The Statistical Complexity of Early-Stopped Mirror Descent

Abstract

Recently there has been a surge of interest in understanding implicit regularization properties of iterative gradient-based optimization algorithms. In this paper, we study the statistical guarantees on the excess risk achieved by early-stopped unconstrained mirror descent algorithms applied to the unregularized empirical risk with the squared loss for linear models and kernel methods. By completing an inequality that characterizes convexity for the squared loss, we identify an intrinsic link between offset Rademacher complexities and potential-based convergence analysis of mirror descent methods. Our observation immediately yields excess risk guarantees for the path traced by the iterates of mirror descent in terms of offset complexities of certain function classes depending only on the choice of the mirror map, initialization point, step-size, and the number of iterations. We apply our theory to recover, in a clean and elegant manner via rather short proofs, some of the recent results in the implicit regularization literature, while also showing how to improve upon them in some settings.

1 Introduction

In a typical statistical learning setup, we observe a dataset of input-output pairs sampled i.i.d. from some unknown distribution . When learning with respect to the quadratic loss, the goal is to output a function which minimizes the risk defined as follows, for any square-integrable function :

Among the most studied statistical estimators is the empirical risk minimization (ERM) algorithm, which given a function class outputs a function defined as

| (1) |

in some cases with a regularization penalty term added to the optimization objective , such as norm of the model parameters. We consider the non-realizable or agnostic setting, i.e., the case in which there is no assumption that is determined by a well-specified model from a reference class of functions. In the agnostic case, a key performance measure of an estimator is its excess risk with respect to some reference class of functions :

Traditionally, in learning theory, statistical and computational properties of ERM estimators have been considered separately. From a statistical point of view, localized complexity measures have become a default tool in statistical learning theory and empirical processes theory for controlling the excess risk of ERM algorithms with respect to the function class itself, i.e., for controlling [10, 24]. A rich and general theory regarding these complexity measures has been developed and used to provide excess risk bounds in both classification and regression settings, yielding minimax-optimal results in several cases. Such complexity measures depend on combinatorial or geometric parameters of interest, such as the VC-dimension or eigenvalue decay of the kernel matrix and, in particular, they serve as a guiding principle to choose a suitable explicit regularizer for a set of candidate models , where is a hyper-parameter that controls the amount of regularization. In practice, some is then chosen via some model selection procedure such as cross-validation, aiming to select a model with the smallest risk. From a computational point of view, computing the estimators can be done by solving the corresponding optimization problems defined in Equation (1), one for each . An appealing aspect of this approach is that the design and analysis of efficient optimization algorithms, exploiting the geometry of that arises from the the structure of the model as well as the distribution , can be done independently of the statistical analysis of its performance.

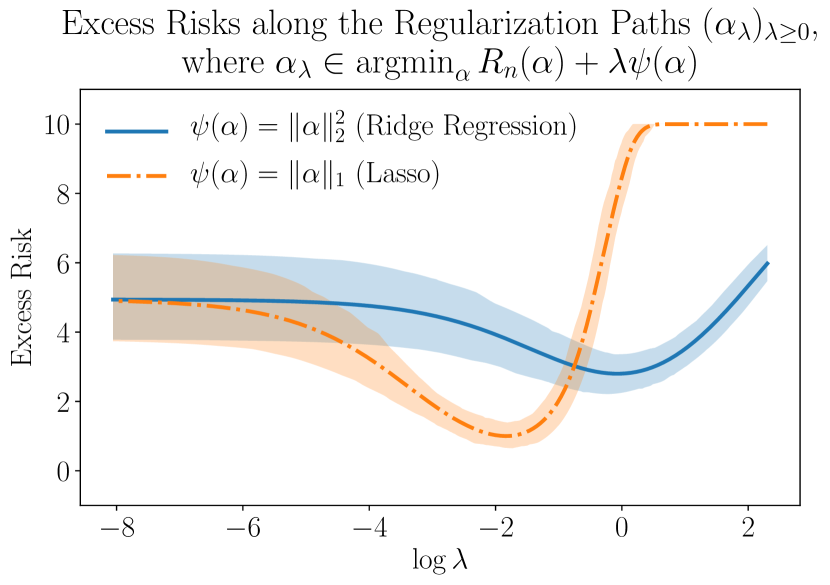

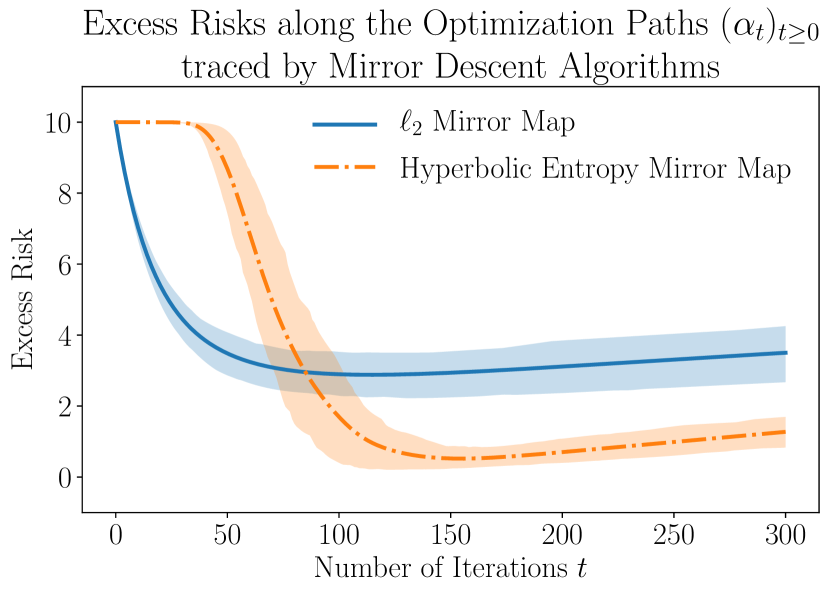

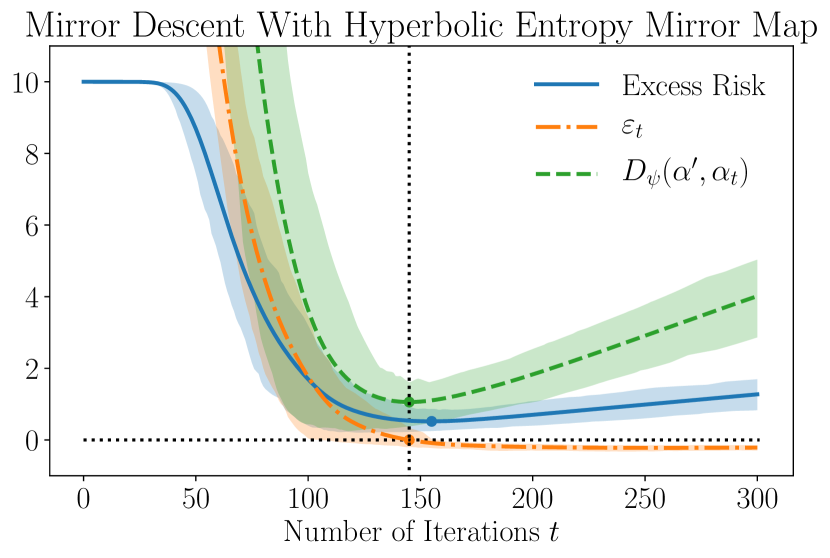

Recent years have also witnessed an increased interest in directly studying the statistical properties of models trained by gradient-based methods, particularly in relation to the notions of implicit regularization and early stopping. For a family of functions parametrized by a vector , such methods are fully characterized by the initialization point and an update rule, which given and the gradient of the empirical risk at , generates the next iterate , yielding a set of candidate estimators . Early stopping has an effect akin to explicit regularization discussed above, and the stopping time can be chosen in practice via cross-validation, just as in the case of choosing the explicit regularization parameter corresponding to the best model among . In modern large-scale machine learning applications, early stopping is often the preferred way to perform model selection, since obtaining a new model is as cheap as performing a step of gradient descent, as opposed to solving a new optimization problem with a different regularization parameter. In Figure 1, we demonstrate that different choices of optimization algorithms applied to the unregularized empirical risk yield different statistical performance along the optimization path , in a similar way that a choice of an explicit regularizer affect the statistical performance along the corresponding regularization path.

It is by now well understood that changing the update rule that generates the sequence , e.g., by changing the optimization algorithm or parametrization of the model class, can directly affect both the statistical properties of the iterates , as well as computational properties, such as an upper-bound on the optimal stopping time . However, most of the literature has focused on the investigation of vanilla gradient descent updates: (cf. Section 2.1). The existing theory does not easily generalize to other update rules corresponding to different problem geometries. A general theory that connects the notion of early stopping for a more general class of update rules with the well-established theory of localized complexities is still missing. More broadly, a general “language” to reason about the statistical properties of trajectories traced by optimization algorithms applied to the unregularized empirical risk is still lacking.

In this paper, we study a family of update rules given by the mirror descent algorithm [34, 12]. Mirror descent, which includes vanilla gradient descent as a special case, is increasingly becoming the tool of choice in optimization and machine learning, applied well beyond the traditional settings of convex optimization and online learning. Among the properties that make mirror descent appealing are its ability to exploit non-Euclidean geometries via properly designed mirror maps, the fact that the algorithm admits a general potential-based convergence analysis in terms of Bregman divergences, and its ability to represent a large class of algorithms in a unified and well-developed framework.

We consider a setting where conditionally on the observed data there exists a matrix such that the parametric family of functions satisfies for all . As special cases, our setup admits linear regression and kernel methods (cf. Section 4), cornerstones of modern statistics and machine learning. Our work reveals an inherent connection between the statistical properties of the mirror descent iterates and the notion of offset Rademacher complexity [27]. Consequently, our work unearths a simple and elegant way to simultaneously analyze upper-bounds on the stopping time , as well as the excess risk for all in terms of the mirror map, the initialization point , the step-size, and the function class . Through a simple one page analysis, we are able to rederive (nearly identical) results from prior work connecting early stopping and (optimal) statistical performance that previously involved several pages of low-level arguments.111 In some cases, the results we obtain are not exactly comparable to the ones obtained in the related work, as some of our assumptions are considerably weaker, e.g. non-realizable setting, and our guarantees stronger, excess risk vs bounds in or norms defined in Section 1.1. However, in some applications we require boundedness which is not required in some of the prior work, and some of our results are stated only in expectation, rather than high probability. We note that we can also easily obtain high-probability results in some settings (e.g. heavy-tailed classes under the lower-isometry assumption) that are outside the scope of the related work in the early stopping literature. See Section 4.1 for an extended discussion. Additionally, in the well-studied case of Euclidean gradient descent, our work improves upon the prior results connecting early stopping to localized complexity measures [39, 50] by providing upper-bounds on the expected excess risk without any distributional assumptions on other than boundedness (cf. Section 2.1).

1.1 Background

We begin this section by explaining the difficulties involved in analyzing early-stopped iterative algorithms via the classical notion of localized complexities. We then describe the offset Rademacher complexities, which is a form of localization based on a different mathematical machinery that is more suitable for our setting. Finally, we define the mirror descent updates and outline a short well-known potential-based proof of its convergence.

In what follows, we let and denote the empirical and population distances between functions and , respectively. Further, given a function class , we denote by a function that attains risk equal to .222 If such a function does not exist, we can redefine to be any function in such that for any arbitrarily small . A table of notation is provided in Appendix B.

Localized Rademacher complexities.

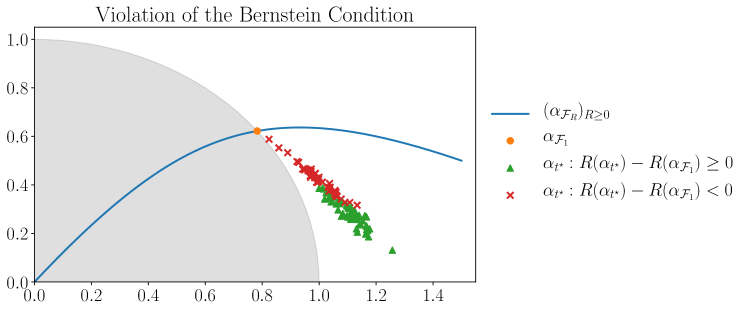

The classical notion of global Rademacher complexities [8] can only establish the slow rates of order on the excess risk (cf. [9, Theorem 2.3]). This observation was one of the primary motivating factors in the development of localized Rademacher complexities [10, 24]. Let be the range of an estimator . Rather than considering the Rademacher complexity of the whole function class , localization builds on the idea of computing the Rademacher complexity of the smaller class for some suitably defined radius that can be obtained by solving a certain fixed-point equation. More recent work focuses on unbounded and, in particular, heavy-tailed settings [32] as well as extending the scope of localization to study estimators other than ERM, e.g., to study the statistical performance of tournament procedures [30, 33]. Crucially, this line of research is rooted in the following two assumptions. First, is assumed to satisfy a convexity type assumption known in the literature as the Bernstein condition (cf. [9]), which states that for some constant , for any . If the class is convex and the loss function is quadratic then this condition follows immediately by convexity with (see [33, Definition 5.2] for more details). The second condition is imposed on the estimator itself (rather than its range ), which requires that the inequality holds for all realizations of , a property naturally satisfied by the ERM algorithm over the class . Our setting, however, does not easily fit into the above assumptions. To see why, note that the sequence obtained by some iterative algorithm aimed at minimizing the unconstrained empirical risk is not necessarily explicitly constrained to lie in the class . Thus by the time the inequality is satisfied, the iterate can already be outside the class , potentially violating the Bernstein condition (cf. Figure 2) in all cases except when is taken to be the union of ranges of over all .

Offset Rademacher complexities.

When learning with the quadratic loss, a theory of localization based on shifted Rademacher processes was developed by Liang et al. [27] inspired by prior work in online learning [37]. The use of shifted empirical processes in order to bypass technicalities present in the classical localization arguments date back at least to [49] and have recently found applications in cross-validation [25], classification [55] and PAC-Bayes bounds [52]. For a function class , a dataset , an independent sequence of Rademacher random variables , and any , the empirical offset Rademacher complexity is defined as, conditionally on the observed data :

| (2) |

Note that since the terms are always non-positive, the above notion of complexity is never larger than global Rademacher complexity of the class , which is recovered with . On the other hand, for any , the quadratic term in the above definition has a localization effect by compensating for the fluctuations in the term involving Rademacher variables (see Section 5.2 and the discussion following Theorem 3 in [27]). Importantly, the theory of localization via offset complexities replaces the Bernstein condition used in the classical theory of localization by the offset condition defined below.

Definition 1 (Offset condition).

A triple satisfies the offset condition with parameters , if for , with probabilty , we have

The above condition with was introduced in [27] where it was called the geometric inequality and shown to hold for ERM estimators over convex classes as well as the two-step star estimator [5] over general classes for finite aggregation.333 We show in Appendix A that the term affects the resulting excess risk bounds only by an additive term equal to , which can be chosen to be arbitrarily small in our main results. A key advantage offered by the theory of offset complexities is that the range of need not be a subset of , as long as the offset condition is satisfied. This allows us to consider very general estimators , possibly with non-convex ranges . In this respect, our work can be seen as showing that early-stopped mirror descent satisfies the offset condition defined above. Once an estimator is shown to satisfy the offset condition, its excess risk can be controlled in terms of the offset complexity . The theory developed in [27] establishes high-probability bounds under the lower-isometry assumption, which can hold even for possibly heavy-tailed classes ([27, Theorem 4]), as well as bounds in expectation under no assumptions other than boundedness ([27, Theorem 3]). The result in expectation states that given and for some , we have

| (3) |

where and and the expectation is taken over datasets ; here and are those that appear in the offset condition. The generality of the above result allows us to improve upon the existing bounds in the early stopping literature even for gradient descent updates (cf. Section 2.1).

Mirror descent.

The key object characterizing the geometry of the mirror descent algorithm is the mirror map , a strictly convex and differentiable function mapping some open set to whose gradient is surjective, i.e. . By slightly abusing notation, we use to denote the empirical risk of . When optimizing the empirical risk , the mirror descent updates in continuous and discrete time are given respectively by

| (4) |

where is the step-size. We remark that the choice reduces the above updates to gradient descent. A key notion in the analysis of mirror descent algorithms is the Bregman divergence, defined as for all in the domain of . By convexity of , the Bregman divergence is non-negative and enters the analysis of mirror descent algorithms through the following elementary equality:

| (5) |

Let . In the optimization literature, the above equation can be used to establish that can get arbitrarily close to from above, for any reference point . In particular, by convexity of , we have and so

| (6) |

where the last line follows by convexity of . Remarkably, the above proof works independently of the choice of the mirror map , establishing convergence for a family of algorithms in a unified framework. For more information we refer the interested reader to the surveys by Bubeck [13] and Bansal and Gupta [7]. The latter survey focuses entirely on such potential-based proofs in a variety of settings, including acceleration.

2 Summary of Techniques and Main Results

We develop a general theory for learning linear models (including kernel machines) with the squared loss that shows how the optimization trajectory of unconstrained mirror descent applied to minimize the unregularized empirical risk is inherently connected to excess risk guarantees via offset Rademacher complexity. Unlike in most prior work on early stopping, the notion of statistical complexity appears naturally from intrinsic properties of mirror descent applied to the unregularized empirical risk, without invoking lower-level arguments related to concentration to the fictitious population version of the algorithm. Furthermore, our theory leads to an explicit characterization of stopping times from the point of view of both optimization and statistics, which directly yields excess risk bounds and allows us to re-derive previously established results, and some new results, in a much simpler fashion.

As discussed in Section 1.1, early-stopped unconstrained iterative algorithms do not easily fit within the mathematical framework of classical localization techniques, partially explaining the scarcity of results connecting localized complexity measures with such algorithms. Offset Rademacher complexities, on the other hand, open up another avenue for establishing such connections via the design of update rules tailored to satisfy the offset condition (cf. Definition 1). Instead of optimizing the empirical risk , a natural approach to consider is an application of some iterative optimization algorithm to directly minimize the term appearing in the definition of the offset condition: . For any , the gradient depends on the unknown reference point and hence cannot be computed in practice. Remarkably, we show that the mirror descent updates applied to the empirical loss simultaneously implicitly minimizes for all reference points up to a certain stopping time (which depends on ), while also staying inside a certain Bregman “ball” centered at up to the corresponding stopping time. While mirror descent was developed within the framework of convex optimization, it has also found applications in a wide range of problems including bandits [1], online learning [22], the k-server problem [14] and metrical task systems [15]. In this respect, our work can be seen as an exposition of yet another example where mirror descent naturally solves a problem outside of its originally intended scope.

The key insight behind our main result is the following identity, linking the potential-based analysis of mirror descent (cf. Section 1.1) to the statistical guarantees derived from offset complexities via the offset condition (cf. Definition 1).

Lemma 1.

For any , the following holds:

Proof.

Recall that by the existence of some such that for any parameter we have (cf. Section 1), we can express the empirical loss function as , where is a vector with the th entry equal to . Hence, for any we have

where the fourth line follows by applying the equality which holds for any vectors . ∎

To appreciate the significance of the above lemma we revisit the potential-based proof of mirror descent presented in Equation (6) in Section 1.1. This time, instead of using the convexity of which gives , we directly plug in the identity given in Lemma 1 into Equation (5) which yields the following equality:

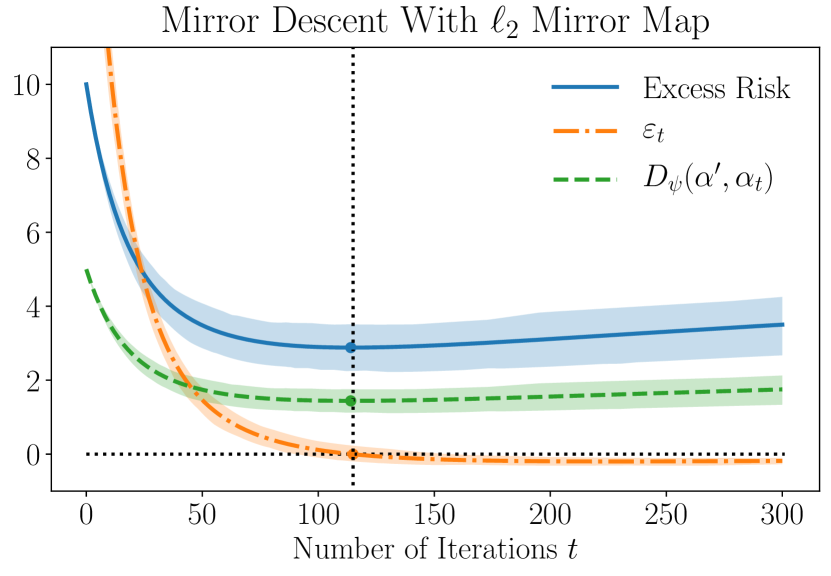

The above equation shows that while , the iterates of mirror descent stay withing the Bregman ball . At the same time, the integration argument used in Equation (6) establishes that the term eventually gets arbitrarily close to , and thus the early-stopped mirror descent iterates satisfy the offset condition (cf. Definition 1). For a visual demonstration of the above proof sketch see Figure 3. We provide full details of this argument in the proof of Theorem 1 as well as a discrete-time version in Theorem 2.

Summary of contributions:

-

1.

Our work extends the scope of offset Rademacher complexities to a family of early-stopped mirror descent methods. Additionally, we extend the scope of mirror descent to be used as a computationally efficient statistical device in an i.i.d. batch statistical learning setting.

-

2.

Our main results, in a short and transparent way, yield bounds on the excess risk of the iterates of (both continuous-time and discrete-time) mirror descent using offset Rademacher complexities. In contrast to prior work, our arguments require no direct use of low-level mathematical techniques such as symmetrization, peeling, or concentration to the population version of the algorithm.

-

3.

In Section 4, we demonstrate some selected applications of our main results and comment on the connections to the related work therein.

2.1 Comparison with Related Work

Statistical and computational properties of unconstrained gradient descent updates have been a subject of intense study over the past two decades, with most of the existing results focusing on the quadratic loss in reproducing kernel hilbert spaces (RKHS) [16, 53, 11, 39, 50]. In contrast to our work, the above work focuses either on bounds in or in norms, which can be arbitrarily smaller than the excess risk considered in our work (see [44, Section 1] for an example). In addition, the analysis in [16, 53, 11, 39] is closely tied to the geometry of the gradient descent updates, which allows one to view the algorithm as a particularly simple linear operator acting on the observed labels. Spectral properties of these linear operators are then analyzed as a function of the number of iterations, which can be solved for a stopping time via some form of bias-variance decomposition. Our work, in contrast, enables simultaneously studying a family of update rules, characterized by different choices of the mirror map, in a unified framework without relying on their particular form.

One of the primary contributions of our work is the connection between mirror descent iterates and localized complexity measures. To the best of our knowledge, there are only two prior works making connections of a similar nature, albeit only in the setting of Euclidean gradient descent updates, that is, with the choice of the mirror map [39, 50]. Such connections are observed in an algebraic fashion in the former work, while localized complexities appear more naturally in [50], via the analysis of the range of estimators defined by gradient descent iterates up the stopping time. In this respect, the work in [50] is the closest to ours. In Theorem 3, we show how a straightforward application of our main results immediately recovers results similar to the ones obtained in [39, 50] and defer an extended discussion of similarities and differences to Section 4.1.

Beyond the Euclidean setup, interest in understanding the generalization properties of neural networks has sparked research into implicit regularization properties of various factorized models. In the context of neural networks, the authors of [20, 26, 4, 51, 19] show that iterates of gradient descent applied to factorized matrix models are implicitly biased towards some sparsity-inducing structure such as low-rankness or low nuclear norm. Such results, however, hold under certain limit statements, such as vanishing initialization or step-size, the number of iterations going to infinity, or no noise in the problem. In the setting of linear regression, matrix factorization models reduce to vector Hadamard product factorizations, where early-stopped gradient descent was shown to yield minimax optimal rates for sparse recovery with the analysis vitally relying on the restricted isometry property [54, 46]. In Theorem 4, we demonstrate a simple analysis of such updates within our framework without any assumptions on the design matrix other than bounded columns, yielding an (up to a log factor) minimax optimal algorithm for in-sample linear prediction under norm constraints.

Implicit regularization properties of mirror descent have recently attracted a considerable amount of attention; however, most results in this area either focus on optimization guarantees that do not provide any direct link to statistical guarantees on out-of-sample prediction [21, 6], or establish a connection to statistics via some forms of explicit regularization [45]. The work [45] shows connections between the iterates on the entire path and the solutions on the regularization path for a suitable regularized risk minimization problem. In Theorem 5, we show how the analysis of such problems naturally fit into our framework and defer an extended discussion and comparison to the other related work [2] to Appendix 4.3. Yet other papers have used early stopping to solvers applied directly to appropriately constrained problems and regularization-promoting structures encoded directly into the loss function [31].

Recent work has also focused on providing statistical guarantees for iterates generated via gradient descent updates in stochastic [42, 29, 35, 3], accelerated [17, 36], and distributed settings [28, 40, 41]. These works provide statistical guarantees without establishing connections to localized complexity measures; we anticipate such connections to be studied within our framework in future work, for a family of mirror descent algorithms.

3 Main Results

We first state and prove a continuous-time version of our main theorem, which demonstrates the key ideas behind our approach in the simplest setting. The first part of the theorem shows that the iterates of mirror descent stay within a certain Bregman ball up to the prescribed stopping time . The second part of the theorem immediately establishes that when the parametrization given by is independent of the data, the early-stopped estimator satisfies the offset condition (cf. Definition 1) with parameters and any .444 When the parametrization is data dependent, such as in the setting of kernel methods, our main theorems also establish that the early-stopped mirror descent iterates satisfy the offset condition (cf. Definition 1). We analyze a concrete example and provide full details in Theorem 3. For the applications we consider, we choose to match the complexity measure of interest and recover the statistical-computational trade-offs consistent with the previous results in the literature. In particular, , so that achieving higher statistical accuracy requires more computational power. Finally, we note that the dependence of on the unknown radius is unavoidable purely from an optimization point of view.

Theorem 1.

Consider the continuous-time mirror descent updates given in Equation (4). Let be the initialization point, be any chosen reference point, and fix any . Then, there exists a stopping time such that:

-

1.

For all ,

-

2.

At the stopping time , we have .

Proof.

In the next theorem, we prove an equivalent result in discrete-time. Let denote any norm. We say that is -smooth with respect to if for any in the domain of . We also say that the mirror map is -strongly convex with respect to if for any we have .

Theorem 2.

Consider the discrete-time mirror descent updates given in Equation (4). Suppose that is -smooth and is -strongly convex with respect to some norm . Let be the initialization point, be any reference point, , and fix any . Then, there exists a stopping time such that:

-

1.

For all , .

-

2.

At the stopping time , we have .

Before providing the proof we briefly comment on the above theorem. First, the step-size condition and the number of iterations needed to reach a desired level of accuracy are identical to the guarantees proved in purely convex optimization settings (cf. Theorem 4.4 in [13]). On the other hand, comparing Theorems 1 and 2, in the discrete setting we pay a price of in the radius of the Bregman ball where our early-stopped estimator lies. This is consistent with prior work in the early stopping literature, where such an expansion of the radius dependent on the noise level555 Since is independent of the data and since it corresponds to the best parameter in some class of interest, and hence it can be interpreted as the noise level of the problem. propagates into the resulting bounds (cf. definition of in Theorem 1 in [50]). Our work, on the other hand, allows for a more fine-grained control of statistical-computational trade-offs via a selection of a small enough step-size .

We now introduce two lemmas supporting the proof of Theorem 2. The first lemma is a well-known generalization of the Euclidean identity , which holds for any Bregman divergence induced by any mirror map .

Lemma 2.

For any mirror map and any points in the domain of we have

Proof.

The identity follows by the definition of Bregman divergence. ∎

The second lemma proves a discrete-time counterpart to the identity given in Equation (5), which combined with Lemma 1 states that . We remind our reader that and .

Lemma 3.

Consider the discrete-time mirror descent updates given in Equation (4). Suppose that is -smooth and is -strongly convex with respect to some norm , and the step-size satisfies . Then, the following inequality holds for all :

Proof.

Combining Lemma 2 with the definition of discrete-time mirror descent updates (cf. Equation (4)) we have

| (7) |

By the -strong convexity of the mirror map , the second term in Equation (7) can be lower-bounded as . The last term in Equation (7) can be lower-bounded by using the -smoothness condition of the empirical risk function , which yields We can hence continue from Equation (7) as follows:

Since , the second term is lower-bounded by . Also, by Lemma 1, the first term becomes . Combining these two observations with the last equation above we obtain

which completes our proof. ∎

With Lemma 3 at hand, we can prove Theorem 2 following along the same steps used to prove Theorem 1, albeit with the continuous-time equation replaced with its discrete-time counterpart In the discrete-time equation, is replaced with , which results in the expansion of the radius of the Bregman ball in which the mirror descent iterates lie before the prescribed stopping time (cf. the discussion following the statement of Theorem 2 above).

Proof of Theorem 2.

By Lemma 3 we have . Let . Summing both sides of the above equation for we obtain

where in the last line we have used the definition of and facts that , , and .

It follows that the following minimum is well defined: Hence, , which completes the second part of the theorem. To complete the first part of the theorem, note that for any by telescoping the equation from to we obtain

where in the last line we have used the facts that and . ∎

4 Selected Applications of the Main Results

In this section, we discuss three selected applications of our main theorems, each of which is meant to demonstrate a particular facet of our framework as we discuss below.

Most of the results on early stopping in prior literature are shown in the non-parametric regression setting over RKHS (cf. Section 2.1). In such settings, the parametrization depends on the observed data. Theorem 3 that we present in Section 4.1 demonstrates that such data-dependent parametrizations easily fit within our framework. Additionally, we obtain results that in some ways improve upon related work, e.g., we obtain bounds on excess risk with no assumptions on the distribution other than boundedness.

In Section 4.2 we prove Theorem 4 to demonstrate two features of our main results. First, via a proper choice of the mirror map, we can derive a nearly minimax optimal algorithm for linear prediction under norm constraints. Our choice of the mirror map models the updates previously studied in the early stopping literature in the works [54, 46], both of which heavily rely on the restricted isometry assumption. In contrast, our work only requires that the columns of the fixed-design matrix are bounded in norm. Hence, Theorem 4 expands the scope of the results proved in [54, 46]. Second, we demonstrate that not only is our framework suitable to study excess risk bounds, but our main results can also be flexibly adapted to the setting of interest, in this case, proving bounds on the in-sample prediction error.

Some recent work [45, 2] investigated the connections between continuous-time optimization paths traced by gradient and mirror descent algorithms, and regularization paths of suitably regularized problems. Via Theorem 5 proved in Section 4.3, we demonstrate that such questions can also be addressed within our framework. In contrast, the prior work drawing connections between early stopping and classical localized complexity measures [39, 50] is unlikely to be easily adjustable to approach such questions due to the limitations that we have outlined in Section 1.1.

Crucially, various different questions recently studied in the related literature naturally fit within the framework developed in our paper, which provides a simple and unified way to approach such problems. Moreover, in all of the three considered examples, we prove results that in some aspects improve upon the prior work spanning several different sub-areas in the early stopping literature.

4.1 Early Stopping for Non-Parametric Regression

Let be any distribution supported on and let be a Mercer kernel which induces a Hilbert space of functions equipped with norm . Assume that for some constant and, conditionally on the observed data, denote by a matrix such that . Such a setup is standard in the literature and we refer the interested reader to the book by Scholkopf and Smola [43] for more background on RKHS.

In the theorem below, we consider the updates defined as

| (8) |

with , where is the maximum eigenvalue of . We let so that and thus the updates given in (8) correspond to mirror descent updates with the mirror map .666 Typically, the map is required to be surjective to ensure that the elements of the dual space can always be mapped back to the primal space, which is not necessarily the case with the choice of the mirror map . However, note that pre-multiplying both sides of Equation (8) by , for any it holds that and hence the updates defined in (8) are mirror descent updates. Note that is -smooth with respect to the norm defined as . To see that, note that any by Lemma 1 we have

Also, the mirror map is -strongly convex with respect to the norm. Hence the choice of the step-size given above satisfies the pre-conditions of Theorem 2.

To each , we associate a defined as . For any , the squared distance between the functions and with respect to the RKHS norm is given by the Bregman divergence :

Since our parameter system is data-dependent (both and the parametrization given by depend on the observed data points), there is, in general, no single such that for all realization of , where is some arbitrary reference function of interest. Hence, Theorem 2 does not immediately establish that early-stopped mirror descent iterates satisfy the offset condition. Our proof that we present below demonstrates how a data-dependent parameter system can be analyzed within our framework. The key idea is to find , one for each dataset , such that is “close enough” to a reference function of interest .

Theorem 3.

Consider the setup described above. Fix any and let . There exists a data-dependent stopping time such that

where constants depend only on the boundedness constants and .

Before presenting the proof, we compare the above theorem with the related work connecting early stopping and localized complexity measures [39, 50] in the setting of RKHS. First, the bounds obtained in [39, 50] hold with high-probability rather than in expectation, as we prove in Theorem 3. We note that high-probability results can also be readily obtained in our setting, via an application of [27, Theorem 4], for classes that satisfy the lower-isometry assumption (cf. [27, Definition 1]), which in some cases can hold even in heavy-tailed setups. Thus, while there is some loss in our results being stated in expectation, we can also obtain high-probability results that sometimes fall outside of the scope of the sub-Gaussian setting considered in [39, 50]. Second, the work of [50] considers a more general class of loss functions, characterized by certain strong-convexity and smoothness assumptions imposed at the population level, the reason being that the classical theory of localized complexities allows for a fairly general class of loss functions. On the other hand, while the theory of offset complexities has been developed only for the quadratic loss thus far, it allows us to consider a general class of algorithms, as characterized by the mirror map, and, in contrast to the works of [39, 50], our main results can also be applied to provide statistical guarantees along the whole optimization path (cf. Theorem 5). Third, the bounds in [39, 50] were proved under a well-specified model and i.i.d. noise assumptions, neither of which is present in Theorem 3 considered in this section. Finally, we provide bounds on the excess risk, in contrast to bounds in norm considered in [39, 50], which coincide with the excess risk only in some limited settings (cf. discussion in [44]). The differences aside, Theorem 3 is remarkably similar to the results obtained in [39, 50]. In particular, we recover similar conditions on the step-size and provide almost identical statistical and computational guarantees. We refer to [27, Corollary 12] and [50, Section 3.3] for discussions concerning the statistical optimality of localized complexity measures for non-parametric regression.

Proof of Theorem 3.

By the Representer theorem, there exists , such that and hence, by convexity of , the triple satisfies the offset condition with parameters (, ) (cf. [27, Lemma 1]). Consequently, with probability we have

| (9) |

Since , we have . Also, by the boundedness assumption on the kernel , for any we have . Hence, for any we have and in particular, 777 In a well-specified setting this quantity can be made as small as the variance of the noise modulo an absolute multiplicative constant. Applying Theorem 2 with , for any , there exists a data-dependent stopping time satisfying

such that the following two inequalities hold with probability :

| (10) |

where the second inequality follows from the fact that . Combining the first inequality above with Equation (9), the following holds with probability :

Thus, the triple satisfies the offset condition with parameters . In addition, by Equation (10) we have

Hence , where depends only on and .888 A smaller step-size can make depend only on . See the discussion following the statement of Theorem 2. Applying [27, Theorem 3], as stated in Equation (3), there exist constants , that depend only on and , such that

The result follows by taking . ∎

4.2 In-Sample Linear Prediction Under Constraints

Let be a fixed-design matrix such that the norms of columns of are bounded by some constant . Assume a well-specified model, i.e., the existence of a vector such that the observations follow the distribution , where is a vector with i.i.d. zero-mean -subGaussian components. We aim to find a vector that achieves a small in-sample prediction error defined as .

A candidate implicit regularization based algorithm, known to be minimax optimal for sparse recovery under restricted isometry assumption [54, 46], is defined as follows. Let denote the iterate obtained at time , let denote the Hadamard product, and let denote a vector with all entries equal to one. Consider the parametrization where . Instead of running gradient descent directly on , the algorithm considered in the works [54, 46] is defined by running gradient descent updates on the concatenated parameter vector , yielding the following updates (where ):

We remark that the above updates were also studied in [51], albeit with a focus on how the initialization scale affects the gradient descent solution obtained at convergence. Noting that for small , we can approximate the above updates (with the step-size rescaled by a constant factor) by the unconstrained algorithm [23] whose updates are given by

It was shown in [18] that the above updates correspond to running unconstrained mirror descent initialized at with the mirror map given by

In the rest of the section, we denote by to make the dependence on explicit. We consider running mirror descent with the hyperbolic entropy mirror map with any and with any step-size that satisfies . The theorem below yields minimax-optimal rates [38] for the in-sample prediction error up to the multiplicative factor .

Theorem 4.

Consider the setup described above. There exists a data-dependent stopping time such that with probability at least , where is an absolute constant, we have

Before proving the above theorem, we state two lemmas, which relate the Bregman divergence induced by the mirror map to the geometry induced by the norm. We prove both lemmas at the end of this section.

Lemma 4.

For any we have

Denote by an ball of radius . The following lemma will be applied to show that before stopping, the mirror descent iterates stay inside an ball with radius at most .

Lemma 5.

For any and any we have

We are now ready to prove Theorem 4. We remark that since the slow rate is minimax optimal [38] in the setting considered in Theorem 4, the localization effect provided by offset complexities is not needed in this example. However, we can apply Theorem 2 together with the basic inequality proof technique, as demonstrated in the proof below.

Proof of Theorem 4.

First note that since the norms of the columns of are bounded by , the empirical loss function is -smooth with respect to the norm. Let

As shown in [18, Lemma 4], is also -strongly convex with respect to the norm on . Thus, we set the smoothness parameter and the strong convexity parameter .

Condition on the event . Since the noise random variables are -subGaussian, by sub-Exponential concentration we have where is an absolute constant independent of any problem parameters. (cf. [47, Section 5.2.4]). By Theorem 2, Lemma 4 and , it is hence enough to set

so that there exists a stopping time

such that for all it holds that

| (11) |

and also, such that the following inequality holds:

| (12) |

Rearranging the above inequality, as is typically done via the basic inequality proof technique (see, for example, [48, Theorem 7.20]) we obtain

Define the event . Since the norms of the columns of are bounded by and since the noise vector consists of independent sub-Gaussian random variables, by standard sub-Gaussian concentration.

By the union bound, the events and happen simultaneously with probability at least . Setting concludes our proof. ∎

4.3 Statistical Guarantees Along the Optimization Path

Theorem 1 immediately implies that along its optimization path, continuous-time mirror descent satisfies excess risk guarantees that one would obtain for a series of ERM solutions over a corresponding set of explicitly constrained convex and bounded problems.

Fix any radius , let and suppose that for some constant . For simplicity, in the proof below, we assume that the coordinate system represented by the parametrization is independent of the data. A data dependent coordinate system can be handled via the same technique used to prove Theorem 3, thus we note that the result stated in Theorem 5 also holds in the kernel regime. For smooth loss functions and sufficiently small step-sizes, Theorem 2 can be applied to derive a corresponding result in discrete time.

Theorem 5.

Fix any , and let For any , there exists a data-dependent stopping time such that for some , depending only on the boundedness constants and , we have

Proof of Theorem 5.

Let be the parameter corresponding to the function . Then, by Theorem 1 there exists a data-dependent stopping time such that the triple satisfies the offset condition (cf. Definition 1) with parameters and . Thus, by [27, Theorem 3], as stated in Equation (3), there exist constants that depend only on and such that . ∎

Through the lens of the offset complexities, similar excess risk guarantees hold for any ERM estimator over the function space , which we denote by . To see why, note that since Bregman divergences are convex in the first argument, the class is convex. Thus, by [27, Lemma 1], the triple satisfies the offset condition (cf. Definition 1) with parameters . Hence, with the same choice of and as in Theorem 5, it holds that

In particular, Theorem 5 shows, that along the optimization path , the mirror descent iterates satisfy almost identical excess risk guarantees that also hold for the regularization path obtained by ERM solutions over classes with varying radius .

The above observation is related to some of the recent work in the implicit regularization literature, which has sought to provide statistical guarantees on solutions along the optimization path of gradient descent and mirror descent. The work [45] establishes that the optimization paths and the regularization paths of corresponding regularized problems, when suitably aligned via some mapping between the number of mirror descent iterations and the regularization parameter of the penalized problem, are point-wise close. This allows them to port existing results on regularized optimization to early-stopped descent algorithms; in contrast, our result proved in Theorem 5 shows that the excess risk of solutions along the optimization path of mirror descent can be directly bounded by the offset Rademacher complexity. We also do not require the loss function to be strongly convex as a function of parameter . The work [2] studies the optimization path of continuous time gradient descent for linear regression, which can be computed analytically, and show that the solution at time has risk at most times the risk of the ridge solution with . In contrast to our results, their results are derived under the well-specified model and their out-of-sample analysis is performed via a certain Bayesian averaging that is not needed in our work.

5 Future Directions

Our work provides a simple and transparent framework for simultaneously analyzing statistical and computational properties of iterates traced by a family of mirror descent algorithms applied to the i.i.d. batch statistical learning setting. Among the research directions that would yield additional computational savings are extensions of our results to stochastic and accelerated frameworks, where connections between early stopping and localized complexity measures are yet to be established, even in the restricted setting of Euclidean gradient descent updates.

Beyond the computational savings, our main results reveal a curious property of mirror descent. For an unknown parameter of interest denoted by , the statistical complexity of an appropriately stopped mirror descent iterate is given by the offset complexity of the class . Thus, is implicitly constrained to lie in a possibly non-convex Bregman ball centered at the unknown with unknown radius . Therefore, in general, solutions traced by mirror descent iterates cannot be practically expressed as solutions of explicitly constrained optimization problems. Consequently, early-stopped mirror descent can potentially solve problems that cannot be tractably solved by the means of explicit regularization. This observation necessitates further investigation.

Acknowledgments

Tomas Vaškevičius is supported by the EPSRC and MRC through the OxWaSP CDT programme (EP/L016710/1). Varun Kanade and Patrick Rebeschini are supported in part by the Alan Turing Institute under the EPSRC grant EP/N510129/1.

References

- Abernethy et al. [2008] Jacob D. Abernethy, Elad Hazan, and Alexander Rakhlin. Competing in the dark: An efficient algorithm for bandit linear optimization. In COLT, 2008.

- Ali et al. [2019] Alnur Ali, J Zico Kolter, and Ryan J Tibshirani. A continuous-time view of early stopping for least squares regression. In International Conference on Artificial Intelligence and Statistics, pages 1370–1378, 2019.

- Ali et al. [2020] Alnur Ali, Edgar Dobriban, and Ryan J Tibshirani. The implicit regularization of stochastic gradient flow for least squares. arXiv preprint arXiv:2003.07802, 2020.

- Arora et al. [2019] Sanjeev Arora, Nadav Cohen, Wei Hu, and Yuping Luo. Implicit regularization in deep matrix factorization. In Advances in Neural Information Processing Systems, pages 7411–7422, 2019.

- Audibert [2008] Jean-Yves Audibert. Progressive mixture rules are deviation suboptimal. In Advances in Neural Information Processing Systems, pages 41–48, 2008.

- Azizan and Hassibi [2019] Navid Azizan and Babak Hassibi. Stochastic gradient/mirror descent: Minimax optimality and implicit regularization. In International Conference on Learning Representations, 2019.

- Bansal and Gupta [2019] Nikhil Bansal and Anupam Gupta. Potential-function proofs for gradient methods. Theory of Computing, 15(1):1–32, 2019.

- Bartlett and Mendelson [2002] Peter L Bartlett and Shahar Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482, 2002.

- Bartlett and Mendelson [2006] Peter L Bartlett and Shahar Mendelson. Empirical minimization. Probability theory and related fields, 135(3):311–334, 2006.

- Bartlett et al. [2005] Peter L Bartlett, Olivier Bousquet, and Shahar Mendelson. Local rademacher complexities. The Annals of Statistics, 33(4):1497–1537, 2005.

- Bauer et al. [2007] Frank Bauer, Sergei Pereverzev, and Lorenzo Rosasco. On regularization algorithms in learning theory. Journal of complexity, 23(1):52–72, 2007.

- Beck and Teboulle [2003] Amir Beck and Marc Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- Bubeck [2015] Sébastien Bubeck. Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357, 2015.

- Bubeck et al. [2018] Sébastien Bubeck, Michael B Cohen, Yin Tat Lee, James R Lee, and Aleksander Mądry. K-server via multiscale entropic regularization. In Proceedings of the 50th annual ACM SIGACT symposium on theory of computing, pages 3–16, 2018.

- Bubeck et al. [2019] Sébastien Bubeck, Michael B Cohen, James R Lee, and Yin Tat Lee. Metrical task systems on trees via mirror descent and unfair gluing. In Proceedings of the Thirtieth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 89–97. SIAM, 2019.

- Bühlmann and Yu [2003] Peter Bühlmann and Bin Yu. Boosting with the loss: regression and classification. Journal of the American Statistical Association, 98(462):324–339, 2003.

- Chen et al. [2018] Yuansi Chen, Chi Jin, and Bin Yu. Stability and convergence trade-off of iterative optimization algorithms. arXiv preprint arXiv:1804.01619, 2018.

- Ghai et al. [2019] Udaya Ghai, Elad Hazan, and Yoram Singer. Exponentiated gradient meets gradient descent. arXiv preprint arXiv:1902.01903, 2019.

- Gidel et al. [2019] Gauthier Gidel, Francis Bach, and Simon Lacoste-Julien. Implicit regularization of discrete gradient dynamics in deep linear neural networks. arXiv preprint arXiv:1904.13262, 2019.

- Gunasekar et al. [2017] Suriya Gunasekar, Blake E Woodworth, Srinadh Bhojanapalli, Behnam Neyshabur, and Nati Srebro. Implicit regularization in matrix factorization. In Advances in Neural Information Processing Systems, pages 6151–6159, 2017.

- Gunasekar et al. [2018] Suriya Gunasekar, Jason Lee, Daniel Soudry, and Nathan Srebro. Characterizing implicit bias in terms of optimization geometry. In Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 1832–1841, Stockholmsmässan, Stockholm Sweden, 10–15 Jul 2018. PMLR.

- Hazan [2016] Elad Hazan. Introduction to online convex optimization. Foundations and Trends in Optimization, 2(3-4):157–325, 2016.

- Kivinen and Warmuth [1997] Jyrki Kivinen and Manfred K Warmuth. Exponentiated gradient versus gradient descent for linear predictors. information and computation, 132(1):1–63, 1997.

- Koltchinskii [2006] Vladimir Koltchinskii. Local rademacher complexities and oracle inequalities in risk minimization. The Annals of Statistics, 34(6):2593–2656, 2006.

- Lecué et al. [2012] Guillaume Lecué, Charles Mitchell, et al. Oracle inequalities for cross-validation type procedures. Electronic Journal of Statistics, 6:1803–1837, 2012.

- Li et al. [2018] Yuanzhi Li, Tengyu Ma, and Hongyang Zhang. Algorithmic regularization in over-parameterized matrix sensing and neural networks with quadratic activations. In Conference On Learning Theory, pages 2–47, 2018.

- Liang et al. [2015] Tengyuan Liang, Alexander Rakhlin, and Karthik Sridharan. Learning with square loss: Localization through offset rademacher complexity. In Conference on Learning Theory, pages 1260–1285, 2015.

- Lin and Cevher [2018] Junhong Lin and Volkan Cevher. Optimal distributed learning with multi-pass stochastic gradient methods. In Proceedings of the 35th International Conference on Machine Learning, number CONF, 2018.

- Lin et al. [2016] Junhong Lin, Raffaello Camoriano, and Lorenzo Rosasco. Generalization properties and implicit regularization for multiple passes sgm. In International Conference on Machine Learning, pages 2340–2348, 2016.

- Lugosi and Mendelson [2016] Gabor Lugosi and Shahar Mendelson. Risk minimization by median-of-means tournaments. arXiv preprint arXiv:1608.00757, 2016.

- Matet et al. [2017] Simon Matet, Lorenzo Rosasco, Silvia Villa, and Bang Long Vu. Don’t relax: early stopping for convex regularization. arXiv preprint arXiv:1707.05422, 2017.

- Mendelson [2014] Shahar Mendelson. Learning without concentration. In Conference on Learning Theory, pages 25–39, 2014.

- Mendelson [2017] Shahar Mendelson. Extending the small-ball method. arXiv preprint arXiv:1709.00843, 2017.

- Nemirovsky and Yudin [1983] Arkadiĭ Nemirovsky and David Yudin. Problem complexity and method efficiency in optimization. Wiley, New York, 1983.

- Neu and Rosasco [2018] Gergely Neu and Lorenzo Rosasco. Iterate averaging as regularization for stochastic gradient descent. arXiv preprint arXiv:1802.08009, 2018.

- Pagliana and Rosasco [2019] Nicolò Pagliana and Lorenzo Rosasco. Implicit regularization of accelerated methods in hilbert spaces. In Advances in Neural Information Processing Systems, pages 14454–14464, 2019.

- Rakhlin and Sridharan [2014] Alexander Rakhlin and Karthik Sridharan. Online non-parametric regression. In Conference on Learning Theory, pages 1232–1264, 2014.

- Raskutti et al. [2011] Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Minimax rates of estimation for high-dimensional linear regression over balls. IEEE transactions on information theory, 57(10):6976–6994, 2011.

- Raskutti et al. [2014] Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Early stopping and non-parametric regression: an optimal data-dependent stopping rule. The Journal of Machine Learning Research, 15(1):335–366, 2014.

- Richards and Rebeschini [2019] Dominic Richards and Patrick Rebeschini. Optimal statistical rates for decentralised non-parametric regression with linear speed-up. In Advances in Neural Information Processing Systems, pages 1214–1225, 2019.

- Richards and Rebeschini [2020] Dominic Richards and Patrick Rebeschini. Graph-dependent implicit regularisation for distributed stochastic subgradient descent. Journal of Machine Learning Research, 21(34):1–44, 2020.

- Rosasco and Villa [2015] Lorenzo Rosasco and Silvia Villa. Learning with incremental iterative regularization. In Advances in Neural Information Processing Systems, pages 1630–1638, 2015.

- Scholkopf and Smola [2001] Bernhard Scholkopf and Alexander J Smola. Learning with kernels: support vector machines, regularization, optimization, and beyond. MIT press, 2001.

- Shamir [2015] Ohad Shamir. The sample complexity of learning linear predictors with the squared loss. The Journal of Machine Learning Research, 16(1):3475–3486, 2015.

- Suggala et al. [2018] Arun Suggala, Adarsh Prasad, and Pradeep K Ravikumar. Connecting optimization and regularization paths. In Advances in Neural Information Processing Systems, pages 10608–10619, 2018.

- Vaškevičius et al. [2019] Tomas Vaškevičius, Varun Kanade, and Patrick Rebeschini. Implicit regularization for optimal sparse recovery. In Advances in Neural Information Processing Systems, pages 2968–2979, 2019.

- Vershynin [2010] Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- Wainwright [2019] Martin J Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press, 2019.

- Wegkamp et al. [2003] Marten Wegkamp et al. Model selection in nonparametric regression. The Annals of Statistics, 31(1):252–273, 2003.

- Wei et al. [2019] Yuting Wei, Fanny Yang, and Martin J Wainwright. Early stopping for kernel boosting algorithms: A general analysis with localized complexities. IEEE Transactions on Information Theory, 65(10):6685–6703, 2019.

- Woodworth et al. [2019] Blake Woodworth, Suriya Gunasekar, Jason Lee, Daniel Soudry, and Nathan Srebro. Kernel and deep regimes in overparametrized models. arXiv preprint arXiv:1906.05827, 2019.

- Yang et al. [2019] Jun Yang, Shengyang Sun, and Daniel M Roy. Fast-rate pac-bayes generalization bounds via shifted rademacher processes. In Advances in Neural Information Processing Systems, pages 10803–10813, 2019.

- Yao et al. [2007] Yuan Yao, Lorenzo Rosasco, and Andrea Caponnetto. On early stopping in gradient descent learning. Constructive Approximation, 26(2):289–315, 2007.

- Zhao et al. [2019] Peng Zhao, Yun Yang, and Qiao-Chu He. Implicit regularization via Hadamard product over-parametrization in high-dimensional linear regression. arXiv preprint arXiv:1903.09367, 2019.

- Zhivotovskiy and Hanneke [2018] Nikita Zhivotovskiy and Steve Hanneke. Localization of vc classes: Beyond local rademacher complexities. Theoretical Computer Science, 742:27–49, 2018.

Appendix A On the Term in the Offset Condition

Suppose that an estimator that always returns a function from some set and the triple satisfies the offset condition (cf. Definition 1) with parameters . Then, following along the lines of Liang et al. [27, Corollary 2] we obtain

The penultimate term, excluding , is the same as the term obtained in [27, Corollary 2]. Since the range of is , the function is constrained to lie in the set , which gives the term on the last line involving the supremum (cf. [27, Equation 11]). From this point, offset Rademacher complexity bounds in expectation [27, Theorem 3] and probability [27, Theorem 4] are obtained via symmetrization of the above term in expectation and probability respectively.

Appendix B Table of Notation

| Symbol | Description |

|---|---|

| The number of data points. | |

| The data generating distribution. | |

| The th data point sampled independently from the distribution . | |

| A collection of data points sampled i.i.d. from . | |

| The population risk of a function defined as . | |

| The empirical risk of a function defined as . | |

| An estimator, which maps datasets to some set of functions . | |

| The set of possible values of functions, that some estimator can select. | |

| Some generic class of functions. | |

| The excess risk of an estimator with respect to . | |

| A function such that . | |

| Population distance between and defined as | |

| Empirical distance between and defined as . | |

| The offset Rademacher complexity of (cf. Equation (2)). | |

| The dimensionality of the parameter space. | |

| A function parameterized by . | |

| A matrix such that conditionally on , for any . | |

| A shorthand notation for . | |

| A mirror map. | |

| Bregman divergence induced by the mirror map . | |

| The initialization point of the mirror descent iterates. | |

| The mirror descent iterate at time . | |

| An arbitrarily chosen reference point. | |

| A shorthand notation for . | |

| A shorthand notation for . |