Multiply robust matching estimators of average and quantile

treatment effects

Shu Yang and Yunshu Zhang

Department of Statistics, North Carolina State University, North Carolina

27695, U.S.A. Email: syang24@ncsu.eduDepartment of Statistics, North Carolina State University, North Carolina

27695, U.S.A. Email: yzhan234@ncsu.edu

Abstract

Propensity score matching has been a long-standing

tradition for handling confounding in causal inference, however requiring

stringent model assumptions. In this article, we propose double score

matching (DSM) for general causal estimands utilizing two balancing

scores including the propensity score and prognostic score. To gain

the protection of possible model misspecification, we posit multiple

candidate models for each score. We show that the de-biasing DSM estimator

achieves the multiple robustness property in that it is consistent

for the true causal estimand if any model of the propensity score

or prognostic score is correct.

Keywords: Bahadur representation; Causal effect on the treated;

Double robustness; Quantile estimation; Weighted bootstrap.

1 Introduction

Causal inference plays an important role in science, education, medicine,

policy, and economics. If all confounders of the treatment-outcome

relationship are observed, one can use standard techniques, such as

regression adjustment, inverse probability of treatment weighting

(IPW), augmented IPW (AIPW), and matching to adjust for confounding

(Imbens and Rubin, 2015). Among them, the AIPW estimator is most

popular because it achieves the so-called double robustness

property by combining the use of models for the probability of treatment

assignment, also known as the propensity score (Rosenbaum and Rubin, 1983b),

and the outcome mean function. More specifically, it consistently

estimates the treatment effect if either one of these functions is

modeled correctly (e.g., Lunceford and Davidian, 2004; Bang and Robins, 2005).

However, inevitably, weighting estimators can have a high variability

by inverting the estimated propensity scores (e.g., Kang and Schafer, 2007; Guo and Fraser, 2014),

especially if these probabilities are close to zero or one. Matching

has multiple features that are more desirable than weighting:

a)

matching does not involve weighting by the inverse of the propensity

score and therefore avoids the possibly large variability due to weighting

(Frölich, 2004);

b)

matching is transparent and intuitively appealing with the goal of

replicating the ideal randomized experiment (Rosenbaum, 1989; Heckman et al., 1997a; Dehejia and Wahba, 2002, 1999; Rubin, 2006; Stuart, 2010);

c)

matching can be viewed as a hot deck imputation method which can provide

valid estimators of general parameters depending on the entire distribution,

such as quantiles (Ford, 1983).

Although matching has a substantial promise, its

applications are still less popular compared to weighting, partly

due to the issue of the curse of dimensionality. In the presence of

many covariates, matching directly on high-dimensional covariates

is incapable of removing all confounding biases. To overcome this

challenge, researchers have proposed different dimension reduction

techniques to facilitate matching. On the one hand, Rosenbaum and Rubin (1983b)

demonstrated the central role of the propensity score as being a balancing

score in the sense that same propensity score distributions in different

treatment groups lead to same covariate distributions. Therefore,

matching solely on the propensity score (PSM) can remove all confounding

biases (e.g., Abadie and Imbens, 2016). On the other hand, Hansen (2008)

proposed an alternative balancing score: the prognostic score, also

called the disease risk score (i.e., a sufficient statistic for the

potential outcomes given which the potential outcomes and covariates

are independent). This score provides a balance of disease risks between

the treatment groups, as distinct from the balance of treatment propensities

provided by the propensity score. In economics, matching based on

prognostic score (PGM) has been previously proposed in Imbens (2004)

and Zhao (2004), where the prognostic score is a vector

of linear predictors in treatment-specific outcome regressions. PGM

is also similar to predictive mean matching (Rubin, 1986; Yang and Kim, 2019)

in the missing data literature to compensate for nonresponse. In the

comparative effectiveness research, PGM has been shown to be more

advantageous than PSM when the propensity score distributions are

strongly separated (Wyss et al., 2015; Kumamaru et al., 2016).

Smith and Schaubel (2015) extended PGM to a time-dependent treatment

setting. While PGM is gaining its popularity, it relies on a correctly

specification of the prognostic score (Wyss et al., 2015, 2017).

As analogous to AIPW, it is advantageous to combine the use of the

propensity and prognostic score in matching (Hansen, 2008).

Leacy and Stuart (2014) showed empirically that the joint use of two

scores in matching (which we refer to as double score matching, DSM)

improves the treatment effect estimation. Antonelli et al. (2018)

later established the double robustness of matching jointly on propensity

and prognostic scores in the sense that the matching estimator is

consistent for the average treatment effect (ATE) if either one of

the score models is correctly specified.

In this article, we propose new DSM estimators based on the propensity

score and the prognostic score. Because each score creates a balance

between the treated and control groups, the augmented score serves

as a “double balancing score” as shown by Antonelli et al. (2018).

To estimate the ATEs, existing DSM would require adjusting for the

vector of the propensity score and possibly multiple treatment-specific

prognostic scores (i.e., one for each treatment group). Instead of

estimating the ATEs directly, we focus on estimating the average of

the potential outcomes separately for each treatment level, which

requires adjusting only for the propensity score and the prognostic

score for that particular level of the treatment. This insight allows

us to reduce the dimension of the double score further without giving

up the double balancing property. This strategy also plays an important

role for the dimension reduction for constructing improved DSM estimators.

In practice, the double score is unknown and therefore requires modeling

and estimation. Similar to Antonelli et al. (2018), the new DSM

estimator is doubly robust, which includes one propensity score model

and one prognostic score model. With an unknown data generating process,

there is no guarantee that either of the two models is correctly specified.

To gain additional protection against model misspecification, we posit

multiple models for the propensity score and prognostic score. Doing

so, however, may introduce bias due to matching discrepancy based

on a moderately high-dimensional matching variable (Abadie and Imbens, 2011),

although our strategy of estimating the average of potential outcomes

separately helps dimension reduction. In this case, we propose the

de-biasing DSM estimator that corrects for the bias due to matching

discrepancy. We show that the DSM estimator has the multiple

robustness property, which guarantees the estimation consistency

if any one of the candidate models for the propensity score or prognostic

score is correctly specified. This result is similar in essence to

the multiply robust weighting estimators in the missing data and survey

literature (Han and Wang, 2013; Han, 2014; Chen and Haziza, 2017b, a)).

Because the double scores are estimated prior to matching, it is necessary

to account for the uncertainty due to parameter estimation. The theoretical

task is non-trivial. The typical Taylor expansion technique can not

be used, because of the non-smooth nature of matching. Our derivation

is based on the technique developed by Andreou and Werker (2012),

which offers a general approach for deriving the limiting distribution

of statistics that involve estimated nuisance parameters. This

technique has been successfully used in Abadie and Imbens (2016)

for the matching estimators based on the estimated propensity score.

We extend their results to the DSM estimators requiring any one of

the models to be correctly specified.

The current matching literature has focused primarily on estimating

the ATEs; however, other aspects of the distribution such as quantiles

may be more appropriate in certain applications. For example, a treatment

strategy may not decrease average health cost but instead lowers the

upper tail of the cost distribution, so focusing only on ATEs would

not reveal the beneficial effect of the treatment strategy. In these

cases, it is more informative to study quantile treatment effects

(QTEs), which are defined as the differences in population quantiles

of the potential outcome distributions. Taking the advantage of matching

as a hot deck imputation method, we extend the multiply robust DSM

framework to estimate QTEs.

The rest of this paper proceeds as follows. Section 2

introduces notation, assumptions, and lemmas for various balancing

scores. Section 3 provides the new

perspective of using the double score as a dimension reduction tool

and proposes the new DSM estimator of the ATE with multiple candidate

models for the double score. Section 4 establishes

the multiple robustness of the DMS estimator and its limiting distribution,

which allows quantifying the impact of the nuisance parameter estimation.

Section 5 extends the DSM framework to the estimation

of the QTE. Section 6 uses simulation to

evaluate the finite-sample properties of the DMS estimators. The simulation

results demonstrate that matching estimators outperform weighting

estimators. Section 7 applies the DMS

estimators to an observational study from the job training program.

Section 8 concludes, the supplementary material

contains the proofs and extensions to the average treatment effect

on the treated (ATT) and quantile treatment effect on the treated

(QTT), and an R package dsmatch is available at https://github.com/Yunshu7/dsmatch.

2 Notation, assumptions, and balancing scores

Let be a vector of pre-treatment covariates, the

binary treatment, and the outcome for unit .

We follow the potential outcomes framework. Let be the

potential outcome had unit been given treatment ().

The observed outcome is .

We assume that , ,

are independent and identically distributed. Thus, ,

, are also independent and identically distributed.

Various causal estimands are useful to provide a comprehensive assessment

of treatment effects. The ATE is . For

the overall -QTE is , where

, . When the

outcome data follow a skewed distribution, QTEs may be more informative

measures of treatment effect. Similarly, the ATT is ,

and the QTT is ,

where ,

. We focus on estimating and in the

main text and provide extensions to the ATT and QTT in the supplementary

material.

For simplicity of exposition, for a generic variable , denote

where is an outcome mean function,

is a variance function, and is the propensity score.

We focus on the setting where the standard positivity and treatment

ignorability assumptions hold (Rosenbaum and Rubin, 1983b).

Assumption 1

There exist constants

and such that almost surely.

Assumption 1 implies a sufficient overlap of the

covariate distribution between the treatment groups. If this assumption

is violated, a common approach is to trim the sample; see Yang and Ding (2018).

Assumption 2

,

where means “independent of”.

Assumption 2 has no testable implications. Generally,

it can be made more plausible by collecting detailed information on

characteristics of the units that are related to treatment assignment

and outcome. As a result, the dimension of may be high.

Then we can estimate through PGM and subclassification to

remove the confounding biases.

Combining the propensity score and the prognostic score, Antonelli et al. (2018)

showed that the double score is also a balancing score in the sense

that treatment ignorability maintains by conditioning on the double

score.

Lemma 3 (Double score as a balancing score; Antonelli et al, 2018)

Then we can estimate through DSM or subclassification based

on the double score.

DSM is an attractive alternative to PSM; however, the dimension reduction

property of Lemma 3 depends on the dimension of the prognostic

score. In Example 1, the dimension of the prognostic score

is two; thus, the dimension of the double score is three. Antonelli et al. (2018)

made an additional assumption that there does not exist treatment

effect modification, under which the prognostic score is a scalar.

Nonetheless, such additional assumptions may be controversial. The

problem is that if the dimension of the matching variable is higher,

the bias order of the matching estimator becomes larger, see Section

3.1, suggesting that the advantages

of PSM do not carry over to DSM. To preserve the simplicity of matching

(avoiding de-biasing), we show that further improvement of the dimension

reduction property of the double score is possible without additional

assumptions. Then, the advantage of PSM carries over to DSM, see Section

3.2. Moreover, because the double score

is unknown in practice, one must posit models and estimate the double

score from the observed data. To gain robustness to model misspecification,

we posit multiple candidate models for the double score. We propose

a multiply robust DSM procedure and show that the de-biasing matching

estimator achieves multiple robustness, see Section 3.3.

3 DSM estimators of the ATE

3.1 General matching estimators

To fix ideas, we consider matching with replacement with the number

of matches fixed at . Matching estimators hinge on imputing the

missing potential outcome for each unit. In practice, the most common

choice of is , then the matching procedure becomes nearest

neighbor imputation (Little and Rubin, 2002; Chen and Shao, 2000, 2001).

To be precise, for unit , the potential outcome under

is the observed outcome the (counterfactual) potential outcome

under is not observed but can be imputed by the observed

outcomes of the nearest units with .

To illustrate the properties of the matching estimator, we first consider

a generic variable as the matching variable. Table 1

summarizes the choices of . To stabilize the numerical performance,

it is desirable to standardize such that each component has mean

zero and variance one. Without loss of generality, we use the Euclidean

distance to determine neighbors; the discussion applies to other distances

(Abadie and Imbens, 2006). We denote

as the index set for these matched units for unit and

as the number of times that unit is used as a match, where the

subscript “” in and indicates the name

of the matching variable. Table 1 (I) illustrates

the above matching scheme to impute the missing potential outcomes.

For unit with , the imputed potential outcomes are

and .

For unit with ,

and . Once we approximate both potential

outcomes for all units, a simple matching estimator of is

To establish the asymptotic properties of , Abadie and Imbens (2006)

derived the following decomposition

where

(4)

By Assumptions 1 and 2, for

to be , propensity score, prognostic score or double score,

we have , and therefore .

The difference in (4)

accounts for the matching discrepancy, so contributes to

the asymptotic bias of the matching estimator. In general, if the

matching variable is -dimensional, we have

(Abadie and Imbens, 2006, Theorem 1). Table 2

demonstrates the relationship of the bias order and . If ,

the bias is non-negligible. If , the bias shrinks to zero

as increases but the convergence rate is slow. If

and , the bias shrinks to zero at much faster rates and

, respectively. Therefore, in finite samples, matching based

on a -dimensional double score is likely to

have a noticeable bias. Reducing to or is worthwhile

to make the bias achieve faster rates of converging to zero.

Table 1: Two matching schemes for imputing potential

outcomes. denotes the index set for

the matched units for unit , where the subscript “” represents

the name of the matching variable. In (I), the matching variable

is the same for imputing the missing values of and .

In (II), the matching variables and are different

for imputing the missing values of and

(I) Matching imputation

(II) New matching imputation

Unit

Unit

(I) Matching Variable

(II) Matching Variable

M.X

PSM

PGM

DSM

DSM

Table 2: The order of bias of the matching variable

in terms of the dimension of the matching variable

For its interpretation, it is useful to compare it to the result (3)

by Lemma 3. By Lemma 3, we create subpopulations

where we can simultaneously compare the treated units and the control

units, leading to (3). These subpopulations were defined

by common values for . By Lemma 4,

we do not construct such populations. The key insight is that in order

to estimate it is not necessary to do so. Instead, we construct

subpopulations where we can estimate the average value of the potential

outcomes for and separately. For a given , these subpopulations

are defined by the value of , leading to (5).

This difference allows us to reduce the dimension of the double score

from three to two, a small reduction of the dimension of the matching

variable, a big reduction of the bias order of the matching estimator.

We focus on estimating separately for .

Let the matching variable be the double score

or for shorthand. Table 1 (II)

illustrates the new matching scheme to impute the missing potential

outcomes. For unit with , and

. For unit

with ,

and . Importantly, the new matching scheme

uses different matching variables, namely and , to

impute the missing values of and . This is in contrast

to matching scheme (I) that uses the same matching variable for imputing

the missing values of and . Once we approximate both

potential outcomes for all units, a simple DSM estimator of

is

(6)

where

for . Following Abadie and Imbens (2006), we can derive the

following decomposition

where

(7)

and , for . By Lemma

4, we have for . Again,

contributes to the asymptotic bias of the matching estimator. By Theorem

1 of Abadie and Imbens (2006), . Therefore,

is asymptotically unbiased.

3.3 Multiply robust DSM

In practice, and are unknown, requiring modeling

and estimation from the observed data. Following the empirical literature,

one can posit a logistic regression model for the propensity score

and a generalized linear model for the prognostic score. To provide

additional protection against model misspecification, we can posit

multiple candidate models for both scores. The intuition is that if

at least one of the candidate models is correctly specified, whether

it is a propensity score model or a prognostic score model, balancing

at lease one score suffices to remove confounding biases. Therefore,

the DSM estimator achieves the so-called multiple robustness.

Following Han and Wang (2013), we postulate multiple candidate

models

•

for

with unknown parameters ;

•

and

for and respectively, with unknown

parameters

and .

Let , and

be the maximum likelihood estimators or the method of moments estimators

of , and under the

corresponding working model, respectively.

For each treatment level , let ,

where , be the the

set of candidate models for the propensity score and the prognostic

score for treatment , for . Under matching scheme (II),

we use to impute the missing values of

, separately for . The corresponding dimension of the

matching variable is . Let ,

where ,

be the set of candidate models for the propensity score and the prognostic

score for both treatment groups. Under matching scheme (I), one would

use as the matching variable; the corresponding

dimension is thus . If the number of candidate models for the

prognostic score is large, the dimension reduction of the double score

under new matching scheme (II) can be much larger than under matching

scheme (I).

The initial DSM estimator of is given by

in (6) with replaced by

for . We denote the initial estimator as

to reflect its dependence on . As discussed in Section

3.2, if , the dimension of

is two for . In this case, the asymptotic bias of the matching

estimator due to matching discrepancy is negligible. We do not require

further steps to correct the asymptotic bias of .

This preserves the simplicity of matching in practice. However, if

, the dimension of each matching variable is larger than

or equal to four. Consequently, as shown in Table 2,

the bias of the matching estimator due to matching discrepancy is

not asymptotic negligible. In this case, we propose

the de-biasing matching estimator that corrects the asymptotic bias

due to matching discrepancy.

Let be a nonparametric estimator of ,

for , e.g., using the method of sieves (Chen, 2007).

The de-biasing DSM estimator of is

(8)

where is an estimator of by replacing

with for .

Before delving into the discussion of the theoretical properties of

, we summarize the DSM algorithm

that contains nuts and bolts as follows.

Step

Posit multiple candidate parametric models ,

, and for

, , and , respectively. Obtain

the parameter estimators , and

. For each unit , calculate

for . The propensity scores are probability estimates, ranging

from zero to one. To stabilize the numerical performance, it is desirable

to use a monotone mapping to transform each propensity score estimate

in ,

e.g., to .

We also recommend standardize such that

each component has mean zero and variance one for .

Step

For each unit with treatment , find

nearest neighbors from the treatment group based on the

matching variable . Obtain

that contains the indexes of the matched

units for unit and calculate that

counts the number of time that unit is matched to other units.

Obtain the initial matching estimator

in (6) with replaced by .

If , let the DSM estimator be .

If , we proceed to Steps 3 and 4 below. Even with ,

Steps 3 and 4 can help to reduce the matching discrepancy in finite

samples.

Step

Obtain a nonparametric estimator of ,

denoted by , e.g. by the method of sieves based

on , for .

Step

The DSM estimator of is given by

in (8) with replaced by .

4 Main results

In this section, we establish the asymptotic properties of ,

which depends on the estimators of all nuisance parameters in the

propensity score and prognostic score models. Without loss of generality,

we consider the prognostic score

in Example 2 and multiple candidate models

for

and . Consider ,

and that solve the estimating equation

(9)

where

for and . Then, solves

the joint estimating equation

where stacks for

, and

for .

Let be the probability limit of We

divide our theoretical investigation into two steps: first, we establish

the asymptotic results for the DSM estimator when is

known, and second, building on the step-one results, we quantify the

impact of the estimation of on the asymptotic distribution.

4.1 Asymptotic results with known

We allow possible model misspecification, so may not

be the true parameter values. If is a correctly

specified model, we have ; if

is a correctly specified model, we have ,

for . The key insight is that if any model of the propensity

score or prognostic score is correctly specified,

remains as a balancing score in the sense that

holds for (Lemma 4). Based on this key observation,

we will show that the DSM estimator is multiply robust.

Before presenting the asymptotic properties of ,

we require technical conditions. For simplicity, let

and let and be the conditional density

of given and , respectively.

Assumption 3

For , (i) the matching

variable has a compact and convex support ,

with a continuous density bounded and bounded away from zero: there

exist constants and such that

for any ; (ii) and

satisfy Lipschitz continuity conditions: there exists a constant

such that

for any and , and similarly for ;

and (iii) there exists such that

is uniformly bounded for any

Assumption 3 has been considered by Abadie and Imbens (2006)

and Abadie and Imbens (2016) for matching estimators based on the

covariates and the propensity score. Assumption 3 (i)

a convenient regularity condition. Assumption 3

(ii) imposes smoothness conditions for the outcome mean function

and the variance function . Assumption 3

(iii) is a moment condition for establishing the central limit theorem.

In the following theorem, we establish the multiple robustness and

asymptotic distribution of .

Theorem 1

Under Assumptions 1–3,

if any model of the propensity score or prognostic score is correctly

specified, we have

in distribution, as , where

(10)

It is worth comparing the three matching methods namely PSM, PGM

and DSM based on the variance formula in (10). To simplify

the discussion, we consider one propensity score model and one prognostic

score model. We show in the supplementary material that if

the prognostic score model is correctly specified, the DSM estimator

may be less efficient than the PGM estimator of . If

the propensity score model is correctly specified, the DSM estimator

is more efficient than the PSM estimator of for ;

however, this improvement is not guaranteed for estimating .

Importantly, DSM has the advantage of double robustness compared

to single score matching: the DSM estimator of is consistent

if either model of the propensity score or prognostic score is correctly

specified, but not necessarily both. Moreover, the consistency is

agnostic to which model is correctly specified. The multiple model

specification offers additional protection against model misspecification.

From Theorem 1, the consistency of the DSM estimator is

guaranteed if any model for the propensity score or prognostic score

is correctly specified. Both the number of the posited models and

their functional forms can affect the efficiency of the DSM estimator

in a very complex way. In addition, with a finite sample size, the

matching performance can be unstable if there are a large number of

working models. In particular, the discrepancy of the matched units

may be large when some of the models are poorly constructed. To reduce

the chance of running into these issues, we suggest positing a few

well-constructed working models instead of a large number of poorly

built ones.

4.2 Asymptotic results with estimated

To acknowledge the fact that is estimated prior to matching,we will establish the approximate distribution of

and examine the impact of nuisance parameter estimation on the properties

of the DSM estimator. As in Abadie and Imbens (2016),

the typical Taylor expansion technique can not be used because of

the non-smooth nature of matching. Our derivation is based on the

technique developed by Andreou and Werker (2012), which offers

a general approach for deriving the limiting distribution of statistics

that involve estimated nuisance parameters. This

technique has been successfully used by Abadie and Imbens (2016)

for the PSM estimators of the ATE and ATT based on a correctly specified

propensity score model. We extend their results to the DSM estimator

requiring only one of the double score models to be correctly specified.

The main theorem of Abadie and Imbens (2016)

is the application of Le Cam’s third lemma (see Section S3)

to Locally Asymptotically Normal (LAN) models. Let

be the true probability measure of copies of the random variables,

contiguous to , and

the probability measure with the local parameter . Assuming

that under ,

has a limiting Normal distribution. By Le Cam’s third

lemma, under ,

has a limiting Normal distribution. Heuristically, by replacing

with , one can then approximate the asymptotic distribution

of .

Under a correctly specified propensity score model,

is naturally the probability measure governed

by the likelihood function of . In our setting, we posit

multiple working models for the propensity score and prognostic score

and require only one model to be correctly specified. In this case,

it is difficult to characterize . Our key

step is to recognize that is defined based on ,

which entails a semiparametric model with mean restrictions. To invoke

the Le Cam’s lemma, we consider a semiparametric

model for based on the asymptotic distribution of the

estimating function . We then carry over the

inferential framework of to our context.

Theorem 2

Under Assumptions 1–3,

and regularity conditions specified in the supplementary material,

if any model of the propensity score or prognostic score is correctly

specified, the approximate distribution of

is where

(11)

where is given in (10),

, ,

,

and are given in (S16) and

(S12), respectively.

We discuss the impact of estimating the nuisance parameters on the

matching estimators. Abadie and Imbens (2016)

showed that for , matching on the estimated propensity score

always improves the estimation efficiency compared to matching on

the true propensity score. This improvement is due to the correlation

of the matching estimator and the score function for the parameters

in the propensity score. In our context, comparing the asymptotic

variances in Theorems 1 and 2, the difference

between and , ,

can be either positive, negative, or zero; i.e.,

matching on the estimated double score can either increase, decrease,

or maintain the estimation efficiency compared to matching on the

true double score. To explain the difference, we note that the variance

reduction term is still

due to the correlation of the matching estimator and the score function

for the parameters in the double score, while the variance inflation

term is because if

either the prognostic score model or the propensity score model is

misspecified, may depend on the nuisance parameters through

which contributes to the variance inflation term. On the other hand,

Abadie and Imbens (2016) focused on the setting

when the propensity score model is the only nuisance model and is

correctly specified. In this case, does not depend on ,

is zero, and therefore the variance inflation term is

zero.

4.3 Variance estimation and inference

Theorem 2 provides a guidance for variance estimation of

the DSM estimators that can take all sources of variability into account.

However, such variance estimators are complicated to construct. We

consider variance estimation based on replication methods (Efron, 1979; Wolter, 2007).

Lack of smoothness makes the standard replication methods invalid

for the matching estimator. When the number of matches remains fixed,

Abadie and Imbens (2008) demonstrated the failure

of the bootstrap for matching estimators. This is because the non-parametric

bootstrap cannot preserve the distribution of the number of times

that each unit is used as a match. In this case, Otsu and Rai (2017)

proposed a wild bootstrap procedure for the matching estimator when

matching is directly based on the covariates. Yang and Kim (2019)

proposed a replication based procedure for predictive mean matching

in survey data.

Given the two-stage estimation procedure for the DSM estimator, the

variability of the matching estimator results from two sources: first,

the estimation of the double score function, and second, matching.

To faithfully take into account all sources of variability, we propose

a two-stage replication variance estimation procedure, in parallel

to the two-stage point estimation procedure. First, we construct replicates

of the nuisance parameter estimators in the double score. Second,

based on the asymptotic linear representations of the DSM estimator,

we construct replicates of the DSM estimator directly based on the

linear terms with the replicated nuisance parameters. In this way,

the distribution of the number of times that each unit is used as

a match can be retained.

Specifically, the replication variance estimation algorithm proceeds

as follows.

VE-Step

Obtain a bootstrap sample, or equivalently the

bootstrap replication weights with

is a multinomial random vector with

draws on equal probability cells. Obtain a bootstrap replicate

of , , by solving the estimating

equation .

For each unit , calculate for .

VE-Step

Obtain a bootstrap replicate of

as

VE-Step

Repeat VE-Steps 1 and 2 for a large number of

times. Calculate the bootstrap variance estimator of

as the empirical variance of

over a large number of bootstrap replicates.

Remark 1

In VE-Step1, instead of generating bootstrap resamples,

we can generate replication weights from general distributions that

satisfy , ,

and , where ’obs’ denotes the

observed data. For example, one can generate the ’s

from Exp independently from the observed data.

5 Multiply robust matching estimator of the QTE

Matching is attractive for general causal estimation, because it can

be viewed as a hot deck imputation method (Ford, 1983),

where for each unit the donors for the missing potential outcome are

actually observed values from the opposite treatment group. An advantage

of hot deck imputation is that it preserves the distribution of the

potential outcomes so that valid estimators for parameters depending

on the entire distribution of the potential outcomes such as the mean

and quantiles can be obtained based on the imputed data set. In this

section, we extend the DSM framework to estimate the QTE.

We focus on estimating separately for . Similar

to (5), we have

Based on the above equation, we propose the DSM estimator of

as

(12)

where

(13)

(14)

and is a semi/nonparametric estimator of ,

for . Note that is an initial

matching estimator of and

is the bias correction term; see the supplementary material. Then

the DSM estimator of is .

For estimating , Steps and of DSM in Section

3.3 remain the same; Steps and

proceed as follows:

Step

Obtain a semiparametric estimator of

based on , for .

For example, we can consider the method of sieves for the normal linear

model after a Box-Cox transformation of Zhang et al. (2012) or

the single-index conditional distribution model of Chiang and Huang (2012).

Step

The DSM estimator of is given by (12)

with replaced by . We denote the final

estimator of as

to reflect its dependence on , for . Then,

the DSM estimator of is .

To establish the multiple robustness and asymptotic distributions

of and ,

we require further technical conditions.

Assumption 4

For , the following conditions

hold for the parameter and the estimating function :

(i) lies in a closed interval ; (ii) the estimating

equation has a unique root in the interior of ;

(iii) is strictly increasing and absolutely continuous

with finite first derivative in , and the derivative

is bounded away from for all in ; and (iv) for

satisfies a Lipschitz continuity condition: there

exists a constant such that

for any and .

Under Assumptions 1–2,

3 (i) and 4, if any model of the propensity

score or prognostic score is correctly specified, similar to the proof

in Section S1, we have ,

and then we express as

(15)

Expression (15) is called the Bahadur-type representation

for (Francisco and Fuller, 1991). With the

representation (15), it is straightforward to

extend the multiple robustness and asymptotic distributions of the

ATE estimation to and .

Theorem 3

Under Assumptions 1–2,

3 (i) and 4, if any model of the propensity

score or prognostic score is correctly specified,

in distribution, as , where is

given in (S19).

Theorem 4

Under Assumptions 1–2,

3 (i) and 4, and regularity conditions

specified in the supplementary material, if any model of the propensity

score or prognostic score is correctly specified, the approximate

distribution of

is where

(16)

is given in (S19), and

are given in Theorem 2, and are given

in (S20) and (S21), respectively.

For variance estimation of ,

VE-Step 1 in Section 4.3 remains the same;

VE-Steps 2 and 3 proceed as follows:

VE-Step

For , obtain a bootstrap replicate of

, ,

by solving

for . Then a bootstrap replicate of

is .

VE-Step

Repeat VE-Steps 1 and 2’ for a large number of

times. Calculate the bootstrap variance estimator of

as the empirical variance of

over a large number of bootstrap replicates.

6 Simulation

We conduct a simulation study to investigate the finite-sample performance

of the proposed DSM estimators relative to existing weighting and

matching estimators. In the causal inference and missing data literature,

previous simulations (e.g., Kang and Schafer, 2007) have

found that weighting estimators can have high variability, especially

if the probabilities are close to zero or one. Frölich (2004)

found that the weighting estimator was inferior to matching estimators

in terms of root mean squared error. It has been found that matching

on high-dimensional covariates is not practical for commonly found

sample sizes (e.g., Abadie and Imbens, 2006). In the comparative

effectiveness research, PGM has been shown to be more advantageous

than PSM when the propensity score distributions are strongly separated

(Wyss et al., 2015; Kumamaru et al., 2016). Imbens (2004)

noted that if the regression models are misspecified, PGM may be inconsistent.

These results motivate us to compare the weighting and matching estimators

in a setting with complex data generative models, and where the propensity

scores may be close to zero or one.

Let the sample size be Confounder

is generated by Uniform []

for . To introduce nonlinear relationships between

and dependent variables, let be a nonlinear

transformation of , where , ,

, , ,

, , ,

, , which are further scaled

and centered such that and for all .

The potential outcomes are and

, where ,

and .

Under the data generative model, the ATE is and the th

QTE is . The treatment indicator follows Bernoulli,

where logit, where .

Some values of are close to zero or one.

To assess the multiple robustness property of the DSM estimators,

we consider two model specifications for the propensity score: 1)

a correctly specified logistic regression model

and 2) a misspecified logistic regression model ;

we also consider two model specifications for the prognostic score:

3) a correctly specified regression model

for and 4) a misspecified regression model

for .

We compare the following estimators:

a)

naive, which is the simple difference of standard estimators from

two treatment groups;

b)

the weighting estimators including the IPW and AIPW estimators (“ipw”

and “aipw”);

c)

the matching estimators based on (“m.x”; bias-corrected Abadie and Imbens, 2011),

or propensity score (“psm”) or prognostic score (“pgm”) or

double score (“dsm”).

Each weighting and matching estimator is assigned a name in the form

of “method-0000”, where each digit of the four-digit number, from

left to right, indicates if , ,

, or

is used in the construction of the method, with “1” meaning yes

and “0” meaning no, respectively. For example, “ipw1000” is

the IPW estimator with the propensity score model

and “dsm1110” is the DSM estimator with two propensity score models

, and one prognostic

score model . We implement

standard IPW and AIPW estimators for the ATE estimation and the corresponding

estimators of Zhang et al. (2012) for the QTE estimation. For

all matching estimators, the conditional outcome mean functions are

approximated using power series; and the conditional distribution

functions are approximated based on the power series for the Normal

linear model Zhang et al. (2012).

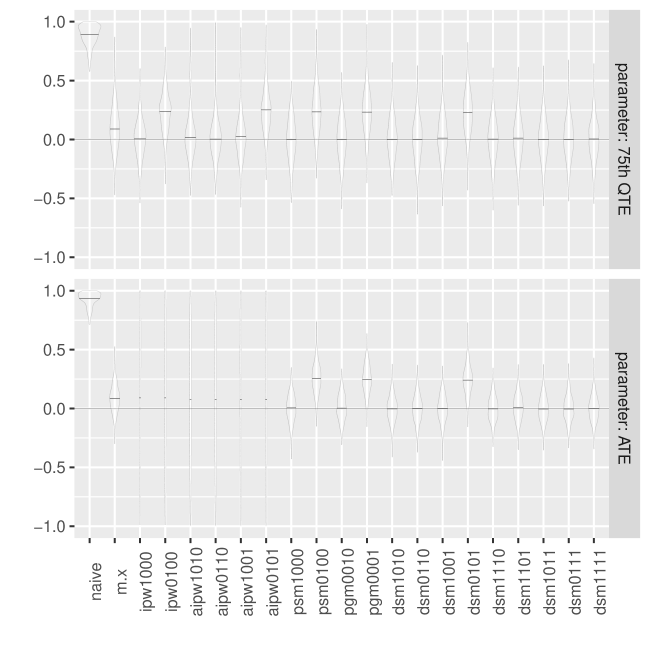

Figure 1: Simulation results of various weighting and matching

estimators. There are two panels of results: the top for the th

QTE and the bottom for the ATE. Each violin plot shows the distribution

of the estimator subtracting the true parameter value based on

Monte Carlo simulated datasets. Due to the extreme estimates of the

weighting estimators of the ATE, the violin plots for “ipwXXXX”

and “aipwXXXX” (with each X being or ) are truncated

at and and appear to be slim.

Figure 1 shows the distributions of the estimation

error (i.e.; the estimator minus the true parameter value) based on

1000 repeated sampling. The naive estimator is biased for the th

QTE and the ATE. Matching directly based on -dimensional

(indicated by “m.x”) is biased for the QTE and the ATE even with

bias correction. This suggests that matching on high-dimensional covariates

is not practical and calls for dimension reduction. We discuss the

results from the IPW and AIPW estimator separately for the QTE and

ATE estimation. For the QTE estimation, the IPW estimator relies on

a correct specification of the propensity score: it has small biases

if the propensity score model is correctly specified (indicated by

“ipw1000”); while it is biased if the propensity score model is

misspecified (indicated by “ipw0100”). The AIPW estimator is doubly

robust: it has small biases if either the propensity score model or

the prognostic model is correctly specified (indicated by “aipw1010”,

“aipw1001”, “aipw0110”). These performances are expected based

on the existing results for the IPW and AIPW estimators. Surprisingly,

the IPW and AIPW estimators are biased and have very large variability

for estimating the ATE, even when the involving models are correctly

specified. We examine the empirical distribution of the estimated

propensity score weights and find that there are extremely large weights

that dominate other weights. To mitigate this issue, one can stabilize

the weighting estimators by normalizing the weights (Hernán et al., 2001).

However, we do not find this strategy effective in our setting. Although

the AIPW estimator is constructed to be semiparametrically efficient,

its performance can be severely poor when it involves large weights.

By construction, matching does not invert the estimated propensity

scores and therefore is more robust to outliers of the propensity

score estimates. We now compare performances of the score-based matching

estimators. The single score matching estimators (indicated by “psm1000”,

“psm0100”, “pgm0010”, “pgm0001”) are singly robust and

rely on a correct specification of the underlying score model. The

DSM estimators are multiply robust in that it has small biases for

the QTE and the ATE if any model of the propensity score or prognostic

score is correctly specified. Unlike the AIPW estimators, the DSM

estimators are robust to extreme values of the propensity score estimates.

Table 3 reports the coverage rates of the DSM estimators

of the th QTE and the ATE using the proposed replication-based

method. Under the multiple robustness condition (i.e., if any model

of the propensity score or prognostic score is correctly specified),

the coverage rates are all close to the nominal coverage except for

“dsm0101”.

Table 3: Simulation results based on

Monte Carlo simulated datasets for the coverage properties of the

DSM estimators using the replication-based method: empirical coverage

rate and (empirical coverage rate Monte Carlo

standard error)

75th QTE

ATE

“dsm1010”

95.4

(94.6, 97.2)

95.6

(94.4, 96.9)

“dsm0110”

96.5

(95.2, 97.1)

95.9

(94.7, 97.1)

“dsm1001”

96.6

(95.3, 98.2)

96.0

(94.9,97.1)

“dsm0101”

79.7

(77.2, 82.2)

55.1

(52.0, 58.2)

“dsm1111”

95.4

(94.1, 96.7)

95.6

(94.3, 96.9)

“dsm1110”

95.9

(94.7, 97.1)

96.1

(94.9, 97.3)

“dsm1101”

95.7

(94.5, 96.9)

95.5

(94.3, 96.9)

“dsm1011”

95.0

(93.6, 96.4)

95.5

(94.3, 96.9)

“dsm0111”

95.1

(93.8, 96.2)

95.8

(94.6, 97.2)

7 Real-data application

In this section, we apply the proposed DSM method as well as other

existing methods in Section 6 to the well-known

National Supported Work (NSW) data (LaLonde, 1986; Firpo, 2007).

This dataset documented the effect of a job training program for the

unemployed on future earnings. Following Dehejia and Wahba (1999),

we include the comparison group from Westat’s Matched Current Population

Survey-Social Security (CPS) Administration File. In our analysis,

we include treated units and control units from the

NSW, as well as comparison units from the CPS-3, a subset of

the CPS data (LaLonde, 1986; Firpo, 2007). Seven

baseline confounding covariates are used for this application: age,

education, race, Hispanic, married, having no college degree, and

real earnings in 1975. The outcome of interest is the real earnings

in 1978.

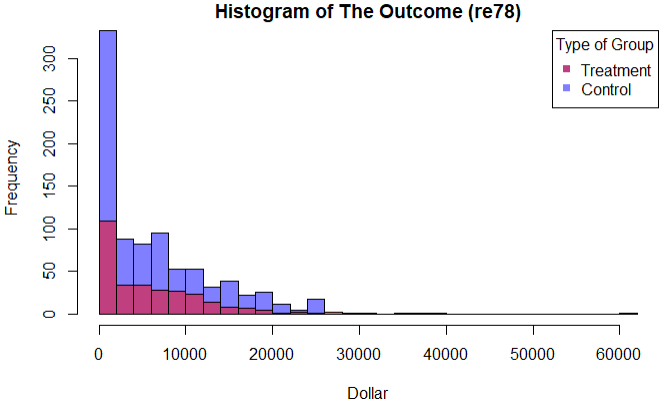

Because the outcome distributions are highly skewed (see Figure S1),

the average treatment effect may not provide a comprehensive evaluation

of the job training program. Therefore, we estimate the ATT and QTTs.

The propensity score is estimated based on a logistic regression model

with all first-order terms of the covariates and

second-order terms of numerical variables, following Dehejia and Wahba (1999).

The prognostic score is estimated based on a linear regression of

the earnings with the same predictors as in the propensity score model

for the control group.

Table 4: Covariate balance check before and after DSM

age

educ

black

hisp

married

nodegr

re75

Before

Treatment group mean

24.63

10.38

0.80

0.09

0.17

0.73

3066

Matching

Control group mean

26.25

10.21

0.50

0.13

0.34

0.70

2745

Stand diff. in means

-0.19

0.08

0.61

-0.10

-0.37

0.06

0.07

After

Treatment group mean

24.63

10.38

0.80

0.09

0.17

0.73

3066

Matching

Control group mean

25.04

10.39

0.80

0.11

0.17

0.72

2898

Stand diff. in means

-0.05

0.00

0.01

-0.05

-0.01

0.01

0.04

Table 5: Estimated ATT and QTTs at the , , ,

, and quantiles, and Wald confidence

intervals

Estimand

m.x

psm

pgm

dsm

Naive(ATE&QTE)

ATT

372 (-746,1489)

918 (-222,2058)

-150 (-1215,914)

1088 (-57,2233)

-65 (-957,827)

0.1-QTT

0 (0,0)

0 (0,0)

0 (0,0)

0 (0,0)

0 (0,0)

0.25-QTT

549 (-90,1189)

549 (-55,1154)

549 (-104,1202)

549 (-76,1175)

549 (-55,1153)

0.3-QTT

935 (57,1813)

1064 (268,1860)

1039 (96,1982)

1019 (134,1904)

604 (-641,1170)

0.5-QTT

524 (-1606,2654)

889 (-741,2519)

1296 (-252,2844)

757 (-997,2511)

69 (-1093,1230)

0.75-QTT

-391 (-2752,1970)

617 (-1451,2686)

737 (-2070,3544)

1763 (-656,4182)

-195 (-1441,1578)

0.9-QTT

-963 (-3482,1556)

897 (-1750,3543)

-936 (-4770,1795)

864 (-1395,3123)

-2326 (-2021,2158)

Matching admits a transparent assessment of covariate balance before

and after matching. Table 4 presents the means of

all covariates by treatment group and the standardized difference

in means before and after DSM. The standardized difference is calculated

as the difference of the group means divided by the overall standard

error in the original sample. DSM makes standardized differences fall

between to for all covariates, reducing the differences

of the observed covariates in the treated and the control.

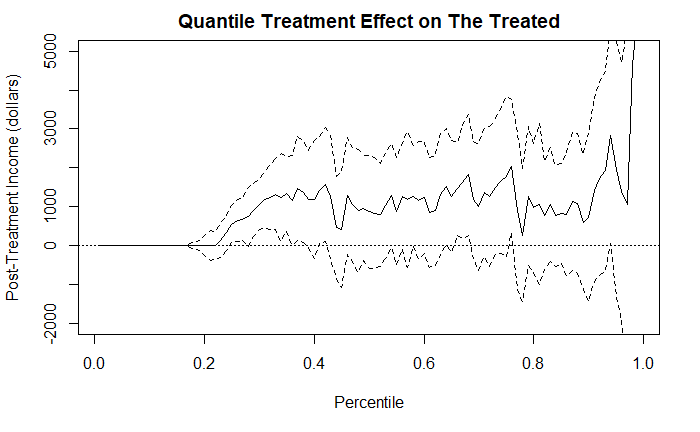

Table 5 shows the estimated ATTs and QTTs at the ,

, , , and quantiles, and

Wald confidence intervals from the four matching methods, as well

as ATE and QTE estimated by naive method. All four matching estimators

show that the job training program does not have a significant effect

on the average earning for the treated. Figure 2

shows the QTT plot estimated by DSM algorithm. A closer inspection

of the QTT plot reveals that the effect is in fact significant around

percentile of , which suggests that the program is beneficial

for the lower middle class.

Figure 2: Quantile effect plot on the treated

from the DSM algorithm

8 Discussion

We have developed multiply robust matching estimators for general

causal estimands. This framework offers a new “metric” to summarize

the differential roles of different covariates and also serves as

a powerful dimensional reduction tool in high-dimensional confounding.

The improved robustness comes from multiple model specifications for

the propensity score and prognostic score. The proposed DSM estimators

thus provide multiple protections to model misspecification and therefore

is an attractive alternative to existing weighting estimators.

Several issues are worth discussing. As with PSM, although the matching

variables are well balanced, individual covariates may not for a given

application. In this case, if the researchers know important confounders

based on substantive knowledge, they can augment the double score

by adding those confounders to ensure balance for these confounders;

however, adding too many variables will results in potential bias

as demonstrated in our simulation. Alternatively, one can use regression

adjustment for the matched sample Abadie and Spiess (2016), which

can remove remaining confounding biases. We focus on a binary treatment.

Yang et al. (2016) has developed the generalized propensity

score matching for estimating the treatment effects for more then

two treatments. Instead of creating a matched set to estimate the

treatment contrast directly, Yang et al. (2016) proposed

to create matched sets to estimate potential outcome means separately.

This approach allows matching based on one scalar function, namely

the generalized propensity score at a given treatment level, one at

a time. It is also of interest to extend our DSM algorithm to more

than two treatment comparison. It is important to highlight that as

for all existing matching methods, the DSM method cannot account for

unmeasured confounding. Following Rosenbaum and Rubin (1983a)

and Robins et al. (2000), we will develop sensitivity analyses

to no unmeasured confounding in the matching framework.

Acknowledgment

We are grateful to Alberto Abadie for providing comments. Yang is

partially supported by the National Science Foundation grant DMS 1811245,

National Cancer Institute grant P01 CA142538, National Institute on

Aging grant 1R01AG066883, and National Institute of Environmental

Health Science grant 1R01ES031651.

References

(1)

Abadie and Imbens (2006)

Abadie, A. and Imbens, G. W. (2006).

Large sample properties of matching estimators for average treatment

effects, Econometrica74: 235–267.

Abadie and Imbens (2008)

Abadie, A. and Imbens, G. W. (2008).

On the failure of the bootstrap for matching estimators, Econometrica76: 1537–1557.

Abadie and Imbens (2011)

Abadie, A. and Imbens, G. W. (2011).

Bias-corrected matching estimators for average treatment effects,

Journal of Business & Economic Statistics29: 1–11.

Abadie and Imbens (2012)

Abadie, A. and Imbens, G. W. (2012).

A martingale representation for matching estimators, J. Am.

Stat. Assoc.107: 833–843.

Abadie and Imbens (2016)

Abadie, A. and Imbens, G. W. (2016).

Matching on the estimated propensity score, Econometrica84: 781–807.

Abadie and Spiess (2016)

Abadie, A. and Spiess, J. (2016).

Robust post-matching inference, Unpublished Paper. MIT and

Harvard University. Retrieved from https://editorialexpress.

com/cgi-bin/conference/down load.

Andreou and Werker (2012)

Andreou, E. and Werker, B. J. (2012).

An alternative asymptotic analysis of residual-based statistics, Rev. Econ. Stat.94: 88–99.

Antonelli et al. (2018)

Antonelli, J., Cefalu, M., Palmer, N. and Agniel, D. (2018).

Doubly robust matching estimators for high dimensional confounding

adjustment, Biometrics74: 1171–1179.

Bang and Robins (2005)

Bang, H. and Robins, J. M. (2005).

Doubly robust estimation in missing data and causal inference models,

Biometrics61: 962–973.

Bickel et al. (1993)

Bickel, P. J., Klaassen, C., Ritov, Y. and Wellner, J.

(1993).

Efficient and Adaptive Inference in Semiparametric Models,

Johns Hopkins University Press, Baltimore.

Billingsley (1995)

Billingsley, P. (1995).

Probability and Measure, 3 edn, Wiley: New York.

Chen and Shao (2000)

Chen, J. and Shao, J. (2000).

Nearest neighbor imputation for survey data, J. Offic. Stat.16: 113–131.

Chen and Shao (2001)

Chen, J. and Shao, J. (2001).

Jackknife variance estimation for nearest-neighbor imputation, J. Am. Stat. Assoc.96: 260–269.

Chen and Haziza (2017a)

Chen, S. and Haziza, D. (2017a).

Multiply robust imputation procedures for the treatment of item

nonresponse in surveys, Biometrika104: 439–453.

Chen and Haziza (2017b)

Chen, S. and Haziza, D. (2017b).

Multiply robust nonparametric multiple imputation for the treatment

of missing data, Stat. Sin29: 2035–2053.

Chen (2007)

Chen, X. (2007).

Large sample sieve estimation of semi-nonparametric models, Handbook of Econometrics6: 5549–5632.

Chiang and Huang (2012)

Chiang, C.-T. and Huang, M.-Y. (2012).

New estimation and inference procedures for a single-index

conditional distribution model, Journal of Multivariate Analysis111: 271–285.

Dehejia and Wahba (1999)

Dehejia, R. H. and Wahba, S. (1999).

Causal effects in nonexperimental studies: Reevaluating the

evaluation of training programs, J. Am. Stat. Assoc.94: 1053–1062.

Dehejia and Wahba (2002)

Dehejia, R. H. and Wahba, S. (2002).

Propensity score matching methods for non-experimental causal

studies, Rev. Econ. Stat.84: 151–161.

Efron (1979)

Efron, B. (1979).

Bootstrap methods: another look at the jackknife, Annals of

Statistics7: 1–26.

Firpo (2007)

Firpo, S. (2007).

Efficient semiparametric estimation of quantile treatment effects,

Econometrica75: 259–276.

Ford (1983)

Ford, B. L. (1983).

An overview of hot-deck procedures, Incomplete data in sample

surveys2(Part IV): 185–207.

Francisco and Fuller (1991)

Francisco, C. A. and Fuller, W. A. (1991).

Quantile estimation with a complex survey design, Annals of

Statistics19: 454–469.

Frölich (2004)

Frölich, M. (2004).

Finite-sample properties of propensity-score matching and weighting

estimators, Rev. Econ. Stat.86: 77–90.

Guo and Fraser (2014)

Guo, S. and Fraser, M. W. (2014).

Propensity Score Analysis: Statistical Methods and

Applications, Vol. 11, Thousand Oaks, CA: SAGE.

Han (2014)

Han, P. (2014).

Multiply robust estimation in regression analysis with missing data,

J. Am. Stat. Assoc.109(507): 1159–1173.

Han and Wang (2013)

Han, P. and Wang, L. (2013).

Estimation with missing data: beyond double robustness, Biometrika100: 417–430.

Hansen (2008)

Hansen, B. B. (2008).

The prognostic analogue of the propensity score, Biometrika95: 481–488.

Heckman et al. (1997a)

Heckman, J. J., Ichimura, H. and Todd, P. E. (1997a).

Matching as an econometric evaluation estimator: Evidence from

evaluating a job training programme, The Review of Economic Studies64: 605–654.

Heckman et al. (1997b)

Heckman, J. J., Ichimura, H. and Todd, P. E. (1997b).

Matching as an econometric evaluation estimator: Evidence from

evaluating a job training programme, The Review of Economic Studies64: 605–654.

Hernán et al. (2001)

Hernán, M. A., Brumback, B. and Robins, J. M. (2001).

Marginal structural models to estimate the joint causal effect of

nonrandomized treatments, J. Am. Stat. Assoc.96: 440–448.

Imbens (2004)

Imbens, G. W. (2004).

Nonparametric estimation of average treatment effects under

exogeneity: A review, Rev. Econ. Stat.86: 4–29.

Imbens and Rubin (2015)

Imbens, G. W. and Rubin, D. B. (2015).

Causal Inference in Statistics, Social, and Biomedical

Sciences, Cambridge University Press, Cambridge UK.

Kang and Schafer (2007)

Kang, J. D. and Schafer, J. L. (2007).

Demystifying double robustness: A comparison of alternative

strategies for estimating a population mean from incomplete data, Statistical Science22: 523–539.

Kumamaru et al. (2016)

Kumamaru, H., Schneeweiss, S., Glynn, R. J., Setoguchi, S. and Gagne,

J. J. (2016).

Dimension reduction and shrinkage methods for high dimensional

disease risk scores in historical data, Emerging Themes in Epidemiology13: Article 5.

LaLonde (1986)

LaLonde, R. J. (1986).

Evaluating the econometric evaluations of training programs with

experimental data, The American Economic Review76: 604–620.

Le Cam and Yang (1990)

Le Cam, L. and Yang, G. L. (1990).

Asymptotics in Statistics: Some Basic Concepts, Springer:

Berlin.

Leacy and Stuart (2014)

Leacy, F. P. and Stuart, E. A. (2014).

On the joint use of propensity and prognostic scores in estimation of

the average treatment effect on the treated: a simulation study, Stat.

Med.33: 3488–3508.

Little and Rubin (2002)

Little, R. J. and Rubin, D. B. (2002).

Statistical Analysis with Missing Data, Wiley, Hoboken.

Lunceford and Davidian (2004)

Lunceford, J. K. and Davidian, M. (2004).

Stratification and weighting via the propensity score in estimation

of causal treatment effects: a comparative study, Stat. Med.23: 2937–2960.

Otsu and Rai (2017)

Otsu, T. and Rai, Y. (2017).

Bootstrap inference of matching estimators for average treatment

effects, J. Am. Stat. Assoc.112: 1720–1732.

Robins et al. (2000)

Robins, J. M., Rotnitzky, A. and Scharfstein, D. O. (2000).

Sensitivity analysis for selection bias and unmeasured confounding in

missing data and causal inference models, Statistical Models in

Epidemiology, the Environment, and Clinical Trials, Springer, New York:

Springer, pp. 1–94.

Rosenbaum (1989)

Rosenbaum, P. R. (1989).

Optimal matching for observational studies, J. Am. Stat. Assoc.84: 1024–1032.

Rosenbaum and Rubin (1983a)

Rosenbaum, P. R. and Rubin, D. B. (1983a).

Assessing sensitivity to an unobserved binary covariate in an

observational study with binary outcome, J. R. Stat. Soc. Ser. B Stat.

Methodol.45: 212–218.

Rosenbaum and Rubin (1983b)

Rosenbaum, P. R. and Rubin, D. B. (1983b).

The central role of the propensity score in observational studies for

causal effects, Biometrika70: 41–55.

Rubin (1986)

Rubin, D. B. (1986).

Statistical matching using file concatenation with adjusted weights

and multiple imputations, Journal of Business & Economic Statistics4: 87–94.

Rubin (2006)

Rubin, D. B. (2006).

Matched Sampling for Causal Effects, Cambridge University

Press, Cambridge, England.

Smith and Schaubel (2015)

Smith, A. R. and Schaubel, D. E. (2015).

Time-dependent prognostic score matching for recurrent event analysis

to evaluate a treatment assigned during follow-up, Biometrics71: 950–959.

Stuart (2010)

Stuart, E. A. (2010).

Matching methods for causal inference: A review and a look forward,

Statistical Science25: 1–21.

van der Vaart (2000)

van der Vaart, A. W. (2000).

Asymptotic Statistics, Cambridge University Press, Cambridge,

MA.

Wolter (2007)

Wolter, K. (2007).

Introduction to Variance Estimation, 2 edn, Springer, New York.

Wyss et al. (2015)

Wyss, R., Ellis, A. R., Brookhart, M. A., Jonsson Funk, M., Girman, C. J.,

Simpson Jr, R. J. and Stürmer, T. (2015).

Matching on the disease risk score in comparative effectiveness

research of new treatments, Pharmacoepidemiology and Drug Safety24: 951–961.

Wyss et al. (2017)

Wyss, R., Hansen, B. B., Ellis, A. R., Gagne, J. J., Desai, R. J., Glynn, R. J.

and Stürmer, T. (2017).

The “dry-run” analysis: a method for evaluating risk scores for

confounding control, Am. J. Epidemiol.185: 842–852.

Yang and Ding (2018)

Yang, S. and Ding, P. (2018).

Asymptotic inference of causal effects with observational studies

trimmed by the estimated propensity scores, Biometrika105: 487–493.

Yang et al. (2016)

Yang, S., Imbens, G. W., Cui, Z., Faries, D. E. and Kadziola, Z.

(2016).

Propensity score matching and subclassification in observational

studies with multi-level treatments, Biometrics72: 1055–1065.

Yang and Kim (2019)

Yang, S. and Kim, J. K. (2019).

Asymptotic theory and inference of predictive mean matching

imputation using a superpopulation model framework, Scand. J. Stat.

p. doi.org/10.1111/sjos.12429.

Zhang et al. (2012)

Zhang, Z., Chen, Z., Troendle, J. F. and Zhang, J. (2012).

Causal inference on quantiles with an obstetric application, Biometrics68: 697–706.

Zhao (2004)

Zhao, Z. (2004).

Using matching to estimate treatment effects: Data requirements,

matching metrics, and Monte Carlo evidence, Rev. Econ. Stat.86: 91–107.

Supplementary Material for “Multiply robust matching

estimators for average and quantile treatment effects”

Sections S1, S4,

S5, and S6

present the proofs of Theorems 1, 2, 3,

and 4, respectively. Section S2

compares the efficiency of PSM, PGM, and DSM. Section S3

presents Le Cam’s third lemma. Section S7

presents the extensions to the ATT and QTT. Section S8

presents a figure for the application.

For simplicity of the presentation, we omit the dependence of

for if there is no ambiguity. Following Abadie and Imbens (2011)

and Abadie and Imbens (2012), under mild regularity conditions

on the nonparametric estimation, we have .

Then, has the following asymptotic

linear form:

(S3)

If any model of the propensity score or prognostic score is correctly

specified, by Lemma 4, we have

and therefore

converges to zero.

We show the covariances of the three terms are zero:

similarly, , and by construction, .

Thus, the asymptotic variance of

is

The first term becomes

Following Abadie and Imbens (2006), the second and third term, as

, becomes

S2 Comparison of PSM, PGM, and DSM

We compare the asymptotic variances of the PSM, PGM, and DSM estimators

of the ATE. To simplify the discussion, we assume one working model

for the propensity score and one working model

for the prognostic score. In fact, the derivation for the DSM estimator

in Section S1 applies to the PSM estimator

and the PGM estimator by replacing

() with and , respectively.

If the prognostic score model is correctly specified, we

have and therefore

(S4)

for . Then, for the DSM estimator, in (10)

becomes

For the PGM estimator, it is easy to derive that the corresponding

asymptotic variance is

By Jensen’s inequality, we have

for . It follows that .

If the propensity score model is correctly specified, we

have and therefore

For the PSM estimator, it is easy to derive that the corresponding

asymptotic variance is

To compare and , we decompose

where and have mean

zero and satisfy that

and . With this decomposition,

and . Then, it follows

that

The last two terms are always non-negative; however, the sign of

and therefore that of can be either

positive, negative, or zero. Therefore, for estimating , it

is not guaranteed that DSM is more efficient than PSM. For estimating

, using the similar argument as above,

is absent, so DSM is more efficient than PSM.

S3 Le Cam’s third Lemma

Consider two sequences of probability measures

and . Assume that under ,

a statistic and the likelihood ratios

satisfy

in distribution, as . Then, under ,

in distribution, as . See Le Cam and Yang (1990),

Bickel et al. (1993), and van der Vaart (2000) for textbook

discussions.

We follow the technique in Andreou and Werker (2012) and Abadie and Imbens (2016).

In Abadie and Imbens (2016), the PSM estimators rely on the nuisance

parameter estimator under a correct specification of the propensity

score model. In our setting, the nuisance parameters include both

parameters in the propensity score model and the prognostic score

model, and require only one of the models to be correctly specified.

Without loss of generality, we assume one working model

for the propensity score and one working model

for the prognostic score. The proof for the case with more than two

working models for each score is similar at the expense of heavier

notation. Let be the distribution

of . Consider

to be indexed by ,

which satisfies

(S6)

We invoke standard regularity conditions on Z-estimation (van der Vaart; 2000)

as follows.

Assumption S1

(i) Under ,

in distribution,

as , where

; (ii)

is nonsingular around ; and (iii) for any vector of constant

,

is uniformly integrable.

To derive the large sample distribution of ,

following Abadie and Imbens (2016), we impose the following regularity

conditions.

Assumption S2

There exists a neighborhood of such that for any

in this region, the following conditions hold: for , (i) the

matching variable has a compact and convex support

, with a continuous density bounded and bounded away

from zero; (ii) and satisfy the Lipschitz continuity condition; and (iii) there exists

such that

is uniformly bounded for any

Following Andreou and Werker (2012), because we consider a semiparametric

model for , to invoke the Le Cam’s lemma, we specify

an auxiliary parametric model defined locally

though , , with a density

(S8)

By Assumption S1 (iii),

is uniformly integrable, and thus model (S8) is uniformly

locally asymptotically normal. Because under ,

in distribution,

the normalizing constant in the denominator converges to one as .

The Fisher information under the parametric model (S8)

is Therefore, is efficient

under model (S8).

Now consider , for ,

with the local shift (Bickel et al.; 1993).

Under model (S8), the likelihood ratio under

is

(S9)

where the second equality follows by the Taylor expansion of

at . Moreover, under :

in distribution, as , and

(S10)

We also assume the following regularity condition.

Assumption S3

For all bounded continuous

functions , the conditional expectation

converges in distribution to , where

is the expectation taken with respect to .

In the first step, under , we write

to reflect its dependence on ; to be specific, we have

We derive that under ,

(S11)

in distribution, as . We then express ,

where

(S12)

By Le Cam’s third lemma, under ,

in distribution, as . Replacing

by yields that under ,

(S13)

in distribution, as .

In the second step, we provide a heuristic derivation for (S13)

to obtain the approximate distribution (11). If the

Normal distribution were exact, then

(S14)

Given that , we have ,

and hence .

Marginalizing (S14) over the asymptotic distribution of

, we derive (11).

The formal technique to derive (11) can be find in

Andreou and Werker (2012) and Abadie and Imbens (2016). To

avoid repetition, we omit this step.

In the following, we provide the proof to (S11) in the

first step of the proof. Asymptotic normality of

under follows from Theorem 1 and the

uniform local asymptotic normality of model (S8). Asymptotic

joint normality of

and follows from (S9)

and (S10). Also, ,

where

Therefore, the remaining is to show that, under :

(S15)

in distribution, as . To prove (S15),

consider the linear combination

where . We analyze

using the martingale theory. We rewrite

where

Consider the -fields

Then, we have

is a martingale for each , which follows by the following

reasons:

(i)

because is a double balancing score,

(ii)

let

for , then

(iii)

because ;

(iv)

by the conditioning argument,

(v)

and

due to that fact that is unbiased conditional on

;

(vi)

because

is unbiased given ;

(vii)

because

is unbiased given .

Therefore, we can apply the martingale central limit theorem (Billingsley; 1995)

to derive the limiting distribution of . Under Assumption

S2, we can verify the conditions for the martingale

central limit theorem hold. It follows that under ,

in distribution, as ,

where .

Under Assumption S3, we thus derive the expression

of and specify the components in (S15) with

Then the Bahadur-type representation for

in (15) follows.

We obtain the following decomposition

and denote

(S18)

Because of (1) and (2), ,

so . The difference

in (S18) accounts for the matching discrepancy, and therefore

contributes to the asymptotic bias of the matching estimator.

To correct for the bias due to matching discrepancy, let

be a nonparametric estimator of , for . We propose

a de-biasing DSM estimator of in

(13).

Therefore, by the Bahadur-type representation for ,

we have

Following a similar derivation in the proof for Theorem 1,

the asymptotic variance of

is given by

The proof of Theorem 4 is similar to that of Theorem

2. It suffices to replace

in (S13) by

and derive the corresponding and , denoted

by and .

Toward that end, the key is to write

where

and repeat a similar analysis in Section S4

with the following changes to ,

and :

Then, we can derive

(S20)

where

and

(S21)

S7 Extensions to the causal effects on the treated

In this extension, we estimate the average causal effect on the treated

and the quantile treatment effect on the treated

,

where ,

. Here, because , the outcome

distribution for the treated is identifiable. Therefore,

and .

To identify the outcome distribution for the control, Assumptions

2 and 1 can be relaxed (Heckman et al.; 1997b).

Assumption S4

.

Assumption S5

There exists a constant

such that almost surely.

For the causal effects on the treated, the prognostic score

is a sufficient statistic for in the sense that

according to Hansen (2008). Then, under Assumptions

S4 and S5,

and

encoding the double balancing properties of .

The DSM estimators for and

follow similar steps as for and . We describe

the differences below.

In the matching step, for each unit with treatment ,

find nearest neighbors from the control group based

on the matching variable . Let

these matched units for unit be indexed by .

The initial and de-biasing DSM estimators of

are

Let the estimator of be

Then, we estimate by

The initial and de-biasing DSM estimators of

are

Then, we estimate by

Lastly, the DSM estimator of is .

For variance estimation, we replace the VE-Step 2 and VE-Step 2’ for

and by the following steps:

ATT-VE-Step

Obtain a bootstrap replicate of ,

QTT-VE-Step

For , obtain a bootstrap replicate

of , ,

by solving

For , obtain a bootstrap replicate of ,

, by solving

for . Then a bootstrap replicate of

is .

S8 Figure

Figure S1 shows that the outcome distributions are

highly skewed in the data from the job training program.