On the Hauck-Donner Effect in Wald Tests: Detection, Tipping Points, and Parameter Space Characterization

Abstract The Wald test remains ubiquitous in statistical practice despite shortcomings such as its inaccuracy in small samples and lack of invariance under reparameterization. This paper develops on another but lesser-known shortcoming called the Hauck–Donner effect (HDE) whereby a Wald test statistic is not monotonely increasing as a function of increasing distance between the parameter estimate and the null value. Resulting in an upward biased -value and loss of power, the aberration can lead to very damaging consequences such as in variable selection. The HDE afflicts many types of regression models and corresponds to estimates near the boundary of the parameter space. This article presents several new results, and its main contributions are to (i) propose a very general test for detecting the HDE, regardless of its underlying cause; (ii) fundamentally characterize the HDE by pairwise ratios of Wald and Rao score and likelihood ratio test statistics for 1-parameter distributions; (iii) show that the parameter space may be partitioned into an interior encased by 5 HDE severity measures (faint, weak, moderate, strong, extreme); (iv) prove that a necessary condition for the HDE in a 2 by 2 table is a log odds ratio of at least 2; (v) give some practical guidelines about HDE-free hypothesis testing. Overall, practical post-fit tests can now be conducted potentially to any model estimated by iteratively reweighted least squares, such as the generalized linear model (GLM) and Vector GLM (VGLM) classes, the latter which encompasses many popular regression models.

Keywords: Iteratively reweighted least squares algorithm; Matrix derivatives; Significance testing; Regularity conditions; Vector generalized linear model.

1 Introduction

In classical likelihood theory three test statistics are used for general hypothesis testing and inference. They are the likelihood ratio test (LRT), Rao’s score (Lagrange multiplier) test, and the Wald test. It is well-known the LRT generally performs the best, and that the Wald test suffers from shortcomings such as its lack of invariance under reparameterization and inaccuracy in small samples. Despite these, the Wald test is probably the most widespread test, as output such as Table 3 is ubiquitous in statistical practice.

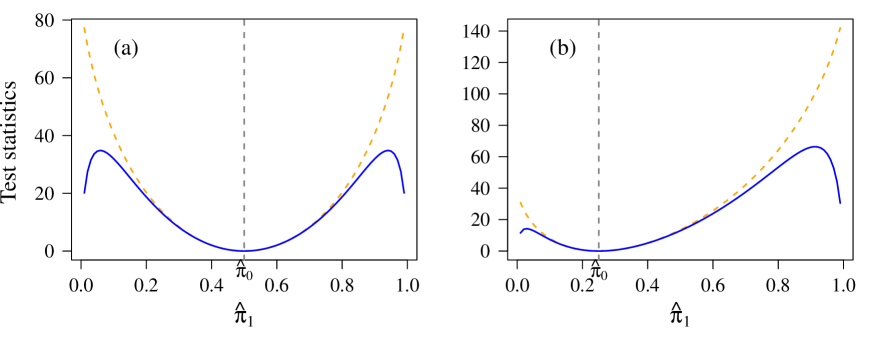

A lesser known but no less pernicious problem of the Wald test is that it suffers potentially from the Hauck-Donner effect (HDE; Hauck and Donner, 1977, 1980) whereby the test statistic fails to increase monotonically as a function of its distance from the null value, e.g., as in Figure 1. Consequently, a truly large effect contaminated by the HDE might be construed as being nonsignificant. The loss of power problem is aggravated by variable selection procedures that are based on Wald’s test.

In general likelihood theory, much of statistical inference is dichotomized into the cases where the true parameter value is either in the interior of parameter space or lies on its boundary. This article is concerned with the interface of the two. Informally, partition the closure into its interior and boundary, and further partition where may be the empty set. The usual regularity conditions fully operate practically in but start breaking down in for want of sufficient Taylor series terms, which we define as the subspace where an aberration of the Wald statistic occurs. Failure to distinguish between and can result in incorrect inferences, therefore special attention should be made to identify it if it occurs. This article sheds light on (Figure 5).

One reason for choosing and defining as such is the huge popularity of Wald tests in general regression modelling, including generalized linear models (GLMs; Nelder and Wedderburn, 1972). They appear almost universally as standard computer output in the form of a 4-column matrix (called a Wald table in this article) consisting of the point estimates, standard errors, Wald statistics, and -values, with optional embellishments of astericks and dots.

Despite four decades since it was first observed, there has been relatively very little general work characterizing the Hauck-Donner phenomenon, or even to detect it. This work is an attempt to address these. We use ‘general’ because special cases such as for the (normal approximation to the) binomial are very well-known special cases only. An empirical approach is taken in this article and we develop new methods that can be used routinely on any GLM or potentially any model based on a weighted crossproduct matrix of the form (, say) within an iteratively reweighted least squares (IRLS) algorithm. Consequently the results are very general and widely applicable for HDE detection.

Væth (1985) studied the HDE but mainly restricted his investigation to the one-sample problem for one-parameter exponential families. His results were heavily dependent on the nice mathematical properties of exponential families and it was stated that these do not easily generalize to arbitrary families of distribution functions. He showed that, in general, the Wald test statistic should be used cautiously with discrete probability models due to certain boundary problems, and that the test may also be misleading in certain families of continuous distributions. He also advised that Wald’s test should be used cautiously in logistic regressions with many explanatory variables. This caution has been repeated by others, e.g., Xing et al. (2012) in the context of genome-wide case-control association studies for genetic screening suggested the LRT as a better alternative.

It is stressed here, as does Væth (1985), that it is the behaviour of the Wald statistic for , for fixed sample size , as the maximum likelihood estimate (MLE) moves away from the null value that is of concern and not the distributional properties of as . This article concerns simple null hypotheses of the form for some known prespecified that is usually taken to be 0; the signed square root of the Wald statistic for the th coefficient is where the Wald statistic is asymptotically under . Note that while the denominator of is sometimes evaluated at (in which case the HDE will be absent), the vast majority of software such as glm() in R evaluate the standard error SE at the MLE so that the HDE is an ever-present threat.

Notationally, let the element of the inverse of a matrix A having element be denoted by , and and indicates that the symmetric matrix A is positive-definite and positive semi-definite respectively. The Hadamard (element-by-element) and Kronecker products of two matrices A and B are denoted by and respectively. If and are -vectors then is an order- matrix whereas is an -vector with elements . We also let be a vector of 0s except for a 1 in the th position, whose dimension is obvious, and the indicator function equals 1 if and 0 otherwise. We use to denote the LRT statistic.

An outline of the paper is as follows. As a concrete example, we consider the original data set of Hauck and Donner (1977) in Section 2 (as well as citing more instances of the HDE by others for additional motivation) before describing elements of a class of models called VGLMs—the detection test specifically applies to this (large) class. The general test is described for VGLMs in Section 3, and supporting asymptotic results are given in Section 4. Section 5 proposes two important refinements: finite-difference approximations for derivatives to make HDE detection applicable to all VGLMs, and categorizing the HDE into 4 severity measures that form a partition of . Some numerical examples are given in Section 6, and Section 7 discusses computational details and provides some practical guidelines. The paper concludes with a discussion of the overall findings. The methodology here is implemented in the R package VGAM 1.0-6 or later (available on CRAN) for 100+ models. Some extensions for detecting the HDE in related contexts are given in Appendices A2–A5.

2 The Hauck & Donner Data Set

Hauck and Donner (1977) apply logistic regression to a table of counts to illustrate the HDE. Because of its simplicity a more complete analysis of the behaviour of is permitted here. We will generalize the data slightly to afford a little more flexibility (Table 1(a)). The actual data has , , , and we will generally keep these fixed but vary . The sample proportions are at , and at . Fit

| (1) |

so that and is the estimated log odds ratio. The HDE becomes pronounced once past a certain threshold as or , corresponding to sparsity in one off-diagonal cell. In Figure 2 the larger threshold corresponds to . For such count tables the well-known formula

| (2) |

is routinely used. For handling low counts, there are several popular pre-fit improvisions, e.g., adding 0.5 to each cell count in the SE calculation give a bias-corrected log odds ratio, and applying the Mantel-Haenszel method. However, in the context of routine logistic regressions, it is far more convenient for some post-fit test for HDE to be applied to a fitted model—if the HDE is absent then we can conclude that the counts are sufficiently large that no adverse behaviour on the SE was seen.

In this particular example the HDE can be explained by a situation already well-known to practitioners. This is not the case in general because the HDE has been observed in other regression models by various authors since. Some examples include Storer et al. (1983) in conditional logistic regression with matched and stratified samples, Væth (1985) in one-sample problems for one-parameter exponential families and GLMs, Nelson and Savin (1990) in Tobit and nonlinear regression models, Fears et al. (1996) in a balanced 1-way random effects ANOVA design, Therneau and Grambsch (2000, p.60) in Cox proportional hazards models, and Kosmidis (2014) in cumulative link models. In general the Wald test can be expected to be valid only if a normal likelihood can be used to approximate the profile likelihood for the parameter well (Meeker and Escobar, 1995) and the observed value of the sufficient statistic is away from .

Regardless of its underlying cause, it would be very useful to have a procedure for detecting the HDE that could be routinely applied to a given regression model. To this end, Section 3 proposes a method for this, and the method applies very generally to models estimated by IRLS. This general purpose algorithm has been used to fit many popular regression models, and most notable is the GLM class, of which a multivariate extension called vector GLMs (VGLMs; Yee, 2015) have been proposed.

Continuing with this example, when the full model is fitted by IRLS, then

| (5) |

Consequently, (2) is obtained, as is

| (6) |

which is plotted in Figure 2(b). It appears impossible to write a closed form expression for upon setting (6) to 0; this indicates that it is impractical trying to determine beforehand the threshold of how low the counts can be before observing the HDE—and likewise for more complicated situations. This supports the view that a detection test post-fit is more practical than trying to avoid it pre-fit.

Incidentally, the LRT cannot exhibit the HDE

for all , provided that , therefore is convex in . It will also be seen that the Rao score (Lagrange multiplier) test is also immune to the HDE as it does not depend on the third derivatives of the log-likelihood.

| (a) | (b) | |||||

|---|---|---|---|---|---|---|

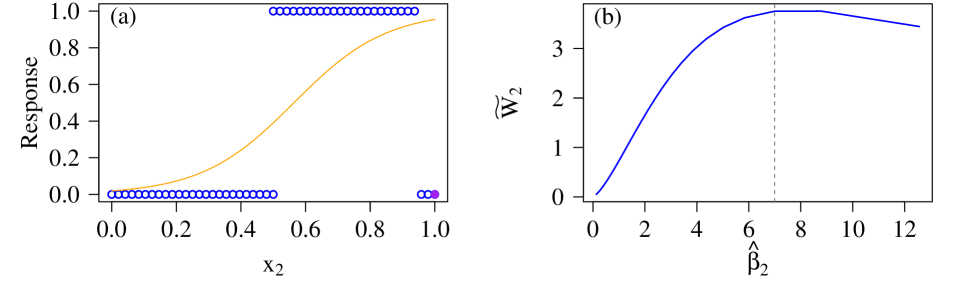

Somewhat similar to the Hauck & Donner data set, it is noted that the HDE can arise as a result of data exhibiting near overlap, quasi-complete separation or complete separation (see, e.g., Albert and Anderson, 1984; Lesaffre and Albert, 1989). For example, starting off with a data set comprising , , plus , we replace each successive on the RHS of by (Figure 3) except for the very rightmost. As the number of increases the logistic regression (1) fitted to these data has increasing and the HDE will become present eventually. Figure 3(b) shows the Wald statistic as a function of , and the HDE is evident at the RHS. Data separation is likely in Big Data situations when extraneous covariates are included in regression models of high dimensionality.

2.1 VGLMs

The detection test specifically applies to this (large) class, therefore we briefly summarize them. They can loosely be thought of as multivariate GLMs applied to parameters but extending far beyond the exponential family; more details can be found in Yee (2015). The data is , , independently, with response and usually with intercept . The th linear predictor is

| (7) |

for some parameter link function satisfying the usual properties (strict monotonicity and twice-differentiable). If then linear constraints between the regression coefficients are accommodated, as

| (11) |

for known constraint matrices of full column-rank (i.e., rank ncol()), and is a possibly reduced set of regression coefficients to be estimated. While trivial constraints are denoted by , other common examples include parallelism (), exchangeability, and intercept-only parameters . The overall ‘large’ model matrix is , which is with trivial constraints, while is the ‘smaller’ model matrix associated with a model.

Some models have -specific explanatory variables, such as a time-varying covariate, then (11) extends to

| (12) |

with provision for offsets . The results of this paper apply most generally to this case.

The are the working weight matrices, comprising at iteration , for each log-likelihood component . Here, is the log-likelihood, and Fisher scoring is adopted as opposed to Newton-Raphson. Usually the individual expected information matrices (EIMs) are closely related to the working weight matrices as , i.e.,

for . In particular, (2.1) holds for 1-parameter link functions .

For VGLMs the estimated variance-covariance matrix is

| (14) |

evaluated at the final iteration, where are all the regression coefficients to be estimated. The iteration number will be suppressed henceforth. One reason for the widespread use of the Wald test is their computationally convenience: the estimated variance-covariance matrix (14) is a by-product of the IRLS algorithm, and importantly it is evaluated at the MLE .

3 HDE Detection

The overall model matrix has form so that and

| (15) |

for , and and . For simplicity map the coefficients to so that for the th coefficient because A is positive-definite. Then can be computed by

| (16) |

Of central interest for testing versus is

| (17) |

This equation furnishes a first-derivative detection test: the HDE is evident for if (17) is negative-valued. Consequently that coefficient’s SE and -value should be flagged as unreliably biased upwards. Only a quadratic form needs to be computed in (16) for each .

With provision to handle constraint matrices and as in (12),

because the working weight matrices have the simple outer product form (2.1).

3.1 Some Remarks and Properties

Several remarks are in order at this stage, which mainly pertain to models with parameter.

- 1.

-

2.

The following are some sufficient conditions for to be monotonic as .

- (i)

-

(ii)

If . For example, the full-likelihood LM

(21) whose EIM is diagonal so that each parameter can be treated separately, the regression coefficients corresponding to do not suffer from the HDE because the (1, 1) element of the EIM is not a function of . For the choice of link function does matter, e.g., using an identity link then , so that if then and so that ; thus if .

-

3.

For 1-parameter VGLMs, (3) simplifies to

This makes allowance for a variety of link functions, e.g., probit and complementary log-log links for binary regression.

-

4.

For standard logistic regression , which is an odd function about . Thus the model becomes more susceptible to the HDE as approaches a boundary (observed in Figure 2 as becomes large.) It is shown that is a necessary condition for the HDE in Section 4.2. In fact, if then it is shown in Appendix A6 that approximately is needed in order for the HDE to occur, e.g., this corresponds to an odds ratio of about or higher.

-

5.

For the standard Poisson regression model, applying a similar derivation as logistic regression to a data set comprising points at and points at , yields

(22) Thus conducive conditions for the HDE are when and . Figure 4 shows this for , and taking on successive values in . It can be seen that if were rejected when then it would do so only for or 3 but not 1.

-

6.

Given that is computable, it can be of interest to determine the rate at which the -value decreases as a function of the effect size. Assuming that for a two-sided alternative, called say, then

(23) An application might be in designing simple experiments to determine how the -value will decrease given an increasing treatment effect.

- 7.

-

8.

If and are orthogonal then the element of the information matrix remains 0 upon differentiation, therefore agrees intuitively that the Wald statistic for is minimally affected by .

-

9.

Second derivatives for the Wald statistic follow as before; these can be used, for example, to determine whether is a convex function, i.e., is a particular model impervious to the HDE? Use

(24) and

(25) to allow for the computation of . To compute (25) requires

(26) This in turn requires the third derivatives of the link function in its inverse form. The ordinary form is straightforward while the inverse form can be reexpressed as

(27) e.g., for logistic regression and (27) is .

4 Inference

4.1 Results for a 1-Parameter Regular Model

The results for models can be investigated further. Consider the special case of being the sole parameter of a regular distribution. For simplicity use the observed information here. We have the following result concerning two tipping points.

Theorem 1. For versus , and where the observed information is evaluated at , if the HDE is present then

-

(a)

the ratio of the Wald and LRT statistics satisfies

(28) -

(b)

and the ratio of the Wald and Rao score test statistics satisfies

(29)

Proof.

(a)

As

the HDE is present iff (19):

| (30) |

A Taylor series expansion of about gives

The inequality (28) follows from the property .

(b) Expand about the MLE:

where if and only if the HDE occurs. Divide both sides by so that

i.e.,

when the HDE occurs. Take the reciprocal

and square both sides to obtain (29).

Equation (28) can be interpreted by saying that if the Wald statistic becomes too small relative to the LRT statistic (which is likely to be more accurate) then the HDE will become present. Likewise we can interpret (30) by saying that as , if the negative second derivative of does not grow fast enough compared to the the third derivative of then the HDE will become present. The accuracy of the bound depends upon the fourth and higher derivatives of .

Equations (28) and (29) suggest that when the HDE first starts to occur. In fact empirical findings indicate that in the presence of a strong HDE.

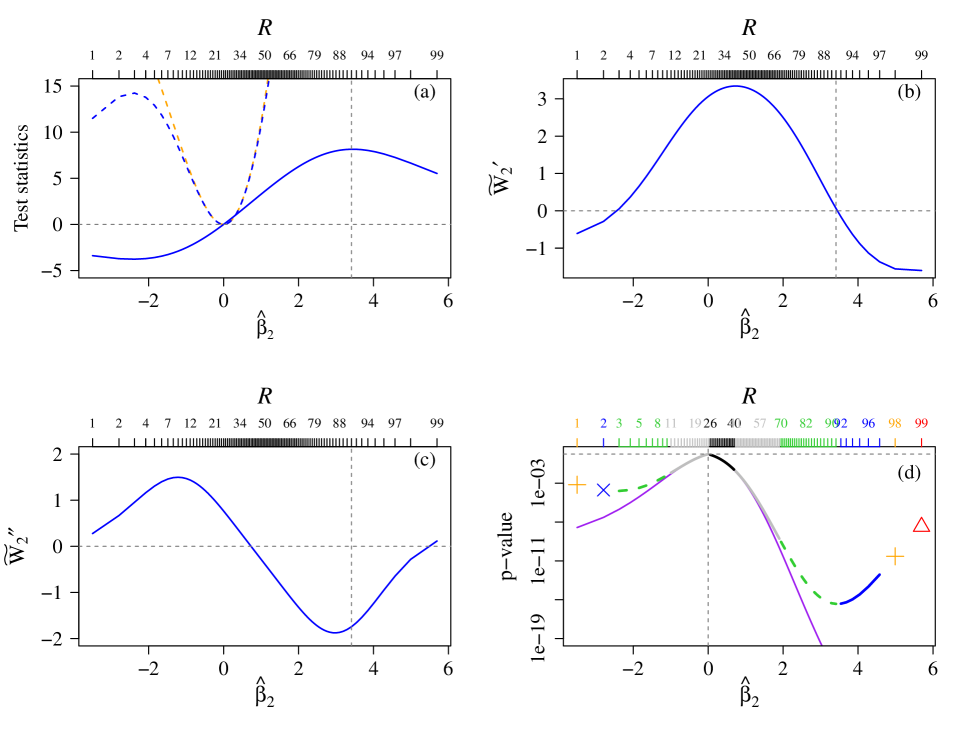

Extending the result to the two-parameter case is wieldy. However, applying this result to the 2-parameter Hauck and Donner (1977) data, the 3/5 threshold lies between and 94 successes, whereas the HDE becomes present for at (Figure 2(a)–(b)). This suggests that the method can work well when the number of parameters is low or are orthogonal. As another numerical example, when fitting a Poisson regression to the data described for (22) one obtains a perfect match because the two cases of HDE present corresponds to a ratio and the other cases have a ratio .

Unfortunately the LRT and Wald statistics are not independent; if they were then their ratio would have a distribution whose mean is infinite. The lower tail probability at the quantile of this distribution is , indicating that their positive correlation creates a bias away from the null.

As , it follows that . Indeed, has approximate asymptotic expectation , where

as under , and for a normal distribution. Hence

| (31) |

Thus

| (32) |

and similarly

An approximate upper bound from Chebyshev’s inequality shows that

as the probability of the HDE occuring by chance, given , however the bound is not very sharp.

A closing remark is that the asymptotic normality of the MLE can be augmented with an additional regularity condition to prevent the HDE, by restricting the parameter space. Under , the extra condition is

| (33) |

so that in (see, e.g., Cox and Hinkley, 1974, pp.294–5). Here, E1 is the expected information of one observation, and denotes convergence in distribution.

4.2 Disproportional Sampling

In the case of a table it is now shown that, for a fixed size effect , disproportional sampling can be used to circumvent the HDE.

Table 1(b) is a modification of the HD data to allow for disproportional sampling. Here, so that the (2, 1) cell becomes low, hence individuals with need to be sampled with greater intensity. This is achieved by having where the parameter . With being the usual scenario, increasing had no affect on the HDE as the sign of (17) is unchanged. The quantity is then used to measure the relative sampling intensity. The sample proportions and remain unchanged.

With a logit link the new sampling scheme affects the intercept only. The inverse crossproduct matrix is

and then by (16), . The HDE will be present for if

| (35) |

This shows that is needed before the HDE is possible, provided that and is away from the boundaries. This corresponds to an odds ratio of about 7.4 or higher. If then the HDE is unlikely, in particular, the quantity

measures the sampling effect on the HDE: small/large values of implies HDE is unlikely/likely respectively. This make intuitive sense as the (2, 1) cell increases as a function of the total sample size by choosing so that .

5 Refinements

5.1 Finite-Differences

Unfortunately implementing HDE detection for any particular model based on (3) is labor-intensive, e.g., Appendix A1, which has two consequences. Firstly, this work suggests that the EIM is to be preferred over the observed information matrix (cf. Efron and Hinkley (1978) who prefer the latter), because terms often vanish upon expectation and therefore lead to simplification, e.g., (21). Secondly, numerical computation of the first two derivatives of circumvents this problem and provides a general method that empirical testing has shown to work well. In particular, simplify (3) to

| (36) |

where may be approximated by, e.g., central finite differences. Similarly,

| (37) |

with separate formulas to handle the diagonal and off-diagonal elements. A step value of has been found to be reasonable for most models, being on the -scale.

5.2 Severity Measures and Parameter Space Partitioning

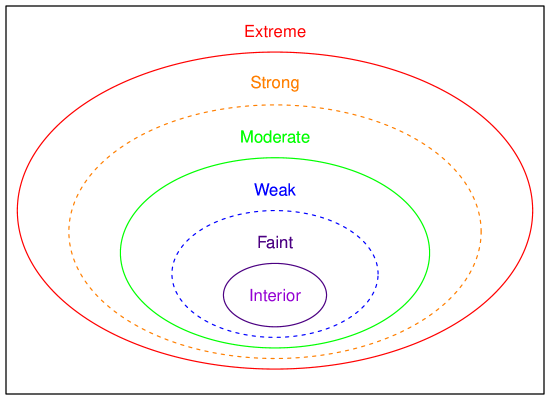

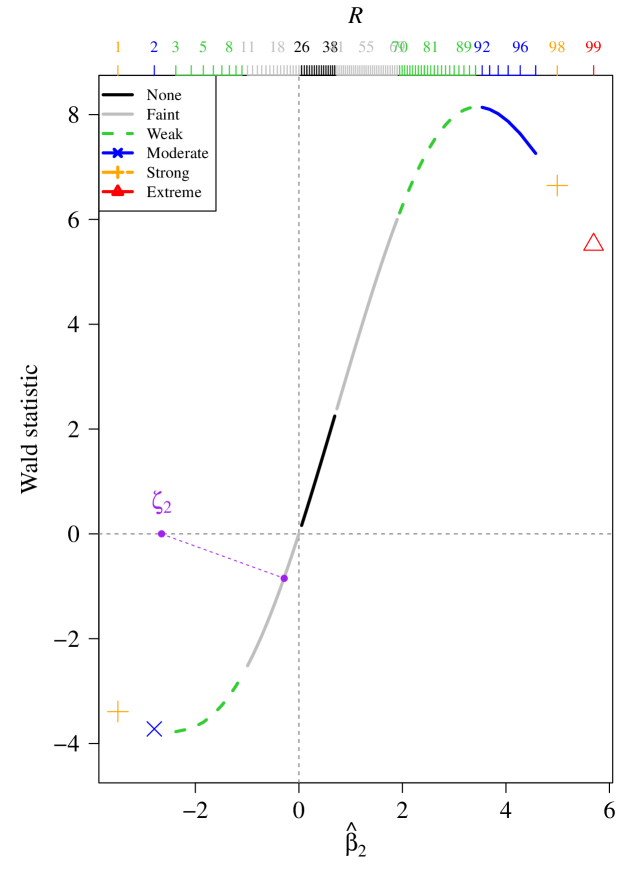

So far, the above establishes whether a particular model suffers from the HDE, however, a small negative derivative could indicate a mild or extreme effect. It could also be argued that once the Wald statistic starts to decrease but without having a negative derivative, then the HDE has already started to occur. Fortunately, it is possible to gauge how severe the HDE is based the first two derivatives of . As is asympotically locally quadratic about the origin, is assumed piecewise convex–concave–convex for , and ditto for . Table 2 is a summary.

Using the simple notation to denote the -axis, let be the intersection of the normal line at with the -axis (purple dashed line of Figure 6). The movement of as the coefficient changes allows further properties of the curve to be determined additional to the location of inflection points. (The use of is a more convenient alternative to using the tangent.) Denoting the cutpoints as , , , , for none, faint, weak (mild), moderate, severe (strong), extreme, they are defined by , , , , , so that and are inflection points. For positive estimates

and

| (38) | |||||

For the data set of Table 1(a) the scheme classifies no HDE for , faint HDE for , mild HDE for , moderate HDE for , severe HDE for , and extreme HDE for (Fig. 6).

| Severity | Key property | ||||

|---|---|---|---|---|---|

| None | convex | ||||

| [boundary] | |||||

| Faint (Very mild) | concave | ||||

| [boundary] | |||||

| Weak (Mild) | concave | ||||

| [boundary] | |||||

| Moderate | concave | ||||

| [boundary] | |||||

| Strong (Severe) | concave | ||||

| [boundary] | |||||

| Extreme (Very severe) | convex |

As a consequence, the HDE severity measures allow the parameter space to be partitioned practically into an interior where the regularity conditions hold, which is encased by layers at the boundary of increasing HDE severity. Figure 5 displays this schematically. For a given data set and regression model, not all the layers present and may be discrete. The descriptors should be interpreted relatively rather than absolutely—their purpose is to provide an ordinal categorization of the HDE severity.

6 Examples

6.1 Birds and Logistic Regression

Mangiafico (2015) applies a variable selection algorithm based on the AIC to choose covariates in a logistic regression applied to a bird data set with 67 cases after missing values have been removed. Six variables plus an intercept were chosen out of a possible 13 variables (Table 3) for the response Status.

For this model, 3 variables display the HDE: Upland, Migr and Indiv (Table 3), and Mass is weakly affected. According to the usual Wald test, the former two have p-values of moderate strength: 2% and 3%, while Indiv is more strongly significant (0.005). However, LRT p-values for the 3 variables are 0.00135, 0.0076, respectively. This suggests that these variables are considerably more statistically significant than would naïvely appear; the ratios of the p-values are approximately 15, 4 and . The latter is huge and shows that a moderate HDE can be associated with an enormous relative effect on the p-value (although qualitatively similar); that variable is actually skewed and a log-transformation would be recommended.

| Parameter | MLE | SE | HDE severity | ||||

|---|---|---|---|---|---|---|---|

| (Intercept) | 3.44 | 2.06 | 1.67 | 0.03 | Faint | 0.56 | 0.18 |

| Upland | 4.73 | 2.04 | 2.32 | 0.05 | Strong | 0.47 | 0.13 |

| Migr | 2.02 | 0.93 | 2.17 | 0.05 | Moderate | 0.48 | 0.33 |

| Mass | 0.00 | 0.00 | 2.73 | 186.40 | Weak | 0.32 | 559.30 |

| Indiv | 0.01 | 0.00 | 3.48 | 46.19 | Moderate | 0.34 | 35.03 |

| Insect | 0.27 | 0.14 | 1.90 | 7.87 | Faint | 0.06 | 1.38 |

| Wood | 1.95 | 1.30 | 1.50 | 0.75 | Faint | 0.02 | 0.06 |

6.2 Wine and the Partial Proportional Odds Model

Table 1 of Kosmidis (2014) reports the Wald table of a partial proportional odds model (PPOM) fitted to a wine tasting data set where the response bitterness was measured on a 5-level ordinal scale. The two binary variables ‘temperature’ and ‘contact’ were measured in this experiment, and the parallelism assumption was applied to only. Three of the SEs are inflated. The data was first analyzed in Randall (1989).

Table 4 provides additional information to the Wald table, viz. the first two derivatives of the signed root Wald statistics. (The sign of some of the coefficients differ from his table because the reversed PPOM, , was used so that the direction matches logistic regression.) The HDE is evident in 3 of the regression coefficients: , , , where the latter two have the extreme form. Furthermore, and are weakly affected. The causes of the HDE in the first two, which relate to the intercepts, may be confounded with the requirement of satisfying the ordering . For the SE is so inflated that one of its Wald statistics’ slopes is only slightly negative. For this, the LRT p-value for testing is 0.006, which differs totally from the Wald test p-value of 1.00!

Kosmidis (2014) discusses adjustments specifically for cumulative link models and proposes bias reduction methods in order to safeguard against infinite parameter estimates. In this example, the number of coefficients manifesting the HDE ought to alert the practitioner of a nonstandard situation. Furthermore, suspicion for something gone awry should have been raised by monitoring convergence and observing that this took 19 IRLS iterations—this is considerably more than the usual 6–8 iterations—and that the decrease in deviance during the last 10 iterations was only slight.

| Parameter | MLE | SE | HDE severity | |||

|---|---|---|---|---|---|---|

| 1.27 | 0.51 | 2.48 | 1.25 | 1.32 | Weak | |

| 1.10 | 0.44 | 2.51 | 1.92 | 0.86 | Faint | |

| 3.77 | 0.80 | 4.71 | 0.44 | 0.79 | Moderate | |

| 23.23 | 6904.18 | 0.00 | 0.00 | 0.00 | Extreme | |

| 21.53 | 11433.17 | 0.00 | 0.00 | 0.00 | Extreme | |

| 2.15 | 0.59 | 3.65 | 1.02 | 0.94 | Weak | |

| 2.87 | 0.81 | 3.54 | 1.22 | 0.15 | Faint | |

| 20.89 | 6904.18 | 0.00 | 0.00 | 0.00 | Faint | |

| 1.47 | 0.47 | 3.13 | 1.87 | 0.15 | Faint |

7 Computational Details and Recommendations

One can obtain an HDE-free Wald test by evaluating the denominator of the Wald statistic at rather than . For simplicity of notation, this section enumerates the regression coefficients to be estimated of a general VGLM as for . The tests are versus where usually . By an “HDE-free Wald test”, it is meant that is replaced by its hypothesized value when computing the test statistic’s SE so that its derivative with respect to vanishes. Then two options open up: whether or not to perform IRLS iterations for the other coefficients. If so, then this is equivalent to fitting the LRT model under , so it is not surprising that the time cost is similar. Notationally, let correspond to no (further) iteration and be with iteration.

Computationally, the use of instead of is implemented by deleting the th column of and adding to the matrix of offsets. If iterating for the other coefficients, initial values can be obtained from the original model and then convergence is usually rapid (often only 1 or 2 IRLS iterations are needed).

To obtain the SE for for a HDE-free Wald test, the main steps are as follows.

-

(i)

Optionally iterate (i.e., compute ), else use the MLEs for the following.

-

(ii)

Compute using or .

-

(iii)

Update the generic fitted values and the working weights from .

-

(iv)

Compute the Cholesky decompositions of the .

-

(v)

Compute and its QR-decomposition.

-

(vi)

Compute and then to obtain SEk.

These steps are performed for each .

A small numerical study involving timing various VGLMs fitted with the author’s software gave the following results.

-

•

The cost of conducting an HDE test on all the regression coefficients is typically about the cost of obtaining the HDE-free iterated Wald statistics.

-

•

Without iterations, HDE-free Wald tests can be about 25% less costly time-wise compared to LRTs.

-

•

With iteration, HDE-free Wald tests can be about 30% more costly time-wise than LRTs.

-

•

The cost of a score test is similar to an iterated Wald test.

These results suggest that the cost of a LRT and a HDE-free Wald test is roughly comparable.

For the practitioner, the above suggests that a reasonable strategy is to firstly apply an HDE test to all the regression coefficients. If any are affirmative, then the next step is applied to those coefficients and depends on whether SEs are sought, e.g., as a rough measure of statistical uncertainty. Thus, secondly, when SEs are required, HDE-free Wald tests should be conducted for those coefficients, and should only -values be necessary, then LRTs should be computed instead. As for deciding whether iterations are required, if the computational expense is of concern, then the non-iterated variant is suggested as it can be approximately half the cost of the iterated variant.

It should be noted that conducting hypothesis tests may be difficult for some models, such as a non-parallel cumulative link model because of intrinsic order restrictions such as . Circumventing the difficulties involved is an area for future research. Another note is that the score test lacks the intuitive appeal of the Wald test and may be inconsistent (Freedman, 2007), therefore it is suggested that the order of preference of the tests be, in decreasing order, LRTs followed by HDE-free Wald tests followed by score tests.

8 Discussion

In an era of high-dimensional statistics and Big Data the -value remains a chief centerpiece of classical frequentist statistical inference (Dezeure et al. (2015), Fan (2014), Meinshausen et al. (2009)) despite recent statements about their misuse Wasserstein and Lazar (2016). Indeed, Siegfried (2010) writes: “It’s science’s dirtiest secret: The ‘scientific method’ of testing hypotheses by statistical analysis stands on a flimsy foundation.” Although most of the weakness is interpretative this article highlights another deficiency in the form of the HDE.

This work was motivated by practical Wald testing in a general regression setting, and has developed methods for testing whether an estimate gives rise to parameters so close to the parameter space boundary that some Wald statistics are aberrant. The practical implication is clear: for SEs computed at the MLE establishing whether the HDE is manifest in a fitted model should be determined where possible, and if so then the LRT or other large-sample tests be conducted instead. Ideally HDE testing should be carried out whenever a Wald table is presented, and statistical software should be upgraded to make this practical and automatic. Software for variable selection based on the usual Wald statistics need modification too. With business intelligence software companies being a major driver of Big Data, it is plausible that litigation could occur if they fail to respond adequately to implement new methodologies such as here to address known flaws such as the HDE. As a minimum, disclaimer statements that the HDE is not detected could be issued as interim measures.

This article is a first step towards shedding light on the structure of the parameter space in a practical sense. There is further work to be done, such as refining the severity measures of Section 5.2, exploring consequences under a Bayesian framework, and seeing if adjustments are needed for multiplicity if we switch to another test. Some new results can be found in Yee (2021). This manuscript has appeared in published form as Yee (2022).

A parting remark is that it has been disappointing to see that most texts on statistical inference and practice do not even mention the HDE, especially those making heavy use of Wald tables. Of the few that do, various authors have described the HDE as ‘the major statistical problem of ’ and ‘certainly disturbing’. It is hoped that this work will help make the HDE a more recognized problem and provide a practical solution.

Acknowledgements I wish to thank the Centre for Applied Statistics and School of Mathematics and Statistics at the University of Western Australia for hospitality during a workshop given there in early 2017 and for valuable feedback that helped lead to this work. Helpful feedback from George Seber and Elbert Chia is gratefully acknowledged.

Appendices

Notes:

- VGAM

-

Version 1.0-4 introduced hdeff() and appeared on CRAN in July 2017.

- VGAM

-

Version 1.1-1 introduced hdeffsev() and appeared on CRAN in Feb 2019.

A1. Two Working Weights Examples

As two simple examples of (3), the following drop the subscript simplicity.

-

(i)

For the zero-inflated Poisson distribution parameterized by

(39) with mixing probability the two derivative matrices are

and

where is the probability of an observed 0. When implementing these in software, symbolic differentiation may be useful for higher order derivatives.

-

(ii)

For the cumulative link model taking levels , let the cumulative probabilities be , then its EIM is tridiagonal and yields non-zero elements of its derivative matrix centered at the th element as

with straightforward truncation of rows and columns for and . The second derivative matrices are

It is possible to use symbolic differentiation, such as R’s deriv3(), however it is not very efficient and produce numerically unstable estimates; it fails to be a general purpose method.

A2. Sandwich Estimators

Extensions to handle sandwich estimators are available, e.g., for GLMs this is (, say)

| (44) |

where is diagonal with elements and variance . Then

| (45) | |||||

by (16) so that can be computed.

For logistic regression the diagonal elements of are so that

Applied to the Hauck & Donner data, it is easily shown that the ordinary SEs and sandwich estimators coincide (i.e., ) because .

A3. Multiple Tests

Up till now simple null hypotheses of the form have been considered. More generally, suppose we wish to test for some matrix L of rank comprising known fixed constants, and -vector of known fixed constants. With the usual regularity conditions holding the Wald statistic

| (46) |

is asymptotically under . To detect any HDE in (46) let , and we conclude that the test suffers from HDE degradation if for any component of . The handling of (46) follows from the main treatment of the paper but with the additional computation

subject to

where the elements of are enumerated by . This admits the solution

| (47) |

A simple example is which yields

Another simple example, relevant for a partial proportional odds model, is

which results in

A4. The Proportional Hazards Model

The Cox model suffers potentially from the HDE (Therneau and Grambsch, 2000, p.60), and we give details for two methods to detect it post-fit.

The first is to utilize Whitehead (1980) who fitted the Cox model as a Poisson GLM. It relies on producing artificial data based on the Poisson-multinomial ‘trick’ (e.g., Baker (1994)) so that the Poisson and partial likelihoods are proportional to each other. However, the setting up of many indicator variables results in the need to estimate many nuisance parameters and the resulting data set can be much larger than the original data set—all this makes the procedure computationally expensive. The supplementary R script gives a numerical example of this method.

The second method is direct computation of the derivatives of the observed information matrix with respect to the and using (16). This is quite manageable since the matrix has a simple form. In the following we adopt a notation similar to Lawless (2003) and assume there are no ties or time-varying covariates for simplicity. The data is of the form , , containing distinct lifetimes and censoring times. Let denote the risk set at . Let or 1 for censored and complete survival times respectively. For individual define so that if and only if .

The observed information matrix is

| (48) |

where, for , . Writing and , and letting the numerator of (48) be called , then

| (49) | |||||

A5. Profile Likelihoods

Suppose where comprise nuisance parameters, and that has continuous first derivatives. Let be the concentrated log-likelihood and the observed information matrix be partitioned as

| (54) |

Then the derivative of the Wald statistics based on requires

where and . Some slight simplification follows by exploiting symmetry through , etc.

A6. Logistic Regression with a Binary Covariate

It is shown here that it is possible to determine whether the HDE will occur for a binary covariate in a logistic regression. The notation here differs slightly from the rest of the paper. We wish to fit the logistic regression

| (56) |

where or 1, and contains other covariates including the intercept. The data can be summarized by Table 5, albeit without being able to reflect the . Order the data so that for , and for , and let

Then

where the summations are over the appropriate suffixes. The (1, 1) element of its inverse is

Its first derivative with respect to is

The last term is

where

Thus the HDE will be present if

| (59) |

The results of Section 4.2 are a special case of this. In particular, suppose that in Table 1(a) so that the intercept in (1) vanishes and need not be estimated. Then straightforward calculations show that the boundary where HDE occurs corresponds to the nonlinear equation . Its numerical solution means that, approximately, is needed in order for the HDE to occur. For positive , this corresponds to an odds ratio of about .

References

- Albert and Anderson [1984] A. Albert and J. A. Anderson. On the existence of maximum likelihood estimates in logistic regression models. Biometrika, 71(1):1–10, 1984.

- Baker [1994] S. G. Baker. The multinomial-Poisson transformation. J. Roy. Statist. Soc. Ser. D, 43(4):495–504, 1994.

- Cox and Hinkley [1974] D. R. Cox and D. V. Hinkley. Theoretical Statistics. Chapman & Hall, London, 1974.

- Dezeure et al. [2015] R. Dezeure, P. Bühlmann, L. Meier, and N. Meinshausen. High-dimensional inference: Confidence intervals, -values and R-software hdi. Statist. Sci., 30(4):533–558, 2015.

- Efron and Hinkley [1978] Bradley Efron and David V. Hinkley. Assessing the accuracy of the maximum likelihood estimator: observed versus expected Fisher information. Biometrika, 65(3):457–487, 1978. With discussion.

- Fan [2014] J. Fan. Features of big data and sparsest solution in high confidence set. In X. Lin, C. Genest, D. L. Banks, G. Molenberghs, D. W. Scott, and J.-L. Wang, editors, Past, Present, and Future of Statistical Science, pages 507–523, Boca Raton, FL, USA, 2014. Chapman and Hall/CRC.

- Fears et al. [1996] T. R. Fears, J. Benichou, and M. H. Gail. A reminder of the fallibility of the Wald statistic. Amer. Statist., 50(3):226–227, 1996.

- Freedman [2007] David A. Freedman. How can the score test be inconsistent? Amer. Statist., 61(4):291–295, 2007.

- Hauck and Donner [1977] W. W. Hauck and A. Donner. Wald’s test as applied to hypotheses in logit analysis. J. Amer. Statist. Assoc., 72(360):851–853, 1977.

- Hauck and Donner [1980] W. W. Hauck and A. Donner. Corrigenda: Wald’s test as applied to hypotheses in logit analysis. J. Amer. Statist. Assoc., 75(370):482, 1980.

- Kosmidis [2014] I. Kosmidis. Improved estimation in cumulative link models. J. Roy. Statist. Soc. Ser. B, 76(1):169–196, 2014.

- Lawless [2003] J. F. Lawless. Statistical Models and Methods for Lifetime Data. John Wiley & Sons, Hoboken, NJ, USA, second edition, 2003.

- Lesaffre and Albert [1989] E. Lesaffre and A. Albert. Partial separation in logistic discrimination. J. Roy. Statist. Soc. Ser. B, 51(1):109–116, 1989.

- Mangiafico [2015] S. S. Mangiafico. An R Companion for the Handbook of Biological Statistics. Version 1.3.1, 2015. URL http://rcompanion.org/documents/RCompanionBioStatistics.pdf.

- Meeker and Escobar [1995] W. Q. Meeker and L. A. Escobar. Teaching about approximate confidence regions based on maximum likelihood estimation. Amer. Statist., 49(1):48–53, 1995.

- Meinshausen et al. [2009] N. Meinshausen, L. Meier, and P. Bühlmann. P-values for high-dimensional regression. J. Amer. Statist. Assoc., 104(488):1671–1681, 2009.

- Nelder and Wedderburn [1972] J. A. Nelder and R. W. M. Wedderburn. Generalized linear models. J. Roy. Statist. Soc. Ser. A, 135(3):370–384, 1972.

- Nelson and Savin [1990] F. D. Nelson and N. E. Savin. The danger of extrapolating asymptotic local power. Econometrica, 58(4):977–981, 1990.

- Randall [1989] J. H. Randall. The analysis of sensory data by generalized linear model. Biometr. J., 31(7):781–793, 1989.

- Seber [2008] G. A. F. Seber. A Matrix Handbook for Statisticians. Wiley, Hoboken, NJ, USA, 2008.

- Siegfried [2010] T. Siegfried. Odds are, it’s wrong: Science fails to face the shortcomings of statistics. Science News, 177(7):26–29, 2010.

- Storer et al. [1983] B. E. Storer, S. Wacholder, and N. E. Breslow. Maximum likelihood fitting of general risk models to stratified data. J. Roy. Statist. Soc. Ser. C, 32(2):172–181, 1983.

- Therneau and Grambsch [2000] T. M. Therneau and P. M. Grambsch. Modeling Survival Data: Extending the Cox Model. Springer, New York, USA, 2000.

- Væth [1985] M. Væth. On the use of Wald’s test in exponential families. Int. Statist. Rev., 53(2):199–214, 1985.

- Wasserstein and Lazar [2016] R. L. Wasserstein and N. A. Lazar. The ASA’s statement on p-values: Context, process, and purpose. Amer. Statist., 70(2):129–133, 2016.

- Whitehead [1980] J. Whitehead. Fitting Cox’s regression model to survival data using GLIM. J. Roy. Statist. Soc. Ser. C, 29(3):268–275, 1980.

- Xing et al. [2012] G. Xing, C.-Y. Lin, S. P. Wooding, and C. Xing. Blindly using Wald’s test can miss rare disease-causal variants in case-control association studies. Ann. Human Genet., 76:168–177, 2012.

- Yee [2015] T. W. Yee. Vector Generalized Linear and Additive Models: With an Implementation in R. Springer, New York, USA, 2015.

- Yee [2021] T. W. Yee. Some new results concerning the Hauck–Donner effect. In preparation, 2021.

- Yee [2022] T. W. Yee. On the Hauck-Donner effect in Wald tests: Detection, tipping points, and parameter space characterization. J. Amer. Statist. Assoc. (in press), 2022.