:

\theoremsep

\jmlrproceedingsAABI 2019Mbuvha Boulkaibet and Marwala

An Automatic Relevance Determination Prior Bayesian Neural Network for Controlled Variable Selection

Abstract

We present an Automatic Relevance Determination prior Bayesian Neural Network(BNN-ARD) weight l2-norm measure as a feature importance statistic for the model-x knockoff filter. We show on both simulated data and the Norwegian wind farm dataset that the proposed feature importance statistic yields statistically significant improvements relative to similar feature importance measures in both variable selection power and predictive performance on a real world dataset.

1 Introduction

Central to many machine learning tasks is a feature selection problem where candidate features are considered such that they maximise the quality and strength of the signal they give about the dynamics of the system or process being modelled(Lu et al., 2018; Candes et al., 2018). This will typically require expert judgement or computationally expensive iterative variable selection methods(Candes et al., 2018).

The knockoff filter of Candes et al. (2018) provides a framework for performing variable selection while controlling the false discovery rate (FDR) of null features. Model-X knockoffs work by creating ’knockoff’ variables that imitate the dependency structure within the original candidate feature space but critically with no relationship with the target variable (Barber et al., 2015). These knockoff features can thus be used as variable selection controls for their corresponding candidate features. If a candidate feature on the basis of a specified feature importance metric is less important than its corresponding knockoff then it follows that the candidate feature is irrelevant. Various feature importance metrics have been suggested for determining the relative importance between candidate features and their knockoffs. These have included LASSO coefficients(Barber et al., 2015; Candes et al., 2018), filtering neural network layers (Lu et al., 2018) and permutation based methods(Gimenez et al., 2018).

In this paper we integrate weight l2-norm feature importance statistics derived from Automatic Relevance Determination(ARD) prior Bayesian Neural Networks(BNNs) into the knockoff filter framework. We show that the proposed feature importance statistics obtain the desired FDR control and display outperformance in statistical power to other nonlinear feature importance measures.

2 Background

The modelling setting we consider is one where we have independent and identically distributed observations of candidate feature vectors and a corresponding scalar , . We assume that Y depends on a subset of the complete set of candidate features and is conditionally independent of the features in complement of given the features in .

The controlled variable selection problem is one that aims to discover as many of the features in as possible while controlling the FDR which is defined as follows for a set of selected features (Gimenez et al., 2018):

| (1) |

The recently proposed model-x knockoffs filter (Candes et al., 2018) has been widely employed as a mechanism for achieving FDR control below some desired threshold .

Definition 2.1 (Model-X Knockoffs features(Candes et al., 2018)).

A model-x knockoff for a -dimensional random variable vector is a p-dimensional random variable vector that satisfies the following properties for any subset :

-

1.

where swap(s) is an operation swapping corresponding entries of and for each

-

2.

i.e. the response Y is conditionally independent of the knockoff features given the candidate features.

In special cases where features are Gaussian , model-x knockoffs can be constructed by solving constrained optimisation problems for matching second order moments.

Once the model-x knockoffs are constructed feature importance statistics and for and with . ard then defined as distance metric between feature importance of a candidate feature and its knockoff this is typically the l1-norm. Given the relative feature importance statistics , the are sorted in descending order and we then select the features where exceed the threshold which is defined for a target FDR as :

| (2) |

3 Automatic Relevance Determination and Weight l2-norm Feature importance Statistics

An ARD prior for a BNN is one where weights associated with each input feature connection to the first hidden layer belong to a distinct class and have unique precision parameters for each input. The posterior distribution will then be as follows(MacKay, 1995):

| (3) |

Where is the kernel of the prior distribution on the weights , is the kernel of the data likelihood and is the normalisation constant. The precision hyperparameters for each group of weights are estimated by evidence maximisation or Markov chain Monte Carlo(MacKay, 1995; Neal, 2012). Irrelevant features will have high values of the regularisation parameter meaning that their weights will be forced to decay to values close to zero.

In order to manage the scaling of the regularisation parameters we then consider the l2-norm of the resulting weights as a measure of relative feature importance. We infer the importance of a feature using the l2-norm all the weights connecting a specific input to the first hidden layer units i.e.

| (4) |

We incorporate this feature importance measure in the model-x knockoff filter by setting = .

4 Experiments

4.1 Simulation Studies

We use simulated data to compare the variable selection performance of our proposed BNN-ARD weight l2-norm feature importance statistic with other non-linear feature importance statistics. We simulate non-linear data from the data model; . Where Y is a vector of the response, is a p dimensional vector of coefficients, is a feature matrix sampled independently from where elements of the co-variance matrix are set to with and .

We randomly set the amplitudes of a subset of relevant features of 10 randomly selected elements to a value of . The total number of candidate features in , was set to 100. We the compare knockoff filters with the following feature importance statistics: BNN-ARD weight l2-norm; Multi-layer Perceptron(MLP) weight l2-norm ;Random forest(RF) mean decrease in accuracy(Breiman, 2001). We repeat the experiment with 100 random initialisations and report on the mean power and FDR as the target FDR varies.

4.2 Real Data Experiments

We further assess the relative performance of the knockoff filters based on the various feature importance statistics on the Norwegian wind farm dataset. The dataset consists of 7384 records covering the period from January 2014 to December 2016(Mbuvha et al., 2017). The eleven candidate features include the wind farm online capacity, one and two hour lagged historical power production values as well as numerical weather prediction(NWP) estimates of humidity, temperature and wind speed.

We compare the performance of the various feature importance statistics based on the testing set Root Mean Square(RMSE) of an MLP trained on features selected by each of the respective feature importance statistics.

5 Results and Discussion

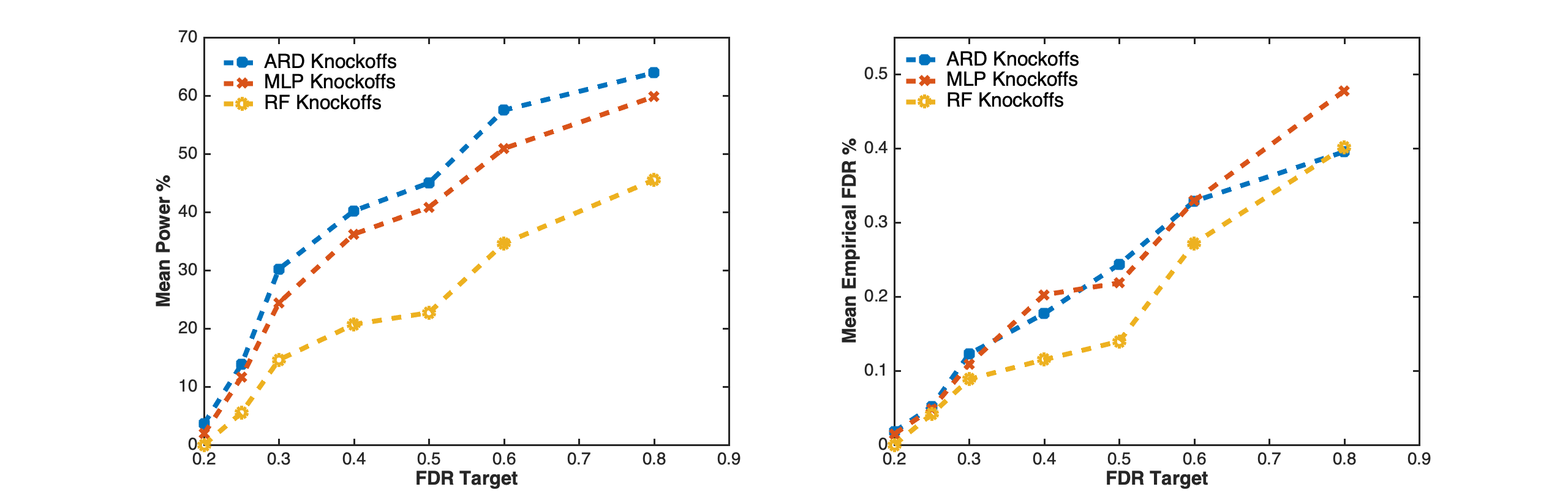

Figure 1 shows the mean power and empirical FDR across various target FDR levels of the 100 simulations. The results show that the BNN-ARD l2-norm knockoff filter displays persistently higher power in recovering non-null features, relative to the MLP l2-norm knockoff filter and the RF knockoff filter respectively. The corresponding empirical FDR plot is relatively linear below the 45 degree line meaning that all knockoff filters maintained the theoretical Target FDR. A non-parametric Kruskal Wallis(McKight and Najab, 2010) test for statistical significance of the differences in power yields a strongly significant p-value of . A further Bonferroni test(Hochberg and Tamhane, 2008) on the pair wise differences in power show statistical significance at a 10 percent level between the BNN-ARD l2-norm and MLP l2-norm filters and at the 5 percent level for both neural network based filters relative to the RF filter.

Table 1 shows the mean testing RMSE on the Norwegian wind farm dataset. The results show that the mean testing RMSE based in features selected by the BNN-ARD l2-norm filter is lower than that of the MLP l2-norm filter with statistical significance at FDR target levels greater than 0.25. The features selected by both filters at their respective minimum testing RMSE displayed an 88% overlap. Features such as the third order lag in power production, the second order lag in plant availability and the NWP temperature forecast were irrelevant. The RF filter results are unavailable as the filter yielded empty sets for FDR targets below 0.5. These results show congruence with work previously done on the same dataset by Mbuvha et al. (2017).

| Feature Importance Statistic | FDR Target | ||||

|---|---|---|---|---|---|

| 0.2 | 0.25 | 0.3 | 0.4 | 0.5 | |

| MLP-l2 Norm | 7257.59 | 6744.63 | 7427.79 | 4398.25 | 3229.72 |

| ARD-l2 Norm | 7325.57 | 6124.28 | 5173.02 | 3717.99 | 2991.72 |

References

- Barber et al. (2015) Rina Foygel Barber, Emmanuel J Candès, et al. Controlling the false discovery rate via knockoffs. The Annals of Statistics, 43(5):2055–2085, 2015.

- Breiman (2001) Leo Breiman. Random forests. Machine learning, 45(1):5–32, 2001.

- Candes et al. (2018) Emmanuel Candes, Yingying Fan, Lucas Janson, and Jinchi Lv. Panning for gold:‘model-x’knockoffs for high dimensional controlled variable selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):551–577, 2018.

- Gimenez et al. (2018) Jaime Roquero Gimenez, Amirata Ghorbani, and James Zou. Knockoffs for the mass: new feature importance statistics with false discovery guarantees. arXiv preprint arXiv:1807.06214, 2018.

- Hochberg and Tamhane (2008) Yosef Hochberg and Ajit C. Tamhane. Distribution-Free and Robust Procedures, pages 234–273. John Wiley & Sons, Inc., 2008. ISBN 9780470316672.

- Lu et al. (2018) Yang Lu, Yingying Fan, Jinchi Lv, and William Stafford Noble. Deeppink: reproducible feature selection in deep neural networks. In Advances in Neural Information Processing Systems, pages 8676–8686, 2018.

- MacKay (1995) David JC MacKay. Probable networks and plausible predictions—a review of practical bayesian methods for supervised neural networks. Network: computation in neural systems, 6(3):469–505, 1995.

- Mbuvha et al. (2017) Rendani Mbuvha, Mattias Jonsson, Niclas Ehn, and Pawel Herman. Bayesian neural networks for one-hour ahead wind power forecasting. In 2017 IEEE 6th International Conference on Renewable Energy Research and Applications (ICRERA), pages 591–596. IEEE, 2017.

- McKight and Najab (2010) Patrick E McKight and Julius Najab. Kruskal-wallis test. Corsini Encyclopedia of Psychology, 2010.

- Neal (2012) Radford M Neal. Bayesian learning for neural networks, volume 118. Springer Science & Business Media, 2012.