MS-RMA-20-02481.R1

Johari, Li, Liskovich, and Weintraub

Experimental Design in Two-Sided Platforms

Experimental Design in Two-Sided Platforms:

An Analysis of Bias

Ramesh Johari \AFFManagement Science and Engineering, Stanford University, \EMAILrjohari@stanford.edu \AUTHORHannah Li \AFFManagement Science and Engineering, Stanford University, \EMAILhannahli@stanford.edu

Inessa Liskovich \AFFAirbnb Inc., \EMAILinessa.liskovich@airbnb.com

Gabriel Y. Weintraub \AFFGraduate School of Business, Stanford University, \EMAILgweintra@stanford.edu

We develop an analytical framework to study experimental design in two-sided marketplaces. Many of these experiments exhibit interference, where an intervention applied to one market participant influences the behavior of another participant. This interference leads to biased estimates of the treatment effect of the intervention. We develop a stochastic market model and associated mean field limit to capture dynamics in such experiments, and use our model to investigate how the performance of different designs and estimators is affected by marketplace interference effects. Platforms typically use two common experimental designs: demand-side “customer” randomization () and supply-side “listing” randomization (), along with their associated estimators. We show that good experimental design depends on market balance: in highly demand-constrained markets, is unbiased, while is biased; conversely, in highly supply-constrained markets, is unbiased, while is biased. We also introduce and study a novel experimental design based on two-sided randomization () where both customers and listings are randomized to treatment and control. We show that appropriate choices of designs can be unbiased in both extremes of market balance, while yielding relatively low bias in intermediate regimes of market balance.

1 Introduction

We develop a framework to study experiments (also known as A/B tests) that two-sided platform operators routinely employ to improve the platform. Platforms use experiments to test many types of interventions that affect interactions between participants in the market; examples include features that change the process by which buyers search for sellers or interventions that alter the information the platform shares with buyers. The goal of the experiment is to introduce the intervention to some fraction of the market and use the resulting outcomes to estimate the effect if the intervention were introduced to the entire market. Platforms rely on these estimated effect sizes to make decisions about whether or not to launch the intervention to the entire market.

However, in marketplace experiments, these estimates are often biased due to interference between market participants. Market participants interact and compete with each other and, as a result, the treatment assigned to one individual may influence the behavior of another individual. These interactions violate the Stable Unit Treatment Value Assumption (SUTVA) (Imbens and Rubin (2015)) that guarantees unbiased estimates of the treatment effect. Previous work has shown that the resulting bias can be quite large, and at times as large as the treatment effect itself (Blake and Coey (2014), Fradkin (2015), Holtz et al. (2020)). In this work, we model the platform competition dynamics, investigate how they influence the performance of different canonical experimental designs, and also introduce novel designs that can yield improved performance.

We are particularly motivated by marketplaces where customers do not purchase goods, but rather book them for some amount of time. This covers a broad array of platforms, including freelancing (e.g., Upwork), lodging (e.g., Airbnb and Booking.com), and many services (tutoring, dogwalking, child care, etc.). While we explicitly model such a platform, the model we describe also captures features of a platform where goods are bought and supply must be replenished for future demand.

Our model consists of a fixed number of listings; customers arrive sequentially over (continuous) time. For example, in an online labor platform, a freelancer offering work is a listing, and a client looking to hire a freelancer is a customer. On a lodging site, listings include hotel rooms or private rooms and customers are travelers wanting to book. Naturally, an arriving customer can only book available listings (i.e., those not currently booked). The customer forms a consideration set from the set of available listings and then, according to a choice model, chooses which listing to book from this set (including an outside option). Once a listing is booked, it is occupied and becomes unavailable until the end of its occupancy time.

We focus on interventions by the platform that change the parameters governing the choice probability of the customer, such as those described above; we refer to the new choice parameters as the treatment model and the baseline as the control model.111The same modeling framework that we employ in this paper can be used to consider interventions that change other parameters, such as customer arrival rates or the time that listings remain occupied when booked; such application is outside the scope of our current work. We assume the platform wants to use an experiment to assess the difference between the rate at which bookings would occur if all choices were made according to the treatment parameters and the corresponding rate if all choices were made according to the control parameters . This difference is the global treatment effect or . In particular, we assume that the quantity of interest is the steady-state (or long-run) , i.e., the long-run average difference in rental rates.222Our framework can also be used to evaluate other metrics of interest based on experimental outcomes; for simplicity we focus on rate of booking in this work.

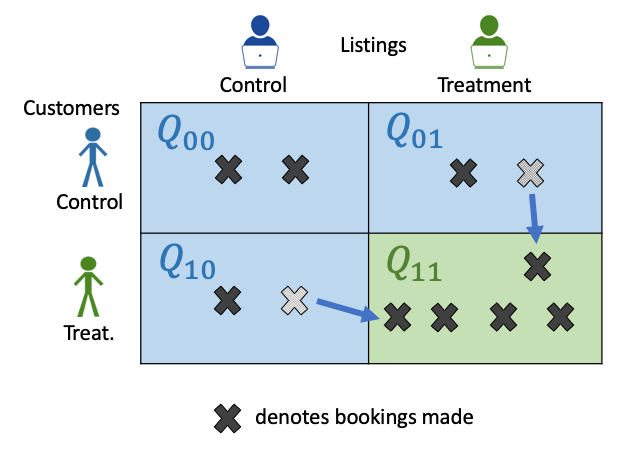

Most platforms employ one of two simple designs for testing such an intervention: either customer-side randomization (what we call the design) or listing-side randomization (what we call the design). In the design, customers are randomized to treatment or control. All customers in treatment make choices according to the treatment choice model and all customers in control make choices according to the control choice model. In the design, listings are randomized to treatment or control, and the utility of a listing is then determined by its treatment condition. As a result, in the design, in general each arriving customer will consider some listings in the treatment condition and some listings in the control condition. As an example, suppose the platform decides to test an intervention that shows badges for certain listings. In the design, all treatment customers see the badges and no control customers see the badges. In the design, all customers see the badges on treated listings, and do not see them on control listings.

Each of these designs are associated with natural estimators. In the design, the platform measures the difference in the rate of bookings between treatment and control customers; this is what we call the naive estimator. In the design, the platform measures the difference in the rate at which treatment and control listings are booked; this is what we call the naive estimator.

To develop some intuition for the potential biases, first consider an idealized static setting where listings are instantly replenished upon being booked; in other words, every arriving customer sees the full set of original listings as available. As a result, in the design there is no interference between treatment and control customers, and consequently the estimator is unbiased for the true . On the other hand, in the design, every arriving customer considers both treatment and control listings when choosing whether to book, creating a linkage across listings through customer choice. In other words, in the design there is interference between treatment and control, and in general the estimator will be biased for the true .

Now return to a dynamic model where the inventory of listings is limited, and listings remain unavailable for some time after being booked. In this case, observe that on top of the preceding discussion, there is a dynamic linkage between customers: the set of listings available for consideration by a customer is dependent on the listings considered and booked by previously arriving customers. This dynamic effect introduces a new form of bias into estimation and is distinctly unique to our work. In particular, because of this dynamic bias, in general the naive estimator will be biased as well.

Our paper develops a dynamic model of two-sided markets with inventory dynamics, and uses this framework to compare and contrast both the designs and estimators above. We also introduce and study a novel class of more general designs based on two-sided randomization (of which the two examples above are special cases). In more detail, our contributions and the organization of the paper are as follows.

Benchmark model and formal mean field limit. Our first main contribution is to develop a general, flexible theoretical model to capture the dynamics described above. In Section 3, we present a model that yields a continuous-time Markov chain in which the state at any given time is the number of currently available listings of each type. In Section 4, we propose a formal mean field analog of this continuous-time Markov chain, by considering a limit where the number of listings in the system and the arrival rate of customers both grow to infinity. Scaling by the number of listings yields a continuum mass of listings in the limit. In the mean field model, the state at a given time is the mass of available listings and this mass evolves via a system of ODEs. Using a Lyapunov argument, we show that this system is globally asymptotically stable and give a succinct characterization of the resulting asymptotic steady state of the system as the solution to an optimization problem. We formally establish that the mean field limit arises as the fluid limit of the corresponding finite market model, as market size grows; in other words, the mean field model is a good approximation to large markets. The mean field model allows us to tractably analyze different estimators, as well as to study their biases in the large market regime.

Designs and estimators: Two-sided, customer-side, and listing-side randomization. In Section 5, we introduce a more general form of experimental design, called two-sided randomization (); an analogous idea was independently proposed recently by Bajari et al. (2019) (see also Section 2). In a design, both customers and listings are randomized to treatment and control. However, the intervention is only applied when a treatment customer considers a treatment listing; otherwise, if the customer is in control or the listing is in control, the intervention is not seen by the customer. (In the example above, a customer would see the badge on a listing only if the customer were treated and the listing were treated.) Notably, the and designs are special cases of . We also define natural naive estimators for each design.

Analysis of bias: The role of market balance. In Section 6 we study the bias of the different designs and estimators proposed. Our main theoretical results characterize how the bias depends on the relative volumes of supply and demand in the market. In particular, in the highly demand-constrained regime (where customers arrive slowly and/or listings replenish quickly): the naive estimator becomes unbiased, while the naive estimator is biased. On the other hand, in the highly supply-constrained regime (where customers arrive rapidly and/or listings replenish slowly) we find that in fact the naive estimator becomes unbiased, while the naive estimator is biased. These findings suggest that platforms can potentially reduce bias by choosing the type of experiment based on knowledge of market balance.

Given the findings that and experiments offer benefits in different extremes, it is natural to ask whether good performance can be achieved in moderately balanced markets by “interpolating” between the naive and estimators. We define a naive estimator that achieves this interpolation and has low bias in both market extremes, but still has large bias for moderate market balance. We then define more sophisticated estimators that explicitly aim to correct for interference in regimes of moderate market balance. These latter estimators exhibit substantially improved performance in simulations. Appendix 12 shows that these estimators perform well across a wide range of market parameters.

Insights from simulations. In Section 7 we turn to simulations in the finite system to study the variance of the estimators. The simulations corroborate the theoretical findings that offers benefits with respect to bias, albeit at the cost of moderate increases in variance. Among the estimators that we study, we find that those with smaller reductions in bias have smaller increases in variance, while those with larger reductions in bias have larger increases in variance, thus revealing a tradeoff between bias and variance for the estimators.

In Section 8, we compare the approach with cluster-randomized experiments, an existing approach that platforms utilize to reduce bias. The simulations suggest that while both approaches can reduce bias when the market is tightly clustered, estimators can reduce bias in highly interconnected markets where cluster randomized experiments cannot.

Taken together, our work sheds light on what experimental designs and associated estimators should be used by two-sided platforms depending on market conditions, to alleviate the biases from interference that arise in such contexts. We view our work as a starting point towards a comprehensive framework for experimental design in two-sided platforms; we discuss some directions for future work in Section 9.

2 Related work

SUTVA. The types of interference described in these experiments are violations of the Stable Unit Treatment Value Assumption (SUTVA) in causal inference (Imbens and Rubin 2015). SUTVA requires that the (potential outcome) observation on one unit should be unaffected by the particular assignment of treatments to the other units.t A large number of recent works have investigated experiment design in the presence of interference, particularly in the context of markets and social networks.

Interference in marketplaces. Biases from interference can be large: Blake and Coey (2014) empirically show in an auction experiment that the presence of interference among bidders caused the estimate of the treatment effect to be wrong by a factor of two. Fradkin (2019) finds through simulations that a marketplace experiment changing search and recommendation algorithms can overestimate the true effect by 50 percent. More recent work by Holtz et al. (2020) randomizes clusters of similar listings to treatment or control, and finds the bias due to interference can be almost 1/3 of the treatment effect. Interestingly, Holtz et al. (2020) also finds weak empirical evidence that the extent of interference depends on market balance; our paper provides strong theoretical grounding for such a claim.

Inspired by the goal of reducing such bias, other work has developed approaches to bias characterization and reduction both theoretically (e.g., Basse et al. (2016) in the context of auctions with budgets), as well as via simulation (e.g., Holtz (2018) who explores the performance of designs). Our work complements this line, by developing a mathematical framework for the study of estimation bias in dynamic platforms. Key to our analysis is the use of a mean field model to model both transient and steady-state behavior of experiments. A related approach is taken in Wager and Xu (2019), where a mean field analysis is used to study equilibrium effects of an experimental intervention where treatment is incrementally applied in a marketplace (e.g., through small pricing changes).

Interference in social networks. A bulk of the literature in experimental design with interference considers an interference that arises through some underlying social network: e.g., Manski (2013) studies the identification of treatment responses under interference; Ugander et al. (2013) introduces a graph cluster based randomization scheme and analyzes the bias and variance of the design; and many other papers, including Athey et al. (2018), Basse et al. (2019), Saveski et al. (2017) focus on estimating the spillover effects created by interference. In particular, Pouget-Abadie et al. (2019) and Zigler and Papadogeorgou (2018) consider interference on a bipartite network, which is closer to a two-sided marketplace setting. In general, this line of work considers a fixed interference pattern (social network) over time. Our work is distinct because the interference caused by supply and demand competition is endogenous to the experiment and dynamically evolving over time.

Other experimental designs. In practice, platforms currently mitigate the effects of interference through either clustering techniques that change the unit of observation to reduce spillovers among them (e.g., Chamandy (2016)), similar to some of the works mentioned above (e.g., Holtz (2018), Ugander et al. (2013)); or by switchback testing (Sneider et al. 2019), in which the treatment is turned on and off over time. Both cause a substantial increase in estimation variance due to a reduction in effective sample size and thus the naive and designs remain popular workhorses in the platform experimentation toolkit. In addition to these broad classes of experiments, other work has also introduced modified experiment designs for specific types of interventions, such as Ha-Thuc et al. (2020) for ranking experiments.

Two-sided randomization. Finally, a closely related paper is Bajari et al. (2019). Independently of our own work, there the authors propose a more general multiple randomized design of which is a special case. They focus on a static model and provide an elegant and complete statistical analysis under a local interference assumption. By contrast, we focus on a dynamic platform model with market-wide interference patterns and focus on a mean field analysis of bias.

3 A Markov chain model of platform dynamics

In this section, we first introduce the basic dynamic platform model that we study in this paper with a finite number of listings. In the next section, we describe a formal mean field limit of the model inspired by the regime where . This mean field limit model then serves as the framework within which we study the bias of different experimental designs and associated estimators in the remainder of the paper.

We consider a two-sided platform where we refer to the supply side as listings and the demand side as customers. Customers arrive over time and at the time of arrival, the customer forms a consideration set from the set of available listings in the market and then decides whether to book one of them. If the customer books, then the selected listing is occupied for a random length of time during which it is unavailable for other customers. At the end of this booking, the listing again becomes available for use for other customers.

The formal details of our model are as follows.

Time. The system evolves in continuous time .

Listings. The system consists of a fixed number of listings. We refer to “the ’th system” as the instantiation of our model with listings present. We use a superscript “” to denote quantities in the ’th system where appropriate.

We allow for heterogeneity in the listings. Each listing has a type , where is a finite set (the listing type space). Note that in general, the type may encode both observable and unobservable covariates; in particular, our analysis does not presume that the platform is completely informed about the type of each listing. For example, in a lodging site may encode observed characteristics of a house such as the number of bedrooms, but also characteristics that are unobserved by the platform because they may be difficult or impossible to measure. Let denote the total number of listings of type in the ’th system. For each , we assume that . Note that .

State description. At each time , each listing can be either available or occupied (i.e., occupied by a customer who previously booked it). The system state at time in the ’th system is described by , where denotes the number of listings of type available in the system at time . Let be the total number of listings available at time . In our subsequent development, we develop a model that makes a continuous-time Markov process.

Customers. Customers arrive to the platform sequentially and decide whether to book, and if so, which listing to book. Each customer has a type , where is a finite set (the customer type space) that represents customer heterogeneity. As with listings, the type may encode both observable and unobservable covariates, and again, our analysis does not presume that the platform is completely informed about the type of each customer. Customers of type arrive according to a Poisson process of rate ; these processes are independent across types. Let be the total arrival rate of customers. Let denote the arrival time of the ’th customer.

We assume that , i.e., the arrival rate of customers grows proportionally with the number of listings when we take the large market limit. Further, we assume that for each , we have . Note that .

Consideration sets. In practice, when customers arrive to a platform, they typically form a consideration set of possible listings to book; the initial formation of the consideration set may depend on various aspects of the search and recommendation algorithms employed by the platform. To simplify the model, we capture this process by assuming that on arrival, each listing of type that is available at time is included in the arriving customer’s consideration set independently with probability for a customer of type . For example, can capture the possibility that the platform’s search ranking is more likely to highlight available listings of type that are more attractive for a customer of type , making these listings more likely to be part of the customer’s consideration set; this effect is made clear via our choice model presented below. After the consideration set is formed, a choice model is then applied to the consideration set to determine whether a booking (if any) is made.

Formally, the customer choice process unfolds as follows. Suppose that customer arrives at time . For each listing , let if the listing is unavailable at . Otherwise, if listing is available, then let with probability , and let with probability , independently of all other randomness. Then the consideration set of customer is .

Our theoretical results in this paper are developed with this model of consideration set formation. Other models of consideration set formation are also reasonable, however. As one example, customers might sample a consideration set of a fixed size, regardless of total number of listings available. We explore such a consideration set model through simulations in Appendix 12 and show that similar insights hold.

Customer choice. Customers choose at most one listing to book and can choose not to book at all. We assume that customers have a utility for each listing that depends on both customer and listing types: a type customer has utility for a type listing. Let denote the probability that arriving customer of type books listing of type .

In this paper we assume that customers make choices according to the well-known multinomial logit choice model. In particular, given the realization of , we have:

| (1) |

Here is the value of the outside option for type customers in the ’th system. The probability that customer does not book any listing at all grows with . We let the outside option scale with ; this is motivated by the observation that in practical settings, the probability a customer does not book should remain bounded away from zero even for very large systems. In particular, we assume that .

We note that this specification of choice model, although it relies on the multinomial logit model, can be quite flexible because we allow for arbitrary heterogeneity of listings and customers.

For later reference, we define:

| (2) |

where the expectation is over the randomness in . With this definition, is the probability that customer books an available listing of type , where the probability is computed prior to realization of the consideration set.

Dynamics: A continuous-time Markov chain. The system evolves as follows. Initially all listings are available.333As the system we study is irreducible and we analyze its steady state behavior, it would not matter if we chose a different initial condition. Every time a customer arrives, the choice process described above unfolds. An occupied listing remains occupied, independent of all other randomness, for an exponential time that is allowed to depend on the type of the listing.444An even more general model might allow the occupancy time to depend on both listing type and the type of the customer who made the booking; such a generalization remains an interesting open direction. More formally, let and for each type define such that, once booked, a listing of this type will remain occupied for an exponential time with parameter . We overload notation and define . Once this time expires, the listing returns to being available.

When fixing and all system parameters except for , increasing will make the system less supply constrained and decreasing will make the system more supply constrained, while preserving the relative occupancy times of each listing type.

Our preceding specification turns into a continuous-time Markov process on a finite state space . We now describe the transition rates of this Markov process. For a state , represents the number of available listings of type .

There are only two types of transitions possible: either (i) a listing that is currently occupied becomes available, or (ii) a customer arrives, and books a listing that is currently available. (If a customer arrives but does not book anything, the state of the system is unchanged.) Let denote the unit basis vector in the direction , i.e., , and for . The rate of the first type of transition is:

| (3) |

since there are booked listings of type , and each remains occupied for an exponential time with mean , independently of all other randomness.

The second type of transition requires some more steps to formulate. In principle, our choice model suggests that the identity of both the arriving guest and individual listings affect system dynamics; however, our state description only tracks the aggregate number of listings of each type available at each time . The key here is that our entire specification depends on customers only through their type, and depends on listings only through their type.

Formally, suppose a customer of type arrives to find the system in state . For each let be a Binomial random variable, independently across . Recall that for each available listing , each is a Bernoulli random variable. Recalling as defined in (2), it is straightforward to check that:

| (4) |

In other words, the probability an arriving customer of type books a listing of type when the state is is given by ; and this probability depends on the past history only through the state (ensuring the Markov property holds).

With this definition at hand, for states with , the rate of the second type of transition is:

| (5) |

Note that the resulting Markov chain is irreducible, since customers have positive probability of sampling into, and booking from, their consideration set, and every listing in the consideration set has positive probability of being booked.

Steady state. Since the Markov process defined above is irreducible on a finite state space, there is a unique steady state distribution on for the process.

4 A mean field model of platform dynamics

The continuous-time Markov process described in the preceding section is challenging to analyze directly because the customers’ choices and consideration sets induce complex dynamics. Instead, to make progress we consider a formal mean field limit motivated by the regime where , in which the evolution of the system becomes deterministic. We first present a formal mean field analogue of the Markov process introduced in the previous section and provide intuition for its derivation. We then formally prove that the sequence of Markov processes converges to this mean field model as . The mean field model provides tractable expressions in the large market regime for the different estimators we consider, allowing us to study and compare their bias.

The mean field model we study consists of a continuum unit mass of listings. The total mass of listings of type in the system is (recall that ). We represent the state at time by ; represents the mass of listings of type available at time . The state space for this model is:

| (6) |

We first present the intuition behind our mean field model. Consider a state with for all . We view this state as analogous to a state in the ’th system. We consider the system dynamics defined by (3)-(5). Note that the rate at which occupied listings of type become available is , from (3). If we divide by , then this rate becomes as . On the other hand, note that for large , if is Binomial, then concentrates on . Thus the choice probability is approximately:

| (7) |

(Here we use the fact that as .) This is the mean field multinomial logit choice model for our system. In the finite model, the rate at which listings of type become occupied is , from (5). If we divide by , this rate becomes as .

Inspired by the preceding observations, we define the following system of differential equations for the evolution of :

| (8) |

This is our formal mean field model. In the remainder of this section, we first show that this system has a unique solution for any initial condition. Then we characterize the behavior of the system. By constructing an appropriate Lyapunov function, we show that the mean field model has a unique limit point to which all trajectories converge (regardless of initial condition). This limit point is the unique steady state of the mean field limit. Finally, we prove that the sequence of Markov processes indeed converges to this mean field model (in an appropriate sense). Hence, the mean field model provides a close approximation to the evolution of large finite markets.

4.1 Existence and uniqueness of mean field trajectory

First, we show the straightforward result that the system of ODEs defined in (8) possesses a unique solution. This follows by an elementary application of the Picard-Lindelöf theorem from the theory of differential equations. The proof is in Appendix 10.

Proposition 4.1

Fix an initial state . The system (8) has a unique solution satisfying and for all and , and .

4.2 Existence and uniqueness of mean field steady state

Now we characterize the behavior of the mean field limit. We show that the system of ODEs in (8) has a unique limit point, to which all trajectories converge regardless of the initial condition. We refer to this as the steady state of the mean field system. We prove the result via the use of a convex optimization problem; the objective function of this problem is a Lyapunov function for the mean field dynamics that guarantees global asymptotic stability of the steady state.

Formally, we have the following result. The proof is in Appendix 10.

Theorem 4.2

There exists a unique steady state for (8), i.e., a unique vector solving the following system of equations:

| (9) |

This limit point has the property that for all , i.e., it is in the interior of . Further, this limit point is globally asymptotically stable, i.e., all trajectories of converge to as , for any initial condition .

The limit point is the unique solution to the following optimization problem:

| minimize | ||||

| (10) | ||||

| subject to | (11) |

The function appearing in the proposition statement is not convex; our proof proceeds by first noting that it suffices to restrict attention to such that for all , then making the transformation . The objective function redefined in terms of these transformed variables is strictly convex, and this allows us to establish the desired result.

4.3 Convergence to the mean field limit

Finally, we formally describe the sense in which our system converges to the system in (8). We first move from analyzing the number of listings available in the ’th system to analyzing the proportion of listings available. To this end, define the normalized process where

Note that under this definition, is also a continuous time Markov process with dynamics induced by the dynamics of ; in particular, the chain has the same transition rates as , but increments are of size . The following theorem establishes the convergence of to the solution of the ODE described in (8) as .

Theorem 4.3

Assume that for all and for all as . Fix and assume that is deterministic, with for all . Let denote the unique solution to the system defined in (8), with initial condition .

Then for all and for all times ,

| (12) |

The proof for this result relies on an application of Kurtz’s Theorem for the convergence of pure jump Markov processes; full details are in Appendix 10. We note that this result holds for any sequence of initial conditions , as long as the proportion of available listings at time converges to a constant vector as ; further, the vector can be any (feasible) initial state in the mean field model.

We now utilize the mean field model to study experimental designs and interference.

5 Experiments: Designs and estimators

In this section, we leverage the framework developed in the previous section to undertake a study of experimental designs a platform might employ to test interventions in the marketplace. For simplicity, we focus on interventions that change the choice probability of one or more types of customers for one or more types of listings, and we assume the platform is interested in estimating the resulting rate at which bookings take place. However, we believe the same approach we employ here can be applied to study other types of interventions and platform objectives as well.

Formally, the platform’s goal is to design experiments with associated estimators to assess the performance of the intervention (the treatment), relative to the status quo (the control). In particular, the platform is interested in determining the steady-state rate of booking when the entire market is in the treatment condition (i.e., global treatment), compared to the steady-state rate of booking when the entire market is in the control condition (i.e., global control). We refer to the difference of these two rates as the global treatment effect (). We focus on these steady-state quantities as a platform is typically interested in the long-run effect of an intervention.

Two types of canonical experimental designs are typically employed in practice: listing-side randomization (denoted ) and customer-side randomization (denoted ). In the former design, listings are randomized to treatment or control; in the latter design, customers are randomized to treatment or control. Each design also has an associated natural “naive” estimator of booking rates, that is, a (scaled) difference in means estimators for the two groups. As we discuss, these estimators will typically be biased, due to interference effects.

The and designs are special cases of a novel, more general two-sided randomization () design that we introduce in this work, where both listings and customers are randomized to treatment and control simultaneously. As we discuss, this type of experiment can be combined with design and analysis techniques to reduce bias. On the design side, designs allow us to construct experiments that interpolate between and designs in such a way that bias is reduced. On the analysis side, designs allow us to observe different competition effects, that we can use to heuristically debias our estimators. ( designs were also independently introduced and studied in recent work by Bajari et al. (2019); see Section 2 for discussion.) In the next subsection we develop the relevant formalism for these designs; we then subsequently define natural “naive” estimators that are commonly used for the and designs, as well as an estimator for a design. In the remainder of the paper we study the bias of these different designs and estimators under different market conditions.

5.1 Experimental design

Since and are special cases of a design, we first describe how to embed experimental designs into our model, and then subsequently describe and designs in our model.

Treatment condition. We consider a binary treatment: every customer and listing in the market will either be in treatment or control. (Generalization of our model to more than two treatment conditions is relatively straightforward.) We model the treatment condition by expanding the set of customer and listing types. For every customer type , we create two new customer types ; and for every listing type , we create a two new listing types . The types are control types; the types are treatment types.

Two-sided randomization. In this design, randomization takes place on both sides of the market simultaneously. We assume that a fraction of customers are randomized to treatment, and a fraction to control, independently; and we assume that a fraction of listings are randomized to treatment, and a fraction to control, independently.

Treatment as a choice probability shift. Examples of interventions that platforms may wish to test include the introduction of higher quality photos for a hotel listing on a lodging site, showing previous job completion rates of a freelancer on an online labor market, or reducing the friction for an item in the checkout flow. Such interventions change the choice probability of listings by customers either through the consideration probabilities or perceived utility for a listing. In particular, we continue to assume the multinomial logit choice model, and we assume that for a type customer and a type listing that have been given the intervention, the utility becomes and the probability of inclusion in the consideration set becomes . Since we focus on changes in choice probabilities, we assume that the holding time parameter of a listing of type is , regardless of whether it is assigned to treatment or control.555Our current work allows us to relatively easily incorporate depending on treatment condition of the listing, and as such we can extend our results to study designs where varies with treatment condition. In general, however, when customers are also randomized to treatment or control, the holding time parameter of a listing should also depend on the treatment condition of the customer who booked that listing. Adapting our framework to incorporate this possibility remains an interesting direction for future work.

In the designs that we consider, a key feature is that the intervention is applied only when a treated customer interacts with a treated listing. For example, when an online labor marketplace decides to show previous job completion rates of a freelancer as an intervention, only treated customers can see these rates, and they only see them when they consider treated freelancers. We model this by redefining quantities in the experiment as follows:

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) |

This definition is a natural way to incorporate randomization on each side of the market. However, we remark here that it is not necessarily canonical; for example, an alternate design would be one where the intervention is applied when either the customer has been treated or the listing has been treated. Even more generally, the design might randomize whether the intervention is applied, based on the treatment condition of the customer and the listing. In all likelihood, the relative advantages of these designs would depend not only on the bias they yield in any resulting estimators, but also in the variance characteristics of those estimators. We leave further study and comparison of these designs to future work.

Customer-side and listing-side randomization. Two canonical special cases of the design are as follows. When , all listings are in the treatment condition; in this case, randomization only takes place on the customer side of the market. This is the customer-side randomization () design. When , all customers are in the treatment condition and randomization only takes place on the listing side of the market. This is the listing-side randomization () design.

System dynamics. With the specification above, it is straightforward to adapt our mean field system of ODEs, cf. (8), and the associated choice model (7), to this setting. The key changes are as follows:

-

1.

The mass of control (resp., treatment) listings of type (resp., ) becomes (resp., ). In other words, abusing notation, we define , and .

-

2.

The arrival rate of control (resp., treatment) customers of type (resp., ) becomes (resp., ). Thus we define , and .

- 3.

Using Proposition 4.1 and Theorems 4.2, we know that there exists a unique solution to the resulting system of ODEs; and that there exists a unique limit point to which all trajectories converge, regardless of initial condition. This limit point is the steady state for a given experimental design. For a experiment with treatment customer fraction , and treatment listing fraction , we use the notation to denote the ODE trajectory, and we use to denote the steady state.

Rate of booking. In our subsequent development, it will be useful to have a shorthand notation for the rate at which bookings of listings of treatment condition are made by customers of treatment condition , in the interval . In particular, we define:

| (17) |

Since is globally asymptotically stable, bounded, and converges to as , we have:

| (18) |

Global treatment effect. Recall we assume the steady-state rate of booking is the quantity of interest to the platform. In particular, the platform is interested in the change in this rate from the global control condition () to the global treatment condition ().

In the global control condition, the steady state rate at which customers book is: , and in the global treatment condition, the steady state rate at which customers book is . Under these definitions, the global treatment effect is .

We remark that the rate of booking decisions made by arriving customers will change over time, even if the market parameters are constant over time (including the arrival rates of different customer types, as well as the utilities that customers have for each listing type). This transient change in booking rates is driven by changes in the state ; in general, such fluctuations will lead the transient rate of booking to differ from the steady-state rate, for all values of and (including global treatment and global control). In this work, we focus on the steady state quantities to capture, informally, the long run change in behavior due to an intervention. 666Note that in two-sided markets, certain types of interventions will also cause long-run economic equilibration due to strategic responses on the part of market participants; for example, if prices are lowered during an experiment, this may affect entry decisions of both buyers and sellers, and thus the long-run market equilibrium. While our model allows the choice probabilities to change due to treatment, a more complete analysis of long run economic equilibration due to interventions remains a direction for future work.

5.2 Estimators: Transient and steady state

The goal of the platform is to use the experiment to estimate . In this section we consider estimators the platform might use to estimate this quantity. We first consider the and designs, and we define “naive” estimators that the platform might use to estimate the global treatment effect. These designs and estimators are those most commonly used in practice. We define these estimators during the transient phase of the experiment and then define the associated steady-state versions of these estimators. Finally, we combine these estimation approaches in a natural heuristic that can be employed for any general design.

Estimators for the design. We start by considering the design, i.e., where and . A simple naive estimate of the rate of booking is to measure the rate at which bookings are made in a given interval of time by control customers, and compare this to the analogous rate for treatment customers. Formally, suppose the platform runs the experiment for the interval , with a fraction of customers in treatment. The rate at which customers of treatment condition book in this period is . The naive estimator is the difference between treatment and control rates, where we correct for differences in the size of the control and treatment groups, by scaling with the respective masses:

| (19) |

We let denote the steady-state naive estimator.

Estimators for the design. Analogously, we can define a naive estimator for the design, i.e., where and . Formally, suppose the platform runs the experiment for the interval , with fraction of listings in treatment. The rate at which listings with treatment condition are booked in this period is . The naive estimator is the difference between treatment and control rates, scaled by the mass of listings in each group:

| (20) |

We let denote the corresponding steady-state naive estimator.

Estimators for the design. As with the and designs, it is possible to design a natural naive estimator for the design as well. In particular, we have the following definition of the naive estimator:

| (21) |

To interpret this estimator, observe that the first term is the normalized rate at which treatment customers booked treatment listings in the experiment; we normalize this by , since a mass of customers are in treatment, and a mass of listings are in treatment. This first term estimates the global treatment rate of booking. The sum is the total rate at which control bookings took place: either because the customer was in the control group, or because the listing was in the control group, or both. (Recall that in the design, the intervention is only seen when treatment customers interact with treatment listings.) This is normalized by the complementary mass, . This second term estimates the global control rate of booking. As before, we can define a steady-state version of this estimator as , with the steady-state versions of the respective quantities on the right hand side of (21).

It is straightforward to check that as , we have , the naive estimator. Similarly, as , we have , the naive estimator. In this sense, the naive estimator naturally “interpolates” between the naive and estimators. In the next section, we exploit this interpolation to choose and as a function of market conditions in such a way as to reduce bias.

More generally, the design also contains much more information about competition in the marketplace, and the resulting interference effects, than either the or designs. Inspired by this observation, together with the idea of interpolating between the naive estimator and the naive estimator, in Section 6.3 we explore alternative, more sophisticated estimators that heuristically debias interference due to competition effects. As we show, these estimators can offer substantial bias reduction over the naive estimator above.

6 Analysis of bias

We now utilize the framework defined to analyze the bias of two common experiment types, experiments and experiments. Recall from Section 1 that, in a setting where listings are immediately replenished, all customers see the full set of original listings as available. There is no competition between customers but there is still competition between listings, and so, intuitively, we expect to be unbiased and to be biased. Meanwhile, in a setting where listings remain unavailable for some amount of time, the resulting dynamic linkage across customers creates a bias in as well. Now, consider the extreme where the market is highly supply-constrained: most customers who arrive see no available listings, but some customers arrive just as a booked listing becomes available and see a single available listing. Such customers compare the listing against the outside option, but, since no other listings are available, do not compare listings against each other. In this regime, there is no competition across listings but there is competition between customers, and so we expect to be unbiased and to be biased.

In this section, we formalize this intuition about the behavior of the estimators in the extremes of market balance. We establish two key theoretical results: in the limit of a highly supply-constrained market (where ), the naive estimator becomes an unbiased estimator of the , while the naive estimator is biased. On the other hand, in the limit of a highly demand-constrained market (where ), the naive estimator becomes an unbiased estimator of the GTE, while the naive estimator is biased. In other words, each of the two naive designs is respectively unbiased in the limits of extreme market imbalance. At the same time, we find empirically that neither estimator performs well in the region of moderate market balance.

Inspired by this finding, we consider and associated estimators that naturally interpolate between the two naive designs depending on market balance. Given the findings above, we show that a simple approach to adjusting and as a function of market balance yields performance that balances between the naive estimator and the naive estimator. Nevertheless, we show there is significant room for improvement, by adjusting for the types of interference that arise using observations from the experiment. In particular, we propose a heuristic for a novel interpolating estimator for the design that aims to correct these biases, and yields surprisingly good numerical performance.

6.1 Theory: Stead-state bias of and in unbalanced markets

In this subsection, we study theoretically the bias of the steady-state naive and estimators in the limits where the market is extremely unbalanced (either demand-constrained or supply-constrained). The key tool we employ is a characterization of the asymptotic behavior of as defined in (18) in the limits where and . We use this characterization in turn to quantify the asymptotic bias of the naive estimators relative to the . We derive these results in the next two subsections and provide a simple example in Section 6.1.3 to illustrate the effects.

6.1.1 Highly demand-constrained markets.

We start by considering the behavior of naive estimators in the limit where . We start with the following proposition that characterizes behavior of as . The proof is in Appendix 10.

Proposition 6.1

Fix all system parameters except and , and consider a sequence of systems in which . Then along this sequence,

| (22) |

The expression on the right hand side depends on both and through and respectively. In particular, we recall that , , and , . In our subsequent discussion in this regime, to emphasize the dependence of on below, we will write . With this definition, we have , .

This proposition allows us to characterize the bias of both and estimators in the demand constrained limit. Note that Proposition 6.1 shows that, in this limit, the (scaled) rate of booking behaves as if the available listings of type was exactly for every and treatment condition . That is, it is as if every arriving customer sees the entire mass of listings as being available, and so bookings are immediately replenished. This observation drives our first main result, that in the demand constrained limit the estimator is unbiased and estimator is biased.

Theorem 6.2

Consider a sequence of systems where . Then for all such that , . However, for , generically over parameter values777Here ”generically” means for all parameter values, except possibly for a set of parameter values of Lebesgue measure zero. we have .

The full proof can be found in Appendix 10. The key insight is that as the market becomes more demand constrained, there is a weakening of the competition between arriving customers, which leads to less interference in a experiment. In the limit, the estimator becomes unbiased. On the other hand, in an experiment there is a positive mass of control and treatment listings available in steady state, leading to competition between listings and bias in the estimator.

6.1.2 Heavily supply-constrained markets.

We now characterize the behavior of naive estimators in the limit where . We start with the next proposition, where we study the behavior of as . The proof is in Appendix 10. To state the proposition, we define:

Proposition 6.3

Fix all system parameters except and , and consider a sequence of systems in which . Along this sequence, the following limit holds:

| (23) |

As before, the expression on the right hand side depends on both and through and respectively. In particular, we recall that , , and , .

A key intermediate result we employ is to demonstrate that in the steady-state in this limit, for all . We know that in the steady state of the mean field limit, the rate at which occupied listings become available must match the rate at which available listings become occupied (flow conservation). We use this fact to show that to first order in , in the limit where we have:

The proposition follows by using this limit to characterize the choice probabilities.

The proof of the preceding proposition reveals that in the limit where , we have:

This preceding expression is the formalization of our intuition that, in the limit where the market is heavily supply-constrained, it is as if each arriving customer seeing an available listing compares only that listing to the outside option; there is no longer any competition between listings.

We can use the preceding proposition to understand the behavior of the , the naive estimator, and the naive estimator in steady-state, as . For simplicity, we hold constant and take the limit . In this case, the preceding proposition shows that:

The global treatment effect in this limit. Bookings occur essentially instantaneously after a listing becomes available, which happens at rate .

We also note that:

The preceding two expressions reveal that the steady-state naive estimator in this setting approaches zero, matching the ; thus it is asymptotically unbiased.

It is also now straightforward to see why the design will be biased. Note that:

An analogous expression holds for . We see that the right hand side reflects the dynamic interference created between treatment and control customers: just as in our simple example, whether or not an available listing is seen by, e.g., a control customer depends on whether it has previously been booked by a treatment customer. That is, customers compete for listings. As in the example, the naive estimator will remain nonzero in general in the limit, even though the approaches zero.

We summarize our discussion in the following theorem.

Theorem 6.4

Consider a sequence of systems where . Then , and for all such that , there also holds . However, for , generically over parameter values we have .

Although the preceding theorem shows that the absolute bias of the naive estimator approaches zero, in fact in general the relative bias will not generally approach zero; this is because the is also approaching zero, and so the second-order behavior of the naive estimator matters. This is in contrast to the behavior of the naive estimator in the demand-constrained limit: in that limit, the remains nonzero in general, and so the naive estimator is both absolutely and relatively unbiased. Nevertheless, note that relative bias of the naive estimator will be significantly smaller than the relative bias of the naive estimator in the supply-constrained limit, since the naive estimator has a nonzero absolute bias in this limit while the approaches zero.

6.1.3 An example: Homogeneous customers and listings.

To more clearly understand the behavior of the bias, in this section we apply Propositions 6.1 and 6.3 to a simpler setting where both listings and customers are homogeneous, i.e., there is only one type of customer and one type of listing. This example illustrates the symmetry between the two sides of the market and the resulting implications for bias in marketplace experiments.

Let denote the control utility and the treatment utility of a customer for a listing. Let denote the outside option value of both control and treatment customers, , and . In this example, we consider two limits: one where is fixed and (the demand-constrained regime), and one where is fixed and (the supply-constrained regime).

In the first case, when with fixed, if we apply Proposition 6.1, we obtain:

| (24) |

In this limit,

From these expressions it is clear that the naive estimator is unbiased, while the naive estimator is biased. Further, the expressions reveal that listing-side randomization creates interference across listings.

In the second case, when with fixed, if we apply Proposition 6.3, we obtain:

| (25) |

In this limit, . From these expressions it is clear that the naive estimator is biased, while the naive estimator is unbiased. Further, these expressions also reveal that customer-side randomization creates interference across customers.

Interestingly, these expressions highlight a remarkable symmetry. As expected, in the limit of a highly demand-constrained market, customers choose among listings; thus there is competition for customers among listings, and this is the source of potential interference in designs. The expressions reveal that in the limit of a highly supply-constrained market, it is as if listings choose among customers; thus there is competition among customers, and this is the source of potential interference in designs. Indeed, the expressions for and in (25) take the form of a multinomial logit choice model of listings for customers. We believe this type of symmetry provides important insight into the nature of experimental design in two-sided markets, and in particular the roots of the interference typically observed in such settings.

6.1.4 Sign of the bias in and estimates.

Theorems 6.2 and 6.4 state that the estimate is biased in the demand constrained limit and the estimate is biased in the supply constrained limit, but make no claim as to whether the estimators overestimate or underestimate the . In general, we cannot provide guarantees for the sign of the bias, as it depends on the distribution of listings, the rates at which listing replenish, and the lift on the individual and induced by the interventions. However, for a broad class of interventions, we can show that the estimate overestimates in the demand constrained limit and overestimates in the supply constrained limit. In such cases where we know the bias to be positive, and experiments can be used to bound the size of the .

We call an intervention positive if for all and . Such an intervention can be viewed as an improvement on the platform for all customer and listing type pairs, since for each pair at least one of the customer’s consideration probability or utility for the listing type must increase. Note that this class of interventions is broad enough to allow for heterogeneous treatment effects across different pairs.888A symmetric analysis can be applied for “negative” interventions, where for all and ; though, of course, interventions known to be negative in advance are less likely to be desirable from the platform’s perspective.

For positive interventions, straightforward applications of Propositions 6.1 and 6.3 show that overestimates the in the demand constraint limit and overestimates the in the supply constrained limit. The result follows from the fact that in a customer-side (resp., listing-side) experiment in a supply constrained (resp., demand-constrained) setting, the individuals in the treatment group face less competition than they would in the global treatment setting, whereas the individuals in the control group face more competition than in the global control setting.

Proposition 6.5

Suppose that the treatment is positive, i.e., for all . Then we have the following.

-

1.

bias when demand constrained: Consider a sequence of systems where . For any , we have .

-

2.

bias when supply constrained: Consider a sequence of systems where . For any , we have .

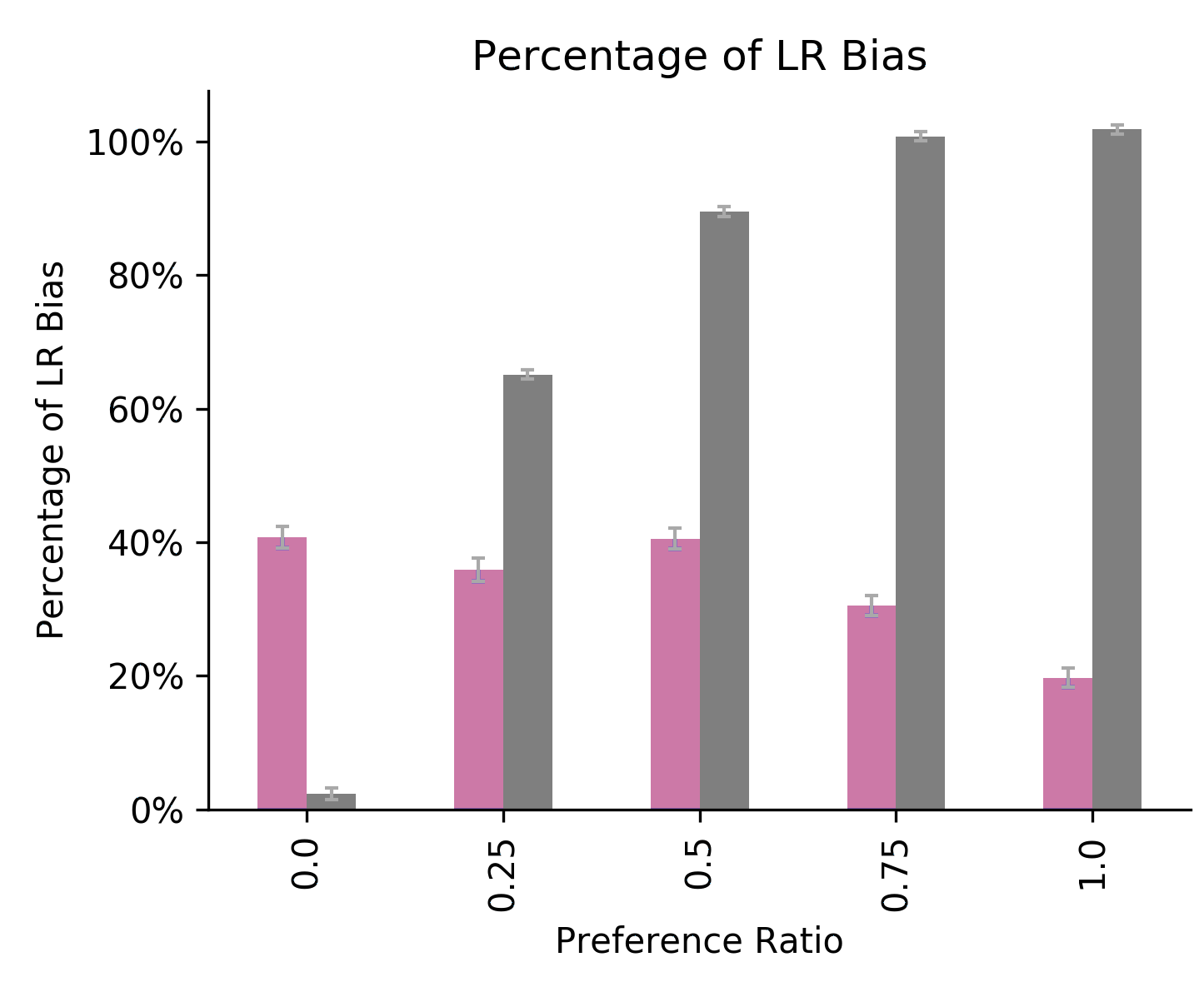

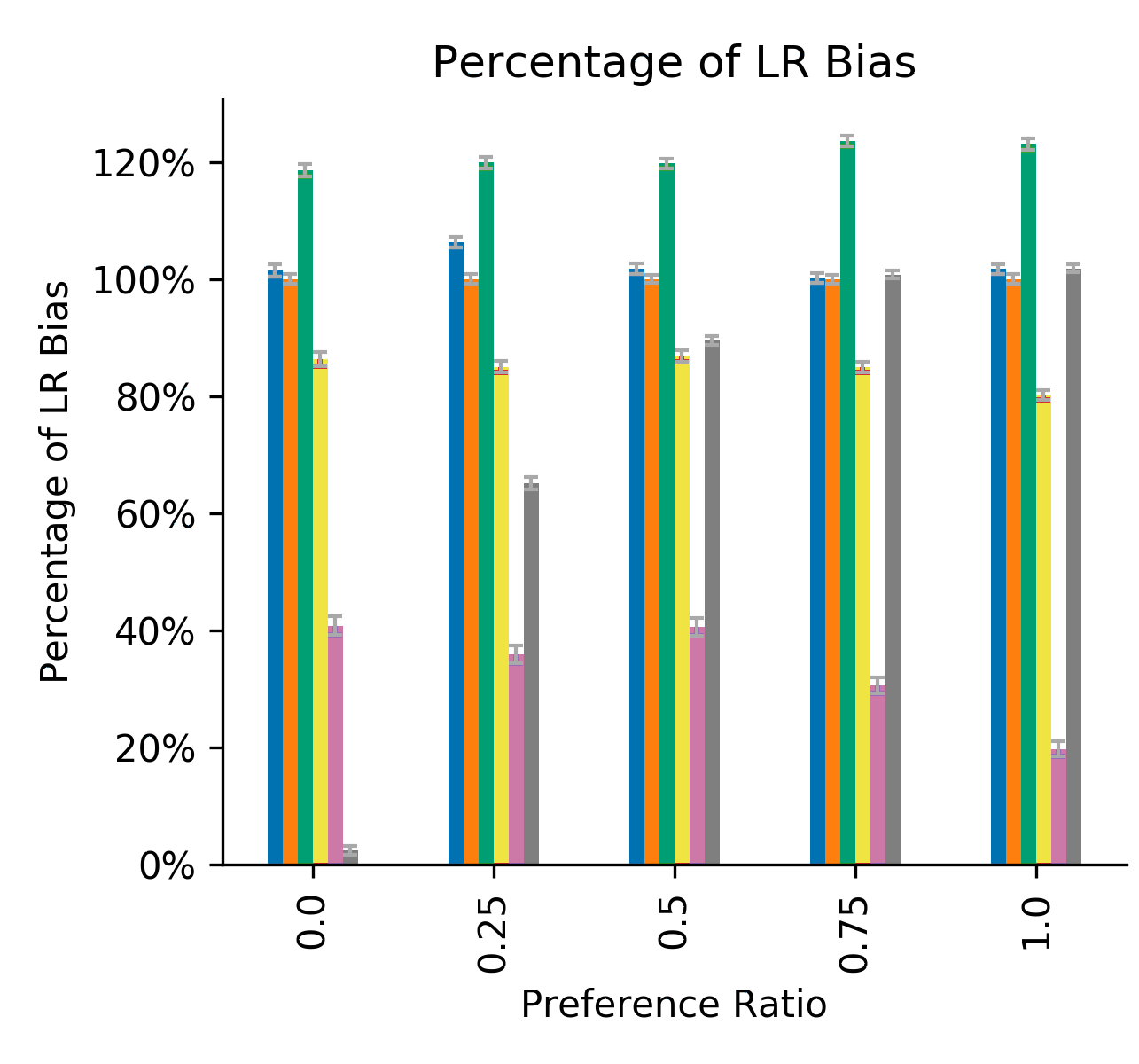

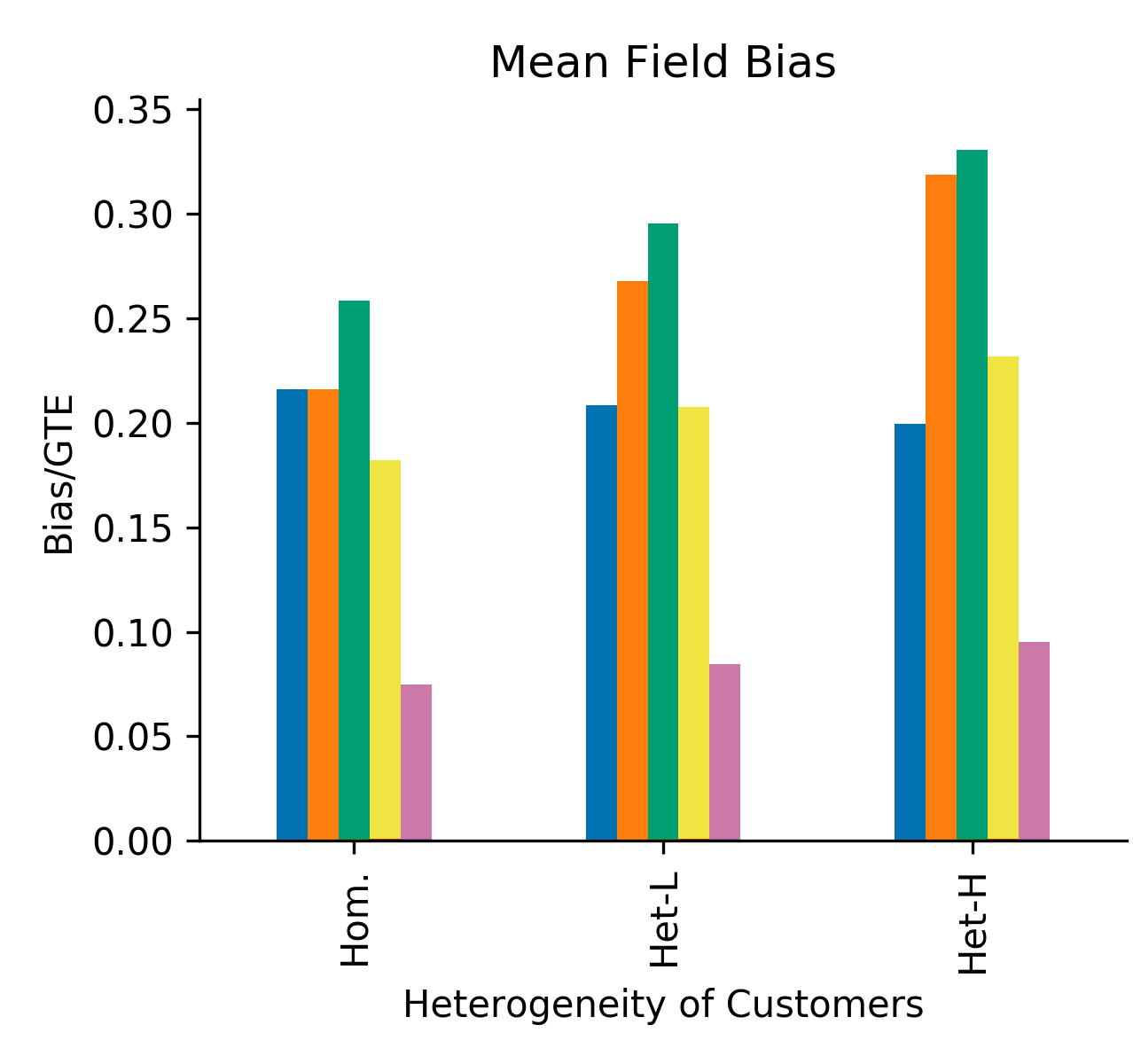

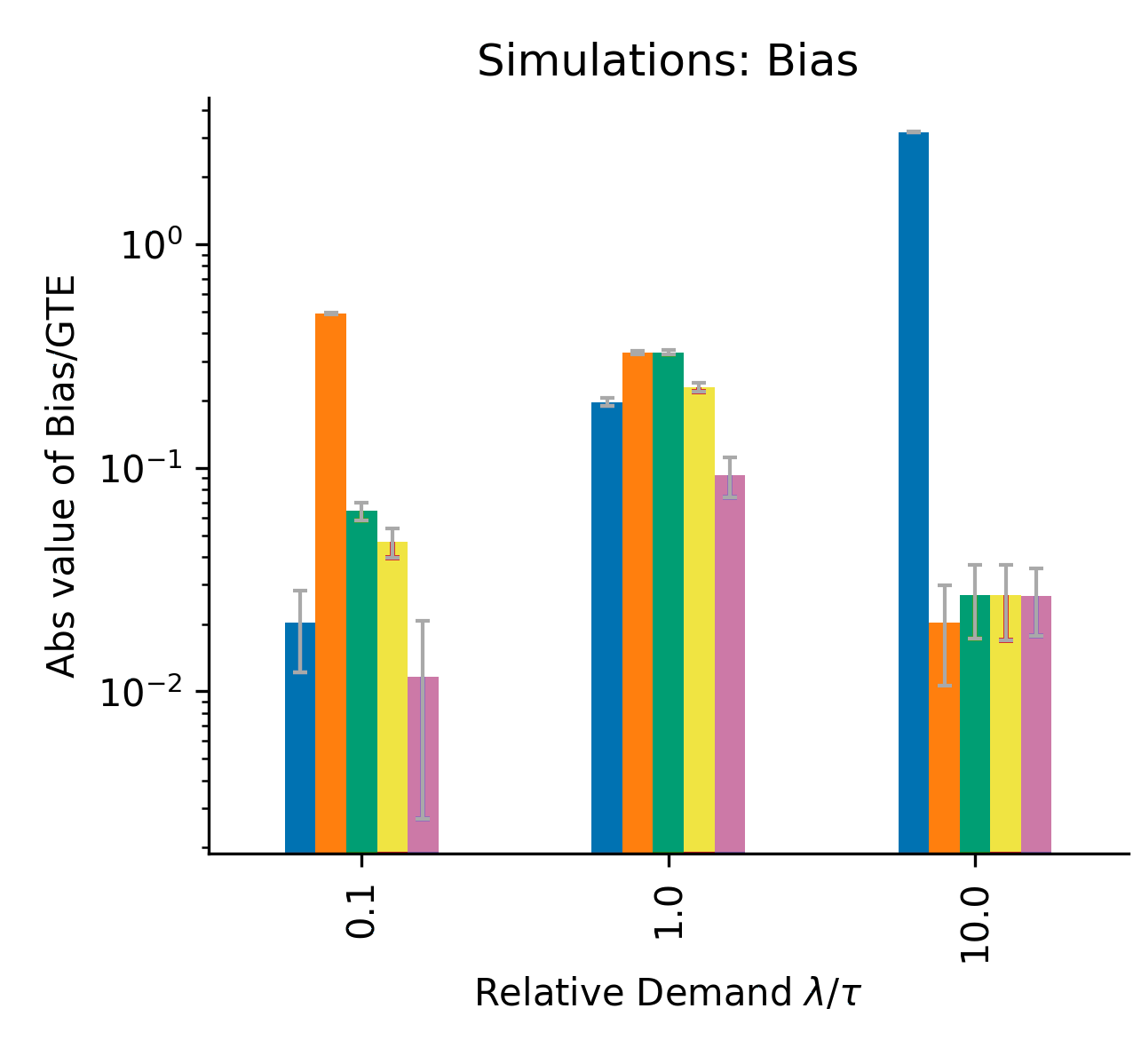

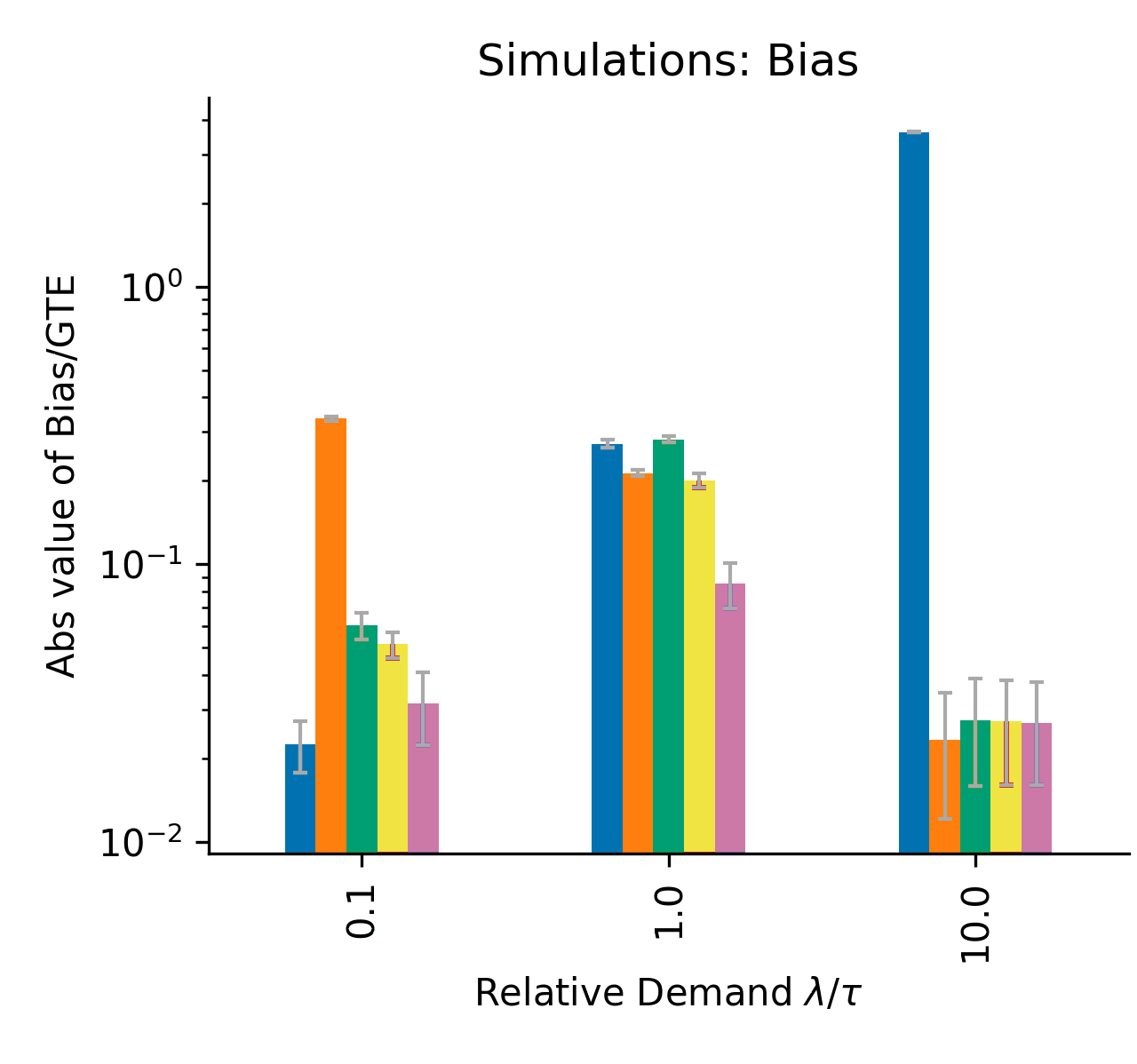

Further, we find through simulations that and overestimate the with positive treatments in intermediate ranges of market balance, for all parameter regimes that we study in the examples in this section (see Figure 3 as well as Appendix 12). We do find in some cases that the estimators underestimate the , and so, since we plot bias on a log scale, we report the absolute value of the bias.

6.2 Discussion: Violation of SUTVA

Our results on the bias of the naive and experiments can be interpreted through the lens of the classical potential outcomes model. An important result from this literature is that when the stable unit treatment value assumption (SUTVA) holds, then naive estimators of the sort we consider will be unbiased for the true treatment effect. SUTVA requires that the treatment condition of units other than a given customer or listing should not influence the potential outcomes of that given customer or listing. The discussion above illustrates that in the limit where , there is no interference across customers in the design; this is why the naive estimator is unbiased. Similarly, in the limit where , there is no interference across listings in the design; this is why the naive estimator is unbiased. On the other hand, the cases where each estimator is biased involve interference across experimental units.

6.3 Estimation with the design

The preceding sections reveal that each of the naive and estimators has its virtues, depending on market balance conditions. In this section, we explore whether we can develop designs and estimators in which and are chosen as a function of , to obtain the beneficial asymptotic performance of the naive estimator in the highly-demand constrained regime, as well as the estimator in the highly supply-constrained regime. We also expect that an appropriate interpolation should yield a bias for that is comparable to, if not lower than, and in intermediate regimes of market balance.

Recall the naive estimator defined in (21), and in particular the steady-state version of this estimator. Suppose the platform observes ; note that this is reasonable from a practical standpoint as this is a measure of market imbalance involving only the overall arrival rate of customers and the average rate at which listings become available. For example, consider the following heuristic choices of and for the design, for some fixed values of and :

| (26) |

Then as , we have and , while as we have and .999Our choice of exponent here is somewhat arbitrary; the same analysis follows even if we replace with for any value of .. With these choices, it follows that in the highly demand-constrained limit (), the estimator becomes equivalent to the naive estimator, while in the highly supply-constrained limit (), the estimator becomes equivalent to the naive estimator. In particular, using Propositions 6.1 and 6.3, it is straightforward to show that the steady-state naive estimator is unbiased in both limits; we state this as the following theorem, and omit the proof.

Corollary 6.6

For each , consider the design with and defined as in (26). Consider a sequence of systems where either , or . Then in either limit:

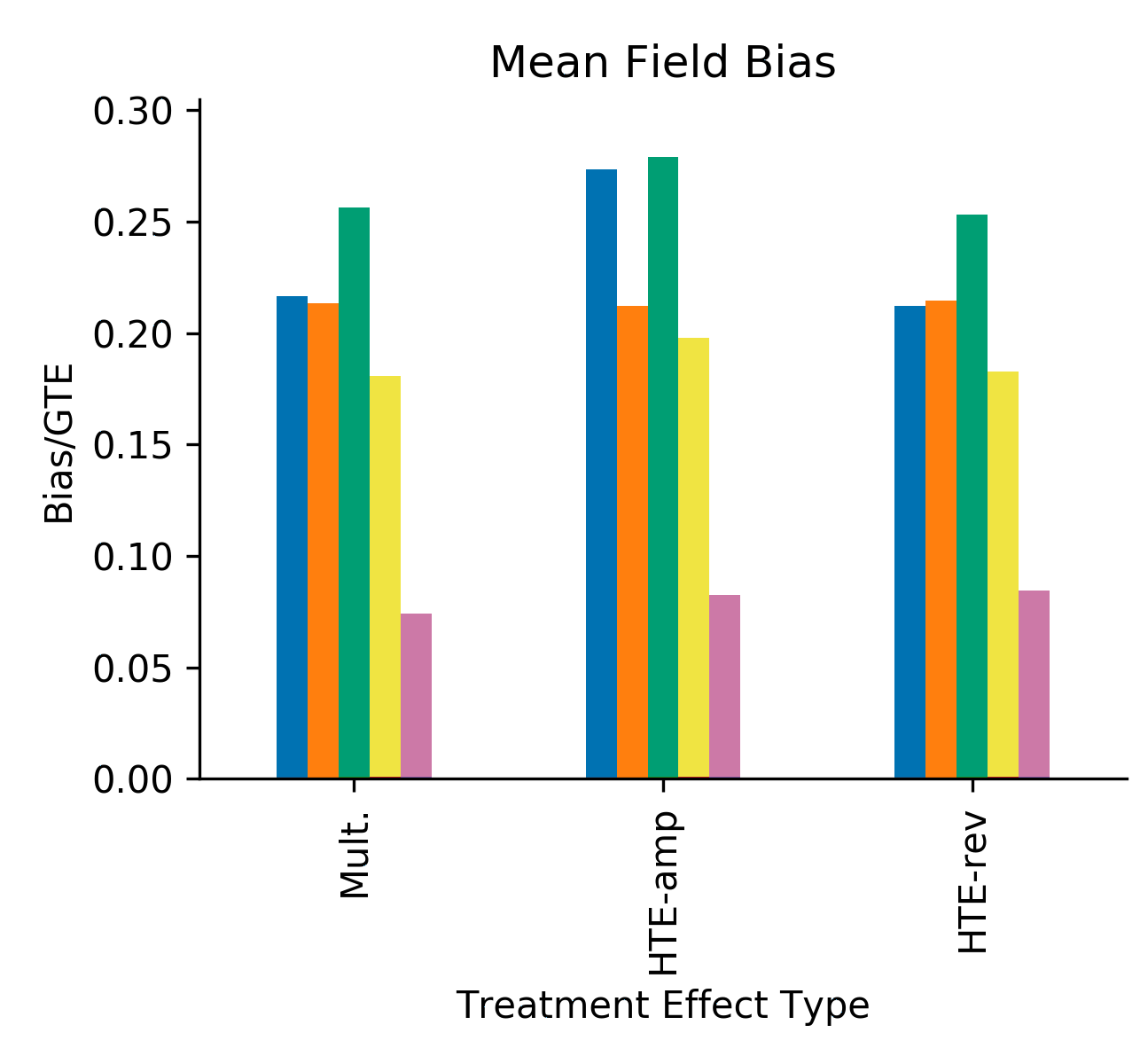

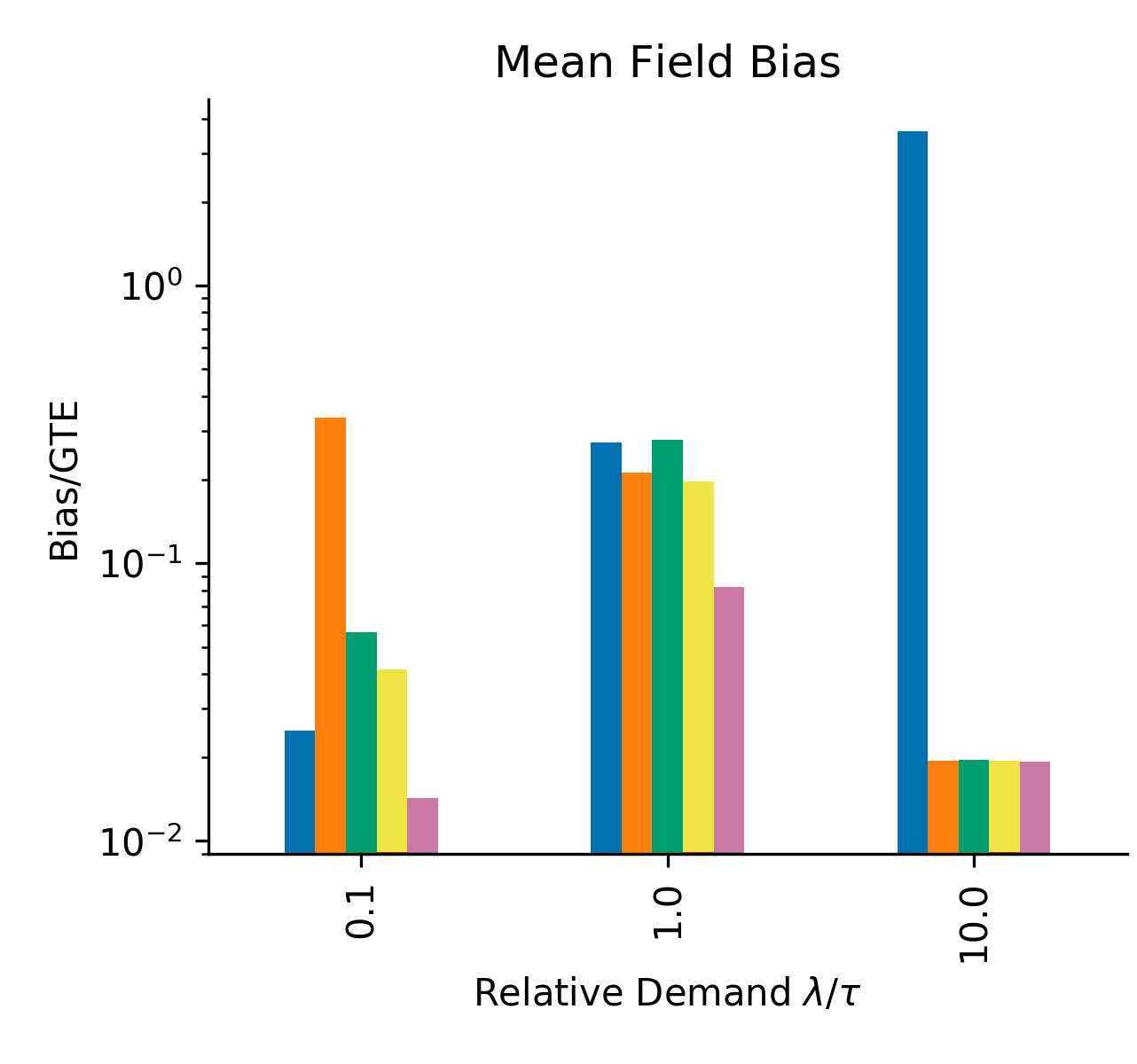

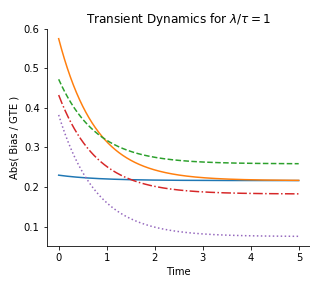

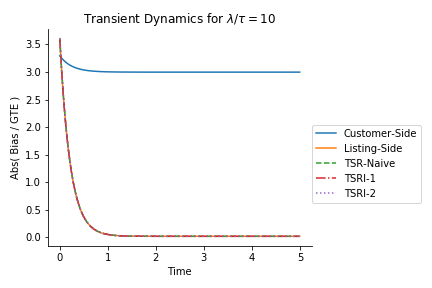

We are also led to ask whether we can improve upon the naive estimator when the market is moderately balanced. Note that the estimator does not explicitly correct for either the fact that there is interference across listings, or the fact that there is interference across customers. We now suggest a heuristic for correcting these effects, which we use to define two improved interpolating estimators; these estimators are the fourth and fifth estimators appearing in Figure 2, which we call “-Improved (1)” and “-Improved (2)”. These effects are visualized in Figure 1.

First, abusing notation, let denote the estimator in (19) using the same terms from a design, and dividing through by on both terms as normalization. Similarly abusing notation, let denote the estimator in (20) using the same terms from a design, and dividing through by on both terms as normalization. Motivated by these naive estimators, we explicitly consider an interpolation between the and estimators of the form:

| (27) | ||||

Now, consider the quantity in a design. This is the (appropriately normalized) difference between the rate at which control customers book control listings, and the rate at which treatment customers book control listings. Note that both treatment and control customers have the same utility for control listings, due to the design, but potentially different utilities for treatment listings. Hence, the difference in steady-state rates of booking among control and treatment customers on control listings must be driven by the fact that treatment customers substitute bookings from control listings to treatment listings (or vice versa). This difference captures the “cannibalization” effect (i.e., interference) that was found in designs in the demand-constrained regime.

Thus motivated, we can think of this difference as a “correction term” for the design from our interpolating estimator in (27). Using a symmetric argument we can also consider an appropriately weighted correction term associated to interference across customers in a design: . (Similar estimates were also studied in Bajari et al. (2019); see the related work for further details on this work.) See Figure 1 for an illustration of these competition effect estimates.

We can weight these correction terms with different factors to control their impact. In addition, we can choose these weights in a market-balance-dependent fashion, based on the direction of market balance in which we have seen that the respective interference grows. Combining these insights, for and we define a class of improved estimators given by:

| (28) |

Given market balance , we set , and we choose and as in (26).

In the limit where , note that approaches as expected. Similarly, in the limit where , approaches . It is straightforward to show that for any is unbiased in both the highly demand-constrained and highly supply-constrained regimes, since the correction terms play no role in the limits.

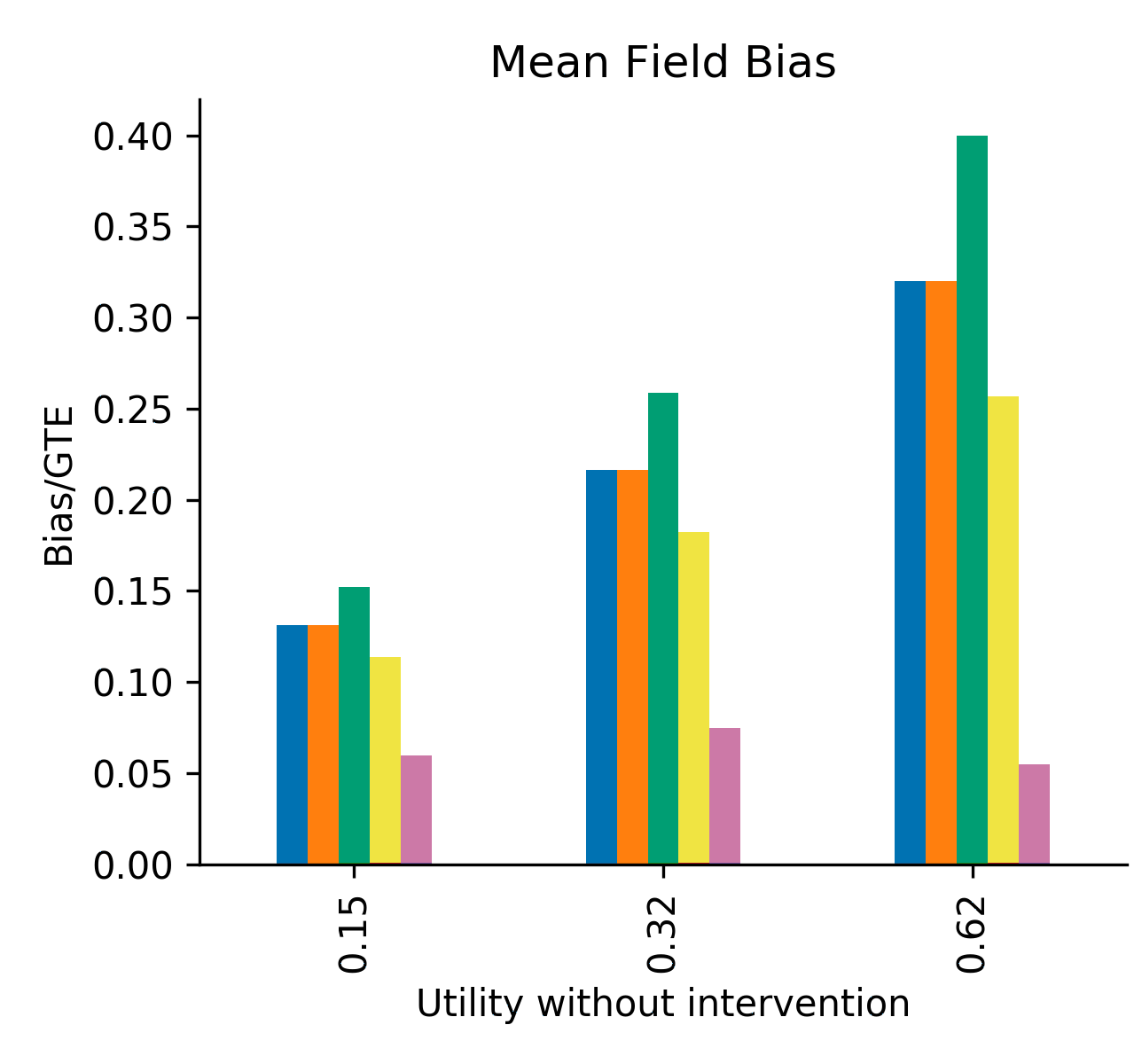

For moderate values of market balance, both the cannibalization correction terms kick in, which lead to improvements over naive as seen in Figure 2. To simplify the exposition, we only consider two factors ; we see that has lower bias than the naive , but , which has a higher weight in front of the correction terms, has a lower bias than both naive and , as well as the naive and estimators. In Appendix 12, we explore the robustness of our results to other model primitives, specifically scenarios with smaller or larger utilities and the introduction of heterogeneity on one or both sides of the market. We find that the bias of and estimators can increase with the introduction of these factors, but remarkably the bias of the estimators remains low across the ranges that we study. We emphasize the fact that the three estimators presented here are examples to illustrate the potential for bias reduction using this new design. There is of course a much broader range of both designs and estimators; some of these may offer even better performance.

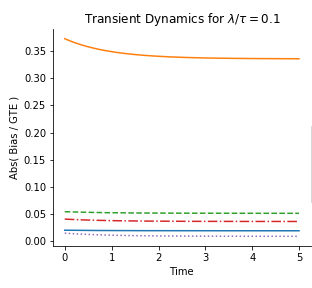

We conclude this section with two additional observations. First, note that all our analysis in this section has been carried out in the mean field steady state; in particular, Figure 2 shows the bias of the estimators in steady state. For practical implementation, it is also important to consider the relative bias in the candidate estimators in the transient system, since experiments are typically run for relatively short time horizons. For discussion of the transient behavior for a finite time horizon, see Appendix 13. Second, in the next section, we discuss variance of the estimators we have studied. There we find that the estimators with the lowest bias also have the highest variance; in other words, there is a bias-variance tradeoff.

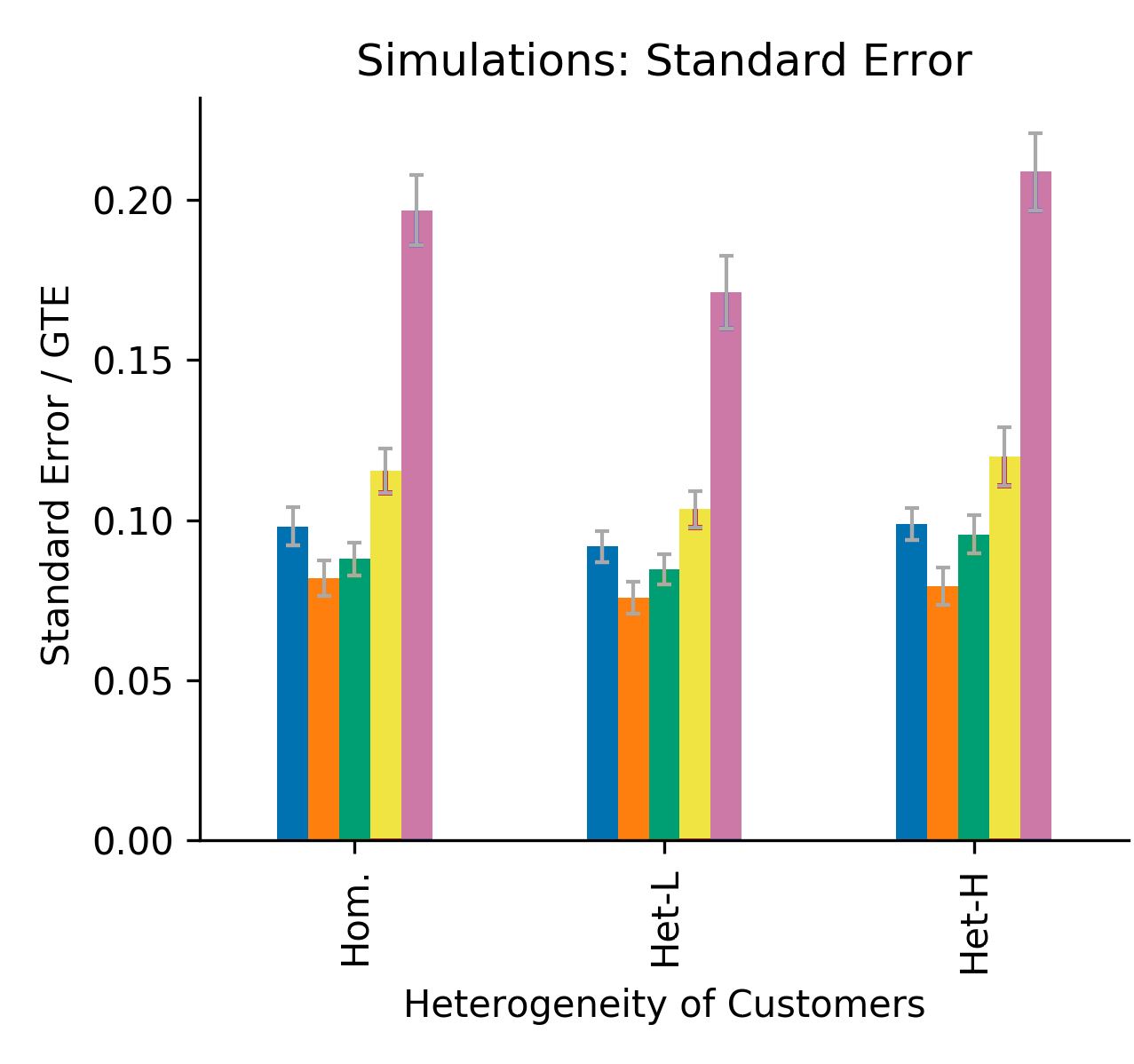

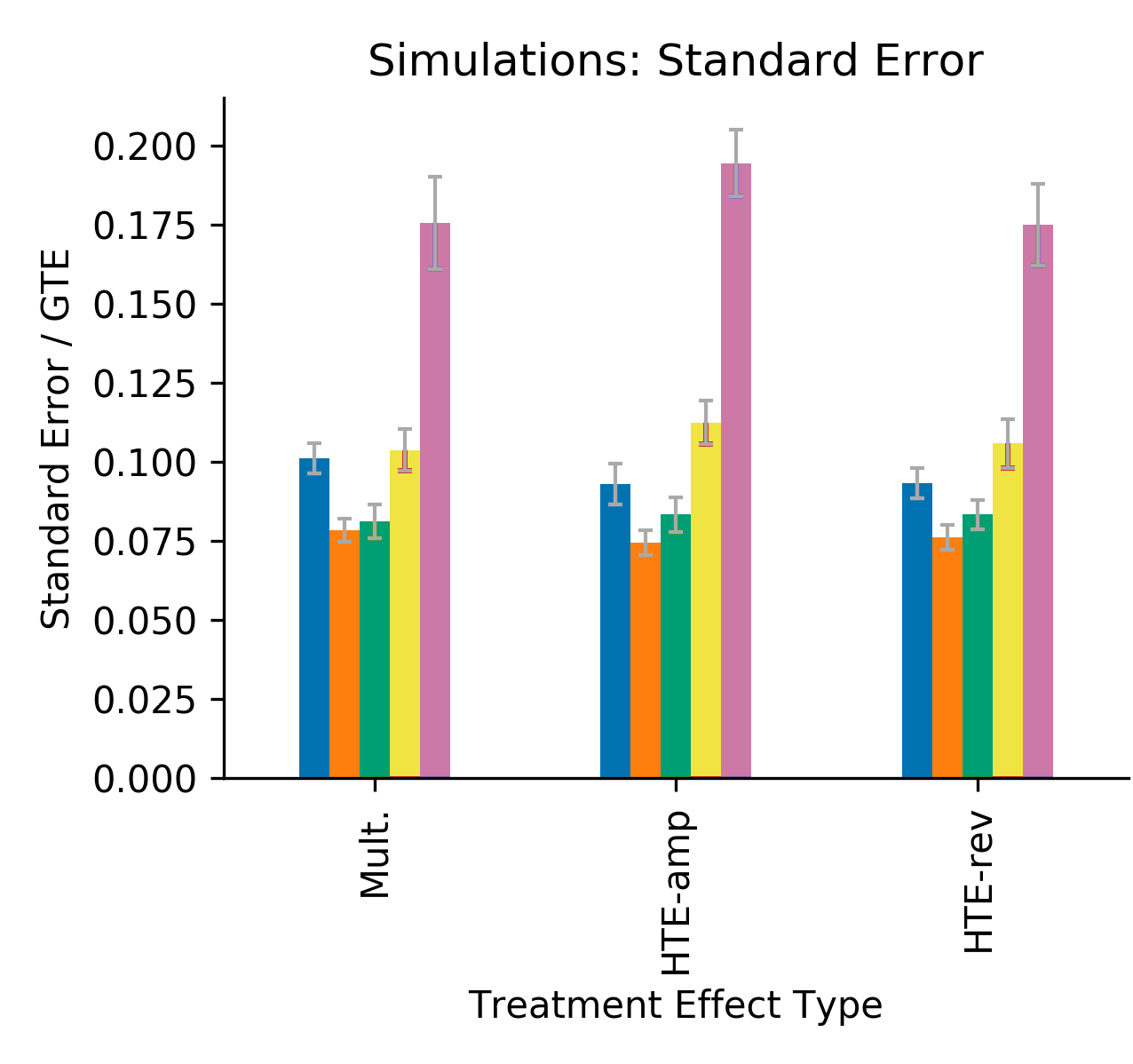

7 Bias-variance tradeoff of estimators

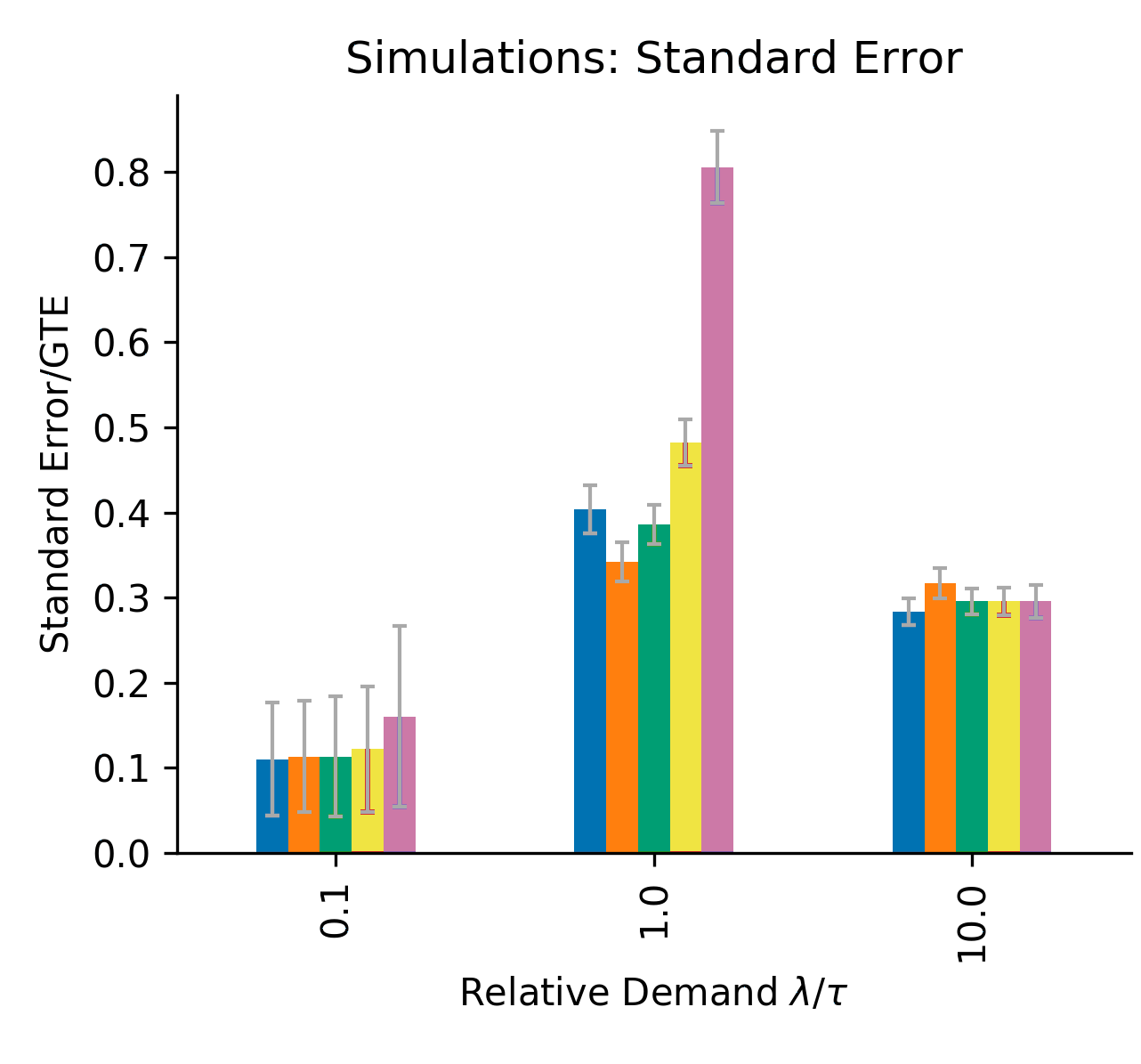

Our mean field model is deterministic, so it does not allow us to study the variance of the different estimators. In practice, however, markets consist of finitely many listings and experiments are run for finite time horizon , and so the variance of any estimator will be nonzero.101010We note that even if the system only consists of a finite number of listings , as the standard error of the various estimators proposed in this paper will converge to zero. However, for finite , this is not the case; since A/B tests are always run to a finite horizon , this nonzero variance will impact the accuracy of any estimates obtained. In particular, the variance of estimators becomes an important consideration alongside bias, particularly in choosing between multiple estimators with similar bias. The variance of the estimators is especially important, given the earlier discussion that many heuristics that platforms use to minimize bias do so at the cost of increased variance, leading to under-powered experiments (see Section 2).

With this background as motivation, in this section we provide a preliminary yet suggestive simulation study of variance. The simulations highlight two important considerations that a platform must take into account when designing and analyzing an experiment. First, similar to the results from Section 6 on bias, we find that the estimator with the lowest variance depends on market balance. Second, we see a bias-variance tradeoff between the , and estimators, with the estimators offering bias improvements at the cost of an increase in variance. We emphasize the point that whether a platform should care more about bias or variance depends on the size of the platform (number of listings ) and the time horizon on which the experiment is run. The bias of the experiment is relatively unaffected by changes in these two factors, but of course variance decreases in the size of the market and the length of the time horizon. Thus these two factors dictate whether bias or variance contribute more to the overall .

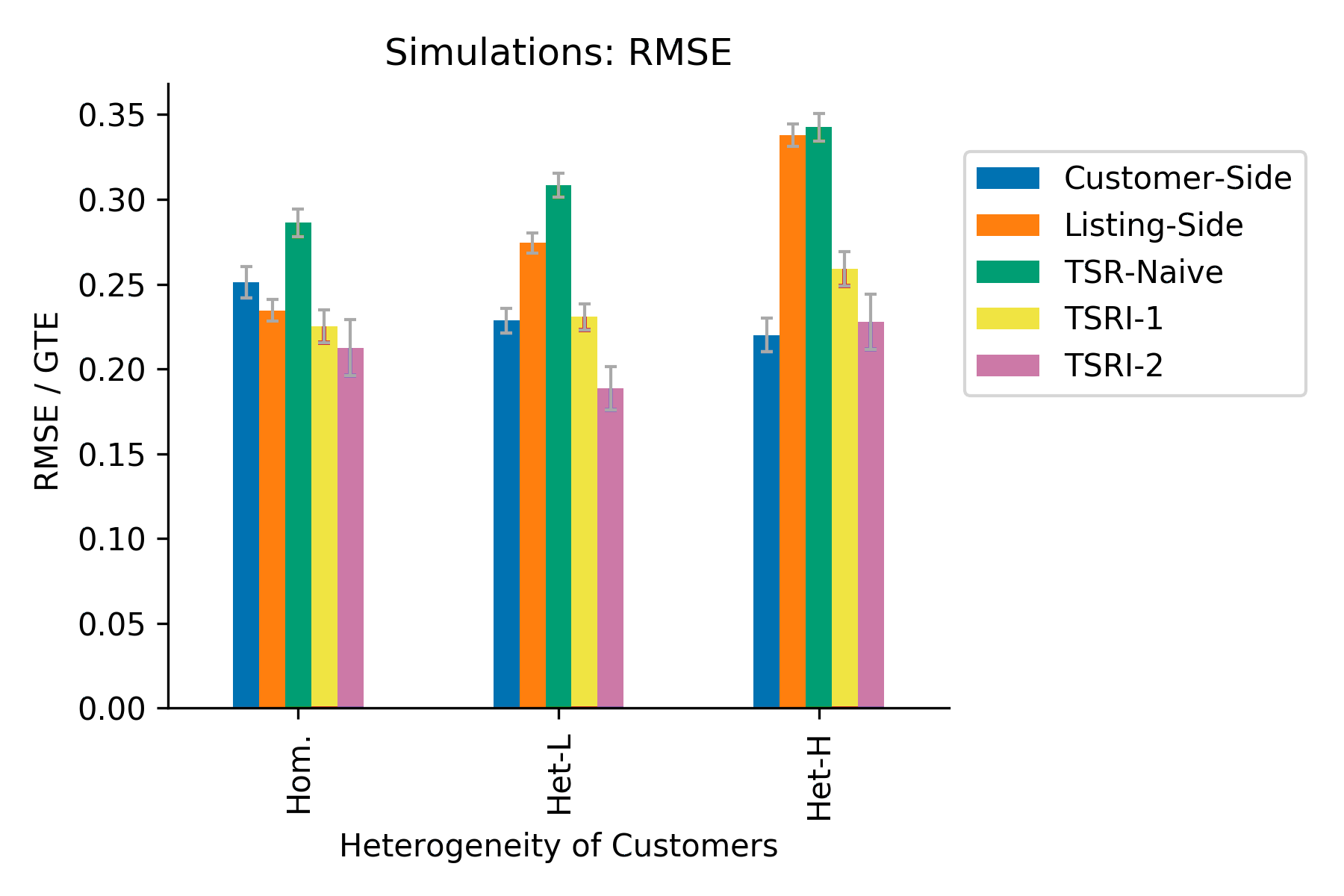

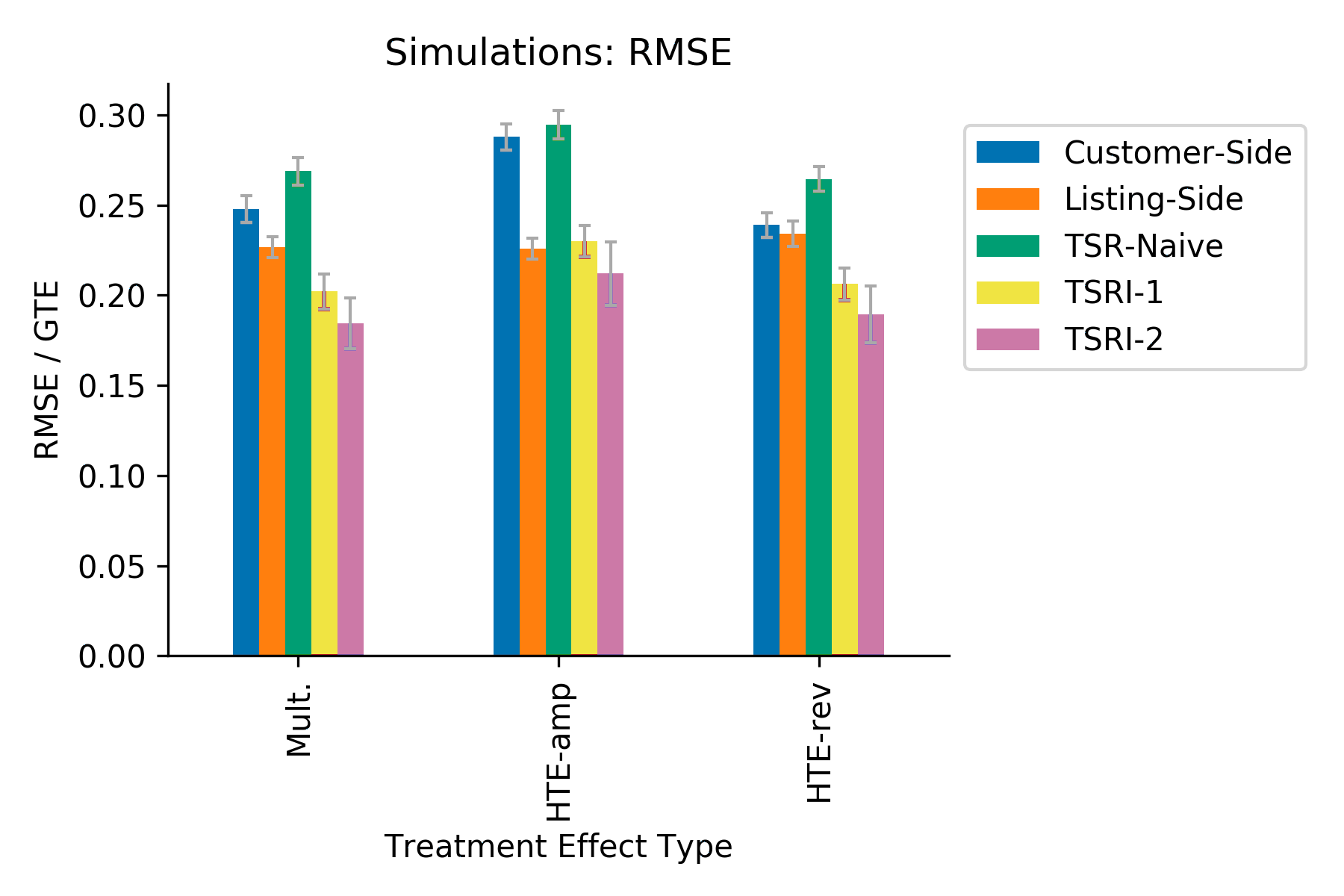

Full details of the simulation environment and parameters are in Appendix 12, which we briefly summarize here. We simulate marketplace experiments with varying market parameters for a finite system with a number of listings and fixed time horizon . For each run of the simulation, we fix an experiment design (e.g., , , ) and simulate customer arrivals and booking decisions until time . System evolution is simulated according to the continuous time Markov chain specified in (3)-(5). We calculate the estimator corresponding to the experiment design, defined in (19)-(21) and (28) (for ) for the time interval , where is chosen to eliminate the transient burn-in period. We then simulate multiple runs and compare the bias and standard error of the estimators across runs. Note that we report the true standard errors, calculated across simulation runs. For discussion on the estimation of standard errors, see Section 9.

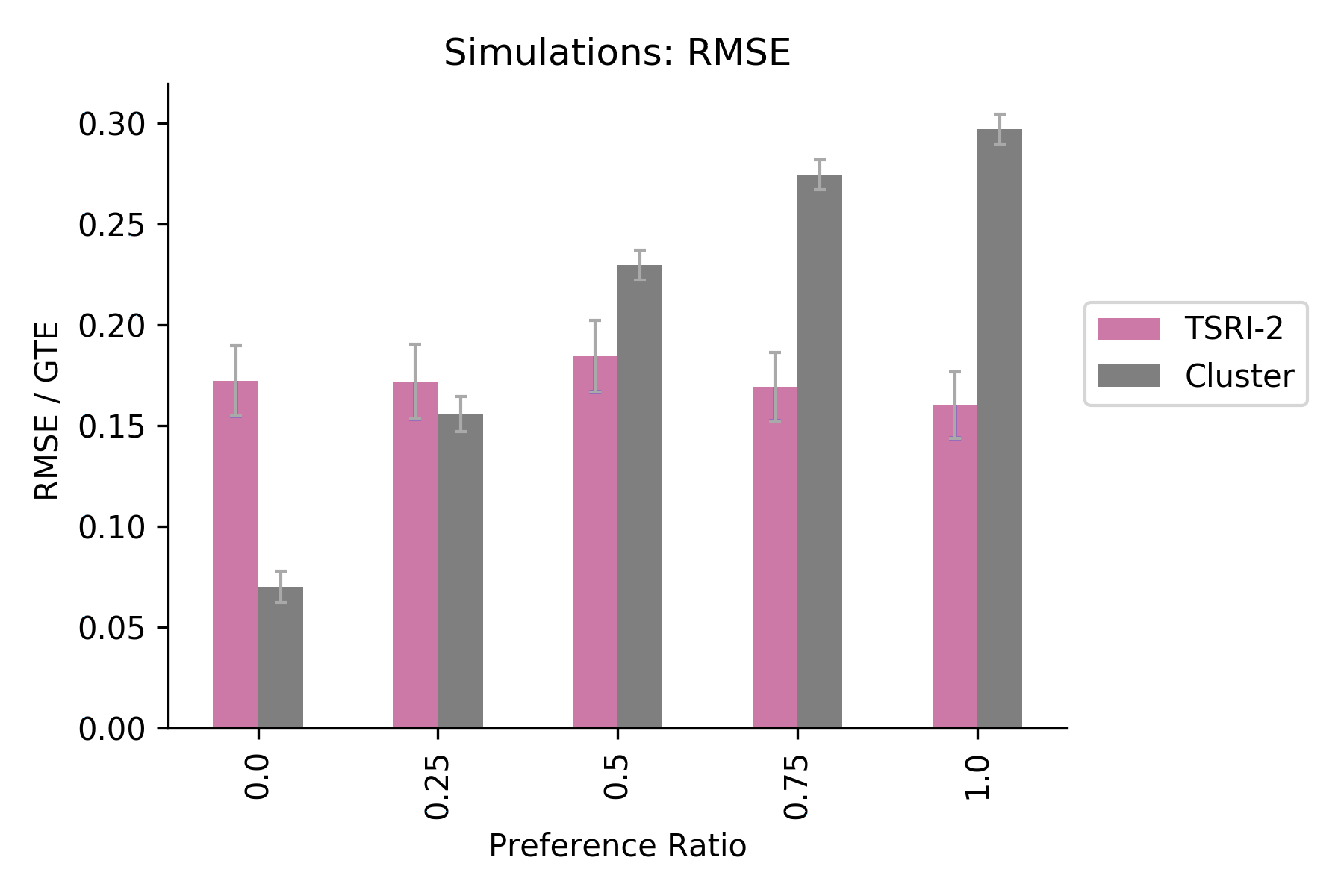

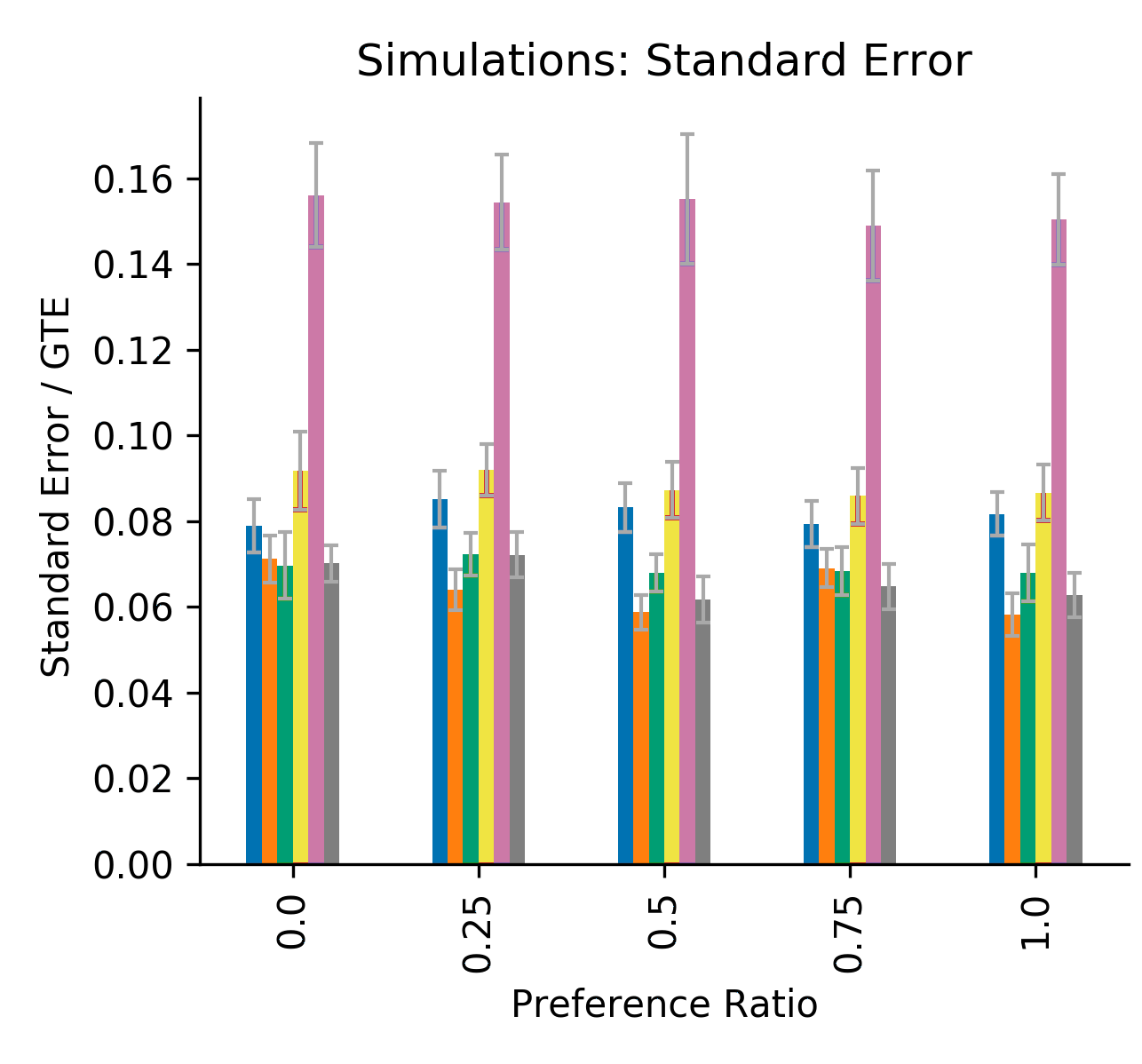

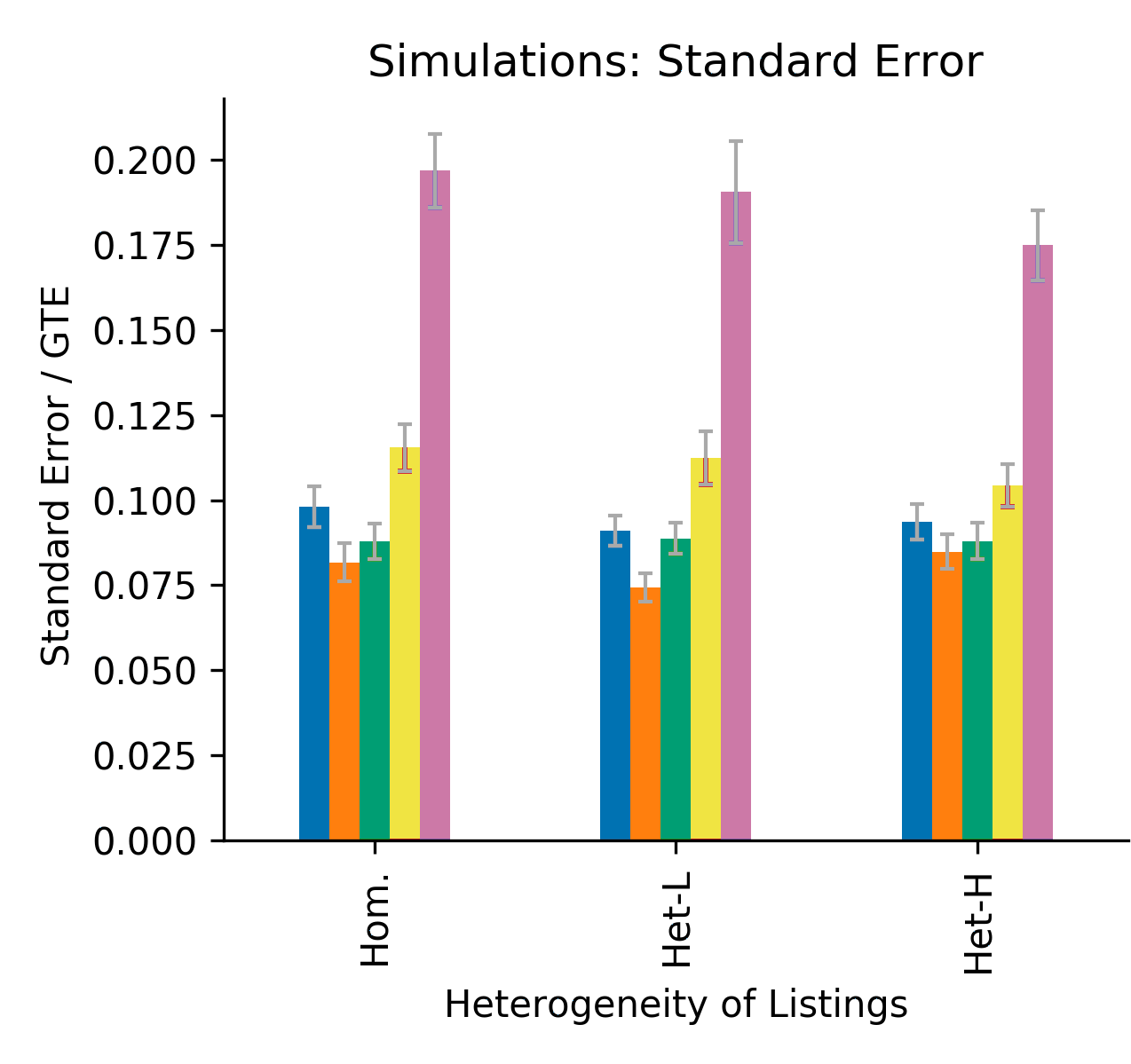

Figure 3 shows simulations for a homogeneous system with only one customer and one listing type, with the same parameters as the mean field numerics presented in Figure 2. Note that the bias of the estimators in these large market simulations echo the qualitative insights about bias obtained from the mean field model. Similar findings are obtained in more general scenarios, cf. Appendix 12, where we investigate the effect of heterogeneity in the marketplace.

These simulations point to a bias variance-tradeoff between estimators and the naive and estimators, as well as between the three estimators themselves. The estimators, as discussed earlier, offer benefits over the naive and estimators with respect to bias, but they do so at the cost of an increase in variance. Moreover, among the three estimators that we explore, those with lower bias also have higher variance. The naive estimator has similar variance with the lowest of and , but the bias of this estimator is also similar to the lowest bias of and . On the other hand, shows a substantial improvement in bias over both and for several market conditions, but this estimator also has the largest variance among all five estimators, especially in the regime of intermediate market balance (cf. Appendix 12).

Further, the minimum variance estimator depends on market conditions. For example, in a demand-constrained market with , has the lowest standard error, whereas in a supply-constrained market with , has the highest standard error.

We conclude this section by highlighting the potential for the class of experiments, which open up a large class of both designs and estimators. Among the three estimators we explore, we see that there is a estimator with low bias and another estimator with low variance. It is possible that, with further optimization of these designs and estimators, one can devise a new estimator that optimizes this bias-variance tradeoff.

8 Comparison with cluster-randomized experiments

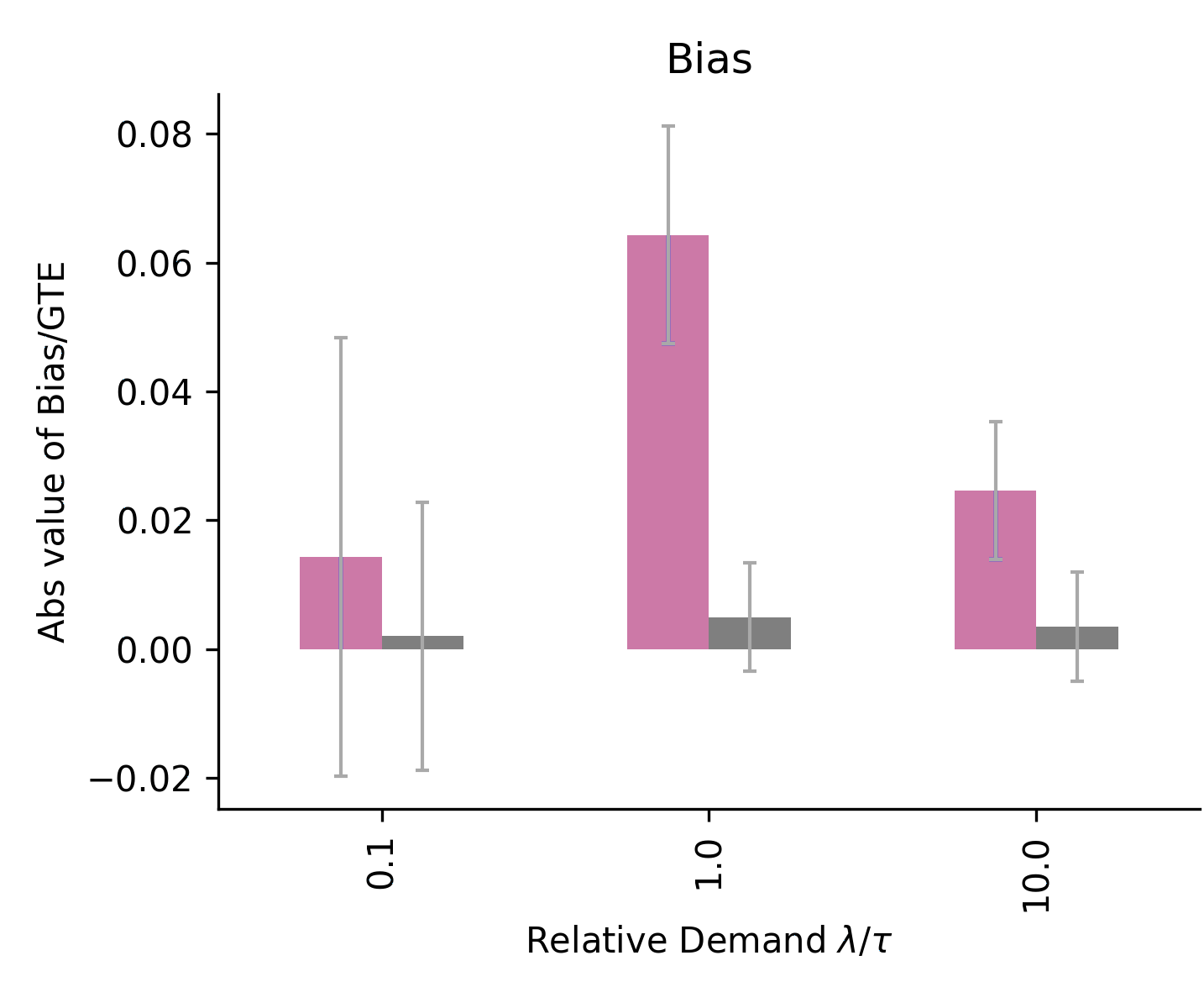

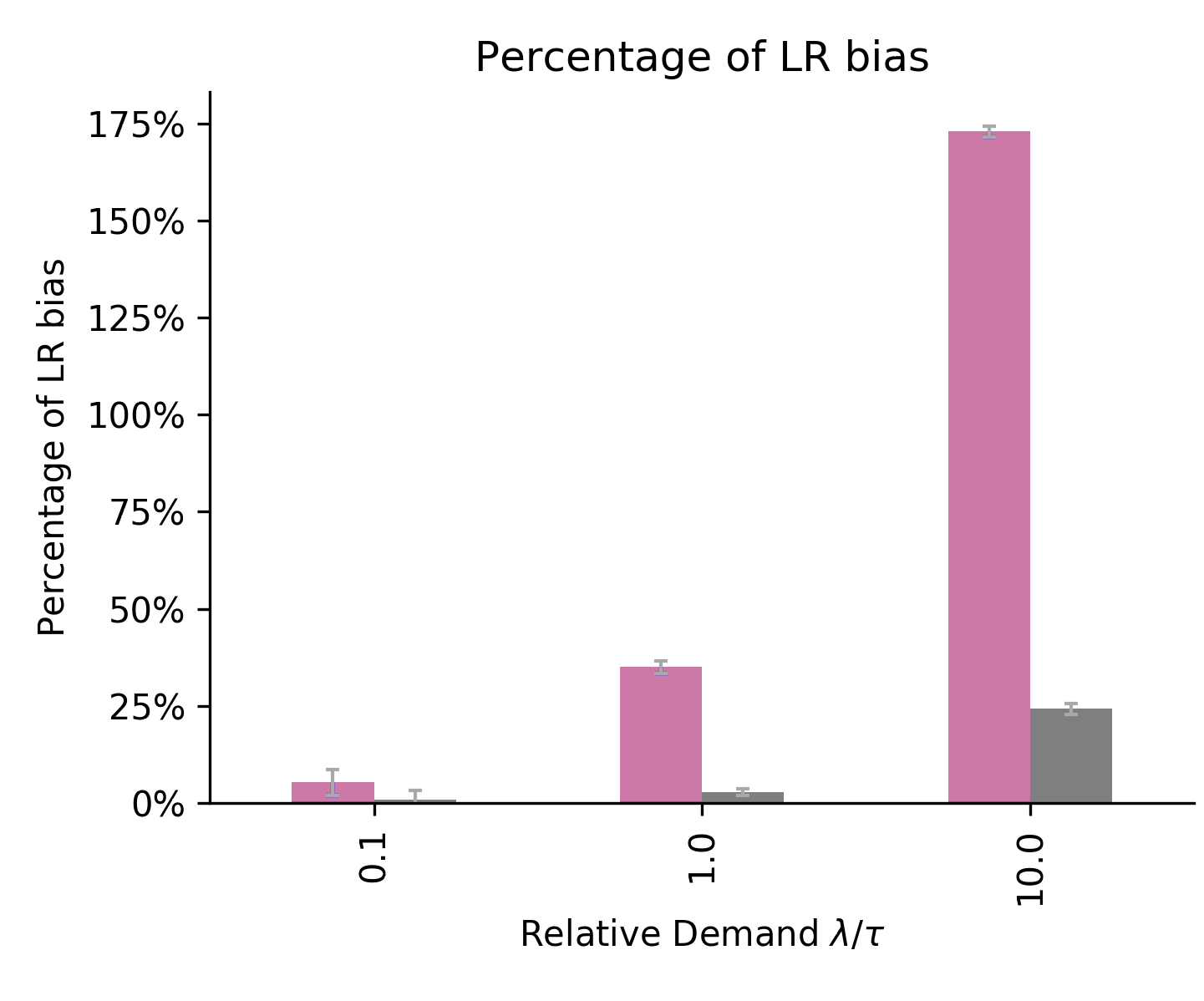

In this section we compare the approach to existing approaches to reduce bias in marketplace experiments. One such approach is to run a cluster-randomized experiment, which changes the unit of randomization in order to reduce interference effects across units. The typical approach is to divide the marketplace into clusters, such as geographical regions, such that there is less interaction of market participants across different clusters. All participants within a cluster receive the same treatment condition. The platform then estimates the by comparing the outcomes within the treatment clusters versus the outcomes in the control clusters. It is important to note that many markets and social networks are highly connected and it is not possible to avoid all interference across clusters; see, e.g., Holtz et al. (2020) for an example in the context of Airbnb. Thus cluster-randomized experiments will reduce but not fully remove the bias.

To compare the performance of the cluster-randomized and approaches, we use our existing model to define a regime that gives the best-case performance for cluster-randomized experiments, where there are tightly clustered preferences in the marketplace and the platform knows ex-ante the true clusters (without having to learn them).

The simulations suggest that cluster-randomized estimators offer substantial bias reductions over when the market is tightly clustered, but these improvements diminish if the market becomes more interconnected. The estimators, however, offer bias reductions in both clustered and interconnected markets and, in interconnected markets, are less biased than the cluster-randomized estimator. In our simulations, the variance of the cluster-randomized estimator is lower than that of in our example, although the variance of the cluster-randomized estimator will likely change if we deviate from this best-case scenario with perfect knowledge of the clusters, identical listings within clusters, and uniform treatment effects across different clusters. Hence, while our model for market clusters is stylized, we believe our results suggest that designs can be a useful alternative to cluster-randomized experiments in interconnected markets.

8.1 Market setup for cluster randomization

We consider the case where clusters are defined on the listing side, so that the cluster-randomized experiment is expected to improve upon a listing-randomized experiment.111111Because we analyze a model where customers are short-lived while listings remain on the platform, it is likely that the platform has more information on the listings, and is better able to learn clusters on the listing side. To induce a clustered structure, we model a setting with two customer types and two listing types, where each type of customer prefers a different type of listing. Formally, there are customer types and listing types . All customers consider all listings ( for all ) but customers have different utilities for different listings.121212Alternatively, we can induce a clustered structure by modifying the consideration probabilities . Both approaches of modifying the and modifying the are equivalent in the mean field model. The global control utilities have the following form:

where . Note that if , then the market can be perfectly decomposed into two sub-markets, where customers of type (resp., ) only book listings of type (resp., ). If , then each customer prefers both listings equally. Thus we can interpret the ratio as a measure of how equally a customer prefers both products, where intuitively the market is tightly clustered when is small. We call the preference ratio.

The platform then runs a cluster randomized experiment where it first assigns listings to clusters and then randomizes entire clusters to either treatment or control. In practice, the platform must learn how to create the clusters, likely through observational data in the global control setting,131313See Holtz et al. (2020) in the context of marketplaces and Ugander et al. (2013) in the context of social networks. but in these simulations, we assume that the platform observes the cluster structure perfectly. The platform assigns all listings to one cluster and listings to another, and runs a completely randomized design on the clusters, assigning one of the clusters to treatment and one to control. For simplicity, assume that the intervention has a multiplicative lift on all customer-listing pairs, so that the treatment utilities satisfy .

The cluster-randomized estimator , with clusters defined on the listing side, compares the (scaled) rate of bookings of listings in treatment clusters to the rate of bookings of listings in control clusters. Formally, in the mean field setting, once the clusters are randomized, let denote the mass of listings assigned to a treatment cluster. Then

| (29) |