Stochastic optimization of the Dividend strategy with reinsurance in correlated multiple insurance lines of business

Khaled Masoumifarda111Email: k-masoumifard@sbu.ac.ir and Mohammad Zokaeia222Corresponding author. Email: zokaei@sbu.ac.ir. Postal Code: 1983969411

a Department of Statistics, Faculty of Mathematical Sciences, Shahid Beheshti University, Tehran, Iran

Abstract

The present paper addresses the issue of the stochastic control of the optimal dynamic reinsurance policy and dynamic dividend strategy, which are state-dependent, for an insurance company that operates under multiple insurance lines of business. The aggregate claims model with a thinning-dependence structure is adopted for the risk process. In the optimization method, the maximum of the cumulative expected discounted dividend payouts with respect to the dividend and reinsurance strategies are considered as value function. This value function is characterized as the smallest super Viscosity solution of the associated Hamilton-Jacobi-Bellman (HJB) equation. The finite difference method (FDM) has been utilized for the numerical solution of the value function and the optimal control strategy and the proof for the convergence of this numerical solution to the value function is provided. The findings of this paper provide insights for the insurance companies as such that based upon the lines in which they are operating, they can choose a vector of the optimal dynamic reinsurance strategies and consequently transfer some part of their risks to several reinsurers. The numerical examples in the elicited results show the significance increase in the value function in comparison with the previous findings.

1 Introduction

Suppose a insurance company based on a dynamic strategy distributes a ratio of its dividend amongst the shareholders and transfers a part of its risk to a secondary insurance company by a dynamic reinsurance strategy. The dividend and reinsurance strategies are shown as

and

, respectively. A paramount issue for an insurance company is the optimization of these strategies. For this reason, first an objective function should be considered and then

and

strategies should be found as such that the objective function is optimized. A very common function in literature is the cumulative expected discounted dividends which is displayed as .

In the following, we will outline some research on thinning-dependence structure and optimization with respect to the dividend and reinsurance.

Optimization of with respect to the dividend strategy:

In 1957, De Finetti (De Finetti (1957)) considered the band strategy for paying dividends to shareholders and addressed the issue of optimizing .

Gerber Gerber (1969) demonstrated that if the company’s capital is modeled using the Cramer-Landbrug process, then an optimal strategy for paying the dividends is always based on a band strategy, and when the severity of the claim follows an exponential distribution, the band strategy is reduced to the barrier strategy.

Later, the issue of optimizing the dividend distribution strategy has attracted many researchers, for example,

when the company’s capital is modeled using Brownian risk, Gerber (1969), Grandits et al. (2007), and Jeanblanc-Picqué & Shiryaev (1995) investigated the problem of optimal dividend distribution, and when the company’s capital is modeled using the classical risk process, Zhou (2005), Avram et al. (2007), Kyprianou & Palmowski (2007) and Loeffen (2008) investigated the barrier model for distributing dividends.

Recently, the issue of stochastic control of dividend strategy by researchers has been investigated in a situation where several insurance companies are co-operating and the company’s capital is modeled through multi-dimensional stochastic process( refer to

Loeffen (2008), Albrecher et al. (2017) and Azcue et al. (2016)).

Optimization of with respect to the dividend strategy and reinsurance strategy:

Azcue & Muler (2005)

is one of the first articles that optimizes with respect to the dividend and reinsurance strategies.

Schmidli (2006)

has examined two important issues; maximizing with respect to the dividend strategy and minimizing the ruin probability with respect to the reinsurance strategy.

Thonhauser & Albrecher (2007) suggested that the optimization of dividend and reinsurance should be based on a value function that depends on the expectation of the dividends and the ruin time. With this approach, when the number of claims follows a Poisson distribution with exponential intensity, an optimal barrier strategy is obtained for both the diffusion model and the Cramer-Lundberg model. Some studies have addressed this issue(e.g.

Beveridge et al. (2007), Meng & Siu (2011) and Zhou & Yuen (2012)).

The thinning-dependence structure:

An insurance company usually operates in several insurance lines, each of which may behave differently vis-à-vis another. Therefore, it is reasonable for the insurance company to make different decisions about each line.

For example, using proportional reinsurance in one line and excess-of-loss reinsurance in another line or use one type of excess-of-loss in one line and a different type of excess-of-loss insurance in another line. Masoumifard & Zokaei (2020), considering a vector of independent compound Poisson process for the lines, have dealt with optimization of reinsurance strategies corresponding to each line. However, the problem is that usually there is a correlation between the lines. Therefore a method for modeling this correlation is required. In this regard pertinent models can be found in the related literature.

Yuen & Wang (2002) introduce the idea of claim thinning for investigating this issue and provide a clear explanation of how it works. Some literature on the

aggregate claims model

with thinning-dependence structure as follows; Wu & Yuen (2003),

Lindskog & McNeil (2003), Pfeifer & Nešlehová (2004), Bäuerle & Grübel (2005) and Wang & Yuen (2005). Although research on optimal reinsurance is increasing apace, only a few papers deal with

the problem concerning the dependent risks. For two lines of insurance business with common shock dependence, in the dynamic setting, Bai et al. (2013) probed

the optimal excess of loss reinsurance to minimize the ruin probability for the diffusion risk model and Liang & Yuen (2016) adopted

the variance premium principle to study the optimal proportional reinsurance problem for both

the compound Poisson risk model and the diffusion approximation risk model. For more than two lines

of insurance business with the common shock dependence, Yuen et al. (2015) considered the objective

of maximizing the expected exponential utility and derived the optimal reinsurance

strategy not only for the diffusion approximation risk model but also for the compound

Poisson risk model. Furthermore, Wei et al. (2017) considered a model where the claim-number

processes amongst the lines of the insurance business have the thinning-dependence structure. For this risk

model, they derived the optimal reinsurance strategies with the objective of maximizing the adjustment coefficient for two commonly-used premium principles.

In this paper, the optimization of the control strategy (dividend and reinsurance strategies) is utilized, implementing a dynamic programming approach for an insurance company with several dependent lines. In modeling the risk process, we adopt a thinning dependence structure that covers a large part of the dependency structures which can be expressed and the control strategy that maximizes the cumulative expected discounted dividends (value function) with the value function have being characterized.

2 Model and problem formation

In the classical Cramer-Lundberg process, the reserve of an insurance company can be described by

| (2.1) |

where is the deterministic initial capital, is the number of claims arriving in with claim arrival intensity , and the claim severity are i.i.d random variable with distribution . The premium rate per unit of time is calculated using the expected value principle with relative safety loading ; that is, . A limitation of the existing in this model is the implicit or explicit assumption that the insurers produce only one type of insurance, even though most insurers produce multiple types of coverage (e.g., automobile insurance, general liability insurance, fire insurance, workers’ compensation insurance, etc.). The dependency can be introduced between the processes through thinning. Suppose that an insurance company has lines of business and stochastic sources that may cause a claim in at least one of the lines are classified into class. It is assumed that each event in the th class may cause a claim in the th line with probability for and . Consider the number of events of the th class occurred up to time and the number of claims of the th line up to time generated from the events in class . Then the claim number process of the th line can be written as

Let us define the process such that;

| (2.2) |

where the claims severity of the th line , , are i.i.d random variables with distribution . Let the risk process of the th line of insurance company is modeled by . The premium rate is calculated using the expected value principle with relative safety loading . Given an initial surplus , the surplus of the insurance company at time can be written as

To analyze mathematically tractable, we assume

-

(A1)

the processes are independent Poisson processes with intensities , respectively,

-

(A2)

are independent random variables where is the sum of all simultaneous claims that spring from the class at a moment,

-

(A3)

all claims made at different times are independent, and

-

(A4)

for any , , , are i.i.d random variable where is the claim incurred in the line by class .

In the following proposition, we show that is a compound Poisson process.

Proposition 2.1

Suppose , and , where a subset of a set , with exactly elements. Then, is still a compound Poisson risk process which can be rewritten as

| (2.3) |

where is a Poisson process with claim arrival intensity and the are i.i.d random variable with distribution

where is the claim incurred in the line .

Proof : The sum of claims arrived to the insurance company that spring from the class up to time will be displayed as

where is the sum of all simultaneous claims that spring from the class at a moment. By using assumptions (A1) and (A3), it is quit axiomatic is a compound Poisson process where is a Poisson distribution with intensity parameter and has the following distribution:

wherein indicates the probability of occurrences which arrive from class , having resulted in the claims at the set of the lines. From assumption (A4), . Given the fact that are independent (assumptions (A1) and (A2)), is also a compound Poisson process like , where is a Poisson distribution with intensity parameter and has the distribution function (refer to Klugman et al. (2012), Theorem 7.5).

Note that the risk process , defined in (2.3), is an càdlàg stochastic process and satisfies the Markov property. We can describe this model by defining as the smallest filtered probability space produced by (refer to section 1.1 of Azcue & Muler (2014)).

Remark 2.1

If and for , then of (2.3) is the risk model considered by Yuen & Wang (2002). For example, let :

If , , , , , and , then of (2.3) is the risk model with common shock for three dependent lines of business;

For , more general risk models with common shock can also be constructed from (2.3) by choosing the values of and appropriately.

2.1 Control strategy

A control strategy is a process where is a vector of reinsurance strategies and is a dividend strategy. Reinsurance can be an effective way to manage risk by transferring risk from an insurer to a second insurer (referred to as the reinsurer). A reinsurance contract is an agreement between an insurer and a reinsurer under which, claims that arise are shared between the insurer and reinsurer. Let a Borel measurable function , be called retained loss function, describing the part of the claim that the company pays and satisfies . The reinsurance company covers , where the severity of the claim is . Now, to reduce the risk exposure of the portfolio, assume that the insurer can take reinsurances in a dynamic way for some insurance lines, each of these reinsurances is indexed by . We denote by the vector , in which is the family of retained loss functions associated to the reinsurance policy in ’th line. Thus, the reinsurances control strategy is a collection of the vector functions for any .

Well-known reinsurance types are:

-

(1)

Proportional reinsurance with .

-

(2)

Excess of loss reinsurance (XL) with , .

-

(3)

Limited XL reinsurance (LXL) with , .

The numbers and are named priority and limit, respectively.

A dividend strategy is a process where is the cumulative amount of dividends paid out by the reinsurance. Denote by the set of all control strategies with initial surplus . Now, for any , the surplus process can be written as

| (2.4) | |||||

It is easy to see that is equivalent to the following process

| (2.5) |

where is a Poisson process with claim arrival intensity and the are i.i.d random variable with distribution

| (2.6) |

where . The time of ruin for this process is defined by

| (2.7) |

In this paper, we assume that the reinsurance calculates its premium using the expected value principle with reinsurance safety loading factor :

and so , where

Let is the smallest filtered probability space produced by . The control strategy is admissible if satisfies

-

•

the process is predictable, that is, the function is measurable and the function is measurable for every and , and

-

•

the process is predictable, nondecreasing and càglàd (left continuous with right limits).

2.2 Problem formation

Regarding an admissible control strategy and an initial reserve , we define the following value function:

In the case that insurance company considers only one type of reinsurance contract for all the risks which it encounters and insurance portfolio was modeled by Cramer-Lundberg model; Azcue & Muler (2005) was considering , and found a general dynamic control strategy that maximizes this value function. Our aim in this paper is to extend this result for the model described earlier, in other words, we are looking for

| (2.8) |

The method of dynamic programming is used to characterize the optimal value function (2.8) and the corresponding optimal reinsurance strategies via the Hamilton-Jacobi-Bellman (HJB) equation. To obtain the Hamilton-Jacobi-Bellman (HJB) equation associated with the value function (2.8), we need to state the so-called Dynamic Programming Principle (DPP). Similar to the Proposition 3.1 of Azcue & Muler (2005), we can obtain the following result.

Lemma 2.1

Given any initial , we have

| (2.9) |

We now deduce the HJB equation assuming some regularity on . For any continuously differentiable function defined in , we define the discounted infinitesimal generator of the controlled process by

Assume that is continuously differentiable at x. Given any and any , let us consider the admissible control strategy . Now, similarly as in section 1.4 of Azcue & Muler (2014)

where denotes the first claim arrival. Note that from Lemma 2.1 we have:

Hence, dividing the above inequality by and taking gives

where

| (2.10) |

So, the HJB equation can be written as

| (2.11) |

2.3 Dividend band strategy with reinsurance

Let , , and are disjoint sets with , we say is a band partition if is closed, bounded, and nonempty; is open from the right; is open from the left, the lower limit of any connected component of belongs to , and there exists such that .

Definition 2.1

Consider an initial surplus , a stationary reinsurance control , and a band partition . An admissible control strategy is defined as follows,

-

•

if , we set and . Afterward, follow the strategy corresponding to initial surplus where is the severity of first claim and , where indicates that is a claim from the line ,

-

•

if , there exists such that , then we set and . Afterward, follow the strategy corresponding initial surplus and

-

•

if , there exists such that . Then and up to . Afterward, follow the strategy corresponding initial surplus .

The family is called the reinsurance band strategy associated with and .

We need to define the following operator,

| (2.12) |

It is easy to see that, if then . Consider a stationary reinsurance control and a band partition . In following proposition, using two operators and , a verification result is given for the value function of the reinsurance band strategy .

Proposition 2.2

Let is left continuous at the upper limit of the connected component of , right continuous at the lower limits of the connected components of , has derivative equal to 1 on , and an almost-everywhere solution in the connected components of , and a solution of in . Then is equivalent to .

2.4 Viscosity solutions

The dynamic programming method is a cogent means to scrutinize the stochastic control problems through the HJB equation. In (2.11), we have obtained the associated equation to the value function (2.8). Nonetheless, in the classical approach, this method is adopted only when it is assumed a priori that optimal value functions are smooth enough. In general, the optimal value function is not expected to be smooth enough to satisfy these equations in the classical sense. These call for the desideratum of week notation of solution of the HJB equation: the theory of viscosity solutions. Let us define this notion(see Azcue & Muler (2014)).

Definition 2.2

Let be the set of locally Lipschitz functions in . Given a function and a domain , consider the first-order differential equations of the form

| (2.13) |

A function is a viscosity subsolution of the differential equation (2.13) at if is locally Lipschitz and for all , where is the set of all the super-differentials, that is,

A function is a viscosity supersolution of the differential equation (2.13) at if is locally Lipschitz and for all , where is the set of all the sup-differentials,that is,

Finally, a function is a viscosity solution of (2.13) at , if it is both viscosity subsolution and supersolution.

There is an equivalent formulation for viscosity subsolution and supersolution.

Definition 2.3

We say that a function is a viscosity subsolution of (2.13) at if it is locally Lipschitz and any continuously differentiable function (called test function), with such that reaches the maximum at , satisfies . We say that a continuous function is a viscosity supersolution of (2.13) at if it is locally Lipschitz any continuously differentiable function (called test function), with such that reaches the maximum at satisfies .

3 Main results

In this section, we state a comparison result between viscosity subsolutions and supersolutions of (2.11) with a suitable boundary condition that gives us the uniqueness of viscosity solution. Also, we characterize the optimal value function as the smallest supersolution of the HJB equation. Before stating the main results, we need the following lemmas. The proofs of these lemmas are very similar to the same results in section 2.1.2 of Azcue & Muler (2005), we thus omit them.

Lemma 3.1

For , the optimal value function is well defined and admits the following bound:

Lemma 3.2

The optimal value function is increasing and locally Lipschitz in and for satisfies

Since the optimal value function is locally Lipschitz but possibly not differentiable at some points, we cannot say that is a solution of the HJB equation, we prove instead that is a viscosity solution of the corresponding HJB equation.

Theorem 3.1

is a viscosity solution of the HJB equation (2.11) at any .

Now, we first provide the comparison principle for viscosity solution of the HJB equation (2.11). This result implies the uniqueness among a certain class of the viscosity solution of (2.11) to which the optimal value function belongs. To be more precise, we introduce the following definition.

Definition 3.1

We say that a function belongs class if satisfies

-

(i)

is locally Lipschitz,

-

(ii)

if , then , and

-

(iii)

there exists a constant such that for all .

We also define; { is viscosity solution of (2.11) and belongs to }.

It is interesting to note that if is of class , then is strictly positive, linearly bounded, nondecreasing and absolutely continuous. Absolute continuity follows from the local Lipschitz continuity on a compact set. Clearly, by Lemma 3.1 and 3.2 the optimal value function belongs to .

Proposition 3.1

(Comparison principle) Let and are the sup and super-viscosity solution of (2.11) respectively. If both and are of class , then for implies that in .

The comparison principle states that there is at most one viscosity solution of (2.11) with boundary condition at zero among all the functions in with the same boundary condition. Since if and are two viscosity solutions of (2.11) with , then is a viscosity sub-solution and is a viscosity super-solution, then according to the above proposition . Also, with a similar argument, and as a result . Therefore, by having this result, if we know then would be characterized. However, the problem here is that is not known a priori; therefore, this result is not enough to characterize . By the following proposition, we can finalize the characterization .

Proposition 3.2

The optimal value function is the smallest viscosity supersolution of (2.11) that belongs to .

These results allows us to characterize V as the unique viscosity solution of (2.11) with boundary condition . From the previous proposition we can deduce the usual viscosity verification result: If we can find a stationary reinsurance strategy such that is a viscosity supersolution of (2.11), then ; because and by above proposition is the smallest viscosity supersolution of (2.11). Now we can show that the optimal control strategy is a reinsurance band strategy.

Proposition 3.3

Let the vector , where is one of the reinsurance families , and . Then, is a band partition, where

In the rest of this paper, whenever is used, it refers to the introduced in the previous proposition.

Theorem 3.2

Let the vector , where is one of the reinsurance families; proportional reinsurance family (), excess of loss reinsurance family () and limited excess of loss reinsurance family (). Then, there exists an admissible reinsurance control such that , the reinsurance band strategy associated to and , is optimal.

4 Numerical results

For a numerical solution of the value function and optimal control strategy, we use a method that is similar to the method described in Section 6.2 of Azcue & Muler (2014). In fact, by use the finite difference method, we first solve Equation (2.8) in the following way: starting with

and for , we approximate by

It is easy to show that converges to as tends zero. Then we define by

| (4.14) |

and set . Now, if we set

| (4.15) |

where , then, for we have and . If is satisfied in (2.11) almost everywhere, we claim that the optimal strategy is as follows, , and . If does not satisfy in (2.11) almost everywhere, we consider the following function

| (4.16) |

where, for , is solved by numerical solution the (2.10), using the finite difference method and boundary condition . Now, set where

If is satisfied in (2.11) almost everywhere, we claim that the optimal strategy is as follows, , and . If does not satisfy in (2.11) almost everywhere, we continue the process in the way described above. The reinsurance and control strategy obtained using the above algorithm are exhibited, respectively, by and .

Theorem 4.1

If , then the sequence converges to the unique viscosity .

Now, we obtain numerically some examples by using the above algorithm.

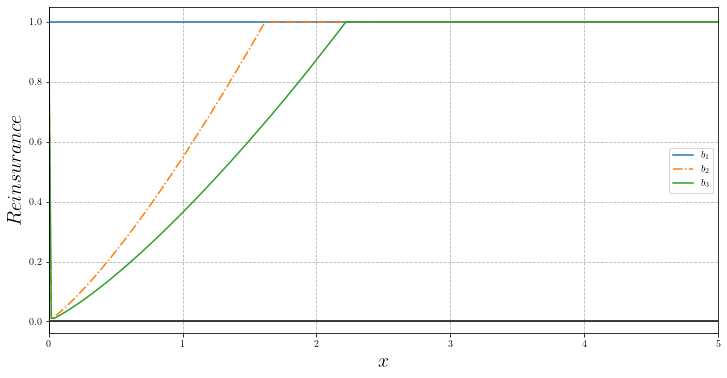

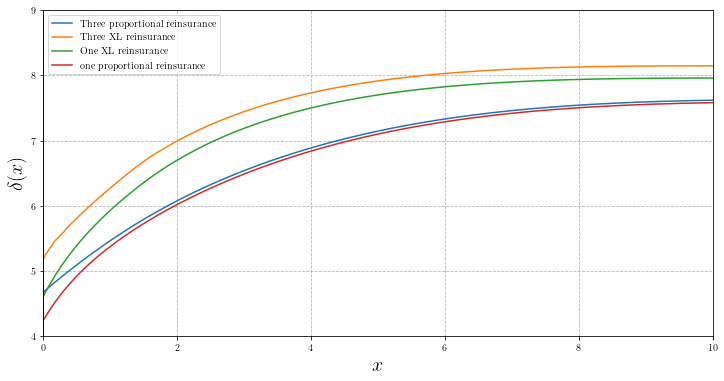

Example 4.1

Let insurance company has three lines of business such that it’s risk process has the Thinning-dependence structure, defined in Remark 2.1; , , and , and . The reinsurance strategy in th line is depicted by . As was mentioned before, if then and if then , where and are functions of the company’s capital. If the insurance company considers a reinsurance contract for three lines, the optimization issue will be equal with the uni-dimensional model scrutinized by Azcue & Muler (2014). Using the recently explained numerical method, the following results are gleaned,

-

(i)

if , then, ,

-

(ii)

if , then, ,

-

(iii)

if , then, ,

-

(iv)

if , then, .

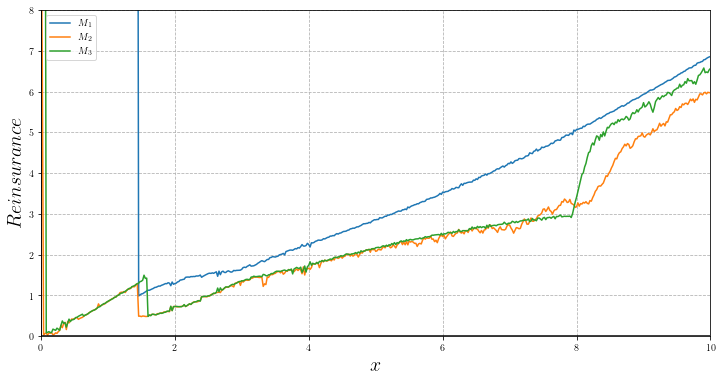

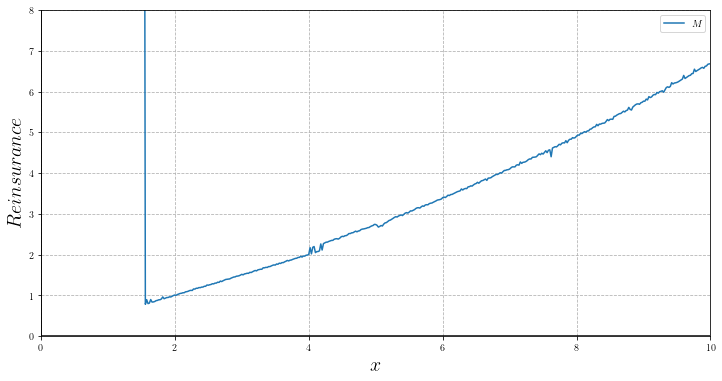

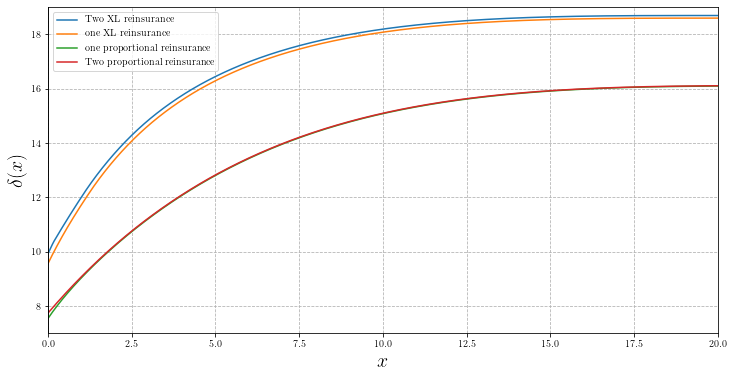

Example 4.2

(Common shock model) If , , and , then defined in (2.5) is the risk process with common shock for two dependent lines of business;

The following results are obtained by the numerical approach

-

(i)

if , then, ,

-

(ii)

if , then, ,

-

(iii)

if , then, and

-

(v)

if , then, .

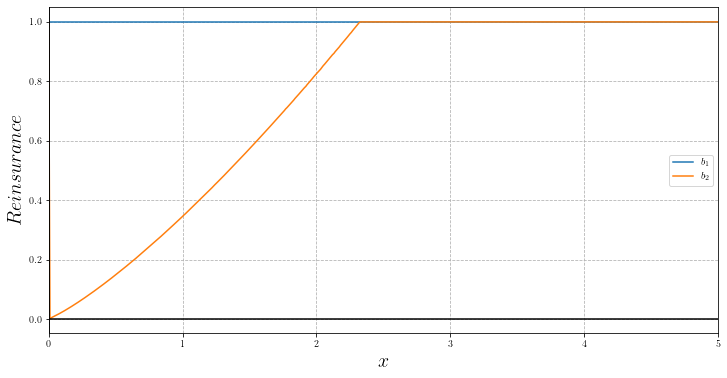

Also, optimization results for the value functions and reinsurance strategy are reported in Figures 3 and 4.

5 Conclusion

To solve this optimization issue, an HJB equation associated with the value function defined in (2.8) is adapted. Usually, the value function does not have the smoothness properties required for interpreting it as a solution for corresponding HJB equation in the classical sense, but it is satisfying in this equation in a weaker concept. The optimal survival function is characterized as the smallest super-viscosity solution of the HJB equation. Unfortunately, obtaining a closed form for the value function or the control strategy in the issue discussed in this paper is complicated or impossible. Therefore, it was more practical to adopt a numerical solution. For constructing a numerical solution, the FDM has been employed because the convergence of a numerical solution to the value function can be proved through the techniques prevalent in the literature. The convergent findings are displayed in section 4. The results of the present paper give the insurance companies this opportunity to share their risk with the reinsurers. In section 5, examples reveal that using this approach, the survival function will be increased. To sum up, with the implementation of this dynamic method for drawing the vector of the reinsurance contracts, the value function might augment significantly.

Appendix A

Proof of Proposition 2.2 Let us define

where is the time of the first claim and defined in Definition 2.1. It is obvious that , i.e., is a fixed point of . Let any , define the following complete metric space

with the metric . For any , we have that and so is well defined and bounded in . It is easy to see that

Therefore is a contraction with modulus and so, by the contraction mapping theorem, has a unique fixed point.

Now, for complete proof, it is enough to show that . If , then

Since we have . If , we have and so

For , consider and

We can find such that and for . So, and

Suppose

The HJB equation related to in is as follows

where

and is a distribution function under a reinsurance strategy. If that is so, our results are in harmony with the finding of Azcue & Muler (2005) and Azcue & Muler (2014). In the present paper, the HJB equation pertained to is as follows

where

and is defined in (2.6). Therefore, the proof of Proposition 3.8, Proposition 4.2 and Proposition 5.1 from Azcue & Muler (2005) hold water for Theorem 3.1, Proposition 3.1 and Proposition 3.2. Moreover, Proposition 3.3 and Theorem 3.2 are akin to Proposition 5.7 and Theorem 5.2 by Azcue & Muler (2014); notwithstanding, proving these theorems depends on the structure of reinsurance strategy which will be discussed accordingly.

Lemma 5.1

For any , define

If satisfying either or , then

Lemma 5.2

Let the vector , where is one of the reinsurance families , and . If u is positive and continuously differentiable, then the function is right continuous and upper semicontinuous. Moreover,

Proof For proving this lemma, we must prove that is right upper semicontinuous, left lower semicontinuous and right lower semicontinuous. Right continuous is follows from right upper semicontinuous and right lower semicontinuous, and upper semicontinuous is follows from right upper semicontinuous and left upper semicontinuous. Let us prove first that is left upper semicontinuous. For assumed , , consider reinsurance strategies such that

| (5.17) |

Then, the following is straightforward,

So, we have,

| (5.18) |

Then, from (5.17) and (5.18), the following result can be derived;

Consequently, the following relation is dominant

Now, Let us prove first that is right upper semicontinuous. We must to show that Given any sequence , take the reinsurance strategies such that

If one of the reinsurance contracts is LXL reinsurance, for example , take

such that

and . If then

Suppose , and , where a subset of a set , with exactly elements, then we have

Let us define . If , then

According to the property of right-continuously of distribution function; if , then

Now, the term should become the focus of attention. In this case, there are two situations as outlined below:

-

(I)

If there is a finite value satisfying the following,

So,

-

(II)

If

then

So,

With a similar argument we can obtain

It should be noted that So . Thus

and so we get that is right upper semicontinuous. The proof for the case and are simpler, we therefore omit them. Now, repeating the arguments presented in the proof of Proposition 7.4 of Azcue & Muler (2005) (replacing with ), the right lower semicontinuous is obtained.

Lemma 5.3

For any , let us define the function

where

Then, we have the following result;

-

(a)

is well defined and Borel measurable, , and

-

(b)

If : , and where is differentiable (i.e., a.e. in ).

-

(c)

If then .

Lemma 5.4

Let the vector , where is one of the reinsurance families , and . Then, there exists a such that

Proof It is enough to show that, there exists a , where is one of the reinsurance families , and , such that the maximum of

is attained at . Let us assume

Let denoted all the reinsurance parameters. It is easy to see that is a left-continuous function with negative jumps with respect to ’s and ’s, and right-continuous function with positive jumps with respect to ’s. For example, let , , , and :

We only investigate

Suppose that there are , and such that . It is easy to see that

So we obtain

we have that is a left-continuous function with negative jumps with respect to , and , and right-continuous function with positive jumps with respect to . So there exists at least one vector where the maximum of is attaind.

Proof of Proposition 3.3 we should prove the following,

-

(a)

is a closed set,

-

(b)

the lower limit of any connected component of belongs to ,

-

(c)

is a left-open set,

-

(d)

there is an such that ,

-

(e)

is a right-open set, and

-

(f)

both and are nonempty.

By Lemma 5.2, we get that

is closed.

Now, we must show that if and , then , that is, the lower limit of any connected component of belongs to . At first, we will take . Let us define as the severity of the first claim and as the time of this claim; then, consider the admissible strategy as such that for , . In this regard,

| (5.19) |

Now, if belong to and is immediately paid as a dividend, then and according to Lemma5.1 we have the following

Moreover, therefore the only possible state that remains is and here we obtain,

Now, let consider

then can be concluded; so, .

Now, we will take . Here, on the one hand, it is crystal clear if , then due to , will be gleaned. On the other hand, let’s consider . Here, we suppose

then based upon the Definition 2.2, the following will be satisfied

for all . So

and therefor,

for all . Then, by Lemma 5.2, we have that . Similar to the proof of Theorem 8.2 (c) by Azcue & Muler (2005), we can gain the similar result for the case

Proof for cases (c), (d), (e) and (f) is similar to proof of Theorem 8.2 of Azcue & Muler (2005).

Proof of Theorem 3.2 Based on Lemma 5.4 for , there is a such that Now we define

Where is any retained loss function. Furthermore, according to proposition 3.3, is a partition. Now, is demonstrated to be optimal, that is, . By using Proposition 2.2, we should prove the following,

-

(a)

is left continuous at the upper limits of the connected component of ,

-

(b)

is right continuous at the lower limits of the connected component of ,

-

(c)

has derivative equal to one on ,

-

(d)

is an almost-everywhere solution of in the connected components of ,

-

(e)

is a solution of

in .

By Lemma 3.2, is locally Lipschitz, so the cases (a) and (b) are true; by Definition 2.1 and Lemma 5.1, on and on , so (c) and (e) are true. Finally, is an almost-everywhere solution of in the connected components of because is a viscosity solution of (2.11), and by Lemma 5.3(b) at any of where is differentiable, hence (d) is true.

Before going in the proof of Theorem 4.1, we need the following two lemmas.

Lemma 5.5

Let some small step size such that and let . Then for all .

Proof For the assertion holds. Assume that is a positive integer with . Then and thus

So for

and thus obviously

which completes the induction.

Lemma 5.6

Let, and . In the setting of the above lemma, and define

| (5.20) |

and

| (5.21) |

if , then the functions and are respectively, sub and super viscosity solution of (2.11).

proof Firstly, we show that the function is locally Lipschitz and a viscosity subsolution of 2.11. Fix and let and that are belong to the and . Take sequences , , such that

It is easy to see that

But we have

Now, according to the above inequality and , the following relation is obtained:

where

For the case that or , or both do not belong to , proof is obvious.

To show that is a viscosity subsolution, suppose that is a test function such that has a maximum at . Note that, for sufficiently small we can find such that So, we have

| (5.22) |

Take sequences and such that , and . Then by Fatou’s lemma,

| (5.23) |

So, from 5.22 and 5.23, we have

Thus, is a viscosity subsolution. Similarly, is locally Lipschitz and a viscosity supersolution of 2.11.

Proof of Theorem 4.1. By Lemma 5.6, and are locally Lipschitz and based on Lemma 5.5 and the numerical algorithm described above, and are greater than one, and therefore satisfy the conditions (i) and (ii) of Definition 3.1. Moreover, according to the condition , and are bounded from above by . Hence, and belong to . In the proof of Proposition 3.2 we show that is smaller or equal than any supersolution of (2.11) that belongs to . So, . On the other hand, given that is a band partition and is a Lipschitz function, it is to see that is satisfied in the conditions of Proposition 2.2, and therefore , where is reinsurance band strategy associated with and . Therefore . Since by definition, we have convergence and therefore .

References

- (1)

- Albrecher et al. (2017) Albrecher, H., Azcue, P. & Muler, N. (2017), ‘Optimal dividend strategies for two collaborating insurance companies’, Advances in Applied Probability 49(2), 515–548.

- Avram et al. (2007) Avram, F., Palmowski, Z., Pistorius, M. R. et al. (2007), ‘On the optimal dividend problem for a spectrally negative lévy process’, The Annals of Applied Probability 17(1), 156–180.

- Azcue & Muler (2005) Azcue, P. & Muler, N. (2005), ‘Optimal reinsurance and dividend distribution policies in the cramér-lundberg model’, Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 15(2), 261–308.

- Azcue & Muler (2014) Azcue, P. & Muler, N. (2014), Stochastic optimization in insurance: a dynamic programming approach, Springer.

- Azcue et al. (2016) Azcue, P., Muler, N. & Palmowski, Z. (2016), ‘Optimal dividend payments for a two-dimensional insurance risk process’, arXiv preprint arXiv:1603.07019 .

- Bai et al. (2013) Bai, L., Cai, J. & Zhou, M. (2013), ‘Optimal reinsurance policies for an insurer with a bivariate reserve risk process in a dynamic setting’, Insurance: Mathematics and Economics 53(3), 664–670.

- Bäuerle & Grübel (2005) Bäuerle, N. & Grübel, R. (2005), ‘Multivariate counting processes: copulas and beyond’, ASTIN Bulletin: The Journal of the IAA 35(2), 379–408.

- Beveridge et al. (2007) Beveridge, C. J., Dickson, D. C. & Wu, X. (2007), Optimal dividends under reinsurance, Centre for Actuarial Studies, Department of Economics, University of Melbourne Melbourne.

- De Finetti (1957) De Finetti, B. (1957), Su un’impostazione alternativa della teoria collettiva del rischio, in ‘Transactions of the XVth international congress of Actuaries’, Vol. 2, New York, pp. 433–443.

- Gerber (1969) Gerber, H. U. (1969), Entscheidungskriterien für den zusammengesetzten Poisson-Prozess, PhD thesis, ETH Zurich.

- Grandits et al. (2007) Grandits, P., Hubalek, F., Schachermayer, W. & Žigo, M. (2007), ‘Optimal expected exponential utility of dividend payments in a brownian risk model’, Scandinavian Actuarial Journal 2007(2), 73–107.

- Jeanblanc-Picqué & Shiryaev (1995) Jeanblanc-Picqué, M. & Shiryaev, A. N. (1995), ‘Optimization of the flow of dividends’, Russian Mathematical Surveys 50(2), 257.

- Klugman et al. (2012) Klugman, S. A., Panjer, H. H. & Willmot, G. E. (2012), Loss models: from data to decisions, Vol. 715, John Wiley & Sons.

- Kyprianou & Palmowski (2007) Kyprianou, A. & Palmowski, Z. (2007), ‘Distributional study of de finetti’s dividend problem for a general lévy insurance risk process’, Journal of Applied Probability 44(2), 428–443.

- Liang & Yuen (2016) Liang, Z. & Yuen, K. C. (2016), ‘Optimal dynamic reinsurance with dependent risks: variance premium principle’, Scandinavian Actuarial Journal 2016(1), 18–36.

- Lindskog & McNeil (2003) Lindskog, F. & McNeil, A. J. (2003), ‘Common poisson shock models: applications to insurance and credit risk modelling’, ASTIN Bulletin: The Journal of the IAA 33(2), 209–238.

- Loeffen (2008) Loeffen, R. L. (2008), ‘On optimality of the barrier strategy in de finetti’s dividend problem for spectrally negative lévy processes’, The Annals of Applied Probability pp. 1669–1680.

- Masoumifard & Zokaei (2020) Masoumifard, K. & Zokaei, M. (2020), ‘The optimal dynamic reinsurance strategies in multidimensional portfolio’, arXiv preprint arXiv:2001.01646 .

- Meng & Siu (2011) Meng, H. & Siu, T. K. (2011), ‘On optimal reinsurance, dividend and reinvestment strategies’, Economic Modelling 28(1-2), 211–218.

- Pfeifer & Nešlehová (2004) Pfeifer, D. & Nešlehová, J. (2004), ‘Modeling and generating dependent risk processes for irm and dfa’, ASTIN Bulletin: The Journal of the IAA 34(2), 333–360.

- Schmidli (2006) Schmidli, H. (2006), ‘Optimisation in non-life insurance’, Stochastic models 22(4), 689–722.

- Thonhauser & Albrecher (2007) Thonhauser, S. & Albrecher, H. (2007), ‘Dividend maximization under consideration of the time value of ruin’, Insurance: Mathematics and Economics 41(1), 163–184.

- Wang & Yuen (2005) Wang, G. & Yuen, K. C. (2005), ‘On a correlated aggregate claims model with thinning-dependence structure’, Insurance: Mathematics and Economics 36(3), 456–468.

- Wei et al. (2017) Wei, W., Liang, Z. & Yuen, K. C. (2017), ‘Optimal reinsurance in a compound poisson risk model with dependence’, Journal of Applied Mathematics and Computing pp. 1–24.

- Wu & Yuen (2003) Wu, X. & Yuen, K. C. (2003), ‘A discrete-time risk model with interaction between classes of business’, Insurance: Mathematics and Economics 33(1), 117–133.

- Yuen et al. (2015) Yuen, K. C., Liang, Z. & Zhou, M. (2015), ‘Optimal proportional reinsurance with common shock dependence’, Insurance: Mathematics and Economics 64, 1–13.

- Yuen & Wang (2002) Yuen, K. C. & Wang, G. (2002), Comparing two models with dependent classes of business, in ‘Proceedings of the 36th Actuarial Research Conference, ARCH’.

- Zhou & Yuen (2012) Zhou, M. & Yuen, K. C. (2012), ‘Optimal reinsurance and dividend for a diffusion model with capital injection: Variance premium principle’, Economic Modelling 29(2), 198–207.

- Zhou (2005) Zhou, X. (2005), ‘On a classical risk model with a constant dividend barrier’, North American Actuarial Journal 9(4), 95–108.