Choosing the Right Return Distribution and the Excess Volatility Puzzle

Abstract

Proponents of behavioral finance have identified several “puzzles” in the market that are inconsistent with rational finance theory. One such puzzle is the “excess volatility puzzle”. Changes in equity prices are too large given changes in the fundamentals that are expected to change equity prices. In this paper, we offer a resolution to the excess volatility puzzle within the context of rational finance. We empirically show that market inefficiency attributable to the volatility of excess return across time, is caused by fitting an improper distribution to the historical returns. Our results indicate that the variation of gross excess returns is attributable to poorly fitting the tail of the return distribution and that the puzzle disappears by employing a more appropriate distribution for the return data. The new distribution that we introduce in this paper that better fits the historical return distribution of stocks explains the excess volatility in the market and thereby explains the volatility puzzle. Failing to estimate the historical returns using the proper distribution is only one possible explanation for the existence of the volatility puzzle. However, it offers statistical models within the rational finance framework which can be used without relying on behavioral finance assumptions when searching for an explanation for the volatility puzzle.

Keywords: Rational dynamic asset pricing theory, Behavioral finance, Market efficiency, Excess returns volatility, Normal compound inverse Gaussian distribution.

1 Introduction

Proponents of behavioral finance have attacked the models put forth by proponents of traditional finance which assumes that market participants should behavior rationally in making financial decisions. For this reason, traditional finance proponents are commonly referred to as proponents of rational finance. Those in the behavioral finance camp have pointed to the historical behavior of the stock market that is inconsistent with financial theory based on rational finance as evidence for the failure of rational finance. These empirical observations that are inconsistent with rational finance are referred to as finance “puzzles”. One of the most striking puzzles is the volatility puzzle.

The volatility puzzle has been used to describe two observations in the market: idiosyncratic volatility puzzle and the excess volatility puzzle. With respect to the former, there are several empirical studies that have investigated the relationship between future return and risk. These studies have used various proxies for risk such as the expected return from the capital asset pricing model and idiosyncratic risk. According to financial theory, there should be a positive relationship between expected return and risk. Many empirical studies do indeed report a positive relationship. However, several studies, starting with Ang et al., (2006) and almost a decade later by Stambaugh et al., (2015), have found that contrary to what finance theory would predict, there is an inverse relationship, idiosyncratic risk and future return. This has been labeled the idiosyncratic volatility puzzle or simply the volatility puzzle and as the low volatility anomaly by the asset management community. Several studies have used other measures of risk such as idiosyncratic skewness, co-skewness, maximum daily return, and liquidity risk to explain the idiosyncratic volatility puzzle. The behavioral finance camp has offered a solution based on investor sentiment and the lottery effect.

The volatility puzzle that we focus on in this paper is the excess volatility puzzle, first identified by Shiller, (1981) and LeRoy and Porter, (1981). Excess volatility in the equity market means that changes in equity prices are too large given changes in the fundamentals that are expected to move equity prices. As Shiller, (2003) notes “The most significant market anomaly that efficient market theory fails to explain is excess volatility. The idea that stock prices change more than they rationally should is more troubling for efficient market theorists than any other anomaly, such as the January effect or the day-of-the-week effect.” The behavioral finance explanation for the existence of excess volatility offered by Shiller and others is that the influence of investor behavior attributable to either psychological or sociological beliefs is more important than the pricing models proposed by rational finance.

Earlier studies have measured excess volatility by comparing the stock price volatility to volatility bounds obtained from stock prices derived from an assumed dividend discount model. To measure the variation in excess returns, LeRoy and Lansing, (2016) defined a variation measure based on a composite variable, , that depends on the stochastic discount factor, the growth rate of dividends, and the price-dividend ratio. In the LeRoy and Lansing model (LLM), the gross return on a stock and a bond are written as a function of the composite variables and respectively. They demonstrated that if the conditional variances of and are constant across date- events, then excess returns on a stock are unpredictable. In that case, markets are efficient. In their model, LeRoy and Lansing assume that the composite variables and are both conditionally log-normal.

In this paper, we show that if the composite variables are independent and identically log-normally distributed, then the conditional variances of and are not constant across date- events. Therefore, the excess returns on a stock are predictable (i.e., markets are inefficient). If the distribution of financial risk-factors are indeed non-Gaussian distributed and exhibit tails that are heavier than the normal distribution, the LLM can explain the excess volatility puzzle. In this paper, we revisit the puzzle by extending the LeRoy and Lansing, (2016) approach to accommodate rare events. We assume two different distributions for the composite variables.

First, we assume that the distribution of the composite variables exhibits a log-normal inverse Gaussian (NIG) distribution.111See Barndorff-Nielsen, (1997). We propose this distribution because the class of NIG distributions is a flexible system of distributions that includes fat-tailed and skewed distributions. Moreover, the normal distribution is a special case of NIG (see Barndorff-Nielsen,, 1997). We investigate the excess volatility puzzle by fitting the NIG distribution to the LeRoy and Lansing’s log-composite variables and evaluate conditional variances of and . We find that the estimates of the conditional variances of and obtained from the NIG fitted model are constant across date- events and the variation of the excess return is almost equal to zero. Thus, the excess returns on stock are unpredictable, and therefore markets are efficient.

Second, we generalize the NIG distribution by defining a new fat-tail distribution, the normal compound inverse Gaussian (NCIG), assuming that the distribution of the log-composite variables is NCIG. By fitting the NCIG distribution, the variability of excess return is constant across date- event and the estimates of excess returns variation declines to zero. Thus, the excess volatility puzzle can be explained by fitting a more appropriate distribution for the excess gross return and thereby markets are efficient when the excess volatility puzzle is considered.

There are three sections that follow in this paper. In the next section, Section 2, we define the LLM model and derive a formula for the excess log-return of stocks and bonds by assuming a NIG distribution for the the composite variables. In Section 3 we describe our data set and fit three distributions normal, NIG and NCIG distributions to the data. We demonstrate that the variability in the conditional variances of and produced by the models is partially attributable to the poor fit of the tail of the return distribution. We show that both the NIG and NCIG distributions are flexible enough to demonstrate the efficiency of markets in terms of the excess volatility puzzle. Section 4 concludes the paper.

2 Volatility Puzzle

Behavioral finance proponents assert that investors believe that the mean dividend growth rate is more variable than it actually is. Similarly, price-dividend ratios and returns might also be excessively volatile because, as behavioralists claim, investors extrapolate past returns too far into the future when forming expectations of future returns.222Shafir et al., (1997), and Ritter and Warr, (2002) claim that the variation in ratios and returns are due to investors mixing real and nominal quantities when forecasting future cash flows. Barberis et al., (2001) show that the degree of loss aversion depends on prior gains and losses.

LeRoy and Lansing, (2016) offered a model that provides an explanation for the excess volatility puzzle. By extending their framework, we offer resolutions to the excess volatility puzzle within the theory of rational finance to demonstrate how the excess volatility puzzle can be resolved.

In the LLM, , is the stock gross return333For a dividend-paying stock, the gross return on a stock is where is the ex-dividend stock price at and is the dividend received in period . in the period , and it has the representation 444See LeRoy and Lansing, (2016).

| (1) |

where is the ex-dividend stock price at , , denotes the information set consisting of all linear functions of the past returns available until time , is the dividend received in , is the stochastic discount factor at , and

| (2) |

LeRoy and Lansing, (2016, p. 4) introduced as a composite variable that depends on the stochastic discount factor, the growth of dividends and the price-dividend ratio.

Similarly, in the LLM, the gross bond return in the period , has the representation

| (3) |

where is the price at of a default-free bond, is the coupon-rate at time , and

| (4) |

Thus, the stock excess return by taking the logs and subtracting (1) from (3) has the form

| (5) |

In (5), and are the errors in forecasting and respectively.

Next, in the LLM, it is assumed that conditional on , the composite variables and are log-normally distributed; in the other words, and .555Here, stands for equal in distribution between two random variables or two stochastic processes. This assumption for the distribution of the composite variables yields the following expression for the excess return:

| (6) |

By taking the mathematical expectation of both sides of (6), the excess gross return forecast is

| (7) |

Taking the unconditional variance in (7), leads to

| (8) |

LL-Efficiency Claim: “The left-hand side of (8) gives a measure of the variation in excess returns. Eq. (8) shows that if the conditional variances of and are constant across date- events (although generally not equal to zero), then excess returns on stock are unpredictable. In that case markets are efficient. If, on the other hand, the conditional variances differ according to the event, then a strictly positive fraction of excess returns are forecastable, so markets are inefficient.”

We show that because the distribution of financial risk factors is non-Gaussian distributed and exhibits tails heavier than the Gaussian distribution, this can explain the efficiency of the market according to the LeRoy and Lansing, (2016) approach.

We now extend LLM, assuming that the composite variables, and are log-NIG distributed. Recall that a random variable has a NIG distribution, denoted , , if its density is given by

| (9) |

Then, has mean , variance , skewness and excess kurtosis . The moment-generating function of , is given by

| (10) |

Now, we assume that the composite variables and are log-NIG distributed, denoted

Therefore, the excess gross return is

Then, similar to (7), we have the following expression for the excess gross forecast return

| (11) |

Taking the unconditional variance in (11), leads to the following extension of the variation in excess returns:

However, in general, we can adjust LeRoy and Lansing, (2016, p. 6)’s claim as follows:

Revised Efficiency Claim: “The left-hand side of (12) gives a measure of the variation in excess returns. Eq.(12) shows that if the tail indices , , the asymmetric parameters , and the scale parameters , of and are constant across date- events (although generally not equal to zero), then excess returns on stock are unpredictable. In that case, markets are efficient. If, on the other hand, those parameters differ according to the event, more precisely, the right-hand side of (11) is time dependent, then a strictly positive fraction of excess returns are forecastable, so markets are inefficient.”

3 Numerical example

In this section, we investigate the LL-Efficiency Claim and Revised Efficiency Claim using a numerical example. To determine market efficiency, we estimate the excess return variation by applying the three models proposed in this paper.

3.1 Estimating the excess return variation measures using the normal distribution

Let and be the cumulative (gross) daily closing stock and bond returns, respectively. Under the LLM, it is assumed that conditional on , the composite variables and are log-normally distributed. Then, and , which leads to:

-

1.

Stock log-return, , condition on , at is , where is the dynamics of the risk-free rate and

-

2.

Bond log-return, , condition on , at is .

To estimate the excess return variability measure, we use market indices for the quadruple where (i) , the risky asset, is the SPDR S&P 500 index;666 https://www.marketwatch.com/investing/index/spx (ii) is the cumulative VIX 777http://www.cboe.com/products/vix-index-volatility/vix-options-and-futures/vix-index/vix-historical-data (i.e., represent the cumulative of VIX in ), (iii) , the riskless asset as proxied by the 10-year Treasury yield 888https://ycharts.com/indicators/10\_year\_treasury\_rate, and (iv) is the cumulative TYVIX (i.e., represent the cumulative of CBOE 10-year Treasury Note Volatility Index (TYVIX) index in ).999http://www.cboe.com/products/vix-index-volatility/volatility-on-interest-rates/cboe-cbot-10-year-u-s-treasury-note-volatility-index-tyvix The database to estimate the excess returns variation covers the period from January 2014 to December 2018 (1,258 daily observations) collected from Bloomberg Financial Markets.

From (8), the estimates for using a fixed windows of size 252 each (one-year of daily data) are obtained by

| (13) |

where .

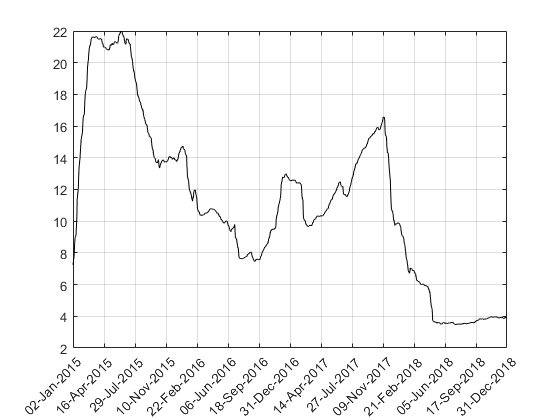

Figure 1 displays estimates for the variation in excess returns when the composite variables are normally distributed. The estimated values vary in the interval , indicating that the conditional variances of the composite variables are not constant across date- event. As to the LL-Efficiency Claim, it is concluded that a strictly positive fraction of excess returns is forecastable, so markets are inefficient. We show that there is a problem in fitting the log-normal distribution that is reflected by the variability of the conditional variances of the composite variables. Thus, we re-estimate the excess returns variation by fitting the NIG to the log-composite variables.

3.2 Estimating the excess return variation measures using the NIG distribution

We believe that a distribution with tails heavier than the

normal distribution can explain why the unconditional variances of the composite variables are constant across time. Here it is assumed that conditional on , the composite variables and are log-NIG distributed. In the other words, and

This leads to

and ,

where and (see the Appendix).

Thus, having daily return data for the S&P500, for , one-year of daily data, we fit the NIG distribution of daily S&P 500 returns (assuming that these returns are iid NIG) and find estimates for Moving the estimation window , we estimate and we continue in this manner for four years of daily data. Similarly, having daily return data for the yield on 10-year Treasury notes for we fit the NIG distribution to the daily yield of 10-year Treasury note returns (assuming that the daily returns are iid NIG) and we find estimates for Moving the estimation window , we estimate and continue in this manner for four years of daily data.

From (12), having computed (estimated) we compute

| (14) |

From (11), the estimates for using of fixed windows of size 252 each (one-year of daily data) are

| (15) |

where .

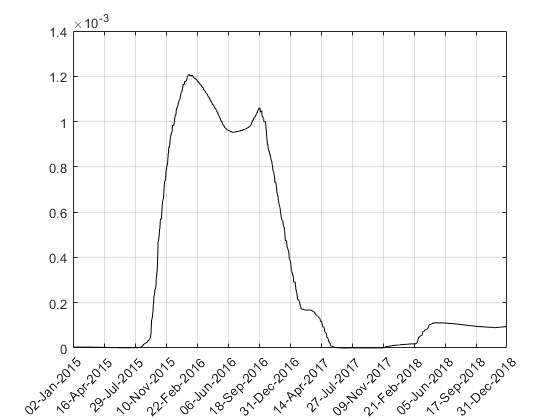

Figure 2 shows the estimates of the excess return variation across time. Comparing Figure 2 to Figure 1, one can graphically check the difference between the two methods for estimating the excess return variation. The estimates of the excess return variation in the interval are constant and significantly lower when the NIG distribution is fitted compared to when the log-normal distribution is fitted. Thus the tail indices , , the asymmetric parameters , and the scale parameters , of the composite variables are constant across date- events. Therefore, according to the Revised Efficiency Claim, it is demonstrated that the excess returns for the stock market are unpredictable, and therefore markets are efficient.

The estimates of the excess return variation plotted in Figure 2 indicate that the variation of gross excess returns is attributable to poorly fitting the tail of the return distribution and that the puzzle disappears by employing a more appropriate distribution for the return data. However, to demonstrate that the inefficiency of the market, attributable to the volatility of excess returns across time, is caused by fitting the wrong distribution, we reexamine the puzzle by fitting a new fat-tail distribution. We modify the probability distribution of the composite variables with a new heavy tail distributions and re-estimate the excess return variation to explain the excess volatility in the market.

3.3 Estimating the excess return variation measures using the normal compound inverse Gaussian distribution

In this subsection, we use a new type of Lévy process relative to the NIG distribution described by Shirvani et al., 2019a , which they call the normal compound inverse Gaussian (NCIG) distribution. We use this distribution to estimate the excess variation measure. The NCIG is a mixture of the normal and doubly compound of the inverse Gaussian (IG) distribution. It is a heavy-tailed distribution with tails that are heavier compared to the NIG distribution. The moment-generating function (MGF) of the NCIG distribution has an exponential form, and it gives an explicit formula for the excess return variation measure. It seems that the NCIG distribution is an efficient distribution for composite variables because it is a heavy tail distribution, and its MGF has an exponential form. To define the NCIG distribution, we first describe the Doubly Subordinated IG Process.101010See Shirvani et al., 2019b .

Definition 1: Doubly Subordinated IG Process: Let and , be independent IG Lévy subordinators,111111A Lévy subordinator is a Lévy process with an increasing sample path (see Sato,, 1999). , , then the compound subordinator has density function given by

| (16) |

where . The MGF of is

| (17) |

where .

A special case of the Doubly Subordinated IG Process is when and . In this case, the NCIG is defined as follows.

Definition 2: Normal compound inverse Gaussian Let and , be independent IG Lévy subordinators, , , and Let be a doubly subordinator IG process with MGF given by (17), and is a Brownian motion Lévy process, denoted by . Then the Lévy process is a NCIG Lévy process, denoted , with MGF given by

| (18) |

where . Furthermore, , i.e. . By setting , the characteristic function

of is obtained, and thus is omitted.

Now it is assumed that conditional on , the composite variables and are log-NCIG distributed. In the other words, and

Then, similarly to (11), we have the following expression for the excess gross forecast return

| (19) |

Taking the unconditional variance in (11) leads to the following extension of the excess return variation measure:

| (20) |

Similar to the NIG case, we fit the NCIG distribution to daily returns for the S&P500 index and the yield on 10-year Treasury notes. We estimate model parameters by applying the empirical characteristic function method (see Yu,, 2003).

From (19) and the estimated values for we compute

| (21) |

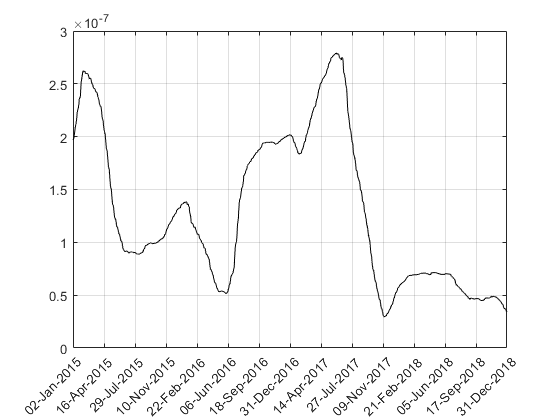

We compute the variation of excess returns by equation (15). Figure 3 shows the estimates of the variation of excess returns over a rolling estimation with windows of size 252. The estimates of excess returns variation are almost zero across date- events. These estimates are significantly lower compared to when the normal distribution and NCIG distribution are fitted. It shows that the parameters , , , , , and are constant across date- events. With respect to the Revised Efficiency Claim, it is concluded that the excess returns on the stock market are unpredictable, and that markets are efficient.

4 Conclusion

In this study, we demonstrate that the excess volatility puzzle can be explained by fitting an appropriate distribution for the gross rate of returns for the stock market and the bond market. We empirically show that the reported market inefficiency, attributable to the volatility of excess return across time is caused by fitting the wrong distribution to historical returns. We fit the normal, normal inverse Gaussian, and normal compound inverse Gaussian distributions to the historical returns to evaluate the variation of excess gross returns. The results indicate that the variability of excess gross returns disappears by employing the normal inverse Gaussian and normal compound inverse Gaussian distributions to the return data. The estimated values of the excess gross returns variation are constant and markedly lower when the normal inverse Gaussian and normal compound inverse Gaussian distributions are fitted compared to when the normal is fitted. Thus, the excess volatility puzzle can be explained by fitting a more appropriate distribution for the excess gross return and thereby markets are efficient when the excess volatility puzzle is considered.

Finally,we note that our approach, fitting a proper probability distribution to capture extreme events, is not the only possible explanation for the excess volatility puzzle. However, it is a statistical model within the framework of the rational theory of finance that can be used without relying on behavioral finance assumptions when searching for an explanation of the excess volatility puzzle.

References

- Ang et al., (2006) Ang, A., Hodrick, R., Xing, Y., and Zhang, X. (2006). The cross-section of volatility and expected returns. Journal of Finance, 61(1):259–299.

- Barberis et al., (2001) Barberis, N., Huang, M., and Santos, T. (2001). Prospect theory and asset prices. Quarterly Journal of Economics, 116:1–53.

- Barndorff-Nielsen, (1997) Barndorff-Nielsen, O. (1997). Normal inverse Gaussian distributions and stochastic volatility modeling. Scandinavian Journal of Statistics, 24(1):1–13.

- LeRoy and Lansing, (2016) LeRoy, S. F. and Lansing, K. J. (2016). Capital market efficiency: A reinterpretation. Technical Report, Department of Economics, University of California, Santa Barbara, 28.

- LeRoy and Porter, (1981) LeRoy, S. F. and Porter, R. D. (1981). Tests based on implied variance bounds. Journal of Financial Economics, 49(3):555–574.

- Ritter and Warr, (2002) Ritter, J. and Warr, R. (2002). The decline of inflation and the bull market of 1982 to 1997. Journal of Financial and Quantitative Analysis, 37:29–61.

- Sato, (1999) Sato, K.-I. (1999). Lèvy Processes and Infinitely Divisible Distributions. Cambridge, UK, Cambridge.

- Shafir et al., (1997) Shafir, E., Diamond, P., and Tversky, A. (1997). Money illusion. Quarterly Journal of Economics, 112:341–374.

- Shiller, (1981) Shiller, R. J. (1981). Do stock prices move too much to be justified by subsequent changes in dividends? American Economic Review, 71(3):421–435.

- Shiller, (2003) Shiller, R. J. (2003). From efficient market theory to behavioral finance. Journal of Economic Perspectives, 17:83–104.

- (11) Shirvani, A., Rachev, S., and Fabozzi, F. (2019a). Multiple subordinated modeling of asset returns. arXiv:1907.12600.

- (12) Shirvani, A., Stoyanov, S., Fabozzi, F., and Rachev, S. (2019b). Equity premium puzzle or faulty economic modelling. arXiv:1909.13019v2.

- Stambaugh et al., (2015) Stambaugh, R., Yu., J., and Yua, Y. (2015). Arbitrage asymmetry and the idiosyncratic volatility puzzle. Journal of Finance, 70(5):1903–1948.

- Yu, (2003) Yu, J. (2003). Empirical characteristic function estimation and its applications. Econometric Reviews, 23(1):93–123.

Appendix

In this appendix, we derive the distribution of the stock gross return when the conditional distribution of the composite variable is log-NIG distributed.

Let conditional on , be log-NIG distributed. This leads to

Therefore,

where