where and . For , it follows from (41) and (17) that

Now, note that , the last two estimates respectively become

and for , it holds that

By induction and , this estimate leads to

Since , if we define , then the last inequality implies

which leads to (20). The last statement of this theorem is a direct consequence of either (19) or (20), and we omit the detailed derivation here. ∎

Appendix C High Probability Inequalities and Variance Bounds

Since our methods are stochastic, we recall some mathematical tools from high probability and concentration theory, as well as variance bounds that will be used for our analysis. First, we need the following lemmas to estimate sample complexity of our algorithms.

Lemma C.1 (Matrix Bernstein inequality (Tropp, 2012)(Theorem 1.6)).

Let be independent random matrices in . Assume that and a.s. for and given , where is the spectral norm. Define . Then, for any , we have

As a consequence, if for a given , then

Lemma C.2 (Lohr (2009)).

Lemma C.3 (Nguyen et al. (2017); Pham et al. (2020)).

Let and be the mini-batch SARAH estimators of and , respectively defined by (27), and be the -field generated by . Then, we have the following estimate

| (44) |

where if , and , otherwise, i.e., .

Similarly, we also have

| (45) |

where if , and , otherwise, i.e., .

Appendix D The Proof of Technical Results in Section 4

This appendix provides the full proof of technical results in Section 4 on our stochastic Gauss-Newton methods.

D.1 The Proof of Theorem 4.1: Convergence of The Stochastic Gauss-Newton Method for Solving (1)

Theorem. 4.1. Suppose that Assumptions 1.1 and 1.2 hold for (1). Let and defined by (21) be mini-batch stochastic estimators of and , respectively. Let be generated by Algorithm 1 called SGN to solve (1). For a given tolerance , assume that and in (21) are chosen as

| (22) |

Furthermore, let be chosen uniformly at random in as the output of Algorithm 1 after iterations. Then

| (23) |

where with . Moreover, the total number of function evaluations and the total number of Jacobian evaluations to achieve do not exceed

| (24) |

Proof.

Let be the -field generated by . By repeating a similar proof as of (19), but taking the full expectation overall the randomness with , we have

| (46) |

where with . Moreover, by the choice of , we have . Combining this relation and (46), we proves (23).

Next, by Lemma C.2, to guarantee the condition (16) in expectation, i.e.:

we have to choose and , which respectively lead to

By rounding to the nearest integer, we obtain (22). Using (19), we can see that since , to guarantee , we impose , which leads to . Hence, the total number of stochastic function evaluations can be bounded by

Similarly, the total number of stochastic Jacobian evaluations can be bounded by

These two last estimates prove (24). ∎

D.2 The Proof of Theorem 4.2: Convergence of The Stochastic Gauss-Newton Method for Solving (2)

Theorem. 4.2. Suppose that Assumptions 1.1 and 1.2 hold for (2). Let and defined by (21) be mini-batch stochastic estimators to approximate and , respectively. Let be generated by Algorithm 1 for solving (2). Assume that and in (21) are chosen such that and for , where

| (25) |

for , and and given in Condition 2, where is a given tolerance.

Then, we have the following conclusions:

- •

-

•

Moreover, the total number of stochastic function evaluations and the total number of stochastic Jacobian evaluations to guarantee do not exceed

(26)

Proof.

We first use Lemma C.1 to estimate the total number of samples for and . Let be the -field generated by . We define for . Conditioned on , due to the choice of , are independent vector-valued random variables and . Moreover, by Assumption 1.2, we have for all . This implies that a.s. and . Hence, the conditions of Lemma C.1 hold. In addition, we have

Since , by Lemma C.1, we have

Let us choose such that and , then . Hence, we have .

To guarantee the first condition of (17), we choose . Then, the condition on leads to . To guarantee the first condition of (18), we choose . Then, the condition on leads to . Rounding both and , we obtain

Since for all , we have for , which proves the first part of (25).

Next, we estimate a sample size for . Let us define . Then, similar to the above proof of for , we have . Under Assumption 1.2, the sequence satisfies all conditions of Lemma C.1. Hence, we obtain

Hence, we can choose . From the second condition of (17), if we choose , then we have . From the second condition of (18), if we choose , then we have . Rounding , we obtain

Since for all , combining these conditions, we obtain for , which proves the second part of (25).

For , we have . Otherwise, the algorithm has been terminated. Therefore, we can even bound and as

From (20), to guarantee , we impose , which leads to . Hence, the total number of stochastic function evaluations can be bounded by

Similarly, the total number of stochastic Jacobian evaluations can be bounded by

Taking the upper bounds, these two last estimates prove (26). ∎

D.3 The Proof of Theorem 4.3: Convergence and Complexity Analysis of Algorithm 2 for (1)

Theorem. 4.3. Suppose that Assumptions 1.1 and 1.2, and 4.1 are satisfied for (1). Let be generated by Algorithm 2 to solve (1). Let and be chosen by (28), and the mini-batches , , , and be set as in (29). Assume that the output of Algorithm 2 is chosen uniformly at random in . Then:

Proof.

We first analyze the inner loop. Using (15) with and , and then taking the expectation conditioned on , we have

for any , where we use and the Jensen inequality in the second line. Taking the full expectation both sides of the last inequality, and noting that , we obtain

| (47) |

where , and and are given.

Next, from Lemma C.3, using the Lipschitz continuity of in Assumption 1.2, we have

| (48) |

Similarly, using Lemma C.3, we also have

Taking the full expectation both sides of this inequality, and using Assumption 4.1, we obtain

| (49) |

Let us define a Lyapunov function as

| (50) |

for some and .

Combining (47), (48), and (49), and then using the definition of in (50), we have

| (51) |

If we assume that

| (52) |

then, from (51), we have

| (53) |

where .

Let us first fix . Next, we choose and . Clearly, and they both satisfy the condition (52). Then, we choose and for some and . In this case, we have due to (28) by appropriately choosing and . Consequently, (53) reduces to

Summing up this inequality from to , we obtain

Using the fact that and , we have

Summing up this inequality from to and multiplying the result by , we obtain

| (54) |

Since and , we obtain from (54) that

| (55) |

Note that and due to the choice of and at Step 4 of Algorithm 2. Hence, we can further bound (D.3) as

Since , to guarantee for a given tolerance , we need to set

Let us break this condition into

Hence, we can choose , , , and .

Now, let us choose for some constant . Then, we can estimate the total number of stochastic function evaluations as follows:

Similarly, the total number of stochastic Jacobian evaluations can be bounded as

Hence, taking the upper bounds, we have proven (31). ∎

Appendix E Solution Routines for Computing Gauss-Newton Search Directions

One main step of SGN methods is to compute the Gauss-Newton direction by solving the subproblem (2.2). This subproblem is also called a prox-linear operator, which can be rewritten as

| (56) |

where , , , is convex, , and is given. This is a basic convex problem, and we can apply different methods to solve it. Here, we describe two methods for solving (56).

E.1 Accelerated Dual Proximal-Gradient Method

For accelerated dual proximal-gradient method, we consider the case for simplicity. Using Fenchel’s conjugate of , we can write . Assume that strong duality holds for (56), then using this expression, we can write it as

Solving the inner problem , we obtain . Substituting it into the objective, we eventually obtain the dual problem as follows:

| (57) |

We can solve this problem by an accelerated proximal-gradient method (Beck & Teboulle, 2009; Nesterov, 2004), which is described as follows.

Note that in Algorithm 3, we use the proximal operator of . However, by Moreau’s identity, , we can again use the proximal operator of .

E.2 Primal-Dual First-Order Methods

We can apply any primal-dual algorithm from the literature (Bauschke & Combettes, 2017; Chambolle & Pock, 2011; Esser, 2010; Goldstein et al., 2013; Tran-Dinh et al., 2018; Tran-Dinh, 2019) to solve (56). Here, we describe the well-known Chambolle-Pock’s primal-dual method (Chambolle & Pock, 2011) to solve (56).

Let us define and . Since (56) is strongly convex with the strong convexity parameter , we can apply the strongly convex primal-dual variant as follows.

Choose and such that . For example, we can choose , or we choose first, and choose . Choose and and set . Then, at each iteration , we update

| (58) |

Alternatively to the Accelerated Dual Proximal-Gradient and the primal-dual methods, we can also apply the alternating direction method of multipliers (ADMM) to solve (56). However, this method requires to solve a linear system, that may not scale well when the dimension is large.

Appendix F Details of The Experiments in Section 5

In this supplementary document, we provide the details of our experiments in Section 5, including modeling, data generating routines, and experiment configurations. We also provide more experiments for both examples. All algorithms are implemented in Python 3.6 running on a Macbook Pro with 2.3 GHz Quad-Core, 8 GB RAM and on a Linux-based computing node, called Longleaf, where each node has 24 physical cores, 2.50 GHz processors, and 256 GB RAM.

F.1 Stochastic Nonlinear Equations

Our goal is to solve the following nonlinear equation in expectation as described in Subsection 5.1:

| (59) |

Here, is a stochastic vector function from . As discussed in the main text, (59) covers the first-order optimality condition of a stochastic optimization problem as a special case. More generally, it also covers the KKT condition of a stochastic optimization problem with equality constraints. However, these problems may not have stationary point, which leads to an inconsistency of (59). As a remedy, we can instead consider

| (60) |

for a given norm (e.g., -norm or -norm). Problem (59) also covers the expectation formulation of stochastic nonlinear equations such as stochastic ODEs or PDEs.

In our experiment from Subsection 5.1, we only consider one instance of (60) by choosing and () as

| (61) |

where is the -row of an input matrix , is a vector of labels, is a bias vector in binary classification, and . Note that the binary classification problem with nonconvex loss has been widely studied in the literature, including Zhao et al. (2010), where one aims at solving:

| (62) |

for a given loss function . If is nonnegative, then instead of solving (62), we can solve . If we have different losses for and we want to solve problems of the form (62) for different losses simultaneously, then we can formulate such a problem into (60) to have , where . Since we use different losses, under the formulation (60), we can view it as a binary classification task with an averaging loss.

| Algorithm | w8a | ijcnn1 | covtype | url_combined | ||||||||

| Inner Iterations | Inner Iterations | Inner Iterations | Inner Iterations | |||||||||

| SGN | 256 | 512 | 512 | 1,024 | 1,024 | 4,096 | 20,000 | 50,000 | ||||

| SGN2 | 64 | 128 | 2,000 | 128 | 256 | 1,000 | 256 | 512 | 2000 | 5,000 | 10,000 | 5,000 |

| a9a | rcv1_train.binary | real-sim | skin_nonskin | |||||||||

| Inner Iterations | Inner Iterations | Inner Iterations | Inner Iterations | |||||||||

| SGN | 512 | 1,024 | 512 | 1,024 | 1,024 | 4,096 | 512 | 1024 | ||||

| SGN2 | 64 | 128 | 2000 | 128 | 256 | 1,000 | 256 | 512 | 2,000 | 128 | 256 | 5,000 |

| Algorithm | w8a | ijcnn1 | covtype | url_combined | ||||||||

| Inner Iterations | Inner Iterations | Inner Iterations | Inner Iterations | |||||||||

| SGN | 256 | 512 | 512 | 1,024 | 512 | 1,024 | 20,000 | 50,000 | ||||

| SCGD | 256 | 512 | 512 | 1,024 | 512 | 1,024 | 20,000 | 50,000 | ||||

| SGN2 | 64 | 128 | 5,000 | 128 | 256 | 2,000 | 128 | 256 | 5,000 | 5,000 | 10,000 | 5,000 |

| N-SPIDER | 64 | 128 | 5,000 | 128 | 256 | 2,000 | 128 | 256 | 5,000 | 5,000 | 10,000 | 5,000 |

| a9a | rcv1_train.binary | real-sim | news20.binary | |||||||||

| Inner Iterations | Inner Iterations | Inner Iterations | Inner Iterations | |||||||||

| SGN | 128 | 256 | 128 | 512 | 256 | 512 | 128 | 512 | ||||

| SCGD | 1,024 | 2,048 | 128 | 512 | 256 | 512 | 128 | 512 | ||||

| SGN2 | 64 | 128 | 2,000 | 64 | 128 | 5,000 | 64 | 128 | 5,000 | 64 | 128 | 5,000 |

| N-SPIDER | 64 | 128 | 2,000 | 64 | 128 | 5,000 | 64 | 128 | 5,000 | 64 | 128 | 5,000 |

Datasets. We test three algorithms: GN, SGN, and SGN2 on four real datasets: w8a (), ijcnn1 (), covtype (), and url_combined () from LIBSVM.

Parameter configuration. We can easily check that defined by (61) satisfies Assumption 1.1 and Assumption 2. However, we do not accurately estimate the Lipschitz constant of since it depends on the dataset. We were instead experimenting with different choices of the parameter and , and eventually fix and for our tests. We also choose the mini-batch sizes for both and in SGN and SGN2 by sweeping over the set of to estimate the best ones. Table 1 presents the chosen parameters for the instance when .

In the case of smooth , i.e., using Huber loss, we add two competitors: N-SPIDER (Yang et al., 2019, Algorithm 3) and SCGD Wang et al. (2017a, Algorithm 1). The learning rates of N-SPIDER and SCGD are tuned from a set of different values: . Eventually we obtain and set for N-SPIDER, see (Yang et al., 2019, Algorithm 3). For SCGD, we use and , see Wang et al. (2017a, Algorithm 1). The mini-batch sizes of these algorithm are chosen using similar search as in the previous case. Table 2 reveals the parameter configuration of the algorithms when using the Huber loss.

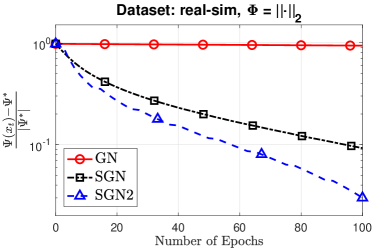

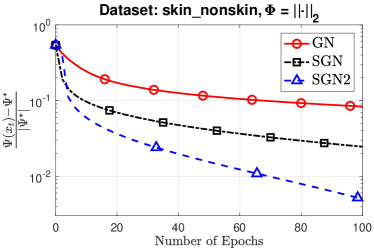

Additional Experiments. When , we also run these algorithms on other classification datasets from LIBSVM: a9a (), rcv1_train.binary (), real-sim (), and skin_nonskin (). We set and for three datasets. Other parameters are obtained via grid search and the results are shown in Table 1. The performance of three algorithms on these datasets are presented in Figure 6.

SGN2 appears to be the best among the 3 algorithms while SGN is much better than the baseline GN. SGN appears to have advantage in the early stage but SGN2 makes better progress later on.

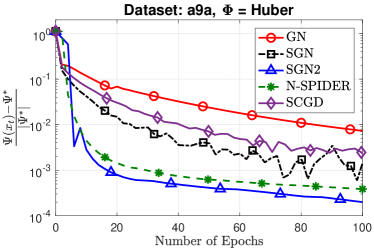

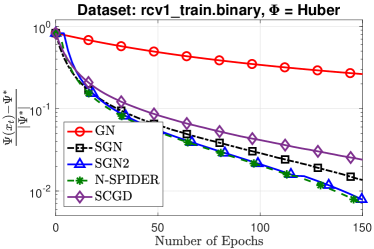

In addition, we also run 5 algorithms on these datasets in the smooth case when using the Huber loss. We still tune the parameters for these algorithms and obtain the learning rate of for both N-SPIDER and SCGD. We again use for N-SPIDER. More details about other parameters selection are presented in Table 2 and the performance of these algorithms are shown in Figure 7.

From Figure 7, SGN2 performs better than other algorithms in most cases while N-SPIDER is better than SGN and somewhat comparable with SGN2 in the rcv1_train.binary and news20.binary datasets. SGN and SCGD appear to have similar behavior, but SGN is slightly better than SCGD in these datasets.

F.2 Optimization Involving Expectation Constraints

We consider an optimization problem involving expectation constraints as described in (34). As mentioned, this problem has various applications in different fields, including optimization with conditional value at risk (CVaR) constraints and metric learning, see, e.g., Lan & Zhou (2016) for detailed discussion.

Instead of solving the constrained setting (34), we consider its exact penalty formulation (35):

| (35) |

where with is a penalty function, and is a given penalty parameter. It is well-known that under mild conditions and sufficiently large (e.g., , the dual norm of the optimal Lagrange multiplier ), if is a stationary point of (35) and it is feasible to (34), then it is also a stationary point of (34).

As a concrete instance of (34), we solve the following asset allocation problem studied in Rockafellar & Uryasev (2000); Lan & Zhou (2016):

| (63) |

Here, denotes the standard simplex in , and is a given range of . The exact penalty formulation of (63) is given by (36):

| (36) |

where with given . However, since is nonsmooth, we smooth it by for sufficiently small value of . Hence, (36) can be approximated by

| (64) |

If we introduce , for , and , where is the indicator of , then we can reformulate (64) into (3). It is obvious to check that is Lipschitz continuous with and its gradient is also Lipschitz continuous with . Hence, Assumptions 1.1 and 4.1 hold.

Datasets. We consider both synthetic and US stock datasets. For the synthetic datasets, we follow the procedures from Lan et al. (2012) to generate the data with and . We obtain real datasets of US stock prices for , , and types of stocks as described, e.g., Sun & Tran-Dinh (2019). Then, we apply a bootstrap strategy to resample in order to obtain three corresponding new datasets of sizes .

| Algorithm | Synthetic: p = 300 | Synthetic: p = 500 | Synthetic: p = 700 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Inner Iterations | Inner Iterations | Inner Iterations | |||||||

| SGN | 1,024 | 2,048 | 1,024 | 2,048 | 1,024 | 2,048 | |||

| SGN2 | 128 | 256 | 5,000 | 128 | 256 | 2,000 | 256 | 512 | 2,000 |

| Algorithm | US Stock 1: p = 889 | US Stock 1: p = 865 | US Stock 1: p = 500 | ||||||

| Inner Iterations | Inner Iterations | Inner Iterations | |||||||

| SGN | 512 | 1,024 | 512 | 1,024 | 512 | 1,024 | |||

| SGN2 | 128 | 256 | 5,000 | 128 | 256 | 5,000 | 128 | 256 | 5,000 |

Parameter selection. We fix the smoothness parameter and choose the range to be . The parameter as discussed in Lan & Zhou (2016). Note that we do not use the theoretical values for as in our theory since that value is obtained in the worst-case. We were instead experimenting different values for the penalty parameter and , and eventually get and as default values for this example.

Experiment setup. We implement our algorithms: SGN and SGN2, and also a baseline variant, the deterministic GN scheme (i.e., we exactly evaluate and its Jacobian using the full batches) as in the first example. Similar to the first example, we sweep over the same set of possible mini-batch sizes, and the chosen parameters are reported in Table 3.

Additional experiments. We run three algorithms: GN, SGN, and SGN2 with synthetic datasets, where the first one was reported in Figure 2 of the main text. We also use two other US Stock datasets and the performance of three algorithms on these synthetic and real datasets are revealed in Figure 8.

Clearly, SGN2 is the best, while SGN still outperforms GN in these two datasets. We believe that this experiment confirms our theoretical results presented in the main text.

Appendix G Convergence of Algorithm 2 for the finite-sum case (2) without Assumption 4.1

Although Theorem 1 significantly improves stochastic oracle complexity of Algorithm 2 compared to Theorem 4.1, it requires additional assumption, Assumption 4.1. Assumption 4.1 is usually used in compositional models such as neural network and parameter estimations. However, we still attempt to establish a convergence and complexity result for Algorithm 2 to solve (2) without Assumption 4.1 in the following theorem.

Theorem G.1.

Suppose that Assumptions 1.1 and 1.2 are satisfied for (2). Let be generated by Algorithm 2 to solve (2). Let the mini-batches , , , and be set as follows:

| (65) |

Then, with probability at least , the following statements hold:

The following bound holds

The total number of iterations to achieve

is at most . Moreover, the total stochastic oracle calls and to approximate and its Jacobian , respectively do not exceed

Remark G.1.

Proof.

We first analyze the inner loop of Algorithm 2. For simplicity of notation, we drop the superscript (s) in the following derivations until it is recalled. We first verify the conditions (18) if we use the SARAH estimators (27) for and . Let be the -field generated by . We define . Then, clearly, conditioned on , we have is mutually independent and . Moreover, by Assumption 1.2, we have

We consider . We have

For any , we can apply Lemma C.1 to obtain the following bound

Hence, if we choose and , we obtain for all . The condition in leads to

By the update (27), we have . Hence, by the triangle inequality, we get

On the other hand, by the update (21) of as , where and , with a similar proof as of Theorem 4.2, we can show that if we choose then . Then with probability at least , we have

This inequality implies

| (66) |

Our next step is to estimate the . We define and for . In this case, is mutually independent and . We also have

Here, we use the facts that for and from Assumption 1.2 into the last inequality. Moreover, we have

where .

Now, we consider . For any , we can apply Lemma C.1 to obtain the following bound

Hence, if we choose and , then we obtain for all . The condition in leads to .

By the update of from (27), we have . Hence, by induction, it implies that , which leads to

| (67) |

Now, we analyze the inner loop of to . Using (15) with and , we have

| (68) |

where and is given. Combining (68), (66), and (67), we have

Summing up this inequality from to , we obtain

Since and , the last inequality becomes

| (69) |

where is defined as

Let . Then, we can rewrite as

If we impose the following condition

| (70) |

then .

Under this condition, (69) reduces to

Summing up this inequality from to and rearranging the result, we obtain

Using and , we obtain from the last inequality that

Clearly, if we choose , , , and for some positive constant , , , and , then we obtain from the last estimate that

| (71) |

where we use the fact that . Now, assume that the condition (70) is tight. Using the choice of accuracies, we obtain

If we choose , then this condition becomes and .

Now, with the choice of , , , and as above, we can set the mini-batch sizes as follows:

| (72) |

Since , if we choose , then . The total complexity is

This proves our theorem. ∎