A Newton Frank-Wolfe Method for Constrained Self-Concordant Minimization

Abstract

We demonstrate how to scalably solve a class of constrained self-concordant minimization problems using linear minimization oracles (LMO) over the constraint set. We prove that the number of LMO calls of our method is nearly the same as that of the Frank-Wolfe method in -smooth case. Specifically, our Newton Frank-Wolfe method uses LMO’s, where is the desired accuracy and . In addition, we demonstrate how our algorithm can exploit the improved variants of the LMO-based schemes, including away-steps, to attain linear convergence rates. We also provide numerical evidence with portfolio design with the competitive ratio, D-optimal experimental design, and logistic regression with the elastic net where Newton Frank-Wolfe outperforms the state-of-the-art.

1 Introduction

In this paper, we consider the following constrained convex optimization problem:

| (1) |

Among the first-order methods, the Frank-Wolfe (FW), aka conditional gradient method [9] has gained tremendous popularity lately due to its scalability and its theoretical guarantees when the objective is -smooth.

The scalability of FW is mainly due to its main computational primitive, called the linear minimization oracle (LMO):

| (2) |

There are many applications, such as latent group lasso and simplex optimization problems where computing the LMO is significantly cheaper as compared to projecting onto the set .

However, there are many machine learning problems where the objective function involves logarithmic, ridge regularized exponential, and log-determinant functions. These problems so far cannot exploit the rate as well as the scalability of the FW algorithm or its key variants.

Our work precisely bridges this gap by focusing on objective functions where is standard self-concordant (see Definition 2.1) and is a nonempty, compact and convex set in . We emphasize that the class of self-concordant functions intersects with the class of Lipschitz continuous gradient functions, but they are different. In particular, we assume

Assumption 1.1.

The solution set of (1) is nonempty. The function in (1) is standard self-concordant and its Hessian is nondegenerate111This condition can be relaxed to the case where is self-concordant with nondegenerate Hessian, but may have degenerate Hessian. for any . is compact and its LMO defined by (2) can be computed efficiently and accurately.

Under Assumption 1.1, problem (1) covers various applications in statistical learning and machine learning such as D-optimal design [14, 21], minimum-volume enclosing ellipsoid [6], quantum tomography [12], logistic regression with elastic-net regularization [31], portfolio optimization [27], and optimal transport [26].

Related work: Motivated by the fact that, for many convex sets, including simplex, polytopes, and spectrahedron, computing a linear minimization oracle is much more efficient than evaluating their projection [15, 16], various linear oracle-based algorithms have been proposed, see, e.g., [9, 15, 16, 19, 20]. Recently, such approaches are extended to the primal-dual setting in [33, 34].

The most classical one is the Frank-Wolfe algorithm proposed in [9] for minimizing a quadratic function over a polytope. It has been shown that the convergence rate of this method is and is tight under the -smoothness assumption, where is the iteration counter.

Many recent papers have attempted to improve the convergence rate of the Frank-Wolfe algorithm and its variants by imposing further assumptions or exploiting the underlying problem structures. For instance, [3] showed a linear convergence of the Frank-Wolfe method under the assumption that is a quadratic function and the optimal solution is in the interior of . [13] firstly proposed a variant of the Frank-Wolfe method with away-step and proved its linear rate to the optimal value if is strongly convex, is a polytope, and the optimal solution is in the interior of .

Recently, [10] and [18] showed that the result of [13] still holds even is on the boundary of . This can be viewed as the first general global linear convergence result of Frank-Wolfe algorithms. [11] showed that the convergence rate of the Frank-Wolfe algorithm can be accelerated up to if is strongly convex and is a “strongly convex set” (see their definition).

All the results mentioned above rely on the -smooth assumption of the objective function . Moreover, the primal-dual methods [33, 34] suffer in convergence rate since they can only handle the self-concordant function by splitting the objective and then relying on the proximal operator of the self-concordant function.

For the non--smooth case, the literature is minimal. Notably, [24] is the first work, to our knowledge, that proved that the Frank-Wolfe method could converge with rate for the Poisson phase retrieval problem where is a logarithmic objective. This result relies on a specific simplex structure of the feasible set and proved that the objective function is eventually -smooth on .

In addition, [6] showed a linear convergence of the Frank-Wolfe method with away-step for the minimum-volume enclosing ellipsoid problem with a log-determinant objective. The algorithms and the analyses in the respective papers exploit the cost function and the structure, but it is not clear how they can handle more general self-concordant objectives. Note that since both objective functions in the aforementioned works are self-concordant, they are covered by our framework in this paper.

Our approach and contribution: Our first goal is to tackle an important class of problems (1), where existing LMO-based methods do not have convergence guarantees. Our results make sense when computing the LMO is cheaper than computing projections. Otherwise, the first-order methods of [30] can also be applied.

For this purpose, we apply a projected Newton method to solve (1) and use the Frank-Wolfe method in the subproblems to approximate the projected Newton direction. This approach leads to a double-loop algorithm, where the outer loop performs an inexact projected Newton scheme, and the inner loop carries out an adaptive Frank-Wolfe method.

Notice that our algorithm enjoys several additional computational advantages. When the feasible set is a polytope, our subproblem becomes minimizing a quadratic function over a polytope. By the result of [18], we can use the Frank-Wolfe algorithm with away-steps to attain linear convergence. Since in the subproblem our objective function is quadratic, the optimal step size at each iteration has a closed-form expression, leading to structure exploiting variants (see Algorithm 2). Finally, our algorithm can enhance Frank-Wolfe-type approaches by using the inexact projected Newton direction.

To this end, our contribution can be summarized as follows:

- (a)

-

(b)

We prove that the gradient and Hessian complexity of our method is , while the LMO complexity is where for some constants and . When approaches zero, the complexity bound also approaches as in the Frank-Wolfe methods for the -smooth case.

To our knowledge, this work is the first in studying LMO-based methods for solving (1) with non-Lipschitz continuous gradient functions on a general convex set . It also covers the models in [6] and [24] as special cases, via a completely different approach.

Paper outline: The rest of this paper is organized as follows. Section 2 recalls some basic notation and preliminaries of self-concordant functions. Section 3 presents the main algorithm. Section 4 proves the local linear convergence of our algorithm and gives a rigorous analysis of the total oracle complexity. Three numerical experiments are given in Section 5. Finally, we give the conclusion in Section 6. All the technical proofs are deferred to the supplementary document (Supp. Doc).

2 Theoretical Background

Basic notation: We work with Euclidean spaces, and , equipped with standard inner product and Euclidean norm . For a given proper, closed, and convex function , denotes the domain of , denotes the subdifferential of , and is its Fenchel conjugate. For a symmetric matrix , denotes the largest eigenvalue of . We use to denote the set , and to denote the vector whose elements are s. For a vector , is a diagonal matrix formed by . We also define two nonnegative and monotonically increasing functions for and for .

2.1 Self-concordant Functions

We recall the definition of self-concordant functions introduced in [23] here.

Definition 2.1.

A three-time continuously differentiable univariate function is said to be self-concordant with a parameter if for all . A three-time continuously differentiable function is said to be self-concordant with a parameter if is self-concordant with the same parameter for any and . If , then we say that is standard self-concordant.

Note that any self-concordant function can be rescaled to the standard form as . When does not contain straight line, is positive definite, and therefore we can define a local norm associated with together with its dual norm as follows:

These norms are weighted and satisfy the Cauchy-Schwarz inequality for .

The class of self-concordant functions is sufficiently broad to cover many applications. It is closed under nonnegative combination and linear transformation. Any linear and convex quadratic functions are self-concordant. The function and are self-concordant. For matrices, is also self-concordant, which is widely used in covariance estimation-type problems. In statistical learning, the regularized logistic regression model with and the regularized Poisson regression model with are both self-concordant. Note that all the functions introduced above are not -smooth except for . In addition, any strongly convex function with Lipschitz Hessian continuity is also self-concordant. See [29, 25] for more examples and theoretical results.

2.2 Approximate Solutions

Since the Hessian is nondegenerate, (1) has only one optimal solution . Moreover, . Our goal is to design an algorithm to approximate as follows:

Definition 2.2.

Given a tolerance , we say that is an -solution of (1) if

| (3) |

Different from existing Frank-Wolfe methods where an approximate solution is defined by , we define it via a local norm. However, we show in Theorem 4.4 that these two concepts are related to each other.

3 The Proposed Algorithm

Since in (1) is standard self-concordant, we first approximate it by a quadratic surrogate and apply a projected Newton method to solve (1).

More precisely, given , the projected Newton method computes a search direction at by solving the following constrained convex quadratic program:

| (4) |

Since is positive definite by Assumption 1.1, is the unique solution of (4). However, this problem often does not have a closed-form solution, and we need to approximate it up to a given accuracy. Since we aim at exploiting LMO of , we apply a Frank-Wolfe scheme to solve (4). The optimality condition of (4) becomes

| (5) |

where . Using this optimality condition, we can define an inexact solution of (4) as follows:

Definition 3.1.

Given a tolerance , we say that is an -solution of (4) if

| (6) |

The following lemma, whose proof is in Supp. Doc. 1.1, shows that the distance between and can be bounded by . Therefore, this justifies the well-definedness of Definition 3.1.

Lemma 3.1.

Now, we combine our inexact projected Newton scheme and the well-known Frank-Wolfe algorithm to develop a new algorithm as presented in Algorithm 1.

Let us make a few remarks on Algorithm 1.

Discussion on structure: Algorithm 1 integrates both damped-step and full-step inexact projected Newton schemes. First, it performs the damped-step scheme to generate starting from an initial point that may be far from the optimal solution . Then, once is satisfied, it switches to the full-step scheme. For the damped-step stage, we will show later that Algorithm 1 only performs a finite number of iterations.

Discussion on : The quantity upper bounds . In the damped-step stage, we keep unchanged while in the full-step one, we decrease by a factor of . Consequently, will converge linearly to in the full-step stage (see Theorem 4.2).

Discussion on : The quantity is used to measure (see (4) for the definition of ). In Algorithm 1, is calculated as

| (7) |

and can be viewed as an approximate solution of (4) at . Therefore, measures the accuracy for solving the subproblem. In the damped-step stage, we keep as a constant. In the full-step one, is decreased by a factor of at each iteration to guarantee that we get a more accurate projected Newton direction when the algorithm approaches the optimal solution .

Discussion on : When , we use a damped-step scheme with the step-size . This step-size is derived from Lemma A.1 in Supp. Doc., and is in . Once is satisfied, we move to the full-step stage and no longer use the damped-step one. In addition, from Lemma A.2 in Supp. Doc., we can see that if , then we have , which means that we already find a good initial point for the full-step stage.

Discussion on the FW subroutine: The subroutine is a customized Frank-Wolfe method to solve the following convex constrained quadratic program:

The step size in FW is computed via the exact linesearch condition (see [19] for further details):

Discussion on : In practice, we do not need to evaluate the full Hessian . We only need to evaluate the matrix-vector operator for a given direction . Similarly, the computation of does not incur significant cost. Indeed, since we have already computed in the FW, computing requires only one additional vector inner product .

4 Convergence and Complexity Analysis

Our analysis closely follows the outline below:

-

•

Given , we show that we only need a finite number of damped-steps to reach such that .

-

•

Once is satisfied, we prove a linear convergence of the full-step projected Newton scheme.

-

•

We finally estimate the overall linear oracle (LMO) complexity of Algorithm 1.

4.1 Finite Complexity of Damped-Step Stage

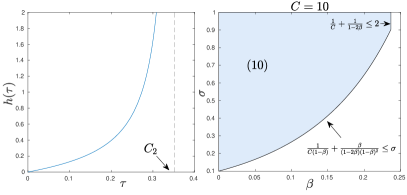

Before we present the main theorem of this section, let us first define a univariate function as

| (8) |

The shape of is shown in Figure 1.

From Figure 1, is nonnegative and monotonically increasing on for the constant such that .

The following theorem, whose proof is in Supp. Doc. 1.2, states that Algorithm 1 only needs a finite number of LMO calls to achieve such that . Although is independent of tolerance , it depends on the pre-defined constants in the algorithm and the data structure of .

Theorem 4.1.

Let . If we choose the parameters as in Algorithm 1, then after at most

| (9) |

outer iterations of the damped-step scheme, we can guarantee that for some , which implies that . Moreover, the total number of LMO calls is at most

where . The number of gradient and Hessian evaluations is also .

4.2 Linear Convergence of Full-Step Stage

Since Theorem 4.1 shows that we only need a finite number of damped-steps to obtain such that . Therefore, without loss of generality, we always assume that in the rest of this paper. Using this assumption, we analyze convergence rate of to the unique optimal solution of (1). In this case, Algorithm 1 always choose full-steps, i.e., .

The following theorem states a linear convergence of and . The convergence of will be used in Theorem 4.3 to bound which is key to our LMO complexity analysis. The proof can be found in Supp. Doc. 1.3.

Theorem 4.2.

Suppose and the triple satisfies the following conditions:

| (10) |

Let and be updated by the full-step scheme in Algorithm 1. Then, for , we have

4.3 Overall LMO Complexity Analysis

This subsection focuses on the analysis of LMO complexity of Algorithm 1. We first show that Algorithm 1 needs LMO calls to reach an -solution defined by (3) where . Consequently, we can show that it needs -LMO calls to find an -solution such that . See Supp. Doc. 1.4 for details.

Theorem 4.3.

From Theorem 4.3, we can observe that a small value of gives a better oracle complexity bound, but increases the number of oracle calls in the damped-step stage. Hence, we trade-off between the damped-step stage and the full-step stage. In practice, we do not recommend to choose an extremely small but some value in the range of .

Finally, the following theorem states the LMO complexity of Algorithm 1 on the objective residuals.

Theorem 4.4.

4.4 Complexity Trade-off Between Two Stages

Given a sufficiently small target accuracy , our goal is to find such that the LMO complexity in Theorem 4.3 dominates in Theorem 4.1. Let us choose . Then, the number of iterations of the damped-step stage in Theorem 4.1 is , where is a fixed constant. Moreover, for sufficiently small , we have . Hence, by Theorem 4.1, the total LMO calls of the damped-step stage can be bounded by

We conclude that the LMO complexity in the full-step stage dominates the one in the damped-step stage.

5 Numerical Experiments

We provide three numerical examples to illustrate the performance of Algorithm 1. We emphasize that the objective function of these examples does not have Lipschitz continuous gradient. Hence, existing Frank-Wolfe and projected gradient-based methods may not have theoretical guarantees. In the following experiments, we implement Algorithms 1 in Matlab running on a Linux desktop with 3.6GHz Intel Core i7-7700 and 16Gb memory. Our code is available online at https://github.com/unc-optimization/FWPN.

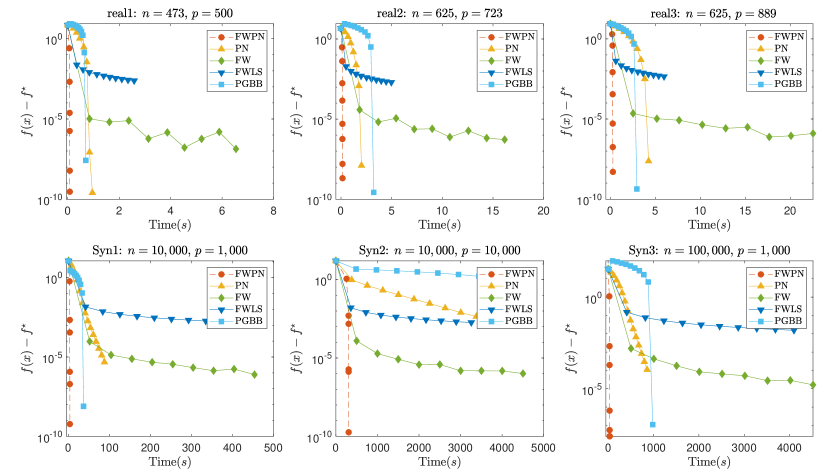

5.1 Portfolio Optimization

Consider the following portfolio optimization model widely studied in the literature, see e.g., [27]:

| (11) |

where for . Let . In the portfolio optimization model, represents the return of stock in scenario and is the utility function. Our goal is to allocate assets to different stock companies to maximize the expected return.

We implement Algorithm 1, abbreviated by FWPN, to solve (11). We also implement the standard projected Newton method which uses accelerated projected gradient method to compute the search direction, the Frank-Wolfe algorithm [9] and its linesearch variant [16], and a projected gradient method using Barzilai-Borwein’s step-size. We name these algorithms by PN, FW, FW-LS, and PG-BB, respectively.

We test these algorithms both on synthetic and real data. For the real data, we download three US stock datasets from http://www.excelclout.com/historical-stock-prices-in-excel/. We name these datasets by real1, real2, and real3. We generate synthetic datasets as follows. We generate a matrix as which allows each stock to vary about 10% among scenarios. We test with three examples, where, , and , respectively. We call these three datasets Syn1, Syn2, and Syn3, respectively. The results and the performance of these five algorithms are shown in Figure 2.

From Figure 2, one can observe that our algorithm, FWPN, clearly outperforms the other competitors on both real and synthetic datasets. In our algorithm, we use a Frank-Wolfe method with away-step to solve the simplex constrained quadratic subproblem which has a linear convergence rate as proved in [18]. Both PGBB and PG work relatively well compared to other candidates. As expected, the standard FW and its linesearch variant cannot reach a highly accurate solution.

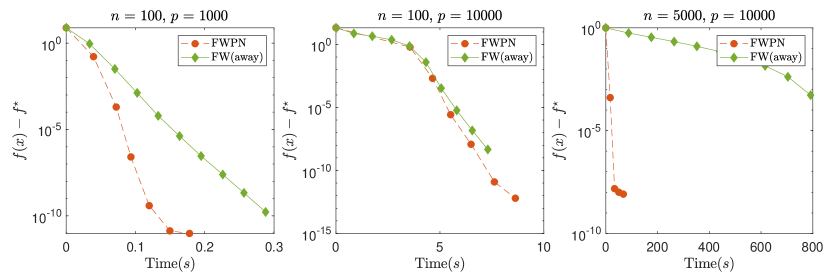

5.2 -Optimal Experimental Design

The second example is the following convex optimization model in -optimal experimental design:

| (12) |

where , , and for . It is well-known that the dual problem of (12) is the minimum-volume enclosing ellipsoid (MVEE) problem:

| (13) |

The objective of this problem is to find the minimum ellipsoid that covers the points . The datasets are generated using independent multinomial Gaussian distribution as in [6]. For this problem, one state-of-the-art solver is the Frank-Wolfe algorithm with away-step [18]. Its attraction is from the observation that the linesearch problem for determining optimal step-size :

has a closed-form solution (see [17] for more details). Therefore, we do not have to carry out a linesearch at each iteration of the Frank-Wolfe algorithm.

Recently, [6] showed that the Frank-Wolfe away algorithm has a linear convergence rate for this specific problem. Figure 3 reveals the performance of our algorithm (FWPN) and Frank-Wolfe algorithm with away-step on three datasets, where the dimension varies from to . Note that existing literature only tested for problems with . As far as we are aware of, this is the first attempt to solve problem (12) with up to .

Figure 3 shows that when the size of the problem is small, our algorithm is slightly better than the Frank-Wolfe method with away-step. However, when the size of the problem becomes large, our algorithm highly outperforms the Frank-Wolfe method in terms of computational time. This happens due to a small number of projected Newton steps while each inner iteration requires significantly cheap computational time.

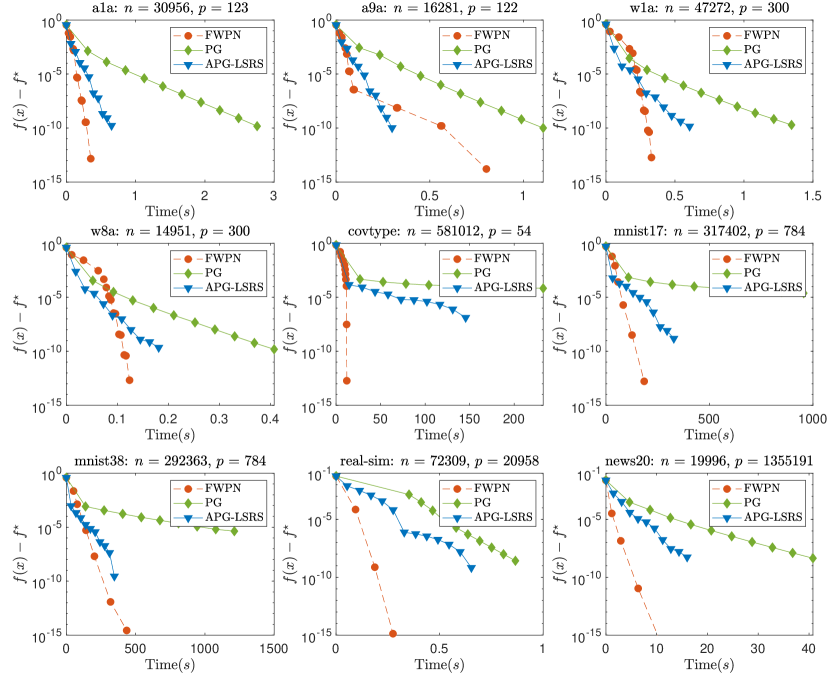

5.3 Logistic Regression with Elastic-net

Finally, let us consider the following logistic regression with elastic-net regularizer:

| (14) |

where , , and for .

It is well-known that (14) is equivalent to the following problem with a suitable penalty parameter :

| (15) |

It is has been shown in [29] that is self-concordant. Therefore, (15) fits into our template (1) with in this case.

We compare Algorithm 1 (FWPN) with a standard proximal-gradient method [2] and an accelerated proximal-gradient method with linesearch and restart [4, 28]. These methods are abbreviated by PG and APG-LSRS, respectively. We use binary classification datasets: a1a, a9a, w1a, w8a, covtype, news20, real-sim from [5] and generate the datasets mnist17 and mnist38 from the mnist dataset where digits are chosen from and , respectively. We set as in [7], and is set to be , which guarantees that the sparsity of the solution is maintained between and .

Since we need to evaluate the projection on a -norm ball at each iteration of PG and APG-LSRS, we use the algorithm provided by [8] which only need time. For our algorithm, since the -norm ball is still a polytope, we can linearly solve the subproblem by using the Frank-Wolfe algorithm with away-step from [18]. The performance and results of three algorithms on the above datasets are presented in Figure 4.

From Figure 4, one can observe that our algorithm outperforms PG and APG-LSRS both on small and large datasets. This happens thanks to the low computational cost of the linear oracle and the linear convergence of the FW method with away-step. It is interesting that although our algorithm is a hybrid method between second-order and first-order methods, we can still solve high-dimensional problems (e.g., when in news20 dataset) as often seen in first-order methods. We gain this efficiency due to the use of Hessian-vector products instead of full Hessian evaluations.

6 Conclusion

In this paper, we have combined the well-known Frank-Wolfe (first-order) method and an inexact projected Newton (second-order) method to form a novel hybrid algorithm for solving a class of constrained convex problems under self-concordant structures. Our approach is different from existing methods that heavily rely on the Lipschitz continuous gradient assumption. Under this new setting, we give the first rigorous convergence and complexity analysis. Surprisingly, the LO complexity of our algorithm is still comparable with the Frank-Wolfe algorithms for a different class of problems. In addition, our algorithm enjoys several computation advantages on some specific problems, which are also supported by the three numerical examples in Section 5. Moreover, the last example has shown that our algorithm still outperforms first-order methods on large-scale instances. Our finding suggests that sometimes it is worth carefully combine first-order and second-order methods for solving large-scale problems in non-standard settings.

Acknowledgments:

Q. Tran-Dinh was partly supported by the National Science Foundation (NSF), grant No. 1619884 and the Office of Naval Research (ONR), grant No. N00014-20-1-2088. V. Cevher was partly supported by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement n 725594 - time-data) and by 2019 Google Faculty Research Award.

Appendix A Appendix: The proof of technical results

Let us recall the following key properties of standard self-concordant functions. Let be standard self-concordant and such that and . Then

| (16) |

These inequalities can be found in [22][Theorem 4.1.6].

1.1 The Proof of Lemma 3.1

1.2 The Proof of Theorem 4.1

We would need two Lemmas to prove Theorem 4.1. The following lemma describles the decreasing of objective value when apply damped-step update.

Lemma A.1.

Let be the local distance between to , and . If we choose such that and update , then we have

| (17) |

Assume . If and the step size is then we have . Moreover, we have

| (18) |

where and are two nonnegative and convex functions.

Proof.

The following lemma shows that the residual can be bounded by the projected Newton decrement .

Lemma A.2.

Let , , , and be defined by (8). If , then we have

| (22) |

Proof.

Firstly, we can write down the optimality condition of (4) and (1), respectively as follows:

Substituting for into the first inequality and for into the second inequality, respectively we get

Adding up both inequalities yields

which is equivalent to

Since is self-concordant, by [22][Theorem 4.1.7], we have

By the Cauchy-Schwarz inequality, this estimate leads to

| (23) |

Now, we can bound the right-hand side of the above inequality as

| (24) |

where the last inequality is from [32][Theorem 1]. From (23) and (24), we have

which can be reformulated as

| (25) |

Next, since we want to use to bound , we can derive

| (26) |

Notice that is monotonically increasing and , we finally get

which proves (22). ∎

Now we can prove Theorem 4.1. We first restate the Theorem.

Theorem A.1.

Let . If we choose the parameters as in Algorithm 1, then after at most

| (27) |

outer iterations of the damped-step scheme, we can guarantee that for some , which implies that . Moreover, the total number of LO calls is at most

where .

Proof.

Notice that in Algorithm 1, we always choose in the damped-step stage. Clearly, if , then , where . Therefore, we have

Using Lemma A.1 and the monotonicity of we also have

Consequently, we need at most outer iterations to get as stated in (27).

From Lemma A.4, we can show that the number of LO calls needed at the -th outer iteration is . Since is self-concordant, we have

which implies that . Hence, the total number of LO calls can be computed by

Finally, if , then we have . ∎

1.3 The Proof of Theorem 4.2

The following lemma shows that and can both be bounded by when is sufficiently small.

Lemma A.3.

Suppose that , where is chosen by Algorithm 1. Then, we have

| (28) |

In addition, we can also bound as follows:

| (29) |

Proof.

Now, we bound as follows. Firstly, the optimality conditions of (4) and (1) can be written as

This can be rewritten equivalently to

| (31) |

Similar to the proof of [1][Theorem 3.14], we can show that (31) is equivalent to

| (32) |

Using the nonexpansiveness of the projection operator we can derive

| (33) |

where the second last inequality is from [32][Theorem 1]. Plugging (33) into (30), we get (28).

Now we can prove Theorem 4.2. We first restate the Theorem.

Theorem A.2.

Suppose and the triple satisfies the following condition:

| (34) |

In addition, we set and update by full-step in Algorithm 1. Then, for , we have

| (35) |

1.4 The proof of Theorem 4.3

Firstly, the following lemma establishes the sublinear convergence rate of the Frank-Wolfe gap in each outer iteration.

Lemma A.4.

Proof.

Now we can prove Theorem 4.3. We first restate the Theorem.

Theorem A.3.

Proof.

By self-concordance of , using [22][Theorem 4.1.6], it holds that

By induction, we have

Therefore, we can bound the maximum eigenvalue of as

| (39) |

Let us denote by . Then, fromLemma A.4, we can see that the number of LO calls at the -th outer iteration is at most

| (40) |

where the last equality holds because we set in Theorem 4.2.

To obtain an -solution defined by (3), we need to impose (recall that by Theorem 4.2), which is equivalent to . Since , the outer iteration number is at most . This number is also the total number of gradient and Hessian evaluations.

Finally, using (40), the total number of LO calls in the entire algorithm can be estimated as

where the last equality holds since . ∎

1.5 The Proof of Theorem 4.4

The following lemma states that we can bound by and . Therefore, from the convergence rate of and in Theorem 4.2, we can obtain a convergence rate of .

Lemma A.5.

Let and . Suppose that . If , then we have

| (41) |

where .

Proof.

Firstly, from [22][Theorem 4.1.8], we have

provided that . Next, using , we can further derive

| (42) |

Now, we bound as follows. Notice that this term can be decomposed as

Since is an -solution of (4) at , we have

| (43) |

Using the Cauchy-Schwarz inequality and the triangle inequality, can also be bounded as

| (44) |

where, the second inequality is due to [32][Theorem 1]. Finally, we can bound as

which proves (41). ∎

Now we can prove Theorem 4.4. We first restate the Theorem.

Theorem A.4.

Proof.

It is easy to check that for . Therefore, there exists such that for . Since , , and in Theorem 4.2, for , we have

| (46) |

Let be a constant. To guarantee , we impose i.e. . Therefore, the outer iteration number is at most . Using (40), the total number of LO calls will be

where the last equality follows from the fact that . ∎

References

- [1] H. H. Bauschke and P. Combettes. Convex analysis and monotone operators theory in Hilbert spaces. Springer-Verlag, 2nd edition, 2017.

- [2] A. Beck and M. Teboulle. A fast iterative shrinkage-thresholding agorithm for linear inverse problems. SIAM J. Imaging Sci., 2(1):183–202, 2009.

- [3] Amir Beck and Marc Teboulle. A conditional gradient method with linear rate of convergence for solving convex linear systems. Mathematical Methods of Operations Research, 59(2):235–247, Jun 2004.

- [4] S. Becker, E. J. Candès, and M. Grant. Templates for convex cone problems with applications to sparse signal recovery. Math. Program. Compt., 3(3):165–218, 2011.

- [5] C.-C. Chang and C.-J. Lin. LIBSVM: A library for Support Vector Machines. ACM Transactions on Intelligent Systems and Technology, 2:27:1–27:27, 2011.

- [6] S. A. Damla, P. Sun, and M. J. Todd. Linear convergence of a modified Frank–Wolfe algorithm for computing minimum-volume enclosing ellipsoids. Optimisation Methods and Software, 23(1):5–19, 2008.

- [7] A. Defazio, F. Bach, and S. Lacoste-Julien. SAGA: A fast incremental gradient method with support for non-strongly convex composite objectives. In Advances in Neural Information Processing Systems (NIPS), pages 1646–1654, 2014.

- [8] John Duchi, Shai Shalev-Shwartz, Yoram Singer, and Tushar Chandra. Efficient projections onto the l1-ball for learning in high dimensions. In Proceedings of the 25th International Conference on Machine Learning, ICML ’08, pages 272–279, New York, NY, USA, 2008. ACM.

- [9] M. Frank and P. Wolfe. An algorithm for quadratic programming. Naval Research Logistics Quarterly, 3:95–110, 1956.

- [10] D. Garber and E. Hazan. A linearly convergent conditional gradient algorithm with applications to online and stochastic optimization, 2013.

- [11] D. Garber and E. Hazan. Faster rates for the frank-wolfe method over strongly-convex sets. In Proceedings of the 32nd International Conference on Machine Learning, volume 951, pages 541–549, 2015.

- [12] D. Gross, Y.-K. Liu, S. Flammia, S. Becker, and J. Eisert. Quantum state tomography via compressed sensing. Physical review letters, 105(15):150401, 2010.

- [13] J. Guelat and P. Marcotte. Some comments on wolfe’s away step. Math. Program., 35(1):110–119, 1986.

- [14] R. Harman and M. Trnovská. Approximate D-optimal designs of experiments on the convex hull of a finite set of information matrices. Mathematica Slovaca, 59(6):693–704, 2009.

- [15] Elad Hazan. Sparse approximate solutions to semidefinite programs. In Latin American symposium on theoretical informatics, pages 306–316. Springer, 2008.

- [16] M. Jaggi. Revisiting Frank-Wolfe: Projection-Free Sparse Convex Optimization. JMLR W&CP, 28(1):427–435, 2013.

- [17] Leonid G Khachiyan. Rounding of polytopes in the real number model of computation. Mathematics of Operations Research, 21(2):307–320, 1996.

- [18] S. Lacoste-Julien and M. Jaggi. On the global linear convergence of Frank-Wolfe optimization variants. In Advances in Neural Information Processing Systems, pages 496–504, 2015.

- [19] G. Lan and Y. Zhou. Conditional gradient sliding for convex optimization. SIAM J. Optim., 26(2):1379–1409, 2016.

- [20] Guanghui Lan and Yuyuan Ouyang. Accelerated gradient sliding for structured convex optimization. Arxiv preprint:1609.04905, 2016.

- [21] Z. Lu and T.K. Pong. Computing optimal experimental designs via interior point method. SIAM J. Matrix Anal. Appl., 34(4):1556–1580, 2013.

- [22] Y. Nesterov. Introductory lectures on convex optimization: A basic course, volume 87 of Applied Optimization. Kluwer Academic Publishers, 2004.

- [23] Y. Nesterov and A. Nemirovski. Interior-point Polynomial Algorithms in Convex Programming. Society for Industrial Mathematics, 1994.

- [24] G. Odor, Y.-H. Li, A. Yurtsever, Y.-P. Hsieh, Q. Tran-Dinh, M. El-Halabi, and V. Cevher. Frank-Wolfe works for non-lipschitz continuous gradient objectives: Scalable poisson phase retrieval. In 2016 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 6230–6234. IEEE, 2016.

- [25] D. M. Ostrovskii and F. Bach. Finite-sample Analysis of M-estimators using Self-concordance. Arxiv preprint:1810.06838v1, 2018.

- [26] G. Peyré and M. Cuturi. Computational optimal transport. Foundations and Trends® in Machine Learning, 11(5-6):355–607, 2019.

- [27] E. K. Ryu and S. Boyd. Stochastic proximal iteration: a non-asymptotic improvement upon stochastic gradient descent. Author website, early draft, 2014.

- [28] W. Su, S. Boyd, and E. Candes. A differential equation for modeling Nesterov’s accelerated gradient method: Theory and insights. In Advances in Neural Information Processing Systems (NIPS), pages 2510–2518, 2014.

- [29] T. Sun and Q. Tran-Dinh. Generalized Self-Concordant Functions: A Recipe for Newton-Type Methods. Math. Program. (online first), pages 1–63, 2018.

- [30] Q. Tran-Dinh, A. Kyrillidis, and V. Cevher. Composite self-concordant minimization. J. Mach. Learn. Res., 15:374–416, 2015.

- [31] Q. Tran-Dinh, L. Ling, and K.-C. Toh. A new homotopy proximal variable-metric framework for composite convex minimization. Tech. Report (UNC-STOR), pages 1–28, 2018.

- [32] Q. Tran-Dinh, T. Sun, and S. Lu. Self-concordant inclusions: A unified framework for path-following generalized Newton-type algorithms. Math. Program., 177(1–2):173–223, 2019.

- [33] A. Yurtsever, Q. Tran-Dinh, and V. Cevher. A universal primal-dual convex optimization framework. Advances in Neural Information Processing Systems (NIPS), pages 1–9, 2015.

- [34] Alp Yurtsever, Olivier Fercoq, and Volkan Cevher. A conditional gradient-based augmented lagrangian framework. arXiv preprint arXiv:1901.04013, 2019.