Predictive Risk Analysis in Collective Risk Model: Choices between Historical Frequency and Aggregate Severity

Abstract

Typical risk classification procedure in insurance is consists of a priori risk classification determined by observable risk characteristics, and a posteriori risk classification where the premium is adjusted to reflect the policyholder’s claim history. While using the full claim history data is optimal in a posteriori risk classification procedure, i.e. giving premium estimators with the minimal variances, some insurance sectors, however, only use partial information of the claim history for determining the appropriate premium to charge. Classical examples include that auto insurances premium are determined by the claim frequency data and workers’ compensation insurances are based on the aggregate severity. The motivation for such practice is to have a simplified and efficient posteriori risk classification procedure which is customized to the involved insurance policy. This paper compares the relative efficiency of the two simplified posteriori risk classifications, i.e. based on frequency versus severity, and provides the mathematical framework to assist practitioners in choosing the most appropriate practice.

Keywords: Collective Risk Model, Bühlmann Premium, Predictive Analysis, Posteriori Risk Classification, Premium

1 Introduction

Determination of the premiums is a major and interesting problem in Actuarial science. Fair insurance premiums are established via risk classification procedures, which involve the grouping of risks into various classes that share a homogeneous set of characteristics allowing the actuary to reasonably price discriminated. This paper examines the statistical properties of the Collective Risk Model(CRM) for the application in risk classification procedures. The CRM (Klugman et al., 2012) is, defined as the random sum, , of claim severities,

where an independence assumption is made between the frequency, , and individual severities, ’s. Due to the mathematical elegance and relative robustness of the model, such independence assumption is widely applied by the insurance industry for modeling the aggregate claim experience of their portfolios over a fixed time horizon in pricing and reserving exercises. However, in empirical studies such as (Gschlößl and Czado, 2007), the number and the size of claims are significantly dependent. Extending from is its original form, there are various dependence structured studied to better capture the stochastic nature of the insurance portfolio.

Generally speaking, there are two ways of describing CRM. The first method is the two-part approach where the frequency and the severity part are described separately, and then their joint distribution is described statistically via random effects (Hernández-Bastida et al., 2009; Baumgartner et al., 2015; Lu, 2016; Oh et al., 2019b), copula specifications (Czado et al., 2012; Krämer et al., 2013; Frees et al., 2016b; Cossette et al., 2019; Oh et al., 2019a), hierarchical structures (Shi et al., 2015; Garrido et al., 2016; Park et al., 2018; Jeong et al., 2019) or the dependence specification between the inter-arrival time and the severity (Albrecher and Teugels, 2006; Boudreault et al., 2006; Cheung et al., 2010). Alternatively, the direct approach models the distribution of aggregate severity, , directly. The most frequently used distribution for the aggregate severity in the insurance literature is the Tweedie distribution (Tweedie, 1984). To reflect the skewness and the heavy tails of the loss, (McDonald, 2008) introduced the generalized beta distribution of the second kind for the modeling of the aggregate severity.

In this paper, we address the problem of risk classification procedure in predicting the mean of aggregate severity, , based on a set of information. Usually, it involves first classifying risks based on a priori risk classification procedure involving a priori risk characteristics, i.e. risk characteristics of each policyholder at the moment of contract. It forms the basis for premium settings when a policyholder is new and insufficient information may be available. After a priori risk classification, the policyholder is further classified based on the claim history of each policyholder. This secondary classification is called a posteriori risk classification. In effect, the resulting a posteriori premium allows one to correct and adjust the previous a priori premium making the price discrimination even fairer and more reasonable.

While full information which consists of claim history of frequency and severities is guaranteed to give the best posteriori prediction, we are mainly interested in comparison of two simpler versions of the posteriori risk classification methods

-

•

one based on the historical frequency information only,

-

•

one based on the historical aggregate severity information only,

under the general dependence structure in frequencies and severities. Such simplified a posteriori risk classification is common, and the type of a posteriori risk classification depends on the characteristics of insurance to facilitate efficient communication with the policyholder while keeping the reasonable efficiency of a posteriori risk classification. For example, auto insurance prefers to use the former type while the workers’ compensation insurance generally adapts the latter.

For the fair comparison of two a posteriori risk classification methods, we need a CRM which can accommodate both a posteriori risk classification methods. Since the historical frequency information cannot be used in the direct approach, we use two-part approaches where both a posteriori classification methods are possible. In particular, we use the two-step frequency-severity model in Jeong et al. (2019) where the analytical comparison between two posteriori risk classifications is possible.

The actuarial credibility theory is designed for a posteriori rating system that takes into account the history of claims as it emerges. We construct and compare the quality of two simplified posteriori classification methods, i.e. by conditioning on the aggregate claim history and the claim frequency history respectively, via the Bühlmann estimators (Bühlmann and Gisler, 2006), i.e. a linear version of a posteriori mean. Bühlmann estimators of premium based on the history of frequency as well as severity are first considered in Hewitt (1970) and further studied in Frees (2003) and Goulet et al. (2006). While those studies assumed independence between the frequency and the severity, we develop Bühlmann premiums based on the historical frequency information as well as Bühlmann premiums based on the historical aggregate severity information claim frequency under the dependence assumption between the frequency and the severity. Furthermore, we derive the Mean square errors (MSE) of the Bühlmann premiums, which facilities the analysis and comparison of the quality of two premiums. Our, non-technical, yet equally important contribution to the insurance society is that, with such analytical tools and related numerical study, we are the first to provide a practical guideline for choosing the appropriate posteriori risk classification method.

In the numerical study, we compare the quality of two Bühlmann premiums under various scenarios, which hopefully provide the practical guideline about the choice of premium method between the historical frequency information and the historical aggregate severity information. In general, Bühlmann premiums based on the historical aggregate severity information have a tendency to outperform Bühlmann premiums based on the historical frequency information when there is a strong dependence among individual severities, and vice versa. Yet, the preferable method also dynamically changes over time as the number of observations increases. Hence, there is no simple rule-of-thumb in deciding the appropriate information set, but to make cases by case analysis.

We apply our analysis to a practical application with real data obtained from the auto insurance of the Wisconsin Local Government Property Insurance Fund (LGPIF) as in Frees et al. (2016a). First, the comparison of two Bühlmann premiums via numerical procedure indicates relatively stronger dependence among severities, which in turn recommends the prediction based on the historical aggregate severity information rather than the prediction based on the historical frequency information. We confirm that the historical aggregate severity information has more predictive power in this particular example via out-of-sample validation.

The rest of the paper is organised as follows. In Section 2, we fix the notations and the model for our analysis, as well as present a motivating problem. Section 3 contains the derivation of the two Bühlmann premiums. In Section 4, we study the criteria for choosing appropriate models for premium settings. An application to the auto insurance of the Wisconsin Local Government Property Insurance Fund is presented in Section 5.

2 Problem Formulation

2.1 Notations

We consider a portfolio of policyholders in the context of short-term insurance, where a policyholder could decide whether or not to renew the policy at the end of each policy year and the insurer can adjust the premium at the beginning of each policy year based on the policyholder’s claim experience. We denote , , , and by the set of natural numbers, the set of non-negative integers, the set of real numbers, and the set of positive real numbers, respectively. We consider a set of discrete-time stochastic processes that the associated data is collected over time that

-

•

denotes the claim count at time and denotes the natural filtration generated by ,

-

•

denote the size of the th claim and

denote the vector of claim sizes observed at time ,

-

•

denotes the natural filtration generated by and , i.e. the information of the full claim history

-

•

denotes the aggregate claim at time and denotes the natural filtration generated by ,

-

•

denotes the average claim amount at time .

We use lower case letters to denotes the realisation of these random variables. The actuarial science literature often refers to as the frequency, as the individual severity, and as the average severity of the insurance claims. We emphasize that our proposed method requires only information on the average severity, and imposes no constraints on individual severity. In the following text, we refer to the model for as the frequency-severity model.

In the risk classification, premiums are determined by a set of risk characteristics. Let and denote, respectively, the observed and unobserved risk characteristics, and the superscripts [1] and [2] are indices for the frequency and the severity components, respectively. For convenience, we call the observed risk characteristics as a priori risk characteristics. Note that , and do not have the subscript , as we assume that they are constant in time. The marginal distributions of the residual effect characteristics are given by and , respectively, for the proper distribution functions and . We use and to denote the density version of and , respectively. Furthermore, denote

where is called as the risk characteristics.

2.2 The Motivating problem

Predictions of can be made based on different information sets, i.e.

| (1) |

| (2) |

| (3) |

By definition, all three predictors are unbiased estimators of the premium, and it is obvious that the quality of the predictor in Equation (1) is the best among three in the sense

which follows from the set inclusions

In the comparison of the quality of two predictors in Equation (2) and (3), the statement that Equation (3) is superior in the sense

does not hold in general. The main focus of this paper is to compare these two approaches of setting premiums and set out guidelines in choosing the appropriate when in practice.

2.3 Model Assumption on Dependent Collective Risk Models

To model the frequency and the severity of insurance claims, we follow De Jong et al. (2008) and use generalized linear models (GLMs). Specifically, we consider the exponential dispersion family (EDF) in McCullagh and Nelder (1989). Now we are ready to present the collective risk model equipped with various dependence structures.

Model 1.

(Jeong et al., 2019) Suppose the insurer predetermines risk classes based on the policyholders’ risk characteristics. Let define the a priori risk characteristics of the -th risk class, and be the weight of the risk class:

Denote as the a priori premium for the given policyholder, which is determined by the observed risks characteristics as follows:

| (4) |

where and are link functions, and and are parameters to be estimated. We also assume that and are independent. For the easiness of the analysis, we assume that priori risk characteristics are fixed across time . Assume that and ’s are independent conditional on the risk characteristics .

-

•

The frequency is specified using a count regression model conditioning on the risk characteristics

for where the distribution has the mean and the dispersion parameter .

-

•

The individual severity is specified using a regression model conditioning on the risk characteristics, and the frequency

(5) where the distribution has the mean with

and the dispersion parameter .

For the brevity of the notation, we only use log-link function for such that

where

To further simplify the analysis in the later sections, we shall assume the following parametric model.

Model 2 (Parametric Model).

Assume the settings in Model 1 with the following parametric assumptions:

-

1.

For the frequency, assume that

-

2.

For the individual severity, assume that

(6) -

3.

For the random effect, assume that

and

We provide the mean, variance and covariance formulae for the statistics of Model 2 in Proposition 5 (see Appendix). It is often the case that using the individual severity in (6) is inconvenient for estimation purposes, yet insurance literature often provides the distributional assumption for the average severity (Shi et al., 2015). The following corollary provides the equivalence of two representations based on the individual severity and the average severity in the case of gamma distributional assumption. The same result for EDF distribution can be found in Lemma 1 (see Appendix).

Corollary 1.

Proof.

The proof is an immediate result of Lemma 1. ∎

Finally, for the brevity of the paper, define the following symbols under the settings in Model 2.

Definition 1.

Under the settings in Model 2, define

For the brevity of the paper, we also abuse symbols , , and as follows in a clear context. Under the settings in Model 2, we use , , and to stand for , , and , respectively, in a clear context. For example, we have the following two expressions are equivalent

3 Two Bühlmann Premiums in Dependent CRM

With the introduction of more complicated and dynamic insurance products, a major challenge of the actuarial profession can be found in the measurement and construction of a fair insurance premium. Pricing risks based upon certain specific characteristics has a long history in actuarial science. In light of the heterogeneity within an insurance portfolio, an insurance company should not apply the same premium for its policyholders, but group the risks in the portfolio so that people with similar risk profiles pay the same reasonable premium rate. To reflect the various risk profiles in a portfolio within a statistically sound basis, the standard technique that actuaries use is a regression-based approach. The standard GLM type structure as in Equation (4) gives a natural candidate for the a priori risk classification.

Based on such a priori risk classification, this section considers two different type of premiums under the dependent assumption between frequency and severity. The first premium is a classical method where the historical aggregate severity information is used to predict the aggregate severity in the future. The second premium that we are proposing is a non-traditional approach in that the historical frequency information is used to predict the aggregate severity in the future. For the analytical of comparison of two methods, we consider Bühlmann premiums rather using the exact posteriori mean of the aggregate severity as a posteriori premiums. Note that Bühlmann premiums can deal with both approaches as long as one can calculate the covariance matrix of the observations and premium (Hewitt, 1970).

3.1 Bühlmann Premiums based on the Historical Aggregate Severity Information

Under Model 2, our goal in this subsection is to find the Bühlmann premium based on the historical aggregate severity.

Definition 2.

The Bühlmann premium based on the historical aggregate severity information is

where

For the known random effect and a priori rate , the conditional mean can be obtained as follow.

Proposition 1.

Under Model 2, for the known random effect and a priori rate , we have

Proof.

where the last equality comes from Lemma 2 in Appendix. ∎

Note that the Bühlmann premium in (2) can be regarded as the best linear unbiased estimator (BLUE) of the conditional mean . By the classical procedure in Bühlmann and Gisler (2006), one can easily show that

| (7) |

where Bühlmann factor is given by

The following result provides the analytical expression of premium in (2).

Proposition 2.

and

Proof.

3.2 Bühlmann Premiums based on the Historical Frequency Information

Similar to the previous subsection, our goal in this subsection is to derive the Bühlmann premium based on claim frequencies. The followings

| (9) |

are the Bühlmann observation, that are functions of the historical frequency and priori characteristics, are used as if they are observations in the determination of the Bühlmann premiums, and we shall denote

In Model 2, the statistics in (9) can be analytically expressed as follows.

Proof.

Based on the law of total expectation, we have

∎

Definition 3.

The Bühlmann premium based on the historical frequency information is defined as

where

Similar to Bühlmann type premium in (2), the classical procedure in Bühlmann and Gisler (2006) shows that

| (10) |

where the Bühlmann factor is

The following result provides the analytical expression of premium in (3).

Proposition 4.

and

Proof.

3.3 Linkage with Bühlmann Premium for the Frequency

This section assumes the independence between frequency and individual severities by assuming in Model 2. From the assumption in Model 2, we have the following intuitive interpretation about the Bühlmann observation and Bühlmann premium based on the historical frequency information

and

| (12) |

where

with

Note that the expression

in (12) coincides with the Bühlmann premium of frequency defined by

| (13) |

where

4 Numerical comparisons of the two Bühlmann premiums

The aggregate claim amount is the key element for an insurer’s balance sheet, as it represents the amount of money paid on claims, hence they must understand the dynamics of the aggregate claim overtime. Yet, depending on features of contracts as well as policyholder behaviour and risk mitigation practices, some insurance products use only partial information on the claim history for the posteriori risk classification, i.e. the frequency of claims or the aggregate claim amounts, but not both. We conduct a numerical study to investigate the effect of various dependence structures in Model 2 on the two proposed Bühlmann premiums, and in Section 3 that based on the frequency and the aggregate claim respectively. The following analysis forms the basis of choosing the appropriate pricing and risk mitigation practices for standard general insurance portfolios.

4.1 Numerical Set-up

We assume only one priori risk class for the simplicity of the analysis and the following parametric assumption for the unobserved heterogeneities

where IG is inverse Gaussian distribution. In particular, we set

with and . The parameters varies in 27 scenarios that different dependence structure is considered. Note here, controls the dependence between the frequency and severity whereas and controls the correlation among the frequencies and severities over time, respectively. For each scenario with the combination of parameters , we choose

so that is fixed.

4.2 The Case of Independent between frequency and individual severities

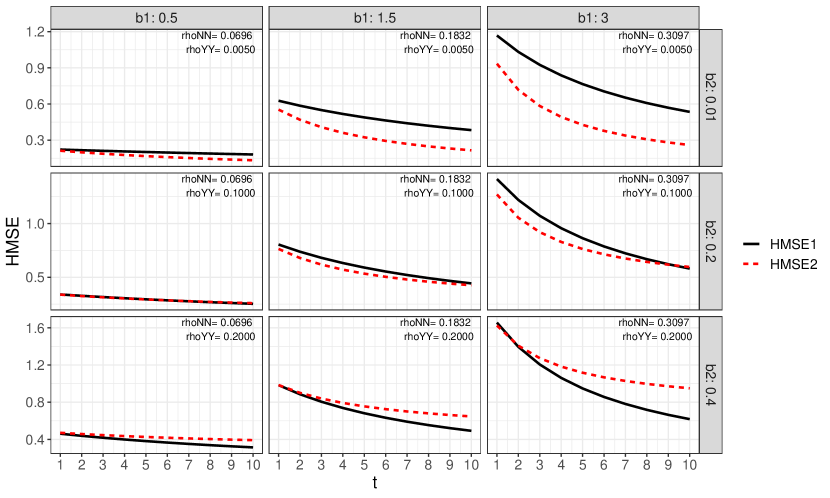

First, we consider an independence between the frequency and individual severities, i.e. , while and is allowed to vary in nine scenarios that different correlations are implied among the frequencies and the individual severities, respectively. The comparison of MSEs is in Figure 1.

Theoretically, when there is a relatively weak dependence among individual severities while a relatively strong dependence among frequencies, , we expect that the claim history of frequency has the most predictive power for the premium, while the additional information on the severities provides little benefit. Especially, in the the extreme case of and , is the only valid information for predicting premiums, the prediction suffers from the loss of information. This is demonstrated by the following comparison of premiums

and

where the equalities in both of expressions are from the assumption . Together with

it implies that

if Bühlmann premiums are not very different from posteriori mean of the aggregate severity. As shown in Figure 1, for the case where , outperforms consistently over time while the absolute values of HMSEs increase as the variance of increases.

On the other hand, when there is a relatively strong dependence among individual severities while relatively weak dependences among frequencies , we expect, in theory, that only the historical aggregate severity information provides meaningful information in the prediction of premium. Especially in the extreme case and , does not provide any information for the prediction of premium, while can provide some information for the prediction. Such a difference can be explained by the fact that the equations

and

together with the inequality

implies that

if Bühlmann premiums are not very different from posteriori mean of the aggregate severity. Indeed as shown in Figure 1, for the cases , outperforms consistently over time.

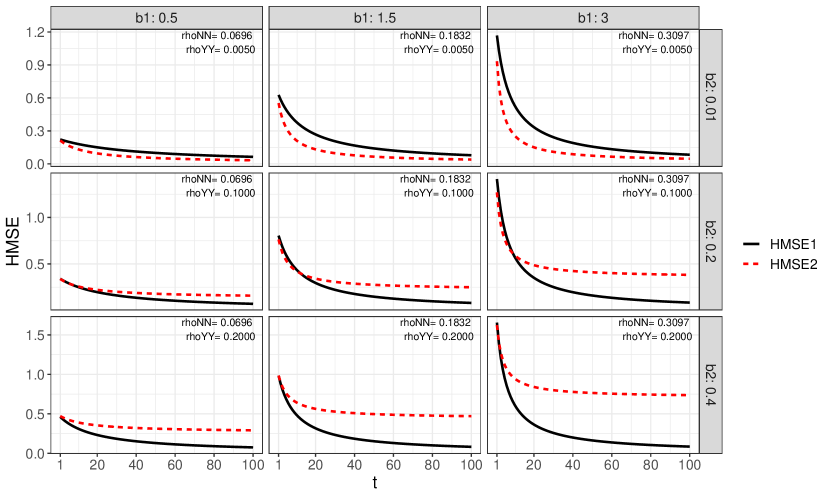

Another interesting point is the asymptotic behaviour of and for larger as seen in Figure 2. First, converges to zero as increases. Such a convergence is an expected result because of the convergence of in (8). On the other hand, the convergence of to zero is not guaranteed. This is also expected as the convergence of

is not guaranteed in general. Instead,

converges to

which further implies the convergence of the Bühlmann premium in (12) to

as the number of observations, , increases. Hence, in such case can be written as

where the equality holds if .

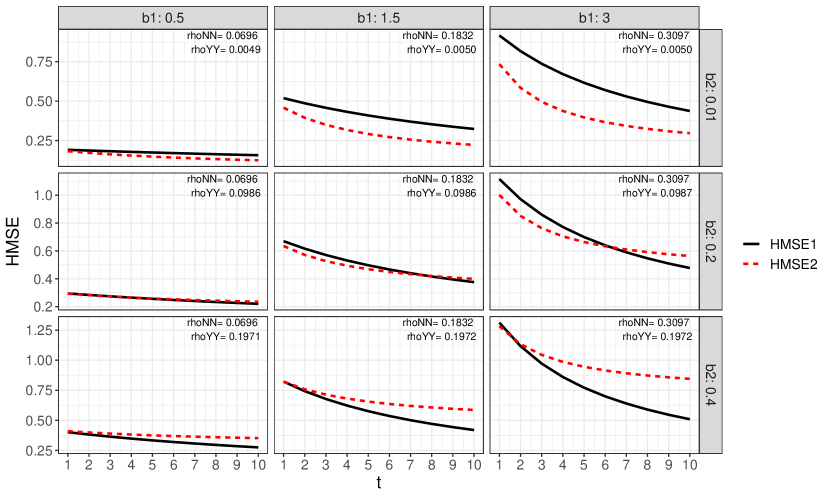

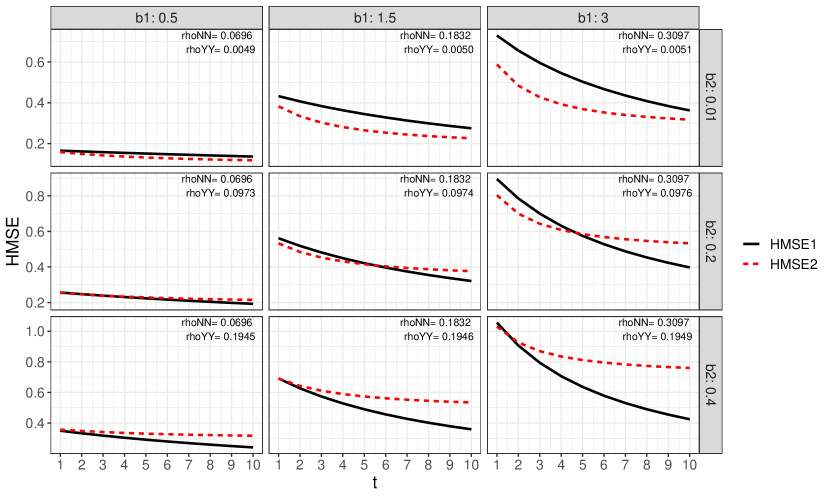

4.3 The Case of dependent between frequency and individual severities

Here, we consider the case where both the frequency and individual severities are dependent, which is the case . Motivated by the real data analysis in Section 5, a moderate dependence with and a relatively strong dependence with are assumed in Figures 3 and 4 respectively. The overall patterns are similar to the independent case that while a relatively weak dependence among individual severities is combined with a relatively strong dependence among frequencies, the historical frequency information has the most predictive power for the premium, and vice versa.

Specific results for HMSE are summarized in Table 1.

| 0.5 | 1.5 | 3 | ||||||||||||||||||

| t | 1 | 5 | 10 | 1 | 5 | 10 | 1 | 5 | 10 | |||||||||||

| 0 | 0.01 | 0.1652 | 0.1509 | 0.1363 | 0.4325 | 0.3446 | 0.2748 | 0.7298 | 0.5031 | 0.3624 | ||||||||||

| 0.1579 | 0.1316 | 0.1180 | 0.3821 | 0.2650 | 0.2260 | 0.5878 | 0.3690 | 0.3171 | ||||||||||||

| 0.2 | 0.2565 | 0.2237 | 0.1928 | 0.5615 | 0.4214 | 0.3212 | 0.8941 | 0.5749 | 0.3975 | |||||||||||

| 0.2551 | 0.2288 | 0.2151 | 0.5326 | 0.4154 | 0.3764 | 0.8036 | 0.5848 | 0.5329 | ||||||||||||

| 0.4 | 0.3500 | 0.2915 | 0.2411 | 0.6916 | 0.4900 | 0.3592 | 1.0565 | 0.6364 | 0.4251 | |||||||||||

| 0.3573 | 0.3310 | 0.3173 | 0.6910 | 0.5738 | 0.5348 | 1.0307 | 0.8119 | 0.7601 | ||||||||||||

| -0.05 | 0.01 | 0.1913 | 0.1744 | 0.1570 | 0.5190 | 0.4092 | 0.3236 | 0.9161 | 0.6164 | 0.4376 | ||||||||||

| 0.1829 | 0.1482 | 0.1250 | 0.4580 | 0.2918 | 0.2224 | 0.7345 | 0.3967 | 0.2964 | ||||||||||||

| 0.2 | 0.2951 | 0.2566 | 0.2206 | 0.6699 | 0.4973 | 0.3762 | 1.1156 | 0.6999 | 0.4775 | |||||||||||

| 0.2935 | 0.2587 | 0.2356 | 0.6353 | 0.4691 | 0.3997 | 1.0017 | 0.6639 | 0.5637 | ||||||||||||

| 0.4 | 0.4014 | 0.3333 | 0.2750 | 0.8220 | 0.5761 | 0.4193 | 1.3125 | 0.7716 | 0.5092 | |||||||||||

| 0.4098 | 0.3751 | 0.3520 | 0.8219 | 0.6557 | 0.5863 | 1.2831 | 0.9453 | 0.8450 | ||||||||||||

| -0.1 | 0.01 | 0.2221 | 0.2019 | 0.1813 | 0.6270 | 0.4888 | 0.3833 | 1.1679 | 0.7651 | 0.5346 | ||||||||||

| 0.2125 | 0.1676 | 0.1332 | 0.5531 | 0.3238 | 0.2157 | 0.9339 | 0.4269 | 0.2596 | ||||||||||||

| 0.2 | 0.3404 | 0.2951 | 0.2530 | 0.8046 | 0.5905 | 0.4431 | 1.4134 | 0.8633 | 0.5808 | |||||||||||

| 0.3385 | 0.2937 | 0.2593 | 0.7632 | 0.5340 | 0.4258 | 1.2701 | 0.7631 | 0.5958 | ||||||||||||

| 0.4 | 0.4614 | 0.3819 | 0.3143 | 0.9835 | 0.6814 | 0.4924 | 1.6554 | 0.9480 | 0.6179 | |||||||||||

| 0.4713 | 0.4265 | 0.3920 | 0.9844 | 0.7552 | 0.6470 | 1.6240 | 1.1171 | 0.9497 | ||||||||||||

In conclusion, we construct the following guidelines for practitioners in choosing the appropriate posteriori risk classification approach

-

1.

choose when there is a stronger dependence among individual severities than that among frequencies

-

2.

choose when there is a stronger dependence among individual frequencies than that among individual severities

-

3.

the choice needs to be made dynamically over time as and

5 Application to Auto Insurance in Wisconsin Local Government Property Insurance Fund

We illustrate our approach using data from the Wisconsin Local Government Property Insurance Fund as in Frees et al. (2016a). This fund offers insurance protection for (i) property; (ii) motor vehicle; and (iii) contractors’ equipment claims. Detailed information on the project is available on the LGPIF project website. The LGPIF provides property insurance for various governmental entities, including counties, cities, towns, villages, school districts, fire departments, and other miscellaneous entities. Collision coverage provides coverage for the impact of a vehicle with an object, the impact of a vehicle with an attached vehicle, or the overturn of a vehicle.

5.1 Empirical Specification

For the training sample data, we have used the longitudinal data from 1,234 local government entities cover from 2006 to 2010. We also have hold-out sample data with 1098 observations from 379 local government entities in the year of 2011. We removed the observations for policyholders whose new collision coverage and old collision coverage are zero. Hence, we use longitudinal data from 497 governmental entities in our data analysis.111We adjust the values of the individual severity in the training sample data so that the average individual severity in each year coincides with the average individual severity in the year of 2011. We have two categorical variables:

-

1.

the entity type with six levels, miscellaneous, city, county, school, town and village, and average,

-

2.

the coverage with three levels, coverage 1 , coverage 2 , and coverage 3 .

Under the settings in Model 2, we further assume

so that

5.2 Estimation via Bayesian MCMC

Our model specification in Section 2.3 is in the form of multivariate nonlinear time-series with random effects, that its estimation can be problematic in practice. Bayesian Econometric methods (Koop (2003)) have made its popularity over the last decade for its theoretical novelty and empirical performance, especially for its application in economics and finance. The application to the Actuarial research community has flourished over the last decades (see Klugman (2013) and Makov et al. (1996)) due to its intrinsic compatibility with Actuarial credibility theory.

To estimate the model under the Bayesian framework, we assume multivariate Gaussian priors for the regression coefficients, i.e.

and assume conjugate prior structure for

where are the prior hyper-parameters. Note that is inverse gamma distribution with shape parameter and scale parameter .

Due to the relatively complicated hierarchical structure, the posterior distribution of the model parameters is not analytically feasible. We reply to Markov Chain Monte-Carlo(MCMC) methods for obtaining empirical estimates of the posterior statistics. The conjugate prior specification gives known conditional likelihood that a simple Gibbs sampler is used for estimating the parameters, and , and a Metropolis-Hasting with random walk proposal is used for estimating the coefficients. A more realistic prior structure can be assumed, yet it implies a more computationally intensive MCMC algorithm and possibly poor mixing. Hence, we alleviate this from the current analysis. For running MCMC, we use a software, JAGS (Plummer et al., 2003), that is a program for analysis of Bayesian hierarchical models using MCMC. We have run 30,000 MCMC iterations saving every 5th sample after burn-in of 20,000 iterations. Multiple parallel MCMC chains are run to cross-validate the convergence of the results.

Summary statistics of the posterior samples for the parameters in Model 2 using the Bayesian approach are presented in Table 4 in Appendix C: Tables. The table includes the posterior median (EST), the posterior standard deviation (Std.dev), and the 95% highest posterior density Bayesian credible interval (95 CI). Note that a sign indicates the parameters whose 95 CI does not contain zero.

| t | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 199.46 | 129.83 | 96.92 | 77.60 | 64.83 | 55.74 | 48.92 | 43.62 | 39.37 | 35.88 | ||

| 229.21 | 189.60 | 173.06 | 163.93 | 158.11 | 154.07 | 151.10 | 148.83 | 147.03 | 145.57 |

Figure 5 shows the comparison of the HMSE’s of two Bühlmann premiums, and in Section 3. The results are also summarized in Table 2. In terms of HMSE, Bühlmann premium outperforms Bühlmann premium regardless of the number of observations, while their gap becomes larger as the number of observations increases. Moreover, while the HMSE of Bühlmann premium asymptotically converges to zero, the HMSE of Bühlmann premium converges to a non-zero constant. In conclusion, it is recommended to use aggregate severity in the posteriori risk classification rather than using the frequency. out-of-sample validation results in Table 3 show that outperforms consistently.

| t | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 161.73 | 176.00 | 202.48 | 188.08 | 189.53 | |

| 173.39 | 172.40 | 195.27 | 192.89 | 196.74 |

6 Remark on the Statistical Modelling of Collective Risk Model

As briefly discussed in introduction, there are two ways of describing the CRM, i.e. the two-part model and the direct model, discussed in this paper. While the latter demonstrate robust prediction of the mean regardless of the parametric distribution used, however, the use of the partial information on aggregate severity can be insufficient in the estimation procedure and predictive analysis. On the other hand, the two-part model is sensitive to the model specification meaning that its prediction ability is not guaranteed under the model misspecification. Yet, when the model assumption is appropriate, it shows better performance in the prediction of aggregate severity compared to the direct model since it uses the full information on both the historical frequency and severities. As we have shown in Section 4, using the historical aggregate severity information can damage the prediction especially when the dependence among individual severities is not so significant. Hence, our general suggestion for the use of the direct approach is only for cases where there is a relatively strong dependence among individual severities assuming no non-statistical preferences.

Acknowledgements

Jae Youn Ahn was supported by a National Research Foundation of Korea (NRF) grant funded by the Korean Government (NRF-2017R1D1A1B03032318). Rosy Oh was supported by Basic Science Research Program through the National Research Foundation of Korea(NRF) funded by the Ministry of Education (Grant No. 2019R1A6A1A11051177).

Appendix A: Important Lemmas

Lemma 1.

Consider the settings in Model 1, and let the conditional distribution of a random variable be given by

| (15) |

for , and

for based on the same EDF in (5). Then, we have the distributional assumption on in (5) and the distribution assumption on in (15) are equivalent if the index set of the exponential dispersion family in (5) is .

Proof.

First, note that the members of the model are infinitely divisible if and only if the index set (Jorgensen, 1997). Then, the proof follows from the reproductive property of EDF and the infinitely divisible property of EDF. ∎

Lemma 2.

Under the settings in Model 2, we have the moment generating function of is given by

| (16) |

Furthermore, we have

and

Proof.

Lemma 3.

Under the settings in Model 2, if we assume that

we have the moment generating function of is given by

| (17) | ||||

Furthermore, we also have

and

Proof.

Lemma 4.

Proof.

Lemma 5.

Proof.

Then, following the procedure in Bühlmann premium, under Model 2, we have the conditional mean and the Bühlmann factor, , can be expressed as

Similarly, the conditional mean and Bühlmann factor can be expressed as

Appendix B: Auxiliary Results for the numerical illustration

In the following proposition, we provide the analytical expressions of useful statistics in Model 2. Note that the conditional expressions are of primary interest to insurers because a priori information is usually available at the time of the contract.

First, we provide the auxiliary lemma which is necessary for Proposition 5 and the calculation of MSE.

Proof.

Proposition 5.

Under Model 2, we have the following conditional expressions.

-

1.

The mean and variance of the aggregate severity are

and

(18) -

2.

The covariance of aggregate severities is

for .

-

3.

The covariance among the frequencies is

for .

-

4.

The variance of the individual severities is

-

5.

The covariances among the individual severities are

and, for ,

-

6.

The covariances among the individual severities are

and, for ,

Proof.

Assume Model 2 and use conditional expectation, covariance, and variance. Then, the mean and variance of the aggregate severity conditional on the priori premium are calculated as

where the second equality comes from Proposition 1, and

where the second last equality comes from Lemma 6, respectively.

The covariance of aggregate severities conditional on the priori premium for is

where the second last equality comes from Lemma 6.

The covariance among the frequencies conditional on the priori premium for is

Note that the all last equalities of following proofs comes from Lemma 6. The variance of the individual severities conditional on the priori premium is

The covariances among the individual severities conditional on the priori premium are

and, for ,

The covariances among the individual severities conditional on the priori premium are

and, for ,

∎

Finally, we provide the MSE formulas for two Bühlmann methods in Section 3.

Proposition 6.

Proof.

First, can be expressed as

| (19) | ||||

where the second equality is just expansion of the square expression. Finally, (19) and the following equalities

and

conclude the proof of the first part.

Appendix C: Tables

| 95 CI | ||||||||||||

| parameter | Est | Std.dev | lower | upper | ||||||||

| Frequency part | ||||||||||||

| Intercept | -1.884 | 0.292 | -2.442 | -1.294 | * | |||||||

| City | 0.002 | 0.324 | -0.636 | 0.634 | ||||||||

| County | 1.279 | 0.317 | 0.644 | 1.883 | * | |||||||

| School | -0.289 | 0.280 | -0.819 | 0.271 | ||||||||

| Town | -2.038 | 0.365 | -2.737 | -1.312 | * | |||||||

| Village | -0.701 | 0.307 | -1.291 | -0.101 | * | |||||||

| Coverage2 | 1.009 | 0.211 | 0.602 | 1.430 | * | |||||||

| Coverage3 | 1.898 | 0.223 | 1.464 | 2.328 | * | |||||||

| Severity part | ||||||||||||

| Intercept | 8.394 | 0.366 | 7.712 | 9.140 | * | |||||||

| City | -0.034 | 0.345 | -0.726 | 0.616 | ||||||||

| County | 0.527 | 0.333 | -0.126 | 1.169 | ||||||||

| School | -0.130 | 0.325 | -0.748 | 0.532 | ||||||||

| Town | 0.497 | 0.434 | -0.362 | 1.342 | ||||||||

| Village | 0.291 | 0.340 | -0.364 | 0.974 | ||||||||

| Coverage2 | 0.189 | 0.233 | -0.281 | 0.625 | ||||||||

| Coverage3 | 0.048 | 0.250 | -0.451 | 0.525 | ||||||||

| 1.478 | 0.091 | 1.309 | 1.664 | * | ||||||||

| -0.034 | 0.013 | -0.058 | -0.009 | * | ||||||||

| Random effect part | ||||||||||||

| 1.563 | 0.297 | 1.066 | 2.199 | * | ||||||||

| 0.222 | 0.049 | 0.129 | 0.320 | * | ||||||||

References

- Albrecher and Teugels [2006] Hansjörg Albrecher and Jef L Teugels. Exponential behavior in the presence of dependence in risk theory. Journal of Applied Probability, 43(1):257–273, 2006.

- Baumgartner et al. [2015] Carolin Baumgartner, Lutz F Gruber, and Claudia Czado. Bayesian total loss estimation using shared random effects. Insurance: Mathematics and Economics, 62:194–201, 2015.

- Boudreault et al. [2006] Mathieu Boudreault, Helene Cossette, David Landriault, and Etienne Marceau. On a risk model with dependence between interclaim arrivals and claim sizes. Scandinavian Actuarial Journal, 2006(5):265–285, 2006.

- Bühlmann and Gisler [2006] Hans Bühlmann and Alois Gisler. A course in credibility theory and its applications. Springer Science & Business Media, 2006.

- Cheung et al. [2010] Eric CK Cheung, David Landriault, Gordon E Willmot, and Jae-Kyung Woo. Structural properties of gerber–shiu functions in dependent sparre andersen models. Insurance: Mathematics and Economics, 46(1):117–126, 2010.

- Cossette et al. [2019] Hélène Cossette, Etienne Marceau, and Itre Mtalai. Collective risk models with dependence. Insurance: Mathematics and Economics, 87:153–168, 2019.

- Czado et al. [2012] Claudia Czado, Rainer Kastenmeier, Eike Christian Brechmann, and Aleksey Min. A mixed copula model for insurance claims and claim sizes. Scandinavian Actuarial Journal, 2012(4):278–305, 2012.

- De Jong et al. [2008] Piet De Jong, Gillian Z Heller, et al. Generalized Linear Models for Insurance Data. Cambridge Books, 2008.

- Frees [2003] Edward W Frees. Multivariate credibility for aggregate loss models. North American Actuarial Journal, 7(1):13–37, 2003.

- Frees et al. [2016a] Edward W Frees, Gee Lee, and Lu Yang. Multivariate frequency-severity regression models in insurance. Risks, 4(1):4, 2016a.

- Frees et al. [2016b] Edward W Frees, Gee Lee, and Lu Yang. Multivariate frequency-severity regression models in insurance. Risks, 4(1):4, 2016b.

- Garrido et al. [2016] José Garrido, Christian Genest, and Juliana Schulz. Generalized linear models for dependent frequency and severity of insurance claims. Insurance: Mathematics and Economics, 70:205–215, 2016.

- Goulet et al. [2006] Vincent Goulet, Antoni Forgues, and Jiatao Lu. Credibility for severity revisited. North American Actuarial Journal, 10(1):49–62, 2006.

- Gschlößl and Czado [2007] Susanne Gschlößl and Claudia Czado. Spatial modelling of claim frequency and claim size in non-life insurance. Scandinavian Actuarial Journal, 2007(3):202–225, 2007.

- Hernández-Bastida et al. [2009] A. Hernández-Bastida, M. P. Fernández-Sánchez, and E. Gómez-Déniz. The net Bayes premium with dependence between the risk profiles. Insurance Math. Econom., 45(2):247–254, 2009. ISSN 0167-6687.

- Hewitt [1970] Charles C Hewitt. Credibility for severity. PCAS LVII, page 148, 1970.

- Jeong et al. [2019] Himchan Jeong, Emiliano A Valdez, Jae Youn Ahn, and Sojung Park. Generalized linear mixed models for dependent compound risk models. Working Paper, 2019.

- Jorgensen [1997] Bent Jorgensen. The theory of dispersion models. CRC Press, 1997.

- Klugman [2013] Stuart A Klugman. Bayesian statistics in actuarial science: with emphasis on credibility, volume 15. Springer Science & Business Media, 2013.

- Klugman et al. [2012] Stuart A Klugman, Harry H Panjer, and Gordon E Willmot. Loss models: from data to decisions, volume 715. John Wiley & Sons, 2012.

- Koop [2003] Gary M Koop. Bayesian econometrics. John Wiley & Sons Inc., 2003.

- Krämer et al. [2013] Nicole Krämer, Eike C Brechmann, Daniel Silvestrini, and Claudia Czado. Total loss estimation using copula-based regression models. Insurance: Mathematics and Economics, 53(3):829–839, 2013.

- Lu [2016] Yang Lu. Flexible (panel) regression models for bivariate count–continuous data with an insurance application. Journal of the Royal Statistical Society: Series A (Statistics in Society), 2016.

- Makov et al. [1996] Udi E Makov, Adrian FM Smith, and Y-H Liu. Bayesian methods in actuarial science. Journal of the Royal Statistical Society: Series D (The Statistician), 45(4):503–515, 1996.

- McCullagh and Nelder [1989] Pa McCullagh and Ja Aa Nelder. Generalized Linear Models, second ed. Chapman and Hall, London, 1989.

- McDonald [2008] James B McDonald. Some generalized functions for the size distribution of income. Springer, 2008.

- Oh et al. [2019a] Rosy Oh, Jae Youn Ahn, and Woojoo Lee. On copula-based collective risk models. arXiv preprint arXiv:1906.03604, 2019a.

- Oh et al. [2019b] Rosy Oh, Peng Shi, and Jae Youn Ahn. Bonus-malus premiums under the dependent frequency-severity modeling. Scandinavian Actuarial Journal, pages 1–24, 2019b.

- Park et al. [2018] Sojung C Park, Joseph HT Kim, and Jae Youn Ahn. Does hunger for bonuses drive the dependence between claim frequency and severity? Insurance: Mathematics and Economics, 83:32–46, 2018.

- Plummer et al. [2003] Martyn Plummer et al. Jags: A program for analysis of bayesian graphical models using gibbs sampling. In Proceedings of the 3rd international workshop on distributed statistical computing, volume 124, pages 1–10. Vienna, Austria., 2003.

- Shi et al. [2015] Peng Shi, Xiaoping Feng, and Anastasia Ivantsova. Dependent frequency–severity modeling of insurance claims. Insurance: Mathematics and Economics, 64:417–428, 2015.

- Tweedie [1984] Maurice CK Tweedie. An index which distinguishes between some important exponential families. In Statistics: Applications and new directions: Proc. Indian statistical institute golden Jubilee International conference, volume 579, pages 579–604, 1984.