Sequential monitoring of changes in housing prices

Abstract.

We propose a sequential monitoring scheme to find structural breaks in real estate markets. The changes in the real estate prices are modeled by a combination of linear and autoregressive terms. The monitoring scheme is based on a detector and a suitably chosen boundary function. If the detector crosses the boundary function, a structural break is detected. We provide the asymptotics for the procedure under the stability null hypothesis and the stopping time under the change point alternative. Monte Carlo simulation is used to show the size and the power of our method under several conditions. We study the real estate markets in Boston, Los Angeles and at the national U.S. level. We find structural breaks in the markets, and we segment the data into stationary segments. It is observed that the autoregressive parameter is increasing but stays below 1.

Key words and phrases:

sequential change point detection, weak dependence, linear model, autoregressive model, real estate marketJEL classification. C32, C58, R30

1. Introduction

Housing has been the most substantial investment or cost for a large portion of the households so modeling changes in housing prices has received a considerable amount of attention in the literature. Following Case and Shiller (1989, 2003), Piazzesi and Schneider (2009) and Zheng et al. (2016) we write the change in the of the housing prices as a linear combination of macroeconomic fundamentals and we also include a first–order autoregressive term of the change in the housing prices. One of the fundamental questions is if the model stayed stable during the observation or it is segmented into several periods including stationary and nonstationary epochs. Himmelberg et al. (2005), Mayer (2011), Granziera and Kozicki (2015), Burnside et al. (2016) and Glaeser and Nathanson (2017) were interested in possible “bubbles” in housing prices, i.e. a short explosive segment in the data.

The historical prices of the U.S. real estate markets have gone through several periods of booms, like the California housing boom of the 1880s, the Florida land boom of the 1920s and the peaks in the national real estate market in the 1980s and 2000s. Providing a suitable model for the dynamics of the U.S. housing market has been an important theoretical question in the literature. The national wide booms of the 1980s and the 2000s show common as well as different features. Both booms started on the east coast and spread to the west. According to the S&P CoreLogic Case–Shiller Home Price Indices, Boston housing price increases peaked in early 2005, while Los Angeles real estate price increases reached their maximum in 2006, as the national level price. On the other hand, while the 1980s boom can be explained by a general economic expansion, the source of the housing price increase in the 2000s is different. It has been explained by the “amplification mechanism” of positive expectation of future housing price appreciation. Home buyers started to see real estate as an investment instrument. We refer to Case and Shiller (2003) and Shiller (2008) for more detailed reviews of the U.S. real estate market peaks. Our data example provides a sequential monitoring framework to see how this “amplification mechanism” evolves in the 2000s.

In this paper we develop and study a sequential monitoring scheme to detect changes in the parameters of a model which contains linear as well as autoregressive terms. The assumptions on the regressors and the errors are mild, and they are satisfied by nearly all linear as well as nonlinear time series processes. Roughly speaking, they are well approximated with finitely dependent sequences. Under the null hypothesis the model describing the price changes is stable, i.e. it is a stationary process. Following Chu et al. (1996), the proposed monitoring is based on a detector and a boundary function. When the detector reaches the boundary function, a change is detected. The detector is based on the sum of residuals, but only the training sample is used to estimate some unknown parameters. The boundary function is chosen such that the probability of a false detection under the stability of the parameters null hypothesis is fixed. We also provide results for the consistency of the monitoring under various types of changes in the original model. In the sequential setup consistency means that we stop in finite time with probability one if a change occurred. We also provide several results on the distribution of the stopping time under the alternative. The limits can be normal or not normal depending on the type of the change and the size of the change. We focus on the autoregressive parameter and after the change we can have a new stationary regime, random walk or explosive autoregressive process.

The paper is organized as follows: in Section 2 we formulate our model and the detection scheme. We also detail the conditions which are needed in the paper and obtain the limit distribution of the monitoring under the null hypothesis. Section 3 contains the distributions of the stopping time introduced in Section 2 under three types of alternatives. Detailed proofs are given in Appendices A and B. We study the empirical size and power of the sequential scheme in Section 4. Section 5 provides in illustration for our method using data on three U.S. real estate markets. The conclusion of our research is in Section 6.

2. Mathematical model to sequentially detect changes in real estate prices

In our model we assume that a training (historical) sample of size is available

| (2.1) |

where and

| (2.2) |

The model in (2.1) combines linear and autoregressive models. It is a linear model in the first coordinates and autoregressive in the last coordinate of . After the training sample further observations are obtained, and under the null hypothesis

| (2.6) |

This means that the structure of the observations is the same during the training sample and the observations collected after the training sample obey the same model. Under the alternative the structure of the observations changes at an unknown time :

| (2.9) |

The first monitoring scheme to find changes in the regression parameter was introduced by Chu et al. (1996) and it has become the starting point of substantial research. Zeileis et al. (2005) and Aue et al. (2014) studied monitoring schemes in linear models with dependent errors. Kirch (2007, 2008) and Hušková and Kirch (2012) provided resampling methods to find critical values for sequential monitoring.

Hlávka et al. (2012) investigated the sequential detection of changes of the parameter in autoregressive models, i.e. no regression terms are included in their theory. Homm and Breiting (2012) compared several methods to find bubbles in stock markets, detecting a change in an autoregressive process to an explosive one. Horváth et al. (2019+) showed that sequential methods will detect changes when the observations change from stationarity to mild non–stationarity.

The least square estimator for is given by

where and

Following Chu et al. (1996) we choose a detector , a boundary function , and define the stopping time

If , we stop at time and we say that the null hypothesis is rejected. We choose the detector and the boundary such that

| (2.10) |

where is prescribed number and

| (2.11) |

According to (2.10), the probability of stopping the procedure and rejecting , when , is . We stop in finite time under the alternative. The definition of the detector follows Chu et al. (1996) and Horváth et al. (2004).

The residuals of the model are defined as

| (2.12) |

i.e. in the definition of the residuals we also use even after the training period. The ’s are stationary in the training sample under the null as well as under the alternative. Our detector is

where

We use the boundary function

| (2.13) |

where is chosen such that (2.10) holds under the null hypothesis and

| (2.14) |

We discuss the choice of in Section 4. Following Brown et al. (1975), Horváth et al. (2004) also used recursive residuals to define the detector in case of linear regression ( under the null and the alternative). Homm and Breiting (2012) applied fluctuation detectors when they wanted to test if a random walk changes to an explosive autoregression. They did not allow regression terms.

Next we discuss some conditions which will be needed to find for our boundary function such that (2.10) holds. Let

The Euclidean norm of vectors and matrices is denoted by .

Assumption 2.1.

where is a nonrandom functional defined on with values in and is a measurable space. Also, is jointly measurable in and are independent and identically distributed random variables in . The sequences can be approximated with –dependent sequences in the sense that with some , and , ,

| (2.15) |

where and the ’s are independent copies of , independent of

Assumption 2.1 appeared first in Ibragimov (1959, 1962) in the proof of the central limit theorem for dependent variables. Billingsley (1968) also utilized –decomposability. Nearly all time series, including linear and several nonlinear processes satisfy Assumption 2.1 (cf. Hörmann and Kokoszka, 2010 and Aue et al., 2014).

Assumption 2.2.

, and for all

Assumption 2.2 means that and are uncorrelated sequences. Clearly, if the ’s are independent random variables, Assumption 2.2 holds but it is also satisfied by ARCH/GARCH type volatility sequences and orthogonal martingales. We show in Lemma A.2 that

| (2.16) |

Assumption 2.3.

is nonsingular.

The asymptotic normality of has been established in case of independent and identically distributed ’s (cf. Zeckenhauser and Thompson, 1970). These results are extended by Wu (2007), Zhu (2013) and Caron (2019) to a large class of estimators for time series errors.

Theorem 2.1.

We note that is not allowed in Theorem 2.1 since in this case the limit distribution would be infinity. Horváth et al. (2007) studied the “square–root–boundary” case, i.e. when , and they obtained a Darling–Erdős type extreme value result for the limit distribution of the stopping time under the no change null hypothesis in linear regression. Chu et al. (1996) obtained an upper bound for the probability of false stopping under the null hypothesis (cf. Homm and Breitung, 2012).

The stopping time is an open ended since if there is no change we never stop collecting further observations. In some applications we might want to stop at time , i.e. only observations are collected after the training period. Let

denote the closed end version of . Let and define

Remark 2.1.

3. Asymptotic distribution of the stopping time under the alternative

In this section we investigate the properties of the sequential detection rule when the regression is not stable. Our procedure is tailored for early changes, i.e. is small, so we assume in this section that the changes occur early. We concentrate on the autoregressive parameter . We consider the cases (i) the observations stay stationary after the change, (ii) they change to a “unit root” sequence and (iii) explosive autoregression after the change.

First we assume that the regression parameter at time changes from to satisfying

Assumption 3.1.

So for any fixed , the sequence changes from a stationary segment to an other stationary one. We allow that , i.e. the difference between the regression parameters can be small. We measure the size of change with

where with

| (3.1) |

and . Under the alternative converges in distribution to . The assumption says that the size of the change cannot be too small:

Assumption 3.2.

Analogue of Assumption 3.2 first appeared in retrospective change point detection in Picard (1985) and Dümbgen (1991) when the time of change in the mean was estimated.

Next we show that the upper bound for in Theorem 3.1 is the best possible when we get the asymptotic normality of . Let

and

Theorem 3.2.

Aue and Horváth (2004) proved Theorem 3.1 when the mean can change under the alternative. Their result was extended to linear regression by Horváth et al. (2007).

Next we consider the case when changes to a random walk at time :

Assumption 3.3.

and the other parameters in the regression also might change

Assumption 3.4.

To describe the size of change we introduce

where .

Theorem 3.3.

Remark 3.1.

If , i.e. only the autoregressive parameter changes, then . In this case

for all .

Let

and

with

In Theorem 3.3 and Remark 3.1 the change to a random walk in the autoregressive part dominates the limit distribution. Hence is a partial sum after and the limit is determined by the sums of partial sum processes. In the next result the change in the regression parameters are larger than in Theorem 3.3 and while is still a random walk after the change, we have the same limit as in Theorem 3.2.

Theorem 3.4.

Next we consider the case when the sequence turns explosive after the change at time . Now we replace Assumption 3.3 with

Assumption 3.5.

Let

| (3.7) |

and define

It follows from Assumption 2.1 that the infinite series defining is finite with probability 1.

Assumption 3.5 is often used to find “bubbles” in financial data. Phillips and Yu (2011) and Phillips et al. (2014, 2015a,b) estimated the autoregressive parameter in an AR(1) sequence and if the estimate is significantly larger than 1, a “bubble” is detected. For a survey on “bubble” detection we refer to Homm and Breiting (2012).

4. Monte Carlo simulations

In this section we investigate the performance of our limit theorems in case of a finite training sample of size . Preliminary results showed that the boundary of (2.13) over rejects when holds. The false positive rates were improved when the boundary function

| (4.1) |

where . The values of are defined from the equation

| (4.2) |

Since the correction term

under the conditions of Theorem 2.1

| (4.3) |

and under the alternatives in Theorems 3.1–3.5

| (4.4) |

| 0.010 | 0.025 | 0.050 | 0.100 | 0.250 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 2.7912 | 2.4948 | 2.2365 | 1.9497 | 1.5213 | ||||||||||

| 0.15 | 2.8516 | 2.5475 | 2.2996 | 2.0273 | 1.6126 | ||||||||||

| 0.25 | 2.9445 | 2.6396 | 2.3860 | 2.1060 | 1.7039 | ||||||||||

| 0.35 | 3.0475 | 2.7394 | 2.5050 | 2.2433 | 1.8467 | ||||||||||

| 0.45 | 3.3015 | 3.0144 | 2.7992 | 2.5437 | 2.1729 | ||||||||||

| 0.49 | 3.5705 | 3.2944 | 3.0722 | 2.8259 | 2.4487 |

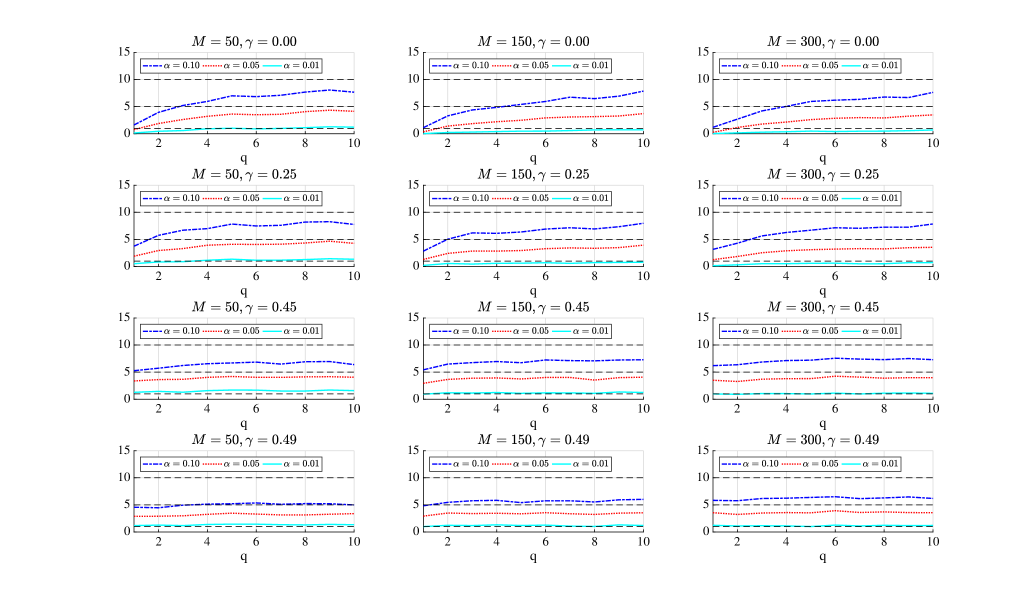

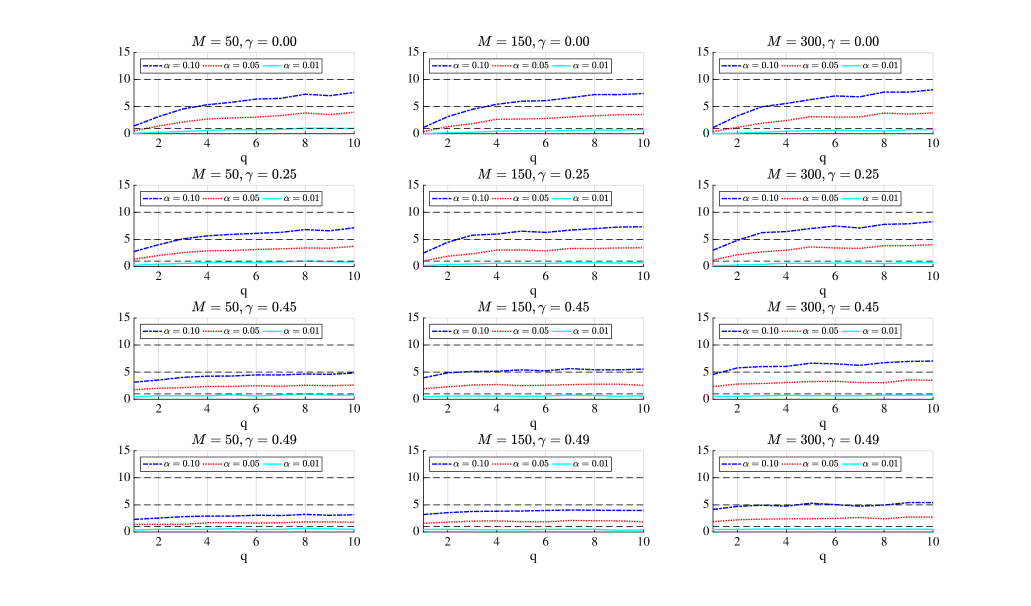

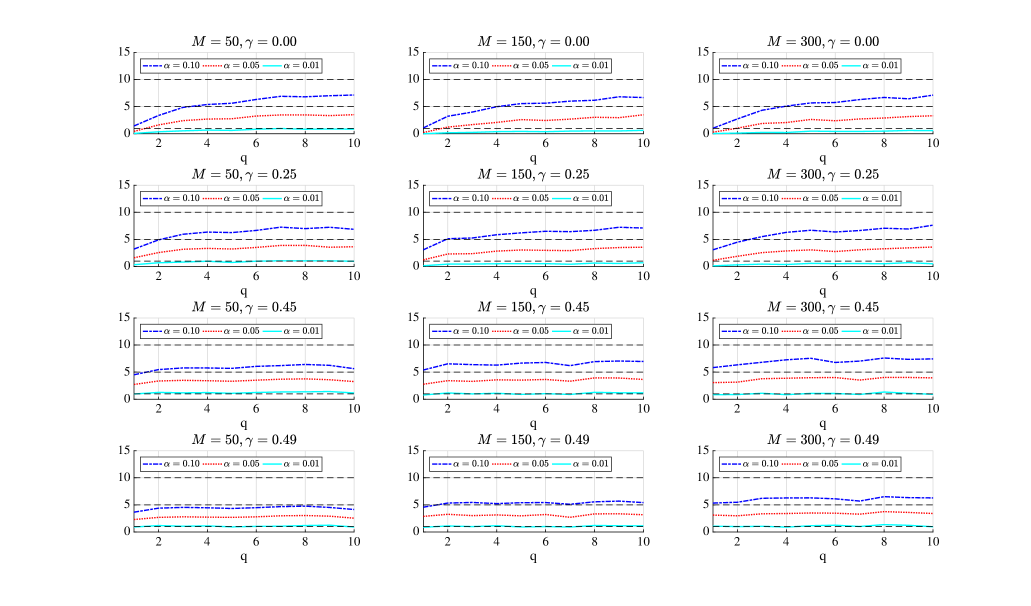

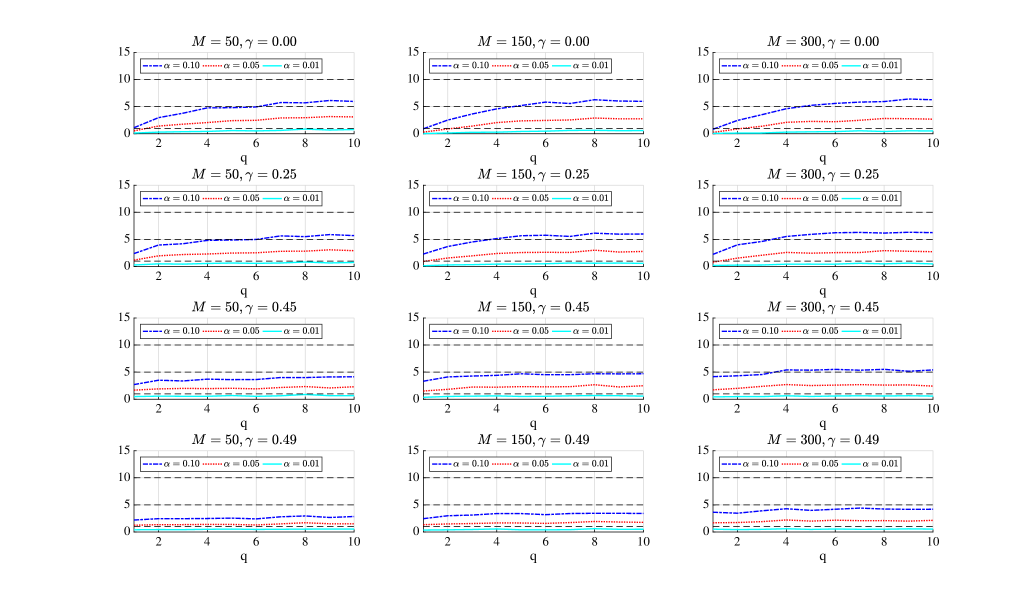

The critical values of (4.2) were reported in Horváth et al. (2004) and for convenience we provide them in Table 4.1. The results in Table 4.1 are based on repetitions of . The Wiener process was approximated on a grid of 10,000 equi–spaced points in [0,1]. We chose in our simulations and under the null hypothesis and the autoregressive parameter was Our procedure is open ended but, of course, during the simulations we stopped the testing after additional observations were collected in the detection period. In Figures 4.1–4.4 we exhibit the number of false alarms before time . We used the boundary function of (4.1) with and the size of the training sample was and . The results are based on 10,000 repetitions. Under the null hypothesis we considered the following data generating processes:

DGP(i)

| (4.5) |

where the ’s are independent, identically distributed standard normal random variables. Also, the forms a GARCH(1,1) process defined by

| (4.6) |

where the ’s are independent, standard normal random variables, independent of . We used to get the values in Figure 4.1.

DGP(ii) satisfy (4.5) but now are independent and identically distributed standard normal random variables, independent of . The variables are independent standard normal random variables.

DGP(iii) Now in addition to (4.6), the explanatory sequences are also given by GARCH(1,1) processes

| (4.7) |

where the innovations are standard normal random variables, independent of of DGP(i). We used , and

.

DGP(iv) The explanatory variables satisfy (4.7) but now which are independent and identically distrubuted standard normal random variables. The variables are independent, standard normal random, independent of .

In our Monte Carlo simulations the variables and are independent. In case of DGP(i) and (iii), the coordinates of are independent while strongly dependent under DGP(ii) and (iv). The simulation results in Figures 4.1–4.4 show good performance, the empirical rate of false detections is at the described level. The structure of the ’s has little effect on false detection.

Next we consider the behaviour of the monitoring scheme under the alternatives discussed in Theorems 3.1–3.5. We recall that under

| (4.8) |

The explanatory variables are generated as in DGP(ii), i.e. dependent AR(1) sequences. The variables are independent standard normals or GARCH (1,1) sequences. As before, we used the boundary function of (4.1). The significance levels were and . We considered the following data generating processes:

DGP(v) We used the initial values which changes to

at time after the training sample. The errors are independent and identically distributed random variables, independent of .

DGP(vi) The data generating process is as in DGP(v) but now is given by the GARCH (1,1) sequence

| (4.9) |

where are independent standard normal random variables, independent of .

DGP(vii). In this case , but changes to and . As in DGP(v), the ’s are independent standard normals, independent of .

DGP(viii) We have the same parameters as in DGP(vii) but now is a GARCH(1,1) sequence satisfying (4.9).

DGP(ix) The initial values are the same as in DGP(v)–DGP(viii) but now as in DGP(v) but and . The variables are independent standard normals.

DGP(x) The assumptions are the same as in DGP(ix) but now we use the GRACH(1,1) sequence of (4.9) to generate the ’s.

DGP(xi) The values of and are the same as in DGP(ix) and DGP(x), but now = 1.01, 1.05, 1.10 and 1.25. The variables are independent standard normals.

DGP(xii) The assumptions are the same as in DGP(xi) but now we use the GRACH(1,1) sequence of (4.9) to generate the ’s.

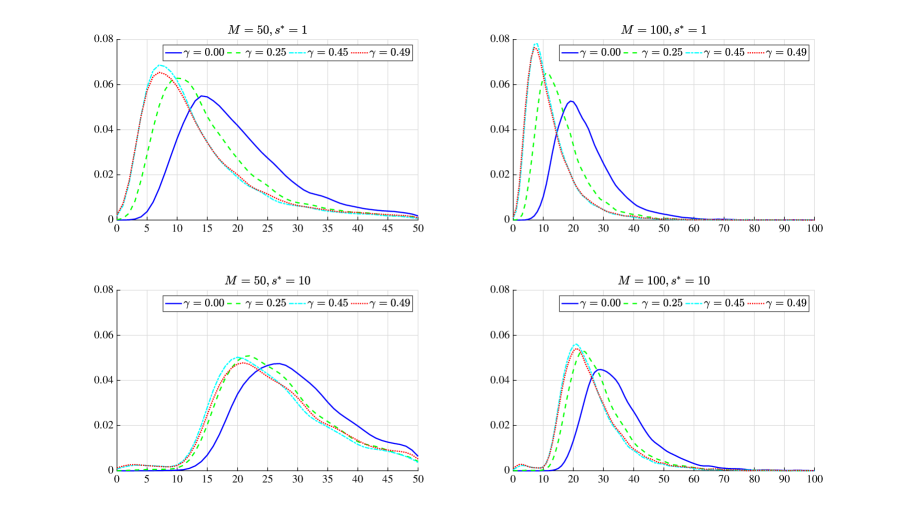

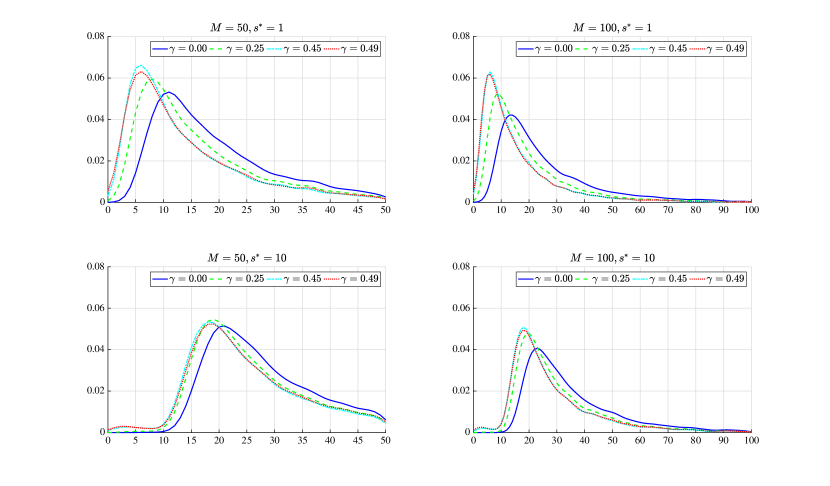

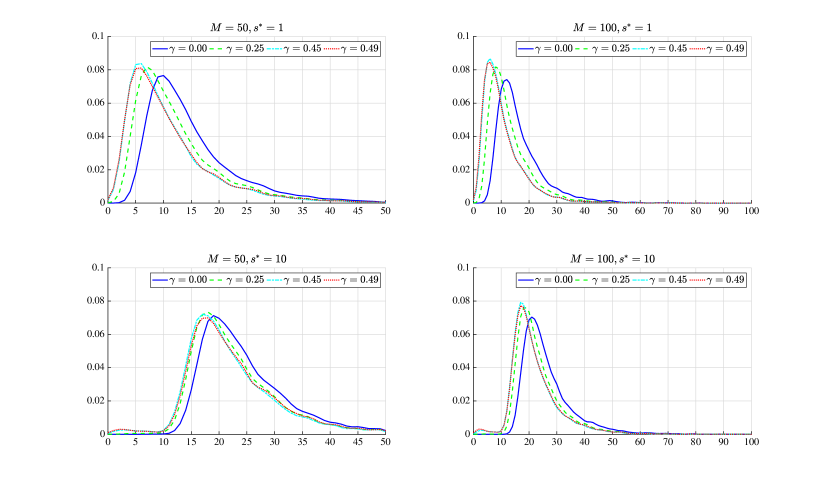

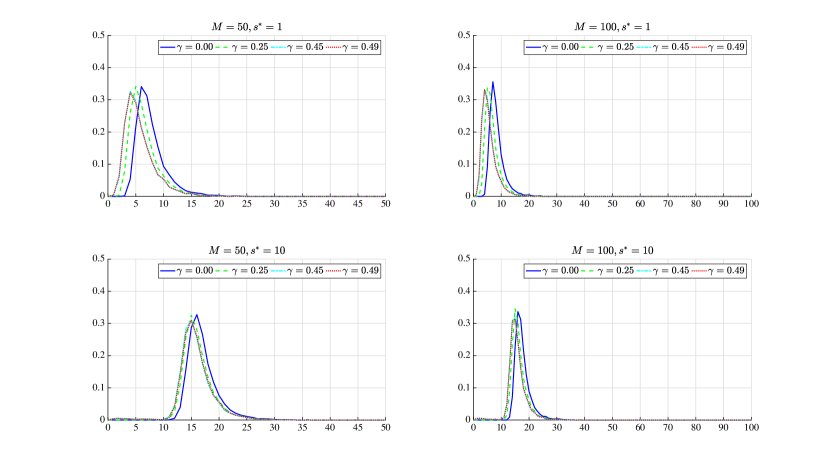

The results of the simulations are given in Tables 4.2–4.8. The empirical probability of stopping under the alternative is high in all cases we considered. The power increases with except with slight drop at which is very close to the boundary case. The rate of convergence to the limit slows with the increase of which is a possible explanation for the unexpected slight drop in power. Also the results show that our method is tailored to detect early changes, i.e. when is small. As expected, the power is increasing in Tables 4.3–4.6 as gets closer to 1. Allowing to differ, we increased the power substantially for and but only mildly for and 1. In this case the change to partial sum dominates the power. Based on our simulation study, we recommend to achieve fast and reliable detection. This recommendation is also confirmed in Figures 4.5–4.8, where the empirical density of the stopping time is exhibited under different assumptions. We note that according to Theorems 3.2 and 3.4, the limit distributions on Figure 4.5 and 4.7 can be approximated with normal densities as . The empirical densities have longer right tails than a normal density but they are clearly approaching a normal density. By Theorem 3.3, the limits of the empirical densities on Figure 4.6 are not normal densities (cf. Remark 3.1). The limit distribution in Theorem 3.5 is not necessarily normal. However, if the are jointly normal, then the variable of (3.7) is normally distributed. In Figure 4.8 the exhibited density is not derived from a normal distribution due to (4.9), the errors are only conditionally normal. Comparing Figures 4.5–4.8, one sees that the limit distributions are getting less spread as increases, i.e. we need less and less observations to detect the change.

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | |

| DGP(v) | ||||||||||||

| 0 | 87.64 | 80.75 | 62.63 | 99.64 | 99.07 | 95.98 | 72.68 | 61.53 | 40.26 | 98.78 | 97.53 | 92.44 |

| 0.25 | 91.00 | 86.08 | 72.70 | 99.75 | 99.52 | 97.91 | 77.57 | 68.88 | 50.09 | 99.29 | 98.52 | 95.70 |

| 0.45 | 89.67 | 85.29 | 74.78 | 99.71 | 99.47 | 98.25 | 73.80 | 66.07 | 51.13 | 99.03 | 98.39 | 96.06 |

| 0.49 | 86.31 | 81.29 | 70.45 | 99.54 | 99.22 | 97.71 | 67.56 | 60.53 | 45.82 | 98.53 | 97.66 | 94.61 |

| DGP(vi) | ||||||||||||

| 0 | 98.53 | 97.08 | 91.73 | 99.96 | 99.90 | 99.76 | 94.23 | 90.18 | 78.52 | 99.96 | 99.91 | 99.38 |

| 0.25 | 99.14 | 98.23 | 94.57 | 99.97 | 99.95 | 99.86 | 95.70 | 93.25 | 84.49 | 99.99 | 99.94 | 99.65 |

| 0.45 | 98.80 | 97.88 | 95.00 | 99.98 | 99.95 | 99.86 | 94.75 | 92.19 | 85.10 | 99.95 | 99.94 | 99.69 |

| 0.49 | 98.12 | 97.09 | 93.90 | 99.95 | 99.92 | 99.81 | 92.74 | 89.91 | 82.30 | 99.94 | 99.90 | 99.62 |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 73.61 | 65.89 | 52.28 | 88.13 | 82.27 | 70.43 | 62.16 | 54.38 | 40.15 | 84.16 | 77.53 | 64.44 | |

| 0.25 | 81.25 | 74.96 | 62.56 | 93.96 | 90.45 | 81.93 | 68.30 | 61.39 | 48.28 | 90.07 | 85.64 | 74.94 | |

| 0.45 | 82.13 | 77.26 | 67.44 | 95.33 | 93.00 | 87.26 | 66.81 | 61.00 | 50.56 | 90.69 | 87.31 | 79.50 | |

| 0.49 | 78.92 | 74.49 | 65.13 | 94.13 | 91.80 | 86.25 | 62.63 | 57.62 | 47.11 | 88.50 | 85.22 | 77.39 | |

| 0 | 86.12 | 81.37 | 71.56 | 96.32 | 94.45 | 89.09 | 76.66 | 70.76 | 59.95 | 94.63 | 91.81 | 85.13 | |

| 0.25 | 90.51 | 86.91 | 78.61 | 98.24 | 97.05 | 94.09 | 81.09 | 75.91 | 66.23 | 96.91 | 95.33 | 90.52 | |

| 0.45 | 90.68 | 88.00 | 81.87 | 98.61 | 97.97 | 95.99 | 79.84 | 75.47 | 67.84 | 97.11 | 95.88 | 92.70 | |

| 0.49 | 88.95 | 86.32 | 80.19 | 98.27 | 97.56 | 95.60 | 76.43 | 72.82 | 65.31 | 96.32 | 95.05 | 91.66 | |

| 0 | 92.84 | 90.41 | 84.54 | 98.99 | 98.36 | 96.96 | 86.69 | 82.86 | 75.06 | 98.74 | 97.80 | 95.51 | |

| 0.25 | 95.11 | 93.22 | 88.93 | 99.60 | 99.27 | 98.34 | 89.33 | 86.14 | 79.35 | 99.34 | 98.83 | 97.34 | |

| 0.45 | 95.22 | 93.76 | 90.50 | 99.70 | 99.51 | 98.91 | 88.48 | 85.96 | 80.46 | 99.34 | 98.97 | 97.95 | |

| 0.49 | 94.23 | 92.87 | 89.39 | 99.60 | 99.39 | 98.78 | 86.66 | 83.87 | 78.58 | 99.11 | 98.71 | 97.68 | |

| 0 | 93.67 | 91.50 | 86.86 | 99.36 | 98.88 | 97.78 | 88.50 | 85.55 | 78.53 | 99.15 | 98.49 | 96.91 | |

| 0.25 | 95.49 | 93.86 | 90.25 | 99.74 | 99.52 | 98.85 | 90.62 | 88.16 | 82.35 | 99.56 | 99.18 | 98.20 | |

| 0.45 | 95.70 | 94.32 | 91.73 | 99.83 | 99.66 | 99.34 | 89.97 | 87.93 | 83.29 | 99.50 | 99.27 | 98.60 | |

| 0.49 | 94.72 | 93.58 | 90.83 | 99.72 | 99.61 | 99.16 | 88.54 | 86.44 | 81.68 | 99.35 | 99.16 | 98.42 | |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 75.13 | 68.33 | 55.77 | 88.99 | 84.01 | 74.10 | 64.15 | 57.01 | 44.35 | 85.80 | 80.24 | 68.90 | |

| 0.25 | 82.01 | 76.59 | 65.66 | 94.00 | 91.02 | 83.63 | 70.26 | 63.71 | 51.88 | 90.93 | 87.07 | 77.96 | |

| 0.45 | 82.89 | 78.76 | 70.23 | 95.14 | 93.08 | 88.17 | 69.26 | 64.15 | 54.44 | 91.39 | 88.58 | 81.78 | |

| 0.49 | 80.38 | 76.63 | 68.24 | 94.06 | 91.94 | 87.24 | 65.49 | 60.84 | 51.73 | 89.50 | 86.69 | 80.09 | |

| 0 | 86.77 | 82.47 | 73.56 | 96.73 | 94.85 | 90.20 | 77.44 | 72.22 | 61.89 | 95.15 | 92.93 | 87.36 | |

| 0.25 | 90.70 | 87.57 | 80.45 | 98.38 | 97.38 | 94.43 | 81.78 | 77.03 | 68.42 | 97.07 | 95.65 | 91.87 | |

| 0.45 | 91.18 | 88.73 | 83.39 | 98.60 | 97.93 | 96.18 | 80.99 | 77.18 | 70.27 | 97.06 | 96.19 | 93.42 | |

| 0.49 | 89.68 | 87.36 | 81.97 | 98.33 | 97.56 | 95.75 | 78.23 | 74.78 | 67.93 | 96.51 | 95.49 | 92.63 | |

| 0 | 93.38 | 90.80 | 86.08 | 99.23 | 98.73 | 97.24 | 86.59 | 82.91 | 76.30 | 98.60 | 97.75 | 95.80 | |

| 0.25 | 95.32 | 93.72 | 89.67 | 99.55 | 99.34 | 98.58 | 89.39 | 86.40 | 80.28 | 99.06 | 98.70 | 97.48 | |

| 0.45 | 95.51 | 94.18 | 91.20 | 99.66 | 99.46 | 98.96 | 88.82 | 86.26 | 81.38 | 99.07 | 98.76 | 97.89 | |

| 0.49 | 94.68 | 93.34 | 90.58 | 99.53 | 99.38 | 98.85 | 86.99 | 84.61 | 80.07 | 98.90 | 98.43 | 97.67 | |

| 0 | 94.48 | 92.64 | 88.34 | 99.48 | 99.07 | 98.14 | 88.52 | 85.27 | 79.45 | 99.01 | 98.51 | 97.22 | |

| 0.25 | 96.28 | 94.69 | 91.41 | 99.71 | 99.55 | 99.05 | 90.78 | 88.20 | 82.92 | 99.34 | 99.02 | 98.22 | |

| 0.45 | 96.32 | 95.20 | 92.71 | 99.77 | 99.63 | 99.32 | 90.32 | 88.17 | 83.80 | 99.38 | 99.14 | 98.53 | |

| 0.49 | 95.55 | 94.44 | 91.97 | 99.74 | 99.58 | 99.24 | 88.80 | 86.81 | 82.64 | 99.19 | 98.97 | 98.31 | |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 90.28 | 86.93 | 80.03 | 98.74 | 98.01 | 95.81 | 81.91 | 77.41 | 68.04 | 97.90 | 96.75 | 94.03 | |

| 0.25 | 93.28 | 90.73 | 84.82 | 99.36 | 99.01 | 97.68 | 85.13 | 81.13 | 73.23 | 98.84 | 98.06 | 96.02 | |

| 0.45 | 93.53 | 91.35 | 86.92 | 99.51 | 99.23 | 98.46 | 83.84 | 80.78 | 74.35 | 98.84 | 98.30 | 96.64 | |

| 0.49 | 92.14 | 90.05 | 85.37 | 99.38 | 99.10 | 98.22 | 81.44 | 78.20 | 71.89 | 98.51 | 97.84 | 96.27 | |

| 0 | 95.29 | 93.55 | 89.47 | 99.75 | 99.51 | 98.89 | 90.00 | 86.92 | 80.91 | 99.42 | 99.09 | 98.07 | |

| 0.25 | 96.90 | 95.56 | 92.63 | 99.92 | 99.78 | 99.41 | 91.93 | 89.54 | 84.02 | 99.70 | 99.48 | 98.87 | |

| 0.45 | 96.94 | 95.91 | 93.84 | 99.93 | 99.86 | 99.61 | 91.25 | 89.16 | 84.76 | 99.63 | 99.48 | 99.12 | |

| 0.49 | 96.23 | 95.30 | 93.07 | 99.88 | 99.82 | 99.54 | 89.69 | 87.65 | 83.25 | 99.54 | 99.37 | 98.96 | |

| 0 | 97.61 | 96.79 | 94.85 | 99.94 | 99.90 | 99.67 | 94.07 | 92.33 | 88.86 | 99.82 | 99.78 | 99.45 | |

| 0.25 | 98.40 | 97.68 | 96.40 | 99.97 | 99.95 | 99.88 | 95.27 | 93.92 | 90.87 | 99.89 | 99.82 | 99.70 | |

| 0.45 | 98.47 | 97.96 | 96.87 | 99.97 | 99.95 | 99.92 | 94.90 | 93.68 | 91.31 | 99.89 | 99.85 | 99.76 | |

| 0.49 | 98.08 | 97.63 | 96.48 | 99.97 | 99.95 | 99.91 | 93.98 | 92.92 | 90.52 | 99.87 | 99.82 | 99.72 | |

| 0 | 98.02 | 97.18 | 95.47 | 99.97 | 99.89 | 99.79 | 94.92 | 93.37 | 90.47 | 99.85 | 99.80 | 99.69 | |

| 0.25 | 98.62 | 97.99 | 96.68 | 99.98 | 99.97 | 99.87 | 96.13 | 94.69 | 92.13 | 99.94 | 99.86 | 99.78 | |

| 0.45 | 98.66 | 98.05 | 97.18 | 99.98 | 99.98 | 99.92 | 95.73 | 94.45 | 92.50 | 99.95 | 99.89 | 99.80 | |

| 0.49 | 98.21 | 97.80 | 96.83 | 99.98 | 99.97 | 99.91 | 94.75 | 93.73 | 91.82 | 99.89 | 99.86 | 99.78 | |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 97.23 | 95.82 | 92.95 | 99.89 | 99.80 | 99.59 | 93.21 | 90.62 | 85.31 | 99.80 | 99.63 | 99.23 | |

| 0.25 | 98.24 | 97.34 | 94.90 | 99.97 | 99.92 | 99.75 | 94.66 | 92.74 | 88.30 | 99.89 | 99.83 | 99.54 | |

| 0.45 | 98.17 | 97.38 | 95.64 | 99.97 | 99.94 | 99.85 | 94.14 | 92.69 | 88.91 | 99.87 | 99.82 | 99.62 | |

| 0.49 | 97.62 | 96.93 | 95.13 | 99.96 | 99.92 | 99.77 | 93.01 | 91.32 | 87.77 | 99.86 | 99.73 | 99.54 | |

| 0 | 98.88 | 98.36 | 96.95 | 99.98 | 99.97 | 99.92 | 96.67 | 95.42 | 92.57 | 99.93 | 99.88 | 99.81 | |

| 0.25 | 99.26 | 98.94 | 98.00 | 100.00 | 100.00 | 99.98 | 97.41 | 96.49 | 94.28 | 99.94 | 99.93 | 99.88 | |

| 0.45 | 99.25 | 98.96 | 98.34 | 100.00 | 100.00 | 99.99 | 97.18 | 96.40 | 94.59 | 99.93 | 99.93 | 99.89 | |

| 0.49 | 99.09 | 98.80 | 98.12 | 100.00 | 100.00 | 99.98 | 96.57 | 95.76 | 93.94 | 99.93 | 99.92 | 99.87 | |

| 0 | 99.47 | 99.28 | 98.69 | 99.99 | 99.98 | 99.97 | 98.09 | 97.56 | 95.93 | 99.98 | 99.96 | 99.94 | |

| 0.25 | 99.62 | 99.48 | 99.13 | 100.00 | 100.00 | 99.99 | 98.57 | 98.04 | 96.90 | 99.99 | 99.99 | 99.96 | |

| 0.45 | 99.61 | 99.54 | 99.22 | 100.00 | 100.00 | 100.00 | 98.47 | 98.04 | 97.10 | 99.99 | 99.99 | 99.96 | |

| 0.49 | 99.55 | 99.44 | 99.15 | 100.00 | 100.00 | 100.00 | 98.14 | 97.76 | 96.67 | 99.99 | 99.96 | 99.96 | |

| 0 | 99.58 | 99.36 | 98.96 | 100.00 | 99.99 | 99.98 | 98.42 | 97.84 | 96.58 | 99.99 | 99.97 | 99.94 | |

| 0.25 | 99.71 | 99.56 | 99.28 | 100.00 | 100.00 | 99.99 | 98.82 | 98.27 | 97.38 | 99.99 | 99.99 | 99.97 | |

| 0.45 | 99.69 | 99.56 | 99.38 | 100.00 | 100.00 | 100.00 | 98.72 | 98.25 | 97.58 | 99.99 | 99.99 | 99.97 | |

| 0.49 | 99.59 | 99.51 | 99.29 | 100.00 | 100.00 | 100.00 | 98.33 | 98.00 | 97.16 | 99.99 | 99.98 | 99.96 | |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 99.98 | 99.98 | 99.97 | 100.00 | 100.00 | 100.00 | 99.94 | 99.87 | 99.74 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 99.98 | 99.98 | 99.98 | 100.00 | 100.00 | 100.00 | 99.96 | 99.93 | 99.80 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 99.99 | 99.99 | 99.98 | 100.00 | 100.00 | 100.00 | 99.95 | 99.93 | 99.84 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 99.99 | 99.99 | 99.98 | 100.00 | 100.00 | 100.00 | 99.93 | 99.91 | 99.80 | 100.00 | 100.00 | 100.00 | |

| 0 | 99.98 | 99.98 | 99.94 | 100.00 | 100.00 | 100.00 | 99.96 | 99.96 | 99.89 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 99.98 | 99.98 | 99.97 | 100.00 | 100.00 | 100.00 | 99.99 | 99.96 | 99.93 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 99.98 | 99.98 | 99.97 | 100.00 | 100.00 | 100.00 | 99.97 | 99.97 | 99.94 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 99.98 | 99.97 | 99.97 | 100.00 | 100.00 | 100.00 | 99.97 | 99.96 | 99.92 | 100.00 | 100.00 | 100.00 | |

| 0 | 100.00 | 100.00 | 99.99 | 100.00 | 100.00 | 100.00 | 99.97 | 99.95 | 99.91 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.98 | 99.97 | 99.94 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.98 | 99.97 | 99.95 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.97 | 99.95 | 99.93 | 100.00 | 100.00 | 100.00 | |

| 0 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.98 | 99.98 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 99.98 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 99.98 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.98 | 99.98 | 100.00 | 100.00 | 100.00 | |

| 0 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 99.98 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 99.99 | 99.99 | 99.99 | 100.00 | 100.00 | 100.00 | |

| 0 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.25 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.45 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

| 0.49 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | |

5. An application to housing prices in the U.S.A. at the national level, in the Los Angeles and Boston markets

In this section, as an example for our theory, we focus on the U.S. housing prices to illustrate our online monitoring procedure. The literature has discussed the link of housing prices to macroeconomic fundamental variables using linear regression model.

The fundamental variables frequently applied in the literature include personal income per capita, mortgage interest rate, employment on the demand side and housing starts on the supply side. These variables are used to explain the dynamics of U.S. real estate prices in the long run horizon (Case and Shiller, 2003; Gallin, 2006; Shiller, 2015). Beside these macroeconomic fundamental variables, first–order autoregressive term of the change in the log housing prices was included in the regression model to account for the momentum effect because real estate acts as an investing instrument. For further information we refer to Case and Shiller (1989, 2003), Piazzesi and Schneider (2009) and Zheng et al. (2016). In addition, Himmelberg et al. (2005), Davis and

Heathcote (2007), Saiz (2010) and Gyourko et al. (2013) suggested land supply elasticity, cost of ownership, demographic and geographic statistics to explain the difference of housing prices across cities.

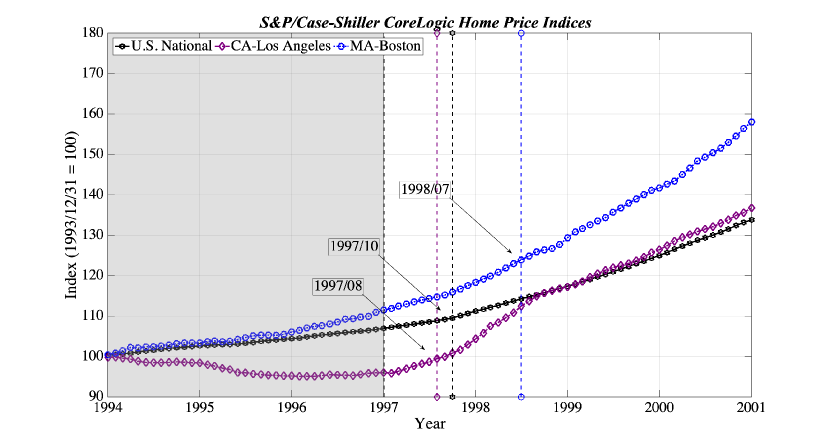

We used the S&P CoreLogic Case–Shiller Home Price Index series, which is the leading measure of U.S. residential real estate prices and tracks changes in the value of residential real estate, as the proxy of housing prices. We studied the housing prices in U.S. at the national level and at two metropolitan areas: Los Angeles and Boston. The S&P CoreLogic Case–Shiller Home Price Index series for these three markets are exhibited

in Figure 5.1. Figure 5.1 depicts an upward housing price trend in the U.S. at the national level, as well as in Los Angeles and Boston between January 1994 to December 2000.

The set of macroeconomic fundamental variables included in our model:

: the lagged disposable personal income per capita change, we used the national level data as a proxy for Los Angeles and Boston since only yearly data of personal income per capita for states and Metropolitan Statistical Areas are available by the U.S. Bureau of Economic Analysis.

: the lagged change of 30-year fixed rate of mortgage average in U.S., transformed from weekly frequency to monthly.

: the lagged all non–farm employment change in terms of the national level and corresponding Metropolitan Statistical Areas level originally released by the U.S. Bureau of Labor Statistics.

: the lagged change of housing starts at the national level and the U.S. Census Bureau Regions (West Region series was used for Los Angeles and Northeast Region series was used for Boston). We use the lagged term of these variables here to mitigate the endogenous problem because of the interactive effect among the housing prices and these macroeconomic fundamentals (Case and Shiller, 2003).

All data that we used are seasonally adjusted monthly data from the economic database of the Federal Reserve Bank of St. Louis111https://fred.stlouisfed.org.

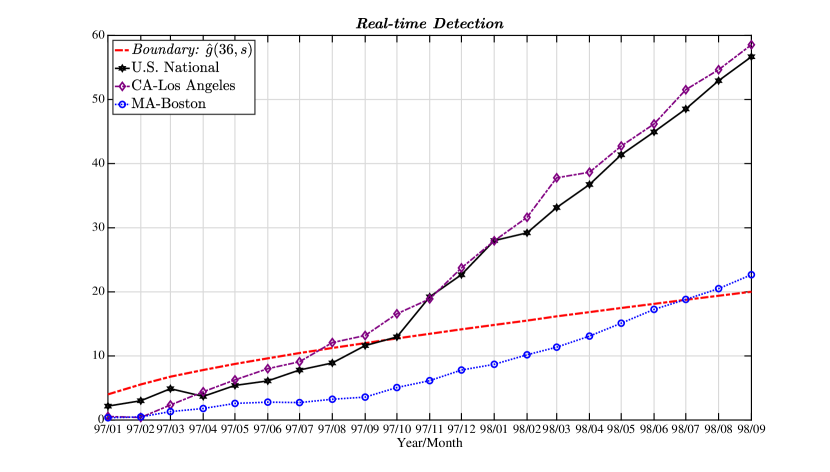

According to Shiller (2008), the beginning of 1991 was the turning point in the 1980s boom. The housing prices started to drop and later they flattened out. Thus we used January 1994–December 1996 as the training (historical) sample , so in our calculations. The upper part of Table 5.1 reports the summary statistics of all variables of the training sample we used in the regression. Statistics, including the number of observations, mean, standard deviation, minimum, maximum and the testing results of the KPSS test (Kwiatkowski et al. 1992) to check stationarity without linear term are tabulated. According to our results, stationarity cannot be rejected for the training sample. The detector is defined by (4.1) with and . The boundary function as well as the detectors are given in Figure 5.2. According to our calculations, (October 1997) for the national level, (August 1997) for Los Angeles and (July 1998) for Boston. The detections of changes in the parameters of the model in (2.1) are denoted by vertical lines in Figure 5.1. Table 5.2 shows the estimated values of the parameters for the periods (training sample), (before detection) and (after detection).

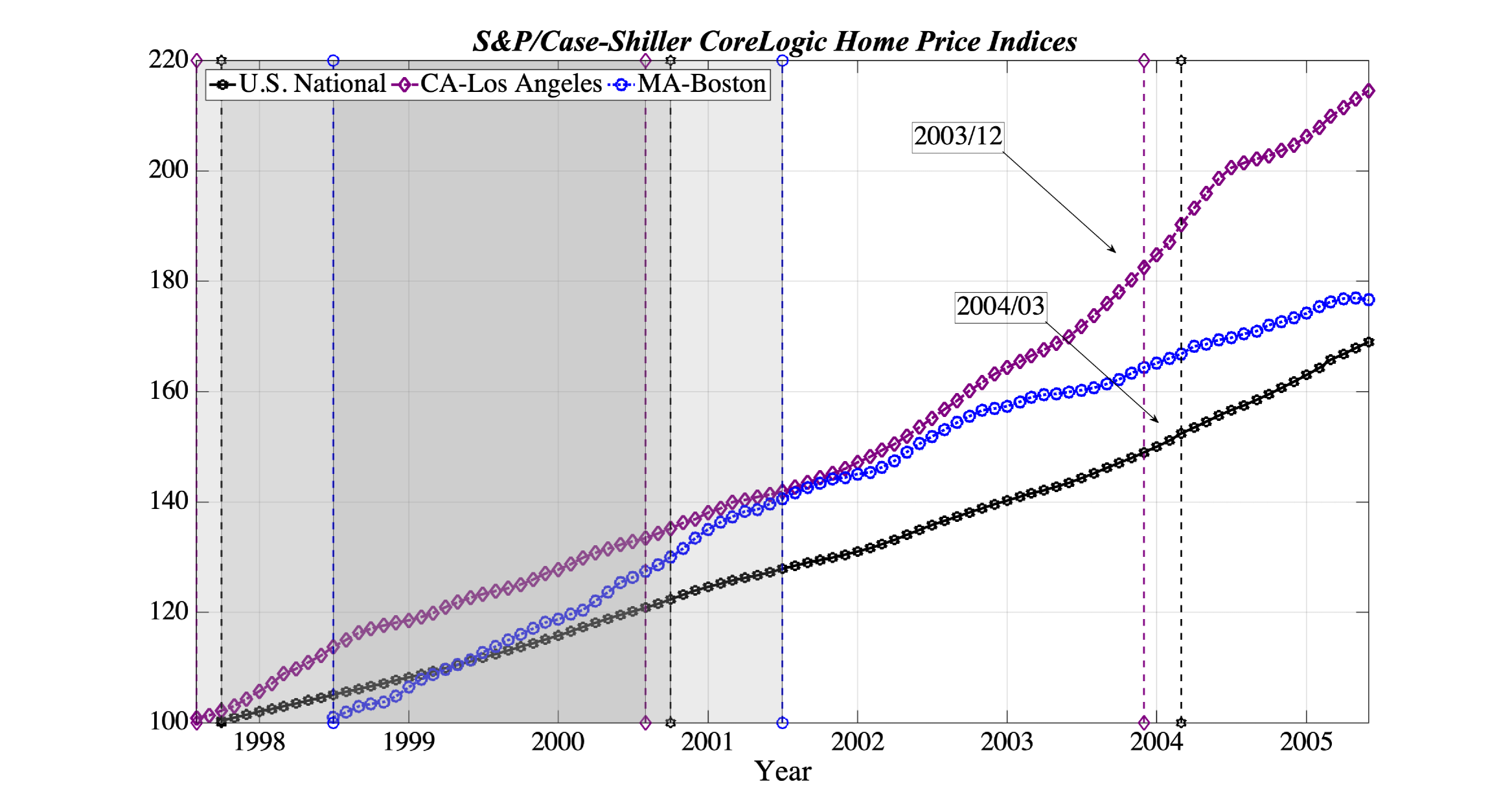

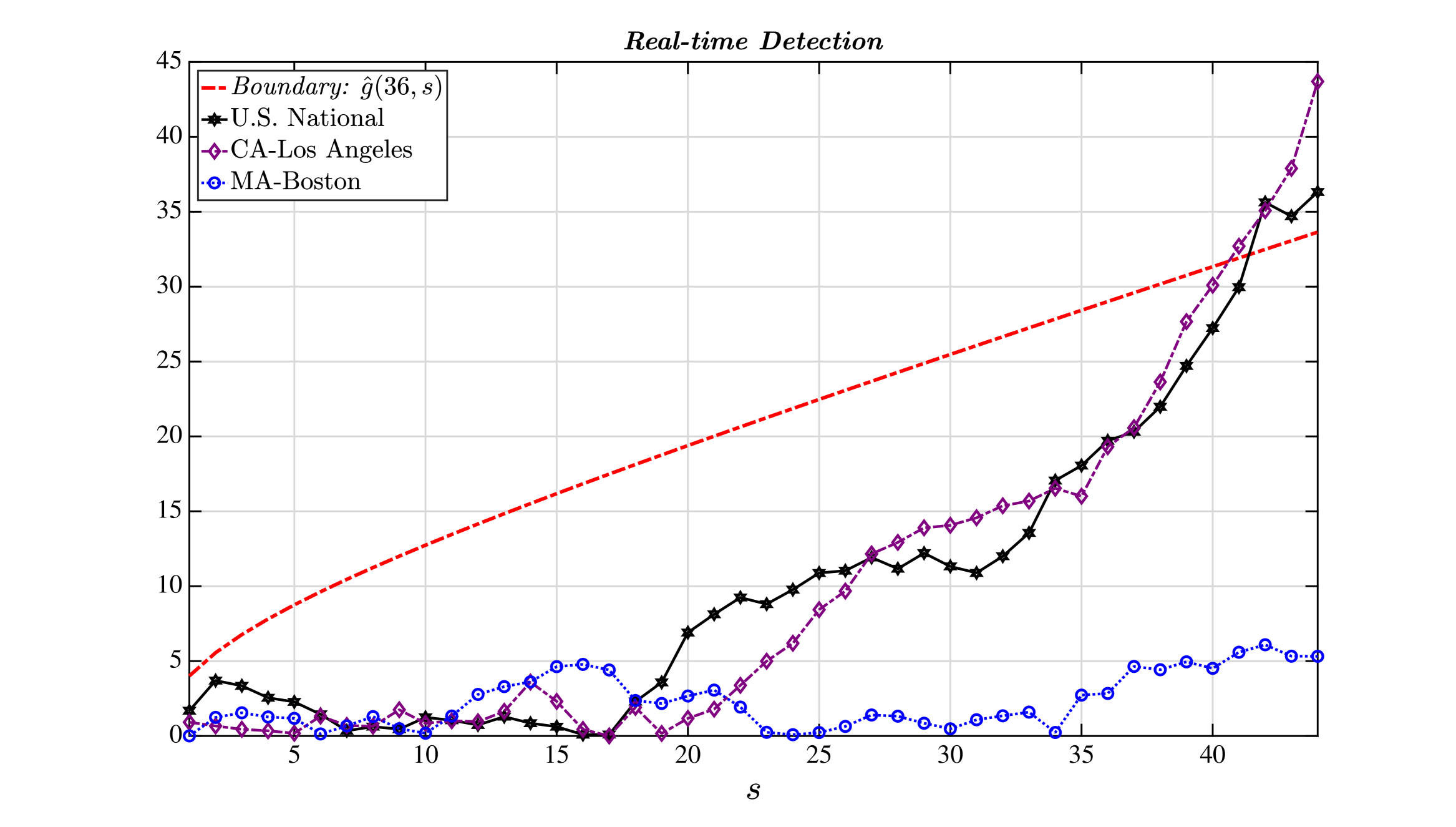

We checked for more possible changes in the data in each market after the detection of changes at . We used the training periods , i.e. October 1997–September 2000 for the national market, August 1997–July 2000 for Los Angeles and July 1998-June 2001 for Boston. The lower part of Table 5.1 shows the summary statistics and the values of the stationarity test for these training samples. We started a new monitoring procedure for all three markets, the starting dates were October 2000 at the national level, August 2000 for Los Angeles and July 2001 for Boston. Our procedure detected changes at the national level and March 2004 was the estimated time of change. A change was also found for the Los Angeles market dated December 2003. No further changes were found on the Boston market. Figure 5.3 exhibits the housing price indices and the time of the changes are indicated by vertical lines. Figure 5.4 shows the boundary function and the detectors. We note that on Figure 5.4 the monitoring starts at the same point but it is a different physical time for the three markets. It is clear from Table 5.2 that the autoregressive parameter changes if there is a change and it is increasing with time. However, with the exception of the national market, the autoregressive parameter stays far away from 1. The estimates are .93 and .84 for the national market and for Los Angeles, respectively. During the second monitoring phase, structural breaks were detected almost two years before the prices peaked in 2006 during the 2000s real estate boom.

Our monitoring process finds increasing autoregressive parameters in the three markets and hence it confirms the “amplification mechanism” advocated by Case and Shiller (2003). The “amplification mechanism” is the strongest in Los Angeles, which was undergoing faster price changes than Boston. Since the autoregressive parameters are below 1 in the first and also in the second phase of our monitoring, it is unlikely that “bubbles” formed in the sense of Linton (2019). It is also useful to note that the estimated R–square is increasing with the autoregressive parameter, so the autoregressive part explains more and more of the changes in the housing prices. The momentum effect, caused by the herding behavior of transactions, tends to disengage the of housing price index changes from the macro fundamentals.

| Variables | Sample Size | Mean | SD | Min | Max | KPSS-test | |

|---|---|---|---|---|---|---|---|

| Training Sample for the first monitoring: January 1994 - December 1996 | |||||||

| Housing Market Indicators: | S&P Case–Shiller Home Price Indices | ||||||

| U.S. National Level | 36 | 0.0019 | 0.0006 | 0.0005 | 0.0034 | 0.1300 | |

| Los Angeles | 36 | -0.0011 | 0.0023 | -0.0075 | 0.0032 | 0.3070 | |

| Boston | 36 | 0.0030 | 0.0026 | -0.0021 | 0.0098 | 0.2647 | |

| Fundamentals: | |||||||

| Disposable Personal Income per Capita | 36 | 0.0011 | 0.0054 | -0.0198 | 0.0116 | 0.2328 | |

| 30-Year Fixed Mortagage Rate | 36 | 0.0016 | 0.0342 | -0.0501 | 0.0802 | 0.1795 | |

| All Employees, Total Nonfarm | |||||||

| U.S. National Level | 36 | 0.0021 | 0.0009 | -0.0002 | 0.0041 | 0.3036 | |

| Los Angeles | 36 | 0.0012 | 0.0015 | -0.0034 | 0.0040 | 0.2872 | |

| Boston | 36 | 0.0017 | 0.0013 | -0.0027 | 0.0038 | 0.1188 | |

| New Privately Owned Housing Units Started | |||||||

| U.S. National Level | 36 | -0.0031 | 0.0633 | -0.1866 | 0.1568 | 0.1173 | |

| Los Angeles | 36 | -0.0082 | 0.1275 | -0.3027 | 0.2446 | 0.1848 | |

| Boston | 36 | 0.0028 | 0.1439 | -0.2776 | 0.3502 | 0.1517 | |

| Training Sample for the second monitoring : October 1997–September 2000 (national level), August 1997–July 2000 (Los Angeles) and July 1998–June 2001 (Boston) | |||||||

| Housing Market Indicators: | S&P Case–Shiller Home Price Indices | ||||||

| U.S. National Level | 36 | 0.0060 | 0.0010 | 0.0035 | 0.0078 | 0.3505 | |

| Los Angeles | 36 | 0.0091 | 0.0033 | 0.0039 | 0.0176 | 0.2429 | |

| Boston | 36 | 0.0110 | 0.0038 | 0.0036 | 0.0188 | 0.2626 | |

| Fundamentals: | |||||||

| Disposable Personal Income per Capita | 36 | 0.0030 | 0.0025 | -0.0029 | 0.0079 | 0.1355 | |

| 30-Year Fixed Mortagage Rate | 36 | 0.0017 | 0.0218 | -0.0293 | 0.0551 | 0.1987 | |

| All Employees, Total Nonfarm | |||||||

| U.S. National Level | 36 | 0.0019 | 0.0009 | -0.0003 | 0.0036 | 0.3527 | |

| Los Angeles | 36 | 0.0019 | 0.0018 | -0.0018 | 0.0062 | 0.1853 | |

| Boston | 36 | 0.0011 | 0.0024 | -0.0043 | 0.0062 | 0.2207 | |

| New Privately Owned Housing Units Started | |||||||

| U.S. National Level | 36 | -0.0007 | 0.0442 | -0.0963 | 0.0807 | 0.2275 | |

| Los Angeles | 36 | 0.0023 | 0.1094 | -0.2840 | 0.1909 | 0.2834 | |

| Boston | 36 | -0.0010 | 0.1341 | -0.3432 | 0.1569 | 0.1961 | |

Note: The critical values for the KPSS test are 0.347 (10% level), 0.463 (5% level), 0.739 (1% level).

| U.S. National | Los Angeles | Boston | ||||||||||

| Variables | Training | Before | After | Training | Before | After | Training | Before | After | |||

| Sample | Detection | Detection | Sample | Detection | Detection | Sample | Detection | Detection | ||||

| Estimated Coefficients During the first Monitoring (the size of the training sample is ) | ||||||||||||

| 0.0006 | 0.0006 | 0.0011 | -0.0009 | -0.0006 | 0.0010 | 0.0020 | 0.0012 | 0.0028 | ||||

| 0.0246 | 0.0271 | -0.1202 | -0.0452 | -0.0355 | 0.2139 | 0.0570 | 0.0766 | 0.0186 | ||||

| 0.1511 | 0.0625 | -0.0582 | 0.3545 | 0.5183 | 0.5264 | 0.0842 | 0.1432 | 0.1166 | ||||

| 0.0026 | 0.0014 | -0.0084 | 0.0002 | -0.0052 | -0.0337 | -0.0035 | -0.0114 | 0.0159 | ||||

| 0.0008 | 0.0010 | 0.0011 | 0.0017 | 0.0007 | -0.0107 | -0.0017 | -0.0018 | -0.0027 | ||||

| 0.4612 | 0.6295 | 0.8820 | 0.4060 | 0.6007 | 0.7135 | 0.2639 | 0.6316 | 0.6152 | ||||

| 0.5172 | 0.4872 | 0.7347 | 0.3019 | 0.5153 | 0.7035 | 0.0673 | 0.3819 | 0.4155 | ||||

| Estimated Coefficients During the Second Monitoring (the size of the training sample is ) | ||||||||||||

| 0.0015 | 0.0006 | 0.0008 | 0.0031 | 0.0020 | 0.0019 | 0.0054 | ||||||

| 0.0008 | 0.0051 | 0.0019 | 0.3234 | 0.0434 | 0.0179 | -0.0689 | ||||||

| 0.0363 | 0.0133 | 0.1101 | 0.1053 | -0.1486 | -0.0556 | 0.3305 | ||||||

| 0.0059 | 0.0054 | 0.0072 | -0.0192 | -0.0031 | 0.0105 | 0.0189 | ||||||

| -0.0005 | 0.0009 | 0.0008 | -0.0039 | -0.0020 | 0.0014 | -0.0067 | ||||||

| 0.7474 | 0.9294 | 0.9100 | 0.5363 | 0.8353 | 0.8686 | 0.4854 | ||||||

| 0.6998 | 0.8234 | 0.8623 | 0.4766 | 0.6450 | 0.7850 | 0.2932 | ||||||

6. Conclusion

In this paper we consider a model which includes linear and autoregressive terms to model changes in real estate prices. The observations and errors are weakly dependent, including the most often used linear and nonlinear time series sequences. We propose a sequential method to detect possible changes in the parameters of the model. The monitoring scheme is based on a detector and a suitably chosen boundary function. The limit distribution of the sequential monitoring scheme is established under the null hypothesis of stability of the model. We determine the asymptotic distribution of the stopping time when structural break is present. We focus on the possible changes in the autoregressive parameter. Using Monte Carlo simulations we illustrate that our results can be applied in case of finite sample sizes. We suggest a boundary function which provides the right size of the monitoring even in case of small and moderate historical (training) samples. We also study the power of the procedure and the time to detect the structural break. A data example is also given. We sequentially looking for possible structural breaks in the real estate markets of Boston, Los Angeles and at the U.S. national level. We find structural breaks in the data, and find stationary segments. The autoregressive parameter of the segments is increasing but it stays below 1. Hence the “amplification mechanism” of Case and Shiller (2003) is confirmed by the data analysis but no bubbles in the sense of Linton (2019) were found.

Acknowledgements Part of the research was done while Shanglin Lu was visiting the University of Utah. We appreciate the support of the Department of Mathematics.

References

- [1] Aue, A., Hörmann, S., Horváth, L. and Hušková, M.: Dependent functional linear models with applications to monitoring structural change. Statistica Sinica 24(2014), 1043–1073.

- [2] Aue, A. and Horváth, L.: Delay time in sequential detection of change. Statistics & Probability Letters 67(2004), 221–231.

- [3] Aue,A., Horváth, L., Hušková and Kokoszka, P.: Change‐point monitoring in linear models. The Econometrics Journal 9(2006), 373–-403.

- [4] Aue, A., Horváth, L., Kokoszka, P. and Steinebach, J.: Monitoring shifts in mean: asymptotic normality of stopping times. TEST 17(2008) 515–530.

- [5] Billingsley, P.:Convergence of Probability Measures, Wiley, New York, 1968.

- [6] Burnside, C., Eichenbaum, M. and Rebelo, S.: Understanding booms and busts in housing markets. Journal of Political Economy 124(2016), 1088–1147.

- [7] Caron, E.: Asymptotic distribution of least square estimators for linear models with dependent errors. Statistics 53(2019), 885–902.

- [8] Case, K.E. and Shiller, R.J.: The efficiency of the market for single–family homes. American Economic Review 79(1989), 125–137.

- [9] Case, K.E. and Shiller, R.J.: Is there a bubble in the housing market? Brookings Papers on Economic Activity, 2003, No. 2, 299–362.

- [10] Chu, C.-S.J., Stinchcombe, M. and White, H.: Monitoring structural change. Econometrica 64(1996), 1045–-1065.

- [11] Davis, M.A. and Heathcote, J.: The price and quantity of residential land in the united states. Journal of Monetary Economics 54(2007), 2595–2620.

- [12] Dümbgen, L.: The asymptotic behavior of some nonparametric change–point estimators. Annals of Statistics 19(1991), 1471–-1495.

- [13] Gallin, J.: The long-run relationship between house prices and income: evidence from local housing markets. Real Estate Economics 34(2006), 417–438.

- [14] Glaeser, E. L. and Nathanson, C. G.: An extrapolative model of house price dynamics. Journal of Financial Economics 126(2017), 147–170.

- [15] Granziera, E. and Kozicki, S.: House price dynamics: fundamentals and expectations. Journal of Economic Dynamics and Control 60(2015), 152–165.

- [16] Gyourko, J., Mayer, C. and Sinai, T.: Superstar cities. American Economic Journal: Economic Policy 5(2013), 167–99.

- [17] Himmelberg, C., Mayer, C. and Sinai, T.: Assessing high house prices: Bubbles, fundamentals and misperceptions. Journal of Economic Perspectives 19(2005), 67–92.

- [18] Hlávka, Z., Hušková, M., Kirch, C. and Meintanis, S.: Monitoring changes in the error distribution of autoregressive models based on Fourier methods. TEST 21(2012), 605–634.

- [19] Hoga, Y.: Monitoring multivariate time series. Journal of Multivariate Analysis 155(2017), 105–121.

- [20] Homm, U. and Breitung, J.: Testing speculative bubbles in stock markets: a comparison of alternative methods. Journal of Financial Econometrics 10(2012), 198–231.

- [21] Hörmann, S. and Kokoszka, P.: Weakly dependent functional data. Annals of Statistics 3(2010), 1845–1884.

- [22] Horváth, L., Hušková, M., Kokoszka, P. and Steinebach, J.: Monitoring changes in linear models. Journal of Statistical Planning and Inference 116(2004), 225–251.

- [23] Horváth, L., Kokoszka, P. and Steinebach, J.: On sequential detection of parameter changes in linear regression. Statistics & Probability Letters 77(2007) 885–895.

- [24] Horváth, L., Liu, Z., Rice, G. and Wang, S.: Sequential monitoring for changes from stationarity to mild non–stationarity. Journal of Econometrics To appear (2019+).

- [25] Hušková, M. and Kirch, C.: Bootstrapping sequential change–point tests for linear regression. Metrika 75(2012), 673–708.

- [26] Ibragimov, I.A.: Some limit theorems for strict–sense stationary stochastic processes (in Russian). Doklady Akademii Nauk SSSR 125(1959), 711–714.

- [27] Ibragimov, I.A.: Some limit theorems for stationary processes. Theory of Probability and Its Applications 7(1962), 349–382.

- [28] Kirch, C.: Block permutation principles for the change analysis of dependent data. Journal of Statistical Planning and Inference 137(2007), 2453–2474.

- [29] Kirch, C.: Bootstrapping sequential change–point tests. Sequential Analysis 27(2008), 330–349.

- [30] Kwiatkowski, D., Phillips, P.C.B., Schmidt, P. and Shin, Y.: Testing the null hypothesis of stationarity against the alternative of a unit root: how sure are we that economic time series have a unit root? Journal of Econometrics 54(1992), 159–178.

- [31] Lee, J.H. and Phillips, P.C.B.: Asset pricing with financial bubble risk. Journal of Empirical Finance 38(2016), 590-622.

- [32] Linton, O.: Financial Econometrics: Models and Methods. Cambridge University Press, 2019.

- [33] Mayer, C.: Housing bubbles: A survey. Annual Review of Economics 3(2011), 559–577.

- [34] Phillips, P.C.B., Shi, S. and Yu. J.: Specification sensitivity in right–tailed unit root testing for explosive behaviour. Oxford Bulletin of Economics and Statistics 76(2014), 15–333.

- [35] Phillips, P.C.B., Shi, S. and Yu, J.:Testing for multiple bubbles: historical episodes of exuberance and collepse. in the S&P 500. International Economic Review 56(2015a), 1043–1177.

- [36] Phillips, P.C.B., Shi, S. and Yu, J.: Testing for multiple bubbles: limit theory of real–time detectors. International Economic Review 56(2015b), 1079–1133.

- [37] Phillips, P.C.B. and Yu, J: Dating the timeline of financial bubbles during the subprime crisis. Quantitative Economics 2(2011), 455–491.

- [38] Piazzesi, M. and Schneider, M.: Momentum traders in the housing market: survey evidence and a search model. American Economic Review 99(2009), 406–411.

- [39] Picard, D.: Testing and estimating change-points in time series. Advances in Applied Probability 17(1985), 841–867.

- [40] Saiz, A.: The geographic determinants of housing supply. The Quarterly Journal of Economics 125(2010), 1253–1296.

- [41] Shiller, R. J.: Historic turning points in real estate. Eastern Economic Journal 34(2008), 1–13.

- [42] Shiller, R. J.: Irrational Exuberance. (Revised and expanded third edition), Princeton University Press, 2015.

- [43] Wu, W.B.: –estimates of linear models with dependent errors. Annals of Statistics 35(2007), 495–521.

- [44] Zeckerhauser, R. and Thompson, M.: Linear regression with non–normal error terms. Review of Economics and Statistics 52(1970), 280–286.

- [45] Zeileis,A., Leisch, F., Kleiber, C. and Hornik, K.: Monitoring structural change in dynamic econometric models. Journal of Applied Econometrics 20(2005), 99–121.

- [46] Zheng, S., Sun, W. and Kahn, M. E.: Investor confidence as a determinant of China’s urban housing market dynamics. Real Estate Economics 44(2016), 814–845.

- [47] Zhu, Z.: Inference for linear models with dependent errors. Journal of the Royal Statistical Society Ser. B 75(2013), 1–21.

Appendix A Proof of Theorem 2.1

We assume in this section that holds. According to Assumption 2.1, is an –decomposable Bernoulli shift. Next we show that the autoregressive term , the last coordinate of , is also is an –decomposable Bernoulli shift. We also show that some functions of and are also decomposable and we obtain the corresponding rate. Since is stationary under , we obtain immediately that

| (A.1) |

Lemma A.1.

Proof.

Elementary arguments give that

| (A.5) |

where is defined in (3.1) and . By the stationarity of and we have

Using now Assumption 2.1, the Bernoulli representation for is established. According to the definition of we have that

and therefore

Using Assumption 2.1

Assumption 2.1 and (A.2) imply that

where is the coordinate of and is a constant. Hence (A.3) is proven. Similar argument gives (A.4). ∎

Lemma A.2.

where with

(ii) If and are independent, then .

Proof.

Using Lemma A.1 and Lemma B.1 in Aue et al. (2014) we obtain that

and

so by Markov’s inequality we have

| (A.7) |

and

Hence

| (A.8) |

where ,

| (A.9) |

and therefore (2.16) is proven. Using Assumption 2.3 we get that

| (A.10) |

It follows from Assumption 2.2 that

| (A.11) |

Applying now Theorem B.1 in Aue et al. (2014) we conclude that

| (A.12) |

where is a –dimensional normal random vector with and .

Hence the proof the first part of Lemma A.2 is now complete.

It follows immediately from the independence of and and Assumption 2.2 that

for

Similarly,

Proof.

By the stationarity of , Assumption 2.1 and Lemma A.1 yield for all (cf. Lemma B.1 of Aue et al. 2014 and the maximal inequality in Billingsley 1968, p. 94) that

where is a constant. We write that

Hence for any we have that

with some constant and on account of Thus we conclude that for all

completing the proof of Lemma A.3. ∎

Proof.

Lemma A.5.

If Assumption 2.1 holds, then for every we can define two independent Wiener processes and such that

| (A.14) |

and

| (A.15) |

with some .

Proof.

Proof of Theorem 2.1. First we note that by the proof of Lemma A.4 we have

| (A.16) |

Hence according to Lemma A.4 we need to show only

| (A.17) |

where stands for a Wiener process. Using (A.14) we get

| (A.18) | ||||

Similarly, (A.15) implies

| (A.19) | ||||

since we can assume without loss of generality that . By the scale transformation of the Wiener process we have that

| (A.20) | ||||

where and are independent Wiener processes. It is shown in Chu et al. (1996) (cf. also Horváth et al., 2004) that

where stands for a Wiener process. Hence

Appendix B Proof of Theorems 3.1–3.5

Proof of Theorem 3.1. It follows from the proof of Theorem 2.1

Using Lemma A.3 we get

| (B.1) |

Following the proof of Lemma B.1, Assumption 3.1 implies that for any

and

Thus we conclude

| (B.2) |

Hence Lemma A.2 yields

Let

We showed that

Assumptions of Theorem 3.1 yield

completing the proof.

∎

The proof of Theorem 3.2 is based on a series of lemmas. The first lemma considers the detector before the time of change and it will be used in the proofs of Theorems 3.3–3.5 as well.

Proof.

We can assume without loss of generality the . Let

Proof.

Proof.

Proof.

We note that for we have

| (B.11) |

It follows from Lemmas A.5 and B.2 that

Lemmas A.2, A.3 and (B.2) yield

and therefore

Similarly to Lemma A.3 with some we have

| (B.12) |

and therefore by Lemma A.3 and Assumption 3.2 we conclude

Thus the proof of the first part of lemma B.4 is complete.

To prove the second part we note that

(cf. the proof of Lemma 3.3 of Aue and Horváth, 2014). ∎

Lemma B.5.

Proof.

Lemma B.6.

Proof.

Proof of Theorem 3.1. Elementary calculus gives

and

So by Lemma B.6 we have for all

completing the proof of Theorem 3.2. ∎

Lemma B.7.

Proof.

The upper bound in (B.14) is an immediate consequence of Lemmas A.2 and A.3.

It follows from Aue et al. (2014)

with some Wiener processes

which implies (B.16).

Using Lemma A.5 we get

and by the scale transformation of the Wiener process we have

where stands for a Wiener process. Hence (B.17) is proven. ∎

Proof of Theorem 3.3. Let

We note that

Following the proof of Theorem 2.1 we get

since . Thus we conclude

| (B.18) |

Using (B.17) we obtain

Now (B.17) results in

Since

we get by (B.16)

Since the distribution of does not depend on we note that

concluding the proof of Theorem 3.3. ∎

Lemma B.8.

If is a Wiener process, then is normally distributed with zero mean and

Proof.

Since is Gaussian, the normality of the integral is clear. Direct calculations give the value of the variance. ∎

Let

with

with

We can assume without loss of generality that

Lemma B.9.

Proof.

Proof.

Proof.

Lemma B.12.

Proof.

Lemma B.13.

Proof.

According to Lemmas B.10–B.12 we need to show only

It follows from Lemma B.7 that

and

Thus (B.24) is proven. Following the proof of Lemma B.4, one can verify (B.25).

∎

Proof.

By definition,

| (B.26) |

Let be a Wiener process. Let . Putting together Lemmas B.9–B.13, and (B.26) we need to show only that

| (B.27) |

Let be a Wiener process. We note that and are equal in distribution. By the scale transformation of the Wiener process we have

Hence

We note that

It follows from Lemma B.8 that

where stands for a standard normal random variable. Using now (B.21), the lemma is proven. ∎