First-Order Algorithms for Constrained Nonlinear Dynamic Games

Abstract

This paper presents algorithms for non-zero sum nonlinear constrained dynamic games with full information. Such problems emerge when multiple players with action constraints and differing objectives interact with the same dynamic system. They model a wide range of applications including economics, defense, and energy systems. We show how to exploit the temporal structure in projected gradient and Douglas-Rachford (DR) splitting methods. The resulting algorithms converge locally to open-loop Nash equilibria (OLNE) at linear rates. Furthermore, we extend stagewise Newton method to find a local feedback policy around an OLNE. In the of linear dynamics and polyhedral constraints, we show that this local feedback controller is an approximated feedback Nash equilibrium (FNE). Numerical examples are provided.

keywords:

Constrained Dynamic Games; Projected Gradient; Douglas-Rachford Algorithm., ,

1 Introduction

This paper describes numerical algorithms for finite-horizon, constrained, discrete-time dynamic games with full information. In this setup, agents with different objectives but coupled constraints choose inputs to a dynamic system. Due to coupling in the constraints, we examine generalized Nash equilibrium problems (GNEP). The formulation and all results in this paper automatically apply to standard Nash equilibrium problems when the action constraints are not coupled. The dynamic system can be naturally discrete-time or emerge from discretization of a differential game [1, 2, 3, 4]. Dynamic games have many applications including pursuit-evasion [5], active-defense [6, 7], economics [8] and the smart grid [9]. Despite a wide array of applications, the computational methods for dynamic games are considerably less developed than the single-agent case of optimal control.

Our previous work [10] extended stagewise Newton algorithm and differential dynamic programming (DDP), which originated from single-agent optimal control, to unconstrained non-zero-sum dynamic games. We proved that the methods converge quadratically to an open-loop Nash equilibrium (OLNE), the resulting closed-loop policies are local feedback -Nash equilibria (FNEs), and that both algorithms enjoyed a linear complexity with respect to the horizon. This paper generalizes [10] to the case of constrained dynamic games.

Below we review generalized Nash equilibrium problems and their relation to variational inequalities. Additionally, we describe projected gradient and Douglas-Rachford splitting methods, which can solve variational inequalities (VI) problems. For a more detailed review of relevant game theory literature, see [10].

General Nash equilibrium problems (GNEP) study games with constraints that couple different players’ strategies [11]. For games with continuous variables, necessary conditions for the solution of a GNEP can be formulated as a variational inequality (VI). These inequalities can be solved via generic VI methods or classic feasibility problem methods, such as Newton’s method [12] or others [13]. First order VI methods require calculation of gradients, while second order methods require inverting Hessian matrices. Naïve implementations of these calculations respectively require and steps, where is the number of stages. Our stagewise Newton method from [10] exploits dynamic structure to compute gradients, Hessians, and inverse Hessians with complexity. Below, we describe two VI algorithms in greater detail.

Projected gradient algorithms alternate between taking gradient descent steps and projecting onto constraints. They have been well studied for optimization [14] and variational inequality (VI) problems [15], and proven to converge linearly in both cases. This paper describes how the projected gradient method can be applied to constrained dynamic games, including convergence conditions and convergence rate of the algorithm.

Douglas-Rachford (DR) splitting methods alternate between solving two VI problems when applied to constrained game problems. Typically one problem corresponds to an unconstrained optimization or game problem, while the other corresponds to projection onto constraints [15]. As with the projected gradient method, the DR method converges linearly [16]. In optimization, the DR method is closely related to the alternating direction method of multipliers (ADMM) [17] and has been extended to (single-agent) optimal control problems [18, 19].

1.1 Our Contribution

We describe efficient implementations of projected gradient and Douglas-Rachford splitting methods for computing OLNEs of constrained dynamic games. In both cases, we show how to exploit temporal structure to achieve iterations of complexity. Finally, we adapted the stagewise Newton to solve for a feedback policy around OLNE trajectories. In the case of games with linear dynamics and polyhedral constraints, we show that it is an approximate (generalized) feedback Nash equilibrium.

1.2 Paper Outline

The paper can be divided into three major parts. The first part, Section 2, describes the problem formulations and solution concepts. The second part, Section 3 on the projected gradient method and Section 4 on the Douglas-Rachford splitting method, describe methods for computing local OLNE solutions. The third part focuses on local feedback Nash equilibria. It includes Section 5, which lays the groundwork, and Section 6, which analyzes local FNE for constrained dynamic games. Numerical examples are offered in Section 7 and future extensions discussed in Section 8.

2 Problem Formulations and Solution Concepts

We introduce some standard notation, formulate the constrained dynamic game problems, and introduce the associated solution concepts.

2.1 Dynamic and Static Game Formulation

The main problem of interest is a constrained, deterministic, full-information dynamic game with players of the form below.

Problem 1.

Constrained nonlinear dynamic game

Each player aims to minimize their own cost

| (1) |

Subject to dynamic constraints and extra constraints

| s.t. | (2a) | |||

| (2b) | ||||

| (2c) | ||||

| (2d) | ||||

Here, is the starting point for a game. When , we call it the full game, and , a subgame . Here, the state of the system at time is denoted by . Player ’s action at time is given by . The vector of all players’ actions at time is denoted . The cost for player at time is . This encodes the fact that the cost for each player can depend on the actions of all the players. We assume that the costs are twice differentiable with locally Lipschitz Hessians.

In later analysis, some other notation is helpful. The actions of player from time to in a vector is denoted . The vector of actions other than those of player from time to is denoted by . The vector of states from time to is denoted while the vector of all players’ actions from to is given by . denote all states and actions collected over all time in a vector.

We denote the set of trajectories satisfying the dynamic constraint with given as and the extra constraints . Feasible sets of state and actions are denoted and for subgame . The subscript or initial condition can be suppressed later in this paper indicating values for the full game.

Note that the dynamics are deterministic, the cost for each player in a subgame can be expressed as a function of all following actions and given state , i.e., . The dynamics are implicitly substituted to eliminate when we use such notation. Problem 1 can be written in an equivalent static game form for ease of notation and analysis.

2.2 Solution Concept of Games

We focus on local open-loop Nash equilibria and feedback Nash equilibria in this paper. Technically, we are studying generalized Nash equilibria, since players’ actions can be coupled in the constraints [20]. However, for simplicity, we will refer to them as Nash equilibria.

Definition 1.

Problem 1 and Problem 2 are equivalent in terms of a local OLNE. An OLNE does not dynamically adjust if the state changes. In contrast, a feedback Nash equilibrium for dynamic games Problem 1 requires players to be able to measure the state at each step and execute a step-by-step policy to account for changes in the state. FNE has the valuable property of being subgame perfect [21].

Definition 2.

(Local) feedback Nash equilibrium

A collection of feedback policies , with is said to be a feedback Nash equilibrium of the full game if no player can benefit from changing their policy unilaterally for any subgame , i.e.,

| (5) |

where indicates the total cost of player when all players follow policy for subgame . All policies should be compatible with the constraints. Furthermone, if (5) only holds around and the resulting trajectories remain in a neighborhood of , it is called a local feedback Nash equilibrium (local-FNE).

This definition only applies to Problem 1 because Problem 2 does not have explicit state information. In this definition, must be an OLNE since (5) could be violated at otherwise. Thus, we focus on local FNEs that are built around OLNEs in this paper. Ideally, an FNE is solved via the Bellman recursion, which originated from optimal control problems, and was extended to dynamic games [22, 21]. Instead of solving the minimizing action at each stage, equilibrium of stagewise games are computed via the following recursion

| (6a) | ||||

| (6b) | ||||

| (6c) | ||||

| (6d) | ||||

Here and are referred to as equilibrium value functions for player at time step . Note that (6c) defines a parametric static game in terms of the variable at step and parameterized by . For dynamic games with quadratic costs, linear dynamics and polyhedral constraints, the analytical FNE can be obtained in theory as described in Section 5 and Appendix B. In general, this backward recursion is intractable, so we focus on solving it approximately around an OLNE trajectory. Note that the game ends at , and setting is only for ease of notation and that by construction, for .

2.3 Variational Inequality (VI) Formulation

For continuous-variable games, variational inequalities (VIs) give a necessary condition for the solution of generalized Nash equilibrium problems [15]. We describe the VI formulation of the full game, which starts at . The formulation for games starting at is simular. We omit the dependency on , stack all of the gradient vector and define

| (7) |

Note that has the same dimension as . When the dependence on must be emphasized, we denote the corresponding function by . The VI formulation of the full game, Problem 2, is as following.

Problem 3.

VI formulation of static game

| (8) |

Note that is the solution of VI formulation is only necessary to being a local OLNE to Problem 2. To ensure sufficiency, it should also be checked if each player’s action is a local minimizer to their objective. Two sufficient conditions for player ’s cost to be locally minimized are 1) and 2) and is locally convex. If is a local minimizer for all players, then it is also a local OLNE solution to 2. We refer to this procedure as playerwise local minimizer check.

2.4 Sufficient Conditions for Existence of Solutions

A commonly applicable sufficient condition for a solution of the VI problem to exist is that is locally strongly monotone and is convex. Another sufficient condition is that, is compact convex and is continuous on [15]. In the case if is convex w.r.t. , the playerwise local minimizer check described above is satisfied for all players, and therefore the game has an OLNE solution. If is continuous in (which is guaranteed by our differentiability assumption) and locally strongly monotone with respect to , the dynamic games can be solved for all states near . This guarantees the existence of a local FNE.

3 The Projected Gradient Method

The projected gradient method for monotone VI problems was explained in details in [15]. We briefly describe the method and its basic application to Problem 3, which helps find an OLNE for Problem 2. We show how this leads to an algorithm for constrained dynamic games.

3.1 Projected Gradient Method for VI

The projection algorithm follows an iterative update

| (9) |

where is a step size and is the projection operator. The algorithm converges linearly with constant when is -strongly monotone, -Lipschitz, i.e.,

| (10a) | ||||

| (10b) | ||||

and that [15]. There exists a small that guarantees the linear convergence, although smaller leads to slower convergence. To apply the projection method to constrained dynamic games, we need procedures to compute the gradient and the projection onto .

Given feasible and such that , the gradient can be found efficiently by first performing a backward pass (11)[10], then extracting and stacking corresponding elements in .

| (11a) | ||||

| (11b) | ||||

| (11c) | ||||

| (11d) | ||||

where are derivatives of the dynamics and cost evaluated around defined in (34) in Section 6.

The projection onto requires solving a constrained optimal control problem with quadratic step costs, which can be solved via classic optimal control methods [23].

Problem 4.

Constrained optimal control around nominal trajectory

| (12a) | ||||

| s.t. | (12b) | |||

| (12c) | ||||

| (12d) | ||||

The notation is overloaded and is different from that of the formulations of Problem 1 and 2. Note that a trajectory found via projected gradient method is a solution to the VI problem but not necessarily the game. A playerwise local minimizer check needs to be done as discussed in Section 2.3. We summarize the projected gradient method in Algorithm 1.

4 The Douglas-Rachford Operator Splitting Method

This section concerns with solving an OLNE with the Douglas-Rachford splitting method, which is an alternative to the projected gradient method. The DR splitting method, in its most general form, finds the vector that solves a monotone inclusion problem of the form

| (13) |

where and are two maximally monotone operators in this section. The DR algorithm is defined by the iteration

| (14) |

is called the reflected resolvent of where is the of . The same notation applies for operator . is a constant such that . The key steps are solving for the two operators’ resolvents, which we elaborate in the case of constrained dynamic games in this section. The DR splitting method has been proven to converge linearly in cases when at least one operator has stronger properties such as strong monotonicity and Lipschitz continuity. See [16] for more details.

4.1 VI Reformulation of Static Game with States

For ease of notation we interpret as a column vector vertically stacking and in this section. We create an extended gradient prepending of zeros in front of , i.e.,

| (15) |

and use it to reformulate Problem 3 equivalently as

Problem 5.

VI formulation of static game with extended gradient

| Find | (16a) | |||

| s.t. | (16b) | |||

| (16c) | ||||

Problem 5 is equivalent to an inclusion problem, when and are convex and is strongly monotone as explained in Appendix A.1. Note that is also a decision variable in this formulation. This VI problem can also be formulated as an inclusion problem such that we can apply the DR-splitting method.

Problem 6.

Inclusion problem form of the static game Problem 2

| (17) |

where and indicate the normal cone operators of and , and is a positive regularization constant. The smaller the , the more regularized the problems are, but the slower the convergence would be. should be tuned so that the relevant problems in Section 4.2, 4.3 and 4.4 are either strongly convex of monotone for better solvability. Note that there are three adding operators in Problem 6, in contrast to (13) which has only two. We can single out any one operator and combine the other two to form an inclusion problem with two adding operators and apply the DR algorithm. The algorithm requires alternately solving two problems that are the resolvents of different operators. Which combination to chose ultimately depends on which resolvents are easier to solve, which varies with the specific dynamic game and available solvers. Ideally, when both resolvents are analytically solvable, the DR algorithm is preferred.

We summarize the implementation of the DR splitting in Algorithm 2 and elaborate the optimization/game problems derived from the resolvents later in this section. We use to indicate a nominal trajectory that follows the same convention as . The notation is overloaded to indicate costs for these different resolvent problems. For details regarding how the problems are derived from resolvents, see Appendix A.2.

| (18a) | ||||

| (19) |

| (20) |

4.2 Singling out

Problem 6 becomes the following when singling out

| (21) |

The resolvent of corresponds to solving a regularized, unconstrained dynamic game and the resolvent of is the projection onto .

Problem 7.

Regularized unconstrained dynamic game around nominal trajectory

| (22a) | ||||

| s.t. | (22b) | |||

This problem can be solved via our previously proposed stagewise Newton or DDP methods with linear complexity in and quadratic convergence [10].

Problem 8.

Projection of a nominal trajectory onto the extra constraints set

| (23) |

When the extra constraints sets are convex at each stage, this projection is equivalent to solving the projection onto a convex set at each stage.

4.3 Singling out

Problem 6 becomes the following when singling out

| (24) |

The resolvent of corresponds to solving a series of regularized, constrained static games and the resolvent of is the projection onto , which is an optimal control problem.

Problem 9.

Regularized constrained static games around nominal trajectory

| (25a) | ||||

| s.t. | (25b) | |||

| (25c) | ||||

Note that the objectives are not coupled cross time, therefore this is equivalent to solving constrained static games, which can be solved via solving the KKT conditions [20] or other static game methods. Note that there is an additional player with decision variable at each stage.

Problem 10.

Projection of a nominal trajectory onto the dynamics

| (26a) | ||||

| s.t. | (26b) | |||

This is an optimal control problem with quadratic step cost, which can be solved via classic optimal control methods [24].

4.4 Singling out

Problem 6 becomes the following when singling out

| (27) |

The resolvent of corresponds to solving a constrained optimal control problem and the resolvent of is a series of unconstrained optimization.

Problem 11.

Constrained optimal control around nominal trajectory

| (28a) | ||||

| s.t. | (28b) | |||

| (28c) | ||||

| (28d) | ||||

This is an constrained optimal control problem with quadratic step cost, which can be solved via classic optimal control methods [24].

Problem 12.

Regularized unconstrained games around a nominal trajectory

| (29a) | ||||

Because the objectives are not coupled cross time, this becomes unconstrained static games, which can be solved via classic VI methods. Similar to Problem 9, an additional player with decision variable at each stage is added.

5 Parametric Games and Feedback Equilibria

Solving a parametric game is the backbone of solving an explicit feedback Nash equilibrium of a game. We briefly describe the results of analytically solvable parametric games and dynamic games in this section. Section 5.1 explains the result for linear equality constrained quadratic parametric games, which is directly applied to stagewise Newton method in Section 6. Section 5.2 describes the form of feedback equilibrium of linearly constrained quadratic dynamic games, which is piecewise affine but can be exponentially complex. We assume each player’s cost function is continuous and strictly convex throughout this section.

The detailed development of the results can be found in the Appendix B, which is extending the analytical solution of linearly constrained, quadratic objective optimization and optimal control in Chapter 7 of [23].

5.1 Linear Equality Constrained Quadratic Parametric Game

Problem 13 is a basic form that is encountered when approximating a constrained dynamic game, where collects all players’ action and is a vector parameter. An FNE policy is desired. This game has an explicit analytical solution with simple assumptions.

Problem 13.

Linear equality constrained quadratic parametric game

| (30a) | ||||

| s.t. | (30b) | |||

The following lemma describes its solution.

5.2 Linearly Constrained Quadratic Dynamic Games

A linearly constrained quadratic dynamic game is formulated as following. It is one of the most complicated form of dynamic games of which we can acquire analytical solution in theory.

Problem 14.

Linearly Constrained Quadratic Dynamic Games

| (33a) | ||||

| s.t. | (33b) | |||

| (33c) | ||||

This problem can be viewed as a static game in parameterized by . As developed in detail in Appendix B, the explicit FNE solution found via Bellman recursion to this problem is a piecewise affine policy, with polyhedral domains, and the value functions are piecewise quadratic. However, the required number of polyhedral domains on the space can grow exponentially, causing the procedure to be computationally prohibiting. It is reasonable to believe that the feedback Nash equilibrium of general constrained dynamic games can be more complex. This fact drives us to seek local FNE.

6 Local Feedback Equilibrium

OLNEs solved via projected gradient or DR splitting might not be applicable to systems with noise. Thus, we aim to find a local feedback policy around the OLNE that can accommodate disturbances of the system to a certain degree. As discussed above, even for linear-quadratic dynamic games with polyhedral constraints, explicit feedback strategies can require exponential computational complexity. In this section, we describe a simplified strategy based on linearly constrained problems. When the constraints are polyhedral, we prove that the feedback policy is indeed a local FNE.

6.1 Stagewise Newton Method for Local Feedback Policy

We introduce the stagewise Newton method for computing a local feedback policy for Problem 1. The method is based on the stagewise Newton method for unconstrained dynamic games from our previous work [10]. The key difference is that, at each step, an approximated linear equality constrained quadratic game Problem 13 is solved, instead of the unconstrained quadratic game in [10].

Suppose a trajectory has been found along with the active constraints at each step. The set of indices of active constraints in is denoted and we use to indicate the active constraints at , therefore .

We inherit the following notation of derivatives for stagewise Newton method from [10].

| (34a) | |||

| (34b) | |||

| (34c) | |||

| (34d) | |||

We introduce new notation related to the derivatives of the active constraints , .

| (35a) | ||||

| (35b) | ||||

| (35c) | ||||

We can form a local linear-quadratic approximation that is still analytically solvable via dynamic programming as following.

Problem 15.

Linear-quadratic approximation to Problem 1

| (36a) | ||||

| subject to | ||||

| (36b) | ||||

| (36c) | ||||

| (36d) | ||||

| (36e) | ||||

| (36f) | ||||

| (36g) | ||||

where the states of the dynamic game are given by and as

| (37a) | ||||

| (37b) | ||||

The following lemma describes the solution to Problem 15.

Lemma 2.

The equilibrium value functions found via the Bellman recursion (6) for the dynamic game Problem (15) are denoted as and , which can be expressed as

| (38a) | ||||

| (38b) | ||||

where the matrices , , and can be computed in a backward pass, which also finds a local feedback policy of the form around this trajectory.

The matrices , , and in (38) are computed recursively by , , and

| (39a) | ||||

| (39b) | ||||

| (39c) | ||||

| (39d) | ||||

| (39e) | ||||

| (39f) | ||||

| (39g) | ||||

| (39h) | ||||

| (39i) | ||||

for .

Proof. The stagewise Newton method for unconstrained dynamic game and its solution was proved in [10]. The only difference in the dynamic programming procedure for Problem 15 is that an equality constrained static quadratic game is solved at each time step, resulting in different expressions for the feedback parameters and , which are justified by the solution of Problem 13. ∎

Note that the differential dynamic programming (DDP) method for unconstrained dynamic games [10] can be adapted to constrained games in a similar fashion, for the sake of completeness of generalizing our previous work. As in the unconstrained dynamic game case, DDP and stagewise Newton do not manifest obvious advantages over each other.

6.2 Remarks on the Feedback Policy by Stagewise Newton Method

Stagewise Newton method solves a linear equality constrained quadratic dynamic game that approximates Problem 1 around and finds a local feedback policy. Without constraints , i.e., setting , the method reduces to the unconstrained version of stagewise Newton method [10]. However, unlike its counterpart for unconstrained game, because of the introduction of constraints, the policy found might not be feasible, therefore we cannot perform the iterative process as in [10]. We consider in this paper the case when is an OLNE and the feedback policy found by one backward pass of the stagewise Newton method. In this case, will be will be a fixed-point of the Newton iteration and the feedback policy simplifies to . Furthermore, the matrices are computed in complexity. The possibility of infeasible policy remains and is overcome with tightened constraints as in Section 6.3.

The proposed algorithm neglects the inactive constraints. A problem arises, in that deviations in the state can cause these neglected constraints to become violated. A simple method to ensure feasibility is to tighten the inequality constraints, as is common in model predictive control [23]. We will see below that in the case of polyhedral constraints, the feedback policy is indeed an local -FNE.

6.3 Problems with Polyhedral Constraints

In this section, we introduce a special class of dynamic problems, restricting to affine dynamics and polyhedral constraints, such that the stagewise Newton method can be utilized to find a local -FNE for a partially tightened problem (defined below). We first introduce a fully tightened version of a polyhedrally constrained linear dynamic game

Problem 16.

Game with tightened polyhedral constraints

| (40a) | ||||

| s.t. | (40b) | |||

| (40c) | ||||

| (40d) | ||||

Here are vectors used to tighten the inequality constraints. As above, say that is an OLNE trajectory. We use superscripts and to denote values associated with active and inactive constraints on and . If we find a local feedback policy using the stagewise Newton method, it can be shown that it is feasible for the following partially tightened problem:

Problem 17.

Game with partially tightened polyhedral constraints

| (41a) | ||||

| s.t. | (41b) | |||

| (41c) | ||||

| (41d) | ||||

| (41e) | ||||

Recall that the dynamics, constraints, and control law are all affine. Thus, when a local variation of the state happens with a sufficiently small , the trajectories remain feasible.

The next theorem summarizes this local feedback Nash equilibrium result. The detailed proof can be found in Appendix A.4.

Theorem 1.

7 Numerical Examples

We demonstrate the approximated local feedback Nash equilibrium around an OLNE with a common-property fishery resource problem and Douglas-Rachford algorithm with a linear quadratic games with analytically projectable convex constraints.

7.1 A Common-Property Fishery Resource Problem

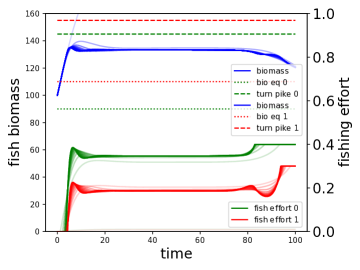

The common-property fishery game was considered in Chapter 13, [2], which is a classic renewable resource manage problem that dates back to 1970s. The analysis in [2] settled at the conclusion that efficient players will drive some opponents out of the competition and maintain at the bionomic equilibrium with zero sustained economic rent. We demonstrate the dynamic equilibrium of two players jointly utilize the resource for a given period of time.

The game is discretized. Scalars and , denote the biomass of fish and fishing effort of two players. The fishing effort is constrained by . The dynamics of the system from time to is given by

| (43) |

where the natural growth rate is

| (44) |

is half the maximal biomass the environment can sustain and is the maximal growth rate which happens when . is the catchability coefficient for player . is a I.I.D. Gaussian noise we injected for simulating a noisy system. Step profit of each player is modeled as

| (45) |

where is the unit price of landed fish and is the unit cost of effort.

Constants chosen are chosen in favor of player .

| (46) |

The turnpike for a player is the most profitable level of fish biomass if the player is managing the resource alone. And the bionomic equilibrium for a player is the minimal fish biomass that a player can turn a profit.

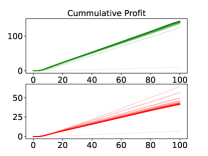

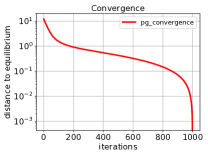

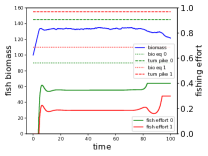

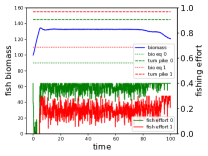

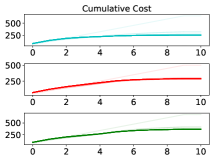

We first applied the projected gradient method with stepsize for 1,000 iterations on the deterministic system (neglecting ), finding the OLNE shown in Fig. 1. The cumulative profit and convergence of actions is summarized in Fig 2. We further applied the stagewise Newton method, found the local feedback Nash equilibrium and implemented it for the noisy system, setting the variance of zero-mean Gaussian noise to . The comparison between OLNE and FNE for noisy system is shown in Fig. 3.

7.2 Linear Quadratic Game with Convex Constraints

When a dynamic linear-quadratic(LQ) game has an convex constraint set onto which, the projection is analytically solvable, both problems in Section 4.2 can be analytically solved and the Douglas-Rachfor splitting method is preferred.

We demonstrate the DR splitting method on a 2-D locomotion problem with players. Each player directly controls its own location. The system state contains sets of 2-D coordinates of each player and action for each players. We use to denote player ’s coordinate at step , naturally we have , where the variables are all column vectors. The dynamics is simply

| (47a) | |||

where is a identity matrix. The initial position and each players target position are known. Each player’s action is subject to a magnitude constraint . The cost of each player consists of two parts, reaching to the target and conserving its own energy.

| (48) | |||

| (49) |

It is also required that all three players should meet at , i.e., , which makes the problem a coupled dynamic game problem rather than 3 separated optimal control problems. The particular constraint also causes the projected gradient method or Algorithm 1, if applied to the problem at hand, to require solving a constrained optimal control problem in each iteration, which needs another iterative procedure. The DR splitting on the other hands, presents two analytically solvable subproblems. In particular, the corresponding Problem 7 is solved via stagewise Newton for unconstrained game [10] and Problem 8 becomes a simple projection onto .

The parameters are chosen as

| (50) |

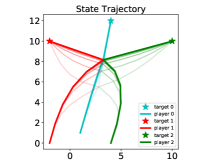

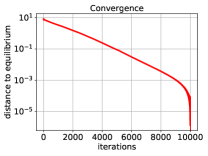

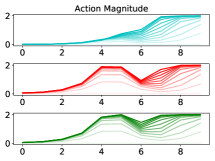

We applied the DR splitting method with the splitting scheme in Section 4.2. We found and produced stable iteration and solution. iterations were performed and shown in Fig. 4.

8 Conclusion and Extensions

We demonstrated how the projected gradient method and the Douglas-Rachford algorithm can be used to compute open-loop Nash equilibrium of constrained dynamic games. These algorithms converge locally with a linear rate, and our algorithms require linear iteration complexity in the horizon. We showed how the OLNE solutions computed from these methods can be combined with the stagewise Newton method to find a local feedback strategy. In the case of polyhedrally constrained games with linear dynamics, was saw that this feedback policy provides an approximate feedback Nash equilibrium. The approximation properties of this feedback policy for more general nonlinearly constrained games is worth further study. Another promising direction would be to utilize methods from model predictive control to compute approximate feedback equilibria.

References

- [1] Tamer Basar, Alain Haurie, and Georges Zaccour. Nonzero-sum differential games, July 2018.

- [2] Suresh P Sethi. Differential games. In Optimal Control Theory, pages 385–407. Springer, 2019.

- [3] Dario Bauso. Game theory with engineering applications, volume 30. Siam, 2016.

- [4] Alberto Bressan. Noncooperative differential games. Milan Journal of Mathematics, 79(2):357–427, 2011.

- [5] Ilan Rusnak. The lady, the bandits, and the bodyguards–a two team dynamic game. In Proceedings of the 16th world IFAC congress, pages 934–939, 2005.

- [6] Oleg Prokopov and Tal Shima. Linear quadratic optimal cooperative strategies for active aircraft protection. Journal of Guidance, Control, and Dynamics, 36(3):753–764, 2013.

- [7] Eloy Garcia, David W Casbeer, Khanh Pham, and Meir Pachter. Cooperative aircraft defense from an attacking missile. In Decision and Control (CDC), 2014 IEEE 53rd Annual Conference on, pages 2926–2931. IEEE, 2014.

- [8] Fouad El Ouardighi, Steffen Jørgensen, and Federico Pasin. A dynamic game with monopolist manufacturer and price-competing duopolist retailers. OR spectrum, 35(4):1059–1084, 2013.

- [9] Quanyan Zhu, Zhu Han, and Tamer Başar. A differential game approach to distributed demand side management in smart grid. In Communications (ICC), 2012 IEEE International Conference on, pages 3345–3350. IEEE, 2012.

- [10] Bolei Di and Andrew Lamperski. Newton’s Method and Differential Dynamic Programming for Unconstrained Nonlinear Dynamic Games. arXiv e-prints, page arXiv:1906.09097, Jun 2019.

- [11] Francisco Facchinei and Christian Kanzow. Generalized nash equilibrium problems. 4OR, 5(3):173–210, 2007.

- [12] Francisco Facchinei, Andreas Fischer, and Veronica Piccialli. Generalized nash equilibrium problems and newton methods. Mathematical Programming, 117(1-2):163–194, 2009.

- [13] Giancarlo Bigi, Marco Castellani, Massimo Pappalardo, and Mauro Passacantando. Nonlinear programming techniques for equilibria. 2018.

- [14] Jorge Nocedal and Stephen J Wright. Numerical optimization. Springer, 2nd edition, 2006.

- [15] Francisco Facchinei and Jong-Shi Pang. Finite-dimensional variational inequalities and complementarity problems. Springer Science & Business Media, 2007.

- [16] Pontus Giselsson. Tight global linear convergence rate bounds for douglas–rachford splitting. Journal of Fixed Point Theory and Applications, 19(4):2241–2270, 2017.

- [17] Pontus Giselsson and Stephen Boyd. Linear convergence and metric selection for douglas-rachford splitting and admm. IEEE Transactions on Automatic Control, 62(2):532–544, 2016.

- [18] Brendan O’Donoghue, Giorgos Stathopoulos, and Stephen Boyd. A splitting method for optimal control. IEEE Transactions on Control Systems Technology, 21(6):2432–2442, 2013.

- [19] Giorgos Stathopoulos, Harsh Shukla, Alexander Szucs, Ye Pu, Colin N Jones, et al. Operator splitting methods in control. Foundations and Trends® in Systems and Control, 3(3):249–362, 2016.

- [20] Francisco Facchinei, Andreas Fischer, and Veronica Piccialli. On generalized nash games and variational inequalities. Operations Research Letters, 35(2):159–164, 2007.

- [21] Jacek B Krawczyk and Vladimir Petkov. Multistage games. Handbook of Dynamic Game Theory, pages 157–213, 2018.

- [22] Alain Haurie, Jacek B Krawczyk, and Georges Zaccour. Games and dynamic games, volume 1. World Scientific Publishing Company, 2012.

- [23] James Blake Rawlings, David Q. Mayne, and Moritz Diehl. Model Predictive Control: Theory, Computation, and Design. Nob Hill Publishing, 2019.

- [24] Moritz Diehl and Sebastien Gros. Numerical Optimal Control. –, expected to be published in 2018.

- [25] Asen L Dontchev and R Tyrrell Rockafellar. Implicit functions and solution mappings. Springer Monographs in Mathematics. Springer, 2014.

- [26] Shu Lu and Stephen M Robinson. Variational inequalities over perturbed polyhedral convex sets. Mathematics of Operations Research, 33(3):689–711, 2008.

- [27] Stephen M Robinson. Normal maps induced by linear transformations. Mathematics of Operations Research, 17(3):691–714, 1992.

Appendix A Auxiliary Proofs

A.1 Problem 5 is Equivalent Problem 6

Because the normal cone of intersections of convex sets is equal to the sum of normal cones of the convex sets [25], the inclusion problem Problem 6 is equivalent to

| (51) |

According to the definition of normal cone

| (52) |

When is strongly monotone, and are convex, , and are all maximally monotone operators. Because adding operators preserve maximal monotonicity, so we can apply DR splitting algorithm to Problem 6.

A.2 Resolvents of Operators in Problem 6

The resolvent of a set-valued/single-valued monotone map is defined by

| (54) |

which is single-valued and non-expansive [15].

A.2.1 Resolvent of the normal cone of a convex set

Suppose we have a convex set . Following the definition, the resolvent of

| (55a) | ||||

which is equivalent to

| (56) | |||

| (57) |

This VI problem is equivalent to the optimization of a projection of onto

| (58a) | ||||

| s.t. | (58b) | |||

Therefore the resolvent of a normal cone of a convex set is the projection onto the convex set. This justifies Problem 8 and 10.

A.2.2 Resolvent of a gradient vector

We study the resolvent of the gradient operator of a game as in (7). Suppose , equivalently we have

| (59a) | |||

Consider a static game problem

| (60a) | ||||

whose Nash equilibrium is equivalent to the solution of

| (61) |

which is equivalent to (59a). Therefore, the resolvent is equivalent to the solution of a static game.

A.3 Generative Cone Condition to Linear Inequalities

Lemma 3.

A generative cone condition, where has full row rank

| (62) |

can be equivalently expressed as

| (63) |

where

| (64) |

Proof. The generative condition is equivalent to

| (65a) | ||||

| (65b) | ||||

which is equivalent to

| (66) | ||||

| (67) |

Choose , the equivalent conditions can be easily checked

| (68a) | |||

Given the SVD decomposition of

| (69) |

It is easy to check that

| (70) |

Since , (66) is true. ∎

A.4 Proof of Theorem 1

First we show that the policy produces feasible trajectories.

Recall that is an OLNE for the equality-constrained problem. Thus, it is a fixed-point of Newton’s method, so that the feedback policy has the form:

| (71) |

By construction, (36f) ensures that active constraints for remain active for .

Now we analyze the inactive constraints. Note that satisfies

| (72) |

Furthermore, if the affine dynamics and polyhedral constraints imply that we must have that and for all . It follows that for sufficiently small , the constraint (41d) holds. Thus, the feedback policy produces a feasible trajectory.

Finally, we show that the approximate feedback equilibrium condition, (42), holds. Note that left inequality always holds by construction, so we only need to prove the right inequality.

Fix a player and a time . Assume that the other players are using the strategy profile . Then, with the strategies of the other players fixed, the policy, , that minimizes can be computed from the following optimal control problem:

| (73a) | ||||

| s.t. | (73b) | |||

| (73c) | ||||

| (73d) | ||||

| (73e) | ||||

| (73f) | ||||

The quadraticization around of the optimal control problem (73) is exactly the same as that of player in Problem 17. Thus, when all other players follow the stagewise Newton strategy, the minimizer should be the same as , since player will have no incentive to change its strategy on the quadraticized problem. Then, to show that the strategy is an approximate feedback equilibrium, it suffices to show that is approximately optimal. The bound on optimality follows from the general result on parameterized optimization from Lemma 5 below. ∎

A.5 Lemmas on Optimization Approximation

In this section, we present Lemma 5 which is used to prove Theorem 1, along with supporting results.

Let be a strongly convex with respect to in a neighborhood of . Assume that minimizes with respect to . Let be its quadratic approximation around the nominal point . Let . Define the policies by

| (74a) | ||||

| (74b) | ||||

Note that has the form

| (75) |

each pair corresponds to the active indices, , of .

Let , where is the active set of . Note that in the game context, this strategy corresponds precisely to the individual players’ approximate strategy computed by stagewise Newton methods.

The eventual goal is to show that and give similar costs. As an intermediate result, we show that and give similar costs.

Lemma 4.

Let . Say that has Lipschitz second derivatives and is strongly convex with respect to in a neighborhood of . Further assume that is non-empty for all in this neighborhood. Then the following bounds hold:

| (76) |

Proof. Note that the first inequality of (76) is immediate from the definition of . Thus, we focus on the second inequality.

We will show that . To do this, we will show that both functions are Lipschitz and that .

Note that is the solution to the following VI

| (77) |

By strong convexity and differentiability, is positive definite. This implies that for any matrix, with full column rank, we have that is also positive definite, and thus has positive determinant. Then general results on perturbed VIs show that must be Lipschitz. See [26]. Furthermore, by construction .

By the same reasoning, we must also have that is Lipschitz and again by construction we have that . It follows that . Thus

Now we will prove the upper bound. For compact notation, let and let . Then we have the approximation:

By optimality of and feasibility of , we have that

Thus, the proof will be completed if we can bound this term above by .

Let . Since is differentiable and , we have that

where the partial derivatives are evaluated at .

Thus, the desired bound is given by

where the second inequality due to optimality of for the corresponding affine VI. ∎

Now we present the optimization approximation result required for Theorem 1.

Lemma 5.

Assume that and let . Then the following bounds hold.

| (78) |

Proof . The bound on the left holds automatically since is feasible and is the corresponding optimal solution.

Specializing Lemma 4 to the case of optimization implies that . Thus, it suffices to show that

| (79) |

Let , let , let be the active set for , and let be the inactive set. We will show that the active sets only switch a finite number of times.

We claim that for each subset , the set is convex. In particular, must be an interval.

Proposition 7.10 of [23] implies that the set of such that has active set is a polyhedron. Since each is the projection of the intersection of this set with a line, we must have that is convex.

Since there are at most active sets, it follows that there are sets with such that are intervals that partition . These sets can be arranged so that for and .

Let be the affine strategy corresponding to . Then by construction, we have

| (80) |

These active sets have the property that either or . Either must be open on the right or must be open on the left. Consider the case that is open on the right. (The case of open on the left is similar.) Then the boundary between and is a point . By continuity, all of the constraints in must be tight at . Thus, we must have that .

Consider the case that . (The other case is similar.) In particular, the constraints from must be active for both corresponding VI solutions. Thus, if is the Moore-Penrose pseudoinverse of and is a matrix with full column rank such that , we must have that

for , and some vectors . It follows that

| (81) |

Let be some value for which is the active set for , and let be the corresponding optimizer. Note that . It follows that

Since minimizes , with active, we must have that

for all sufficiently small . It follows that .

Thus, we can get the bound:

| (82) |

An analogous argument argument in the case of shows that the same bound holds.

Appendix B Parametric Games and Feedback Equilibrium in Details

This section contains the detailed development for Section 5. Some problem definitions and lemmas are restated so this section is self-contained for ease of reading. We study in this section some basic parametric quadratic games with polyhedral constraints to gain insight of the feedback Nash equilibrium of dynamic games in general. We assume each player’s cost function is continuous and strictly convex throughout this section.

B.1 Linear Equality Constrained Quadratic Parametric Game

Problem 18 is a basic form that is encountered when approximating a constrained dynamic game, where collects all players’ action and is a vector parameter. An FNE policy is desired. This game has an explicit analytical solution with simple assumptions.

Problem 18.

Linear equality constrained quadratic parametric game

| (83a) | ||||

| s.t. | (83b) | |||

The following lemma describes its solution.

Lemma 6.

Proof. The feedback Nash equilibrium can be solved via solving the KKT conditions of all players [20]. The Lagrangians can be formulated as

| (86a) | ||||

| (86b) | ||||

Therefore the KKT conditions are

| (87a) | ||||

| (87b) | ||||

| (87c) | ||||

Thus, for any , the unique solution (87a) for is given by . Plugging this result into (87c) and solving for gives

| (88) |

Plugging this back into the expression for gives the result. ∎

B.2 Linearly Constrained Quadratic Parametric Game

The more generalized problem with inequality constraints are studied in this section. Related problems are studied and the piecewise affine solution was recognized in the variational inequality literature [26, 27]. Our analysis focuses on games which in addition, recognizes the piecewise quadratic value functions. We inherit the notation of and from Section B.1. Such problems serve as a backbone for analyzing FNE for dynamic games when we solve the static game (6c) formed by the state-action value function at a stage.

Problem 19.

Linearly constrained quadratic parametric game

| (89a) | ||||

| s.t. | (89b) | |||

We use and to indicate the feasible sets of and , i.e.,

| (90a) | |||

| (90b) | |||

Note that we do not lose generality without explicit linear equality constraints, since a linear equality constraint can be equivalently formulated with two inequality constraints. The following lemma and proof offers a descriptive solution to this problem.

Lemma 7.

Given playerwise convexity of objective functions, i.e., are positive definite, Problem 19 has a piecewise affine feedback Nash equilibrium on a finite polyhedral partition of if and only if is invertible.

Proof. Assume has rows and we use to indicate the power set of . For a set of indices , we use , and to denote picking the corresponding rows. The solution to Problem 19 can be found via the following procedure.

Pick one element , which we suppose to be the indices of active constraints, and solve a linear equality constrained quadratic parametric game with the method in Section B.1 as following

| (91a) | ||||

| s.t. | (91b) | |||

We obtain an affine policy and the matrices , , following Lemma 6. Note that we are adding subscribes a to indicate values found associated with the active constraints set of .

We apply the optimality conditions of VI problem [15] to find the set in which the policy is an equilibrium in terms of

| (92) |

where means the cone generated by the rows of . Condition (92) can be reformulated as a polyhedral constraint , since the second condition is equivalent to an linear inequality as shown in Appendix A.3, where

| (93a) | ||||

| (93b) | ||||

Hence we have found an affine policy on a polyhedral region in . In the case of , the policy is not an equilibrium.

The procedure can be repeated for all combinations of active constraints, i.e., . For any , there exists an equilibrium and a set of active constraints, therefore must fall in one of the . Because there are a finite number of combinations of active constraints, a finite number of partitions of with and corresponding equilibria policy in each partition can be found. ∎

B.3 Linearly Constrained Piecewise Quadratic Parametric Game

We focus on static game problems where each player’s cost function is continuous, strictly convex and piecewise quadratic on a polyhedral partition . Due to the complexity of the problem, we refrain from obtaining explicit solutions, but study the properties of the solution in this section.

Problem 20.

Linearly Constrained Piecewise Quadratic Parametric Game

| (94a) | ||||

| s.t. | (94b) | |||

| (94c) | ||||

| (94d) | ||||

Assume all players share the same polyhedral partition W.L.O.G and that is strongly monotone for any given to guarantee the existence and uniqueness of a solution. In each partition , the problem reduces to a linearly constrained quadratic parametric game as Problem 19, and are inherited from Section B.1, where the subscript i denotes the values in . Suppose there are polyhedral partitions, i.e., . The exact quadratic expression is suppressed. We define an auxiliary problem for each .

Problem 21.

Auxiliary problem

| (95a) | ||||

| s.t. | (95b) | |||

Each auxiliary problem can be solved as in Section B.2, obtaining a piecewise affine policy and piecewise quadratic value functions. Since Problems 20 and 19 are closely connected, it is sensible to study the connection between the solutions of these two problems.

We define the concept of active polyhedrons for in as the set of indices such that contains , i.e., . The next lemma explains how to recover the solution to Problem 20 from the auxiliary problems. We use the to indicate the set of feasible with given and define .

The following lemma answers the question of how to solve the equilibrium of Problem 20 for a given with the help of auxiliary problems Problem 21.

Lemma 8.

is the open-loop Nash equilibrium to Problem 20 given parameter if and only if it is the solution to .

Proof. Because for any given there is a unique solution for Problem 20, a local solution is also the global solution. The equivalent VI problem for finding the local solution to Problem 20 is

| find | (96a) | |||

| (96b) | ||||

The condition (96b) can be expanded to . Due to the same argument that local and global solution are equivalent, this expansion does not change the solution found. Therefore, (96) is equivalent to being the solution to simultaneously. We can find the solution of Problem 20 via the solutions of . ∎

Next we focus on finding the feedback Nash equilibrium in terms of . Suppose there are a total of inequalities. The inequalities defining all partitions can be collected together as

| (97) |

Therefore we can create a one-to-one mapping from an index set to the inequality . For any pair of , we can check the partition(s) it is living in and collect the indices in , and check the active constraints and collect them in . We call acitve inequalities. Note that though and are tied to pairs of , there could only be a finite number of different and since there are only a finite number of partitions and inequality constraints. In other words, we can find a finite number of representative pairs of , such that and contain all possible active polyhedrons and active constraints combinations. We can get rid of the dependency on , use the index to indicate different feasible active polyhedrons and feasible active constraints . Finding the sets and requires studying the structure of the polyhedral partition , which is not within the scope of this paper.

The next lemma describes the feedback Nash equilibrium of Problem 20.

Lemma 9.

Given playerwise convexity of objective functions, i.e., are positive definite, Problem 20 has a piecewise affine feedback Nash equilibrium on a finite polyhedral partition of if and only if is invertible .

Proof. Similar to the proof for Lemma 7, we describe a procedure for finding affine policies and their corresponding region of where they are feedback Nash equilibrium. Then we conclude by arguing all are included in the procedure.

We iterate through all pairs of and . For each , we can solve for an affine policy with the feasible active inequalities and the objective functions of all players as they constitute an instance of Problem 13. To find the region where this policy is indeed an FNE, we need to solve the corresponding optimality conditions

| (98) |

where means picking the rows of active inequalities in that are also in . The second condition (98) can be expressed with linear inequalities as in Appendix A.3, therefore the feasible region , if non-empty, is polyhedral, and is the FNE in this region. We omit the explicit expression here.

This procedure can be repeated . For any in , we can find via a solver for monotone VI problems, find the active polyhedrons and active inequalities, therefore the . The solution is covered by the condition (98) with because they share the same local optimality condition. Note that such procedure may require exponentially many steps w.r.t. the number of polyhedrons and inequality constraints. ∎

B.4 Linearly Constrained Quadratic Dynamic Games

Now that we are equipped with some basic results, we can move on to dynamic games. A linearly constrained quadratic dynamic game is formulated as following. It is one of the most complicated form of dynamic games of which we can acquire analytical solution in theory. We briefly discuss the dynamic programming solution to such problems.

Problem 22.

Linearly Constrained Quadratic Dynamic Games

| (99a) | ||||

| s.t. | (99b) | |||

| (99c) | ||||

The first static problem required to be solved by dynamic programming is a piecewise quadratic, resulting in a piecewise affine policy and piecewise quadratic value functions on , which is the space of . Based on the linear dynamics and constraints at step , we can form a polyhedral partition for , resulting in the next static game to be a linearly constrained piecewise quadratic parametric game. As we have seen in Section B.2, the solution remains to be a piecewise affine policy and quadratic value functions. Therefore, the backward pass by dynamic programming can be done obtaining a series of piecewise quadratic value functions with linear inequality constraints. However, the number of partitions on each space can grow exponentially causing the procedure to be computationally prohibiting. It is reasonable to believe that the feedback Nash equilibrium of general constrained dynamic games can be more complex. This fact drives us to seek local FNE.