∗ Department of Mathematics, Karlsruhe Institute of Technology (KIT), D-76128 Karlsruhe, Germany

Robust Optimal Investment and Reinsurance Problems with Learning

Abstract.

In this paper we consider an optimal investment and reinsurance problem with partially unknown model parameters which are allowed to be learned. The model includes multiple business lines and dependence between them. The aim is to maximize the expected exponential utility of terminal wealth which is shown to imply a robust approach. We can solve this problem using a generalized HJB equation where derivatives are replaced by generalized Clarke gradients. The optimal investment strategy can be determined explicitly and the optimal reinsurance strategy is given in terms of the solution of an equation. Since this equation is hard to solve, we derive bounds for the optimal reinsurance strategy via comparison arguments.

otsep5

- Key words :

-

Risk Theory, Stochastic Control, Filter, Robust Approach

1. Introduction

The insurance industry is currently facing a variety of challenges. On the one hand, the number and amount of insurance losses are growing caused by an increasing frequency of weather extremes due to climate change (see [16]). On the other hand, the current structural low interest rate environment and higher volatility on the financial markets make it more difficult to achieve profitable investments. These challenges call for effective strategies to reduce insurance risk and to optimize capital investments and have attracted interest from researches in actuarial mathematics for many years. In fact, a classical task in risk theory is to deal with optimal risk control and optimal asset allocation for an insurance company. Such problems have been intensively studied in literature using various optimization criteria, where maximizing the utility and minimizing the probability of ruin are the two main optimization criteria (see e.g. [26] and references given there).

However, in most articles, the assumption of full information is used as a common feature, which means that the insurer has complete knowledge of the model. However, in reality, insurance companies operate in a setting with partial information. That is, with regard to the net claim process, only the claim arrival times and magnitudes are directly observable; the claim intensity, which is required by all net claim models, is not observable by the insurer as pointed out in [17, Ch. 2]. Therefore we study the optimal investment and reinsurance problem in a partial information framework. More precisely we consider a Bayesian approach which means that we allow for learning unknown model parameters. On the other hand we use an exponential utility function as optimization criterion which can be interpreted as a robust approach.

There are quite a number of papers on robust decision making in actuarial sciences, in particular for optimal reinsurance and investment, see e.g. [30, 31, 19, 18] among others. But all the approaches so far consider a classical optimization problem like utility maximization under alternative models given in form of different probability measures. In this paper indeed we explain that the exponential utility can be interpreted as a robust control approach, thus avoiding a second complicated optimization.

A paper with partial information is e.g. [22]. Based on the suggestion in [1, p. 165], the authors there consider the optimal investment and reinsurance problem for maximizing exponential utility under the assumption that the claim intensity and loss distribution depend on the states of a non-observable Markov chain (hidden Markov chain), which describes different states of the environment, whereby the net claim process is modelled as compound Poisson process and the fully observable financial market is modelled as Black-Scholes financial market with one risky and one risk-free asset.

However, the sparse literature with partial information focuses on just one line of business to gain an optimal reinsurance strategy. But in reality there is often a dependence between different risk processes of an insurance company. This results from the fact that the customers of a typical insurance company have insurance policies of different types such as building, private liability or health insurance contracts. A simplified example of a possible dependence between several types of risk is that of a storm event accompanied by heavy rainfall where flying roof tiles cause damages to third parties and flooding leads to building damages. Therefore, to model the insurance risks of an insurer appropriately, we need to capture the dependence structure using a multivariate model.

A commonly used approach to impose dependence between several types of insurance risks is accomplished by thinning, which is also the case in this paper. The idea of this approach is that the occurrence of claims depends on a certain process which generates events that cause damages of the line of business with probability and of the line of business with probability , where all caused claims occur simultaneously at the trigger arrival time. Therefore these models are referred to as common shock risk models. An example of a shock event is the above-described storm event. Typically the corresponding claim sizes are determined independently of the appearance times (see e.g. [4]).

Another multivariate model that avoids a reference to an external mechanism is given in [5], where the authors propose a multivariate continuous Markov chain of pure birth type with interdependency arising from dependences of the birth rates on the number of claims in other component processes. In [25], the dependence of the marginal processes of a multiple claim arrival process is constructed by introducing a Lévy subordinator serving as a joint stochastic clock, which leads to a multivariate Cox process in the sense that the marginal processes are univariate Cox processes. In connection with optimal reinsurance problems, a Lévy approach is discussed in [3]. There, the authors have shown that a constant investment and reinsurance strategy (proportional reinsurance as well as the mixture of proportional and excess-of-loss reinsurance) is the optimal strategy for maximizing the exponential utility of terminal wealth.

In addition to the Lévy model, optimization problems with common shock models have been investigated in [12], where optimal excess-of-loss retention limits are studied for a bivariate compound Poisson risk model in a static setting. The corresponding dynamic model was used in [2] to derive optimal excess-of-loss reinsurance policies (which turns out to be constant) under the criterion of minimizing the ruin probability making use of a diffusion approximation. For the same model, [23] have derived a closed-form expression for the optimal proportional reinsurance strategy of the exponential utility maximizing problem both with and without diffusion approximation by using the variance premium principle. In the presence of a Black-Scholes financial market, the same problem has been investigated in [9] with the expected value premium principle. For the case of an insurance company with more than two lines of business, [29] and [28] seek optimal proportional reinsurance to maximize the exponential utility of terminal wealth and the adjustment coefficient, respectively, where the strategies are only stated for two classes of business. However, all optimization problems with multivariate insurance models are considered under full information.

We will describe the dependence structure between different lines of business by the thinning approach while we deal with unobservable thinning probabilities. To the authors’ knowledge, this is the first time that an optimal reinsurance and investment problem under partial information using a multivariate claim arrival model with possibly dependent marginal processes is studied. To solve the optimal control problem, the dynamic programming approach will be applied. However since the value function may not be differentiable, a generalization using the Clarke gradient will be applied (this idea has been used before in [6], [22]).

The outline of our paper is as follows: We introduce the partial information problem under the assumptions of observable claim size distribution, unobservable background intensity taking values in a finite set and Dirichlet distributed thinning probabilities in Section 2. We also explain the robust approach which is inherit in the criterion of maximizing exponential utility. Using a filter as an estimator for the background intensity and the conjugated property of the Dirichlet distribution, we proceed in Section 3 by stating the reduced control problem. The corresponding generalized Hamilton Jacobi Bellman (HJB) equation will be introduced in Section 4, where we need to replace partial derivatives w.r.t. the time and the components of the filter for the background intensity by the corresponding Clarke gradient. The HJB equation yields the same optimal investment strategy as in the classical Merton problem and the optimal reinsurance strategy has to be characterized implicitly. Next we prove a verification theorem and show the existence and optimality of the proposed strategy. Finally in Section 5, we provide a comparison result under the assumption of identical claim size distributions for all insurance classes, which is visualized by some examples in the last section.

2. The Optimal Investment and Reinsurance Model

We consider an insurance company with several lines of business. The aim is to maximize the expected utility of the terminal surplus of the considered insurance company by choosing optimal investment and reinsurance strategies. For the moment we assume that all model data is known.

2.1. The claim arrival process

In the following, let be the number of business lines of the insurer. The claim arrival model is a Poisson process with intensity . We interpret the arrival times of the Poisson process , denoted by , as events which trigger various kinds of insurance claims. The lines of business which are affected by the trigger event at are given by a random variable with values in (power set of ). We assume that are i.i.d. with and denote . The interdependencies between the lines of business are fully determined by . We call the components of thinning probabilities since they thin the trigger arrival times. Moreover, w.l.o.g. , i.e. every shock event leads to at least one insurance damage. Otherwise we could reduce the intensity of . Therefore the (multivariate) claim arrival process, denoted by , is defined by

So is a -dimensional counting process, where counts the number of claims of the th business line up to time . The claim sizes are described by a -dimensional sequence with of i.i.d. -valued random variables with distribution . It is worth to note that the claims sizes from various business lines can be dependent. We assume that are independent of the sequences and . The sum of the claim sizes of all insurance classes which appear at the arrival times of the multivariate claim arrival process up to time , denoted by , gives the aggregated claim amount process, i.e. it is given by

From now on, we set and let . That is, is the -Marked Point Process which contains the information of the claim arrival times, the thinning sequence and the claim sizes. The filtration generated by is denoted by and the intensity measure of is given by Using the introduced Marked Point Process , we can write

| (2.1) |

It should be noted that the aggregated claim amount process is observable for the insurance company and thus the natural filtration of , denoted by , is known by the insurer. We can interpret given by (2.1) as the aggregated claim amount process of a heterogeneous insurance portfolio where the random elements yield the information of which type the claim size distribution of the claim at time is. Finally we need the following assumption on the integrability of the claim size distribution:

| (2.2) |

2.2. The financial market

The surplus will be invested by the insurer into a financial market, which will be modelled as a classical Black-Scholes market. So it is supposed that there exists one risk-free asset and one risky asset. The price process of the risk-free asset, denoted by , is given by

where denotes the risk-free interest rate. That is, for all . The price process of the risky asset, denoted by , is given by

where and are constants describing the drift and volatility of the risky asset, respectively, and is a standard Brownian motion. We assume that the Brownian motion is independent of , and . We denote by the augmented Brownian filtration of . Throughout this work, denotes the observable filtration of the insurer which is given by

2.3. The strategies

We assume that the wealth of the insurance company is invested into the previously described financial market.

Definition 2.1.

An investment strategy, denoted by , is an -valued, bounded, càdlàg and -progressively measurable process.

Note that for simplicity we assume here bounded strategies, i.e. for . We will later see that this is no restriction. Further, we assume that the first-line insurer has the possibility to take a proportional reinsurance. Therefore, the part of the insurance claims paid by the insurer, denoted by , satisfies

with retention level and insurance claim . Here we suppose that the insurer is allowed to reinsure a fraction of her/his claims with retention level at every time .

Definition 2.2.

A reinsurance strategy, denoted by , is a -valued, càdlàg and -predictable process.

We denote by the set of all admissible strategies on . We assume that the policyholder’s payments to the insurance company are modelled by a fixed premium (income) rate with safety loading and fixed constant , which means that premiums are calculated by the expected value principle. If the insurer chooses retention levels less than one, then the insurer has to pay premiums to the reinsurer. The part of the premium rate left to the insurance company at retention level , denoted by , is , where denotes the reinsurance premium rate. We say is the net income rate. Moreover, the net income rate should increase in , which is fulfilled by setting with which represents the safety loading of the reinsurer. Therefore

| (2.3) |

where . This reinsurance premium model is used e.g. in [32]. The surplus process under an admissible investment-reinsurance strategy is given by

We suppose that is the initial capital of the insurance company. An alternative representation of the surplus process with the help of the random measure will be useful. The dynamics of the surplus can for be written as

| (2.4) |

2.4. The optimization problem

Clearly, the insurance company is interested in an optimal investment-reinsurance strategy. But there are various optimality criteria to specify optimization of proportional reinsurance and investment strategies. We consider the expected utility of wealth at the terminal time as criterion with exponential utility function

| (2.5) |

where the parameter measures the degree of risk aversion. The choice of this criterion will be justified below. Next, we are going to formulate the dynamic optimization problem. We define the value functions, for any and , by

| (2.6) | ||||

where the expectation is taken w.r.t. the conditional probability measure where is given (when we simply write ). This optimization criterion has an interesting interpretation. Instead of we can equivalently maximize which is the entropic risk measure of terminal wealth. For small this is approximately equal to (see e.g. [10], [7])

Thus, for small we maximize the expectation penalized by the variance. This is a risk-sensitive criterion on one hand, but can also be seen as the Lagrange-function of a mean-variance problem. Another interesting feature of this criterion is that it has a dual representation as

for r.v. which are bounded from above with

for the relative entropy function or Kullback-Leibler distance between two probability measures (see e.g. [14]). From this representation we see that the case corresponds to the case of a robust optimization problem or worst-case optimization problem where the insurer maximizes the surplus if nature chooses the least favourable measure for the model. For this means that potentially a whole range of beliefs about is considered but deviations from the baseline model are penalized. In some cases this yields an alternative method to solve the optimization problem. Let us for example consider the classical (one-dimensional) Cramér-Lundberg model with reinsurance which is a special case of our model. The surplus process is given by

It is well-known that the worst-case probability measure in this representation is also equivalent to . So we can restrict our search of the worst-case measure to measures with a density of the form (see e.g. [20] [27]),

| (2.7) |

where

is a -martingale under . Thus, we can parametrize by the random intensity measure . Hence

| (2.8) | |||||

Minimizing this expression w.r.t. can be done pointwise and yields by simple differentiation that the worst case measure is given by

Plugging this expression in (2.8) yields

and maximizing for which can again be done pointwise finally gives the Euler equation

| (2.9) |

for the first-order condition implying the optimality of . The optimal strategy is here given by with solving (2.9) (see also [3], [22]). This discussion illustrates that the exponential utility function is really useful on one hand since by choosing we can interpolate between a risk-sensitive criterion and a robust point of view. Moreover, it is still tractable as we will see in the next sections. However, the robust approach is often too pessimistic and we want to combine it with learning model parameters. That’s why we further generalize the model in the next section.

3. A Model with Learning

Now we assume that the precise parameters and of the model are not known. Instead we take a Bayesian approach and suppose that is a realization of a random variable which takes values in a set and has initial distribution W.l.o.g. . Moreover, we assume that the initial distribution of is a Dirichlet distribution with parameter , where .

Definition 3.1 (Dirichlet distribution; [15], p. 49).

A random vector has a Dirichlet distribution with parameter , if the probability density function is given by

where denotes the interior of and the gamma function. We shortly write .

Thus, we allow that model parameters are learned by observing the process. In what follows we define

| (3.1) |

and . Thus is an -valued process and counts the number of realizations of equal to up to time .

The reason for the choice of the Dirichlet distribution as prior is the conjugated property of the Dirichlet prior, which is stated next.

Theorem 3.2 ([15], Thm 9.8.1).

The posterior distribution of given with is a Dirichlet distribution with parameter vector .

It should also be noted that the marginal distribution of the th component of a Dirichlet-distributed random vector with parameter , is Beta distributed with parameters and , compare [15, p. 50]. In particular . This fact implies immediately the following result.

Corollary 3.3.

The posterior distribution of given with is a Beta distribution with parameters and .

3.1. Filtering

Since the strategies have to be -predictable and -progressively measurable respectively, the task is to reduce the partially observable control problem (2.6) within the introduced framework to one with a state process that describes the available information about the unknown background intensity and interdependencies between the line of business. The conditional distribution of can immediately be derived from with Theorem 3.2. For the background intensity we determine a filter process. Throughout this paper, we denote by the càdlàg modification of the process and we write

| (3.2) |

Moreover, we denote by the -dimensional process defined by

The following result provides the dynamics of the filter process . It is a standard result and can be found e.g. in [11], [6].

Theorem 3.4.

For any , the process satisfies

| (3.3) |

Note that is a piecewise deterministic Markov process. With increasing time the filter converges against the true parameter exponentially fast (see e.g. [8]). Let and assume . Then the evolution of up to the next jump time is the solution, denoted by , of the following system of ordinary differential equations

| (3.4) |

and the new state of the filter at the jump times is

where

| (3.5) |

for .

Proposition 3.5.

The -intensity kernel of , denoted by , is given by

where is the -norm.

Proof.

First note that is a transition kernel. The -intensity is derived from the intensity by conditioning on . Note here in particular that (see Corollary 3.3) and . ∎

We denote by the compensated random measure given by

| (3.6) |

where is defined as in Proposition 3.5. Thus, we obtain the following indistinguishable representation of the surplus process :

| (3.7) | ||||

This dynamic will be one part of the reduced control model discussed in the next section.

3.2. The Reduced Control Problem

The processes in (3.2) and in (3.1) carry all relevant information about the unknown parameters and contained in the observable filtration of the insurer. Therefore, the state process of the reduced control problem with complete observation is the -dimensional process

where is given by (3.7), is given by (3.3) and is given by (3.1) for some fixed initial time and . We can now formulate the reduced control problem. For any , the value functions are given by

| (3.8) | ||||

where denotes the conditional expectation given . As before, an investment-reinsurance strategy is optimal if

4. The Solution

In a first step we derive the Hamilton-Jacobi-Bellman (HJB) equation. Using standard methods and assuming full differentiability of we obtain

| (4.1) | ||||

where . For solving (4.1) we apply the usual separation approach: For any , we assume

| (4.2) |

This implies that we conclude from (4.1)

| (4.3) | ||||

However, is probably not differentiable w.r.t. and , . Assuming is Lipschitz on for all , we can replace the partial derivatives of w.r.t. and , , by the generalized Clark gradient (see appendix). Throughout, we denote by an operator acting on functions and which is defined by

| (4.4) |

where

| (4.5) |

and

Using this operator and replacing the partial derivatives of w.r.t. and , , in (4.3) by the generalized Clarke gradient, we get the generalized HJB equation for :

| (4.6) |

for all with boundary condition

| (4.7) |

Note that we set at the points where the gradient exists. The notation indicates that the derivative is w.r.t. and for fixed .

4.1. Candidate for an Optimal Strategy

To obtain candidates for an optimal strategy, we rewrite the generalized HJB equation (4.6) as

| (4.8) | ||||

Hence we can conclude that the unique candidate of an optimal investment strategy is given by

| (4.9) |

The following lemma will yield the first order condition for a candidate of an optimal reinsurance strategy. In order to avoid confusion with a reinsurance strategy, we will use instead of as an argument for the function in the following.

Lemma 4.1.

For any , the function is strictly convex and

Proof.

Strict convexity follows since is the sum of a linear and a strictly convex function in . The derivative is straightforward. ∎

For any and , we define in case

| (4.10) | ||||

Furthermore, we set

Obviously . Setting to zero (c.f. Lemma 4.1), we obtain the first order condition

| (4.11) |

If a minimizer exists it is unique due to the strict convexity property of w.r.t. . The next proposition states that this equation is solvable and the solution takes values in depending on the safety loading parameter of the reinsurer.

Proposition 4.2.

For any , Equation (4.11) has a unique root w.r.t. , denoted by , which is increasing w.r.t. the safety loading parameter of the reinsurer . Moreover, it holds,

-

(a)

if ,

-

(b)

if ,

-

(c)

if .

Proof.

Note that is strictly increasing. The proof then follows from considering the zeros of (4.11) in when and when . ∎

Therefore, the proposition above provides the candidate for an optimal reinsurance strategy. For any , we set

| (4.12) |

Then the candidate for an optimal reinsurance strategy is given by .

4.2. Verification

This section is devoted to a verification theorem to ensure that the solution of the stated generalized HJB equation yields the value function (see Theorem 4.3). We also demonstrate an existence theorem of a solution of the HJB equation (see Theorem 4.5). Both proofs can be found in the appendix.

Theorem 4.3.

Suppose there exists a bounded function such that and are Lipschitz on for all as well as is concave for all . Furthermore, satisfies the generalized HJB equation (4.6) for all with boundary condition

| (4.13) |

Then

and with given by (4.9) and given by (4.12) (with replaced by in and ) is an optimal feedback strategy for the given optimization problem (), i.e. .

4.3. Existence result for the value function

We now show that there exists a function satisfying the conditions stated in Theorem 4.3. For this purpose let

| (4.14) |

where

| (4.15) | ||||

where denotes the conditional expectation given . The next lemma summarizes useful properties of . A proof can be found in the appendix.

Lemma 4.4.

The function defined by (4.14) has the following properties:

-

(a)

is bounded on by a constant and .

-

(b)

for all and .

-

(c)

is concave for all .

-

(d)

is Lipschitz on for all .

-

(e)

with is Lipschitz on for all .

Notice that denotes the th unit vector. We are now in the position to show the following existence result of a solution of the generalized HJB equation.

Theorem 4.5.

5. Comparison Results with the complete Information Case

First note that the case with complete information is always a special case of our general model. We obtain this case when the prior is concentrated on a single value. With complete information the optimal investment strategy is given by

which is exactly the same as in the case of partial observation. This is no surprise since the partial observation only concerns the reinsurance strategy. In order to state the optimal reinsurance strategy in the complete information case define for any and

| (5.1) |

with

| (5.2) |

Furthermore, we define

From now on, denotes the unique root of

| (5.3) |

which exists. By the same line of arguments as in Proposition 4.2, we obtain under the notation above that the optimal reinsurance strategy is given by

| (5.4) |

Note that , and are continuous in . Consequently, the optimal reinsurance strategy is continuous. Moreover, is deterministic and can be calculated easily.

We will now compare the reinsurance strategies. In order to do so, we need the following properties of (see appendix for the proof):

Lemma 5.1.

The function defined by (4.14) has the following properties for :

-

(a)

for all .

-

(b)

for all .

First of all we derive bounds for the optimal strategy which can be calculated a priori, i.e. independent of the filter process and the process . For this determination, we introduce the following terms. Let and . Throughout this section, we set

The proof of the next result is straightforward:

Proposition 5.2.

Let . Then and are strictly increasing and strictly convex. Furthermore,

This proposition justifies the following notation: For some fixed , we denote by the unique root of the equation w.r.t. , and by the unique root of the equation w.r.t. . The announced a-priori-bounds are a direct consequence of the following theorem in connection with Proposition 5.2.

Proposition 5.3.

For any and , we have for from (4.10)

Proof.

Choose some and . Recall that . For any , an application of Lemma 5.1 yields

Hence, by taking the infimum over all on both sides, we get . The other announced inequality is obtained in the same way. ∎

The proposition directly implies the following corollary:

Corollary 5.4.

The optimal reinsurance strategy from Theorem 4.5 has the following bounds:

These bounds provide only a rough estimate for the optimal reinsurance strategy. The next theorem provides the comparison statement. For this theorem we need the following assumption: From now on, we suppose that

| (5.5) |

where is a distribution on with existing moment generation function.

The next theorem is now the main statement of this section. It provides a comparison of the optimal reinsurance strategy to the optimal one in the case of complete information where the unknown quantities and are replaced by their expectations.

Theorem 5.5.

Proof.

For any , we define by

i.e. whereas the components of count the number of events where claims in set are affected, the components of count the number of events where lines are affected. Due to Assumption (5.5) contains the same information as . Thus, we can interpret as a function With a slight abuse of notation we keep the same name for the function. We also have that is increasing. We obtain from Lemma 5.1 a)

Next we can write this as

The inequality is due to Lemma 7.7 and the fact that and the second factor both are increasing in . The last expression can due to Lemma 5.1 b) be written as

Further we have

again by Lemma 7.7, Lemma 5.1 and the fact that and are increasing. Thus, we obtain

In summary, we have

which yields by taking the infimum over all on both sides and the proof follows by inspecting the minimum points. ∎

6. Numerical Results

In this section we illustrate some numerical results in the case of two lines of business (i.e. ). The set of possible background intensities is and the prior probability mass function of is supposed to be

Furthermore, we assume that the prior parameter of the Dirichlet distribution of the thinning probabilities is

Since we want to present the comparison result graphically, we choose the same claim size distribution for both business lines, namely a right-truncated exponential distribution with rate 1 and truncation at 3, i.e.

For the parameter of the premium principle, we choose

The remaining parameters are chosen as in Table 1.

| parameter | value |

|---|---|

| 100 | |

| 10 | |

| 0.01 | |

| 0.2 | |

| 3 | |

| 0.2 | |

| 0.4 | |

| 0.6 |

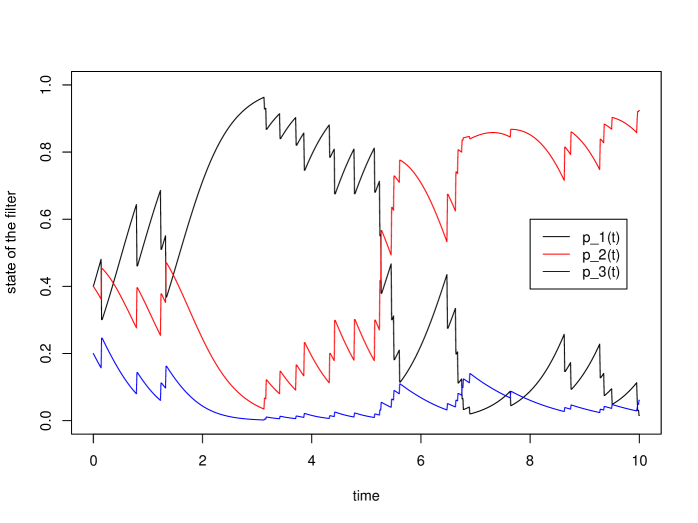

The following simulations are generated under the assumption that the realization of is and that the true background intensity is 4 (i.e. the realization of is 4). Trajectories of the filter can be seen in Figure 1. It is illustrative to see the fast convergence against the true parameter.

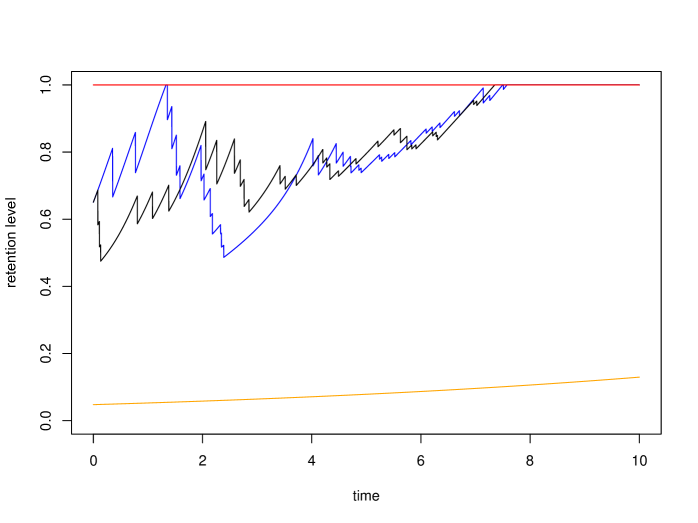

In Figure 2 the a-priori-bounds (red and orange) are illustrated together with two trajectories (black and blue) of the reinsurance strategy with and , which provide for each scenario an upper bound for the corresponding optimal reinsurance strategy according to Theorem 5.5. So the black and blue lines depend on the realized trigger arrival times and the affected business lines. In both scenarios, the upper bounds (black and blue) obtained from the comparison result are only useful up to approximaltely time 8. Before this, a strong dependence on the realizations can be seen. Only until the first trigger event both paths provide the same bound.

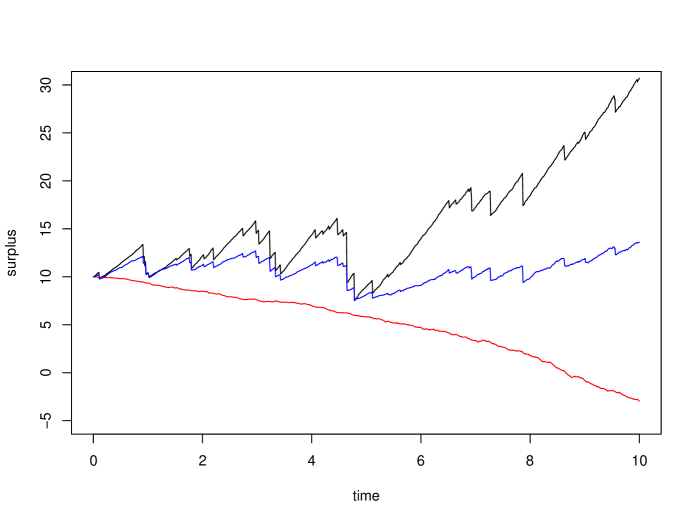

Concluding the numerical illustration, we show the path of the surplus process in an insurance loss scenario for three different insurance strategies in Figure 3. In the case of full reinsurance (i.e. retention level of 0) the trajectory of the surplus process tends downwards (red) due to a negative premium rate. The blue line displays a trajectory of the surplus for a constant reinsurance strategy of 0.5 and the black line for the reinsurance strategy with and . From Figure 2, we known that the latter reinsurance strategy tends upwards, which is evident in Figure 3 since jump sizes of the black line are higher at the end of the considered time interval than those of the blue line. But because of the lower level of reinsurance, the surplus between losses rises stronger (as the premium rate is higher) than in the case of the constant reinsurance strategy.

7. Appendix

7.1. The Generalized Clark Gradient

The following definition and results are taken from Section 2.1 in [13].

Definition 7.1 ([13], p. 25).

Let be a given point and let . Moreover, let be Lipschitz near . Then the generalized directional derivative of at in the direction , denoted by , is defined by

Definition 7.2 ([13], p. 27).

Let be Lipschitz near . Then the generalized Clarke gradient of at , denoted by , is given by

In the following, we denote by the differential operator taking the partial derivative of the function .

Proposition 7.3 ([13], Prop. 2.2.4).

If is strictly differentiable at , then is Lipschitz near and . Conversely, if is Lipschitz near and reduces to a singleton , then is strictly differentiable at and .

In what follows we denote by the set of point at which the function is is not differentiable.

Theorem 7.4 ([13], Thm. 2.5.1).

Let be Lipschitz near and let be an arbitrary set of Lebesgue-measure in . Then

7.2. Auxiliray Results

Detailed calculations can be found in [21].

Lemma 7.5.

Suppose that is an arbitrary strategy and is a bounded function such that and are absolutely continuous on for all as well as is concave for all . Then, the function defined by

satisfies

where is a -martingale and we set zero at those points where does not exist.

Proof.

Let and be some function satisfying the conditions stated in the lemma, where is some constant which bounds , i.e. for all . Furthermore, we set

| (7.1) |

for any . Let us fix . Applying the product rule to , we get

and hence,

| (7.2) | ||||

Using the introduced compensated random measure the variation becomes

Substituting this into (7.2), we obtain

where Therefore, by definition of the operator given in (7.4), we have

where with

To complete the proof we need to show that the introduced processes are -martingales on . For details we refer the reader to [21]. ∎

Lemma 7.6.

Let be the function defined by (7.1). Furthermore, let where is only adapted w.r.t. and is predictable w.r.t. the filtration generated by and let be the density process given by

Then there exists a constant such that

for all .

Proof.

Fix and . We obtain

where is independent of as well as . ∎

The following result can be found in [24].

Lemma 7.7.

Let and be real numbers and . Then

7.3. Proofs

For convenience we introduce the operator acting on functions by

| (7.3) |

for all functions , where the right-hand side exists. Furthermore, we define an operator

| (7.4) |

for all functions and , where the right-hand side is well-defined. Using this notation, the generalized HJB equation (4.6) can be written as

| (7.5) |

at those points with existing .

Proof of Theorem 4.3.

Let be a function satisfying the conditions stated in the theorem. Note that every Lipschitz function is also absolutely continuous. We set, for any ,

Let us fix and . From Lemma 7.5 in the appendix, it follows

| (7.6) |

where is a -martingale and we set to zero at those points where does not exist. Note that is partially differentiable w.r.t. almost everywhere in the sense of the Lebesgue measure according to the absolute continuity of for all . The generalized HJB equation (7.5) implies

As a consequence

due to the negativity of . Thus, by (7.6), we get

| (7.7) |

Using the boundary condition (4.13), we obtain

Now, we take the regular conditional expectation in (7.7) given , and on both sides of the inequality which yields

since is a -martingale. Taking the supremum over all investment and reinsurance strategies , we obtain

| (7.8) |

To show equality, note that given by (4.9) and given by (4.12) (with replaced by in and ) are the unique minimizer of the HJB equation (4.6). Therefore,

So we can deduce that

This implies

Consequently,

Again, taking the regular conditional expectation given and on both sides then yields

and the proof is complete. ∎

Proof of Lemma 4.4.

-

(a)

By the definition of we immediately obtain . In order to show that is bounded from above we consider the strategy . What remains is

To show that we use the change of measure introduced in Lemma 7.6. With its help it is possible to prove that is bounded from below by a positive constant independent of and .

-

(b)

Follows by conditioning.

-

(c)

Let us fix and and . Suppose . We obtain

for all and .

-

(d)

The Lipschitz condition is proven in much the same way as in [6, Lemma 6.1 d)].

-

(e)

The Lipschitz condition is proven in much the same way as in [6, Lemma 6.1 e)]. ∎

Proof of Theorem 4.5.

Fix and and set , Let be the first jump time of after and . It follows from Lemma 7.5 and Lemma 4.4 that

| (7.9) | ||||

where is a -martingale and we set to zero at those where the does not exist. For any we can construct a strategy with for all from the continuity of such that

From the arbitrariness of we conclude

Using this statement and (7.9) we obtain

We have

Thus

Consequently,

By the dominated convergence theorem, we can interchange the limit and the expectation and we obtain by the fundamental theorem of Lebesgue calculus and for ,

From now on, let and as well as be a fixed strategy with for . Then

at those points where exists. Due to the negativity of , we get

We show next the inequality above if does not exist. For this purpose, we denote by the set of points at which exists for any . On the basis of Theorem 7.4, we have, for any ,

That is, for every , there exists and such that , where for sequences with along existing . From what has already been proved, it can be concluded that, for any

where denotes the th component of the -dimensional vector . Thus, by the continuity of , and , we get for

which yields

Due to the arbitrariness of and , we obtain

Our next objective is to establish the reverse inequality. For any and , there exists a strategy such that

Using Lemma 7.5 it follows

In the same way as before, we get

We can again interchange the limit and the infimum by the dominated convergence theorem which yields

Thus the same conclusion can be draw as above, i.e.

at those point where exists. According to the negativity of and the arbitrariness of , we get, by ,

at those point where exists. By the same way as before, we obtain in the case of no differentiability of w.r.t. and , , that

Summarizing, we have equality in the previous expression. The optimality of follows as in the proof of Theorem 4.3. ∎

References

- [1] H. Albrecher and S. Asmussen, Ruin Probabilities, World Scientific, Singapore, 2010.

- [2] L. Bai, J. Cai and M. Zhou, Optimal reinsurance policies for an insurer with a bivariate reserve risk process in a dynamic setting, Insurance: Mathematics and Economics 53(3), 664–670, 2013.

- [3] N. Bäuerle, N. and A. Blatter, Optimal control and dependence modeling of insurance portfolios with Lévy dynamics. Insurance: Mathematics and Economics 48(3), 398–405, 2011.

- [4] N. Bäuerle and R. Grübel, Multivariate Counting Processes: Copulas and Beyond, Advances in Applied Probability 35(2), 379–408, 2005.

- [5] N. Bäuerle and R. Grübel, Multivariate risk processes with interacting intensities, Advances in Applied Probability 40(2), 578–601, 2008.

- [6] N. Bäuerle and U. Rieder, Portfolio optimization with jumps and unobservable intensity, Mathematical Finance 17(2), 205–224, 2007.

- [7] N. Bäuerle and U. Rieder, Markov Decision Processes under Ambiguity. Banach Center Publications 2020.

- [8] P. Baxendale, P. Chigansky and R. Liptser, Asymptotic stability of the Wonham filter: ergodic and nonergodic signals, AIAM J. Control Opt., 43(2), 643–669, 2004.

- [9] J. Bi and K. Chen, Optimal investment-reinsurance problems with common shock dependent risks under two kinds of premium principles, RAIRO Operations Research 53(1), 179–206, 2019.

- [10] T. Bielecki and S.R. Pliska, Economic properties of the risk sensitive criterion for portfolio management. Rev. Account. Fin. 2, 3–17, 2003.

- [11] P. Brémaud, Point processes and queues, Springer-Verlag, New York, 1981.

- [12] M. Centeno, Dependent risks and excess of loss reinsurance, Insurance: Mathematics and Economics 37(2), 229–238, 2005.

- [13] F.H. Clarke, Optimization and nonsmooth analysis, Canadian Mathematical Society series of monographs and advanced texts - A Wiley-Interscience publication, New York, 1983.

- [14] P. Dai Pra, L. Meneghini, and W.J. Runggaldier. Connections between stochastic control and dynamic games. Mathematics of Control, Signals and Systems 9(4), 303–326, 1996.

- [15] M.H. DeGroot, Optimal statistical decisions. John Wiley & Sons, 2005.

- [16] E.Faust and E.Rauch, Series of hot years and more extreme weather. Available online: https://www.munichre.com/topics-online/en/climate-change-and-natural-disasters/climate-change/climate-change-heat-records-and-extreme-weather.html (accessed on 18 December 2019).

- [17] J. Grandell, Aspects of Risk Theory. Springer Series in Statistics, New York, 1991.

- [18] A. Gu, F.G. Viens and H. Yao, Optimal robust reinsurance-investment strategies for insurers with mean reversion and mispricing. Insurance: Mathematics and Economics, 80, 93–109, 2018.

- [19] A. Gu, F.G. Viens and B.Yi, Optimal reinsurance and investment strategies for insurers with mispricing and model ambiguity. Insurance: Mathematics and Economics, 72, 235–249, 2017.

- [20] J. Jacod, Multivariate point processes: predictable projection, Radon-Nikodym derivatives, representation of martingales. Probability Theory and Related Fields 31(3), 235–253, 1975.

- [21] G. Leimcke, Bayesian Optimal Investment and Reinsurance to Maximize Exponential Utility of Terminal Wealth for an Insurer with Various Lines of Business. PhD Thesis, Karlsruhe Institute of Technology, 2020.

- [22] Z. Liang and E. Bayraktar, Optimal reinsurance and investment with unobservable claim size and intensity. Insurance: Mathematics and Economics 55, 156–166, 2014.

- [23] Z. Liang and K.C. Yuen, Optimal dynamic reinsurance with dependent risks: variance premium principle, Scandinavian Actuarial Journal 2016(1), 18–36, 2016.

- [24] D.S. Mitrinovic, J. Pecaric and A.M. Fink, Classical and New Inequalities in Analysis. Mathematics and its Applications. Kluwer Academic Publishers, Dordrecht, 1993.

- [25] M. Scherer and D. Selch, A Multivariate Claim Count Model for Applications in Insurance, Springer International Publishing, Springer Actuarial, 2018.

- [26] H. Schmidli, On minimizing the ruin probability by investment and reinsurance. The Annals of Applied Probability 3, 890–907, 2002.

- [27] A. Segall and T. Kailath, Radon-Nikodym derivatives with respect to measures induced by discontinuous independent-increment processes. The Annals of Probability 449-464, 1975.

- [28] W. Wei, Z. Liang and K.C. Yuen, Optimal reinsurance in a compound Poisson risk model with dependence, Journal of Applied Mathematics and Computing 58, 1–24, 2017.

- [29] K.C. Yuen, Z. Liang abd M.Zhou, Optimal proportional reinsurance with common shock dependence, Insurance: Mathematics and Economics 64, 1–13, 2015.

- [30] X. Zhang and T.K. Siu, Optimal investment and reinsurance of an insurer with model uncertainty. Insurance: Mathematics and Economics, 45(1), 81–88, 2009.

- [31] X. Zheng, J. Zhou and Z. Sun, Robust optimal portfolio and proportional reinsurance for an insurer under a CEV model. Insurance: Mathematics and Economics 67, 77–87, 2016.

- [32] S. Zhu and J. Shi, Optimal Reinsurance and Investment Strategies under Mean-Variance Criteria: Partial and Full Information, arXiv.org, 2019.