Dating the Break in High-dimensional Data

Abstract

This paper is concerned with estimation and inference for the location of a change point in the mean of independent high-dimensional data. Our change point location estimator maximizes a new U-statistic based objective function, and its convergence rate and asymptotic distribution after suitable centering and normalization are obtained under mild assumptions. Our estimator turns out to have better efficiency as compared to the least squares based counterpart in the literature. Based on the asymptotic theory, we construct a confidence interval by plugging in consistent estimates of several quantities in the normalization. We also provide a bootstrap-based confidence interval and state its asymptotic validity under suitable conditions. Through simulation studies, we demonstrate favorable finite sample performance of the new change point location estimator as compared to its least squares based counterpart, and our bootstrap-based confidence intervals, as compared to several existing competitors. The asymptotic theory based on high-dimensional U-statistic is substantially different from those developed in the literature and is of independent interest.

keywords:

[class=MSC]keywords:

, and

t1Runmin Wang is Ph.D. Candidate and Xiaofeng Shao is Professor, Department of Statistics, University of Illinois at Urbana-Champaign, Champaign, IL 61820 (e-mail: rwang52, xshao@illinois.edu).

1 Introduction

Advances in science and technology have led to an explosion of data of high dimension. Examples of high-dimensional data include fMRI imaging data in neuroscience, genomic data in biological science, panel time series data from economics and finance, and spatio-temporal data from climate science, among others. Often statisticians assume some kind of homogeneity assumptions in analyzing such data, such as i.i.d. (independent and identically distributed) or stationarity with weak serial dependence for a sequence of high-dimensional data. The validity of methodology they develop can be sensitive with respect to such assumptions. In this paper, we shall focus on a particular type of non-homogeneity, a change point in the mean of an otherwise i.i.d. sequence of high-dimensional data. That is, we assume that our observed data follows the one-change point model,

where are i.i.d. -dimensional data with zero mean, and . In this model, both parameters and where , are unknown. Our main goal is to provide a new estimator of break point and a confidence interval, which works in the high-dimensional setting that allows and also dependence within components. To achieve this, we develop a new -statistic based objective function and propose to use its maximizer as our location estimator. Under some mild assumptions, this new estimator is shown to be consistent with suitable convergence rate and asymptotic distribution upon centering and normalization. It is also shown to be superior to the least squares based counterpart in Bai, (2010) and Bhattacharjee et al., (2019), for some specific models of interest. Furthermore, we provide a bootstrap-based confidence interval that can be adaptive to the magnitude of change, theoretically justified and works well in finite sample.

The literature on change point testing and estimation for high-dimensional data has been growing at a fast pace lately, as stimulated by the practical needs of analyzing high-dimensional data with change points. From the viewpoint of mathematical statistics, the high dimensionality can bring substantial methodological and theoretical challenges, as many classical estimation and testing procedures developed for low-dimensional data may not work in the high-dimensional setting. This also brings interesting opportunities to the mathematical statistics community, as there is a great need to develop new estimation and testing methods that can accommodate high dimensionality and dependence within components and over time. As there is a vast literature on retrospective change point testing and estimation in the low-dimensional setting, we refer the readers to several excellent review papers and books, see e.g., Csörgő and Horváth, (1997), Perron, (2006), and Aue and Horváth, (2013) for many references.

Below we shall provide a brief review of the more recent literature on high-dimensional change point inference. For testing a change point in the mean of high-dimensional data, Horváth and Hušková, (2012) considered an aggregation of one-dimensional CUSUM statistics, which targets at dense alternative. For a sequence of Gaussian vectors, Enikeeva and Harchaoui, (2019) proposed a new test to detect the presence of a change point in mean and established the detection boundary in different regimes that allow the dimension to approach the infinity. Their test was formed on the basis of a combination of a linear statistic and a scan statistic, which can capture both sparse and dense alternatives, but their critical values were obtained under strong Gaussian and independent components assumptions. Cho and Fryzlewicz, (2015) proposed a sparse binary segmentation algorithm for detecting multiple change points in the second order structure of a high-dimensional time series, by aggregating the low-dimensional CUSUM statistics that pass a certain threshold. Cho, (2016) developed a double CUSUM statistic that can be viewed as an interesting extension of the ideas in Enikeeva and Harchaoui, (2019) and Cho and Fryzlewicz, (2015), and her test was shown to be consistent in estimating the change points with binary segmentation allowing for dependence over time and across cross-sections. Jirak, (2015) considered an aggregation of CUSUM statistics, which aims for sparse alternatives. The “INSPECT” method proposed in Wang and Samworth, (2018) was based on sparse projection method for a single change point and it has been extended to multiple change point estimation by combining with the wild binary segmentation [Fryzlewicz, (2014)]. Wang et al., (2019) proposed a U-statistic based approach to test for change points in independent high-dimensional data via self-normalization, as an extension of Shao and Zhang, (2010), and also provided an segmentation algorithm by using the wild binary segmentation. Chen et al., (2019) proposed an based statistic to test for change points in trends for high-dimensional time series with a consistent estimator of the long-run covariance matrix. Also see Yu and Chen, (2017) for another based test for one change point alternative in mean.

For the estimation and confidence interval construction of the break point (or ), there have been many papers written on this topic when the dimension is low and fixed; see early work by Hinkley, (1970), Hinkley, (1972), Picard, (1985), Bhattacharya, (1987), Yao, (1987) and Bai, (1994), among others. There have been extensions to the change point problems in linear regression and multivariate time series; see Bai, 1997b , Bai and Perron, (1998) and Bai et al., (1998), but all these works focused on the low-dimensional case. Relatively little is done in the high-dimensional setting. Bai, (2010) considered a least square estimator for the change point location in the panel data with independent cross section units and weak dependence over time, and obtained the asymptotic distribution of break date estimator. Recently Bhattacharjee et al., (2019) extended the least squares method in Bai, (2010) to high-dimensional time series and their setting allowed for both cross-sectional and serial dependence. Bai, (2010), Bhattacharjee et al., (2019) and Chen et al., (2019) provided an asymptotic distribution for the suitable centered and normalized break date estimator and constructed a confidence interval for the break date. Since both Bai, (2010) and Bhattacharjee et al., (2019) tackled the one-change point model, we shall provide a detailed comparison with these two papers in theory and numerical simulations later. It is worth noting that the temporal independence assumption is often assumed in change point analysis for genomic data; see Zhang et al., (2010), Jeng et al., (2010) and Zhang and Siegmund, (2012) among others.

A word on notations. For a vector , is the Euclidean norm. For a matrix , denote and as the spectral norm and the Frobenious norm respectively, and denote as the trace of . Define as the floor function. We use to represent the joint cumulants of random variables . Throughout the paper, all asymptotic results are stated under the regime .

The rest of the article is organized as follows. Section 2 presents a new method to estimate based on the U-statistic, and contains all the asymptotic results. Section 3 introduces several methods of constructing confidence intervals for , including a bootstrap-based method and its theoretical justification. Section 4 gathers all simulation results. Section 5 concludes and mentions a few future research topics. All technical proofs are relegated to Sections 6 and 7.

2 Estimation Method and Asymptotic Theory

Under the one-change point model CP1: for , where are -dimensional i.i.d. random vectors with mean and variance matrix . Here we follow the convention in the change point literature and denote the true unknown location of the change point as , , i.e., is a fixed positive fraction of the sample size . Without loss of generality, assume as our estimation method is invariant to the value of . For notational convenience, we shall not use the double-array notation , , etc.

Consider the statistic such that for all ,

We define

as the estimate of the change point location (or break date) . This is a natural estimator since achieves its maximum when is the true change point location, as shown in the lemma below. We define as the estimate of the relative position . Let , which is the rate of convergence for to be shown later.

Lemma 2.1.

when and when . Hence achieves its maximum at .

In Bai, (2010), the location of change point is estimated by minimizing a least squares criterion, that is

| (2.1) |

where is the sample average based on the subsample , for any . The least squares method is natural in the low-dimensional setting; see Bai, (1994), Bai, 1997a , Bai and Perron, (1998), among others in either one break or multiple break model with or without covariates.

In the high-dimensional setting, the use of U-statistic was first initiated by Chen and Qin, (2010) in the two sample testing for the equality of means. Recently, Wang et al., (2019) extended the U-statistic based approach to high-dimensional change point testing, coupled with the idea of self-normalization [Shao, (2010), Shao and Zhang, (2010), Shao, (2015)]. In this paper, we further advance the U-statistic based approach to the estimation of change point location in the one change-point model, and our proof techniques are substantially different from that in Bai, (2010) and Bhattacharjee et al., (2019) due to the use of a different objective function, and also very different from that in Wang et al., (2019) due to the focus on the asymptotic behavior of the estimator. We shall compare the performance of our location estimator with the least squares based counterpart in theory and simulations later.

To investigate the asymptotic properties of our location estimator , we introduce the following assumptions.

Assumption 2.2.

-

(a)

.

-

(b)

There exists a positive constant independent of such that

for .

-

(c)

.

-

(d)

and .

Remark 2.3 (Discussion of Assumptions).

Assumption 2.2(a) and 2.2(b) are identical to the assumptions used in Wang et al., (2019), where a U-statistic based approach was developed for change point testing in the high-dimensional setting. These assumptions essentially impose weak dependence among the components, which can be verified for AR type correlation or models with banded componentwise dependence, but are violated when the variance-covariance matrix is compound symmetric; see detailed discussion in Remark 3.2 of Wang et al., (2019).

Assumption 2.2(c) guarantees the change point signal dominates the noise in the U-statistic and it is equivalent to . In the special case , it is reduced to . Assumption 2.2(d) defines the particular regime we are considering. Note that when , the U-statistic based test developed in Wang et al., (2019) delivers trivial power asymptotically; see Theorem 3.5 therein. This suggests that the restriction is almost necessary in order for to be consistently estimated; see Theorem 2.4 below. The condition represents a particular regime under which a meaningful asymptotic distribution for the suitably centered and normalized location estimator can be obtained. In the case that , Assumption 2.2(d) is equivalent to and We offer more discussions about what happens in other regimes later; see Theorem 2.8.

Theorem 2.4 (Rate of Convergence).

Suppose that Assumptions 2.2 hold. Then for any , there exists , such that for large enough ,

where .

Theorem 2.4 implies that is a rate- consistent estimator for . Following the conventional argument in studying the limiting behavior of -estimator [Van der Vaart and Wellner, (1996)], we reparametrize and define . Then

where

To proceed, we define

as an analog of . Let denote the set of essentially bounded measurable functions on .

Theorem 2.5.

Theorem 2.5 gives a process convergence result for the properly normalized increment of the process around the true change point in a shrinking neighborhood. By directly applying argmax continuous mapping theorem [Theorem 3.2.2, Van der Vaart and Wellner, (1996)], we can get the following corollary.

Corollary 2.6 (Asymptotic Distribution).

Remark 2.7 (Discussion of ).

In fact, the distribution of has been well studied in the literature. According to Proposition 1 in Stryhn, (1996), the probability density function of , denoted as , is

where is the cumulative distribution function of a standard normal random variable. It is straightforward to see that is symmetric, i.e. , for all , and the densities of and are identical. Furthermore achieves its unique maximum at and . In addition, the tail of the distribution is exponential and .

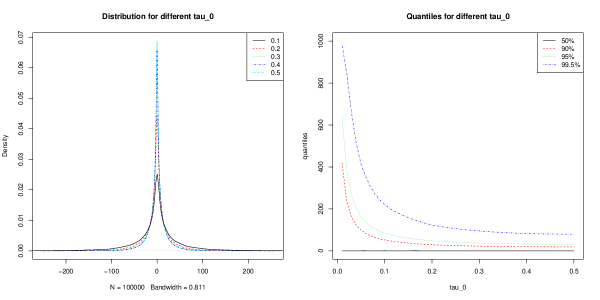

To approximate the distribution of and its critical values, we approximate the standard Brownian motion by standardized sum of i.i.d. standard normal random variables, and generate Monte-Carlo replicates of for . Then we plot their densities and critical values over in Figure 1.

| Please insert Figure 1 here! |

From Figure 1, we see that as moves from to , the density is less concentrated around , indicating the relative difficulty of accurately estimating when is close to or . Correspondingly, the critical calues increase as goes from to .

If Assumptions 2.2(a), 2.2(b) and 2.2(c) hold, there are indeed three regimes that correspond to different rates of . Given , if , this situation is covered by Corollary 2.6. There are two more regimes, under which the behavior of our estimator is discussed in the following theorem.

Theorem 2.8.

We shall offer some comparison with the methods, theory and assumptions in Bai, (2010) and Bhattacharjee et al., (2019), as the latter two papers both addressed change point estimation in the one change point model. To elaborate the differences, we shall separate our discussions into several categories as follows.

1: Model assumptions and estimation methods. Although all three papers assumed one change point in mean for a sequence of high-dimensional observations, there are substantial differences. In particular, Bai, (2010) assumed componentise independence (or so-called cross-sectional independence) but allowed weak temporal dependence for each series; Bhattacharjee et al., (2019) relaxed the cross-sectional independence assumption in Bai, (2010) and allowed weak dependence over time and also within components. By contrast, we require the data to be independent over time but allow for weak componentwise dependence. This makes a direct comparison of the three papers quite challenging, so we shall focus on some specific cases only. Note that in both Bai, (2010) and Bhattacharjee et al., (2019), an infinite order vector moving average process (i.e., VMA()) was assumed.

Denote the break date estimator in Bai, (2010) as , which is obtained as the minimizer of a least squares criterion, see (2.1). Let denote the estimator used in Bhattacharjee et al., (2019) where the minimum is taken over for some prespecified . It should be expected that if . By contrast, our break date estimator is the maximizer of a new U-statistic based objective function.

2: Asymptotic framework, regimes and technical assumptions. In Bai, (2010), he studied two asymptotic frameworks, fixed and as (Bai, (2010) used for our , and for our in his paper). We shall only focus on a comparison with his result in the latter case, i.e., . To make a fair comparison, we shall discuss the case for which both theories are expected to work, which is the case of cross-sectional and temporal independence. To facilitate the comparison, we further assume . Under this condition, our Assumptions 2.2(a) and 2.2(b) are automatically satisfied.

Under the assumption that , Theorem 3.2 in Bai, (2010) stated that if , then . This corresponds to our third regime, where and , which implies that as well, see Theorem 2.8. Under the assumption that , and , Theorem 4.2 of Bai, (2010) asserted the asymptotic distribution for . These assumptions imply , however is no longer . This does not belong to any one of our three regimes stated early. But interestingly, under this specific setting our estimator converge to the same distribution as , and we shall prove this result below in Proposition 2.9.

In addition to these two cases, our theory also uncovers an important and interesting regime Bai, (2010) did not consider, that is . In this case, as we showed earlier, there is a very nice interplay between the order of and that allows to diverge faster than , such that there is an asymptotic distribution for . Thus in a sense, our theory is more complete than the one in Bai, (2010) for this specific model.

Bhattacharjee et al., (2019) extended the method and theory in Bai, (2010) to accommodate both cross-sectional and temporal (serial) dependence. They also used the model with a mean shift, but to accommodate the cross-sectional dependence, many additional assumptions were imposed. For example, Bhattacharjee et al., (2019) required finite fourth moment, whereas Bai, (2010) did not. Also they required that the number of nonzero elements in cannot vary with ; see assumption (A4) in their paper. Such requirement is not needed in our technical analysis. Different from the conditions used in Bai, (2010), there is no explicit restriction on the relative relationship between and in Bhattacharjee et al., (2019). See Remark 2.10 for additional explanations.

3: Convergence rates and efficiency comparison. To compare with the theory in Bhattacharjee et al., (2019), we shall focus on the following model,

where are i.i.d. -dimensional random vectors with zero mean and identity covariance matrix, is real-valued matrix and is the vector of mean change. In our setting, we can set , and hence . This model allows cross-sectional dependence but enforces temporal independence, so is included in our framework. It can also be viewed as a special case of the VMA model with a mean shift in Bhattacharjee et al., (2019) as basically we let when and for in their VMA representation. According to Theorem 2.1 and Theorem 2.2 of Bhattacharjee et al., (2019), to guarantee the consistency of , the signal-to-noise ratio (SNR) has to grow to infinity, i.e. Under this condition, is consistent with the rate of convergence . Notice that the rate of convergence for is . When ,

where the first inequality is due to the fact that , and the second inequality in the above derivation is because . This is a significant finding as it means that for the above specific model, if assumptions for both methods are satisfied, the convergence rate corresponding to our U-statistic based estimator is faster.

To ensure the consistency of our break point estimator , we also require a signal-to-noise condition, i.e., . Since as shown in the above display, provided that (a) and or (b) and is fixed. This implies that our U-statistic based estimator can be consistent with suitable convergence rate under a weaker signal setting as compared to the least squares counterpart. In other words, is a consistent estimator of under much weaker conditions than . We shall provide some theoretical explanation for this phenomenon in Remark 2.10.

Furthermore, similar to our Theorem 2.8 where we have described two additional regimes according to different orders of , the asymptotic behavior of also has three regimes depending on the order of . Under certain assumptions, if , the asymptotic distribution of is degenerate at zero. In this case, since , the limiting distribution of is also degenerate at zero, as implies that under the assumption that . This suggests that the regime that corresponds to the degenerate limiting distribution for is well included in the regime that corresponds to degenerate limiting distribution for .

Of course, the results in Bhattacharjee et al., (2019) are generally applicable to the temporal dependent case, so the slower convergence rate relative to our estimator, which is tailed to the independent high-dimensional data, is probably not surprising. Nevertheless, it shows that our new location estimator can bring substantial efficiency gain relative to the least squares based counterpart in the case of independent high-dimensional data.

Proposition 2.9.

Both estimators and converge to the same limiting distribution if

-

(a)

,

-

(b)

-

(c)

.

Remark 2.10.

The main reason why Bai, (2010) only provided theories under the setting is that the objective function he used is least squares based and it contains extra diagonal terms that need to be controlled under certain restriction on the growth rate of as a function of . To be specific, as we showed in the proof of Proposition 2.9, the first three terms of (i.e., , ) are of form (up to a multiplication constant) for some that needs to be of smaller magnitude than the leading terms in his theoretical derivation, so these three terms have to be controlled under the assumption since if the three diagonal terms can dominate the others. In contrast, in our U-statistic based objective function, we essentially remove the diagonal terms, so no growth rate assumption as is required and we are able to cover the “large small ” case automatically.

The advantage of U-statistic over the least squares counterpart was in fact stated in Chen and Qin, (2010) under the two sample testing framework. Compared to an important early paper by Bai and Saranadasa, (1996), which involves a least squares term in the test statistic, Chen and Qin, (2010) used a U-statistic to remove the diagonal terms, which are not useful in the testing and incur unnecessary growth rate constraints in the theoretical analysis. Therefore in a sense, our U-statistic based approach inherits this advantage from Chen and Qin, (2010) and allows our theory to cover the interesting ”large small ” case (i.e., ).

It is worth noting that Bhattacharjee et al., (2019) considered almost the same estimator as Bai, (2010) but extended the theory to a more general setting including the large small case. In Bhattacharjee et al., (2019), the control of diagonal terms in the least squares based objective function was explicitly done by imposing some extra conditions. In particular their condition (A4) was used to control the order of the diagonal terms. However, these additional assumptions seem hard to verify in practice. In comparison, our four assumptions are relatively more transparent and interpretable.

3 Confidence interval construction

Given the asymptotic theory presented in Section 2, we shall first describe a way of constructing a confidence interval for based on asymptotic approximation. Note that the normalizing constant depends on two unknown quantities, and . Fortunately, their consistent estimators have been provided by Chen and Qin, (2010) in the two sample testing context, and we can easily adapt them to our setting. Algorithm 1 describes the procedure for the plug-in approach below.

-

1.

Estimate : .

-

2.

Estimate : .

-

3.

Estimate : .

-

4.

Estimate : .

-

5.

confidence interval for : , where denotes the -quantile of the distribution of .

In the Algorithm 1, we have used the jackknife type estimator introduced in Chen and Qin (2010), to estimate , i.e.,

where is the sample average of excluding .This slightly differs from the one used in Chen and Qin, (2010) in that we removed two terms that correspond to the two double sums within the pre-break sample and post-break sample. Simulation suggests that there is little impact on the coverage and length of intervals.

After preliminary simulations, we realize that there is considerable amount of coverage error for the above plug-in based confidence interval since this only covers the regime described in Corollary 2.6. There can be other regimes which have different convergence rates and in reality we may not be able to know which regime the data generating process falls into. This motivates us to propose the following bootstrap-based interval.

-

1.

Estimate by and .

-

2.

Estimate by , and let ,where is a -dimensional vector with all elements equal to 1.

-

3.

Estimate by some positive semi-definite estimator .

-

4.

Generate random vectors ,…, in from the distribution .

-

5.

Generate if and if .

-

6.

Calculate the bootstrap estimate by where denotes the value of calculated based on , and calculate the bootstrap estimate of the proportion by .

-

7.

Repeat step 4-6 for times to generate ,…,, and 95% bootstrap CI for is , where and are the sample and quantiles for .

In Algorithm 2 we consider to use a uniform vector with squared norm equal to to estimate the mean change vector, regardless of the sparsity of the truth . The reason why this works is because the limiting distribution only depends on the norm of the mean change, not the vector of the mean change itself. To verify this we have also tried variants of the above algorithm by imposing different sparsity on while maintaining the same norm, the finite sample performance turns out to be stable.

Theorem 3.1 (Bootstrap Consistency).

Remark 3.2.

For the other two regimes besides the regime covered by Assumption 2.2, the bootstrap estimator has the same asymptotic behavior as if the three conditions in the above theorem are satisfied. The proof is very similar to the proof of Theorem 3.1 so we skip the details. The verification of the two conditions (a) and (b) in Theorem 3.1 depend on what type of positive definite estimator we adopt, and it requires a case-by-case analysis. Hence details are omitted.

Remark 3.3.

Bhattacharjee et al., (2019) required a stronger signal-to-noise condition for the bootstrap consistency result. Specifically, instead of the , they required . By contrast, the requirement for the signal-to-noise ratio in our bootstrap consistency result is identical to that for the consistency of our original estimator [cf. Theorem 2.5], which is .

4 Simulation studies

In this section, we study the finite sample performance of our proposed estimator and confidence intervals. We consider the single change point model (CP1) with the change point located at , i.e.

| (4.1) |

where are i.i.d. multivariate normal random vectors with mean zero and covariance , is the mean change vector, and or . To study the impact of componentwise dependence on the performance, we include four different models for : (1) Identity (ID: ); (2) AR(1) (AR: ); (3) Banded (BD: ); (4) Compound Symmetric (CS: ).

The sample size is chosen from and the dimension is chosen from . Furthermore we consider two cases for the sparsity of . One is dense change where is formed by i.i.d. random values generated from Uniform distribution . The other is sparse change, where we first generate a -dimensional random vector by the same procedure as what we have done for dense change and record its norm as , and then generate as the sparse vector. We fix for all Monte-Carlo replicates with the same combination.

We conduct two simulation studies under the above settings to evaluate the performance of the point estimators and confidence intervals, and we comment on the results below for these two studies respectively.

4.1 Finite sample performance of location estimators

We examine the finite sample performance of the location estimators, including our U-statistic based estimator (denoted as ) and the least squares based estimator described in Bai, (2010) (denoted as ) by Monte-Carlo replicates. The bias, variance and mean squared error (MSE) are summarized in Table 1 for and in Table 2 for . As we can observe, outperforms for almost all settings in terms of the MSE. There are two settings for with banded covariance structure ( for sparse change and for dense change), where has slightly larger MSE, and this could be due to random Monte Carlo errors. As we break the MSE criterion into (squared) bias and variance, we spot an interesting pattern. The biases for and are mostly comparable, with no one dominating the other. The advantage of in MSE is mostly attributed to its smaller variance, which may be explained by the usage of a U-statistic based objective function, as U-statistic has the well-known minimal variance property in estimation.

It can also be seen that when comparing the results for and , there are substantially smaller bias and variance for all settings when , which is consistent with our intuition that estimation is easier when . Additionally, both methods exhibit a larger MSE for the compound symmetric case, as compared to other covariance structures. This is not surprising since the compound symmetric covariance matrix corresponds to strong componentwise dependence and violates the weak cross-sectional dependence assumptions necessary for both methods. Nevertheless, as sample size gets larger, the MSE gets smaller for all cases. A direct comparison between the dense change and the sparse charge shows that the results for both cases are very similar for all combinations of and models. This is quite reasonable since the performance of both methods essentially depends on the norm of the mean change, which we hold at the same level. Thus the sparsity of the mean change is not the critical factor in determining the finite sample performance of both estimators. Overall, our new estimator enjoys the efficiency gain over the least squares counterpart in almost all settings and should be preferred in the high-dimensional environment.

4.2 Finite sample performance of confidence intervals

In this section we evaluate the finite sample performance for confidence intervals. For each setting, we generate 3000 Monte-Carlo replicates and construct 7 different 95% confidence intervals for including:

-

1.

Oracle U-statistic based CI (): Constructed by Algorithm 1 with the true value for replacing .

-

2.

U-statistic based CI (): Constructed by Algorithm 1.

-

3.

U-statistic based parametric bootstrap I (): Constructed by modifying Algorithm 4. We estimate the location by , and follow steps 2-5 to generate bootstrap samples. For each bootstrap sample we used our U-statistic based method instead of least squares based method to estimate the location.

-

4.

U-statistic based parametric bootstrap II (): Constructed by Algorithm 2.

-

5.

U-statistic based nonparametric bootstrap (): We sample with replacement based on the pre-break sample and post-break sample separately to generate bootstrap data, where the break date is estimated by . The break date for the bootstrap sample is estimated by our method.

- 6.

-

7.

Adaptive CI in Bhattacharjee et al., (2019) (): Constructed by Algorithm 4, which is a modified version of the one in Bhattacharjee et al., (2019) due to the temporal independence model we assume here. This main difference between this one and is that the least squares based approach was used for the break date estimation for both original and bootstrap sample, whereas the U-statistic based approach was used in the construction of .

One thing worth pointing out is that in Algorithm 4, Bhattacharjee et al., (2019) originally used banded autocovariance matrix to generate bootstrap samples. However we found during our simulation that the banded covariance matrix may not be positive semi-definite and the sample covariance matrix itself is not a good estimate when the dimension is high. To solve this issue, we use the R package ”PDSCE” to get a positive definite estimate for the high-dimensional covariance matrix. Specifically, denote as the sample covariance matrix and as the sample correlation matrix. Denote as the diagonal matrix with the same diagonal as and . Then the correlation matrix estimator is constructed as

where is a fixed small positive constant, is a non-negative tuning parameter, is the determinant and is the norm of the vectorized matrix. The tuning parameters are selected via a default cross-validation step in “PDSCE”. Then the estimated covariance matrix is constructed as . See Rothman, (2012) for more details about this methodology. Note that this is the covariance matrix estimate we used for our Algorithms 2 and 4, i.e., in the construction of and .

The results are summarized in Tables 3-6. We calculate the sample coverage probability as well as the average length for each CI. Each table corresponds to a particular covariance model with all results for both sparse and dense changes, all combinations of s and two cases . It is apparent for some combinations of , the coverages for all seven intervals are far below the nominal coverage level , indicating the difficulty of constructing an interval with proper coverage, especially when is small and the dependence among components is strong.

The three intervals (, and ) are based on asymptotic approximation, which seem quite coarse as all these intervals exhibit serious undercoverage. It appears that in most cases and have better coverage than when but have worse coverage than when , which is consistent with the asymptotic theory. Note that the undercoverage for and are tied to the fact that we always use for and for as the rate of convergence, which is only correct for our regime . However for other regimes the rates of convergence can be slower than . This leads to an undercoverage. For the same reason, fails to achieve the desired coverage probability since the theory is only valid for a specific regime and requires the cross-sectional independence.

The four bootstrap-based intervals (, , and ) have overall almost uniform better coverages than the three counterparts based on asymptotic approximation. Among these four intervals, the ranking appears to be (in the order of preferences) . We can see that and have very comparable results for all settings. Both have about 95% coverage probability even for small when . When , the problem gets harder but they can still have a desired coverage when and are large, sometimes even too conservative. We have no theoretical justification for the nonparametric bootstrap procedure yet, but the simulation results are quite encouraging. We have also tried variants of by using a sparse estimate of and keeping the same norm, the results turn out to be similar to what we have here.

As a comparison, is another least squares based interval and it has better coverage comparing to by using a bootstrap procedure. But it still cannot achieve the desired confidence level for most settings when . When , it has decent coverage probability when the sample size is large. As we have discussed before, the rate of convergence of our estimator is faster than the least squares based estimator. Hence our methods (, and ) can achieve the desired coverage with smaller . Furthermore we observe that for large small situation, our methods still provide a good coverage whereas cannot. This may be related to the fact that our methods work for both and in theory, but the least squares based method only works for the case . Note that a higher coverage probability is usually associated with a longer interval.

Among other observations, we mention that for the same setting, the results for are always comparable or better than the results (in terms of more coverage and shorter interval length) for due to the fact the estimation problem for is easier. For most settings, the results for sparse and dense changes are similar, which is consistent with the fact that the performance is mainly determined by the norm of the mean change rather than the mean change vector itself. For the same , there are relatively less differences between the results for “ID”, “AR” and “BD” covariance models, compared to their differences from the ”CS” case. This can be explained by the fact that the former three cases belong to the class of weakly dependent components model whereas the compound symmetric covariance structure implies strong dependence.

Among all methods, the U-statistic based bootstrap procedures (, ) perform the best, achieving the desired coverage level in most settings even with a small sample size and moderate dependence within components.

4.3 Impact of on the finite sample coverage

As shown in the previous subsection, the confidence intervals constructed by the asymptotic approximation have substantially lower coverage probabilities than the desired 95%. One possible explanation is that we used the limiting distribution corresponding to a particular regime to approximate the finite sample distribution of regardless of which regime the data generating process falls into, which yields large approximation errors in many cases. Another plausible explanation is that the finite sample approximation error is related to the magnitude of , which controls the amount of noise in the U-statistic based objective function. This can be seen from our theoretical derivation, as our objective function contains terms as , for . These terms are asymptotically negligible under Assumption 2.2(c), but in finite sample, these interaction terms can have a substantial impact on the finite sample coverage. Theoretically the order of these interaction terms is proportional to . To examine the impact of these interaction terms, as measured by the magnitude of , we shall design a small simulation experiment as follows.

In the following experiment, the sample size is still chosen from and is selected from . The change occurs at . We set as a diagonal matrix with elements if and for . We consider three cases for to represent different strength of the interaction terms. We fix , and set (1) Weak: ;(2) Moderate: ;(3) Strong: . It is easily seen that the magnitude of gradually increases as we move from case (1) to (2) and to (3). The results are summarized in Table 7.

As we fix , the signal of the problem is fixed. When we increase the strength of the interaction as quantified by , we essentially increase the level of the noise, so the (finite sample) signal to noise ratio decreases. Consequently, for a fixed sample size and dimension combination, the coverage probabilities for all methods decrease as the interaction gets stronger. For all intervals based on asymptotic approximations (, and ), it is interesting to observe that while the average length does not change much, the coverage drops as the strength of interaction terms moves from weak to moderate and then to strong. When is small, we see that and can indeed achieve a coverage of more than for , when and , which corroborates our asymptotic theory. There is some noticeable impact on the coverage of bootstrap-based intervals (, , and ) but compared to the impact on asymptotic approximation based intervals (, and ), the strength of interaction terms plays a less significant role in the finite sample coverage. This might be due to the adaptive nature of the bootstrap method. A good theoretical explanation for this adaptiveness presumably involves second-order edgeworth expansion of the distribution of both and , which seems very challenging. Overall and have the best coverage probabilities among all methods, although they appear to be conservative (i.e., over-coverage) in a few settings.

5 Conclusions

In this article, we introduce a new estimation method for the change point location in the mean of independent high-dimensional data. The new U-statistic based objective function is natural given its unbiased and minimal variance property in classical estimation problems, and brings substantial efficiency gain to the change point location estimation in the high-dimensional setting, as demonstrated in both theory and simulations. The convergence rate and asymptotic distribution of the location estimate are obtained under mild assumptions using new technical arguments that involve some nontrivial asymptotic theory for the high-dimensional U-statistics. A bootstrap-based approach was also proposed to construct a confidence interval, which seems to work well in all simulation settings. Our theoretical results and numerical findings are significant as they suggest that (i) the U-statistic based point estimator is preferred to the least squares based counterpart in break date estimation, especially when ; (ii) Bootstrap-based interval is fairly adaptive to different magnitude of change, and should be preferred to the asymptotic plug-in approach. In addition, U-statistic based estimation approach is recommended to couple with either nonparametric bootstrap or parametric bootstrap with a suitably estimated covariance matrix in constructing an interval for the break date.

To conclude, the work we present in this article opens up several new directions for future research. The assumption of independence (over time) is crucial for the formulation of our U-statistic based objective function and derivation of asymptotic property of our estimator. It would be desirable to extend our methodology and theory to cover the temporally dependent case, as in practice many high-dimensional time-ordered data have weak dependence over time. In view of recent work of Wang and Shao, (2019), some trimming might be needed in forming the U-statistic based objective function. In addition, nonparametric bootstrap-based confidence interval performs well in simulation but our theory can only cover the parametric bootstrap. A complete theoretical justification for nonparametric bootstrap would be interesting. At last, our method and theory are limited to the relatively simple model with only one change point. For the linear regression model with low-dimensional covariates, see Bai and Perron, (1998) for a suite of least squares based procedures for the estimation of change point locations and the construction of tests that allow inference to be made about the presence of structural change and the number of change points. It would be certainly interesting to extend our U-statistic based approach to the model with multiple change points in mean and also to high-dimensional regression setting. We leave these important topics for future investigation.

| Sparse | Dense | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | |||||||

| ID | 50 | 50 | 792.8 | 309.6 | 372.4 | 50 | 50 | 796.9 | 316.6 | 380.1 | ||

| 763.5 | 401.6 | 459.9 | 771.4 | 411.1 | 470.6 | |||||||

| 100 | 86.0 | 31.1 | 31.8 | 100 | 86.9 | 31.6 | 32.3 | |||||

| 69.8 | 41.0 | 41.5 | 71.8 | 38.9 | 39.4 | |||||||

| 200 | 4.9 | 0.8 | 0.8 | 200 | 4.6 | 0.8 | 0.8 | |||||

| 3.0 | 0.7 | 0.7 | 2.6 | 0.8 | 0.8 | |||||||

| 150 | 50 | 77.1 | 22.1 | 22.7 | 150 | 50 | 71.0 | 19.9 | 20.4 | |||

| 48.4 | 22.3 | 22.5 | 48.4 | 22.5 | 22.8 | |||||||

| 100 | 4.6 | 0.6 | 0.6 | 100 | 5.8 | 0.6 | 0.6 | |||||

| 1.9 | 0.6 | 0.6 | 2.4 | 0.6 | 0.6 | |||||||

| 200 | 0.6 | 0.1 | 0.1 | 200 | 0.7 | 0.1 | 0.1 | |||||

| 0.1 | 0.1 | 0.1 | 0.3 | 0.1 | 0.1 | |||||||

| AR | 50 | 50 | 1847.9 | 629.2 | 970.6 | 50 | 50 | 1871.0 | 626.9 | 977.0 | ||

| 1871.3 | 860.4 | 1210.6 | 1926.5 | 861.1 | 1232.1 | |||||||

| 100 | 920.7 | 379.7 | 464.4 | 100 | 821.0 | 345.9 | 413.3 | |||||

| 1011.4 | 578.5 | 680.7 | 924.1 | 538.5 | 623.9 | |||||||

| 200 | 128.6 | 55.6 | 57.2 | 200 | 46.0 | 18.4 | 18.6 | |||||

| 134.0 | 86.1 | 87.9 | 49.4 | 31.4 | 31.6 | |||||||

| 150 | 50 | 907.7 | 356.7 | 439.1 | 150 | 50 | 804.7 | 320.3 | 385.0 | |||

| 909.4 | 477.2 | 559.9 | 799.0 | 419.9 | 483.7 | |||||||

| 100 | 161.4 | 66.0 | 68.6 | 100 | 81.4 | 32.0 | 32.6 | |||||

| 152.6 | 90.9 | 93.3 | 75.0 | 44.9 | 45.5 | |||||||

| 200 | 7.0 | 1.6 | 1.6 | 200 | 1.8 | 0.3 | 0.3 | |||||

| 4.1 | 1.6 | 1.6 | 1.3 | 0.3 | 0.3 | |||||||

| BD | 50 | 50 | 1215.9 | 462.6 | 610.4 | 50 | 50 | 1175.5 | 446.0 | 584.1 | ||

| 1196.9 | 607.4 | 750.6 | 1147.1 | 578.1 | 709.7 | |||||||

| 100 | 318.7 | 131.5 | 141.7 | 100 | 221.8 | 90.9 | 95.9 | |||||

| 299.5 | 177.5 | 186.4 | 222.5 | 132.3 | 137.2 | |||||||

| 200 | 16.0 | 4.6 | 4.7 | 200 | 5.1 | 1.0 | 1.0 | |||||

| 10.4 | 4.3 | 4.3 | 3.0 | 1.0 | 1.0 | |||||||

| 150 | 50 | 254.0 | 95.8 | 102.3 | 150 | 50 | 181.2 | 66.1 | 69.4 | |||

| 209.0 | 113.0 | 117.3 | 139.9 | 74.2 | 76.1 | |||||||

| 100 | 19.2 | 3.6 | 3.7 | 100 | 7.8 | 1.4 | 1.4 | |||||

| 11.4 | 3.8 | 3.8 | 3.6 | 1.2 | 1.2 | |||||||

| 200 | 1.8 | 0.3 | 0.3 | 200 | 1.1 | 0.1 | 0.1 | |||||

| 0.6 | 0.3 | 0.3 | 0.6 | 0.1 | 0.1 | |||||||

| CS | 50 | 50 | 2359.6 | 706.3 | 1263.1 | 50 | 50 | 2334.9 | 701.0 | 1246.1 | ||

| 2453.7 | 982.6 | 1584.6 | 2446.0 | 983.2 | 1581.5 | |||||||

| 100 | 1623.2 | 597.2 | 860.6 | 100 | 1641.8 | 603.7 | 873.2 | |||||

| 1881.3 | 963.0 | 1316.9 | 1848.8 | 953.0 | 1294.8 | |||||||

| 200 | 604.7 | 274.7 | 311.2 | 200 | 549.8 | 250.8 | 281.0 | |||||

| 813.5 | 528.5 | 594.7 | 744.2 | 482.7 | 538.1 | |||||||

| 150 | 50 | 2202.7 | 684.4 | 1169.6 | 150 | 50 | 2194.8 | 684.6 | 1166.3 | |||

| 2279.0 | 949.4 | 1468.7 | 2301.1 | 957.4 | 1486.8 | |||||||

| 100 | 1508.2 | 568.9 | 796.3 | 100 | 1487.9 | 566.2 | 787.6 | |||||

| 1747.2 | 909.5 | 1214.7 | 1757.0 | 913.6 | 1222.3 | |||||||

| 200 | 561.6 | 257.1 | 288.6 | 200 | 525.6 | 242.8 | 270.4 | |||||

| 775.7 | 503.5 | 563.7 | 737.7 | 485.7 | 540.1 | |||||||

| Sparse | Dense | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Variance | MSE | Bias | Variance | MSE | |||||||

| ID | 50 | 50 | 3.6 | 80.0 | 80.0 | 50 | 50 | 5.2 | 81.4 | 81.4 | ||

| 2.8 | 110.5 | 110.5 | -8.2 | 112.9 | 113.0 | |||||||

| 100 | 1.7 | 6.1 | 6.1 | 100 | -3.2 | 6.4 | 6.4 | |||||

| 2.1 | 6.6 | 6.6 | -3.2 | 6.9 | 6.9 | |||||||

| 200 | 0.0 | 0.5 | 0.5 | 200 | 0.0 | 0.5 | 0.5 | |||||

| 0.0 | 0.5 | 0.5 | -0.1 | 0.5 | 0.5 | |||||||

| 150 | 50 | 2.3 | 3.2 | 3.2 | 150 | 50 | -0.7 | 3.1 | 3.1 | |||

| 2.0 | 3.3 | 3.3 | -0.4 | 3.2 | 3.2 | |||||||

| 100 | 0.3 | 0.3 | 0.3 | 100 | 0.5 | 0.3 | 0.3 | |||||

| 0.2 | 0.3 | 0.3 | 0.5 | 0.3 | 0.3 | |||||||

| 200 | -0.2 | 0.0 | 0.0 | 200 | -0.1 | 0.0 | 0.0 | |||||

| -0.2 | 0.0 | 0.0 | -0.1 | 0.0 | 0.0 | |||||||

| AR | 50 | 50 | -2.1 | 342.2 | 342.2 | 50 | 50 | 4.7 | 339.8 | 339.7 | ||

| -8.9 | 521.1 | 521.1 | 1.5 | 519.7 | 519.7 | |||||||

| 100 | -23.0 | 127.2 | 127.2 | 100 | 0.9 | 82.1 | 82.1 | |||||

| -25.2 | 202.1 | 202.2 | 9.4 | 143.5 | 143.5 | |||||||

| 200 | 4.2 | 12.4 | 12.4 | 200 | 0.7 | 2.6 | 2.6 | |||||

| 4.1 | 14.6 | 14.6 | 0.4 | 2.7 | 2.7 | |||||||

| 150 | 50 | -1.2 | 90.4 | 90.4 | 150 | 50 | 2.2 | 59.4 | 59.4 | |||

| -11.5 | 133.7 | 133.7 | -3.4 | 90.7 | 90.7 | |||||||

| 100 | -1.7 | 10.8 | 10.8 | 100 | 0.5 | 2.9 | 2.9 | |||||

| -1.2 | 12.1 | 12.1 | 0.7 | 3.0 | 3.0 | |||||||

| 200 | -0.5 | 0.9 | 0.9 | 200 | -0.5 | 0.1 | 0.1 | |||||

| -0.5 | 0.9 | 0.9 | -0.4 | 0.1 | 0.1 | |||||||

| BD | 50 | 50 | -7.4 | 170.4 | 170.4 | 50 | 50 | 10.7 | 148.5 | 148.5 | ||

| -0.8 | 245.5 | 245.5 | -1.8 | 222.2 | 222.2 | |||||||

| 100 | 0.8 | 31.2 | 31.1 | 100 | 0.5 | 15.4 | 15.4 | |||||

| -0.4 | 38.5 | 38.5 | -0.1 | 19.2 | 19.2 | |||||||

| 200 | 0.3 | 2.4 | 2.4 | 200 | -0.3 | 0.6 | 0.6 | |||||

| 0.3 | 2.4 | 2.4 | -0.3 | 0.6 | 0.6 | |||||||

| 150 | 50 | -2.7 | 15.6 | 15.6 | 150 | 50 | 1.0 | 6.9 | 6.9 | |||

| -1.6 | 18.8 | 18.8 | 0.6 | 7.6 | 7.6 | |||||||

| 100 | 0.1 | 1.7 | 1.7 | 100 | 0.1 | 0.6 | 0.6 | |||||

| 0.0 | 1.7 | 1.7 | 0.1 | 0.6 | 0.6 | |||||||

| 200 | 0.0 | 0.2 | 0.2 | 200 | 0.3 | 0.1 | 0.1 | |||||

| 0.1 | 0.2 | 0.2 | 0.3 | 0.1 | 0.1 | |||||||

| CS | 50 | 50 | -13.0 | 501.9 | 501.9 | 50 | 50 | -18.1 | 493.2 | 493.3 | ||

| -13.8 | 767.3 | 767.3 | -12.8 | 756.6 | 756.5 | |||||||

| 100 | 6.7 | 301.3 | 301.3 | 100 | -4.1 | 279.7 | 279.7 | |||||

| 2.9 | 572.7 | 572.7 | 12.7 | 541.1 | 541.1 | |||||||

| 200 | 6.4 | 63.1 | 63.1 | 200 | 7.7 | 57.2 | 57.2 | |||||

| 10.9 | 132.1 | 132.1 | 11.1 | 117.5 | 117.5 | |||||||

| 150 | 50 | 19.3 | 437.2 | 437.2 | 150 | 50 | -0.4 | 426.2 | 426.2 | |||

| 12.4 | 684.4 | 684.3 | -2.1 | 685.6 | 685.6 | |||||||

| 100 | -0.9 | 245.2 | 245.1 | 100 | 6.8 | 235.5 | 235.5 | |||||

| -7.1 | 471.3 | 471.2 | 2.6 | 464.5 | 464.4 | |||||||

| 200 | 2.9 | 57.5 | 57.5 | 200 | 4.1 | 49.5 | 49.5 | |||||

| 7.4 | 114.3 | 114.3 | 12.9 | 108.5 | 108.5 | |||||||

| Dense | Sparse | Dense | Sparse | |||||||||

| 50 | ||||||||||||

| 0.765 | 0.740 | 0.611 | 0.754 | 0.792 | 0.579 | 0.881 | 0.744 | 0.833 | 0.879 | 0.780 | 0.827 | |

| Length | 0.113 | 0.076 | 0.008 | 0.113 | 0.076 | 0.008 | 0.049 | 0.015 | 0.004 | 0.049 | 0.015 | 0.004 |

| 0.797 | 0.768 | 0.685 | 0.798 | 0.798 | 0.661 | 0.862 | 0.800 | 0.833 | 0.846 | 0.833 | 0.827 | |

| Length | 0.172 | 0.098 | 0.009 | 0.164 | 0.096 | 0.009 | 0.067 | 0.018 | 0.004 | 0.068 | 0.018 | 0.004 |

| 0.727 | 0.732 | 0.917 | 0.722 | 0.787 | 0.920 | 0.738 | 0.859 | 0.966 | 0.718 | 0.889 | 0.954 | |

| Length | 0.071 | 0.062 | 0.022 | 0.072 | 0.061 | 0.023 | 0.008 | 0.014 | 0.009 | 0.008 | 0.014 | 0.010 |

| 0.886 | 0.902 | 0.961 | 0.894 | 0.923 | 0.961 | 0.959 | 0.975 | 0.977 | 0.955 | 0.967 | 0.969 | |

| Length | 0.460 | 0.345 | 0.035 | 0.268 | 0.223 | 0.035 | 0.174 | 0.037 | 0.012 | 0.141 | 0.037 | 0.012 |

| 0.831 | 0.812 | 0.930 | 0.837 | 0.844 | 0.929 | 0.913 | 0.937 | 0.971 | 0.907 | 0.947 | 0.961 | |

| Length | 0.194 | 0.097 | 0.025 | 0.172 | 0.094 | 0.025 | 0.093 | 0.031 | 0.011 | 0.092 | 0.030 | 0.011 |

| 0.601 | 0.626 | 0.885 | 0.575 | 0.677 | 0.874 | 0.780 | 0.827 | 0.893 | 0.776 | 0.840 | 0.890 | |

| Length | 0.035 | 0.034 | 0.017 | 0.035 | 0.034 | 0.017 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.643 | 0.607 | 0.888 | 0.606 | 0.657 | 0.877 | 0.686 | 0.732 | 0.889 | 0.671 | 0.779 | 0.873 | |

| Length | 0.034 | 0.032 | 0.017 | 0.034 | 0.031 | 0.017 | 0.001 | 0.001 | 0.004 | 0.000 | 0.000 | 0.004 |

| 0.761 | 0.789 | 0.617 | 0.742 | 0.762 | 0.605 | 0.763 | 0.818 | 0.858 | 0.792 | 0.802 | 0.867 | |

| Length | 0.072 | 0.049 | 0.005 | 0.072 | 0.049 | 0.005 | 0.031 | 0.010 | 0.003 | 0.031 | 0.010 | 0.003 |

| 0.820 | 0.755 | 0.625 | 0.772 | 0.754 | 0.611 | 0.830 | 0.818 | 0.858 | 0.851 | 0.803 | 0.867 | |

| Length | 0.098 | 0.056 | 0.006 | 0.093 | 0.058 | 0.006 | 0.037 | 0.011 | 0.003 | 0.037 | 0.010 | 0.003 |

| 0.839 | 0.850 | 0.940 | 0.818 | 0.844 | 0.952 | 0.814 | 0.941 | 0.974 | 0.836 | 0.944 | 0.974 | |

| Length | 0.073 | 0.064 | 0.023 | 0.072 | 0.065 | 0.023 | 0.012 | 0.018 | 0.010 | 0.012 | 0.017 | 0.010 |

| 0.950 | 0.958 | 0.967 | 0.957 | 0.945 | 0.970 | 0.968 | 0.972 | 0.974 | 0.978 | 0.972 | 0.976 | |

| Length | 0.250 | 0.166 | 0.030 | 0.240 | 0.170 | 0.029 | 0.071 | 0.026 | 0.010 | 0.070 | 0.026 | 0.010 |

| 0.916 | 0.887 | 0.946 | 0.903 | 0.872 | 0.949 | 0.963 | 0.962 | 0.972 | 0.968 | 0.961 | 0.971 | |

| Length | 0.136 | 0.081 | 0.024 | 0.133 | 0.083 | 0.024 | 0.052 | 0.021 | 0.010 | 0.052 | 0.020 | 0.010 |

| 0.781 | 0.777 | 0.911 | 0.767 | 0.770 | 0.924 | 0.838 | 0.895 | 0.914 | 0.876 | 0.891 | 0.929 | |

| Length | 0.055 | 0.043 | 0.019 | 0.055 | 0.045 | 0.019 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.750 | 0.782 | 0.925 | 0.736 | 0.772 | 0.933 | 0.763 | 0.837 | 0.947 | 0.789 | 0.827 | 0.951 | |

| Length | 0.041 | 0.040 | 0.019 | 0.041 | 0.041 | 0.019 | 0.000 | 0.002 | 0.008 | 0.000 | 0.002 | 0.007 |

| Dense | Sparse | Dense | Sparse | |||||||||

| 50 | ||||||||||||

| 0.740 | 0.751 | 0.820 | 0.773 | 0.713 | 0.622 | 0.801 | 0.843 | 0.898 | 0.780 | 0.791 | 0.725 | |

| Length | 0.490 | 0.330 | 0.036 | 0.315 | 0.212 | 0.023 | 0.253 | 0.077 | 0.013 | 0.141 | 0.044 | 0.012 |

| 0.676 | 0.639 | 0.802 | 0.688 | 0.650 | 0.600 | 0.760 | 0.837 | 0.872 | 0.751 | 0.768 | 0.650 | |

| Length | 0.622 | 0.378 | 0.041 | 0.579 | 0.360 | 0.027 | 0.346 | 0.094 | 0.014 | 0.183 | 0.052 | 0.013 |

| 0.627 | 0.644 | 0.910 | 0.753 | 0.729 | 0.911 | 0.564 | 0.781 | 0.931 | 0.712 | 0.845 | 0.890 | |

| Length | 0.494 | 0.344 | 0.061 | 0.381 | 0.287 | 0.086 | 0.090 | 0.044 | 0.014 | 0.092 | 0.055 | 0.029 |

| 0.666 | 0.719 | 0.970 | 0.825 | 0.817 | 0.971 | 0.763 | 0.939 | 0.995 | 0.906 | 0.950 | 0.970 | |

| Length | 0.743 | 0.686 | 0.297 | 0.661 | 0.591 | 0.203 | 0.627 | 0.335 | 0.057 | 0.415 | 0.171 | 0.064 |

| 0.645 | 0.682 | 0.943 | 0.784 | 0.783 | 0.933 | 0.726 | 0.888 | 0.970 | 0.858 | 0.910 | 0.922 | |

| Length | 0.570 | 0.489 | 0.084 | 0.456 | 0.397 | 0.108 | 0.344 | 0.099 | 0.023 | 0.261 | 0.090 | 0.040 |

| 0.220 | 0.274 | 0.720 | 0.357 | 0.352 | 0.605 | 0.367 | 0.537 | 0.816 | 0.464 | 0.531 | 0.610 | |

| Length | 0.032 | 0.028 | 0.018 | 0.038 | 0.035 | 0.020 | 0.020 | 0.020 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.430 | 0.429 | 0.852 | 0.584 | 0.594 | 0.861 | 0.421 | 0.662 | 0.898 | 0.586 | 0.774 | 0.960 | |

| Length | 0.110 | 0.088 | 0.034 | 0.140 | 0.122 | 0.064 | 0.034 | 0.022 | 0.010 | 0.046 | 0.037 | 0.023 |

| 0.780 | 0.771 | 0.817 | 0.723 | 0.720 | 0.614 | 0.857 | 0.824 | 0.904 | 0.769 | 0.779 | 0.742 | |

| Length | 0.315 | 0.212 | 0.023 | 0.313 | 0.212 | 0.023 | 0.141 | 0.044 | 0.012 | 0.141 | 0.044 | 0.012 |

| 0.711 | 0.719 | 0.781 | 0.648 | 0.648 | 0.586 | 0.856 | 0.910 | 0.862 | 0.749 | 0.757 | 0.673 | |

| Length | 0.356 | 0.231 | 0.025 | 0.300 | 0.223 | 0.027 | 0.163 | 0.048 | 0.013 | 0.172 | 0.052 | 0.013 |

| 0.754 | 0.766 | 0.938 | 0.694 | 0.738 | 0.898 | 0.780 | 0.912 | 0.941 | 0.705 | 0.829 | 0.898 | |

| Length | 0.363 | 0.245 | 0.049 | 0.333 | 0.266 | 0.087 | 0.069 | 0.034 | 0.017 | 0.090 | 0.055 | 0.029 |

| 0.824 | 0.854 | 0.995 | 0.782 | 0.830 | 0.961 | 0.949 | 0.987 | 0.999 | 0.905 | 0.953 | 0.973 | |

| Length | 0.684 | 0.610 | 0.197 | 0.556 | 0.519 | 0.204 | 0.416 | 0.162 | 0.064 | 0.390 | 0.171 | 0.064 |

| 0.779 | 0.812 | 0.949 | 0.721 | 0.785 | 0.923 | 0.910 | 0.956 | 0.970 | 0.863 | 0.886 | 0.928 | |

| Length | 0.454 | 0.374 | 0.058 | 0.397 | 0.361 | 0.110 | 0.189 | 0.059 | 0.023 | 0.221 | 0.090 | 0.040 |

| 0.386 | 0.445 | 0.786 | 0.321 | 0.343 | 0.601 | 0.576 | 0.738 | 0.786 | 0.467 | 0.553 | 0.611 | |

| Length | 0.042 | 0.037 | 0.020 | 0.038 | 0.035 | 0.020 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.561 | 0.595 | 0.901 | 0.539 | 0.596 | 0.852 | 0.679 | 0.852 | 0.904 | 0.595 | 0.771 | 0.882 | |

| Length | 0.115 | 0.097 | 0.032 | 0.139 | 0.118 | 0.065 | 0.036 | 0.020 | 0.010 | 0.046 | 0.038 | 0.023 |

| Dense | Sparse | Dense | Sparse | |||||||||

| 50 | ||||||||||||

| 0.751 | 0.770 | 0.575 | 0.763 | 0.775 | 0.615 | 0.877 | 0.801 | 0.816 | 0.888 | 0.773 | 0.817 | |

| Length | 0.113 | 0.076 | 0.008 | 0.113 | 0.076 | 0.008 | 0.049 | 0.015 | 0.004 | 0.049 | 0.015 | 0.004 |

| 0.801 | 0.796 | 0.648 | 0.785 | 0.785 | 0.665 | 0.856 | 0.861 | 0.816 | 0.866 | 0.827 | 0.817 | |

| Length | 0.179 | 0.097 | 0.009 | 0.170 | 0.099 | 0.009 | 0.067 | 0.017 | 0.004 | 0.066 | 0.018 | 0.004 |

| 0.714 | 0.777 | 0.912 | 0.719 | 0.763 | 0.928 | 0.742 | 0.912 | 0.952 | 0.728 | 0.885 | 0.949 | |

| Length | 0.072 | 0.061 | 0.023 | 0.073 | 0.062 | 0.022 | 0.008 | 0.013 | 0.009 | 0.008 | 0.013 | 0.010 |

| 0.886 | 0.919 | 0.961 | 0.882 | 0.925 | 0.971 | 0.951 | 0.978 | 0.962 | 0.965 | 0.977 | 0.972 | |

| Length | 0.468 | 0.338 | 0.035 | 0.273 | 0.225 | 0.034 | 0.168 | 0.037 | 0.001 | 0.138 | 0.038 | 0.012 |

| 0.827 | 0.833 | 0.925 | 0.824 | 0.837 | 0.943 | 0.900 | 0.960 | 0.962 | 0.921 | 0.951 | 0.962 | |

| Length | 0.199 | 0.096 | 0.025 | 0.175 | 0.096 | 0.025 | 0.092 | 0.030 | 0.001 | 0.091 | 0.030 | 0.011 |

| 0.609 | 0.646 | 0.876 | 0.602 | 0.650 | 0.899 | 0.770 | 0.864 | 0.885 | 0.788 | 0.857 | 0.900 | |

| Length | 0.035 | 0.034 | 0.017 | 0.036 | 0.034 | 0.017 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.626 | 0.632 | 0.870 | 0.617 | 0.652 | 0.899 | 0.683 | 0.803 | 0.870 | 0.678 | 0.781 | 0.878 | |

| Length | 0.035 | 0.031 | 0.017 | 0.035 | 0.031 | 0.017 | 0.000 | 0.001 | 0.004 | 0.000 | 0.000 | 0.004 |

| 0.755 | 0.758 | 0.632 | 0.738 | 0.755 | 0.645 | 0.769 | 0.801 | 0.851 | 0.758 | 0.796 | 0.859 | |

| Length | 0.072 | 0.049 | 0.005 | 0.072 | 0.049 | 0.005 | 0.031 | 0.010 | 0.003 | 0.031 | 0.010 | 0.003 |

| 0.792 | 0.752 | 0.638 | 0.788 | 0.748 | 0.648 | 0.826 | 0.803 | 0.851 | 0.839 | 0.799 | 0.859 | |

| Length | 0.092 | 0.060 | 0.006 | 0.095 | 0.058 | 0.006 | 0.037 | 0.011 | 0.003 | 0.038 | 0.011 | 0.003 |

| 0.814 | 0.839 | 0.943 | 0.826 | 0.833 | 0.945 | 0.818 | 0.942 | 0.972 | 0.825 | 0.935 | 0.977 | |

| Length | 0.072 | 0.065 | 0.023 | 0.072 | 0.065 | 0.023 | 0.012 | 0.018 | 0.010 | 0.013 | 0.018 | 0.010 |

| 0.942 | 0.941 | 0.965 | 0.938 | 0.945 | 0.961 | 0.970 | 0.965 | 0.974 | 0.972 | 0.962 | 0.980 | |

| Length | 0.239 | 0.172 | 0.030 | 0.239 | 0.171 | 0.029 | 0.072 | 0.026 | 0.010 | 0.072 | 0.026 | 0.010 |

| 0.903 | 0.882 | 0.946 | 0.902 | 0.878 | 0.947 | 0.955 | 0.956 | 0.973 | 0.958 | 0.951 | 0.976 | |

| Length | 0.132 | 0.084 | 0.024 | 0.133 | 0.084 | 0.024 | 0.052 | 0.020 | 0.010 | 0.053 | 0.021 | 0.010 |

| 0.766 | 0.776 | 0.933 | 0.769 | 0.758 | 0.913 | 0.858 | 0.888 | 0.911 | 0.848 | 0.870 | 0.922 | |

| Length | 0.055 | 0.044 | 0.020 | 0.056 | 0.044 | 0.019 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.750 | 0.762 | 0.925 | 0.741 | 0.750 | 0.931 | 0.770 | 0.817 | 0.948 | 0.758 | 0.824 | 0.956 | |

| Length | 0.041 | 0.041 | 0.019 | 0.041 | 0.041 | 0.019 | 0.000 | 0.002 | 0.008 | 0.000 | 0.003 | 0.007 |

| Dense | Sparse | Dense | Sparse | |||||||||

| 50 | ||||||||||||

| 1.000 | 0.818 | 0.777 | 1.000 | 0.800 | 0.738 | 1.000 | 0.738 | 0.746 | 1.000 | 0.719 | 0.743 | |

| Length | 0.949 | 0.754 | 0.108 | 0.952 | 0.748 | 0.108 | 1.000 | 0.508 | 0.157 | 1.000 | 0.504 | 0.157 |

| 0.591 | 0.573 | 0.717 | 0.588 | 0.575 | 0.689 | 0.583 | 0.588 | 0.682 | 0.574 | 0.595 | 0.659 | |

| Length | 0.451 | 0.428 | 0.113 | 0.491 | 0.448 | 0.118 | 0.481 | 0.364 | 0.151 | 0.487 | 0.381 | 0.156 |

| 0.558 | 0.584 | 0.857 | 0.553 | 0.592 | 0.824 | 0.502 | 0.648 | 0.797 | 0.523 | 0.635 | 0.792 | |

| Length | 0.357 | 0.376 | 0.277 | 0.375 | 0.364 | 0.279 | 0.355 | 0.353 | 0.300 | 0.369 | 0.342 | 0.310 |

| 0.565 | 0.601 | 0.871 | 0.561 | 0.598 | 0.837 | 0.579 | 0.668 | 0.809 | 0.537 | 0.649 | 0.808 | |

| Length | 0.372 | 0.689 | 0.315 | 0.389 | 0.376 | 0.313 | 0.374 | 0.371 | 0.321 | 0.390 | 0.359 | 0.330 |

| 0.548 | 0.578 | 0.859 | 0.547 | 0.582 | 0.826 | 0.505 | 0.653 | 0.796 | 0.523 | 0.632 | 0.794 | |

| Length | 0.351 | 0.373 | 0.286 | 0.367 | 0.362 | 0.288 | 0.355 | 0.354 | 0.297 | 0.371 | 0.344 | 0.307 |

| 0.135 | 0.122 | 0.442 | 0.137 | 0.105 | 0.391 | 0.118 | 0.115 | 0.281 | 0.092 | 0.128 | 0.235 | |

| Length | 0.027 | 0.023 | 0.016 | 0.028 | 0.022 | 0.016 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.420 | 0.394 | 0.736 | 0.394 | 0.383 | 0.694 | 0.375 | 0.460 | 0.662 | 0.392 | 0.464 | 0.623 | |

| Length | 0.241 | 0.222 | 0.090 | 0.250 | 0.215 | 0.104 | 0.232 | 0.188 | 0.115 | 0.246 | 0.191 | 0.125 |

| 1.000 | 0.848 | 0.835 | 1.000 | 0.865 | 0.767 | 1.000 | 0.770 | 0.811 | 1.000 | 0.778 | 0.804 | |

| Length | 0.831 | 0.602 | 0.069 | 0.831 | 0.604 | 0.069 | 0.911 | 0.368 | 0.101 | 0.915 | 0.369 | 0.101 |

| 0.608 | 0.589 | 0.813 | 0.602 | 0.588 | 0.734 | 0.578 | 0.651 | 0.775 | 0.586 | 0.677 | 0.761 | |

| Length | 0.467 | 0.397 | 0.071 | 0.443 | 0.409 | 0.073 | 0.457 | 0.314 | 0.100 | 0.465 | 0.336 | 0.101 |

| 0.652 | 0.663 | 0.950 | 0.648 | 0.656 | 0.922 | 0.590 | 0.750 | 0.911 | 0.600 | 0.766 | 0.910 | |

| Length | 0.505 | 0.518 | 0.198 | 0.502 | 0.526 | 0.240 | 0.473 | 0.494 | 0.342 | 0.476 | 0.503 | 0.357 |

| 0.674 | 0.683 | 0.968 | 0.668 | 0.673 | 0.942 | 0.617 | 0.777 | 0.921 | 0.626 | 0.782 | 0.923 | |

| Length | 0.566 | 0.570 | 0.613 | 0.562 | 0.575 | 0.592 | 0.535 | 0.617 | 0.660 | 0.541 | 0.623 | 0.658 |

| 0.642 | 0.659 | 0.950 | 0.630 | 0.650 | 0.927 | 0.586 | 0.758 | 0.908 | 0.602 | 0.770 | 0.910 | |

| Length | 0.496 | 0.511 | 0.248 | 0.493 | 0.518 | 0.291 | 0.479 | 0.521 | 0.341 | 0.485 | 0.529 | 0.355 |

| 0.218 | 0.190 | 0.667 | 0.219 | 0.206 | 0.574 | 0.136 | 0.216 | 0.456 | 0.157 | 0.258 | 0.423 | |

| Length | 0.032 | 0.027 | 0.019 | 0.031 | 0.027 | 0.019 | 0.020 | 0.010 | 0.005 | 0.020 | 0.010 | 0.005 |

| 0.527 | 0.513 | 0.877 | 0.560 | 0.536 | 0.861 | 0.499 | 0.627 | 0.825 | 0.497 | 0.618 | 0.840 | |

| Length | 0.248 | 0.229 | 0.064 | 0.277 | 0.248 | 0.090 | 0.255 | 0.171 | 0.083 | 0.247 | 0.165 | 0.094 |

| Weak | Moderate | Strong | |||||||

| 50 | |||||||||

| 0.883 | 0.946 | 0.924 | 0.809 | 0.881 | 0.726 | 0.778 | 0.759 | 0.594 | |

| Length | 0.087 | 0.022 | 0.005 | 0.087 | 0.022 | 0.005 | 0.087 | 0.022 | 0.005 |

| 0.859 | 0.909 | 0.924 | 0.797 | 0.814 | 0.730 | 0.770 | 0.668 | 0.614 | |

| Length | 0.118 | 0.024 | 0.006 | 0.131 | 0.026 | 0.006 | 0.132 | 0.027 | 0.006 |

| 0.862 | 0.959 | 0.991 | 0.790 | 0.928 | 0.947 | 0.808 | 0.892 | 0.939 | |

| Length | 0.067 | 0.022 | 0.010 | 0.091 | 0.037 | 0.017 | 0.109 | 0.053 | 0.027 |

| 0.943 | 0.991 | 1.000 | 0.891 | 0.963 | 0.962 | 0.888 | 0.907 | 0.918 | |

| Length | 0.247 | 0.063 | 0.021 | 0.241 | 0.068 | 0.021 | 0.234 | 0.074 | 0.021 |

| 0.918 | 0.976 | 0.991 | 0.862 | 0.948 | 0.957 | 0.863 | 0.906 | 0.943 | |

| Length | 0.139 | 0.031 | 0.010 | 0.168 | 0.047 | 0.019 | 0.181 | 0.064 | 0.028 |

| 0.718 | 0.945 | 0.995 | 0.610 | 0.874 | 0.935 | 0.559 | 0.738 | 0.862 | |

| Length | 0.024 | 0.025 | 0.015 | 0.027 | 0.023 | 0.015 | 0.027 | 0.022 | 0.014 |

| 0.723 | 0.878 | 0.934 | 0.703 | 0.888 | 0.919 | 0.683 | 0.833 | 0.921 | |

| Length | 0.020 | 0.006 | 0.000 | 0.041 | 0.021 | 0.011 | 0.048 | 0.035 | 0.021 |

| 0.802 | 0.916 | 0.916 | 0.795 | 0.861 | 0.839 | 0.786 | 0.822 | 0.738 | |

| Length | 0.261 | 0.066 | 0.016 | 0.261 | 0.066 | 0.016 | 0.261 | 0.066 | 0.016 |

| 0.801 | 0.908 | 0.926 | 0.789 | 0.845 | 0.863 | 0.763 | 0.806 | 0.761 | |

| Length | 0.305 | 0.076 | 0.017 | 0.283 | 0.079 | 0.018 | 0.281 | 0.082 | 0.018 |

| 0.523 | 0.804 | 0.923 | 0.484 | 0.746 | 0.907 | 0.523 | 0.717 | 0.860 | |

| Length | 0.046 | 0.024 | 0.011 | 0.047 | 0.031 | 0.018 | 0.052 | 0.036 | 0.022 |

| 0.820 | 0.965 | 0.987 | 0.791 | 0.942 | 0.971 | 0.792 | 0.900 | 0.918 | |

| Length | 0.321 | 0.169 | 0.034 | 0.313 | 0.168 | 0.036 | 0.311 | 0.164 | 0.036 |

| 0.728 | 0.893 | 0.949 | 0.690 | 0.850 | 0.935 | 0.707 | 0.838 | 0.904 | |

| Length | 0.209 | 0.061 | 0.018 | 0.203 | 0.066 | 0.024 | 0.210 | 0.072 | 0.029 |

| 0.421 | 0.651 | 0.831 | 0.379 | 0.577 | 0.744 | 0.401 | 0.550 | 0.658 | |

| Length | 0.020 | 0.010 | 0.006 | 0.020 | 0.010 | 0.007 | 0.020 | 0.010 | 0.007 |

| 0.330 | 0.631 | 0.836 | 0.302 | 0.692 | 0.839 | 0.352 | 0.655 | 0.788 | |

| Length | 0.007 | 0.007 | 0.005 | 0.009 | 0.019 | 0.010 | 0.015 | 0.020 | 0.014 |

-

1.

Estimate by in Bai, (2010).

-

2.

Estimate the pre-mean and post-mean by sample average for the pre-sample and the post-sample using as the break point. Denote the estimation as and .

-

3.

Estimate the variance by for each individual series:

for all .

-

4.

Estimate by where

-

5.

A 95% CI for : , where .

-

1.

Estimate by in Bhattacharjee et al., (2019)

-

2.

Estimate the pre-mean and post-mean by sample average for the pre-sample and the post-sample using as the break point. Denote the estimation as and .

-

3.

Estimate by some positive semi-definite estimator .

-

4.

Generate random vectors ,…, in from distribution .

-

5.

Generate if and if .

-

6.

Estimate by where

-

7.

Repeat step 4-6 for times to generate ,…,, and 95% CI for is , where and are the sample and quantiles based on ,…,.

References

- Aue and Horváth, (2013) Aue, A. and Horváth, L. (2013). Structural breaks in time series. Journal of Time Series Analysis, 34(1):1–16.

- Bai, (1994) Bai, J. (1994). Least squares estimation of a shift in linear processes. Journal of Time Series Analysis, 15(5):453–472.

- (3) Bai, J. (1997a). Estimating multiple breaks one at a time. Econometric Theory, 13(3):315–352.

- (4) Bai, J. (1997b). Estimation of a change point in multiple regression models. Review of Economics and Statistics, 4:551–563.

- Bai, (2010) Bai, J. (2010). Common breaks in means and variances for panel data. Journal of Econometrics, 157(1):78–92.

- Bai et al., (1998) Bai, J., Lumsdaine, R., and Stock, J. (1998). Testing for and dating common breaks in multivariate time series. Review of Economic Studies, 65:395–432.

- Bai and Perron, (1998) Bai, J. and Perron, P. (1998). Estimating and testing linear models with multiple structural changes. Econometrica, 66(1):47–78.

- Bai and Saranadasa, (1996) Bai, Z. and Saranadasa, H. (1996). Effect of high dimension: by an example of a two sample problem. Statistica Sinica, 6:311–329.

- Bhattacharjee et al., (2019) Bhattacharjee, M., Banerjee, M., and Michailidis, G. (2019). Change point estimation in panel data with temporal and cross-sectional dependence. arXiv preprint arXiv:1904.11101.

- Bhattacharya, (1987) Bhattacharya, P. K. (1987). Maximum likelihood estimation of a change-point in the distribution of independent random variables: General multiparameter case. Journal of Multivariate Analysis, 23:183–208.

- Birnbaum and Marshall, (1961) Birnbaum, Z. and Marshall, A. W. (1961). Some multivariate chebyshev inequalities with extensions to continuous parameter processes. The Annals of Mathematical Statistics, 32(3):687–703.

- Chang and Park, (2003) Chang, Y. and Park, J. Y. (2003). A sieve bootstrap for the test of a unit root. Journal of Time Series Analysis, 24(4):379–400.

- Chen et al., (2019) Chen, L., Wang, W., and Wu, W. (2019). Inference of break-points in high-dimensional time series. Available at SSRN 3378221.

- Chen and Qin, (2010) Chen, S.-X. and Qin, Y. (2010). A two sample test for high dimensional data with application to gene-set testing. Annals of Statistics, 38:808–835.

- Cho, (2016) Cho, H. (2016). Change-point detection in panel data via double cusum statistic. Electronic Journal of Statistics, 10(2):2000–2038.

- Cho and Fryzlewicz, (2015) Cho, H. and Fryzlewicz, P. (2015). Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77(2):475–507.

- Csörgő and Horváth, (1997) Csörgő, M. and Horváth, L. (1997). Limit Theorems in Change-Point Analysis. John Wiley & Sons Chichester.

- Enikeeva and Harchaoui, (2019) Enikeeva, F. and Harchaoui, Z. (2019). High-dimensional change-point detection with sparse alternatives. Annals of Statistics, 47(4):2051–2079.

- Fryzlewicz, (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection. The Annals of Statistics, 42(6):2243–2281.

- Hall and Heyde, (1980) Hall, P. and Heyde, C. C. (1980). Martingale Limit Theory and Its Application. Academic press.

- Hinkley, (1970) Hinkley, D. V. (1970). Inference about the change-point in a sequence of random variables. Biometrika, 57:1–17.

- Hinkley, (1972) Hinkley, D. V. (1972). Time-ordered classification. Biometrika, 59:509–523.

- Horváth and Hušková, (2012) Horváth, L. and Hušková, M. (2012). Change-point detection in panel data. Journal of Time Series Analysis, 33(4):631–648.

- Jeng et al., (2010) Jeng, Jessie, X., Cai, Tony, T., and Li, H. (2010). Optimal sparse segment identification with application in copy number variation analysis. Journal of the American Statistical Association, 105(491):1156–1166.

- Jirak, (2015) Jirak, M. (2015). Uniform change point tests in high dimension. The Annals of Statistics, 43(6):2451–2483.

- Perron, (2006) Perron, P. (2006). Dealing with structural breaks. Palgrave handbook of econometrics, 1(2):278–352.

- Picard, (1985) Picard, D. (1985). Testing and estimating change-points in time series. Journal of Applied Probability, 14:411–415.

- Rothman, (2012) Rothman, A. J. (2012). Positive definite estimators of large covariance matrices. Biometrika, 99(3):733–740.

- Shao, (2010) Shao, X. (2010). A self-normalized approach to confidence interval construction in time series. Journal of the Royal Statistical Society, Series, B, 72(3):343–366.

- Shao, (2015) Shao, X. (2015). Self-normalization for time series: a review of recent developments. Journal of the American Statistical Association, 110(512):1797–1817.

- Shao and Zhang, (2010) Shao, X. and Zhang, X. (2010). Testing for change points in time series. Journal of the American Statistical Association, 105(491):1228–1240.

- Stryhn, (1996) Stryhn, H. (1996). The location of the maximum of asymmetric two-sided brownian motion with triangular drift. Statistics and Probability Letters, 29(3):279–284.

- Van der Vaart and Wellner, (1996) Van der Vaart, A. and Wellner, J. (1996). Weak Convergence and Empirical Processes. Springer, New York.

- Wang and Shao, (2019) Wang, R. and Shao, X. (2019). Hypothesis testing for high-dimensional time series via self-normalization. Annals of Statistics, to appear.

- Wang et al., (2019) Wang, R., Volgushev, S., and Shao, X. (2019). Inference for change points in high dimensional data. Preprint, available at https://arxiv.org/abs/1905.08446.

- Wang and Samworth, (2018) Wang, T. and Samworth, R. J. (2018). High dimensional change point estimation via sparse projection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(1):57–83.

- Yao, (1987) Yao, Y. C. (1987). Approximating the distribution of the ml estimate of the change-point in a sequence of independent r.v.’s. Annals of Statistics, 3:1321–1328.

- Yu and Chen, (2017) Yu, M. and Chen, X. (2017). Finite sample change point inference and identification for high-dimensional mean vectors. arXiv preprint arXiv:1711.08747.

- Zhang and Siegmund, (2012) Zhang, N. R. and Siegmund, D. O. (2012). Model selection for high-dimensional multi-sequence change-point problems. Statistica Sinica, 22:1507–1538.

- Zhang et al., (2010) Zhang, N. R., Siegmund, D. O., Ji, H., and Li, J. Z. (2010). Detecting simultaneous changepoints in multiple sequences. Biometrika, 97(3):631–645.

6 Technical Appendix A

In this section, we gather some auxiliary results in Section 6.1, and present the proofs of all main theorems and corollaries. All the constants , , … stated in the appendix are generic and their specific values may vary from line to line and are not important.

6.1 Preliminary Results

The following identities will be used several times in the proof and are displayed in the following proposition.

Proposition 6.3.

For any ,

-

1.

-

2.

For the simplicity of the notations we denote as for .

Proposition 6.4.

Remark 6.5.

The centered Gaussian process can be regarded as a 2-D analogue of the standard Brownian motion. Suppose is an -by- matrix containing i.i.d. standard normal random variables, and we take as the standardized sum of all variables of in the region bounded by rows , and columns , , for any . As , . The proof of Proposition 6.4 can be found in Wang et al., (2019).

Proposition 6.6 (Tightness).

Remark 6.7.

Lemma 6.8 (Hájek-Rényi’s inequality (Birnbaum and Marshall, (1961) or Bai, (1994))).

Assume that is martingale difference sequence with variance , and is a non-increasing positive sequence of constants. Then for ,

Specifically, if ,

Proposition 6.9.

Under Assumption 2.2, for any positive and , there exists such that for all and sufficiently large and ,

Lemma 6.10.

Under Assumptions 2.2, for any fixed positive constant , we have the following results for some positive constants ,

-

(a)

.

-

(b)

.

-

(c)

.

-

(d)

, for any .

-

(e)

.

-

(f)

.

-

(g)

.

-

(h)

.

6.2 Proof of Lemma 2.1

Consider the case first. By the definition of ,

which is an increasing function of . Thus it achieves its maximum at where . By similar arguments, we see that when , , which achives the maximum when . This completes the proof.

6.3 Proof of Theorem 2.4

Assume first and we need to show for any , there exists , such that for any , ,

where . We further decompose , where , and . It is easy to see that the three sets and are disjoint for large enough , say .

For ,

Since as stated in Lemma 2.1,

Then

Notice that by Proposition 6.3,

By Lemma 6.10(a), the last three terms in the above inequalities are all . In addition,

where the bound for the first term is due to Lemma 6.8 by letting and , and the bounds for the second and third term are due to (b) and (c) in Lemma 6.10.

For , we need to decompose further as

Observing that the third term is always nonnegative, we want to show that it dominates the other terms with probability converging to 1, for every . Then is nonnegative for every with probability converging to 1. Specifically we want to show that for any fixed and for any , when , and are sufficiently large,

| (6.1) |

for all , and

| (6.2) |

To verify Equation (6.1), it follows from Lemma 6.10(a) that for ,

Hence for ,

By Proposition 6.3 we have

The remaining steps are to show is dominated by on the set , for all . Note that in this set, . To show the result, by Lemma 6.10(b), and are all , hence since by Assumption 2.2(d). So and are both asymptotically negligible.

It remains to deal with . Note that

For any , we want to show

This is equivalent to prove that for any positive ,

which was proved in Proposition 6.9. The proof is thus complete.

6.4 Proof of Theorem 2.5

In view of Proposition 6.6 which shows the tightness, we shall only present the proof for the finite-dimensional convergence. For any , it follows from Proposition 6.3 that

Here we only need to consider for any . For simplicity we assume is an integer. Since and , we have .

For ,

for some positive constant . Hence , for any fixed .

By a similar argument, for ,

since

and .

For , we note that

Hence .

The only remaining two terms are and . These two terms are not asymptotically negligible and we can employ martingale CLT to get the asymptotic distribution.

By Corollary 3.1 in Hall and Heyde, (1980), for any square-integrable martingale difference triangular array for with and is the natural filtration for , if

-

1.

(Lyapunov’s Condition), and

-

2.

then we have .

Consider any . Without loss of generality, assume there exists such that and , which means . For any , consider

where we define as

-

1.

, for ;

-

2.

, for ;

-

3.

, for

and define as the natural filtration of . It is easy to verify that is a martingale difference sequence adaptive to .

Then for ,

where we have applied the Cauchy-Schwartz inequality and Lemma 6.2. Furthermore we notice that

For , by essentially the same arguments,

and

For , we have

and

To verify the two conditions for the martingale CLT, we note that for the first condition,

For the second condition, we write

Define where , and we are going to show . For , , and

since

under Assumption 2.2(a) and . Thus . By exactly the same derivation, we have . For , , and

under Assumption 2.2(a). Thus . By a simple calculation we have , and . The proof for the consistency of and are skipped since the arguments are exactly the same.

Therefore, we prove that . So , where

It pays to look into a few special cases. Let , and , we have

which implies where is a standard Brownian Motion. Let , and , we have

Further, by letting , ,, for any , we have

The case can be shown by exactly the same argument, so we skip the details here. For the case that , i.e. and , we can also employ similar arguments. Consider for any ,

where we define as

-

1.

, for ;

-

2.

, for ;

-

3.

,for

and define as the natural filtration of . It is easy to verify that is a martingale difference sequence adaptive to .

By similar arguments, we can show and , where . To see the specific expression of , notice that for , . For , . And for , . Thus,

Letting , ,, for any , we have

where are two independent standard brownian motion defined on .