Efficient Scenario Generation for Heavy-tailed Chance Constrained Optimization

Abstract.

We consider a generic class of chance-constrained optimization problems with heavy-tailed (i.e., power-law type) risk factors. In this setting, we use the scenario approach to obtain a constant approximation to the optimal solution with a computational complexity that is uniform in the risk tolerance parameter. We additionally illustrate the efficiency of our algorithm in the context of solvency in insurance networks.

1. Introduction

In this paper, we consider the following family of chance constrained optimization problems:

| () |

where is a -dimensional decision vector and is a -dimensional random vector in . The elements of are often referred to as risk factors; the function is often assumed to be convex in and often models a cost constraint; the parameter is the risk level of the tolerance. Our framework encompasses the joint chance constraint of the form , by setting .

Chance constrained optimization problems have a rich history in Operations Research. Introduced by Charnes et al. (1958), chance constrained optimization formulations have proved to be versatile in modeling and decision making in a wide range of settings. For example, Prekopa (1970) used these types of formulations in the context of production planning. The work of Bonami and Lejeune (2009) illustrates how to take advantage of chance constrained optimization formulations in the context of portfolio selection. In the context of power and energy control the use of chance constrained optimization is illustrated in Andrieu et al. (2010). These are just examples of the wide range of applications that have benefited (and continue to benefit) from chance constrained optimization formulations and tools.

Consequently, there has been a significant amount of research effort devoted to the solution of chance constrained optimization problems. Unfortunately, however, these types of problems are provably NP-hard in the worst case, see Luedtke et al. (2010). As a consequence, much of the methodological effort has been placed into developing: a) solutions in the case of specific models; b) convex and, more generally, tractable relaxations; c) combinatorial optimization tools; d) Monte-Carlo sampling schemes. Of course, hybrid approaches are also developed. For example, as a combination of type b) and type d) approaches, Hong et al. (2011) show that the solution to a chance constraint optimization problem can be approximated by optimization problems with constraints represented as the difference of two convex functions. In turn, this is further approximated by solving a sequence of convex optimization problems, each of which can be solved by a gradient based Monte Carlo method. Another example is Peña-Ordieres et al. (2020), which combines relaxations of type b) with sample-average approximation associated with type d) methods. In addition to the aforementioned types, Hong et al. (2020) provides an upper bound for the chance constraint optimization problem using a robust optimization with a data-driven uncertainty set, achieving a dimension independent sample complexity.

Examples of type a) approaches include the study of Gaussian or elliptical distributions when is affine both in and . In this case, the problem admits a conic programming formulation, which can be efficiently solved, see Lagoa et al. (2005). Type b) approaches include Hillier (1967), Seppälä (1971), Ben-Tal and Nemirovski (2000, 2002), Prékopa (2003), Bertsimas and Sim (2004), Nemirovski and Shapiro (2006a), Chen et al. (2010), Tong et al. (2020). These approaches usually integrate probabilistic inequalities such as Chebyshev’s bound, Bonferroni’s bound, Bernstein’s approximations, or large deviation principles to construct tractable analytical approximations. Type c) methods are based on branch and bounding algorithms, which connect squarely with the class of tools studied in areas such as integer programming, see Ahmed and Shapiro (2008), Luedtke et al. (2010), Küçükyavuz (2012), Luedtke (2014), Zhang et al. (2014), Lejeune and Margot (2016). Type d) methods include the sample gradient method, the sample average approximation and the scenario approach. The sample gradient method is usually combined with a smooth approximation, see Hong et al. (2011) for example. The sample average approximations studied by Luedtke and Ahmed (2008) and Barrera et al. (2016), although simplifying the constraint’s probabilistic structure via replacing the population distribution by sampled empirical distribution, are nevertheless hard to solve due to non-convex feasible regions. The method we consider in this paper is the scenario approach. The scenario approach is introduced and studied in Calafiore and Campi (2005) and is further developed in a series of papers, including Calafiore and Campi (2006), Nemirovski and Shapiro (2006b).

The scenario approach is the most popular generic method for (approximately) solving chance constrained optimization. The idea is to sample a number of scenarios (each scenario consists of a sample of ) and enforce the constraint in all of these scenarios. The intuition is that if for any scenario, say , the constraint is convex in , and is small, we expect that by suitably choosing the constrained regions can be relaxed by enforcing for all , leading to a good and, in some sense, tractable (if is of moderate size) approximation of the chance constrained region. Of course, this intuition is correct only when is small and we expect the choice of to be largely influenced by this asymptotic regime.

By choosing sufficiently large, the scenario approach allows obtaining both upper and lower bounds which become asymptotically tighter as . In a celebrated paper, Calafiore and Campi (2006) provide rigorous support for this claim. In particular, given a confidence level , if , with probability at least , the optimal solution of the scenario approach relaxation is feasible for the original chance constrained problem and, therefore, an upper bound to the problem is obtained.

Unfortunately, the required sample size of grows with as becomes small, limiting the scope of the scenario methods in applications. Many applications of chance constraint optimization require a very small . For example, in the 5G ultra-reliable communication system design, the failure probability is no larger than , see Alsenwi et al. (2019); for fixed income portfolio optimization, an investment grade portfolio has a historical default rate of , reported by Frank (2008).

Motivated by this, Nemirovski and Shapiro (2006b) developed a method that lowers the required sample size to the order of , making additional assumptions on the function (which is taken to be bi-affine), and the risk factors , which are to be assumed light-tailed. Specifically, the moment generating function is assumed to be finite in a neighborhood of the origin. No guarantee is given in terms of how far the upper bound is from the optimal value function of the problem as .

In the present paper, we focus on improving the scalability of in terms of for the practically important case of heavy-tailed risk factors. Heavy-tailed distributions appear in a wide range of applications in science, engineering and business, see e.g., Embrechts et al. (2013), Wierman and Zwart (2012), but, in some aspects, are not as well understood as light-tails. One reason is that techniques from convex duality cannot be applied as the moment generating function of does not exist in a neighborhood of . In addition, probabilistic inequalities, exploited in Nemirovski and Shapiro (2006b), do not hold in this setting. Only very recently, a versatile algorithm for heavy-tailed rare event simulation has been developed in Chen et al. (2019).

The main contribution of our paper is an algorithm that provides a sample complexity for which is bounded in , assuming a versatile class of heavy-tailed distributions for . Specifically, we shall assume that follows a semi-parametric class of models known as multivariate regular variation, which is quite standard in multivariate heavy-tail modeling, cf. Embrechts et al. (2013), Resnick (2013). A precise definition is given in Section 5. Moreover, our estimator is shown to be within a constant factor to the solution to () with high probability, uniformly as . We are not aware of other approaches that provide a uniform performance guarantee of this type.

We illustrate our assumptions and our framework with a risk problem of independent interest. This problem consists in computing a collective salvage fund in a network of financial entities whose liabilities and payments are settled in an optimal way using the Eisenberg-Noe model, see Eisenberg and Noe (2001). The salvage fund is computed to minimize its size in order to guarantee a probability of collective default after settlements of less than a small prescribed margin. For the sake of demonstrating the broad applicability of our method, we present a portfolio optimization problem with value-at-risk constraints as an additional running example.

The rest of the paper is organized as follows. In Section 2, we introduce the portfolio optimization problem and the minimal salvage fund problem as particular applications of chance constraint optimization. We employ both problems as running examples to provide a concrete and intuitive explanation for the concepts we introduce throughout the paper. In Section 3, we provide a brief review of the scenario approach in Calafiore and Campi (2006).

The ideas behind our main algorithmic contributions are given in Section 4, where we introduce its intuition, rooted in ideas originating from rare event simulation. Our algorithm requires the construction of several auxiliary functions and sets. How to do this is detailed in Section 5, in which we also present several additional technical assumptions required by our constructions. In Section 5, we also explain that our procedure results in an estimate which is within a constant factor of the optimal solution of the underlying chance constrained problem with high probability as . In Section 6 we show that the assumptions imposed are valid in our motivating example (as well as a second example with quadratic cost structure inside the probabilistic constraint). Numerical results for the examples are provided in Section 7. Throughout our discussion in each section we present a series of results which summarize the main ideas of our constructions. To keep the discussion fluid, we present the corresponding proofs in Appendix A unless otherwise indicated.

Notations: in the sequel, is the set of non-negative real numbers, is the set of positive real numbers, and is the extended real line. A column vector with zeros is denoted by , and a column vector with ones is denoted by . For any matrix , the transpose of is denoted by ; the Frobenius norm of is denoted by . The identity matrix is denoted by . For two column vectors , we say if and only if . For and , we use to denote the scalar multiplication of with . For and , we define . The optimal value of an optimization problem is denoted by . We also use Landau’s notation. In particular, if and are non-negative real valued functions, we write if for some and if for some .

2. Running Examples

2.1. Portfolio Optimization with VaR Constraint

We first introduce a portfolio optimization problem. Suppose that there are assets to invest. If we invest a dollar in the -th asset, the investment has mean return and a non-negative random loss . Let represent the amount of dollar invested in different assets, and let and . We assume that follows a multivariate heavy-tailed distribution, in a way made precise later on. The portfolio manager’s goal is to maximize the mean return of the portfolio, which is equal to , with a portfolio risk constraint prescribed by a risk measure called value-at-risk (VaR). The VaR at level for a random variable is defined as

For a given number , we formulate the following portfolio optimization problem.

Using the definition of VaR and the fact that the cumulative distribution function is right continuous, we conclude that is equivalent to . In order to facilitate the technical exposition, we apply the change of variable to homogenize the constraint function, yielding the following equivalent chance constrained optimization problem in standard form:

| (7) |

where . Despite the nonlinear objective, (Calafiore and Campi 2005, Section 4.3) shows that it admits an epigraphic reformulation with a linear objective so that the standard scenario approach is applicable.

2.2. Minimal Salvage Fund

Suppose that there are entities or firms, which we can interpret as (re)insurance firms. Let denotes the vector of incurred losses by each firm, where denotes the total incurred loss that entity is responsible to pay. We assume that follows a multivariate heavy-tailed distribution as in the previous example. Let be a deterministic matrix where denotes the amount of money received by entity when entity pays one dollar. We assume that and . Let denote the total amount that the salvage fund allocated to each entity, and denote the amount of the final settlement. The amount of final settlement is determined by the following optimization problem:

In words, the system maximizes the payments subject to the constraint that nobody pays more than what they have (in the final settlement), and nobody pays more than what they owe. Notice that is also a random variable (the randomness comes from ) satisfying . Suppose that entity bankrupts if the deficit , where is a given vector. We are interested in finding the minimal amount of salvage fund that ensures no bankruptcy happens with probability at least The problem can be formulated as a chance constraint programming problem as follows

| (11) |

Now we write the problem (11) into standard form. Notice that if and only if , where is defined as follows

Therefore, problem (11) is equivalent to

| (15) |

3. Review of Scenario Approach

As mentioned in the introduction, a popular approach to solve the chance constraint problem proceeds by using the scenario approach developed by Calafiore and Campi (2006). They suggest to approximate the probabilistic constraint by sampled constraints for , where are independent samples. Instead of solving the original chance constraint problem (), which is usually intractable, we turn to solve the following optimization problem

| () |

The total sample size should be large enough to ensure the feasible solution to the sampled problem () is also a feasible solution to the original problem () with a high confidence level. According to Calafiore and Campi (2006), for any given confidence level parameter , if

then any feasible solution to the sampled optimization problem () is also a feasible solution to () with probability at least . However, when is small, the total number of sampled constraints is of order , which could be a problem for implementation. For example, as we shall see in Section 7, when , and , the number of sampled constraints is required to be larger than . In contrast, our method only requires to sample constraints.

4. General Algorithmic Idea

To facilitate the development of our algorithm, we introduce some additional notation and a desired technical property. As we shall see, if the technical property is satisfied, then there is a natural way to construct a scenario approach based algorithm that only requires of total sampled constraints. We exploit key intuition borrowed from rare event simulation. A common technique exploited, for example, in Chen et al. (2019), is the construction of a so-called super set, which contains the rare event of interest. The super set should be constructed with a probability which is of the same order as that of the rare event of interest. If the conditional distribution given being in the super set is accessible, this can be used as an efficient sampling scheme. The first part of this section simply articulates the elements involved in setting the stage for constructing such a set in the outcome space of . Later, in Section 5, we will impose assumptions in order to ensure that the probability of the super set, which eventually we will denote by is suitably controlled as . Simply collecting the elements necessary to construct requires introducing some super sets involving the decision space, since the optimal decision is unknown.

Let denote the feasible region of the chance constraint optimization problem (), i.e.,

| (19) |

Here, the subscript is involved to emphasize that the feasible region is parametrized by the risk level . For any fixed , let denote the violation event at .

Property 1.

For any , there exist a set , and an event that satisfy the following statements.

-

a)

The feasible set is a subset of .

-

b)

The event contains the violation event for any .

-

c)

There exist a constant independent of such that .

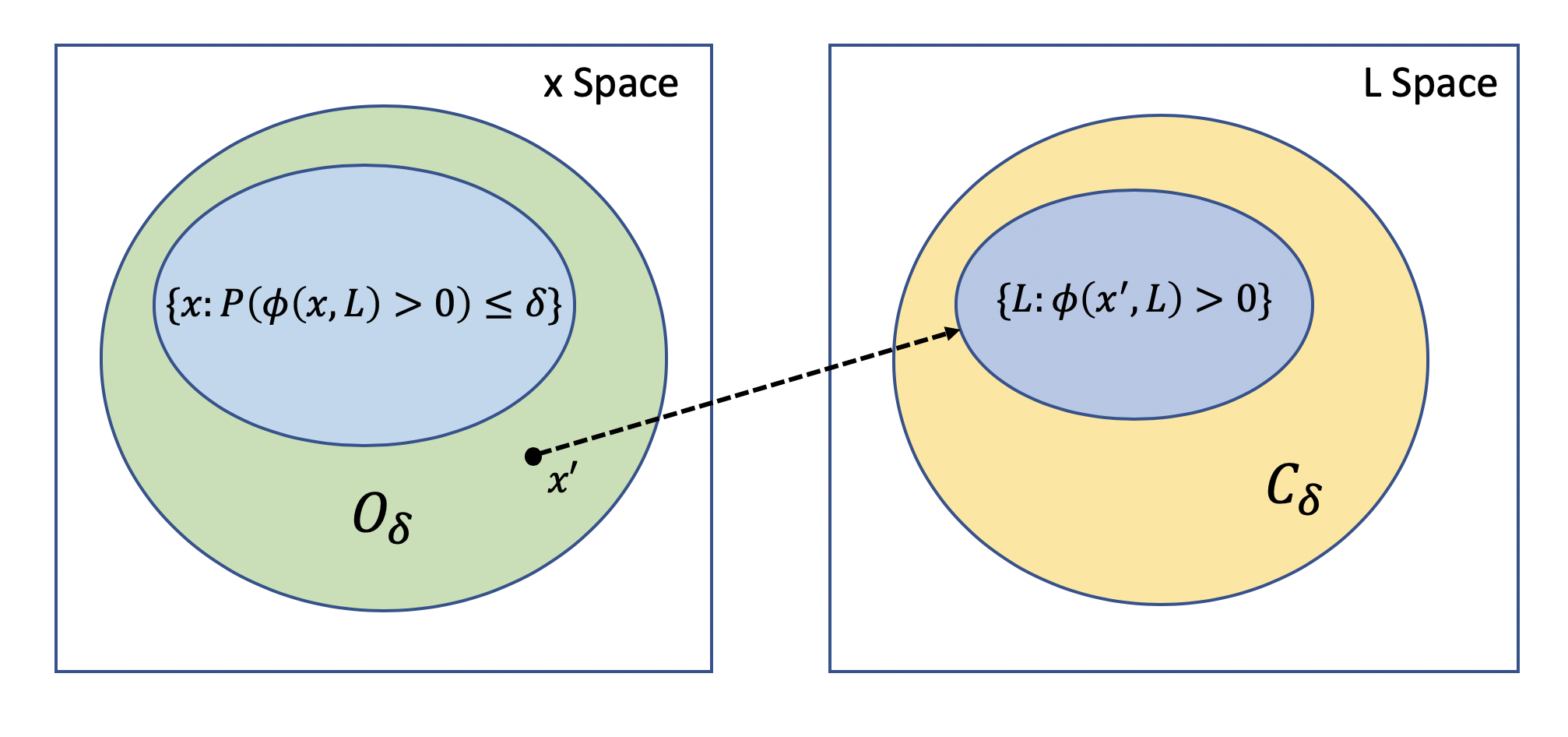

In the rest of this paper, we will refer to as the outer approximation set, and as the uniform conditional event. A graphical illustration of and is shown in Figure 1.

Now, given and that satisfies Property 1, we define the conditional sampled problem ():

| () |

where are i.i.d. samples generated from the conditional distribution .

We now present our main result of this section in Lemma 1, which validates () is an effective and sample efficient scenario approximation by incorporating (Calafiore and Campi 2006, Theorem 2) and Property 1. The proof of Lemma 1 will be presented in Section 4.1.

Lemma 1.

Suppose that Property 1 is imposed, and let be a given confidence level.

- (1)

-

(2)

Let be any integer such that . Assume that the chance constraint problem () is feasible. Then, with probability at least , .

Remark 1.

Remark 2.

Efficiently generating samples of when requires rare event simulation techniques. For example, when is light-tailed, exponential tilting can be applied to achieve sample complexity uniformly in ; when is heavy-tailed, with the help of specific problem structure, one can apply importance sampling, see Blanchet and Liu (2010), or Markov Chain Monte Carlo, see Gudmundsson and Hult (2014), to design an efficient sampling scheme. The specific structure of our salvage fund example results in being the complement of a box, which makes the sampling very tractable if the element of are independent.

Even if the aforementioned rare event simulation techniques are hard to apply in practice, we can still apply a simple acceptance-rejection procedure to sample the conditional distribution . It costs samples of on average to get one sample of , since . Consequently, the total complexity for generating and solving is , which is still much more efficient than the scenario approach in Calafiore and Campi (2006), because it requires computational complexity for solving a linear programming problem with sampled constraints by the interior point method.

Although Property 1 seems to be restrictive at first glance, we are still able to construct the sets and for a rich class of functions , including the constraint function for the minimal salvage fund problem. As we shall see in the proof of Lemma 1, once and are constructed the sampled problem () is a tractable approximation to the problem (). We explain how to construct the sets and in the next section under some additional assumptions. These assumptions relate in particular to the distribution of . It turns out that, if is heavy-tailed, the construction of and becomes tractable.

4.1. Proof of Lemma 1.

If Property 1 is satisfied, () is equivalent to

| (27) |

Let denote the risk level in the equivalent problem (27). The sampled optimization problem related to problem (27) is given by

| () |

where the are independently sampled from . Notice that

According to (Calafiore and Campi 2006, Corollary 1 and Theorem 2), with probability at least , if the sampled problem () is feasible, then the optimal solution to problem () is feasible to the chance constraint problem (27), thus it is also feasible for (). The proof of the first statement is complete.

Now we turn to prove the second statement. Note that the equivalence between () and (27) is still valid, so it is sufficient to compare the optimal values of (27) and (). By applying (Calafiore and Campi 2006, Theorem 2) again, we have with probability at least the value of () is smaller or equal than the optimal value of

| (34) |

The proof is complete by using . So, using for “value of”, .

5. Constructing outer approximations and summary of the algorithm

In this section, we come full circle with the intuition borrowed from rare event simulation explained at the beginning of Section 4. The scale-free properties of heavy-tailed distributions (to be reviewed momentarily) coupled with natural (polynomial) growth conditions (like the linear loss) given by the structure of the optimization problem, provide the necessary ingredients to show that the set has a probability which is of order . In this section, we present two methods for the construction of and satisfying Property 1. We mostly focus on our “scaling method” which is presented in Section 5.1, which is facilitated precisely by the scale-free property that we will impose on . After showing the construction of the outer sets under the scaling method, we summarize the algorithm at the end of Section 5.1. We supply a lower bound guaranteeing a constant approximation for the output of the algorithm in Section 5.2. Our second method for outer approximation constructions is summarized in Section 5.3. This method is simpler to apply because is based on linear approximations, however, it is somewhat less powerful because it assume that is jointly convex.

5.1. Scaling Method

We are now ready to state our assumption on the distribution of . We assume that the distribution of is of multivariate regular variation, a definition that we review first. For background, we refer to Resnick (2013). Let denote all Radon measures on the space (recall that a measure is Radon if it assigns finite mass to all compact sets). If , then converges to vaguely, denoted by , if for all compactly supported continuous functions ,

is multivariate regularly varying with limit measure if

Assumption 1.

is multivariate regularly varying with limit measure .

We give some intuition behind this definition. Write in terms of polar coordinates, with the radius and a random variable taking values on the unit sphere. The radius has a one-dimensional regularly varying tail (i.e. we can write for a slowly varying function and ). The angle , conditioned on being large, converges weakly (as ) to a limiting random variable. The distribution of this limit can be expressed in terms of the measure . For another recent application of multivariate regular variation in operations research, see Kley et al. (2016).

We proceed to analyze the feasible region when . Intuitively, if the violation probability has a strictly positive lower bound in any compact set, then will ultimately be disjoint with the compact set when . Thus, the set is expelled to infinity when in this case. is moving towards the direction that becomes small such that the violation probability becomes smaller. For instance, if is one dimensional and is increasing in , then is moving towards the negative direction. Consider the portfolio optimization problem as another example, in which as .

Now we begin to construct the outer approximation set . To this end, we need to introduce an auxiliary function which we shall call a level function.

Definition 1.

We say that is a level function if

-

(1)

for any and , we have ,

-

(2)

.

We also define the level set .

As is moving to infinity, the level function is helpful to characterize the ‘moving direction’ of as well as the correct rate of scaling as becomes small. As we shall see in the proof of Lemma 2, for any small enough we can choose some and define

To construct , we first select the level set , and then derive the scaling rate of .

The level function and the shape of should be chosen in accordance with the moving direction of to reduce the size of , in order to achieve better sample complexity. For example, when , the level function can be chosen as the Euclidean norm and can be chosen as the unit sphere in . For the portfolio optimization problem, the level function can be chosen as in accordance with our intuition that , and the level set can be chosen as . Therefore, it is natural to impose the following assumption about the existence of the level function.

Assumption 2.

There exist a level function and a level set .

To analyze the asymptotic shape of the uniform conditional event , we connect the asymptotic distribution of to the asymptotic distribution of . We pick a continuous non-decreasing function such that to characterize the scaling rate of . In addition, we pick another positive function to characterize the scaling rate of . Intuitively, the scaling function and should ensure the condition that is tight. For the minimal salvage fund problem with fixed , as the deficit is asymptotically linear with respect to the salvage fund and the loss , we can simply pick in this problem. We next introduce two auxiliary functions and .

Definition 2.

Let , be two Borel measurable functions. We say (resp. ) is the asymptotic uniform upper (resp. lower) bound of over the level set if for any compact set ,

| (35a) | |||

| (35b) |

In Section 6, we show for the salvage fund example how and can be written as maxima or minima of affine functions. Here, we employ the functions and to define the event and , which serve as the inner and outer approximation of the event , where is the violation event at .

Definition 3.

For , let (resp. ) be the -outer (resp. inner) approximation event

| (36a) | |||

| (36b) |

We now define . The following property ensures that the shape of is appropriate and is large enough, hence is an outer approximation of .

Property 2.

There exist such that for any , we have an explicitly computable constant that satisfies

If the violation probability is easy to analyze, we will directly derive the expression of and verify Property 2. Otherwise, we resort to Lemma 2, which provides a sufficient condition of Property 2 by analyzing the asymptotic distribution. The proof of Lemma 2 is deferred to Appendix A.

Lemma 2.

We impose the following Assumption 3 on the asymptotic uniform upper bound so that we can employ the multivariate regular variation of to estimate for large scaling factor .

Assumption 3.

There exist an event with such that

In addition, there exist some such that is bounded away from the origin, i.e.,

For the minimal salvage fund problem, since the deficit function is coordinatewise nondecreasing with respect to the loss vector , it is reasonable to assume that its asymptotic bound is also coordinatewise nondecreasing. For this example, the closed form expression of and the detailed verification of all the assumptions are deferred to Proposition 9. Our next result summarizes the construction of the outer approximation sets.

Theorem 3.

With the aid of Lemma 1 and Theorem 3, we provide Algorithm 1 for approximating () in which the sampled optimization problem is bounded in .

In Section 5.2, our objective is to show that the output of the previous algorithm is guaranteed to be within a constant factor of the optimal solution to () with high probability, uniformly in .

5.2. Constant Approximation Guarantee

We shall work under the setting of Theorem 3, so we enforce Property 2 and Assumptions 3. We want to show that there exist some constant independent of , such that with high probability. This indicates that our result guarantees a constant approximation to () for regularly varying distributions (under our assumptions) in sample complexity when with high probability.

Note that is meaningful only if . We assume that the outer approximation set is good enough such that the following natural assumption is valid.

Assumption 4.

There exist such that .

The previous assumption will typically hold if has strictly positive entries. Theorem 3 and the form of guarantee that the norm of the optimal solution of () grows in proportion to , so we also assume the following scaling property for .

Assumption 5.

There exist a function such that for every compact set , we have

In addition, is continuous in .

Assumption 5 is satisfied by both running examples. For the portfolio optimization problem, we have , thus . For the minimal salvage fund problem, we have such that and .

We define the following optimization problem, which will serve as an asymptotic upper bound of in stochastic order when :

| () |

where are i.i.d. samples from a random variable , whose distribution is characterized by and for all measurable set .

Theorem 4.

Slater’s condition (See Section 5.2.3 in Boyd and Vandenberghe (2004) for reference) can be verified directly on the problem (). This condition is satisfied in the salvage fund problem by standard linear programming duality.

5.3. Linear Approximation Method

Suppose that the constraint function is jointly convex in , and is multivariate regularly varying. We will develop a simpler method in this section to construct the outer approximation set and the uniform conditional event .

We first introduce a crucial assumption in the construction of and .

Assumption 6.

There exist a convex piecewise linear function of the form

such that:

-

(1)

;

-

(2)

there exist some constant such that if .

If itself is a piecewise affine function, then Assumption 6 is satisfied by simply taking . For general jointly convex functions, the following lemma verifies Assumption 6 if has a compact zero sublevel set.

Lemma 5.

If the constraint function is convex and twice continuously differentiable, and it has a compact zero sublevel set , then Assumption 6 is satisfied.

With Assumption 6 enforced, we are now ready to provide our main result in this section to fully summarize the construction of and .

6. Verifying the Assumptions in Examples

In this section, we verify the elements required to apply our algorithm. We provide explicit expressions for sets and in the statement of the propositions. The detailed verification process and the steps for constructing sets and are presented as the proofs in Appendix A.

6.1. Portfolio Optimization with VaR Constraint

6.2. Minimal Salvage Fund

The key observation to solve the minimal salvage fund problem (15) is the following lemma, which provides a closed form piecewise linear expression for the constraint function .

Lemma 8.

In the minimal salvage fund problem (15), we have

where denote the unit vector on the -th coordinate.

6.3. Quadratic Model

In this section, we consider a model with a quadratic control term in as an additional example. Suppose that the constraint function is defined as

| (41) |

where is a symmetric matrix and is a matrix with , i.e. there exist such that .

Proposition 10.

Consider the chance constraint optimization model with constraint function defined as (41).

-

(1)

If is a positive semi-definite matrix and has a positive density, there exist some such that the problem is infeasible.

-

(2)

If has a negative eigenvalue and is multivariate regularly varying, the model satisfies all the assumptions required by Theorem 3.

7. Numerical Experiments

In order to empirically study the computational complexity and compare the quality of the solutions, in this section we conduct numerical experiments for two scenario generation algorithms:

-

(1)

the efficient scenario generation approach proposed in this paper (abbreviated as Eff-Sc);

-

(2)

the scenario approach in Calafiore and Campi (2006) (abbreviated as CC-Sc).

In Section 7.1, we present the results for the portfolio optimization problem. In Section 7.2, we present the results for the minimal salvage fund problem. The numerical experiment is conducted using a Laptop with 2.2 GHz Intel Core i7 CPU, and the sampled linear programming problem is solved using CVXPY (Diamond and Boyd (2016)) with the MOSEK solver (MOSEK ApS (2020)).

7.1. Portfolio Optimization with VaR Constraint

First of all, we present the parameter selection and the implement details for the numerical experiment of portfolio optimization problem (7). Suppose that there are assets to invest, and the parameters of the problem are chosen as follows:

-

•

The mean return vector is .

-

•

are i.i.d. with Pareto cumulative distribution function , for .

-

•

.

-

•

The loss threshold .

Now we explain the implementation detail of Eff-Sc. Recall the expression of and from Proposition 7, which involves the analytically unknown quantity . Since quantile estimation is much more computationally efficient than solving the sampled optimization problem, we generate samples of to estimate a confidence interval of with large enough confidence level , and we denote the resulting confidence interval by . We replace the expressions of and by their sampled version conservative approximations, i.e.

The value of is also estimated using the generated samples. We compute the required number of samples using Lemma 1, and the samples of is generated via acceptance-rejection.

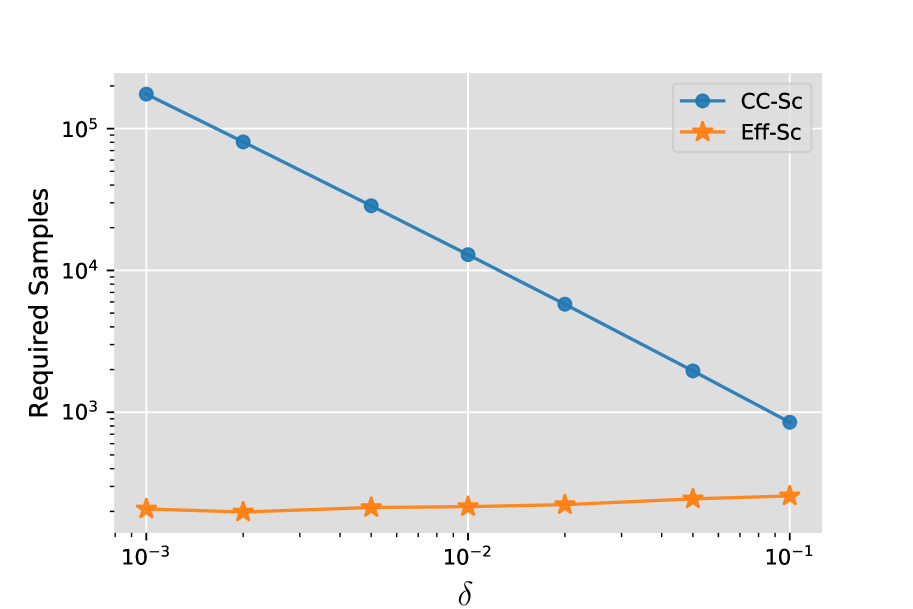

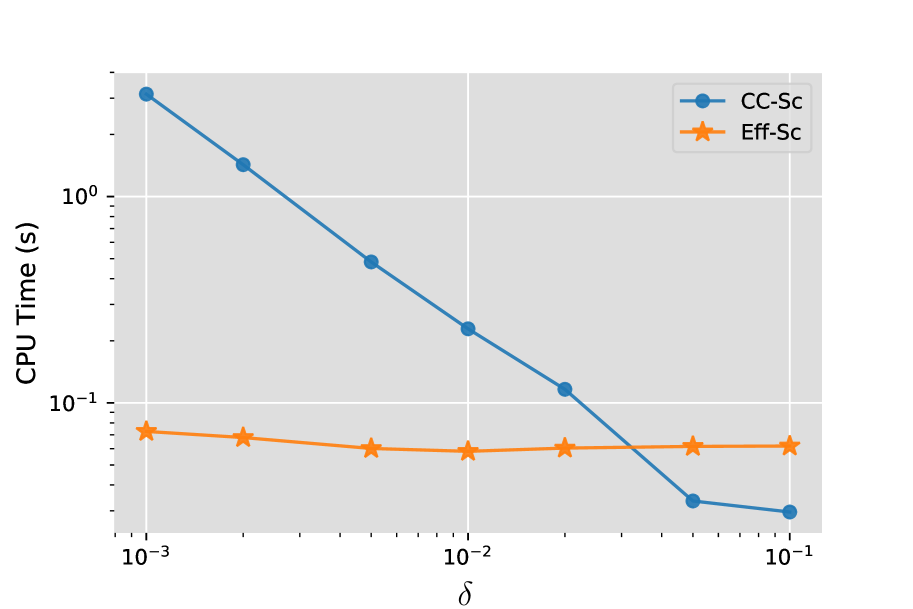

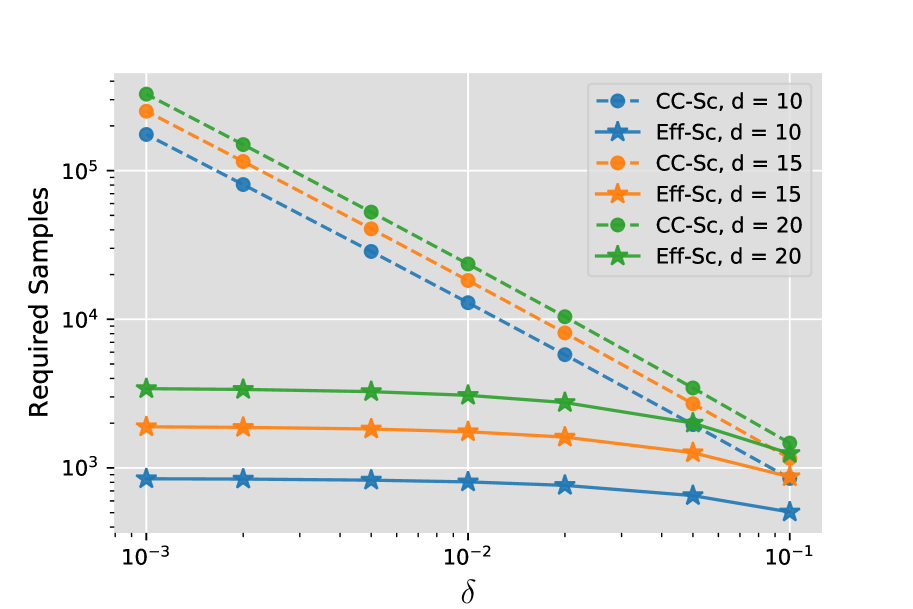

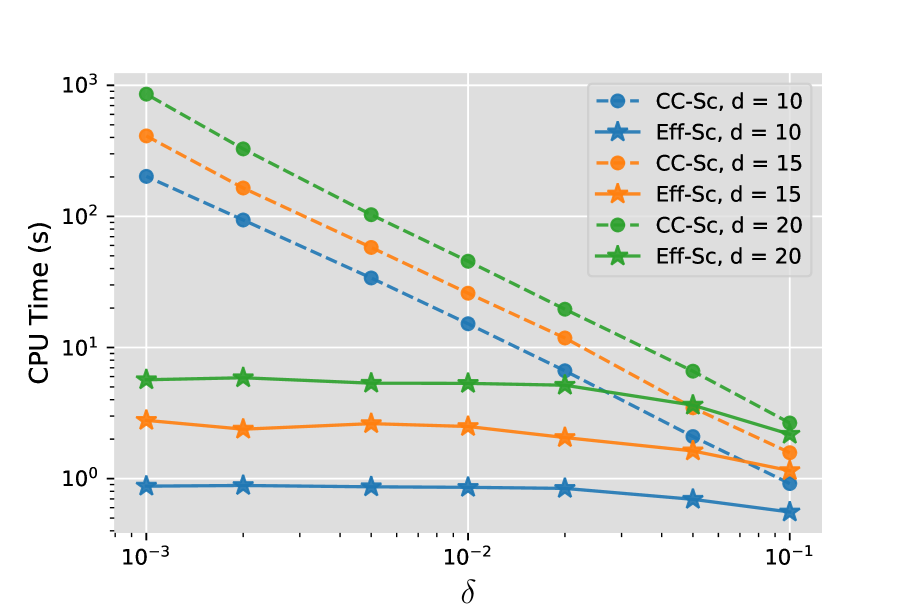

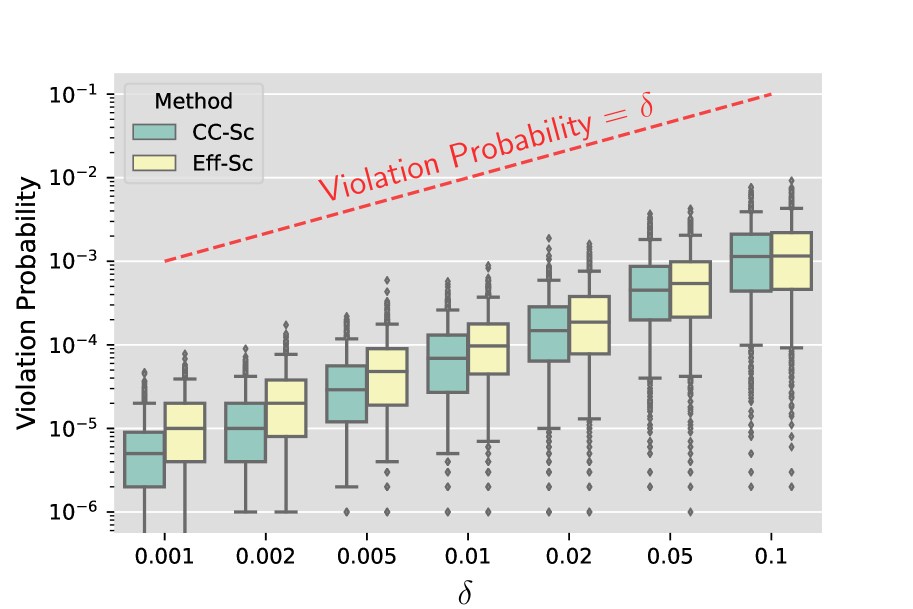

In Figure 2, we compare the efficiency between Eff-Sc and CC-Sc. Figure 2(a) presents the required number of samples for both algorithms, in which one can quickly remark that Eff-Sc requires significantly fewer samples than CC-Sc, especially for the problems with small . In Figure 2(b) we compare the running time for both models. Whereas Eff-Sc costs slightly more time for around due to the overhead cost of computing and , the computational time stays nearly constant uniformly in , indicating that Eff-Sc is a substantially more efficient algorithm than CC-Sc.

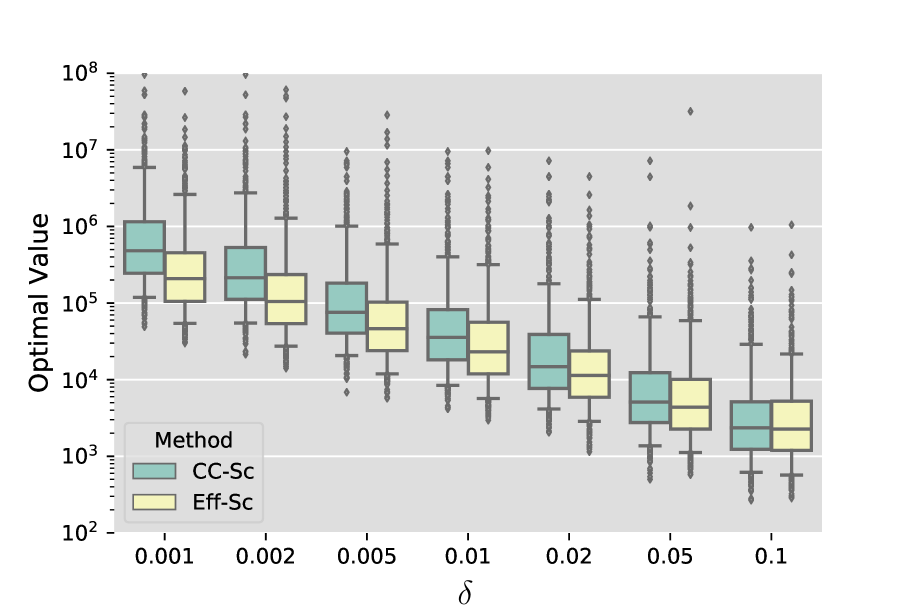

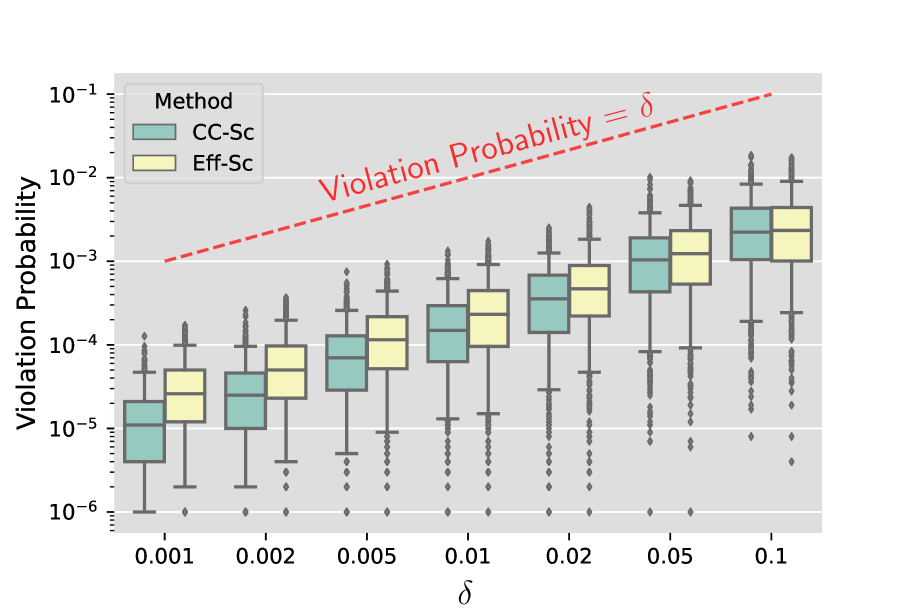

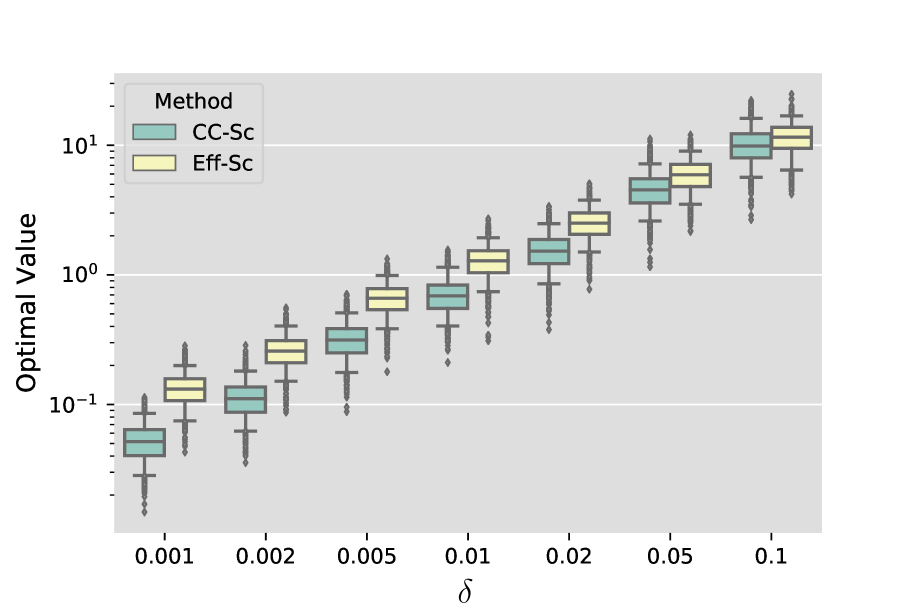

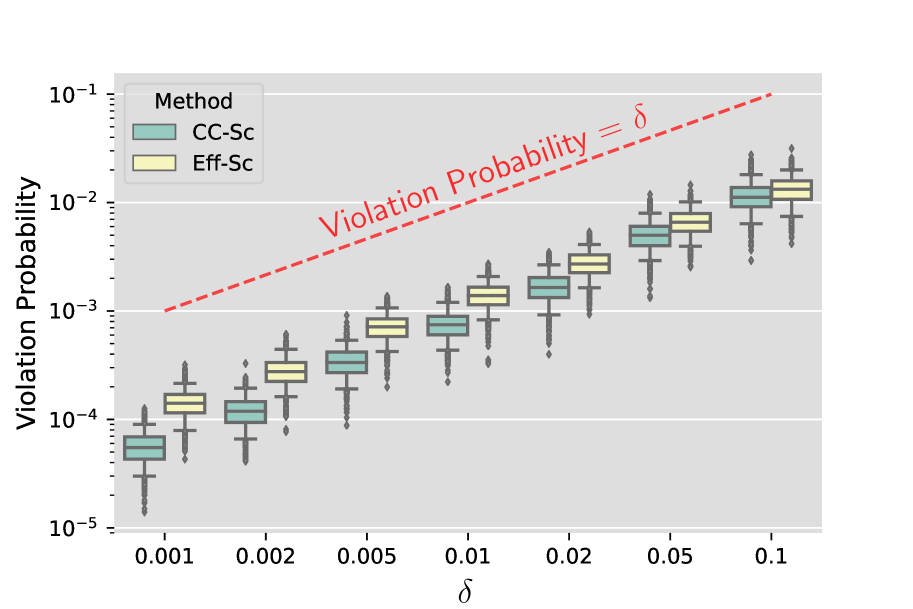

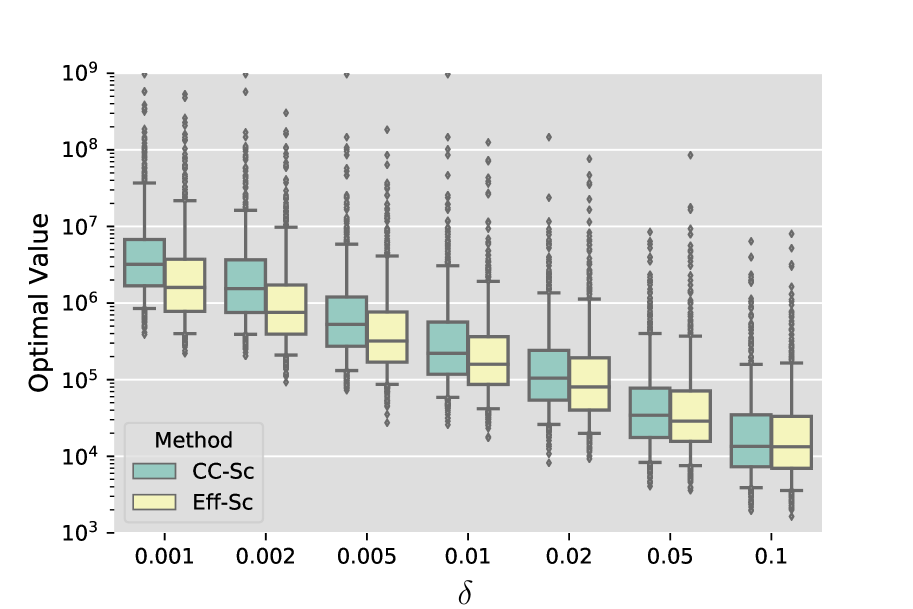

Finally, we compare Eff-Sc and CC-Sc for the optimal values of the sampled problems and the violation probabilities of the optimal solutions. Because both methods require generating random samples, the generated solutions are also random. Thus, the optimal values and the violation probabilities are also random. To compare the distributions of the random quantities, we conduct independent experiments. In each experiment, we execute both algorithms and get two solutions, then we evaluate the solutions’ violation probabilities using samples of . We employ boxplots (See McGill et al. (1978)) to depict the samples’ distribution through their quantiles. A boxplot is constructed of two parts, a box and a set of whiskers. The box is drawn from the quantile to the quantile, with a horizontal line drawn in the middle to denote the median. Two whiskers indicate and quantiles, respectively, and the scatters represent all the rest sample points beyond the whiskers.

In Figure 3, we present (a) the optimal values; and (b) the violation probabilities. One can quickly remark from Figure 3(a) that the optimal value of Eff-Sc is stochastically larger than the optimal value of CC-Sc, while Figure 3(b) indicates that the optimal solutions produced by both methods are feasible for all the experiments. Overall, with both methods successfully and conservatively approximating the probabilistic constraint, Eff-Sc is more computationally efficient and less conservative, producing solutions with better objective values than its counterpart.

7.2. Minimal Salvage Fund

In this section we conduct a numerical experiment for the minimal salvage fund problem (15). In the experiment we pick to test the performance of the problem in different dimensions.

For each fixed , the parameters of the problem (15) are chosen as follows:

-

•

where if and otherwise .

-

•

where for each .

-

•

are i.i.d. with Pareto cumulative distribution function , for .

Recall the explicit expressions for sets and from Proposition 9. To solve the conditional sampled problem (), it remains to sample and compute , the required number of samples. When is small, When , solving the optimization problem () costs much more time than simulating , despite that a simple acceptance rejection scheme is applied to sample in our experiments. We fix the confidence level parameter and set , then we can compute by the first part of Lemma 1.

Similar to Figure 2 of the portfolio optimization problem, we compare the efficiency between Eff-Sc and CC-Sc for different and in Figure 4, in terms of (a) the required number of samples; and (b) the CPU time for solving the sampled approximation problem. We observe that the Eff-Sc has uniformly smaller sample complexity and computational complexity than CC-Sc, where the superiority becomes significant for small . In particular, the required number of samples and the used CPU time are bounded for Eff-Sc, while they quickly deteriorate for CC-Sc when becomes smaller. It is also worth noting that Eff-Sc is consistently more efficient than CC-Sc for all the tested dimensions.

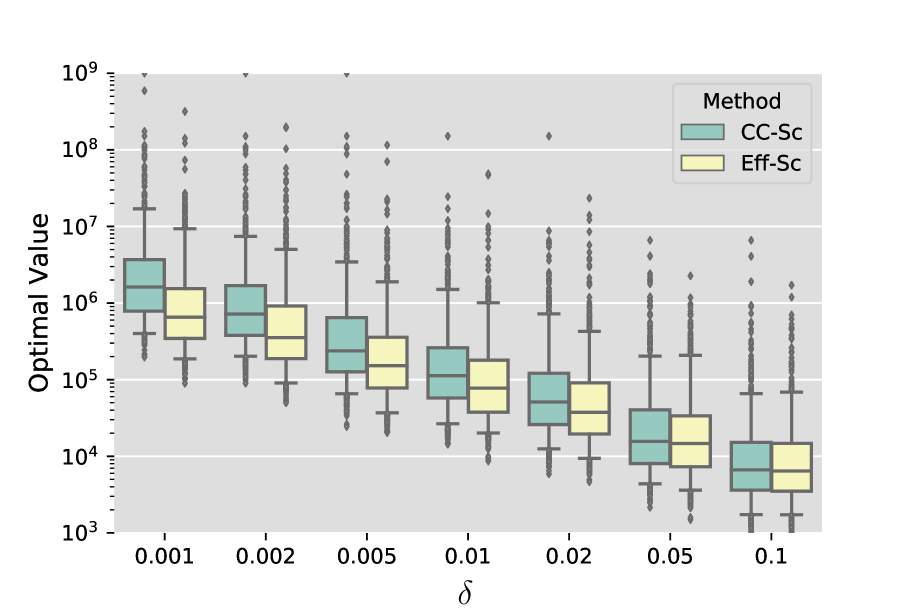

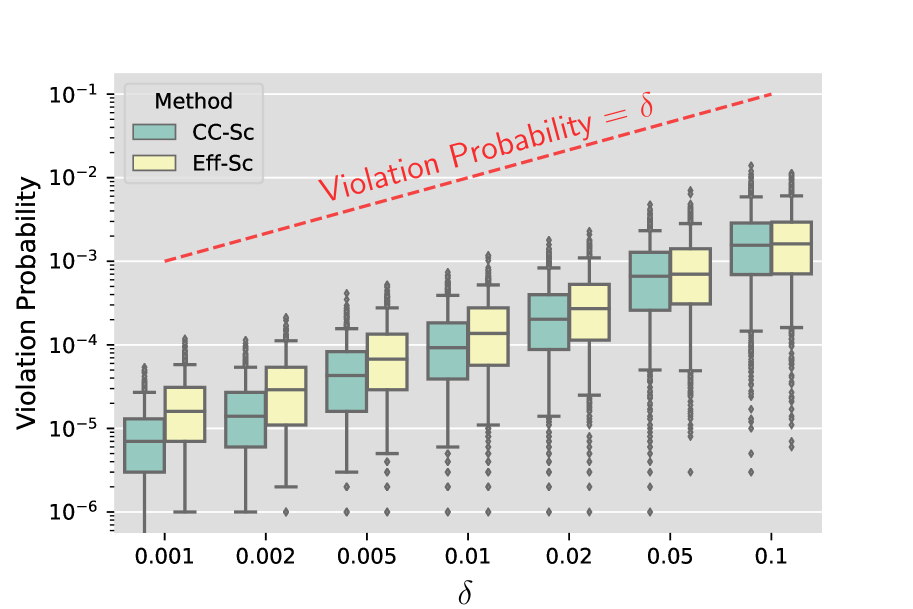

Finally, we compare optimal values of the sampled problems and violation probabilities of the optimal solutions in Figure 5. We present in (5(a)) the optimal values; and (5(b)) the violation probabilities, with fixed dimension (We provide additional results for and in Appendix B.1). One can quickly remark from Figure 5(a) that the optimal value of Eff-Sc is stochastically smaller than the optimal value of CC-Sc, while Figure 5(b) indicates that the optimal solutions produced by both methods are feasible for all the experiments. Therefore, we are able to draw the same conclusion as we have from the portfolio optimization experiment: Eff-Sc efficiently produces less conservative solutions.

Acknowledgement

The authors are grateful to Alexander Shapiro for helpful comments. The research of Bert Zwart is supported by NWO grant 639.033.413. The research of Jose Blanchet is supported by the Air Force Office of Scientific Research under award number FA9550-20-1-0397, NSF grants 1915967, 2118199, 1820942, 1838576, DARPA award N660011824028, and China Merchants Bank.

References

- Ahmed and Shapiro (2008) Ahmed S, Shapiro A (2008) Solving chance-constrained stochastic programs via sampling and integer programming. State-of-the-Art Decision-Making Tools in the Information-Intensive Age, 261–269 (INFORMS).

- Alsenwi et al. (2019) Alsenwi M, Pandey SR, Tun YK, Kim KT, Hong CS (2019) A chance constrained based formulation for dynamic multiplexing of embb-urllc traffics in 5g new radio. 2019 International Conference on Information Networking (ICOIN), 108–113 (IEEE).

- Andrieu et al. (2010) Andrieu L, Henrion R, Römisch W (2010) A model for dynamic chance constraints in hydro power reservoir management. European Journal of Operational Research 207(2):579–589.

- Barrera et al. (2016) Barrera J, Homem-de Mello T, Moreno E, Pagnoncelli BK, Canessa G (2016) Chance-constrained problems and rare events: an importance sampling approach. Mathematical Programming 157(1):153–189.

- Ben-Tal and Nemirovski (2000) Ben-Tal A, Nemirovski A (2000) Robust solutions of linear programming problems contaminated with uncertain data. Mathematical programming 88(3):411–424.

- Ben-Tal and Nemirovski (2002) Ben-Tal A, Nemirovski A (2002) Robust optimization–methodology and applications. Mathematical programming 92(3):453–480.

- Bertsimas and Sim (2004) Bertsimas D, Sim M (2004) The price of robustness. Operations research 52(1):35–53.

- Blanchet and Liu (2010) Blanchet J, Liu J (2010) Efficient importance sampling in ruin problems for multidimensional regularly varying random walks. Journal of Applied Probability 47(2):301–322.

- Bonami and Lejeune (2009) Bonami P, Lejeune MA (2009) An exact solution approach for portfolio optimization problems under stochastic and integer constraints. Operations Research 57(3):650–670.

- Boyd and Vandenberghe (2004) Boyd S, Vandenberghe L (2004) Convex optimization (Cambridge university press).

- Calafiore and Campi (2005) Calafiore G, Campi MC (2005) Uncertain convex programs: randomized solutions and confidence levels. Mathematical Programming 102(1):25–46.

- Calafiore and Campi (2006) Calafiore G, Campi MC (2006) The scenario approach to robust control design. IEEE Transactions on Automatic Control 51(5):742–753.

- Charnes et al. (1958) Charnes A, Cooper WW, Symonds GH (1958) Cost horizons and certainty equivalents: an approach to stochastic programming of heating oil. Management Science 4(3):235–263.

- Chen et al. (2019) Chen B, Blanchet J, Rhee CH, Zwart B (2019) Efficient rare-event simulation for multiple jump events in regularly varying random walks and compound poisson processes. Mathematics of Operations Research 44(3):919–942.

- Chen et al. (2010) Chen W, Sim M, Sun J, Teo CP (2010) From cvar to uncertainty set: Implications in joint chance-constrained optimization. Operations research 58(2):470–485.

- Diamond and Boyd (2016) Diamond S, Boyd S (2016) CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research 17(83):1–5.

- Eisenberg and Noe (2001) Eisenberg L, Noe TH (2001) Systemic risk in financial systems. Management Science 47(2):236–249.

- Embrechts et al. (2013) Embrechts P, Klüppelberg C, Mikosch T (2013) Modelling extremal events: for insurance and finance, volume 33 (Springer Science & Business Media).

- Frank (2008) Frank B (2008) Municipal bond fairness act. 110th Congress, 2d Session, House of Representatives, Report, 110–835.

- Gudmundsson and Hult (2014) Gudmundsson T, Hult H (2014) Markov chain monte carlo for computing rare-event probabilities for a heavy-tailed random walk. Journal of Applied Probability 51(2):359–376.

- Hillier (1967) Hillier FS (1967) Chance-constrained programming with 0-1 or bounded continuous decision variables. Management Science 14(1):34–57.

- Hong et al. (2020) Hong LJ, Huang Z, Lam H (2020) Learning-based robust optimization: Procedures and statistical guarantees. Management Science .

- Hong et al. (2011) Hong LJ, Yang Y, Zhang L (2011) Sequential convex approximations to joint chance constrained programs: A monte carlo approach. Operations Research 59(3):617–630.

- Kley et al. (2016) Kley O, Klüppelberg C, Reinert G (2016) Risk in a large claims insurance market with bipartite graph structure. Operations Research 64(5):1159–1176.

- Küçükyavuz (2012) Küçükyavuz S (2012) On mixing sets arising in chance-constrained programming. Mathematical programming 132(1-2):31–56.

- Lagoa et al. (2005) Lagoa CM, Li X, Sznaier M (2005) Probabilistically constrained linear programs and risk-adjusted controller design. SIAM Journal on Optimization 15(3):938–951.

- Lejeune and Margot (2016) Lejeune MA, Margot F (2016) Solving chance-constrained optimization problems with stochastic quadratic inequalities. Operations Research 64(4):939–957.

- Luedtke (2014) Luedtke J (2014) A branch-and-cut decomposition algorithm for solving chance-constrained mathematical programs with finite support. Mathematical Programming 146(1-2):219–244.

- Luedtke and Ahmed (2008) Luedtke J, Ahmed S (2008) A sample approximation approach for optimization with probabilistic constraints. SIAM Journal on Optimization 19(2):674–699.

- Luedtke et al. (2010) Luedtke J, Ahmed S, Nemhauser GL (2010) An integer programming approach for linear programs with probabilistic constraints. Mathematical Programming 122(2):247–272.

- McGill et al. (1978) McGill R, Tukey JW, Larsen WA (1978) Variations of box plots. The American Statistician 32(1):12–16.

- MOSEK ApS (2020) MOSEK ApS (2020) MOSEK Fusion API for Python. URL https://docs.mosek.com/9.2/pythonfusion.pdf.

- Nemirovski and Shapiro (2006a) Nemirovski A, Shapiro A (2006a) Convex approximations of chance constrained programs. SIAM Journal on Optimization 17(4):969–996.

- Nemirovski and Shapiro (2006b) Nemirovski A, Shapiro A (2006b) Scenario approximations of chance constraints. Probabilistic and Randomized Methods for Design under Uncertainty, 3–47 (Springer).

- Peña-Ordieres et al. (2020) Peña-Ordieres A, Luedtke JR, Wächter A (2020) Solving chance-constrained problems via a smooth sample-based nonlinear approximation. SIAM Journal on Optimization 30(3):2221–2250.

- Prekopa (1970) Prekopa A (1970) On probabilistic constrained programming. Proceedings of the Princeton Symposium on Mathematical Programming, volume 113, 138 (Princeton, NJ).

- Prékopa (2003) Prékopa A (2003) Probabilistic programming. Handbooks in Operations Research and Management Science 10:267–351.

- Resnick (2013) Resnick SI (2013) Extreme values, regular variation and point processes (Springer).

- Seppälä (1971) Seppälä Y (1971) Constructing sets of uniformly tighter linear approximations for a chance constraint. Management Science 17(11):736–749.

- Tong et al. (2020) Tong S, Subramanyam A, Rao V (2020) Optimization under rare chance constraints. arXiv preprint arXiv:2011.06052 .

- Wierman and Zwart (2012) Wierman A, Zwart B (2012) Is tail-optimal scheduling possible? Operations Research 60(5):1249–1257.

- Zhang et al. (2014) Zhang M, Küçükyavuz S, Goel S (2014) A branch-and-cut method for dynamic decision making under joint chance constraints. Management Science 60(5):1317–1333.

Appendix A Proofs of Technical Results

A.1. Proofs for Section 5

Proof of Lemma 2.

We will derive an expression of to ensure that for small enough. Because of Assumption 2, for any there exist some small enough such that . Therefore, it suffices to prove that and are disjoint. In other words,

| (42) |

Let be a positive number such that . Pick the set in (35b) as a compact set such that . It follows from the inequality (35b) that there exist a constant such that

| (43) |

Therefore, for any we have,

| (44) | ||||

Recall that is regularly varying from Assumption 1,

Therefore, there exist a number such that

| (45) |

Note that the right hand side of (45) is nondecreasing in . Thus, if for any there exist satisfying

| (46) |

Substituting (46) into (44), we have

Moreover, Assumption 2 guarantees the existence of such that

Consequently (42) is proved with . ∎

Proof of Theorem 3.

We construct the uniform conditional event that contains all the for . Due to the definition (35) and , there exist such that for all ,

| (47) |

Notice that for any , there exist an such that . Consequently, it follows from (47) that

Applying Assumption 3 yields that

Recall that is a ball in (thus ) and that from Assumption 3, it turns out that . Consequently, whenever for some , we either have implying , or we have . Summarizing these two scenarios,

Thus, we define the conditional set as

It remains to analyze the probability of the uniform conditional event . As is multivariate regularly varying,

Recalling, and invoking Property 2, we get

Hence, the proof is complete. ∎

Proof of Theorem 4.

Using Lemma 1, we immediately have it remains to show that there exist such that .

For simplicity, in the proof we will use as a shorthand for , the random variable with conditional distribution of given . By a scaling of by a factor in (), we have an equivalent optimization problem

| (51) |

where are i.i.d. samples from . Notice that .

For any compact set , since is multivariate regularly varying,

Thus . As the limiting measure is a probability measure, the family is tight and consequently follows directly from the vague convergence, see Resnick (2013). Consequently, since all the samples are i.i.d, we also have

Now we define a family of deterministic optimization problem, denoted by (), which is parameterized by as follows,

| () |

Then, there exist a compact set such that:

- (1)

-

(2)

for all ;

For every and , due to the Slater’s condition, there exist a feasible solution such that . Since is continuous in , there exist an open neighborhood around such that . Notice that such feasible solution and neighborhood exist for every . There exists a finite open cover of due to its compactness. Let be the corresponding feasible solutions to the open cover . Due to Assumption 5, there exist such that for all , we have

| (55) |

Therefore by the triangle inequality, it follows that if ,

Consequently, is a feasible solution for optimization problem (51) if , which further implies that . As a result, we have

Note that . Therefore, let

It follows that

The statement is concluded by using the union bound, combining the lower bound together with the upper bound implied by Theorems 1 and 3, hence obtaining factor . ∎

Proof of Lemma 5..

Without loss of generality, assume that is an integer such that

Let , and let be the integer lattice points in . In addition, let , and for , then define . Since the function is convex, we can invoke the supporting hyperplane theorem to deduce that for , and consequently . In addition, since at the boundary of the cube , there exist a constant such that for and for , for all . Therefore, with being the maximum of the aforementioned linear functions, we have , and we also have that implies .

Define . We can conclude the property of as follows: (1) is a piecewise linear function of form , where ; (2) ; (3) implies . To complete the proof, it remains to verify for the second statement of Assumption 6.

As implies , it suffices to prove that there exist some universal constant such that for all . For an arbitrary point , there exist a lattice point such that Next, since is twice continuously differentiable, the gradient is Lipschitz over with Lipschitz constant denoted by . Therefore, for any ,

The proof is now complete. ∎

Proof of Theorem 6..

Since , the probability constraint implies that , which further implies for . Therefore, we have for , which implies .

Then, consider and . It follows from the second statement of Assumption 6 that implies that . Thus, there exist an index such that . As implies that , so

Therefore, the condition set can be constructed as

Thus, as the distribution is regularly varying in dimension one for each , we have , completing the proof. ∎

A.2. Proofs for Section 6

Proof of Proposition 7.

Let and . The level set is . Let and , it follows that . In view of the inequalities and when , we choose the asymptotic uniform bounds as

Furthermore, by definition we construct two approximation sets as

With all the elements that we have already defined, Assumption 1 follows directly from the assumption on distribution of . Now we turn to verify Assumption 2. As due to the definition of , it suffices to prove that . In view of , we have

Consequently, we have . Taking limit for , we conclude that .

As Assumption 1 and 2 are both satisfied, and we also have , thus Property 2 is verified due to Lemma 2. In addition, if , we have is bounded away from the origin. Thus Assumption 3 is verified with .

Finally, we provide closed form expressions for and . Define , then it follows that , and By setting , we get the expression in the statement of the theorem. ∎

Proof of Lemma 8.

We start by showing some properties of . Since is a non-negative matrix and the row sum is less than 1, it is a sub-stochastic matrix and all of its eigenvalues must be less than 1 in magnitude. This further implies: (1) is invertible; and (2) is a non-negative matrix with strictly positive diagonal terms.

Notice that is the unique vector such that . Let be the optimal solution of

We have , and we multiply the non-negative matrix on both side, yielding . Obviously, Let such that is a feasible solution to above problem. Obviously, it follows from that , thus is also optimal, which completes the proof. ∎

Proof of Proposition 9.

Assumption 1 follows directly from the assumptions of the example. Now we turn to verify Assumption 6. Using Lemma 8, we define . Therefore, Assumption 6 is satisfied with , , , and . Plugging above values into the expressions of and given in Theorem 6, we get the expressions shown in the statement of the proposition. ∎

The following lemma is used in the proof of Proposition 10.

Lemma 11.

There exist sets with positive Lebesgue measure such that for any with , there exist some .

Proof of Lemma 11..

Let denote the unit vector on the th coordinate in for . Fix with , define be the angle between and , which satisfies . Since we have , so there exist some such that , thus . Then, define

we have either or . Thus the proof is complete. ∎

Proof of Proposition 10..

For the first statement, since and , and invoking the assumption that has a positive density,

For the second statement, Assumption 1 is easy to verify. Notice that for all , so we pick the scaling rate function as and . Let denote the maximal eigenvalue of , and denote the minimal eigenvalue of . The rest of the proof will be divided into two cases.

Case 1 (): We pick the level set as . Since , Assumption 2 is verified. Next, we directly show Property 2 instead of using Lemma 2. For any we have

Thus, can be chosen such that , and . As a result, Property 2 is verified. We next turn to derive the asymptotic uniform bound . Observing that

we define . Assumption 3 now follows from the definition of .

Appendix B Additional Numerical Results

B.1. Additional Results for Minimal Salvage Fund

In this section we presents additional numerical experiments that demonstrates the quality of the solutions produced by Eff-Sc is better than the solutions produced by CC-Sc. See Figure 6 for dimension and Figure 7 for .