2021

[]\fnmFangyuan \surZhang

]\orgdivInstitute of Insurance Science, \orgnameUniversity of Ulm, \orgaddress\streetGermany

]\orgdivan.chen@uni-ulm.de (An Chen)

]\orgdivmitja.stadje@uni-ulm.de (Mitja Stadje)

]\orgdivzhang.fangyuan@uni-ulm.de (Fangyuan Zhang)

On the equivalence between Value-at-Risk- and Expected Shortfall-based risk measures in non-concave optimization

Abstract

We study a non-concave optimization problem in which a financial company maximizes the expected utility of the surplus under a risk-based regulatory constraint. For this problem, we consider four different prevalent risk constraints (Expected Shortfall, Expected Discounted Shortfall, Value-at-Risk, and Average Value-at-Risk), and investigate their effects on the optimal solution. Our main contributions are in obtaining an analytical solution under each of the four risk constraints, in the form of the optimal terminal wealth. We show that the four risk constraints lead to the same optimal solution, which differs from previous conclusions obtained from the corresponding concave optimization problem under a risk constraint. Compared with the benchmark (unconstrained) non-concave utility maximization problem, all the four risk constraints effectively and equivalently reduce the set of zero terminal wealth, but do not fully eliminate this set, indicating the success and failure of the respective financial regulations.

keywords:

Expected Shortfall, Value-at-Risk , Average Value-at-Risk, Non-concave optimization, Equivalence1 Introduction

Expected utility theory (EUT) is an underlying hypothesis for many models in economics and finance. For instance, EUT serves as a fundamental model for studying the investor’s decision under uncertainty (merton1969lifetime, ; samuelson1975lifetime, ), and comparing or pricing financial products (chen2015utility, ; liu2021indifference, ). The influential work by Merton merton1969lifetime proposes an optimization problem based on EUT, which became a paradigm model for optimal asset allocation problems in continuous-time settings. Recently, there are many extensions of asset allocation models in order to allow for more practical considerations. For instance, to study the effect of the risk-based regulation in the financial industry, one important stream is to add a risk constraint, e.g. Value-at-Risk and Expected Shortfall, to the optimization problem. In handling the optimization problem under the risk constraints, a dominant and efficient ansatz is the Lagrangian approach from standard convex analysis. For example, the Lagrangian approach has been used to obtain closed-form solutions for the optimal asset allocation problem under a Value-at-Risk (VaR) constraint or a Limited Expected Loss (a.k.a. Expected Discounted Shortfall) constraint basak2001value , under a combined VaR-portfolio-insurance constraint chen2018optimal , and under multiple-VaR constraints in a multi-period model chen2018risk . A recent work uses quantile formulation (he2011portfolio, ; xu2016note, ) and the Lagrangian approach to investigate the optimal asset allocation problem under an Average-Value-at-Risk (AVaR) constraint wei2021risk .

The other important stream of asset allocation models is to consider a non-concave utility maximization problem. For instance, an -shape utility function is considered to model loss aversion and risk seeking behavior of an agent (tversky1992advances, ; berkelaar2004optimal, ; jin2008behavioral, ). A non-concave utility function resulting from a non-linear payoff function is modeled to study the managerial compensation problem (carpenter2000does, ; basak2007optimal, ), the participating contract problem (chen2019constrained, ; nguyen2020nonconcave, ), or the general option-type payoff problem (de2011portfolio, ). To address the non-concavity, some works first try to recover convexity by a decomposition method (jin2008behavioral, ; de2011portfolio, ) or by concavification (carpenter2000does, ; reichlin2011non, ).111jin2008behavioral and de2011portfolio decompose the terminal wealth into two random variables and such that the non-concave function is concave with respect to and convex with respect to . Then, the key challenge is to determine the proper set on which the optimal solution is defined, which is not intuitive. carpenter2000does uses concavification to solve the unconstrained non-concave optimization problem. Concavification means that one first establishes the concave envelope, e.g. the smallest concave function that dominates the original non-concave function, and then applies standard convex analysis. The optimal solution for the problem with the concave envelope is the same as the optimal solution for the original unconstrained non-concave optimization problem. A rigorous proof for this technique can be found for instance in reichlin2013utility . These methods are inspiring but are also complex to apply. More importantly, if we consider risk constraints, recovering convexity is not sufficient to solve the non-concave optimization problem.

In this work, we study non-concave optimization under risk constraints, which is related to both extensions above. We consider an optimal asset allocation problem for a managerial board of a financial company, which maximizes the expected utility arising from the surplus, i.e., the positive difference between the asset and the liability. As the surplus is a non-linear function of the terminal wealth, the resulting expected utility maximization problem is non-concave. In addition, we consider four risk constraints (Expected Shortfall, Expected Discounted Shortfall, Value-at-Risk, Average Value-at-Risk) in the optimization problem. These risk constraints are well known and are discussed widely in both the literature and the industry. Particularly, concave utility maximization under these risk constraints have been extensively studied (basak2001value, ; gandy2005portfolio, ; cuoco2008optimal, ; wei2021risk, ). However, the closed-form solutions for the non-concave utility maximization problem under these risk constraints are not available in the literature except under a VaR constraint.222One can find the optimal solution for a non-concave maximization problem arising from a non-linear payoff function under a VaR constraint in nguyen2020nonconcave , and the optimal solution with an S-shape utility function under a VaR constraint in dong2020optimal . Consequently, a thoroughly comparative analysis of the effect of these risk constraints on the non-concave utility maximization is missing. Our closed-form solutions for the non-concave utility maximization under these risk constraints fill this gap.333We remark that there are some discussions about the non-concave optimization under an AVaR constraint but these discussions are restricted to special cases. de2011portfolio studies a non-linear payoff function under an AVaR constraint, but the AVaR constraint only applies where the utility is not concave, while we do not have such a restriction. armstrong2019risk discusses an S-shape utility function under an AVaR constraint assuming that a loss can be arbitrarily large and that the terminal wealth can be negative. In this case, an AVaR constraint is never efficient in constraining the risk-seeking behavior. On the contrary, we show that an AVaR constraint is effective if the loss is bounded from below and the terminal wealth is non-negative.

We use the Lagrangian approach to solve the non-concave optimization problems under these constraints.444Note that the Lagrangian approach can be used to solve a non-concave maximization problem without risk constraints as well, see berkelaar2004optimal for the case with an S-shape utility function, and basak2007optimal ; chen2019constrained for the case with a non-concave utility arising from the non-linear payoff. Due to the non-concave utility function and the existence of a risk constraint, the constructed Lagrangian for solving the optimization problem is discontinuous and highly non-concave. By decomposing the non-concave Lagrangian into local concave or affine functions on disjoint sets, we obtain the global maximum by comparing the local maximums of the piece-wise Lagrangian, which reduces to finding the zero roots of a sequence of conjugate functions. However, it is non-trivial to determine the global maximum as the conjugate functions do not necessarily have zero roots, which implies that the existence of the optimal solution is not fully ensured. Note that in the concave optimization under these risk constraints, the existence of the optimal solution is guaranteed by the existence of the Lagrangian multipliers. However, in the non-concave optimization under these risk constraints, the optimal solution exists if the Lagrangian multipliers as well as the zero roots of the conjugate functions both exist, which is more challenging to prove. In this paper, we investigate the conditions under which the zero roots of the conjugate functions exist (Lemma A.2), and obtain the optimal solutions for the non-concave utility maximization problems under these risk constraints (Section 4).

Compared to the counterpart concave maximization problems, Expected Shortfall and Expected Discounted Shortfall bring more challenges in solving the non-concave utility maximization problem. Note that the Lagrangian multipliers for the risk constraints (Expected Shortfall or an Expected Discounted Shortfall) are explicitly involved in the optimal solution for the concave utility maximization problem. Therefore, it is straightforward to find an optimal binding solution for these problems.555A non-trivial optimal solution normally satisfies the given risk constraint with an equality, which is also called a binding solution. Contrary to our intuition, the Lagrangian multiplier for those risk constraints (Expected Shortfall and Expected Discounted Shortfall) is no longer involved in the solution, and thus finding an optimal binding solution is non-trivial. Consequently, determining the corresponding global maximum is a substantially more complex problem compared to the case under a VaR constraint in a non-concave model (Appendix B).

The optimization problem under an AVaR constraint is more challenging regardless of the utility function being concave or not. The reason is that an AVaR constraint is formulated based on the quantile function of the terminal wealth, while the optimization problem per se is formulated based on the terminal wealth. We deal with this problem in two steps. In the first step we transform an AVaR constraint to an equivalent set of Expected Shortfall constraints (Lemma 4.1), which transforms the quantile-based constraint to the terminal wealth-based constraint. Then, we show that the optimal solution for a non-concave utility maximization problem under an AVaR constraint is equivalent to the optimal solution under the equivalent Expected Shortfall constraint (Proposition 5).666Recently, the optimal solution for a concave utility maximization problem under an AVaR constraint is provided by Wei wei2021risk . He first formulates an equivalent optimization problem based on the quantile function of the terminal wealth via quantile formulation (he2011portfolio, ; xu2016note, ), and then applies the Lagrangian approach to solve the optimization problem under an AVaR constraint.

Based on the closed-form solutions, we compare these different risk constraints on the non-concave utility maximization to evaluate the efficiency of the risk-based regulation, assuming that the financial company is surplus-driven. Note that in the counterpart concave utility maximization problems, the regulatory risk constraints discussed, mainly affect the tail distribution of the optimal wealth. Moreover, it has been shown that the Expected Discounted Shortfall constraint leads to a higher terminal wealth in the tail than the unconstrained case, while the other three constraints lead to a lower terminal wealth than the unconstrained case in a concave model (basak2001value, ; wei2021risk, ). However in a non-concave model, the four risk constraints, though defined differently, all lead to the same optimal wealth in most relevant situations. In fact, it has been noticed in the literature that the company with a non-concave utility function shows a gambling behavior, by incurring a non-negligible set of zero terminal wealth or the maximum possible loss, see carpenter2000does ; berkelaar2004optimal ; jin2008behavioral . Our results show that all the four popular risk constraints cannot eliminate the set of zero terminal wealth, but can reduce the set of zero terminal wealth compared with the unconstrained case. Therefore, once considering the potential surplus-driven characteristic of the financial company, the four risk constraints are as good as or as bad as each other. Although the optimization problem is formulated to study the optimal asset allocation problem of a surplus-driven financial company under the risk-based regulation, the result in this paper can be easily extended to the area of e.g. the managerial compensation and the participating contracts problems by slightly adjusting the non-linear payoff functions.

The paper is arranged as follows. In Section 2, we define the four risk constraints formally and formulate the non-concave utility maximization problems under these constraints in a complete financial market. In Section 3, we briefly summarize the existing solutions for the counterpart concave utility maximization problems under these constraints. In Section 4, we provide the optimal solutions for the non-concave utility maximization problems under the risk constraints. In Section 5, we discuss the equivalence among these optimal solutions, and illustrate the equivalence by numerical examples. The last section concludes shortly. All technical proofs are put in appendices. Moreover, we provide a general procedure for solving the non-concave utility maximization problems under risk constraints in Appendix A.

2 The model

2.1 The financial market

We assume a complete financial market without transaction costs in continuous time that contains one traded risk-free asset (the bank account) and traded risky assets denoted by the stochastic processes .777Here is an -dimensional vector and ′ denotes the transposed sign. We fix a filtered probability space , . The unique local martingale measure is denoted by . The state price density process is defined by .888The state price density is defined in this way such that the discounted asset process is a local martingale under the risk-neutral probability measure . Throughout the paper, we assume that is atom-less. As the value of is high in a recession and low in a prosperous time, has the property of directly reflecting the overall state of the economy. Therefore, the functional relationship between the optimal wealth and will be used as an interpretation for some of the results.

The financial institution endowed with an initial capital chooses an investment strategy that we describe by , the units of th risky asset in the portfolio at time . The strategy is self-financing (i.e., no intermediate income). We assume that is adaptive with respect to the filtration . The wealth process related to a strategy starting with the initial wealth is then given by

| (1) |

In addition, the set of attainable terminal wealth is defined by

Note that in a complete financial market, it is sufficient to determine the optimal terminal wealth from the set of attainable wealth, and the corresponding investment strategy can be obtained by the martingale approach.101010After determining the optimal terminal wealth, one can calculate the optimal investment strategy for a CRRA investor through a standard procedure via Itô’s Lemma in a Black-Scholes market, see the examples in basak2001value ; carpenter2000does ; basak2007optimal ; chen2018optimal . Hence, from now on we omit the dependence of on and focus on finding the optimal terminal wealth. Without ambiguity, we use instead of to denote the state price density at time .

2.2 The model setup with an additional regulatory constraint

In this section, we formulate the non-concave utility maximization problem under a risk constraint. We consider four risk constraints, i.e., Expected Shortfall (ESP), Expected Discounted Shortfall (ESQ), Value-at-Risk (VaR) and Average Value-at-Risk (AVaR), which are all frequently discussed and applied in the literature and in practice.111111Expected Shortfall takes the expectation under the physical probability measure , and hence is abbreviated as ESP, while Expected Discounted Shortfall takes the expectation under the risk-neutral measure , and hence is abbreviated as ESQ. We first introduce the definition of the risk constraints, and then we formulate the optimization problem under each of them, respectively.

2.2.1 The definition of the risk constraints

In order to ease the notation, we always use to denote a given regulatory threshold in the different risk constraints. However, the economic interpretations of differ in each case.

Expected Shortfall and Expected Discounted Shortfall

Given a regulatory threshold , Expected Shortfall (ESP) is defined by

| (2) |

where . Defined in this way, the risk constraint ESP (2) aims to control the expected shortfall of the portfolio, where the shortfall occurs if the terminal wealth is below the regulatory threshold .

Similarly, Expected Discounted Shortfall under the same regulatory threshold is defined by

| (3) |

Obviously, definition (3) controls the discounted expected shortfall of the portfolio under the risk-neutral measure . We inherit the name “Expected Discounted Shortfall” from shi2012short . Note that the same risk constraint (3) is called Limited Expected Loss in basak2001value .

Value-at-Risk and Average Value-at-Risk

Value-at-Risk (VaR) is a quantile-based risk measure. For a terminal wealth , the VaR constraint at probability (), , is defined by

| (4) |

Thus, the VaR constraint requires the upper -quantile of the terminal wealth to be above a given threshold . Note that the VaR constraint, , is equivalent to

| (5) |

which is consistent with the literature (basak2001value, ; nguyen2020nonconcave, ; dong2020optimal, ).

The economical interpretation behind (5) is that by satisfying the VaR constraint, the terminal wealth of the financial company is above the regulatory threshold with at least probability (or the terminal wealth drops below the regulatory threshold with at most probability ).

Last but not the least, an AVaR constraint is defined by

| (6) |

where is a given regulatory parameter.121212Note that the average quantile in the tail is naturally lower than the -quantile by the definition. Therefore, we use a different notation to allow for free choices of the parameters. The VaR constraint aims to control the -quantile of the portfolio, while Average Value-at-Risk (AVaR) aims to control the average quantile of the portfolio in the tail.

These risk constraints are widely discussed in the literature. However, the same risk constraint can have a different name in other references. In order to avoid ambiguity, we give a remark on the definitions of these risk constraints.

Remark 1.

-

[i)]

-

1.

VaR and AVaR are sometimes defined with a minus sign in other works, e.g., rockafellar2000optimization ; acerbi2001expected . In those contexts, a loss per se is modeled by a (negative) random variable, and the corresponding VaR and AVaR are interpreted as the minimum amount of capital that is needed to make the portfolio acceptable. But in our context, we only focus on the (non-negative) terminal wealth. Consequently, VaR and AVaR are the positive quantile values of the terminal wealth. Other than the minus sign, the mathematical definitions of VaR and AVaR in our setting are consistent with the literature.

-

2.

We use the name AVaR to be consistent with follmer2016stochastic . It is also called conditional Value-at-Risk (rockafellar2000optimization, ; rockafellar2002conditional, ) or Expected Shortfall in other references, e.g., acerbi2001expected ; acerbi2002expected ; acerbi2002coherence ; embrechts2013model ; embrechts2014academic ; armstrong2019risk . Despite the various names, they essentially measure the average quantile of the portfolio in the tail. Moreover, an AVaR constraint can be equivalently represented in the form of an Expected Shortfall constraint under specific conditions, see Lemma 4.1. As we also cover the Expected Shortfall (ESP) constraint, we use the name AVaR to distinguish it from the ESP constraint.

2.2.2 The optimization problem under a risk constraint

We consider a surplus-driven financial institution operating in , . At time 0, the company receives an initial contribution, , from equity holders and an amount, , from debt holders. Consequently, the initial asset value of the company is given by .

We assume that the benefits of the debt holders are paid out as a lump sum at time . The benefits can be represented as follows: if there is no default at maturity, they correspond to the initial contributions of the debt holders accumulated with a (nominal) rate of return, i.e., , with , where is the risk-free rate.131313Note that if , the debt holders are better off by investing the money fully in the risk-free asset. In case of default, i.e., if , is paid out at maturity since the company has limited liability. More compactly, the debt holders’ terminal payoff is represented as

The surplus function of a financial institution, which can also be considered as the payoff to the equity holders, is the residual of the wealth, i.e.,

The surplus-driven company invests the total proceedings in a diversified portfolio of the risky and the risk-free assets as defined in Section 2.1. Further, the utility function of the managerial board is denoted by . We assume that the utility function is defined on the non-negative real line, strictly increasing, strictly concave, bounded from below,141414Unbounded utility functions will be discussed later. continuously differentiable, and satisfying the usual Inada and asymptotic elasticity (AE) conditions,

where denotes the first derivative of the utility function or the marginal utility.

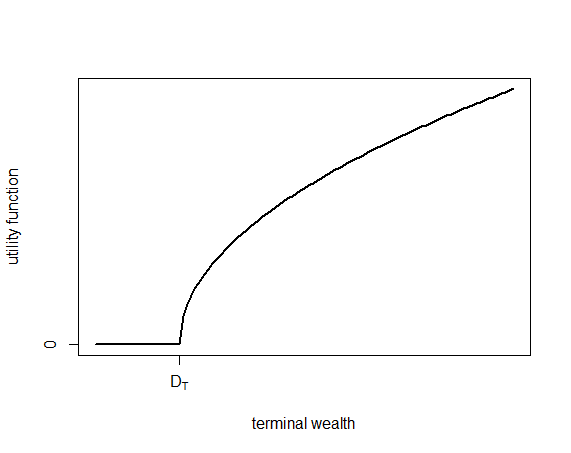

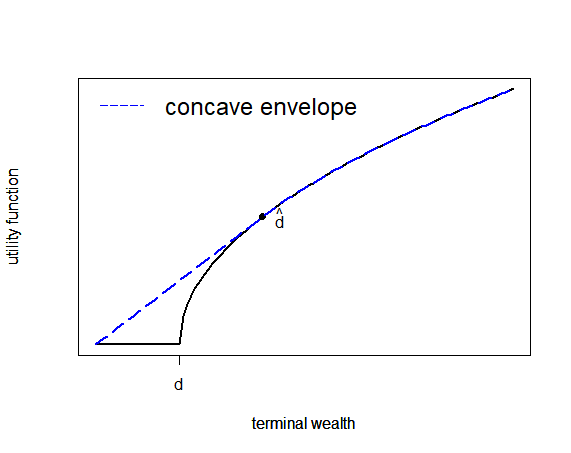

Figure 1 is an illustrative example for the utility function of a surplus-driven company, where the utility level equals zero if the wealth is below the debt level. Although the utility function is strictly concave, the utility of the surplus is not globally concave due to the non-linear function of the surplus. Thus, the consequential target function in the optimization problem is not concave. The optimization problem is formulated to maximize the expected utility of the surplus by choosing the optimal terminal wealth from the set of the attainable wealth (Section 2.1) while satisfying a risk constraint (ESQ, ESP, VaR or AVaR). We formulate the optimization problems as followings,

Problem ESQ

Problem ESP

Problem VaR

Problem AVaR

In order to better understand the distinct effect of a risk constraint on a non-concave optimization problem, we first review the optimal solution for i) a non-concave utility maximization problem without a risk constraint; ii) a concave optimization problem under a risk constraint. The readers who are familiar with these optimization problems and their solutions can jump to Section 4 directly.

3 Review on the existing solutions for (non-) concave optimization problems with(-out) constraints

3.1 Non-concave optimization without a risk constraint

If the surplus-driven company does not consider risk constraints, our optimization problem reduces to a non-concave optimization problem without constraints. We refer to this problem as the benchmark problem:

Benchmark problem

The benchmark problem can be solved with a similar procedure by concavification (carpenter2000does, ; reichlin2013utility, ), or by the Lagrangian approach (berkelaar2004optimal, ). Here, we give the optimal solution without proof.

From now on, let denote the inverse function of (marginal utility). We introduce the indicator function

The optimal solution for the benchmark problem, , is given by the following proposition.

Proposition 1.

-

[i)]

-

1.

If the utility function is bounded from below, i.e., ,

(7) where is the Lagrangian multiplier of the budget constraint obtained by solving , and is the critical value of the state price density defined by . is the unique tangent point of function defined by Lemma A.1.

-

2.

If the utility function is not bounded from below, i.e., ,

(8)

Remark 2.

-

[i)]

-

1.

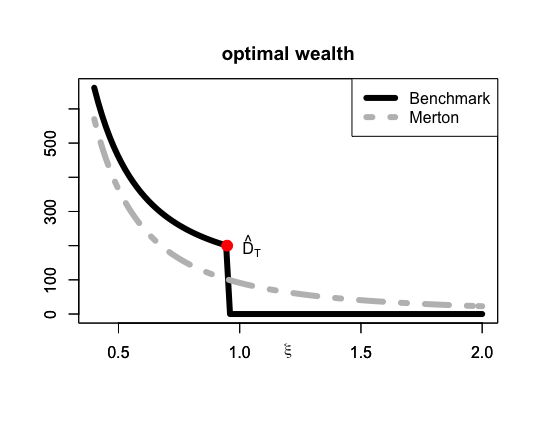

We provide the optimal terminal wealth for a bounded non-concave utility maximization problem and a non-bounded non-concave utility maximization problem, respectively. A non-bounded utility leads to a trivial case mathematically, where the optimal wealth is always above the debt level . In this case, the company will not be motivated to promise the debt holders a return that is higher than the risk-free return () since the default risk is eliminated. Economically, this can be used to model a very risk averse attitude of the managerial board which possibly does not allow for default due to reputation costs, etc.

-

2.

In the non-trivial case (), the surplus-driven company distinguishes the good and bad financial states according to the critical value of the state price density determined by its risk attitude (parametric utility functions) and the terminal debt. Consequently, the benchmark wealth is either , or is zero.151515We remark that is uniquely determined by the utility function and the debt level, and always holds. Compared with a non-surplus-driven company that maximizes the expected utility of the total asset, a surplus-driven company invests more in the good financial states to obtain a higher surplus, and ends up with zero terminal wealth in the bad financial states (Figure 2).161616The optimal terminal wealth of a non-surplus-driven company is a direct application of Merton solution (merton1969lifetime, ).

-

3.

While we consider a simple non-linear payoff function, the benchmark solution and its implication is general enough, and is consistent with the literature. The key intuition is that if the punishment for incurring the zero terminal wealth (or the maximum loss) is not large enough (), the company will anyway incur zero terminal wealth in the worst scenarios. If the punishment is too large (), the model admits a trivial solution mathematically. However, a company’s attitude towards the worst financial scenarios can only be answered by empirical studies. We include both cases for completeness.

3.2 A Concave utility maximization problem under a risk constraint

Since Merton merton1969lifetime and Samuelson samuelson1975lifetime , optimal asset allocation problems based on expected utility theory have been extensively studied. One important stream of extension considers the optimization problem with an additional risk constraint representing the risk-based regulation. In a complete financial market, explicit solutions are obtained. We find that the optimal solutions for the counterpart concave utility maximization problem under the risk constraints ESP (2), ESQ (3), VaR (5) and AVaR (6) are similar in structure, and these risk constraint mainly affect the tail distribution of the optimal terminal wealth. In order to save space, we do not repeat the explicit solution in each case, but summarize the general structure of the optimal solutions in the following proposition.171717We provide the structure of optimal solutions assuming that the risk constraints are not redundant.

Proposition 2.

-

[i)]

-

1.

Let and be the corresponding Lagrangian multipliers for the budget and one of the risk (ESP,ESQ,VaR) constraints, respectively. The general structure of the optimal solution under one of the (ESQ, ESP, VaR) risk constraints is given by

(9) where is a function of the state price density and the Lagrangian multipliers. Its concrete form depends on the exact risk constraint. In addition, and are two critical values of the state price density, and are also determined by the exact risk constraint.181818One can find the specific form for under a VaR or an ESQ constraint in basak2001value , under an ESP constraint in shi2012short .

-

2.

Under the AVaR constraint, the structure of the optimal solution is given by

(10) where is a constant but is implicitly determined by the model parameters.191919One can check wei2021risk for and under an AVaR constraint.

Remark 3.

-

[i)]

-

1.

The optimal wealth under a risk constraint distinguishes the good, intermediate and bad financial states according to the critical values of the state price density and . The exact values of and are determined by the initial wealth, the risk attitude of the company, and the concrete risk constraint. Hence, they differ in different solutions.

-

2.

The constrained optimal wealth is similar to the unconstrained Merton solution (merton1969lifetime, ) in the good financial states, is a constant in the intermediate financial states, and is different in the bad financial states under different risk constraints.

-

3.

By examining the explicit solutions, one can see that the unconstrained optimal wealth in the bad financial states is always lower than the optimal wealth under the ESQ constraint, but is higher than the optimal wealth under the ESP, VaR or AVaR constraint. Hence, compared with the other three risk constraints, the ESQ constraint provides a better protection in the concave utility maximization problem.

In the next section, we will examine how these risk constraints affect the optimal wealth in the non-concave utility maximization.

4 Non-concave utility maximization under a risk constraint

In this section, we provide the explicit solutions for the non-concave utility maximization problems under the risk constraints (ESP,ESQ,VaR,AVaR). Note that if we add a risk constraint to an optimization problem, we always have to check i) whether the optimal solution exists; ii) whether the risk constraint is redundant. A risk constraint is redundant if the unconstrained solution already satisfies the risk constraint. Given a risk constraint, this occurs if the initial wealth exceeds an upper bound (). In this case, the unconstrained solution is also the optimal solution under the risk constraint. On the other hand, the optimal solution under a non-redundant risk constraint exists if the initial wealth is sufficiently large (). Note that the exact boundary values of the initial wealth () depend on the concrete risk constraint. In the following, we provide the optimal solutions under a non-redundant risk constraint assuming that they exist. After obtaining the non-redundant optimal solutions, calculating the boundary values of the initial wealth is straightforward.

Recall that we formulate four optimization problems in Section 2.2.2, i.e., Problem ESQ, Problem ESP, Problem VaR and Problem AVaR. Surprisingly, the structures of the optimal solutions under the four risk constraints are similar. Hence, we provide the general structure of the optimal solutions in Proposition 3. In addition, we give the explicit solutions under the ESP and the AVaR constraints as examples. All other explicit solutions and the corresponding proofs are put in Appendix B.

Proposition 3.

Let and denote the Lagrangian multipliers of the budget constraint and the risk constraint. Let , and be three critical values of the state price density implicitly determined by the risk constraint, the risk attitude of the company, and the terminal debt level. Recall that is the lower bound of the optimal benchmark wealth in the good states (Proposition 1).

-

[i)]

-

1.

The general structure of the optimal solutions for the non-concave utility maximization problems under the (ESQ, ESP or VaR) constraint is given by

(11) where is a function of the Lagrangian multipliers and the state price density. Its form depends on the exact risk constraint.202020One can check Proposition 4 for under the ESP constraint, and Propositions 6 and 7 for under the ESQ and VaR constraints.

-

2.

The general structure of the optimal solution under the AVaR constraint is given by

(12) where is a constant and is implicitly determined by the model parameters, and is a function of the Lagrangian multipliers and the state price density.

Remark 4.

-

[i)]

-

1.

We have three different structures of the optimal wealth for a surplus-driven company under the risk constraints. Mathematically, this is because the highly non-concave Lagrangian can be decomposed into two, or three or four local (concave) Lagrangian on disjoint sets depending on the model parameters. Hence, the global maximum of the Lagrangian could exist on any subset. Moreover, if we fix a risk constraint, each structure of the solution exists within a limited range of the initial wealth. Economically, this means that for a fixed risk constraint, the company chooses different strategies according to its initial wealth. The company with a concave utility function (Proposition 2) has a single structure of the optimal wealth, while a surplus-driven company has multiple structures of the optimal wealth depending on the initial wealth. Hence, the strategy of a surplus-driven company is more sensitive to the change of its initial wealth.

-

2.

Each structure of the optimal solution has a non-negligible set of zero terminal wealth. Compared with the benchmark solution (Proposition 1), these risk constraints do not eliminate but can reduce this set in the non-concave optimization problems, indicating the success and failure of these risk-based financial regulations on a surplus-driven financial company.

-

3.

If the given threshold or the implicit threshold is smaller or equal to , the optimal solutions only differ in critical values of state price density and . Thus, if and are the same in different solutions, these solutions are essentially equivalent. In fact, we can establish a one-to-one relationship between risk constraints such that the optimal solutions under the corresponding risk constraints are the same. Note that the equivalence among risk constraints in a concave model does not exist due to the various distributions of the optimal wealth in the tail. We discuss the equivalence among risk constraints in the non-concave model in Section 5.

Now, we provide the complete explicit solution under the (non-redundant) ESP and AVaR constraints as examples. Other explicit solutions can be found in Appendix B.

Case 1: The optimal solution for Problem ESP

Recall that Problem ESP is given by

The optimal wealth of Problem ESP is given in the following proposition. The proof can be found in Appendix B.

Proposition 4.

-

[i)]

-

1.

If , the optimal wealth is:

(13) (14) where , is the tangent point of , is defined through , and is obtained by solving .

-

2.

If , the optimal wealth is:

(15) (16) where and is defined through , and is obtained by solving .

-

3.

If , the optimal wealth is:

(17) where , , , and are obtained by solving the equations and .

The optimal wealth for Problem ESP in Proposition 4 shows exactly the general structure of the optimal wealth under a risk constraint provided in Proposition 3. Indeed, the specific values of the state price density , and are determined by the ESP constraint, the risk attitude (utility function) and the terminal debt level. Especially, if the regulatory threshold is smaller than , and are not involved in the explicit solution. We obtain similar conclusions for the optimal solutions under the ESQ and the VaR constraints. The case with the AVaR constraint is different. We introduce the optimal solution under the AVaR constraint in the next example.

Case 2: The optimal solution for Problem AVaR

Recall that Problem AVaR is given by

subject to

The maximization problem is formulated based on the terminal wealth , while the AVaR constraint is formulated based on the quantile function of the terminal wealth. Hence, the Lagrangian approach cannot be directly applied. We deal with the problem in two steps: i) We transfer the AVaR constraint to a set of equivalent ESP constraints; ii) We show that the optimal solution under the AVaR constraint is equivalent to the optimal solution under one of the equivalent ESP constraint. The following lemma establishes the connection between the AVaR constraint and the ESP constraint.

Lemma 4.1.

-

[i)]

-

1.

If the threshold in an ESP constraint is exactly the -quantile of the terminal wealth, then the AVaR constraint is equivalent to the following ESP constraint:

(18) where

-

2.

Consider the function . The function attains its minimum if is the -quantile of ;

-

3.

A terminal wealth that satisfies a given risk constraint is called a feasible solution. The set of the feasible solutions for an AVaR constraint is equivalent to the set of the feasible solutions for the ESP constraints (regardless of being the -quantile of ), i.e.,

(19)

Argument in Lemma 4.1 follows from Proposition 4.51 in follmer2016stochastic . Arguments follow from Lemma 2.7 and Theorem 2.9 in gandy2005portfolio . Lemma 4.1 reveals the connection between the quantile-based AVaR constraint and the terminal wealth-based ESP constraint. We show in the following proposition that the optimal solution under the AVaR constraint is the same as the optimal solution under the equivalent ESP constraint. The proof of Proposition 5 can be found in Appendix B.

Proposition 5.

Suppose the AVaR constraint is given by: . Let denote the optimal solution for the following Problem ,

For a given initial wealth , there exists such that the optimal solution for Problem AVaR coincides with the optimal solution for Problem ESP with the constraint: , i.e.,

Lemma 4.1 and Proposition 5 together reveal the connection between the optimal solutions under the AVaR constraint and the ESP constraint. We remark that due to the sophisticated relationship between the various structure of the optimal solution and the initial wealth, a more explicit form of cannot be computed within the current model. However, it is sufficient to conclude that the optimal solution for Problem AVaR shows an identical structure as the optimal solution for Problem ESP. In order to better understand the economical implication of the optimal wealth, we provide a numerical illustration of the optimal solution for Problem ESP in a simple Black-Scholes market.

Numerical illustration

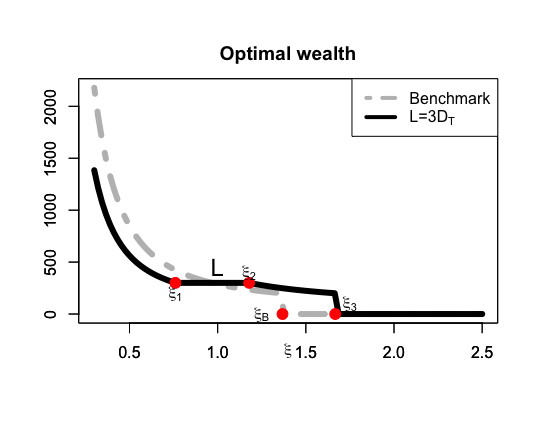

Consider a simple Black-Scholes financial market equipped with one risky asset and one risk-free asset. The basic parameters about the financial market are given in Table 1. In addition, assume that the surplus-driven company has a power utility function with a constant relative risk aversion . Thus, the utility is bounded from below ().

| 0.08 | 0.03 | 0.2 | 1 | 0.5 |

In addition, to illustrate different structures of the optimal wealth, we consider different combinations of model parameters (e.g. initial wealth and ESP constraints) in Table 2. Note that the debt level is assumed to be 100 in each case, i.e., . Consequently, , the lower bound of the benchmark wealth in the good financial states (Proposition 1) is also fixed in each case.212121Mathematically, is the unique tangent point of , and is determined by the utility function and the debt level (Lemma A.2).

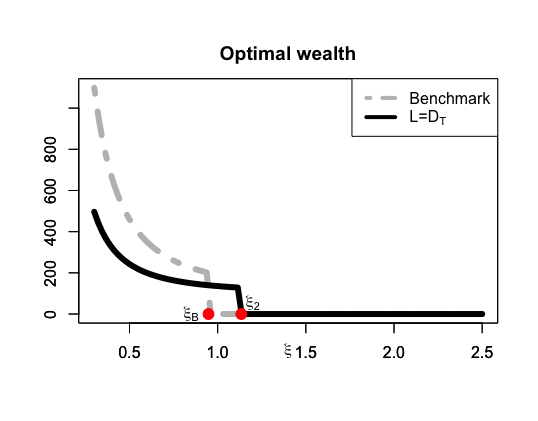

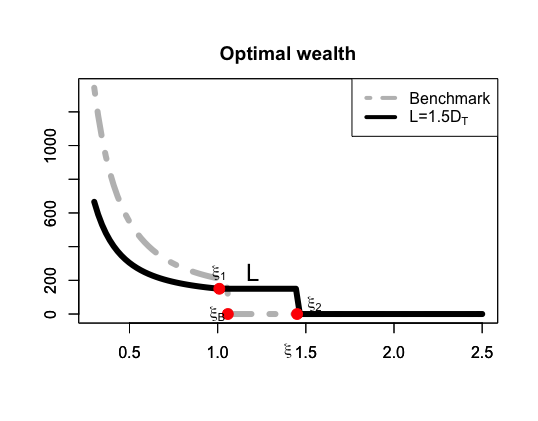

| Case 1: | 100 | 200 | 100 | 100 | 30 |

|---|---|---|---|---|---|

| Case 2: | 100 | 200 | 150 | 150 | 10 |

| Case 3: | 100 | 200 | 292 | 300 | 7 |

We plot the optimal wealth in the three different cases in Figure 3.

From Figure 3 we observe the following: i) the structure of the optimal wealth depends on the model parameters as explained in Remark 4; ii) the optimal wealth is zero in the worst financial states in all cases. However, the set of the zero wealth is always smaller than the corresponding benchmark (unconstrained) wealth.

We obtain a similar conclusion for the optimal wealth under the other risk constraints as well (Propositions 6 and 7). Hence, we conclude that these risk constraints (ESQ, ESP, VaR, AVaR) have a similar regulatory effect, that is to reduce the set of zero wealth of a surplus-driven company.

In fact, if the threshold is below the minimum benchmark wealth in the good financial states, i.e., if , the optimal wealth under different risk constraints (ESQ, ESP, VaR) only differ in the critical values of the state price density and . This implies that these optimal wealth are the same if and are the same in different solutions. Moreover, if the implicit threshold is below , the equivalence result also holds for the optimal wealth under the AVaR constraint. Note that the equivalence holds in a complete financial market and does not depend on a specific utility function or a Black-Scholes market assumption. In the next section, we investigate the equivalence among the risk constraints.

5 Equivalence among risk constraints in non-concave optimization

In this section, we discuss a by-product of obtaining the optimal solutions for the non-concave utility maximization problems under the risk constraints. We know from Proposition 3 that, if the given threshold or the implicit threshold is below , the optimal solutions only differ in the critical values of the state price density. Hence, the optimal wealth under these risk constraints are the same if and are the same. We summarize this finding in Corollary 1.

Corollary 1.

Let , , and denote the optimal wealth for the non-concave uitility maximization problem under the ESQ, ESP, VaR and AVaR constraints, respectively.

-

[i)]

-

1.

For each given VaR constraint with a significance level (5), there exists one ESQ constraint with and one ESP constraint with such that if . Note that with the same regulatory threshold , the equivalent (ESP and ESQ) constraint is unique.

-

2.

For each given AVaR constraint (6), there exists one VaR constraint , one ESQ constraint and one ESP constraint such that . The equivalent (ESP, ESQ and VaR) constraint is unique.

Proof: By examining the explicit optimal wealth under different risk constraints in Section 4 and Appendix B, one can obtain this conclusion via direct calculation.

Next, we use an numerical example in a Black-Scholes market to illustrate the equivalence.

Example

Consider the same simple Black-Scholes market with parameters in Table 1. The terminal debt for the surplus-driven company (Section 4) is fixed, i.e., . Then, the benchmark (unconstrained) wealth is either higher than or is zero.

Consider the AVaR constraint

Thus, the AVaR-based regulation requires that the average quantile of the company’s wealth in the worst 1% scenarios is at least 90% of its terminal debt.

Recall that (Proposition 3) the optimal wealth under the AVaR constraint is given by

The threshold is implicitly determined by the parameters. We construct two cases with different illustrating different structures of optimal wealth.

Case 1: .

The optimal wealth under the AVaR constraint is given by

In the given BS market, we calculate the corresponding VaR, ESQ and ESP constraints such that the optimal wealth has the same structure and is the same for each optimal wealth. To be more precise, the equivalent VaR constraint is

Hence, the equivalent VaR constraint requires that the company’s wealth is above the threshold with probability 99.9%. The equivalent ESP constraint is

which requires that the expected shortfall measured by is no more than 0.1% of its terminal debt. The equivalent ESQ constraint is

which requires that the expected discounted shortfall measured by is no more than 0.22% of its terminal debt level.

Case 2: .

The optimal wealth under the AVaR constraint is

Again, we calculate the equivalent VaR, ESP, and ESQ constraint such that the optimal wealth has the same structure and and are the same in different solutions. The equivalent VaR constraint is

which requires that the company’s wealth is above the threshold with probability 99.7%. The equivalent ESP constraint is

which requires that the expected shortfall measured by is no more than 0.3% of its terminal debt. The equivalent ESQ constraint is

which requires that the expected discounted shortfall measured by is no more than 0.73% of its terminal debt level.

In this section, we have shown an interesting by-product that the optimal wealth under different risk constraints can be made equivalent, if or is smaller than . Recall that the benchmark (unconstrained) wealth is either higher than or is zero. Considering the fact that always holds, the case is more relevant in practice, since the regulatory threshold is always set close to the debt level. This means that in most cases all the four risk constraints have the same regulatory effect on a surplus-driven financial company. There is no equivalence result in the counterpart concave maximization problems (Proposition 2), since the optimal wealth behaves very differently in the bad financial states under different risk constraints. However, if the company is surplus-driven, these risk constraints are as good as or as bad as each other.

6 Conclusion

This paper investigates the effect of risk constraints in non-concave optimization. We solve the optimization problems with a non-concave utility function under four prevalent risk constraints ESP, ESQ, VaR and AVaR, by the Lagrangian approach. Due to the non concavity and the existence of a risk constraint, we obtain several structures of the optimal solutions depending on the model parameters. Although these risk constraints are widely discussed in academia and in the industry, a comparative analysis of these risk constraints on the non-concave utility maximization problem based on the closed form solutions is missing in the literature. Our results fill this gap.

Moreover, we find that the four risk constraints, though defined differently, all lead to the same optimal wealth in the non-concave optimization problems. They equivalently and effectively reduce the set of zero terminal wealth for a surplus-driven company. Hence, we conclude that considering the potential surplus-driven characteristic of a financial company, the four risk constraints are as good as or as bad as each other.

Our results imply that it is not sufficient to rely on the expectation or quantile-based risk measure to restrict the gambling behavior of a surplus-driven financial company. A natural research question is what could be a better substitute risk measure. We leave this topic for future research.

References

- \bibcommenthead

- (1) Merton, R.C.: Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics 51(1969), 247–257 (1969)

- (2) Samuelson, P.A.: Lifetime portfolio selection by dynamic stochastic programming. Stochastic Optimization Models in Finance, 517–524 (1975)

- (3) Chen, A., Hentschel, F., Klein, J.K.: A utility-and cpt-based comparison of life insurance contracts with guarantees. Journal of Banking and Finance 61, 327–339 (2015)

- (4) Liu, H., Tang, Q., Yuan, Z.: Indifference pricing of insurance-linked securities in a multi-period model. European Journal of Operational Research 289(2), 793–805 (2021)

- (5) Basak, S., Shapiro, A.: Value-at-Risk-based risk management: optimal policies and asset prices. The Review of Financial Studies 14(2), 371–405 (2001)

- (6) Chen, A., Nguyen, T., Stadje, M.: Optimal investment under VaR-regulation and minimum insurance. Insurance: Mathematics and Economics 79, 194–209 (2018)

- (7) Chen, A., Nguyen, T., Stadje, M.: Risk management with multiple VaR constraints. Mathematical Methods of Operations Research 88(2), 297–337 (2018)

- (8) He, X.D., Zhou, X.Y.: Portfolio choice under cumulative prospect theory: An analytical treatment. Management Science 57(2), 315–331 (2011)

- (9) Xu, Z.Q.: A note on the quantile formulation. Mathematical Finance 26(3), 589–601 (2016)

- (10) Wei, P.: Risk management with expected shortfall. Mathematics and Financial Economics, 1–37 (2021)

- (11) Tversky, A., Kahneman, D.: Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5(4), 297–323 (1992)

- (12) Berkelaar, A.B., Kouwenberg, R., Post, T.: Optimal portfolio choice under loss aversion. Review of Economics and Statistics 86(4), 973–987 (2004)

- (13) Jin, H., Zhou, X.Y.: Behavioral portfolio selection in continuous time. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 18(3), 385–426 (2008)

- (14) Carpenter, J.N.: Does option compensation increase managerial risk appetite? The Journal of Finance 55(5), 2311–2331 (2000)

- (15) Basak, S., Pavlova, A., Shapiro, A.: Optimal asset allocation and risk shifting in money management. The Review of Financial Studies 20(5), 1583–1621 (2007)

- (16) Chen, A., Hieber, P., Nguyen, T.: Constrained non-concave utility maximization: An application to life insurance contracts with guarantees. European Journal of Operational Research 273(3), 1119–1135 (2019)

- (17) Nguyen, T., Stadje, M.: Nonconcave optimal investment with Value-at-Risk constraint: An application to life insurance contracts. SIAM Journal on Control and Optimization 58(2), 895–936 (2020)

- (18) De Franco, C., Tankov, P.: Portfolio insurance under a risk-measure constraint. Insurance: Mathematics and Economics 49(3), 361–370 (2011)

- (19) Reichlin, C.: Non-concave utility maximization with a given pricing measure. Available at SSRN 1940277 (2011)

- (20) Reichlin, C.: Utility maximization with a given pricing measure when the utility is not necessarily concave. Mathematics and Financial Economics 7(4), 531–556 (2013)

- (21) Gandy, R.: Portfolio optimization with risk constraints. PhD thesis, Universität Ulm (2005)

- (22) Cuoco, D., He, H., Isaenko, S.: Optimal dynamic trading strategies with risk limits. Operations Research 56(2), 358–368 (2008)

- (23) Dong, Y., Zheng, H.: Optimal investment with S-shaped utility and trading and Value at Risk constraints: An application to defined contribution pension plan. European Journal of Operational Research 281(2), 341–356 (2020)

- (24) Armstrong, J., Brigo, D.: Risk managing tail-risk seekers: VaR and expected shortfall vs S-shaped utility. Journal of Banking and Finance 101, 122–135 (2019)

- (25) Shi, Z., Werker, B.J.: Short-horizon regulation for long-term investors. Journal of Banking and Finance 36(12), 3227–3238 (2012)

- (26) Rockafellar, R.T., Uryasev, S.: Optimization of conditional Value-at-Risk. Journal of Risk 2, 21–42 (2000)

- (27) Acerbi, C., Nordio, C., Sirtori, C.: Expected shortfall as a tool for financial risk management. arXiv preprint cond-mat/0102304 (2001)

- (28) Föllmer, H., Schied, A.: Stochastic Finance. de Gruyter, Berlin (2016)

- (29) Rockafellar, R.T., Uryasev, S.: Conditional Value-at-Risk for general loss distributions. Journal of Banking and Finance 26(7), 1443–1471 (2002)

- (30) Acerbi, C., Tasche, D.: Expected shortfall: A natural coherent alternative to Value at Risk. Economic Notes 31(2), 379–388 (2002)

- (31) Acerbi, C., Tasche, D.: On the coherence of expected shortfall. Journal of Banking and Finance 26(7), 1487–1503 (2002)

- (32) Embrechts, P., Puccetti, G., Rüschendorf, L.: Model uncertainty and VaR aggregation. Journal of Banking and Finance 37(8), 2750–2764 (2013)

- (33) Embrechts, P., Puccetti, G., Rüschendorf, L., Wang, R., Beleraj, A.: An academic response to Basel 3.5. Risks 2(1), 25–48 (2014)

- (34) Rockafellar, R.T.: Convex Analysis. Princeton university press, Princeton (2015)

Appendix A Using Lagrangian to solve the optimization problem with a non-concave utility function under risk constraints

In this section, we briefly summarize the procedure for solving the optimization problems by the Lagrangian approach.

Step 1: Constructing the Lagrangian.

Consider the non-concave objective function . Denoting by one of the risk constraints, we write the budget constraint and the risk constraint as inequalities: and . For instance, the VaR constraint can be written as . Letting and be two non-negative Lagrangian multipliers, the constructed Lagrangian is given by:

| (20) |

Note that if the constraints are satisfied by strict inequalities, the Lagrangian multipliers are zero and the Lagrangian multipliers are positive if the constraints are satisfied by equalities. Hence, the optimal solution for the Lagrangian is the same as the optimal solution for the original problem. Note that strict convexity of the utility function is not required for this construction, and thus the Lagrangian can still be analysed if the utility is not globally concave.

Step 2: Determining the global maximum of the Lagrangian.

Due to the non-concave function and the risk constraints, the Lagrangian (20) is highly non-concave. But if we observe closely, the Lagrangian has sufficient convexity such that the problem can be solved. We summarize the method in the following Lemma.

Lemma A.1.

Suppose there exists a partition of , i.e., and such that the local Lagrangian is strictly concave, convex or affine. Letting denote the argmax of the local Lagrangian obtained by the Kuhn Tucker condition, i.e., , then the optimal solution is given by

| (21) |

Lemma A.1 follows directly from the generalised convex programs (rockafellar2015convex ). We only need to decompose the non-concave Lagrangian into local concave or affine Lagrangian on disjoint sets, and the global maximum of the Lagrangian is obtained by comparing the local maximums of the Lagrangian.

After we decompose the Lagrangian, we find that determining the global maximum reduces to solving a sequence of conjugate functions. The so-called conjugate functions essentially arise from comparing the local maximums of Lagrangian. We find that the optimal solutions are always zero on the set where the conjugate functions are negative. Intuitively, it means that one should not invest if the obtained utility is smaller than the cost for satisfying the constraints.

Definition 1.

For a fixed and positive , consider a concave utility function defined on which satisfies the Inada and AE condition. For a given positive , we define the conjugate function , where is the inverse function of the first derivative of and .

Lemma A.2.

-

[i)]

-

1.

is decreasing in .

-

2.

For each positive and fixed , there exists a such that . We call the tangent point of function . We plot the tangent point and the concave envelope of function in Figure 4. In addition, we have that and . In other words, is the unique zero root of the conjugate function .

-

3.

If , we have that where .

-

4.

For positive and , we define a conjugate function . Then has a zero root if and only if .

-

5.

For positive and , we define a conjugate function . Then has a zero root , and .

-

6.

We define a conjugate function , where , decreases on , increases on and hence has the minimum value .

Proof: The conjugate function describes the least upper hyperplane of the static Lagrangian . For a fixed and positive , we have that since holds for the conjugate function, denoting by the inverse function of the first derivative of . The derivative of with respect to is . As , statement i) in Lemma A.2 follows.

Note that the utility function satisfies the following Inada and asymptotic elasticity (AE) condition:

Let and rewrite as . From the Inada and the AE condition we have that

| (22) |

| (23) |

In addition, is a continuous function. Hence by the intermediate value theorem, for each positive , has a zero root. Thus, statement ii) in Lemma A.2 follows.

We see that . With a similar argument, has a unique zero root denoted by . Since and are decreasing functions in (by statement i)), we obtain that . Thus, statement v) is shown.

Statement iii) is a direct application of statement i) and ii). Statement vi) is also a consequence of statement i). Now we only need to show statement iv)

We have and holds. We can see that if , . Therefore, is a decreasing function in . We can write the conjugate function as . It follows from statement ii) in Lemma A.2 that has a unique zero root.

Step 3: Showing the existence of the Lagrangian multipliers.

In the previous steps, we construct the Lagrangian and solve the problem assuming that the Lagrangian multipliers exist. The last step is to show that the Lagrangian multipliers indeed exist such that the Lagrangian method works. We postpone this proof to Appendix C.

Appendix B The optimal solutions for Problems ESQ and VaR

In this section, we derive the optimal solutions for Problems ESQ and VaR. The proof consists of three steps: 1) We use two Lagrangian multipliers to capture the budget constraint and the risk constraint and establish the static Lagrangian. 2) Then, we find out the global maximum of the Lagrangian by discussing the zero roots of the corresponding conjugate functions. 3) We show that the maximizer (where the global maximum is achieved) is indeed the optimal solution to the problem. Because the proofs for different optimal solutions are similar, we only provide the most difficult case, the ESQ problem, in detail.

B.1 The optimal solution for Problem ESQ

The optimal wealth of Problem ESQ is given in the following proposition.

Proposition 6.

-

[i)]

-

1.

If , the optimal wealth is:

(24) (25) where , is the tangent point of , is defined through , and is obtained by solving .

-

2.

If , the optimal wealth is:

(26) (27) where and is defined through , and is obtained by solving .

-

3.

If , the optimal wealth is:

(28) where , , , and are obtained by solving the equations and .

Proof:

Case 1: .

The Lagrangian is given by

Letting denote the inverse function of the first derivative of the utility function, i.e., , the first part of the Lagrangian attains its maximum at . The second part is a negative affine function and obtains its maximum values at 0 or at the jump point since . Further, we have . Therefore, 0 is the local maximizer (argmax of the maximum) of the second part. Moreover, we can see that

| (29) |

Lemma A.2 gives the necessary and sufficient condition for the existence of the zero root of (B.1). In addition, if , we have that . Therefore, if , there is a zero root of (B.1). In particular, if tends to 0, (B.1) uniformly converges to (of which the zero root is ) on each compact set, and thus the zero root of (B.1) converges to . If tends to , (B.1) uniformly converges to ( of which the zero root is ), and the zero root of (B.1) converges to . In the case , we set . Then, the affine part of the Lagrangian is constant on . This means that both and 0 can be the local maximizer in the affine part. Moreover,

| (30) |

We know from Lemma A.2 that (B.1) has a unique zero root which is denoted by . Hence, (37) is the argmax of the Lagrangian.

Case 2:

The static Lagrangian in this case is

The Lagrangian has four possible local maximizers: on the first part, or the jump point on the second part, 0 on the third part.

If we have that , and the Lagrangian increases continuously from to except possibly at and decreases from then on. If , we have that . The Lagrangian increases continuously from to and decreases from then on except possibly at the jump point .

If , we have that , and the Lagrangian increases from to the jump point and decreases from then on. Hence, is the maximizer.

Therefore, the maximizer of the Lagrangian defined on is

| (31) |

Next, we compare the maximum given by (B.1) with in different regions to determine the global maximum.

On , we have that

| (32) |

Lemma A.2 provides the necessary and sufficient condition for the existence of the zero root of (B.1) denoted by . We have that is the global maximizer if .

Similarly on , we have that and is the zero root. Therefore, if , is the global maximizer.

Further, on , we get that of which the zero root is . Hence, if , is the global maximizer. In any other case, zero is the global maximizer.

For the sake of clarity, we formulate a table of all the critical values of .

| zero root of (B.1) |

|---|

The utility function is concave on . Assuming we have that , and . This implies that , , and . Therefore,

| (33) |

is the global maximizer of the Lagrangian in this case.

If , we have that . Hence, , and then cannot be the maximizer.

In addition, we know that holds because

Denote by the zero root of the function . If , is chosen such that . If , is chosen such that . We have proved that (40) and (41) are the global maximizer of the Lagrangian, respectively.

Now we show that Proposition 6 is the optimal solution. Suppose there exists another feasible solution . Consider

| (34) | ||||

| (35) |

The inequality (34) holds because the optimal solution satisfies both constraints with equality. The last inequality (35) is due to the fact that the optimal solution is the argmax of the static Lagrangian. The proof is complete.

B.2 The optimal solution for Problem VaR

The optimal wealth for Problem VaR is given in the following proposition.

Proposition 7.

-

[i)]

-

1.

If , the optimal wealth is:

(36) (37) where , is the tangent point of , is defined through , and is obtained by solving .

-

2.

If , the optimal wealth is:

(38) (39) where and is defined through , and is obtained by solving .

-

3.

If , the optimal wealth is:

(40) (41) where , is defined through , , is obtained by solving the equations .

B.3 Proof of Proposition 5

The proof of Proposition 4 (the optimal solution for Problem ESP) is similar to the proof in Section B.1 (the optimal solution for Problem ESQ). In this section, we provide the proof for Proposition 5, i.e., the optimal solution for Problem AVaR is equivalent to the optimal solution for Problem ESP.

Proof: Let be the supremum of the AVaR constrained problem, that is

where satisfies and . Note that for each given AVaR constraint, there is no feasible solution if the initial wealth is too small. On the other hand, if the initial wealth is too large, the unconstrained benchmark solution is the optimal one. We do not discuss these trivial cases here but only focus on the case where there is a non-trivial solution.

Because of Lemma 4.1, is also the supremum of the ES-constrained problem, that is

where is the optimal solution for Problem ESP with the constraint .

We first show that the set of the implicit threshold is close and bounded for each given initial wealth . Then, we show that the supremum of the expected utility is attainable at the implicit threshold since the expected utility is continuous in the implicit threshold.

Because of Lemma 4.1, for each given initial wealth , it is sufficient to consider the implicit threshold such that there exists an attainable wealth with being its quantile, i.e., . Thus an upper bound of is given by

The solution is given by

where denotes the -quantile of the state price density.

Thus, in a complete financial market, we can use the initial wealth to calculate explicitly the upper bound of the quantile of a feasible solution, that is

which is also the upper bound of the implicit threshold , i.e., since holds in the equivalent problem. Hence, the supremum utility can be rewritten as

From the explicit solutions of the ESP constrained problem we discussed in the previous section, we know that the function: is continuous since is continuous a.s. Therefore, we conclude that there exists such that the supremum utility is attained. By Lemma 4.1, is also the maximum utility for a feasible solution under the AVaR constraint, which implies that the optimal solution under the AVaR constrained coincides with the ES-constrained solution, that is, .

Appendix C The existence of the Lagrangian multipliers

Finally, we show the existence of the Lagrangian multipliers. In the previous section, we applied the Lagrangian approach assuming that the Lagrangian multipliers exist and are non-negative. In this section, we show that the Lagrangian multipliers truly exist.

Lemma C.1.

In the constrained optimization problem with any given feasible initial wealth (), the corresponding Lagrangian multipliers exist such that the budget constraint and the risk constraint are simultaneously binding.

We classify all the optimal solutions into two groups. The first group contains solutions which depend only on the budget Lagrangian multiplier and the second group contains solutions which depend on two Lagrangian multipliers and (see Propositions 4, 6 and 7). We see that all the optimal solutions belong to the first group except for the solutions for Problems ESP and ESQ constraints in the case . In the first group, is a function of assuming the risk constraint is binding. Therefore, as long as we show that exists, exists as well.

Proof: We first prove that the budget Lagrangian multiplier in the first group of solutions exists. Take the two-region solution for Problem ESQ in the case as an example. Recall that is the solution of and is the solution of .

We first show that the map is a strictly decreasing, continuous and surjective function from to .

Showing that is a strictly decreasing function is equivalent to show that for all . Define . Then we have and . We know that is a strictly decreasing function in almost surely. Hence, we conclude that and as long as is not an empty set. Further, we have . Thus, is a strictly decreasing function.

It is intuitive to see that is a continuous function except for countable many points. Therefore, is a continuous function in a.s.

In addition, if tends to then tends to and if tends to zero then tends to . Therefore, is a strictly decreasing, continuous and surjective function from to . Hence, for each fixed , the equation has a unique zero root which is .

Letting denote the inverse function of , from equation (B.1), we know that

and the ESQ-constraint is binding.

The other cases in the first group can be proved with similar arguments.

Next we prove that the two Lagrangian multipliers exist simultaneously such that the budget constraint and the ESQ constraint are binding simultaneously in the case .

In the first step of the proof we show that for a fixed and for , the second constraint always holds.

If tends to , converges to . Hence, the optimal solution converges to

This implies that , which obviously satisfies the ESQ constraint.

If , the optimal solution converges to

which is the benchmark solution. For a given , is a continuous and decreasing function in and thus bijective. By the intermediate value theorem, the zero root of the function exists. Let denote the zero root, which is a function of .

Denoting by the optimal terminal wealth, we have that

By equation (42) we have . If tends to zero, converges to and converges to . On the other hand if tends to , converges to . Moreover, is a continuous function in and thus as long as , by the intermediate value theorem there exists such that .

Following a similar procedure, we can show that and exist in the optimal solution for Problem ESP in the case . Recall that the optimal solution is given by

| (42) |

where , , , and are obtained by solving the equations and .

The first step is to show that given a , there exists a such that the constraint is fulfilled, i.e., there exists a such that .

Note that and . Thus, the solution tends to

Obviously, .

On the other hand, the solution tends to the benchmark solution if . In this case, we know that . Otherwise, the constraint is redundant. Thus, by the intermediate value theorem, there exists a such that . Next, we show that there exists such that . Note that implies that , and the solution tends to

In this case, . On the other hand, . Again, by the intermediate value theorem, there exists a such that .