Dynamic Causal Effects Evaluation in A/B Testing with a Reinforcement Learning Framework

Abstract

A/B testing, or online experiment is a standard business strategy to compare a new product with an old one in pharmaceutical, technological, and traditional industries. Major challenges arise in online experiments of two-sided marketplace platforms (e.g., Uber) where there is only one unit that receives a sequence of treatments over time. In those experiments, the treatment at a given time impacts current outcome as well as future outcomes. The aim of this paper is to introduce a reinforcement learning framework for carrying A/B testing in these experiments, while characterizing the long-term treatment effects. Our proposed testing procedure allows for sequential monitoring and online updating. It is generally applicable to a variety of treatment designs in different industries. In addition, we systematically investigate the theoretical properties (e.g., size and power) of our testing procedure. Finally, we apply our framework to both simulated data and a real-world data example obtained from a technological company to illustrate its advantage over the current practice. A Python implementation of our test is available at https://github.com/callmespring/CausalRL.

Keywords: A/B testing; Online experiment; Reinforcement learning; Causal inference; Sequential testing; Online updating.

1 Introduction

A/B testing, or online experiment is a business strategy to compare a new product with an old one in pharmaceutical, technological, and traditional industries (e.g., google, Amazon, or Facebook). It has became the gold standard to make data-driven decisions on a new service, feature, or product. For example, in web analytics, it is common to compare two variants of the same webpage (denote by A and B) by randomly splitting visitors into A and B and then contrasting metrics of interest (e.g., click-through rate) on each of the splits. There is a growing literature on developing A/B testing methods (see e.g., Johari et al.,, 2015; Kharitonov et al.,, 2015; Johari et al.,, 2017; Yang et al.,, 2017, and the references therein). The key idea of these approaches is to apply causal inference methods to estimating the treatment effect of a new change under the assumption of the stable unit treatment value assumption (SUTVA, Rubin,, 1980). Please see e.g., Wager and Athey, (2018), Imbens and Rubin, (2015), Yao et al., (2020), Hernn and Robins, (2020) and the references therein. SUTVA precludes the existence of the interference effect such that the response of each subject in the experiment depends only on their own treatment and is independent of others’ treatments. Despite its ubiquitousness, however, the standard A/B testing is not directly applicable for causal inference under interference (Zhou et al.,, 2020).

In this paper, we focus on the setting where there is only one unit (or system) in the experiment that receives a sequence of treatments over time. In many applications, the treatment at a given time can impact future outcomes, leading SUTVA being invalid. These studies frequently occur in the two-sided markets (intermediary economic platforms having two distinct user groups that provide each other with network benefits) that involve sequential decision making over time. As an illustration, we consider evaluating the effects of different order dispatching strategies in ride-sharing companies (e.g., Uber) for large-scale fleet management. See our real data analysis in Section 5 for details. These companies form a typical two-sided market that enables efficient interactions between passengers and drivers (Rysman,, 2009). With the rapid development of smart mobile phones and internet of things, they have substantially transformed the transportation landscape of human beings (Frenken and Schor,, 2017; Jin et al.,, 2018; Hagiu and Wright,, 2019). Order dispatching is one of the most critical problems in online ride-sharing platforms to adapt the operation and management strategy to the dynamics in demand and supply. At a given time, an order dispatching strategy not only affects the platform’s immediate outcome (e.g., passengers’ answer time, drivers’ income), but also impacts the spatial distribution of drivers in the future. This in turn affects the platform’s future outcome. The no interference assumption is thus violated.

A fundamental question of interest that we consider here is how to develop valid A/B testing methods in the presence of interference. Solving this fundamental question faces at least three major challenges. (i) The first one lies in establishing causal relationship between treatments and outcomes over time, by taking the carryover effect into consideration. Most of the existing A/B testing methods are ineffective. They fail to identify the carryover effect, leading the subsequent inference being invalid. See Section 3.1 for details. (ii) The second one is that running each experiment takes a considerable time. The company wishes to terminate the experiment as early as possible in order to save both time and budget. As such, the testing hypothesis needs to be sequentially evaluated online as the data are being collected, and the experiment shall be stopped in accordance with a pre-defined stopping rule as soon as significant results are observed. (iii) The third one is that treatments are desired to be allocated in a manner to maximize the cumulative outcomes or to detect the alternative more efficiently. The testing procedure shall allow the treatment to be adaptively assigned. Addressing these challenges requires the development of new tools and theory for A/B testing and causal effects evaluation.

1.1 Contributions

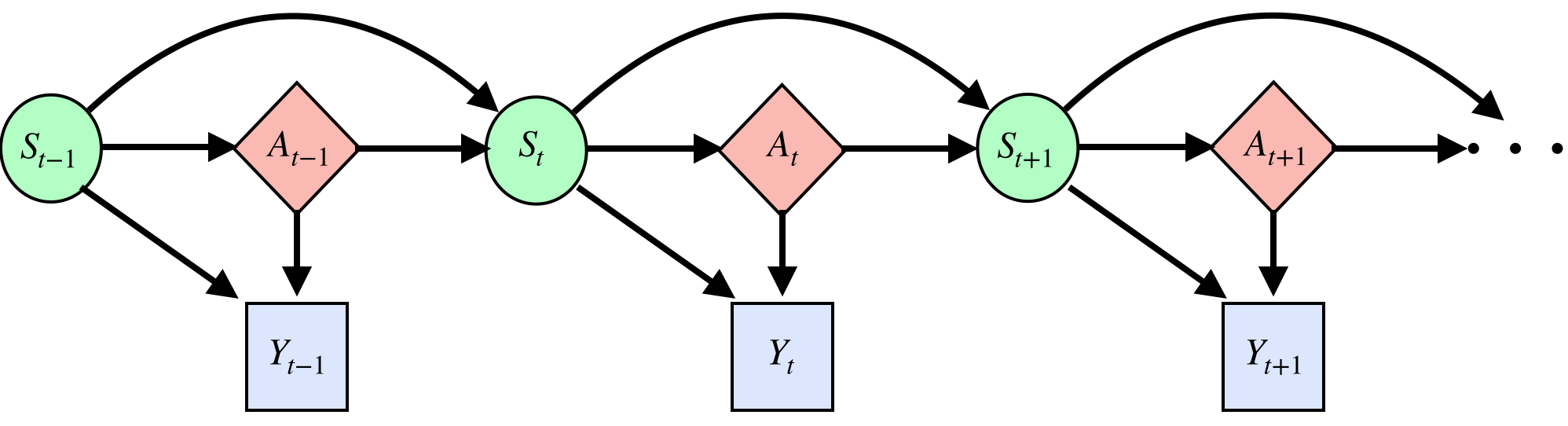

We summarize our contributions as follows. First, to address the challenge mentioned in (i), we introduce a reinforcement learning (RL, see e.g., Sutton and Barto,, 2018, for an overview) framework for A/B testing. RL is suitable framework to handle the carryover effects over time. In addition to the treatment-outcome pairs, it is assumed that there is a set of time-varying state confounding variables. We model the state-treatment-outcome triplet by using the Markov decision process (MDP, see e.g. Puterman,, 1994) to characterize the association between treatments and outcomes across time. Specifically, at each time point, the decision maker selects a treatment based on the observed state variables. The system responds by giving the decision maker a corresponding outcome and moving into a new state in the next time step. In this way, past treatments will have an indirect influence on future rewards through its effect on future state variables. See Figure 1 for an illustration. In addition, the long-term treatment effects can be characterized by the value functions (see Section 2.1 for details) that measure the discounted cumulative gain from a given initial state. Under this framework, it suffices to evaluate the difference between two value functions to compare different treatments. Our proposal gives an example of how to utilize some state-of-the-art machine learning tools, such as reinforcement learning, to address a challenging statistical inference problem for making business decisions.

Second, to address the challenges mentioned in (ii) and (iii), we propose a novel sequential testing procedure for detecting the difference between two value functions. Our proposed test integrates reinforcement learning and sequential analysis (see e.g. Jennison and Turnbull,, 1999, and the references therein) to allows for sequential monitoring and online updating111Our test statistic and its stopping boundary are updated as batches of new observations arrive without storing historical data.. Meanwhile, our proposal contributes to each of these two areas as well.

-

•

To the best of our knowledge, this is the first work on developing valid sequential tests in the RL framework. Our work is built upon the temporal-difference learning method based on function approximation (see e.g., Precup et al.,, 2001; Sutton et al.,, 2008). In the computer science literature, convergence guarantees of temporal difference learning have been derived by Sutton et al., (2008) under the setting of independent noise and by Bhandari et al., (2018) for Markovian noise. However, uncertainty quantification and asymptotic distribution of the resulting value function estimators have been less studied. Such results are critical for carrying out A/B testing. Recently, Luckett et al., (2020) outlined a procedure for estimating the value under a given policy. Shi et al., (2021) developed a confidence interval for the value function. However, these method do not allow for sequential monitoring or online updating.

-

•

Our proposal is built upon the -spending approach (Lan and DeMets,, 1983) for sequential testing. We note that most test statistics in classical sequential analysis have the canonical joint distribution (see Equation (3.1) in Jennison and Turnbull,, 1999) and their associated stopping boundary can be recursively updated via numerical integration. However, in our setup, test statistics no longer have the canonical joint distribution. This is due to the existence of the carryover effects in time. We discuss this in detail in Section 3.4. As such, the numerical integration approach is not applicable to our setting. To resolve this issue, we propose a bootstrap-assisted procedure to determine the stopping boundary. It is much more computationally efficient than the classical wild bootstrap algorithm (Wu et al.,, 1986, see Section 3.4 for details). The resulting test is generally applicable to a variety of treatment designs, including the Markov design, the alternating-time-interval design and the adaptive design (see Section 3.3 for details).

Third, we systematically investigate the asymptotic properties of our testing procedure. We show that our test not only maintains the nominal type I error rate, but also has non-negligible powers against local alternatives. In particular, we show that when the sieve method is used for function approximation in temporal difference learning, undersmoothing is not needed to guarantee that the resulting value estimator has a tractable limiting distribution. This occurs because sieve estimators of conditional expectations are idempotent (Newey et al.,, 1998). It implies that the proposed test will not be overly sensitive to the choice of the number of basis functions. To our knowledge, these results have not been established in the existing RL framework. Please see Section 3.3 for details.

Finally, our proposal addresses an important practical question in ride-sharing companies. In particular, the proposed methodology allows the company to evaluate different policies more accurately in the presence of the carryover effects. It also allows the company to terminate the online experiment earlier and to evaluate more policies within the same time frame. These policies have the potential to improve drivers’ salary and meet more customer requests, providing a more efficient transportation network. Please see Section 5 for details.

1.2 Related work

There is a huge literature on RL in the computer science community such that various algorithms are proposed for an agent to learn an optimal policy and interact with an environment. Recently, a few methods have been developed in the statistics literature on learning the optimal policy in mobile health applications (Ertefaie,, 2014; Luckett et al.,, 2020; Hu et al.,, 2020; Liao et al.,, 2020). In addition, there is a growing literature on adapting reinforcement learning to develop dynamic treatment regimes in precision medicine, to recommend treatment decisions based on individual patients’ information (Murphy,, 2003; Chakraborty et al.,, 2010; Qian and Murphy,, 2011; Zhao et al.,, 2012; Zhang et al.,, 2013; Song et al.,, 2015; Zhao et al.,, 2015; Zhang et al.,, 2015, 2018; Zhu et al.,, 2017; Wang et al.,, 2018; Shi et al., 2018a, ; Shi et al., 2018b, ; Mo et al.,, 2020; Meng et al.,, 2020).

Our work is closely related to the literature on off-policy evaluation, whose objective is to estimate the value of a new policy based on data collected by a different policy. Existing literature can be cast into model-based methods, importance sampling (IS)-based and doubly-robust procedures. Model-based methods first fit an MDP model from data and then compute the resulting value function. The estimated value function might suffer from a large bias due to potential misspecification of the model. Popular IS based methods include Thomas et al., (2015); Thomas and Brunskill, (2016); Liu et al., (2018). These methods re-weight the observed rewards with the density ratio of the target and behavior policies. The value estimate might suffer from a large variance, due to the use of importance sampling. Doubly-robust methods (see, e.g., Jiang and Li,, 2016; Kallus and Uehara,, 2019) learn the Q-function as well as the probability density ratio and combine these estimates properly for more robust and efficient value evaluation. However, both IS and doubly-robust methods required the treatment assignment probability (propensity score) to be bounded away from 0 and 1. As such, they are inapplicable to the alternating-time-interval design, which is the treatment allocation strategy in our real data application (see Section 5 for details).

In addition to the literature on RL, our work is also related to a line of research on causal inference with interference. Most of the works studied the interference effect across different subjects (see e.g., Hudgens and Halloran,, 2008; Pouget-Abadie et al.,, 2019; Li et al.,, 2019; Zhou et al.,, 2020; Reich et al.,, 2020). That is, the outcome for one subject depends on the treatment assigned to other subjects as well. To the contrary, our work focuses on the interference effect over time. We also remark that most of the aforementioned methods were primarily motivated by research questions in psychological, environmental and epidemiological studies, so their generalization to infer time dependent causal effects in two-sided markets remains unknown.

Finally, we remark that there is a growing literature on evaluating time-varying causal effects (see e.g. Robins,, 1986; Sobel and Lindquist,, 2014; Boruvka et al.,, 2018; Ning et al.,, 2019; Rambachan and Shephard,, 2019; Viviano and Bradic,, 2019; Bojinov and Shephard,, 2020). However, none of the above cited works used a RL framework to characterize the treatment effects. In particular, Bojinov and Shephard, (2020) proposed to use IS based methods to test the null hypothesis of no (average) temporal causal effects in time series experiments. Their causal estimand is different from ours since they focused on lag treatment effects, whereas we consider the long-term effects characterized by the value function. Moreover, their method requires the propensity score to be bounded away from 0 and 1, and thus it is not valid for our applications. In addition, these method do not allow for sequential monitoring.

1.3 Organization of the paper

The rest of the paper is organised as follows. In Section 2, we introduce a potential outcome framework to MDP and describe the causal estimand. Our testing procedure is introduced in Section 3. In Section 4, we demonstrate the effectiveness of our test via simulations. In Section 5, we apply the proposed test to a data from an online ride-hailing platform to illustrate its usefulness. Finally, we conclude our paper in Section 6.

2 Problem formulation

2.1 A potential outcome framework for MDP

For simplicity, we assume that there are only two treatments (actions, products), coded as 0 and 1, respectively. For any , let denote a treatment history vector up to time . Let denote the support of state variables and denote the initial state variable. We assume is a compact subset of . For any , let and be the counterfactual state and counterfactual outcome, respectively, that would occur at time had the agent followed the treatment history . The set of potential outcomes up to time is given by

Let be the set of all potential outcomes.

A deterministic policy is a time-homogeneous function that maps the space of state variables to the set of available actions. Following , the agent will assign actions according to at each time. We use and to denote the associated potential state and outcome that would occur at time had the agent followed . The goodness of a policy is measured by its (state) value function,

where is a discount factor that reflects the trade-off between immediate and future outcomes. The value function measures the discounted cumulative outcome that the agent would receive had they followed . Note that our definition of the value function is slightly different from those in the existing literature (see Sutton and Barto,, 2018, for example). Specifically, is defined through potential outcomes rather than the observed data.

Similarly, we define the Q function by

where denotes a time-varying policy where the initial action equals to and all other actions are assigned according to .

The goal of A/B testing is to compare the difference between the two treatments. Toward that end, we focus on two nondynamic (state-agnostic) policies that assign the same treatment at each time point. We remark that this is non-traditional in RL where the goal is to build a policy that depends on the state. In Section 6.1, we discuss the extension to testing two dynamic policies. For these two nondynamic policies, we use their value functions (denote by and ) to measure their long-term treatment effects. Meanwhile, our proposed method is equally applicable to the dynamic policy scenario as well. See Section 6 for details. To quantitatively compare the two policies, we introduce the Conditional Average Treatment Effect (CATE) and Average Treatment Effect (ATE) based on their value functions in the following definitions. These two definitions relate RL to causal inference.

Definition 1. Conditional on the initial state , CATE is defined by the difference between two value functions, i.e., .

Definition 2. For a given reference distribution function that has a bounded density function on , ATE is defined by the integrated difference between two value function, i.e.,

The focus of this paper is to test the following hypotheses:

When holds, the new product is no better than the old one on average and is not of practical interest.

2.2 Identifiability of ATE

One of the most important question in causal inference is the identifiability of causal effects. In this section, we present sufficient conditions that guarantee the identifiability of the value function.

We first introduce two conditions that are commonly assumed in multi-stage decision making problems (see e.g. Murphy,, 2003; Robins,, 2004; Zhang et al.,, 2013). We need to use the notation to indicate that and are independent conditional on . In practice, with the exception of , the set cannot be observed, whereas at time , we observe the state-action-outcome triplet . For any , let denote the observed treatment history.

(CA) Consistency assumption: and for all , almost surely.

(SRA) Sequential randomization assumption: .

The CA requires that the observed state and outcome correspond to the potential state and outcome whose treatments are assigned according to the observed treatment history. It generalizes SUTVA to our setting, allowing the potential outcomes to depend on past treatments. The SRA implies that there are no unmeasured confounders and it automatically holds in online randomized experiments, in which the treatment assignment mechanism is pre-specified. In SRA, we allows to depend on the observed data history and thus, the treatments can be adaptively chosen.

We next introduce two conditions that are unique to the reinforcement learning setting.

(MA) Markov assumption: there exists a Markov transition kernel such that for any , and , we have

(CMIA) Conditional mean independence assumption: there exists a function such that for any , we have .

We make a few remarks. First, these two conditions are central to the empirical validity of reinforcement learning (RL). Specifically, under these two conditions, one can show that there exists an optimal time-homogenous stationary policy whose value is no worse than any history-dependent policy (Puterman,, 1994). This observation forms the foundation of most of the existing state-of-the-art RL algorithms.

Second, when CA and SRA hold, it implies that the Markov assumption and the conditional mean independence assumption hold on the observed data as well,

| (1) | |||||

| (2) |

As such, corresponds to the transition function that defines the next state distribution conditional on the current state-action pair and corresponds to the conditional expectation of the immediate reward as a function of the state-action pair.

Assumption (1) is commonly assumed in the existing reinforcement learning literature (see e.g., Ertefaie,, 2014; Luckett et al.,, 2020). It is testable based on the observed data. See the goodness-of-fit test developed by Shi et al., 2020a . In practice, to ensure the Markov property is satisfied, we can construct the state by concatenating measurements over multiple decision points till the Markovian property is satisfied.

Assumption (2) implies that past treatments will affect future response only through its impact on the future state variables. In other words, the state variables shall be chosen to include those that serve as important mediators between past treatments and current outcomes. By Assumption (1), this assumption is automatically satisfied when is a deterministic function of that measures the system’s status at time . The latter condition is commonly imposed in the reinforcement learning literature and is stronger than (2).

To conclude this section, we derive a version of Bellman equation for the Q function under the potential outcome framework. Specifically, for , let denote the Q function where treatment is assigned at the initial decision point and treatment is repeatedly assigned afterwards. By definition, we have for any .

Lemma 1.

Under MA, CMIA, CA and SRA, for any , and any function , we have .

Lemma 1 implies that the Q-function is estimable from the observed data. Specifically, an estimating equation can be constructed based on Lemma 1 and the Q-function can be learned by solving this estimating equation. Note that and is completely determined by the value function . As a result, ATE is identifiable.

Note that the positivity assumption is not needed in Lemma 1. Our procedure can thus handle the case where treatments are deterministically assigned. This is due to MA and CMIA that assume the system dynamics are invariant across time. To elaborate this, note that the discounted value function is completely determined by the transition kernel and the reward function . These quantities can be consistently estimated under certain conditions, regardless of whether the treatments are deterministically assigned or not. Consequently, the value can be consistently estimated even when the treatment assignments are deterministic. We formally introduce our testing procedure in the next section.

3 Testing procedure

We first introduce a toy example to illustrate the limitations of existing A/B testing methods. We next present our method and prove its consistency under a variety of different treatment designs.

3.1 Toy examples

Existing A/B testing methods can only detect short-term treatment effects, but fail to identify any long-term effects. To elaborate this, we introduce two examples below.

Example 1. , for any and .

Example 2. , for any and .

In both examples, the random errors follow independent standard normal distributions and the parameter describes the degree of treatment effects. When , holds. Suppose . Then holds. In Example 1, the observations are independent and there are no carryover effects at all. In this case, both the existing A/B tests and the proposed test are able to discriminate from . In Example 2, however, treatments have delayed effects on the outcomes. Specifically, does not depend on , but is affected by through . Existing tests will fail to detect as the short-term conditional average treatment effects in this example. As an illustration, we conduct a small experiment by assuming the decision is made once at , and report the empirical rejection probability of the classical two-sample t-test that is commonly used in online experiments, a more complicated test based on the double machine learning method (DML, Chernozhukov et al.,, 2017) that is widely employed for inferring causal effects, and the proposed test. It can be seen the competing methods do not have any power under Example 2.

| Example 1 | Example 2 | ||||

|---|---|---|---|---|---|

| t-test 0.76 | DML-based test 1 | our test 0.98 | t-test 0.04 | DML-based test 0.06 | our test 0.73 |

3.2 An overview of the proposal

We present an overview of our proposal in this section. As commented before, we adopt a reinforcement learning framework to address the limitations of existing A/B testing methods and characterize the long-term treatment effects. First, we estimate based on a version of temporal difference learning. The idea is to apply basis function approximations to solve an estimating equation derived from Lemma 1. Specifically, let be a large linear approximation space for , where is a vector containing basis functions on . The dimension is allowed to grow with the number of samples to alleviate the effects of model misspecification. Let us suppose for a moment. Set the function in Lemma 1 to for , there exists some such that

where denotes the indicator function. The above equations can be rewritten as , where is a block diagonal matrix given by

Let and . It follows that . This motivates us to estimate by

ATE can thus be estimated by the plug-in estimator . We remark that there is no guarantee that is always invertible. However, its population limit, is invertible for any (see Lemma 3 in the supplementary article). Consequently, for sufficiently large , is invertible with large probability. In cases where is not invertible, we may add a ridge penalty to compute the resulting estimator. See Appendix D.4 of Shi et al., (2021) for details.

Second, we use to construct our test statistic at time . Let

| (4) |

It follows that . We will show that is multivariate normal. This implies that is asymptotically normal. Its variance can be consistently estimated by

as grows to infinity, where is the sandwich estimator for the variance of , and that

where is the temporal difference error whose conditional expectation given is zero asymptotically (see Lemma 1). This yields our test statistic , at time . For a given significance level , we reject when , where is the upper -th quantile of a standard normal distribution.

Third, we integrate the -spending approach with bootstrap to sequentially implement our test (see Section 3.4). The idea is to generate bootstrap samples that mimic the distribution of our test statistics, to specify the stopping boundary at each interim stage. Suppose that the interim analyses are conducted at time points . We focus on the setting where both and are pre-determined, as in our application (see Section 5 for details). To simplify the presentation, for each , we assume for some constants . To better understand our algorithm, we investigate the limiting distribution of our test statistics at these interim stages in the next section.

Finally, we remark that in the current setup, we assume the dimension of the state is fixed whereas the number of basis functions diverges to infinity at a rate that is slower than . In Appendix B.1, we extend our proposal to settings with high-dimensional state information. In that case, we recommend to include a rich class of basis functions to ensure that the Q-function can be well-approximated. The number of basis functions is allowed to be much larger than . To handle high-dimensionality, we first adopt the Dantzig selector (Candes et al.,, 2007) which directly penalizes the Bellman equation to compute an initial estimator. We next develop a decorrelated estimator to reduce the bias of the initial estimator and outline the corresponding testing statistic. We also remark that for simplicity, we use the same Q-function model at each interim stage. This works when are of the same order of magnitude, which is the case in our real data application where . Alternatively, one could allow to grow with . The testing procedure can be similarly derived.

3.3 Asymptotic properties under different treatment designs

We consider three treatment allocation designs that can be handled by our procedure as follows:

D1. Markov design: for some function uniformly bounded away from and .

D2. Alternating-time-interval design: , for all .

D3. Adaptive design: For for some , for some that depends on and is uniformly bounded away from and almost surely. We set .

Here, D2 is a deterministic design and is widely used in industry (see our real data example and this technical report222https://eng.lyft.com/experimentation-in-a-ridesharing-marketplace-b39db027a66e). D1 and D3 are random designs. D1 is commonly assumed in the literature on reinforcement learning (Sutton and Barto,, 2018). D3 is widely employed in the contextual bandit setting to balance the trade-off between exploration and exploitation. These three settings cover a variety of scenarios in practice.

In D3, we require to be strictly bounded between 0 and 1. Suppose an -greedy policy is used, i.e. , where denotes some estimated optimal policy. It follows that for any . Such a requirement is automatically satisfied. Meanwhile, other adaptive strategies are equally applicable (see e.g., Zhang et al.,, 2007; Hu et al.,, 2015; Metelkina et al.,, 2017).

For any behaviour policy in D1-D3, define and as the potential outcomes at time , where denotes the action history assigned according to . When is a random policy as in D1 or D3, definitions of these potential outcomes are more complicated than those under a deterministic policy (see Appendix C for details). When is a stationary policy, it follows from MA that forms a time-homogeneous Markov chain. When follows the alternating-time-interval design, both and form time-homogeneous Markov chains.

To study the asymptotic properties of our test, we need to introduce assumptions C1-C3 and move them and their corresponding detailed discussions to Appendix D. In C1, we require the above mentioned Markov chains to be geometrically ergodic. Geometric ergodicity is weaker than the uniform ergodicity condition imposed in the existing reinforcement learning literature (see e.g. Bhandari et al.,, 2018; Zou et al.,, 2019). In C2, we impose conditions on the set of basis functions such that is chosen to yield a good approximation for the Q function. It is worth mentioning that we only require the approximation error to decay at a rate of instead of . In other words, “undersmoothing” is not required and the value estimator has a well-tabulated limiting distribution even when the bias of the Q-estimator decays at a rate that is slower than . This result has a number of importation implications. First, it suggests the proposed test will not be overly sensitive to the choice of the number of basis functions. Such a theoretical finding is consistent with our empirical observations in Section 4.3. Second, the number of basis functions could be potentially selected by minimizing the prediction loss of the Q-estimator via cross validation. We also present examples of basis functions that satisfy C2 in Appendix D.2. In C3, we impose some mild conditions on the action value temporal-difference error, requiring their variances to be non-degenerate.

Let denote the sequence of our test statistics, where . In the following, we study their joint asymptotic distributions. We also present an estimator of their covariance matrix that is consistent under all designs.

Theorem 1 (Limiting distributions).

Assume C1-C3, MA, CMIA, CA, and SRA hold. Assume all immediate rewards are uniformly bounded variables, the density function of is uniformly bounded on and satisfies . Then under either D1, D2 or D3, we have

-

•

are jointly asymptotically normal;

-

•

their asymptotic means are non-positive under ;

-

•

their covariance matrix can be consistently estimated by some , whose -th element equals

This theorem forms the basis of our sequential testing procedure, which we elaborate in the next section.

3.4 Sequential monitoring and online updating

To sequentially monitor our test, we need to specify the stopping boundary such that the experiment is terminated and is rejected when for some .

First, we use the spending function approach to guarantee the validity of our test. It requires to specify a monotonically increasing function that satisfies and . Some popular choices of the spending function include

| (6) |

where denotes the normal cumulative distribution function. Adopting the spending approach, we require ’s to satisfy

| (7) |

Suppose there exist a sequence of information levels such that

| (8) |

for all . Then the sequence satisfies the Markov property. The stopping boundary can be efficiently computed based on the numerical integration method detailed in Section 19.2 of Jennison and Turnbull, (1999). However, in our setup, condition (8) might not hold when adaptive design is used. As commented in the introduction, this is due to the existence of carryover effects in time. Specifically, when treatment effects are adaptively generated, the behavior policy at difference stages are likely to vary. Due to the carryover effects in time, the state vectors at difference stages have different distribution functions. As such, the asymptotic distribution of the test statistic at each interim stage depends on the behavior policy. Consequently, the covariance is a very complicated function of and (see e.g., the form of in Theorem 1) that can not be represented by (8). Consequently, the numerical integration method is not applicable.

Next, we outline a method based on the wild bootstrap (Wu et al.,, 1986). Then we discuss its limitation and present our proposal, a scalable bootstrap algorithm to determine the stopping boundary. The idea is to generate bootstrap samples that have asymptotically the same joint distribution as . By the requirement on in (7), we obtain

To implement the test, we thus recursively calculate the threshold as follows,

| (9) |

where denotes the probability conditional on the data, and reject when for some . In practice, the above conditional probability can be approximated via Monte carlo simulations. This forms the basis of the bootstrap algorithm.

Specifically, let be a sequence of i.i.d. mean-zero, unit variance random variables independent of the observed data. Define

| (12) |

where is the temporal difference error defined. Based on , one can define the bootstrap sample . Based on the definition of , it is immediate to see that each follows a standard normal distribution conditional on the data.

We remark that although the wild bootstrap method is developed under the i.i.d. settings, it is valid under our setup as well. This is due to that under CMIA, forms a martingale sequence with respect to the filtration . It guarantees that the covariance matrices of and are asymptotically equivalent. As such, the bootstrap approximation is valid.

However, calculating requires operations. The time complexity of the resulting bootstrap algorithm is up to the -th interim stage, where is the total number of bootstrap samples. This can be time consuming when are large. To facilitate the computation, we observe that in the calculation of , the random noise is generated upon the arrival of each observation. This is unnecessary as we aim to approximate the distribution of only at finitely many time points .

Finally, we present our bootstrap algorithm to determine , based on Theorem 1. Let be a sequence of i.i.d random vectors, where stands for a identity matrix for any . Let be a zero matrix. At the -th stage, we compute the bootstrap sample

A key observation is that, conditional on the observed dataset, the covariance of and equals

By Theorem 1, the covariance matrices of and are asymptotically equivalent. In addition, the limiting distributions of and are multivariate normal with zero means. As such, the joint distribution of can be well approximated by that of conditional on the data. The rejection boundary can thus be computed in a similar fashion as in (9).

Theorem 2 (Type-I error).

Suppose that the conditions of Theorem 1 hold and is continuous. Then the proposed thresholds satisfy , for all under . The equality holds when .

Theorem 2 implies that the type-I error rate of the proposed test is well controlled. When , the equality in Theorem 2 holds. The rejection probability achieves the nominal level under . We next investigate the power property of our test.

Theorem 3 (Power).

Suppose that the conditions of Theorem 2 hold. Assume , then . Assume for some . Then .

Combining Theorems 2 and 3 yields the consistency of our test. The second assertion in Theorem 3 implies that our test has non-negligible powers against local alternatives converging to at the rate. When the signal decays at a slower rate, the power of our test approaches 1.

Since we use a linear basis function to approximate the Q-function, the regression coefficients as well as their covariance estimator can be online updated as batches of observations arrive at the end of each interim stage. As such, our test can be implemented online. We summarize our procedure in Algorithm 1. Recall that is the number of basis functions. As the th interim stage, the time complexities of Steps 1-3 in Algorithm 1 are dominated by , and , respectively. As such, the time complexity of Algorithm 1 is dominated by . In contrast, one can show that the classical wild bootstrap algorithm would take at least number of flops and is much more computationally intensive when , which is case in phase 3 clinical trials and our real data application.

To conclude this section, we remark that a few bootstrap algorithms have been developed in the RL literature for policy evaluation. Specifically, Hanna et al., (2017) and Hao et al., (2021) proposed to use bootstrap for uncertainty quantification in off-policy evaluation. These algorithms require the number of trajectories to diverge to infinity to be consistent and are thus not applicable to our setting where there is only one trajectory in the experiment. In addition, they are developed in offline settings and do not allow online updating. Ramprasad et al., (2021) developed a bootstrap algorithm for policy evaluation in online settings. Their algorithm generates bootstrap samples upon the arrival of each observation and is thus more computationally intensive than the proposed algorithm.

4 Simulation study

4.1 Settings and implementation

Simulated data of states and rewards was generated as follows,

where the random errors are i.i.d and are i.i.d . Let denote the state at time . Under this model, treatments have delayed effects on the outcomes, as in Example 2. The parameter characterizes the degree of such carryover effects. When , and holds. When , holds. Moreover, increases as increases.

We set and . The discounted factor is set to and is chosen as the initial state distribution. We consider three behavior policies, according to the designs D1-D3, respectively. For the behavior policy in D1, we set for any . For the behavior policy in D3, we use an -greedy policy and set with , for any and .

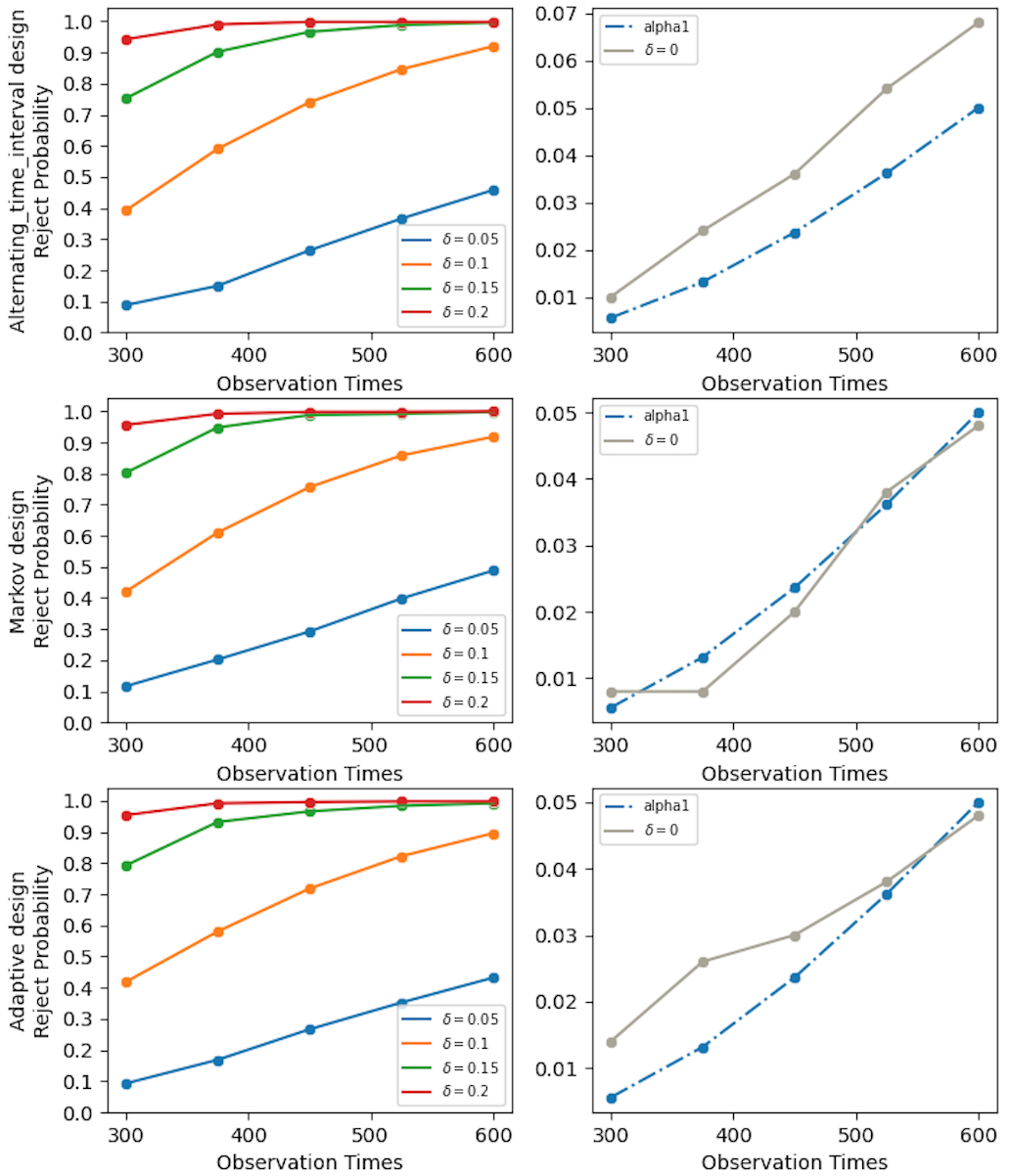

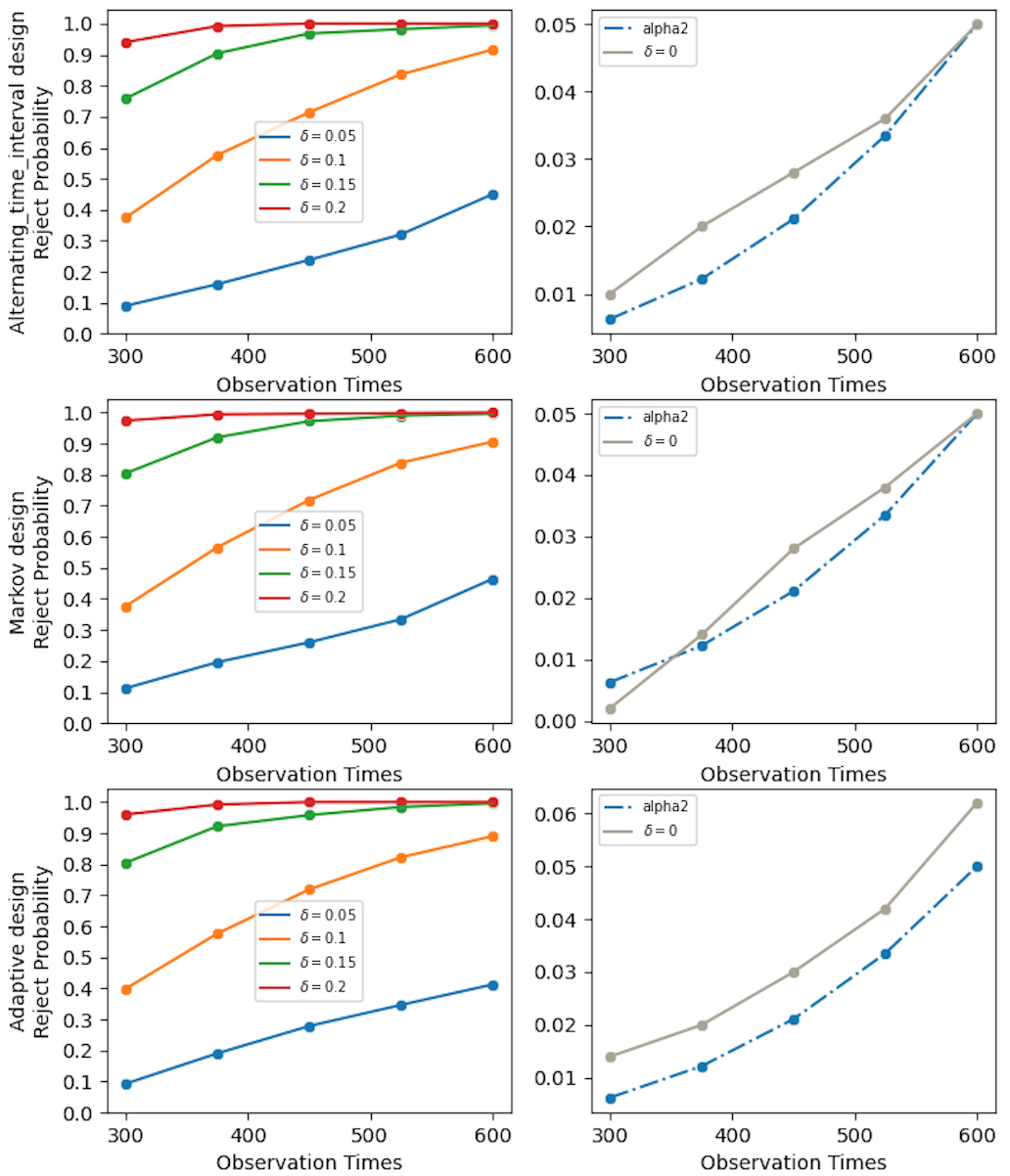

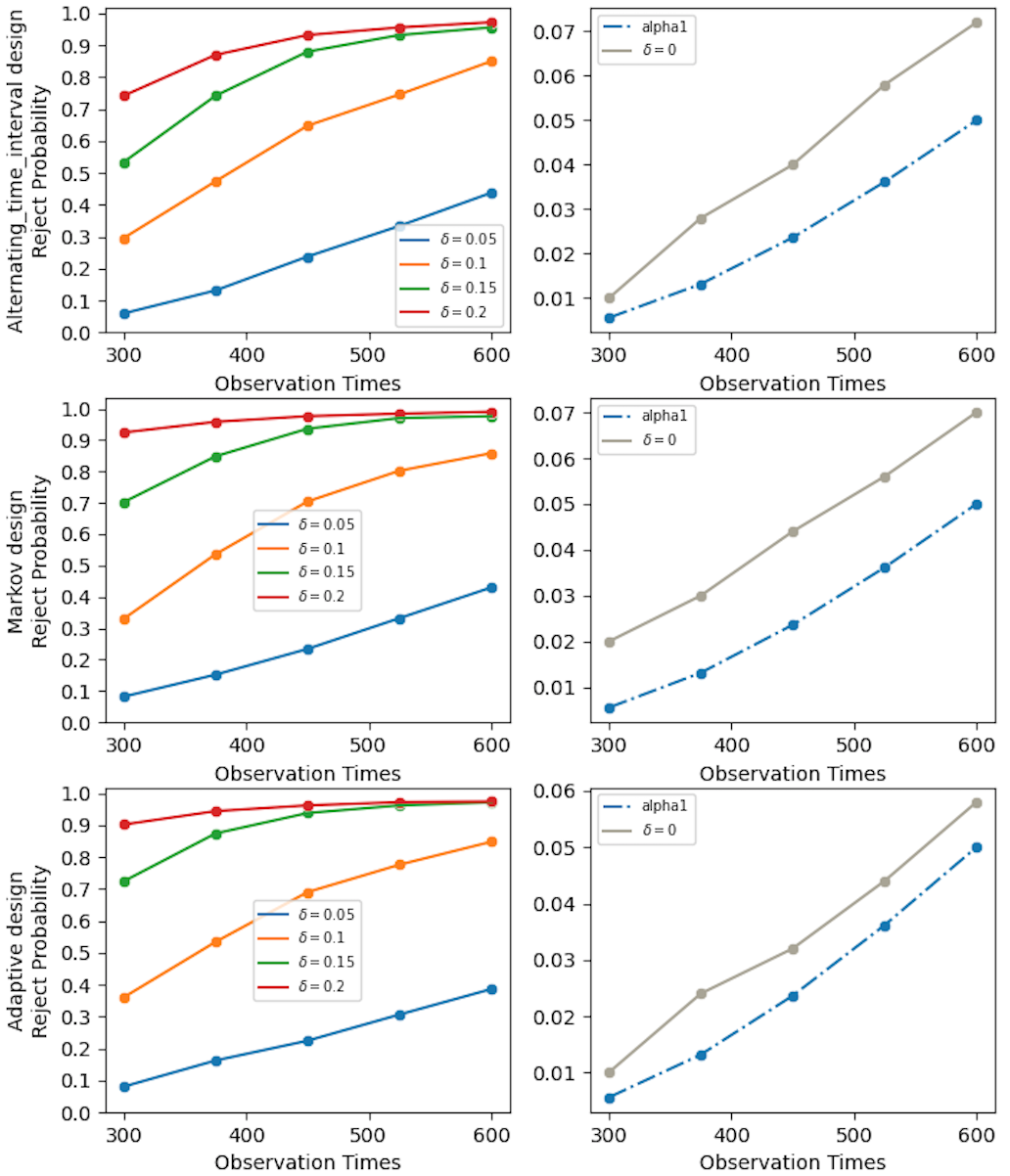

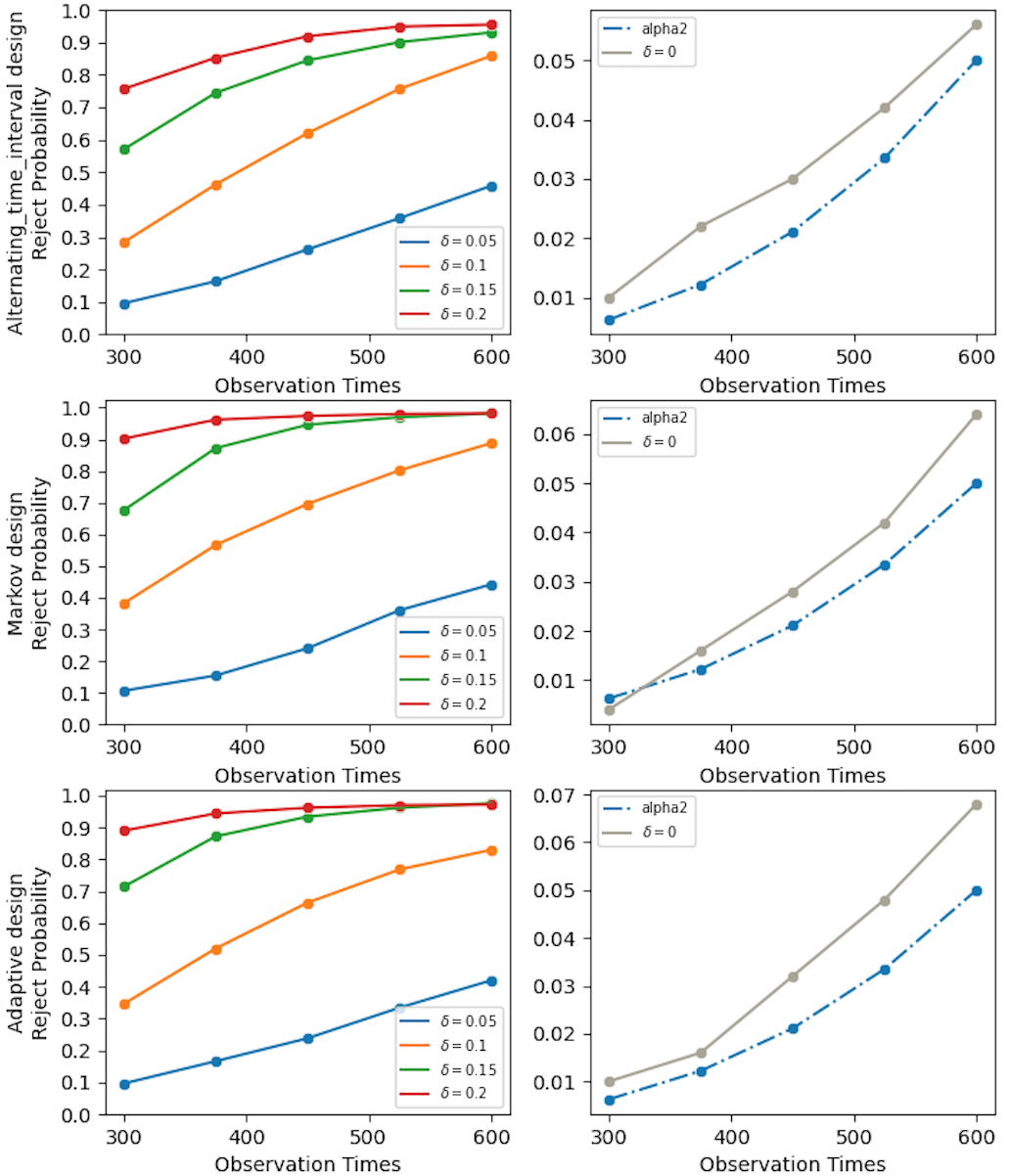

For each design, we further consider five choices of , corresponding to and . The significance level is set to in all cases. To implement our test, we choose two -spending functions, corresponding to and given in (6). The hyperparameter in is set to . The number of bootstrap sample is set to . In addition, we consider the following polynomial basis function, , with .

|

|

|

| (a) The proposed test under and | (b) Two-sample t-test under and | |

| (from left plots to right plots) | (from left plots to right plots) |

|

|

|

| (a) The proposed test under and | (b) Two-sample t-test under and | |

| (from left plots to right plots) | (from left plots to right plots) |

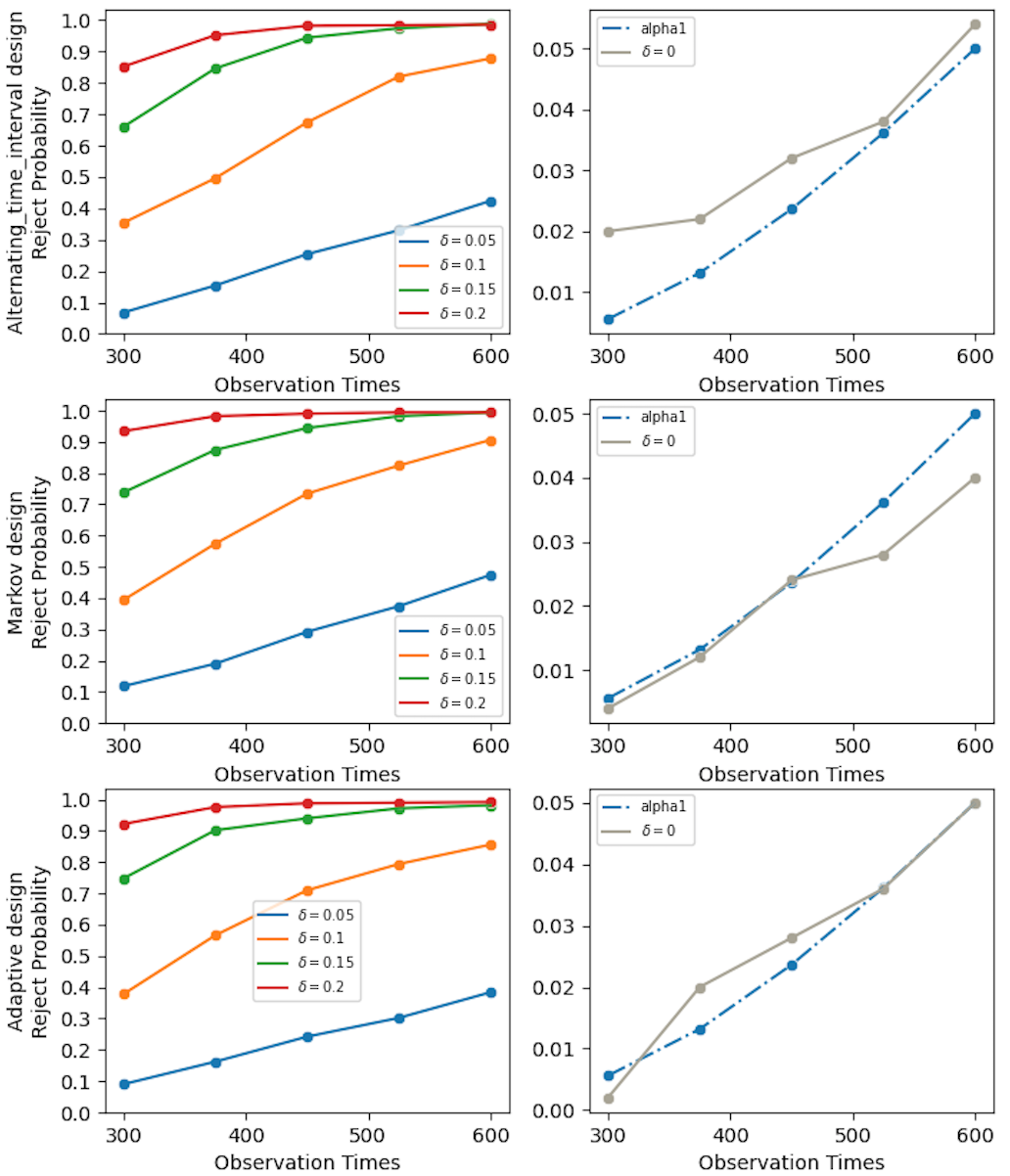

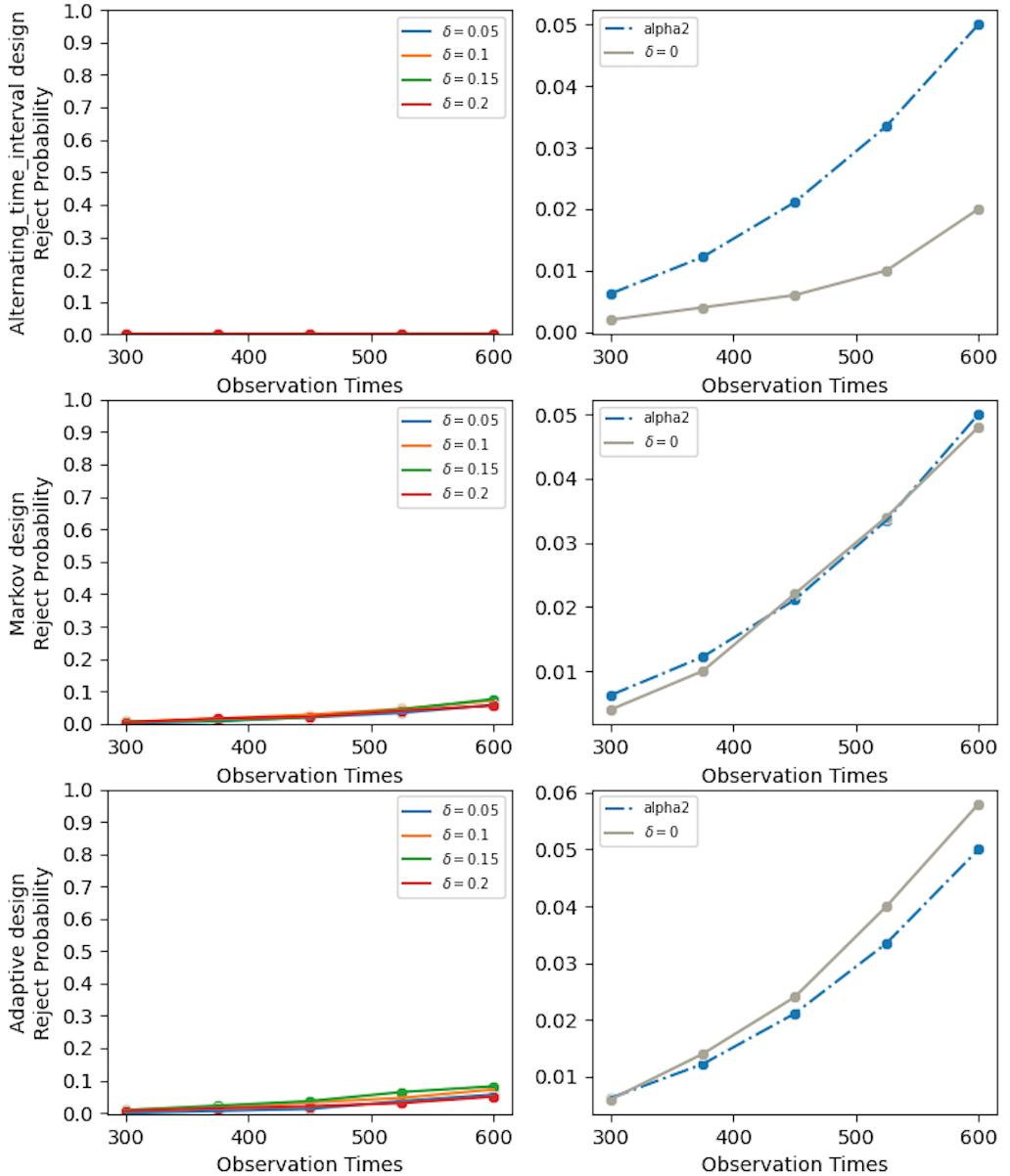

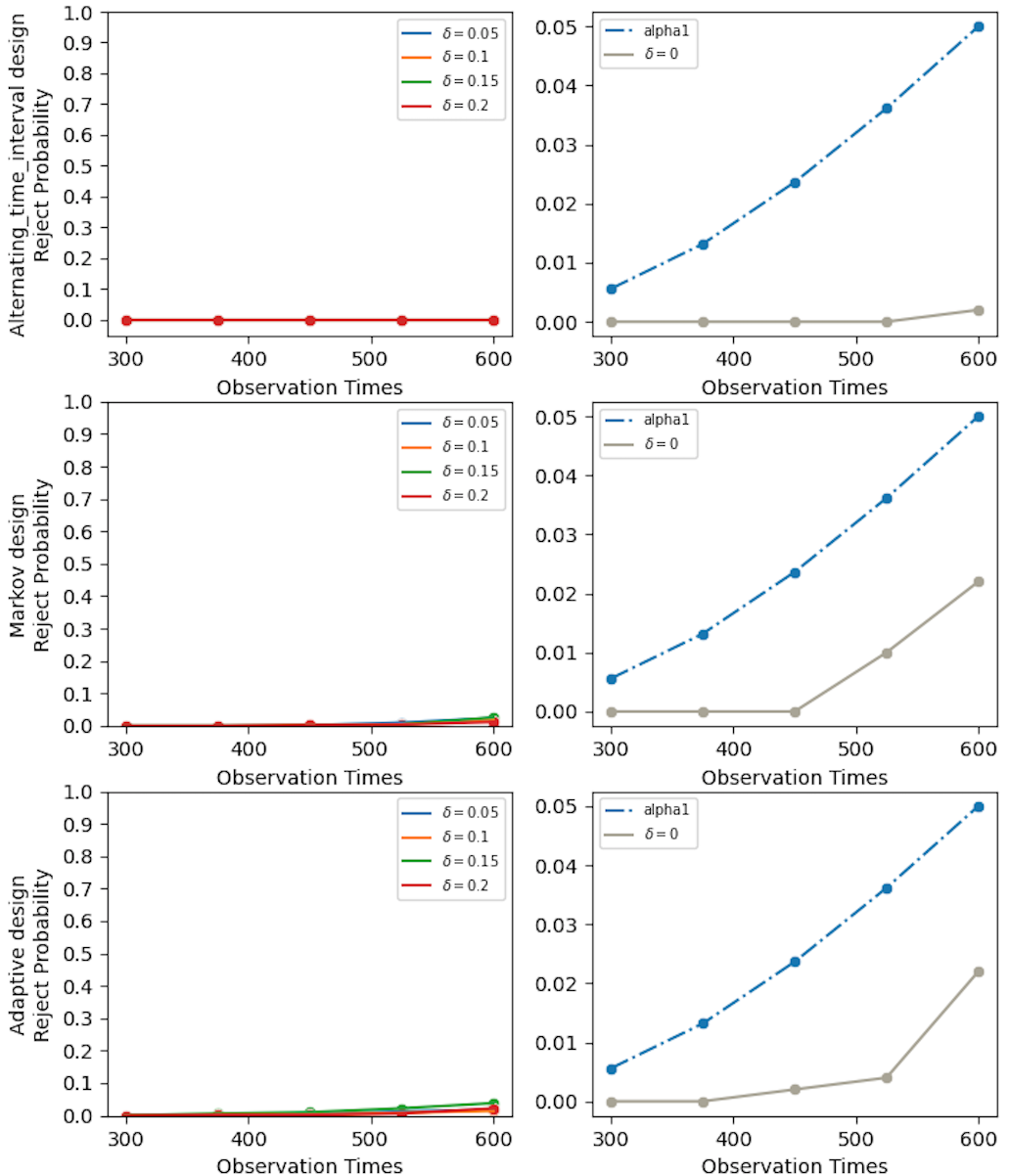

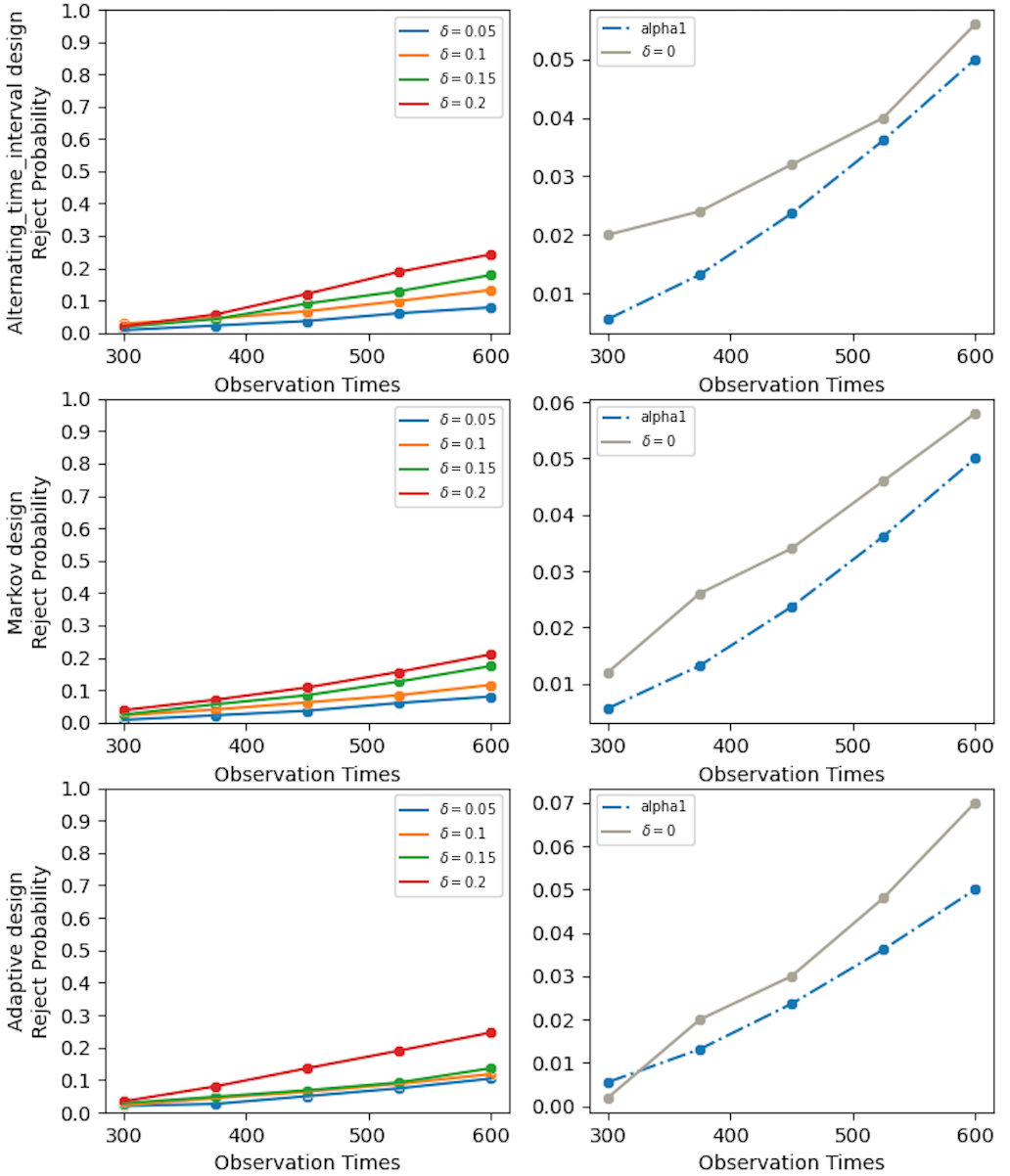

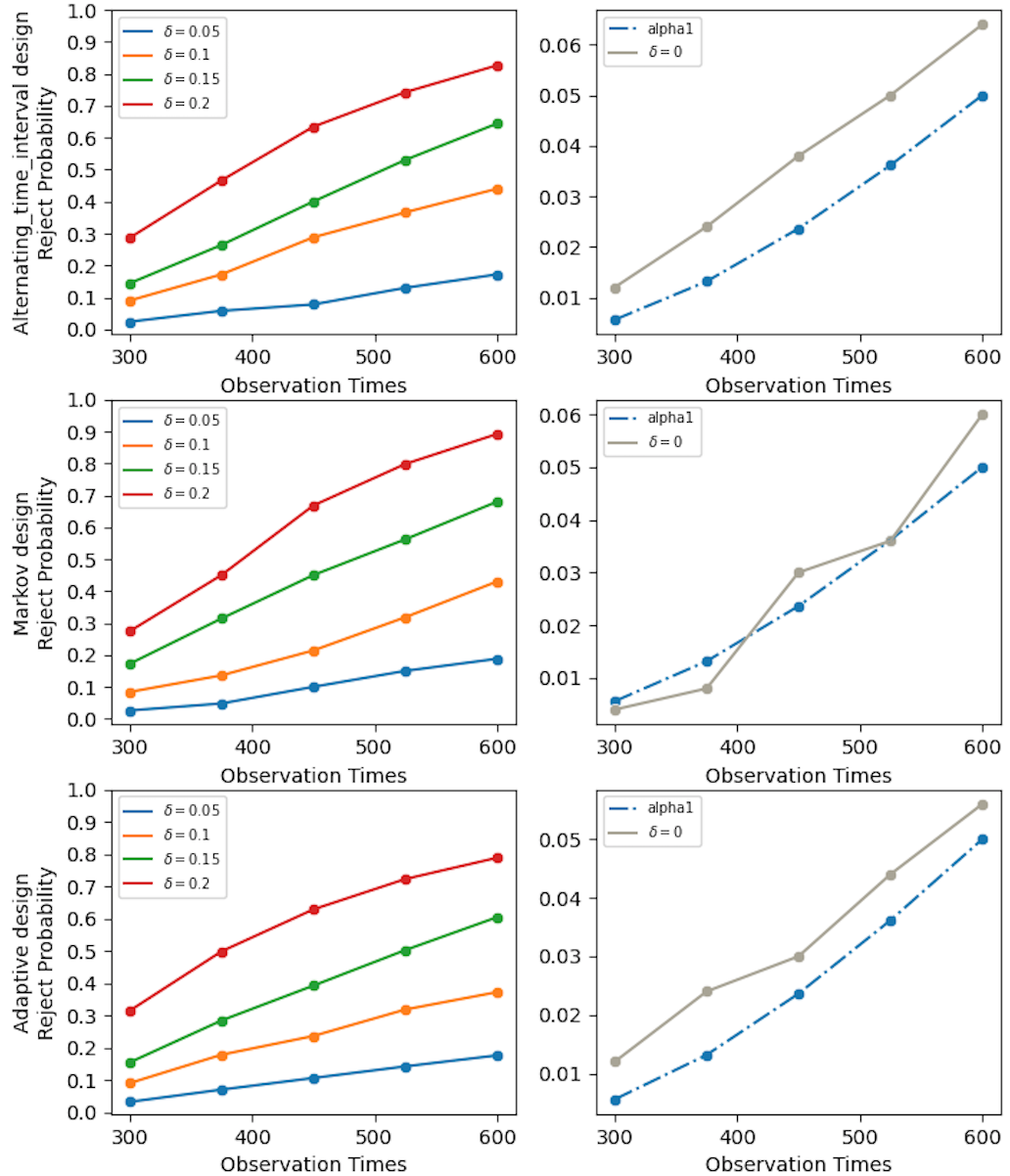

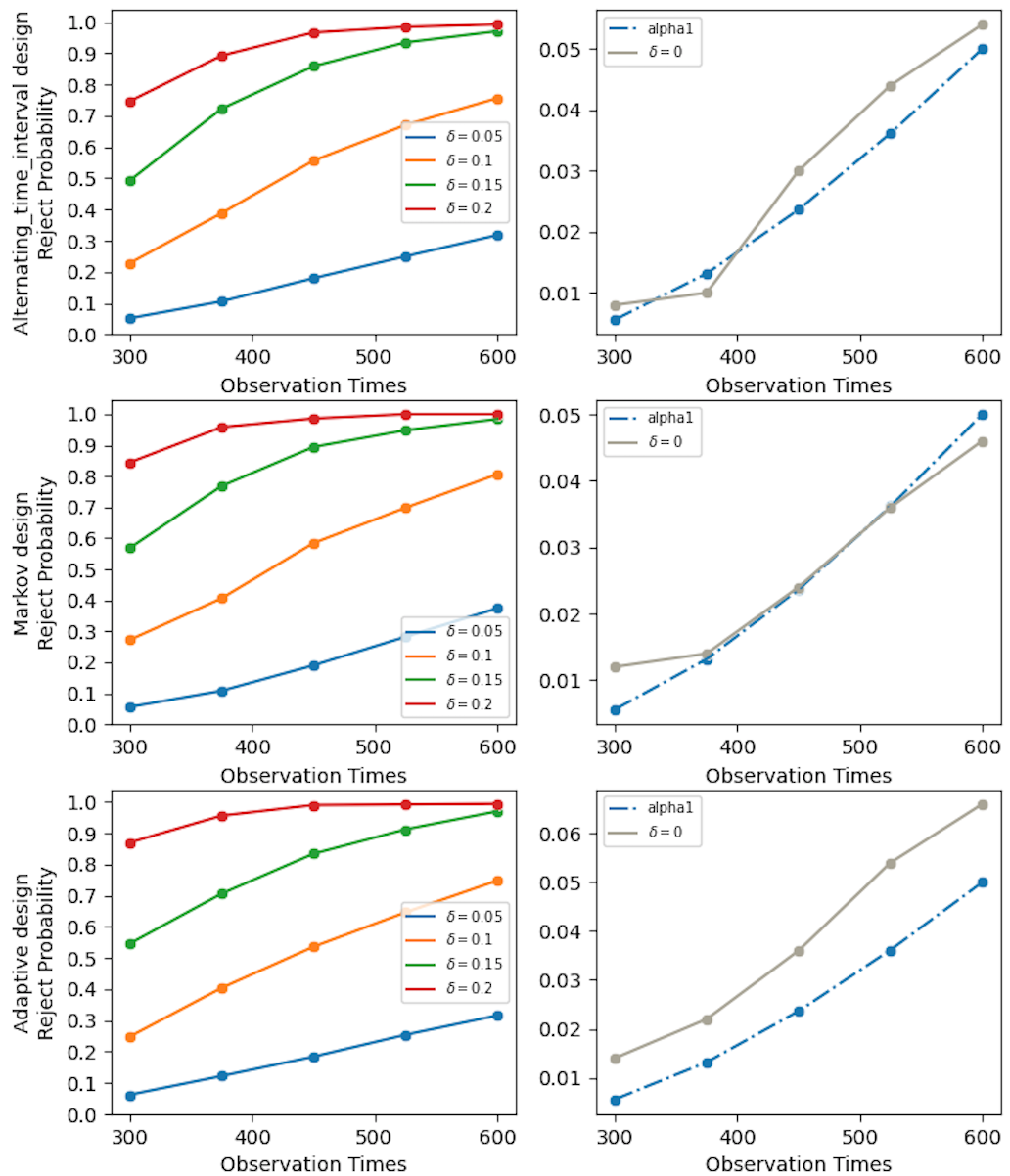

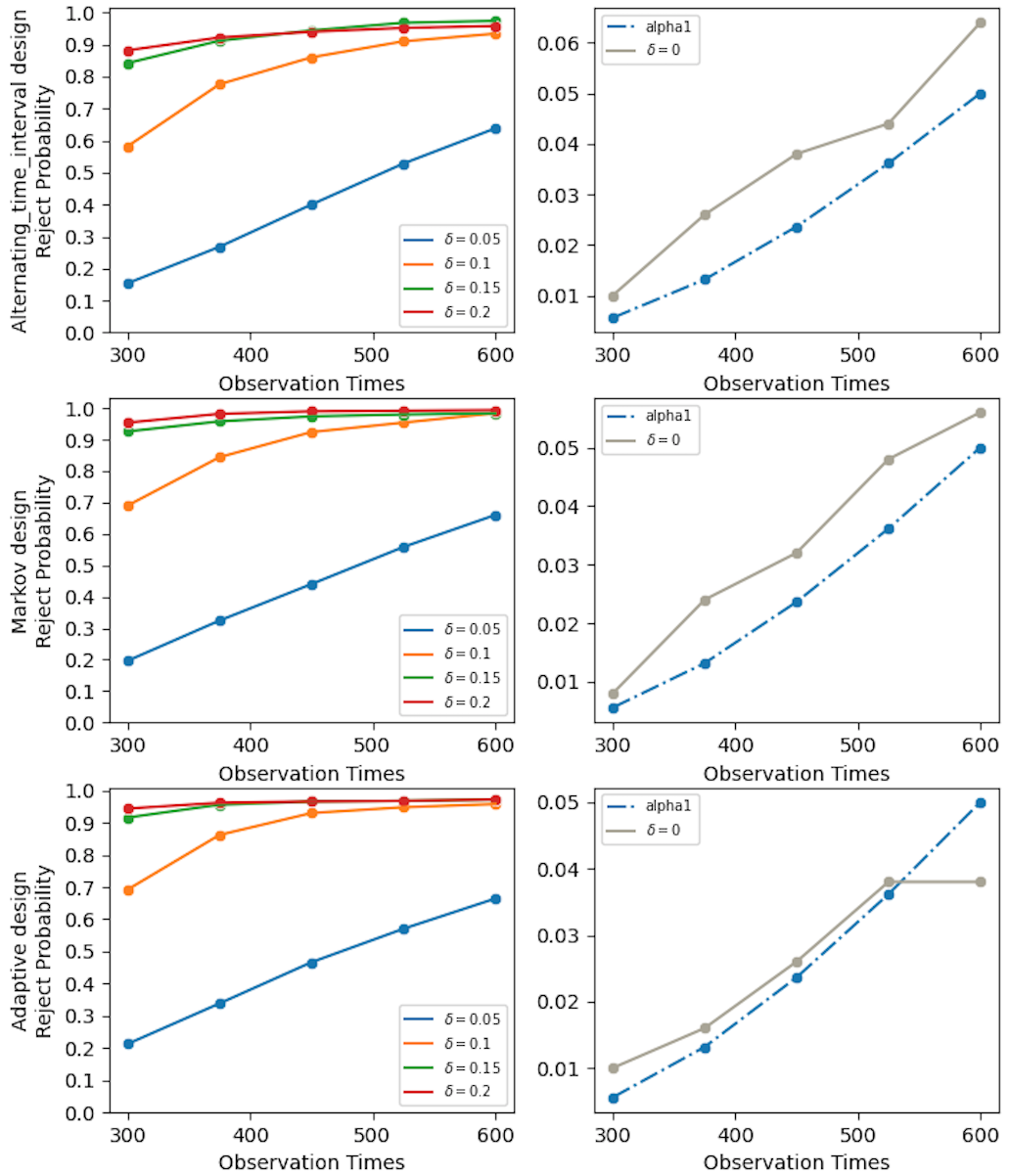

All experiments run on a macbook pro with a dual-core 2.7 GHz processor. Implementing a single test takes one second. Figures 2(a) and 3(a) depict the empirical rejection probabilities of our test statistics at different interim stages under and with different combinations of , and the designs. These rejection probabilities are aggregated over 500 simulations. We also plot and under . Based on the results, it can be seen that under , the Type-I error rate of our test is well-controlled and close to the nominal level at each interim stage in most cases. Under , the power of our test increases as increases, showing the consistency of our test procedure.

4.2 Comparison with baseline methods

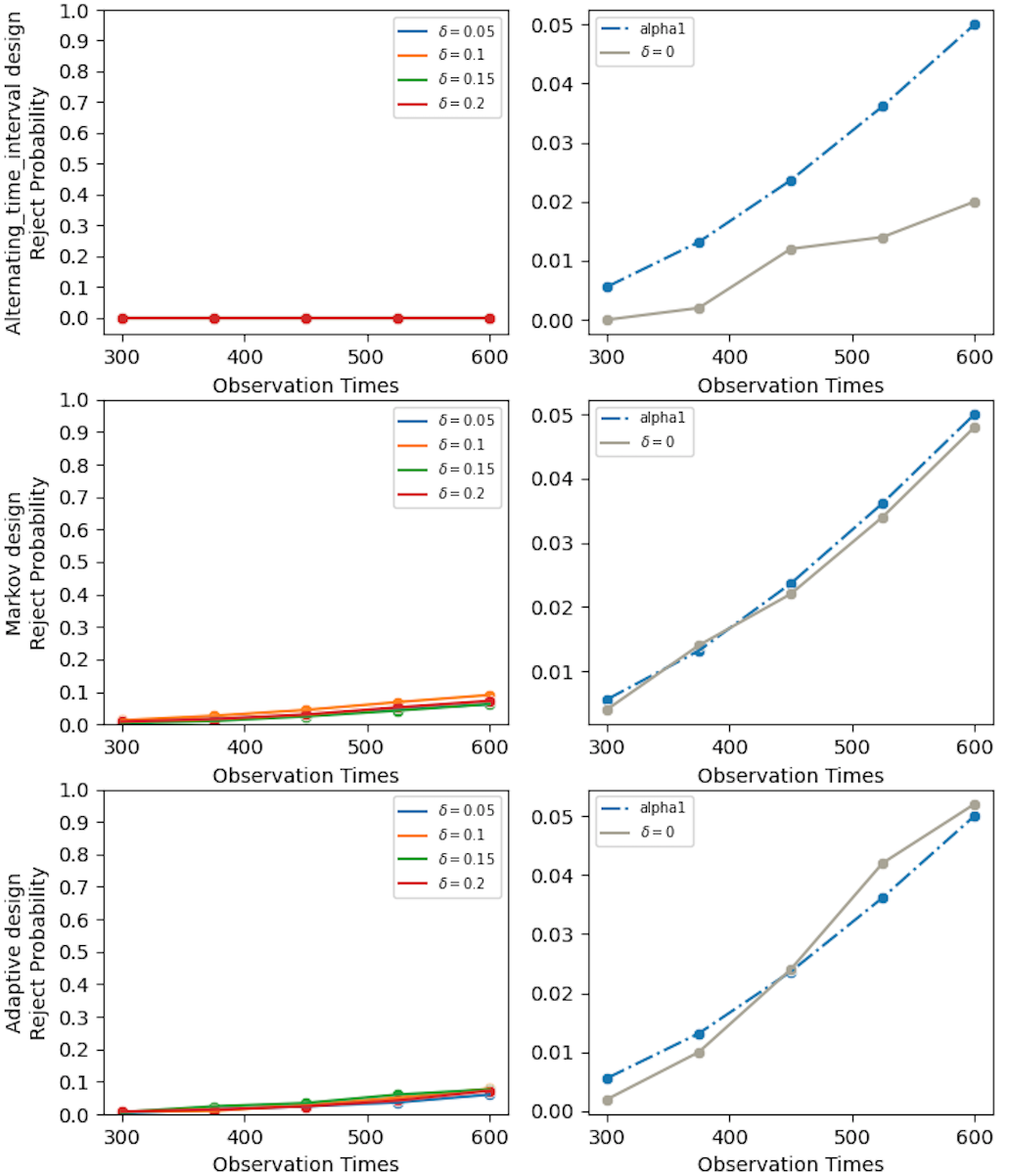

To further evaluate our method, we first compare it with the classical two-sample t-test and a modified version of modified versions of the O’Brien & Fleming sequential test developed by Kharitonov et al., (2015). We remark that the current practice of policy evaluation in most two-sided marketplace platforms is to employ classical two-sample t-test. Specifically, for each , we apply the t-test to the data and plot the corresponding empirical rejection probabilities in Figures 2(b) and 3(b). Figure 4 depicts the empirical rejection probabilities of the modified version of the O’Brien & Fleming sequential test. We remark that such a test requires equal sample size for and is not directly applicable to our setting with unequal sample size. To apply such a test, we modify the decision time and set . As shown in these figures, all these tests fail to detect any carryover effects and do not have power at all.

|

|

|

| (a) The proposed test and the test | (b) The project test and the t-test derived |

| based on V-learning under and | based on analysis of crossover trials under |

| (from left plots to right plots) | and (from left plots to right plots) |

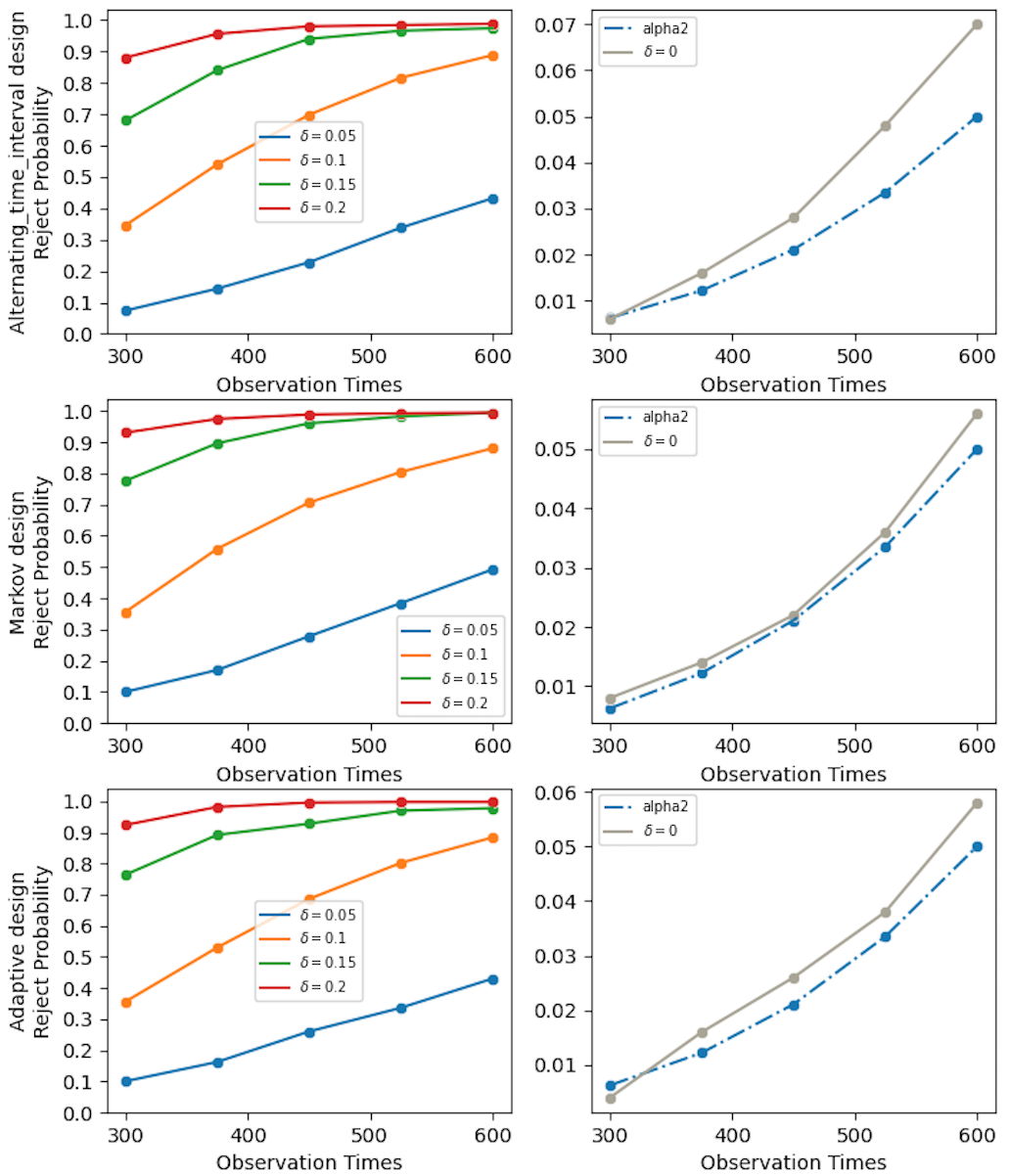

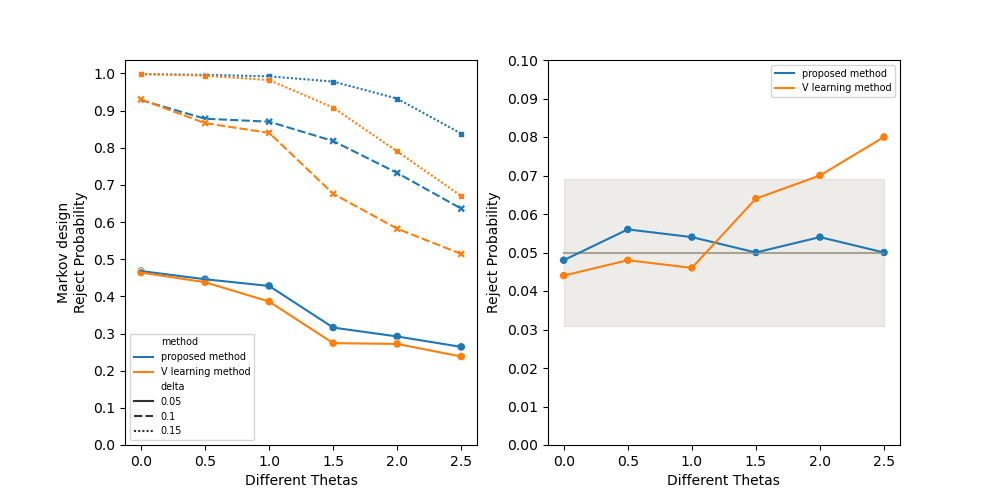

We next compare the proposed test with the test based on the V-learning method developed by Luckett et al., (2020). As we have commented, V-learning does not allow sequential testing. So we focus on settings where the decision is made once at . In addition, V-learning requires the propensity score to be bounded away from 0 and 1. To meet the positivity assumption, we generate the actions according to the Markov design where . Both tests require to specify the discounted factor . We fix . Results are reported in Figure 5(a), aggregated over 500 simulations. It can be seen for large , the test based on V-learning cannot control the type-I error and has smaller power than our test when is large. This is because V-learning uses inverse propensity score weighting. In cases where is large, the propensity score can be close to zero or one for some sample values, making the resulting test statistic unstable.

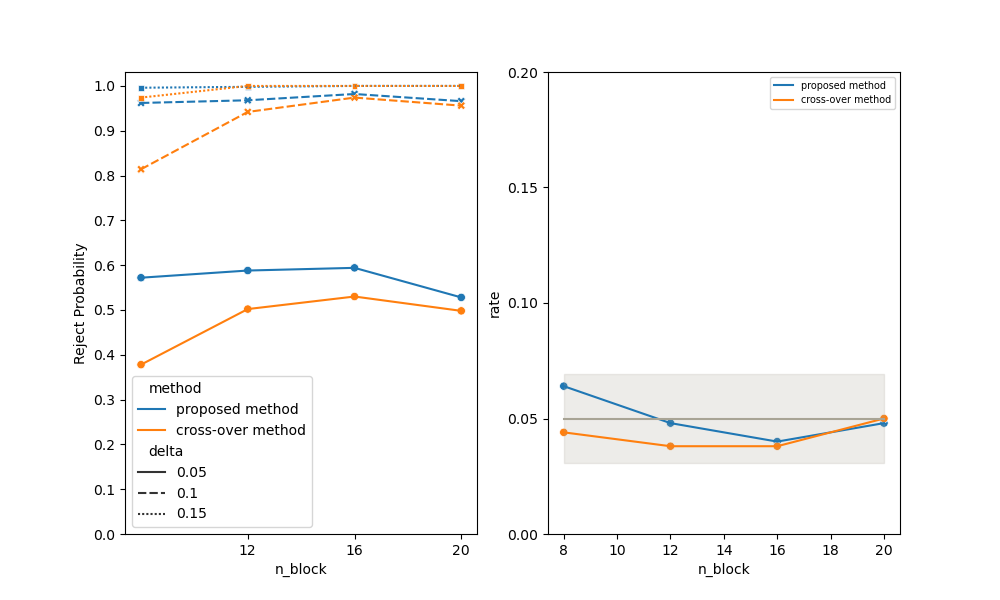

Finally, we compare the proposed test with a t-test based on analysis of crossover trials (see e.g., Jones and Kenward,, 1989). We remark that such a test requires the data to be generated from crossover designs and cannot be applied under D1, D2 or D3. In addition, most crossover trials require to recruit multiple subjects/patients to estimate the carryover effect. The resulting tests are not directly applicable to our setting where only one subject receives a sequence of treatments over time. In Appendix A, we develop a t-test for the carryover effect under our setting, based on analysis of crossover trials. For simplicity, we focus on settings where the decision is made once at . In Figure 5(b), we report the empirical rejection probabilities of such a test and the proposed test under several crossover designs with different number of blocks. Please refer to Appendix A for more details about the design and the test. It can be seen that the proposed test is more powerful in most cases.

4.3 Sensitivity analysis

In Section 4.1, we set the number of polynomial basis function to 4. We also tried some other values of by setting to 3 and 5. Results are reported in Figure 6. It can be seen that the resulting tests have very similar performance and is not sensitive to the choice of . In Appendix A, we fixed to 4 and tried some other values of (0.1, 0.3, 0.5, 0.9). Results are reported in Figure 8. It can be seen that our test controls the type-I error in most cases. In addition, its power increases with . This is consistent with the following observation: characterizes the balance between the short-term and long-term treatment effects. Under the current setup, there is no short-term treatment effects. The value difference increases with . It is thus expected that our test has better power properties for large values of .

|

|

|

| (a) The proposed test under and (from | (b) The proposed test under and (from | |

| left plots to right plots). , . | left plots to right plots). , . | |

|

|

|

| (c) The proposed test under and (from | (d) The proposed test under and (from | |

| left plots to right plots). , . | left plots to right plots). , . |

5 Real data application

We apply the proposed test to a real dataset from a large-scale ride-sharing platform. The purpose of this study is to compare the performance of a newly developed order dispatching strategy with a standard control strategy used in the platform. For a given order, the new strategy will dispatch it to a nearby driver that has not yet finished their previous ride request, but almost. In comparison, the standard control assigns orders to drivers that have completed their ride requests. The new strategy is expected to reduce the chance that the customer will cancel an order in regions with only a few available drivers. It is expected to meet more call orders and increase drivers’ income on average.

The experiment is conducted at a given city from December 3rd to December 16th. Dispatch strategies are executed based on alternating half-hourly time intervals. We also apply our test to a data from an A/A experiment (which compares the baseline strategy against itself), conducted from November 12th to November 25th. Note that it is conducted at a different time period from the A/B experiment. The A/A experiment is employed as a sanity check for the validity of the proposed test. We expect that our test will not reject when applied to this dataset, since the two strategies used are essentially the same.

Both experiments last for two weeks. Thirty-minutes is defined as one time unit. We set and for . That is, the first interim analysis is performed at the end of the first week, followed by seven more at the end of each day during the second week. We discuss more about the experimental design in Section 6.2. We choose the overall drivers’ income in each time unit as the response. The new strategy is expected to reduce the answer time of passengers and increase drivers’ income. Three time-varying variables are used to construct the state. The first two correspond to the number of requests (demand) and drivers’ online time (supply) during each 30-minutes time interval. These factors are known to have large impact on drivers’ income. The last one is the supply and demand equilibrium metric. This variable characterizes the degree that supply meets the demand and serves as an important mediator between past treatments and future outcomes.

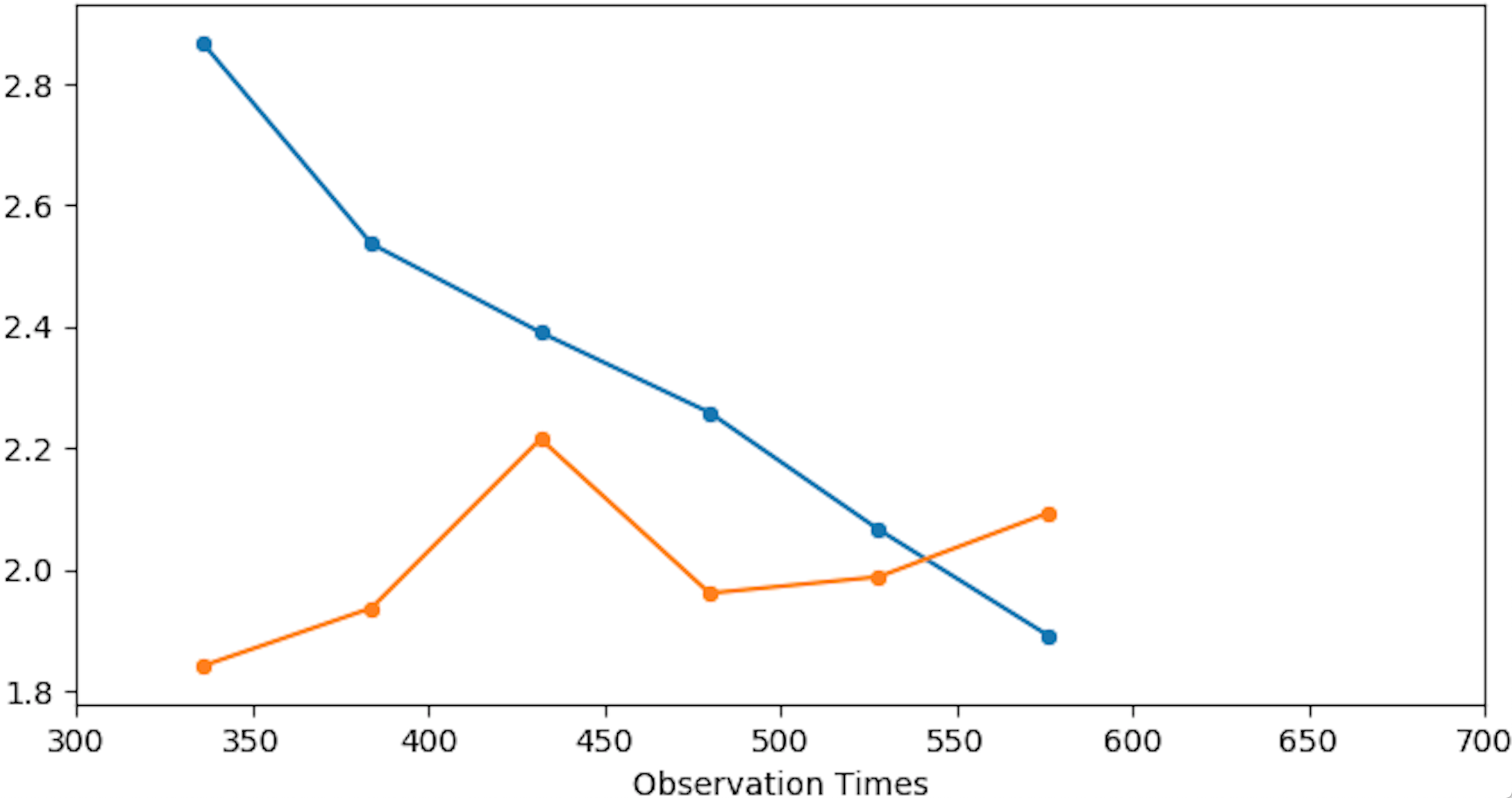

To implement our test, we set , and use a fourth-degree polynomial basis for , as in simulations. We use as the spending function for interim analysis and set . The test statistic and its corresponding rejection boundary at each interim stage are plotted in Figure 7. It can be seen that our test is able to conclude, at the end of the 12th day, that the new order dispatch strategy can significantly increase drivers’ income. When applied to the data from the A/A experiment, we fail to reject , as expected. We remark that early termination of the A/B experiment is beneficial to both the platform and the society. First, take this particular experiment as an example, we find that the new strategy reduces the answer time of orders by 2%, leading to almost 2% increment of drivers’ income. If we were to wait until Day 14, drivers would lose 2% income and customers would have to wait longer on two days. The benefits are considerable by taking the total number of drivers and customers in the city into account. In addition, the platform can benefit a lot from the increase in the driver income, as they take a fixed proportion of the driving fee from all completed trips. Second, the platform needs to conduct a lot of A/B experiments to investigate various policies. A reduction in the experiment duration facilitates the process, allowing the platform to evaluate more policies within the same time frame. These policies have the potential to further improve the driver income and the customer satisfaction, providing safer, quicker and more convenient transportation.

For comparison, we also apply the two-sample t-test to the data collected from the A/B experiment. The corresponding p-value is 0.18. This result is consistent with our findings. Specifically, the treatment effect at a given time affects the distribution of drivers in the future, inducing interference in time. As shown in the toy example (see Section 3.1), the t-test cannot detect such carryover effects, leading to a low power. Our procedure, according to Theorem 2, has enough powers to discriminate from .

6 Discussion

We discuss extensions of the proposed method to evaluate dynamic policies, the experimental design in our data application and the off-policy evaluation problem in this section. In Appendix B of the supplementary article, we discuss extensions of our proposal to high-dimensional models, the methodological difference between our proposal and the V-learning method, and the literature on crossover trials.

6.1 Dynamic policies

In this paper, we focus on comparing the long-term treatment effects between two nondynamic policies. The proposed method can be easily extended to handle dynamic policies as well. Specifically, consider two time-homogeneous policies and where each measures the treatment assignment probability . Note that the integrated value difference function can be represented by

The Q-estimators can be similarly computed via temporal difference learning. More specifically, for a given policy , let

| (15) |

be the Q-estimator given the data where where is defined by

We can plug-in the Q-estimator in (15) to estimate . The corresponding variance estimator and the resulting test statistic can be similarly derived. A bootstrap procedure can be similarly developed as in Section 3.4 for sequential testing. We omit the details for brevity.

6.2 Experimental design

In our real data application, the design of experiment is determined by the company and we are in the position to analyse the data collected based on such a design. It is important and interesting to design experiments to identity the treatment effect efficiently, but it is beyond the scope of the current paper.

In addition, it is worth mentioning that the 30-minute-interval design is adopted by the company to optimize the performance of the resulting A/B test. To elaborate, let us consider a few toy examples and compare the 30-minute-interval design with an alternating-day design where we switch back and forth between the two policies every day.

Example 3. Suppose for some constant and some zero-mean stationary AR(1) process . Here, and denote the collected response and the assigned action in the th 30-minute interval, respectively. There is no carryover effects in this example and the difference in average response between the two groups can be used as the treatment effect estimator. Under the alternating-time-interval design, the difference is taken between adjacent observations. This effectively reduces the variance of the resulting estimator. Specifically, suppose and the number of observations is equal to where denotes the number of days the experiment lasts. The treatment effect estimator takes the following form,

| (17) |

Its asymptotic variance of equals

where denotes the autocorrelation coefficient.

Under the alternating day design, the estimator takes the following form,

| (18) |

It asymptotic variance can be approximated by

Based on the above calculation, when , the asymptotic variance of could be much larger than that of . For instance, when , is approximately 9 times as large as that of .

Example 4: Suppose for and where are i.i.d. measurement errors and are i.i.d. random effects that vary across days. According to (18), the variance of the treatment effect estimator under the alternating-day design depends on that of the random effect, whose accurate estimation is very challenging in cases where is small (e.g., 14). This would inflat the Type-I error of the resulting test. On the contrary, according to (17), the variance of the treatment effect estimator under the alternating-time-interval design relies only on that of the measurement error, as the random effect cancels each other.

We remark that in the above two examples, we focus on settings without carryover effects to better illustrate the advantage of the 30-minute-interval design. In cases where the carryover effects exist and RL methods are applied to A/B testing, it would be appropriate to adopt such a design as well, so as to ensure the resulting test has good size and power properties.

Finally, under the current design, the interim analyses are conducted at the end of the first week as well as the end of each day during the second week. In general, there is a trade-off between the number of interim stages and the power of the test. In particular, the more interim stages, the more likely the test can detect the alternative early. However, it will lead to a less powerful test, which is the price we pay for early termination. This is consistent with findings in classical sequential analysis (Jennison and Turnbull,, 1999).

6.3 Off-policy evaluation

In this paper, we focus on causal effects evaluation in online experiments where the treatment generating mechanism is pre-determined. Under these settings, there are no unmeasured confounders that confound the action-outcome or the action-next state relationship. Another equally important problem is study off-policy evaluation in our application. Unmeasured confounding is a serious issue in the observational dataset. This is because the behavior policy usually involves human interventions to balance supply and demand when severe weather or some large live events occur. However, live events and extreme weather are not recorded, leading to a confounded dataset. In the RL literature, a few methods have been developed to handle latent confounders (see e.g., Namkoong et al.,, 2020; Wang et al.,, 2020; Bennett et al.,, 2021; Liao et al.,, 2021). Some of these methods can be potentially applied to our setting for policy evaluation. For instance, suppose there exists some auxiliary variables in our application that mediate the treatment effect conditionally independent of the unmeasured confounders given the treatments. Then we can apply the front-door adjustment formula to consistently infer the target policy’s value. A similar idea is proposed in Wang et al., (2020) for policy optimization. To summarize, it is practically interesting to investigate the off-policy evaluation problem in our application. However, this is beyond the scope of the current paper. We leave it for future research.

References

- Bennett et al., (2021) Bennett, A., Kallus, N., Li, L., and Mousavi, A. (2021). Off-policy evaluation in infinite-horizon reinforcement learning with latent confounders. In International Conference on Artificial Intelligence and Statistics, pages 1999–2007. PMLR.

- Bhandari et al., (2018) Bhandari, J., Russo, D., and Singal, R. (2018). A finite time analysis of temporal difference learning with linear function approximation. arXiv preprint arXiv:1806.02450.

- Bojinov and Shephard, (2020) Bojinov, I. and Shephard, N. (2020). Time series experiments and causal estimands: exact randomization tests and trading, volume accepted. Taylor & Francis.

- Boruvka et al., (2018) Boruvka, A., Almirall, D., Witkiewitz, K., and Murphy, S. A. (2018). Assessing time-varying causal effect moderation in mobile health. J. Amer. Statist. Assoc., 113(523):1112–1121.

- Burman and Chen, (1989) Burman, P. and Chen, K.-W. (1989). Nonparametric estimation of a regression function. Ann. Statist., 17(4):1567–1596.

- Candes et al., (2007) Candes, E., Tao, T., et al. (2007). The dantzig selector: Statistical estimation when p is much larger than n. Annals of statistics, 35(6):2313–2351.

- Chakraborty et al., (2010) Chakraborty, B., Murphy, S., and Strecher, V. (2010). Inference for non-regular parameters in optimal dynamic treatment regimes. Stat. Methods Med. Res., 19(3):317–343.

- Chen and Christensen, (2015) Chen, X. and Christensen, T. M. (2015). Optimal uniform convergence rates and asymptotic normality for series estimators under weak dependence and weak conditions. J. Econometrics, 188(2):447–465.

- Chernozhukov et al., (2017) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., and Newey, W. (2017). Double/debiased/neyman machine learning of treatment effects. American Economic Review, 107(5):261–65.

- Ertefaie, (2014) Ertefaie, A. (2014). Constructing dynamic treatment regimes in infinite-horizon settings. arXiv preprint arXiv:1406.0764.

- Frenken and Schor, (2017) Frenken, K. and Schor, J. (2017). Putting the sharing economy into perspective. Environmental Innovation and Societal Transitions, 23:3–10.

- Hagiu and Wright, (2019) Hagiu, A. and Wright, J. (2019). The status of workers and platforms in the sharing economy. Journal of Economics & Management Strategy, 28:97–108.

- Hanna et al., (2017) Hanna, J. P., Stone, P., and Niekum, S. (2017). Bootstrapping with models: Confidence intervals for off-policy evaluation. In Thirty-First AAAI Conference on Artificial Intelligence.

- Hao et al., (2021) Hao, B., Ji, X., Duan, Y., Lu, H., Szepesvári, C., and Wang, M. (2021). Bootstrapping statistical inference for off-policy evaluation. arXiv preprint arXiv:2102.03607.

- Hernn and Robins, (2020) Hernn, M. A. and Robins, J. M. (2020). Causal inference: What if. Boca Raton: Chapman & Hall/CRC.

- Hu et al., (2015) Hu, J., Zhu, H., and Hu, F. (2015). A unified family of covariate-adjusted response-adaptive designs based on efficiency and ethics. Journal of the American Statistical Association, 110(509):357–367.

- Hu et al., (2020) Hu, X., Qian, M., Cheng, B., and Cheung, Y. K. (2020). Personalized policy learning using longitudinal mobile health data. Journal of the American Statistical Association, accepted.

- Huang, (1998) Huang, J. Z. (1998). Projection estimation in multiple regression with application to functional ANOVA models. Ann. Statist., 26(1):242–272.

- Hudgens and Halloran, (2008) Hudgens, M. G. and Halloran, M. E. (2008). Toward causal inference with interference. Journal of the American Statistical Association, 103(482):832–842.

- Imbens and Rubin, (2015) Imbens, G. W. and Rubin, D. B. (2015). Causal Inference in Statistics, Social, and Biomedical Sciences. Cambridge University Press.

- Jennison and Turnbull, (1999) Jennison, C. and Turnbull, B. W. (1999). Group sequential methods with applications to clinical trials. Chapman and Hall/CRC.

- Jiang and Li, (2016) Jiang, N. and Li, L. (2016). Doubly robust off-policy value evaluation for reinforcement learning. In International Conference on Machine Learning, pages 652–661.

- Jin et al., (2018) Jin, S. T., Kong, H., Wu, R., and Sui, D. Z. (2018). Ridesourcing, the sharing economy, and the future of cities. Cities, 76:96–104.

- Johari et al., (2017) Johari, R., Koomen, P., Pekelis, L., and Walsh, D. (2017). Peeking at a/b tests: Why it matters, and what to do about it. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1517–1525. ACM.

- Johari et al., (2015) Johari, R., Pekelis, L., and Walsh, D. J. (2015). Always valid inference: Bringing sequential analysis to a/b testing. arXiv preprint arXiv:1512.04922.

- Jones and Kenward, (1989) Jones, B. and Kenward, M. G. (1989). Design and analysis of cross-over trials. Chapman and Hall/CRC.

- Kallus and Uehara, (2019) Kallus, N. and Uehara, M. (2019). Efficiently breaking the curse of horizon: Double reinforcement learning in infinite-horizon processes. arXiv preprint arXiv:1909.05850.

- Kharitonov et al., (2015) Kharitonov, E., Vorobev, A., Macdonald, C., Serdyukov, P., and Ounis, I. (2015). Sequential testing for early stopping of online experiments. In Proceedings of the 38th International ACM SIGIR Conference on Research and Development in Information Retrieval, pages 473–482. ACM.

- Lan and DeMets, (1983) Lan, K. K. G. and DeMets, D. L. (1983). Discrete sequential boundaries for clinical trials. Biometrika, 70(3):659–663.

- Li et al., (2019) Li, X., Ding, P., Lin, Q., Yang, D., and Liu, J. S. (2019). Randomization inference for peer effects. Journal of the American Statistical Association.

- Liao et al., (2021) Liao, L., Fu, Z., Yang, Z., Kolar, M., and Wang, Z. (2021). Instrumental variable value iteration for causal offline reinforcement learning. arXiv preprint arXiv:2102.09907.

- Liao et al., (2020) Liao, P., Qi, Z., and Murphy, S. (2020). Batch policy learning in average reward markov decision processes. arXiv preprint arXiv:2007.11771.

- Liu et al., (2018) Liu, Q., Li, L., Tang, Z., and Zhou, D. (2018). Breaking the curse of horizon: Infinite-horizon off-policy estimation. In Advances in Neural Information Processing Systems, pages 5356–5366.

- Luckett et al., (2020) Luckett, D. J., Laber, E. B., Kahkoska, A. R., Maahs, D. M., Mayer-Davis, E., and Kosorok, M. R. (2020). Estimating dynamic treatment regimes in mobile health using V-learning. J. Amer. Statist. Assoc., 115(530):692–706.

- McLeish, (1974) McLeish, D. L. (1974). Dependent central limit theorems and invariance principles. Ann. Probability, 2:620–628.

- Meitz and Saikkonen, (2019) Meitz, M. and Saikkonen, P. (2019). Subgeometric ergodicity and beta-mixing. arXiv preprint arXiv:1904.07103.

- Meng et al., (2020) Meng, H., Zhao, Y.-Q., Fu, H., and Qiao, X. (2020). Near-optimal individualized treatment recommendations. arXiv preprint arXiv:2004.02772.

- Metelkina et al., (2017) Metelkina, A., Pronzato, L., et al. (2017). Information-regret compromise in covariate-adaptive treatment allocation. The Annals of Statistics, 45(5):2046–2073.

- Mo et al., (2020) Mo, W., Qi, Z., and Liu, Y. (2020). Learning optimal distributionally robust individualized treatment rules. Journal of the American Statistical Association, pages 1–16.

- Murphy, (2003) Murphy, S. A. (2003). Optimal dynamic treatment regimes. J. R. Stat. Soc. Ser. B Stat. Methodol., 65(2):331–366.

- Namkoong et al., (2020) Namkoong, H., Keramati, R., Yadlowsky, S., and Brunskill, E. (2020). Off-policy policy evaluation for sequential decisions under unobserved confounding. arXiv preprint arXiv:2003.05623.

- Newey et al., (1998) Newey, W. K., Hsieh, F., and Robins, J. (1998). Undersmoothing and bias corrected functional estimation.

- Ning et al., (2019) Ning, B., Ghosal, S., and Thomas, J. (2019). Bayesian method for causal inference in spatially-correlated multivariate time series. Bayesian Anal., 14(1):1–28.

- Ning et al., (2017) Ning, Y., Liu, H., et al. (2017). A general theory of hypothesis tests and confidence regions for sparse high dimensional models. Annals of statistics, 45(1):158–195.

- Pouget-Abadie et al., (2019) Pouget-Abadie, J., Saint-Jacques, G., Saveski, M., Duan, W., Ghosh, S., Xu, Y., and Airoldi, E. M. (2019). Testing for arbitrary interference on experimentation platforms. Biometrika, 106(4):929–940.

- Precup et al., (2001) Precup, D., Sutton, R. S., and Dasgupta, S. (2001). Off-policy temporal-difference learning with function approximation. In ICML, pages 417–424.

- Puterman, (1994) Puterman, M. L. (1994). Markov decision processes: discrete stochastic dynamic programming. Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. John Wiley & Sons, Inc., New York. A Wiley-Interscience Publication.

- Qian and Murphy, (2011) Qian, M. and Murphy, S. A. (2011). Performance guarantees for individualized treatment rules. Annals of statistics, 39(2):1180.

- Rabta and Aïssani, (2018) Rabta, B. and Aïssani, D. (2018). Perturbation bounds for Markov chains with general state space. J. Math. Sci. (N.Y.), 228(5):510–521.

- Rambachan and Shephard, (2019) Rambachan, A. and Shephard, N. (2019). A nonparametric dynamic causal model for macroeconometrics. Available at SSRN 3345325.

- Ramprasad et al., (2021) Ramprasad, P., Li, Y., Yang, Z., Wang, Z., Sun, W. W., and Cheng, G. (2021). Online bootstrap inference for policy evaluation in reinforcement learning. arXiv preprint arXiv:2108.03706.

- Reich et al., (2020) Reich, B. J., Yang, S., Guan, Y., Giffin, A. B., Miller, M. J., and Rappold, A. G. (2020). A review of spatial causal inference methods for environmental and epidemiological applications. arXiv preprint arXiv:2007.02714.

- Robins, (1986) Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period—application to control of the healthy worker survivor effect. volume 7, pages 1393–1512. Mathematical models in medicine: diseases and epidemics, Part 2.

- Robins, (2004) Robins, J. M. (2004). Optimal structural nested models for optimal sequential decisions. In Proceedings of the second seattle Symposium in Biostatistics, pages 189–326. Springer.

- Rubin, (1980) Rubin, D. B. (1980). Randomization analysis of experimental data: The fisher randomization test comment. Journal of the American Statistical Association, 75(371):591–593.

- Rysman, (2009) Rysman, M. (2009). The economics of two-sided markets. Journal of Economic Perspective, 23:125–143.

- (57) Shi, C., Fan, A., Song, R., and Lu, W. (2018a). High-dimensional a-learning for optimal dynamic treatment regimes. Annals of statistics, 46(3):925.

- Shi and Li, (2021) Shi, C. and Li, L. (2021). Testing mediation effects using logic of boolean matrices. Journal of the American Statistical Association, page accepted.

- Shi et al., (2019) Shi, C., Song, R., Chen, Z., Li, R., et al. (2019). Linear hypothesis testing for high dimensional generalized linear models. Annals of statistics, 47(5):2671–2703.

- (60) Shi, C., Song, R., Lu, W., and Fu, B. (2018b). Maximin projection learning for optimal treatment decision with heterogeneous individualized treatment effects. Journal of the Royal Statistical Society. Series B, Statistical methodology, 80(4):681.

- (61) Shi, C., Wan, R., Song, R., Lu, W., and Leng, L. (2020a). Does the markov decision process fit the data: Testing for the markov property in sequential decision making. arXiv preprint arXiv:2002.01751.

- (62) Shi, C., Zhang, S., Lu, W., and Rong, R. (2020b). Statistical inference of the value function for reinforcement learning in infinite horizon settings. arXiv preprint arXiv:2001.04515.

- Shi et al., (2021) Shi, C., Zhang, S., Lu, W., and Song, R. (2021). Statistical inference of the value function for reinforcement learning in infinite horizon settings. Journal of the Royal Statistical Society. Series B. Statistical Methodology, accepted.

- Sobel and Lindquist, (2014) Sobel, M. E. and Lindquist, M. A. (2014). Causal inference for fmri time series data with systematic errors of measurement in a balanced on/off study of social evaluative threat. Journal of the American Statistical Association, 109(507):967–976.

- Song et al., (2015) Song, R., Wang, W., Zeng, D., and Kosorok, M. R. (2015). Penalized q-learning for dynamic treatment regimens. Statistica Sinica, 25(3):901.

- Stone, (1982) Stone, C. J. (1982). Optimal global rates of convergence for nonparametric regression. Ann. Statist., 10(4):1040–1053.

- Sutton and Barto, (2018) Sutton, R. S. and Barto, A. G. (2018). Reinforcement learning: an introduction. Adaptive Computation and Machine Learning. MIT Press, Cambridge, MA, second edition.

- Sutton et al., (2008) Sutton, R. S., Szepesvári, C., and Maei, H. R. (2008). A convergent o(n) algorithm for off-policy temporal-difference learning with linear function approximation. Advances in neural information processing systems, 21(21):1609–1616.

- Thomas and Brunskill, (2016) Thomas, P. and Brunskill, E. (2016). Data-efficient off-policy policy evaluation for reinforcement learning. In International Conference on Machine Learning, pages 2139–2148.

- Thomas et al., (2015) Thomas, P. S., Theocharous, G., and Ghavamzadeh, M. (2015). High-confidence off-policy evaluation. In Twenty-Ninth AAAI Conference on Artificial Intelligence.

- Viviano and Bradic, (2019) Viviano, D. and Bradic, J. (2019). Synthetic learner: model-free inference on treatments over time. arXiv preprint arXiv:1904.01490.

- Wager and Athey, (2018) Wager, S. and Athey, S. (2018). Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113:1228–1242.

- Wang et al., (2020) Wang, L., Yang, Z., and Wang, Z. (2020). Provably efficient causal reinforcement learning with confounded observational data. arXiv preprint arXiv:2006.12311.

- Wang et al., (2018) Wang, L., Zhou, Y., Song, R., and Sherwood, B. (2018). Quantile-optimal treatment regimes. Journal of the American Statistical Association, 113(523):1243–1254.

- Wu et al., (1986) Wu, C.-F. J. et al. (1986). Jackknife, bootstrap and other resampling methods in regression analysis. the Annals of Statistics, 14(4):1261–1295.

- Yang et al., (2017) Yang, F., Ramdas, A., Jamieson, K. G., and Wainwright, M. J. (2017). A framework for multi-a (rmed)/b (andit) testing with online fdr control. In Advances in Neural Information Processing Systems, pages 5957–5966.

- Yao et al., (2020) Yao, L., Chu, Z., Li, S., Li, Y., Gao, J., and Zhang., A. (2020). A survey on causal inference. arXiv:2002.02770.

- Zhang et al., (2013) Zhang, B., Tsiatis, A. A., Laber, E. B., and Davidian, M. (2013). Robust estimation of optimal dynamic treatment regimes for sequential treatment decisions. Biometrika, 100(3):681–694.

- Zhang et al., (2007) Zhang, L.-X., Hu, F., Cheung, S. H., Chan, W. S., et al. (2007). Asymptotic properties of covariate-adjusted response-adaptive designs. The Annals of Statistics, 35(3):1166–1182.

- Zhang et al., (2018) Zhang, Y., Laber, E. B., Davidian, M., and Tsiatis, A. A. (2018). Estimation of optimal treatment regimes using lists. J. Amer. Statist. Assoc., 113(524):1541–1549.

- Zhang et al., (2015) Zhang, Y., Laber, E. B., Tsiatis, A., and Davidian, M. (2015). Using decision lists to construct interpretable and parsimonious treatment regimes. Biometrics, 71(4):895–904.

- Zhao et al., (2012) Zhao, Y., Zeng, D., Rush, A. J., and Kosorok, M. R. (2012). Estimating individualized treatment rules using outcome weighted learning. J. Amer. Statist. Assoc., 107(499):1106–1118.

- Zhao et al., (2015) Zhao, Y.-Q., Zeng, D., Laber, E. B., and Kosorok, M. R. (2015). New statistical learning methods for estimating optimal dynamic treatment regimes. J. Amer. Statist. Assoc., 110(510):583–598.

- Zhou et al., (2020) Zhou, Y., Liu, Y., Li, P., and Hu, F. (2020). Cluster-adaptive network a/b testing: From randomization to estimation. arXiv preprint arXiv:2008.08648.

- Zhu et al., (2017) Zhu, R., Zhao, Y.-Q., Chen, G., Ma, S., and Zhao, H. (2017). Greedy outcome weighted tree learning of optimal personalized treatment rules. Biometrics, 73(2):391–400.

- Zou et al., (2019) Zou, S., Xu, T., and Liang, Y. (2019). Finite-sample analysis for sarsa with linear function approximation. In Advances in Neural Information Processing Systems, pages 8665–8675.

Appendix A More on simulations

We first report the rejection probabilities of the proposed test with different choices of the discounted factor in Figure 8. We fix the number of basis functions and the -spending function . It can be seen that the proposed test controls the type-I error in most cases. Its power increases with the discounted factor .

|

|

|

| (a) The proposed test under and (from | (b) The proposed test under and (from | |

| left plots to right plots). . | left plots to right plots). . | |

|

|

|

| (c) The proposed test under and (from | (d) The proposed test under and (from | |

| left plots to right plots). . | left plots to right plots). . |

We next propose a t-test for the carryover effect based on the analysis of crossover trials (see e.g., Jones and Kenward,, 1989, Chapter 2). The main idea is to divide the entire experiment into a sequence of non-overlapping blocks with equal size. We require the number of blocks to be divisible by 2. Let denote the number of blocks. We randomly allocate them with equal probability on the th block for any . If the th block receives one treatment, then the th block will receive the other treatment. Let denote the average response of the th block. Let if the th block receives the new treatment and otherwise. We propose to estimate the carryover effect by where

Its standard error can be estimated by where and

We reject the null hypothesis when exceeds the upper th quantile of a t-distribution with 2n-2 degrees of freedom.

Appendix B Some more discussions

B.1 Extensions to high-dimensional models

In this section, we extend our proposal to settings where the dimension of the state is allowed to diverge with the sample size. We recommend to include a rich class of basis functions to ensure that the Q-function can be well-approximated. Specifically, we assume for any and where the dimension is allowed to be much larger than . In this case, the matrix might not be invertible and the estimator cannot be directly obtained by solving the Bellman equation, as in Section 3.

To handle high-dimensionality, we first adopt the Dantzig selector (Candes et al.,, 2007) to compute an initial estimator , which directly penalizes the Bellman equation. We next develop a decorrelated estimator by debiasing the initial estimator. This decorrelated estimation step is to reduce the bias of . It ensures the entry of , is -consistent and asymptotically normal.

Specifically, for any , we propose to compute by solving

where

for a sequence of tuning parameters such that as .

Next, for simplicity, suppose has a limiting distribution . For any , we observe that , the th element of , satisfies the following equation:

| (19) |

for a state-action-outcome-next state tuple , where denotes the th element of , and denote the subvector of and obtained by removing their th element, respectively, and

We remark that Equation (19) is doubly-robust. It holds as long as either or is correctly specified.

To estimate , we compute another Dantzig-type estimator of ,

where

for a sequence of tuning parameters such that as .

Finally, based on (19), we compute by construct the following estimating equation,

where denotes the subvector of the initial estimator obtained by removing its th element.

The doubly-robustness property ensures the asymptotic normality of in cases when neither the initial estimator nor converges at a parametric rate (see e.g., Theorem 1, Shi and Li,, 2021). Specifically, under certain mild conditions, when the tuning parameters and are set to be for some sufficiently large constant , we can show that and converge at a rate of and , respectively, where and denotes the number of nonzero elements in and (see e.g., Theorem 6.1, Shi et al., 2018a, ). Then using similar arguments in the proof of Theorem 1 of Shi and Li, (2021), we can show that has a tractable limiting distribution when .

Let denote the estimator for based on . Its asymptotic variance can be consistently estimated by whose th element is given by

where corresponds to the estimated Bellman residual . Let . At time , we reject the null if . A bootstrap-assisted procedure can be similarly developed for sequential monitoring, as in Section 3.4. We omit the details for brevity.

B.2 Comparison with Luckett et al., (2020)

Below, we summarize the methodological difference between our proposal and the V-learning method. First, we remark that V-learning focuses on the problem of policy optimization. That is, how to learn an optimal policy based on the observed dataset. This problem is different from policy evaluation, which is the focus of our paper. For a given randomized policy, Luckett et al., (2020) outlined a procedure to learn its value in Section 2. In Theorem 4.2 of Luckett et al., (2020), they proved the asymptotic normality of the value estimator. In Theorem 4.3 of Luckett et al., (2020), they provided a consistent variance estimator when the policy being considered is an estimated optimal policy. Based on these arguments, one can develop a procedure to infer the value difference between two policies. However, its numerical performance remains unknown to us, as no numerical results were available in Luckett et al., (2020) that report the coverage probability of the resulting confidence interval.

Second neither sequential monitoring nor online updating (update the test without storing the historical data) is being considered in Luckett et al., (2020). To the contrary, the focus of our paper is to design a test procedure that allows for sequential monitoring and online updating, as motivated by our application.