Benchmarking Flexible Electric Loads Scheduling Algorithms under Market Price Uncertainty

Abstract

Because of increasing amounts of intermittent and distributed generators in power systems, many demand response programs have been developed to schedule flexible energy consumption. However, proper benchmarks for comparing these methods are lacking, especially when decisions are made based on information which is repeatedly updated. This paper presents a new benchmarking tool designed to bridge this gap. Surveys that classify flexibility planning algorithms were an input to define the benchmarking standards. The framework can be used for different objectives and under diverse conditions faced by electricity energy stakeholders interested in flexibility scheduling algorithms. It includes a simulation environment that captures the evolution of look–ahead information, which enables comparing online planning and scheduling algorithms. The benchmarking tool is used to test seven planning algorithms measuring their performance under uncertain market conditions. The results show the importance of online decision making, the influence of data quality on the algorithm performance, the benefit of using robust and stochastic programming approaches, and the necessity of trustworthy benchmarking.

1 Introduction

The integration of renewable energy is central for achieving energy security in a zero–carbon energy future [1]. Some renewable energy sources are intermittent and difficult to forecast; thus, maximizing their use requires different operation and planning strategies to those traditionally used for more foreseeable or controllable loads and generators. Exploiting the flexibility in demand is a viable strategy for coping with the additional uncertainty [2].

The scientific community has been responsive to this by developing a broad spectrum of algorithms to design effective incentive programs, commonly known as demand response (DR) programs. Over 70 publications of demand–side management were reviewed in [3] to establish a general framework for such approaches; the authors analyzed whether users made selfish or cooperative decisions, the problem is solved with deterministic or stochastic methods, and the algorithms are offline versus online. Deng et al. summarized the objectives and issues in DR programs [4], and Mukherjee and Gupta the control type considered in smart scheduling algorithms [5]. One of the most extensive categorizations of DR programs and algorithms was published in [6]; it accounts for over 200 publications.

With so many options, power sector stakeholders need tools to compare and identify the method that suits their objectives the best. Unfortunately, only a small number of publications focuses on benchmarking existing methods or comparing new contributions to established ones. In [7], a new approach that uses hierarchical control is compared to algorithms assuming central control, which are known for finding system–wide optimal solutions. Four models to maximize the value of flexible resources are proposed and compared in [8].

The challenge from assessing strategies increases when stakeholders consider real–time decisions, which require online algorithms, which update decisions based on new information. Simulation allows evaluating the performance of such online algorithms on multiple criteria. Furthermore, simulation can help developing better online optimization algorithms for complex dynamic problems [9].

This work presents a framework to benchmark offline and online algorithms for scheduling flexible energy loads. This framework is the basis of an open-source toolbox, B-FELSA. To compare results to the input data, check the reproducibility of observed behavior, and compare simulation outcomes using different algorithms, the toolbox includes a simulator. Users can change the input parameters, and use results to perform sensitivity analysis of their decisions. In summary, it is a verification environment, that offers tools for calibration and validation tasks making it an effective benchmarking tool [10].

This benchmarking framework is designed from the perspective of a consumer with flexible demand (or a stakeholder acting on his/her behalf) who wants to minimize total costs considering market incentives for load shifting. It covers shiftable and energy–based electric devices and accounts for the uncertainty associated with market incentives. This framework is used to compare algorithms that schedule this flexible energy demand. Straightforward and advanced heuristics, deterministic optimization and stochastic approaches are tested in a realistic scenario comparable to the Dutch energy market, as well as in an artificial scenario in which the quality of the provided data can be controlled.

The rest of this paper is organized as follows: Section 2 describes and motivates the scheduling context of the benchmark. Section 3 describes the framework and how it addresses the challenge of benchmarking online algorithms. This includes a description of the planning algorithms that are evaluated. Section 4 presents two case studies and discusses the results. Section 5 provides an overview of other energy decision support tools and explains the added value of the presented benchmarking framework. Section 6 concludes this research.

2 Loads Scheduling Context

Transmission system operators (TSOs) as well as distribution system operators (DSOs) around the world have identified the benefit from DR programs to prevent congestion or ensure balance of supply and demand. This has led to a large number of different programs, tariffs and market designs, which are employed to elicit the flexibility in loads from mainly residential, commercial customers, or both. First we explain and motivate which DR context we have chosen for the benchmarking of loads scheduling algorithms, and then we give the type of flexible load that is represented.

2.1 Demand response programs

As described in the surveys on demand side management and demand response [3, 4, 6], DR programs include centralized and decentralized control, advanced tariffs such as time of use, critical peak, real–time pricing and tier tariffs, to short–term electricity markets.

Considering current practice, the short–term electricity and ancillary services markets seem to be the preferred way of trading flexible demand. The most common of these markets consist of a two–sided auction where parties trade energy supply and demand in hourly or block intervals called program time units (PTUs) [11], and typically start about half a day before the day of delivery. Such an auction is known as the day–ahead (DA) market.

Some countries have market designs that allow trading between stakeholders closer to the time of delivery. These markets are known as intraday markets in European countries. They facilitate trading continuously, or sometimes in discrete slots, after closure of the DA market. A similar environment is known as the adjustments market by the Electric Reliability Council of Texas (ERCOT).

Parallel to DA and intraday markets, many TSOs use (voluntary) ancillary services to maintain grid stability. Trading parties can make bids to offer reserves supporting regulation up or down. Regulation up occurs in any instance when the demand exceeds the supply. The opposite case is known as regulation down. The deadline to place bids for offering ancillary services varies across countries, and conditions are typically different for offering voluntary or contracted services. A bid typically consists of both a volume and a price, possibly different for each PTU. Offering ancillary services is equivalent to a demand bidding and buyback DR program, but with the option of also increasing consumption.

After energy delivery, differences between actual energy use and the DA commitment are settled by paying an imbalance price to the TSO. This is called the imbalance market.

In the benchmark we consider participation in the DA, imbalance and reserves markets. Intraday participation is not included but could be developed using the same logic used for online decisions in the imbalance market.

2.2 Type of load and its flexibility

Electric devices in the grid can be classified in fixed, shiftable, and elastic energy–based or comfort–based [3]. Shiftable devices have a fixed load profile that can only move in time. Elastic energy–based devices must consume a fixed amount of electricity within a given window; and comfort–based devices have flexible profiles only constrained by a comfort level target, e.g., temperature control systems [3]. Furthermore, devices with energy storage capacity can offer unidirectional or bidirectional services (when devices can sell energy to the system) [5].

The analysis presented here is restricted to electric vehicle (EV) charging. EVs have relatively high flexibility and capacity, and this makes them good candidates for providing DR. Moreover, they are representative of other elastic energy–based devices such as heat pumps.

3 Overview of B-FELSA

The previous section highlights the broadness of the scope of the DR program context. The large variety in the problem context has resulted in a large number of solution methods. This also makes comparing and benchmarking solution methods a hard task. B-FELSA is designed to deal with this complexity.

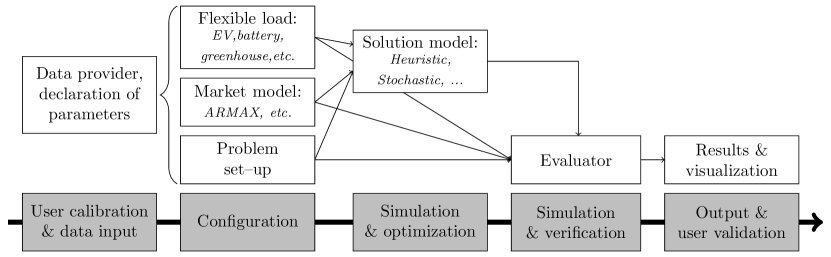

B-FELSA has a modular design, which makes it a flexible platform for testing, comparing and designing new algorithms in various market design settings. The modules are grouped based on the steps followed for evaluating algorithms. The first phase, i.e. the input phase, is managed by the data provider. In the following step, the experiments are configured using the input data and parameters. Three modules are responsible for this: flexible load, market environment and problem set–up. The latter module refers to additional input parameters that define the solution model or external options, such as the existence of physical grid constraints. The next two phases and modules are critical for benchmarking algorithms. They use the market simulation environment to optimize scheduling decisions and measure the outcomes of those decisions. The modules are named solution model and evaluator, respectively. The last phase outputs results and offers a diverse set of visualizations for results validation. Fig. 1 illustrates the structure of B-FELSA. B-FELSA is open-source and its source can be obtained at [12].

Each of these modules is discussed in a separate section below.

3.1 Data provider

The input data consists of the loads, market, and model and simulator configuration. The market data includes DA market prices, regulation price and ancillary service usage. Additional data includes information such as grid constraints, and parameters defined by the user to model the uncertainty and its evolution.

3.2 Flexible load

The flexible load module is designed for EV charging, but with the option of extending it with other energy–based elastic or time–shiftable devices. The algorithms included in B-FELSA consider a single type of flexible load that can be aggregated. The user can implement changes to B-FELSA to account for a mixed pool of flexible loads as explained in [7], or to consider micro–grid cost minimization or utility and maximization problems.

3.3 Market data for simulator

Because DA market prices are relatively easy to predict, in the benchmark these are modeled deterministically, but the uncertainty associated with the final regulation condition (i.e., whether ancillary services are accepted), and real–time energy prices are modeled through scenarios.

The simulation environment consists of a series of discrete trading times from the DA to delivery time. With each time step the information is updated. All decisions made for energy delivery in previous steps are fixed, but all other decisions can be updated. All decisions must be aggregated to verify that the total energy demand is fulfilled within the load constraints.

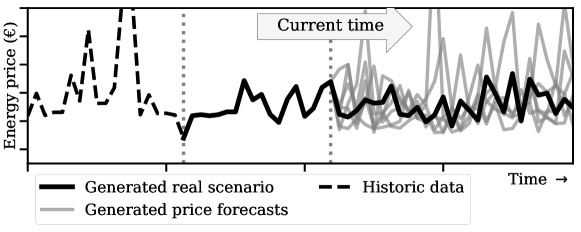

The user can generate scenarios to simulate the decision environment using different methods. One of the models included to generate market price scenarios is the auto–regressive moving average model with exogenous variables (ARMAX), which is widely used for scenario generation and DA market price forecasting [13, 14, 15, 16, 17]. In particular, we follow and adapt the method used by Olsson and Soder [14] for real–time balancing market prices generation. This method was identified as one of the best performing by Klaeboe [16]. Both [14, 16] focus on the Nordic power market prices. Olsson’s method is adapted by using a Box-Cox-transformation [18] instead of a log-transformation to normalize the data, and by using exogenous variables to capture the seasonal (daily) component [19].

Ancillary services are used when the supply and demand need to be balanced. Acceptance happens on a continuous basis, in contrast to the discrete program time units (PTU) for offering the service. Furthermore, the required volume also determines acceptance. Therefore, we use an abstraction that represents these two conditions. For each PTU, we estimate the percentage of time that the total energy offered is completely accepted and deployed, as is similarly done in [20]. Scenarios for this abstraction are also generated. We do this using a discrete Markov model with transition probabilities depending on the time of the day and season of the year. The transition probabilities are based on historic data.

Fig. 2 shows how the ARMAX model is used to generate both an evaluation scenario (the real scenario) and price forecasts. During online evaluation, at every time step, these price forecasts are regenerated creating a series starting at the current time in the evaluation. Multiple scenarios are generated using Monte Carlo simulation. In the same way scenarios are also generated for the ancillary service usage using the Markov model introduced above. This models the market uncertainty and the increase in information as time draws closer to time of delivery.

3.4 Solution model

An algorithm needs to decide the amount of energy purchased on the DA market per hour, and the energy use, the amount of up and down reserves committed, and the up and down reserve price bids per PTU. Every load has a session start and end, a starting state of charge (SOC), a required minimum SOC, a capacity, and a maximum energy usage (charging speed). The data provided to the solution models is the DA price per hour, and a set of scenarios consisting of an up and down regulating price, an imbalance price, and percentage of up and down reserve usages for every PTU.

Solution methods include linear and mixed integer programming, non–linear programming, dynamic programming, particle swarm optimization, Markov process based–methods, evolutionary algorithms and other metaheuristics [5, 6]. Additionally, game theory models can be used when considering solutions that rely on the stakeholders’ interaction and their willingness to cooperate.

B-FELSA can evaluate all such algorithms except for multi–party cooperating and competition models. The following are already included in the toolbox:

-

1.

The Direct model (DI) represents buying energy immediately when plugged in.

-

2.

The Optimal price method (OP) minimizes the costs by charging at those times when the predicted energy market price is minimal. It does not provide reserves.

-

3.

Heuristics can be used to provide reasonable charging decisions. The MaxReg heuristic method (MR) from [21] is included. MR follows a preferred operating point (POP). With MR the POP is defined in such a way that it allows for maximum reserve participation. Reserve bids are quantity-only. For the analysis in this paper, the method has been updated to consider the reserve commitment deadline. It assumes that all its bids will be accepted and fully deployed and makes new robust bids based on this assumption.

-

4.

With the Deterministic model (DT), a user can plan energy and reserves market participation. The user determines a desired acceptance probability, which is used to find the optimal quantity and price bid for bidding in the reserves market. It also optimizes DA, and imbalance markets participation. The algorithm is the interpretation by Van der Linden et al.[22] of the solution method introduced by Sarker et al.[23].

-

5.

The Quantity-only method (QO) offers ancillary services but does not provide a price bid and assumes to be always accepted. It is implemented with DT by setting the desired acceptance probability to 100%.

-

6.

The Stochastic optimization model uses a number of price scenarios to determine optimal reserve price bids and energy trade in DA and imbalance markets. Two versions are included:

-

(a)

A one stage stochastic optimization model (SO1) that is similar to the deterministic model presented above, but optimizes for multiple scenarios instead of only the average scenario.

-

(b)

A two stage stochastic optimization model (SO2) that uses binary variables to determine whether a price bid will be accepted or not. It was originally developed by Van der Linden et al.[22] and improved by making the MIP formulation more tight and compact.

-

(a)

B-FELSA also contains a perfect information (PI) solution model. Its solutions are obtained by providing SO2 with only the real scenario as input. The solution from PI can be used for comparison purposes.

3.5 Evaluator

The evaluator uses simulation to measure the realisation of decisions made in every time step. Therefore, this module is critical to assess how online algorithms use new information to improve results.

The evaluator measures the run time and operation costs of the algorithm. It also measures the unmet demand and the exceeded battery capacity. It is possible that the algorithm makes a reserve commitment but the EV is not able to fulfill this commitment, because its battery capacity is reached. In this case the simulation continues as if it were possible, and the battery overflow is measured and outputted at the end. The same happens when the consumer’s demand is not met.

3.6 Visualization

B-FELSA provides different visualizations to the user with four objectives: first, comparing the market input data to the decisions made; second, the scheduling and bidding decisions as well as the consequences in terms of costs and risk; third, the evolution of decisions over time as well as the consequences of those decisions; and last, the ability to easily compare the effects of different algorithms, parameter settings or market settings side by side.

4 Case studies

The main purpose of B-FELSA is to be able to compare different online solution methods for DR programs quantitatively. In this section B-FELSA is used to study two case studies. The case studies are used to answer the following questions:

-

1.

How does an online algorithm perform in comparison to the optimal decision under perfect information?

-

2.

What algorithm offers the best trade–off between scalability, and solution quality (feasible running time for minimum cost and risk of unmet demand)?

-

3.

What market participation strategy offers the minimum energy costs within my desired level of risk?

-

4.

How does the algorithm deal with new (better) information?

The first case study is a realistic case study with a market configuration similar to the Dutch energy market. It tests the performance of the algorithms mentioned in terms of operational costs, run time, and ability to deal with uncertainty.

The second case study is an artificial case study in which the (increase of the) prediction quality of the market realization can be controlled. It measures the effect of the (increase of) prediction quality (over time) on the algorithm’s performance.

4.1 Dutch energy market case study

TenneT’s market data [24] is used to create 95 historic scenarios. The ARMAX and Markov model are used to generate 10 scenarios per historic scenario, giving 950 of these scenarios in total. Then, at every increment of 15 minutes in every run, a total of 25 scenarios is generated using the same ARMAX and Markov model to represent forecasts. This (renewed) data is given to the algorithms to make or update its decisions. For each of these scenarios the overnight charging of one EV is simulated. The charging session takes 12 hours, so 48 time steps of 15 minutes. The EV has a battery capacity of 30kWh, an initial SOC of 1kWh, needs 26kWh, has a maximum charging speed of 7kW, and a charging efficiency of 90%. Unmet demand is penalized with €60/MWh and battery capacity overflow with €200/MWh (in comparison, the average DA energy price is €32/MWh). Discharging, or vehicle-to-grid, is not allowed.

The Dutch energy market has DA prices per hour, and regulation and imbalance prices per PTU of 15 minutes. Here only voluntary secondary reserve bids are considered and these regulation bids are asymmetric and can be made up to 7 PTUs before delivery. Regulation is rewarded based on the amount of reserves deployed. Imbalance prices are based on the highest (lowest) price of the deployed reserve bids. The Dutch market has a minimum regulation bid size, but this is ignored here.

Based on experiments, the desired acceptance probability for DT is set to 50%, and to 80% for SO1. SO2 optimizes based on 20 scenarios.

All the solution methods were coded in Java. Gurobi 8.1.0 [25] is used as MIP solver for QO, DT, SO1 and SO2, with the MIP gap set to 1%. Run time results are for an Intel i7 6600U CPU with 8GB of RAM.

| Costs + | Unmet | Exceeded | Run | |

| penalty | demand | capacity | time | |

| (€) | (%) | (%) | (s) | |

| DI | 0.470.51 | 0.0 | 0.0 | 1e–32e–3 |

| OP | 0.390.44 | 0.0 | 0.0 | 1e–31e–3 |

| MR | 0.270.46 | 0.0 | 0.0 | 1e-36e-3 |

| QO | 0.280.50 | 0.080.68 | 0.220.80 | 0.590.10 |

| DT | 0.210.54 | 1.632.84 | 0.331.51 | 0.580.08 |

| SO1 | 0.270.48 | 0.110.69 | 0.020.21 | 0.660.10 |

| SO2 | 0.190.58 | 0.241.14 | 0.171.03 | 73.841.2 |

| PI | -0.250.78 | 0.0 | 0.0 |

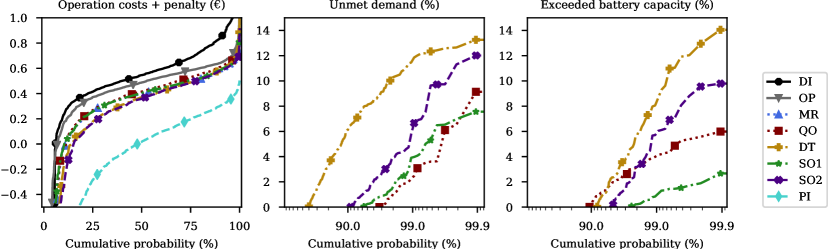

Fig. 3 and Table 1 show the results of this case study. The values shown in the table are averages. Fig. 3 is a quantile plot. A quantile plot shows the fraction of values (vertical axis) that fall below that quantile (horizontal axis). The unmet demand and exceeded battery capacity are reported as percentages of the requested load and battery capacity respectively. An average unmet demand of 1.6% for example (the average unmet demand for DT) means that the battery is charged to 26.6kWh, 0.4kWh below its requested amount of 27kWh. With a charging speed of 7kW, this means that the EV missed approximately 4 minutes of charging time. This unmet demand is reflected in the cost with the penalization of €60/MWh, resulting in a penalty of 2.5 cents.

The results for operation costs show only a small difference between the methods. A student’s t-test proves that these differences are significant with except for MR, QO, and SO1. The differences in unmet demand are significant for all cases, except for again QO and SO1. Differences in exceeded battery capacity are also significant for all cases, except for QO and SO2. It can be concluded therefore that SO2 on average has the best results in terms of costs plus penalty. The difference between SO1 and DT shows that solving for multiple scenarios does not decrease operation costs, but does decrease unmet demand and exceeded battery capacity (this is also the case when SO1 is run with the desired acceptance probability set to 50%). Interestingly, MR has cost results similar to QO and SO1 without having a penalty. What makes it more interesting is that MR does not use the scenario data at all. It also has a run time orders of magnitude smaller.

A general observation from the results is that there is a high variance in the results, and as a result, differences between methods are as small as 2% of the total standard deviation. The largest difference is between DI and SO2, with SO2 being 60% cheaper than DI. Having perfect information is on average yet another 85% of the total standard deviation better in comparison to SO2. But the standard deviation for PI is even higher than the total standard deviation. This means the performance variability is inherent to the problem. This also shows the importance of dealing with uncertainty in this problem.

4.2 Controlled increasing prediction quality case study

The setup of the case study with controlled increasing prediction quality is similar to the previous case study except for the following point. Instead of generating 25 scenarios per time step, the simulator generates scenarios. From these scenarios, 25 scenarios with the smallest error are selected. This error measure is defined in such a way that differences between the real and generated scenario at the beginning of a scenario have a higher weight. By changing the parameter , the quality of the forecast can be regulated, with denoting no information increase, and higher means higher forecast quality.

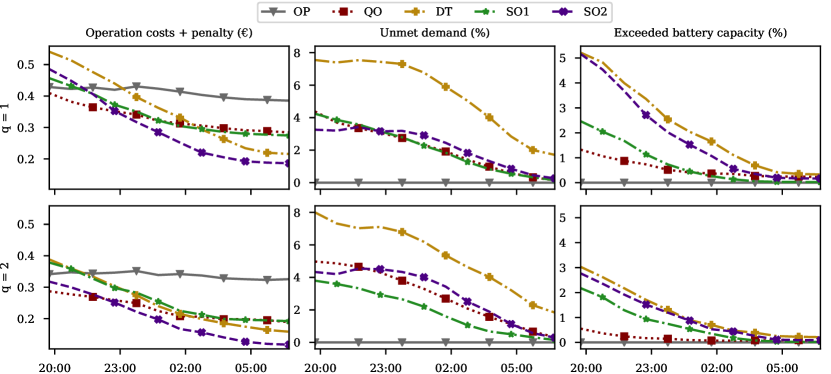

Fig. 4 and Table 2 show the effect of the increase in information over time. As time progresses, the methods are re-evaluated with more up to date data. The results in Fig. 4 shows what the end results would have been if no change in decisions was made from that point. MR, DI and PI have been left out from this evaluation. MR is left out because the value of does not influence its decisions as MR ignores the data.

A first glance shows directly that over time the operation costs for all methods decrease. The updated information allows the methods to improve their decisions and this gives better results. Fig. 4 shows that the four methods that provide reserves improve more over time than OP. This is because OP only optimizes based on the expected energy price. The other methods provide reserves and learn over time whether reserve bids are accepted and deployed or not, and can updated their decisions based on that afterwards.

In the previous case study, the heuristic MR method had similar performance than more complex methods like SO1, even though it does not use any of the provided data. But with improved data quality QO, DT, SO1 and SO2 all perform better on average in terms of penalized costs. This shows the importance of analyzing methods with different information quality.

The amount of exceeded battery capacity and unmet demand also decrease over time. The increased information quality makes only a small difference for the amount of unmet demand at the end of the charging session. For DT, SO1, and SO2 this difference is not statistically significant. Just as with , QO, SO1, and SO2 all score well below 1% unmet demand on average. For these methods more than 90% of the time there is no unmet demand or exceeded battery capacity at all. The difference in exceeded battery capacity is bigger and statistically significant for all methods expect for SO1, but SO1 already has almost no exceeded capacity when .

| Costs + | Unmet | Exceeded | |

| penalty (€) | demand (%) | capacity (%) | |

| OP | 0.33 (-0.06) | 0.0 | 0.0 |

| QO | 0.19 (-0.09) | 0.22 (+0.14) | 0.06 (-0.15) |

| DT | 0.16 (-0.06) | 1.73 (+0.10) | 0.21 (-0.12) |

| SO1 | 0.19 (-0.08) | 0.11 (-0.00) | 0.02 (-0.01) |

| SO2 | 0.12 (-0.07) | 0.26 (+0.02) | 0.09 (-0.08) |

5 Review of energy decision support tools

A broad spectrum of tools and simulators have been developed to address the upcoming challenges for policy makers and other power sector stakeholders. This section highlights the insights from four thorough reviews of computer tools developed in the last 20 years to inform decisions in the electric energy industry. Furthermore, it analyzes two tools that have capabilities comparable to B-FELSA.

Already in 2009, Conolly et al. published a review of the different computer tools that supported decisions relevant to the integration of renewable energy [26]. This survey aimed to inform decision–makers about the best tool to use for their specific situation. Tools were classified in: simulation, scenario, equilibrium–tool, top–down, bottom–up, operation optimization, and investment. None of these classifications focuses on assessing the strategies or algorithms used for scheduling loads.

Soares et al. classified simulation tools in electricity market, and micro–grid and smart grid simulators [27]. Grid simulators are designed to support decisions on the physical integration of the power grid components, which is outside of the scope of B-FELSA.

Energy market simulators model the energy market as a series of interactions between different stakeholders negotiating electricity contracts. These simulators help those stakeholders to prescribe the consequences of their own decisions and those of other parties participating in the markets. Hence, they could include the objectives of B-FELSA as well. Some well–known examples are: the Simulator for Electric Power Industry Agents (SEPIA) [28], Powerweb, which includes both a market and grid model [29], the Short-medium Run Electricity Market Simulator (SREMS) based on game theory [30], the Electricity Markets Complex Adaptive System (EMCAS) [31], the AMES, a wholesale power market test bed [32], the advanced energy systems analysis model, EnergyPLAN [33], and the Multi-agent Simulator of Competitive Electricity Markets (MASCEM) [34]. Many of these energy market simulators are very powerful and include agent models that can learn from their actions. Additionally, some have been enhanced by the integration with packages with important features. For example, ALBids is a decision support tool for agents negotiating in the energy market [35]. It includes different strategies already introduced in the literature. These strategies can be used by agents in MASCEM and compared considering different market environments.

Seventy–five modeling tools to analyze energy systems were studied by Ringkjøb et al. [36]. Similar to [26], this more recent study highlights that energy computer tools are designed to answer specific questions. Ringkjøb et al. classify the tools in power systems analysis; operation decision support, which focus on dispatch problems, such as the unit commitment problem; investment decision support that assess full investment cycles; and scenarios for focusing on long–term industry projections [36]. These classifications do not capture the aim of B-FELSA. Nonetheless, among the tools included, the Distributed Energy Resources Customer Adoption Model Plus (DER-CAM+) has an objective relevant to our work [37]. This tool classifies loads based on their fuel or end–use type. It integrates a power grid model with market data to represent energy, as well as reserve markets. Selecting the best strategy for distributed loads considering the market participation and grid constraints is one of its main objectives.

The tools studied in these four surveys have many applications, but they are mostly based on deterministic models [36]. Furthermore, when agents can consider alternative strategies, these are predetermined or derived from the learning algorithms dependant on the market simulation [38]. Of the tools studied, ALBids and DER-CAM+ aim to find an optimal strategy for parties with distributed and flexible loads participating in energy markets. However, these tools include this capability among an array of options, which hinders their use for studying the effect from different factors (under controlled settings) on algorithms for scheduling decisions.

B-FELSA addresses the absence of a comparison methodology and simulation environment for algorithms that optimally schedule flexible loads. This is achieved by focusing on the decisions made by an agent trading energy to be used or dispatched by flexible loads. This agent is a price–taker. Thus, the uncertainty in the different markets is simulated through scenarios of prices and settlement decisions. Furthermore, we consider the implications of the strategic decisions made by flexibility traders for other important energy sector matters.

6 Conclusions

Large numbers of DR programs and algorithms have been developed for dealing with increasing uncertainty in energy supply. This paper presents a benchmarking tool for quantitative analysis of these methods, called B-FELSA. B-FELSA is designed to be able to consistently compare flexible loads scheduling algorithms under a variety of different market designs, and varying information regarding future price and reserve acceptance scenarios.

The two presented case studies illustrate the value of B-FELSA. The results show first that a simple analysis of algorithms based on expected values is not good enough, because of the highly volatile nature of imbalance prices and ancillary service usage. In particular, the strategy that uses expected values (DT) has the highest percentage of unmet demand and exceeded battery capacity.

Second, the case studies show that it is hard (very costly) to find schedules with reserves that are robust and meet the minimum energy and capacity requirements in all scenarios. This is of particular importance for stakeholders that want to minimize or quantify risk, or for a TSO that considers using flexible loads for maintaining system stability.

Third, B-FELSA gives insight into how the solution methods improve their decisions over time. The uncertainty of the market behavior makes it difficult to trade based on schedules made day-ahead. The online analysis shows that updating your decisions during the day is necessary to decrease costs and to minimize risk, and that the quality of data should be considered when choosing a scheduling algorithm. It also shows the benefit of using stochastic programming or robust approaches, especially with regard to balancing risk and costs.

This paper focuses on the optimization from the perspective of flexible load consumers. With future work the presented framework should also be able to answer research questions from other stakeholders. The consumer is interested in minimizing costs and risk. Distribution system operators want to prevent congestion and maintain voltage level standards, and are therefore interested in consumer behavior and in providing the right incentives to consumers to maintain stability. Similarly, TSOs are interested in prescribing the balancing capacity available considering the incentives offered by the wholesale market and their imbalance settlements. And policymakers want markets that efficiently allocate resources and provide solutions that improve social welfare.

B-FELSA can already answer some of the questions that these stakeholders might have. Still, there are a few important addition that would enlarge the scope of the proposed framework: the intraday market, other types of flexible load, and different types of local grid constraints are examples. The case studies also show that the (quality of the) data influences the performance of the algorithms. By adding other data generation methods it will be clearer what performance can be explained by the data, and what by the solution method. Other future work is to use the insight that B-FELSA provides to make a better online scheduling algorithm.

Regulators must design the right incentive mechanism that enables social welfare of energy systems operations. Operators need to make the best term daily operations, maintenance, and planning decisions that guarantee a reliable and sustainable service. Users want the best and most affordable service. Moreover, users that can sell to the grid or can offer flexibility for a smooth operation may need an incentive and efficient planning algorithms to make their flexibility available. Therefore, there is a high demand for methods to support the diverse set of new decisions faced by the energy sector stakeholders. B-FELSA provides the framework to assess these methods.

Acknowledgments

The work presented in this paper is funded by the Netherlands Organization for Scientific Research (NWO), as part of the Uncertainty Reduction in Smart Energy Systems program (URSES)

References

- International Renewable Energy Agency [2018] International Renewable Energy Agency. Energy transition. https://www.irena.org/energytransition, 2018. Accessed: 2018-11-13.

- Villar et al. [2018] José Villar, Ricardo Bessa, and Manuel Matos. Flexibility products and markets: Literature review. Electric Power Systems Research, 154:329–340, 2018. doi: 10.1016/j.epsr.2017.09.005.

- Barbato and Capone [2014] Antimo Barbato and Antonio Capone. Optimization models and methods for demand-side management of residential users: A survey. Energies, 7(9):5787–5824, 2014. doi: 10.3390/en7095787.

- Deng et al. [2015] Ruilong Deng, Zaiyue Yang, Mo-Yuen Chow, and Jiming Chen. A survey on demand response in smart grids: Mathematical models and approaches. IEEE Transactions on Industrial Informatics, 11(3):570–582, 2015. doi: 10.1109/TII.2015.2414719.

- Mukherjee and Gupta [2015] Joy Chandra Mukherjee and Arobinda Gupta. A review of charge scheduling of electric vehicles in smart grid. IEEE Systems Journal, 9(4):1541–1553, 2015. doi: 10.1109/JSYST.2014.2356559.

- Vardakas et al. [2015] John S Vardakas, Nizar Zorba, and Christos V Verikoukis. A survey on demand response programs in smart grids: Pricing methods and optimization algorithms. IEEE Communications Surveys & Tutorials, 17(1):152–178, 2015. doi: 10.1109/COMST.2014.2341586.

- Xu et al. [2016] Zhiwei Xu, Duncan S Callaway, Zechun Hu, and Yonghua Song. Hierarchical coordination of heterogeneous flexible loads. IEEE Transactions on Power Systems, 31(6):4206–4216, 2016. doi: 10.1109/TPWRS.2016.2516992.

- Kazempour and Hobbs [2018] Jalal Kazempour and Benjamin F Hobbs. Value of flexible resources, virtual bidding, and self-scheduling in two-settlement electricity markets with wind generation—part i: Principles and competitive model. IEEE Transactions on Power Systems, 33(1):749–759, 2018. doi: 10.1109/TPWRS.2017.2699687.

- Dunke and Nickel [2017] Fabian Dunke and Stefan Nickel. Evaluating the quality of online optimization algorithms by discrete event simulation. Central European Journal of Operations Research, 25(4):831–858, 2017. doi: 10.1007/s10100-016-0455-6.

- Bialek et al. [2016] Janusz Bialek, Emanuele Ciapessoni, Diego Cirio, Eduardo Cotilla-Sanchez, Chris Dent, Ian Dobson, Pierre Henneaux, Paul Hines, Jorge Jardim, Stephen Miller, et al. Benchmarking and validation of cascading failure analysis tools. IEEE Transactions on Power Systems, 31(6):4887–4900, 2016. doi: 10.1109/TPWRS.2016.2518660.

- Brijs et al. [2017] Tom Brijs, Cedric De Jonghe, Benjamin F Hobbs, and Ronnie Belmans. Interactions between the design of short-term electricity markets in the CWE region and power system flexibility. Applied energy, 195:36–51, 2017. doi: 10.1016/j.apenergy.2017.03.026.

- van der Linden [2019] Koos van der Linden. Benchmark for flexible electric load scheduling algorithms v1.0. https://github.com/AlgTUDelft/B-FELSA, 2019.

- Conejo et al. [2010] Antonio J Conejo, Miguel Carrión, Juan M Morales, et al. Decision making under uncertainty in electricity markets, volume 1. Springer, 2010. doi: 10.1007/978–1–4419–7421–1.

- Olsson and Soder [2008] Magnus Olsson and Lennart Soder. Modeling real-time balancing power market prices using combined SARIMA and markov processes. IEEE Transactions on Power Systems, 23(2):443–450, 2008. doi: 10.1109/TPWRS.2008.920046.

- Ansari et al. [2015] Muhammad Ansari, Ali T Al-Awami, Eric Sortomme, and MA Abido. Coordinated bidding of ancillary services for vehicle-to-grid using fuzzy optimization. IEEE Transactions on Smart Grid, 6(1):261–270, 2015. doi: 10.1109/TSG.2014.2341625.

- Klæboe et al. [2015] Gro Klæboe, Anders Lund Eriksrud, and Stein-Erik Fleten. Benchmarking time series based forecasting models for electricity balancing market prices. Energy Systems, 6(1):43–61, 2015. doi: 10.1007/s12667-013-0103-3.

- Alipour et al. [2017] Manijeh Alipour, Behnam Mohammadi-Ivatloo, Mohammad Moradi-Dalvand, and Kazem Zare. Stochastic scheduling of aggregators of plug-in electric vehicles for participation in energy and ancillary service markets. Energy, 118:1168–1179, 2017. doi: 10.1016/j.energy.2016.10.141.

- Box and Cox [1964] George EP Box and David R Cox. An analysis of transformations. Journal of the Royal Statistical Society: Series B (Methodological), 26(2):211–243, 1964.

- Deen [2019] Gerrit Deen. Increasing the market value of wind power using improved stochastic process modeling and optimization. Master’s thesis, Delft University of Technology, 3 2019.

- Vagropoulos and Bakirtzis [2013] Stylianos I Vagropoulos and Anastasios G Bakirtzis. Optimal bidding strategy for electric vehicle aggregators in electricity markets. IEEE Transactions on power systems, 28(4):4031–4041, 2013.

- Sortomme and El-Sharkawi [2010] Eric Sortomme and Mohamed A El-Sharkawi. Optimal charging strategies for unidirectional vehicle-to-grid. IEEE Transactions on Smart Grid, 2(1):131–138, 2010.

- van der Linden et al. [2018] Koos van der Linden, Mathijs de Weerdt, and Germán Morales-España. Optimal non-zero price bids for evs in energy and reserves markets using stochastic optimization. In Proceedings of the 15th International Conference on the European Energy Market (EEM), pages 574–578. IEEE, 2018. doi: 10.1109/EEM.2018.8470023.

- Sarker et al. [2016] M. R. Sarker, Y. Dvorkin, and M. A. Ortega-Vazquez. Optimal Participation of an Electric Vehicle Aggregator in Day-Ahead Energy and Reserve Markets. IEEE Transactions on Power Systems, 31(5):3506–3515, September 2016. ISSN 0885–8950. doi: 10.1109/TPWRS.2015.2496551.

- TenneT [2019] TenneT. Market information. http://www.tennet.org/bedrijfsvoering/ExporteerData.aspx, 1 2019. Accessed: 2019-07-03.

- Gurobi Optimization Inc. [2016] Gurobi Optimization Inc. Gurobi optimizer reference manual. http://www.gurobi.com, 2016.

- Connolly et al. [2010] David Connolly, Henrik Lund, Brian Vad Mathiesen, and Martin Leahy. A review of computer tools for analysing the integration of renewable energy into various energy systems. Applied energy, 87(4):1059–1082, 2010. doi: 10.1016/j.apenergy.2009.09.026.

- Soares et al. [2018] João Soares, Tiago Pinto, Fernando Lezama, and Hugo Morais. Survey on complex optimization and simulation for the new power systems paradigm. Complexity, 2018, 2018. doi: 10.1155/2018/2340628.

- Harp et al. [2000] Steven A Harp, Sergio Brignone, Bruce F Wollenberg, and Tariq Samad. SEPIA. a simulator for electric power industry agents. IEEE Control Systems Magazine, 20(4):53–69, 2000. doi: 10.1109/37.856179.

- Zimmerman and Thomas [2004] Ray D Zimmerman and Robert J Thomas. Powerweb: A tool for evaluating economic and reliability impacts of electric power market designs. In IEEE PES Power Systems Conference and Exposition, 2004., pages 1562–1567. IEEE, 2004. doi: 10.1109/PSCE.2004.1397612.

- Migliavacca [2007] G Migliavacca. SREMS: a short-medium run electricity market simulator based on game theory and incorporating network constraints. In 2007 IEEE Lausanne Power Tech, pages 813–818. IEEE, 2007. doi: 10.1109/PCT.2007.4538420.

- North et al. [2003] M North, P Thimmapuram, R Cirillo, C Macal, G Conzelmann, G Boyd, V Koritarov, and T Veselka. EMCAS: An agent-based tool for modeling electricity markets. In 2003 Agent Conference on Challenges in Social Simulation, page 253, 2003.

- Li and Tesfatsion [2009] Hongyan Li and Leigh Tesfatsion. The ames wholesale power market test bed: A computational laboratory for research, teaching, and training. In 2009 IEEE Power & Energy Society General Meeting, pages 1–8. IEEE, 2009. doi: 10.1109/PES.2009.5275969.

- Connolly et al. [2013] David Connolly, Henrik Lund, Brian Vad Mathiesen, Poul Alberg Østergaard, Bernd Möller, Steffen Nielsen, Iva Ridjan, Frede Hvelplund, Karl Sperling, Peter Karnøe, et al. Smart energy systems: holistic and integrated energy systems for the era of 100% renewable energy. 2013.

- Vale et al. [2011] Zita Vale, Tiago Pinto, Isabel Praca, and Hugo Morais. Mascem: electricity markets simulation with strategic agents. IEEE Intelligent Systems, 26(2):9–17, 2011. doi: 10.1109/MIS.2011.3.

- Pinto et al. [2012] Tiago Pinto, Tiago M Sousa, Zita Vale, Isabel Praça, and Hugo Morais. Metalearning in ALBidS: a strategic bidding system for electricity markets. In Highlights on Practical Applications of Agents and Multi-Agent Systems, pages 247–256. Springer, 2012. doi: 10.1007/978-3-642-28762-6˙30.

- Ringkjøb et al. [2018] Hans-Kristian Ringkjøb, Peter M Haugan, and Ida Marie Solbrekke. A review of modelling tools for energy and electricity systems with large shares of variable renewables. Renewable and Sustainable Energy Reviews, 96:440–459, 2018. doi: 10.1016/j.rser.2018.08.002.

- Berkeley Lab [2016] Berkeley Lab. Distributed energy resources customer adoption model plus (DER-CAM+) 2016-075. https://ipo.lbl.gov/lbnl2016-075/, 2016. Accessed: 2019-06-03.

- Zhou et al. [2007] Zhi Zhou, Wai Kin Victor Chan, and Joe H Chow. Agent-based simulation of electricity markets: a survey of tools. Artificial Intelligence Review, 28(4):305–342, 2007. doi: 10.1007/s10462-009-9105-x.