A proximal MM method for the zero-norm regularized PLQ composite optimization problem

Dongdong Zhang111School of Mathematics, South China University of Technology, Guangzhou, China. Shaohua Pan222(shhpan@scut.edu.cn) School of Mathematics, South China University of Technology,

China. and Shujun Bi333(bishj@scut.edu.cn) School of Mathematics, South China University of Technology,

China.

Abstract

This paper is concerned with a class of zero-norm regularized piecewise

linear-quadratic (PLQ) composite minimization problems, which covers the zero-norm

regularized -loss minimization problem as a special case.

For this class of nonconvex nonsmooth problems, we show that its equivalent

MPEC reformulation is partially calm on the set of global optima and make use of

this property to derive a family of equivalent DC surrogates. Then, we propose

a proximal majorization-minimization (MM) method, a convex relaxation approach

not in the DC algorithm framework, for solving one of the DC surrogates which is

a semiconvex PLQ minimization problem involving three nonsmooth terms. For this method,

we establish its global convergence and linear rate of convergence,

and under suitable conditions show that the limit of the generated sequence is

not only a local optimum but also a good critical point in a statistical sense.

Numerical experiments are conducted with synthetic and real data for

the proximal MM method with the subproblems solved by a dual semismooth Newton method

to confirm our theoretical findings, and numerical comparisons

with a convergent indefinite-proximal ADMM for the partially smoothed DC surrogate

verify its superiority in the quality of solutions and computing time.

Keywords: Zero-norm regularized PLQ composite problems; DC equivalent surrogates;

nonconvex and nonsmooth; proximal MM method; semismooth Newton method

1 Introduction

Let be a piecewise linear-quadratic

nonsmooth convex function, and

be the given matrix and vector, and be

a nonempty polyhedral set. We are interested in the following zero-norm regularized

composite minimization problem

(1)

where is a regularization parameter, denotes

the zero-norm (cardinality) of vectors, and is a small regularization

parameter. The term is introduced to ensure that the objective

function of (1) is coercive and then has a nonempty global optimum set.

For convenience, we denote the sum of the first two functions by

(2)

Since the zero-norm is the root to produce sparse solutions,

the problem (1) has been found to have wide applications in

a host of scientific and engineering problems such as regression and

variable selection in statistics (see, e.g., [40, 16]),

compressed sensing [14] and source separation [6]

in signal processing, imaging decomposition [36] in image science,

feature selection and classification in statistical learning

[5, 46], and so on. In particular, the nonsmooth PLQ

loss makes the problem (1) arise frequently from robust models;

for example, when

with for , it becomes the popular sparsity

regularized -loss minimization in robust sparse recovery [47, 26]

and high-dimensional robust statistics [44, 42];

and when for some ,

it reduces to the sparsity regularized check-loss minimization that is often

used to monitor the heteroscedasticity of high-dimensional data [48, 43].

Owing to the combinatorial property of the zero-norm function,

the problem (1) is generally NP-hard and it is impractical

to seek a global minimum with an algorithm of polynomial-time complexity.

For this class of nonconvex nonsmooth problems, a common way is to

use the convex relaxation technique to achieve a desirable solution in

a statistical sense. The -norm convex relaxation, as a popular

relaxation method, has witnessed considerable progress in theory and computation

since the early works [13, 40]. Though the -norm

is the convex envelope of the zero-norm in the -norm unit ball,

its ability to promote sparsity is weak especially in a complicated

constraint set, say, the simplex set. Inspired by this, many nonconvex

surrogates have been proposed for the zero-norm function, which include

the non-Lipschitz surrogate [9, 10],

smooth concave approximation [5, 32, 46],

and the folded concave functions such as SCAD [16] and MCP [51].

All of these nonconvex surrogates are proposed from the primal viewpoint

and the surrogate problems associated to the first two classes are

only an approximation of (1). Although Soubies et al. [37]

proposed a class of exact continuous relaxation for the - minimization,

their proof depends on the structure of the least-square loss function and

it is not clear whether they are exact or not for the problem (1).

One contribution of this work is to show that an equivalent MPEC of (1)

is partially calm on the set of global optima, thereby obtaining a family of

equivalent DC surrogates from a primal-dual viewpoint.

The calmness of a mathematical programming problem at a solution point was

originally introduced by Clarke [11], and received active study from many

researchers in the past several decades (see, e.g., [7, 49, 50]).

Among others, Ye and Zhu [49, 50] extended it to the partial calmness

at a solution point. Inspired by these works, Liu et al. [27] recently

studied the partial calmness on the global optimum set for the equivalent

MPECs of zero-norm and rank optimization problems so as to achieve their global

exact penalty. By [27, Theorem 3.2], if a special structure is

imposed on the set , such an MPEC is indeed partially calm on

the set of global optima, but this structure is very restricted.

Here we achieve this crucial property without any restriction on

by constructing an appropriate multifunction and using the upper Lipschitz

continuity of the polyhedral multifunction due to Robinson [34].

Also, by combining this result with [27, Appendix B], we conclude that

the SCAD is a member of this family of equivalent DC surrogates.

Although Le Thi et al. [20] ever derived an equivalent DC surrogate

for the zero-norm regularized problem from a primal-dual viewpoint,

they required to be a compact box set, and their surrogate

has a great difference from ours; see Section 3.

Then, inspired by the work [39], we propose a proximal

majorization-minimization (MM) method for solving one of the equivalent

DC surrogate models, a semiconvex PLQ minimization problem involving

three nonsmooth terms, by using a tighter majorization of the DC

surrogate function. The other contribution of this work is to

establish the global convergence and linear rate of convergence

for the proximal MM method, and to demonstrate when the limit of

the generated sequence is locally optimal to the surrogate problem

and the origin problem (1), respectively. In particular,

for the scenario where with

an appropriate convex and the data

comes from a linear observation model, we also derive an error bound to

the true vector for the limit of the generated sequence, which shows that

the limit is good from a statistical perspective.

Numerical experiments are conducted with some synthetic and real data

for the proposed proximal MM with the subproblems solved by a dual semismooth

Newton method (PMMSN for short) to confirm our theoretical findings.

In particular, we compare the performance of PMMSN with the performance of

a globally convergent indefinite-proximal ADMM (iPADMM) proposed for solving

the partially smoothed DC surrogate problem. Numerical comparisons indicate

that PMMSN has an advantage in the quality of solutions and computing time

for most of test examples, whereas iPADMM depends on the choice of the smoothing

parameter that is very sensitive to the data.

It is worthwhile to emphasize that for optimization models involving a smooth

loss term and a nonconvex surrogate of the zero-norm, there are some works to

investigate the error bounds of their stationary points to the true vector

(see, e.g., [25, 8]) or the oracle property of a local optimum

yielded by a specific algorithm [17], but to the best of our knowledge,

for optimization models involving a nonsmooth convex loss and such an equivalent

DC surrogate, there are few works on the statistical error bound

of the critical point yielded by an algorithm. The optimization model

in [39] involves a square-root loss and such a DC surrogate,

but the local optimality and statistical error bound of the obtained

critical point was not discussed. For the box constrained zero-norm

regularized nonsmooth convex loss minimization, Bian and Chen [4]

recently presented an exact continuous relaxation and proposed a smoothing

proximal gradient algorithm for finding a lifted stationary point of

the relaxation model, but they did not provide a statistical error bound

for the lifted stationary point. Also, as will be shown in Section 3,

their continuous relaxation model is actually a member of our equivalent DC surrogates.

Notation: In this paper, and denote an identity matrix

and a vector of all ones, respectively, whose dimensions are known from the context.

For any matrix , and

denote the spectral norm, elementwise maximum

norm and column sum norm of , respectively, i.e.,

,

and for given index sets and

, and

denote the matrix consisting of those rows of with

and those columns of with , respectively.

For a set , means the convex hull of and

denotes the indicator function of , i.e., if

and otherwise.

For given vectors with

for each , the notation denotes the box set.

For a vector , represents the smallest nonzero entry of

and denotes the vector obtained by arranging the entries

of in a nonincreasing order. For an extended real-valued ,

we say that is proper if for all

and ,

and denote by the conjugate of , i.e.,

.

For a lower semicontinuous (lsc) function

and a parameter , and

denote the proximal mapping and Moreau envelope of , respectively,

defined as

When is convex,

is a Lipschitzian mapping with Lipschitz constant , and is

a smooth convex function with .

2 Preliminaries

First, we recall the concepts of the proximal, regular and limiting subdifferentials

from [35, Definition 8.45 & 8.3] and the definition of the subderivative

and second subderivative from [35, Definition 8.1 & 13.3] for

an extended real-valued function.

2.1 Generalized subdifferentials and subderivatives

Definition 2.1

Consider a function and a point

with finite. The proximal subdifferential of at , denoted by

, is defined as

the regular subdifferential of at , denoted by , is defined as

and the (limiting) subdifferential of at , denoted by , is defined as

Remark 2.1

(i) At each , the sets and

are always closed convex, is

closed but generally nonconvex, and they satisfy

.

These inclusions may be strict when is nonconvex, and when is convex,

they all reduce to the subdifferential of at in the sense of

convex analysis [33].

(ii) The point at which

(respectively, and

) is called a limiting

(respectively, proximal and regular) critical point of .

By [35, Theorem 10.1], a local minimizer of is necessarily

a regular critical point of , and then a limiting critical point.

However, the converse may not hold; for example, the function

for satisfies ,

but is not a local minimizer of .

(iii) Recall that a function

is said to be semiconvex if there exists a constant such that

is convex, and the smallest

of all such is called the semi-convex modulus of .

For this ,

at all .

Definition 2.2

For a function , a point with

finite and any , the subderivative function is defined by

while the second subderivative of at for and is defined by

2.2 Semismoothness of locally Lipschitzian mappings

Semismoothness was originally introduced by Mifflin [29] for functionals,

and Qi and Sun [30] later developed the class of vector semismooth functions.

Before introducing the semismoothness, we recall the Clarke Jacobian

of a locally Lipschitzian mapping.

Definition 2.3

(see [12, Definition 2.6.1])

Let be a locally Lipschitzian

mapping defined on an open set . Denote by

the set of points where is Fréchet differentiable

and by the Jacobian of at .

For any given , the Clarke (generalized) Jacobian

of at is defined as

Definition 2.4

(see [30, 38])

Let

be a locally Lipschitzian mapping on an open set .

The mapping is said to be semismooth at a point if

is directionally differentiable at and for any and

,

and is said to be strongly semismooth at if is semismooth

at and for any ,

The mapping is said to be a semismooth (respectively, strongly semismooth)

function on if it is semismooth (respectively, strongly semismooth)

everywhere in .

Lemma 2.1

Given and , let

for . Then, for and

its Clarke Jacobian is given by

Notice that in Lemma 2.1

is piecewise affine. By [15, Proposition 7.4.7]

every piecewise affine mapping is strongly semismooth.

Hence, it is strongly semismooth.

Let be the family of proper lsc functions

with which are convex in the interval and

satisfy the following conditions

(3)

Since and is the unique minimizer of over ,

for any we have

As far as we know, such a characterization for

with first appeared in [28]. This implies that the zero-norm

regularized problem (1) is equivalent to the problem

(4)

in the following sense: if is globally optimal to the problem (1),

then is a global optimal solution of the problem (4),

and conversely, if is a global optimal solution of (4),

then is globally optimal to (1). The problem (4) is a mathematical

program with an equilibrium constraint .

Although the MPEC is known to be very tough, in this section we can establish that

the MPEC (4) is partially calm over its global optimal solution set,

denoted by , and employ its relation with exact penalization

to derive a class of equivalent DC surrogates for (1).

As mentioned in Section 1, when has a special structure,

the MPEC (4) is partially calm over the set

by [27, Theorem 3.2], but the required structure is

very restricted. Here, we remove such a restriction and obtain the partial

calmness of (4) over .

Proposition 3.1

The problem (4) is partially calm over the optimal solution set .

Proof:

For each , define the partial perturbation

for the feasible set of (4) by

Fix an arbitrary . Notice that the objective

function of the problem (4) is continuous. By [50, Remark 2.3],

its partial calmness at is equivalent to the existence of

and such that for all and

all ,

(5)

Observe that the solution set is compact. There necessarily exists

such that .

It is easy to check that the function is Lipschitzian

relative to . We denote by

the Lipschitz constant of over the set .

For each , define the multifunction

by

where denotes the Ky Fan -norm of vectors. Since

is a polyhedral multifunction, i.e., its graph is the union of

finitely many polyhedral convex sets, from [34, Proposition 1]

it follows that each is calm at the origin for all ,

which is equivalent to saying that for each ,

there exist and such that

(6)

Set and

. Fix an arbitrary

and an arbitrary .

Take an arbitrary ,

where is such that and

its existence is shown in [27, Lemma 1]. Write

Clearly, . By invoking (6)

with , there exists such that

(7)

Let

and .

Notice that

By invoking [27, Lemma 1] with

for each , it immediately follows that

where the second inequality is since ,

the third one is due to the inequality (7),

the last is using ,

and the equality is due to and .

Notice that since and

by .

From the Lipschitz continuity of over ,

it immediately follows that

Combining with the last inequality, we obtain

(8)

Now take for

and for .

Clearly, is a feasible point

of the MPEC (4) with . Then, it holds that

Together with the inequality (8),

the stated inequality (5) holds.

By the arbitrariness of in , we obtain the desired

result. The proof is then completed.

Notice that Proposition 3.1 still holds when is replaced by

a general Lipschitzian function. Since the objective function of (4)

is coercive relative to ,

combining Proposition 3.1 with [27, Proposition 2.1(b)],

we have the following conclusion.

Theorem 3.1

There exists a threshold such that the following penalty problem

(9)

associated to each has the same global

optimal solution set as the MPEC (4) does. Also,

this conclusion holds when is replaced by a lower bounded

Lipschitzian function.

Remark 3.1

By the proof of Proposition 3.1, it follows that

,

which depends on the Lipschitz constant of over the set

, determined by , and the calmness constant

of . So, it is generally hard to achieve an exact

estimation on , and a varying is suggested in

practical computation. We see that, as the regularization parameter increases,

the corresponding threshold becomes smaller,

and consequently, it is easier to choose an appropriate

such that (9) is a global exact penalty.

It is well known that the handling of nonconvex constraints is

much harder than the handling of nonconvex objective functions.

Thus, Theorem 3.1 provides a convenient way

to deal with the difficult MPEC (4) and then the zero-norm

regularized problem (1). In particular, the nonconvexity of

the objective function of (9) is owing to the coupled

term rather than the combination. Such a structure

ensures that the problem (9) associated to every

is an equivalent DC surrogate of (1).

Indeed, by letting

and using the conjugate of , the problem (9)

can be compactly written as follows:

(10)

Since is a nondecreasing finite convex function in ,

clearly, is a DC function and the problem

(10) associated to every

is an equivalent DC surrogate of (1).

When for , clearly, with .

An elementary calculation yields that for .

Now the last two terms in

is precisely the continuous relaxation

of the zero-norm given by [4]. For other choice of , please refer to

[27, Appendix B]. In the rest of this work, we focus on

(11)

for which an elementary calculation yields that the conjugate

has the following form

(12)

To close this section, we summarize the desirable properties of

associated to this . Their proofs are

included in Appendix A where the following functions are needed:

(13a)

(13b)

Proposition 3.2

For any given and , the following results hold with .

(i)

is a lower bounded,

coercive, semiconvex piecewise linear-quadratic function.

(ii)

For any given , the generalized subdifferentials

of at take the form of

(iii)

If is a (limiting) critical point of

with ,

then is also a regular critical point of the zero-norm regularized problem (1).

By Proposition 3.2 (i) and the discussion in the last section,

the zero-norm regularized composite problem (1) is equivalent to

a piecewise linear-quadratic minimization problem (10)

associated to .

Although the objective function of (10) consists of

a smooth with Lipschitzian gradient and a proper

convex function ,

this composite convex function makes the common proximal gradient method

inapplicable to it. By introducing an additional variable ,

the problem (10) can be rewritten as

(14)

so that the ADMM can be applied to solving it, but to the best of our knowledge

there is no convergence guarantee for the ADMM to such a nonconvex nonsmooth problem.

It is worthwhile to point out that the results developed in [45]

for the ADMM is not suitable for the problem (14).

Motivated by the specific structure of and

the recent work by Tang et al. [39], we in this section develop

a tailored proximal MM method for (10).

Fix an arbitrary . For any ,

the convexity and smoothness of implies

(15)

where is the mapping defined in (13b).

Along with the expression of ,

where .

Notice that .

This means that is a majorization of

at . This majorization is tighter than

the one in [39] obtained by the convexity of .

Indeed, by Lemma 1 in Appendix,

where the inequality is using for each ,

and consequently for any ,

The majorization on the right hand side is precisely the one used by Tang et al. [39].

Our proximal MM method is designed by minimizing a proximal version of

the majorization at the th step, and its iterate steps

are described as follows.

Initialization:

Choose a small . Select ,

and .

Seek a starting point and a suitable . Set .

while the stopping conditions are not satisfied do

1.

Let . Compute the optimal solution of the following problem

(16)

2.

Update the proximal parameters and by the following rule

3.

Let , and go to Step 1.

end while

Remark 4.1

(i) Although the problem (10) is a DC program,

Algorithm 1 does not belong to the DCA framework in [21]

since by Lemma 1 in Appendix A.

In fact, by the definition of in (13b) and the expression of ,

it is easy to obtain that

(17)

The proximal term

involved in the subproblems, inspired by the recent work [39], plays a twofold role:

one is to ensure that the subproblem (16) is solvable and the other,

as will be shown in the sequel, is to guarantee the decreasing of

the objective value sequence of the nonconvex problem (10)

and then its global convergence.

(ii) It is well known that for nonconvex optimization problems,

the choice of the starting point determines the quality of the limit

of the sequence generated from this initial point. This means that

the choice of in Algorithm 1 is very crucial. Inspired by

the good performance of -norm regularized problem, we recommend to

use the following :

(18)

As will be shown in Subsection 4.3, such an is not bad at least

in a statistical sense. In addition, we suggest that the parameter

is chosen by for a suitable .

By combining formula (17) with the term

in (16), such a choice of ensures that those very small

(very likely corresponding to a zero entry) becomes zero quickly

since a weight close to is imposed on , those very large

(very likely corresponding to a nonzero entry) continue to be large

since a weight closed to is imposed on , and for the rest,

a smaller means a larger weight imposed on them.

(iii) By the definition of and [33, Theorem 23.8],

it follows that for each ,

(19)

while by Proposition 3.2(ii) and Lemma 1 in Appendix A,

it holds that

where the second equality is by if

and if . So,

Since each ,

the following stopping criterion is suggested for Algorithm 1

(20)

This guarantees that the obtained is an approximate proximal critical point

of .

We shall follow the recipe of the convergence analysis in [2]

for nonconvex nonsmooth optimization problems to establish the global

and local linear convergence of Algorithm 1.

As the first part of the recipe, we analyze the decreasing of the sequence .

Lemma 4.1

Let be the sequence given by Algorithm 1.

Then, for each ,

and then .

Proof:

Fix an arbitrary . By the definition of , clearly, .

By invoking (15) with and

and using the relation for ,

Notice that the objective function of (16) is a sum of

a convex function and a strongly convex quadratic function.

Along with the definition of and , we have

By adding the last two inequalities, we immediately obtain that

This, by the definition of the function ,

is equivalent to saying that

which implies the first part of the conclusions.

Notice that the sequence

is nonincreasing. From its lower boundedness of

in Proposition 3.2 (i), the sequence

is convergent. Combining this with the first part of the conclusions,

we obtain .

The proof is then completed.

The following lemma provides a subgradient lower bound for the iterate gaps.

Lemma 4.2

For each , there exists a vector

such that

Proof:

From the discussion in Remark 4.1 (iii), for each it holds that

Take .

Since is Lipschitzian of modulus ,

from and (13b) we have

The desired result follows from the last two equations. The proof is completed.

By combining Lemma 4.1 and 4.2 with

Proposition 3.2 (iv) and following the similar arguments

as those for [1, Theorem 3.2 & 3.4],

we get the following convergence results.

Theorem 4.1

Let be generated by Algorithm 1.

The following statements hold.

(i)

The sequence has a finite length, i.e.,

.

(ii)

The sequence converges to a critical point

of , say , which is also a regular

critical point of the zero-norm regularized problem (1)

if .

(ii)

The sequence converges to in a Q-linear rate.

4.2 Local optimality of critical points

We have established that the sequence

generated by Algorithm 1 is convergent, and converges Q-linearly

to a proximal critical point of .

It is natural to ask whether such a critical point is a local minimum of

or not. If yes, is it locally optimal to

the zero-norm problem (1)?

Next we provide affirmative answers to the two questions.

Theorem 4.2

Fix arbitrary and . Consider an arbitrary

with and

.

Then, for any , it holds that

, and consequently,

is a local optimal solution of the problem

(10).

Proof:

Fix an arbitrary nonzero .

Define for .

Clearly, is a locally Lipschitz and regular function.

Let for .

Notice that

for . By [35, Proposition 13.19], we have

(21)

Recall that

with for . By [35, Proposition 13.9],

is twice epi-differentiable at for each

. Moreover,

from [35, Exercise 13.18], it follows that

(22)

where the inequality is due to

by [35, Proposition 13.9]. Let for .

Fix an arbitrary .

Since is locally Lipschitz continuous and directionally differentiable,

it holds that

where is the subderivative

function of . By [35, Proposition 13.5],

when ,

which along with (21)-(22) implies that

.

So, it suffices to consider the case where

.

In this case, by the definition of the second subderivative, it follows that

where the second equality is due to

for any sufficiently small . Since ,

it is immediate to have that with

Recall that

for by (13a). From the last two equations,

By the expression of and the formula of

in (34), for all sufficiently

small and all sufficiently close to , we have

for . Along with the last equation and (21)-(22),

.

By the arbitrariness of

and [35, Theorem 13.24], is a local optimal

solution of (10).

Theorem 4.2 states that those critical points

of with not too small nonzero entries

are local minima of . To answer the second question,

we need the following lemma.

Lemma 4.3

Fix an arbitrary . Define

for . Consider an arbitrary with .

If for

and implies ,

then for any ,

and consequently, is a local optimal solution of the problem (1).

Proof:

Fix an arbitrary . Let for

and be same as in the proof of Theorem 4.2.

From the given assumption and [35, Proposition 13.19],

(23)

Write .

Fix an arbitrary

where the equality is due to [19]. Then

.

On the other hand, a simple calculation yields

This means that .

By [35, Proposition 13.5],

when ,

which along with (22) and (23) implies that

. So, it suffices to consider

the case where .

In this case, from the last equation, .

By the definition of the second derivative, equals

This along with (22) and (23) implies that

. By the arbitrariness of

and [35, Theorem 13.24], is a local optimum of (1).

By combining Theorem 4.2 and Lemma 4.3,

we obtain the following conclusion.

Corollary 4.1

Let be the sequence generated by Algorithm 1.

If its limit satisfies ,

then is a local minimum of the problem (10).

If in addition the constraint qualification in Lemma 4.3 holds,

then is also a local minimum of (1).

4.3 Statistical error bound of the limit

In this part we focus on the scenario where

is from the linear observation model

(24)

where each row of follows the normal distribution

, is the true but unknown sparse vector

with sparsity , and is the noise.

We assume that

is nonzero and

with satisfying Assumption 1.

Assumption 1

The function is convex with

and its square is strongly convex with modulus

. By [33, Theorem 23.4], there exists such that

(25)

Since we are interested in the high-dimensional case, i.e. ,

the sample covariance matrix is not positive definite,

but it may be positive definite on a subset of .

Specifically, for a given subset , we say that the sample

covariance matrix satisfies the restricted eigenvalue

(RE) condition over with parameter if

In the sequel, we need a RE condition of

over with parameter where

Obviously, comprises those vector whose components

for are small. By [31, Corollary 1], when

satisfies the RE condition over with parameter

(for example, is positive definite),

for ,

the matrix satisfies the RE condition over

of parameter with probability at least

, where and are the universal positive constants.

This means that for a larger , has the RE

property over of a large with a high probability.

By Lemma 4 in Appendix B, we can establish the following

error bound to the true for the limit of

under the RE condition of over the set .

Theorem 4.3

Suppose that Assumption 1 holds and

satisfies the RE condition of parameter over .

Write .

Take a constant . If the parameters and are chosen such that

and ,

then for the limit of with

for ,

(26)

Remark 4.2

(i) Theorem 4.3 states that for the problem (1)

with from the model (24) and

for satisfying Assumption 1,

when applying Algorithm 1 with appropriate and

for solving its surrogate problem (10),

the limit of the generated sequence satisfies (26)

provided that for .

Such a requirement on is rather mild since it allows

to have more small nonzero entries than , which seems more reasonable than

the one used in [8, Assumption 3.7] for smooth loss functions.

(ii) Recall that are i.i.d. and follow

. All entries of each column of the submatrix

are independent and follow normal distribution. By [41, Lemma 5.5],

it follows that .

Thus, when the noise vector is sparse enough, say,

and with ,

by recalling that is a very small constant, we have

for an appropriately large ,

and consequently, the choice interval of is nonempty and

will become larger as increases. Different from [25] for the smooth loss,

our choice interval of does not involve the noise but requires a certain restriction

on the sparsity of . We see that as the sparsity of

increases (i.e., decreases), the value of becomes smaller

and then the error bound of to the true becomes better.

In addition, similar to the -regularized squared-root loss in [3],

the parameter is required to belong to an interval depending on

the sparsity . Clearly, a large implies a small interval of

the parameter .

Notice that the limit depends on the starting point .

The following result states that, when is chosen by (18),

for a positive constant dependent on

and , which will become smaller for a larger

and a smaller .

Proposition 4.1

Let be the objective function

of (18) and be an approximate optimal solution in the sense

that there exist and with

such that . Suppose that Assumption 1

holds. If the parameter is chosen such that

then

5 Numerical experiments

We test the performance of Algorithm 1 by applying it

to the problem (1) with and

for .

By Theorem 4.1 and Corollary 4.1,

the sequence generated by Algorithm 1 converges Q-linearly to

a limit which is also a local minimum of (10)

if . Since satisfies

Assumption 1, by Theorem 4.3 and

Remark 4.2 (ii), there is a high probability for

to be close to the true if the noise

is sparse enough. To validate the efficiency of Algorithm 1 via numerical comparison,

we here provide a globally convergent ADMM for the partially smoothed form of (10).

5.1 iPADMM for partially smoothed surrogate

As mentioned in the beginning of Section 4, when the ADMM is

directly applied to the surrogate problem (10) or

its equivalent problem (14), there is no convergence certificate.

Recall that the Moreau envelope of with the parameter

is smooth and is globally Lipschitz

continuous. Moreover,

by noting that

We replace in (14) by its Moreau envelope

and apply the ADMM with an indefinite-proximal term (iPADMM for short) to

the partially smoothed formulation of (14):

(27)

where, for any given ,

for . For a given penalty parameter ,

the augmented Lagrangian function of (27) is defined as

The iteration steps of our iPADMM for solving (27) are

described as follows.

Initialization: Select suitable and .

Choose a penalty parameter and a starting point

. Set and .

while the stopping conditions are not satisfied do

1.

Compute the optimal solution of the following minimization problems

(28a)

(28b)

2.

Update the Lagrange multiplier by .

3.

Set , and then go to Step 1.

Remark 5.1

(i) Since ,

the matrix may be indefinite. So, Algorithm 2

is the ADMM with an indefinite-proximal term. After a rearrangement,

where

and . Since and

are separable, it is easy to achieve their proximal mappings

and .

(ii) By combining the optimality conditions of (28a)-(28b)

and the multiplier update step, and comparing with the stationary point condition

of (27), we terminate Algorithm 2 at the iterate

when or , where

By the Lipschitz continuity of and the semi-convexity

of , it is not difficult to obtain

the following results for the sequence generated by Algorithm 2.

Lemma 5.1

Let be the sequence generated by

Algorithm 2. Then,

which implies that the sequence

is nonincreasing when .

Furthermore, when , the sequence

is lower bounded.

Lemma 5.2

For each , there exists a vector

with

Thus, by the semi-algebraic property of , one may follow

the recipe in [2] to obtain the global convergence

of Algorithm 2. For the convergence analysis of the ADMM

for nonconvex nonsmooth problems, the reader may refer to

the related reference [22, 45].

Next we focus on the solution of the subproblem (16)

involved in Algorithm 1, which is the pivotal part for

the implementation of Algorithm 1. Inspired by the numerical

results reported in [24], we apply a dual semismooth Newton method

for solving it.

For each , write

with . By introducing an additional variable ,

the subproblem (16) can be equivalently written as

(29)

After an elementary calculation, the dual of the problem (5.2) takes the following form

(30)

Clearly, the strong duality result holds for the problems (5.2)

and (30). Since is smooth and convex,

seeking an optimal solution of (30) is equivalent to

finding a root to

(31)

Notice that is strongly semismooth since

and

are strongly semismooth by Section 2.2 and the composition of

strongly semismooth mappings is strongly semismooth by [15, Proposition 7.4.4].

By [12, Proposition 2.3.3 & Theorem 2.6.6], we have

(32)

where, by Lemma 2.1, and take

the following form with :

For each and ,

the matrix

is positive semidefinite, and moreover, it is positive definite when

or the matrix has full row rank with .

Motivated by these facts, we apply the following semismooth Newton method to seeking

a root of the system (31), which by [30] is

expected to have a superlinear even quadratic convergence rate.

Algorithm 3 A semismooth Newton-CG algorithm

Initialization: Fix . Choose ,

and . Set .

while the stopping conditions are not satisfied do

1.

Choose and

and set .

Solve

with the conjugate gradient (CG) algorithm to find an approximate such that

,

where .

2.

Set , where is the first nonnegative integer satisfying

3.

Set and , and then go to Step 1.

end while

Remark 5.2

Fix an arbitrary . Let be a root to the semismooth system (31).

Set

and .

Then and

That is, is a feasible solution to (5.2) and

the gap between its objective value and the dual optimal value is

.

This motivates us to terminate Algorithm 3 at when

or the following conditions are satisfied:

(33)

where

and .

5.3 Numerical comparisons on synthetic and real data

We compare the performance of Algorithm 1 armed with

Algorithm 3 solving the subproblems (PMMSN for short) with

that of iPADMM (i.e., Algorithm 2) via synthetic and real data,

in terms of the computing time, approximate sparsity and relative -error.

Among others,

denotes the approximate sparsity of a vector and

means

the relative -error of the output . All numerical tests

are done with a desktop computer running on 64-bit Windows Operating System

with an Intel(R) Core(TM) i7-7700 CPU 3.6GHz and 16 GB memory.

Unless otherwise stated, the two solvers are using for ,

, and the same yielded by applying Algorithm 3

to (18) with and .

By Remark 4.1(ii), we choose

for and for the case ,

i.e., a little larger for since now is positive definite.

The parameter (or ) and are specified in the test examples.

The other parameters of Algorithm 1 are chosen as ,

and the parameter of Algorithm 2 is chosen as

by its convergence analysis. For Algorithm 1,

besides using the stopping criterion in Remark 4.1 with

and , we also terminate it at when

for and

, and Algorithm 3 is using

the stopping criterion in Remark 5.2 with and

for . For Algorithm 2,

we use the stopping criterion described in Section 5.1 with

and .

Before testing, we take a closer look at the choice of for

Algorithm 2. Figure 1 below shows that as increases,

the sparsity and relative -error of the output

of iPADMM for solving (27)

associated to becomes better and keeps unchanged when

is over a threshold, but the loss value

first increases and then decreases a certain level and keeps it unchanged.

In view of this, we regard the smallest one among those for which

has the sparsity closest to that of the true

for synthetic data (respectively, that of the output of PMMSN for real data)

as the best, by noting that such usually has

a favorable -error and the model (27)

with a smaller is closer to (10).

For the subsequent tests, we search such a best

from an appropriate interval (specified in the examples) by comparing the sparsity

of corresponding to ’s.

To search the best in this way, despite of impracticality,

is just for numerical comparison.

Figure 1: The influence of on sparsity and loss value

for Example 5.2 with

5.3.1 Synthetic data examples

We use some synthetic data to evaluate the performance of PMMSN and iPADMM

for solving the surrogate problem (10). The data is given

by (24) with each

and a nonzero noise vector whose nonzero entries are i.i.d.,

where the covariance matrix and the distribution

of the nonzero entries of are specified in the examples.

1. Influence of the sparsity of on the solvers

The following example involves the noise with

following the normal distribution. We use it to test the performance of

two solvers under different sparsity of .

Figure 2 below plots the relative -error and time curves

of two solvers under different sparsity rate (i.e., ) of

the noise vector , where PMMSN is solving the surrogate problem

(10) with

and iPADMM is solving its smoothed form (27) with

the same and .

We see that as the sparsity rate increases, the relative -error of two solvers

increases, but the -error of PMMSN is always lower than that of iPADMM

and their difference is remarkable after . This is consistent

with the conclusion of Theorem 4.3 by Remark 4.2(ii).

In addition, as increases, the time required by PMMSN has a small

change but the time of iPADMM has a remarkable increase.

This shows that PMMSN has a better performance for this example.

Figure 2: The relative -error and computing time of two solvers

under different

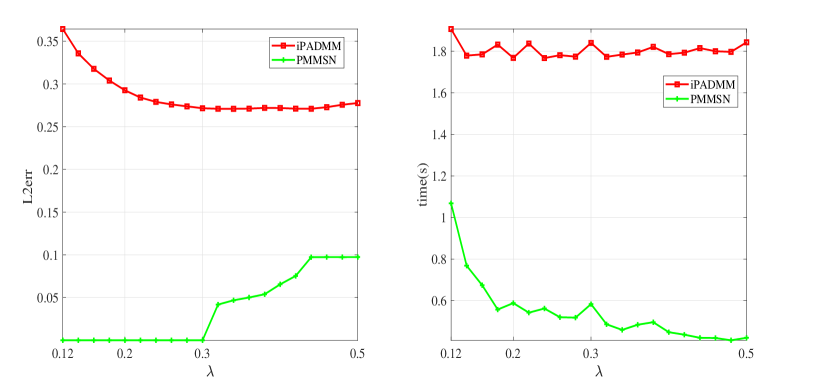

2. Influence of the parameter on the solvers

The following example is also from [18] which involves

a heavy-tailed noise. We employ it to test the performance of

two solvers under different or .

Example 5.2

Be same as Example 5.1 except that

with and all entries of

follow the Cauchy distribution of density .

Figure 3: The relative -error and computing time of two solvers under different

Figure 3 plots the relative -error and computing time curves

of two solvers under different , where iPADMM is solving (27)

with . We see that as the parameter increases,

the relative -error of iPADMM first decreases and then increases slightly,

whereas the relative -error of PMMSN has a remarkable increase after

but is still much lower than that of iPADMM. This means that

if the sparsity of the noise is well controlled, the increase of

in a certain range has a small influence on the error bound of the output of PMMSN.

In addition, as increases, the time of iPADMM has a tiny change,

but the time of PMMSN becomes less and is always less than that of iPADMM.

This shows that PMMSN has a better performance for this class of noise.

3. Performance of two solvers for other sparse noises

We test the performance of two solvers for other types of sparse noises via

six examples, generated randomly with

and . The sparsity of the noise vector

is always set as and the nonzero entries

of follow . The covariance matrix includes

the autoregressive structure denoted by

and the compound symmetric structure

for ,

denoted by . Such covariance matrices are highly relevant

although they are positive definite. The nonzero entries of obey

the following distributions: (1) the normal distribution ;

(2) the scaled Student’s -distribution with degrees of freedom

; (3) the mixture normal distribution

with , denoted by ;

(4) the Laplace distribution with density ;

and (5) the Cauchy distribution with density .

Table 1 reports the average of the loss values,

relative -errors and computing time of total 10 test problems

for each example with a fixed , for which we always take

by

the assumption on in Theorem 4.3.

In Table 1, aiPADMM and bPMMSN,

denotes the approximate zero-norm of ,

Loss means the loss value , means

the average of the square spectral norm of for test problems,

and respectively represents the number of false positives and false zeros

of , and column lists the interval to search the best

. During the testing, we find that when takes ,

the noise of Cauchy distribution will have a norm over , for which the two solvers

both fail to yielding a reasonable solution. In view of this, we choose the 10

test problems generated randomly with for testing.

Table 1: The performance of iPADMM and PMMSN for sparse noise

Problem

Nz

Loss

L2err

FP

FN

Time(s)

|

|

1.08e+4

[15,30]

25

9.90

38.1|35.0

1.501|1.489

2.34e-3|5.68e-7

3.2|0

0.1|0

42.4|45.9

|

1.08e+4

[10,30]

15

12.4

39.6|35.0

0.464|0.448

3.01e-3|2.21e-6

4.7|0

0.1|0

44.5|42.3

|MN

1.08e+4

[10,30]

20

12.07

36.2|35.0

0.734|0.725

1.73e-3 |1.68e-6

1.3|0

0.1|0

46.7|53.5

|Laplace

1.08e+4

[10,30]

15

6.32

35.7|35.0

0.301|0.294

1.18e-3|8.21e-6

0.8|0

0.1|0

43.8|49.8

|Cauchy

1.08e+4

[20,35]

27

322.7

90.5|34.0

2.208|1.477

2.81e-1|9.96e-3

60.3|0

4.8|1

42.1|108.5

|

1.77e+6

[1600,2000]

1800

9.90

34.5|34.8

2.907|1.504

3.59e-1|4.54e-3

11.6|0.1

12.1|0.3

50.6|28.6

|

1.77e+6

[1000,1500]

1225

12.4

39.3|34.9

1.571|0.462

2.44e-1|4.07e-3

12.1|0

7.8|0.1

50.4|19.5

|MN

1.77e+6

[1000,1500]

1350

12.07

39.5|34.6

1.968|0.753

2.84e-1|8.19e-3

13.2|0

8.7|0.4

59.5|24.9

|Laplace

1.77e+6

[1000,1500]

1150

6.32

36.3|35.1

1.341|0.302

2.15e-1|2.24e-3

8.6|0.2

7.3|0.1

60.2|22.5

|Cauchy

1.80e+6

[1200,1800]

1500

322.7

226.7|29.4

3.523|1.828

9.35e-1|9.28e-2

209.3|0.2

17.6|5.8

51.1|93.8

From Table 1, we see that the average sparsity yielded by PMMSN and iPADMM for

all test examples except for |Cauchy and |Cauchy is

close to that of the true vector , but the average relative -error and

yielded by iPADMM are worse than those yielded by PMMSN, especially for

those examples of . For the most difficult |Cauchy,

the average sparsity, relative -error and given by

iPADMM are much worse than those yielded by PMMSN since, the parameter

is very sensitive to the data and the best

is not suitable for all test problems. This shows that replacing with

a smooth approximation is not effective for highly relevant

covariance matrix and heavy-tailed sparse noises, though

is elaborately selected.

5.3.2 Real data examples

This part uses the LIBSVM datasets from https://www.csie.ntu.edu.tw

to test the efficiency of PMMSN for large scale problems. For those data sets

with a few features, such as pyrim, abalone, bodyfat, housing, mpg, space ga,

we follow the same line as in [39] to expand their original features

by using polynomial basis functions over those features. For example,

the last digit in pyrim5 indicates that a polynomial of order

is used to generate the basis function. Such a naming convention is also

applicable to the other expanded data sets. These data sets are quite difficult

in terms of the dimension and the largest eigenvalues of .

Table 2 reports the numerical results of two solvers to

solve the corresponding problems

with .

Table 2: The performance of two solvers for LIBSVM datasets

Name of data

NZ

Loss

Time(s)

E2006.test

3308;150358

4.79e+4

0.3776

[0.1,10]

2.5

1|1

0.2361|0.2361

42|42

log1p.E2006.test

3308;4272226

1.46e+7

0.5395

[1500,2500]

2000

1|1

0.2362|0.2361

7071|3208

abalone7

4177;6435

5.23e+5

0.1

[500,1500]

1250

28|20

1.5140|1.4800

433|165

bodyfat7

252;116280

5.30e+4

0.1

[0.1,1]

0.3

3|3

7.45e-4|4.50e-4

604|466

housing7

506;77520

3.28e+5

0.1

[200,600]

470

137 |139

2.6596|1.0204

791|604

mpg7

392;3432

1.30e+4

0.1

[50,150]

90

pyrim5

74;201376

1.22e+6

0.1

[15,150]

60

space ga9

3107;5005

4.10e+3

0.1

[0.1,10]

5

From Table 2, PMMSN works well in solving large scale

difficult problems. Although the sparsity of its output is very close to

that of the output of iPADMM, the loss value of its output is lower than

that of the output of iPADMM. From the numerical tests for synthetic

example, the loss value is usually consistent with the relative error.

This means that the output yielded by PMMSN has better quality.

In particular, the computing time required by PMMSN is less than

the time required by iPADMM.

From the above numerical comparisons, we conclude that PMMSN has

an advantage in the quality of solutions and computing time, and

it is robust under the scenario where has

a highly-relevant covariance and the noise is heavily-tailed,

while the performance of iPADMM depends much on the smoothing

parameter , and for those tough examples,

the parameter is very sensitive to the data.

In addition, from the numerical results on synthetic examples,

we find that when the sparsity of the noise attains

a certain level, say, for Example 5.1

and for Example 5.2 and the first

fourth examples in Table 1, the relative

-error has an order about which is close to

the exact recovery. Then, it is natural to ask for which kind of

covariance matrix and noises, the exact recovery of the limit

can be achieved by controlling the sparsity of the noise

vector . We leave this interesting question for a future research topic.

6 Conclusions

For the zero-norm regularized PLQ composite problem, we have shown that

its equivalent MPEC is partially calm over the set of global optima and

obtain a family of equivalent DC surrogates by using this important property,

which greatly improves the result of [27, Theorem 3.2] for

this class of problems. We develop a proximal MM method for solving

one of the DC surrogates, and provide its theoretical certificates by

establishing its global and local linear convergence, analyzing when

the limit of the generated sequence is a local minimum, and deriving

the error bound of the limit to the true vector for the data

from a linear observation model. Numerical comparisons with the convergent

iPADMM for synthetic and real data examples verify that the proximal MM method

armed with a dual semismooth Newton method for solving the subproblems

has an advantage in the quality of solutions and the computing time,

and is robust for the case where has a large spectral norm

and is corrupted by the heavily-tailed noise; whereas the convergent

iPADMM for the partially smoothed surrogate is ineffective for those

tough test examples even with an elaborate selection of the smoothing

parameter .

Acknowledgements The authors would like to express their sincere thanks

to Prof. Kim-Chuan Toh from National University of Singapore for helpful suggestions

on the implementation of Algorithm 3 when visiting SCUT in March of 2019,

and give thanks to Prof. Liping Zhu from RenMin University of China for helpful discussion

on the result of Theorem 4.3. The research of Shaohua Pan and

Shujun Bi is supported by the National Natural Science Foundation of China under project

No.11971177 and No.11701186.

References

[1]H. Attouch, J. Bolte, P. Redont and A. Soubeyran,

Proximal alternating minimization and projection methods for nonconvex problems: an approach

based on the Kurdyka-Łojasiewicz inequality,

Mathematics of Operations Research, 35(2010): 438-457.

[2]H. Attouch, J. Bolte and B. F. Svaiter,

Convergence of descent methods for semi-algebraic and tame problems:

proximal algorithms, forward-backward splitting, and reguarlized Gauss-Seidel methods,

Mathematical Programming, 137(2013): 91-129.

[3]A. Belloni and V. Chernozhukov,

Square-root lasso: pivotal recovery of sparse signals via conic programming,

Biometrika, 4(2010): 791-806.

[4]W. Bian and X. J. Chen,

A smoothing proximal gradient algorithm for nonsmooth convex regression with

cardinality penalty, to appear in SIAM Journal on Numerical Analysis.

[5]P. S. Bradley and O. L. Mangasarian,

Feature selection via concave minimization and support vector machines,

In Proceeding of international conference on machine learning ICML, 1998.

[6]A. M. Bruckstein, D. L. Donoho and M. Elad,

From sparse solutions of systems of equations to sparse modeling of signals and images,

SIAM Review, 51(2009): 34-81.

[7]J. V. Burke,

Calmness and exact penalization,

SIAM Journal on Control and Optimization, 29(1991): 493-497.

[8]S. S. Cao, X. M. Huo and J. S. Pang,

A unifying framework of high-dimensional sparse estimation with difference-of-convex (DC) regularizations,

arXiv:1812.07130, 2018.

[9]R. Chartrand,

Exact reconstruction of sparse signals via nonconvex minimization,

IEEE Signal Processing Letters, 14(2007): 707-710.

[10]X. J. Chen, F. M. Xu and Y. Y. Ye,

Lower bound theory of nonzero entries in solutions of - minimization,

SIAM Journal on Scientific Computing, 32(2010): 2832-2852.

[11]F. H. Clarke,

A new approach to Lagrange multipliers,

Mathematics of Operations Research, 1(1976): 165-174.

[12]F. H. Clarke,

Optimization and Nonsmooth Analysis, New York, 1983.

[13]D. L. Donoho and B. F. Stark,

Uncertainty principles and signal recovery,

SIAM Journal on Applied Mathematics, 49(1989): 906-931.

[14]D. L. Donoho,

Compressed sensing,

IEEE Transactions on Information Theory, 52(2006): 1289-1306.

[15]F. Facchinei and J. S. Pang,

Finite-dimensional Variational Inequalities and Complementarity Problems.

Springer, New York, 2003.

[16]J. Q. Fan and R. Z. Li,

Variable selection via nonconcave penalized likelihood and its oracle properties,

Journal of American Statistics Association, 96(2001): 1348-1360.

[17]J. Q. Fan, L. Z. Xue and H. Zou,

Strong oracle optimality of folded concave penalized estimation,

The Annals of Statistics, 42(2014): 819-849.

[18]Y. W. Gu, J. Fan, L. C. Kong, S. Q. Ma and H. Zou,

ADMM for high-dimensional sparse penalized quantile regression,

Technometrics, 60(2018): 319-331.

[19]Y. Hai Le,

Generalized subdifferentials of the rank function,

Optimization Letters, 7(2013): 731-743.

[20]H. A. Le Thi, H. M. Le and T. Pham Dinh,

Feature selection in machine learning: an exact penalty approach using

a difference of convex function algorithm,

Machine Learning, 101(2015): 163-186.

[21]H. A. Le Thi and D. T. Pham,

Recent advances in DC programming and DCA. Nguyen N-T, Le Thi HA, eds.

Trans. Comput. Collective Intelligence, Lecture Notes in Computer Science,

Vol. 8342 (Springer, Berlin), 1-37.

[22]G. Y. Li and T. K. Pong,

Global convergence of splitting methods for nonconvex composite optimization,

SIAM Journal on Optimization, 25(2015): 2434-2460.

[23]G. Y. Li and T. K. Pong,

Calculus of the exponent of Kurdyka-Łojasiewicz inequality and its applications

to linear convergence of first-order methods,

Foundations of Computational Mathematics, 18(2018): 1199-1232.

[24]X. D. Li, D. F. Sun, and K. C. Toh,

A highly efficient semismooth Newton augmented Lagrangian method for solving Lasso problems,

SIAM Journal on Optimization, 28(2016): 433-458.

[25]P. L. Loh and M. J. Wainwright,

Regularized M-estimators with nonconvexity: statistical and algorithmic theory for local optima,

Journal of Machine Learning Research, 16(2015): 559-616.

[26]

Q. Liu, C. Z. Yang, Y. T. Gu and H. C. So,

Robust sparse recovery via weakly convex optimization in impulsive noise,

Signal Processing, 152(2018): 84-89.

[27]

Y. L. Liu, S. J. Bi and S. H. Pan,

Equivalent Lipschitz surrogates for zero-norm and rank optimization problems,

Journal of Global Optimization, 72(2018): 679-704.

[28]O. L. Mangasarian,

Machine learning via polyhedral concave minimization,

In H. Fischer, B. Riedmueller & S. Schaeffler (Eds.),

Applied mathematics and parallel computing-Festschrift for Klaus Ritter

(pp. 175-188), 1996.

[29]R. Mifflin,

Semismooth and semiconvex functions in constrained optimization,

SIAM Journal on Control and Optimization, 15(1977): 959-972.

[30]L. Q. Qi and J. Sun,

A nonsmooth version of Newton’s method,

Mathematical Programming, 58(1993): 353-367.

[31]G. Raskutti and M. J. Wainwright,

Restricted eigenvalue properties for correlated Gaussian designs,

Journal of Machine Learning Research, 11(2010): 2241-2259.

[32]F. Rinaldi, F. Schoen and M. Sciandrone,

Concave programming for minimizing the zero-norm over polyhedral sets,

Computation Optimization and Applications, 46(2010): 467-486.

[33]R. T. Rockafellar,

Convex Analysis, Princeton University Press, 1970.

[34]S. M. Robinson,

Some continuity properties of polyhedral multifunctions,

Mathematical Programming Study, 14(1981): 206-214.

[35]R. T. Rockafellar and R. J-B. Wets,

Variational Analysis, Springer, 1998.

[36]E. Soubies, L. Blang-Fraud and G. Aubert,

A continuous exact penalty (CEL0) for least squares regularized problem,

SIAM Journal on Imaging Science, 8(2015): 2034-2060.

[37]E. Soubies, L. Blang-Fraud and G. Aubert,

A unified view of exact continuous penalities for - minimization,

SIAM Journal on Optimization, 8(2017): 1067-1639.

[38]D. F. Sun and J. Sun,

Semismooth matrix-valued functions,

Mathematics of Operations Research, 27(2002): 150-169.

[39]P. P. Tang, C. J. Wang, D. F. Sun and K. C. Toh,

A sparse semismooth Newton based proximal majorization-minimization algorithm

for nonconvex square-root-loss regression problems, arXiv:1903.11460v2.

[40]R. Tibshirani,

Regression shrinkage and selection via the Lasso,

Journal of the Royal Statistical Society, Series B, 58(1996): 267-288.

[41]R. Vershynin,

Introduction to the non-asymptotic analysis of random matrices,

Compressed sensing, 210-268, Cambridge Univ. Press, Cambridge, 2012.

[42]L. WANG,

The penalized LAD estimator for high dimensional linear regression,

Journal of Multivariate Analysis, 120(2013): 135-151.

[43]L. WANG, Y. C. Wu and R. Z. Li,

Quantile regression for analyzing heterogeneity in ultra high dimension,

Journal of the American Statistical Association, 107(2012): 214-222.

[44]H. S. Wang, G. D. Li and G. H. Jiang,

Robust regression shrinkage and consistent variable selection through the LAD-Lasso,

Journal of Business & Economic Statistics, 25(2007): 347-355.

[45]Y. Wang, W. T. Yin and J. S. Zeng,

Global convergence of ADMM in nonconvex nonsmooth optimization,

Journal of Scientific Computing, 78(2019): 29-63.

[46]J. Weston, A. Elisseef, B. Schölkopf and M. Tipping,

Use of the zero norm with linear models and kernel methods,

Journal of Machine Learning Research, 3(2003): 1439-1461.

[47]J. Wright and Y. Ma,

Dense error correction via -mininization,

IEEE Transactions on Information Theory, 56(2010): 3540-3560.

[48]Y. C. Wu and Y. F. Liu,

Variable selection in quantile regression,

Statistica Sinica, 19(2009): 801-817.

[49]J. J. Ye and D. L. Zhu,

Optimality conditions for bilevel programming problems,

Optimization, 33(1995): 9-27.

[50]J. J. Ye, D. L. Zhu and Q. J. Zhu,

Exact penalization and necessary optimality conditions for generalized bilevel programming problems,

SIAM Journal on Optimization, 7(1997): 481-507.

[51]C. H. Zhang,

Nearly unbiased variable selection under minimax concave penalty,

Annals of Statistics, 38(2010): 894-942.

Proof:

By the expressions of and in equation (13a)-(13b),

it suffices to argue that

for each . By the expression of , for any ,

(34)

On the other hand, by the expression of in (12),

it is easy to check that

By comparing with ,

the stated equality holds.

Proof of Proposition 3.2(i) The lower boundedness and coerciveness of

follows by the expressions of and the lower boundedness on .

By equation (34), a simple calculation shows is

Lipschitz continuous in of modulus .

Notice that . Then,

is globally Lipschitz on with the same Lip-constant.

By invoking the descent lemma, this means that is semiconvex

of modulus

and so is the function .

(ii) Since is semiconvex,

the first two equalities follow by Remark 2.1(iii).

By using the smoothness of and [35, Exercise 8.9],

it follows that

In addition, since ,

from [33, Theorem 23.8] it follows that

The result directly follows from the last two equations.

(iii) Since is a critical point of

, from part (ii) and Lemma 1 it follows that

where is the mapping defined

in equation (13b), and the equality is using the fact that

if and if . Notice that

for each . Since by the given assumption,

we have for all . Combining this with the last equation

and the subdifferential characterization of in [19], we conclude that

The right hand side of the last inclusion is exactly the regular subdifferential

of the objective function of (1).

Thus, is a regular critical point of (1).

(iv) Since the set is polyhedral and the function

is continuous and piecewise linear-quadratic, it follows that

is a piecewise

linear-quadratic function with .

By [35, Definition 10.20], there exist symmetric matrices

, vectors and

scalars such that

where each is a polyhedral set. Notice that

is continuous on the set by the convexity of and

. This means that

is continuous on

the set . In addition, by Proposition 3.2(ii),

we know that .

The two sides show that is continuous on

.

Now by invoking [23, Corollary 5.2] and the last equation,

we obtain the desired result. The proof is then completed.

Appendix B

Lemma 2

Let be a convex function

with . For any given ,

Proof:

By [35, Theorem 10.49], we have

where

denotes the coderivative of the function at .

From [35, Proposition 9.24(b)], it follows that

which implies the desired result.

In order to complete the proof of Theorem 4.3,

we introduce the following notation

(35a)

(35b)

With these notation, we can establish the following important technical lemma.

Lemma 3

Suppose for some there exists with

Then, when ,

it holds that .

Proof:

Since is a feasible solution and is an optimal one to (16), respectively,

from the strong convexity of the objective function of (16),

it follows that

which by

is equivalent to saying that

(36)

where the equality is due to the definition of .

By using and equation (25),

(37)

Recall and the definition of the index set .

For each , define . Then,

together with the expression of and (37), we have

(38)

Fix an arbitrary .

Since is strongly convex of modulus , it holds that

Suppose that the matrix satisfies the RE condition of parameter

over and for some there exists an index set

with such that and .

If the parameter is chosen such that , then

where the last inequality is due to

.

By Lemma 3, we know that

,

which by the given assumption means that .

From the given assumption on , we have

. Then,

Multiplying the both sides of this inequality by

yields that

Note that .

Along with ,

we have .

So, the right hand side of the last inequality satisfies

From the last two equations, a suitable rearrangement yields that

which by

implies the desired result.

Proof of Theorem 4.3:

Since as and

and , by the definition of in (35b),

we have . So, there exists such that

for all .

Since , there is

such that for all ,

This, by the assumption on , implies that

for , and from (17)

we have for each when .

Set and for each

define .

If for ,

from Lemma 4 we have

(43)

where the third inequality is due to the restriction on ,

and the last one is since

and . Taking the limit

to the both sides of (A proximal MM method for the zero-norm regularized PLQ composite optimization problem), we obtain the desired result.

So, it suffices to argue that for all .

When , this statement holds by the above discussions.

Assuming that holds for with ,

we prove that it holds for . Indeed,

since ,

we have for . Together with

the formula (17), we deduce that , and hence

the following inequality holds:

Since the statement holds for , it holds that

.

Thus,

(44)

where the last inequality is due to .

The inequality (44) implies that .

This shows that the stated inequality holds.

Appendix C

Proof of Proposition 4.1:

Write . From the given condition,

the strong convexity of and the fact that ,

it follows that

(45)

From and Assumption 1,

it is not difficult to obtain that

A simple calculation, together with , immediately yields that