suppmat[suppmat.pdf] \externaldocumentrgmwm_app

Robust Two-Step Wavelet-Based Inference

for Time Series Models

Abstract

Complex time series models such as (the sum of) ARMA models with additional noise, random walks, rounding errors and/or drifts are increasingly used for data analysis in fields such as biology, ecology, engineering and economics where the length of the observed signals can be extremely large. Performing inference on and/or prediction from these models can be highly challenging for several reasons: (i) the data may contain outliers that can adversely affect the estimation procedure; (ii) the computational complexity can become prohibitive when models include more than just a few parameters and/or the time series are large; (iii) model building and/or selection adds another layer of (computational) complexity to the previous task; and (iv) solutions that address (i), (ii) and (iii) simultaneously do not exist in practice. For this reason, this paper aims at jointly addressing these challenges by proposing a general framework for robust two-step estimation based on a bounded influence M-estimator of the wavelet variance. In this perspective, we first develop the conditions for the joint asymptotic normality of the latter estimator thereby providing the necessary tools to perform (direct) inference for scale-based analysis of signals. Taking advantage of the model-independent weights of this first-step estimator that are computed only once, we then develop the asymptotic properties of two-step robust estimators using the framework of the Generalized Method of Wavelet Moments (GMWM), hence defining the Robust GMWM (RGMWM) that we then use for robust model estimation and inference in a computationally efficient manner even for large time series. Simulation studies illustrate the good finite sample performance of the RGMWM estimator and applied examples highlight the practical relevance of the proposed approach.

Keywords: Wavelet Variance, Scale-Based Analysis of Variance, Large Scale Time Series, Signal Processing, Generalized Method of Wavelet Moments, State-Space Models.

1 Introduction

As for many other fields of statistical research, time series analysis is also facing different challenges due to the increasing amounts of data being recorded over time within a wide variety of contexts going from biology and ecology to finance and engineering. Among others, these challenges include (i) the need for more complex (parametric) models (e.g. to deal with possible long-term non-stationary features), (ii) the need for computationally efficient (or simply feasible) methods to analyze data and estimate such models as well as (iii) the need to deal with the increased probability of observing measurement errors in the form of contamination (outliers), model deviations, etc. In this context, there is currently a large variety of models and statistical methods available to analyze and draw conclusions from time series (see e.g. Percival and Walden, 2006; Durbin and Koopman, 2012; Shumway and Stoffer, 2013, for an overview). However, many of the existing methods may become unfeasible, for example, when estimating even slightly complex models on large time series data. In addition, the use of robust methods to perform inference when the data suffers from contamination is often a daunting task even for relatively simple (parametric) settings and moderate sample sizes, without considering more complex models in larger data settings (for motivating examples and robust inferential approaches, see e.g. Maronna et al., 2006, 2019).

In response to the above challenges and limitations, this paper proposes an alternative and general robust inference framework for (latent) parametric time series models that include (the sum of) ARMA and rounding error models as well as non-stationary models such as drifts and random walks. This framework is based on a two-step approach where the first (and most important) step consists in the proposal of a robust estimator of the Wavelet Variance (WV) (see e.g. Percival, 1995) with adequate asymptotic properties based on minimal conditions, while the second step integrates these results within the Generalized Method of Wavelet Moments (GMWM) framework (see Guerrier et al., 2013) for the purpose of inference on time series models111The method (with relative graphical tools) is implemented partly in the simts R package on CRAN and in a more complete manner in an open source R package, available at github.com/SMAC-Group/gmwm; see also Clausen et al. (2018); Bakalli et al. (2018); Radi et al. (2019). With regards to the first step, the WV has been widely used within the natural and physical sciences for analysis of variance, model building and prediction (see e.g. Percival and Walden, 2006, for an overview), and more recently within other fields of research (see e.g. Gallegati, 2012; Xie and Krishnan, 2013; Foufoula-Georgiou and Kumar, 2014; Jia et al., 2015; Ziaja et al., 2016; Abry et al., 2018, to mention a few). In this context, the properties of the standard estimators of WV have been developed (see Percival, 1995; Serroukh et al., 2000) while their limitations in presence of contamination or outliers have been underlined in Mondal and Percival (2012a) where a robust estimator was also put forward for this purpose. However, as explained further on, the use of an alternative M-estimator is preferable in different settings, including the two-step framework considered in the present paper.

With respect to parametric inference for time series, robust methods (including two-step approaches) have been proposed in abundance over the past decades and a detailed overview of these can be found, for example, in Maronna et al. (2006, 2019) (Chapter 8) while Appendix LABEL:LitRev also provides a short literature review. More specifically, a general approach in this context is to maximize asymptotic efficiency of the resulting estimators with respect to a specific model (or class of models). For this purpose, a traditional approach consists in placing estimation (and inference) in the framework of bounded-influence estimators that are obtained by bounding the corresponding estimating equations (Hampel et al., 1986), such as the Maximum Likelihood Estimator (MLE) equations or indeed those of other efficient (non robust) estimators. In this setting, a correction factor is often required to ensure consistency of the resulting robust estimator and needs to be defined for each model considered for a given time series. The computation of this model-dependent correction factor generally requires numerical approximations of possibly high-dimensional integrals or multiple one-dimensional integrals (for conditionally unbiased estimators, see Künsch, 1984), whose dimensions or number grow proportionally to the sample size. These consistency corrections can therefore not only be too burdensome to compute, relying on more computationally intensive simulation-based procedures to approximate these quantities, but also are rarely accounted for in the derivation of the statistical properties of the resulting estimator. On the other hand, robust two-step estimators (based for example on robust filtering methods or on robust autocovariance/autocorrelation estimators), while possibly paying a price in terms of asymptotic efficiency, deliver not only computational advantages but also allow to compare candidate models under a different perspective. Indeed, the first-step estimators provide a set of estimates that remain common to all candidate models and have a bounded Influence Function (IF) (Hampel, 1974) through weights (for weighted estimators) that are computed only once independently from the candidate models. Using these common estimates, aside from guaranteeing that the second step estimators inherit their bounded IF property (hence robustness), the consequence is that the model comparison in terms of fit (or prediction accuracy) is made solely on the structural features of the candidate models. This provides an alternative approach to model comparison based on robust estimators since, in the weighted estimating equation setting, the estimation weights are relative to each model under consideration that is, by assumption, the correct one. On the other hand, a two-step approach alleviates the latter hypothesis in the computation of the robust weights and hence provides an alternative route to robust model comparison. Moreover, this allows to develop graphical robust model selection tools which, in the context of this paper, rely only on a few quantities (even for large samples as seen further on and in Section 5) as well as to build robust model selection criteria in a relatively straightforward manner.

However, while robust two-step approaches have noticeable computational and model comparison advantages, these can nevertheless suffer from some theoretical and practical drawbacks. Indeed, when they are based on robust filtering, they may lead to biased estimators and lack asymptotic theory in order to perform adequate inference (see e.g. Muler et al., 2009). Alternatively, in the case where two-step estimators are based on robust moment estimators (e.g. autocovariance or autocorrelation), these are often computed in the framework of indirect inference (Smith, 1993; Gourieroux et al., 1993) or, similarly, in that of the (simulated) method of moments (McFadden, 1989; Gallant and Tauchen, 1996; Duffie and Singleton, 1993). In these settings, two-step estimators can become computationally intensive in large samples since the number of auxiliary moments that are available in practice increase linearly with the sample size, thereby requiring a moment selection procedure which delivers additional uncertainty in the successive inference phase (see e.g. Andrews, 1999). However, the GMWM framework considerably reduces the latter drawback since its first-step moment is the WV which adequately summarizes the information in the spectral density (or autocovariance) function into moments (with representing the sample size) thereby greatly reducing the number of moments even for large sample sizes while also allowing for inference on non-stationary models. Being a natural extension of the GMWM framework, the Robust GMWM (RGMWM) relies on the proposed robust estimator of WV and makes use of its properties in order to derive the inferential properties of the RGMWM so as to perform adequate estimation and general inference procedures for a wide range of time series models under slight model deviations (such as the presence of outliers) in a computationally efficient manner.

Considering the above goal, the paper is organized as follows. Section 2 proposes the robust WV estimator that constitutes the first step of the RGMWM that is presented in Section 3. In both sections, the necessary asymptotic results are developed in order to perform robust estimation and inference for (intrinsically) stationary time series. Section 4 presents a simulation study where the robustness properties of the RGMWM estimator are compared with other estimators and Section 5 demonstrates the practical usefulness of the proposed method in an economic setting while another applied setting is presented in Appendix LABEL:iner.sens.

2 Robust Wavelet Variance

To introduce the WV, let us denote , , as an intrinsically stationary time series that is either stationary or becomes so when a dth-order backward difference is applied to it. Moreover, let

denote the wavelet coefficients that result from a wavelet decomposition of the time series, where is a known wavelet filter of length at (dyadic) scale , for and . Since the filter sequence has specific properties, the wavelet coefficients can be seen as the result of a particular form of weighted moving-average taken over a number of observations proportional to (which increases as increases, see e.g. Percival and Walden, 2006, for a general overview). Moreover, if and is a dth-order stationary time series, the resulting wavelet coefficients will be stationary. Based on the (stationary) wavelet coefficients, the WV is defined as

i.e. the variance of the wavelet coefficients, which can be expressed in vector form as . While this definition holds independently from a possible parametric model underlying the time series , for the purpose of this work let us assume that the latter is generated from the parametric family of models , with unknown parameter vector denoted by . In order to make the link between the WV and an assumed stationary parametric model explicit, an alternative representation of this quantity is based on the Spectral Density Function (SDF) and is as follows:

with denoting the theoretical SDF and being the Fourier transform of the wavelet filters . The above equality is valid also when considering the theoretical spectral density of the wavelet coefficients themselves which, depending on the length of the wavelet filter, is defined even if the original time series is not stationary (see e.g. Percival and Walden, 2006). Although the results of the present section hold without any parametric assumption for , in this paper we will generally assume that the true WV will depend on a parametric family of models and use the notation for this purpose. We will make use of the notation whenever it is appropriate to explicitly highlight the link with the underlying parametric model.

Based on the above definitions, each parametric time series model has a corresponding theoretical WV vector which summarizes the information contained in the SDF or AutoCovariance Function (ACF) into few quantities () for a wide range of intrinsically stationary time series models (e.g. SARIMA and many state-space models). Considering this, when compared to the SDF or ACF, the information loss of the WV can be offset by its ability to adequately represent a considerably wide range of stationary and non-stationary time series. In this sense, aside from being discussed in Greenhall (1998) and Guerrier et al. (2013), Appendix LABEL:app_ident includes additional results proving that the WV is capable of adequately recovering information on time series models thereby supporting the usefulness of this quantity.

For the rest of this section however, let us disregard any parametric assumption for and simply assume that its corresponding wavelet coefficients are stationary. With this in mind, several estimators have been proposed for the WV, the main one being the standard unbiased estimator of the WV proposed by Percival (1995) and defined as

| (2.1) |

where is the length of the wavelet coefficient process at scale . The theoretical properties of this estimator were further studied in Serroukh et al. (2000) in which the conditions for its asymptotic properties are given. However, as highlighted by Mondal and Percival (2012a), the estimator of WV in (2.1) is not robust and can therefore become considerably biased in the presence of outliers or different forms of data contamination. For this reason they put forward a robust estimator of the WV (developed for Gaussian time series specifically affected by scale-based contamination) by making use of a log-transformation of the (squared) wavelet coefficients to apply standard M-estimation theory for location parameters. However, due to these transformations and the approximate corrections to reverse them, the asymptotic properties of the final estimator are not straightforward to define. Therefore, considering the robustness issues of the standard estimator and the “limitations” of the latter robust estimator, the following paragraphs put forward a new M-estimator of WV that overcomes these issues and, as shown in Appendix LABEL:sim_wv, performs generally better in finite sample settings.

2.1 M-Estimation of Wavelet Variance

Following the above discussion, this section generalizes the standard estimator of WV proposed in Percival (1995) to an M-estimator (Huber, 1964) which can also be made robust by choosing a bounded score function, thereby delivering an appropriate framework for inference on this quantity. Let us therefore re-express (2.1) as an M-estimator defined as follows:

| (2.2) |

where and is a score function (-function) which can be unbounded or bounded with respect to . For bounded -functions, popular choices include Huber’s function and Tukey’s Biweight function (see e.g. Hampel et al., 1986). Based on standard properties of M-estimators in dependent data settings (see e.g. Kunsch, 1984), the following proposition states the sufficient conditions under which the WV estimator has a bounded influence function (IF) and is therefore robust.

Proposition 2.1.

Assuming that is a strictly stationary process, the IF of the estimator of WV is bounded if is bounded.

Given this intuitive result whose proof can be found in Appendix LABEL:app:wv.if, we therefore intend to deliver an M-estimator of the form in (2.2) whose -function can be bounded and directly estimates the quantity of interest . The proposed approach is based on “Huber’s Proposal 2” which was presented in Huber (1981) and was aimed at the estimation of the scale parameter of the residuals in the linear regression framework. Without loss of generality, we assume that and consequently use this proposal by defining as the standardized wavelet coefficients, thereby defining the proposed estimator as:

| (2.3) |

where represents the weight function implied by the chosen -function and is a correction term to ensure Fisher consistency at the marginal distribution of the wavelet coefficients . Indeed, this correction term is defined as

where the latter expectation is taken over the marginal distribution of with variance . It can be noticed that, if the tuning constant , we have that and thereby delivering the estimator in (2.1) which implies that the tuning constant can be chosen to regulate the trade-off between robustness and efficiency of the resulting estimator. A discussion about the choice of the constant can be found in Appendix LABEL:choice_c which highlights how this constant can be implicitly chosen by defining the level of statistical efficiency required with respect to the standard estimator. As mentioned, the term depends on the marginal distribution of the stationary process which is assumed for the wavelet coefficients and on the specific weight function . The exact analytic form of this term therefore may be complicated to derive when considering distributions other than the Gaussian or other symmetric distributions.

Remark 2.1.

In the case where the wavelet coefficients are assumed to come from a Gaussian distribution, the correction term can be expressed as since it only depends on the value of the tuning constant , and can be found explicitly using the results of Dhrymes (2005). This is the case when the time series is itself Gaussian (see e.g. Percival, 2016, for a discussion) or can be assumed as an approximation given the averaging nature of the wavelet filter. On the other hand, if the marginal distribution of the wavelet coefficients is non-Gaussian, the term could eventually be numerically approximated once (based on the standardized simulated values from the assumed distribution with known or estimated parameters) and used for all scales and would need to be accounted for in the subsequent inference phase.

Having defined the M-estimator of WV in (2.3), let us now list a set of conditions which allow us to derive the asymptotic properties of this estimator. Firstly, letting represent the true WV at scale , we define the following conditions for the -function:

-

(C1)

The Bouligand derivative of is continuous almost everywhere.

-

(C2)

if and only if .

The first condition is a technical requirement that allows us to perform an expansion in order to represent in an explicit form (in addition to the Tukey Biweight function, for example, the Huber -function also respects this condition as shown in Lemma LABEL:bdiff in Appendix LABEL:app:asy.norm.wv). On the other hand, Condition (C2) requires the true WV to be identifiable through the chosen function . This condition is verified when choosing the Huber and Tukey Biweight -functions and assuming the wavelet coefficient process is Gaussian as shown in Appendix LABEL:app:wv.ident.

Given these technical conditions on the properties of the function , we can now study the process-related conditions for which we define the filtration where are i.i.d. random variables. With this definition we can now deliver the first process-related condition.

-

(C3)

is a strictly stationary process and can be represented as

where is an -valued measurable function such that is well defined.

Although not necessarily expressed in this form, Condition (C3) is commonly assumed when studying asymptotics within a time series setting and is respected by a very general class of time series models (see Wu, 2005). In our case, this condition is necessary in order to apply the functional dependence measure defined in Wu (2011).

At this stage, we further denote as being the coupled version of , where , with and also being i.i.d. random variables. Hence, the two processes and depend on filtrations that only differ by one element, i.e. and , therefore implying that for . Based on this definition, we can define the functional dependence measure given in Wu (2011):

where for . This dependence measure can be interpreted as the expected impact of the innovation on the moments of with respect to its “original” path given by . Using this defintion, we provide the final process-related condition.

-

(C4)

The process is such that .

This condition can be interpreted as a requirement for the expected difference between the fourth-order moments of the processes and to go to zero as , implying that the innovation has a limited impact in time on how much deviates from and, hence, the process is a “stable” process (see Wu, 2011).

Remark 2.2.

In the case where the chosen filter for the wavelet decomposition belongs to the Daubechies family, Conditions (C3) and (C4) can be placed directly on the dth-order difference of the process , that we will denote as , instead of the process . The advantage of this consists in the fact that, if the length of the wavelet filter at the first level is such that (where is the required differencing such that is stationary), then we only need to respect these conditions to ensure that all levels of decomposition respect them too. Indeed, in the case of a Daubechies wavelet filter, all levels of wavelet coefficients simply correspond to a deterministic linear combination of and we would therefore have and where and would be uniquely related to and constants and only depend on the chosen wavelet filter. For example, the process in Conditions (C3) and (C4) would be replaced by the process in the case of the Haar wavelet filter and hence we would have and .

We can now determine the asymptotic properties of the proposed M-estimator of WV in (2.3). For this reason, let us further define as the vector of wavelet coefficients at time and as the vector of estimated WV using the proposed M-estimator. Moreover, we define the projection operator (see Wu, 2011) as

This operator therefore represents a measure of how much the conditional expectation of a process can change once the immediately previous information is removed. As for the previously defined functional dependence measure, intuitively the projection operator should not be too sensitive if the underlying process is stable (in the sense of Wu, 2011).

Using the above definitions, we finally define the quantities and to deliver the following theorem on the asymptotic distribution of the proposed estimator .

Theorem 2.1.

The proof of this theorem can be found in Appendix LABEL:app:asy.norm.wv where the proofs for Condition (C2) (for Huber and Tukey Biweight functions in the Gaussian setting) and consistency of can also be found.

Remark 2.3.

The asymptotic covariance matrix is a long-run covariance matrix which can be estimated via different methods. For example, the moving block bootstrap, the batched-mean estimator (see Zhang and Wu, 2017) or the progressive batched-mean method generalized from the idea in Kim et al. (2013) are available methods for such a purpose. In the setting of this paper, we generally assume a parametric family for and, for this reason, the parametric bootstrap can also be considered.

Aside from studying the behaviour of the proposed M-estimator as a first-step estimator for the RGMWM (Section 4), as an additional exercise in Appendix LABEL:sim_wv we compare the behaviour of with the standard WV estimator and the median-type robust estimator in Mondal and Percival (2012b). In the latter simulation it appears clearly that the proposed M-estimator is the best alternative to the standard estimator in the uncontaminated setting and the best overall in the contaminated setting. Based on the robustness properties of the proposed estimator (for bounded -functions) and its asymptotic properties, this new estimator provides a suitable tool to perform robust scale-based analysis of variance for time series (see e.g. Percival and Walden, 2006, and references therein). More importantly, it delivers a first-step estimator with adequate properties based on which it is possible to perform robust parametric inference for a wide range of time series models as well as for large data sets as discussed in the following section.

3 Robust Generalized Method of Wavelet Moments

The properties of the proposed M-estimator of WV can be transferred directly within the GMWM framework (see Guerrier et al., 2013). Indeed, as suggested in Guerrier et al. (2014), one can replace the standard estimator used in the GMWM with a robust estimator which, in this case, is the proposed M-estimator allowing us to deliver the RGMWM defined as:

| (3.1) |

where is a symmetric positive definite weighting matrix chosen in a suitable manner (for example, one can choose where is a suitable estimator of , see Guerrier et al., 2013). Moreover, the robustness (bounded IF) of the RGMWM estimator is inherited from the robustness of as shown in Genton and Ronchetti (2003) in the indirect inference framework.

With this in mind, in the following paragraphs we list and discuss the conditions for the consistency and asymptotic normality of the RGMWM which summarize and reduce those in Guerrier et al. (2013) for the standard GMWM. For this reason, let us define as an estimator of and as the matrix spectral norm which allow us to state the following conditions:

-

(C5)

is compact.

-

(C6)

is continuous and differentiable for all .

-

(C7)

For , if and only if .

-

(C8)

.

Condition (C5) is commonly assumed but could be replaced by imposing other technical constraints if deemed more appropriate with respect to the parametric setting of reference (as proposed, for example, in Theorem 2.7 of Newey and McFadden, 1994). Condition (C6) is easy to verify and is respected for most intrinsically stationary processes. However, Condition (C7) is an essential one which is often hard to verify. In this case, with respect to the Haar wavelet filter (which is one of the most commonly used wavelet filters), the discussion in Guerrier et al. (2013) and the results in Greenhall (1998) support the identifiability of a large class of (latent) time series models and are extended in Appendix LABEL:app_ident as well as in Guerrier and Molinari (2016) thereby relaxing Condition (C7). Finally, Condition (C8) addresses the choice of the weighting matrix and its corresponding estimator . In this perspective, the RGMWM is consistent for any matrix that is symmetric positive definite and, therefore, one needs to select an estimator that converges to the chosen matrix . A final condition which has not been stated is the consistency of the WV estimator which is implied by Conditions (C2) to (C4) as seen in Section 2.

With these conditions we can now state the consistency of the RGMWM estimator .

The proof of this proposition can be found in Appendix LABEL:app_rgmwm_cons. With this result, we can finally give the conditions for the asymptotic normality of . For this reason, let us define

which exists for a wide class of time series models (see e.g. Zhang, 2008). Using this definition, we can state these final conditions.

-

(C9)

.

-

(C10)

exists and is non-singular.

Condition (C9) is a standard regularity condition while Condition (C10) is also usually assumed since it depends on the specific parametric model from which the time series is generated and cannot therefore be verified in general. Since is non-singular by definition, we have that this condition relies mainly on the non-singularity of (the first rows of) which is used, for example, to discuss Condition (C7) in Appendix LABEL:app_ident. Finally, as for the results of consistency in Proposition 3.1, an additional condition for the asymptotic normality of the RGMWM is the asymptotic normality of which is stated in Theorem 2.1. Having discussed these conditions, we can use them to state the following lemma.

Lemma 3.1.

The proof of Lemma 3.1 is provided in Appendix LABEL:app_rgmwm_norm. With the above results on the asymptotic properties of the RGMWM, the next paragraphs discuss some practical and theoretical advantages of the proposed robust framework.

3.1 Discussion: Practical Properties and Extensions

The RGMWM delivers various advantages that are mainly due to its two-step nature which allows it to benefit from the generality of the M-estimation framework presented in Section 2.1. A first advantage resides in the fact that the correction term needed to ensure Fisher consistency of the estimator defined in (2.3) only depends on the marginal distribution of the wavelet coefficients which, if assumed to be Gaussian, can have an explicit form (for common -functions) and only needs to be computed once for all levels . A main advantage however resides in the fact that the dimension of the auxiliary parameter vector is always reasonable since in general which allows to make use of all the scales of WV without the need to select specific moments. This is not the case, for example, for Generalized Method of Moments (GMM) estimators where moment-selection is an important issue since, according to the model that is being estimated, the choice should fall on all moments (which can be highly impractical) or on moments that are more “informative” than others (see e.g. Andrews, 1999). The RGMWM on the other hand can make use of all the possible scales of WV even for extremely large sample sizes, allowing it to preserve its statistical efficiency while gaining in terms of computational speed which is approximately of order while for the MLE, for example, it is roughly . Appendix LABEL:sim_compeff reports results on the computational time required to estimate the parameters of some (complex) models for sample sizes up to 10 million, confirming the considerable computational advantage of the RGMWM over both standard and robust alternatives. Moreover, the wavelet decomposition (and consequent variance estimation) is computationally efficient based on well-known algorithms (see e.g. Rioul and Duhamel, 1992) and more recent approaches (see e.g. Stocchi and Marchesi, 2018) allowing the RGMWM to be scalable. Nevertheless, a possible limitation of this approach is that it requires a large enough sample size to estimate more complex models (although, for example, it can already estimate four-parameter models with a sample size of if using a Haar wavelet filter).

For model comparison purposes, using its “model-independent” nature based on the robust weights of the proposed M-estimator in (2.3), the latter allows to graphically compare potential candidate models on the basis of the estimated WV as is routinely done, for example, with error characterization in the field of signal processing (see e.g. El-Sheimy et al., 2008). Indeed, decreasing linear trends in the log-log plot of the WV can indicate the presence of white noise or rounding-error models while increasing linear trends can indicate the presence of non-stationary components such as drifts and random walks whereas slight “bumps” in the plot can indicate the presence of ARMA components. In Section 5, for example, the graphical display of the WV is used to detect and check the fit of the model when analysing a real data set on personal saving rates. Moreover, continuing with its model comparison advantages, the RGMWM estimator also delivers a general framework for robust goodness-of-fit tests and model selection. Indeed, the objective function in (3.1) can be used as a statistic for a goodness-of-fit test (Sargan-Hansen test or -test) as proposed by Hansen (1982), where the asymptotic distribution under the null hypothesis is chi-squared with degrees of freedom. Moreover, model selection criteria can also be built based on the (penalized) GMM objective function which in the RGMWM setting would be given by

| (3.2) |

where and denote respectively the estimated parameter vector and weighting matrix for the model within a set of candidate models, while is a possible penalty term. Penalized objective functions have been proposed for model and moment selection for GMM estimators such as, for example, Andrews (1999) and successively Andrews and Lu (2001) who proposed penalty terms that reflect the number of moment conditions or Zhang and Guerrier (2019) who derived a penalty term using the covariance penalty criterion of Efron (2004). Nevertheless, since these model selection criteria only rely on a consistent estimator for the model’s parameters , a robust version is (almost) readily available by using the RGMWM framework. Moreover, the estimator in (3.2) can be made model-independent by choosing (e.g. based only on the empirical WV) making model comparison computationally more efficient. While the -test statistic will be used in the analysis of real data in Section 5, the study of a possible implementation of a robust model selection criterion is left for further research.

Finally, aside from providing the basis for model-independent outlier-detection (which can be of great importance for fault-detection algorithms, see for example Guerrier et al., 2012, and references therein), another advantage of the RGMWM estimator is that it can easily be extended to more complex settings such as multivariate time series (see e.g. Xu et al., 2019) or to random fields (see e.g. Mondal and Percival, 2012b, a) thereby delivering a computationally efficient framework for robust inference in these settings as well.

4 Simulation Studies

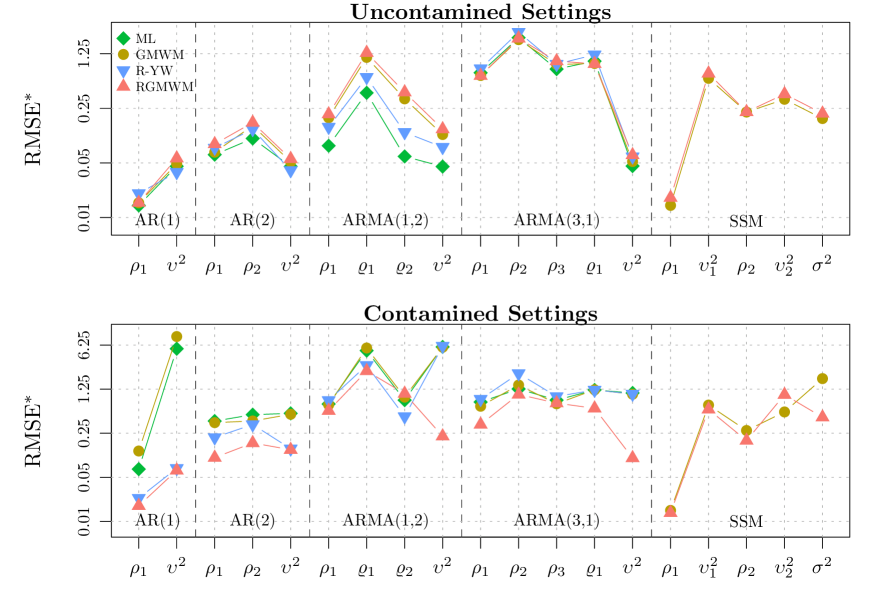

The aim of this section is to show that the RGMWM has a reasonable performance in settings where there is no data contamination and has a better performance than the classical (and possibly robust) alternatives when the data are contaminated. Concerning the robust alternatives, there is a lack of implemented and generally available (or usable) robust methods for parametric inference on time series models. For this reason, we were only able to successfully implement two robust estimators with which to compare the proposed RGMWM estimator: the Yule-Walker estimator based on the robust autocovariance estimator (YW) (as used for example in Sarnaglia et al., 2010) and the indirect inference estimator based on the YW estimator (as proposed in Genton and Ronchetti, 2003) using a Tukey Biweight function with tuning constant (chosen based on preliminary simulation studies in order to be highly robust). In the latter case, AR() models were used as auxiliary models with where, in this case, represents the number of parameters in the models of interest (excluding the innovation variance parameter). Since the YW estimator is appropriate for autoregressive models while the indirect inference estimator is used for all other models, we will denote both with a common acronym i.e. R-YW (for Robust Yule-Walker based estimators). On the other hand, the GMWM and RGMWM estimators are made available through the open-source R package gmwm222The gmwm package can be downloaded from https://github.com/SMAC-Group/gmwm. where the default options are the Haar wavelet filter and a diagonal matrix for the weighting matrix with elements proportional to the estimated variance of (which was used for the simulations also to make more reasonable comparisons with the indirect inference estimators which were based on the identity matrix). The Tukey Biweight was used also for the RGMWM with tuning constant based on an asymptotic efficiency of 60% thereby guaranteeing high robustness of the resulting estimator.

For the simulation studies different types of contamination were used, going from scale-contamination to additive and replacement outliers as well as patchy outliers and level-shifts. Innovation-type contamination was not considered since it does not affect the estimators much (see Maronna et al., 2006, 2019, for an overview of different contamination settings). We denote the proportion of contaminated observations with and the size of contamination (i.e. the variance of the observations which are added to the uncontaminated observations) with . Finally, when dealing with level-shifts, we denote as the size of the shift in level.

The performance of these estimators is investigated on the following models and contamination settings:

-

•

AR(1): a zero-mean first-order autoregressive model with parameter vector , scale-based contamination at level , and ;

-

•

AR(2): a zero-mean second-order autoregressive model with parameter vector , isolated outliers, and ;

-

•

ARMA(1,2): a zero-mean autoregressive-moving average model with parameter vector , and level-shift contamination with , and ;

-

•

ARMA(3,1): a zero-mean autoregressive-moving average model with parameter vector , patchy outliers, and ;

-

•

SSM: a state-space model interpreted as a composite (latent) process in certain engineering applications. This model is defined as

with parameter vector

isolated outliers, and .

To measure the statistical performance of the estimators we choose to use a robust and relative version of the Root Mean Squared Error (RMSE) defined as follows

with representing the median, the median absolute deviation and and representing the element of the estimated and true parameter vectors respectively. Finally, for each simulation, the number of simulated samples is 500 while the sample size is which delivers scales for the GMWM-type estimators.

Figure 1 displays the (logarithm of the) RMSE* of the estimators in both uncontaminated and contaminated settings for all the models presented above. When considering the AR(1) and AR(2) and ARMA(3,1) models, the RGMWM does not lose much in uncontaminated settings while it performs generally as well or better than the R-YW estimator in contaminated ones, especially concerning the variance parameter in the ARMA(3,1). As for the ARMA(1,2) model, the RGMWM is not as efficient as the others in the uncontaminated case while it adequately bounds the influence of outliers in contaminated ones, performing generally better than the R-YW estimator, especially for the variance parameter as in the case of the ARMA(3,1) model. For the SSM model, standard estimators in their default implementation did not appear to be numerically stable while, to the best of our knowledge, robust alternatives have never been implemented. From Figure 1, it can be seen how the RGMWM is extremely close to the GMWM in uncontaminated settings while it remains more stable than the GMWM in the contaminated ones. When considered jointly with the additional simulation study in Appendix LABEL:sim_compeff, this simulation exercise shows that the RGMWM provides a computationally efficient and numerically stable method to robustly estimate the parameters of many linear state-space models which, to date, has been almost unfeasible in practice with alternative robust estimators. Indeed, Appendix LABEL:sim_compeff illustrates the computational efficiency of the RGMWM for time series models with a moderately high number of parameters for sample sizes of for which the RGMWM is computed in just over a minute, denoting the added value of this approach since these models and sample sizes are extremely common, for example, in the natural sciences and engineering. As a final note, since this simulation study does not use a full weighting matrix for , the efficiency of the (R)GMWM could be improved by choosing an alternative matrix.

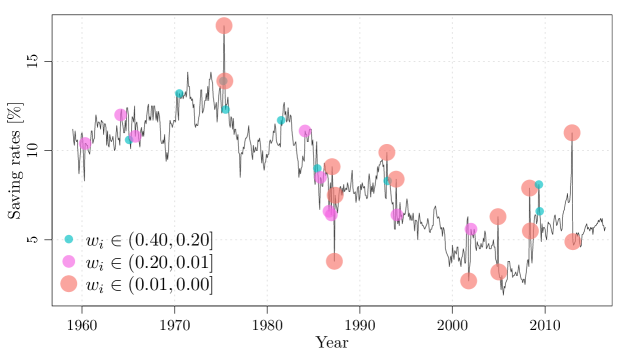

5 Application: Personal Saving Rates

Having highlighted the properties of the RGMWM in a controlled simulated setting, in this section we conclude this work by presenting the results when using the RGMWM for an analysis on real data concerning personal saving rates. In addition, in Appendix LABEL:iner.sens we present the results of an analysis on the measurement error issued from an inertial sensor based on a calibration sample of size that requires the estimation of a state-space model with 6 parameters. Indeed, the wide class of intrinsically stationary models for which the RGMWM can be used allows it to be employed in a large variety of applications where outliers and other types of data contamination can often occur. As mentioned above, in this section the RGMWM will be used to analyse data consisting in the monthly seasonally adjusted Personal Saving Rates (PSR) from January 1959 to May 2015 provided by the Federal Reserve Bank of St. Louis333U.S. Bureau of Economic Analysis, Personal Saving Rate [PSAVERT], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/PSAVERT. The study of PSR is an essential part of the overall investigation on the health of national and international economies since, within more general economic models, PSR can greatly impact the funds available for investment which in turn determine the productive capacity of an economy. Understanding the behaviour of PSR is therefore an important step in correct economic policy decision making. In this sense, Slacalek and Sommer (2012) study the factors behind saving rates and investigate different models which, among others, are compared to the random-walk-plus-noise (local level) model (RWN). As opposed to the latter model, various time-varying models are proposed in the literature to explain precautionary PSR together with risk aversion in the light of different factors such as financial shocks or others (see, for example, Videras and Wu, 2004; Brunnermeier and Nagel, 2008). Nevertheless, as emphasized in Pankratz (2012), modelling the time series with a stationary model, or a dth-order non-stationary model such as an ARIMA, can be useful under many aspects such as, for example, to understand if a dynamic model is needed for forecasting and, if so, what kind of model is appropriate.

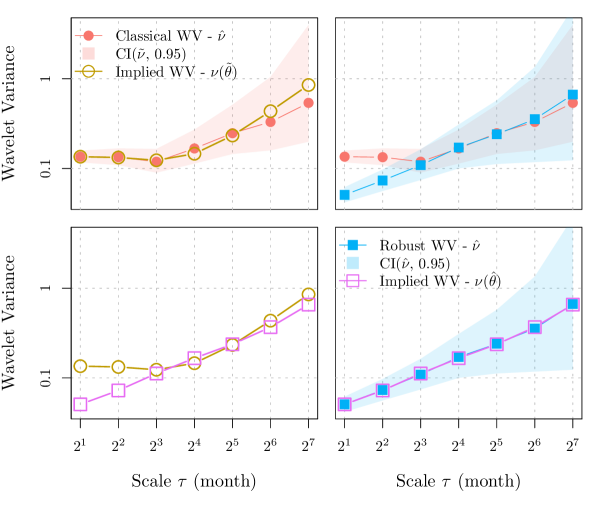

In this example, we consider the RWN model and we use the WV log-log plot and a -test (see Section 3.1) to understand what kind of model could fit the time series. Considering both the visual fit of the WV of the candidate models in the plots as well as the p-values of the -tests (for which the null hypothesis is that the model fits the data well), we find that a random walk plus an ARMA(2,1) appears to be a good fit and therefore, in this case, we have that the “noise” in the RWN model is an ARMA(2,1) (-test p-values are 0.109 and 0.279 for GMWM and RGMWM respectively). This can be seen in Figure 2 where, in the top part, the saving rate time series is represented along with the identified outliers and, in the bottom part, we see the log-log representation of the classic and robust estimated and model-implied WV respectively. Indeed, for the bottom part, the diagonal plots show the classic and robust estimations respectively, each with the estimated WV and the WV implied by the estimated RWN model; when the difference in the two lines lies within their confidence intervals, the chosen model can be considered as adequate. The off-diagonal plots compare the classic and robust estimated WV (upper off-diagonal) and the WV implied by the GMWM and RGMWM model parameter estimates (lower off-diagonal).

It can be seen how there is a significant difference between the standard and robust WV estimates, especially at the first scales where the confidence intervals of the estimated WV do not overlap (upper off-diagonal plot). This leads to a difference in the model-implied WV whose parameters have been estimated through the GMWM and RGMWM (lower off-diagonal plot).

The estimated parameters of the RWN model using the GMWM and RGMWM are given in Table 1 along with their respective confidence intervals.

| GMWM | RGMWM | |||

|---|---|---|---|---|

| Estimate | CI(, 95%) | Estimate | CI(, 95%) | |

There are two main differences between the two estimations: (i) the estimates of the first autoregressive parameter and innovation variance are significantly different; (ii) the second autoregressive parameter is not significant using the GMWM. These differences highlight how the conclusions concerning parameter values and model selection can considerably change when outliers are present in the data. Indeed, the choice of the model would then affect the decisions taken towards the selection of appropriate causal and dynamic models to better explain the behaviour of saving rates. The selected model based on the robust fit can in fact be interpreted as a sum of latent models along the lines given in Slacalek and Sommer (2012) where the ARMA(2,1) can be seen as a sum of two AR(1) models (see Granger and Morris, 1976) where each of them represents, for example, the reaction of PSR to changes in uncertainty (affected by unemployment) and interest rates, respectively, while the random walk describes the continuous fluctuations of target wealth which also drives PSR.

The additional benefit of the RGMWM, and more specifically of the proposed M-estimator of WV, is also to deliver weights that allow to identify outliers which may not be visible simply by looking at the time series. As shown in the top part of Figure 2, the outliers identified by the RGMWM can be interpreted in the light of the national and global economic and political events. Limiting ourselves to the major identified outliers, the first one corresponds to a rise in the precautionary savings in the aftermath of the OPEC oil crisis and the 1974 stock market crash. In the months following October 1987 we can see an instability in the PSR with a rise and sudden fall linked to the “Black Monday” stock market crash which added to the savings and loans crisis which lasted to the early 1990s. This period also saw an economic recession where a rise in the saving rates, highlighted by the presence of high outliers, led to a drop in aggregate demand and bankruptcies. Finally, the various financial crises of the 21st century led to sudden and isolated rises in PSR as indicated again by the outliers.

Acknowledgements

We would like to thank Stephen Portnoy and Roger Koenker for their valuable inputs and suggestions throughout the development of this work. We would also like to thank Fabio Trojani for his interesting and helpful considerations. Moreover, we would like to thank Donald Percival and Debashis Mondal for sharing wavelet variance code and some data for the case studies presented in the paper and in its supplemental materials. Moreover, we thank Charles Greenhall for his precious insight into the discussion on the injective relationship between the spectral density and the wavelet variance. Finally, we would like to thank Mucyo Karemera, Marc-Olivier Boldi, Samuel Orso and Marco Avella for discussing the results of this work with us.

References

- Abry et al. (2018) Patrice Abry, Gustavo Didier, et al. Wavelet estimation for operator fractional brownian motion. Bernoulli, 24(2):895–928, 2018.

- Andrews (1999) D. Andrews. Consistent moment selection procedures for generalized method of moments estimation. Econometrica, 67(3):543–563, 1999.

- Andrews and Lu (2001) D. W.K. Andrews and B. Lu. Consistent model and moment selection procedures for GMM estimation with application to dynamic panel data models. Journal of Econometrics, 101:123–164, 2001.

- Bakalli et al. (2018) G. Bakalli, A. Radi, S. Nassar, S. Guerrier, Y. Zhang, and R. Molinari. A two-step computationally efficient procedure for imu classification and calibration. In 2018 IEEE/ION Position, Location and Navigation Symposium (PLANS), pages 534–540, April 2018.

- Brunnermeier and Nagel (2008) M. K. Brunnermeier and S. Nagel. Do wealth fluctuations generate time-varying risk aversion? micro-evidence on individuals’ asset allocation (digest summary). American Economic Review, 98(3):713–736, 2008.

- Clausen et al. (2018) P. Clausen, J. Skaloud, R. Molinari, J. Lee, and S. Guerrier. Use of a new online calibration platform with applications to inertial sensors. IEEE Aerospace and Electronic Systems Magazine, pages 30–36, 2018.

- Dhrymes (2005) J. Dhrymes. Moments of truncated (normal) distributions. Unpublished note, 10:95–107, 2005.

- Duffie and Singleton (1993) D. Duffie and K. J. Singleton. Simulated moments estimation of markov models of asset prices. Econometrica: Journal of the Econometric Society, pages 929–952, 1993.

- Durbin and Koopman (2012) J. Durbin and S. J. Koopman. Time series analysis by state space methods. Number 38. Oxford University Press, 2012.

- Efron (2004) B. Efron. The Estimation of Prediction Error. Journal of the American Statistical Association, 99(467):619–632, 2004.

- El-Sheimy et al. (2008) N. El-Sheimy, H. Hou, and X. Niu. Analysis and Modeling of Inertial Sensors using Allan Variance. IEEE Transactions on Instrumentation and Measurement, 57(1):140–149, January 2008.

- Foufoula-Georgiou and Kumar (2014) E. Foufoula-Georgiou and P. Kumar. Wavelets in geophysics, volume 4. Academic Press, 2014.

- Gallant and Tauchen (1996) A Ronald Gallant and George Tauchen. Which moments to match? Econometric Theory, pages 657–681, 1996.

- Gallegati (2012) M. Gallegati. A wavelet-based approach to test for financial market contagion. Computational Statistics & Data Analysis, 56(11):3491–3497, 2012.

- Genton and Ronchetti (2003) M. G. Genton and E. Ronchetti. Robust indirect inference. Journal of the American Statistical Association, 98:1–10, 2003.

- Gourieroux et al. (1993) C. Gourieroux, A. Monfort, and E. Renault. Indirect Inference. Journal of Applied Econometrics, 8(S1):S85–S118, 1993.

- Granger and Morris (1976) C. W. J. Granger and M. J. Morris. Time series modelling and interpretation. Journal of the Royal Statistical Society. Series A (General), pages 246–257, 1976.

- Greenhall (1998) C. A. Greenhall. Spectral ambiguity of allan variance. IEEE Transactions on Instrumentation and Measurement, 47(3):623–627, 1998.

- Guerrier and Molinari (2016) S. Guerrier and R. Molinari. On the identifiability of latent models for dependent data. Submitted manuscript, Full text: http://arxiv.org/abs/1607.05884, 2016.

- Guerrier et al. (2012) S. Guerrier, A. Waegli, J. Skaloud, and M. P. Victoria-Feser. Fault detection and isolation in multiple mems-imus configurations. Aerospace and Electronic Systems, IEEE Transactions on, 48(3):2015–2031, 2012.

- Guerrier et al. (2013) S. Guerrier, J. Skaloud, Y. Stebler, and M. P. Victoria-Feser. Wavelet-variance-based estimation for composite stochastic processes. Journal of the American Statistical Association, 108(503):1021–1030, 2013.

- Guerrier et al. (2014) S. Guerrier, R. Molinari, and M. P. Victoria-Feser. Estimation of Time Series Models via Robust Wavelet Variance. Austrian Journal of Statistics, pages 267–277, 2014.

- Hampel (1974) F. R. Hampel. The influence curve and its role in robust estimation. 69:383–393, 1974.

- Hampel et al. (1986) F. R. Hampel, E. M. Ronchetti, P. J. Rousseeuw, and W. A. Stahel. Robust Statistics: The Approach Based on Influence Functions. John Wiley, New York, 1986.

- Hansen (1982) L. P. Hansen. Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, pages 1029–1054, 1982.

- Huber (1964) P. J. Huber. Robust estimation of a location parameter. 35:73–101, 1964.

- Huber (1981) P. J. Huber. Robust Statistics. John Wiley, New York, 1981.

- Jia et al. (2015) X. Jia, H. An, W. Fang, X. Sun, and X. Huang. How do correlations of crude oil prices co-move? a grey correlation-based wavelet perspective. Energy Economics, 49:588–598, 2015.

- Kim et al. (2013) Y. Kim, S. N. Lahiri, and D. J. Nordman. A progressive block empirical likelihood method for time series. Journal of the American Statistical Association, 108(504):1506–1516, 2013.

- Künsch (1984) H. Künsch. Infinitesimal robustness for autoregressive processes. 12:843–863, 1984.

- Kunsch (1984) H. Kunsch. Infinitesimal robustness for autoregressive processes. The Annals of Statistics, pages 843–863, 1984.

- Maronna et al. (2006) R. A. Maronna, R. D. Martin, and V. J. Yohai. Robust Statistics: Theory and Methods. Wiley, Chichester, West Sussex, UK, 2006.

- Maronna et al. (2019) Ricardo A Maronna, R Douglas Martin, Victor J Yohai, and Matías Salibián-Barrera. Robust statistics: theory and methods (with R). John Wiley & Sons, 2019.

- McFadden (1989) D. McFadden. A method of simulated moments for estimation of discrete response models without numerical integration. Econometrica: Journal of the Econometric Society, pages 995–1026, 1989.

- Mondal and Percival (2012a) D. Mondal and D. B. Percival. M-estimation of wavelet variance. Annals of the Institute of Statistical Mathematics, 64(1):27–53, 2012a.

- Mondal and Percival (2012b) D. Mondal and D. B. Percival. Wavelet variance analysis for random fields on a regular lattice. IEEE Transactions on Image Processing, 21(2):537–549, 2012b.

- Muler et al. (2009) N. Muler, D. Peña, and V. J. Yohai. Robust estimation for ARMA models. The Annals of Statistics, 37:816–840, 2009.

- Newey and McFadden (1994) W. K. Newey and D. McFadden. Large sample estimation and hypothesis testing. Handbook of econometrics, 4:2111–2245, 1994.

- Pankratz (2012) A. Pankratz. Forecasting with dynamic regression models, volume 935. John Wiley & Sons, 2012.

- Percival (1995) D. B. Percival. On estimation of the wavelet variance. Biometrika, 82(3):619–631, 1995.

- Percival (2016) D. B. Percival. A wavelet perspective on the allan variance. IEEE Transactions on Ultrasonics, Ferroelectrics, and Frequency Control, 63(4):538–554, 2016.

- Percival and Walden (2006) D. B. Percival and A. T. Walden. Wavelet Methods for Time Series Analysis, volume 4. Cambridge University Press, 2006.

- Radi et al. (2019) A. Radi, G. Bakalli, S. Guerrier, N. El-Sheimy, A. B. Sesay, and R. Molinari. A multisignal wavelet variance-based framework for inertial sensor stochastic error modeling. IEEE Transactions on Instrumentation and Measurement, 2019. doi: 10.1109/TIM.2019.2899535. In press.

- Rioul and Duhamel (1992) Olivier Rioul and Pierre Duhamel. Fast algorithms for discrete and continuous wavelet transforms. IEEE transactions on information theory, 38(2):569–586, 1992.

- Sarnaglia et al. (2010) Alessandro José Queiroz Sarnaglia, Valderio Anselmo Reisen, and Céline Lévy-Leduc. Robust estimation of periodic autoregressive processes in the presence of additive outliers. Journal of multivariate analysis, 101(9):2168–2183, 2010.

- Serroukh et al. (2000) A. Serroukh, A. T. Walden, and D. B. Percival. Statistical properties and uses of the wavelet variance estimator for the scale analysis of time series. Journal of the American Statistical Association, 95(449):184–196, 2000.

- Shumway and Stoffer (2013) R. H. Shumway and D. S. Stoffer. Time Series Analysis and its Applications. Springer Science & Business Media, 2013.

- Slacalek and Sommer (2012) J. Slacalek and M. Sommer. What drives household saving? Unpublished note, 10:95–107, 2012.

- Smith (1993) A. A. Smith. Estimating nonlinear time-series models using simulated vector autoregressions. Journal of Applied Econometrics, 8(S1):S63–S84, 1993.

- Stocchi and Marchesi (2018) Marco Stocchi and Michele Marchesi. Fast wavelet transform assisted predictors of streaming time series. Digital Signal Processing, 77:5–12, 2018.

- Videras and Wu (2004) J. Videras and S. Wu. The behavioral effects of financial shocks. 2004.

- Wu (2005) W. Wu. Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences, 102(40):14150–14154, 2005.

- Wu (2011) W. Wu. Asymptotic theory for stationary processes. Statistics and its Interface, 4(2):207–226, 2011.

- Xie and Krishnan (2013) S. Xie and S. Krishnan. Wavelet-based sparse functional linear model with applications to eegs seizure detection and epilepsy diagnosis. Medical & biological engineering & computing, 51(1-2):49–60, 2013.

- Xu et al. (2019) H. Xu, S. Guerrier, R. Molinari, and M. Karemera. Multivariate signal modelling with applications to inertial sensor calibration. IEEE Transactions on Signal Processing, 67(19):5143–5152, 2019.

- Zhang and Wu (2017) D. Zhang and W. Wu. Gaussian approximation for high dimensional time series. The Annals of Statistics, 45(5):1895–1919, 2017.

- Zhang (2008) N. F. Zhang. Allan variance of time series models for measurement data. Metrologia, 45:549–561, 2008.

- Zhang and Guerrier (2019) X. Zhang and S. Guerrier. Covariance Penalty Based Model Selection Criterion for Indirect Estimators. Submitted Working Paper, pages 1–30, 2019.

- Ziaja et al. (2016) Aleksandra Ziaja, Ifigeneia Antoniadou, Tomasz Barszcz, Wieslaw J Staszewski, and Keith Worden. Fault detection in rolling element bearings using wavelet-based variance analysis and novelty detection. Journal of Vibration and Control, 22(2):396–411, 2016.

See pages - of suppmat.pdf