Deep combinatorial optimisation for optimal stopping time problems : application to swing options pricing.

Abstract

A new method for stochastic control based on neural networks and using randomisation of discrete random variables is proposed and applied to optimal stopping time problems. The method models directly the policy and does not need the derivation of a dynamic programming principle nor a backward stochastic differential equation. Unlike continuous optimization where automatic differentiation is used directly, we propose a likelihood ratio method for gradient computation.

Numerical tests are done on the pricing of American and swing options. The proposed algorithm succeeds in pricing high dimensional American and swing options in a reasonable computation time, which is not possible with classical algorithms.

Mathematics Subject Classification (2010). 91G60, 60G40, 90C27, 97R40.

Keywords. Optimal stopping, American option, Swing option, Combinatorial optimisation, Neural network, Artificial intelligence.

1 Introduction

Motivation

Optimal stopping problems are particularly important for risk management as they are involved in the pricing of American options. American-style options are used not only by traditional asset managers but also by energy companies to hedge “optimised assets” by finding optimal decisions to optimise their P&L and find their value. A common modelling of a power plant unit P&L is done using swing options which are options allowing to exercise at most times the option with possibly a constraint on the delay between two exercise dates (see Carmona and Touzi (2008) or Warin (2012)).

Formally, for , we are given a stochastic processes defined on a probability space

and we search for an increasing sequence of stopping times maximizing the expectation of the objective function

Numerical methods to solve the optimal stopping problem when and is Markovian include:

- •

-

•

Partial differential equation (PDE): a variational inequality derived from the Hamilton Jacobi Bellman equation is given by

where is the infinitesimal generator of (Shreve, 2004, Chapter 8, Section 3.3). A numerical scheme can be applied to solve this PDE and find the option value.

- •

-

•

Policy search: the decision rule or exercise region is parametrized by a vector and the parameters are usually optimised by Monte Carlo methods as in reinforcement learning (Glasserman, 2013, Chapter 8, Section 2); Andersen (1999), Garcıa (2003). The algorithm proposed in this paper is strongly related to this class of method.

These approaches generalise well for , see Carmona and Touzi (2008) for dynamic programming principle or Bernhart et al. (2012) for the BSDE method. The non linear case where is of the form is studied by Trabelsi (2013). We refer to (Glasserman, 2013, Chapter 8) for more exhaustive details on numerical methods for American option pricing. All these algorithms suffer from the curse of dimensionality: the number of underlying is hardly above 5. However energy companies portfolio may trade derivatives involving more that 4 commodities at one time (e.g. swing options indexed on C02, natural gas, electricity, volume, fuel) and traditional numerical methods hardly provide good solutions in a reasonable computing time.

Recently, neural network-based approaches have shown good results regarding stochastic control problems and PDE numerical resolution in high dimension, see Han et al. (2017b), Sirignano and Spiliopoulos (2018), Chan-Wai-Nam et al. (2019). In the following, one describes literature related to optimal stopping time problems using neural networks. Kohler et al. (2010), Becker et al. (2020) use neural networks for regression in the dynamic programming equation (1). Huré et al. (2018), Bachouch et al. (2018), Becker et al. (2019a) also use the dynamic programming equation (1) but neural networks are used to parameterize the optimal policy. Weights and bias of the neural network(s) minimise at each time step the right hand side of the dynamic programming equation (1), going backward. The optimal decision consists in a continuous variable (instead of a discrete one) taking value in modeled by a neural network. Han et al. (2017a), E et al. (2017), Huré et al. (2019) use neural networks to solve BSDE’s. In Huré et al. (2019), the neural networks parameterizing the solution and eventually its gradient minimise the loss between the left hand-side and the right hand side of the Euler discretisation of the BSDE, going backward from the terminal value. Bachouch et al. (2018) and Huré et al. (2019) need to maximise one criteria by time step. The approaches of Han et al. (2017a) and E et al. (2017) are quite different: the neural network allows the parameterisation of the initial value of the BSDE and the gradient at each time step, and it minimises the distance between the terminal value obtained by the neural network and the terminal value of the BSDE, going forward. American put options prices are computed in Huré et al. (2019) up to dimension 40 with 160 time steps. Neural networks approaches have also been used in the context of swing options pricing in gas market in Barrera-Esteve et al. (2006). The definition of swing options slightly differs from ours as it considers a continuous control: the option owner buys a certain amount of gas between a minimum and a maximum quantity. It is however related to our problem as in continuous time, this option is bang-bang: it is optimal to exercise at the minimum or the maximum level at each date, that is choosing between two actions. Barrera-Esteve et al. (2006) directly models the policy by a neural network and optimises the objective function as in Fécamp et al. (2020), Buehler et al. (2019).

Contrarily to Kohler et al. (2010), Huré et al. (2018), Bachouch et al. (2018), Han et al. (2017a), E et al. (2017), Huré et al. (2019), Becker et al. (2020), the goal of this paper is to propose a reinforcement learning algorithm to solve optimal multi-exercise (rather than one single) stopping time problems with constraints on exercise times that does not need to derive a dynamic programming equation nor to find an equivalent BSDE of the problem. The only information needed is the dynamic of the state process and the objective function. This kind of algorithm is called policy gradient and is well known in the area of reinforcement learning, see Sutton et al. (2000) for instance. Although continuous control approximation with reinforcement learning shows good results, see Fécamp et al. (2020), Buehler et al. (2019) for European-style option hedging, the case of optimal stopping times is more difficult as it involves controls taking values in a discrete set of actions. The problem is similar to a combinatorial optimisation one: at each time step, an action belonging to a finite set needs to be taken. One way to solve this problem is to perform a relaxation assuming that the control belongs to a continuous space. For instance, if one needs to price an American option, a decision represented by a value in and consisting in exercising or not must be taken. Relaxing the problem consists in searching for solutions in : this relaxation has successfully been applied to a Bermudan option pricing in a high dimensional setting (up to 1000) in Becker et al. (2019b). These methods apply well for American-style option pricing but seem to be not flexible enough to be extended to swing options pricing.

Main results

Our approach follows the spirit of Fécamp et al. (2020) and Becker et al. (2019b): one directly parameterises the optimal policy by a neural network and maximises the objective function moving forward. We propose an algorithm using reinforcement learning in order to solve optimal stopping times problem seen as an combinatorial optimisation problem. Note that solving combinatorial optimisation problems with neural networks have been considered in Bello et al. (2016) in a deterministic framework without dynamics on the state process. The stochastic optimization framework considered in this paper is described in Section 2.

Neural network hardly handles integer outputs which is the main difficulty of the problem addressed in this paper. To encompass this problem, the first step of the algorithm consists in randomizing the optimization variables (that is executing the option or not) and modelling their law by a neural network. The second step consists in computing the gradient of the objective function. It can not be computed as usual by automatic differentiation as the neural network does not output the optimization variables but their law. The use of likelihood ratio method allows to rewrite the gradient as a function of the neural network output gradient that can be computed with automatic differentiation. The algorithm is given in Section 3. Compared to the papers referenced above our approach allows to solve stopping time problems without any knowledge of the dynamic programming equation or of an equivalent BSDE. Furthermore, it presents many advantages as it

-

•

can solve multiple optimal stopping time problems;

-

•

allows to add in a flexible way any constraint on the stopping times;

- •

Let us also notice that our method does not take advantage of the linearity (possible inversion between the sum and the expectation) of the considered optimal stopping problems contrarily to Becker et al. (2019b) and can be applied to non linear problem, making it suitable for impulse control problems. The theoretical convergence study of our algorithm is out of the scope of this paper.

Numerical tests covering Bermudan and swing options are proposed in Section 4 and show good results in the pricing of 10 underlyings Bermudan option and also on 5 underlyings swing options having up to exercise dates. However, our algorithm gives suboptimal results on one of the considered case.

2 Optimal stopping

2.1 Continuous time modelling

We are given a financial market operating in continuous time. Let a filtered probability space and a d-dimensional -Brownian motion. One assumes that satisfies the usual conditions of right continuity and completeness. Let a finite horizon time and be the unique strong solution of the Stochastic Differential Equation (SDE):

| (2) |

with and two measurable functions verifying and for and ( denotes the Euclidian distance in and for a matrix ) and . Using the notations of Carmona and Touzi (2008) and with as defined in (2) for and for , an optimal stopping time problem consists in solving the problem

| (3) |

where is the collection of all vectors of increasing stopping times such that for all , a.s. on the set of events and where is a measurable function. corresponds to the number of possible exercises and to the minimum delay between two exercise dates. One wants to find the optimal value (3) but also the optimal policy

| (4) |

2.2 Discrete time modelling

In practice, one only considers optimal stopping on a discrete time grid (for instance, the valuation of a Bermudan option is used as a proxy of the American option). Let us consider exercise dates belonging to a discrete set , . The problem consists in finding

| (5) |

where is the set of stopping times belonging to such that on , for . This discretisation is needed for our algorithm as it is needed in classical methods such as Longstaff and Schwartz (2001). Problem (5) is equivalent to the following:

| (6) |

where is a sequence of -measurable random variables taking values in such that

| (7) |

and

| (8) |

with

| (9) |

the delay at from the last exercise assuming that we can exercise at time 0 (hence the term in (9) allowing to start at time 0 with a delay ) and with the convention . Given a solution of Problem (6), a proxy for the optimal control (4) is given by

on the event with and .

3 Algorithm description

3.1 Neural network parametrization

As the ’s are discrete we cannot assume that they are the output of a neural network which weights are optimised by applying a stochastic gradient descent (SGD). To overcome this difficulty, one can randomize and consider that at each time step , the discrete variable is a Bernoulli distributed random variable conditionally on (and if ). The Bernoulli distribution parameter depends on the state variable of our control problem. This state variable, denoted , is

-

•

in the case of a Bermudan option, that is with only one execution date,

- •

Of course, one can adapt the state depending on the constraints (for instance if there is no delay constraint (8), the state is ). In a non Markovian framework, one could consider that the probability for to be equal to 1 is a function of all the values of for and for . In this case, one could use a Recurrent Neural Network to parameterise this function but we do not consider this case here. The Bernoulli distribution parameter, which is is parameterised by a neural network defined on and taking values in where is the state space and represents the sets in which the biases and weights of the neural network lie. The neural network architecture is described in Section 3.3. The parametrization is then the following:

| (10) |

with and for and is equal to 0 if the constraints are saturated and 1 otherwise. Typically, if there are no constraints, is always equal to 1, and if there are constraints (7) and (8),

Note that the methodology can be extended to any constraint on the policy. outputs the (the inverse function of ) of (when constraints are not saturated). The function is not necessary and one could only consider to parameterise the logit of the probability. To reduce the values taken by the , we bound the output of the neural using and choose such that and ; is given in Section 3.4.

From now on, is replaced by to indicate the dependence of the law of with . At this step, we still cannot train our neural networks by applying a stochastic gradient descent because of the ’s randomization.

3.2 Optimization

To approximate a solution to (6) we search for

Classical neural network parameter optimization consists first in evaluating the objective function

using Monte Carlo method and replacing it by

with and where and correspond to one realization of simulated according to (2) for and to for . Secondly, a gradient descent is done to update the parameter using gradient of the objective function which is computed using backpropagation. However in our case, it is not possible to directly use backpropagation: is not a function of , but a discrete variable with law depending on .

To encompass this problem, we use a likelihood ratio method. Let us consider a random variable with probability measure , , absolutely continuous with respect to a measure . Let be the likelihood function. We have, under some integrability conditions, . Using this method and iterative conditioning for probability computation, we find that the gradient of is given by:

| (11) |

which is defined in Equation (10) is a continuous function of the neural network: the gradients appearing in Equation (LABEL:eq:derive1) can be easily computed using backpropagation. Let us notice that the method does not take any advantage of the fact that we can exchange the sum and the expectation in (6). It is then suitable for optimization problems of the form

and could be combined with forward neural network continuous optimization algorithms such as those of Fécamp et al. (2020), Buehler et al. (2019) to solve impulse control problems.

Every steps, the objective value is computed over the testing set. The parameters kept at the end are the ones minimising those evaluations. The objective function is finally evaluated on a validation set. While on the training phase actions are sampled from the outputted probability on the training set, they are chosen equal to 1 if the probability is greater than 0.5 and 0 otherwise on the test and validation sets. The algorithm is described in 1 with hyperparameters given in Section 3.4.

3.3 Neural network architecture

The neural network architecture is inspired by Chan-Wai-Nam et al. (2019) and consists in one single feed forward neural network which features are the time step and the current state realisation . Let and that we assume to be included in . The neural network is defined as follow

where for , , for , , for , for and . corresponds to the number of layers and to the number of neurons per layer (that we assume to be the same for every layer). The correspond to the weights and to the biases. The function is the activation function and is chosen as the ReLu function, that is . is then equal to .

3.4 Hyper parameters

-

•

The batch size as the number of iterations depend on the use case and are specified at a later stage. The training set size is then equal to . As the likelihood ratio estimator of the gradient has high variance, choosing a large batch size (>1000) allows for a better estimation. The drawback is that it tends to slow down the algorithm. To reduce the variance, one could also use a baseline function as in Zhao et al. (2011).

-

•

The test set size is chosen equal to 500,000 and the validation set size to 4,096,000 (500,000 and 4,096,000 are chosen high to have very accurate optimisation). The test set is evaluated every steps.

-

•

The number of layers is chosen equal to 3. The number of neurons per layer is constant (but can vary from a case to another).

-

•

The learning rate ( in Algorithm 1) is chosen equal to 0.001.

-

•

As in Chan-Wai-Nam et al. (2019), in our case, regularisation which is classically used to avoid overfitting is not relevant and we won’t use it as our data is not redundant and thus the network does not experience overfitting.

-

•

Since we use the same network at each time step, we use a mean-variance normalisation over all the time steps to center all the inputs for all ’s with the same coefficients. The scaling and recentering coefficients are estimated on 100,000 pre-simulated data that is just used to this end. The mean and the standard deviation are first computed for every time step over the simulations then averaged over the time steps.

-

•

We use Xavier initialisation Glorot and Bengio (2010) for the weights and a zero initialisation for the biases.

-

•

The parameter that bounds the input of the function is chosen such that and . We choose .

-

•

The library used is Abadi et al. (2015) and the algorithm runs on a laptop with 8 cores of 2,50 GHz, a RAM memory of 15,6 Go and without GPU acceleration.

4 Numerical results

In this section Algorithm 1 is applied to the valuation of Bermudan and swing options. The function is of the form where is the payoff of the option and is the risk free rate. We place ourselves in the Black-Scholes framework: , with corresponding to the dividend rate and with a positive definite matrix. We choose to work with a regular time grid for . The probability measure corresponds to the risk neutral probability and finding the value of the option consists in solving Problem (6).

4.1 Bermudan options

In this section, we assume that (only one exercise) and we consider different options to price.

Put option

with , payoff , , , , , , , . We consider a batch size equal to , a neural network with a depth of 3 layers having 10 neurons each and iterations.

Max-call option

with , payoff , , , , , , ( is the identity matrix with size ), , . We consider a batch size equal to for and for , a neural network with 3 layers of size 30 for and 70 for and iterations.

Strangle spread option

with , payoff , , , , , , , ,

, . We consider a batch size equal to , a neural networks with 3 layers size 60 and iterations.

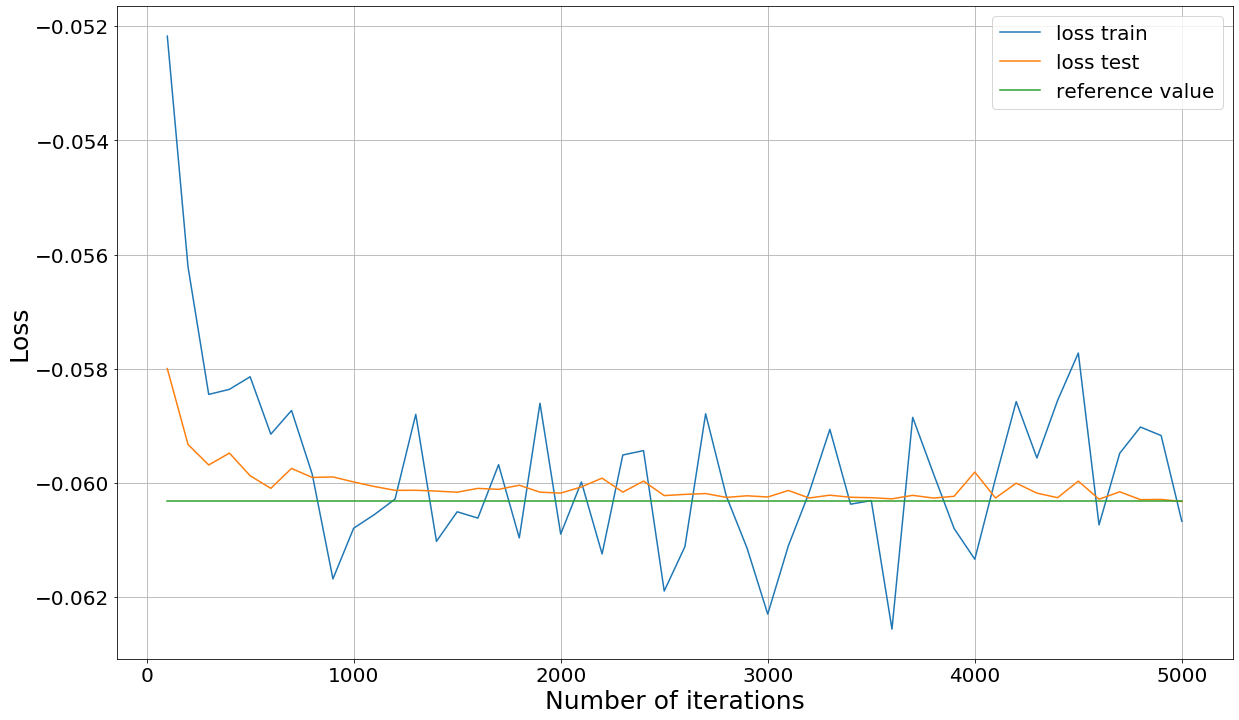

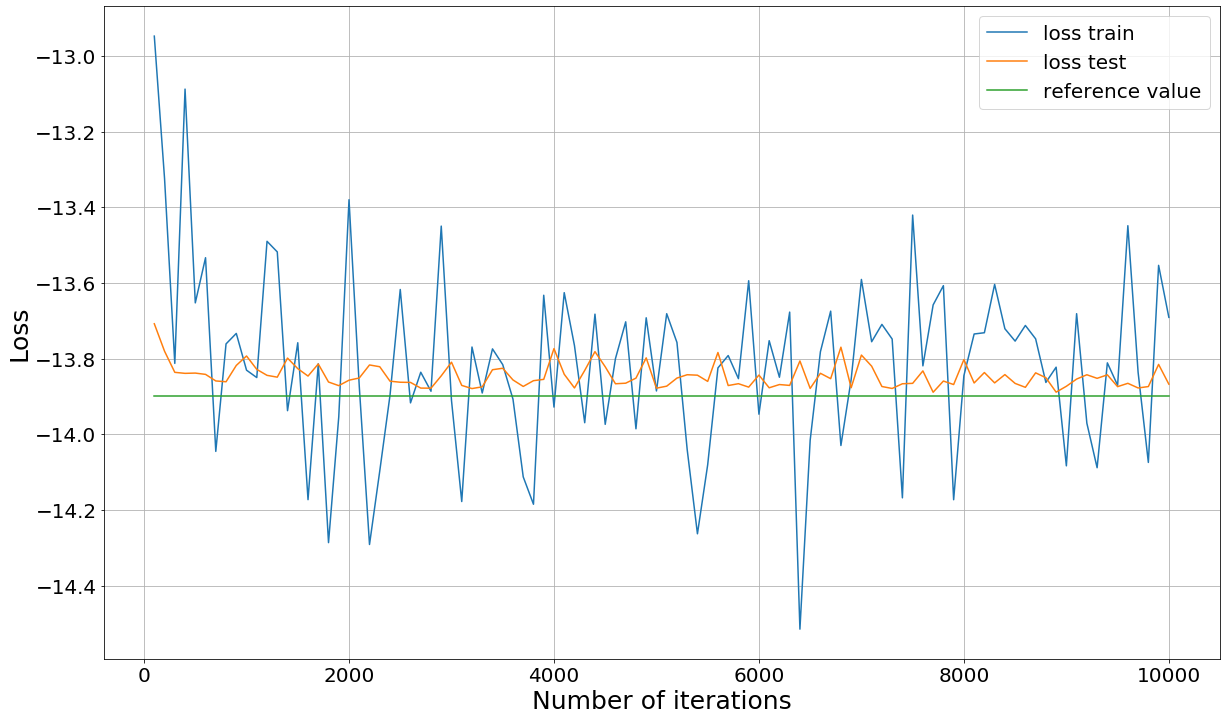

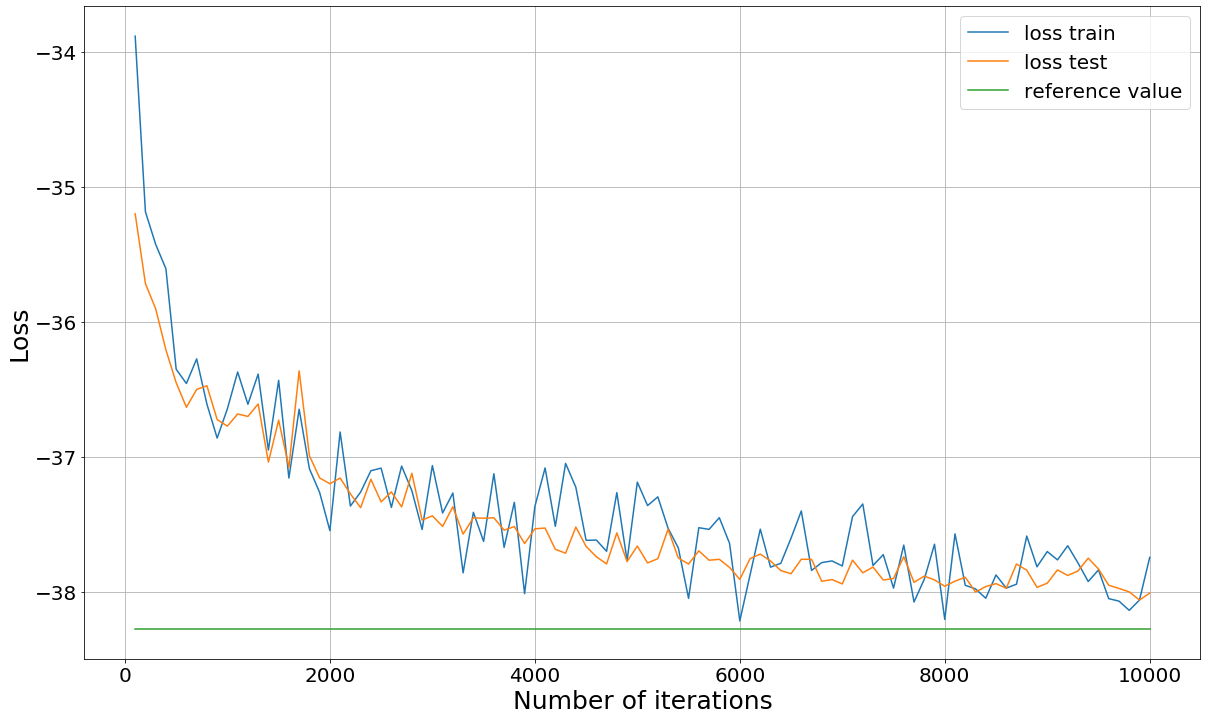

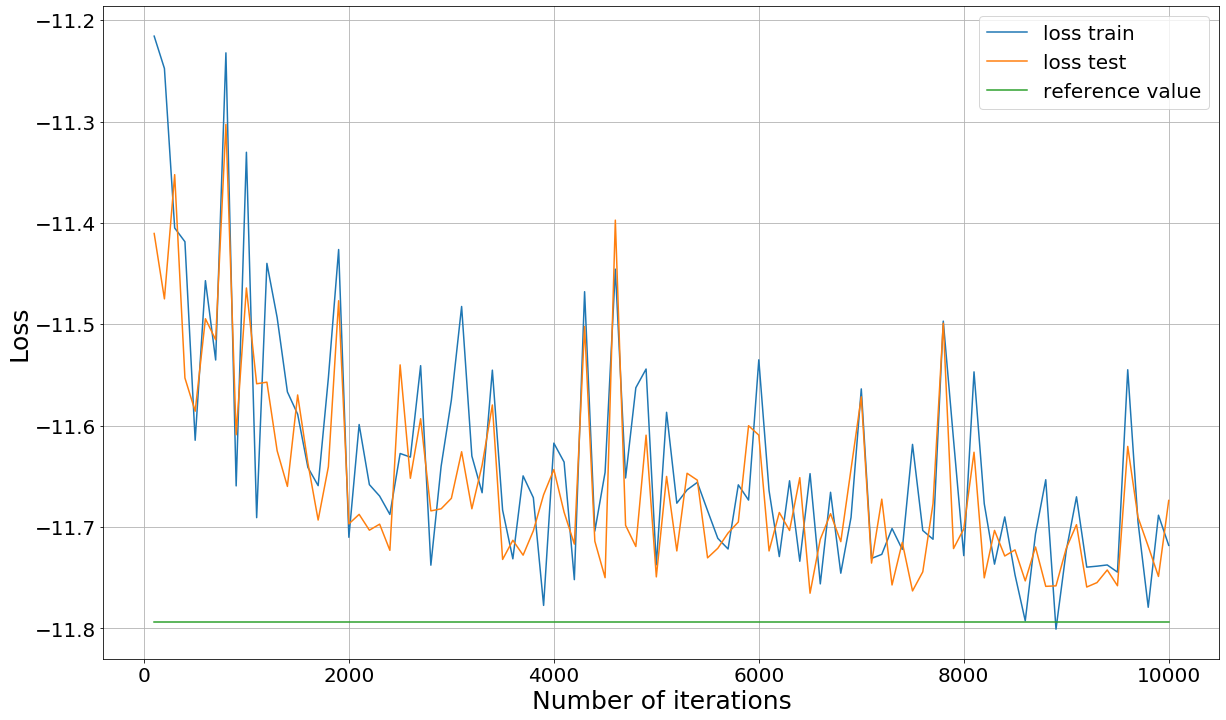

Losses and times obtained with Algorithm 1 are given in Table 1 for each case and losses are compared to a reference value (Bouchard and Chassagneux (2008) for the put option and Becker et al. (2019b) for the other options). The algorithm succeeds in pricing Bermudan options with a high precision (relative error <1%) in dimension up to 10 and number of time steps up to 50. The computing time is more sensitive to the number of time steps than to the dimension: the number of neural network estimation is equal to the number of time steps. The increase of computing time when dimension increases is mostly caused by a need to increase the batch size and a more important simulation time. Algorithm 1 succeeds in pricing Bermudan options and solves problems that are usually hard to solve and very expensive in terms of computation time as they suffer from the curse of dimensionality. The training and testing learning curves are given in Figure 1. The testing errors are relatively stable for the put and the max-call options but less stable for the strangle spread. For the put and the 2 dimensional max-call, the testing error converges quickly to the optimal value. The testing error of the 10 dimensional max-call decreases more slowly. The different training errors are all noisy as they are of smaller size.

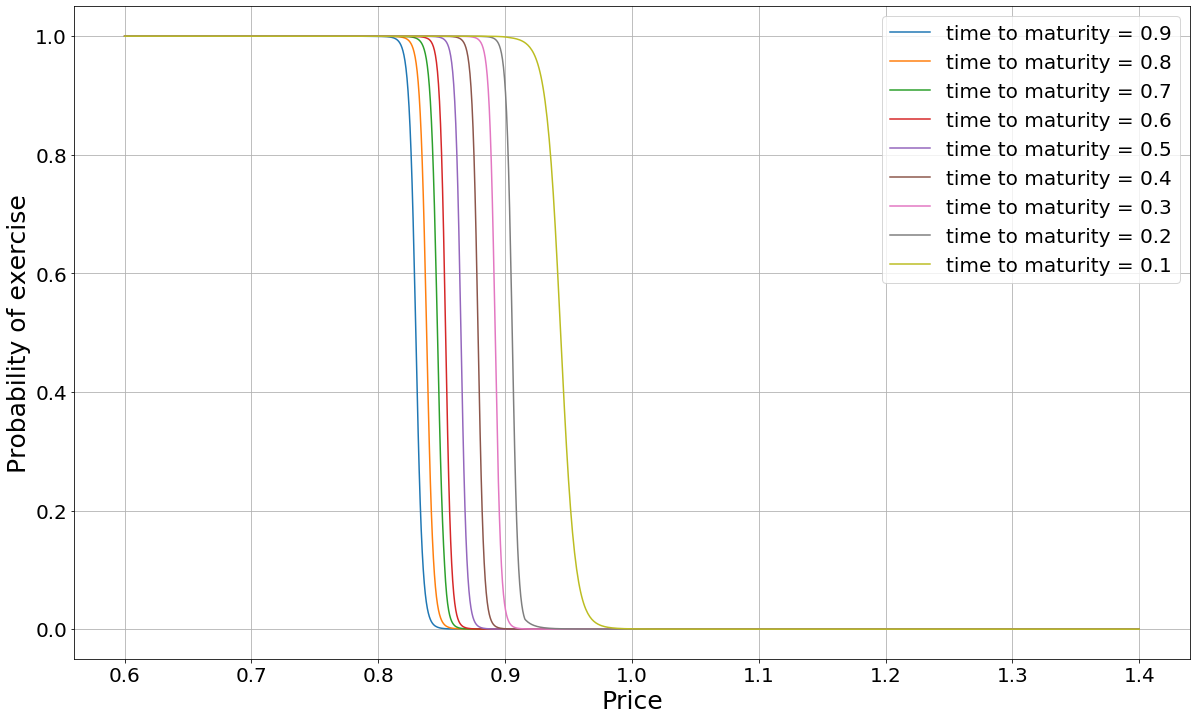

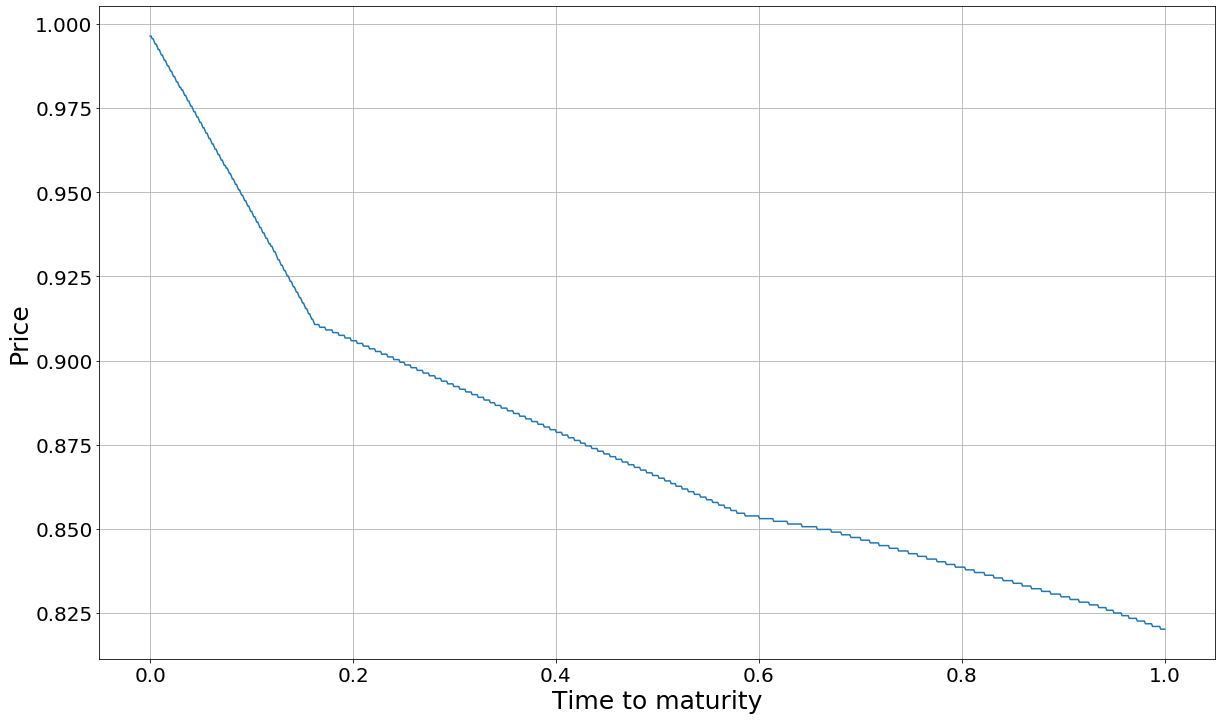

Once trained, the neural network allows to compute the probability to exercise according to the price and time to maturity and the exercise region in a few seconds, see Figure 2 for the Bermudan put option. The probability to exercise has a S-shape with limit values 0 and 1 (do not exercise and exercise) and a small transition region between those two values. As expected, the first value such that the probability becomes 0 increases when time to maturity decreases. This is confirmed in the exercise region in Figure 1 with the frontier decreasing with time to maturity. The exercise region is the one below the curve, which is computed using the first value such that the probability of exercise is below 0.5. The frontier is extrapolated from the neural network trained only on a discrete time grid but that allows to use different time to maturity values (even ones not used in the training), which is not possible with classical backward optimisation.

| Use case / Method | Algorithm 1 | Reference | Difference | Time (s) |

|---|---|---|---|---|

| Bermudan put | 0.0603 | 0.0603 | 0.06% | 393.9 |

| Max-call, d = 2 | 13.8787 | 13.8990 | 0.15% | 1377.8 |

| Max-call, d = 10 | 38.0347 | 38.2780 | 0.64% | 5968.7 |

| Strangle spread | 11.7681 | 11.7940 | 0.22% | 12991.3 |

4.2 Swing options without delay

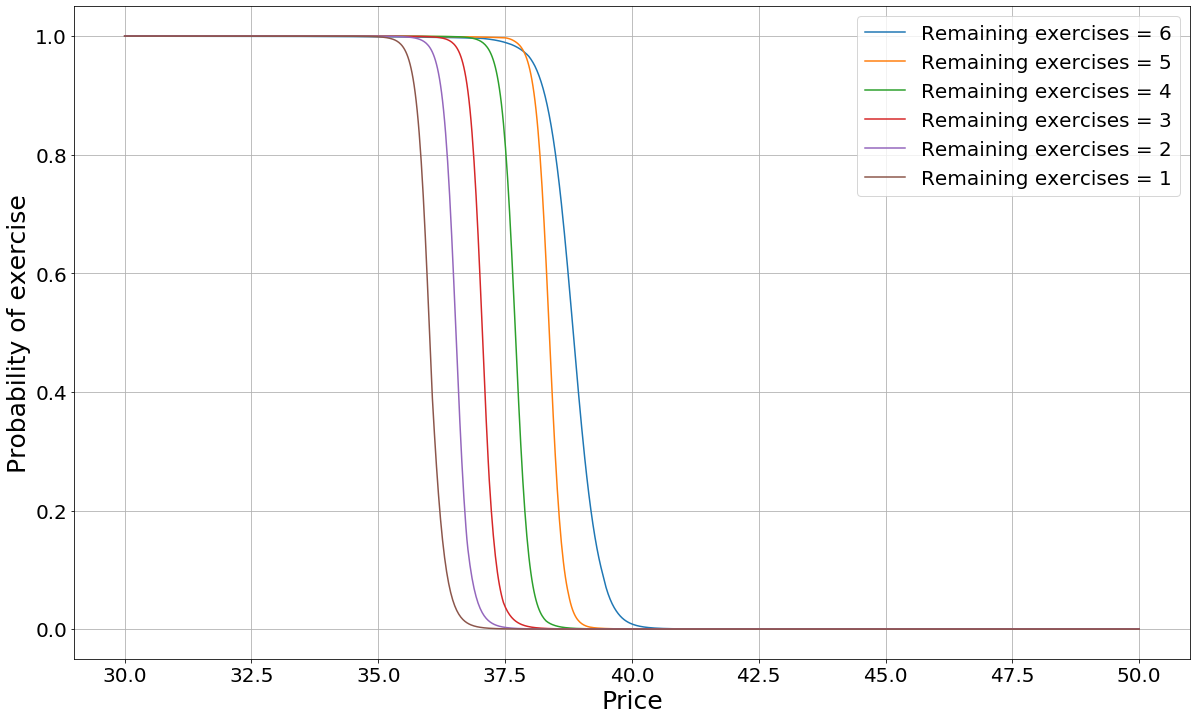

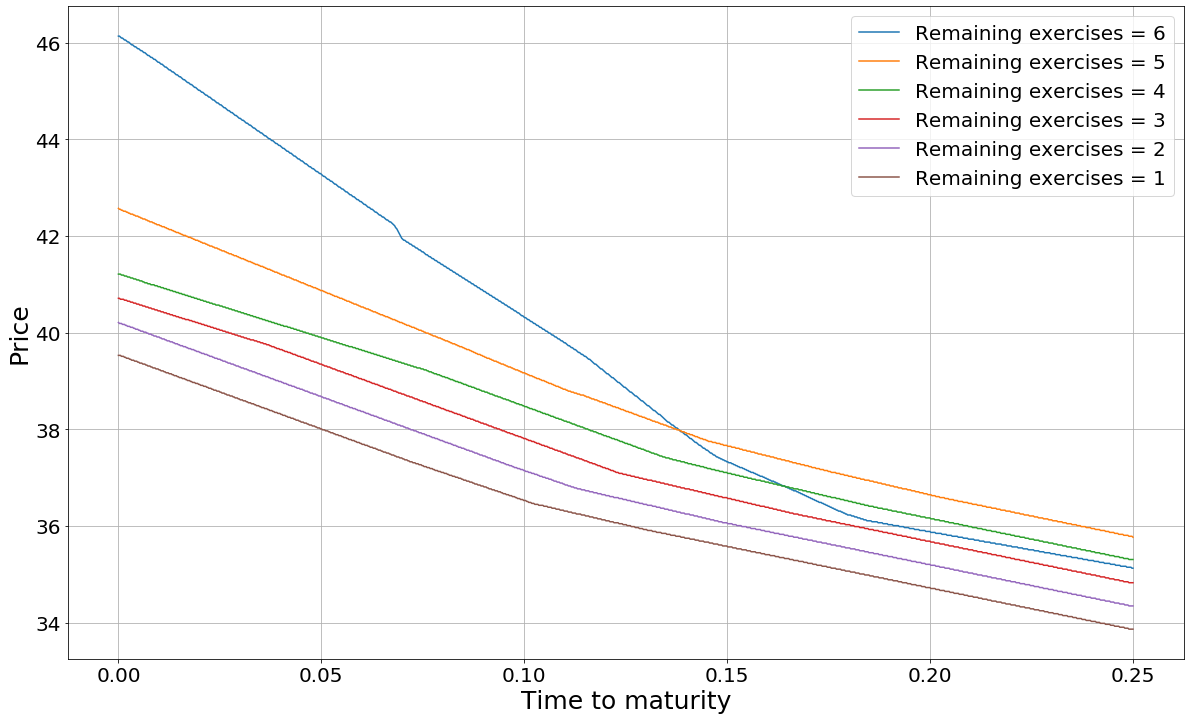

In this section, we consider a swing option without delay constraint. We compare in Table 2 the results obtained by Algorithm 1 with the results of Ibáñez (2004) in the case of a put option with , , , , , , , , , and no delay. We consider a batch size equal to , a neural networks with 3 layers size 10 and iterations. Every case takes around 4 minutes to converge, see Table 3. The algorithm gives very accurate results in a short period of time for the valuation of the swing options. As for the Bermudan put option, it is possible to compute the probability of exercise and the exercise region for this swing option, see Figure 3. Those quantities depend now on the remaining number of exercises. As expected, the first value such that the probability to exercise is 0 increases with the remaining number of exercises. The exercise frontier should increase with the remaining number of exercises which is the case most of the time : the curve for a remaining number of exercises equal to 6 goes below the ones with a remaining number of exercises equal to 5 (resp. 4) when time to maturity is greater than 0.1 (resp. 0.15).

| / | 35 | 40 | 45 |

|---|---|---|---|

| 1 | (5.104, 5.114, 0.19%) | (1.776, 1.774, 0.12%) | (0.409, 0.411, 0.42%) |

| 2 | (10.165, 10.195, 0.29%) | (3.492, 3.48, 0.34%) | (0.772, 0.772, 0.06%) |

| 3 | (15.194, 15.23, 0.24%) | (5.115, 5.111, 0.07%) | (1.09, 1.089, 0.09%) |

| 4 | (20.188, 20.23, 0.21%) | (6.658, 6.661, 0.05%) | (1.358, 1.358, 0.0%) |

| 5 | (25.19, 25.2, 0.04%) | (8.148, 8.124, 0.3%) | (1.58, 1.582, 0.12%) |

| 6 | (30.156, 30.121, 0.12%) | (9.494, 9.502, 0.09%) | (1.764, 1.756, 0.44%) |

| / | 35 | 40 | 45 |

|---|---|---|---|

| 1 | 270.1 | 278.6 | 249.9 |

| 2 | 241.6 | 246.6 | 236.8 |

| 3 | 240.6 | 237.7 | 243.4 |

| 4 | 239.6 | 242.4 | 240.0 |

| 5 | 271.3 | 239.9 | 235.3 |

| 6 | 243.8 | 240.9 | 241.7 |

To assess the performance of Algorithm 1 in high dimension, let us consider the pricing of the geometrical put option having payoff . Let , , , , , , , and . Prices dynamic parameters are chosen in order to have an option value equal to the one dimensional case put option value: the product of the components of follows a Black-Scholes dynamic with drift parameter equal to and volatility equal to . It allows to have a reference value (from Ibáñez (2004)) while considering a high dimensional case. We consider a batch size equal to , a neural networks with 3 layers of size 30 and iterations. Results are given in Table 4. The algorithm succeeds in pricing this option with 5 underlyings in a reasonable time (less than 30 minutes). By using a less costly hyperparameterization (20 neurons density instead of 30, iterations instead of , instead of we are able to obtain results in less than 4 minutes with a accuracy as shown in Table 5

| Use case / Method | Algorithm 1 | Reference | Difference | Time (s) |

|---|---|---|---|---|

| l = 1 | 1.767 | 1.774 | 0.39% | 1814.3 |

| l = 2 | 3.478 | 3.480 | 0.04% | 1686.6 |

| l = 3 | 5.100 | 5.111 | 0.22% | 1701.5 |

| l = 4 | 6.639 | 6.661 | 0.32% | 1661.0 |

| l = 5 | 8.117 | 8.124 | 0.09% | 1689.2 |

| l = 6 | 9.478 | 9.502 | 0.25% | 1675.7 |

| Use case / Method | Algorithm 1 | Reference | Difference | Time (s) |

|---|---|---|---|---|

| l = 1 | 1.733 | 1.774 | 2.33% | 221.9 |

| l = 2 | 3.435 | 3.480 | 1.29% | 222.0 |

| l = 3 | 5.074 | 5.111 | 0.71% | 212.2 |

| l = 4 | 6.591 | 6.661 | 1.05% | 199.4 |

| l = 5 | 8.033 | 8.124 | 1.13% | 197.0 |

| l = 6 | 9.392 | 9.502 | 1.16% | 203.0 |

4.3 Swing options with delay

Let us now consider the case of a put option with , , , , , , , , , and . Delay constraint is now present and a higher number of dates is considered. We consider a batch size equal to , a neural networks with 3 layers of size 10 and iterations. We compare in Table 6 the results obtained with Algorithm 1 to the ones obtained with Carmona and Touzi (2008). The algorithm gives satisfying results but in this situation we can see that the relative error increases with the number of exercises.

| Use case / Method | Algorithm 1 | Reference | Difference | Time (s) |

|---|---|---|---|---|

| l = 1 | 9.844 | 9.85 | 0.06% | 5430.5 |

| l = 2 | 19.093 | 19.26 | 0.87% | 6658.0 |

| l = 3 | 27.827 | 28.80 | 3.38% | 5518.4 |

| l = 4 | 36.058 | 38.48 | 6.29% | 5566.1 |

| l = 5 | 43.638 | 48.32 | 9.69% | 5472.1 |

5 Conclusion and perspectives

A stochastic control algorithm able to deal with (discrete) optimal stopping variables is presented. The different use cases show that the proposed algorithm is able to solve optimal stopping time problems in a reasonable time, even when the dimension is high and also for multi-exercise. The algorithm is simple and allows us to find an optimal policy without any knowledge on the dynamic programming equation. The method presented in this paper avoids a costly backward pass and only need a forward pass. While the computation time increases a little with dimension, it increases a lot more with the number of time steps and the algorithm can have troubles to converge. To confirm all those results, one should study the theoretical convergence of the algorithm. This algorithm could easily be extended to impulse control if combined with Fécamp et al. (2020) in order to solve problems involving both continuous and discrete controls such as hedging with fixed transaction costs.

Acknowledgements. This research is supported by the department OSIRIS (Optimization, SImulation, RIsk and Statistics for energy markets) of EDF Lab which is gratefully acknowledged.

References

- Abadi et al. (2015) M. Abadi, A. Agarwal, P. Barham, E. Brevdo, Z. Chen, C. Citro, G. S. Corrado, A. Davis, J. Dean, M. Devin, S. Ghemawat, I. Goodfellow, A. Harp, G. Irving, M. Isard, Y. Jia, R. Jozefowicz, L. Kaiser, M. Kudlur, J. Levenberg, D. Mane, R. Monga, S. Moore, D. Murray, C. Olah, M. Schuster, J. Shlens, B. Steiner, I. Sutskever, K. Talwar, P. Tucker, V. Vanhoucke, V. Vasudevan, F. Viégas, O. Vinyals, P. Warden, M. Wattenberg, M. Wicke, Y. Yu, and X. Zheng. TensorFlow: Large-scale machine learning on heterogeneous systems, 2015. Software available from tensorflow.org.

- Andersen (1999) L. B. Andersen. A simple approach to the pricing of bermudan swaptions in the multi-factor libor market model. Available at SSRN 155208, 1999.

- Bachouch et al. (2018) A. Bachouch, C. Huré, N. Langrené, and H. Pham. Deep neural networks algorithms for stochastic control problems on finite horizon, part 2: numerical applications. arXiv preprint arXiv:1812.05916, 2018.

- Barrera-Esteve et al. (2006) C. Barrera-Esteve, F. Bergeret, C. Dossal, E. Gobet, A. Meziou, R. Munos, and D. Reboul-Salze. Numerical methods for the pricing of swing options: a stochastic control approach. Methodology and computing in applied probability, 8(4):517–540, 2006.

- Becker et al. (2019a) S. Becker, P. Cheridito, and A. Jentzen. Deep optimal stopping. Journal of Machine Learning Research, 20(74):1–25, 2019a.

- Becker et al. (2019b) S. Becker, P. Cheridito, A. Jentzen, and T. Welti. Solving high-dimensional optimal stopping problems using deep learning. arXiv preprint arXiv:1908.01602, 2019b.

- Becker et al. (2020) S. Becker, P. Cheridito, and A. Jentzen. Pricing and hedging american-style options with deep learning. Journal of Risk and Financial Management, 13(7):158, 2020.

- Bello et al. (2016) I. Bello, H. Pham, Q. V. Le, M. Norouzi, and S. Bengio. Neural combinatorial optimization with reinforcement learning. arXiv preprint arXiv:1611.09940, 2016.

- Bernhart et al. (2012) M. Bernhart, H. Pham, P. Tankov, and X. Warin. Swing options valuation: A bsde with constrained jumps approach. In Numerical methods in finance, pages 379–400. Springer, 2012.

- Bouchard and Chassagneux (2008) B. Bouchard and J.-F. Chassagneux. Discrete-time approximation for continuously and discretely reflected bsdes. Stochastic Processes and their Applications, 118(12):2269–2293, 2008.

- Bouchard and Warin (2012) B. Bouchard and X. Warin. Monte-carlo valuation of american options: facts and new algorithms to improve existing methods. In Numerical methods in finance, pages 215–255. Springer, 2012.

- Buehler et al. (2019) H. Buehler, L. Gonon, J. Teichmann, and B. Wood. Deep hedging. Quantitative Finance, 19(8):1271–1291, 2019.

- Carmona and Touzi (2008) R. Carmona and N. Touzi. Optimal multiple stopping and valuation of swing options. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 18(2):239–268, 2008.

- Chan-Wai-Nam et al. (2019) Q. Chan-Wai-Nam, J. Mikael, and X. Warin. Machine learning for semi linear pdes. Journal of Scientific Computing, Feb 2019.

- E et al. (2017) W. E, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- El Karoui et al. (1997) N. El Karoui, C. Kapoudjian, É. Pardoux, S. Peng, M.-C. Quenez, et al. Reflected solutions of backward sde’s, and related obstacle problems for pde’s. the Annals of Probability, 25(2):702–737, 1997.

- Fécamp et al. (2020) S. Fécamp, J. Mikael, and X. Warin. Deep learning for discrete-time hedging in incomplete markets. Journal of computational Finance, 2020.

- Garcıa (2003) D. Garcıa. Convergence and biases of monte carlo estimates of american option prices using a parametric exercise rule. Journal of Economic Dynamics and Control, 27(10):1855–1879, 2003.

- Glasserman (2013) P. Glasserman. Monte Carlo methods in financial engineering, volume 53. Springer Science & Business Media, 2013.

- Glorot and Bengio (2010) X. Glorot and Y. Bengio. Understanding the difficulty of training deep feedforward neural networks. In Proceedings of the thirteenth international conference on artificial intelligence and statistics, pages 249–256, 2010.

- Han et al. (2017a) J. Han, A. Jentzen, and E. Weinan. Overcoming the curse of dimensionality: Solving high-dimensional partial differential equations using deep learning. arXiv preprint arXiv:1707.02568, pages 1–13, 2017a.

- Han et al. (2017b) J. Han, A. Jentzen, and E. Weinan. Overcoming the curse of dimensionality: Solving high-dimensional partial differential equations using deep learning. arXiv:1707.02568, 2017b.

- Huré et al. (2018) C. Huré, H. Pham, A. Bachouch, and N. Langrené. Deep neural networks algorithms for stochastic control problems on finite horizon, part i: convergence analysis. arXiv preprint arXiv:1812.04300, 2018.

- Huré et al. (2019) C. Huré, H. Pham, and X. Warin. Some machine learning schemes for high-dimensional nonlinear pdes. arXiv preprint arXiv:1902.01599, 2019.

- Ibáñez (2004) A. Ibáñez. Valuation by simulation of contingent claims with multiple early exercise opportunities. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 14(2):223–248, 2004.

- Kohler et al. (2010) M. Kohler, A. Krzyżak, and N. Todorovic. Pricing of high-dimensional american options by neural networks. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 20(3):383–410, 2010.

- Longstaff and Schwartz (2001) F. A. Longstaff and E. S. Schwartz. Valuing american options by simulation: a simple least-squares approach. The review of financial studies, 14(1):113–147, 2001.

- Øksendal and Sulem (2005) B. K. Øksendal and A. Sulem. Applied stochastic control of jump diffusions, volume 498. Springer, 2005.

- Shreve (2004) S. E. Shreve. Stochastic calculus for finance II: Continuous-time models, volume 11. Springer Science & Business Media, 2004.

- Sirignano and Spiliopoulos (2018) J. Sirignano and K. Spiliopoulos. Dgm: A deep learning algorithm for solving partial differential equations. Journal of computational physics, 375:1339–1364, 2018.

- Sutton et al. (2000) R. S. Sutton, D. A. McAllester, S. P. Singh, and Y. Mansour. Policy gradient methods for reinforcement learning with function approximation. In Advances in neural information processing systems, pages 1057–1063, 2000.

- Trabelsi (2013) F. Trabelsi. Study of undiscounted non-linear optimal multiple stopping problems on unbounded intervals. International Journal of Mathematics in Operational Research, 5(2):225–254, 2013.

- Warin (2012) X. Warin. Gas storage hedging. In Numerical methods in finance, pages 421–445. Springer, 2012.

- Zhao et al. (2011) T. Zhao, H. Hachiya, G. Niu, and M. Sugiyama. Analysis and improvement of policy gradient estimation. In Advances in Neural Information Processing Systems, pages 262–270, 2011.