How Safe are European Safe Bonds? An Analysis from the Perspective of Modern Credit Risk Models 111We are grateful to Sam Langfield and to two anonymous referees for very useful comments and suggestions.

Rüdiger Frey, Kevin Kurt, Camilla Damian,222Email: ruediger.frey@wu.ac.at, kevin.kurt@wu.ac.at, camilla.damian@wu.ac.at.

Institute for Statistics and Mathematics, Vienna University of Economics and Business (WU)333Postal address: Welthandelsplatz 1, A-1020 Vienna

Abstract

Several proposals for the reform of the euro area advocate the creation of a market in synthetic securities backed by portfolios of sovereign bonds. Most debated are the so-called European Safe Bonds or ESBies proposed by \citeasnounbib:brunnermeier-et-al-17. The potential benefits of ESBies and other bond-backed securities hinge on the assertion that these products are really safe. In this paper we provide a comprehensive quantitative study of the risks associated with ESBies and related products, using an affine credit risk model with regime switching as vehicle for our analysis. We discuss a recent proposal of Standard and Poors for the rating of ESBies, we analyse the impact of model parameters and attachment points on the size and the volatility of the credit spread of ESBies and we consider several approaches to assess the market risk of ESBies. Moreover, we compare ESBies to synthetic securities created by pooling the senior tranche of national bonds as suggested by \citeasnounbib:leandro-zettelmeyer-19. The paper concludes with a brief discussion of the policy implications from our analysis.

Keywords.

European Safe Bonds, European monetary union, Securitization of credit risk, Markov modulated affine models

1 Introduction

Synthetic securities backed by portfolios of sovereign bonds from the euro area have recently been proposed as a tool to improve the stability of the European monetary union and to increase the amount of safe assets in the euro area, see for instance \citeasnounbib:EU-17 or \citeasnounbib:cepr-on-euro-18. The most debated proposal is due to \citeasnounbib:brunnermeier-et-al-17, who advocate the creation of a market in so-called European Safe Bonds or ESBies. In credit risk terminology, ESBies form the senior tranche of a CDO backed by a diversified portfolio of sovereign bonds from all members of the euro area. According to \citeasnounbib:brunnermeier-et-al-17, ESBies would be standardized and issued by tightly regulated private institutions or by a public agency. The junior tranche of the underlying bond portfolio would be sold in the form of European Junior Bonds (EJBies) to investors traditionally bearing default risk, such as hedge funds or insurance companies.

bib:brunnermeier-et-al-17 argue that a liquid market in ESBies would enhance the stability of the euro area in a number of ways: first, it would increase the supply of safe assets in the euro area; second, it would help to break the vicious circle between bank solvency and the credit quality of sovereigns created by the fact that most euro area banks hold large amounts of risky sovereign bonds of the nation state in which they reside; third, it might reduce the distortions on bond markets caused by the flight-to-safety behavior of investors in crisis times. Moreover, ESBies respect the no-bailout clause and their introduction would not distort market discipline, as the agency issuing ESBies would buy these bonds at market prices and as sovereigns would remain responsible for their own bonds, which exerts discipline on borrowing decisions. Another important approach for creating a safe asset for the euro area consistent with the no-bailout clause is to issue national sovereign bonds in several seniority levels and to pool the bonds from the senior tranche, see for instance \citeasnounbib:leandro-zettelmeyer-19. These products and ESBies are therefore different from eurobonds that are currently discussed in the context of the Corona crisis. Eurobonds are jointly issued and guaranteed by all euro area member states so that every member state is liable for the entire issuance. Loosely speaking, ESBies are designed for improving the functioning of the euro area “in normal times”, whereas eurobonds are crisis-intervention instruments.

The potential benefits of ESBies hinge on the assertion that these products are really safe. To address this issue, \citeasnounbib:brunnermeier-et-al-17 carry out a simulation study in an one-period mixture model where defaults are independent given the aggregate state of the euro area economy. They find that, with reasonably high levels of subordination, the expected loss of ESBies is comparable to that of triple-A rated bonds. However, their model is calibrated in a fairly ad hoc manner. More importantly, \citeasnounbib:brunnermeier-et-al-17 do not study the market risk of ESBies (the risk of a change in the market value of these products due to changes in the credit quality of the underlying bonds or in the state of the euro area economy). Now, the bad performance of many highly rated rated senior CDO tranches during the financial crisis has shown that the market risk of such products can be substantial. Clearly, a high amount of market risk is inappropriate for a safe asset intended to serve as collateral in security market transactions, as an investment vehicle for money market funds or as a crisis-resilient store of value on the balance sheet of banks. A thorough quantitative analysis of the risks associated with ESBies is thus needed to assess if these securities can in fact perform the function of a safe asset for the euro area. This is the aim of the present paper.

We propose to work in a novel dynamic credit risk model that captures salient features of the credit spread dynamics of euro area member states and that is at the same time fairly tractable. Such a model is a prerequisite for the analysis of the market risk associated with ESBies. In mathematical terms, we consider a reduced-form model with conditionally independent default times; the hazard rate or default intensity of the different obligors is modelled by CIR-type processes whose mean-reversion level is a function of a common finite state Markov chain. Considering a Markov modulated mean-reversion level permits us to model different regimes, such as a crisis regime where the default intensity of all sovereigns is high and an expansionary regime where all default intensities are low. This generates default dependence in a natural way. We successfully calibrate the model to a time series of euro area CDS spreads over the period January 2009 until September 2018. The main part of the paper is devoted to the risk analysis of ESBies and EJBies. We begin by discussing a recent proposal of S&P for the rating of ESBies, see \citeasnounKraemer2017HowESBies. Using novel results on model-independent price bounds for ESBies, we show that the S&P proposal is ultra-conservative in the sense that it attributes to an ESB the worst rating that is logically consistent with the ratings attributed to the euro area sovereigns. As a next step, we study the robustness of the credit spread (or equivalently the risk-neutral expected loss) of ESBies and EJBies with respect to subordination levels and model parameters. In particular, we consider several parameterizations for the transition intensities of the common Markov chain, as these largely drive the default dependence in our model. It turns out that, from this perspective, ESBies are very safe already for low subordination levels (around 15%), in line with the findings of \citeasnounbib:brunnermeier-et-al-17.

We use several approaches to gauge the market risk of ESBies. First, we compute spread-trajectories for ESBies via historical simulation, using as input the calibrated trajectories of the default intensities and of the common Markov chain, and we analyse the relation between the attachment point of an ESB and the volatility of the ESB-spreads. Second, we carry out a scenario analysis and study how the risk-neutral default probability of these products is affected by changes in the underlying risk factors. To robustify our conclusions, we consider also various contagion scenarios. The results of this analysis are more nuanced. For low subordination levels and adverse scenarios (such as the case where the default of a major euro area sovereign leads to a recession in the euro area), the loss probability of ESBies can be fairly large and spread trajectories can be quite volatile. For high subordination levels exceeding 30–35%, on the other hand, ESBies remain ‘safe’ even in these adverse scenarios. Third, we compare the risk characteristics of ESBies to those of a safe asset created by pooling the senior tranche of national bonds. Finally, we use simulations to compute value at risk and expected shortfall for the return distribution of ESBies. For this we need to estimate the historical dynamics of the default intensities and the common Markov chain which is done via a suitable variant of the EM algorithm. From this perspective, the market risk of ESBies is fairly low. Summarizing, we find that while in normal times ESBies are indeed very safe (in fact safer than assets created by pooling the senior tranche of national bonds), they may become risky under extreme circumstances and in contagion scenarios, in particular if the attachment point is not sufficiently high.

We continue with a discussion of the relevant literature. The report of the \citeasnounbib:ESRB-18 extends the quantitative analysis of \citeasnounbib:brunnermeier-et-al-17 and considers risk and return characteristics of ESBies and EJBies in various stress scenarios for default correlation and loss given default; similar issues are studied in \citeasnounbib:barucci-brigo-19 in the context of standard copula models for defaults. The relevance of market risk for ESBies is discussed verbally in \citeasnounbib:grauwe-ji-19. An interesting quantitative analysis of the market associated with ESBies is \citeasnounbib:de-sola-perea-et-al-19. They compute hypothetical spread trajectories for tranches of sovereign bond-backed securities in a copula framework, using observed bond spreads as input. Techniques from time series analysis (a VAR for VaR analysis and multivariate GARCH modelling) are used to compute value at risk and marginal expected shortfall for the daily spread change of these tranches. Further interesting contributions on sovereign bond-backed securities for the euro area are \citeasnounbib:langfield-20 or \citeasnounbib:cronin-dunne-19.

Our work is also related to other strands of the literature on sovereign credit risk, securitization and financial innovation. \citeasnounAng2013SystemicEurope and \citeasnounbib:aitsahalia-et-al-14 carry out interesting empirical work on euro area credit spreads. \citeasnounbib:brigo-et-al-10 give an extensive discussion of CDO pricing models and their empirical properties before and during the financial crisis, see also \citeasnounbib:mcneil-frey-embrechts-15. We also use insights from \citeasnounbib:gennaioli-shleifer-vishny-12 or \citeasnounbib:golec-perotti-17 regarding safe assets and financial innovation. Mathematical results on affine processes with Markov modulated mean reversion level can be found in \citeasnounbib:elliott-siu-09 and in \citeasnounbib:vanBeek-et-al-20.

The remainder of the paper is structured as follows. In Section 2 we formally introduce the model and the relevant credit products. Section 3 outlines the calibration of our model to market data. The main part of the paper is Section 4 where we carry out a thorough analysis of the risks associated with ESBies: in Section 4.1 we discuss the proposal for the rating of ESBies and we relate this to model-independent price bounds, Section 4.2 focuses on expected loss, while Sections 4.3 to 4.6 deal with the market risk of ESBies. In Section 5 we summarize the findings from the risk analysis and discuss policy implications.

2 The Setup

Default model.

Throughout we consider a portfolio of sovereigns with default times and default indicators , , defined on a probability space with filtration . is the global filtration, that is all processes introduced are adapted. In financial terms the -field describes the information available to investors at time . We assume that supports a -dimensional standard Brownian motion and a finite-state Markov chain , independent of , with state space and generator matrix . The chain will be used to model transitions between different states or regimes of the euro area economy, and for , gives the intensity of a jump from state to state . The measure is the risk-neutral measure used for the valuation of ESBies; price dynamics under the historical measure are considered in Section 4.6. In the analysis of the model we also use the filtration that is generated by the Brownian motion and the Markov chain .

Our default model under the pricing measure is outlined in the following two assumptions.

- A1)

-

The default times are conditionally independent doubly stochastic default times with adapted hazard rate processes , see for instance \citeasnoun[Chapter 17]bib:mcneil-frey-embrechts-15. In mathematical terms, for all it holds that

- A2)

-

The processes follow CIR-type dynamics with Markov modulated and time-dependent mean-reversion level, that is

(2.1) for constants and functions . For notational convenience, we introduce the vector process .

Discussion.

For small the quantity gives the probability that firm defaults in the period , that is is the default intensity of firm . Assumption A1 implies that given the path of the hazard rate process, are independent default times. Dependence of default events is caused by the special form of the hazard rate dynamics in A2. More precisely, the assumption that the mean-reversion levels of the hazard rate processes depend on the common finite-state Markov chain creates co-movement in the hazard rate of different sovereigns, so that, unconditionally, default times are dependent. Our setup permits also country-specific fluctuations in hazard rates; these are generated by the independent Brownian motions driving the hazard rate dynamics. Adding the factor implies that the mean-reversion level of the hazard rates is upward-sloping between transitions of . This helps to calibrate the model to the observed term structures of sovereign CDS spreads which are typically upward-sloping as well; see Section 3 for details.

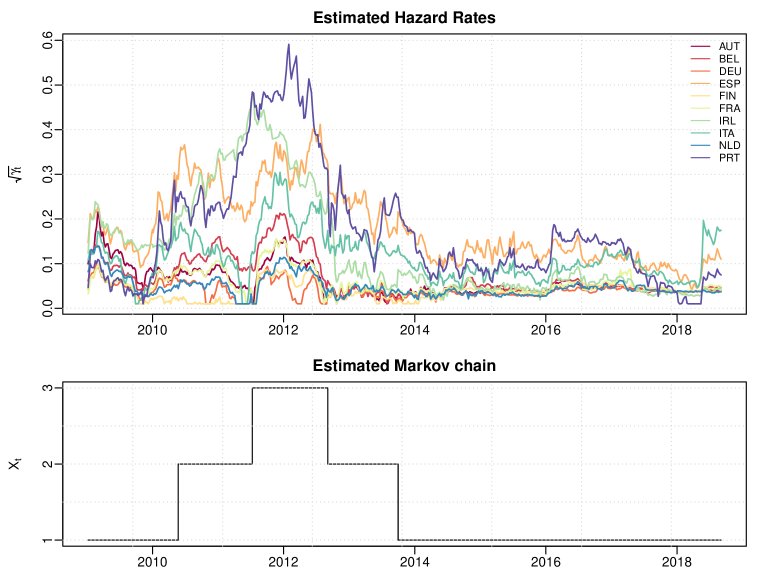

Following \citeasnounbib:brunnermeier-et-al-17, we usually consider states of the euro area economy. In the model calibration in Section 3 we find that, for the vast majority of euro area members, ; that is, the mean reversion level of the hazard rates of euro area members is lowest in state one and highest in state three. This allows us to interpret these states as expansion (state one), mild recession (state two) and strong recession (state three). A statistical analysis in Section 4.6 shows that a model of the form (2.1) with states can also be used to describe the evolution of the calibrated hazard rates under the historical measure .

The default model outlined in Assumptions A1) and A2) is well-suited for a risk analysis of ESBies. In contrast to the copula models used for instance in \citeasnounbib:barucci-brigo-19 or in the work of the \citeasnounbib:ESRB-18, we model the dynamic evolution of hazard rates and credit spreads. This allows us to generate future spread trajectories, which is important in the analysis of market risk. By assuming that the hazard rates depend on the common state of the Euro area economy we generate default dependence in a natural way. This gives a lot of flexibility for the valuation of ESBies. In fact, the whole range of arbitrage-free prices of ESBies and EJBies consistent with observed CDS spreads can be obtained within our model if parameters are chosen appropriately; see Section 4.1 for details. At the same time the model is fairly tractable: due to the conditional independence assumption it is possible to calibrate the model simultaneously to CDS spreads of all euro area sovereigns444Without conditional independence, the price of single-name credit derivatives depends on the default state and the hazard rate of other sovereigns in the portfolio, and the calibration of the model to single-name CDS spreads is practically possible only for very small portfolios. For instance, in the Hawkes process model of \citeasnounbib:aitsahalia-et-al-14 spillover effects are only studied for the bivariate case. and the form of hazard rate dynamics allows for a fairly efficient computation of credit derivative prices.

On the other hand, our pricing model with conditionally independent defaults does not allow for contagion effects (upward jumps in the credit spreads of non-defaulted sovereigns in reaction to a default event in the euro area), which might arise if insufficient measures are taken to mitigate the economic fallout from the default of a major euro area member, see \citeasnounbib:cepr-on-euro-18. This is, however, not an issue for studying the risks associated with ESBies. In fact, with appropriately chosen hazard rate dynamics our pricing model is able to generate arbitrarily conservative (low) valuations for ESBies. Moreover, contagion matters most in the analysis of short term price fluctuations and market risk in Section 4.4, and we do consider contagion scenarios in that context.

Loss process and credit default swaps.

The payoff of credit default swaps (CDSs), ESBies and EJBies depends on the exact form of the losses generated by defaults in the underlying sovereign-debt portfolio. Next we therefore describe the mathematical model for the loss processes that we use in our analysis. We fix a horizon and a set of payment dates which, in practical applications, usually correspond to quarterly payments. We define for the cumulative loss process of sovereign by

| (2.2) |

where the random variable gives the loss given default (LGD) of sovereign at time .555We prefer to work with (2.2) instead of the more standard definition as (2.2) is more convenient for CDS pricing. In any case, for small the two definitions of are close to each other. We assume that, given , the LGD is beta distributed with for a function . We further assume that, given , is independent of all other model quantities. Working with a random LGD is realistic and, at the same time, helps to robustify our analysis with respect to the exact values chosen for . Given portfolio weights such that , we define the portfolio loss by

| (2.3) |

The cash flow stream of the protection-buyer position in a CDS on sovereign with spread and premium payment dates can be described in terms of the process ; it is given by

| (2.4) |

ESBies and EJBies.

ESBies have not been issued so far, so there is no description of the payment structure of an actual product and no term sheet. Therefore, we consider stylized versions of these products. These stylized ESBies and EJBies do capture the essential features of every CDO structure, namely pooling and tranching of default risk, so they suffice to analyze the qualitative properties of ESBies. Denote by the normalized value of the asset pool and note that if there are no defaults in the portfolio. The constant denotes the lower (upper) attachment point of the senior (junior) tranche. Then the payoff of a stylized ESB respectively a stylized EJB at is defined to be

| (2.5) | ||||

| (2.6) |

In this way, the EJB bears the first percent of the loss in the portfolio, if the loss exceeds , the ESB is affected as well. While stylized ESBies and EJBies are path independent, in the sense that their payoff is a function of the portfolio loss at the maturity date only, our analysis is easily extended to path dependent payoffs.

Note that, by definition, we have the following put-call-parity-type relation for the payoff of a stylized ESB and a stylized EJB with identical attachment point

| (2.7) |

Pricing.

For simplicity, we assume that the risk-free short rate is constant and equal to . We introduce the money market account , , so that is the discount factor at time for a payoff due at time . We use standard risk-neutral valuation for the pricing of credit derivatives. Hence the price at of any integrable measurable contingent claim is equal to , where the expectation is taken under the risk-neutral measure .

For further use we introduce some notation related to the pricing of ESBies. Let . The price of an ESB at time is given by

| (2.8) |

for a suitable function . This follows from the fact that the processes are jointly Markov; we omit the details. Similarly, the price of an EJB is given by

| (2.9) |

The key tool for the numerical computation of derivative prices is the extended Laplace transform of the hazard rates. For Markov modulated CIR processes this transform is available in almost closed form; see Appendix A for details.

3 Calibration

Data and calibration design.

The available data consist of weekly CDS spread quotes from ICE data services for ten euro area sovereigns and times-to-maturity equal to 1, 2, 3, 4 and 5 years over the period January 7, 2009 until September 3, 2018, giving rise to 510 observation dates. The sovereigns used in our analysis are Austria (AUT), Belgium (BEL), Germany (DEU), Spain (ESP), Finland (FIN), France (FRA), the Republic of Ireland (IRL), Italy (ITA), the Netherlands (NLD) and Portugal (PRT), making up more than 90% of the euro area GDP in 2018. Table 4 reports summary statistics (sample mean, sample standard deviation, minimum and maximum) of the CDS spreads, together with the most recent Standard & Poor’s credit-rating of the ten sovereigns. Average spreads vary considerably across countries and, with the exception of Ireland, the term structures of the average spreads is upward sloping.

We calibrate the model by minimizing the sum of squared differences between the CDS spreads observed on the market and the spreads generated by the model. In order to reduce the dimension of the parameter space, we fix the mean function and the concentration parameter of the beta distribution of the loss given default at the outset.666The parametrization in terms of mean and concentration parameter is a useful alternative to the standard representation of the beta distribution. Denote by the beta density for given parameters . Then the mean is given by and the concentration parameter is . A high value of implies that the LGD is very concentrated around its conditional mean. The distinct values for the mean function can be found in Table 5 in the appendix. Following \citeasnounbib:brunnermeier-et-al-17 we assume that the mean LGD is highest in state 3 (the recession state) and lowest in state 1. Moreover, we work with a concentration parameter ; this is a conservative choice as it leads to a fairly widespread LGD distribution (and we will see in Section 4 that a widespread LGD distribution makes ESBies riskier). While the order of magnitude of the mean LGD is in line with the sovereign-debt literature, the exact numerical values for the mean LGD and the concentration parameter were handpicked by the authors.777In fact, cannot be calibrated from CDS spreads, since model CDS spreads depend only on the conditional mean of the LGD. In Section 4.5 we therefore study the robustness of our risk analysis with respect to the parameters of the LGD distribution.

In the calibration we work with states of and we use the EONIA at date as a proxy for . We have to determine the trajectories of and and the parameters with . We impose the restriction that all parameters are nonnegative, and, to preserve the interpretation of as mean-reversion level, we impose the uniform lower bound for all . We use to denote the observation dates and we write and for trajectories of and . Denote by the market CDS spread with time to maturity at time and by the corresponding model spread as function of , and of the model parameters. We determine the model parameters and the realized trajectories and by minimizing the global calibration error

using a set of modern optimization algorithms. For this we use an iterative approach which is described in detail in Appendix C.

Results.

We implement the calibration methodology on the full time series of available CDS data. We use maturities of one and five years since one-year CDS spreads are particularly informative regarding the current value of the hazard rates whereas five-year CDS markets are most liquid. To assess the quality of the calibration, we report in Table 1 the root mean squared error (RMSE) for all countries and both maturities. As RMSE is scale-dependent, we also report a relative measure for the calibration error, namely the mean absolute percentage error (MAPE). The quality of the calibration is illustrated further in Figure 9 in Appendix C, where we plot the time series of CDS spreads together with the model prices and the absolute pricing errors for the Germany and Italy. Given the complexity of the calibration task, we conclude that the calibrated model fits the observed CDS spreads reasonably well.

| Mat. | AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|---|

| RMSE (bp) | ||||||||||

| 1 | ||||||||||

| 5 | ||||||||||

| MAPE () | ||||||||||

| 1 | ||||||||||

| 5 | ||||||||||

Tables 2 and 3 report the parameter values resulting from the calibration. First, note that for all sovereigns except Germany, where .888This reverse ordering is easily explained by Germany’s prominent role as the euro area’s safe haven in times of financial distress. The uniform ordering of the mean-reversion levels allows us to interpret the states of as expansion, mild and strong recession, and it provides clear evidence that there is strong co-movement in the market’s perception of the credit quality of euro area members. The resulting ordering of the mean reversion levels is also in line with the empirical findings of \citeasnounbib:altman-05, who show that the LGD of corporate bonds is typically positively correlated with their respective default rates (recall that the mean function of the LGD satisfies for all sovereigns). The mean reversion speed is quite low for all countries, and for four of them (Austria, Belgium, Finland and France) it is equal to the exogenously imposed lower bound of . Consequently, market participants expect idiosyncratic credit shocks to have a long-lasting effect across the term structure of CDS spreads. The motivation for including the parameter is to better capture the upward sloping term structure of most of the CDS series. In fact, for and unrestricted , the calibration frequently leads to negative values for — a common phenomenon also reported e.g. in \citeasnounAng2013SystemicEurope. Table 3 reports the estimate of the generator matrix . Note that, for the estimated , transitions to non-neighbouring states have zero probability.

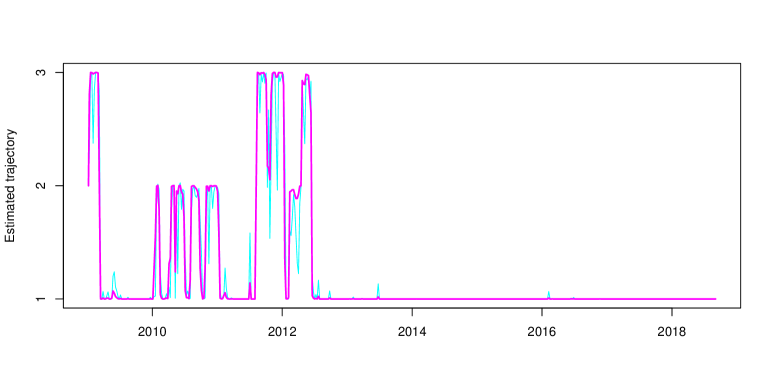

Figure 1 plots the calibrated hazard rates together with the calibrated trajectory of the Markov chain . The process remains in state one for most of the sample period, the only exceptions occur at the height of the European sovereign debt crisis from mid-2010 until late 2013, when the chain visits states two and three before settling in state one again. In general, the paths of the hazard rates are in line with the movement of the Markov chain; exceptional individual events such as the rise of the Portuguese hazard rates at the beginning of 2016 or the sudden upward movement of Italian rates during mid-2018 are of idiosyncratic nature.

| Param. | AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|---|

| State 1 | State 2 | State 3 | |

|---|---|---|---|

| State 1 (expansion) | |||

| State 2 (mild recession) | |||

| State 3 (strong recession) |

4 Risk analysis

After the successful calibration of our model, we may now analyze the risks associated with ESBies. We begin with a short overview. In Section 4.1 we discuss a recent proposal of the rating agency Standard and Poors (S&P) for the rating of ESBies (\citeasnounKraemer2017HowESBies) and we relate the S&P proposal to a worst-case default scenario where the arbitrage-free price of ESBies attains its lower bound. In Section 4.2 we compute the risk-neutral expected loss (or equivalently the credit spread) of ESBies as a function of the attachment point for different parameter sets. We consider a base parameter set corresponding largely to the parameters obtained in the model calibration of Section 3, two crisis sets with higher default correlation and an extremal distribution that corresponds to the worst-case default scenario.

The subprime credit crisis has shown that the expected loss at maturity gives only limited information regarding the riskiness of tranched credit products such as ESBies. In fact, the market value of AAA-rated senior tranches of mortgage backed securities (MBS) fell sharply during the crisis (some were even downgraded), creating huge losses for many MBS investors. To analyze if ESBies can perform all functions of a safe asset, we thus need to take a closer look at the associated market risk. We do this in several ways. First, we use a historical simulation approach and compute credit spread trajectories of ESBies for different attachment points, using as input the calibrated trajectories and from Section 3. This analysis gives useful information on the relation between and the volatility of ESB credit spreads. Second, many potential ESB investors, such as managers of money market funds, are extremely risk averse so that “behavior in (quasi) safe asset markets may be subject to sudden runs when new information suggests even a minimal chance of a loss” [bib:golec-perotti-17]. In Section 4.4 we therefore study how the risk-neutral loss probability of ESBies is affected by changes in the underlying risk factors. To guard against model misspecification and to incorporate stylized facts regarding investor behavior on markets for safe assets, we include various contagion scenarios into this analysis. Third, we compare the risk profile of ESBies to that of a safe asset created by pooling the senior tranche of national bonds and we study the robustness of both product classes with respect to the LGD distribution, see Section 4.5. In Section 4.6 we finally use simulations to study Value at Risk and Expected Shortfall for the mark-to-market loss of ESBies. For this we resort to the model dynamics under the real-world measure.

4.1 The weak-link approach of S&P and worst-case default scenarios

In a recent technical document, \citeasnounKraemer2017HowESBies discusses how the rating agency Standard and Poors (S&P) would determine a rating for ESBies and EJBies. The proposed methodology is termed weak-link approach. The S&P proposal has led to a lot of discussion since it associates a BBB- rating to an ESB with attachment point (given sovereign-bond ratings of 2017), which is at odds with the idea that ESBies are safe assets meriting top ratings.

To facilitate the description of the approach, we assume that the sovereigns are ordered according to their rating, so that sovereign one has the best rating and sovereign has the worst rating. Given an ESB with attachment point , define the index by Then, under the weak-link approach, the ESB is assigned the rating of sovereign . The assumption underlying this approach is that “sovereigns will default in the order of their ratings, with lowest rated sovereigns defaulting first” [Kraemer2017HowESBies, Page 4] and that the LGD of all sovereigns is equal to one, so that the ESB incurs a loss as soon as the sovereign defaults.

In this section we show that the weak-link approach is extremely conservative in various respects. We begin by a concise mathematical description. We drop the time index and consider sovereign debt portfolios with generic loss variables , , with values in the interval . We assume that the expected loss of each sovereign is fixed, that is for a constant . This is a stylized way of calibrating the model to given ratings or credit spreads of the sovereigns. We order the sovereigns by their credit quality and assume that . Next, we define loss variables that represent the default scenario of the weak link approach. Fix some standard uniform random variable and define the loss vector by

| (4.1) |

Clearly, , so that respects the expected-loss constraint. Moreover, under (4.1) sovereigns default exactly in the order of their credit quality with sovereign defaulting first and for all , that is is indeed a mathematical model for the weak link approach. Note that the loss vector is comonotonic since its components are given by increasing functions of the same one-dimensional random variable , see \citeasnoun[Chapter 7]bib:mcneil-frey-embrechts-15. Hence, under the weak-link approach, diversification effects between euro area members are ignored completely.

The next result shows that the loss variables in (4.1) can be interpreted as worst-case default scenario in the sense that they minimize the value of ESBies over all loss variables that respect the expected loss constraints. Hence, the price of an ESB under the worst-case scenario is a lower bound for the arbitrage-free price of that bond in any model consistent with these constraints. In the rating context this means that the weak link approach associates with an ESB the worst rating logically consistent with the ratings of the individual euro area sovereigns.

Proposition 4.1.

Define for generic loss variables such that takes values in the interval and and fixed weights summing to one the portfolio loss by . Then it holds for that

| (4.2) |

The proof can be found in Appendix B.

We now discuss several economic implications. First, under the worst-case default scenario the LGD of all sovereigns is almost surely equal to one. Note that under constraints on the expected loss a high LGD implies a low value for the default probability of a given sovereign, so that corresponds to a default scenario with ‘few but large losses’. Second, the worst-case default scenario maximizes the probability of large default “clusters” given the expected loss constraints. This is explained in detail in Appendix B where we discuss properties of the distribution of . Third, note that it is possible to approximate the worst-case default scenario by properly parameterized versions of the model introduced in Section 2; a precise construction is given in Appendix B. This shows that it is possible to generate arbitrarily conservative valuations for ESBies in our setup.

The qualitative properties of suggest that, in the dynamic default model from Section 2, an ESB is more risky for a given expected-loss level of the sovereigns if one chooses high values for the mean reversion level of the default intensities in the recession state , so that many defaults are quite likely in that state; at the same time the generator matrix has to be parameterized in such a way that state is visited relatively infrequently in order to meet the expected loss constraints. This intuition underlies the construction of the crisis scenarios in the numerical experiments reported in the next sections. More generally, Proposition 4.1 gives a theoretical justification for the qualitative properties of ESBie prices observed in Section 4.2 and in the work of \citeasnounbib:barucci-brigo-19, \citeasnounbib:brunnermeier-et-al-17 or \citeasnounbib:ESRB-18: for a given expected-loss level of the sovereigns higher default correlations and a higher LGD leads to a higher expected loss for ESBies.

4.2 Expected Loss of ESBies

From now on we consider ESBies with a time to maturity of five years and, for simplicity, a risk free interest rate . In order to make the prices of ESBies with different attachment points comparable, we consider normalized ESBies with payoff , so that the payoff of a normalized ESB is equal to one if there is no default, i.e. for . Moreover, we introduce the risk-neutral expected tranche loss

| (4.3) |

Here , is the generator matrix of and the function gives the price of an ESB with attachment point at time , see equation (2.8). We have made the parameters and explicit in (4.3) since we want to study how variations in their values affect the expected loss of ESBies. Note that we may interpret the annualized expected loss as credit spread of a normalized ESB with attachment point . In fact, since and since for close to one , it holds that

Parameters.

As before, we work with states of . We choose the portfolio weights according to the GDP proportions within the euro area; numerical values are given in Table 6 in Appendix C. We use the mean LGD from Table 5, the volatility parameters and the calibrated trajectories and obtained in Section 3. In our numerical experiments we consider three different parameter sets and the worst-case distribution (the distribution of the worst case default scenario from Proposition 4.1). In the base parameter set we use the generator matrix from Section 3. We take 999Using a different value for has only a very minor impact on the spread and the loss probability of ESBies. and calibrate and to the full CDS term structure at the valuation date, so that the parameterized model accurately reflects the market’s expectation at that date.101010The calibration in Section 3, on the other hand, yields a fixed set of parameters giving a reasonable fit throughout the entire observation period. This provides evidence for the good performance of our model in explaining market data, but is of course subject to small pricing errors at any given date.

The generator matrix is hard to calibrate from historical data, essentially since products depending on the default correlation of euro area countries are not traded. To deal with the ensuing model risk, we introduce two crisis parameter sets. In these parameterizations the recession state (state three) occurs less frequently than under the base parametrization, but if it occurs default intensities are (on average) substantially larger than for the base parameter set. To achieve this, we consider two generator matrices and chosen such that, on average, spends less time in state three than under the base parametrization. The corresponding mean reversion levels and and are determined from the constraint that the expected loss is identical for all parameter sets; this typically leads to . The entries of , are provided in Table 7.

Results.

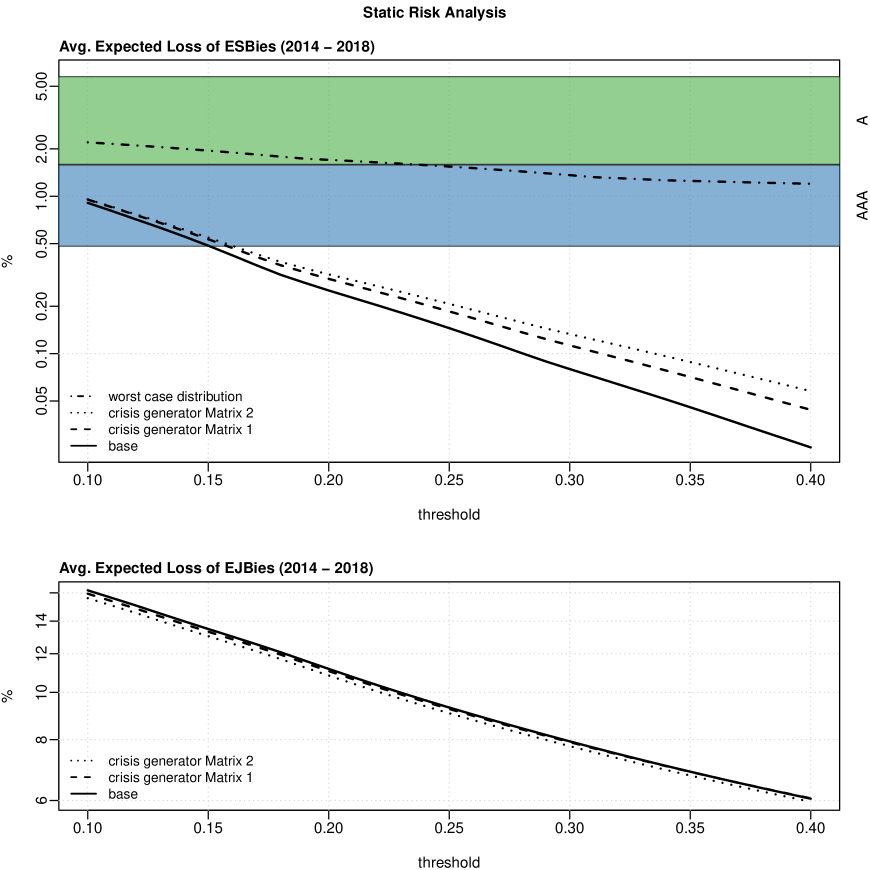

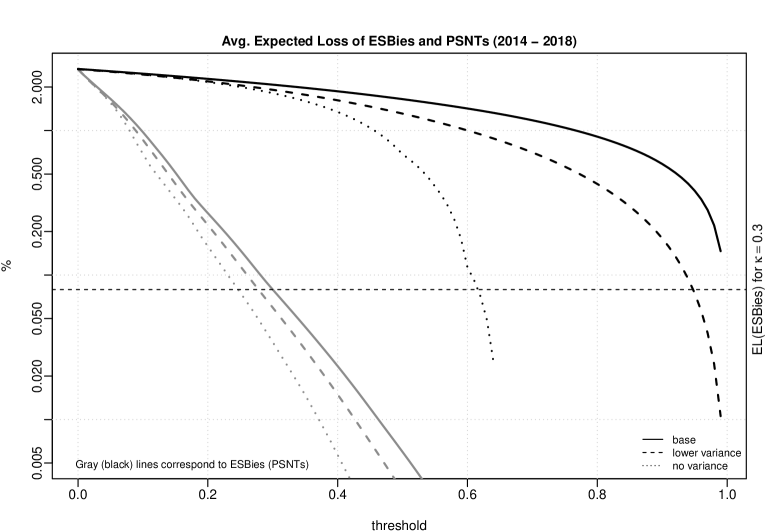

In the top panel of Figure 2, we graph the average expected loss111111Here the term “average” refers to the average over observation dates, but with a fixed time to maturity of five years, that is we plot the function . of ESBies over the period from 2014 to September 2018 as a function of the threshold . We do this for the base parametrization, the two crisis parameterizations and the worst-case distribution from Proposition 4.1. The scale for the -axis is logarithmic and values are given in percentage points. In addition, we consider AAA- and A- rated sovereigns (DEU, NLD and IRL, ESP, respectively) and compute the 1%- and 99%-quantile of the risk-neutral expected loss over the period from 2014 to September 2018. Those quantiles form the boundaries of the colored areas in Figure 2; they are supposed to give an indication of the credit quality for the ESBies on a rating scale.121212We stress that these indicative ratings should not be taken as actual ratings of ESBies, since they are computed from risk-neutral expected losses and not from historical ones, and since a rating is more than a mechanical mapping of expected loss to some rating scale.

From Figure 2 we draw the following conclusions. First, the average risk-neutral expected loss of ESBies is indeed small. For example, the average expected loss corresponding to the proposed attachment point of 0.3 is below 0.1%. Most strikingly, except for the worst-case distribution, the average expected loss of ESBies with thresholds of 0.15 or higher is well below the lower bound of the AAA-region. Second, the expected loss is lowest for the base parameters, followed by crisis parameterizations 1 and 2; this is fully in line with the economic intuition underlying the construction of these parameter sets. Third, the expected loss for the worst-case distribution (which is highest by construction) is substantially higher than the expected loss in the crisis parameterizations, underlining the fact that the worst-case distribution, and the associated weak-link approach of \citeasnounKraemer2017HowESBies, are extremely conservative. Nonetheless, for the average expected loss for the worst-case distribution is still comparable in size to that of AAA-rated sovereigns. Fourth, the expected loss of an ESB is decreasing approximately at an exponential rate in in all four parameter sets (recall that we use a logarithmic scale for the -axis). Summarizing, these findings show that an investor willing to hold ESBies with an attachment point of 0.15 or higher until maturity faces little risk of default-induced losses, which is in agreement with the analysis of \citeasnounbib:brunnermeier-et-al-17 or \citeasnounbib:barucci-brigo-19.

The bottom panel of Figure 2 shows the average expected loss of EJBies for varying attachment points. With five-year expected loss levels ranging from 6% to around 15% (and hence annualized credit spreads between 1.2% and 3%) the risk of EJBies is comparable to that of lower-quality euro area sovereigns. Comparing the expected loss of ESBies and EJBies, we see that, in line with the proposal of \citeasnounbib:brunnermeier-et-al-17, EJBies bear the bulk of the credit risk associated to the eurozone sovereigns. Note that the reverse ordering of the lines in the two panels of Figure 2 is an immediate consequence of the put-call parity relation (2.7).

4.3 Spread Trajectories of ESBies

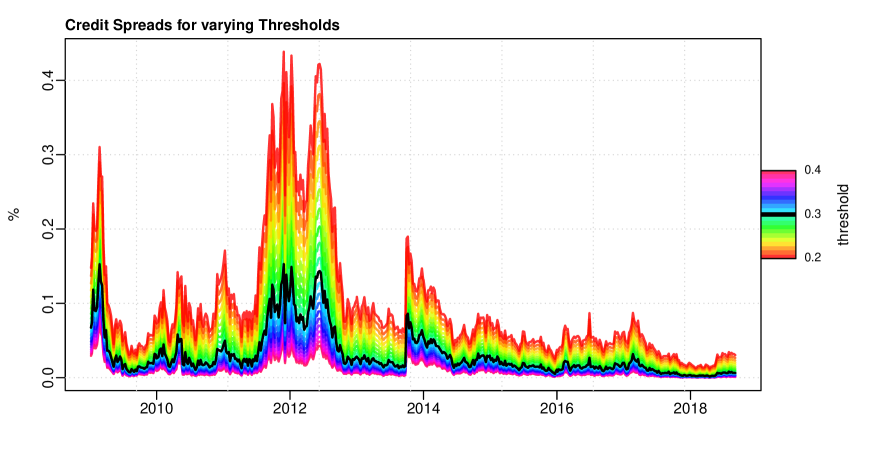

In Figure 3 we plot trajectories of the annualized credit spread of ESBies over the whole sample period for different levels of . These spreads were computed from our model by a historical simulation approach using the calibrated trajectories and as input. The solid line gives the spread of an ESB with attachment point (the value proposed by \citeasnounbib:brunnermeier-et-al-17); the colored lines correspond to different attachment points . The simulated ESB spreads peak in 2009 (the height of the financial crisis) and in the period 2011–2013 (the height of the European sovereign debt crisis). We see that the attachment point has a large impact on the volatility of ESB spreads. In particular for close to 0.2 spreads are very volatile; for on the other hand spread fluctuations are quite small.

4.4 Market risk analysis via scenarios

In this section, we analyze how the risk-neutral loss probability of ESBies is affected by changes in the underlying risk factors and . In mathematical terms, we consider the function

We consider different sets of risk factor changes or scenarios. First we study scenarios which are included in the support of the default model from Section 2, such as a change in the state of . Moreover, we consider several contagion scenarios where, in reaction to a default of Italy,131313We consider a default of Italy since on the day we used for this analysis (September 3, 2018, the last observation date in our sample) Italy had the highest CDS spread of all major euro area economies. A default of another major ‘risky’ euro area sovereign would yield similar results. the market becomes more risk averse and changes its perception of the state of and the parameter set used to value ESBies. In fact, investors on markets for (quasi) safe assets frequently change their expectations in reaction to adverse events, putting more mass on bad outcomes; see for instance \citeasnounbib:gennaioli-shleifer-vishny-12.

Non-contagion scenarios.

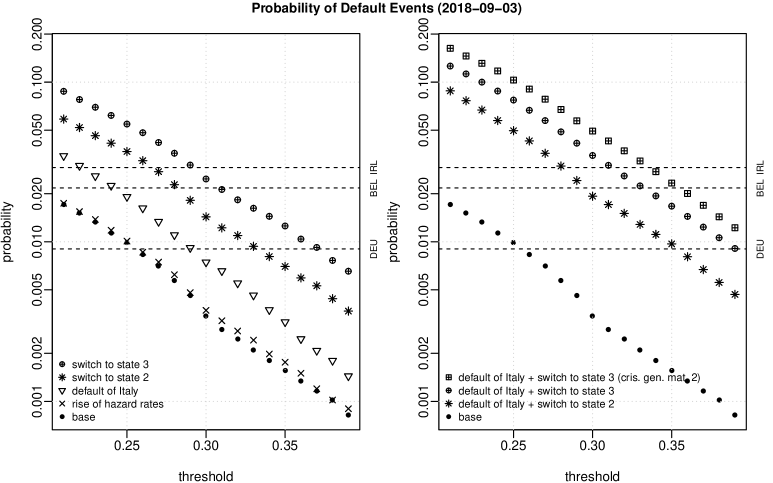

In the left panel of Figure 4, we graph the function on a log-scale using the parameters of the base scenarios and the calibrated values of and for September 3, 2018 (the last observation date in our sample). The full circles give the loss probability for varying for the base scenario, where the chain is in state one (the good economic state) and no euro area member is in default (in mathematical terms this is the function ). Moreover, we consider four types of changes in the underlying risk factors:

-

(i)

the scenario where all hazard rates experience an upward jump of 10%, that is we plot the function ;

-

(ii)

the scenario where the economy moves to a light recession, corresponding to the function ;

-

(iii)

the scenario where the economy moves to a severe recession ();

-

(iv)

the scenario where Italy defaults with random LGD . We assume that is beta distributed with mean , i.e. the loss vector at takes the form , but all other risk factors stay unchanged.

The horizontal dashed lines correspond to the risk-neutral five year default probabilities of Germany, Belgium and Ireland under the base parametrization.

Inspection of the left panel of Figure 4 shows first that a change in the hazard rates has only a small impact on the loss probability of ESBies. The default of a major euro area sovereign such as Italy has a stronger effect, but for , the loss probability remains small even after a major default. The most important risk factor changes are clearly changes in the state of the economy. For instance, for the loss probability of an ESB in state three is slightly larger than the risk-neutral default probability of Belgium, whereas in state one the loss probability is considerably smaller than the risk-neutral default probability of Germany. Second, we observe that for the given range of the threshold probabilities are decreasing in roughly at an exponential rate, similarly as the expected loss does.141414We found this exponential decay for a wide range of parameter values, but we do not have a fully convincing theoretical justification for this effect. In fact, the loss probability is quite sensitive with respect to the choice of the attachment point (to see this, one may compare the values of for and in scenario (iii)).

Contagion scenarios.

In the right panel of Figure 4 we graph the function (again on a log-scale) for the base parametrization and for three different contagion scenarios, namely

-

(i)

the case where Italy defaults and where, as a reaction, jumps to state two (mild recession);

-

(ii)

the case where Italy defaults and where, as a reaction, jumps to state three (strong recession);

-

(iii)

the case where Italy defaults and where, as a reaction, jumps to state three and the market uses the crisis parametrization two (instead of the base parameter set). This scenario is motivated by the observation that, in the subprime crisis, investors used much more conservative assumptions for default dependence than before the crisis, see for instance \citeasnounbib:brigo-et-al-10 for details.

We see that, for an attachment point , the change in the loss probability caused by one of the contagion scenarios is quite substantial. For instance, in the extreme scenario (iii), the risk-neutral loss probability is of the order of 5%. For attachment points the impact is less drastic. However, under scenario (iii), even for we get a risk-neutral threshold probability of around 2%, which is definitely non-negligible for a safe asset. This is in stark contrast to the analysis of the expected loss in Section 4.2, where ESBies appeared ‘safe’ already for .

4.5 Pooling senior national tranches and robustness with respect to the LGD distribution

bib:leandro-zettelmeyer-19 and a few other recent contributions suggest an alternative approach for constructing a safe asset for the euro area. In these proposals, the euro area sovereigns issue national bonds in (at least) two tranches, a senior and a junior tranche. A safe asset is then formed by pooling the senior tranche of the national debt, so that we use the acronym PSNT (pooled senior national tranche) for these products.151515From a financial engineering viewpoint also the E-Bonds of \citeasnounbib:monti-10 fall in the category of national tranching followed by pooling; ESBies on the other hand correspond to pooling followed by tranching. In this section we compare the risk-neutral expected loss and the risk-neutral loss probability of PSNTs to those of ESBies. In particular, we focus on the impact of the random LGD since we cannot fully calibrate the distribution of the LGD from available market data. We begin with a formal description of the payoff of PSNTs. Given some attachment level that marks the split between the junior and the senior national bond tranches, we model the payoff of the senior tranche issued by sovereign as Note that the senior national tranche suffers a loss if exceeds the threshold . For fixed weights , the payoff of the PSNT is then given by

Hence the PSNT consists of a safe payment of size and a short position in a weighted portfolio of options on the national losses. The normalized risk-neutral expected loss or equivalently the non-annualized credit spread of a PSNT is given by

It follows that the credit spread of PSNTs is independent of the dependence structure of the national losses . Assumptions on the distribution of the loss given default, on the other hand, have a huge impact on the spread of PSNTs. We begin with a few qualitative observations: first, it is easily seen that for fixed expected loss , the option price is maximal if . Hence, for fixed expected loss level of the sovereigns, the expected loss of a PSNT is maximal if the LGD of all sovereigns is equal to one. In fact, in that case the tranching on the national level offers no additional protection for the PSNT compared to simply pooling the national bonds. Second, if the LGD of all sovereigns is almost surely smaller than , the PSNT is entirely riskless. Finally, due to the convexity of the function the expected loss of the PNST increases with increasing variance of the LGD distribution (keeping fixed).

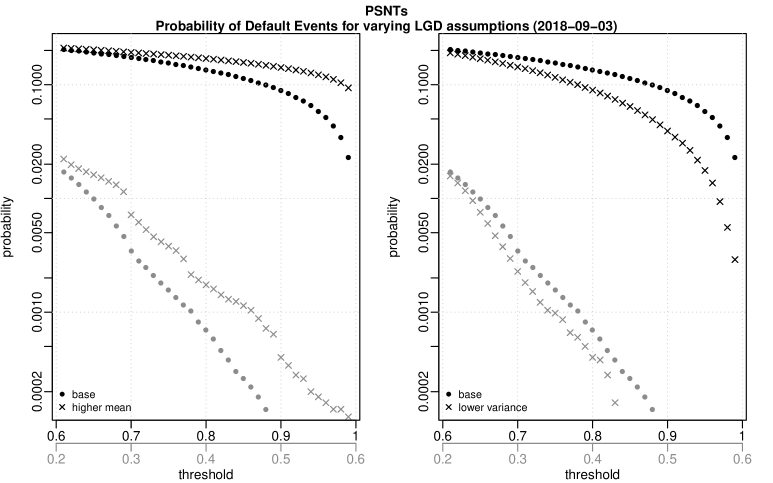

Next, we provide quantitative results comparing the behavior of PSNT credit spreads to that of ESBies. Throughout this section, whenever we vary the mean of the random LGD, we also recalibrate the remaining model parameters such that any considered LGD setup is still in line with market data. Figure 5 shows the average spread for ESBies (grey) and for PSNTs (black) over the period 2014-2018 for three different LGD distributions with identical mean function given in Table 5 and different variance/concentration parameter. We make the following observations. First, the spread of PNSTs is very sensitive to assumptions on the variance of the LGD distribution whereas the spread of ESBies is comparatively stable. Second, for the given mean function the spread of PNSTs is substantially higher than for ESBies. In fact, even with deterministic LGD the expected loss of an ESBie with equals the expected loss of a PNST with ; with higher LGD variance the two expected losses are equal only if the attachment point of the PSNT is close to one. The difference between the spreads of ESBies and of PSNTs is due to the fact that the default of a single euro area sovereign is sufficient to cause a loss for a PSNT, whereas ESBies are only affected in a severe default scenario with multiple defaults. Moreover, for the payoff of a PSNT it makes a substantial difference if a sovereign defaults only on its junior bond tranche or on both tranches which explains the sensitivity with respect to the LGD variance.

Finally, we consider the risk-neutral loss probability. Note first that the risk-neutral loss probability of PSNTs is affected by the dependence structure of (other than the spread). In fact, for fixed marginal distributions of the sovereign losses, the risk-neutral loss probability of PSNTs decreases with increasing default correlation. This is akin to the behaviour of the equity tranche in standard CDO structures. In Figure 6 we graph the risk-neutral loss probability of ESBies and PSNTs for various values of the mean and the concentration parameter of the LGD distribution. We observe the following: first, for the parameter values considered the loss probability of PSNTs is substantially higher than that of ESBies. Second, changes in the mean and in the concentration parameter have a profound impact on the loss probability of PSNTs; for ESBies these effects are less pronounced. For a , the loss probability of an ESB increases from in the base setup to for the higher mean case (which is still below the loss probability of a German bond, cf. Section 4.4). In comparison, for a relatively high , the risk-neutral loss probability of an PSNT increases from to .

4.6 Market Risk Analysis via Loss Distributions

So far we were concerned with the value of ESBies and EJBies in different scenarios; values were computed using the risk-neutral measure , so that model parameters were derived via calibration. On the other hand, for computing measures of market risk for the return of ESBies, we have to simulate their loss distribution under the historical measure , so that we need to estimate the dynamics of and using statistical methods. This issue is addressed next.

EM estimation of hazard rate dynamics.

In this section, we report the results of an empirical study where a model of the form (2.1) is estimated from the calibrated hazard rates of the euro area countries (the trajectories generated in the calibration procedure of Section 3). Here we assume that the trajectory of the Markov chain is not directly observable; rather, the available information is carried by the filtration generated by the hazard rates process . This assumption is motivated by the fact that the calibration of the trajectory in Section 3 is quite sensitive with respect to the chosen model parameters, whereas the calibration of is very robust (essentially due to the close connection between hazard rates and one-year CDS spreads).

Using stochastic filtering and a version of the EM algorithm adapted to our setting, we obtain the filtered and smoothed estimate for the trajectory of , an estimate of the generator matrix of and of country-specific parameters such as mean reversion levels and speed, all under the real-world measure . In the EM algorithm we use robust filtering techniques, which perform well in a situation where observations are only approximately of the form (2.1). For further details on the methodology see \citeasnounbib:elliott-93 or \citeasnounbib:damian-eksi-frey-18.

We consider possible states of , corresponding to a expansionary regime, a light recession and a strong recession, respectively. The EM estimates for the generator matrix of are given in Tables 8 and 9 in Appendix C, together with country-specific parameters such as mean reversion speed and levels. Note that we do not estimate the volatility, but we work with quadratic variation instead.161616In order to robustify the EM estimation procedure, we scale the quadratic variation of the strong euro area countries slightly upward. Overall the estimates appear reasonable. In particular, the estimated mean reversions levels for most countries respect the ordering , supporting the interpretation of the states of .171717For Spain and Portugal, the highest mean reversion level is estimated for state 2, which is probably due to the idiosyncratic behavior these two countries, particularly Portugal, exhibit in the first months of 2012. As expected, for any given state of the economy the estimated levels are lowest for the stronger euro area countries. In Figure 7, we give a trajectory of the filtered and the smoothed state of , that is we plot the trajectories and . These results show that the proposed model describes the qualitative properties of euro area credit spreads and, in particular, the co-movement of spread levels of the weaker euro-area members reasonably well. The frequent transitions in and out of the middle state are not surprising, given that this state reflects a situation where only a few countries experience a rise in default intensities.

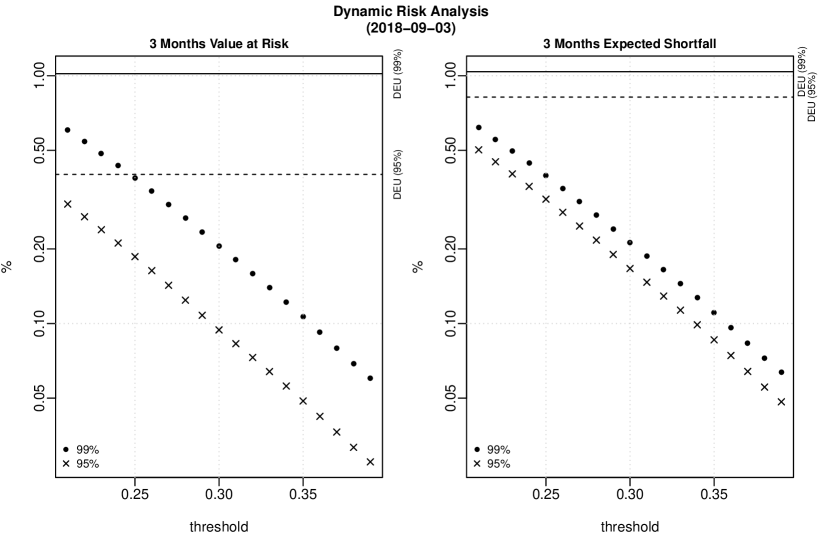

Measures of market risk.

We use two popular risk measures, Value at Risk () and Expected Shortfall () at confidence level , to study the tail of the loss distribution of ESBies over a horizon of three months. Denote by and the calibrated hazard rates and the state of for September 3, 2018. We generate realizations of the hazard rates and the Markov chain with initial values and over a three-month horizon, using the -parameters estimated in the previous paragraph, and we index the simulation outcome by . We then compute the corresponding relative loss

VaR and expected shortfall are then computed from the empirical distribution of the sampled relative losses , see \citeasnoun[Section 9.2.6]bib:mcneil-frey-embrechts-15 for details.

Figure 8 summarizes our analysis. We plot estimates of (left) and of (right) for the three-month distribution of negative ESB-returns for different and confidence levels (points) and (crosses). We see that both risk measure estimates decrease approximately at an exponential rate in . The horizontal lines in each plot represent the 95% and 99% level of the corresponding risk measure estimate for a German zero coupon bond. We observe that both the and the of ESBies with are considerably smaller than the German benchmark. We conclude that, from the viewpoint of a standard market risk analysis, ESBies appear safe and that very low risk capital levels are required to back these products. This observation is fully in line with the market risk analysis of \citeasnounbib:de-sola-perea-et-al-19, who find that “(spread changes for) senior tranches have low tail risk exposure, often lower than the tail risk of lowest-risk euro area sovereigns.” This coincidence is interesting since the analysis of \citeasnounbib:de-sola-perea-et-al-19 uses a completely different methodology, namely a time-series approach based on GARCH models and a VAR for VaR analysis.

5 Summary and Policy Implications

We draw the following key conclusions from the risk analysis of ESBies and PSNTs. Both the static risk analysis of Section 4.2 and the investigation of the loss distribution in Section 4.6 suggest that, in normal circumstances, diversification works and ESBies with are indeed very safe products.181818In fact, from the perspective of an expected loss analysis, already an attachment point might suffice to make ESBies safe. In line with this finding, we showed that the weak link approach for the rating of ESBies proposed by S&P is extremely conservative as it corresponds to a worst-case default scenario. We have also seen that for typical parameter values, the spread and the loss probability of ESBies are substantially lower than those of PSNTs (securities created by pooling the senior tranche of national debt). Moreover, for PSNTs, spread and loss probability are more sensitive to changes in the LGD distribution than for ESBies. This shows that from a risk perspective ESBies might be preferable to PSNTs.

However, considering solely the results of Section 4.2 and Section 4.6 could lead to an overly optimistic picture. The analysis of credit spread trajectories in Section 4.3 and the scenario based analysis of Section 4.4 show that the attachment point needs to be chosen more conservatively in order to make ESBies robust with respect to fluctuations in the underlying risk factors or to changes in the market perception of default dependence. In fact, one has to take attachment points for ESBies to be safe even in very adverse scenarios. Moreover, ESBies are most likely to generate large market losses in the aftermath of severe economic shocks and in contagion scenarios.

From a policy perspective, it is therefore important that a large-scale introduction of ESBies is accompanied by appropriate policy measures to limit the economic implications of external shocks and default events in the euro area (and thus default contagion). Such measures include a substantial weakening of the sovereign-bank nexus; a completion of the banking and capital markets union and the creation of a European deposit insurance scheme to improve risk sharing; more flexible forms of ESM (European Stability Mechanism) lending to countries in financial difficulties and bond clauses to allow for an orderly restructuring of sovereign debt and a bail-in of private investors, and perhaps even limited direct transfers to countries hit by severe economic shocks, see \citeasnounbib:cepr-on-euro-18 for details. In conjunction with these measures, the introduction of ESBies would be a useful step in improving the financial architecture of the euro area.

Appendix A Pricing methodology

Our main tool for computing prices of credit derivatives is the following extended Laplace transform for Markov modulated CIR processes. A related result was derived in \citeasnounbib:elliott-siu-09 for the case a single CIR-type process, see also \citeasnounbib:vanBeek-et-al-20

Proposition A.1.

Denote by the filtration generated by the Brownian motion and the Markov chain . Consider vectors and a function . Fix some horizon date . Then it holds that for

| (A.1) |

Here and the functions , solve the Riccati equation

| (A.2) |

with initial condition . Moreover, with , the function satisfies the linear ODE system

| (A.3) |

with terminal condition and with .

The functions are known explicitly, see for instance \citeasnounfilipovic2009term for details. Essentially, Proposition A.1 shows that computing the extended Laplace transform of is not much more complicated than in the classical case of independent CIR processes; the only additional step is to solve the -dimensional linear ODE system (A.3) for the function , which is straightforward to do numerically.

Proof.

We start by conditioning in (A.1) on . Due to the independence of the Brownian motions , we have conditional independence of given , which in turn leads to

| (A.4) |

Conditional on , the hazard rates are time-inhomogeneous affine diffusions. Standard references on affine models, such as \citeasnounbib:duffie-pan-singleton-00, consequently give that

| (A.5) |

where solves (A.2) and where and ; see for instance \citeasnounbib:duffie-pan-singleton-00 or Section 10.6 of \citeasnounbib:mcneil-frey-embrechts-15 for a proof. Integration thus gives . By iterated conditional expectation, we hence get

The Feynman Kac formula for functions of the Markov chain finally gives that

and hence the result. ∎

Next we consider the pricing of a survival claim and of a CDS on sovereign .

Survival claim.

The payoff of a survival claim on sovereign with maturity date and payoff function is of the form . Using standard results on doubly stochastic default times, the price of this claim at time is

and the expectation on the right can be computed from Proposition A.1 with , and .

Credit default swap.

We briefly discuss CDS pricing in our setup, since this is crucial for model calibration. From the payoff description (2.4), pricing a CDS contract amounts to computing the conditional expectation

| (A.6) |

Denote by and the present value of the premium and the default leg, that is

| (A.7) |

To obtain (A.7), we have used the fact that the default leg of the CDS is linear in the loss given default, so that we can replace with its conditional expectation. The premium leg is simply the sum of survival claims. The evaluation of (A.7) is more involved, and we now show how this can be achieved via Proposition A.1. Fix any two consecutive payment dates of and assume w.l.o.g. that . Since , we can write the term in the form

| (A.8) |

The second term in (A.8) is a survival claim. By iterated conditional expectations, we get that the first term is equal to

| (A.9) |

Since is Markov, it holds that for a suitable function (given by the solution of an ODE system), so (A.9) reduces to computing , which is a standard pricing problem for a survival claim.

Finally, we turn to the pricing of ESBies. In order to evaluate the function we use Monte Carlo simulation. For the computation of the function we use that and we compute the expected discounted portfolio loss analytically.

Appendix B Worst-case default scenario and price bounds

In this section we provide some additional results underpinning our discussion of the worst-case default scenario and lower price bounds for ESBies in Section 4.1.

Proof of Proposition 4.1.

By the put call parity (2.7) for ESBies and EJBies, the claim of the proposition is equivalent to showing that maximizes the value of EJBies. More precisely, we show that for any random vector with , , and any , it holds that

| (B.1) |

We may use call options instead of put options in (B.1) since is fixed. To establish the inequality (B.1) we use a result on stochastic orders from \citeasnounbib:bauerle-muller-06. According to the equivalence ((iii) (iv)) in Theorem 2.2 of that paper, (B.1) is equivalent to the inequality

| (B.2) |

where for a generic random variable , gives the expected shortfall of at confidence level and where denotes the quantile of at level .

To establish (B.2) we show first that maximizes the quantity over all rvs with value in the interval and expectation , simultaneously for all . In fact, the random variable has to satisfy the constraints (since ) and (since , so that

Moreover, we get from the coherence of expected shortfall that

where the last equality follows since are comonotonic. This gives inequality (B.2) and hence the result. ∎

Distribution of .

Next we discuss properties of the distribution of the worst-case default scenario. This distribution is a discrete probability measure on which charges points; it is given by

We call the worst-case distribution. Note that, under , the probability of large default “clusters” is maximal given the expected loss constraints. First, under the event where all sovereigns default has probability . Since

this is the maximum value possible. Next, under the default scenario where all sovereigns except the first default has probability . It is easily seen that this is the maximum possible value given the expected-loss constraints and the probability attributed to the first cluster (the cluster where all sovereigns default). Similarly, the probability of the ()-th cluster, where all but the first sovereigns default, is maximal given the probability attributed to the first clusters.

Finally we sketch an approach for the approximation of the worst-case distribution within our model. Note first that, for large and small, the hazard-rate trajectory is essentially determined by the trajectory of and by the choice of the mean reversion level , so that we concentrate on these quantities. We consider a model with states of that correspond to the different default “clusters” under . Choose some large and define the mean reversion level by ; ; …; . Note that in state the default probability of obligor to obligor is small, the default probability of obligor up to obligor is large; that is, the state corresponds to the -th default cluster.

Next we define the generator matrix of . We assume that states 2 to are absorbing, so that for and all . Define probabilities by , for , and finally , that is corresponds to the probability of the -th default cluster under . Since states are absorbing, we get for any valid choice for the first row of that and

(recall ). We want to choose so that for all . This gives

| (B.3) |

Since , we get that so that (B.3) defines indeed a valid generator matrix. Moreover, for , and ,

converges to which gives the result by definition of the .

Appendix C Details on Calibration

C.1 Data

In Table 4 below we present summary statistics of the data we use in the model calibration.

| Yrs. | AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|---|

| AA | AA | AAA | A | AA | AA | A | BBB | AAA | BBB | |

| Panel A: Mean | ||||||||||

| 1 | ||||||||||

| 2 | ||||||||||

| 3 | ||||||||||

| 4 | ||||||||||

| 5 | ||||||||||

| Panel B: Standard Deviation | ||||||||||

| 1 | ||||||||||

| 2 | ||||||||||

| 3 | ||||||||||

| 4 | ||||||||||

| 5 | ||||||||||

| Panel C: Minimum | ||||||||||

| 1 | ||||||||||

| 2 | ||||||||||

| 3 | ||||||||||

| 4 | ||||||||||

| 5 | ||||||||||

| Panel D: Maximum | ||||||||||

| 1 | ||||||||||

| 2 | ||||||||||

| 3 | ||||||||||

| 4 | ||||||||||

| 5 | ||||||||||

C.2 Methodology

In order to determine the parameters , , the generator matrix and the realised trajectories and , we use an iterative approach which is compactly summarized in Algorithm 1 below. We set and we use , and to denote the -th estimate of the distinct variables within the iteration.

The assumption of conditionally independent defaults substantially facilitates the calibration procedure: given an estimate for and , estimation of and of the parameter vector can be done independently for each sovereign . We initiate the calibration by applying -means clustering on the relevant CDS spreads to get an estimate for . For small maturities , it holds that . We use this approximation along with the initial estimate to get an estimate for and we consequently solve the optimization problem of line 1 in Algorithm 1 to obtain the initial value . To compute the estimates for , we use that the quadratic variation of satisfies

and we approximate the integral with Riemann sums. For a given (estimated) realisation of the Markov chain, we use the standard MLE estimator for continuous-time Markov chains to get an estimate of .

The main numerical challenge in the application of Algorithm 1 is to solve the optimization problem

| (C.1) |

We impose the restriction that all parameters are non-negative and, for regularization purposes, we set the lower bound of the mean-reversion speed to for all . During the first iteration of Algorithm 1, we employ an algorithm for constrained optimization as presented in \citeasnounRunarsson2005SearchOptimization. The algorithm uses heuristics to escape local optima. In order to refine the estimation, in the subsequent calibration steps (i.e. for steps ) we use the local optimizer of \citeasnounPowell1994AInterpolation, which provides a derivative-free optimization method based on linear approximations of the target function. After successful convergence of Algorithm 1, we perform a final refinement step in which we keep all input variables except , , fixed.

C.3 Results

| State | AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||||

| 2 | ||||||||||

| 3 |

The following figure illustrates the quality of the model fit for two different sovereigns.

C.4 Parameters used in Risk Analysis

| AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|

| State 1 | State 2 | State 3 | State 1 | State 2 | State 3 | |

| State 1 (expansion) | ||||||

| State 2 (mild recession) | ||||||

| State 3 (strong recession) | ||||||

C.5 Results of EM Estimation

| Param. | AUT | BEL | DEU | ESP | FIN | FRA | IRL | ITA | NLD | PRT |

|---|---|---|---|---|---|---|---|---|---|---|

| State 1 | State 2 | State 3 | |

|---|---|---|---|

| State 1 (expansion) | |||

| State 2 (mild recession) | |||

| State 3 (strong recession) |

References

- [1] \harvarditem[Aït-Sahalia et al.]Aït-Sahalia, Laeven and Pelizzon2014bib:aitsahalia-et-al-14 Aït-Sahalia, Y., Laeven, J. and Pelizzon, L.: 2014, Mutual excitation in Eurozone sovereign CDS, Journal of Econometrics 183(2), 151–167.

- [2] \harvarditem[Altman et al.]Altman, Brady, Resti and Sironi2005bib:altman-05 Altman, E., Brady, B., Resti, A. and Sironi, A.: 2005, The Link between Default and Recovery Rates: Theory, Empirical Evidence, and Implications, Journal of Business 78(6), 2203–2228.

-

[3]

\harvarditemAng and Longstaff2013Ang2013SystemicEurope

Ang, A. and Longstaff, F. A.: 2013, Systemic sovereign credit risk: Lessons

from the U.S. and Europe, Journal of Monetary Economics 60(5), 493–510.

\harvardurlhttp://dx.doi.org/10.1016/j.jmoneco.2013.04.009 - [4] \harvarditem[Barucci et al.]Barucci, Brigo, Francischello and Marazzina2019bib:barucci-brigo-19 Barucci, E., Brigo, D., Francischello, M. and Marazzina, D.: 2019, On the design of sovereign bond backed securities, working paper, available via SSRN.

- [5] \harvarditemBäuerle and Müller2006bib:bauerle-muller-06 Bäuerle, N. and Müller, A.: 2006, Stochastic orders and risk measures: Consistency and bounds, Insurance: Mathematics and Economics 38, 132–148.

- [6] \harvarditemBénassy-Quéré et al.2018bib:cepr-on-euro-18 Bénassy-Quéré, A., Brunnermeier, M., Enderlein, H., Farhi, E., Marcel Fratzscher, M., Fuest, C., Gourinchas, P., Martin, P., Pisani-Ferry, J., Rey, H., Schnabel, I., Véron, N., Weder di Mauro, B. and Zettelmeyer, J.: 2018, Reconciling risk sharing with market discipline: A constructive approach to euro area reform, CEPR Policy Insight No 91.

- [7] \harvarditem[Brigo et al.]Brigo, Pallavicini and Torresetti2010bib:brigo-et-al-10 Brigo, D., Pallavicini, A. and Torresetti, R.: 2010, Credit Models and the Crisis: A Journey into CDOs, Copulas, Correlations and Dynamic Models, Wiley Finance Series, Wiley.

- [8] \harvarditem[Brunnermeier et al.]Brunnermeier, Langfield, Pagano, Reis, Van Nieuwerburgh and Vayanos2017bib:brunnermeier-et-al-17 Brunnermeier, M., Langfield, S., Pagano, M., Reis, R., Van Nieuwerburgh, S. and Vayanos, D.: 2017, ESBies: Safety in the tranches, Economic Policy .

- [9] \harvarditemCronin and Dunne2019bib:cronin-dunne-19 Cronin, D. and Dunne, P.: 2019, How effective are sovereign bond-backed securities as a spillover prevention device?, Journal of International Money and Finance 96, 49–66.

- [10] \harvarditem[Damian et al.]Damian, Eksi-Altay and Frey2018bib:damian-eksi-frey-18 Damian, C., Eksi-Altay, Z. and Frey, R.: 2018, EM algorithm for Markov chains observed via Gaussian noise and point process information: Theory and case studies, Statistics and Risk Modelling 35, 51–72.

- [11] \harvarditemde Grauwe and Ji2019bib:grauwe-ji-19 de Grauwe, P. and Ji, Y.: 2019, Making the eurozone sustainable by financial engineering or political union?, Journal of Common Market Studies 57, 40–48.

- [12] \harvarditem[de Sola Perea et al.]de Sola Perea, Dunne and Reininger2019bib:de-sola-perea-et-al-19 de Sola Perea, M., Dunne, P. and Puhl, M. and Reininger, T.: 2019, Sovereign bond-backed securities: A VAR for VaR and marginal expected shortfall assessment, Journal of Empirical Finance 53, 33–52.

- [13] \harvarditemDombrovskis and Moscovici2017bib:EU-17 Dombrovskis, V. and Moscovici, P.: 2017, Reflecting Paper on the Deepening of the Economic and Monetary Union, Technical report, European Commission.

- [14] \harvarditem[Duffie et al.]Duffie, Pan and Singleton2000bib:duffie-pan-singleton-00 Duffie, D., Pan, J. and Singleton, K.: 2000, Transform analysis and asset pricing for affine jump diffusions, Econometrica 68(6), 1343–1376.

- [15] \harvarditemElliott1993bib:elliott-93 Elliott, R. J.: 1993, New finite-dimensional filters and smoothers for noisily observed Markov chains, IEEE Trans. Info. theory 39(1), 265–271.

- [16] \harvarditemElliott and Siu2009bib:elliott-siu-09 Elliott, R. and Siu, T. K.: 2009, On Markov-modulated exponential-affine bond price formulae, Applied Mathematical Finance 16(1), 1–15.

- [17] \harvarditem[ESRB]European Systemic Risk Board2018bib:ESRB-18 ESRB High-Level Task Force on Safe Assets: 2018, Sovereign bond backed securities: A feasibility study, Technical report, European Systemic Risk Board.

- [18] \harvarditemFilipovic2009filipovic2009term Filipovic, D.: 2009, Term-Structure Models. A Graduate Course., Springer.

- [19] \harvarditem[Gennaioli et al.]Gennaioli, Shleifer and Vishny2012bib:gennaioli-shleifer-vishny-12 Gennaioli, N., Shleifer, A. and Vishny, R.: 2012, Neglected risks, financial innovation, and financial fragility, Journal of Financial Economics 104(3), 452–468.

- [20] \harvarditemGolec and Perotti2015bib:golec-perotti-17 Golec, P. and Perotti, E.: 2015, Safe assets: a review, ECB working paper No 2035, European Central Bank.

- [21] \harvarditemKraemer2017Kraemer2017HowESBies Kraemer, M.: 2017, How S&P Global Ratings Would Assess European ”Safe” Bonds (ESBies), Technical report, Standard & Poors.

- [22] \harvarditemLangfield2020bib:langfield-20 Langfield, S.: 2020, Bridge over troubled monetary union: A reply to de Grauwe and Li.

- [23] \harvarditemLeandro and Zettelmeyer2019bib:leandro-zettelmeyer-19 Leandro, A. and Zettelmeyer, J.: 2019, Creating a Euro area safe asset without mutualizing risk (much), Capital Markets Law Journal 14(4), 488–517.

- [24] \harvarditem[McNeil et al.]McNeil, Frey and Embrechts2015bib:mcneil-frey-embrechts-15 McNeil, A. J., Frey, R. and Embrechts, P.: 2015, Quantitative Risk Management: Concepts, Techniques and Tools, 2nd edn, Princeton University Press, Princeton.

- [25] \harvarditemMonti2010bib:monti-10 Monti, M.: 2010, A new strategy for the single market at the service of Europe’s economy and society, Report to the President of the European Commission.

- [26] \harvarditemPowell1994Powell1994AInterpolation Powell, M. J.: 1994, A direct search optimization method that models the objective and constraint functions by linear interpolation, in S. Gomez and J.-P. Hennart (eds), Advances in optimization and numerical analysis, pp. 51–67.

- [27] \harvarditemRunarsson and Yao2005Runarsson2005SearchOptimization Runarsson, T. P. and Yao, X.: 2005, Search biases in constrained evolutionary optimization, IEEE Trans. on Systems, Man, and Cybernetics Part C: Applications and Reviews 35(2), 233–243.

- [28] \harvarditem[van Beek et al.]van Beek, Mandjes, Spreij and Winands2020bib:vanBeek-et-al-20 van Beek, M., Mandjes, M., Spreij, P. and Winands, E.: 2020, Regime switching affine processes with applications to finance, Finance and Stochastics 24(2), 309–333.

- [29]